China’s Xi: “I Can’t Believe What President Trump Says”

With equity futures gradually rolling over overnight, there was the obligatory dose of trade war optimism in this morning’s news flow, with Trump reiterating that China wants to talk, while China was said to be hopeful the US can create conditions for trade talks; this was followed by a CCTV report according to which U.S. delegates said they hope U.S.-China trade talks can achieve progress and reach a deal as soon as possible, while China’s premier Li was quoted as saying that China and US should find solutions to disputes based on consensus reached by leaders of the two nations, adding that “China treats domestic, foreign companies fairly” and “puts more focus on intellectual property protection”, noting that “companies including U.S. firms are welcome to increase investment in China.”

This was more than enough to stabilize the drop in futures. But a bigger problem may be emerging behind the scenes, as the true feelings of China’s president toward president Trump have finally emerged on the record.

According to Kyodo, President Xi Jinping voiced distrust of U.S. President Donald Trump during his meeting with the Japanese Prime Minister Shinzo Abe in June amid the U.S.-China trade dispute, a source close to the matter said Tuesday.

“I can’t believe what President Trump says” concerning trade negotiations, Xi told Abe during a meeting on the fringe of the Group of 20 summit in Osaka. And while Abe told Xi that Trump trusts the Chinese president, Xi continued to air his grievances about his U.S. counterpart, the diplomatic source told Kyodo News.

The reason for Xi’s distrust: despite agreeing to Xi’s proposal on the phone to deal with Chinese telecommunication giant Huawei Technologies during the next working-level negotiations, “once the negotiations began, the U.S. side said that Huawei is not a trade issue but a security issue and did not deal with it,” Xi told Abe, pointing out that Trump’s remarks proved unreliable.

According to the Chinese Foreign Ministry, Xi had a telephone conference with Trump on June 18, during which he expressed China’s hope that “the U.S. side can treat Chinese firms in a fair manner.”

Xi further complained to Abe that while the Trump administration has repeatedly criticized Beijing for supporting state-owned companies with subsidies, “the U.S. is also providing Boeing with subsidies,” referring to the Chicago-based U.S. airplane manufacturer.

Last week, the United States slapped China with the first stage of a new round of tariffs that will see nearly all Chinese imports taxed. China retaliated on the same day with its own round of tariffs on U.S. goods and announced the following day its decision to lodge a case at the World Trade Organization over the latest U.S imposition of import duties on Chinese exports to the United States.

While the United States and China are planning to hold ministerial- level trade talks in October in Washington, it is uncertain whether there will be any breakthrough, especially with neither side trusting anything the other says.

Eager to claim a major trade victory to boost his 2020 re-election bid, Trump is likely to strengthen his hardline attitude toward China, according to Kyodo. But with no mutual trust between the two leaders, a major concession by Xi seems unlikely, making a prolonged conflict between the United States and China almost inevitable.

Meanwhile, relations between Japan and China have been improving recently, with the two sides preparing for Xi’s first state visit to Japan planned for next spring.

French President Emmanuel Macron failed to promote successfully his Iranian initiative with the US administration despite the initial blessing of his US counterpart. This failure led Iran to make a third gradual withdrawal from its JCPOA nuclear deal commitment, raising two main issues.

Iran has become a regional power to be reckoned with, so we can now scrap from reactions to its policies the words “submit,” or “bow to the international community”. Moreover, since Europe is apparently no longer in a position to fulfill its commitments, Iran will now be headed towards a total pull-out following further gradual withdrawal steps. Just before the US elections due in November 2020, Iran is expected to become a nuclear country with the full capability of producing uranium enriched to more than 20% uranium-235, weapons-usable and therefore in a position to manufacture dozens of nuclear bombs (for which uranium must be enriched to about 90%). However, this does not necessarily mean that this is Iran’s ultimate objective.

Screenshot of Iranian President Hassan Rouhani inspecting and touring a facility.

Industry data shows that half of the effort goes into enriching from 0.7% to 4%. If Iran reaches the level of 20%, the journey towards 90% is almost done. A few thousand centrifuges are needed to reach 20% enrichment while a few hundred are enough to cross from 20% to the 90% needed for a nuclear bomb.

When Iran announces it is reaching a level which is considered critical by the west, there is the possibility that Israel might act militarily against Iran’s capability as it did in Iraq in 1981, in Syria in 2009, and in assassinating nuclear scientists. If this happens, the Middle East will be exposed to a mega earthquake whose outcome is unpredictable. But if Israel and the US are not in a position to react against Iran’s total withdrawal from the JCPOA (nuclear deal), Iran will no longer accept a return to the 2015 deal. Its position will become much stronger and any deal would be difficult to reach.

Sources within the decision-making circle have said “Iran will become a state with full nuclear capability. It is also aiming for self-sufficiency and is planning to move away from counting solely on its oil exports for its annual budget. It is starting to generate and manufacture in many sectors and it will certainly increase its missile development and production. Missile technology has proved to be the most efficient and cheapest deterrent weapon for Iran and its allies in Lebanon, Syria, Iraq and the Yemen.”

Iran has been following a “strategy of patience” since US President Donald Trump unlawfully revoked the nuclear deal. Tehran allowed Europe, for an entire year, to think about a way to tempt Iran to stay within the nuclear deal on the basis of 4 (France, Russia, China, UK) + 1 (Germany), excluding the US. After that long waiting period, Iran has taken the initiative into its own hands and is gradually pulling out of the deal. It seems Trump did not learn from President Obama who signed the deal, convinced that US sanctions would be ineffective.

But Iran is not missing an opportunity worth trying to make its case. At the G7 in France, Iranian Foreign Minister Javad Zarif cut short his visit to Beijing to meet European leaders and ministers at the request of President Macron. It was hinted that there were chances for Iran to sell its oil and that Macron had managed to break through the US-Iran tension.

Iran’s President Hassan Rouhani thought there was a real opportunity to smooth over tensions and that Trump, according to the source in Tehran, was ready to ease the sanctions in exchange for a meeting and the beginning of discussion. This is why Rouhani overtly stated his readiness to meet any person if that helped. But Zarif was surprised to learn that Macron didn’t fulfil his promises – because Trump had changed his mind. The initiative was stillborn and all are back at square one.

Macron understood that the problem doesn’t lie with the US President but in his consigliere Prime Minister Benyamin Netanyahu and his neocon team of Pompeo-Bolton. The meeting between the French Minister of Armed Forces Florence Parly and the Pentagon Chief Mark Esper was an attempt to convince the US Secretary of Defence to distance himself from the Pompeo-Bolton team before the situation gets out of control and Iran became unstoppable.

“Trump rejected the French idea to offer Iran a line of credit of 15 billions of Euros (not Dollars). This credit is part of Iran’s acquired right since it has agreed with Europe to sell 700,000 barrels of oil daily as part of a signed deal. Following the US sanctions on any country or company buying Iranian oil, Europe refrained from honouring the agreement. Vice Foreign Minister Abbas Araghchi calculated the amount at stake of 15 billion euros with European representatives. The agreement was that Iran would sell oil to Europe for this amount in the future, and that Iran could buy any product, not limited to food and medicine which were originally excluded from the US sanctions. Iran, according to the deal with European partners, would have had the right to take the money in cash and transfer it to any other country, including Iran”, said the source.

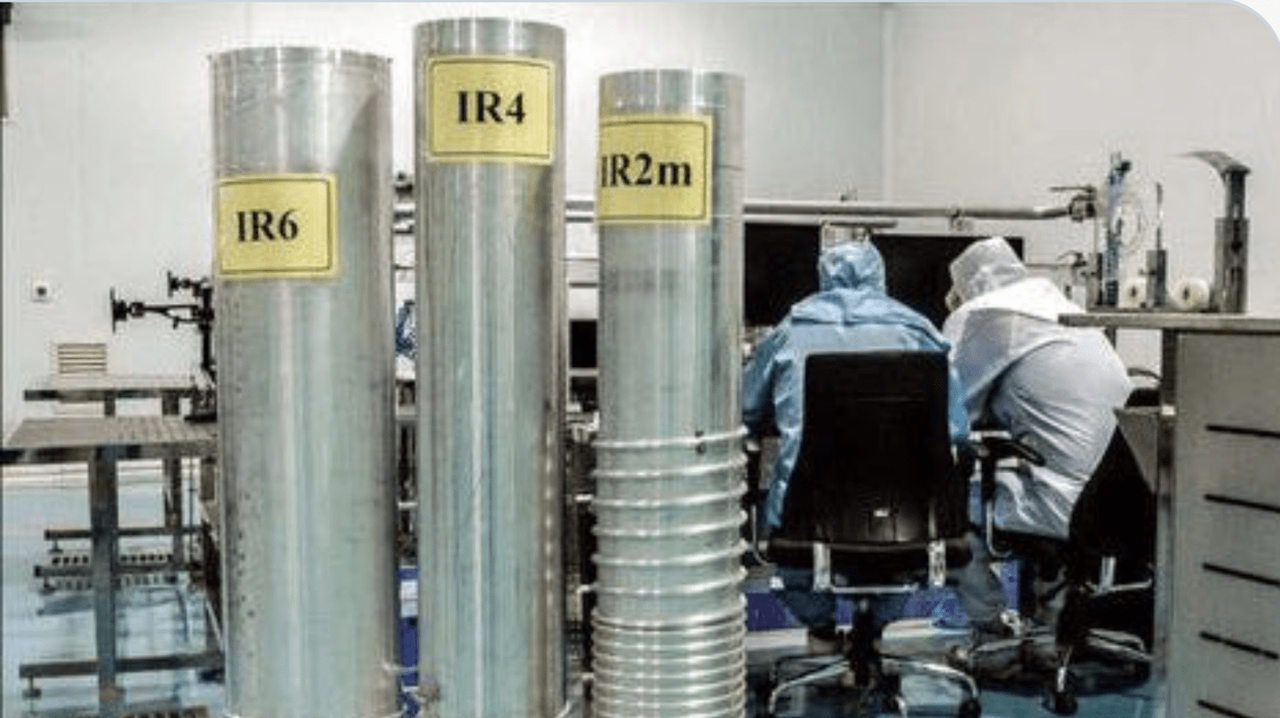

All this has been thrown to the winds. The result is simple: Iran will continue its nuclear program but will allow the International Atomic Energy Agency to monitor development. It is relying on the nuclear deal articles 26 and 36 to partially withdraw, a deal that was not signed based on trust, but on respect for law. This is the reason why Iran announced its third withdrawal step, increasing its stockpile of enriched uranium and replacing its IR-1 and IR-2m with IR-6 centrifuges (supposed to happen in 2026, as stated in paragraph 39).

Europe has used all its resources to persuade Iran from taking withdrawal steps, but to no avail. Iran has moved from a “patience strategy” to an “aggressive strategy” and will no longer accept a soft approach. It has undergone sanctions since 1979 and though it has learned to live with them, its patience is exhausted.

The US has nothing to offer to Iran but further sanctions and additional pressure on Europe, so the old continent follows its withdrawal path. The US administration planned to form various coalitions, including an Arab NATO, but failed so far to pull off any such alliance. US officials believed the Iranian regime would fall in months and that the population would turn against their leaders. Nothing of the sort happened. On the contrary: Trump and his neocons brought Iranian pragmatists and hardliners together for the same cause. The US destroyed the possibility of any moderate argument with people like Rouhani and Zarif, and showed that it was too untrustworthy for any reliable deal or agreement.

Iran FM Javad Zarif with French President Emmanuel Macron on the sidelines of the recent G7 summit, via mfa.ir

Iran is feeling stronger: it has downed a US drone, sabotaged several tankers and confiscated a British-flagged tanker despite the presence of the Royal Navy nearby. It has shown its readiness for war without pushing for it. Iran knows its allies in Lebanon, Syria, Iraq, Yemen and Palestine will be united as one in the case of war. The Iranian officials did not use revolutionary or sectarian slogans to face down US sanctions but instead managed to create national solidarity behind its firm policy of confrontation with the US. Washington, largely responsible for the status quo in the Gulf, failed to weaken Iran’s resolve and has so far been unsuccessful in undermining the Iranian economy. It is putting about the idea that its “suffocation policy” has been successful, but Iran is not giving the submission signals the US administration wants and needs, to justify the tension it has created in the Middle East and the Gulf.

Iran is handling its policy towards the US and Europe in the same way Iranians weave carpets. It takes several years to finish an artisanal carpet and many more years to sell it. The nuclear deal needed several years of preparation but even more time for establishing acceptance and the bona fides of the signatories. Trump’s simple-minded decision destroyed all that work. The US and Europe have lost the initiative. Europe is not politically in any position to stand against the US sanctions, nor does it have sufficient tools or standing to offer Iran and thus force it to the negotiating table.

Iran is becoming stronger and much more difficult to tame than in the past. It is imposing itself as a regional power and a challenge to the west. It has advanced nuclear technology and capabilities, a self-sufficient armament program and it is strengthening its allies in the Middle East.

It is difficult to foresee any negotiation between Iran and the West before November 2020, the date of the US elections.Iran is no longer willing to accept in 2019 what it signed in 2015; Trump is responsible for the new scenario. Destroying the nuclear deal now redounds to the benefit of Iran. There will be a time when the US administration, due to the realization of its ignorance in Iranian affairs, will feel regret, and will ask to return to the negotiating table – perhaps after Trump? But conditions will definitely no longer be the same and it may very well come too late to see Iran accepting what it signed for in 2015.

US Futures Drift Higher On Chinese Invitation To Bagholders, Trade And Central Bank Optimism

There wasn’t the usual trade talk optimism overnight, nor central bank trial balloons that record low interest rates will be dragged even deeper into negative territory.

Instead, what helped send European equity markets and US equity futures back in the green after an overnight slump that pushed the Emini from 2,985 to 2,965, was news that China removed one more hurdle for foreign investment into its capital markets almost 20 years after it first allowed access, when Beijing scrapped quotas for approved foreign institutional investors in domestic bond and equity markets. This means that all those WeWork bagholders who may have lost a majority of their investments, can no go ahead and lose the other have by investing in China, where the auditors have a habit of “community adjusting” everything.

In any case, the news helped send the Emini back in the green from overnight session lows just after the European open..

… with global markets back to unchanged.

Meanwhile, what we said about no central bank trial balloons, well we were kidding, because just after 7am, Reuters leaked that the BOJ “may be open to debate additional easing”, because apparently the existing easing has worked so well. According to the report, the BOJ is considering taking rates further into negative territory if it decides to ease, but other options – such as tiering – also remain on the table, Reuters reports, citing unidentified people familiar. The BOJ’s decision on whether and when to ease is expected to be a close call; conclusion may not be final until the last minute which will be just after the Fed’s own rate cut announcement. Ultimately, the BOJ’s thinking is driven by the bank’s growing less confident about early pickup in global growth

Actually, it turns out that we were also kidding about the lack of trade optimism: according to Bloomberg, China’s Premier Li said that US and China should find a solution to the ongoing trade dispute, adding that he hopes (there’s that word again) that trade talks make progress. In response there was an immediate “risk on” move as European equity indices spiked higher as a result of these headlines with the DAX Sep’ 19 futures spiking higher to 12,265 from 12,235, while the crude complex and USD/JPY also saw positive ticks. That said, the sharp move higher in US equities was less pronounced and quickly faded.

The Stoxx Europe 600 Index dropped a second day, led by financial services and health-care shares, although it rebounded following the China Li and BOJ more easing news. The pound fluctuated as embattled British Prime Minister Boris Johnson insisted he won’t ask for another Brexit delay, while U.K. wage and unemployment data beat estimates. Most euro-zone sovereign bonds nudged lower as European Central Bank officials prepare to meet.

Earlier in the session, Asian stocks fluctuated, with energy producers advancing and health-care firms retreating. Markets in the region were mixed as investors assessed the global growth outlook and China-U.S. trade negotiations with South Korea up and Thailand down. The Topix climbed 0.4%, as Japanese banks contributed most to gains following a rebound in long-term U.S. Treasury yields, which in turn pushed JGB yields modestly higher as well. The Shanghai Composite Index edged down 0.1%, snapping a six-day rising streak, with Kweichow Moutai and Ping An Insurance Group among the biggest drags. The big news out of China, as noted above, is that global funds no longer need approvals to purchase quotas to buy Chinese stocks and bonds, the State Administration of Foreign Exchange said in a statement on Tuesday. It removed the $300 billion overall cap on overseas purchases of the assets, about two-thirds of which remain unused.

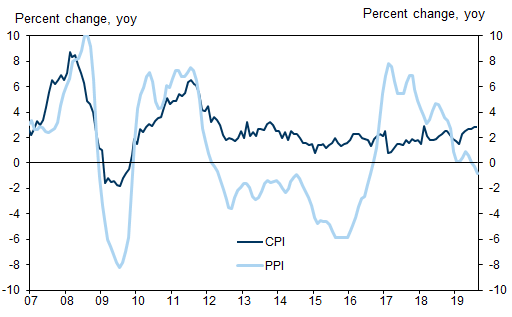

Also overnight, China reported that its headline CPI inflation was flat at 2.8% year-on-year in August, just above consensus expectations and close to the 3% policy target; in month-on-month terms, headline CPI inflation moderated to +2.9% in August from +3.5% in July. A bigger problem was the second consecutive print of negative year-over-year PPI inflation, which moderated further to -0.8% yoy in August, on both a high base (PPI up 3.6% mom s.a. ann in August 2018) and a sequential decline of 2.8% mom s.a. ann in August. Inflation in the ferrous metals sector slowed the most, followed by petroleum industry, suggesting corporate profits will be further depressed in coming months.

In emerging markets, a four-day rally in equities stalled and the risk premium on sovereign debt rose as investors marked time before the resumption of trade talks between China and the U.S. as well as central-bank meetings in coming days. Developing-nation stocks climbed almost 4% in the previous four days after China and the U.S. announced face-to-face negotiations aimed at ending the tariff war would be held in Washington next month. China, meantime, removed one more hurdle for foreign investment into its capital markets almost 20 years after it first allowed access, when it said Tuesday that global funds no longer need approvals to purchase quotas to buy Chinese stocks and bonds.

With the European Central Bank announcing its policy decision in Thursday and the Federal Reserve next up, investors are hoping on increased monetary stimulus to prop up markets. A gauge of emerging-market currencies gained for a fifth day, the longest streak since June, with South Africa’s rand leading the advance.

“Markets were oversold, rebounded and without any genuinely positive catalysts are faltering again,” said Julian Rimmer, a trader at Investec Bank in London. “Funds were clearly bearishly positioned over the summer with the salami slicing of global growth expectations, low volumes and the worldwide hunt for yield. Some of that negativity has diminished slightly so we had some short-covering and a bit more risk-on, but fundamentally nothing has changed and all those concerns are still apparent.”

In rates, European bond markets inched lower while the region’s stocks declined for a second day ahead of Thursday’s ECB policy announcement. Bear steepening resumed in the German curve although the long-end claws back some initial weakness to trade back at 0%. Peripheral spreads widened to core, with the long-end of the Spanish curve underperforming. Gilts drifted lower after robust domestic employment and wages data, but as ever, Brexit keeps any hawkish repricing in check.

The recent pullback in the bond rally “is a correction to an outsized move in yields during August, not a turn in the trend,” Kit Juckes, chief global FX strategist at Societe Generale SA, wrote in his daily note. “Last Friday’s U.S. labor market data show, clearly enough for me, that the U.S. economy is slowing slowly but steadily as the global trade slowdown infects it.”

In geopolitical news, North Korea launched 2 projectiles; a Japanese Defence Ministry official later commented that the latest North Korea missiles pose no immediate threat to Japan’s national security. Pakistani Foreign Minister has told UN Human Rights council that India’s “illegal Kashmir military occupation” raises spectre of “genocide”. Additionally, Pakistan’s Qureshi says that he sees ‘no possibility of a bilateral engagement with India’.

In FX, the Bloomberg Dollar Spot Index halted a five-day slide Tuesday as the yield on 10-year U.S. Treasuries fell 2bps, its first decline in five days. The only G-10 currency to climb against the dollar was the Swiss franc but moves were limited; meanwhile, the largest losses were seen by the Swedish krona, as the currency weakened by almost 1% to the dollar and the euro after Swedish inflation unexpectedly slowed to its lowest in three years, in more bad news for the Riksbank which is keen to increase interest rates. Finally, the Norwegian krone tumbled alongside its Swedish peer after similarly disappointing inflation reading.

Elsewhere, oil extended gains to the highest level in almost six weeks as Saudi Arabia’s new energy minister signaled his commitment to production cuts ahead of an OPEC+ meeting later this week. Gold headed for its fourth day of declines, sinking to around $1,495 an ounce. Sweden’s krona tumbled after the country’s inflation unexpectedly slowed.

Expected data include NFIB Small Business Optimism. HD Supply and Zscaler are reporting earnings

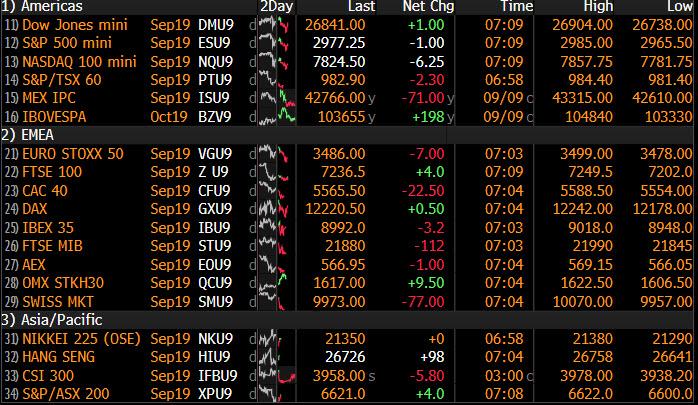

Market Snapshot

S&P 500 futures down 0.1% to 2,973.75

STOXX Europe 600 down 0.5% to 383.96

MXAP down 0.01% to 156.79

MXAPJ down 0.2% to 507.06

Nikkei up 0.4% to 21,392.10

Topix up 0.4% to 1,557.99

Hang Seng Index up 0.01% to 26,683.68

Shanghai Composite down 0.1% to 3,021.20

Sensex up 0.4% to 37,145.45

Australia S&P/ASX 200 down 0.5% to 6,614.06

Kospi up 0.6% to 2,032.08

Brent futures up 0.2% to $62.74/bbl

Gold spot down 0.2% to $1,496.06

U.S. Dollar Index up 0.1% to 98.41

German 10Y yield rose 0.6 bps to -0.579%

Euro down 0.05% to $1.1043

Italian 10Y yield rose 6.6 bps to 0.603%

Spanish 10Y yield rose 1.5 bps to 0.233%

Top Overnight News from Bloomberg

After Parliament blocked his Brexit strategy, and then refused to give him the election he wanted, U.K. Prime Minister Boris Johnson is promising to work for a deal with the EU. Monday night saw him suffer his sixth consecutive defeat in a vote in the House of Commons, after his attempt to get approval for a snap poll was rejected for a second time

The U.K. economy continued to create jobs over the summer and wages jumped, despite the escalating turmoil over Brexit. The jobless rate fell to the lowest since the 1970s but jitters weighing on the wider economy were appearing. Employment growth was weaker than forecast; vacancies slipped to the lowest since 2017

Mario Draghi needs to go out with a bang if he’s to renew a surge in bond prices that sent yields to unprecedented lows. Markets have factored in the ECB slashing interest rates and restarting QE, so it will take a multi-faceted stimulus package in his penultimate meeting Thursday to impress investors

Germany’s worship of fiscal discipline is being challenged by a looming recession and tantalizingly cheap credit — and a silent revolution is under way at the finance ministry to shed its economic dogma

Executives of WeWork and its largest investor, SoftBank, are discussing whether to shelve plans for an initial public offering of the money-losing co-working company, said people with knowledge of the talks

China removed one more hurdle for foreign investment into its capital markets almost 20 years after it first allowed access

Asian equity markets traded mixed as they followed suit to the indecisive tone seen on Wall St amid a sell-off in treasuries and as the region also digested ambiguous inflation figures from China. ASX 200 (-0.5%) was negative with gold miners frontrunning the declines in Australia after the precious metal slipped below the psychological key USD 1500/oz level but with further losses in the index stemmed by strength in the energy sector following the recent rally in oil prices, while Nikkei 225 (+0.4%) was kept afloat by favourable currency moves. Elsewhere, Hang Seng (Unch.) and Shanghai Comp. (-0.1%) gave back initial gains despite the liquidity efforts by the PBoC and firmer than expected Chinese inflation data, as the figures were largely influenced by a 10% increase in food prices amid the swine fever epidemic and also showed PPI at its sharpest contraction in 3 years. Finally, 10yr JGBs were lower following the bear-steepening seen in US and broad declines across global bonds, while the absence of the BoJ from the market today also added to the lacklustre demand.

Top Asian News

North Korea Tests More Weapons After Floating Fresh U.S. Talks

Hong Kong Leaders Grow More Frustrated by Leaderless Protesters

Hong Kong Dollar Peg Questions Seen Fading One Way or Another

Chinese Exporters Cut Currency Hedges in Sign of Yuan Pessimism

European equities are modestly softer [Eurostoxx 50 -0.3%] following on from a mixed Asia-Pac session as participants remain on standby ahead of Thursday’s ECB monetary policy decision. Sectors are mixed with underperformance in the IT sector, whilst energy names outperform as the oil complex holds onto its recent gains and banking names remain supported by yesterday’s surge in yields (RBS +4.4%, UBS +3.4%, Barclays +4.5%). In terms of stocks on the move, EDF (-7.5%) share fell from the open after the Co. noted deviations in technical standards governing the manufacture of nuclear-reactor components. On the flip side, Subsea 7 (+2.7%) shares opened higher after the Co. announced its current COO as the new CEO effective January 1st 2020, additionally the Co. were awarded an offshore contract in Saudi Arabia. Finally, JD Sports (+3%) shares are supported post earnings after H1 sales rose 47% Y/Y and the Co. forecasts FY results to be at the mid-point of their previously guided range.

Top European News

EDF Flags Issues in Reactor Parts in Blow to Nuclear Industry

Spanish Banks Risk Setback in Fight Over Unfair Mortgage Claims

Germany Doesn’t Need to Splurge to Address Slowdown, Scholz Says

Sweden Inflation Slows to 3-Year Low in Blow to Riksbank

In FX, the major underperformers in wake of softer than forecast Swedish and Norwegian inflation data that calls into question hawkish guidance from the Riksbank and Norges Bank. Eur/Sek has rebounded from sub-10.7000 levels through 10.7500 and breached several technical resistance points in the process, including 10 and 21 DMAs plus a Fib retracement, while Eur/Nok is back above 9.9000 from almost 9.8500 and also taking on board the latest Norges Bank regional network survey showing that contacts envisage slightly slower growth in the coming 6 months.

USD – The Dollar is mixed to marginally firmer awaiting this week’s top-tier US data for more input ahead of the September FOMC after last Friday’s rather inconclusive BLS report and broadly upbeat comments from Fed chair Powell, on balance. However, the DXY remains rangebound between 98.260-463 and well within near term chart support and resistance not to mention recent highs and lows for the index.

CHF/NZD/AUD – The Franc has pared some losses vs the Greenback and single currency as risk appetite wanes/falters and selling abates into key technical psychological markers, like 0.9950 in Usd/Chf and 1.1000 in Eur/Chf. Meanwhile, the Aussie and Kiwi have lost some momentum, with Aud/Usd drifting back towards 0.6850 in wake of a downturn in NAB business sentiment and dip in conditions overnight, and Nzd/Usd fading ahead of 0.6450 as Aud/Nzd meanders between 1.0645-85.

GBP/CAD/JPY/EUR – Sterling staged another attempt to hunt out stops around 1.2385 vs the Buck and briefly crossed the 100 DMA against the Euro (0.8930), but failed to sustain momentum again amidst the ongoing UK political and Brexit paralysis. However, the ensuing Pound pull-back was arrested by more encouraging data as earnings beat consensus on a headline basis and the jobless rate eased to 3.8% from 3.9%. Note also, 2 bn option expiries in Cable at the 1.2300 strike have provided a buffer. Elsewhere, trade has been considerably more rangebound with the Loonie straddling 1.3175, Yen holding within 107.19-49 parameters and Euro stuck in a 1.1037-59 band awaiting Thursday’s ECB policy pronouncements for more direction.

EM – Contrasting fortunes again for the Rand and Lira, as Usd/Zar continues its deep reversal from 15.0000+ towards 14.6900 regardless of more SA ratings warnings from Moody’s, but Usd/Try elevated above 5.7500 in the run up to this week’s CBRT rate verdict and heeding even more dovish calls (-500 bp touted in a Turkish paper) alongside the persistent threat of US sanctions.

In commodities, WTI and Brent futures are holding onto most of its recent gains with the two benchmarks around 58.00/bbl and 63/bbl respectively at the time of writing. News-flow for the complex has been light, although reports stated that Russia’s Energy Minister Novak will be meeting with newly appointed Saudi Energy Minister Abdulaziz in Jeddah later today to discuss the energy market alongside strengthening Saudi-Russia cooperation ahead of Thursday’s JMMC meeting. Meanwhile, Nigeria’s Finance Ministry notes of strong indications of an oil glut next year, and thus lowered its benchmark forecast to 55/bbl from 60/bbl. This evening will also see the release of EIA’s Short-Term Energy Outlook with focus on global demand growth forecasts. Looking further ahead, participants will also be eyeing the weekly API crude inventory data with markets expecting a headline drawdown of 2.5mln barrels. Elsewhere, gold prices are largely unchanged below the 1500/oz mark amid the undecisive risk tone in the market ahead of this week’s key events. Meanwhile, copper prices have seen a more pronounced downside compared to yesterday with the red-metal flirting with 2.60/lb to the downside at the time of writing. Finally, Dalian iron ore prices advanced as much as 4% amid expectations that China will ratify further economic stimulus that would boost steel demand.

US Event Calendar

6am: NFIB Small Business Optimism, est. 103.5, prior 104.7

10am: JOLTS Job Openings, est. 7,331, prior 7,348

DB’s Jim Reid concludes the overnight wrap

Every year in early September the financial world takes in a new breed of graduates and to you all I say welcome and good luck in your career. If you’d have started as a newbe last Thursday then the whole of your career would have been in a big bond bear market. You’d be excused for wondering if bonds ever actually rally. Indeed yesterday saw another fixed income sell-off, as reports on the German fiscal stance and positive comments on the US-China trade war supported investor sentiment. 10yr Bund yields rose +5.3bps, reaching their highest level in nearly a month at -0.59%, while 30y bunds rose +7.8bps but after spending much of the day in positive territory closed at -0.003%. Nearly but not quite. Lending to the German government out to 2049 will still involve a small haircut. For context the long run return on US equities has been around 9% p.a. over the last couple of hundred years and by my calculations that would mean you would earn 13 times your original investment over an average 30 year period through history. Even at the lower long run return for German equities of c.8% you would earn over 10 times your original investment over the same period. I’m not wildly excited about current equity valuations but this is food for thought for all you new graduates as you invest for your retirement. It’s too late for us but you can save yourselves.

The bond sell-off was global with 10y Treasuries up +7.7bps, BTPs up +6.7bps, and Gilts +8.5bps. Yield curves also steepened, with US 2s10s up +3.2bps to 4.9bps and to its highest level in three weeks. In credit, spreads widened in Europe, with Euro IG spreads +2.0bps and at a 7-week high, while Euro HY spreads were flat. In the US it was a different story as IG and HY spreads tightened further, down -1.3bps and -9bps respectively. Safe havens sold off across the board however, with gold down -0.53%, while the Swis Franc was the worst performing G10 currency, down -0.48% against the dollar, followed by the Japanese Yen (-0.32%).

The sell-off came as Reuters reported that Germany is considering creating a “shadow budget”, which would allow the government to get round the country’s fiscal rules. This would be done by setting up independent bodies, which could take advantage of the country’s low borrowing costs and invest in “infrastructure and climate protection”, but this spending would not count under the debt brake. Meanwhile, the euro strengthened after a letter obtained by Bloomberg News showed Bettina Hagedorn, a deputy finance minister, wrote that the government could change its plans to run balanced budgets if the economic situation required. The reports come ahead of this morning’s debate on the 2020 budget, which will be taking place in the Bundestag. These stories have become more frequent in recent weeks and whilst the market always gets more excited by the headlines than is justified by hard evidence of any change in policy, it’s fair to conclude that market pressure and chatter on this story is building.

Other drivers behind the bond sell-off included data which showed German exports unexpectedly rising by +0.7% (vs. -0.5% expected) in July, while imports fell by -1.5% (vs. -0.3% expected), sending the current account balance for July up to 22.1bn (vs. 16.4bn expected). So good news on exports even if declining imports might be demand led. Meanwhile comments from Secretary Mnuchin further helped things, as he said “we’ve made a lot of progress” in the trade talks, ahead of the planned meeting between China and the US in Washington next month. Ahead of Thursday’s much-anticipated ECB meeting, these positive developments seem to have marginally reduced the implied odds that markets have given to a larger 20bps reduction in the deposit rate, which now stand at 44%, having been at 61% just a week ago.

In equity markets, US stock indices were mixed with relatively high divergence between sectors. The S&P 500 ended just about flat (-0.01%) while the DOW gained +0.14%. Relatively more of the DOW is made up of bank stocks, which performed well (+3.15%) amid the higher yields. Tech lagged, with the NASDAQ down -0.19%. In Europe, the picture was similarly mixed, with the STOXX 600 losing -0.28%. Much of the fall came from UK stocks, with the FTSE 100 -0.72% as it reacted to sterling’s appreciation, but the CAC 40 (-0.27%) also declined, while the DAX and the FTSE MIB only made modest gains. European banks mirrored their American cousins’ positive performance, with the STOXX Banks up +2.72% on rising yields, while energy stocks also saw gains as Brent Crude rose +1.85% to reach a one-month high.

Overnight in Asia, markets are trading mixed with the Nikkei (+0.36%) and Kospi (+0.37%) both up while the Hang Seng (+0.08%) is trading flattish and the Shanghai Comp (-0.36%) is trading down. In Fx, all G10 currencies are slightly weaker against the greenback this morning with the exception of the New Zealand dollar (+0.19%). The onshore Chinese yuan is trading up c. 0.1% at 7.1164. Sovereign bond yields have ticked up in Asia this morning following the global sell-off with 10y JGB yields up +2.9bps at -0.234%. Elsewhere, futures on the S&P 500 are trading flattish (-0.06%) while WTI crude oil is up +0.45% after Saudi Arabia’s new energy minister signaled his commitment to production cuts ahead of an OPEC+ meeting on Thursday in Abu Dhabi to discuss their production pact. In terms of overnight data releases, China’s August CPI and PPI both came in one tenth higher than consensus at +2.8% yoy and -0.8% yoy, respectively.

In other news, top North Korean diplomat Choe Son Hui issued a statement this morning that the country would be willing to hold nuclear talks with the US, “at the time and place to be agreed late in September.” However, shortly after the statement North Korea fired two “short-range projectiles” into its eastern seas. Meanwhile, President Trump was a bit cautious in his response over the North Korean statement, citing the regime’s continued freeze on nuclear weapons testing and added, “We’ll see what happens, but I always say having meetings is a good thing, not a bad thing.”

In the UK, MPs rejected the chance of having a mid-October general election for the second time in a week, as the motion failed to reach anything close to the required two-thirds majority once again (239 to 46; PM Johnson needed 434 to call an early election). Opposition parties mostly abstained as they want Mr Johnson to be forced to ask for an extension he has said he will never do. Parliament has now been prorogued, so it won’t sit again until October 14th, which is also the week of the next European Council Summit. The political chatter now points to a late November election but there will be an incredible amount of water flowing under the bridge between now and then. Mr Johnson seems to have pushed his energy into getting a deal now but that is as far away as it ever has been. I wonder whether he may have one go at passing a deal through Parliament before October 31st just to show the electorate that he did everything he could to deliver Brexit by that date and hope the leave vote feels emboldened to vote for him by Parliament’s likely rejection of it.

DB’s Oli Harvey published his latest Brexit update yesterday (link here ), where his base case is that the government fails to secure agreement with the EU27 at the October Council meeting, leaving Johnson with a choice between requesting an extension, resigning as Prime Minister, or ignoring or circumventing the legislation. Looking at his full probabilities, he maintains his view that the cumulative probability of a no-deal Brexit is 50%, be that either at the end of October or after a general election, and places just a 10% chance on Johnson completing his aim of a successful renegotiation and a ratified Withdrawal Agreement by the end of October.

Earlier in the day, sterling rallied as markets approved of the more conciliatory remarks from Prime Minister Johnson, who described a no-deal Brexit as “a failure of statecraft”, and said that “I would overwhelmingly prefer to find an agreement.” The currency strengthened +0.49% against the dollar to its highest level in over a month.

In terms of data yesterday, as well as the aforementioned German export numbers, UK GDP surprised to the upside, with the economy growing by +0.3% mom in July (vs. +0.1% expected). All sectors outperformed, with services +0.3% (vs. +0.1% expected) and manufacturing production +0.3% (vs. -0.3% expected). Looking at the whole 3 months to end-July the UK economy saw a flat 0.0% growth rate over the previous three months.

Meanwhile the Federal Reserve’s consumer credit numbers showed a $23.29 billion expansion in credit, the largest monthly increase since 2017. Revolving credit, which includes mostly credit card debt, drove the increase as it rose by $10 billion, also the highest since 2017. Separately, the NY Fed’s inflation expectations survey showed 1-year expectations falling to their lowest level on record at 2.4%, while 3-year expectations also fell, by 0.1pp to 2.5%.

Looking at the day ahead, data releases include France’s July industrial and manufacturing production, along with Italy’s July industrial production. In the UK, the monthly employment report, including the unemployment rate and average weekly wage growth will be released, while from the US, we have the NFIB small business optimism index and the JOLTS job openings release.

After 31 years of marriage, Todd Palin – the husband of former Alaska governor and vice presidential candidate Sarah Palin, has filed for divorce.

In the April 29th filing eight days after their most recent anniversary, Todd cited “incompatibility of temperament” and that the couple “find it impossible to live together as husband and wife” in his request to dissolve their marriage in Anchorage Superior Court.

The filing, first reported by the Anchorage Daily News, only uses initials but details the couple’s marriage date and the birth date of their 11-year-old son, Trig, and asks for an equal separation of assets and debts.

The Palins, both 55-years-old, have been together through Sarah’s rise to governor of Alaska in 2006, her resignation in 2009 (before the end of her four-year term), and her brief tenure as John McCain’s running mate in the 2008 presidential election – losing to Barack Obama and Joe Biden. According to the New York Times, McCain regretted picking Palin vs. Joe Lieberman.

McCain’s daughter, current “The View” host Meghan McCain, wrote in her 2010 book, “Dirty Sexy Politics,” that Palin brought “drama, stress, complications, panic and loads of uncertainty” to the campaign, but also lauded the enthusiasm she generated. –ABC News

While Todd Palin has avoided the spotlight, Sarah Palin has been a frequent political commentator on cable news, and wrote the book “Sweet Freedom: A Devotional.”

Trump SCOTUS Pick Neil Gorsuch Says US Is In “Civility Crisis”

In his first book since being appointed to the Supreme Court to fill the seat vacated by Antonin Scalia, Neil Gorsuch writes that the US is facing a “civility crisis” and that the president and Congress are both guilty of violating the separation of powers laid out in the Constitution.

The book, “A Republic, If You Can Keep It”, has a title that reflects Benjamin Franklin’s reported reply as he left the Constitutional Convention in 1787. In it, Gorsuch describes his vision for the Supreme Court’s proper role: That judges should interpret the constitution according to its original meaning, and therefor overturn ObamaCare, slash abortion rights and bolster gun rights, according to Bloomberg.

Gorsuch also describes the run-up to his nomination. For example, he and his wife caught their flight to Washington after a neighbor drove them down a bumpy farm track so they wouldn’t be spotted by reporters staking out the family house in Colorado.

The Justice said the drive left a lasting impression on him.

“That drive threw me face first into the topsy-turvy world of modern-day Supreme Court confirmation battles,” Gorsuch writes in the 323-page book, officially released Tuesday. He was confirmed on a 54-45 vote, with only three Democrats voting in favor.

Notably, Gorsuch’s book makes only passing reference to President Trump, even though the president is often blamed for “coarsening” the public discourse.

But he does point to surveys showing that “incivility” is broadly deterring Americans from dedicating themselves to public service.

“Without civility, the bonds of friendship in our communities dissolve, tolerance dissipates, and the pressure to impose order and uniformity through public and private coercion mounts,” Gorsuch, 52, writes.

Gorsuch also lamented the fact that the executive branch and legislative branch had grown beyond their proper spheres.

“The framers firmly believed that the rule of law depends on keeping all three governmental powers in their proper spheres,” Gorsuch writes.

Gorsuch also complains about more “niche” issues, like the rising cost and complexity of the US legal system.

“Our civil justice system is too expensive for most to afford; our criminal code is too long for most to comprehend; and our legal education system is too monolithic to allow lawyers to serve clients as affordably and well as we might,” he writes.

The rest of the book, which was co-authored by two of the justice’s former law clerks, is a compilation of the Justice’s speeches and court opinions. But the book also includes newly written original sections.

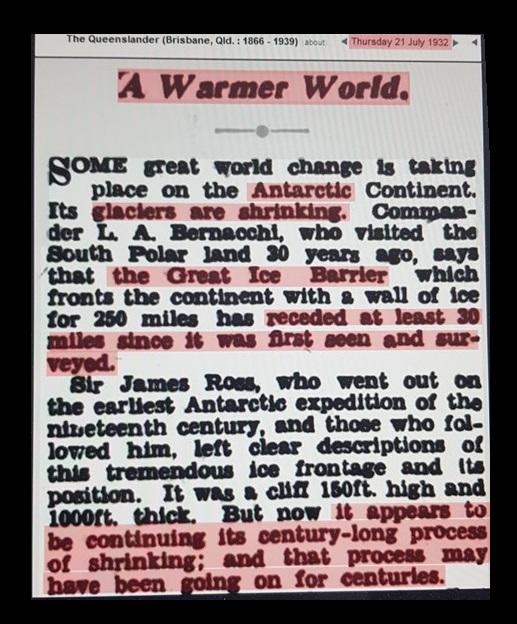

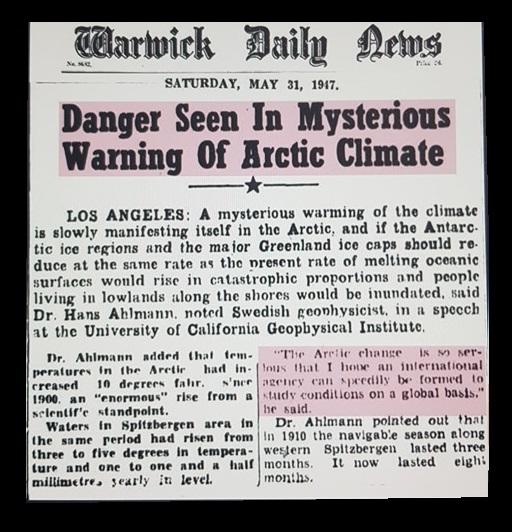

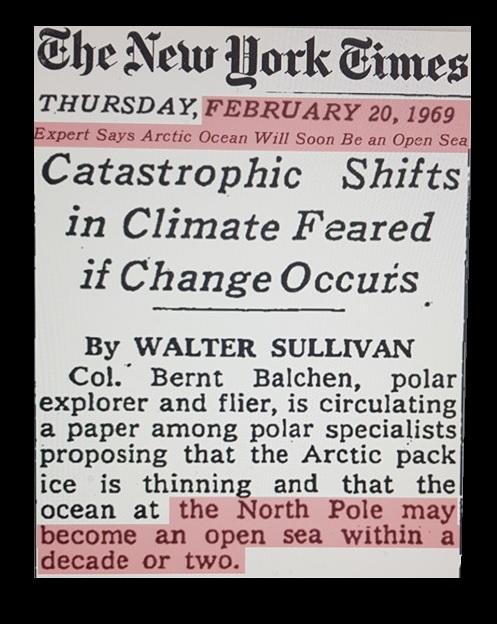

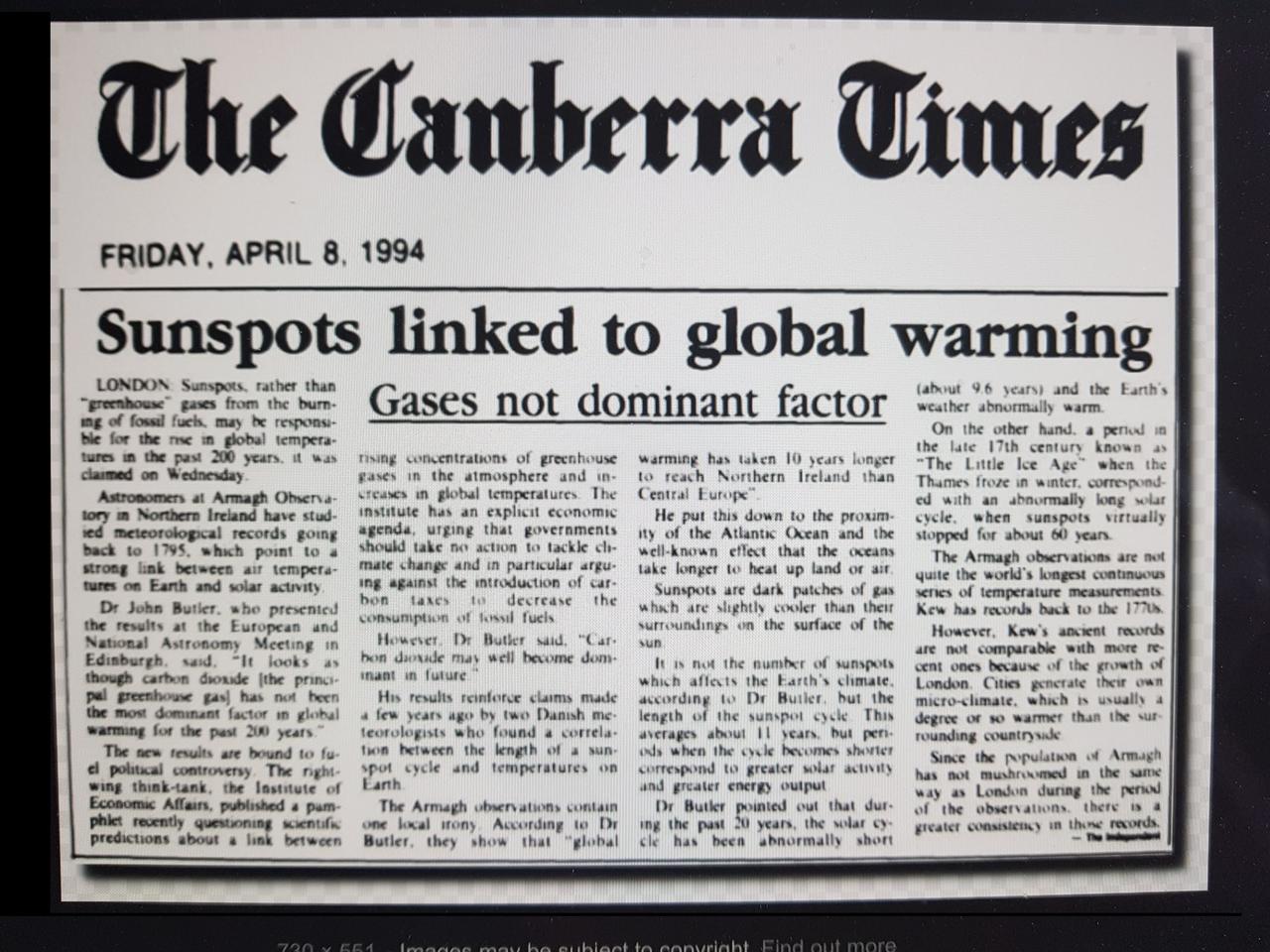

ANSWER:For whatever reason, these people have been promoting that the cities will all sink and we are the cause of it all.

They have been touting this scenario since the 1930s when there was the Dust Bowl. It resurfaced after World War II when they were trying to stop rebuilding industry and the housing market which had been destroyed. The same argument appeared again in the 1960s when there was a great expansion in housing.

However, during the 1970s when things got colder, everything flipped upside down and then it was global cooling that would destroy civilization.

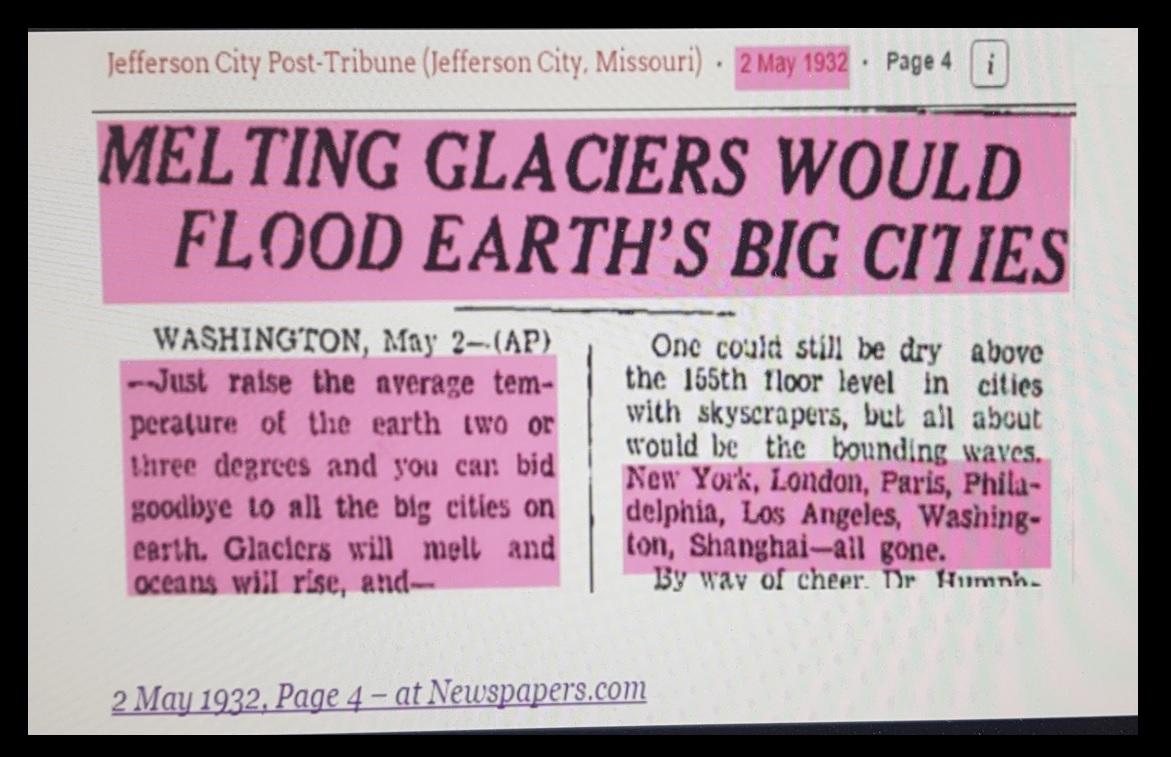

On April 28, 1975, Newsweek magazine published an article in which they sounded the alarm bell and proposed solutions to deliberately melt the ice caps:

“Climatologists are pessimistic that political leaders will take any positive action to compensate for the climatic change, or even to allay its effects. They concede that some of the more spectacular solutions proposed, such as melting the arctic ice cap by covering it with black soot or diverting arctic rivers, might create problems far greater than those they solve. But the scientists see few signs that government leaders anywhere are even prepared to take the simple measures of stockpiling food or of introducing variables of climate uncertainty into economic projections of future food supplies.”

Then TIME magazine’s January 31, 1977 edition had the cover story featuring “The Big Freeze.” They reported that scientists were predicting that Earth’s average temperature could drop by 20 degrees fahrenheit. Their cited cause was, of course, that humans created global cooling. It just seems that humans are so powerful we can alter the universe but cannot manage to create corrupt-free governments.

The difference this time is they have been able to get governments interested on the basis that they can stop it by raising taxes. Canada imposed a $1,000 tax per home to stop global warming. Perhaps the theory is if the politicians get more money they will speak less and reduce the hot air they spout out by yelling the end is near.

I see this as a derivative of the Populationists theory which was instituted by Thomas Robert Malthus (1766-1834). It was Malthus who first published his “Essay on thePrinciple of Population as it Affects the Future Improvement of Society” in 1798. He published it anonymously, afraid to put his name on it, but he was soon discovered to be the author. Malthus argued that the resources of production would be exceeded by the population leading to real misery.

Malthus’ theory proved to be completely wrong because he too failed to comprehend that there are cycles to everything. He never considered the cycle in technology and how farming has improved from ancient times up to his own time during the 18th century. Of course, food production has more than kept pace with population growth and even the population goes through cycles. Currently, birth rates have been declining. Then there are diseases and plagues that visit our societies, not to mention war, which all combines to thin the herd so to speak.

The climate has ALWAYS moved cyclically. Anyone who dares to argue that climate change is NOT caused by humans is ridiculed because this is a political issue being used to raise taxes and to regulate human activity by removing ever-greater proportions of our human rights and freedom. Those who attack anyone who denies human-induced climate change are either brainwashed or have a self-interest in the entire scam.

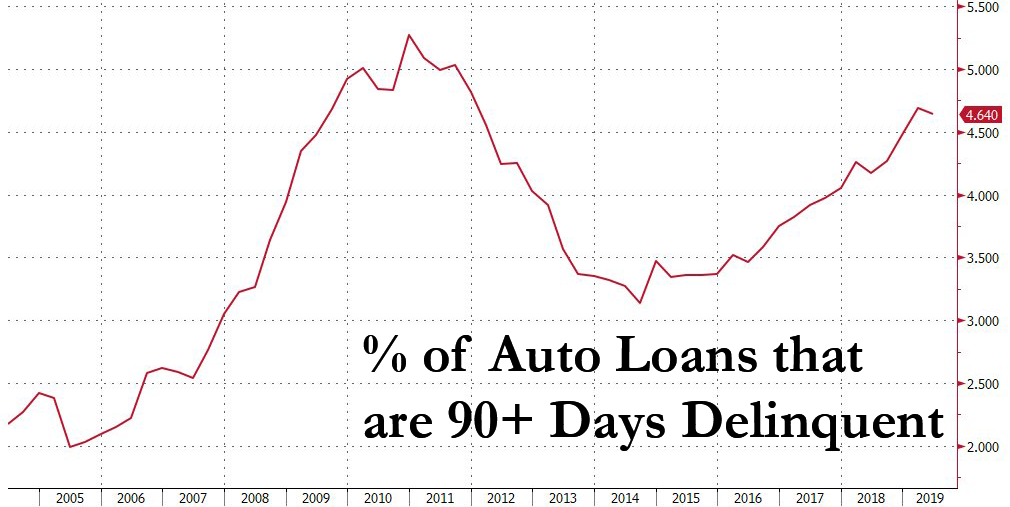

Shades Of 2007: Subprime Auto Lender Verified Income On Only 3% Of Loans In Latest Bond

The US subprime auto industry is doing everything in its power to recreate another 2008 crisis. After all, it takes a (Potemkin) village.

One of the largest subprime auto finance companies, Santander Consumer USA Holdings, verified the income on less than 3% of borrowers this year, according to Bloomberg. And in painfully vivid shares of 2008, it then took those loans and bundled them into more than $1 billion in bonds sold this year.

This laughable number which was taken straight from the Countrywide playbook (“If they can fog a mirror, we’ll give ’em a loan“) was down from 17% for loans for various asset-backed securities issued as recently as 2017. For comparison, GM Financial’s AmeriCredit, another major ABS issuer, verified income on about 68% of loans for a deal it priced in June and 66% of loans that it priced for a deal in March, according to Bloomberg.

And no, you didn’t read that wrong: according to Moody’s – which this time has no intention of getting blamed for the bursting of the biggest asset bubble in history – Santander’s ABS priced in June had 2.6% of loans verified for income and the one priced prior to that had 3.2% checked.

Another transaction being marketed by Santander will also be in the 3% range “or possibly lower”, said Moody’s analysts. Borrowers involved in the bond that Santander is currently marketing have an average FICO score of 581 and are paying an average annual interest rate of 18.9%.

What can possibly go wrong? Oh wait, everything, because as Bloomberg notes, these ridiculously lax underwriting standards is why expected losses on Santander subprime auto bonds are higher than bonds from its peers, Moody’s analyst Nicky Dang said. Moody’s expects average losses up to 17% for loans underlying the bonds from Santander’s typical subprime series of transactions, although it forecasts losses of 24% for the deal currently marketing, which is from a deeper subprime series. In comparison, expected losses for comparable peers are roughly half, and stand at about 10% for similar subprime auto ABS from GM Financial.

The decline in Santander’s income verification levels suggest the obvious that there is a higher chance of borrowers having weaker credit profiles than they have stated.”

Santander didn’t comment, but instead pointed to information on its earnings calls stating that the percentage of income verification has decline as the company is working to refine its processes of screening high risk dealers and borrowers from its securitizations. Meanwhile, we guess that just means give up on income verification altogether?

Santander also claims that the “performance of those transactions has been consistent or better than the historical deals that had a higher percentage of income-verified loans.” We’ll check back in on this statement in 12 months, although at the rapid surge in 90+ day delinquent auto loans, we doubt we will have to wait nearly that long.

Meanwhile, ratings firms have demanded higher levels of credit protection in deals over recent years to mitigate increasing delinquencies in underlying loans, although judging by Santander’s actions, they did not get them.

Moody’s Dang said: “Income verification is only one part of the entire underwriting process for the loans. It’s only one factor that is baked into the historical deal performance we’ve seen, which has generally been consistent and stable.”

Then again, considering that one of the biggest subprime auto lenders barely bothers with any income verification we won’t be holding our breath to find out just how much more thorough it has been with the remainder of underwriting process checklists. On the other hands, those who naively hold their money at Santander, may want to consider doing just that as their funds now appear to be collaterlized by billions in worthless subprime auto bonds.

Hungary’s populist Prime Minister Viktor Orbán says the “sickness of Europe” is the continent’s native population decline as he urged for more incentives to encourage citizens to have children.

During a speech at Budapest’s 3rd Demographic Summit, Orbán warned that the biggest problem Europe faced was demographic suicide.

“Why is this the case? It’s most certainly not because of some sickness of Christian civilization – after all, the number of Christians are rising all around the world. This is a sickness of Europe in general,” he said.

The Prime Minister said that the solution was not to import vast numbers of migrants, asserting, “We must never accept population exchange.”

According to Orbán, the remedy should be to ensure that families were financially rewarded for having children, not punished.

“We win only if we can build a system where those who bear children live significantly better than if they hadn’t started a family,” he said.

Orbán emphasized that the west was doomed if the current model of atomization and demographic decline isn’t halted.

“Without families and children, the national community will disappear,” said Orbán, adding, “and if a nation disappears, something irreplaceable will disappear from the world.”

As we previously highlighted, as part an effort to boost the country’s population without having to rely on mass migration, Hungary will hand out €30,600 to married couples who have three or more children.

A married couple receives the €30,600 as a loan from the government upon getting married. The loan then has to be repaid until the couple has three children. At this point, the debt is completely forgiven.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Plastic Apocalypse: Dangerous Microplastics Now Turning Up In Human Stool

Last month we revealed how high levels of dangerous microplastics had been detected in some of the most remote regions of the world. Now there are new reports that microplastics are turning up in human stool, a new study suggests.

“This small prospective case series showed that various microplastics were present in human stool, and no sample was free of microplastics,” wrote the team of scientists, led by Dr. Philipp Schwabl of the Medical University of Vienna.

“Larger studies are needed to validate these findings. Moreover, research on the origins of microplastics ingested by humans, potential intestinal absorption, and effects on human health is urgently needed.”

Schwabl said volunteers came from Japan, Russia, the Netherlands, the United Kingdom, Italy, Poland, Finland, and Austria. Their daily food intake was the likely entry point for microplastic exposure.

The study didn’t rule out that microplastic exposure could be coming from food wrappers and bottles. None of the volunteers were vegetarians, while six out of the eight had consumed ocean-going fish.

All stool samples were examined at the Environment Agency Austria for ten different types of plastics. As many as nine plastics were found in sample stool, ranging in size from 50 to 500 micrometers. Schwabl said the most common plastics were polypropylene and polyethylene terephthalate.

On average, each stool sample contained about 20 microplastic particles per 10g of stool.

The study wasn’t entirely sure where the microplastics came from or how they were ingested, but because there were various types of plastics, Schwabl said the sources could be from food processing and packaging to seafood consumption.

Since microplastics is relatively a new topic for the scientific community – health impacts, of tiny bits of plastics in human bodies are still unknown.

“Discussion is ongoing about the potential health effects of ingested microplastics and nanoplastics, which (at least in animals) may translocate into gastrointestinal tissues or other organs and cause deleterious effects,” he noted.

Jennifer Adibi, an assistant professor in the department of epidemiology at the University of Pittsburgh Graduate School of Public Health, told Reuters that the new study offers “no insight into health implications” of microplastics in the human body.

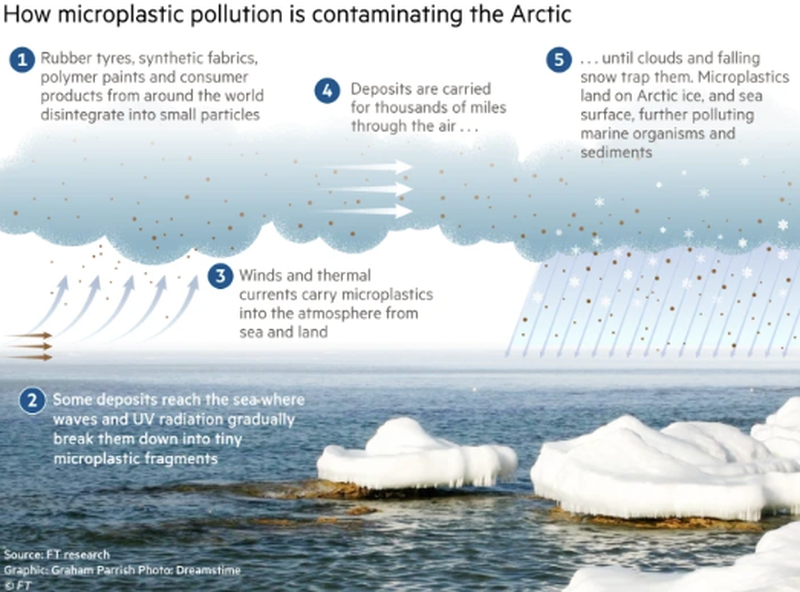

Our report from last month shows how microplastics come from industrial economies where rubber and paints are used.

The tiny fragments end up in the sea, where they’re broken down by waves and ultraviolet radiation, before absorbing into the atmosphere. From there, the plastic particles are captured from the air during cloud development, can drift across the Earth via jet streams. At some point, the particles act as a nucleus around supercooled droplets can condense, and travel to Earth as snow or other forms of precipitation.

As far as environmental and health impacts of microplastics, these two studies could suggest a silent plastic apocalypse has infected Earth.

The psychological condition known as Stockholm Syndrome, in which hostages irrationally sympathize with their captors, could well be applied to European leaders when it comes to US bullying.

The US has always been the dominant –and domineering– party in the transatlantic relationship. But past administrations in Washington have been careful to indulge European states as “partners” in a seemingly mutual alliance.

Under President Donald Trump, the Europeans are pushed around and hectored in a way that shows their true status as mere vassals to Washington.

Take the Nord Stream 2 project. The 1,220-kilometer-long undersea pipeline, which will significantly increase delivery of gas to Europe, is due to be completed by year’s end. The new supply stands to benefit the European Union’s economy, in particular Germany’s, by providing cheaper energy fuel to drive businesses and heat homes.

Yet last week, US Senator Ted Cruz threatened that his country “has the ability to halt” the entire project being completed. Cruz is on the Senate Foreign Relations Committee which in July passed a bill that will impose sanctions on companies involved in the construction of the pipeline. Germany, Austria, France and Britain are part of the building consortium, along with Russia’s Gazprom.

Ironically, the Senate bill is called ‘Protecting Europe’s Energy Security’. It’s a curious form of ‘protection’ when US-threatened sanctions will deprive European businesses and consumers of affordable gas. Cruz, as with President Trump, has accused Russia of trying to tighten its economic grip on Europe. Closer to the truth, and more cynically, Washington wants Europe to buy its more expensive liquefied natural gas. Texas, the biggest source of US gas, is Cruz’s home state. Maybe his bill should be renamed ‘Protecting American Energy Exports.’

Related to that is the wider imposition of sanctions by Washington and Europe against Russia since 2014. Several reasons are cited for the punitive measures on Moscow, including alleged destabilization of Ukraine and the ‘annexation’ of Crimea, alleged interference in elections, and the dubious Skripal poisoning affair. The sanctions policy has largely been promoted by Washington, with Europe dutifully following.

Last week, EU ambassadors voted to extend sanctions for another six months, in spite of the fact that they have been substantially more harmful to Europe’s economy than America’s, and in spite of the fact that German businesses in particular are opposed to the futile economic hostility towards Moscow.

The lack of any European pushback to such blatant American interference in its supposed sovereignty and independence on matters of vital interest is simply astounding.

Another glaring example is the way the Trump administration is insisting that European states abandon major investment plans with the Chinese telecoms firm Huawei to modernize mobile phone and internet infrastructures. Washington hasthreatened reprisal sanctions if Europe goes ahead in partnering with Huawei. The US has also warned that it may withhold “intelligence sharing” from European “allies” on security and terror risks. How’s that for a ‘friend’?

Again, there is the same pattern of mealymouthed acquiescence from European leaders, instead of a robust censure to the US to mind its own business.

The international JCPOA nuclear accord with Iran is another crowning demonstration of the fundamentally abusive relationship Washington has with Europe. This week, the Trump administration poured cold water on a French proposal to extend a $15 billion credit line to Tehran. The French move was meant to ease economic pressure on Iran and to keep it onboard the faltering nuclear accord.

Washington declared that “it will sanction anyone buying Iranian crude oil exports”. There will be no waivers or exceptions to American sanctions. That pretty much tells the European Union to forget about its hesitant efforts to save the Iran nuclear deal, to which it is a signatory, along with Russia and China.

So, because Trump crashed out of the accord, that means the Europeans have to as well, in his domineering view. Evidently, the EU has no freedom to act independently from American diktat. Wrecking relations between Europe and Iran will jeopardize economic interests and security concerns over conflict and non-proliferation of weapons in the region. Are European concerns so irrelevant to Washington?

Now steel yourself for the following stupendous double-think. US Secretary of Defense Mark Esper last week lectured European “friends” to be more vigilant in fending off alleged Russian and Chinese malignancy.

Speaking at the Royal United Services Institute think tank in London, it was billed as a showpiece address, Esper’s first major speech since becoming Pentagon chief in July.

“It is increasingly clear that Russia and China want to disrupt the international order by gaining a veto over other nations’ economic, diplomatic, and security decisions,” he said.

“To put it simply, Russia’s foreign policy continues to disregard international norms,” added the former lobbyist for Raytheon and other American weapons manufacturers, without a hint of shame.

Europe’s response? Did European leaders and media laugh uncontrollably at such patent absurdity, hypocrisy and vice-projection? Were there stern official statements or editorials telling the American representative for the military-industrial complex to not insult ordinary intelligence?

Europe’s tolerance for abuse by its American ‘partner’ really does invoke a Stockholm Syndrome problem. Sure, sometimes the European leaders like Merkel or Macron snivel about the need to be more independent from Washington, but when the chips are down, they all show a contemptible toadying to American policy even when it is actually damaging to their own national interests.

When Trump recommended that Russia be admitted to the Group of Seven economic powers at last month’s summit in France, the rest of the group reacted in horror, demanding Moscow’s exclusion. How twisted is that? The pathetic European leaders want to stay in a club with their biggest tormentor – Washington – while shutting out a country which is a neighbor and a potentially important strategic partner. How irrational can you get?

Psychologists explain Stockholm Syndrome as a “coping mechanism” to deal with trauma. It is observed among hostages, prisoners of war, survivors of concentration camps, slaves and prostitutes. Irrational sympathy with a party that actually inflicts hardship and injury is a way to minimize trauma by seeming to adopt the same values.

Apparently, the syndrome can be treated. Victims have to gradually be introduced to the objective truth of their situation. Europe needs to wake up from delusions about its American ‘ally.’

{kind=link}

{kind=link}