WTI Slides Back Below $40 After Surprise Crude Build Tyler Durden

Tue, 10/06/2020 – 16:34

Oil prices held gains (WTI above $40) despite Trump spoiling the Pelosi-bailout party.

“The petroleum complex desperately needed that stimulus to come through so that the economy could perk back up and refined-product demand could hopefully rebound,” said John Kilduff, a partner at Again Capital LLC. “This is a big hit to that.”

Still, oil prices are keeping some strength with U.S. Gulf operators shutting 29% of oil output in the region ahead of Hurricane Delta (unlikely to affect this week’s data).

API

Crude +951k (-2mm exp)

Cushing +749k

Gasoline -867k (-800k exp)

Distillates -1.033mm (-2.9mm exp)

After three weeks of draws, API reports a crude build (unexpectedly rising 951k barrels vs -2mm exp) and a smaller than expected product draw…

Source: Bloomberg

WTI hovered just above $40, having bounced off that level after plunging on Trump’s tweet, and slipped back below

Finally, as Bloomberg notes, oil may not be out of the woods yet. In recent days, there have been a flurry of options trades that would profit a buyer from lower prices.

via ZeroHedge News https://ift.tt/34wDhTn Tyler Durden

DNI Declassifies Brennan Notes; Briefed Obama On Intelligence That Hillary Clinton Concocted Trump-Russia Allegations Tyler Durden

Tue, 10/06/2020 – 16:19

Director of National Intelligence John Ratcliffe on Tuesday declassified several documents, including handwritten notes from former CIA John Brennan after he briefed former President Obama on an alleged plot by Hillary Clinton to tie then-candidate Donald Trump to Russia as “a means of distracting the public from her use of a private email server” ahead of the 2016 US election, according to Fox News.

Ratcliffe declassified Brennan’s handwritten notes – which were taken after he briefed Obama on the intelligence the CIA received – and a CIA memo, which revealed that officials referred the matter to the FBI for potential investigative action.

The Office of the Director of National Intelligence transmitted the declassified documents to the House and Senate Intelligence Committees on Tuesday afternoon.

“Today, at the direction of President Trump, I declassified additional documents relevant to ongoing Congressional oversight and investigative activities,” Ratcliffe said in a statement to Fox News Tuesday. –Fox News

“We’re getting additional insight into Russian activities from [REDACTED],” read Brennan’s notes. “CITE [summarizing] alleged approved by Hillary Clinton a proposal from one of her foreign policy advisers to vilify Donald Trump by stirring up a scandal claiming interference by the Russian security service.”

As we noted last week after Ratcliffe previewed the allegation:

On September 7, 2016, US intelligence officials forwarded an investigative referral to former FBI officials James Comey and Peter Strzok concerning allegations that Hillary Clinton approved a plan to smear then-candidate Donald Trump by tying him to Russian President Vladimir Putin and Russian hackers, according to information given to Sen. Lindsey Graham by the Director of National Intelligence.

According to Fox News’ Chad Pergram, “In late July 2016, U.S. intelligence agencies obtained insight into Russian intelligence analysis alleging that U.S. Presidential candidate Hillary Clinton had approved a campaign plan to stir up a scandal against U.S. Presidential candidate Donald Trump,” after one of Clinton’s foreign policy advisers proposed vilifying Trump “by stirring up a scandal claiming interference by Russian security services.”

2) DNI info to Grahm:…by tying him to Putin and the Russians’ hacking of the Democratic National Committee. The IC does not know the accuracy of this allegation or the extent to which the Russian intelligence analysis may reflect exaggeration or fabrication.”

Nancy Pelosi is asking for $2.4 Trillion Dollars to bailout poorly run, high crime, Democrat States, money that is in no way related to COVID-19. We made a very generous offer of $1.6 Trillion Dollars and, as usual, she is not negotiating in good faith. I am rejecting their request, and looking to the future of our Country.

I have instructed my representatives to stop negotiating until after the election when, immediately after I win, we will pass a major Stimulus Bill that focuses on hardworking Americans and Small Business.

I have asked Mitch McConnell not to delay, but to instead focus full time on approving my outstanding nominee to the United States Supreme Court, Amy Coney Barrett. Our Economy is doing very well. The Stock Market is at record levels, JOBS and unemployment also coming back in record numbers.

We are leading the World in Economic Recovery, and THE BEST IS YET TO COME!

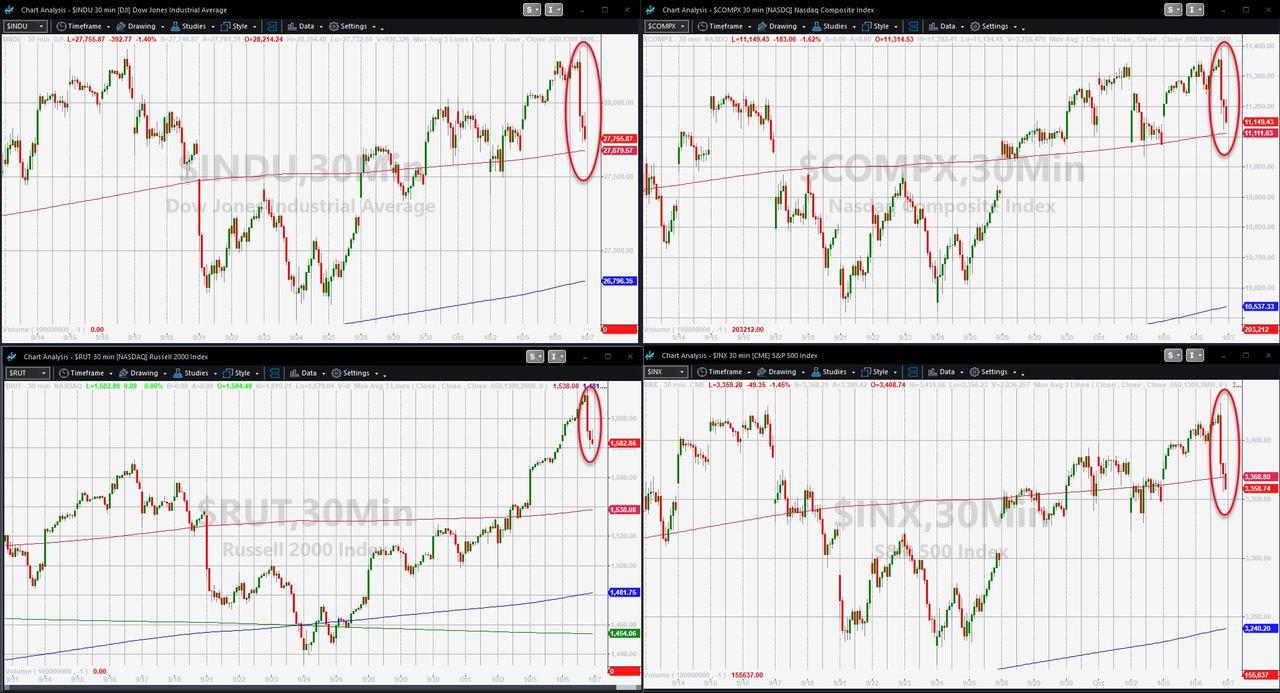

Which prompted this reaction in stocks…

Or put another way…

Small Caps were soaring relative to mega-Tech for most of the day until the Trump tweet reversed things… but its notable where the relative level was when it reversed…

S&P broke below its 50DMA, Dow and Nasdaq also pushed down to that key technical level…

Which prompted Dave Portnoy to explains why traders should “buy the dip.”

I’m on a plane. @realDonaldTrump is trying to show people what will happen to stock market if people don’t elect him. However he can’t win by intentionally tanking the stock market like he just did. He will lose any economic votes he has. He will change his tune soon. #ddtg

Financial and precious metals expert Egon von Greyerz (EvG) stores gold for clients at the biggest gold vault in the world buried deep in the Swiss Alps. This year, EvG’s company, Matterhorn Asset Management, has seen “a major inflow, a massive inflow of big amounts of gold” being vaulted by his wealthy clients. Why the big spike in people wanting physical gold?

EvG says, “You have seen this year incredible money creation around the world by central banks along with the massive debt increases…”

“You are looking at… the money supply, which has been going up for 50 years, but now… it’s going up in a straight line. So, we are now entering into the exponential phase of this financial system. We are seeing unlimited money printing, helicopter money like Ben Bernanke (former Fed Head) called it. Then we are going to see accelerated debasement of the currency. The real moves in gold and silver haven’t started yet.”

This next move, according to EvG, is going to be a global phenomenon. EvG explains, “The bond market is going to collapse, and interest rates are going to go a lot higher…”

“Inflation is going to go a lot higher, and, eventually, the currency collapses, and it is a collapsing currency that leads to hyperinflation. When the currency falls, we will see hyperinflation. . . . The next group of people that are going to come into this are the institutional investors. We’ve already seen signs of that. . . . The risk I would say is the highest ever in history. You have never had a situation in history where basically every country in the world is in the same position.

In the past, you have had individual countries that have had problems, economic collapse and hyperinflation. You have never had a situation where the whole world has had an insoluble debt problem. That is now about to collapse. That’s never happened in history, and that’s why it’s going to be on a much bigger scale than before. I am not a prophet of doom and gloom. I am just someone who analyzes risk, and I say it is inevitable. This has to happen. It’s not a question of when, it’s just a question of how long will it take.”

What also has to happen are dramatically higher gold and silver prices? EvG says, “Silver at $25 per ounce is incredibly cheap. In my view, silver is going to go to at least $600 per ounce…”

“Gold should be at least $10,000 per ounce right now. . . . Gold should be $20,000 per ounce on an inflation adjusted basis. . . . When gold is $100,000 or $100 million (per ounce) or whatever it reaches, then everyone is going to be talking about gold. Gold is going to reach an ultimate peak, but that depends on the amount of money printed. . . . America has had a budget deficit for 90 years. What’s your forecast? It’s so easy. It’s going to get worse because now you are getting into the crisis situation. That’s why it’s going to accelerate. . . .

Nobody can believe these forecasts of gold and silver. People just like to extrapolate a few percent a year. That’s not where we are now. We are not at a point now where it’s going to happen gradually. We are at the exponential point, and the super exponential point of money printing, deficit and of currency collapse. That’s why this will be reflected in the precious metals prices.”

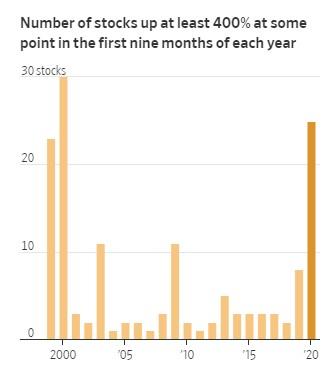

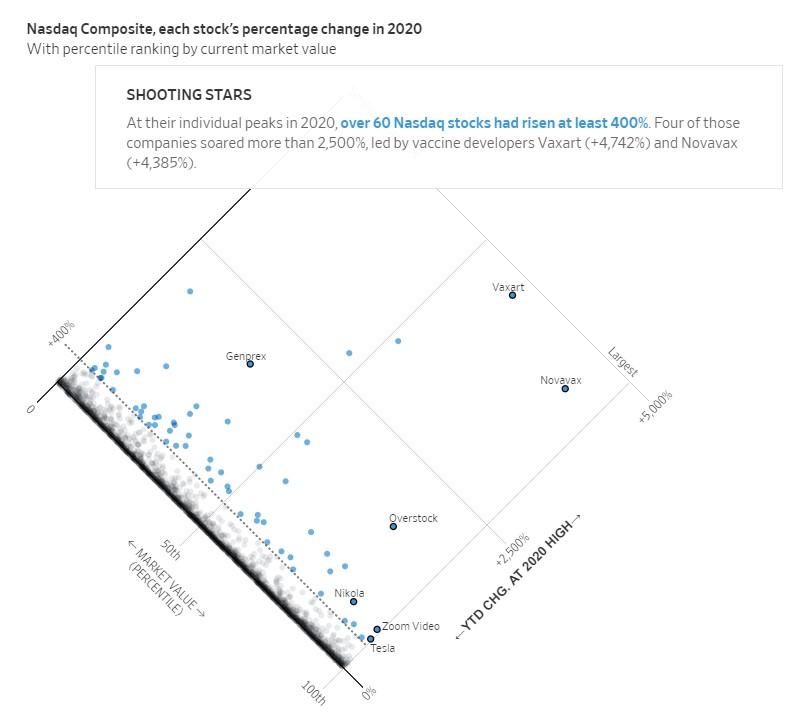

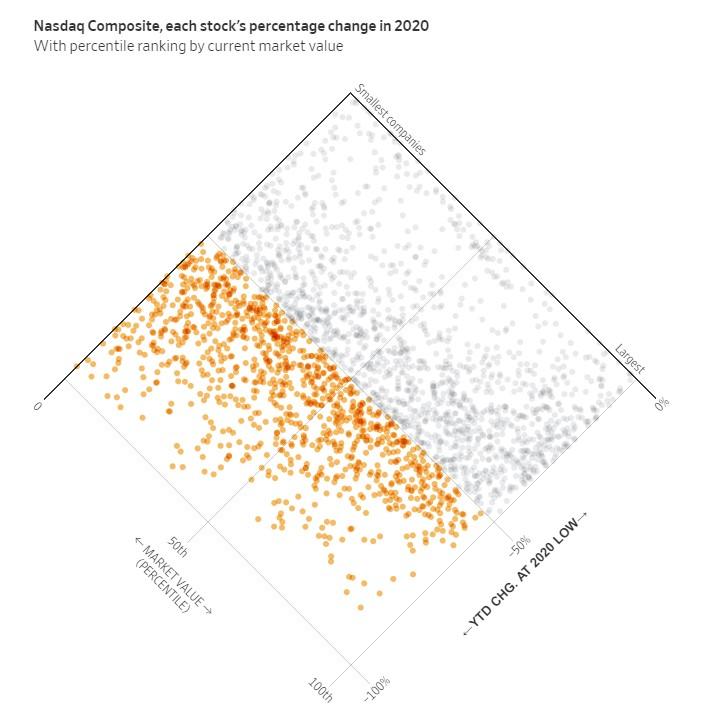

More Stocks Have Risen By 400% This Year Than Any Year Since 2000 Tyler Durden

Tue, 10/06/2020 – 15:10

If the SPAC boom minting new billionaires every day and the NASDAQ raging to new highs almost daily weren’t enough to give 2020 a certain “1999 vibe”, perhaps some additional stunning statistics from the Wall Street Journal will.

In a recent article the Journal published detailing stocks posting astonishing rallies off lows this year (thanks Powell and Kashkari), it was revealed that the number of stocks that have risen 400% or more in the first nine months of this year is the most since the year 2000.

The study looked at companies that were at least $100 million to start the year. This year’s winners were replete with technology and biotech companies, as investors flocked to both sectors as a response to the coronavirus pandemic.

Outliers like Overstock have risen 956% so far this year. Names like Tesla and Zoom are both up 413% and 591%, respectively.

The Journal says that the run in stock prices was one that “few saw coming”, however the Fed’s early intervention during the beginning of the pandemic made it clear – at least to those paying attention – that the Central Bank’s only policy was to save the stock market at all costs, sacrificing it on the altar of price discovery. And thus, here we are.

Justin White, a portfolio manager at T. Rowe Price, said: “The rate at which momentum and enthusiasm and exuberance took hold over the summer…it hit a fever pitch that I have not seen in the five years that I’ve been managing my fund.”

And while the Journal is also quick to attribute the gains to individual investors, we pointed out weeks ago that a large catalyst behind a recent rally in tech had to do with nothing more than market manipulation, through the purchase of options, by Softbank.

That gamma squeeze disproportionately affected the NASDAQ, with more than 60 stocks in the index rising at least 400% at their peak in 2020. More than 1,000 of the index’s 2,500 stocks suffered declines of at least 50% at their low points, as well.

In addition to Apple and Tesla engaging in stock splits, IPO and SPAC enthusiasm has also continued to fuel what is left of actual investor sentiment heading into the fall. Names like Snowflake and Unity Software have been widely talked about names and relative successes, post-IPO. Compass Pathways, a biotech company focusing on psilopsybin, also had a successful IPO this year, as we pointed out weeks ago.

White had grappled with the reality of buying Zoom back in March after it had started to rally: “I kept a pretty small position because I didn’t want to make a heroic bet at what could have been the top. In hindsight, the stock was actually pretty cheap at $200.”

But, as White learned, reality doesn’t seem to matter anymore. David Malmgren, senior portfolio manager at FBB Capital Partners, recalled the pushback he received while buying Tesla at $800 (pre-split) earlier this year. “The managing director of the firm came to me and said: ‘Seriously, we’re buying Tesla at $800?’ You’re buying at the highs…it takes courage.”

Courage is one word for it…

via ZeroHedge News https://ift.tt/3lh05xi Tyler Durden

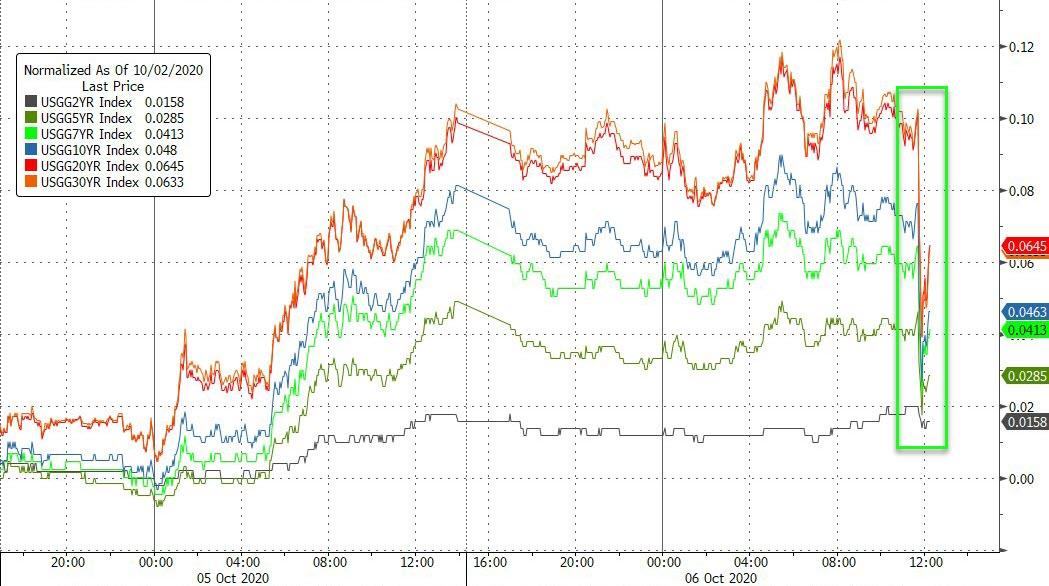

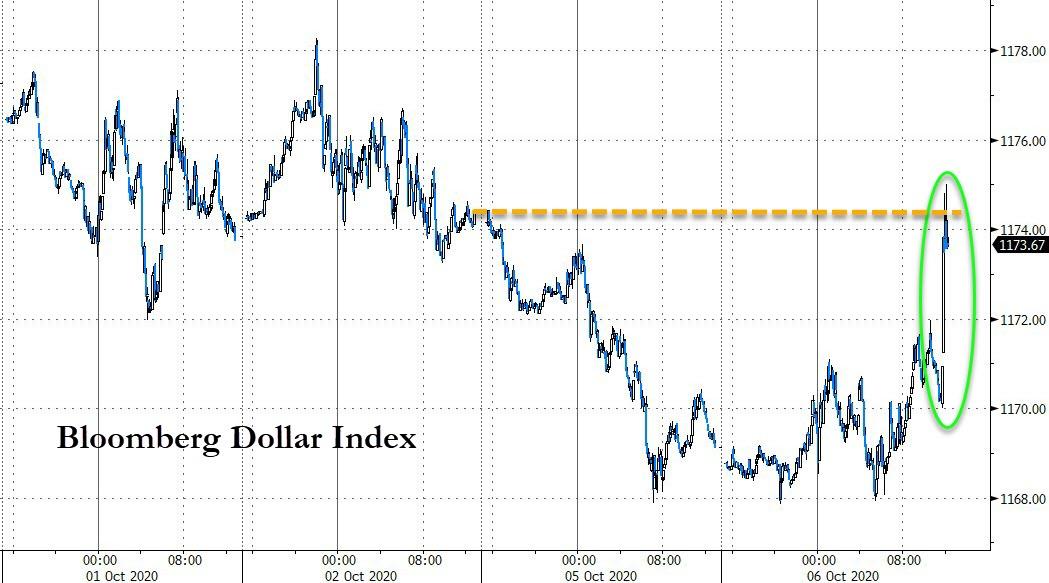

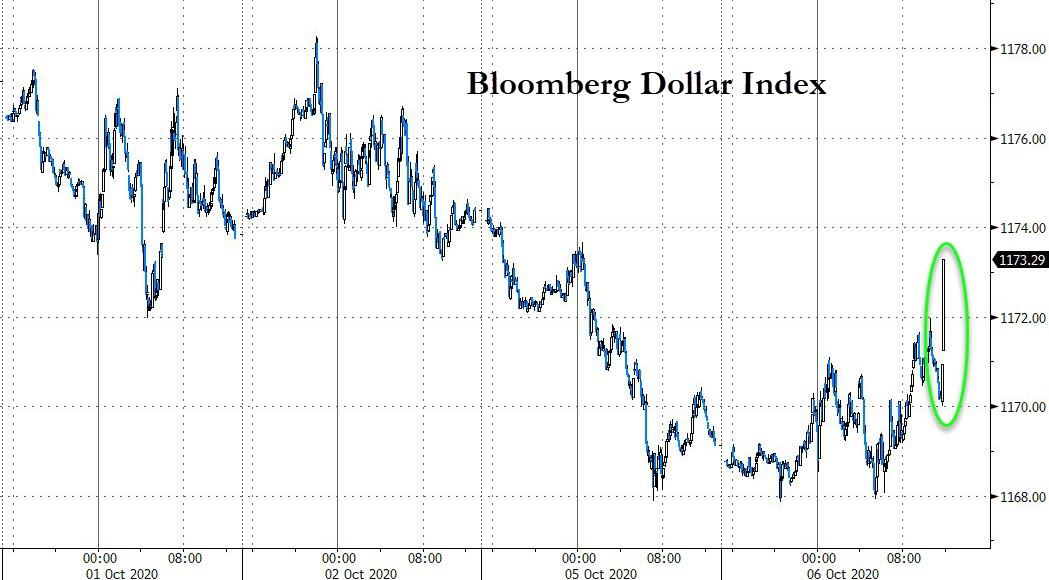

Stocks Plunge After Trump Says He Stopped Stimulus Talks Until After The Election Tyler Durden

Tue, 10/06/2020 – 14:57

We have been warning for weeks that no stimulus deal would happen before the election, and moments ago none other than president Trump confirmed just that.

Trump, who has been in the White House less than a day since his return from Walter Reed, just crashed stocks, bond yields and sent the dollar soaring, when he tweeted that due to Nancy Pelosi’s “bad faith” negotiations, he has instructed representatives “to stop negotiating until after the election.”

The full Trump tweetstorm:

Nancy Pelosi is asking for $2.4 Trillion Dollars to bailout poorly run, high crime, Democrat States, money that is in no way related to COVID-19.

We made a very generous offer of $1.6 Trillion Dollars and, as usual, she is not negotiating in good faith.

I am rejecting their request, and looking to the future of our Country. I have instructed my representatives to stop negotiating until after the election when, immediately after I win, we will pass a major Stimulus Bill that focuses on hardworking Americans and Small Business.

I have asked Mitch McConnell not to delay, but to instead focus full time on approving my outstanding nominee to the United States Supreme Court, Amy Coney Barrett.

Our Economy is doing very well. The Stock Market is at record levels, JOBS and unemployment also coming back in record numbers. We are leading the World in Economic Recovery, and THE BEST IS YET TO COME!

…request, and looking to the future of our Country. I have instructed my representatives to stop negotiating until after the election when, immediately after I win, we will pass a major Stimulus Bill that focuses on hardworking Americans and Small Business. I have asked…

And speaking of the stock market being at record levels, well not so much as algos were clearly stunned by this unexpected development ending all hopes for a stimulus deal before the election, with risk assets plunging…

… yields tumbled…

… and the dollar soared.

via ZeroHedge News https://ift.tt/30C2jQ8 Tyler Durden

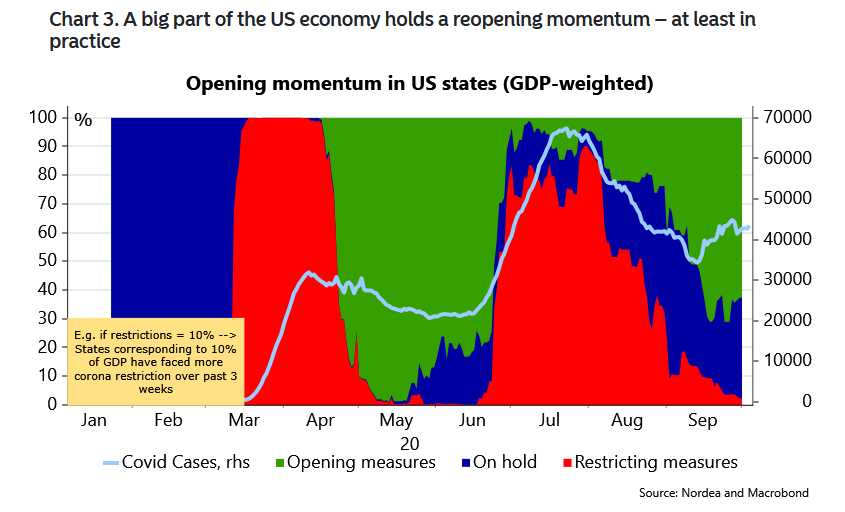

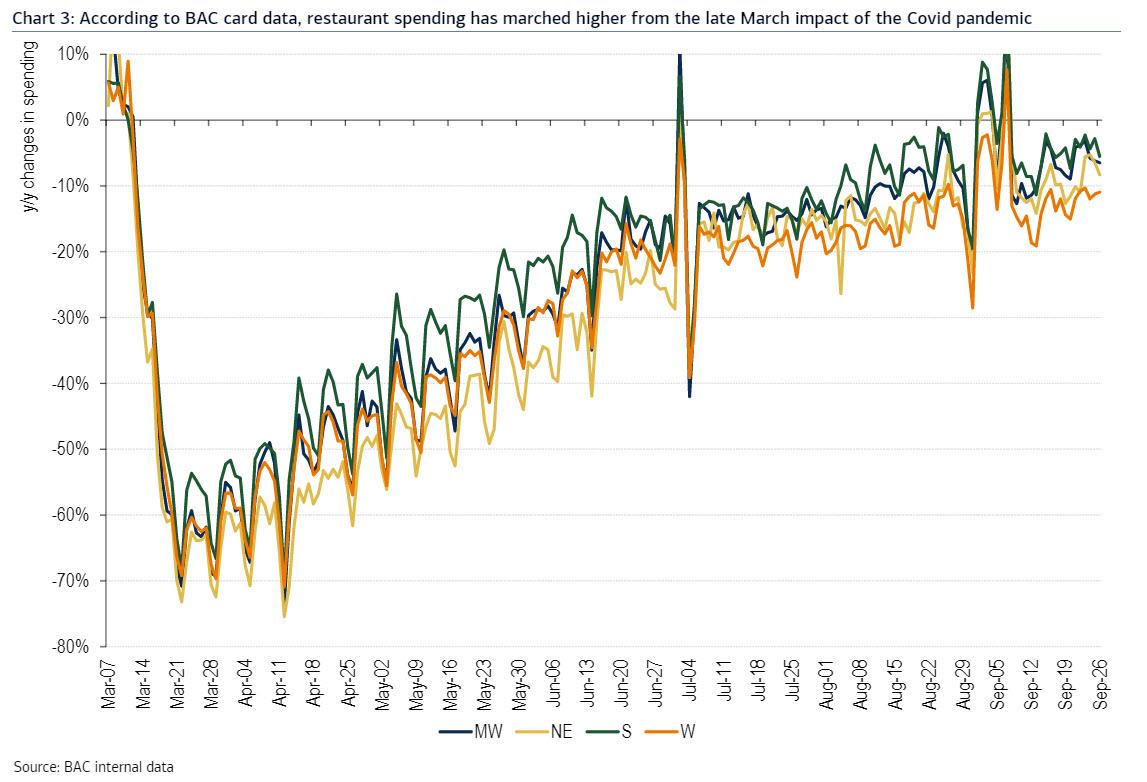

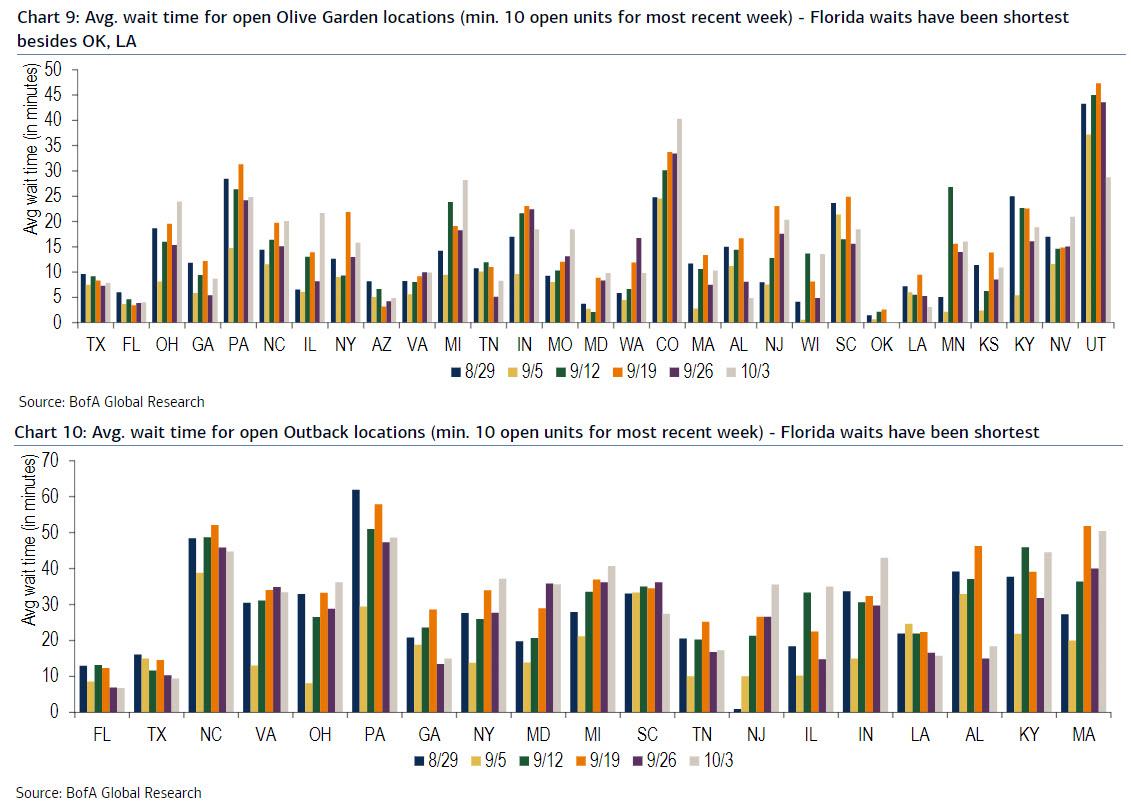

US Restaurant Spending Is Almost Back To Pre-COVID Levels Tyler Durden

Tue, 10/06/2020 – 14:45

Something odd happened to the US economy in the past two months as many in the media, the political establishment and even various Fed hacks (recall on August 3 Neel Kashkari Saying Only Way To “Save Economy” Is To Lock It Down “Really Hard” For 6 Weeks), were feverishly counting the daily new US covid cases and warning that only a new shutdown could spare the US from imminent disaster: it has almost fully reopened and according to real-time indicators, it is now recovering at a far faster pace than most had expected (as the Fed’s latest economic projections confirmed).

And nowhere is this more visible than in the US restaurant space where with various exceptions – most notably across Manhattan where policy seems to change on a daily if not hourly basis – spending appears to be almost back to pre-covid levels.

In an analysis conducted by BofA analysts looking at daily restaurant trends through September 26th, the Bank of America aggregated credit and debit data showed national restaurant spending improving another 1.7% to down 8% (for the seven days ended September 26th) from a down 9% (from the week prior). While the BofA analysts note that performance on weekends continues to lag weekdays by about 1%-2%, the trend is clear: we are almost back to normalcy.

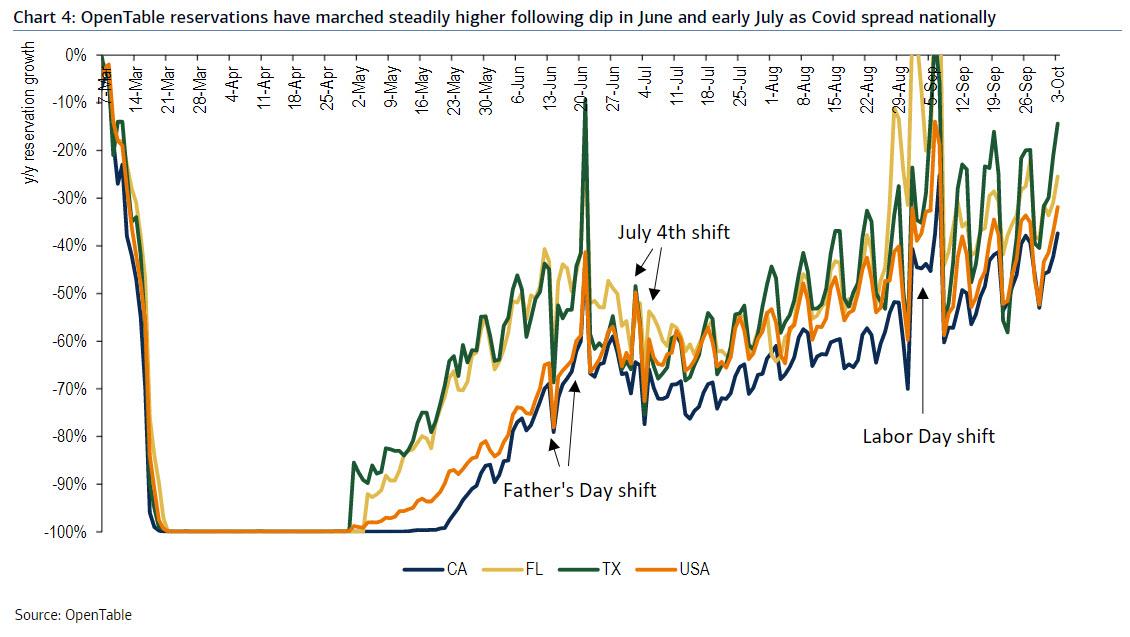

In addition to the normalization in overall restaurant spending, BofA also looked at OpenTable data on dining room reservations. Here too reservation counts have steadily moved higher over the past two and a half months as new Covid cases have been falling. The week ended October 3rd was down 41% y/y, a 2% improvement from the down 43% the prior week.

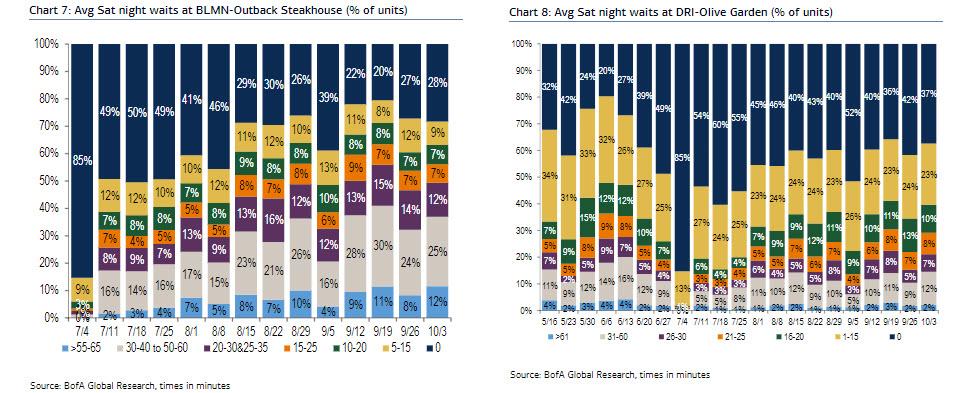

To get a more comprehensive picture of the current state of restaurants, BofA also include the average Saturday night quoted dine-in wait times at Outback Steakhouse locations around the U.S. Wait times show a similar trend to the Olive Garden wait times.

Taking this analysis one step further, and expanding it to states, in the charts below BofA shows the wait times by state over the past six weeks which has seen Florida with some of the shortest waits in the country, suggesting limited new demand as capacity restrictions get raised. At the same time, several states stand out as having longer waits including North Carolina, South Carolina, Pennsylvania, Colorado, Utah, Michigan, and Indiana. According to the BofA strategists, “it is possible that eating times are more spread out, earlier, or later in certain states vs our measuring time.”

In short, while it hasn’t fully recovered yet, as more of the US continues to reopen expect one of the service sectors most adversely impacted by the covid shutdowns, to creep ever higher back to a return to normalcy.

via ZeroHedge News https://ift.tt/3nnzd0y Tyler Durden

‘Dip-Buyers’ Send Gold ETF Holdings Soaring To Record Highs Tyler Durden

Tue, 10/06/2020 – 14:30

“There seems to be a battle between [precious metals] investors going on,” notes Georgette Boele, precious metals strategist at ABN Amro Bank NV.

The last few weeks have seen Gold ETFs register significant inflows (6 days in a row most recently) as precious metal prices have been lower and the infamous ‘dip-buyers’ take advantage of these lower prices to stack some more paper gold.

Bullion prices have come under pressure as real yields have accelerated amid positional shifts by investors around the election and fiscal stimulus.

Source: Bloomberg

But as gold prices dipped, ETF inflows accelerated, sending the total gold ETF holdings to a record high as ABN’s Boele points out that “ETF buyers have more confidence than buyers in the futures market.”

Source: Bloomberg

We saw this similar pattern emerge in the early summer, only for gold prices to rapidly catch up to the demand picture.

via ZeroHedge News https://ift.tt/33D311s Tyler Durden

GE Dips After Admitting Wells Notice Probing Revenue Recognition Practices Tyler Durden

Tue, 10/06/2020 – 14:12

On a broadly positive day, GE shares are sliding after their latest 8K revealed SEC staff have issued a “Wells Notice,” questioning the company’s revenue recognition practices related to long-term agreements.

Full comment from 8K…

Item 8.01 Other Events.

As previously reported, the staff of the U.S. Securities and Exchange Commission (“SEC”) has notified General Electric Company (“GE”) that they are conducting an investigation of GE’s revenue recognition practices and internal controls over financial reporting related to long-term service agreements. Following GE’s investor update in January 2018 about the increase in future policy benefit reserves for GE Capital’s run-off insurance operations, the SEC staff expanded the scope of its investigation to encompass the reserve increase and the process leading to the reserve increase. Following GE’s announcement in October 2018 about the expected non-cash goodwill impairment charge related to GE’s Power business, the SEC expanded the scope of its investigation to include that charge as well. We are providing documents and other information requested by the SEC staff, and we are cooperating with the ongoing investigation.

On September 30, 2020, the SEC staff issued a “Wells notice” advising GE that it is considering recommending to the SEC that it bring a civil injunctive action against GE for possible violations of the securities laws. GE has been informed that the issues the SEC staff may recommend that the SEC pursue relate to the historical premium deficiency testing for GE Capital’s run-off insurance operations, as well as GE’s disclosures relating to such run-off insurance operations. The staff has not made a preliminary decision whether to recommend any action with respect to the other matters under investigation.

The Wells notice is neither a formal allegation nor a finding of wrongdoing. It allows GE the opportunity to provide its perspective and to address the issues raised by the SEC staff before any decision is made by the SEC on whether to authorize the commencement of an enforcement proceeding. GE disagrees with the SEC staff with respect to this recommendation and will provide a response through the Wells notice process. If the SEC were to authorize an action against GE, it could seek an injunction against future violations of provisions of the federal securities laws, the imposition of civil monetary penalties, and other relief within the Commission’s authority. The results of the Wells notice and any enforcement action are unknown at this time.

Shares are lower, but not dramatically for now…

via ZeroHedge News https://ift.tt/3nndMg3 Tyler Durden

Saturday, Sept. 26, was among the best days of the Trump presidency, or so some of us thought watching the president introduce in the Rose Garden his sterling candidate for Ruth Bader Ginsburg’s seat on the Supreme Court.

The academic and professional credentials of Amy Coney Barrett, 48, a U.S. appeals court judge, were superb. Moreover, she was a devout Catholic and mother of seven, two of whom were adoptees from Haiti.

From every standpoint, a 10-strike for Donald Trump.

Ahead was the Tuesday debate, the first of three with Joe Biden, and the long-awaited opportunity to expose Sleepy Joe’s visible loss of mental and verbal acuity in the four years since he was vice president.

Sunday, however, The New York Times detonated a bomb directly beneath the Trump campaign. Declaring that it had Trump’s tax returns, the Times story blared:

“Donald J. Trump paid $750 in federal income taxes the year he won the presidency. In his first year in the White House, he paid another $750. He had paid no income taxes at all in 10 of the previous 15 years — largely because he reported losing much more money than he made.”

Far from being a billionaire, the Times said, Trump was mired in debt with hundreds off millions of dollars in loans coming due in 2021.

Suddenly, Trump was on the defensive.

And in the Cleveland debate, he began a series of accusations and insults that lasted 90 minutes. The debate was widely declared the worst in U.S. presidential history.

Moderator Chris Wallace and the media agreed that the descent into chaos was caused by the endless interruptions of Trump.

Believing he accomplished what he had come to do, Trump headed out for the friendly country of Minnesota’s Iron Range. On the return trip on Air Force One, Hope Hicks, feeling unwell, was quarantined.

She later tested positive for COVID-19.

At 1 a.m. Friday, came word came that both the president and first lady had tested positive. By evening, Marine One was transporting Trump from the White House to Walter Reed hospital in Bethesda.

Saturday came the doctors’ report that the president was doing well, followed by chief of staff Mark Meadows’ backgrounder suggesting that Trump’s situation had been more serious than the country knew.

Came then news that some of Trump’s guests at the Rose Garden ceremony had tested positive: campaign manager Bill Stepien, Governor Chris Christie of his debate prep team, Kellyanne Conway, and Sens. Mike Lee of Utah and Thom Tillis of North Carolina, both of the Senate Judiciary Committee that will vote on Judge Barrett.

Sunday, with a crowd in front of Walter Reed loudly cheering for him, Trump commandeered an SUV and ordered it to drive by his followers so he could wave to them. In the front seat of the SUV, in masks and protective gear, were Trump’s Secret Service agents.

The cumulative impact of these 10 days has been distracting at best and dreadful at worst. And the pressure from Trump, to get back to the White House and the campaign, suggests this is his take as well.

The coronavirus and how he has handled it, the contraction of COVID-19 and how Trump got infected, his prior mockery of masks and ridicule of many who wear them, the specter of thousands of maskless Trumpsters at MAGA rallies – all are now the stuff of front-page news and back-page commentary.

The nation tends to respond sympathetically when the president faces a life-threatening situation. It did so to Ike’s heart attack in 1955, and to Reagan after he was shot at the Washington Hilton by John Hinckley and then had colon cancer surgery early in his second term.

But Trump may have forfeited some of that sympathy by his mocking the wearing of masks.

On the weekend after the Trump-Biden debate, a Wall Street Journal poll found that Trump had fallen 14 points behind Biden, and, in an average of national polls, Biden now led him by 8 points.

Trump has four weeks to turn it around. And his task, while easy to describe, is not so easy to accomplish. He needs to persuade undecided and soft Biden voters that Joe is simply not up to the job of president.

Assuming he is well enough to campaign as he used to, Trump has to convince the country that Joe Biden is too big a risk to take. He has two more debates to do what he failed to do in the first debate.

Wednesday will be Mike Pence’s opportunity, in his debate with Kamala Harris, to show that Trump made the right call in choosing him.

He can pay back the favor by exposing the radicalism of the people and policies Joe Biden would bring with him into the White House.

via ZeroHedge News https://ift.tt/33AW3K7 Tyler Durden

{kind=link}