How many times have you seen a gun control debate in which someone chimes in, “Nobody needs an AR-15. What are you going to do, hunt deer with it?” It’s been a busy year for gun control advocates, passing draconian law after draconian law.

Sometimes it’s part of a heartfelt essay, like this, which is just another essay where a man bloviates about his views on high-velocity weapons.

There is no place for high-velocity weaponry in the hands of the citizenry. No number of lengthy oratories by National Rifle Association leadership and pandering politicians will ever justify the deaths this nation has already endured. “Every Marine a Rifleman” is an adage for Marines, not for civilians. We are no longer under the oppressive rule of a foreign king, and it is folly to think that by keeping civilians from such weapons that we risk our republic. We risk nothing more than offending the bloated gun lobby in Washington. But by doing nothing, we continue to risk our children’s lives. (source)

The author of that piece feels that since a pistol isn’t a match for an AR-15, nobody but police and military should be allowed to have one.

But that’s exactly why we should be able to own guns like AR-15s.

A disabled gentleman in Summerfield, Florida demonstrated exactly why one needs an AR-15 last Wednesday when he handily dealt with four home invaders who thought he was a soft target.

Deputies got the call at 8:21 p.m. Wednesday and went to the home at 14999 SE 32nd Court Road in response to a report of shots fired.

Sgt. Micah Moore found Doyle with a gunshot wound and a shotgun next to him on the ground. Deputies entered the home and found Jackson dead on the dining room floor. Detectives said he was wearing a “Jason” mask on top of his head, gloves on both hands, jeans and a black shirt.

Near Jackson’s head was a semi-automatic pistol, detectives said.

Continuing into the home, deputies found the 61-year-old homeowner in a bedroom.

He had an AR-15 rifle on his legs and was bleeding from a gunshot wound to the stomach, according to sheriff’s officials. Doyle and the homeowner were transported to Ocala Regional Medical Center, where Doyle died.

Deputies continued to search the area.

Deputy Austin Coon and K-9 Deputy Alberto Gago, with his dog Nitro, found Rodriguez and Hamilton in the 15000 block of Southeast 36th Avenue, according to arrest reports. Rodriguez was hiding in tall grass on the side of the road.

He was wearing sweat pants and a purple shirt. Hamilton was wearing all black clothing.

I’ll bet they were sweating when they discovered how outmatched they were. Here’s what went down. Police have opted not to name the brave homeowner.

The homeowner told Detective Travis O’Cull that, about an hour before the shooting, a male who he barely remembers from a past Craigslist transaction, knocked on the front door, according to sheriff’s officials.

The homeowner said he did not open the door but saw the male peering through a back sliding-glass door. He said he asked the male what he was doing and was told he needed help with his vehicle.

The homeowner said he told the individual he was disabled and couldn’t help him. That person then left and [the] homeowner went to sleep.

The homeowner told the detective he was awakened by a loud noise and grabbed his AR-15, which was near his bed. He saw a masked person inside the home, he said, and he and the intruders exchanged gunfire. He said he shot at the man in the mask and at a second person coming toward him.

The homeowner said it was Jackson who shot him. (source)

If ever there was a case for being ready to defend one’s home, this is it.

The other two suspects were interviewed and then placed under arrest.

Two of the four of the suspects have criminal records. Local police say that the homeowner faces no charges and that he’s done nothing to prevent him from owning guns. He is in stable condition, recovering at the hospital.

Here are the mug shots of the alleged home invaders.

I’ve written before about why preppers need guns, but it’s important to note that you need guns in good times too if you intend to defend yourself. This story is a perfect example of why. There’s no ongoing disaster or SHTF event happening in Summerfield, Florida. It was just an ordinary night in July…until 4 people allegedly decided to invade an innocent man’s home.

If the homeowner had not had greater firepower, this story probably would have had a very different ending. Imagine taking on 4 armed home invaders with a Glock.

Turkish President Recep Tayyip Erdogan celebrated the delivery of the first S-400 anti-air missiles on Tuesday, even going so far as to suggest that Turkey and Russia (the system is made by Russian defense contractor Almaz-Almaty) might collaborate on building weapons. But across the Atlantic, President Trump was less than amused.

Washington has repeatedly insisted that if Turkey bought the S-400 over a steeply discounted Patriot missile system, that the US would block the sale of Lockheed Martin’s F-35 fighter jets – and unprecedented punishment for a NATO member. And as it turns out, that’s exactly what President Trump is planning to do.

During a Cabinet meeting on Tuesday, Trump said “we are now telling Turkey…we’re not going to sell you the F-35 fighter jets.”

Trump added: “It’s a very tough situation that they’re in. And it’s a very tough situation that we’ve been placed in the United States,” Trump said. “With all of that being said, we’re working through it. We’ll see what happens, but it’s not really fair.”

But Trump was mum on a more pressing issue: Whether Washington will subject Ankara to sanctions under the Countering America’s Adversaries Through Sanctions Act, or CAATSA. While Erdogan has suggested that Trump would find a way to avoid the sanctions, last year, Congress set a high bar for waiving sanctions under CAATSA.

Trump isn’t the only senior US official talking tough about the S-400. During his Senate Armed Services Committee confirmation hearing, Esper said that he has told his Turkish counterpart that “you can either have the S-400 or the F-35, you cannot have both.”

But who knows? Maybe one one-on-one phone call between Erdogan and Trump will resolve everything.

via ZeroHedge News https://ift.tt/2jSh2UU Tyler Durden

House Speaker Nancy Pelosi (D-CA) was briefly banned from speaking on the House floor on Tuesday after she made disparaging comments about President Trump’s ‘racist’ behavior, sparking chaos in the chamber.

GOP lawmakers fumed after Pelosi slammed Trump as “xenophobic” for a Sunday tweet in which he told progressive Democrats to “go back” and “fix the totally broken and crime infested places from which they came.”

“How shameful to hear him continue to defend those offensive words, words that we have all heard him repeat, not only about our members, but about countless others,” said Pelosi, adding “”There is no place anywhere for the president’s words, which are not only divisive but dangerous, and have legitimized and increased fear and hatred of new Americans and people of color.”

In response to Pelosi’s comments, Rep. Doug Collins (R-GA) claimed that her remarks violated House rules forbidding personal attacks against the president or lawmakers.

After Collins asked Pelosi if she would like to rephrase her comments, Pelosi said she had cleared them with the parliamentarian in advance.

“I would like to make a point of order that the gentlewoman’s words are unparliamentary and ask they be taken down,” Collins said.

Rep. Emmanuel Cleaver (D-Mo.), who was presiding over the floor then reminded members “to refrain from engaging in personalities toward the president.” –The Hill

House Majority Leader Steny Hoyer, a Democrat, said “The words used by the gentlewoman from California contained an accusation of racist behavior on the part of the President,” adding “The words should not be used in debate.

Hoyer’s comments technically banned Pelosi from speaking on the House floor for the rest of the day, while the debate over Pelosi’s comments caused the House to come to a standstill as lawmakers debated what to do next.

Rep. Cleaver dramatically ‘abandoned the chair’ and dropped the gavel on the dais while the situation unfolded.

Rep. Cleaver: “We don’t ever, ever want to pass up, it seems, an opportunity to escalate, and that’s what this is. I dare anybody to look at any of the footage and see if there was any unfairness. But unfairness is not enough, because we want to just fight. I abandon the chair.” pic.twitter.com/pvfJL54kw1

Ultimately, Pelosi’s comments were allowed to stand after a motion to strike her comments failed 190-232. Every Republican voted in favor of the motion.

via ZeroHedge News https://ift.tt/2lhnfde Tyler Durden

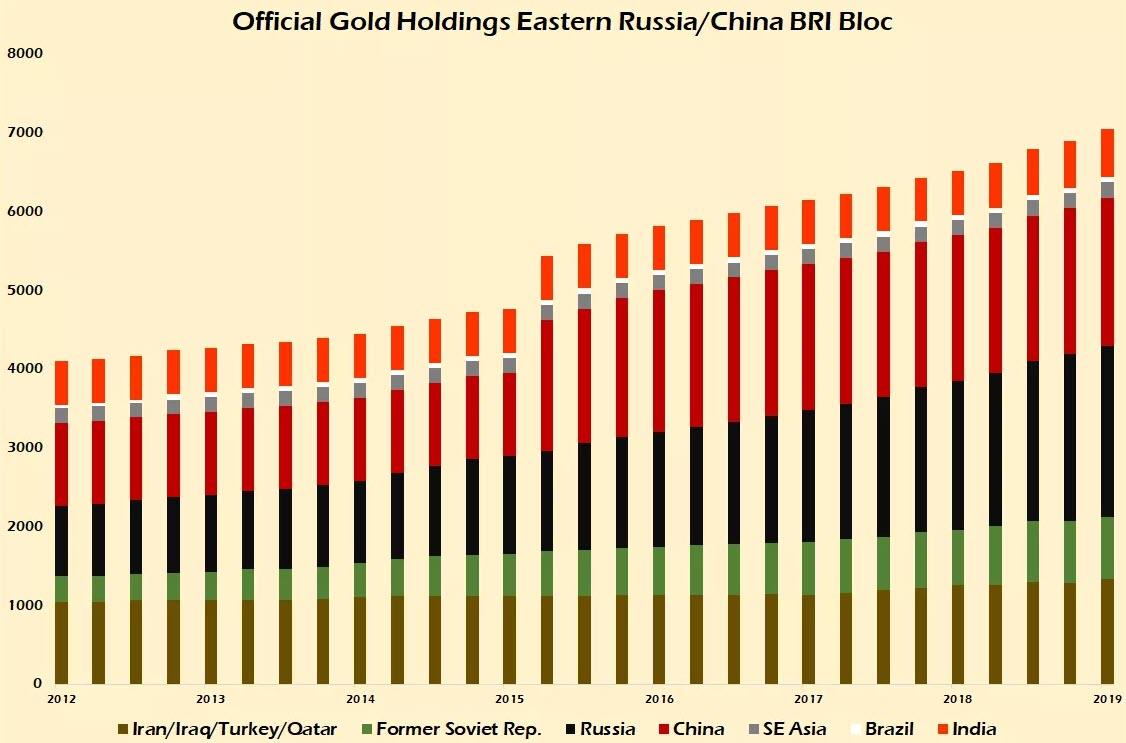

It’s not news that China and Russia have been buying gold by the hundreds of tonnes. It’s not news that Russia divested itself of most of its U.S. Treasury holdings last year in response to Donald Trump’s sanctions on Rusal, upsetting the global Aluminum market.

Russia has led the charge on central bank gold buying, having increased its official holdings from 400.3 tonnes in Q1 of 2007 to 2168.3 tonnes as of the end of Q1 2019. That’s a 442% increase in gold reserves.

China, on the other hand, has only in the past couple of years joined Russia’s party of announcing its gold buying on a monthly basis. Previously, China would simply drop a 500-600 tonne bomb on the markets and see what would shake out of it.

Now, few people who follow this stuff believe China’s government only owns 1916.3 tonnes of gold. Estimates range from 4000 to 6000 tonnes. Like Russia, very little of China’s domestic production of gold (404 tonnes in 2018) leaves China and makes its way into the global market.

It is mostly absorbed by the Chinese population via purchases off the Shanghai Gold Exchange (SGE). And the PBoC itself uses Chinese banks as proxies to buy its gold overseas from the U.K., Singapore and Switzerland.

Russia’s gold buying consumes most, and sometimes all, of Russia’s domestic production (297 tonnes in 2017). The same is true for Kazakhstan (68.4 tonnes) and a few other countries.

It’s easy when looking at these trends to see that something big may be on the horizon, that gold is on the verge of being re-monetized and a major shakeup to the world financial system is imminent.

That the multi-polar world is here. It’s not, but it’s coming.

The boys at The Duran had a fascinating (if a bit forward-looking) video recently where they discuss the situation brewing between the U.S. and China.

The basic thesis is that the U.S. and China are headed for a mostly amicable divorce of their economies, a disentangling as it were. And that that would then allow for the emergence of the so-called multi-polar world that both Russian President Vladimir Putin and Chinese Premier Xi Jinping are working towards.

On this point I don’t disagree. It’s a strong point Alex Mercouris makes here that the U.S. and China have acknowledged their growing contention in the global economy but that there is no need for a completely antagonistic relationship.

The U.S. doesn’t have to extend the unipolar moment into infinity to ‘win’ this ‘war’ with China. That is globalist thinking, maximalism to the extreme.

The U.S. and China can, strategically, disengage from each other while cultivating different paths for their futures. And this is the essence of the phrase ‘multi-polar.’ If that is Trump’s vision on this that is an improvement over the globalist Davos Crowd perspective so entrenched in Europe, which brooks no dissent from its Borg-like behavior.

It’s neither optimal nor likely but it sets a tone that will shift the future outcomes in the right direction. To do this Trump has to win re-election and be successful in confronting the Swamp via Jeffrey Epstein like I believe he’s doing.

However, and this is the bigger point coming back to gold, I do think Russia and China setting up their part of the multi-polar world based on a gold standard similar to Bretton-Woods is not workable.

There are a number of reasons for this but the main one is that Bretton-Woods never worked in the first place. The discipline of the reserve currency nation, the U.S., was never in observed. We violated the terms of the $35/ounce gold peg immediately.

First, by selling off the greatest hoard of silver ever amassed and then by simply printing the money during the Johnson and Nixon Administrations. It is insane to think that Russia and/or China will for any length of time exhibit any real fiscal discipline that would allow for a Bretton-Woods-style currency regime to work.

This is libertarian critique 101, folks. Just because the U.S. can’t keep its hand out of the cookie jar, doesn’t mean Russia post-Putin will. And the less said about the Chinese shadow banking bubble the better.

Moreover, the U.S. and the EU still have their gold reserves. Even if some or all of it has been lent out to suppress the price at times. I don’t believe that’s been the case since China opened up the Shanghai Gold Exchange and Russia began accumulating in earnest.

That would have put explosive upward pressure on the price of gold as thousands of tonnes would have had to be sourced to settle those positions. Instead, the U.S. and the EU were likely allowed to unwind any short positions over time which allowed years of annual production to flow east.

And this is the fundamental problem of a government-backed gold standard. It will not ever last. Governments create market interventions which have to be paid for via money printing or debt. And both of those things belie the discipline of the gold standard.

There is an infinite gap between the intention of China and Russia to build a multi-polar global financial system between East and West and the re-emergence of a gold-backed currency regime.

Because, for a moment, let’s get real about who owns what gold.

On the West side of the world we have the U.S., EU, BIS, the IMF and the Gulf states.

On the other side we have the central banks in the Russia/China orbit who are currently accumulating gold or are becoming independent actors on the world stage. It’s a bigger list than in the past twenty years, but that list is still small (The BRI Bloc (as defined by me herein) consists of the following countries: Russia, China, India, Iran, Iraq, Turkey, Qatar, Belarus, Uzbekistan, Tajikistan, Kyrgyzstan, Kazakhstan, Thailand, Malaysia, Serbia and Brazil).

Going through World Gold Council numbers for Q1 2019 we get the following numbers. Just over 7000 tonnes of gold for what I’m calling Eastern BRI Bloc, those countries that are both accumulating gold in their reserves and are important partners in China’s Belt and Road Initiative (BRI). It’s impressive that they have added more than 3000 tonnes over the past six-plus years.

Total Belt + Road Bloc Gold Holdings Still Dwarfed by U.S. Reserves.

However, that’s still less than the U.S.’s 8133.5 tonnes let alone the more than 10,000 tonnes that make up the reserves of the European Union countries and doesn’t include the 2814 tonnes owned by the IMF, the 504 tonnes owned by the ECB itself or the 102 tonnes owned by the Bank of International Settlements.

For any discussion of this bloc challenging the reserve status of the U.S. and European systems, There would have to be at least another 6000 tonnes available between China and Russia that are not on their official books to even being to make that argument look realistic.

Let’s use M1 money supply figures for a proxy of what gold backing would look like, just to get a lay of the land.

For all of the talk of the U.S.’s imminent bankruptcy, the gold reserves at current prices make up 9.6% of M1 at current prices ($1415/oz). China’s official gold reserves make up just 1.0% of M1. Even if you believe the upper end of China’s estimated real gold holdings it’s still only 3.3% of M1.

If you count the estimated 16,000 tonnes held privately in China and that was convertible into currency that would still only get China up to 12.2% backing of M1 with gold.

Russia is the closest there is to a gold-backed currency there is. The ruble by that metric (M1) 84.0% backed by Russia’s official gold reserves.

That is an eye-popping number and it tells you that the Russians have very prudently saved over the past fifteen years or so. They have built what we Austrian economists like to call a ‘pool of real savings’ to lever into higher order investments.

Russia is now ready to deploy a significant part of its trade surplus and even some of its pool of real savings to build new and needed infrastructure for Russia. Putin mentioned in his annual 4-hour direct line that he was ready to begin spending some of Russia’s oil revenues, drifting away from neoliberal and monetarist Alexei Kudrin and towards the nationalist/Keynesian Sergei Glazyev.

Given the state of Russia’s finances and a 10+ billion per month trade surplus, this is a no-brainer really. It’s their down-payment on the multi-polar world.

And it marks a specific shift in attitude which will assist China in building out Belt and Road but it will do nothing to allow for a return to any kind of gold standard until China gets its financial house in order.

To sum up, what killed Bretton-Woods was the same thing that killed the British pound post-WWI, a refusal to price gold accurately by the governments printing the money. Britain could have kept the gold standard and more of its empire had it re-valued the pound to reflect the money supply in 1918.

It didn’t and it destroyed the British post-war economy. The same thing is happening now. And the U.S. will either have to allow the world’s assets to plunge by 50-90% or allow the price of gold to rise to reflect the amount of money in circulation.

Given the numbers I just laid out that should give you an idea of just how much higher gold has to go to balance the books of the world. And no one in power, other than the Russians, are prepared for that kind of event.

Because until that happens there is no incentive for gold to circulate as money, or the discipline of the gold standard to be observed.

What China is doing, like Russia and the rest of the BRI Bloc, is they are building gold reserves to build the confidence of the world for the day when trust in the Western system fails. By having significant gold ‘backing’ but without convertibility those countries today adding to their rainy day funds will be the places capital will flow towards to avoid the whirlwind.

That is when the multi-polar world can be inaugurated.

When it comes to attempts to explain why the market just keeps rising, few case studies are more notable – or comical – than the in-house feud that appears to have developed between JPMorgan’s “good cop”, head quant, Marko Kolanovic, and JPMorgan’s “bad cop” flow strategist, Nikolaos Panigirzoglou.

For the latest example of how two financial professionals can reach diametrically different conclusions, look no further than the latest note published by Kolanovic on Tuesday morning, in which the JPM strategist tries to justify the levitation of the S&P above 3,000 not in the framework of overly dovish global central banks (as that would make his job redundant – after all, just buy everything when central banks are injecting liquidity, and sell when they are draining it), but in terms of investor positioning, as in not enough of it.

Specifically, in explaining which way the market will trade now that it is above 3,000 Kolanovic writes that “over the past month, equity exposure increased” following “record low positioning in equities and other risky assets” earlier in the year when Kolanovic predicted that the S&P would hit 3,000: “In particular, the equity beta of all hedge funds increased to ~60th historical percentile.” However, he notes, “equity long-short investors still have relatively low exposure, in their ~30th percentile, despite running high gross exposure.”

This is problematic because as we wrote over the weekend, just last Friday, JPMorgan’s other quant and fund flow strategist, Panigirtzoglou came to the opposite conclusion, writing that he finds “little support for the idea that there are prevalent equity underweights and “bears everywhere”. Focusing on the key equity long-short investor class, Panigirtzoglou wrote that “Long/Short hedge funds which represents the most important equity hedge fund universe produced a return of 3.2% in June according to HFR and 9.5% in H1, with the two largest L/S sub-categories fundamental growth and fundamental value returning 3.9% and 3.5% in June, respectively. This implies a beta at or higher than 0.5, which is the historical average relative to the MSCI AC World index. Equity Long/Short hedge funds would struggle to produce such returns if they were underweight equities.“

Incidentally, the above observation was in the context of Panigirtzoglou’s forecast that there is only roughly 8% of S&P upside, suggesting” limited upside for equities from here even if the 1995/1998 insurance-rate-cuts scenario plays out over the coming months” and, worse, “any equity upside would become even more limited if bond markets fail to sustain their H1 gains.”

Amusingly, just hours after Panagirtzoglou wrote down those words, JPM completely ignored its in house “bad cop” and as if to rub salt in the wounds of bears and skeptics, upgraded its 12 month price target to 3,200.

And while the recently uberbullish Kolanovic is quick to temper his optimism, noting that “given that the S&P 500 returned over 20% in 6 months, 3,200 in 12 months implies quite a bit lower rate of returns”, the quant instead brings attention to what he calls an “unprecedented divergence” between various market segments, which “offers a once in a decade opportunity to position for convergence.”

So what is this unmissable opportunity Kolanovic refes to?

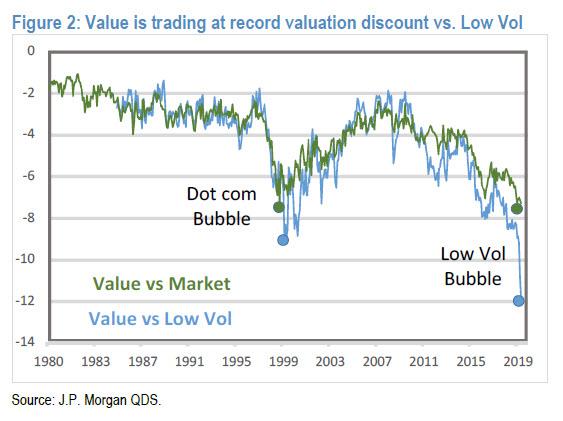

As he explains, there has emerged “a record divergence between value/cyclical stocks on one side, and low volatility/ defensive stocks on the other side” with “the level of divergence much more significant even when compared to the dot com bubble valuations of late ’90s.” The valuation difference (in forward P/E turns) between value and the broad market, as well as between value stocks and low volatility stocks, is shown below.

One can claim that this divergence is entirely the result of central banks taking over the market, injecting trillions in the global economy and stocks, thereby crushing all value propositions, while the destruction of volatility by central banks whether direct or indirect, has made low vol stocks spectacular winners.

As Kolanovic adds, while there is a secular trend of value becoming cheaper and low volatility stocks becoming more expensive due to secular decline in yields, “the nearly vertical move the last few months is not sustainable”, and “the bubble of low volatility stocks vs value stocks is now more significant than any relative valuation bubble the equity market experienced in modern history.”

So what could catalyze such a convergence of low volatility/defensives and value/cyclical stocks? According to Kolanovic, several possible triggers are:

Stabilization of economic numbers (e.g. recent US retail sales, China IP, etc.),

progress in the trade war,

the Fed cutting short term rates and related yield curve steepening would help.

That said, given the extreme divergence, the JPM quant thinks that as little as hedge funds increasing net and decreasing gross exposure during the summer rally could trigger this rotation. Hedge Funds’ net is low due to the high level of shorts, most of which come from cyclical and high volatility stocks.

This could, in turn, trigger a chain reaction of short covering, fundamental flows, and equity long-short quant rebalances in a low liquidity environment. This rotation would push significantly higher all the laggards such as small caps, oil and gas, materials, and more broadly stocks with low P/E and P/B ratios.

Whether Kolanovic is right remains to be seen – after all countless traders have bet the house on value outperforming “any minute”, only to get carted out feet first. We are, however, delighted regardless, as the “old” Kolanovic, the one who looked for – and found – unique arbitrage opportunities and dislocations in the market, appears to be making a tentative return and whose presence will be far more valuable and greatly appreciated compared to his current stock bubble-chasing ‘at all costs’ successor.

via ZeroHedge News https://ift.tt/2lP9Ycc Tyler Durden

President Donald Trump’s playground taunt Sunday that “the Squad” of four new radical liberal House Democrats, all women of color, should “go back and help fix the totally broken and crime-infested places from which they came,” dominated Monday morning’s headlines.

Yet those headlines smothered the deeper story.

The Democrats are today using language to describe their own leaders that is similar to the language of the 1960s radicals who denounced Democratic segregationist governors like Ross Barnett and George Wallace.

Consider what the four women have been saying.

Alexandria Ocasio-Cortez has accused Speaker Nancy Pelosi of attacking “newly elected women of color.” Was she calling Pelosi a “racist”?

“No!” protested AOC. But it sure sounded like it.

AOC’s chief of staff Saikat Chakrabarti attacked Native American Rep. Sharice Davids for her vote on a Pelosi-backed bill that sent $4.6 billion in aid to the border but lacked the restrictions on Trump policies progressives had demanded.

Chakrabarti described Davids’ vote as “showing her … enable a racist system,” adding that some Democrats “seem hell bent to do to black and brown people what the old Southern Democrats did in the ’40s.”

The House Democratic Caucus ripped Chakrabarti, “Who is this guy and why is he explicitly singling out a Native American woman of color?”

At a Netroots Nation conference this weekend, African American Rep. Ayanna Pressley declared: “We don’t need any more brown faces that don’t want to be a brown voice. … We don’t need any more black faces that don’t want to be a black voice.”

This comes close to calling members of the Black Caucus “Uncle Toms.”

Monday, the president doubled down, tweeting:

“We all know that AOC and this crowd are a bunch of Communists, they hate Israel, they hate our own Country, they’re calling the guards along our Border (the Border Patrol Agents) Concentration Camp Guards, they accuse people who support Israel as doing it for the Benjamin’s”

The “Benjamins” recalls the accusation of Somali-born Ilhan Omar of Minnesota that the Israel Lobby buys the votes of members of Congress.

“It’s all about the Benjamins baby.”

Rashida Tlaib of Michigan is the other congresswoman in Trump’s sights. Together, the four have achieved a prominence that almost exceeds that of Majority Leader Steny Hoyer or Majority Whip James Clyburn.

The four — AOC, Tlaib, Pressley, Omar — have no clout in the Democratic caucus. But because of the confrontations they have caused and the controversy they have created, they have a massive media following.

Paradoxically, their interests in winning cheers as the fighting arm of the Democratic Party coincide with the interests of Donald Trump. He entertains and energizes his base by answering in kind their attacks on him and by adopting incendiary rhetoric of his own. He is now assuming the old “America! Love it or Leave it!” stance in going after the four women as anti-American ingrates.

They, by calling Trump a criminal, racist and fascist for whom impeachment proceedings should have begun months ago, elate and energize the outraged left of their party.

Among the presidential candidates, some have begun to side with the four, with Bernie Sanders saying Pelosi has been “a little” too tough on them.

On “Meet the Press,” Bernie added: “You cannot ignore the young people of this country who are passionate about economic and racial and social and environmental justice. You’ve got to bring them in, not alienate them.”

Trump’s Sunday attack forced Pelosi to stand with her severest critics, and she re-elevated the race issue with this tweet: “When Trump tells four American Congresswomen to go back to their countries, he reaffirms his plan to ‘Make America Great Again’ has always been about making America white again.”

Do Democrats believe that refighting the racial battles of the 1960s that were thought to have been resolved is a winning hand in 2020?

Does Pelosi think that demeaning white America is going to rally white or minority Americans to Democratic banners?

The race issue had already arisen in the first debate when Sen. Kamala Harris called out front-runner Joe Biden for befriending segregationist Senate colleagues in the ’70s and ’80s, and for colluding with them to block court-ordered busing to achieve racial balance in the public schools.

Observing the clash between Trump and these women, the rank and file of the Democratic Party are being forced to take sides. Many will inevitably side with the fighters, as Democratic moderates appear timid and tepid.

Trump is driving a wedge right through the Democratic Party, between its moderate and militant wings. With his attacks over the last 48 hours, Trump has signaled whom he prefers as his opponent in 2020. It is not Biden; it is “the Squad.”

Sunday, Pelosi recited again her mantra, “Diversity is our strength; unity is our power.” It sounded less like a proclamation than a plea.

We see the diversity. Where is the unity?

via ZeroHedge News https://ift.tt/2k86pxq Tyler Durden

A NATO-affiliated body accidentally published a document which revealed the locations of US nuclear weapons throughout Europe, according to the Washington Post. The document was subsequently deleted and replaced with a final version of the report which omits where US bombs are stored.

A version of the document, titled “A new era for nuclear deterrence? Modernisation, arms control and allied nuclear forces,” was published in April. Written by a Canadian senator for the Defense and Security Committee of the NATO Parliamentary Assembly, the report assessed the future of the organization’s nuclear deterrence policy.

But what would make news months later is a passing reference that appeared to reveal the location of roughly 150 U.S. nuclear weapons being stored in Europe. –Washington Post

A copy of the document was published Tuesday by Belgian newspaper De Morgen, which reads “These bombs are stored at six US and European bases — Kleine Brogel in Belgium, Büchel in Germany, Aviano and Ghedi-Torre in Italy, Volkel in The Netherlands, and Incirlik in Turkey.”

As a matter of practice, neither the US nor its European partners disucss the location of America’s nuclear weapons on the continent.

“We do not comment on the details of NATO’s nuclear posture,” said a NATO official cited by the Post, who added “This is not an official NATO document.”

A number of European outlets, however, viewed the report as confirmation of an open secret. “Finally in black and white: There are American nuclear weapons in Belgium,” ran the report in De Morgen. “NATO reveals the Netherlands’s worst-kept secret,” said Dutch broadcaster RTL News.

The presence of U.S. nuclear weapons in Europe was indeed “no surprise,” Kingston Reif, director for disarmament and threat-reduction policy at the Arms Control Association, said in an email. “This has long been fairly open knowledge.” –Washington Post

And while there has never been an official disclosure of this nature regarding the US stockpiles, a diplomatic cable from a US ambassador to Germany revealed concerns over how long the weapons would be stored.

“A withdrawal of nuclear weapons from Germany and perhaps from Belgium and the Netherlands could make it very difficult politically for Turkey to maintain its own stockpile,” reads the November 2009 memo written by then-US Ambassador Philip Murphy.

As the Post notes, the placement of US weapons around Europe stems from an agreement reached during the 1960s, designed as both a Cold War deterrent to the Soviet Union, as well as to convince European nations that they don’t need to develop their own nuclear weapons programs.

But times have changed. In 2016, after a coup attempt and the rapid spread of the Islamic State extremist group next door, analysts openly wondered whether Turkey was really such a great place to store nuclear weapons.

“The military mission for which these weapons were originally intended — stopping a Soviet invasion of Western Europe because of inferior U.S. and NATO conventional forces — no longer exists,” according to Reif.

via ZeroHedge News https://ift.tt/2k7TMT2 Tyler Durden

Submitted by Eric Peters, CIO of One River Asset Management

“Imagine Congress appropriates $1BN to refurbish Air Force One,” said Warren Mosler, pioneer of Modern Monetary Theory.

We were discussing the financial architecture that allows the Fed to create money. “The Department of Defense hires General Dynamics to upgrade the airplane. The US Treasury instructs the Fed to credit General Dynamic’s account at JP Morgan with +$1bln.

The Fed simultaneously debits the US Treasury account with -$1bln and the books are balanced.” Notice, the government did not need to collect taxes or issue bonds.

“The US Treasury basically now has a -$1bln overdraft at the Fed. There’s no practical limit to how high the US Treasury overdraft at the Fed could become, but politicians don’t want the Treasury balance to be negative, so the Treasury issues $1bln in bonds, and deposits those proceeds at the Fed to eliminate its -$1bln overdraft.”

The $1bln the Fed created is trapped in the banking system and finds its way to purchase the $1bln in bonds the Treasury issued to balance its Fed account.

“Even if General Dynamics chooses to move the $1bln into Euros, it will do so by instructing JP Morgan to buy Euros from Deutsche Bank, which also has a Fed account. The Fed will debit JP Morgan’s account by -$1bln and credit Deutsche Bank’s account by +$1bln. The ECB will debit Deutsche Bank’s Euro account by -$1bln and credit JP Morgan’s.”

The dollar’s exchange rate may fall, but that’s what Washington wants.

“People misunderstand debt and money. Government debt is simply money the government has spent that hasn’t yet been used to pay taxes. Holders of that debt prefer saving over consuming or they wouldn’t own bonds. At some point, these people may choose to spend more than they save, and if that sparks excess demand and inflation (in Warren’s experience, large inflations are caused by other factors), then that’s easily dealt with. The government simply raises taxes or cuts spending.”

Easy eh?

via ZeroHedge News https://ift.tt/2lElnve Tyler Durden

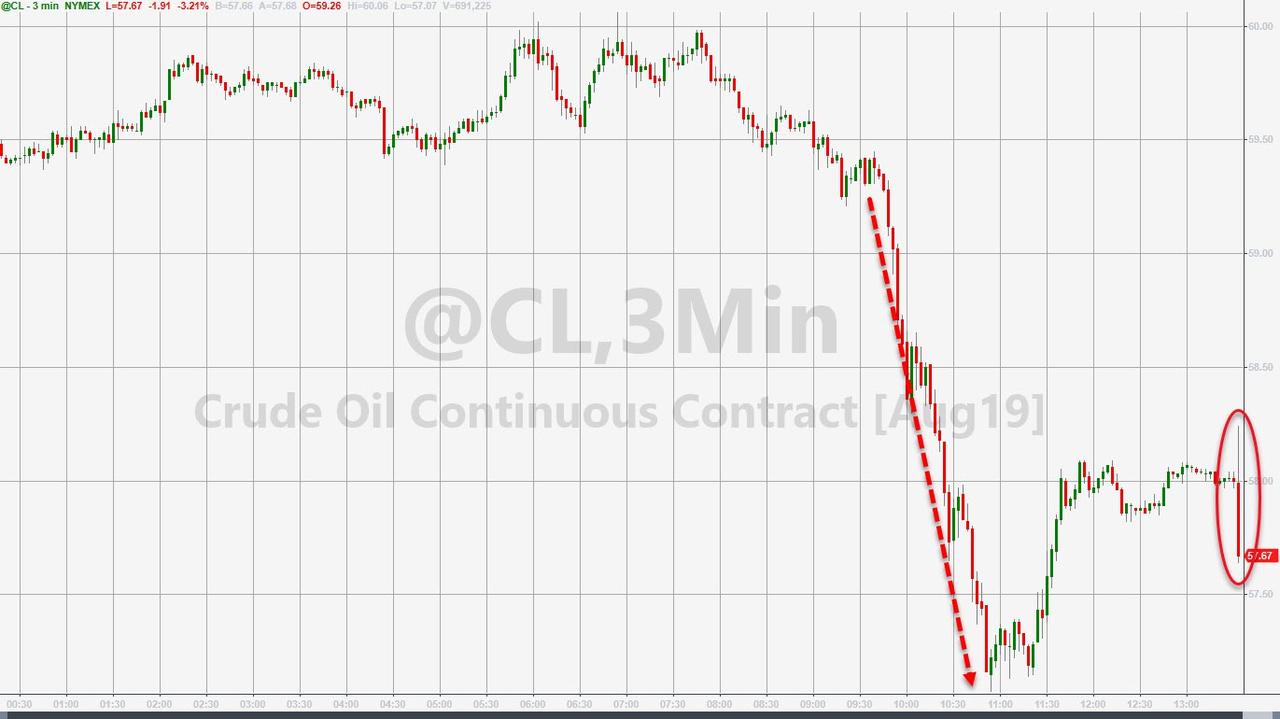

Oil prices plunged today as Trump and Pompeo defused some tensions with Iran and geopolitical risk premiums were squeezed out suddenly.

“Bullish catalysts are in short supply,” analysts at London-based broker PVM Oil Associates Ltd. said in a note to clients.

“The Gulf Coast of Mexico hurricane premium is fading as offshore operations in the region resume. At the same time, the U.S. shale engine continues to give oil bulls a sleepless night.”

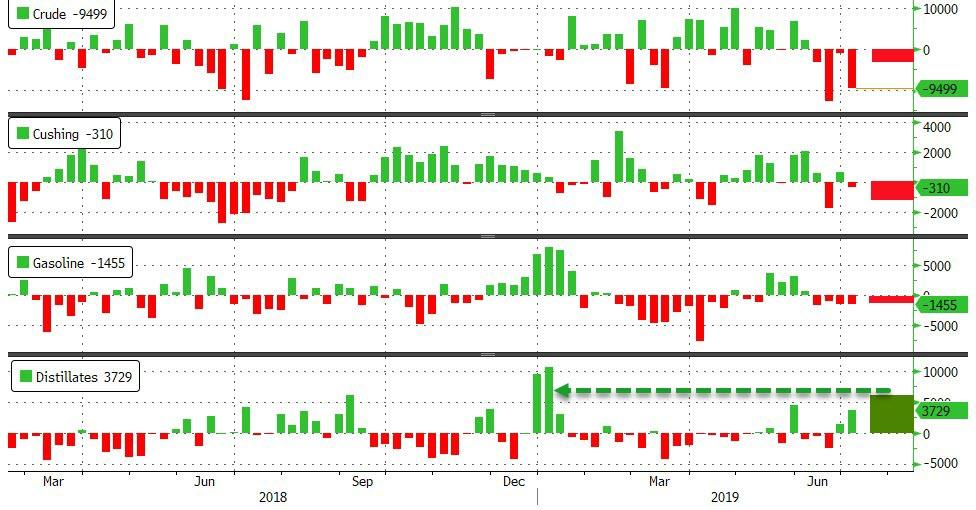

API

Crude -1.401mm (-3mm exp)

Cushing -1.115mm

Gasoline -476k

Distillates +6.226mm – biggest build since Jan 2019

After last week’s big crude draw (the 4th week in a row), expectations were for another sizable draw but API reported a smaller than expected 1.4mm draw. Also a major distillates build weighed on sentiment.

WTI bounced back up to around $58 ahead of the API print but slipped lower after the smaller than expected draw…

via ZeroHedge News https://ift.tt/2lBGCOf Tyler Durden

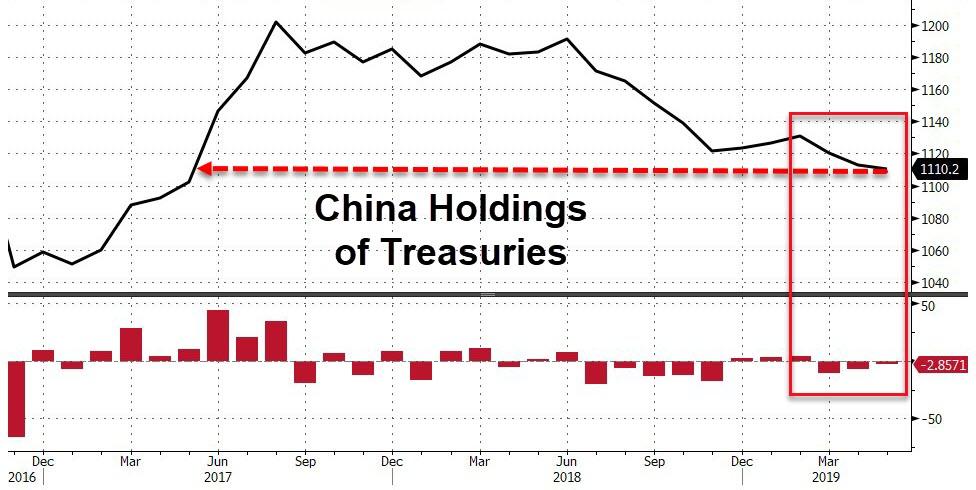

The latest TIC data for the month of May, released just after the close, showed that China continued to sell US Treasurys for the third straight month, bringing its total to just $1.11 trillion, down another $3 billion, and the lowest since May 2017…

… Even as Japan bought a whopping $37 billion in US paper in May, its largest monthly purchase since August 2013, and bringing its total to $1.101 trillion, just $9BN shy of China’s $1.110 trillion.

Meanwhile, in a surprising development, the UK – which has been aggressively buying US paper either for itself, or in proxy for other purchasers – saw its holdings jump once again, rising to $323.1 billion, an increase of $22.3 billion in the month.

Similar to Belgium and Euroclear, it is far more likely that this surge is simply the result of some offshore fund serving a sovereign, but based in the UK, is doing the buying. Whether it’s China or someone else, will be revealed in due course.

Yet despite the occasional purchaser, foreign official institutions (central banks, reserve managers, sov wealth funds) have seen their holdings of US TSYs slide by another $22 billion, the 9th consecutive drop in the holdings of foreign official institutions, and yet because the decline this May was smaller than the drop in May of 2018, the LTM net sales posted a modest drop.

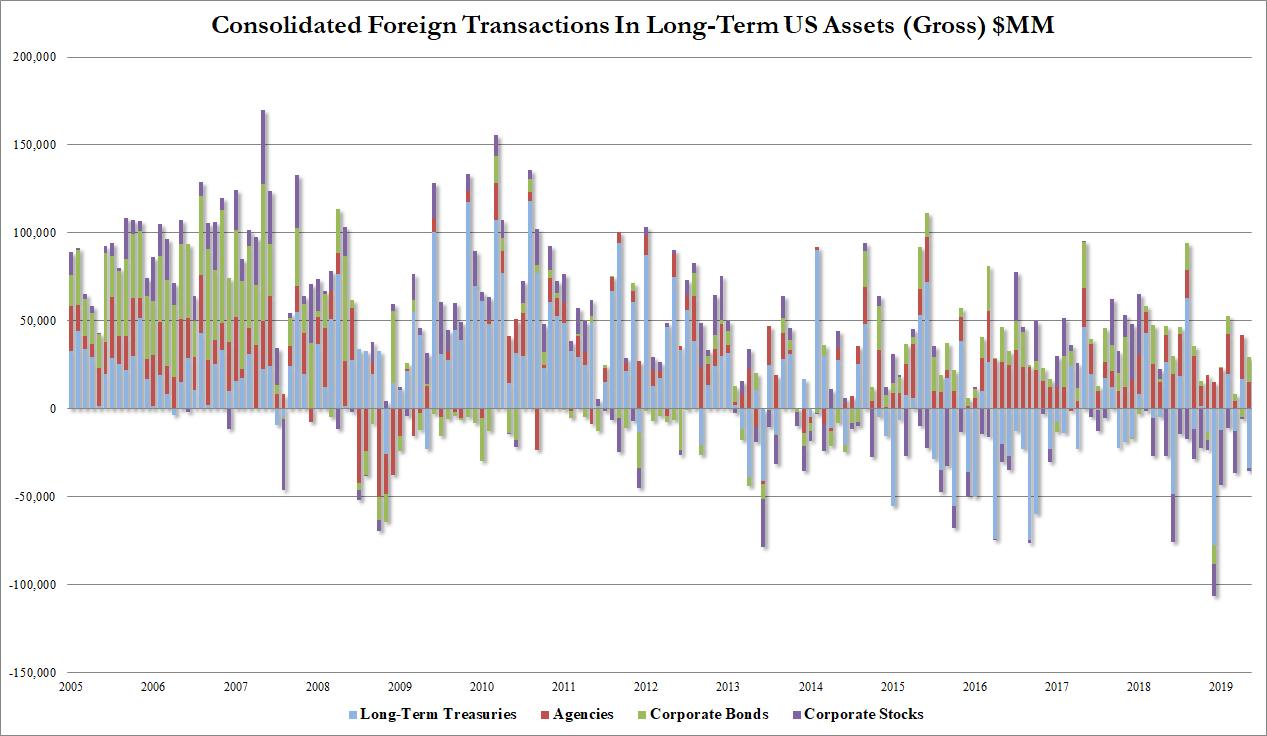

Overall, May – and the past 12 months in general – were not good for US Treasurys, as foreigners, both public and private sold a total of $33.8 billion in US Treasurys and $1.4 billion in corporate stocks, offset by purchases of $15.1 billion in Agencies and $14.9 billion in Corporate bonds.

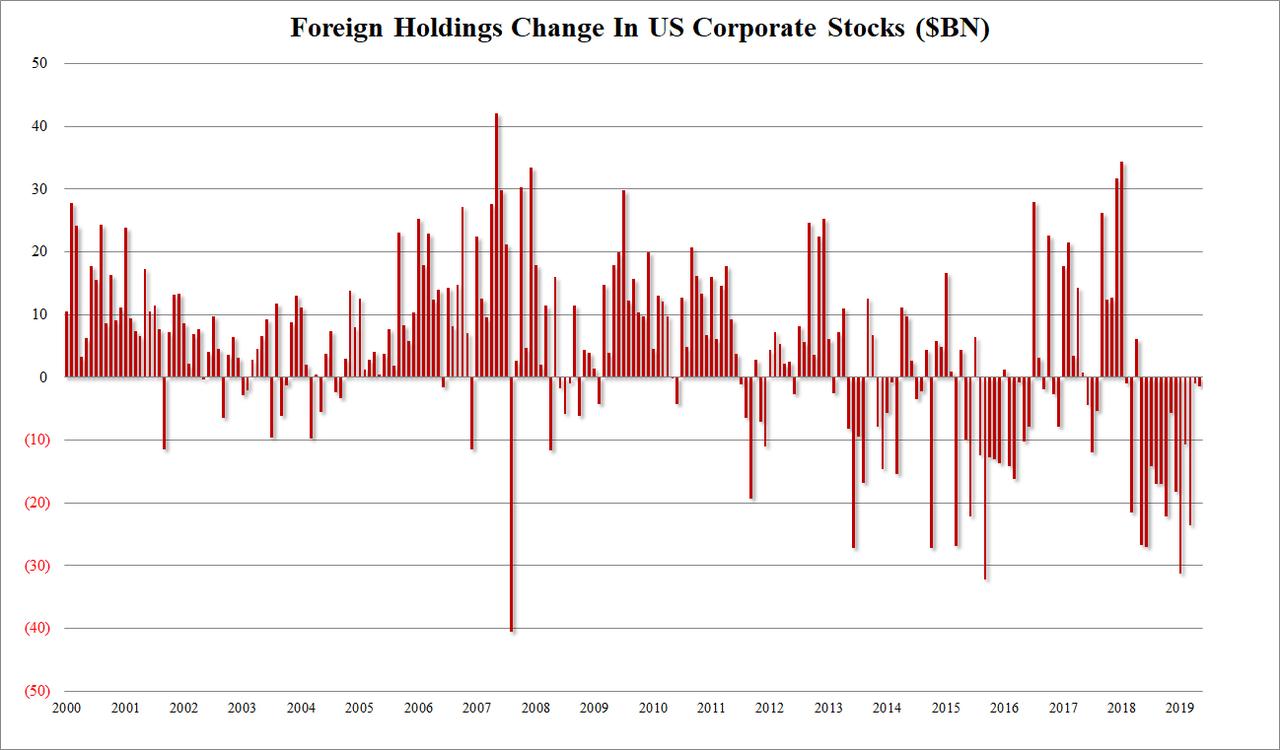

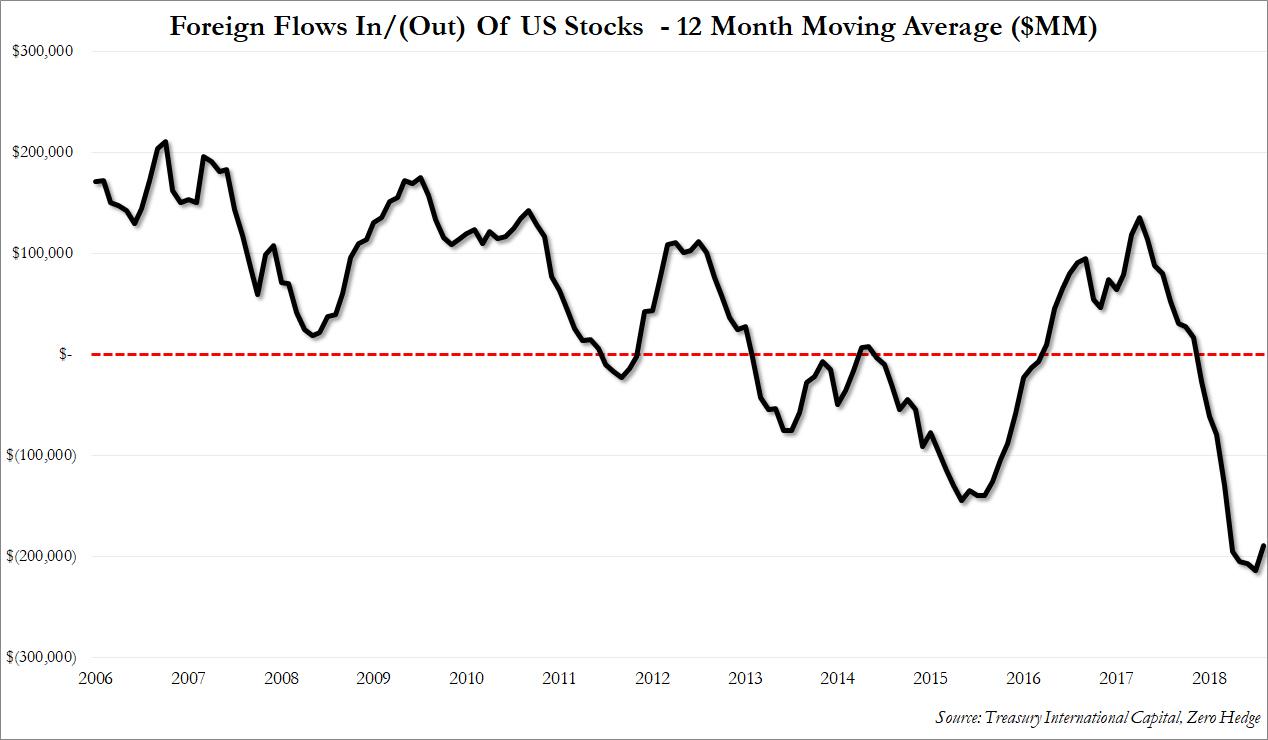

However, for yet another month, the real action was away from the bond market, and in US stocks, where TIC data showed that foreigners sold US stocks for a record 13th consecutive month and 153 of the past 16:

The aggregate $215 billion in sales in the past 13 months, is the largest liquidation of US equities by foreigners on record.

And while it is perhaps not surprising that in May foreigners dumped US stocks – after all it was the worst month for the S&P in 2019 – what is odd, is that in June and July, US stocks barely noticed the ongoing liquidation, and after several attempts at taking out 3,000 in the S&P, finally pushed right through in July, despite what we showed just this weekend continues to be relentless selling by both individual and institutional investors, and – now – also by foreigners.

So with the S&P at all time highs, are we going to find out in two months that foreigners continued to dump anything that wasn’t nailed down?

Which again begs the question, just how powerful are stock buybacks – which were the only official buyers of stocks in the past few months – to not only offset selling by virtually everyone else, but also push the market to new highs?

via ZeroHedge News https://ift.tt/2khfuUy Tyler Durden