The Washington Post and New York Times have recently opened up their platforms to Op-Eds defending, justifying and promoting abhorrent behavior committed against conservatives. Calling them out is the Washington Examiner‘s Byron York, who notes that “the toxicity of the resistance to President Trump has risen in recent days,” with both papers “publishing rationalizations for denying Trump supporters public accommodation and for doxxing career federal employees.”

First up, Stephanie Wilkinson, the owner of the infamous Red Hen restaurant in Lexington, Virginia. Wiklinson unapologetically booted White House spokeswoman Sarah Huckabee Sanders and her family last June. Wilkinson told the Washington Post at the time that her gay employees were too triggered by Sanders to serve her due to the Trump administration’s transgender military ban.

On Friday, Wilkinson essentially told conservatives that it’s their own fault if they are attacked in public.

In her new article, Wilkinson discussed the case of The Aviary, a trendy bar in Chicago where a waitress recently spat on Eric Trump, the president’s son. Wilkinson wrote that the incident, along with her own decision to oust Sanders, shows that in the age of Trump “new rules apply” in public accommodations: Americans who work for the administration or support the president should stay away.

“If you’re directly complicit in spreading hate or perpetuating suffering, maybe you should consider dining at home,” Wilkinson wrote.

Wilkinson noted that “no one in the industry condones the physical assault of a patron,” but at the same time declared that Americans should understand that a “frustrated person” — for example, a restaurant employee — will “lash[] out at the representatives of an administration that has made its name trashing norms and breaking backs.” Americans should accept that such things will happen.

“If you’re an unsavory individual,” Wilkinson concluded, “we have no legal or moral obligation to do business with you.” Better to stay home than risk the spittle. (And of course, Wilkinson and her colleagues in the hospitality industry will decide who is “unsavory.”) –Washington Examiner

And what constitutes an unsavory individual? Apparently half of the country!

New York Times and Doxxing

York next calls out the New York Times for allowing a University College London assistant professor of human rights, Kate Cronin-Furman, who justifies doxxing the personal details of low-and-mid level Customs and Border Protection employees who are responsible for taking care of migrant children at border detention facilities.

Cronin-Furman discussed the detentions, as well as actions by employees of U.S. Customs and Border Protection, in terms of the Holocaust and genocides in Cambodia and Rwanda. Those are, of course, contexts which most Americans would likely dismiss as preposterous and offensive but which Cronin-Furman and the New York Times apparently take seriously. Her idea is that opponents of the administration should publicly identify and shame low- and mid-level Customs and Border Protection employees who care for migrant children.

Such workers would be dismayed at being publicly shamed because they are “sensitive to social pressure,” Cronin-Furman wrote, “which has been shown to have played a huge role in atrocity commission and desistance in the Holocaust, Rwanda, and elsewhere. The campaign to stop the abuses at the border should exploit this sensitivity.” –Washington Examiner

“This is not an argument for doxxing,” Cronin-Furman continued. “It’s about exposure of their participation in atrocities to audiences whose opinion they care about. The knowledge, for instance, that when you go to church on Sunday, your entire congregation will have seen you on TV ripping a child out of her father’s arms is a serious social cost to bear. The desire to avoid this kind of social shame may be enough to persuade some agents to quit and may hinder the recruitment of replacements. For those who won’t (or can’t) quit, it may induce them to treat the vulnerable individuals under their control more humanely. In Denmark during World War II, for instance, strong social pressure, including from churches, contributed to the refusal of the country to comply with Nazi orders to deport its Jewish citizens.”

As York notes, “Needless to say, that was a clear argument for doxxing.“

Time and time again we’ve heard from the left that ‘hate speech’ is so dangerous because it could inspire people to commit violent acts.If that’s the case, why are the Washington Post and New York Times allowing people to use their platform to justify actual violence and potentially dangerous acts against conservatives? Doesn’t the same theoretical slippery slope of ideological division that ends in tiki torches and lynchings similarly feed the countless acts of actual violence committed by Antifa? We’re guessing you already know the answer.

via ZeroHedge News https://ift.tt/2J0iP3R Tyler Durden

Now that the Osaka G-20 has come and gone, and while nothing has been resolved in the US-China trade war, at least there has been no escalation and China is safe from US tariffs on the remainder of its exports to the US, which in turn has given algos a dose of optimism that all is well pushing S&P futures just shy of 3,000, things in the real world are going from bad to worse.

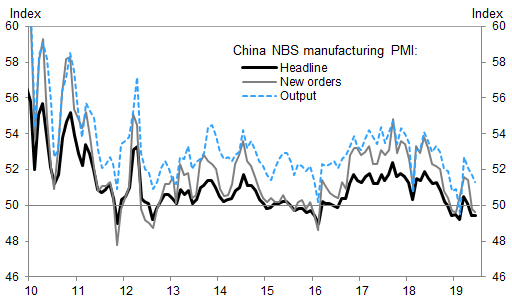

One day after China’s official NBS manufacturing PMI on Sunday printed unchanged at 49.4 in June, below expectations of an increase from May…

… with most of the key sub-components sliding to new cycle lows:

production index 0.4 lower at 51.3,

new orders sub-index was 0.2 lower at 49.6

employment sub-index edged down 0.1pp to 46.9.

imports sub-index down to 46.8, from 47.1,

new export order index down to 46.3, vs. 46.5 in May

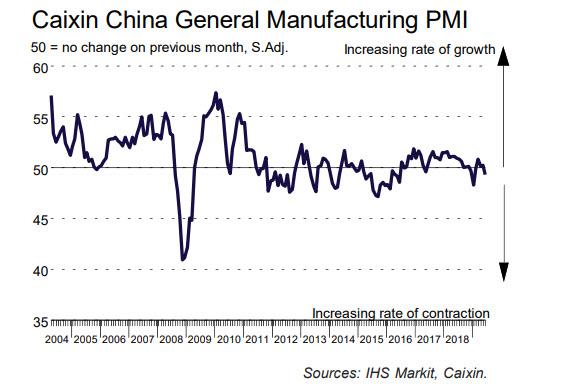

… the other Chinese PMI, the Caixin Manufacturing PMI, hammered expectations as it unexpectedly slumped back into contraction.

Falling from 50.2 in May to 49.4 in June, the Cixin PMI – which differs from the official, NBS report by shifting away from SOEs and large enterprises and instead focusing on small and medium businesses – was below the critical 50.0 threshold which divides contraction and expansion, for the first time in four months.

According to the report, the June data highlighted a “challenging month” for Chinese manufacturers, with trade tensions reportedly causing renewed declines in total sales, export orders and production.

Commenting on the June PMI data, Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said: “The Caixin China General Manufacturing Purchasing Managers’ Index was 49.4 in June, the second lowest since June 2016, indicating a clear contraction in the manufacturing sector, and only for the first time since late 2016, identical to China’s official Mfg PMI print (which was also 49.4).

“The subindex for new orders slid into contractionary territory, pointing to notably shrinking domestic demand. The gauge for new export orders returned to contractionary territory, but was better than the levels seen from last April to last December. Front-loading by exporters was likely to support this gauge as the China-U.S. trade relationship was under great uncertainty.

The output subindex fell into contractionary territory. The employment subindex remained relatively stable in negative territory, likely due to government policies to stabilize the job market. The State Council set up a leading group on employment in late May.

The subindex measuring sentiment toward future output plunged further, albeit staying in expansionary territory, a reflection of continuously weakening business confidence amid the Sino-U.S. trade conflict.

Overall, China’s economy came under further pressure in June. Domestic demand shrank notably, foreign demand was still underpinned by front-loading exports, and business confidence fell sharply. It’s crucial for policymakers to step up countercyclical policies. New types of infrastructure, high-tech manufacturing and consumption are likely to be the main policy focuses.”

In short, the US-China trade war is Trump’s for the taking… if he wants it: companies responded to the latest escalation by reducing headcounts further and making fewer purchases of raw materials and semi-finished items. At the same time, China appears to be sliding into stagflation, as selling prices were raised following another increase in input costs, though rates of inflation were negligible, suggesting that companies failed to pass on costs to consumers. Also, business sentiment was broadly neutral at the end of the second quarter, with firms mainly concerned about the US-China trade dispute.

It wasn’t just China that was a shitshow: Asian factory PMIs were almost universally awful on Monday, adding to the signal from the official China report out Sunday that as Bloomberg put it, “the global economy has been harpooned by the trade wars.” To wit:

Taiwan’s PMI dropped to 45.5, the lowest since 2011, and it’s now been below the 50 line separating contraction from expansion for 9 straight months — the longest since a 10-month stretch that ended in Feb. 2009.

South Korea’s gauge slumped further into contraction (47.5 vs 48.4 in May) to confirm April’s spike above 50 was an outlier

Japan’s came in at 49.3, worse than the initial reading of 49.5.

Australia’s AIG factory gauge fell into contraction for the first time since 2016

Malaysia’s PMI sank again to hold below 50.

Indonesia and Thailand’s gauges fell, while holding above 50.

The Philippines was the only substantial regional economy to see a tick up.

Meanwhile, futures blissfully continue to ignore the collapsing global economic reality, and instead rejoice at the “successful” conclusion of the Trump-Xi meeting, which notd only achieved nothing, but confirmed the status quo – massive tariffs and the threat of more.

The decision to resume talks, meanwhile, offers little cause for optimism given that this conflict has now dragged on for more than a year as Bloomberg Garfield Reynolds says, adding that “the PMIs underscore how much damage has been done by the trade spat, and even the central bank stimulus being forecast by rates markets is looking more and more like band aids that won’t stop the bleeding.”

via ZeroHedge News https://ift.tt/2ZSJcOS Tyler Durden

The Russian military quickly intervened to prevent a deadly confrontation between the Syrian and Turkish forces on Saturday.

The Syrian Arab Army (SAA) first opened fire on the militant-held Sheir Magher area after the Turkish-backed rebels fired several artillery shells towards their positions in northwestern Hama. The Sheir Magher area is where the Turkish observation post is located in northwestern Hama.

Image via AMN

Following the Syrian Army attack on the Turkish observation post area, the Russian Armed Forces quickly intervened to prevent further hostilities, a source near the front-lines told Al-Masdar News.

The source added that the Russian Armed Forces are currently present in the northwestern countryside of Hama, with many of their soldiers deployed to the towns of Mhardeh and Al-Sqaylabiyeh.

Image via AMN

Earlier this week, the Syrian Army killed a Turkish soldier in the Sheir Magher area after the former was responding to an attack by the militants in northwestern Hama.

Eyes in the sky: @NATO Boeing E-3A Sentry over SE Turkey monitoring heavily increased Russian military aircraft movements over #Syriapic.twitter.com/HTZMEB684o

The Turkish Armed Forces later retaliated by shelling the Syrian Army checkpoints near Sheir Magher – no casualties were reported.

That prior deadly incident involved the Syrian Army striking a Turkish observation post in the same area, resulting in the death of one soldier and hospitalization of three others.

First pictures and videos of the . intense shelling by #Assad forces, following the skirmish with the #TurkishArmy last night.

Turkey angered them, civilians take the revenge hits.

And Turkey is just watching from its observation positions …https://t.co/SyAVpFojhZ#Syriapic.twitter.com/MY7wFBcpy3

In retaliation, the Turkish military attacked a couple of the Syrian Army checkpoints in northwestern Hama.

Following the incident, the Turkish authorities summoned the Russian military attache in Syria and demanded that they control the Syrian Army in northwestern Hama.

The potential for further direct Syrian-Turkish clashes in Syria’s north, along with a significant uptick in both Russian and NATO aerial activity over the region, makes for an intensifying and volatile situation.

via ZeroHedge News https://ift.tt/2XH3m0S Tyler Durden

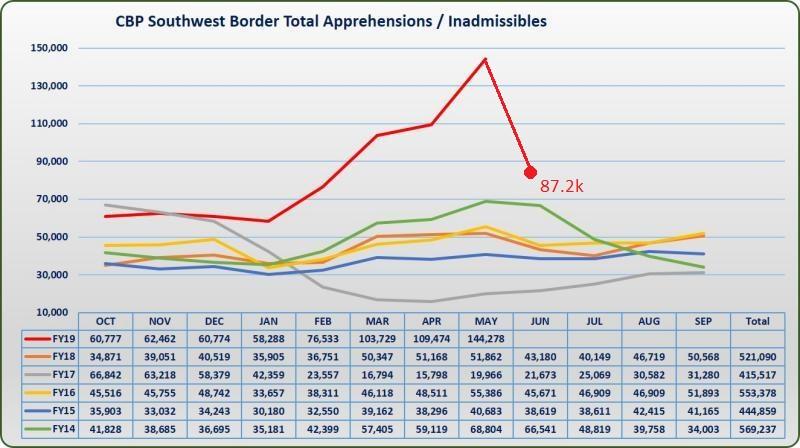

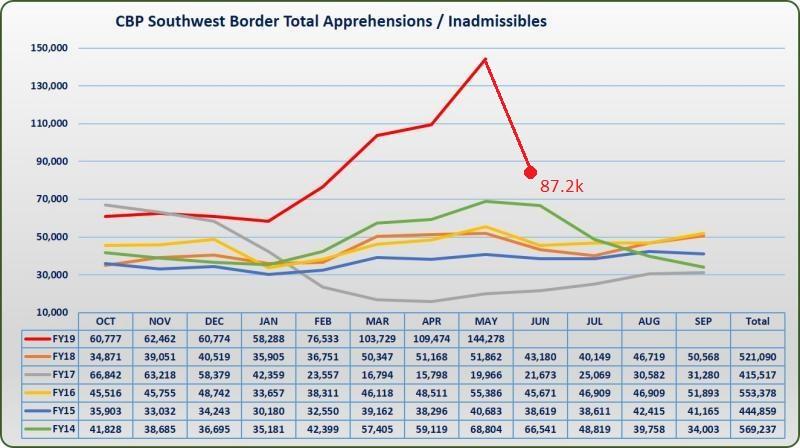

It appears that Mexico’s act of good faith to avoid tariffs may have begun to pay off.

According to leaked figures, US Border Patrol apprehensions of illegal immigrants dropped precipitously in June, weeks after Mexico announced the deployment of 15,000 National Guard troops to the US-Mexico border and froze the bank accounts of 26 human traffickers with “probable links with human trafficking and illegal aid to migrant caravans.”

According to the preliminary figures, leaked to Axios, there were over 87,000 apprehensions in the month of June, a drop of nearly 35% vs. 132,887 apprehensions in May.

Roughly 7,000 of the apprehensions were unaccompanied minors, 52,000 were family units, and 28,000 (roughly 1/3) were single adults according to the report.

That said, Axios’s Alayna Treene says that DHS officials told her border crossings are typically lower in hotter months, and that it would be difficult to gauge whether Mexico’s troop deployment or other policies. On the other hand, one look at the above chart provides a clear look at seasonality going back to 2014.

Worth noting: These preliminary figures only capture the number of apprehensions (those who cross illegally) on the southwest border. They do not include the number of inadmissibles (those who migrate through ports of entry), which is normally included in the total migration data U.S. Customs and Border Protection (CBP) releases each month. They are also subject to change given that they’re continuously updated by CBP until the final figures are published. –Axios

Democrats running for President slammed President Trump’s Sunday visit to North Korea, claiming it was an ill-conceived waste of American bargaining power, according to The Hill‘s Alex Bolton.

The moment President Trump meets Chairman Kim at the DMZ and becomes the first sitting President to enter North Korea: pic.twitter.com/VwqGAEmmxz

After becoming the first US president to set foot on North Korean soil, Trump met with leader Kim Jong Un in a surprise negotiation session that lasted just under an hour on the South Korean side of the Demilitarized Zone – a meeting which will improve future communication just one week after Trump sent Kim a “friendly” letter (probably telling him he’d swing by after the G20).

Unsurprisingly, Democrats threw shade at the US president, who suggested that the meeting was an achievement that former President Obama had strived for but failed.

Former Vice President Joe Biden’s team slammed Trump for “coddling” dictators “at the expense of American national security and interests,” and said “we urgently need a president who can restore our standing in the world, heal relationships with key allies Trump has alienated, and delivered real change for the American people.”

🚨 NEW: @JoeBiden campaign statement on @realDonaldTrump‘s “coddling of dictators at the expense of American national security and interests,” including fawning over Kim Jong-un and joking “with Vladimir Putin about our election security and ‘getting rid’ of journalists.” pic.twitter.com/nTRIYx7aSz

Bernie Sanders (I-VT), the democratic socialist candidate who honeymooned in Moscow, said that Trump’s visit “weakened the state department,” adding “The concern here is his incredible inconsistencies. I have no problem with him sitting down with Kim Jong-un in North Korea or any place else. But I don’t want it simply to be a photo opportunity, the whole world’s media was attracted there.”

Sen. Elizabeth Warren went for the scalp, tweeting “Our President shouldn’t be squandering American influence on photo ops and exchanging love letters with a ruthless dictator.”

Our President shouldn’t be squandering American influence on photo ops and exchanging love letters with a ruthless dictator. Instead, we should be dealing with North Korea through principled diplomacy that promotes US security, defends our allies, and upholds human rights. https://t.co/9ROpNfjYbY

Both Sen. Amy Klobuchar (D-MN) and Julián Castro also weighed in, with Klobuchar telling CNN‘s “State of the Union” on Sunday “We want to see a denuclearization of the Korean peninsula, a reduction in these missiles but it’s not as easy as just going and, you know, bringing a hot dish over the fence to the dictator next door”

“This is a ruthless dictator and when you go forward, you have to have clear focus and a clear mission and clear goals,” she added.

Castro sounded a lot like Sanders, telling ABC‘s “This Week”: “It’s worrisome that this president erratically sets up a meeting without the staff work being done. It seems like it’s all for show, it’s not substantive,” adding ‘I am all for speaking with our adversaries, what’s happened here is this president has raised the profile of a dictator like Kim Jong Un and now three times visited with him unsuccessfully because he’s doing it backward”

Yang did not gang up

Democratic candidate Andrew Yang was the only 2020 Democrat to praise Trump’s meeting with Kim, tweeting: “Anything that improves the political climate on the Korean peninsula and engages North Korea on its nuclear program is a good thing.”

Anything that improves the political climate on the Korean peninsula and engages North Korea on its nuclear program is a good thing.

As politicians today assert, so loudly and sanctimoniously, that things like food, housing, health care, jobs, childcare, a cleaner-safer environment, transportation, schooling, utilities, and even college should be “free,” or publicly subsidized, almost no one asks why such claims are valid.

Are they to be accepted blindly on faith or affirmed by mere intuition (feeling)? It doesn’t sound scientific. Shouldn’t all crucial claims pass tests of logic and evidence?

Typically, a freebie claim receives conditional praise: “it sure sounds good, but it’s probably too costly.” My guess is that freebie proposers like hearing that compliment, which also makes them inclined to offer still further freebies. As for cost warnings, my guess also is that freebie proposers like hearing how others will work on the accounting and locate the necessary funding, especially as it’s already been shown that democratic governments can, almost without limit, tax, borrow, print money, mandate private spending, or nationalize industries. Do these measures harm prosperity? Yes, but that’s of no concern to the freebie promisers.

Why do freebie claims “sound good” to so many people? They don’t sound very good to me. Why not? Because they sound mean, even heartless. Why? Because they’re illiberal, hence fundamentally inhumane. I hope I’m not alone in recognizing that promised freebies are not gifts of nature or manna from heaven, but things produced by actual living human beings who choose to employ their minds and bodies. Who owns the products and services of these minds and bodies? Who should determine whether and how goods or services should be created, exchanged, invested, consumed or bequeathed? Indeed, who owns these minds and bodies?

An increasingly popular motto today is “my body, my choice.” Good motto. How about, also, “my mind, my choice?” “My business, my choice?” My money, my choice?” Why not promote a freedom to choose and act in all aspects of our precious lives, not only in just a few aspects?

To claim that health care is “a basic human right” and should be “free,” is akin to claiming that health care consumers have a “right” to compel health care producers to supply. Is it not obvious that this violates the rights and liberties of health care producers? How, in logic (or in morals) can one claim to have “a right to violate rights?” Do not doctors, nurses, hospitals, drug companies, and medical instrument makers have rights? The principle doesn’t differ, of course, if the exchange is funded by resources forcibly seized from unrelated parties. Nor is the principle inapplicable merely because those who seize are elected by democratic majority. There seems nothing “just” about a society of third parties made to pay for things they don’t get, so that others may get something for nothing. Yet the policy is deemed “socially just.”

Likewise, to claim a college degree is “a basic human right” that should be “free” is akin to claiming consumers of higher education have a “right” to compel its producers to supply it. Doesn’t that violate the rights of college professors and administrators? Are they not to be paid for the value they provide? What aspect of their character or work uniquely fits them to professional servitude, or worse, to abject dependence on the good graces of state officials? Again, the illogic of “a right to violate rights” isn’t altered by making third parties pay the bill.

Imagine cotton is also “a basic human right” to be provided “free.” Cotton-makers are deprived of liberty and the fruits of their own labor. It was a belief implicit in the minds of plantation-slave owners in the American South in the 19th century. It too is a vile belief.

In a free, capitalist system of constitutional government there is to be equal justice under law, not discriminatory legal treatment; there’s no justification for privileging one group over another, including consumers over producers (or vice versa). Every individual (or association) must be free to choose and act, without resorting to mooching or looting. The freebies approach to political campaigning and policymaking brazenly panders to mooching and, by expanding the size, scope, and power of government, also institutionalizes looting.

As politicians contemplate (and effectuate) policies moving us away from capitalism towards more socialism, perhaps it’s no surprise that we also see pervasive, unabashed freebie promising. Don’t forget that socialism means public (state) ownership of the means of production – means that include land, labor and capital. State ownership and control of labor and of its fruits isn’t far removed from ownership of laborers per se – i.e., of people. The ownership of humans by humans is worse than “illiberal” or inhumane; it’s the very definition of slavery. The socialist case is buttressed by its principle of distribution (from Karl Marx, in Critique of the Gotha Program, 1875), that folks in the collective must contribute to the sum of resources “according to ability” while taking out of the same sum “according to need,” a morally dubious and economically unsustainable formula that severs pay from productivity while causing ever-more poverty, neediness, and victimhood, both real and imagined.

In the 1940s, Princeton public finance professor Harley Lutz first wrote that “there’s no such thing as a free lunch,” an adage used subsequently and often by free-market economists. It captures the common sense of the matter, but not quite its morality. Yes, lunches must be produced, before they can be consumed or distributed – confirming Say’s law of markets, contra the Keynesians – but who should decide matters of consumption and distribution?

According to J.B. Say, the producer, by rights, is to decide what’s to be done with his product (A Treatise on Political Economy, 1803); J.S. Mill, in contrast, said that while the laws of production are scientific and economic, those of distribution and consumption are arbitrary and political (Principles of Political Economy, 1848). Producers will always work, he said, but otherwise should be mute as to what’s done with their product. Marx agreed. No wonder then that Say remained a pro-capitalist his entire life, while Mill veered off into socialism.

Political leaders should respect both productive prowess and producers’ rights. Just as lunch-eaters should be left free to pay for lunch, so the lunch-makers should be free to produce and exchange as they wish, and even gift a lunch, out of charity or philanthropy. Instead, many political leaders today openly pander to the free-riding, “something-for-nothing,” mooching mentality. It’s illiberal, undignified, and unworthy of an advanced, constitutional society.

It’s possible, of course, that the freebie-promisers are mistaken only because they’re myopic, or because they don’t know basic economics. If so, they could read Economics in One Lesson (1946) by Henry Hazlitt, who spelled out “the difference between good economics and bad,” as follows:

“The bad economist sees only what immediately strikes the eye; the good economist also looks beyond. The bad economist sees only the direct consequences of a proposed course; the good economist looks also at the longer and indirect consequences. The bad economist sees only what the effect of a given policy has been or will be on one particular group; the good economist inquires also what the effect of the policy will be on all groups.”

If today’s politicians knew at least what Hazlitt knew, it might deter them from being so shortsighted, but would it dissuade them from being freebie promisers? The problem goes much deeper than economics, because the freebie-promisers, while catering to those in need, mistakenly believe they occupy the moral high ground; in truth, they cater with food they didn’t produce and the worst of the many costs they impose on us is that of lost liberty.

via ZeroHedge News https://ift.tt/2XxFFIn Tyler Durden

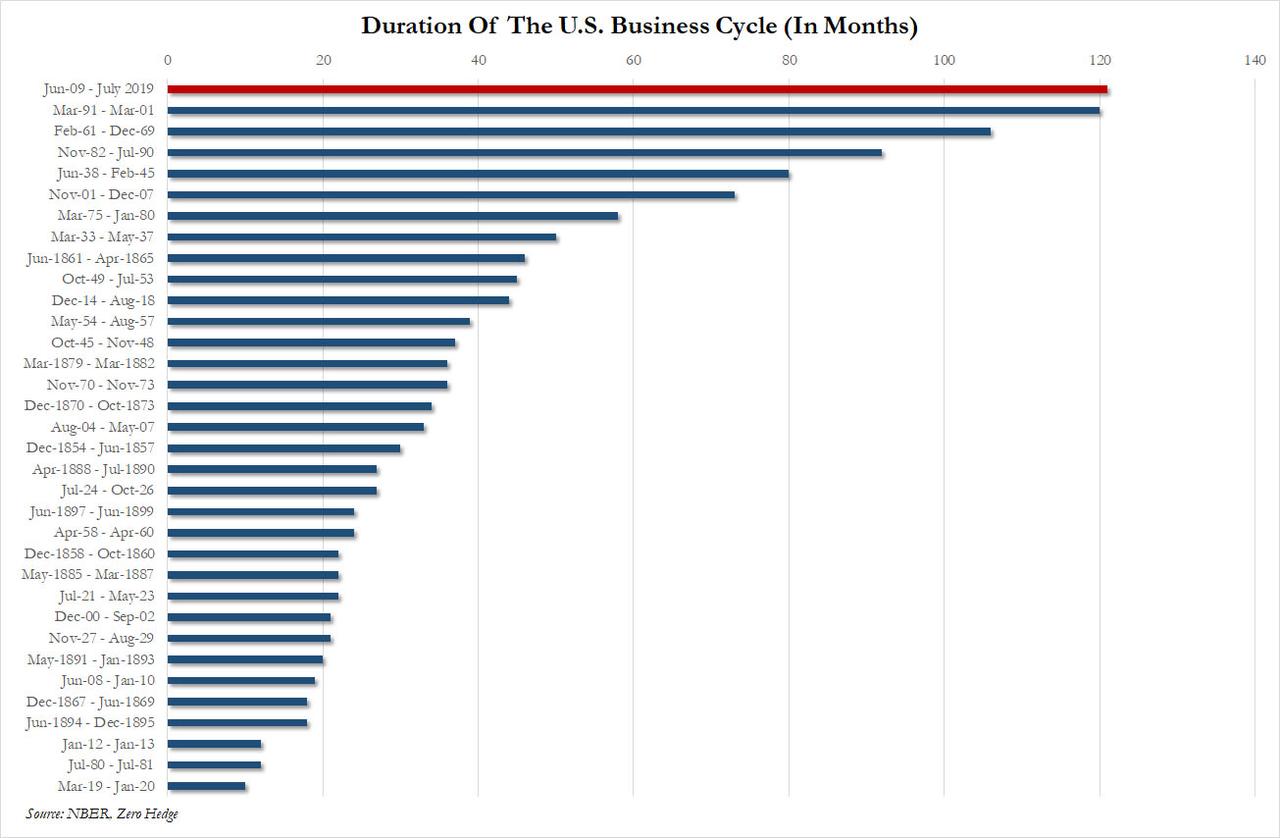

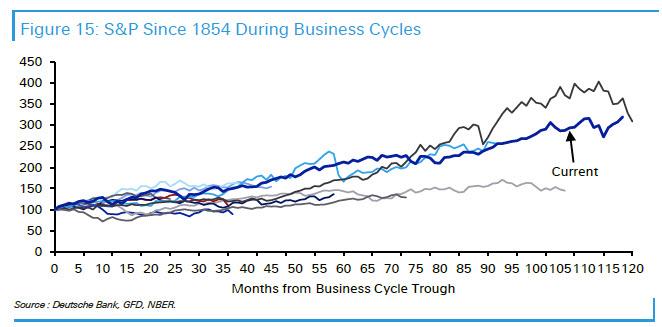

In just a few hours, on July 1, the US economic expansion will become the longest on record, entering its 121st month since the end of the 2009 recession (which according to the NBER ended in June of that year), and surpassing the previous record – the March 1991 – March 2001 expansion – which ended with the bursting of the dot com bubble.

As Deutsche Bank’s Jim Reid writes, since US business cycles have been tracked from 1854 there have been 34 expansions. The last four have all been long relative to the past and are all in the top six in terms of duration. The other two in this top six were the June 1938-cycle which was boosted by the WWII rearmament efforts, and the Feb 1961-cycle where the Fed were late to deal with ever increasing US inflation, leading to too loose monetary policy and an extended cycle.

As part of a recent analysis, Deutsche Bank explains why this cycle – and the past four – have been so long relative to history, show various economic and market indicators from this cycle relative to the past to put the record-breaking expansion in some context, and predict what may happen next.

It may come as a surprise to exactly nobody, that there is a distinct correlation between the rising length of the US business cycle – and ensuing economic and market crashes which terminate said expansion – and the advent of the Federal Reserve. Oh, and globalization has a lot to do with everything too.

But first, a quick stroll down memory lane…

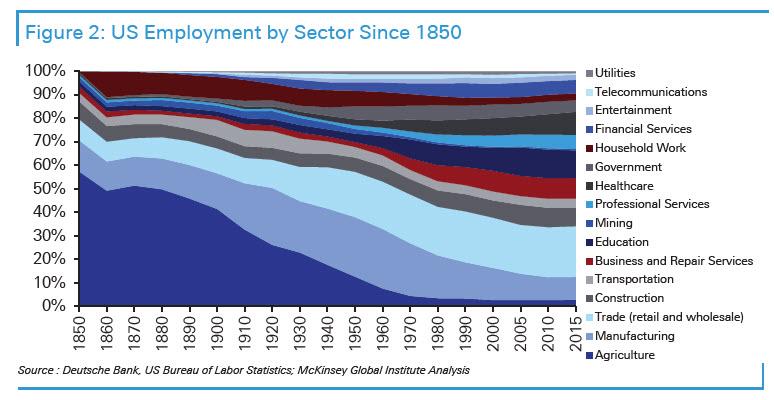

As Deutsche Bank writes, during the earliest monitored business cycles, the US economy was predominantly agriculturally based. Indeed the share of employment made up from this sector was 59% in 1850 and only dipped below 30% by 1920 and below 10% by 1960. This likely made GDP more volatile as the economy was more exposed to the boom and bust crop cycles without much sector diversity. In addition, prior to 1913 there was no central bank and banking runs and panics were a fairly regular feature of the economic landscape.

As the economy became more diverse and less dependent on agriculture and the Federal Reserve appeared in 1913 and became increasingly more active in the economy and capital markets, economic cycles were able to be extended. However, WWI and its aftermath, the stock market crash, the 1930s Depression, and the fact that the US operated under a gold standard ensured that cycles were still relatively short by modern standards until at least WWII.

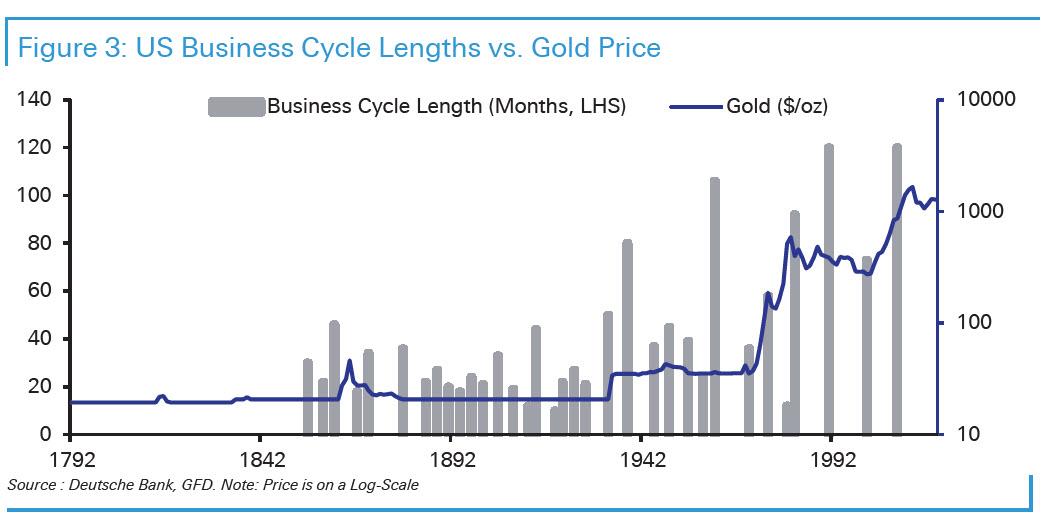

The gold standard and subsequent Bretton Woods system (1946-1971) restricted stimulative policy (both fiscal and monetary). The dollar was convertible into gold at a fixed price and policy had to ensure that there wasn’t a run on gold reserves.

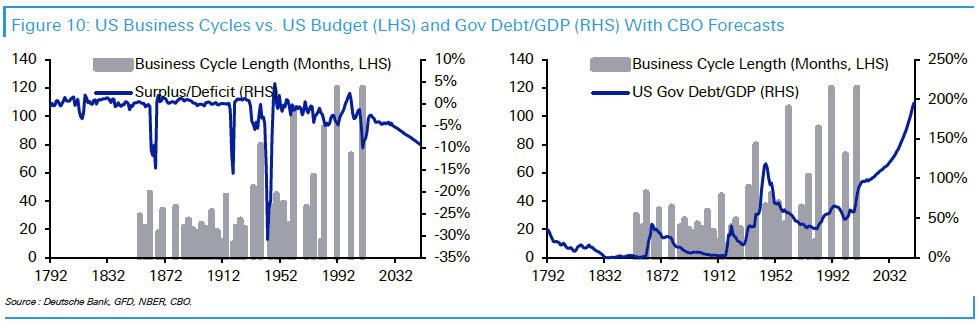

Amusingly, indirectly summarizing the current economic and market climate, Deutsche Bank writes that back int he day, “loose fiscal or monetary policy to extend a business cycle would have likely led to the perception that the authorities were prepared to generate inflation and erode the value of the dollar.” Which, of course, is the current situation, only it’s not just the US that is doing it, but everyone is. In any case, when this happened during various points in the past, gold would have flowed out of the country threatening the economic management model of the time. The chart below shows the price of gold to the USD alongside the length of each business cycle and suggests that business cycles were a lot shorter when the dollar was rigidly price fixed against gold. As the ties slowly loosened to gold – culminating with Nixon closing the gold window on August 15, 1971 and effectively ending the Bretton-Woods system – and devaluations occurred, business cycles started to get longer.

It’s worth noting that as the ties to gold were loosened, economic policy could become more flexible – think more and more debt – allowing the “opportunity” for more stimulus. Deutsche Bank shows this by highlighting the length of each US business cycle but this time with the annual US budget deficit (left) and total Government Debt to GDP (right) overlaid on top. Bottom line: with the US dollar becoming unanchored from gold in the 1970s, it allowed every successive administration to avoid recessions by piling up more debt and spending at an ever faster rate.

What may come as a surprise to several generations of Americans is that prior to the late 1960s, the US ran close to a balanced budget every year outside of war time and the Great Depression. Deficits temporarily ballooned and debt increased on these occasions and membership of the gold standard was often suspended allowing for more flexible policy for a brief period of time. However, the US quickly went back to balanced budgets after these events alongside a stable gold/USD parity which made it very hard to be overly stimulative.

Pressure on this system started to build as the post-WWII landscape emerged, leading to structural deficits slowly building up in the late 1960s. There was huge population growth in this era and at the same time we saw the birth of the welfare state and “great society” type movements. Across the globe, citizens were increasingly demanding more access to education, healthcare, a safety net for the poor and unemployed, better public services, and the increased provision of state pensions. This led to increased demands for governments to spend more and this was funded by deficit spending across the world, a trend that lasts to the current day. Very few countries have managed to balance their fiscal books over the last 50 years.

Of course, this new trend was not sustainable in a precious metal currency system and eventually the increases in US/global deficits put pressure on the Bretton Woods system. In 1971 President Nixon suspended the convertibility of dollars into gold and the US moved to the fiat currency regime that is still in existence today. At that point the vast majority of global currencies – that had been fixed to the USD in the Bretton Woods system – also effectively became fiat currencies.

As currency ties to gold broke around the globe, cycles started to get longer but debt started to increase – a pattern that has extended to the current day with the added kicker in this current cycle being the largest round of central bank balance sheet expansion in history in the US, and at a global level: i.e. the entire world is now all in on avoiding a recession, and the cost is the greatest accumulation of sovereign debt in history.

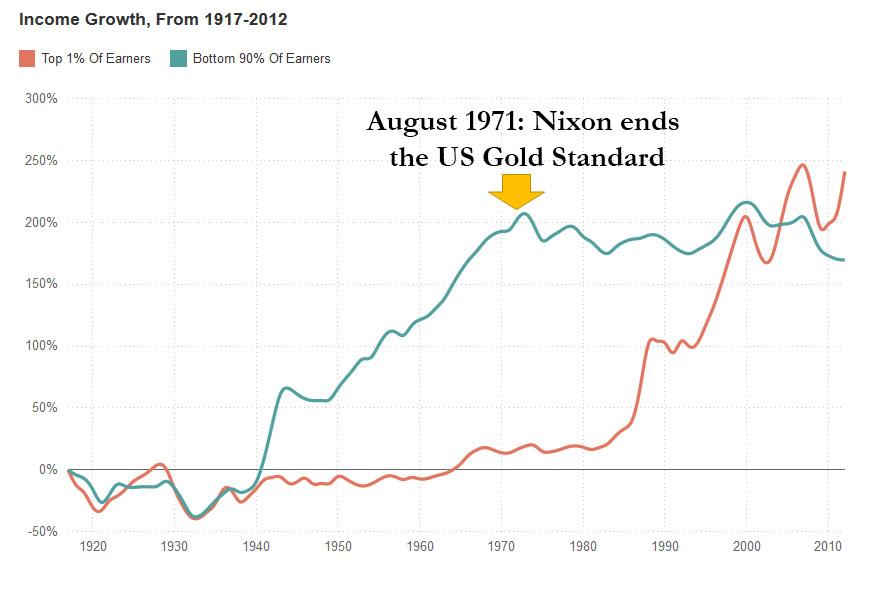

Incidentally, as we showed back in 2015, the end of the US gold standard in 1971 in addition to permitting ever longer economic cycles (at the expense of record debt), also marked the moment when the US middle class stopped growing, as the income of 90% of the US population ended its ascent, while unleashing a golden age for the US “top 1%”, whose asset holdings exploded in “value” at the time the USD was delinked from gold. Which, incidentally, is the solution to the nationalist problem in every developed nation – if you want the middle class to return, and income for the vast majority of the population to increase, all that has to happen is for the gold standard to return. Of course, since that means crippling the wealth of the top 1%, it will never happen.

Obviously the start of this new era (the 1970s), in which fiat currencies emerged as ties to gold were broken, saw great economic challenges with high inflation and the oil shocks ensuring that managing the business cycle was still very difficult. Nevertheless, as DB’s Jim Reid notes, it was interesting that the first full cycle of the post Bretton Woods era starting in 1975 ended up being the third longest on record at the time (out of 29), behind only the 1938- WWII rearmament cycle and 1961- Fed policy error cycle.

What about the Fed?

The next chart shows the Fed Funds rate over the last century with recessions marked. In the Post WWII period, the interesting thing is that there have been two long rate ‘super-cycles’. The first extended from the end of the War until the early 1980s and saw rates structurally head higher across multiple cycles. During this period there were regular recessions with only the 1960s cycle an extended one due to what is now widely believed to be a policy error from the Fed as they failed to hike rates fast enough to control inflation. Rates eventually peaked just before the start of the long cycle era and since then they’ve been on a near four decade reversal of the 1945-1982 trend. So in the former period the Fed was in a long hiking super cycle which would have helped contribute to multiple recessions in that period. The opposite was true post 1982 where the structural ability to cut rates must have elongated cycles that might have otherwise been prone to roll over. This, as Deutsche Bank notes, undoubtedly played a part in the move from short to long cycles.

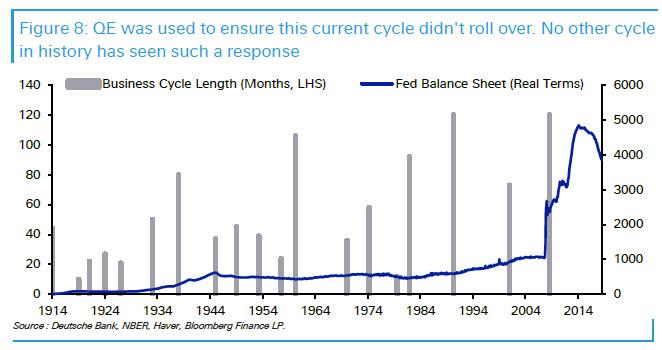

All of this worked great… until the Lehman failure and the global financial crisis unleashed a deflationary shockwave across the globe.

After an economic golden age for the global economy between 1982 and 2008, the Global Financial Crisis was then a huge threat to the era of long business cycles as it exposed the debt fuelled super-cycle that this policy flexibility encouraged. Allowing a great global debt restructuring that may have naturally occurred as a consequence would have restrained the flexibility of governments and central bankers to manage the business cycle and we could have quickly moved to a world of shorter cycles again. Being at the zero rate bound for the first time in history in many countries

(including the US) compounded the risks. However, as Jim Reid observes “global debt has continued to increase post the GFC and central banks found new weapons – namely QE and negative rates – to ensure that the economies could continue to grow over a period where left to their own devices we may have experienced a more sober economic environment and shorter cycles.”

As such, the US now is on the brink of its longest business cycle on record, continuing the trend of long cycles seen over the last 35-40 years

How long will US business cycles be in the future?

With the last four super-long US cycles attributed to globalisation, demographics, downward wage pressures, positive global disinflation, fiat money, increased debt/deficits, and QE, then the answer will come from answers as to how sustainable these trends are.

We’ll skip demographics and globalization as these are slower-acting, tectonic shifts, and focus on topics that are as salient today as ever – especially with another debt ceiling fight looming in D.C. With regards to debt and deficits, if anything the US has moved into an era of higher structural deficits and higher government debt, according to DB. Figure 10 extends the earlier charts to show CBO forecasts for both alongside business cycle lengths historically. Here the conclusion is simple: if the US can maintain such consistent deficits then perhaps it can continue to have long business cycles. Most market participants would likely say that such an increase in debt is not sustainable longer term but it could of course be sustainable for this and the next business cycle.

Similarly, the era of fiat money won’t be under terminal threat until there is sustained inflation – and not just the hyperinflation recorded in asset prices which the US government and Fed, for some reason, continue to ignore. As such central banks will still have money printing and balance sheet expansion in their armoury. Linked into debt and deficits, going forward QE may be used to finance specific government spending more than it has over the last decade where it was used to buy financial assets – particularly government bonds. So this could extend business cycles in the future and is again only likely to be more troublesome for the business cycle length when inflation rises.

So to conclude, retreating globalisation and weakening demographics are more negative for business cycle length going forward. However, while we are still able to run large deficits, accumulate more debt, and conduct more money printing we can still manipulate the length of cycles relative to the past. Maybe inflation is the glue here. Once that starts to structurally increase, business cycle management becomes more challenging.

How does this cycle compare to the past

Now that we know how we got here, and to mark the occasion that in just a few hours this will be the longest US cycle on record, let’s take a look at how this cycle compares to previous US cycles through history. Where Deutsche Bank has data, it stretches back to the start of US business cycle tracking in 1854, covering 34 expansions. Where data is missing, the analysis uses yearly data and start the cycle from the beginning of the year in which the recovery started. The titles indicate the periods covered in the graphs.

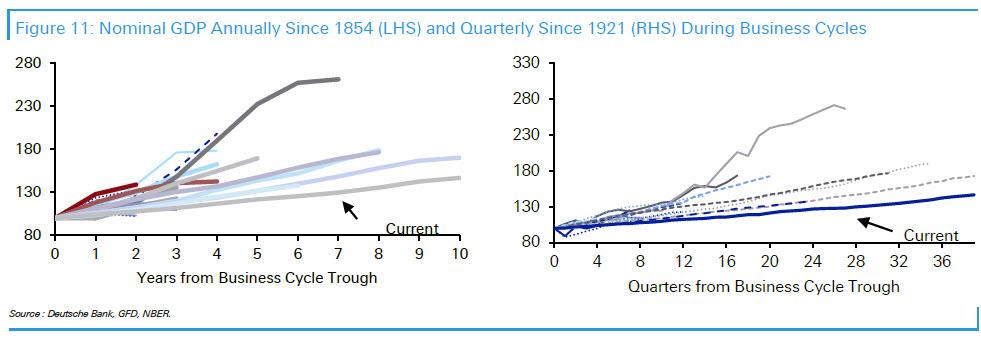

First we look at nominal GDP. As can be seen from the annual data back to 1854 or the quarterly data starting in 1921, this current cycle has seen the lowest growth at all stages of all the 18 cycles that have lasted more than three years. In fact, that might have helped encourage its longevity as economic activity has not got overly ahead of itself. It took until around 2018 for the output gap from the GFC recession to close and as such we were still in ‘catch-up’ mode for most of it.

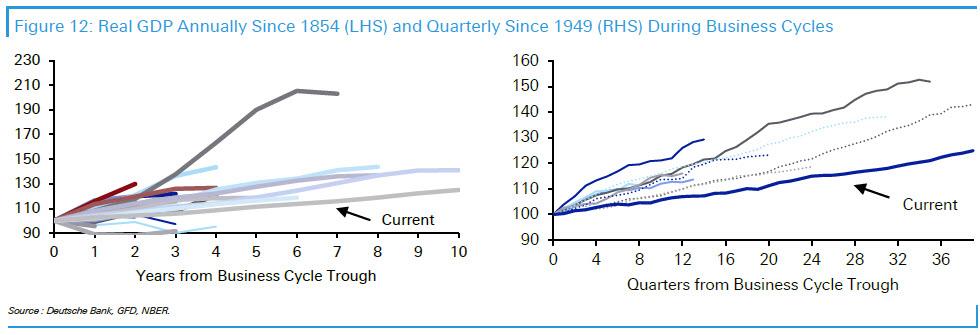

A similar picture emerges in real GDP terms. Using the full annual data series, this is the shallowest recovery of all the 11 that have extended past 4 years. In the quarterly data post 1949, this cycle has been the weakest of any of the 11 expansions at all points through their respective cycles. So perhaps the policy breaks have not been needed to be applied by the authorities in the same manner as in virtually all previous cycles.

Given that population growth in this cycle has been the slowest of all the 34 cycles covered, low nominal and real GDP growth shouldn’t be a surprise. However one could also make the argument that low growth makes recessions more likely as the margin for error is reduced. As such, the longevity of this cycle becomes even more impressive.

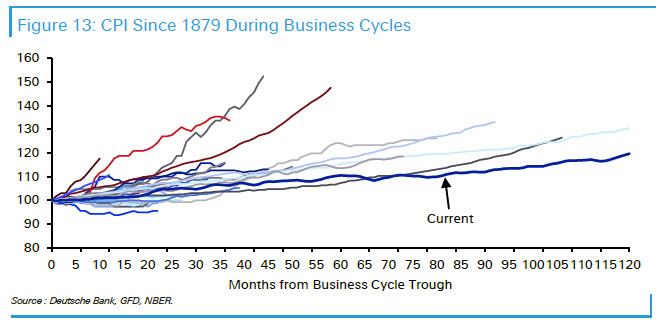

Next, moving to what may be the most critical metric for modern economists – inflation. The early cycles observed covered a period where inflation was structurally much lower. So in this respect, this current expansion looks less extreme on the downside than it does on the growth front. However the impressive element to this cycle is how steady inflation has been throughout. Indeed prices are only up 18.5% over the now 10-year expansion. This has allowed the Fed to maintain an accommodative policy stance for as long as they have and has helped extend the cycle beyond any other.

At the same time, the decline in unemployment doesn’t look particularly unusual in this cycle relative to the past but the key takeaway from this graph is that recessions tend to start with unemployment still trending down or at least flat lining. It also proves the point that employment is a lagging indicator.

Looking at capital markets reveals an entirely different story.

In terms of equities, this cycle has always been at the upper end of those seen through the entire history back to 1854. As we go past the 1991 expansion – that was previously the longest on record – returns on the S&P 500 are similar to that remarkable cycle which ended with the 2000 stock market bubble bursting. In that cycle, the graph highlights that the equity market peaked in March 2000 before the eventual recession was deemed to have begun in March 2001.

As Deutsche Bank concludes, it’s an interesting paradox that this cycle has consistently been one of the weakest in terms of economic growth but one of the strongest in terms of asset price growth. It also hints at the extraordinary lengths global authorities have gone to ensure this recovery continued. Liquidity and intervention has been enormous and this has flowed into assets, not the economy.

So as we celebrate the longest US expansion in history, and the fourth ultra long cycle in a row, the only question worth pondering is what the costs of what as of July 1 will be the longest cycle in history, will end up being?

via ZeroHedge News https://ift.tt/2LujCf4 Tyler Durden

She is the only candidate who has made ending the wars a centerpiece of her campaign, which will likely lead to her undoing…

Democrats, liberals, progressives – call them what you will – don’t really do foreign policy. Sure, if cornered, they’ll spout a few choice talking points, and probably find a way to make them all about bashing President Donald Trump—ignoring the uncomfortable fact that their very own Barack Obama led and expanded America’s countless wars for eight long years.

This was ever so apparent in the first two nights of Democratic primary debates this week. Foreign policy hardly registered for these candidates with one noteworthy exception: Hawaii Representative Tulsi Gabbard—herself an (anti-war) combat veteran and army officer.

Now primary debates are more show than substance; this has long been the case. Still, to watch the first night’s Democratic primary debates, it was possible to forget that the United States remains mired in several air and ground wars from West Africa to Central Asia. In a two-hour long debate, with 10 would-be nominees plus the moderators, the word Afghanistan was uttered just nine times—you know, once for every two years American troops have been killing and dying there. Iraq was uttered just twice—both times by Gabbard. Syria, where Americans have died and still fight, was mentioned not once. Yemen, the world’s worst humanitarian disaster, courtesy of a U.S.-supported Saudi terror campaign didn’t get mentioned a single time, either.

Night two was mostly worse! Afghanistan was uttered just three times, and there was no question specifically related to the war. Biden did say, in passing, that he doesn’t think there should be “combat troops” in Afghanistan—but notice the qualifier “combat.” That’s a cop-out that allows him to keep advisers and “support” troops in the country indefinitely. These are the games most Democrats play. And by the way, all those supposedly non-combat troops, well, they can and do get killed too.

The only bright spot in the second debate was Senator Bernie Sanders’s single mention of the word Yemen—specifically ending U.S. support for that war and shifting war powers back where they belong—with Congress. Still, most of the candidates had just about nothing to say on this or other war-related topics. Their silence was instructive.

Ironically, then, two more American soldiers were killed in another meaningless firefight in the long meaningless war in Afghanistan on the day of the first Democratic presidential primary debate. Indeed, were it not for this horrendous event—the deaths of the 3,550th and 3,551st coalition troops in an 18-year-old war—Afghanistan might not have ever made it onto Rachel Maddow’s debate questions list.

I mourn each and every service-member’s death in that unwinnable war; to say nothing of the far more numerous Afghan civilian fatalities. Still, in a macabre sort of way, I was glad the topic came up, even under such dismal circumstances. After all, Maddow’s question on the first night was one of precious few posed on the subject of foreign policy at all. Moreover, it spurred the most interesting, engaging, and enlightening exchange of either evening—between Gabbard and Ohio Representative Tim Ryan.

Reminding the audience of the recent troop deaths in the country, Maddow asked Ryan, “Why isn’t [the Afghanistan war] over? Why can’t presidents of very different parties and very different temperaments get us out of there? And how could you?” Ryan had a ready, if wholly conventional and obtuse, answer:

“The lesson” of these many years of wars is clear, he opined; the United States must stay “engaged,” “completely engaged,” in fact, even if “no one likes” it and it’s “tedious.”

I heard this, vomited a bit into my mouth, and thought “spare me!”

Ryan’s platitudes didn’t answer the question, for starters, and hardly engaged with American goals, interests, exit strategies, or a basic cost-benefit analysis in the war. In the space of a single sentence, Ryan proved himself just another neoliberal militarist, you know, the “reluctant” Democratic imperialist type. He made it clear he’s Hilary Clinton, Joe Biden, and Chuck Schumer rolled into one, except instead of cynically voting for the 2003 Iraq war, he was defending an off-the-rails Afghanistan war in its 18th year.

Gabbard pounced, and delivered the finest foreign policy screed of the night. And more power to her. Interrupting Ryan, she poignantly asked:

Is that what you will tell the parents of those two soldiers who were just killed in Afghanistan?

Well, we just have to be engaged?

As a soldier, I will tell you that answer is unacceptable. We have to bring our troops home from Afghanistan…

We have spent so much money. Money that’s coming out of every one of our pockets…

We are no better off in Afghanistan today than we were when this war began. This is why it is so important to have a president — commander in chief who knows the cost of war and is ready to do the job on day one.

In a few tight sentences, Gabbard distilled decades’ worth of antiwar critique and summarized what I’ve been writing for years—only I’ve killed many trees composing more than 20,000 words on the topic. The brevity of her terse comment, coupled with her unique platform as a veteran, only added to its power. Bravo, Tulsi, bravo!

Ryan was visibly shaken and felt compelled to retort with a standard series of worn out tropes. And Gabbard was ready for each one, almost as though she’d heard them all before (and probably has). The U.S. military has to stay, Ryan pleaded, because: “if the United States isn’t engaged the Taliban will grow and they will have bigger, bolder terrorist acts.” Gabbard cut him right off. “The Taliban was there long before we came in. They’ll be there long [after] we leave,” she thundered.

But because we didn’t “squash them,” before 9/11 Ryan complained, “they started flying planes into our buildings.” This, of course, is the recycled and easily refuted safe haven myth—the notion that the Taliban would again host transnational terrorists the moment our paltry 14,500 troops head back to Milwaukee. It’s ridiculous. There’s no evidence to support this desperate claim and it fails to explain why the United States doesn’t station several thousand troops in the dozensof global locales with a more serious al-Qaeda or ISIS presence than Afghanistan does. Gabbard would have none of it. “The Taliban didn’t attack us on 9/11,” she reminded Ryan, “al-Qaeda did.” It’s an important distinction, lost on mainstream interventionist Democrats and Republicans alike.

Ryan couldn’t possibly open his mind to such complexity, nuance, and, ultimately, realism. He clearly worships at the temple of war inertia; his worldview hostage to the absurd notion that the U.S. military has little choice but to fight everywhere, anywhere, because, well, that’s what it’s always done. Which leads us to what should be an obvious conclusion: Ryan, and all who think like him, should be immediately disqualified by true progressives and libertarians alike. His time has past. Ryan and his ilk have left a scorched region and a shaken American republic for the rest of us.

Still, there was one more interesting query for the first night’s candidates. What is the greatest geopolitical threat to the United States today, asked Maddow. All 10 Democratic hopefuls took a crack at it, though almost none followed directions and kept their answers to a single word or phrase. For the most part, the answers were ridiculous, outdated, or elementary, spanning Russia, China, even Trump. But none of the debaters listed terrorism as the biggest threat—a huge sea change from answers that candidates undoubtedly would have given just four or eight years ago.

Which begs the question: why, if terrorism isn’t the priority, do far too many of these presidential aspirants seem willing to continue America’s fruitless, forever fight for the Greater Middle East? It’s a mystery, partly explained by the overwhelming power of the America’s military-industrial-congressional-media complex. Good old President Dwight D. Eisenhower is rolling in his grave, I assure you.

Gabbard, shamefully, is the only one among an absurdly large field of candidates who has put foreign policy, specifically ending the forever wars, at the top of her presidential campaign agenda. Well, unlike just about all of her opponents, she didfight in those very conflicts. The pity is that with an electorate so utterly apathetic about war, her priorities, while noble, might just doom her campaign before it even really starts. That’s instructive, if pitiful.

I, too, served in a series of unwinnable, unnecessary, unethical wars. Like her, I’ve chosen to publicly dissent in not just strategic, but in moral, language. I join her in her rejection of U.S. militarism, imperialism, and the flimsy justifications for the Afghanistan war—America’s longest war in its history.

As for the other candidates, when one of them (likely) wins, let’s hope they are prepared the question Tulsi so powerfully posed to Ryan: what will they tell the parents of the next soldier that dies in America’s hopeless Afghanistan war?

via ZeroHedge News https://ift.tt/2RHm0jy Tyler Durden

Hours after Israeli reports said Russian S-300 anti-air defense systems in Syria came online and were “operational,” the Israeli military allegedly launched a major aerial attack on Syria in the middle of the night Sunday.

Massive explosions rocked Damascus overnight, via Al-Masdar News

Syria said Israeli jets attacked several military sites near the capital Damascus and the central city of Homs early Monday, killing several people.

State news agency SANA said that Syrian air defense had intercepted several of the incoming missiles that were fired from Lebanese airspace.

Syria reported its aerial defense systems were active during the assault, which further caused damage to multiple civilian homes in the Damascus suburb of Sahnaya, according to SANA.

The major Syrian military airport at Mezzeh on the western edge of Damascus was also a reported target in the attack.

Though total casualties are still unknown, one well-known journalist from Damascus, Danny Makki, is reportingat least 4 civilians killed — including a baby — and over 20 injured.

Syrian state media published footage showing missile intercepts of inbound projectiles.

It is also as yet unknown if the S-300s were active during the air strikes, however, Israeli media reports suggested both the newly installed S-300s as well as Iranian troop presence was a prime cause behind the Israeli action, despite the Israeli Defense Forces (IDF) neither confirming nor denying the strikes:

The reported strikes came just hours after an Israeli satellite imagery analysis company said Syria’s entire S-300 air defense system appeared to be operational, indicating a greater threat to Israel’s ability to conduct airstrikes against Iranian and pro-Iranian forces in the country.

Until now, only three of the country’s four surface-to-air missile launchers had been seen fully erected at the Masyaf base in northwestern Syria.

Journalist Danny Makki called the overnight air strikes “certainly one of the biggest Israeli attacks on Syria this year” – given that two provinces were targeted as well as multiple installations and a civilian neighborhood being hit.

Really hard to portray these attacks on #Syria as purely #Israel vs #Iran when most of the people killed or wounded are Syrian soldiers or on some occasions civilians.

Australia is continuing down the path of the global low yield charge, about to approach its final percentage point of “interest rate ammunition”, according to Bloomberg.

The 10 year yield in Australia hit an all time low of 1.26% last week, which is more than a full percentage point under where they started the year. This means that every Australian bond – all the way out to the longest maturity in 2047 – is yielding less than the bottom of the central bank’s 2% to 3% inflation target.

And the speed with which the market environment is changing in Australia is catching the attention of many.

Richard Yetsenga, chief economist at Australia & New Zealand Banking Group Ltd. in Sydney said: “On the screen a minute ago, Aussie 10-year bond yields at 1.33? I mean, is that a typo? Even six months ago they were like 100 points higher.”

Additionally, the market is now pricing in an even chance that the Reserve Bank of Australia will cut its policy rate to 0.5% over the next year. Governor Philip Lowe will cut the cash rate by 25 bps on Tuesday, to 1%, according to 18 of 26 economists surveyed.

Sally Auld, a senior interest-rate strategist at JPMorgan Chase & Co. in Sydney said: “There is a sense of inevitability about where we are heading. We’ve seen this play out in a number of other big developed economies over the last decade. Rates have come all the way down to something close to zero, and they stay there for a very long time.”

The cash rate at 0.5% means that bank earnings could slide 15%, hurting the largest component of the country’s equity markets. Companies like annuities provider Challenger Ltd. have already felt the brunt of the lower rates, falling about 30% this year and citing “lower for longer” rates as the problem.

And Governor Lowe has telegraphed that he is open to further cuts, with Australia’s job market lagging full employment. Like the U.S., Australia is also concerned with “putting inflation on course”. Lowe says that QE right now is “really quite unlikely”, but with how things have been going, we wouldn’t be surprised to see that stance reversed fully within a matter of just months.

Rates at 1% have been what has prompted other unorthodox steps across the globe from the Federal Reserve and the Bank of England. Lowe has said that Australia’s lower level is at about 0.25% to 0.5%.

Paul Sheard, a senior fellow at Harvard University’s Kennedy School said:

“The potent policy then becomes monetary policy supporting fiscal policy”. It’s a more pragmatic kind of approach in Australia when it comes to cooperation among policy makers.”

While it is seen as a positive that a lower cash rate could flow quickly to households with floating rate mortgages, Australia finds itself again staving off a problem temporarily that will eventually and inevitably lead to a far worse, longer term problem. But as long as economists and central bankers fail to realize this, we can expect Australia, along with its central banking peers across the globe, to be doomed to repeat history – just an order of magnitude worse than the last crash.

via ZeroHedge News https://ift.tt/2xnftRM Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}