In the wake of the economically disastrous covid-19 shutdowns, the political class has desperately tried to save the failing euro system. On July 21 European leaders agreed on what they called a “historic” deal. It was nothing more than a multitrillion euro stimulus package. However, it is more probable that the “recovery fund” will delay any chance of a much-needed economic restructuring taking place. What it will do is waste scarce resources and capital while setting Europe up for another financial and debt crisis. Another even more important issue is the dangerous path toward political centralization the EU is heading down as a result of the crisis. The European Parliament is very much dominated by pro-centralization forces and contains few individuals who defend the principles of decentralization and economic freedom while seeing with great concern the ever growing power of Brussels.

Has the social democratic project for the EU prevailed?

The Classical Liberal View: Economic Union, Political Decentralization

Even before the signing of the Treaty of Rome in 1957, which created the core institution that later became the EU, there have been tensions between the two paths that a European union should take. The tension is between the classical liberal vision and the social democratic vision. The liberal vision puts its primary focus on defending individual freedom and respecting property rights while promoting a European free trade zone with a robust free market. The treaty of Rome was a major victory for the liberals, as it was built on two basic principles: freedom of movement and the free circulation of goods, services, and financial capital. In short, the treaty aimed at the restoration of rights and values that had been lost during the early twentieth century as nationalism and socialism prevailed in the European Continent.

The liberals also tended to emphasize decentralization, as there is plenty of evidence that decentralization has not been an obstacle to economic progress in Europe. Italy, Germany, and Switzerland (to this day) experienced great progress: competition among varying kingdoms led to more freedom, setting the stage for the creation and rise of the merchant, banking, and urban middle class. Without this the Industrial Revolution, which also took place in an era of decentralization and free trade, would not have been possible.

In a modern “unified” Europe, competition is crucial if the classical liberal vision is to prevail. If currency competition existed, different monetary authorities would be forced to compete, while tax competition would allow people to vote ‘’with their feet” by leaving countries with high taxes.

But this is not a popular view in today’s European Commission.

The European Social Democratic Project

In contrast to the classical liberal vision, the social democrats view Europe as a protectionist and interventionist empire. The predecessor of this vision was the Napoleonic vision, but the key difference with the EU is that its centralization of power wouldn’t happen through military means, but through legislation and the political process. The European Central Bank, the European Commission, and European Parliament have been very effective when it comes to this task. As economic ties between countries have grown, Europhile politicians have effectively managed to create a pan-European welfare redistribution scheme.

Poorer countries in southern Europe have been unable to cope with the growing regulatory state, but subsidies and wealth transfers from the rich north have helped the southern members adapt to new EU rules while also making poorer members dependent on EU subsidies.

The Euro Is a Political Project

Moreover, EU wealth transfers, combined with a single currency, have allowed poorer countries like Greece, Spain, and Italy to increase government spending and debt while taking few steps to strengthen their private sectors. In other words, centralization, both monetary and fiscal, has allowed the poorer members of the south to follow unsustainable economic and monetary policies.

These trends were in place even before the 2008–09 financial crisis. And then came the bailouts of the Great Recession era and now the covid-19 crisis.

The bailouts during the 2009 debt crisis didn’t only come with an economic cost but with a political one: nation-states gave up their control of internal issues and follow more and more instructions and orders from Brussels on how to run their countries, with grave consequences if they don’t comply. Ron Paul was right when he said that the corruption and political ambition of Europhile politicians and bankers turned the EU into “an unelected bully government in Brussels, where the well-connected were well compensated and insulated from the votes of mere citizens.”

Conclusion

Europe needs more than ever the principles that made it successful: decentralization, free trade, and sound markets. Brexit can be the start. We need a Europe of Switzerlands and Lichtensteins rather than a United States of Europe. A step in the right direction would be a reform toward a pure free trade zone between sovereign states instead of a political union. The common currency would need to be abolished; a currency competition system would be preferable, as suggested by F.A. Hayek.

The union has created a huge division between northern and southern countries, with citizens becoming very suspicious and hostile toward each other. Germans, for example, view southern Europeans as lazy and unproductive while southern Europeans view the Germans as the true rulers of their country. Divisions along similar lines have been around since the early twentieth century, but the EU’s centralization scheme has made them worse. This is exactly the opposite of what the creators of the EU promised.

Now, the European project may be failing, and there are two available options for the future. Either the citizens of Europe recognize the dire consequences of a pan-European welfare redistribution scheme and they refuse to go along with the coming bailouts, wealth transfers, and efforts at renewed political centralization, or we head toward a path of repeated banking and debt crises leading to high inflation and political centralization with even bigger problems down the road.

via ZeroHedge News https://ift.tt/3jZZsaT Tyler Durden

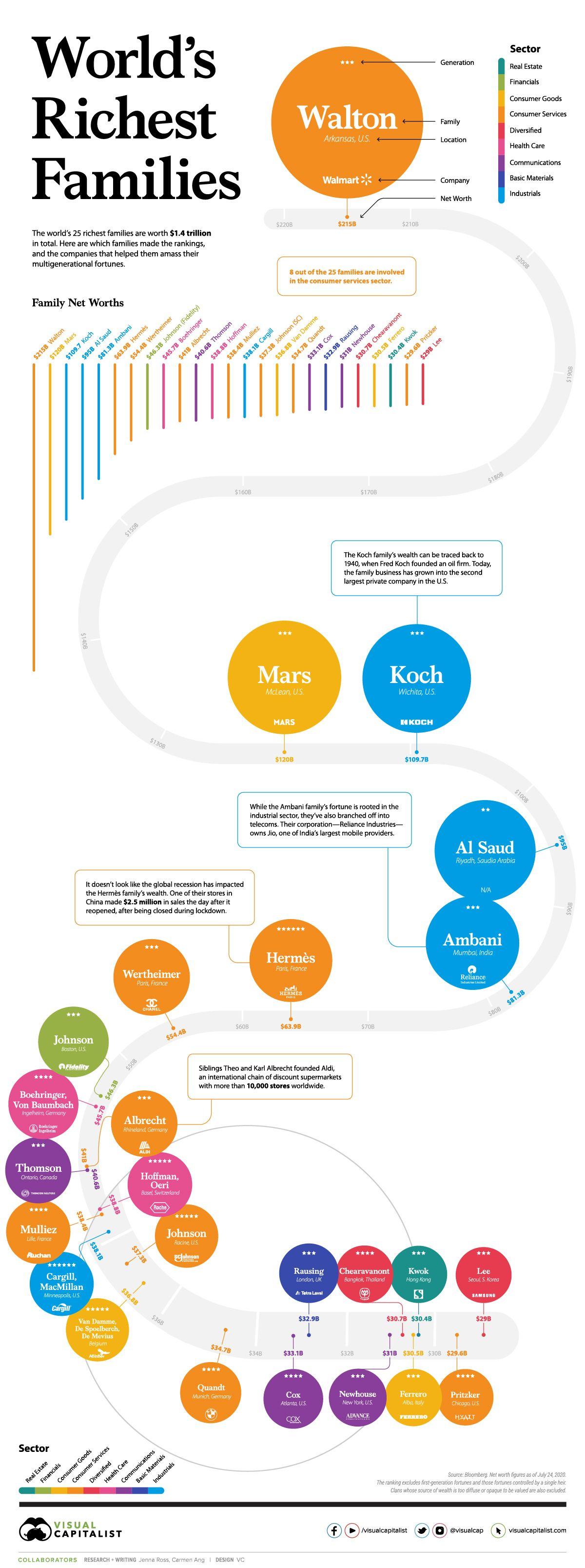

These Are The World’s Richest Families Tyler Durden

Thu, 09/10/2020 – 02:45

The COVID-19 pandemic hasn’t stopped the world’s wealthiest families from growing their fortunes. As Visual Capitalist’s Carmen Ang notes, over the past year, the richest family – the Waltons – grew their wealth by $25 billion, or almost $3 million per hour.

This graphic, using data from Bloomberg, ranks the 25 most wealthy families in the world. The data excludes first-generation wealth and wealth controlled by a single heir, which is why you don’t see Jeff Bezos or Bill Gates on the list. Families whose source of wealth is too diffused or opaque to be valued are also excluded.

The Full Breakdown

Intergenerational wealth is a powerful thing. It often prevails through market crashes, social turmoil, and economic uncertainty, and this year has been no exception.

Here’s a look at the 25 most wealthy families in 2020:

The Waltons are the richest family on the list by far, with a net worth of $215 billion—that’s $95 billion more than the second wealthiest family. Sam Walton, the family’s patriarch, founded Walmart in 1962. Since then, it’s become the world’s largest retailer by revenue.

When Sam passed away in 1992, his three children—James, Alice, and Rob—inherited his fortune. Now, the trio co-owns about half of Walmart.

In second place is the Mars family, with a net worth of $120 billion. The family is well-known for their candy empire, but interestingly, about half of the company’s value comes from pet care holdings. Mars Inc. owns several popular pet food brands, including Pedigree, Cesar, and Royal Canin—and it expanded its pet presence further in 2017 when it acquired VCA, a company with almost 800 small animal vet hospitals across the U.S. and Canada.

The Koch family is the world’s third-richest family. Their fortune is rooted in an oil firm founded by Fred C. Koch. Following Fred’s death in 1967, the firm was inherited by his four sons—Frederick, Charles, David, and William. After a family feud, Frederick and William left the business, and Charles and David went on to build the mega industrial conglomerate known as Koch Industries.

Despite being affected by the oil crash this year, the Koch family’s wealth still sits at $109.7 billion. Before David’s passing in 2019, he and his brother Charles were heavily involved in politics—and their political efforts were the subject of much scrutiny.

Richest Families, by Sector

It’s important to note that many of these families have diversified their investments across a variety of industries. For instance, while the Koch family’s wealth is largely concentrated in the industrial sector and commodities, they also dabble in real-estate—in May 2020, they made a $200 million bet on U.S. rental homes.

That being said, it’s interesting to see where each of these families started, and which sectors have bred the highest number of ultra-wealthy families.

Here’s a breakdown of each sector and how many families on the list got started in them:

The top sector is consumer services—8 of the 25 families are heavily involved in this sector. Walmart helped generate the most wealth out of families in this space, while luxury brands Hermès and Chanel were the source of fortune for the next two wealthiest families.

Industrial is the second largest sector, with 4 of the 25 families involved. It’s also one of the most lucrative sectors—out of the top five wealthiest families on the list, three are in industrials. The Koch family is the wealthiest family in this category, followed by the Al Saud family and the Ambani family, respectively.

Communications and consumer goods are tied for third, with 3 of the 25 families in each. The Thomsons, who founded Thomson Reuters, are the wealthiest family in communications, while the Mars family has the highest net worth in the consumer goods sector.

Resilient, but not Bulletproof

Despite a global recession, most of the world’s wealthiest families seem to be doing just fine—however, not everyone on the list has been thriving this year.

The Koch family’s fortune dropped by $15 billion from 2019 to 2020, and the current political climate in Hong Kong has had a negative impact on the Kwok family’s real estate empire.

While intergenerational wealth certainly has resilience, how much economic and social turmoil can it withstand? It’ll be interesting to see which families make the list in 2021.

via ZeroHedge News https://ift.tt/3jYjbHK Tyler Durden

Timing is everything, they say. Never more so was it crucial in the case of Alexei Navalny, currently coming out of a coma in the Charité hospital in Berlin, Germany, where he was transferred last month from Omsk in Russia after collapsing on a plane. Timing in this detective story is vital to understanding the motive behind the alleged poisoning.

For the West, it is a cut and dried case. Navalny, the Russian opposition activist, was poisoned by a nerve agent ‘Novichok’, probably in a cup of tea he drank at Omsk airport. The German military, after liaising with scientists at the UK’s Porton Down laboratory, came to that conclusion after carrying out tests. The implication is that the Russian state is responsible. In what was an unusually defiant tone, Angela Merkel said that Germany was awaiting answers from the Russian government regarding Navalny’s plight. Heiko Maas, the German Foreign Minister, went further at the weekend to say that he hoped Russia would come up with a response to the allegations of Novichok poisoning, or it could affect the completion of the Nord Stream 2 pipeline project.

And herein lies the rub for the western version of events. For if indeed the Russian state was indeed guilty of poisoning Navalny, why on earth would it allow his transfer to Germany? And why would it carry out such a criminal act during the last phase of the Nord Stream pipeline project, in which so much has been invested? Politically and geopolitically, such an act would absolutely backfire. By eliminating an opposition member such as Alexei Navalny, it would no doubt produce a furious reaction from both foreign powers and domestic opposition, only encouraging anti-government activism.

So why therefore have we not seen protestors take to the streets in Russia in support of Navalny? Partly, it is because many Russians are sceptical of the West’s allegations. Given that Russia would have so much to lose from such a state-sponsored act, the motivation is not there. There are just as many holes in the western narrative as there were with the Skripal case back in 2018. As was the case back then, the Russian state was accused of the poisoning of ex double agent Sergei Skripal and his daughter Yulia, yet no evidence of Russian state involvement was provided. As yet we are to hear from the doctors treating Navalny in the Charité hospital in Berlin, just as we didn’t hear from those involved in the Skripal case. As in the Skripal case, the timing of the incident couldn’t be worse for the Kremlin. Then, it was just before the Russian world cup; in this case, it is just before the completion of Nord Stream 2 and when the Trump administration has spoken of meeting with Putin later this year. Why would the Russian state risk such an act at this time? Furthermore, if it was the nerve agent Novichok, a potent chemical up to eight times stronger than VX, why were other people around Navalny not affected? And why did he not exhibit any of the spasms associated with such nerve agents?

On the contrary, as the doctors treating him in Omsk reported, there was no indication that Navalny was suffering from poisoning by a nerve agent. They suggested various possibilities, including one of a pancreatic disorder which would fit the results of the investigations carried out, and the symptoms exhibited. Why it is that the German experts have come up with a completely different diagnosis is not clear, as they have not released any information. The lack of transparency and in particular, lack of communication with Moscow on the detail of analyses taken, only adds to scepticism about the western narrative.

Furthermore, it’s worth considering Navalny’s popularity and reach within Russia. According to a recent poll by Levada, the opposition activist would gain around 2% of the vote in a presidential election was to be held, compared to 56% who would re-elect Vladimir Putin. In a further survey which asked people to select a candidate which they trusted the most, Navalny only came 7th, with Vladimir Putin in 1st place. Such polls reflect the consistently high approval ratings Vladimir Putin has had for years now. Navalny on the other hand, has not gained the popularity he might have hoped given his years of journalism and anti-government activism – another reason why we haven’t seen demonstrations on the streets of Moscow since his hospitalisation.

Why would the Kremlin seek to annihilate someone who didn’t pose any real threat to established power?

If Navalny was indeed poisoned, then we have to look elsewhere for a motive. And here the old adage ‘Cui Bono?’ comes to mind.

In the last week theheadlines have been dominated by the idea that the Navalny poisoning could end the Nord Stream pipeline. What is more interesting however is the extent to which the current US administration has been fixated with the idea of stopping Nord Stream 2, no matter what. And don’t take my word for it. Mike Pompeo himself said in July this year that the US would ‘do everything’ it could to prevent Nord Stream 2. He told the Senate Foreign Affairs Committee “We need further tools. We’re prepared to use those tools should you provide them to us”.

Just what exactly these tools would consist of, other than support for sanctions, is unclear. But it’s no secret that the US has tried everything in the book to try to stop this pipeline which would guarantee Europe’s energy supply and greatly reduce US chances of competing with its own fracked gas. From sanctions, to pressurising companies and individuals, no stone has been left unturned. Now, by some twist of fate, an issue has arisen to put maximum pressure on the German government to abandon the project. The timing is extraordinary.

We don’t know yet what happened to Alexei Navalny; there just hasn’t been enough evidence released. Until it is, the western narrative cannot be taken at face value, there are simply too many things that don’t add up.

via ZeroHedge News https://ift.tt/3k4uoH6 Tyler Durden

“No one ever seizes power with the intention of relinquishing it. Power is not a means; it is an end.”

– George Orwell

You can map the nearly 20-year journey from the 9/11 attacks to the COVID-19 pandemic by the freedoms we’ve lost along the way.

The road we have been traveling has been littered with the wreckage of our once-vaunted liberties, especially those enshrined in the Fourth Amendment.

The assaults on our freedoms that began with the post-9/11 passage of the USA Patriot Act laid the groundwork for the eradication of every vital constitutional safeguard against government overreach, corruption and abuse.

The COVID-19 pandemic with its lockdowns, mask mandates, surveillance, snitch lines for Americans to report their fellow citizens for engaging in risky behavior, and veiled threats of forced vaccinations has merely provided the architects of the American police state with an opportunity to flex their muscles.

These have become mile markers on the road to tyranny.

Free speech, the right to protest, the right to challenge government wrongdoing, due process, a presumption of innocence, the right to self-defense, accountability and transparency in government, privacy, press, sovereignty, assembly, bodily integrity, representative government: all of these and more have become casualties in the government’s ongoing war on the American people. In the process, the American people have been treated like enemy combatants, to be spied on, tracked, scanned, frisked, searched, subjected to all manner of intrusions, intimidated, invaded, raided, manhandled, censored, silenced, shot at, locked up, denied due process, and killed.

What the past 20 years have proven is that the U.S. government poses a greater threat to our individual and collective freedoms and national security than any terrorist, foreign threat or pandemic.

In allowing ourselves to be distracted by terror drills, foreign wars, color-coded warnings, partisan politics, pandemic scares, and other carefully constructed exercises in propaganda, sleight of hand, and obfuscation, we failed to recognize that the U.S. government—the government that was supposed to be a “government of the people, by the people, for the people”—has become the enemy of the people.

Indeed, the U.S. government has grown so corrupt, greedy, power-hungry and tyrannical over the course of the past 240-plus years that our constitutional republic has since given way to an idiocracy, and representative government has given way to a kleptocracy (a government ruled by thieves) and a kakistocracy (a government run by unprincipled career politicians, corporations and thieves that panders to the worst vices in our nature and has little regard for the rights of American citizens).

Although the Bill of Rights—the first ten amendments to the Constitution—was adopted as a means of protecting the people against government tyranny, in America today, the government does whatever it wants, freedom be damned.

“We the people” have been terrorized, traumatized, and tricked into a semi-permanent state of compliance by a government that cares nothing for our lives or our liberties.

The bogeyman’s names and faces have changed over time (terrorism, the war on drugs, illegal immigration, a viral pandemic), but the end result remains the same: in the so-called name of national security, the Constitution has been steadily chipped away at, undermined, eroded, whittled down, and generally discarded with the support of Congress, the White House, and the courts.

What we are left with today is but a shadow of the robust document adopted more than two centuries ago. Sadly, most of the damage has been inflicted upon the Bill of Rights.

Here is what it means to live under the Constitution, post-9/11 and in the midst of a COVID-19 pandemic.

The First Amendment is supposed to protect the freedom to speak your mind, assemble and protest nonviolently without being bridled by the government. It also protects the freedom of the media, as well as the right to worship and pray without interference. In other words, Americans should not be silenced by the government. To the founders, all of America was a free speech zone.

Despite the clear protections found in the First Amendment, the freedoms described therein are under constant assault. Increasingly, Americans are being arrested and charged with bogus “contempt of cop” charges such as “disrupting the peace” or “resisting arrest” for daring to film police officers engaged in harassment or abusive practices. Journalists are being prosecuted for reporting on whistleblowers. States are passing legislation to muzzle reporting on cruel and abusive corporate practices. Religious ministries are being fined for attempting to feed and house the homeless. Protesters are being tear-gassed, beaten, arrested and forced into “free speech zones.” And under the guise of “government speech,” the courts have reasoned that the government can discriminate freely against any First Amendment activity that takes place within a government forum.

The Second Amendment was intended to guarantee “the right of the people to keep and bear arms.” Essentially, this amendment was intended to give the citizenry the means to resist tyrannical government. Yet while gun ownership has been recognized by the U.S. Supreme Court as an individual citizen right, Americans remain powerless to defend themselves against SWAT team raids and government agents armed to the teeth with military weapons better suited to the battlefield. As such, this amendment has been rendered null and void.

The Third Amendment reinforces the principle that civilian-elected officials are superior to the military by prohibiting the military from entering any citizen’s home without “the consent of the owner.” With the police increasingly training like the military, acting like the military, and posing as military forces—complete with heavily armed SWAT teams, military weapons, assault vehicles, etc.—it is clear that we now have what the founders feared most—a standing army on American soil.

The Fourth Amendment prohibits government agents from conducting surveillance on you or touching you or invading you, unless they have some evidence that you’re up to something criminal. In other words, the Fourth Amendment ensures privacy and bodily integrity. Unfortunately, the Fourth Amendment has suffered the greatest damage in recent years and has been all but eviscerated by an unwarranted expansion of police powers that include strip searches and even anal and vaginal searches of citizens, surveillance (corporate and otherwise) and intrusions justified in the name of fighting terrorism, as well as the outsourcing of otherwise illegal activities to private contractors.

The Fifth Amendment and the Sixth Amendment work in tandem. These amendments supposedly ensure that you are innocent until proven guilty, and government authorities cannot deprive you of your life, your liberty or your property without the right to an attorney and a fair trial before a civilian judge. However, in the new suspect society in which we live, where surveillance is the norm, these fundamental principles have been upended. Certainly, if the government can arbitrarily freeze, seize or lay claim to your property (money, land or possessions) under government asset forfeiture schemes, you have no true rights.

The Seventh Amendment guarantees citizens the right to a jury trial. Yet when the populace has no idea of what’s in the Constitution—civic education has virtually disappeared from most school curriculums—that inevitably translates to an ignorant jury incapable of distinguishing justice and the law from their own preconceived notions and fears. However, as a growing number of citizens are coming to realize, the power of the jury to nullify the government’s actions—and thereby help balance the scales of justice—is not to be underestimated. Jury nullification reminds the government that “we the people” retain the power to ultimately determine what laws are just.

The Eighth Amendment is similar to the Sixth in that it is supposed to protect the rights of the accused and forbid the use of cruel and unusual punishment. However, the Supreme Court’s determination that what constitutes “cruel and unusual” should be dependent on the “evolving standards of decency that mark the progress of a maturing society” leaves us with little protection in the face of a society lacking in morals altogether.

The Ninth Amendment provides that other rights not enumerated in the Constitution are nonetheless retained by the people. Popular sovereignty—the belief that the power to govern flows upward from the people rather than downward from the rulers—is clearly evident in this amendment. However, it has since been turned on its head by a centralized federal government that sees itself as supreme and which continues to pass more and more laws that restrict our freedoms under the pretext that it has an “important government interest” in doing so.

As for the Tenth Amendment’s reminder that the people and the states retain every authority that is not otherwise mentioned in the Constitution, that assurance of a system of government in which power is divided among local, state and national entities has long since been rendered moot by the centralized Washington, DC, power elite—the president, Congress and the courts.

If there is any sense to be made from this recitation of freedoms lost, it is simply this: our individual freedoms have been eviscerated so that the government’s powers could be expanded.

Mind you, by “government,” I’m not referring to the highly partisan, two-party bureaucracy of the Republicans and Democrats. Rather, I’m referring to the Deep State—the corporatized, militarized, entrenched bureaucracy that has set itself beyond the reach of the law and is unaffected by elections, unaltered by populist movements, and staffed by unelected officials who are, in essence, running the country and calling the shots in Washington DC, no matter who sits in the White House.

This is a government that, in conjunction with its corporate partners, views the citizenry as consumers and bits of data to be bought, sold and traded.

This is a government that is laying the groundwork to weaponize the public’s biomedical data as a convenient means by which to penalize certain “unacceptable” social behaviors.

This is a government that uses fusion centers, which represent the combined surveillance efforts of federal, state and local law enforcement, to track the citizenry’s movements, record their conversations, and catalogue their transactions.

This is a government whose wall-to-wall surveillance has given rise to a suspect society in which the burden of proof has been reversed such that Americans are now assumed guilty until or unless they can prove their innocence.

This is a government that treats its people like second-class citizens who have no rights, and is working overtime to stigmatize and dehumanize any and all who do not fit with the government’s plans for this country.

This is a government that uses free speech zones, roving bubble zones and trespass laws to silence, censor and marginalize Americans and restrict their First Amendment right to speak truth to power. The kinds of speech the government considers dangerous enough to red flag and subject to censorship, surveillance, investigation, prosecution and outright elimination include: hate speech, bullying speech, intolerant speech, conspiratorial speech, treasonous speech, threatening speech, incendiary speech, inflammatory speech, radical speech, anti-government speech, right-wing speech, left-wing speech, extremist speech, politically incorrect speech, etc.

This is a government that persists in renewing the National Defense Authorization Act (NDAA), which allows the president and the military to arrest and detain American citizens indefinitely.

This is a government that saddled us with the Patriot Act, which opened the door to all manner of government abuses and intrusions on our privacy.

This is a government that has militarized American’s domestic police, equipping them with military weapons such as “tens of thousands of machine guns; nearly 200,000 ammunition magazines; thousands of pieces of camouflage and night-vision equipment; and hundreds of silencers, armored cars and aircraft,” in addition to armored vehicles, sound cannons and the like.

This is a government that has provided cover to police when they shoot and kill unarmed individuals just for standing a certain way, or moving a certain way, or holding something—anything—that police could misinterpret to be a gun, or igniting some trigger-centric fear in a police officer’s mind that has nothing to do with an actual threat to their safety.

This is a government that treats public school students as if they were prison inmates, enforcing zero tolerance policies that criminalize childish behavior, failing to teach them their rights under the Constitution, and indoctrinating them with teaching that emphasizes rote memorization and test-taking over learning, synthesizing and critical thinking.

This is a government that is operating in the negative on every front: it’s spending far more than what it makes (and takes from the American taxpayers) and it is borrowing heavily (from foreign governments and Social Security) to keep the government operating and keep funding its endless wars abroad. Meanwhile, the nation’s sorely neglected infrastructure—railroads, water pipelines, ports, dams, bridges, airports and roads—is rapidly deteriorating.

This is a government that has allowed the presidency to become a dictatorship operating above and beyond the law, regardless of which party is in power.

This is a government that treats dissidents, whistleblowers and freedom fighters as enemies of the state.

This is a government that has in recent decades unleashed untold horrors upon the world—including its own citizenry—in the name of global conquest, the acquisition of greater wealth, scientific experimentation, and technological advances, all packaged in the guise of the greater good.

This is a government that allows its agents to break laws with immunity while average Americans get the book thrown at them.

This is a government that speaks in a language of force. What is this language of force? Militarized police. Riot squads. Camouflage gear. Black uniforms. Armored vehicles. Mass arrests. Pepper spray. Tear gas. Batons. Strip searches. Surveillance cameras. Kevlar vests. Drones. Lethal weapons.Less-than-lethal weapons unleashed with deadly force. Rubber bullets. Water cannons. Stun grenades. Arrests of journalists. Crowd control tactics. Intimidation tactics. Brutality. Contempt of cop charges.

This is a government that justifies all manner of government tyranny and power grabs in the so-called name of national security, national crises and national emergencies.

This is a government that exports violence worldwide, with one of this country’s most profitable exports being weapons. Indeed, the United States, the world’s largest exporter of arms, has been selling violence to the world in order to prop up the military industrial complex and maintain its endless wars abroad.

This is a government that is consumed with squeezing every last penny out of the population and seemingly unconcerned if essential freedoms are trampled in the process.

This is a government that believes it has the authority to search, seize, strip, scan, spy on, probe, pat down, taser, and arrest any individual at any time and for the slightest provocation, the Constitution be damned.

In sum, this is a government that routinely undermines the Constitution and rides roughshod over the rights of the citizenry.

This is not a government that believes in, let alone upholds, freedom.

So where does that leave us?

As always, the first step begins with “we the people.”

Those who gave us the Constitution and the Bill of Rights believed that the government exists at the behest of its citizens. It is there to protect, defend and even enhance our freedoms, not violate them. Our power as a citizenry comes from our ability to agree and stand united on certain freedom principles that should be non-negotiable.

It was no idle happenstance that the Constitution opens with these three powerful words: “We the people.” In other words, we have the power to make and break the government. We are the masters and they are the servants. We the American people—the citizenry—are the arbiters and ultimate guardians of America’s welfare, defense, liberty, laws and prosperity.

Our national priorities need to be re-prioritized. For instance, some argue that we need to make America great again. I, for one, would prefer to make America free again.

via ZeroHedge News https://ift.tt/33cYr8B Tyler Durden

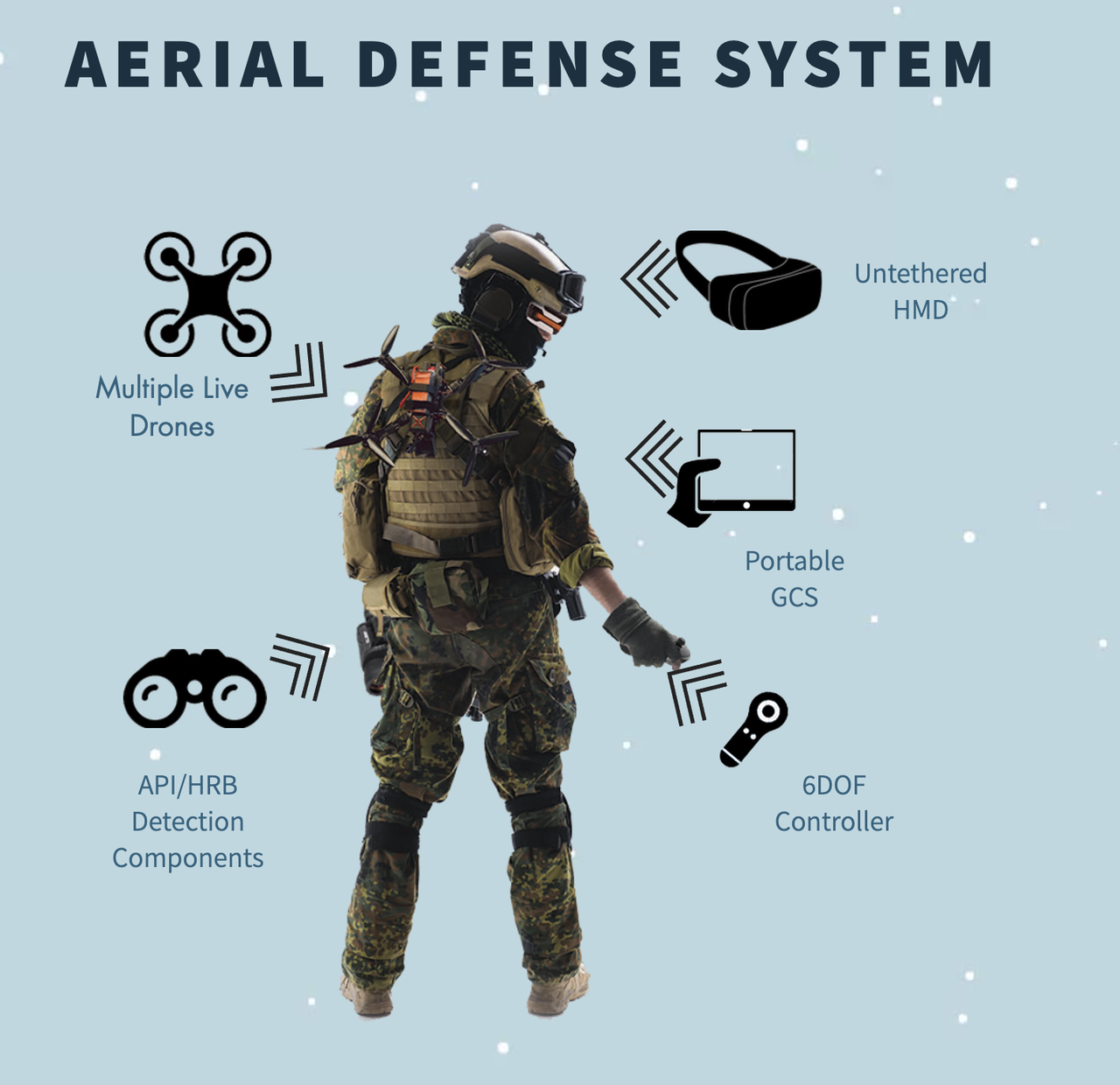

US Military Testing “Skylord” Counter-Drone AR Interception System Tyler Durden

Wed, 09/09/2020 – 23:40

The U.S. Department of Defense (DoD) has partnered with an Israeli-based startup, called Xtend, to pilot test the Skylord drone, initially developed for the gaming world, which would be used as a drone interception system on the modern battlefield.

The joint pilot program will be directed by the Directorate of Defense Research and Development (DDRD), in the Israel Ministry of Defense, with Xtend, and the U.S. Combating Terrorism Technical Support Office, of the DoD, to test Skylord’s full interception capabilities.

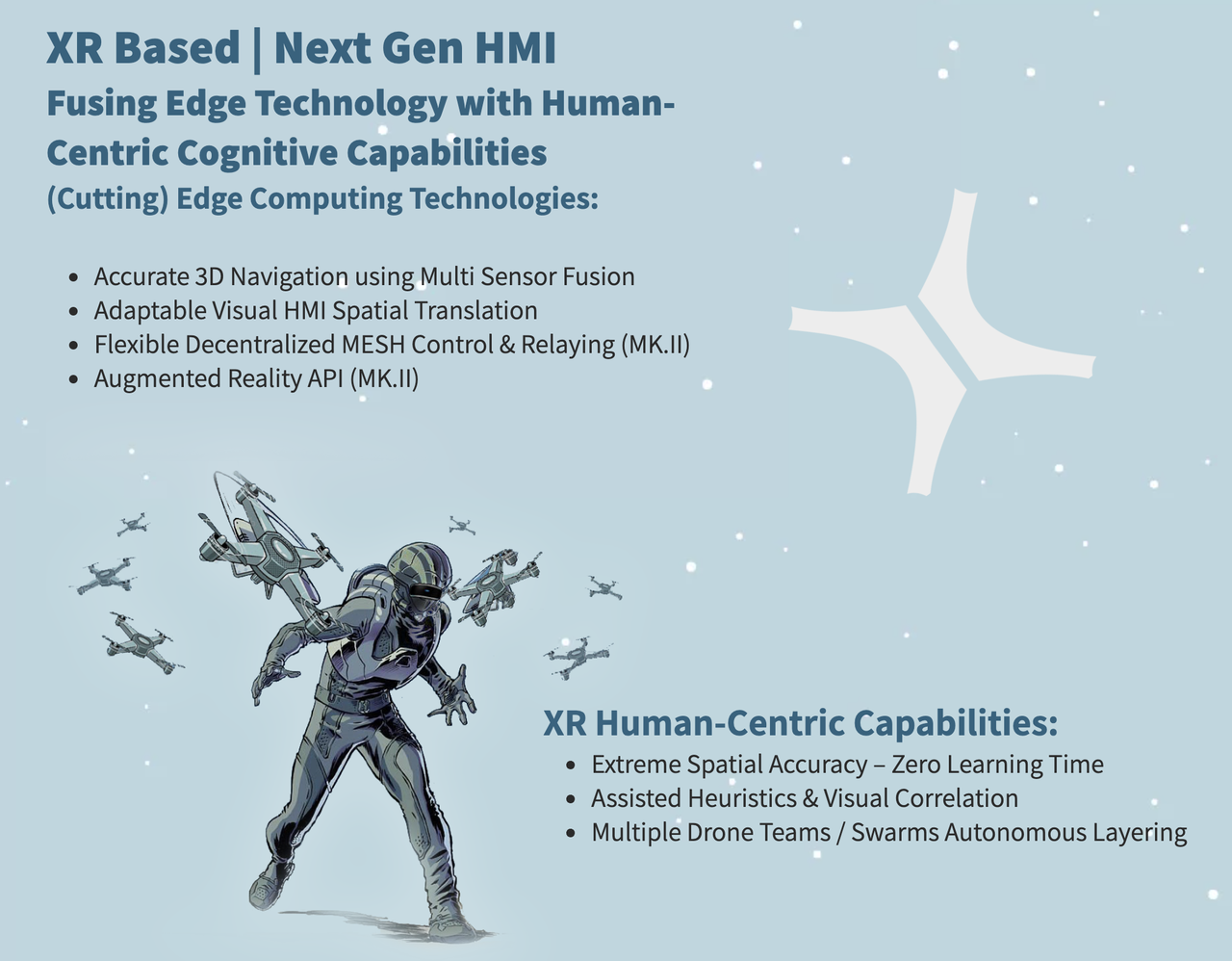

The Skylord drone is small and extremely fast and uses a net to disable small enemy drones. Skylord is equipped with a camera and automatic tracking software. The operator can control the drone via virtual reality and augmented reality glasses.

“Using an augmented reality (A.R.) device and single-handed controller, a military operator may employ the … system to control the drone and perform complex tasks remotely, with great ease and precision. Its interface enables the operator to immerse themselves or ‘step into’ a remote reality and engage targets effectively yet safely,” according to a statement from Xtend.

Xtend’s CEO Aviv Shapira said Skylord is a proven drone interception system that has seen action over the Gaza border.

“The system’s capabilities have been demonstrated in Israel, with confirmed interceptions of incendiary devices flown over the Gaza border by terrorist organizations. The interface allowed the user to feel the area through the ‘eyes’ of the drone, experiencing the event as if the operator was in the drone, without risking their life,” Shapira said.

Lt. Col. Menachem Landau, who leads the unmanned aerial systems branch in the DDRD, said in a statement to Defense News:

“We met the company and began to see what we can do regarding challenges on the battlefield which we had here in Israel… We are developing several capabilities with this technology, instead of sending the soldier into the building, sending the drone into the building [for instance], to get information.”

Here’s Skylord in action:

So the question readers must be asking: Why would the DoD be interested in counter-drone systems? One reason is that weaponized drone swarms are becoming a massive threat that, if large enough, could soon be classified as a “weapon of mass destruction.”

In early August, documents uncovered through the Freedom of Information Act outlined America’s largest nuclear power plant has been the target of ‘mysterious’ drone swarms.

And for all the airline pilots getting laid off – maybe becoming a drone operator might not be such a bad gig (read: here).

via ZeroHedge News https://ift.tt/35lBXF2 Tyler Durden

Variety is the spice of life but when does it go too far? When does a person move from being a nonconformist to where they are just plain weird?

This is not a question that is easily answered.

A sub-group of our population that is difficult to define is that of “weirdos.” Even in our politically correct society, this is a subject that merits more than a quick once over. The dictionary defines a weirdo as a person who is extraordinarily strange or eccentric. With that in mind, it is important to ponder the effect these individuals have upon society and our culture.

A news piece on about a “swingers club” quietly operating in my city. I found myself pondering the implication of its existence. In many ways, the members of such clubs fall into the category of sexual deviants in that many sport values far from society’s norm. Back in college I took a course that explored social deviants, how they were, shall we say, trained and recruited. This is a very interesting subject. While some people move off mainstream values for attention, to emphasize their individuality, or during self-exploration, it does have implications for the overall culture. The growing number of people seeking tattoos is evidence of this trend.

The topic of weirdos is complex because it can also extend into the area of dysfunctional individuals from which society suffers no shortage. Whether crazy, stupid, or simply marching to the beat of a different drummer it seems the number of these people is on the rise. In many parts of the western world, society has been on a mission that encourages people to embrace their individuality and this is apparent by the growing number of eccentric people. What is leading to this explosion of “I am Me” and often self-centered behavior? One thing is clear, more people are being allowed to express their individuality and this can be seen in the way many people claim gender is no longer carved in stone at birth.

Is This Weird Or Very Cool?

Interestingly the effect on society of allowing this sub-group to expand has yet to be determined. I’m not advocating doing anything about controlling social deviants but merely pondering their existence and growing influence. In China conformity is highly valued and fostered by its government that seeks control over all facets of a person’s life. A balance between conformity and over the top diversity is most likely a place where society finds its happy place. Conformity can crush the human soul while the lack of it is often difficult for society to address. because it tends to bring up the issue of where one person’s rights end and another persons begin.

Feeding into this subject is the concern that by adopting a hands-off approach to halting the expansion of this trend we institutionalize or make it a normal and acceptable part of our culture. It could be argued that self-expression is a human right and I’m not advocating denying anyone that right. As an example to highlight the fact this is an issue, the following was lifted from the comment section of a recent online publication where many of those weighing in voiced concern or noted what they saw as a troubling trend. The comment read:

We need a new demographic category: WALMARTIANS.

They are almost always overweight, usually functionally illiterate, often incapable of all but the most basic personal hygiene, not merely unemployed but also unemployable, addicted to corn syrup junk food and TV they were force-fed as children, convinced that nothing is their fault because they’ve never heard otherwise and physically aggressive whenever there is no prospect of immediate punishment.

Such types were rare when I was a lad but now they are 10 to 20 percent of the population and increasing.

It’s not their fault but it’s time to cull the herd.

Morbidly Obese People Are Often Seen As Impaired

It should be noted that I started witting this article in December of 2019 but dropped it onto the back burner because of its questionable nature. At times, it seems deviant and dysfunctional behavior overlap. On occasion I have found myself, surprised, shocked, amazed, and even appalled at just how much the shape of the human body can be distorted by obesity or a lack of exercise. Widening the scope to people “deviating from the norm,” at times it appears these often atypical humans are in a race to present us with the most bizarre. Some of these folks are not just offbeat or unusual but seem to be making an over the top effort to give new meaning to the term freaky.

An article by Ralph Nader that appeared on Common Dreamsexplored the idea that if you want to see where a country’s priorities lie you should look at the direction its culture is moving.The article which is linked above exhibits a very strong bit of a “leftist tinge,” however, some of the points he makes seem valid. Nader writes, Plutocrats like to control the range of permissible public dialogue. Plutocrats also like to shape what society values. If you want to see where a country’s priorities lie, look at how it allocates its money. He contends that while teachers and nurses earn comparatively little for performing critical jobs, corporate bosses including those who pollute our planet and bankrupt defenseless families, make millions.

America’s Caste System

It may be simplistic to label this or that, good or bad but it could be argued our culture and society is geared much like the caste system. Today we are seeing inequality soar and it can be argued this tends to reduce the ability of individuals to move up the social ladder. The question is just how much of this is by design and due to the culturally elite putting their foot on the head of those below them.

Circling back to the subjects of weirdos, diversity, and individuality could it be this is all being encouraged to weaken and divide the power of the masses? For years Japan has been pointed to as a society that functions with little friction. Much of the credit is attributed to their culture and its homogeneous nature. Japan has a strong sense of group and national identity and little or no ethnic or racial diversity. Another unique aspect of Japanese society has a highly structured approach to managing and resolving these differences.

* * *

This article should be viewed in its entirety as a cultural “observation and nothing more.” The fact is our culture is always changing. Please consider it “food for thought.” Also, please note, a big problem we face today is society’s inability to get people to obey its rules and laws. Long-term this has dire consequences. This article explores this trend and its ramifications.

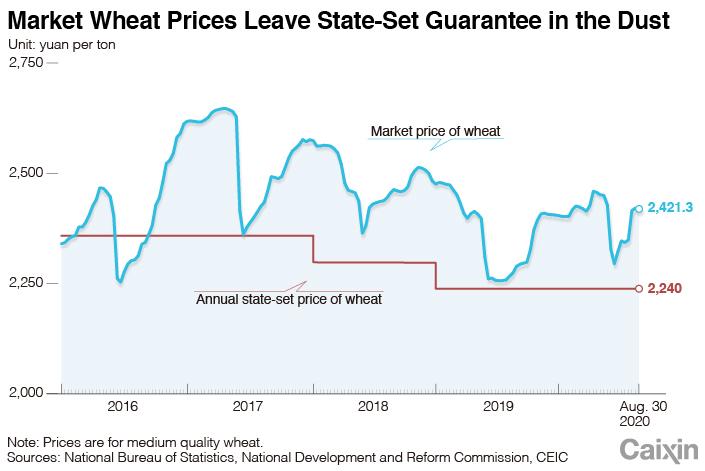

Chinese Farmers Hoard Wheat In Hopes Of Creating Shortages That Push Prices Higher Tyler Durden

Wed, 09/09/2020 – 23:00

The latest Chinese inflation data released overnight showed that consumer prices slowed again, dropping to 2.4% Y/Y, the lowest since early 2019, largely moderating on lower pork inflation (still over 50% y/y, but slowing), while producer price inflation remains negative.

And while Chinese food inflation dropped in half from the record 20% Y/Y increase hit in March as Chinese supply chains were disrupted by the covid lockdowns…

… this decline may not last because as Caixin reports, China’s farmers are stockpiling more of their wheat harvest this year rather than selling to the government and the market as they expect prices to rise and want to hold onto their stocks in case of shortages stemming from the severe summer flooding and fallout from the coronavirus pandemic.

Farmers in the country’s main wheat-growing regions sold only 49.3 million tons of their crop for commercial use and to state reserves as of Aug. 31, 20% less than in the same period last year, according to government data. Within that total, sales to the National Food and Strategic Reserves Administration, which stockpiles and manages the country’s strategic food reserves, sank by almost 70% to 6.2 million tons. Wheat purchased by market participants such as mills accounted for about 86% of the total in 2020, up from 70% last year, the official Xinhua News Agency reported on Aug. 14.

Fears about food security in China have intensified this year amid the coronavirus pandemic and severe flooding that’s hit swathes of agricultural land since June. Speculation that shortages of basic foodstuffs like rice and wheat could emerge has sent prices soaring even as government officials have sought to reassure the population that the country is self-sufficient in staple crops and that the recent price fluctuations in the grain market are temporary.

“As state purchases of wheat dropped this year, market purchases accounted for a higher portion, increasingly becoming the main channel of wheat purchases,” Tang Ke, senior official at Ministry of Agriculture and Rural Affairs said at a press conference on Aug. 26.

In keeping with Chinese tradition of stockpiling strategic reserves across most commodities, since 2006 the government has purchased wheat at annual state-set prices to ensure that any dramatic decline in market prices would not discourage farmers from cultivating the crop. When market prices are low, farmers can opt to sell more of their crop to state purchasers to support their income.

Currently, the market price for medium-quality wheat from China’s major grain-growing regions is around 2,421.3 yuan ($354) per ton. That compares with the minimum state purchase price of 2,240 yuan, according to government data. For high-quality wheat, the market price is around 2,440 yuan to 2,460 yuan per ton, compared with the state purchase price of 2,320 yuan, according to commodity research firm Sublime China Information Co. Ltd.

As the chart below shows, market prices have risen sharply since July amid widespread flooding and an increase in the price of corn, which has prompted many farmers to switch to wheat to feed their animals, adding to demand for the grain. Meanwhile, prices of pork remain elevated due to the recent outbreak of so-called “Pig Ebola” which decimated the local pig population. The Zhengzhou grain wholesale market, located in the major wheat-producing province of Henan in Central China, reported high-quality wheat prices were up 6.6% year-on-year in July.

Similar to oil traders who stockpile crude on ships to take advantage of contango and higher future prices, as Chinese farmers expect further price increases, they are less interested in selling now and are preferring to wait so that they can earn more money, multiple sources including farmers, grain traders, and heads of flour mills told Caixin. However, some industry participants don’t expect prices to rise much further. One insider told Caixin that flour mills will find it difficult to accept further increases while Tang, the agriculture ministry official, said that pressure on wheat prices will moderate as the jump in corn costs gradually eases.

Despite fears of supply shortages, China had a record wheat harvest this summer, with output increasing by 756,000 tons year-on-year, or 0.6%, despite a 1.2% decline in planted acreage, according to data released in July by the National Bureau of Statistics. Nevertheless, production in Henan, which accounts for nearly 30% of the country’s wheat output, may have declined due to natural disasters including a cold wave and drought which hit the southern part of the province earlier this year, several industry insiders said. Official data show that as of Aug. 5, the state purchased 9.1 million tons of wheat in the province, a year-on-year decline of 5.4 million tons, the biggest drop of all major wheat-growing regions.

“Previously, we could harvest at least over 2,700 kilograms per acre, but this year we only had about 2,120 kilograms,” a farmer in southern Henan told Caixin. One grain merchant in the area said he purchased less than 1,000 tons of wheat, half as much as in 2019, as many farmers saw declines in wheat production due to bad weather.

via ZeroHedge News https://ift.tt/3hgpk0v Tyler Durden

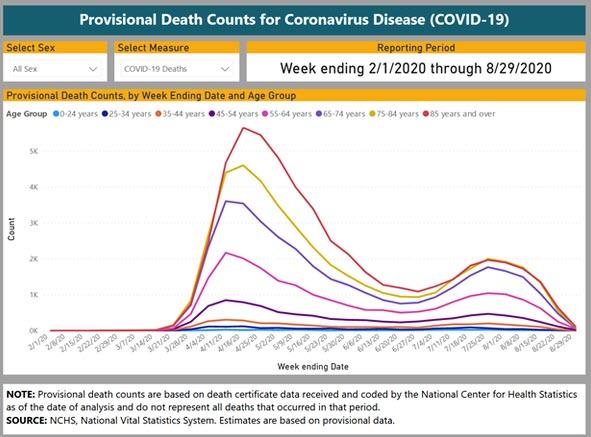

A curious but fortunate characteristic of virus epidemics is their limited lifespans. No one knows why, but guesses include herd immunity and mutations of the virus.

The following graph from the Centers for Disease Control and the National Center for Health Statistics shows the time profile of the COVID-19 weekly death counts from February onward. (For an interactive version of the graph go here.)

In the U.S., the virus got underway in March. For the week ending March 14 the total number of deaths nationwide was 52. During the following month the number of deaths increased rapidly, peaking in the week ending April 18 at a count of 17,026.

From that time onward, the death count declined rapidly to a weekly number of 3,684 in late June. A second “wave” began in July. The peak of that second wave was 6,794 deaths during the week ending July 25. After that a steeper decline commenced and accelerated.

The peak death count for Americans under age 25 was 28 (for the week ending April 11) and has been under that number since. Only a single death occurred in that age group during the latest reported week, and there were no deaths recorded in the 25-34 age group.

Virus epidemics behave differently than virtually all other diseases. If you graphed timelines of the number of cancer deaths, fatal heart attacks, and fatal strokes, those timelines would be virtually flat.

Virus epidemics, however, have relatively short time profiles, like what we’re seeing with COVID-19. There’s nothing unusual about the fact that the coronavirus death count is dying a natural death. That should have been anticipated, and it should now be widely publicized. Why are we pretending not to know this good news? These facts are easy to find. We ought to be celebrating like we did when WWII ended.

This COVID-19 death profile is extremely significant yet is almost totally ignored by the media. Their focus is on cases, not deaths. The number of cases has not decreased as rapidly as the number of deaths. Only a small percentage of cases now ends in death, and the death count is vastly more important than the case count. The case count may linger, but that problem is becoming increasingly manageable.

The latest reported weekly death count (August 29) was 370. That’s out of a population of 330 million people. In a single week, between August 8 and August 15, the number of deaths dropped 85 percent (from 3,169 to 455). The COVID-19 death rate in the U.S. is now barely more than one per million and dropping like a rock. Coronavirus deaths are currently half the number of weekly vehicle fatalities. We’re now seeing the pandemic in our rearview mirror.

via ZeroHedge News https://ift.tt/3m4MiuZ Tyler Durden

Zoltan Pozsar Spots A Possible Year-End Funding Crisis, But Not Everyone Agrees Tyler Durden

Wed, 09/09/2020 – 22:20

It seems like an eternity ago and in far simpler time, when bond markets were worried about such trivial things as bank reserve and funding levels, and repo rate squeezes. And yet, it was almost exactly one year ago, on Sept 16 (the 11th anniversary of the Lehman collapse), when it suddenly became apparent that despite $1.3 trillion in “excess” reserves, there was not enough liquidity in the system. A month later we were the first to piece together the puzzle, which confirmed that it was JPMorgan’s drain of over $100 billion in repo and money market liquidity that was the precipitating factor for the repo market collapse. In other words, not only did JPMorgan precipitate the repocalypse (and it’s not just us who make this claim, but other more “reputable” websites and news sources have since joined our clarion call), but with its actions it also triggered the launch of the repo liquidity flood and, a few weeks later, the Fed $60BN in T-Bill purchases, aka QE4. This dynamic grew to become the biggest market event of 2019.

Of course, considering what happened just 6 months later when the Fed nationalized the bond market on March 23, 2020, launched unlimited QE, injected $3 trillion in liquidity in three months and started corporate bond buying, the gnashing of teeth over the repocalypse seems oddly trivial. Indeed, the recent explosion in bank reserves has made any concerns about repo underfunding an ancient anachronism. If anything, banks – not to mention Robinhood daytraders – are swimming in a sea of liquidity.

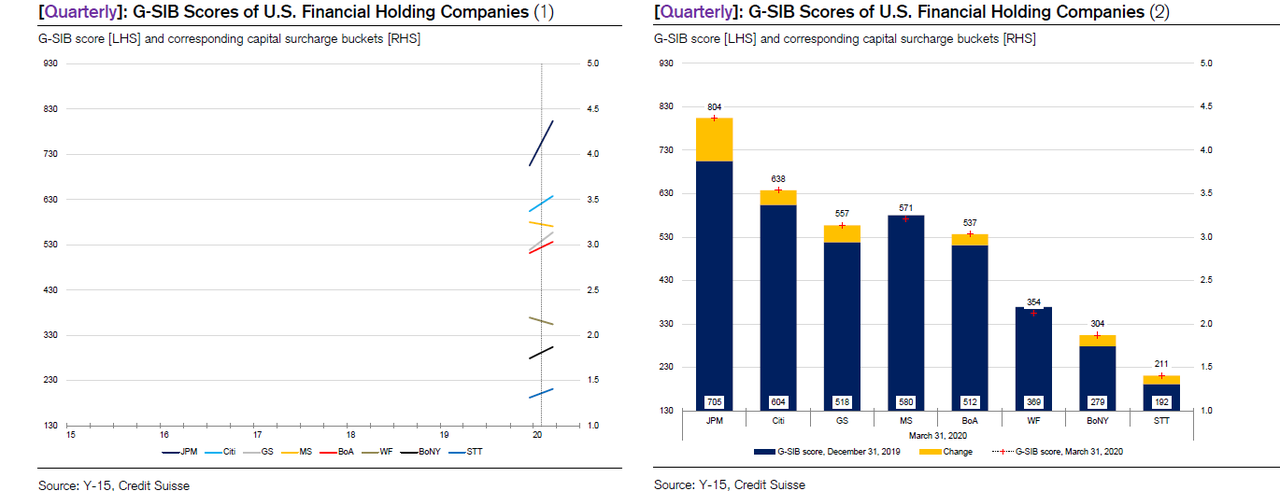

Yet a new dynamic could mean that a year-end funding squeeze is once again on the table, similar to what happened in both 2019 and also 2018.

In a note published earlier this week by former NY Fed staffer and current Credit Suisse strategist, Zoltan Pozsar, the repo guru gives a preview of this week’s release of bank Y-15 report, and looks at various banks’ G-SIB scores with a focus once again on – guess who – JPMorgan, and predicts that as a result of “regulatory changes and market trends since the Covid-19 pandemic”, JPMorgan’s capital surcharge could gap higher from 3.5% in the first quarter by as much as 100 bps to 4.5% in the second quarter.

He explains his reasoning as follows:

Regarding the likely path of the second quarter scores, three developments are worth noting.

First, the April 1st, 2020 exemption of reserves and Treasuries from the calculation of the SLR will reduce “total leverage exposure” used to calculate the size systemic risk scores. This exemption, plus inputs already available from banks’ Y-9C reports on securities outstanding, level 3 assets, and available-for-sale and trading securities that aren’t HQLA point to a 20 point decline in categories that make up about a half of J.P. Morgan’s G-SIB score.

Second, repo books and derivatives activity are down since the first quarter, and that should also help scores fall some.

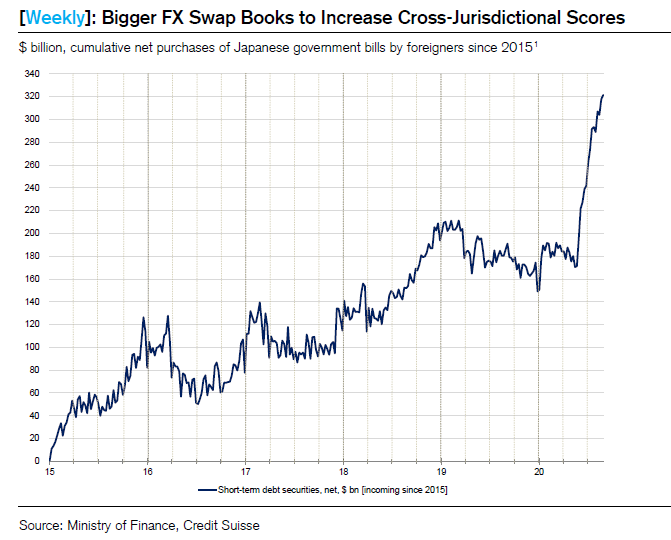

Third, and in contrast to the first two, FX swap books are up a lot since the first quarter, which has the potential to mitigate or even offset the decline in scores coming from the above sources.

This “expansion of FX swap books” on JPM’s balance sheet during Q2 likely pushed its capital surcharge score into the 4.5% capital surcharge bucket…

… which according to Pozsar, “would mean much less FX swap intermediation at J.P. Morgan going into year-end and a year-end turn much worse than what’s currently being priced by the market – unless U.S. banks with lower G-SIB scores or foreign banks pick up the slack.”

Now, when Pozsar – who is among the handful of people who has intimate knowledge and understanding of the US repo system plumbing – speaks everyone – especially those at the Fed shut up and listen: after all, he predicted with uncanny accuracy the events of the repocalypse and also the Fed’s “all in” response to the covid pandemic.

Yet this time not everyone agrees, because now that banks have released the latest Y-15 reports that regulators use to determine how much extra capital the largest banks must hold, debate around the likelihood of funding market stress over year-end has intensified.

Case in point: another prominent STIR strategist, BMO’s Jon Hill, agrees with Pozsar that the balance-sheet snapshots taken of the major banks in the first quarter show four moved into a higher surcharge zone for G-SIBS, global systemically important banks. Hill adds that the largest US bank, JPMorgan, is “by far the most likely” to jump to a higher bucket – meaning at the year-end assessment regulators could require a bigger surcharge. No disagreement with Pozsar here.

However, where Hill disagrees with the closely-followed Hungarian, is in his assessment about year end funding stress: unlike Pozsar, he is “skeptical” that it will emerge for two reasons:

First, snapshots from Q1 “were taken near peak Covid-crisis stress and may not be applicable to later in the year”, and the four banks in question were all able to manage their G-SIB scores in the prior quarter; “if they do so again, three of the four will revert to the prior G-SIB bucket.”

Second, while banks managing their balance sheets may itself cause stress, G-SIB scores were notably lowered last year “without corresponding disruptions to funding markets.”

Will Hill be right in expecting banks to self-police themselves in a time of record excess reserves thus avoiding a year-end funding crunch, or will Pozsar be correct in predicting a collapse in FX intermediation by JPM, which in turn could lead to a sharp liquidity squeeze? The answer could have substantial implications not only on the repo market which will be directly impacted, but also on overall funding conditions and ultimately, widespread risk assets.

How to trade it? As Hill concludes, based on his expectation of “a relatively quiet year-end”, the BMO strategist recommends selling the December 2020 FRA/OIS contract, which however has already collapsed from its March wides. On the other hand, if Pozsar is right then FRA/OIS is likely to blow out, which would be especially odd in a time when the Fed has provided unlimited liquidity via both QE and unlimited repo operations.

And yet… it is Pozsar, and he has yet to make a prediction that falls short.

Of course, it will be ironic if despite the Fed’s $7 trillion balance sheet, it is none other than JPM which demonstrates to the market how even that record liquidity is not sufficient to cover all funding needs. It will be even more ironic if it is JPMorgan that, just like during the “NOT QE” phase is the bank that prompt the next massive, multi-trillion liquidity injection which, one way or another, will push the S&P to fresh all time highs for the simple reason that the Fed will never allow the biggest US bank to fail if the opportunity cost is creating a few trillion electronic dollars with the push of a button.

via ZeroHedge News https://ift.tt/2RdmM8O Tyler Durden

We’re Headed Toward Stagnation Unless The Fed Reins In Its Money Printing Tyler Durden

Wed, 09/09/2020 – 22:00

Submitted by Frank Shostak, chief economist of AAS Economics via Mises.org

The US Fed is considering lifting its inflation target above 2 percent in order to revive the economy. Contrary to the accepted practice, the Fed is not expected to raise an alarm if the measured price inflation begins to rise. The US central bank is not expected to counter this increase with a tighter monetary stance as in the past. In fact, the idea is to continue robust monetary pumping until the economic data points toward a strong economy.

According to most experts, when an economy falls into a recession the central bank can pull it out of the slump by pumping money. This way of thinking implies that money pumping can somehow grow the economy. The question is, How is this possible? After all, if money pumping can grow the economy, then why not pump plenty of it to generate massive economic growth? By doing that central banks worldwide could have already created everlasting prosperity on the planet.

For most commentators the arrival of a recession is due to shocks such as the covid-19 that push the economy away from a trajectory of stable economic growth. Shocks weaken the economy, i.e. lower the economic growth, so it is held. As a rule, however, a recession or an economic bust emerges in response to a decline in the growth rate of money supply. Note that a decline in the monetary growth works with a time lag. This means that the effect of past declines in the growth rate of money supply could start asserting their influence after a prolonged period.

It is likely that the present economic slump was set in motion by a strong downtrend in the yearly growth rate of AMS money supply from 14.3 percent in August 2011 to –0.6 percent by August 2019. As a result, various activities that sprang up on the back of the previous strong money growth rate came under pressure. (Observe that the yearly growth rate of AMS jumped from 0.7 percent in March 2007 to 14.3 percent by August 2009.) These activities cannot fund themselves independently. They survive on account of the support that the increase in money supply provides. The increase in money diverts to them real savings from wealth generating activities and consequently weakens wealth generators.

A decline in the growth rate of money supply undermines various false nonproductive activities, and this is what a recession is all about. Recessions, then, are not about a weakening in economic activity as such but about the liquidation of various nonproductive activities that sprang up on the back of the previous increase in money supply.

Real Savings Fund Economic Activity

Irrespective of whether an activity is productive or nonproductive, it must be funded. At any point in time the number and the size of activities that can be undertaken is determined by the available amount of real savings. From this, we can infer that the overall growth rate of productive and nonproductive activities as a whole is set by the growth rate in the pool of real savings. (Individuals, whether in productive or nonproductive activities, must have access to real savings in order to sustain their lives and well-being. Also, note that money cannot sustain individuals but can only fulfill the role of the medium of exchange.)

As long as wealth producers can generate enough real savings to support productive and nonproductive activities, easy money policies will appear to be successful. Over time a situation could, however, emerge where as a result of persistent easy monetary policy and reckless government fiscal policies, there are not enough wealth generators left. (Wealth generators are badly damaged by loose monetary and reckless government policies.) Consequently, real savings are not large enough to support an increase in economic activity.

Once this happens, the illusion of loose monetary and fiscal policies is shattered—real economic growth must come under downward pressure. Now, if the Fed were to accelerate its monetary pumping while the pool of real savings is declining, it runs the risk of severely damaging further the pool of real savings.

The various commentators who subscribe to the view that the acceleration in money pumping could fix things imply that something can be created out of nothing. Neither the Fed nor the government can grow the economy. All that stimulatory policies can do is redistribute real savings from wealth producers to nonproductive activities. These policies encourage consumption that is not supported by wealth generating production. Without arresting the massive pumping and cutting government outlays, the US economy is heading toward a prolonged slump.

Now, the pool of real savings has been badly hurt by the past reckless monetary policies of the Fed, in particular by Ben Bernanke’s Fed in 2008. Also, the recent huge monetary pumping by the Fed, which is mirrored by the large increase in our monetary measure AMS, is going to weaken significantly the process of real savings formation. This in turn is setting the foundation for a prolonged economic slump. Observe that the yearly growth rate of AMS shot up from 3 percent in September 2019 to 60 percent by July 2020.

The response of the government and the Fed to the covid-19, coupled with the likely depleted pool of real savings on account of the past reckless policies of the Fed and the government, has made the economic bust more severe. Contrary to popular thinking, the covid-19 did not set the economic bust as such. It was set in motion by a downtrend in the monetary growth during August 2011 to August 2019.

The response of central authorities to the covid-19 in terms of lockdowns and massive monetary pumping has damaged further the pool of real savings and pushed the economy into a severe slump. I suspect that the pool of real savings is currently declining. The likely decline in the pool of real savings undermines not only false nonproductive activities but also productive economic activities. Consequently, if reckless Fed and government policies that have weakened the process of real savings formation continue, it is quite likely that the US economy could experience a prolonged economic stagnation.

In the meantime, rather than allowing businesses to get on with wealth generation, American politicians are making plans for how to redistribute further the already diluted real savings of the wealth generators. While the White House proposes a $1.3 trillion coronavirus aid bill, the Democrats hold that this sum is not large enough and are suggesting that it should instead be around $2.2 trillion.

There is a way out of the crisis: by cutting to the bone government spending and the closing of all the loopholes for the creation of money out of “thin air.” By allowing businesses to do their jobs, the process of real wealth generation could be activated and the economy could escape the path of prolonged stagnation in no time. All that is required is that central authorities step aside and allow businesses, which know better how to generate prosperity, to get on with the task of growing the economy.

via ZeroHedge News https://ift.tt/32feiEr Tyler Durden