WaPo Columnist Shreds NBC For Spouting CCP Propaganda On Wuhan Lab Tyler Durden

Tue, 08/11/2020 – 11:50

On Monday, NBC News published a puff-piece for the Wuhan Institute of Virology – giving controversial lab which ‘could pass for a college campus’ a glowing review after a five-hour visit and interviews with several employees.

The report slams the Trump administration for showing “no credible proof to back up claims that the coronavirus was either manufactured at or accidentally leaked from the lab,” while helping the CCP dispute an April Washington Post report over US Embassy cables warning of safety issues at the facility.

The author of that WaPo piece, Josh Rogin, has just shredded NBC News over their report – which he says contains ‘several errors.’

The NBC story says that U.S. officials “said they observed” serious safety issues at the lab. That’s just wrong. The officials reported the Wuhan Institute of Virology scientists TOLD THEM about the safety issues. https://t.co/kgwc21YwBP There’s more…

Rogin continues (condensed thread via Twitter, emphasis ours):

Wang Yanyi, director of the WIV, told NBC reporters the U.S. officials visited in March 2018, two months after the first cable was written. The truth is they visited three times, both before and after the Jan. 2018 cable. Did U.S. officials make an entire visit? Not likely..

That calls into question Wang’s credibility. She also says biosafety was not discussed. Again, calling several U.S. diplomats fabricators? NBC reports that without any pushback. But there’s more…

The NBC reporters toured the lab, as if that would tell them anything. What did they expect to find, a piece of paper they forgot to throw out that says “Coronavirus Origin Evidence”? It’s absurd to think that has any probative value. But there’s more…

The NBC piece also launders more warped logic by Peter Daszak, who has a direct conflict of interest. “The fact that they published the sequence so quickly suggests to me that they weren’t trying to cover up anything.” Or, maybe they were so quick because they recognized it.

This, from Yuan, the Wuhan institute’s vice director is interesting and true: “So far, there is no evidence to show that the novel coronavirus jumped from animals to people in Huanan Seafood Market in Wuhan.” No evidence.

Overall, the Chinese scientists can’t be blamed for toeing the Party line. They deviate from that under penalty of death. But U.S. news organizations must do better than presenting a walk around a lab and an interview with falsehoods in it as telling us anything about the virus.

Rogin then explains why the truth matters:

The actual origin story is critically important scientifically to understanding how the outbreak started and therefore how to fight it and how to prevent the next one. Should we spend our time shutting down wet markets or stopping risky bat research? Get it?

Trump Destroys Abusive Democrats In Stimulus Showdown

President Trump won re-election this weekend with his four executive orders.

We haven’t even reached the DNC convention in Milwaukee and it looks to me like this election season is over.

I know the polls keep trying to convince me that Joe Biden, most likely suffering from dementia, is leading President Trump but I just don’t buy it.

And neither do the Democrats.

Because if they did they wouldn’t be so desperate to push through unlimited mail-in voting as their political hill to die on.

And die on it they have.

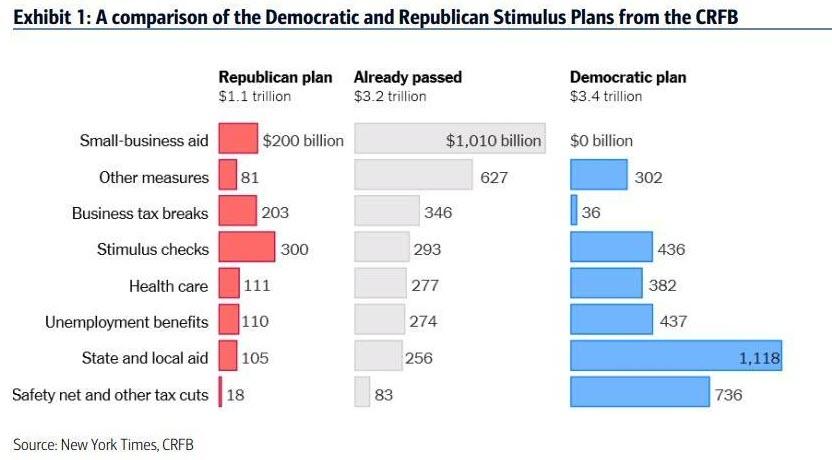

Speaker Nancy Pelosi held up a new round of stimulus legislation over this issue. The massive gap between the GOP and DNC proposals highlight only part of the political divide between the two sides (see graphic, H/T Zerohedge).

The real divide was in enshrining in law the kind of mail-in voting which would ensure near unlimited cheating and ballot harvesting which would give the Democrats their best chance at “winning the election.”

But all he had to do was make payroll tax irrelevant for a majority of taxpayers in this country.

Go over those Executive Orders he signed. And each one attacks a core position the Democrats carve out for themselves in the public discourse.

Defer Payroll Tax Collection — Here Trump is doing at least two things. First, he’s a Republican lowering taxes on the poor and middle class. Second, he lowers the cost of U.S. labor, cuts away red tape and makes it easier for businesses in a cash flow crunch to stay open not having to worry about paying monthly/quarterly tax payments. This attacks a core Democrat talking point, “Republicans don’t care about the little guy, we do!”

Extend Student Loan deferments – This is one step closer to debt jubilee on debt that, again, freezes people in place, dealing with debt servicing rather than creating demand in the real economy for goods and services. This also attacks the banks who made these predatory loans, which most student loan debt is, which undermines the “Occupy Wall. St.” talking point that all the money goes to the banks.

Extend Renter and Mortgage Eviction Moratorium – Again Trump hits the banks where they live by stopping the eviction of people whose income the Federal and State governments destroyed with their COVID-19 lockdown orders. This is a direct attack on the DNC’s plan to see the banks throwing millions of people out of their homes during the height of the election campaign. Restates the argument that the GOP is only for the rich vulture capitalists.

Lower and extend Unemployment Assistance — Trump’s no dummy. At this point the budget deficit is ludicrous. Lowering the assistance through the election season, again, says he’s helping and they are obstructing. It’s not perfect, but it extends the fiscal cliff people are facing until after the election allowing him to make more sweeping changes to the tax code while keeping people in their homes, fed and capable of maintaining some semblance of normality. Trump claims the ‘I care about you’ moral high ground.

The only thing the Democrats could do in response was fulminate about funding Social Security. But that’s an irrelevant argument to anyone other than Boomers who aren’t paying into the system anyway.

Their checks are coming and will continue to come.

High unemployment only makes Social Security’s future less secure. The people out of work aren’t contributing to Social Security now anyway. If you want to get the economy back on its feet you have to let the money circulate.

Removing the deduction from people’s paychecks highlights for the poorest working people in this country just how much of a burden that 15% actually is on their ability to build wealth or even maintain a home.

I never thought I’d see the day where an American President called the social engineers’ bluff about enforced retirement savings. Social Security is a pay-as-you-go death tax for so many people and a blatant wealth transfer system from younger generations to older ones.

This depression will kill off a lot of people, including those Social Security recipients Andrew Cuomo effectively murdered in New York, before they collect on it.

When coupled with inflationary fiat funny money it is an egregiously (and ingeniously) abusive system which ensures the lower and middle classes never get off the hamster wheel no less get out of the cage it’s in.

And it needs to end, at least in its current form.

Between social security and abortion they’ve been the two biggest shibboleths in American politics for the past fifty years. Only one of them is relevant this time around because Trump just made it one.

Trump threatened during the press conference to make the payroll tax exemption permanent if re-elected as well as revamp the capital gains tax. He understands, better than anyone, how difficult it is to build wealth while paying off debt.

Social Security, in its purest form, is a 12.4% interest payment on your labor before you even begin working. It’s a bureaucratic nightmare and robs people of the choice as to how to deploy their capital at the earliest stages of their careers.

Enforced savings for the future for people without a present is not just moronic, it’s counter-productive.

It’s not disciplined, it’s truly abusive.

And once people see how much easier their lives are without carrying that burden before they make their first dollar, the more they will reject all of this social engineering on which the Democrats have based their entire political persona.

This is the first step towards sunsetting the biggest unfunded liability in the U.S. today.

End the fiction that people like me will ever collect Social Security. Begin the hard political fight to face the reality of its insolvency and use the manufactured COVID-19 crisis to get that done.

Local governments are out there today telling you to live in fear of a virus and that they can’t protect your home from rioters and looters.

The cops are overwhelmed and, worse, should be disbanded.

And these are the same people who are also telling you that if you give them power over the Federal Government they will take away all those guns you just bought to protect yourself.

They are also the ones saying they can best safeguard your retirement by extracting one-eighth of your earnings before you ever show up to work for the first time.

Morover, next week they’ll tell you something different because Trump took away another one of their talking points.

With these executive orders, regardless of their legality at this point, Trump is single-handedly changing the entire narrative on which the federal government is premised.

Between now and the election the next narrative to fall will be the idea DNC is running a campaign for any other reason than for its leadership to stay out of jail for treason.

But that narrative only sticks after Trump has made sure things don’t get worse for those already abused by them.

Why Morgan Stanley Expects 10Y Yields To Be “Much Higher” Over The Next 3-6 Months Tyler Durden

Tue, 08/11/2020 – 11:14

Over the weekend, Morgan Stanley’s global macro strategist Andrew Sheets published his latest market outlook, which as we noted, boiled down to one thing: investor duration exposure is at all time highs, and it won’t take much of a reflationary trigger to spark a liquidation puke in fixed income securities which would send yields higher and trigger a risk asset selloff even if ultimately the reflationary signal will push beaten up value stocks higher.

As Sheets noted, “this is one reason why my US colleagues have downgraded software from overweight – a sector with very high valuations and interest rate sensitivity. With duration exposure surfacing across portfolios, we like owning interest rate volatility (while we prefer to sell equity volatility). And for central banks, this dynamic should highlight the dangers of overcooking markets that are already doing quite well.”

Looking ahead, the MS strategist was cautious, warning that “the rise in duration across asset classes, at its most expensive levels on record, suggests that the transition won’t be smooth.”

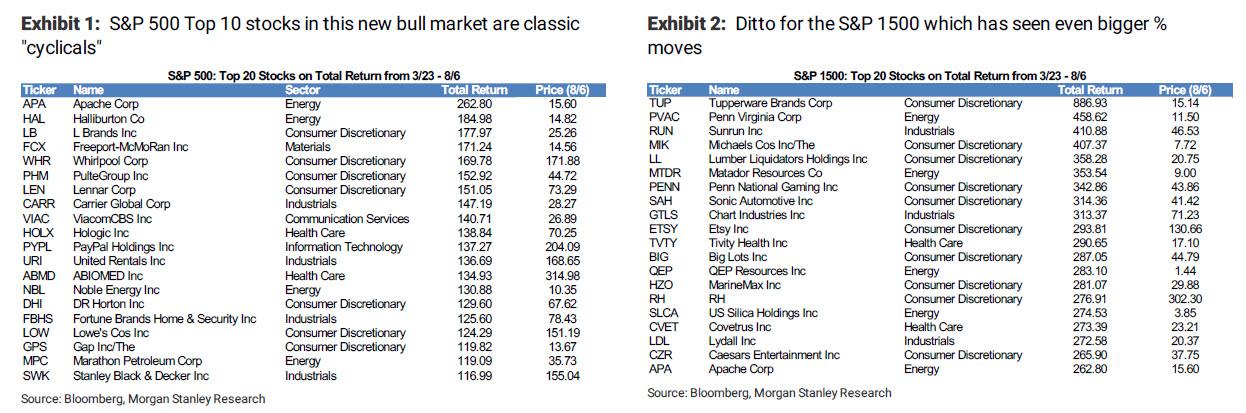

Picking up on this warning, Morgan Stanley’s chief equity strategist Michael Wilson echoes Sheets’ caution, but not before taking a victory lap first, saying that “we have been bullish since late March on the view that a new bull market began with the beginning of the worst recession in modern history. Since then, the bull market has followed the typical script with some of the most cyclical and levered companies showing the best performance. Note the top ten performers in the S&P 500 and S&P 1500…”

“… from the beginning of this new bull market are classic “cyclicals” just as our recession playbook suggested. Furthermore, despite all of the hoopla over the S&P 500, the Russell 2000 has been the better performer.”

In short, as Wilson concludes “it’s paid to move down the quality and cap curve assuming you did it early on.”

Wilson also notes that much of the relative performance in the classic cyclicals and small caps since the March lows occurred in the first 10 weeks of the recovery:

As we’ve been noting, most stocks have been in a correction/consolidation since June 8th when the equal weighted S&P 500 made its recovery highs (that have yet to be taken out). Many of the weakest stocks since then were some of the biggest winners during the initial rally of this new bull market–i.e. the reopening/recovery winners.

So fast forward to today, when the Morgan Stanley strategist sees a “trio of reasons to worry has the market questioning the recovery” which are behind the post-June 8 “correction” to wit:

The New COVID case spike,

Concerns about a potential Blue Sweep in this year’s US election, and

The looming fiscal cliff.

It is these concerns that Wilson believes “convinced some investors to pare back on these classic cyclicals and migrate back to the pandemic beneficiaries”, however as Sheets wrote over the weekend, the bank disagrees with that strategy and thinks portfolios need to have a balance of COVID beneficiaries and recovery/reopening winners.

After the recent run of the former, we believe the better relative opportunity at this point is with the latter–i.e. cyclical stocks most levered to the recovery over the next 12 months.

Ultimately, Wilson’s optimistic view is based on 4 key points which are as follows:

We have not lost faith in the recovery despite these very real concerns. Instead we view all three as simply bumps along the road of what should ultimately be a very sharp and persistent — i.e. V-shaped — recovery.

Our thesis that earnings will likely far surpass investor forecasts over the next year due to sharply increasing operating leverage is starting to play out (see our analysis below). We think economically sensitive companies that have slashed expectations and operating costs in this pandemic will experience the greatest operating leverage over the next year.

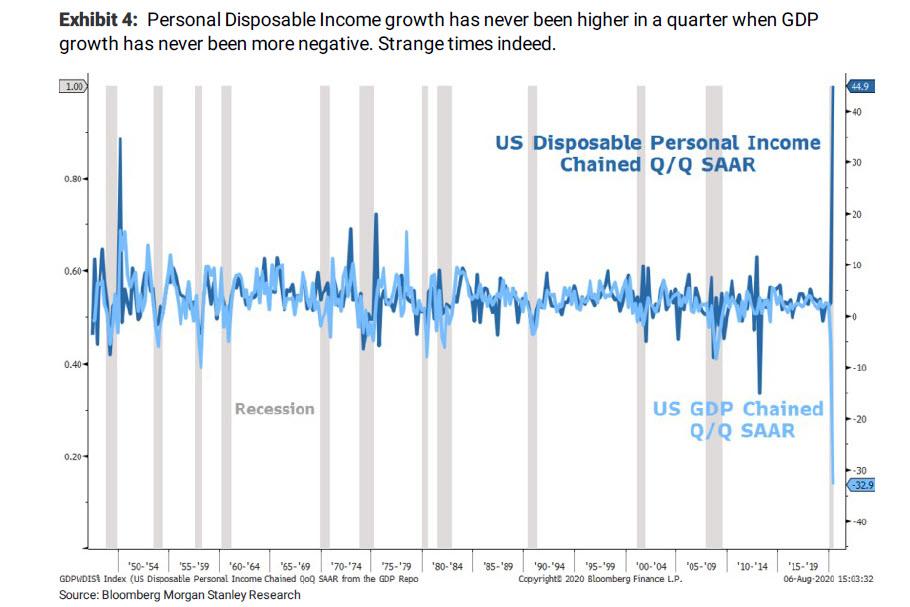

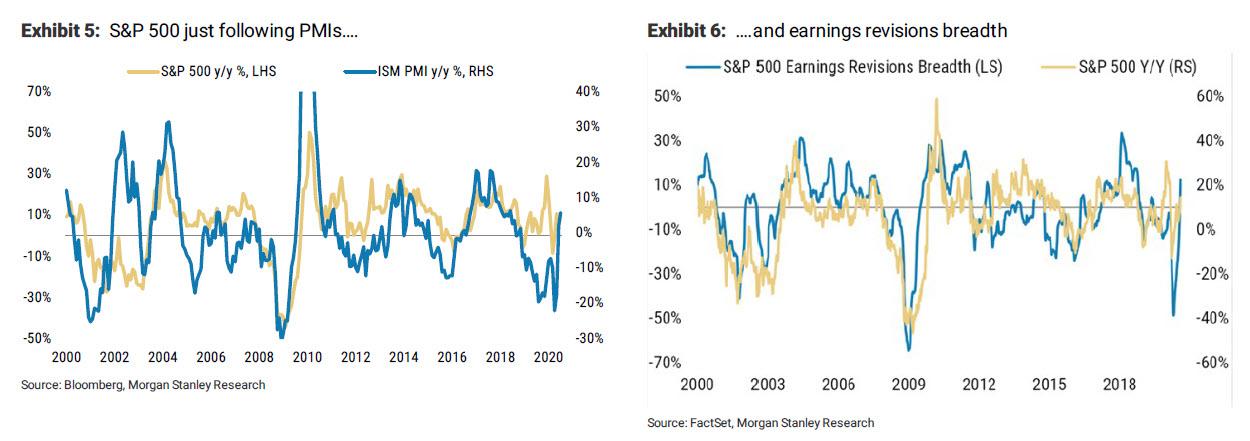

While the economic recession in which we find ourselves is unprecedented in terms of its depth, personal disposable income growth in 2Q has never been higher. Not only is such a divergence unusual, but the magnitude is remarkable (Exhibit 4). This is the direct result of the massive fiscal stimulus being provided to offset the effects of the lock down on employment. Based on Exhibit 4, the programs appear to be accomplishing their goal more effectively than expected

As for the impact on rates, Wilson writes that “given the points above we have high conviction that 10 year Treasury yields are like a coiled spring and are likely to be much higher over the next 3-6 months.“

Wilson also goes back to a point he made a month ago, discussing how the dramatic improvements in corporate operating leverage (read mass layoffs with government stimulus programs picking up the welfare slack), will lead to a surge in corporate profits:

What this really means is that our thesis for a sharp increase in operating leverage is more likely to play out. To recall, at the market trough in March we suggested the government was essentially underwriting this unemployment cycle with its massive Paycheck Protection Program, $1200/$2400 stimulus checks, and supplemental unemployment benefits (Bear Markets End with the Cycle, Time to Employ a Recession Playbook). As with all recessions, companies cut costs aggressively and that includes labor. Usually, cutting employment can have a negative effect on revenues, but this time that may not be the case. Instead, revenues may hold up better than expected as the government subsidizes the unemployed at an even greater level than normal. The impact to the bottom line will be dramatic for those companies that cut costs the most. We think this is already starting to play out. Indeed, the S&P 500 is simply following the impressive rebound in both PMIs (Exhibit 5) and Earnings Revision Breadth (Exhibit 6) as we expected back in April.

Looking ahead, Wilson’s conclusion is that “hile earnings will likely surprise on the upside next year for the S&P 500, “the surprise will be greatest from the parts of the market that are most levered to the economic recovery. While we think the market has it right directionally, the best opportunities from here are likely to be in those stocks that have higher operational gearing to economic activity and low expectations.“

This may well explain the last two days’ surge in beaten down value stocks at the expense of bond-like tech/growth stocks.

Finally, will Wilson be right and are yields indeed about to soar? We’ll know in “3 to 6 months”, but his track record has so far been impressive: just after the March crash, Wilson raised his 12 month S&P base case target for the S&P to 3,350… and we just took it out about 9 months early.

via ZeroHedge News https://ift.tt/2DHlf7F Tyler Durden

General Motors’ CFO Resigns After Just Two Years To Work At Stripe Tyler Durden

Tue, 08/11/2020 – 11:00

Mired in recession and dealing with the toughest environment for auto sales over the last several decades, the U.S. auto industry has seen another top executive depart. Just days after we reported turnover at the CEO role at Ford, General Motors is following with a C-suite shakeup of its own, as its CFO leaves after just two years to work at a fintech startup.

The company announced today that John Stapleton, GM North America chief financial officer, has been named its acting global chief financial officer, effective Aug. 15, after the resignation of the company’s current CFO, Dhivya Suryadevara.

Suryadevara is leaving the company on short notice, similar to the departure of Ford’s CEO, Jim Hackett, who quit last week. According to Bloomberg, Suryadevara will join PayPal competitor Stripe, as its CFO, the San Francisco-based company said.

GM CEO Mary Barra said that “Dhivya has been a transformational leader in her tenure as CFO. She has helped the company strengthen our balance sheet, improve our cost structure, focus on cash generation and drive the right investments for our future. We wish her every success.”

Suryadevara said: “I am grateful for the opportunities I have been given at GM. While I look forward to a new opportunity that will allow me to apply my skills in a new sector, I have great confidence in GM’s trajectory and future.” Stapleton, who is temporarily taking over duties, has been with General Motors since 1990 and has served in several different finance roles with the company.

GM shares were up as much as 3.5% to 28.96 shortly after the open of regular trading Tuesday.

via ZeroHedge News https://ift.tt/2DAUfqy Tyler Durden

Dangerous Chemical Containers Still Leaking At Destroyed Beirut Port; Initial Cause Of Fire Revealed Tyler Durden

Tue, 08/11/2020 – 10:45

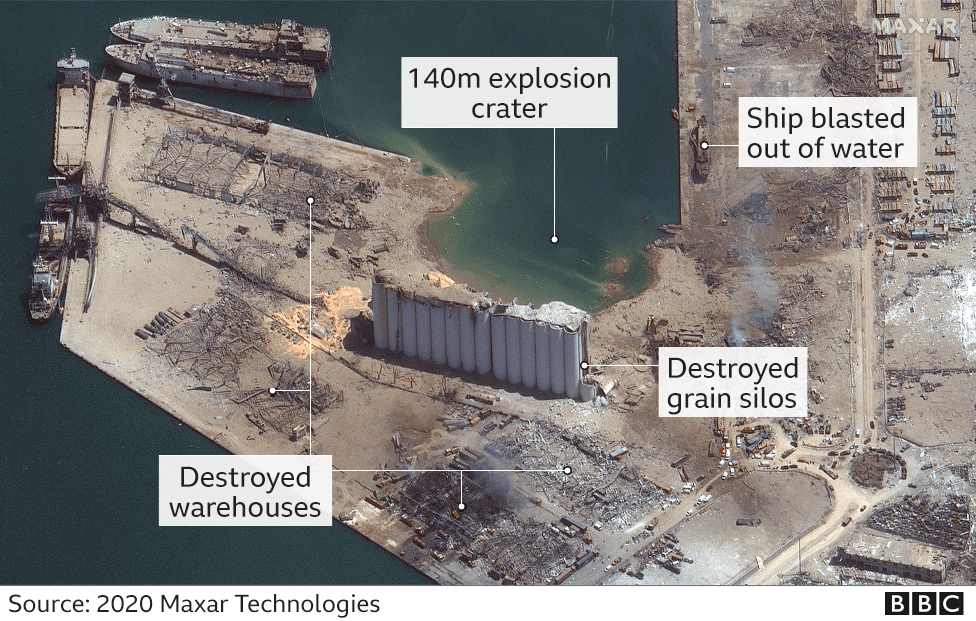

In a continuing clean-up effort amid a dangerous and potentially toxic environment, leaking chemical containers are posing a challenge to crews working to inspect and secure the Beirut port section which was site of what’s being deemed the largest non-military munitions explosion in history on August 4.

“Chemical experts and firefighters are working to secure at least 20 potentially dangerous chemical containers at the explosion-shattered port of Beirut, after finding one that was leaking, according to a member of a French cleanup team,” the AP reports.

An international team, including French experts, is working to assess hazardous materials possibly leaking at the destroyed port, via AP.

Chemical containers were in many cases found punctured following the detonation of over 2,500 tons of ammonium nitrate.

“French and Italian chemical experts working amid the remains of the port have so far identified more than 20 containers carrying dangerous chemicals,” AP continues.

“We noted the presence of containers with the chemical danger symbol. And then noted that one of the containers was leaking,” one French chemical expert working at the site said. “There are also other flammable liquids in other containers, there are also batteries, or other kind of products which could increase the risk of potential explosion,” he added.

An international response team working with the Lebanese government is attempting to identify and contain any leaked chemicals at ground zero for the blast — which was feared to have emitted dangerous gases into the air over the city in the wake of last Tuesday’s deadly accident. The death toll has risen to over 200, including more than 6,000 injured, many of them severely.

More has been learned and confirmed about what precisely started the deadly fire which detonated the highly explosive and volatile ammonium nitrate, commonly used in fertilizer and professional explosives.

Lebanese media as well as Reuters has widely reported the fire started after welding work was done in the very warehouse containing the volatile chemical compound.

It appears the welding crew had no idea that both ammonium nitrate and (astoundingly) a cache of fireworks were being stored on site.

ROCKED: Eyewitness video shot from a boat off Beirut shows a dramatic new angle of the explosion that killed at least 160 people and injured thousands, with the Lebanese government resigning on Monday amid anger and unrest in the wake of the blast. https://t.co/6tgFYYPUPApic.twitter.com/vjlwKm4brS

It was reportedly maintenance work on the door of Warehouse 12 – now location of a huge crater which has forever altered the port and coastline.

Port officials reportedly tried to warn top government officials and the Lebanese judiciary for years that the ammonium nitrate, stored there since 2013 in unsafe conditions, was a ticking time bomb in their midst.

via ZeroHedge News https://ift.tt/31Gwx3V Tyler Durden

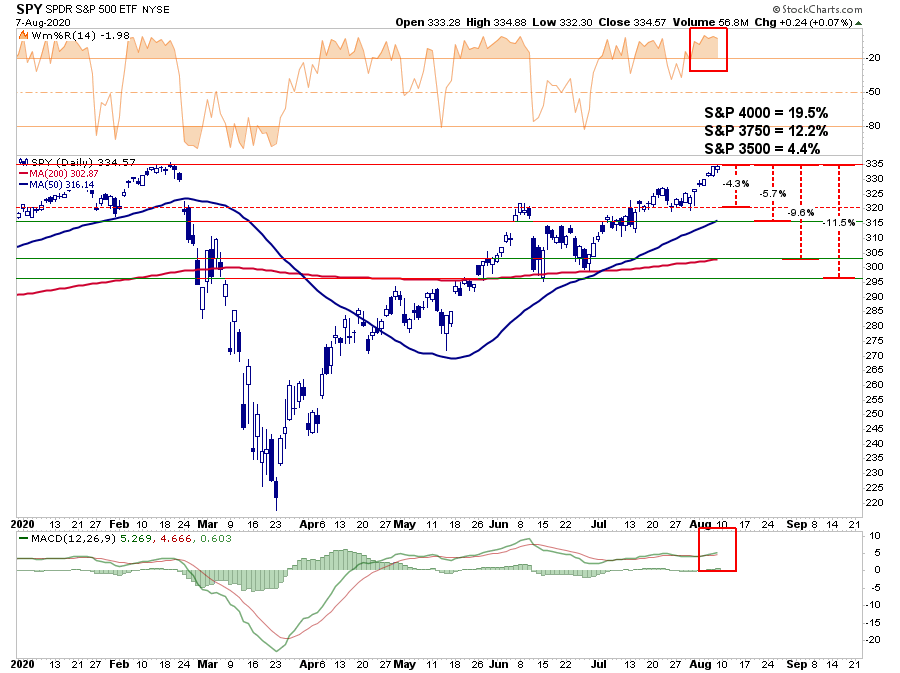

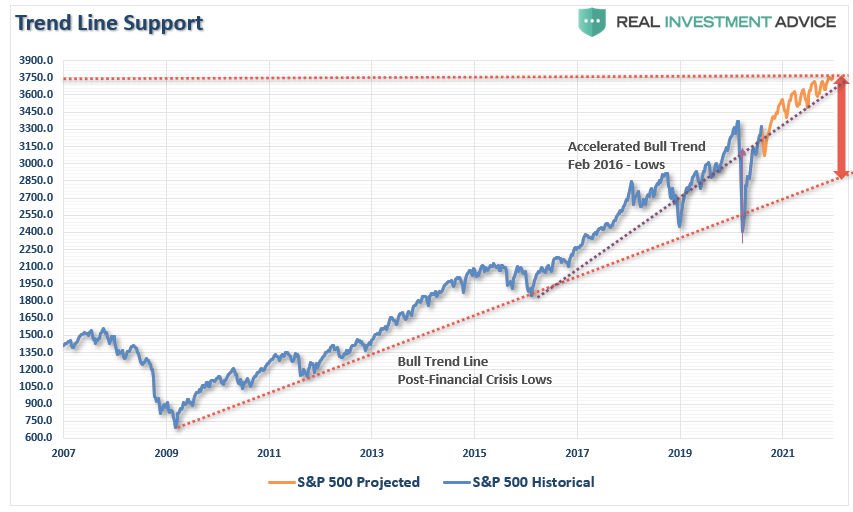

Mentally, it has been a challenge to marry a market challenging all-time highs against a backdrop of weaker earnings, falling profits, surging unemployment, and a recessionary economy. Yet, here we are. While the bulls have set S&P targets to 3750 over the next 12-months while bearish signals persist. For investors it will be the difference in determining the “light” from the “train.”

“A breakout of the consolidation range, which was capped by the June highs, would put all-time highs into focus.”

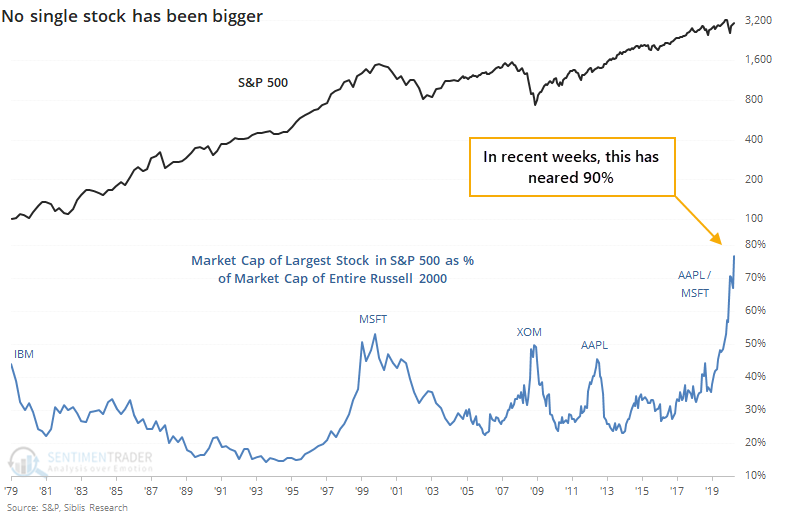

Of course, we also discussed the importance of the issue of the “capitalization effect” on the market’s advance, mainly since Apple and Microsoft make up such a significant weight. As noted by Sentiment Trader last week:

“The most significant stock in the U.S. and nearly the world, Apple, keeps powering higher. At the end of June, the value of Apple alone was almost 80% of the Russell 2000 index’s market capitalization. As of today, it’s nearly 90%. Such is astounding – in the past 40 years, no single stock has come close to dwarfing the value of so many other companies. “

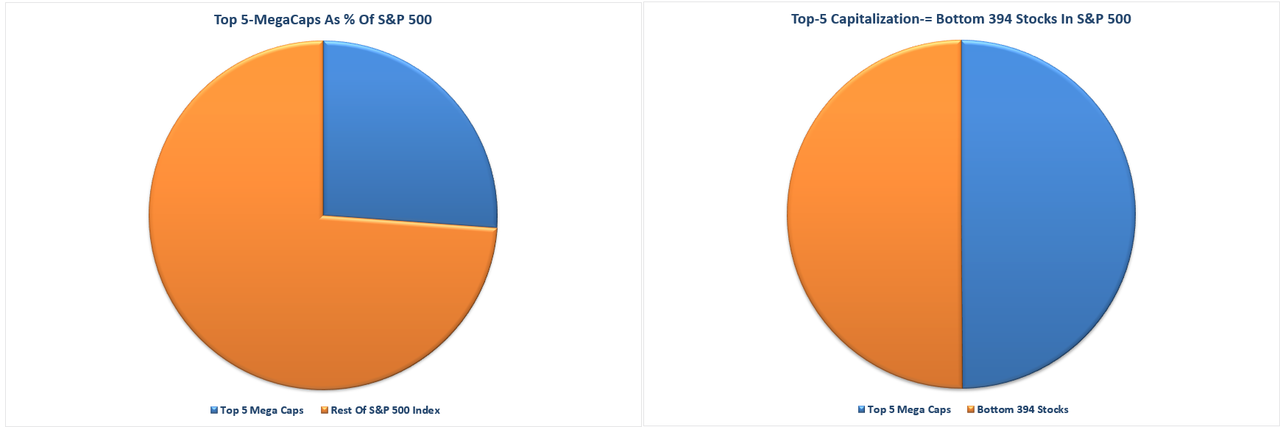

Recapping The Math

“Currently, the top-5 S&P stocks by market capitalization (AAPL, AMZN, GOOG, FB, and MSFT) make up the same amount of the S&P 500 as the bottom 394 stocks. Those same five also comprise 26% of the index alone. “

“What investors are missing is that the top-5 stocks are distorting the movements in the overall index.

Putting $1 into each of the top-5 stocks has the same impact as putting $1 into each of the bottom 394 stocks. Such is not a true representation of either the market or the economy.

As we have noted recently, if you own anything OTHER than those top-5 stocks, your portfolio is likely underperforming the market this year.”

The distortion in the markets caused by the flows into the Mega cap stocks will most certainly be a problem. While investors have chased markets higher, these Megacaps will eventually also lead the markets lower.

The question, as always, is the timing and catalyst, which eventually reverses the money flows.

In the meantime, the question is, what is the most logical next target for the S&P 500 if bulls can achieve new “all-time” highs?

Bulls Target 3750

Technical analysis works well when there are defined “knowns” such as a previous top (resistance) or bottom (support) from which to build analysis. However, when markets break out to new highs, it is becomes much more of a “wild @$$ guess” or “WAG.”

Lately, the bulls are running amok trying to predict how much higher the bull market can go. As noted on CNBC:

“We may stall here for a while into the fall, … but I think you’re going to get a rocket ship coming in the fall. I think the S&P is going to trade out above 4,000.” – Jeffrey Saut

When discussing the current “risk/reward ranges,” , 4000 was one of the targets discussed. To wit:

“With the markets closing just at all-time highs, we can only guess where the next market peak will be. Therefore, to gauge risk and reward ranges, we have set targets at 3500, 3750, and 4000 or 4.4%, 12.2%, and 19.5%, respectively.”

“Given there is no good measure to justify upside potential from a breakout to new highs, you can personally go through a lot of mental exercises. While there is certainly a potential the market could rally 19.9% to 4000, it is also just as reasonable the market could decline 22.2% test the March closing lows.

Just in case you think that can’t happen, just remember no one was expecting a 35% decline in March, either.”

No Real Basis For 4000

The problem with calls for “S&P 4000” is there is no technical or fundamental basis for the assumption.

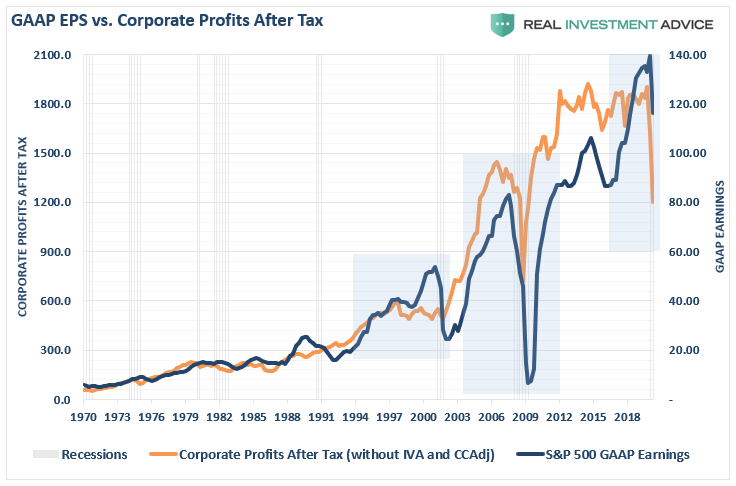

From a fundamental perspective, if we assume current 2021 estimates are correct, the market will be trading at 26x forward reported earnings. However, given estimates are regularly 30% too high, forward reported earnings will be closer to $130/share leaving valuations at 30x.

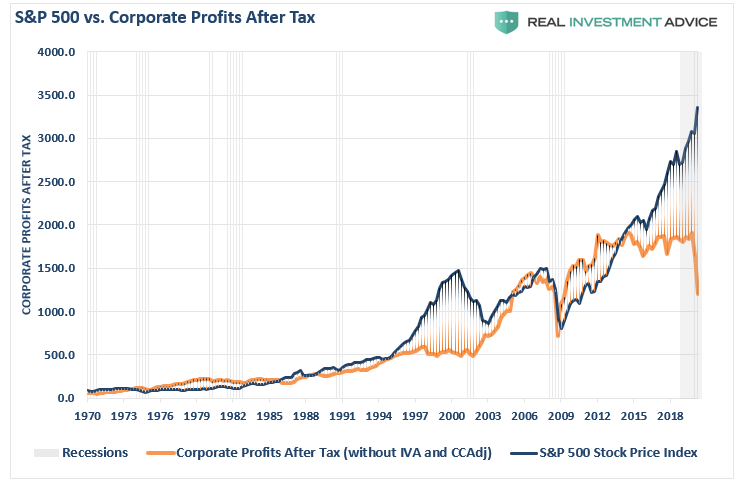

Valuations may not seem to matter currently. However, if the economy continues to lag, and employment and wages weaken, they will. Corporate earnings and profits are going to become more critical. Already, the deviation between the market and corporate profits is at extremes. As with all extremes, an eventual reversion completes the cycle.

Furthermore, given the depth of the profits decline, it is improbable that earnings will remain at these levels and not worsen.

Importantly, while “valuations” may not seem to matter at the moment, they always, without exception, eventually do.

Technical Deviations

Secondly, the technical trends don’t support S&P 4000 either.

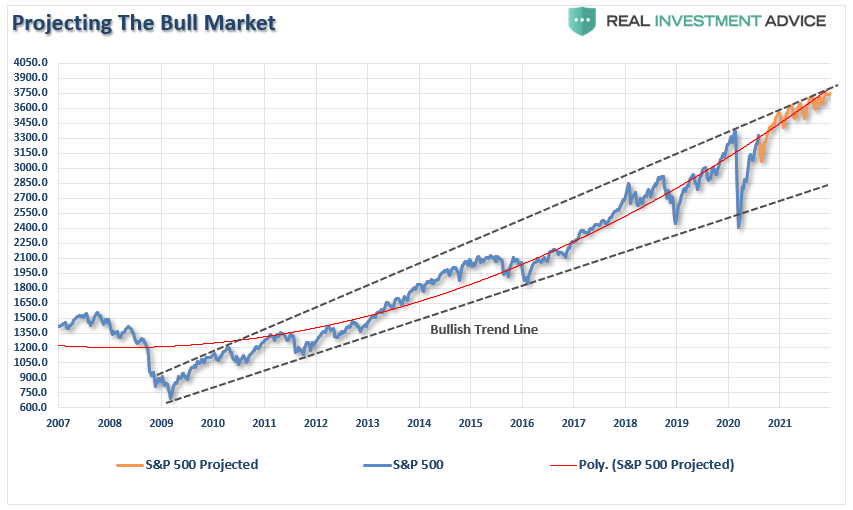

From the 2009 lows, the S&P has traded withing a fairly defined trend channel, as shown below. The upper bullish trend line, which coincides with the February 2020 market peak and the polynomial trend line, suggests 3750 as the next target.

As noted above, such would suggest a 12.2% advance from Friday’s close. While Saut’s 4000 number sounds excellent, such would violate trends that have existed for 11-years.

Furthermore, 3750, much less 4000, is going to stretch the deviation from the long-term bullish trendline (lower line) to more extreme levels. The last time the market reached this extreme was in February of this year. It is also notable that 3750 also intersects with the accelerated trendline from the 2016 lows.

As noted previously, trend lines and moving averages tend to act as “gravity.” The further away from the trendline, the market becomes, the greater the pull becomes.

Warning Signs

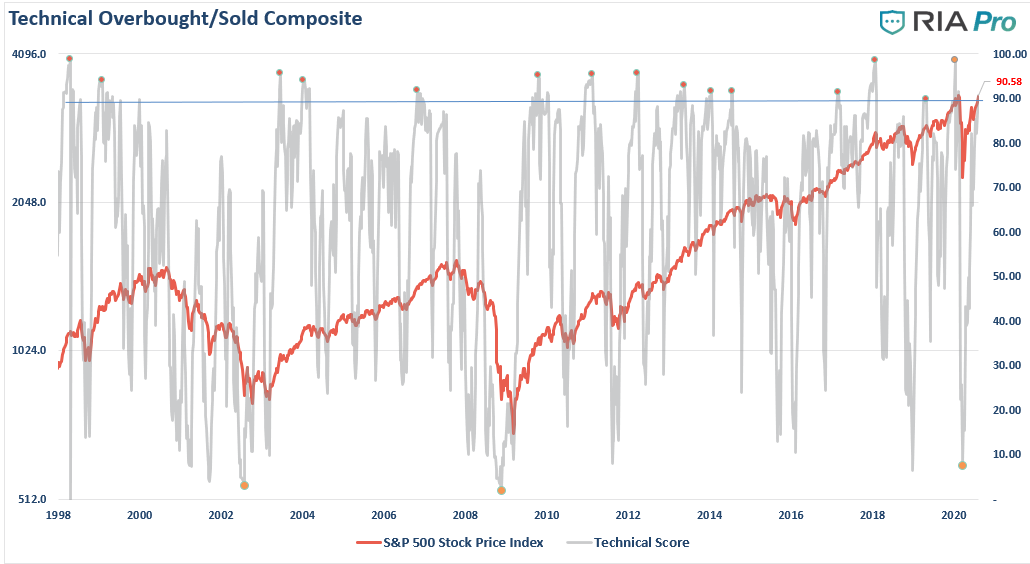

It the short-term, the market seems to be headed higher. However, it is worth remembering that every previous peak of the market since 2016 has been from “all-time” highs.

With the market at all-time highs, there are numerous warning signs of excess built up, which could trigger a reversion.

Low participation

An extremely low put/call ratio (speculative excess)

Markets trading 2- and 3- standard deviations above their means.

Currently, the evidence is mounting that markets are reaching the limits of the current move. By itself, these signs reflect the prevailing extremely bullish attitude of market participants. However, much like an explosive, at some point, an unexpected, exogenous event occurs. That event is the catalyst which ignites the chain reaction. The ensuing “reversion” to the trend catches overly confident “bulls” off guard.

Light At The End Of The Tunnel

The problem for investors currently is there is precious little that hasn’t already been fully priced into the market.

A full economic recovery

A return to full unemployment

More stimulus

Low bond yields

No recession

A return to pre-pandemic earnings levels

The problem comes when one, or more, of those things, fails to occur. Paul Singer of Elliot Management had a significant point in this regard:

“We cannot think of another time when the basic terms and conditions of making – and more to the point keeping – money were more challenged. The planet’s central bankers seem desperate to hold up all stock markets and keep them from tumbling to the floor. They think that’s the way to run monetary policy and, actually, fiscal policy as well. The fact that public policy is on a slippery slope to monetary ruin – and the slide is steepening – escapes their limited reasoning capability.

They appear to think that so long as there is a model or theory to support their policies and no immediate catastrophe, they can keep doing it. The political winds are hot and fierce, blowing in the face of economic freedom and profits. There has never been a time when it was more important to protect the downside, so that at least nominal capital values are preserved.

However, the reason capital doesn’t just build and build (given all the geniuses in the investment world) is simple: With normal approaches to money management, the march up in compounded value gets interrupted by big losses or wipeouts at infrequent, unpredictable intervals. Sometimes one can “see the train a’comin’”

However, most of the time, investors don’t see the “train,” but mistakenly believe it’s the “light at the end of the tunnel.”

Conclusion

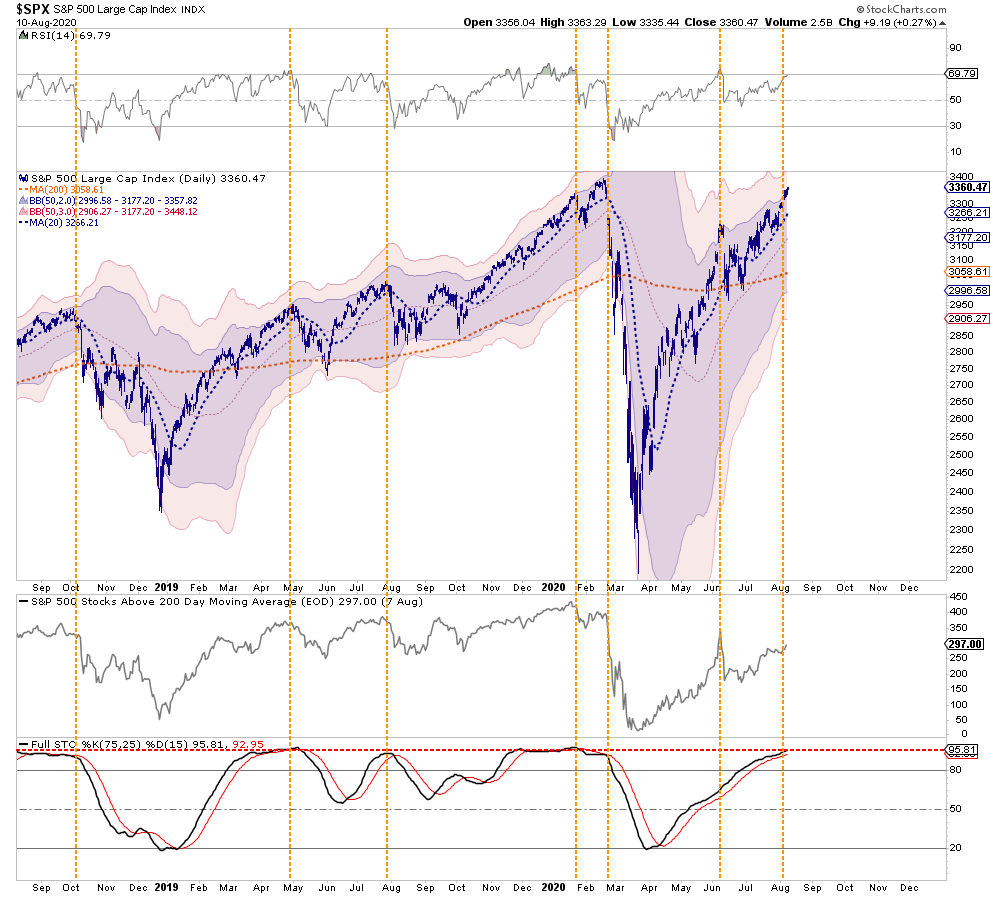

Price action still confirms relative weakness as shown by the percentage of stocks above the 200-dma. Furthermore, the recent rally was primarily focused in the largest capitalization-based companies. These indications suggest market action remains reminiscent of a market topping process rather than the beginning of a new leg of the bull market. With the market trading 3-standard deviations above its 50-dma, and very overbought, such was the same setup we saw at the beginning of the year.

I am not suggesting that the market is on the precipice of another 35% plunge. I am suggesting that the current market and economic dynamics are not as stable as they were following previous market corrections.

The challenge for investors will be the navigation of the markets to ensure they see the “train,” and not the “light.”

Importantly, while the “always bullish” media tends to dismiss warning signs as “just being bearish,” such unheeded warnings have been detrimental.

Complacency is not a great option for managing your capital.

via ZeroHedge News https://ift.tt/3afJvcN Tyler Durden

Trump ‘Seriously Mulling’ Capital Gains Tax Cut Tyler Durden

Tue, 08/11/2020 – 10:11

President Trump on Monday said he’s “very seriously” considering slashing the capital gains tax via executive order, according to Bloomberg.

“We’re looking at also considering a capital gains tax cut, which would create a lot more jobs,” said Trump during a White House news conference.

The president can’t unilaterally cut the 20% long-term capital gains rate without Congress, but some advisers tell him he could issue an executive order that would slash tax bills for investors when they sell assets. The move, known as indexing capital gains to inflation, adjusts the original purchase price of an asset when it is sold so no tax is paid on appreciation tied to inflation. –Bloomberg

The move would undoubtedly face legal challenges by Democrats – which is apparently why President George H.W. Bush’s administration ditched a similar plan, according to the report. Though given Trump’s weekend executive order bypassing Congress to renew lapsed coronavirus relief funds and delay payroll taxes – it’s hard not to wonder if the capital gains tax announcement is designed to goad his political opponents into openly opposing actions that benefit US taxpayers during an election year.

Last year, Trump passed on the idea of indexing capital gains to inflation despite urging from conservatives such as Sen. Ted Cruz (R-TX) and Americans for Tax Reform President Grover Norquist – saying “it’s not something I love.”

Most of the benefit of the tax cut would go to America’s highest earners, with the top 1% receiving 86% of the benefit, according to Bloomberg, citing 2018 estimates by the Penn Wharton Budget Model – and could reduce federal tax revenue by $102 billion over a decade.

Trump is also considering a “cut in the middle income tax” which would require Congress to pass legislation – a move which is unlikely to happen before the end of the year.

via ZeroHedge News https://ift.tt/30Jx71A Tyler Durden

In recent congressional testimony Dr. Anthony Fauci, the primary architect of the Trump administration’s COVID response, painted a bleak picture about the United States’s ability to contain the pandemic. According to Fauci’s narrative, the United States is experiencing a resurgence in regional COVID outbreaks because it failed to sufficiently lock down back in March, and failed to comply with the existing lockdown orders. Fauci specifically contrasted this situation to several European states that imposed lockdowns around the same time, claiming the latter as a successful model for COVID containment.

There are several immediate problems with Fauci’s arguments, including the fact that COVID cases are showing clear signs of a summer resurgence in the same European countries that allegedly tamed the virus through harsh lockdowns in the spring. The American news media however has seized on Fauci’s narrative, and used it to call for renewed lockdowns. The New York Times and the Washington Post both editorialized in favor of a second stricter wave of nationwide lockdowns lasting until October – this despite there being no clear evidence that lockdowns actually work at taming the virus.

So how does the evidence behind this narrative stand up under empirical scrutiny? Let’s consider the claims.

Did the United States react too late?

According to the pro-lockdown narrative, the United States is experiencing a second COVID wave because it took a lackadaisical approach to locking down. We allegedly closed too late and reopened too early, leading to a failure to tame the virus in the spring. This same narrative often holds up Europe as a counterpoint for what a cautious, responsible, and evidence-based reopening process supposedly looks like.

I’ve investigated this claim previously using start and end dates for the lockdowns in various countries. Simply put, it is entirely without merit.

Most of the United States went into lockdown during the second and third weeks of March, following a set of Trump Administration recommendations that were based on the now-discredited Imperial College epidemiology model of Neil Ferguson. In total, 43 of 50 American states imposed shelter-in-place style lockdowns, with the holdouts consisting almost entirely of rural western states with low population density and few signs of the outbreaks that plagued the cities of the northeast at that time.

As far as timing goes, the US lockdowns came into effect at almost exactly the same time as not only Europe but the majority of the world. A few early outbreak hotspots such as Italy preceded this shutdown by about 2 weeks, and a handful of countries (Sweden, Taiwan, Belarus) bucked the international trend. But otherwise, the timeline clearly confirms that the American response directly coincided with most other countries.

Did the US reopen too early?

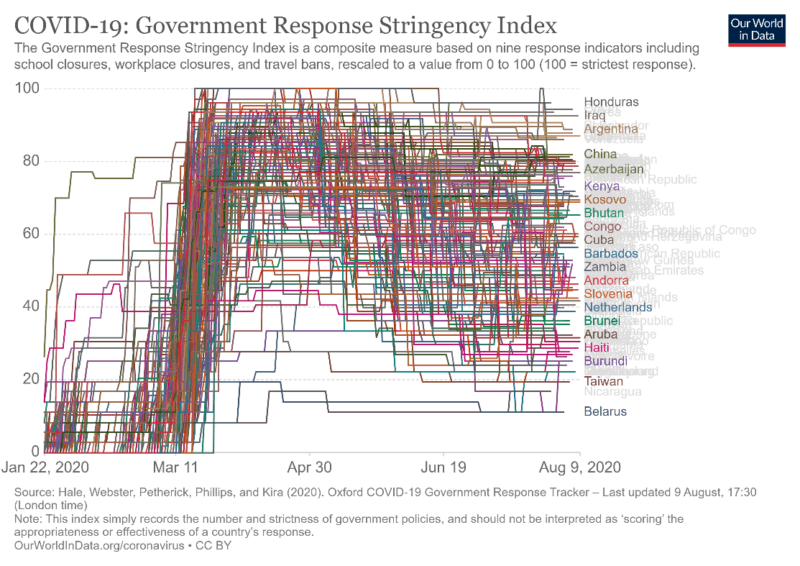

What about reopening then? As I also previously discussed, the United States has generally lagged behind most of Europe in removing the lockdown measures from March and April. Most European countries began their reopening efforts in late April or early May. As of June 1st, the United States’s COVID response stringency score – a measurement of lockdowns and related closures maintained by Oxford University’s Blavatnik School of Government – outranked every Western European nation except for Ireland and Belgium.

Although some US states such as Georgia, Colorado, and Texas began to reopen in late April, this process began no earlier than the first of their European counterparts. Far more often, American states have lagged behind Europe by as much as a month or longer. Several hard-hit states such as New York, New Jersey, and Massachusetts, as well as population centers such as California, adopted a strategy of extremely cautious and tepid reopening. Many extended their shelter-in-place mandates until late May or even June. They also adopted lengthy bureaucratic reopening guidelines that spread the process over several phases to the point that most of the US remains more heavily restricted than Europe to this very moment.

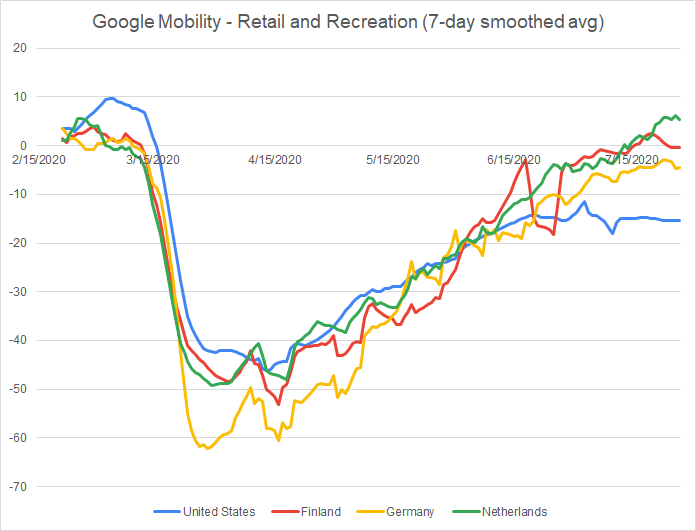

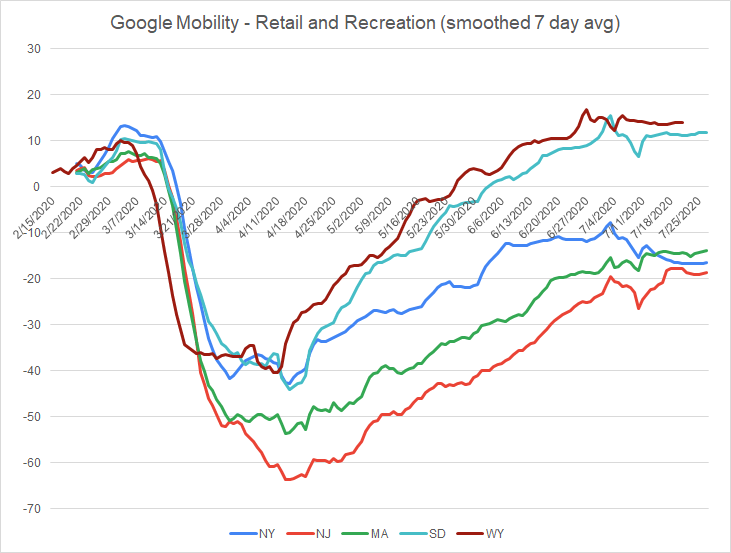

Equally revealing, we may still see the clear effects of the United States’ slower reopening in key metrics from Google’s publicly released cell phone mobility data. From the start of the lockdowns in March until roughly mid-May, US mobility patterns map almost identically onto at least three European countries that similarly locked down: Germany, the Netherlands, and Finland. All three of these countries began to reopen during the first and second weeks of May. Large swaths of the US, and particularly its population centers, remained under lockdown or only a heavily restricted reopening at this point.

The divergence in policies is clearly visible in Google mobility patterns. Whereas Germany, Finland, and the Netherlands all returned to near-normal levels of mobility in late May and June, the United States’ reopening process stalled around the same time and remains at a plateau that is still well-below normal.

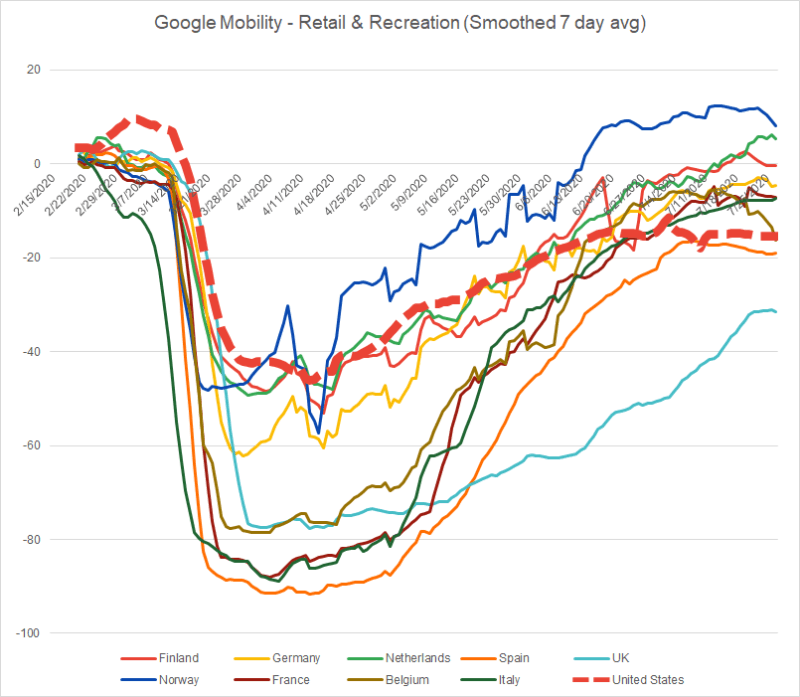

The pattern also appears when we compare the US to other European countries, including those that – at least temporarily – had more stringent shelter-in-place orders in effect. In most European states, mobility patterns rebounded past the United States in early to mid-June after the American reopening stalled. Today, only the UK exhibits a more pronounced closure than the US while Spain similarly plateaued.

Were the US lockdowns less stringent than Europe?

According to Fauci’s testimony, the US imposed far less-stringent lockdown measures than Europe, which he then attributes to the resurgence in cases. This is a complex question to answer because European states varied quite a bit in their lockdown policies and the duration of each. That much noted, nation-level scores such as the Oxford stringency index belie the claim.

The Oxford index uses a 0 to 100 score to measure stringency, awarding points for a variety of policies including border closures, school closures, event cancellation, non-essential business closures, and shelter-in-place mandates, as well as other non-pharmaceutical interventions such as public information campaigns. From the start of the lockdowns in mid-March until June, the United States stringency score sat at 72.69 out of 100. This was comparable to the peak score for the Netherlands (79.63), Germany (73.15), Norway (79.63), Denmark (72.22), and Switzerland (73.15). It was also above Finland’s peak score (60.19) as well as Sweden (40.74), the latter of which did not go into lockdown and only adopted more modest social distancing guidelines.

The US did have a less-stringent score than some of the hardest-hit European countries – but only temporarily. Italy (93.52), France (90.74), Ireland (90.74), and Spain (85.19) imposed more stringent lockdowns than the US, but only for about two months between March and April before rapidly relaxing their restrictions.

Fauci presumably had this much smaller list of countries in mind when he claimed they employed a stricter lockdown than the US, although the evidence is flimsy at best. Measured on a per-capita fatality basis, Italy and Spain had more severe outbreaks than the US, and France currently sits at near-parity. These patterns may change, particularly as each country experiences a second wave in the late summer, but they do not exhibit even modest inverse correlation with the lockdown policies of each country. If anything, the more-stringent policies in locales such as Italy and Spain were likely reactive – they were imposed out of desperation in response to a viral outbreak that appeared to be spinning out of control in these early months. Indeed, the mobility data suggest as much with the most severe declines from the March-April period occurring in the hardest-hit locales and generally starting slightly before they went into lockdown.

Returning to the United States, we see similar variation in the mobility declines when we compare hard-hit states such as New Jersey and Massachusetts with non-lockdown states such as Wyoming and South Dakota (New York breaks somewhat from this trend somewhat, although this is likely a result of substantial in-state variation between hotspots such as New York City and the rest of the state).

These data suggest the claimed effects of more-severe lockdowns cannot be separated from either severity of the outbreak in a given region or the voluntary behavioral responses to the same. This problem afflicts both the worst-hit European countries and the worst-hit US states, but it does not illustrate a failure to impose sufficient lockdowns in each.

In sum, there’s no clear evidence that aligns with Fauci’s claims about European lockdown stringency. On the whole, the US locked down at a comparable level to several European countries according to the Oxford index, with the exception of the hardest-hit locales – and those locales only surpassed us during their peak outbreaks of March and April, followed by a much more rapid relaxation of the restrictions. Meanwhile the US has clearly retained its lockdown policies for longer than almost all of Europe, and continues to stall behind Europe’s reopening process.

Is the US less compliant with public health mandates than Europe?

Although it is more of an implication than a claim from Fauci’s testimony, the media has embraced a final narrative that asserts the United States is less-compliant than Europe in obeying public health mandates. If this were true, the US might have nearly identical policies in place on paper and yet still perform poorly compared to European states where compliance was higher.

Unfortunately, compliance with public health mandates during COVID is difficult to measure. One exception is also a flashpoint of political debate in its own right – the wearing of masks.

Fortunately, extensive survey data exist to track mask-wearing habits of the public since the start of the pandemic. Last month the Economist magazine published a comparison of available survey response rates over time. Briefly summarized, roughly 70% of the US population indicates that it currently wears masks in public places. Mask-wearing has exceeded 60% in the US since early April, despite following several weeks of contradictory advice on masks from public health officials including Fauci himself. US mask-wearing rates are also higher than Canada. It also lags only slightly behind the roughly 80-90% usage rates in east Asian countries, where masks were already a much more common pandemic response.

The fascinating twist to the mask story though is Europe. Mask usage soared in Spain, Italy, and France during the peak of their outbreaks, topping just over 80% or slightly above the US. But mask-usage in Northern Europe remains far below US levels even to this day. No Scandinavian country topped 20% in mask usage even at the April peak of the pandemic (they’ve since declined in number), and the United Kingdom hovers at only 30% in the most recent polling from late June. All said, US mask-wearing is only slightly behind the worst-hit parts of Southern Europe and well ahead of Northern Europe. Insofar as masks may be used to signal compliance with a specific and high-profile public health mandate, there does not appear to be any evidence that the US has fallen behind other countries.

Making sense of it all

Collectively, the data above offer no clear support behind four major claims of the pro-lockdown narrative being spun by American media outlets in the wake of Fauci’s testimony. To the contrary, several data points directly conflict with both the express claims of Fauci’s testimony and its implied interpretations, as advanced by outlets such as the New York Times. The US response to the COVID-19 pandemic largely paralleled Europe in its early months, and only diverged from that pattern in the opposite direction of the media’s narrative. While Europe began to reopen and did so earlier and faster, the United States reopening has stalled.

What then are we to make of the recent case surges in the southern US and on the west coast? Most likely, they reflect the regional nature of the virus’s spread as it migrates into population centers than largely escaped the first wave in March and April. The threat of further spread remains a public health concern, particularly as it pertains to vulnerable populations such as nursing homes. But its pattern has little if anything to do with the lockdown orders – an ineffectual approach to mitigating the virus, but also one with severe social and economic harms.

Unfortunately, the pro-lockdown position favored by Fauci and several US media outlets has become a matter of ideological commitment. Whether they are doing so to rationalize the costs we have already incurred from this disastrous approach or to further politicize the pandemic response for a variety of electoral and partisan purposes, they have embraced a pro-lockdown stance that is unchained from any evidence or clear data.

It should not be surprising that their accompanying narrative to justify that stance is similarly detached from reality.

via ZeroHedge News https://ift.tt/30M8JfS Tyler Durden

Big Ten Waffles After Public Outcry Including Trump Tweet: Might Not Cancel Season After All Tyler Durden

Tue, 08/11/2020 – 09:35

A headline-grabbing story originating in the Detroit Free Press shocked the college and sports world on Monday by reporting the Big Ten is set on cancelling the fall football season on coronavirus concerns. “It’s done,” a high-ranking source in the Big Ten was cited in the report.

“Multiple sources said early Monday morning that presidents voted 12-2 to not play this fall, though the Big Ten said Monday afternoon no official vote had taken place,” according to the report, which was enough to drive headlines declaring the season was canceled.

However, an avalanche of pushback and public outry, from some players, coaches, and even the president of the United States, left the decision anything but final. “The student-athletes have been working too hard for their season to be canceled,” Trump tweeted in response alongside the hashtag #WeWantToPlay, with a shared tweet by Clemson quarterback Trevor Lawrence.

One college sports commentator noted: “A wild and wacky Monday ended without clarity from the Big Ten about a football season. Instead, the wait continues on a decision to play this fall, while pressure builds from some leagues and coaches.”

The immediate public pushback appears to have worked or at least it delayed things, and reports now say the season might not be cancelled after all, with more high level Big Ten meetings set for Tuesday morning.

Not expecting any news tonight from #B1G, per sources. More meetings in the morning, sources say. In all my years covering Big Ten, can’t remember a day when the league seemed more divided (presidents vs. coaches). Certainly could see presidents opting against a full postponement

Thus far the Ivy League, the Pac-12, and the Mid-American Conference, have all canceled their seasons.

While the majority of college presidents appear to stand on the side of cancellation for the sake of safety amid the pandemic, there are said to be other options being considered, like mere postponement of the game schedule.

Whatever happens, severe controversy is already ensured, given as SI describes:

“All of this was sparked by the Big Ten’s impending move to cancel its season. More than 24 hours after first reports published from ESPN, Yahoo Sports and SI of the Big Ten’s potential plans, the conference still hasn’t made an announcement and is now gripped in an internal strife that poured out into public Monday.”

And further: “From high-ranking politicians to the league’s own coaches, a variety of personas strongly voiced their support for a 2020 season, some of them specifically targeting the Big Ten and commissioner Kevin Warren.”

via ZeroHedge News https://ift.tt/3fKzB3Z Tyler Durden

Gold, Silver, Bonds Hit As “Everything Duration”-Momo/Liquidity Trade Unwinds Tyler Durden

Tue, 08/11/2020 – 09:22

Precious metals are getting pummeled this morning as real rates rise amid vaccine optimism and hotter than expected inflation data…

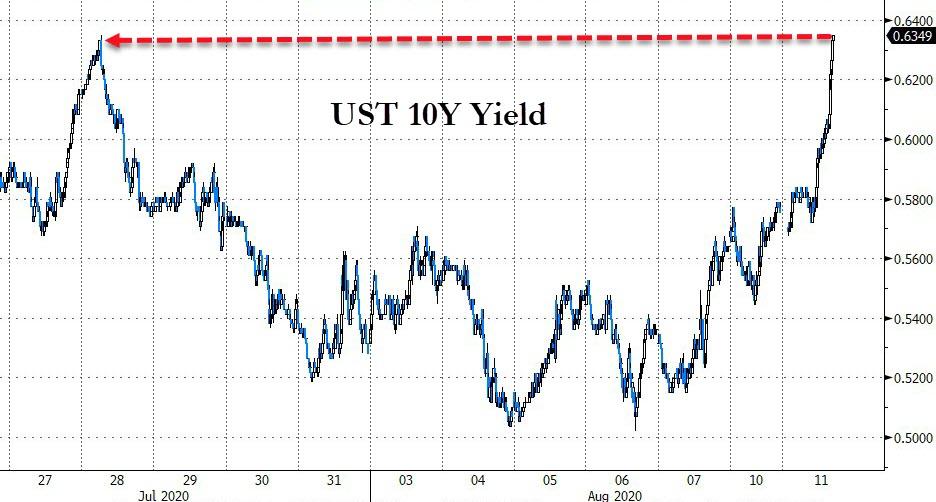

Bonds are also getting slammed with 10Y Yields back above 60bps at 10-day highs…

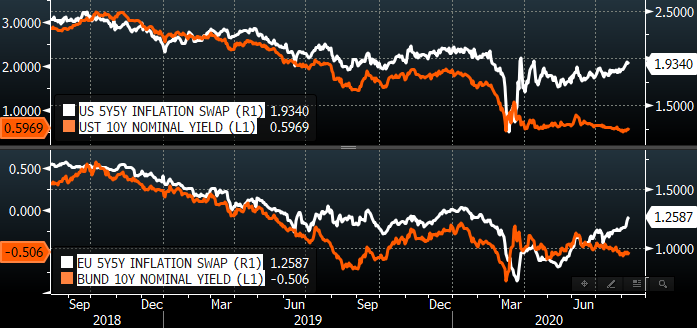

As Nomura’s Charlie McElligott reiterates (from his call last week), “inflation expectations” are beginning to adjust higher – Inflation swaps in U.S. and Europe (fickle traders, no doubt) are beginning to tell a story of nascently accelerating global views towards forward inflation – something that was inconceivable to nearly all just a few months ago and now coinciding with the back-to-back weeks of U.S. M2 decline, showing a decrease in risk-aversion and saving and a “less bad” economic outlook from corporates.

And as real yields rise, gold prices fall…

As the Nomura MD has noted over the past few weeks, the SPX macro factor regime has transitioned from “Liquidity” macro factor measures which led the March Equities recovery:

1. Fed QE Expectations – 1y5y USD Rate Vol,

2. Fed Rate Cut Expectations – ED$ Curve,

3. USD Liquidity – FX Basis Swaps

…now into “Growth” inputs as the largest POSITIVE price-drivers for S&P 500 in the factor PCA model:

1. US and EU GDP NowCasting and

2. Inflation Swaps

But the most dramatic impacts of the reflation trade inflection are evident in the broad equity markets… where Nasdaq is tumbling as Small Caps surge…

And as McElligott notes, US Equities factors are showing the most glaring expression of the market’s flat-footedness in their growth- and inflation- skepticism (and evidencing itself in the crowded “Everything Duration” Momentum-positioning which is evidently being de-grossed by somebody):

The current iteration of this U.S. Equities factor “Value / Momentum” swing (5d aggregate % chg) is a doozy, ranking as in the top six since at least 2010, going hand-in-hand with monster thematic- and sector- reversals.

The question is – how high will The Fed let nominal rate rise before it stomps on this reversal?

via ZeroHedge News https://ift.tt/31DU1H7 Tyler Durden

{kind=link}