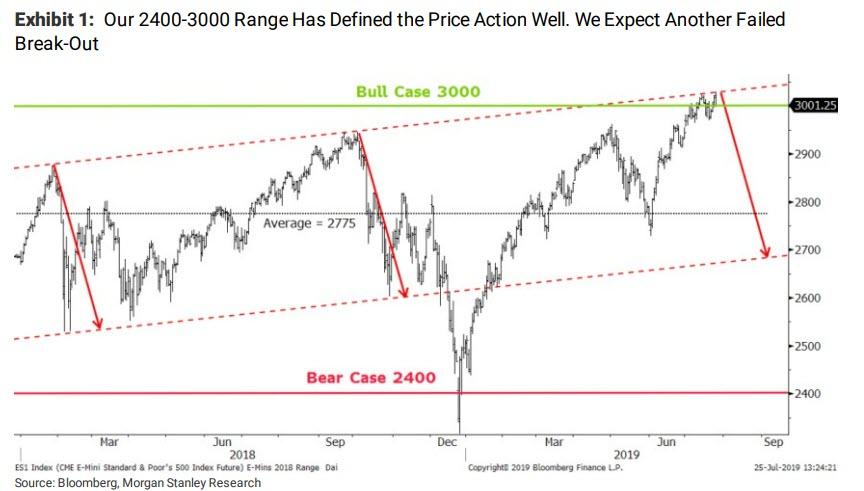

Authored by Michael Wilson, Morgan Stanley chief equity strategist

Don’t Blame the Fed or Trade – It’s the Fundamentals

Rarely has the adage “Don’t fight the Fed” been more apropos than over the past 18 months. In 2018, the Federal Reserve’s aggressive tightening contributed to a bear market for most stocks, while this year’s equally aggressive dovish pivot has resulted in a new bull market for some. Since our call 18 months ago for a multi-year consolidation in global equities, the average global stock and index is flat to down 10%, while the leading S&P 500 Index is now barely up with a lot of intermittent ups and downs. In short, thanks to the Fed’s policy shift, we’ve seen a consolidation that leaves us at the high end of our expected range.

Last Wednesday, the Fed made good on its dovish pivot by cutting the fed funds rate by 25bp – the first cut in 11 years by the world’s most influential central bank. While it wasn’t 50bp as our team and some others were expecting, the Fed also announced an immediate end to its balance sheet reduction program (affectionately known as QT for quantitative tightening). This combination is unequivocally positive for asset prices. However, to the chagrin of many, the markets reacted negatively, with stocks selling off on Wednesday afternoon and rates plummeting at every tenor, leaving the yield curve still inverted. Investors were quick to blame Chair Powell for failing to communicate a more dovish message, suggesting that they had been misled by prior Fedspeak. But this seems unfair, given that the Fed delivered a more dovish action than had been priced in if you include the end of QT.

Investors should have been more focused on the fundamentals. Going into the Fed meeting last week, my contention was that stocks had already discounted a dovish pivot and investors were potentially ignoring the continued deterioration in fundamentals, as well as other risks including trade. In short, I argued that no matter the outcome, the meeting was likely to provide an excuse for the rally to roll over. After a decent bounce in stocks on Thursday morning, trade resurfaced with President Trump’s tweet that the US would levy new 10% tariffs on the remaining US$300 billion of Chinese imports. This led to a sharp reversal in the afternoon, quashing any lingering hopes that the rally from June was intact. Markets look to have been overly complacent about trade as well. Given the lack of any real progress in talks with China earlier in the week, that risk was still very much alive prior to the president’s tweet.

From here, investors must decide if the Fed can deliver the growth needed to justify current or higher prices. Most investors I speak with still think that this is a mid-cycle correction in the economy and that any Fed cuts are simply an insurance policy. If one believes this, shouldn’t a “mid-cycle adjustment” (in Chair Powell’s words) be enough? Given the very broad and steep decline in many leading indicators and corporate earnings growth, I’ve made the case that we are far from mid-cycle and closer to end of cycle, especially for corporate profits.

On that note, I adamantly disagree with the claim that 2Q earnings have been strong or even good. To the contrary, the results and guidance so far indicate that S&P 500 forward 12-month consensus estimates remain too high and are likely to fall another 5-10%.

Bottom line, the financial markets’ initial negative reaction to the Fed’s first rate cut since 2008 shouldn’t have come as a surprise. Trade escalation is not a new risk; it was simply overlooked.

Therefore, I continue to expect a 10% correction in the S&P 500 this quarter.

So what about the adage that you shouldn’t fight the Fed? History suggests that Fed pauses after a long rate-hiking campaign, like the one we had in January, always lead to a strong market rally – exactly what we’ve seen this year. However, the beginning of a new rate-cutting cycle is typically not good for stocks, as the last two examples (January 2001 and September 2007) clearly show. The lesson is that while a change in Fed policy can affect financial conditions – and hence asset prices – almost immediately, reversing an economic slowdown with easier monetary policy takes time. Stay more defensively oriented in your portfolios until the slowdown is properly priced.

via ZeroHedge News https://ift.tt/2T80rtd Tyler Durden

Proposals from interested vendors are due later this month…

The Federal Bureau of Investigations aims to acquire access to a “social media early alerting tool” that will help insiders proactively and reactively monitor how terrorist groups, foreign intelligence services, criminal organizations and other domestic threats use networking platforms to further their illegal efforts, according to a request for proposalamended this week.

“With increased use of social media platforms by subjects of current FBI investigations and individuals that pose a threat to the United States, it is critical to obtain a service which will allow the FBI to identify relevant information from Twitter, Facebook, Instagram, and other Social media platforms in a timely fashion,” the agency said in the RFP.

“Consequently, the FBI needs near real-time access to a full range of social media exchanges in order to obtain the most current information available in furtherance of its law enforcement and intelligence missions.”

Though the request was initially released on July 8, the FBI amended it this week to extend the relevant dates: The agency’s answers to vendors moved from July 25 to Aug. 7, and the proposal due date shifted from Aug. 8 to Aug. 27. Though the original proposal listed the anticipated award date as Aug. 30, it could be pushed back due to these changes.

Still, the proposal comes at a time when society is growing accustomed to the painful reality of the weaponization of social media outlets to cause harm. Earlier this year, a mass shooter in New Zealand opened fire at two mosques killing 50 people and injuring many more – he posted a 74-page manifesto and images of his weapons online ahead of the attack and livestreamed the shooting directly on Facebook Live. And the shooter who killed three people at the Gilroy Garlic Festival in California Sunday also previously posted online about an 1890 racist manifesto, which has been deemed a “staple among neo-Nazis and white supremacists on extremist sites.”

“It is an acknowledged fact that virtually every incident and subject of FBI investigative interest has a presence online,” the bureau said in the project’s statement of objectives.

“The mission critical exploitation of social media enables the Bureau to proactively detect, disrupt, and investigate an ever growing diverse range of threats.”

The FBI ultimately wants an interactive tool that can be accessed by all headquarters division and field office personnel via web browsers and through multiple devices. Interested vendors should have the capabilities to offer the agency the ability to set filters around the specific content they see, send immediate and custom alerts and notifications around “mission-relevant” incidents, have broad international reach and a strong language translation capability and allow for real-time geolocation-based monitoring that can be refined as events develop.

And when it comes to specific persons-of-interest and suspects already involved in open investigations, the bureau wants the ability to obtain their full-scope social media profiles from across the various platforms and insights into their affiliations with various groups across the world wide web.

“Items of interest in this context are social networks, user IDs, emails, IP addresses and telephone numbers, along with likely additional account with similar IDs or aliases,” the agency said.

The firm-fixed-price contract will be awarded on a best-value basis and will include one base year and four one-year option periods.

via ZeroHedge News https://ift.tt/2T58o2A Tyler Durden

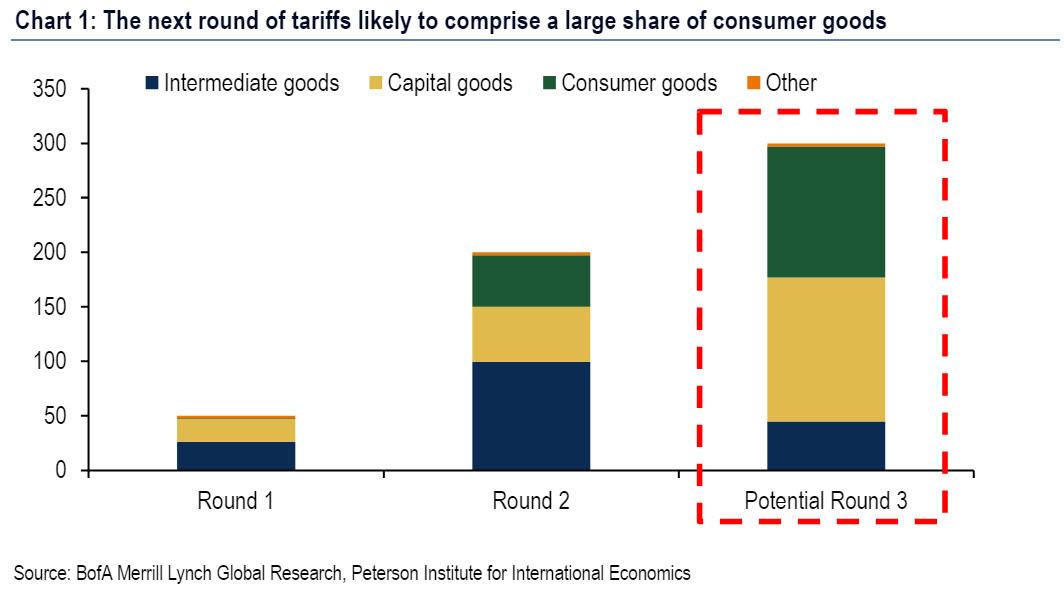

For the past year, one of the points of biggest contention among economists and traders is that despite what is now a 1+ year trade war with China, inflation due to higher tariffs has been strangely missing, with some claiming that the goods targeted in previous tariff rounds were either not “consumer” enough, or simply had more affordable substitutes from other, non-Chinese supply chains, allowing consumers to avoid having higher prices passed upon them.

While this may be correct, everything is about to change, because as Bank of America team of economists writes, Trump’s latest tariff announcement from last Thursday, when the president shockingly unveiled 10% tariffs on $300BN in Chinese imports starting September 1, “is a major escalation.” The reason for this is that past measures had mostly avoided consumer goods. By contrast, the threatened tariffs would cover $120bn of consumer goods, out of $300bn in total, and since BofA expects the tariffs to be implemented, either on schedule or later this year, the period of dormant trade war inflation is about to end with a bang, not a whimper.

What happened?

For those who were blissfully on holiday last week and missed what was without doubt the most insane 72 hours in capital markets in 2019, on Thursday President Trump announced that the US will impose 10% tariffs on all Chinese goods that were excluded from earlier measures. The announcement reportedly came soon after the President was briefed on Treasury Secretary Mnuchin and Trade Representative Lighthizer’s negotiations in Shanghai on Tuesday (July 30). There was also a press report on Wednesday arguing that China was intentionally slow-walking the negotiations in the hope of getting a better deal. It is probably not a coincidence that the President stated after announcing the tariffs that Chinese President Xi was not moving fast enough. Most importantly, and as we predicted just hours before Trump’s “shock” announcement, Bank of America does not think it is a coincidence that the tariffs were announced the day after the Fed cut rates and ended quantitative tightening. Indeed, as we noted yesterday, as a result of the phrasing in the latest FOMC statement which bizarrely ushered in the first easing cycle in 12 years not due to domestic but international considerations, the Fed is now effectively underwriting Trump’s trade war, as shown in the following chart (read more here).

Was Trump’s announcement a negotiating tactic?

Most likely, yes… but as BofA’s Aditya Bhave notes, “that does not mean it is a bluff. We have seen this movie before. President Trump has implemented every measure against China that he has threatened, albeit sometimes after a delay. Prior announcements were probably also meant to up the ante on China, but China has consistently refused to buckle under pressure. Why should this time be different?”

Why indeed, especially if with every incremental escalation in the trade war, the Fed is forced to cut rates further, precisely as Trump demands.

What does this mean for the outlook?

From the perspective of Bank of America, the pattern of US protectionist measures pointed to a desire to avoid tariffs on consumer products due to concern about “sticker shock” for consumers. This was arguably why a large share of consumer goods imports from China were excluded from earlier rounds of tariffs, and why tariffs on autos and parts have repeatedly been threatened but not implemented.

But, as Bhave writes, “the latest announcement is a game changer. About $120bn of the imports covered by the threatened tariffs are consumer goods, compared to less than $50bn in total in the earlier rounds.”

And since the “sticker shock” concern does not appear to be as important for Trump as was previously thought – perhaps as a result of the stock market hitting fresh all time highs, which in Trump’s mind offsets “slightly” higher prices, BofA now expects the US to follow through on the President’s threat and implement the 10% tariffs. In terms of timing, there may be a small delay, particularly if there is a big selloff in equities in August (which however will only force the Fed to cut sooner, thus boosting prices), but in general, the bank is confident that the tariffs will go into effect this year.

This also means that in terms of further escalation in the trade war, “all options are now on the table” even though the baseline assumption is that there will be only modest additional measures on various fronts. However, BofA does see substantial risk that the 10% tariff could get increased to 25%. At that point there would be 25% tariffs on all Chinese imports; Additionally, there is also a high risk of tariffs on imports of autos and parts from outside North America (with South Korea also likely getting an exemption), particularly as such tariffs would incentivize producers to meet the USMCA’s stricter local-content rules.

In keeping with the “more trade wars, more rate cuts” dynamic, there could also be measures against other countries that are benefiting from shifting supply chains, have large and growing trade surpluses with the US, or are allowing Chinese goods to evade US tariffs via trans-shipment. The first target among such countries suggested by BofA, would likely be Vietnam, against whom President Trump has already threatened action. Whether major additional measures get implemented will ultimately depend on political, economic and market incentives.

Impact on the presidential elections.

The US-China trade war is unlikely to de-escalate going into the 2020 Presidential elections, according to BofA. Indeed, the escalation going into the 2018 midterms suggests that “the Trump administration views getting tough on China as an effective strategy in the polls” according to BofA. Meanwhile, escaping the tit-for-tat loop of more tariffs has become next to impossible as there is growing bi-partisan support for a more confrontational policy stance vis-à-vis China because it is a rising geopolitical rival with a non-market economy.

Regarding other fronts of the trade war, it is a closer call, according to the BofA economists. On the one hand, protectionism has been an important part of the Trump agenda from day one. China has been the most prominent target of the President’s critiques, but it has not been the only one. This is why we see risks of measures against other countries and sectors. On the other hand, there is not as much political support for other protectionist policies: China is “special.” The Trump administration also appears to have come around to the view that it is best to fight one battle at a time. Unless there is at least a lasting ceasefire with China, there might not be sufficient bandwidth for other large measures.

A Policy Collar Put

The other key determinant of the future path of the trade war as observed by BofA, will likely be the state of the economy and the markets. After the G-20 meetings, the bank – among many others – cited the risk that the Fed’s dovish turn was emboldening the Trump administration to keep escalating the trade war. This premise was that the markets and the economy were stuck in a “policy collar”, between a very accommodative Fed (the “Fed put”) and the uncertainty shock from the trade war (the “Trump call”).

Of course, this week’s events only confirmed this view (see feedback loop chart above). This is what happened:

On Wednesday, Fed Chair Powell said that concerns about the trade war were one reason for the Fed’s 25bp rate cut.

On Thursday, President Trump escalated the trade war further.

The markets responded by pricing in substantially more Fed accommodation.

Between the time of the announcement and close of business on Thursday (a little over 3.5 hours), the 2-year Treasury yield fell by almost 8bp and the markets priced in about 10bp of additional Fed rate cuts by year-end.

As a result, life for the Fed has become far harder in two ways:

1. It will probably be trying to offset an even larger negative economic shock. But even if that shock does not materialize, the rally in rates means that the Fed will have to use up more ammunition if it wants to meet market expectations and avoid financial tightening. The risk is of a perverse feedback loop in which trade-war escalation keeps offsetting Fed easing, leaving the Fed with very little ammunition to fight the next recession, while the economy remains relatively soft.

What’s worse is that the game theoretical equilibrium that has emerged for the trade war is one of “no pain, no deal.” As we mentioned above, a substantial equity market correction could delay the threatened tariffs. By the same measure, it could disincentivize further escalation. Alas, so far the market refuses to even consider a “substantial correction” – while the S&P 500 did sell off by almost 2% on Thursday after the tariffs were announced, this is a negligible drop from an all time high in the S&P above 3,000. As a result, and given that markets were at all-time highs just a few days earlier, BofA believes that it will probably take at least a market correction (i.e., a 10% decline) to move the needle on trade policy.

2. A shock to consumer spending and confidence could also have a similar impact. So far the US consumer has remained on solid footing because of the strength of the labor market. Even though academic research suggests that the cost of the tariffs has been almost entirely passed on to consumers, confidence has held up. This is likely because the tariffs were mostly on intermediate goods rather than final goods, and so their effects were obfuscated.

That could change with the latest threatened tariffs, which as mentioned above cover $120bn in consumer goods. Most of these goods are electronics-cell phones, laptops and tablets-whose prices are very visible. But the shock to prices will ultimately depend on the renminbi, which is already down almost 10% since the start of the US protectionist push last spring. If the PBoC allows another leg of depreciation, letting USDCNY break above 7, the FX move might largely offset the impact of the tariffs.

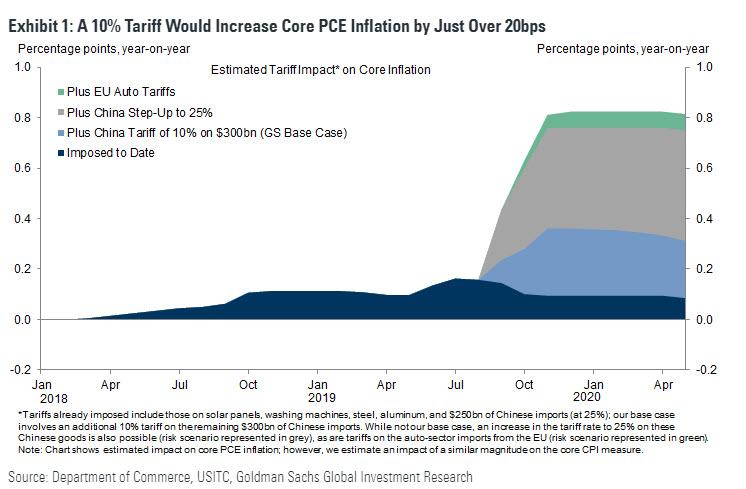

And speaking of a sudden inflation spike, here we refer to a recent Goldman Sachs report which noted that the bank’s economic forecast had already assumed a 10% tariff on $300bn of imports starting in September; as a result, the bank expects these tariffs, if implemented, would increase core PCE inflation by slightly more than 20bps by year-end. And while Goldman’s baseline forecast does not assume that tariffs rise from 10% to 25% on the $300bn just announced, nor does it assume tariffs on EU auto imports, though both are risks. Indeed, as shown in the chart below, even without a full-blown trade war escalation consumer inflation is about to get much hotter. However, should the tariffs step up to 25%, and if Trump implements EU auto tariffs, watch as inflation explodes higher.

And speaking of the economy, Goldman estimates a GDP hit from the 10% tariff on $300bn of China imports of 0.1-0.2%, on top of a 0.2% hit from the tariffs imposed to date. This means that the combined GDP drag would rise to 0.5-0.6% if the tariff rate on $300bn of China imports were raised to 25%, and to 0.7% if 25% tariffs were imposed on EU auto imports. In other words, prepare for the most violent stagflationary episode in decades, one which Powell may simply resign instead of deciding to hike rates to address.

Unintended consequences

Of course, nobody can predict all the possible adverse outcomes from an escalating trade war, especially now that China has its own geopolitical row with Hong Kong to manage: as BofA notes, a conflict of the magnitude of the US-China trade war “is bound to have far-reaching, unintended consequences.” Most importantly, it could extend ongoing global monetary easing. About half of the central banks that we cover have cut rates this year, and many more cuts are likely in the pipeline as further escalation in the trade war likely leads to an even weaker outlook for global (particularly Chinese) demand.

Speaking of pipelines, there could be major implications for oil for two reasons. First, weaker global demand would likely weigh on oil prices. Second, there is now a greater risk that China will decide not to comply with the US oil sanctions against Iran. This would ease global supply conditions, leading prices even lower. Brent was down more than 3% on Thursday after the tariff announcement. This could result in a further deflationary impulse across the core inflation supply chains, which accelerates the Fed’s rate cutting schedule.

Indeed, as BofA points out, “a big drop in oil prices would suppress inflation expectations, making it even harder for the major developed-market central banks to reach their inflation targets. Again, this would mean lower global policy rates, which in turn would imply that Fed easing might not have much impact on the dollar.”

Meanwhile, Trump’s frustration with the strength of the dollar could push his Administration to “retaliate” by intervening in FX markets or imposing tariffs on countries whose currencies are deemed to be too weak, or as BofA puts it, “a tangled web indeed.”

* * *

Finally, a word on Brexit. So far it appears that the BoE has attempted to hold the line on cuts ahead of the October 31 deadline. Will the latest trade escalation push the BoE over the line into talking about rate cuts? If so, the resulting financial accommodation might make a no-deal Brexit slightly less painful and therefore slightly more likely. There might not be enough time for this dynamic to play out. But the feedback loop is very familiar: one only needs to glance across the pond to understand it.

via ZeroHedge News https://ift.tt/2YFwxxC Tyler Durden

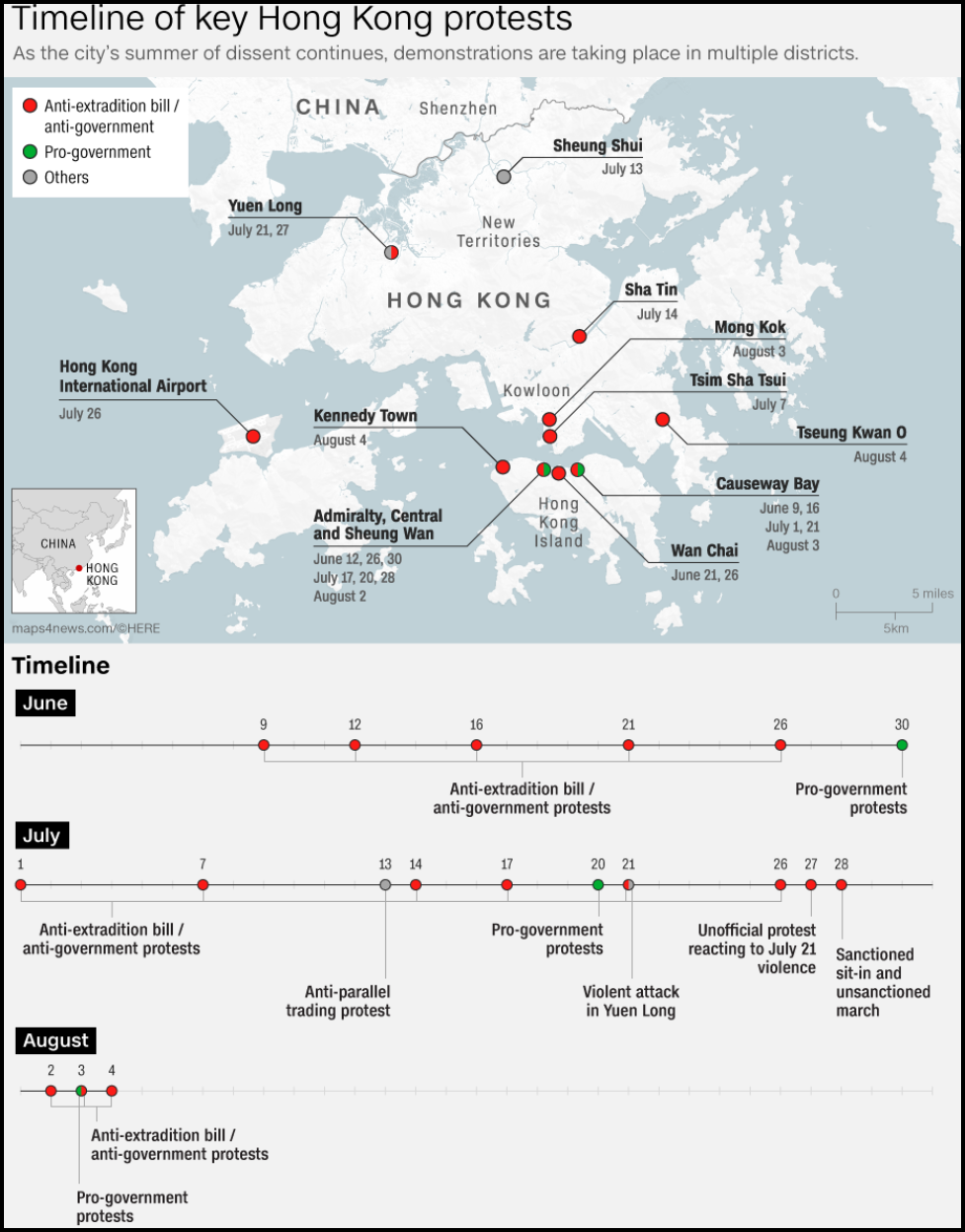

The government of Hong Kong has warned that the ongoing protests could devolve into a “very dangerous situation” after demonstrators filled the streets, squaring off with riot police as traffic came to a complete standstill.

Sunday marked the third consecutive day of demonstrations out of a nine-week protest which began with outrage over a controversial bill which would have allowed suspects to face extradition to mainland China – a measure which has been paused but not taken off the table. Since then, demonstrators have demanded that arrested protesters be exonerated, along with the implementation of universal suffrage.

A protester throws a stone at a police station in Tseung Kwan O, a residential district, in Hong Kong. PHOTO: KIM KYUNG HOON/REUTERS

Protesters staged two massive rallies on opposite sides of the city, according to the Wall Street Journal.

Thousands marched in the largely residential area of Tseung Kwan O while more rallied in Kennedy Town on the west side of Hong Kong Island.

In the city’s Western district, police fired tear gas to disperse protesters who deviated from the approved rally location. Later, many suddenly decided to head to Causeway Bay, a popular shopping and entertainment district, occupying a busy thoroughfare. Sirens blared across the city as a group of protesters blocked the entrance to the cross-harbor tunnel, causing a massive traffic jam. –WSJ

On Sunday night, Hong Kong authorities said that the unrest was a “blatant violation of law, wanton destruction of public peace and violent attacks on the police will harm Hong Kong’s society, economy and our people’s livelihood,” adding “Such acts have already gone far beyond the limits of peaceful and rational protests for which the government and general public will not condone under any circumstances.”

“Otherwise they will push Hong Kong into a very dangerous situation.“

Via CNN

On Saturday, police and protesters clashed across five districts, with multiple police stations besieged and hundreds of activists confronting riot police.

The antigovernment protest movement has appeared to gain steam even as police use more aggressive tactics to bring it to heel. After tense confrontations last weekend, police arrested dozens and took what many here viewed as a hard-line step by charging them with crimes that carry prison terms of as long as 10 years. Police said they arrested more than 20 people in relation to Saturday’s protests, including for unlawful assembly and assault. –WSJ

“If the government is waiting and hoping the protests fade out on their own, they are going to be disappointed,” said attorney Antony Dapiran, who authored a book on dissent in the city.

When the protests began in June, an estimated two million people marched against the extradition bill. Since then, local business leaders say the movement is taking an economic toll – as they have reported soft sales vs. last year. One firm found that travel bookings to Hong Kong appear to have fallen.

That said, the protests show no sign of slowing down – as the mostly younger demonstrators say they are angry over bleaker political and economic prospects than their parents faced. Hong Kong is one of the world’s most expensive places to live, and has one of the largest disparities in wealth to boot.

“The situation is really precarious,” said Hong-Kong human-rights lawyer Albert Ho, who told the WSJ “Right now, there are a lot of young people out there who feel they have nothing to lose, who feel they are looking at the end of rule of law, of a legal system, of a culture.”

via ZeroHedge News https://ift.tt/2T47KCc Tyler Durden

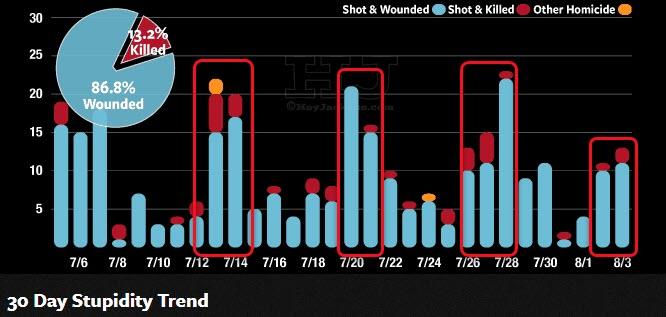

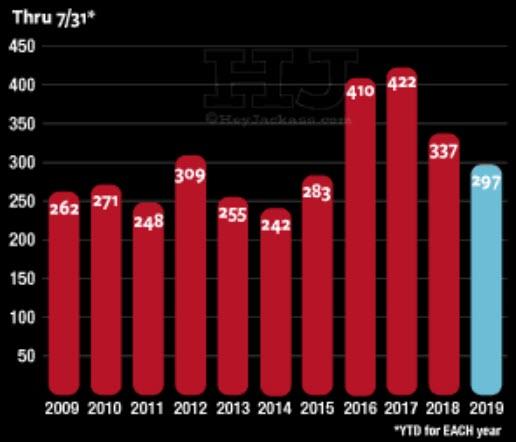

At risk of being slammed for pure racism, amid a duo of terrible mass shootings in El Paso and Dayton, we thought it noteworthy that a somewhat “normal” weekend of death and mayhem in Chicago barely even warranted a mention in mainstream media headlines.

As HeyJackass.com reports (the most definitive tracker of Chicago’s ‘values’), there has been 50 shootings so far in August (yes it’s the 4th of the month):

Shot & Killed: 4

Shot & Wounded: 46

This weekend has seen 4 killed and 38 wounded, but as the chart below shows, this is actually ‘better’ than normal for a Chicago weekend…

As The Epoch Times’ Jack Phillips reports, at least seven people were shot and wounded on Aug. 4 as they gathered near a children’s playground on Chicago’s West Side. The people gathered at 1:20 a.m. as they stood in the park on the 2900 West Roosevelt Road when a person opened fire from a black Chevy Camaro, said Chicago Police.

According to NBC Chicago, a 21-year-old male was shot in the groin before he was taken to Mount Sinai Hospital in critical condition.

A 25-year-old woman was hit in the arm, torso, and leg, and she was taken to Mount Sinai, police told the local station.

A 22-year-old was also shot and was rushed to the hospital, and she is in stable condition, officials said.

Police added that a 20-year-old man and a 19-year-old woman were taken to Stroger Hospital.

A 23-year-old and a 21-year-old took themselves to Mount Sinai with gunshot wounds, ABC7 reported.

So far, in 2019, more than 1,600 people have been shot in the city (of which 274 have been killed), which is about 129 fewer than in 2018, according to the Chicago Tribune.

“Shooting victims are most concentrated in the South and West sides for shooting victims so far in 2019,” the report noted.

What is odd though is the lack of Democratic Party presidential candidates “praying for Chicago” or unleashing hashtags demanding ever more gun control (oh wait isn’t Chicago among the most gun-constrained cities in the country?)

Illinois is one of seven that requires licenses or permits to buy any firearm, and it’s one of five that requires waiting periods for buying any firearm. The Law Center to Prevent Gun Violence, which tracks gun laws nationwide, has given the state a B+ for its gun laws. Chicago itself has some tough laws – there is an assault-weapons ban in Cook County, for example.

via ZeroHedge News https://ift.tt/2ZvXlli Tyler Durden

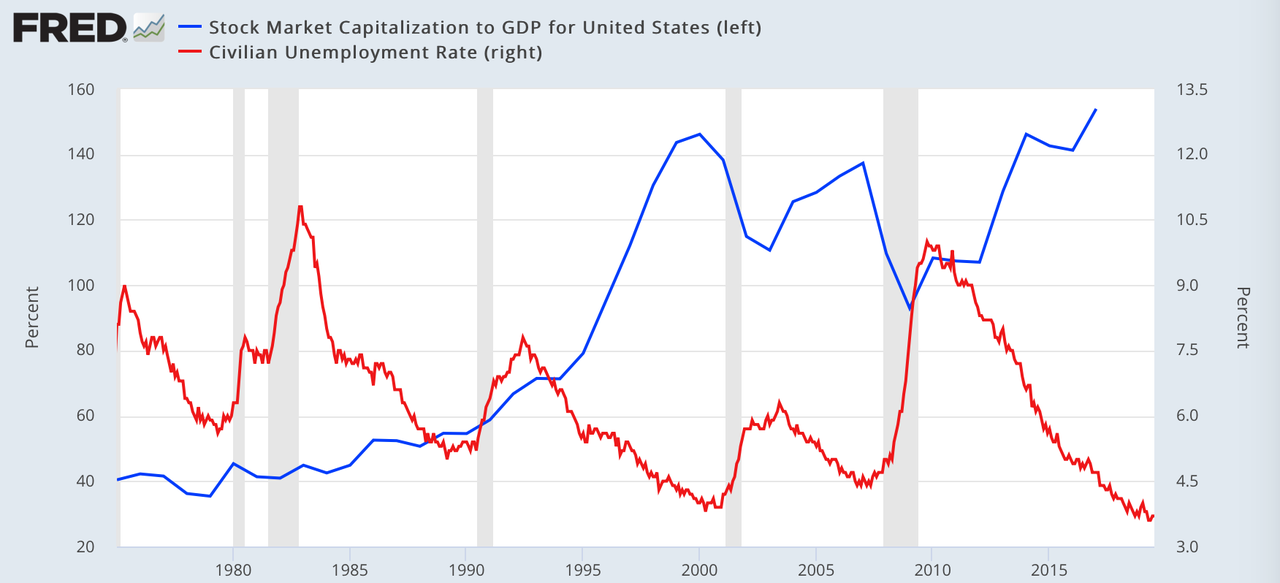

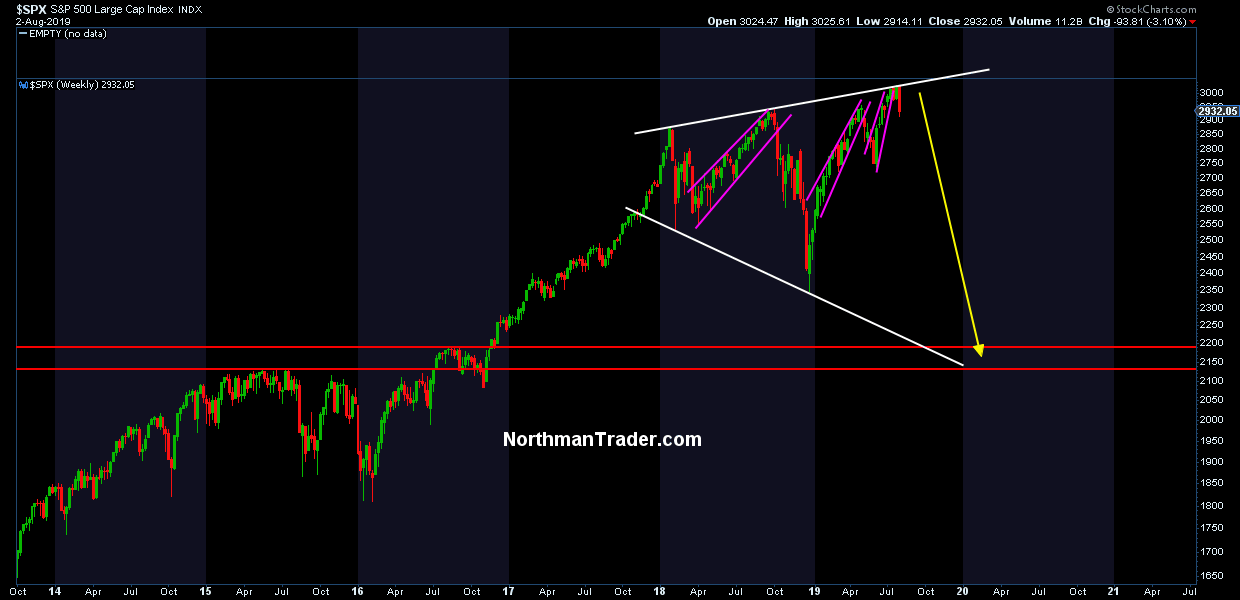

Are we hitting the wall here? Markets. Economy. Technicals. Valuations. All appear at a key crossroads here. Last week’s 3% pullback, while in itself not seemingly dramatic, came at a very key point. Whether it is meaningful is too early to tell, but I have some eye opening data points for you that suggests it may very well turn out to be extremely meaningful.

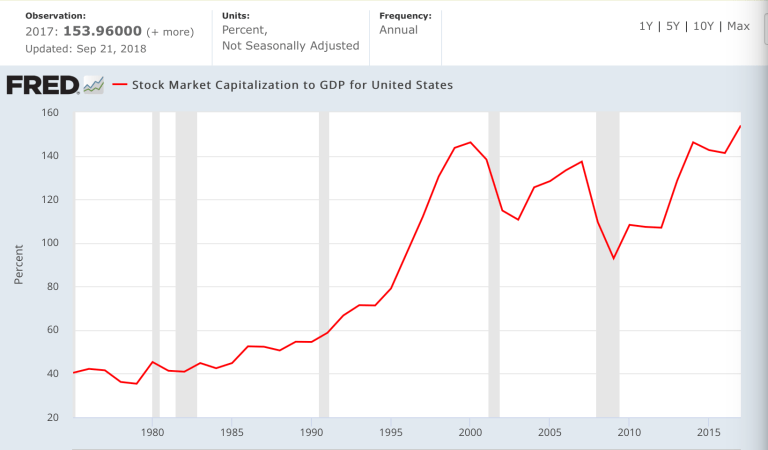

In last weekend’s update (End Game) I highlighted the issue of market capitalization versus the underlying size of the economy. Let me dig a little deeper.

Is there a natural wall beyond which bubbles cannot go before they revert back to a more natural state of valuation? It’s a serious question especially looking at the structural context of the last few bubbles. The biggest bubbles in our lifetimes were the 2000 tech bubble, the 2007 real estate bubble and the monstrosity we are witnessing now, the central bank, cheap money bubble.

All 3 have done something unique. They have vastly accelerated asset prices above their historic track record. In 2000 and 2007 these bubbles moved stock markets wildly above the mean and investors got punished badly. This is the chart I showed last week:

Peaks of 147% and 137% respectively. Now this bubble has arrived in full vengeance on the heels of $20 trillion in central bank intervention, a global collapse in yields and the TINA effects.

Now look closely what just happened in the past 18 months:

We keep hitting the same wall. January 2018 nearly 150% market cap to GDP and stocks got punished with a 10% correction.

Last September/October we hit a slightly lower high around 147% and stocks got hit with a 20% correction.

Now in July we hit 145%, another slightly lower high, and stocks have begun selling off again.

Is that it? Is that the valuation wall? How far and for how long can stock markets stay this far disconnected from the underlying size of the economy? All of history says: Not for very long.

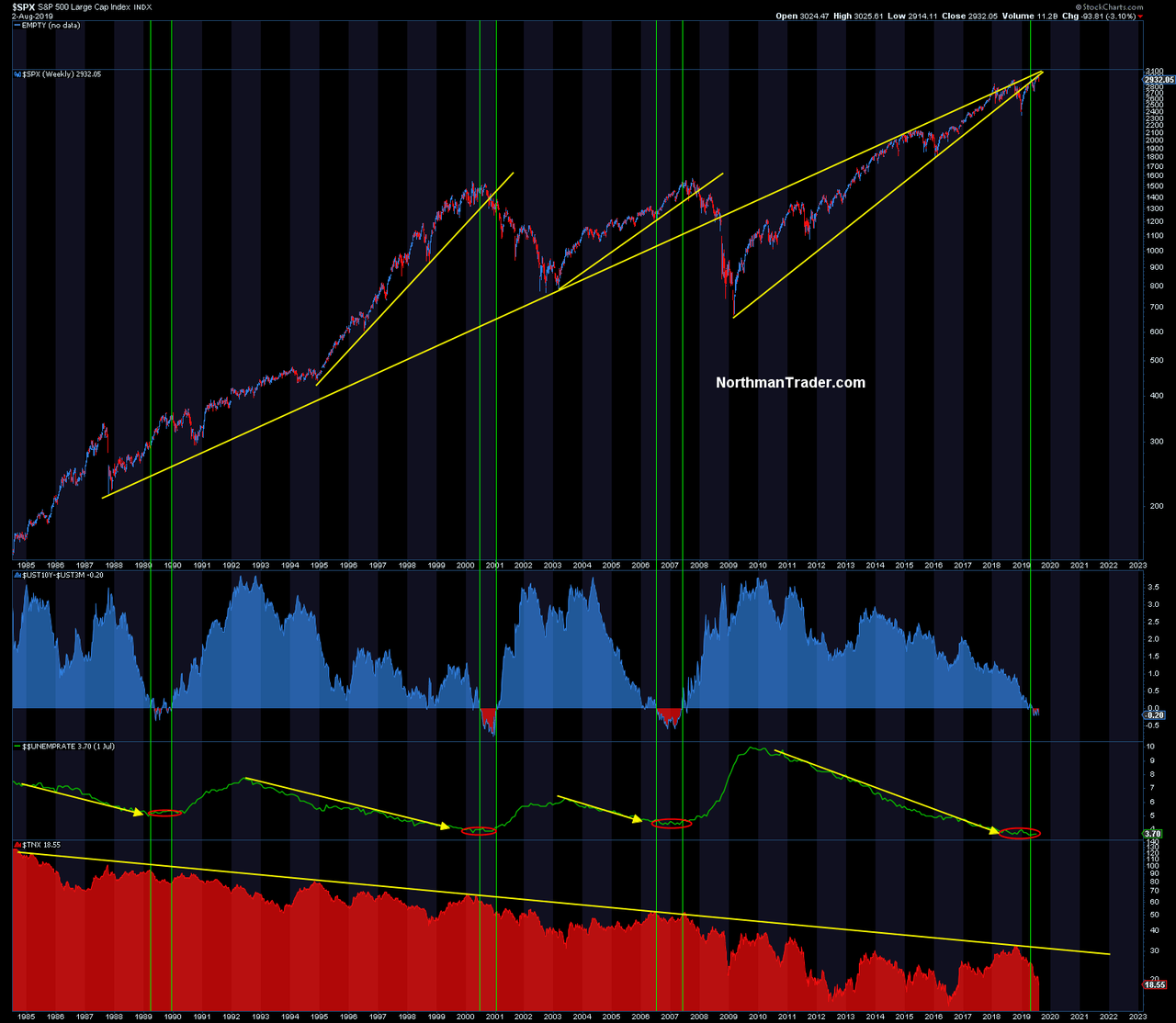

Incidentally, why these slight lower highs? Because the larger stock market is weakening underneath from new high to new high. It’s what I’ve outlined with divergences and weakening participation, but neatly captured by the value line geometric index:

But the plot thickens.

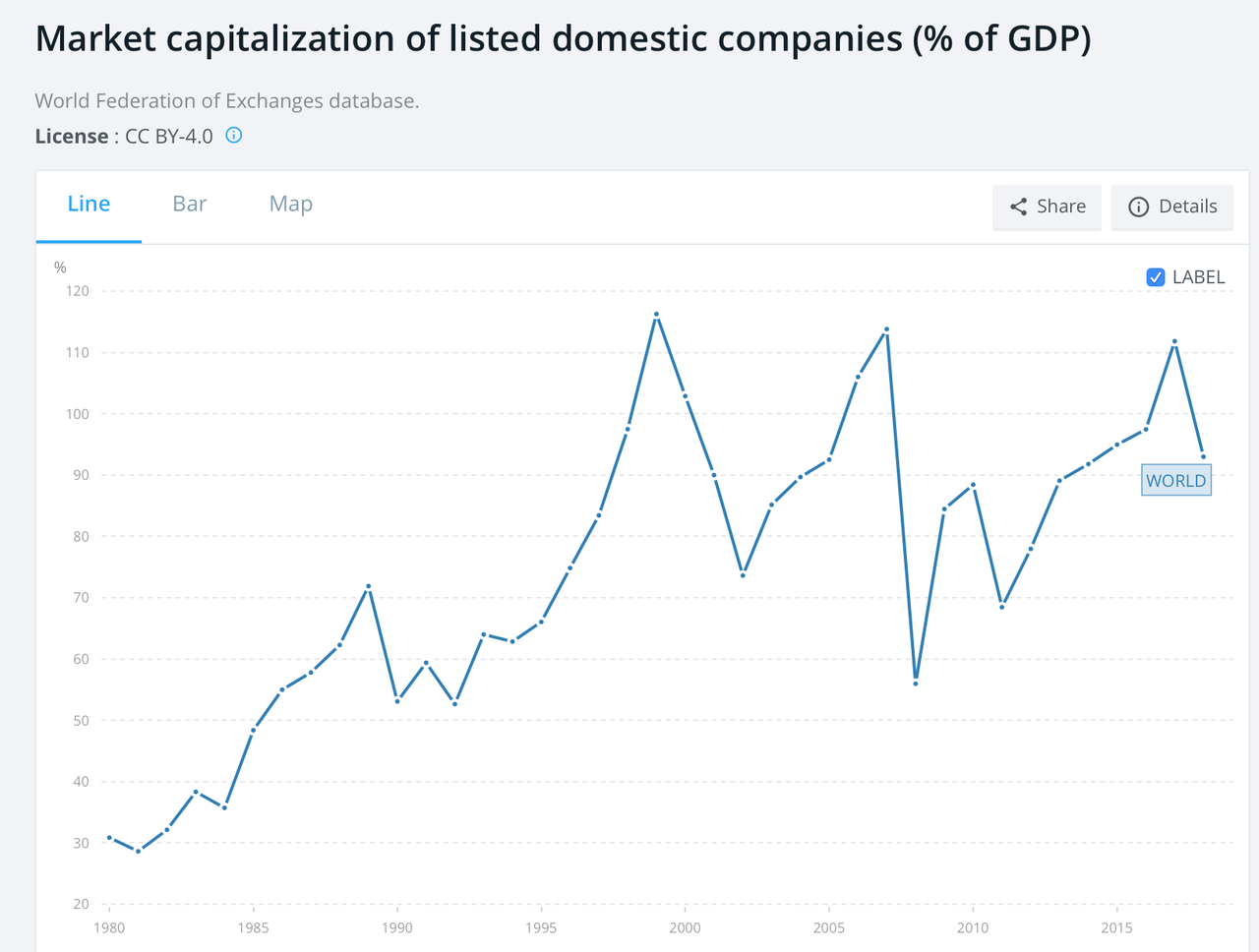

The earth is not flat, despite some adherents to that fantasy, the same valuation wall can be observed across the globe (via Wordbank):

Each time market capitalizations cross the 110% mark things get iffy don’t they? Added plot twist: The world can lead in the realignment to reality process. Note the global valuation scheme peaked in 1999. US markets famously puked some more highs out into March of 2000. Well, this time around the world peaked in 2018 and since then it’s the US again squeezing out marginal new highs in 2019. Not Europe, not Asia, no, it’s the US on its own.

The earth is not flat.

The bull case from here is based on one factor alone: The Fed. I see it in every Wall Street case for new highs. The Fed is cutting, you must buy stocks. That’s it. It’s not earnings, not growth, no, Goldman is cutting earnings and growth, but raising price targets because of the Fed.

I submit to you that, while this may indeed come to fruition, it is structurally a reckless thing to do. For 2 reasons, both of which are predicated on the same thing: History.

There is no history, none, that supports stock market capitalizations above 145% of GDP for an extended period of time. None.

There is also no history, none, that’s suggests unemployment can stay this low for an extended period of time. None.

And their certainly is no history suggests that BOTH can be maintained for an extended period to time concurrently:

None. But you are welcome to believe it if you wish.

And hence, in context, Jay Powell’s comment about a ‘mid-cycle adjustment” was either disingenuous, ignorant or an outright lie.

We are here:

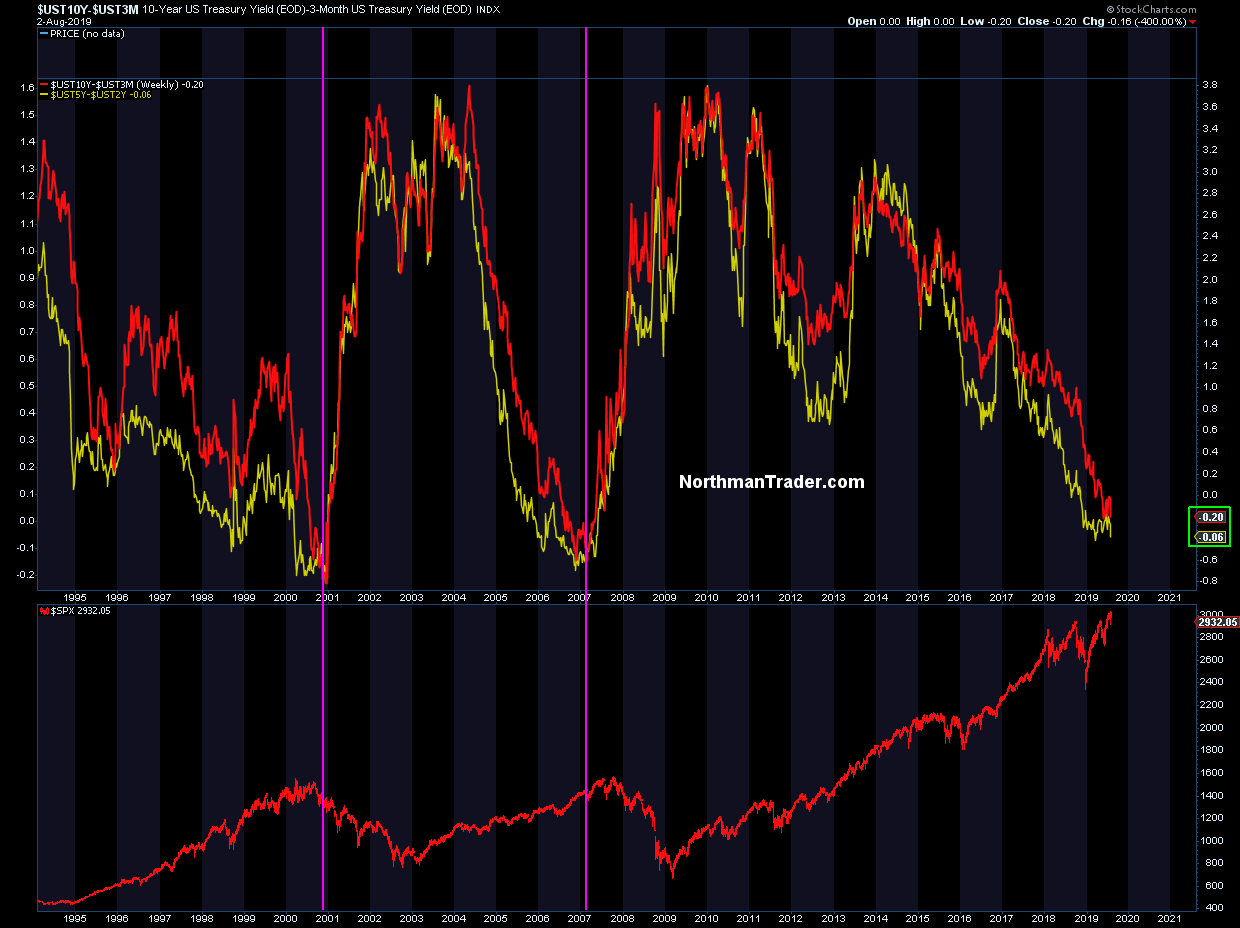

Looking at the yield curve, the reaction of the 10 year off of the 30+ year trend line and the basing of the low unemployment rate, does any of this suggest anything remotely close to mid-cycle? I submit to you that they don’t.

And switching to technicals, look at the trend lines in the $SPX chart above: The 2009 trend line STILL remains broken. I submit to you they jammed stocks higher in 2019 on the Fed pivot, the flip in policy, the promises of a rate cut, and the delivery of a rate cut, aided by still massive buybacks in the system. That’s it. They haven’t changed anything substantive on the economy. It’s still slowing, we still have trade wars and earnings growth remains flat to negative and there’s no growth in CAPEX or business investment.

Previous business cycles came to a sudden end when the employment picture changed trajectory, from a period of basing at the low end to shift to higher unemployment and a sudden steepening in the yield curves:

And guess what? Everything, the yield curves, the stock market valuation to GDP ratio at 145%, the Fed pivot, it all has led to here:

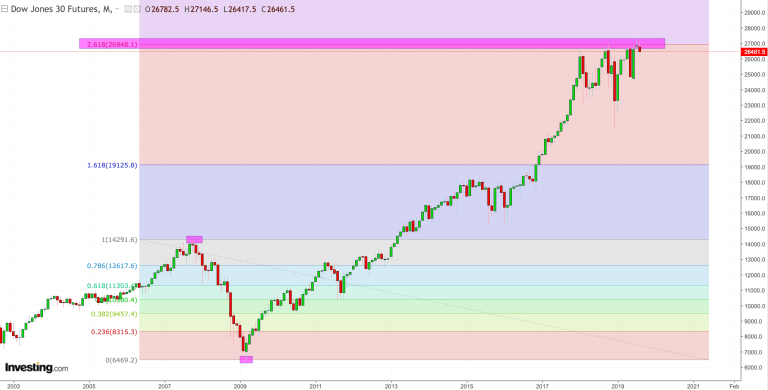

The magic 2.618 fib zone on $SPX (we missed it by a few handles) and exceeded it temporarily on the $DJIA:

We’ve hit walls everywhere. Technically, economically, valuation wise. To trust the Fed and to go long stocks here is to believe that none of these walls mean anything.

It’s to believe unemployment can be maintained at a historic 50 year low for an extended period of time, it’s to believe that stock market capitalization can be accelerated above a historic unproven 145% threshold for an extended period and it’s to believe in one’s ability to time any future steepening in the yield curves.

That’s a lot of believing.

I prefer seeing. And here’s what we just saw. We saw a market enter a technical risk zone that was outlined in advance:

And we saw market cleanly rejecting from that risk zone:

That doesn’t mean immediate confirmed doom and gloom, certainly not with a mere 3% from from the highs, but it speaks to the impressive confluence of technical and valuations factors that suggest that markets may be hitting the wall.

Technicals matter. Valautions matter.

For a run down on the technicals and implications please see the video below:

* * *

To get notified of future videos feel free to subscribe to our YouTube Channel. For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2T43se4 Tyler Durden

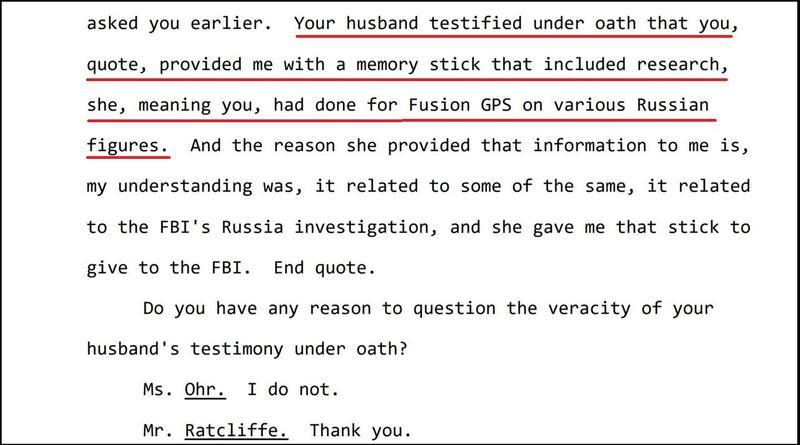

The DOJ will release a cache of FBI documents early next week related to Justice Department official Bruce Ohr, who – along with his CIA-linked wife Nellie, had extensive interactions with Christopher Steele during the period in which the FBI was using the former British spy’s fabricated dossier against the Trump campaign.

In a court filing submitted last Thursday, Justice Department lawyers said the agency will provide FBI notes of interviews conducted with Ohr to Judicial Watch, a conservative watchdog group that sued for the records last year.

Justice Department lawyers said the agency had initially determined that the Ohr transcripts, known as 302s, should be withheld in full. But “after further review in conjunction with DOJ’s preparation of its motion for summary judgment, DOJ has decided to release the requested records in part to Plaintiff,” the lawyers said.

“DOJ will make this release to Plaintiff by August 5, 2019.” –Daily Caller

According to the Daily Caller‘s Chuck Ross, Judicial Watch filed suit on September 10 for a dozen 302 reports – which are summaries of FBI interviews with suspects or witnesses. The lawsuit sought reports compiled between November 22, 2016 and May 15, 2017.

Last August, emails turned over to Congressional investigators revealed that Bruce Ohr was Steele’s conduit to the Obama administration – as Ohr was the #4 DOJ official at the time and reported to former Deputy Attorney General Sally Yates.

Steele and the Ohrs would have breakfast together on July 30, 2016 at the Mayflower Hotel in downtown Washington D.C., while Steele turned in installments of his infamous “dossier” on July 19 and 26. The breakfast also occurred one day before the FBI formally launched operation “Crossfire Hurricane,” the agency’s counterintelligence operation into the Trump campaign.

Steele was under contract by opposition research firm Fusion GPS, which the Clinton campaign hired to dig up dirt on Donald Trump. Notably, Bruce Ohr was demoted twice after the DOJ’s Inspector General discovered that he lied about his involvement with Fusion GPS boss Glenn Simpson.

FBI investigators had tasked Ohr to serve as an unofficial backchannel to Steele as part of the bureau’s investigation of the Trump campaign’s possible ties to Russia. The FBI cut ties with Steele on Nov. 1, 2016, after learning that he had unauthorized contacts with the media about his work as an FBI informant. –Daily Caller

Also interesting is that Bruce Ohr told Congressional investigators that his wife Nellie – a Russia expert who speaks fluent Russian, passed Bruce research conducted during her employment with Fusion GPS.

Republican lawmakers have suggested that the 302 reports could undercut Steele’s credibility – along with that of his largely unproven or discredited dossier.

via ZeroHedge News https://ift.tt/2yEaY6c Tyler Durden

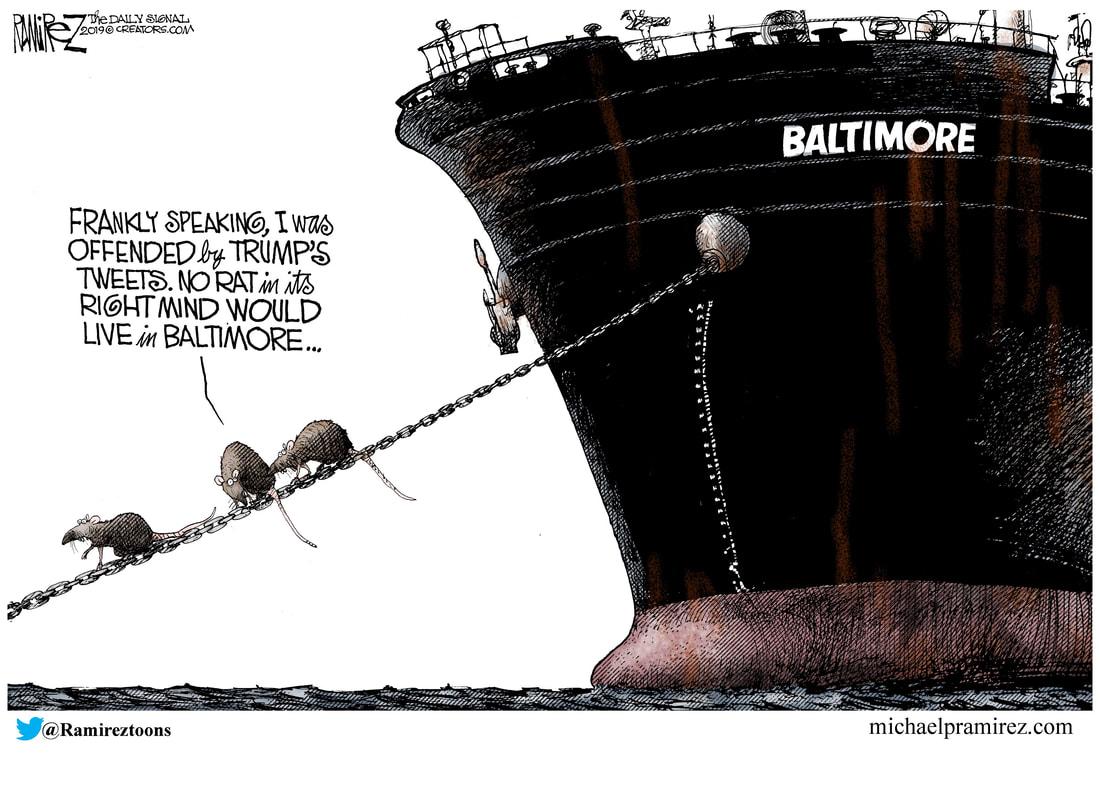

Donald Trump in recent days has repeatedly attacked the city of Baltimore for its very low quality of life, denouncing it as “rodent-infested” and noting it has a very, very high homicide rate.

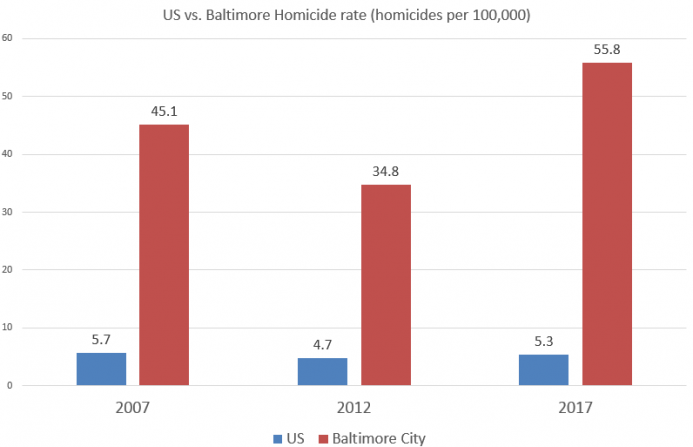

It’s difficult to find reliable stats on Baltimore’s rodent population per capita, but we can consult the FBI crime data on Baltimore’s homicide rate. When it comes to Baltimore being a haven of appalling violent crime, Trump’s not wrong.

The most recent homicide data from the FBI (2017) shows the city of Baltimore with a homicide rate of 55.8 per 100,000 population.That’s a homicide rate comparable to El Salvador (60 per 100,000) and Venezuela (56 per 100,000). Baltimore has more homicides per capita than Honduras, Guatemala, South Africa, and Brazil.

In other words, Baltimore’s homicide problem is worse than those in many of the world’s most violent countries.

In contrast, the US homicide rate in 2017 was 5.3 per 100,000 making Baltimore homicide rate ten times larger than that in the US overall.

Moreover, the gap between the US homicide rate and the Baltimore homicide rate has gotten worse over the past decade. The US rate has fallen since 2007, but it has gone up significantly in Baltimore over that time.

This gap also helps to illustrate the absurdity of referring to a “America’s homicide problem,” when the overwhelming majority of Americans live in places with homicide rates that are a small fraction of the places known for frequent killings.

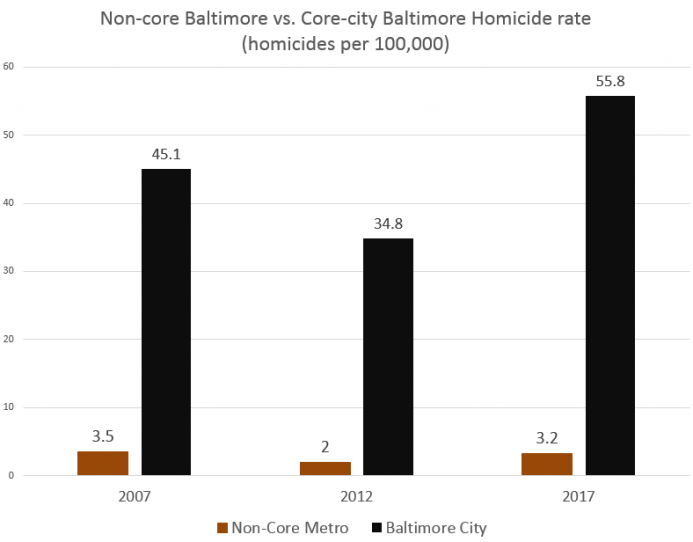

For examples, if we look at homicide rate in metropolitan Baltimore, but remove homicides from the core city, we find the homicide rate was 3.5 per 100,000 in 2017. That makes metro Baltimore — excluding the core city — one of the safest places in the Western hemisphere, similar to that of Manitoba or Saskatchewan in Canada.

Gun Control Failed

Not coincidentally, Baltimore is located in a state which “boasts” of having some of the nation’s most stringent gun laws.

According to the pro-gun-control Giffords Center, Maryland is the “fourth strongest” in terms of gun restrictions.

These restrictions were substantially strengthened in 2013 with the adoption of the Firearms Safety Act of 2013. But, as researcher Brian Bissett has noted, shooting deaths in Baltimore increased significantly after 2013, even as the population decreased:

Shootings were TRENDING DOWNWARD and Population loss was leveling off in Baltimore City prior to the Passage of the FIREARMS SAFETY ACT OF 2013 …

In 2015, DEATHS by SHOOTINGS in Baltimore City roughly doubled and have not fallen since. Baltimore has on average 275 to 300 people shot to death each year, up from about 150 to 175 prior to the passage of the FIREARMS SAFETY ACT OF 2013. Population flight from the City of Baltimore has also resumed as people are fleeing from the sharp increase in violence permeating every area of Baltimore City.” [emphasis in original.]

The Need for Self-Protection in Baltimore

The penchant for increasing gun control restrictions in Baltimore is especially tragic considering the fact that residents have no reason to believe the police are doing much to rid the city of murderers.

In 2017, for example, the “clearance rate” for homicides in Baltimore was just 27 percent. That is, Baltimore police only made arrests or otherwise “solved” homicide cases less than one-third of the time. 2018’s clearance rate increased to 50 percent, but clearance rates only reflect arrests. They don’t mean the police found the right person, and they don’t mean a suspect was successfully prosecuted in court.

Thus, it’s not outlandish to conclude that if you murder someone in Baltimore, you’ll probably get away with it.

Under conditions like these, it becomes increasingly clear why there’s a correlation between gun control and rising homicides. Personal ownership of a firearm may very well be the only thing a person can rely on a defense against being a victim of homicide.

Of course, there are things the police could do to increase their effectiveness.

For example, in a study by B. Forst, J. Lucianovic, and S. J. Cox, the authors

discovered that officers with the most arrests and convictions commonly responded most rapidly to calls for service, were better crime scene managers, were best at identifying, locating, and questioning witnesses, and displayed more of the characteristics commonly identified as relevant to successful investigators. In addition, Forst discovered that cases in which an arrest was made within 30 minutes after the case was reported had the highest chance of resulting in a conviction.

Moreover, studies have shown that other effective strategies include assigning more detectives to homicide cases. But in Baltimore, the police “had 57 homicide detectives assigned to 483 cases. The Citywide Shooting Unit had just 26 detectives for 703 cases.” This means the city — which employs approximately 2,600 police officers —devotes less than three percent of its police officers to homicide investigations.

As in most cities, the city government claims it just doesn’t have enough money. Never mind, of course, that public safety is supposed to be the number-one job of civil government. But while homicides reach new highs, city politicians are busy debating “zero waste plans ” and how to shut down garbage incinerators — plans which only cost the city more money. The city’s “Gun Task Force ” was found to be robbing people. The city’s most recent mayor was on the take.

But the city apparently chooses to fritter away its time and resources on issues other than public safety. Moreover, it appears the resources that are devoted to policing are used mostly to make arrests for small-time offenses.

If this is the case, this would simply make Baltimore’s police department like a great many other law enforcement agencies that rarely focus on violent crime.

are for serious violent crimes. Instead, the bulk of police work is in response to incidents that are not criminal in nature and the majority of arrests involve non-serious offenses like “drug abuse violations”—arrests for which increased more than 170 percent between 1980 and 2016—disorderly conduct, and a nondescript low-level offense category known as “all other non-traffic offenses.”

These offenses are behind 80 percent of all arrests.

Put a little differently: criminologist Victor Kappeler concludes that per capita, police make 14 arrests per year. But, “less than one of these arrests would have been for a violent crime and fewer than two arrests would have been for property crimes. In fact, 12 of the arrests made by our ‘average’ police officer would have been for petty crimes like minor drug or alcohol possession, disorderly conduct, and vandalism.”

Considering all of this, it’s difficult to see how the current problems in Baltimore can be solved easily without major changes in how the police do business and how the city spends its money. The police are already viewed by the residents (with good reason) as too incompetent and corrupt to be of much use in addressing the violent crime problems. So residents do little to provide police with important information in finding violent offenders. Crime then continues to spiral out of control.

Meanwhile, the city government plays the victim, pretending there are no resources to increase public safety, and acting as if the taxpayers should be willing to pay even more. It’s not hard to understand why the city’s population continues to fall.

via ZeroHedge News https://ift.tt/31ngJBz Tyler Durden

It’s Uber for the 1%: “The exclusivity of it, I like that,” a passenger aboard a private helicopter taxi taking a short flight to Southhampton told The New York Times. “I like the efficiency. I’ll be there by sunset with a glass of rosé in my hand.”

Indeed Uber has recently literally taken to the skies through Uber Copter, offering helicopter rides from lower Manhattan to JFK for a bargain deal – bargain for some at least – of on average $200 for an 8-minute, one-way flight, which began in July. “I’m not sitting in that bumper-to-bumper traffic,” another rider was quoted as saying in a report aptly titled, That Noise? It’s the 1%, Helicoptering Over Your Traffic Jam.

Uber competitor “Blade” which launched years earlier, has also been frequently hovering over New York City, making brief cross town trips, and places like the Hamptons. Image source: Forbes/Blade

A flight to the Hampton runs between about $700 and up to $1400, depending on the aircraft. “Life in a new Gilded Age,” the report says, is evidenced more and more by multiple helicopter services now ferrying commuters 3,000 feet above gridlocked New York streets, which has also raised new concerns of not just noise levels above the city, but safety after the rapid uptick in “non-essential” aviation.

In June, a major scare involved one man (the pilot) losing his life when a private helicopter smashed into the roof of a Midtown Manhattan office building, which in the initial confusing moments had people thinking a 9/11 type event could be unfolding.

The air taxi services are now in high demand, per numbers from the report:

The Port Authority of New York and New Jersey, which runs the airports, said helicopter traffic has increased in recent years. At La Guardia, there were 1,096 helicopter takeoffs and landings last year, compared with 874 in 2017, a 25 percent increase. At Newark Liberty, there were 4,391 helicopter takeoffs and landings last year, up from 3,626 in 2017, a 21 percent increase.

At Kennedy, there were 1,966 takeoffs and landings in the first five months of this year, up from 1,064 during the same period a year ago, an 84 percent increase.

But the busier skies overhead are angering others, as one person’s luxury commute becomes another’s cause for annoyance.

Image source: Uber Blog

“There’s a bunch more helicopters than there used to be,” the chairwoman of a local community board in Queens, Betty Brayton, complained to the Times. She expressed an increasingly common complaint of significantly rising noise levels above the city. “Just because somebody’s got a couple hundred bucks to get to the airport doesn’t mean they should be doing that to the negative impact of somebody else. They can get to the airport the same way everybody else gets to the airport.”

There’s actually an initiative in city council to ban all helicopter traffic over the city considered “non-essential” — which would kill the barely launched industry:

Legislation introduced Tuesday by Manhattan Democrats Mark Levine, Helen Rosenthal and Margaret S. Chin would ban all non-essential helicopter travel over the entirety of the five boroughs.

“These flights are run solely for the benefit of the private operators and the few passengers with the means to afford the expensive ticket,” said Levine in a statement. “They are loud, they pollute our air, and have no value to the public.”

Another company, Blade, said it’s about opening up the future of city commuting and experimenting with ride sharing helicopters to make the experience cheaper for all. Its chief executive, Rob Wiesenthal countered that the company seeks to move “the word ‘indulgence’ away from helicopters.”

Scene from “The Wolf of Wall Street”

The new trend in quick, efficient transport actually aims to take the experience outside merely being a luxury, 1% phenomenon.

“We basically say, look, congestion in the city has never been worse,” Wiesenthal said. “We turn a two-hour drive into a five-minute flight. We say this is not an indulgence, this is mobility.”

One new customer cited in the report said it well: “I decided you only live once… I do have to be there for a meeting” — and all with the ease of ordering through an app.

via ZeroHedge News https://ift.tt/2YGt0mS Tyler Durden

Last weekend, I noticed that two of the main newsmakers were both named Cummings, one in the US, the other in the UK. At first glance they don’t look like family, but I’ll readily admit I can’t be sure of that.

Elijah Cummings and Dominic Cummings. Not related.

What I do know is that both are symbolic of what’s wrong with the political systems they figure in.

Also last weekend, I saw a comment somewhere, think it was Twitter, that said something in the vein of:

…let’s hope the British don’t make the same mistake with Boris Johnson that the Americans made -and make- with Donald Trump, that is, labeling every single thing he does as “Bad”, because then they would lose all of their credibility, fast.

And I thought: that could have been my comment, that’s how I look upon the whole political circus too.

The entire blind demonization of Trump has only made him stronger, and the loss of credibility of the ‘accusers’ is a major factor in that. Not everything that goes wrong in America is Trump’s fault, it can’t be. But for large segments of the press, and their affiliated politicians, that has been the message for three years now.

And then you wake up one morning after -another- hearing, this time that of Robert Mueller, which you lost again, and you find that nobody believes you anymore, or cares, except for those who’d believe anything you say whatever it is anyway, and all of the time. But that also means you don’t reach anyone new, anyone not already in your echo chamber.

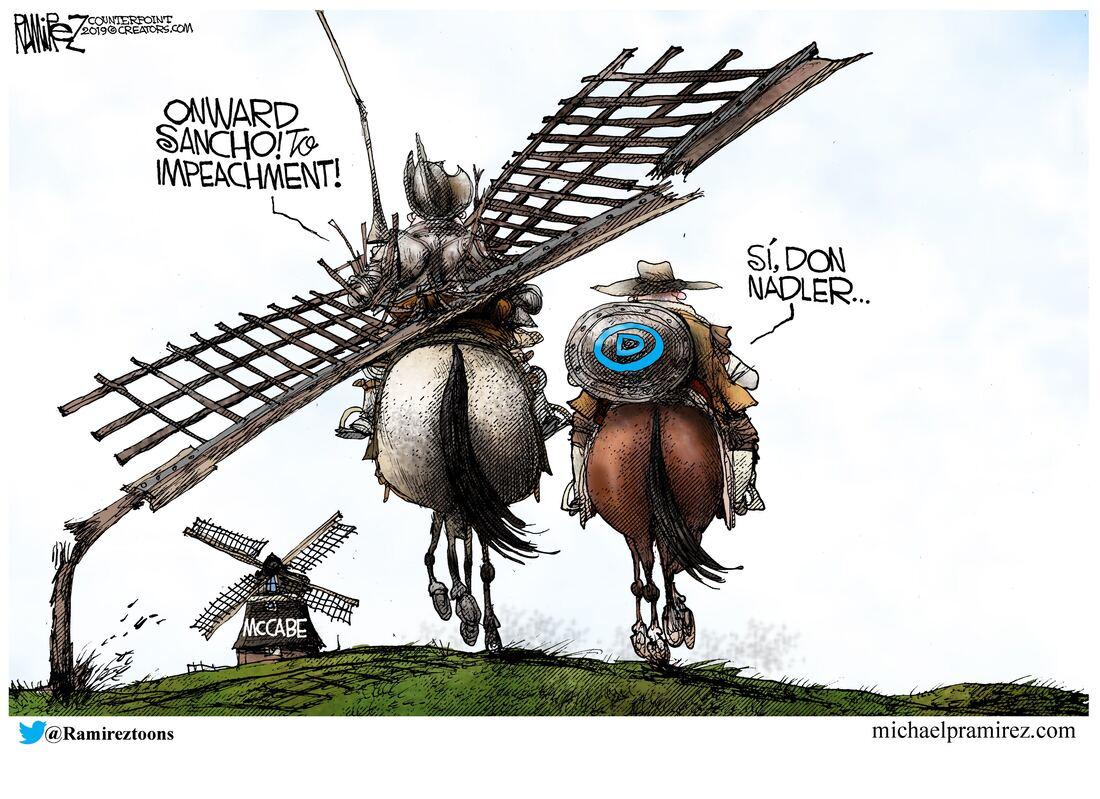

Right before the Mueller hearings, Jerry Nadler once again stated that Mueller had ‘very substantial evidence’ Trump is ‘guilty of high crimes and misdemeanors’”. But not one iota of any such ‘substantial evidence’ was addressed by Mueller in the hearings. And that hurts Nadler’s credibility to no end.

After three years, there’s no more time and space for empty allegations. Just watch Rachel Maddow’s plunging ratings. She lost some 25% of her viewers in the first half of this year. The Democrats would do well to take that into consideration before they speak out again. The latest episode a week ago started with Trump calling out Elijah Cummings (D-MD) on his comments about the border and telling him to take care of Baltimore first.

When Trump said Baltimore was rat infested, a million Democrats called him a racist for it, as in: he wasn’t talking about rats, he was really talking about black people. And subsequently we find out that Baltimore indeed has a substantial problem with rats, various other rodents, garbage, you name it. And one thinks: stop doing it, stop calling him names, stop calling every single thing he does “Bad”.

Elijah Cummings has been one of many people doing just that.

Y’all need to stop it because you’re losing. You have been losing for those entire three years. You helped Maddow and the WaPo and NY Times make a fortune with their 24/7 empty allegations, but in the process you’ve been murdering your own party. If you want to fight Trump, you’ll have to do it with facts and evidence, mere innuendo no longer works, those days are gone. You need to change strategy, urgently, you have less than a year to do so.

And talking about the MSM, you also need to stop only watching and reading those sources. Because they don’t provide a wide enough picture, they put blinders on you. It’s what’s been so profitable for them. But not for your party, though it may seem to be.

But yeah, you look at the line-up of ‘candidates’, most of whom appear completely lost in the ‘field’, and you must wonder what 2020 will bring for your party. There’s Kamala and Biden on the right, and then there’s Bernie and Warren on the left. And you just know the DNC is going to pull another Bernie 2016 move. They don’t want the left, they don’t want the Squad, and they’re conspiring against Tulsi Gabbard too. It’s not the empire that’s coming for Tulsi, it’s the DNC.

If I were you, I’d first make sure the DNC gets no say in the choice of your candidate. I’d say disband the whole thing. They are responsible to a large extent for the losing pro-Hillary tactics that have made Trump that much stronger and got him elected. They are behind the whole Russiagate disaster, and the party must urgently distance itself from that. How you can do that without major internal cleansing, I don’t see.

If I were you, I would get rid of Nadler and Adam Schiff and Cummings and a whole lot more faces. Make a fresh start. As things are, the only people who will vote for you are those who would anyway, the echo chamber inhabitants. But the Democrats need additional voters too, swing voters, the already converted are simply not enough.

I see voices promoting an everything-on-red gamble for Michelle Obama, but that reeks far too much of desperation. Then again, betting on Biden or Kamala doesn’t look to be a winner either. The best person might well be Bernie, but the party made clear in 2016 they don’t want him. Personally, I would like to see a Bernie/Warren ticket, because it would give Americans a choice between truly different ideas and options.

Then again, Bernie keeps you far too close to being the War Party with his Russia comments. Americans deserve better. Embrace Tulsi Gabbard’s voice, even if you don’t want her as your candidate. The people love her, even if the DNC does not. She can get you votes you wouldn’t otherwise get. But overall, I don’t see much hope for you next year. Unless you manage to crash the economy before Christmas. Or Easter at the latest. How about Halloween?

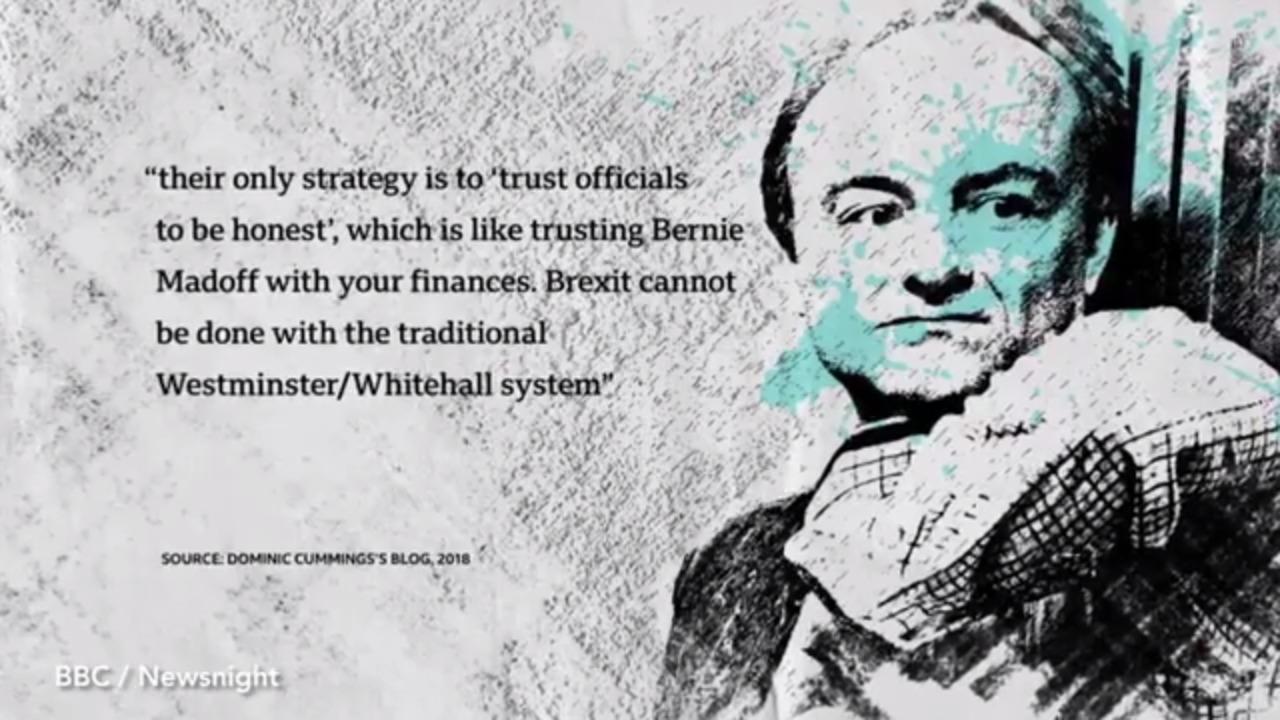

If only because then there’s the other Cummings who made the news this week, Boris Johnson’s special adviser Dominic Cummings. I referenced the movie The Uncivil War a while back, and one thing I think I learned from it is that this Mr. Cummings doesn’t play second fiddles. He only agreed to run the VoteLeave campaign that in the end won the Brexit vote when he was given free rein. I think the same thing might have happened now.

He’s agreed to run Boris Johnson’s “Brexit by Halloween” program on the condition that nobody, very much including Boris himself, gets in his way. In 2016, Cummings pushed Boris forward because his polling data told him Nigel Farage was too unpopular and would cost too many votes (yes, the same Farage who has since pretended he was the big winner). But Cummings had no high opinion of Boris either, and still doesn’t.

What that adds up to is that the real boss in no. 10 is not even the PM nobody elected, it’s a guy who got handed the power by that unelected PM in a backroom meeting. And once Dominic Cummings has delivered Brexit, he’ll vanish into the shadows again, where he feels best. Given his past criticisms of Brexit, as well as the entire political system, it could all be more about the win, the kill, then about the value of what it will achieve. He’s not a politician anyway because he’s not a puppet. Cummings is a puppeteer. Boris, well, you get the picture.

Mind you, Brexit may well be a great idea. Just not this way, certainly not this way. The EU has turned into a very questionable club, no doubt. But does anyone at all have the idea that the UK will be well-prepared when they leave that club at Halloween? The thing I find problematic is that all UK laws, regulations, treaties over the past 40 years were agreed to in team efforts with Brussels. London signed them all.

That is a lot of laws and treaties and pieces of paper. Everything modern, everything that didn’t exist 40 years ago, think communications, internet etc. etc., will be part of that. Are they going to leave but still use all those thousands of pages of legislation anyway to regulate their “new” country? I don’t know how they see that, and frankly I don’t think they know either. They seem to just have been bickering amongst themselves for 3 years, and left preparation on the backburner.

Are their businesses prepared for reams upon reams of new paperwork, digital or not? I can’t be sure, but I don’t see it. And then there’s the Irish border, and the backstop. Westminster largely acts as if that’s a minor nuisance, and Paddy will fall into line, but today it’s not just a matter of talking to Dublin, but of talking to Brussels as well.

And you can despise the EU all you want, but they have no choice but to stand with Ireland. They can’t say: let’s ditch the backstop, that is not an option, Brexit would make the Irish border the border of the EU. And if Cummings and Boris want to head for a no-deal Brexit regardless, Good Friday will be as good as dead. Does Dominic Cummings really want to be held responsible for that? Hard to believe. Boris perhaps, but Cummings?

Boris and his people insist there won’t be new border crossings, that technology can save the day, and do the work away from the border. Haven’t seen them explain it though, and certainly not in any detail. But I did see a video the other day of someone involved in the Good Friday negotiations explaining what would happen.

He said, paraphrased: “you put cameras on -or near- that border, there’ll be militants shooting them down. Then you need police to protect the cameras, and they’ll shoot at the police. So you must bring in the army to protect the police, and you’re right back to the Troubles”. The Irish border is still a highly fragile combustible situation. And if Boris insists on not having a backstop, it’s hard to see how new Troubles can be avoided. The Good Friday Agreement came into effect less than 20 years ago, in December 1999.

The dysfunctional political systems Elijah Cummings and Dominic Cummings are part of may appear to be dysfunctional for different reasons. But the role of the media in both cases is very similar.

The media wants to be -and define- the message, because that’s where the money is, and the power.

via ZeroHedge News https://ift.tt/2T7E5Ij Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}