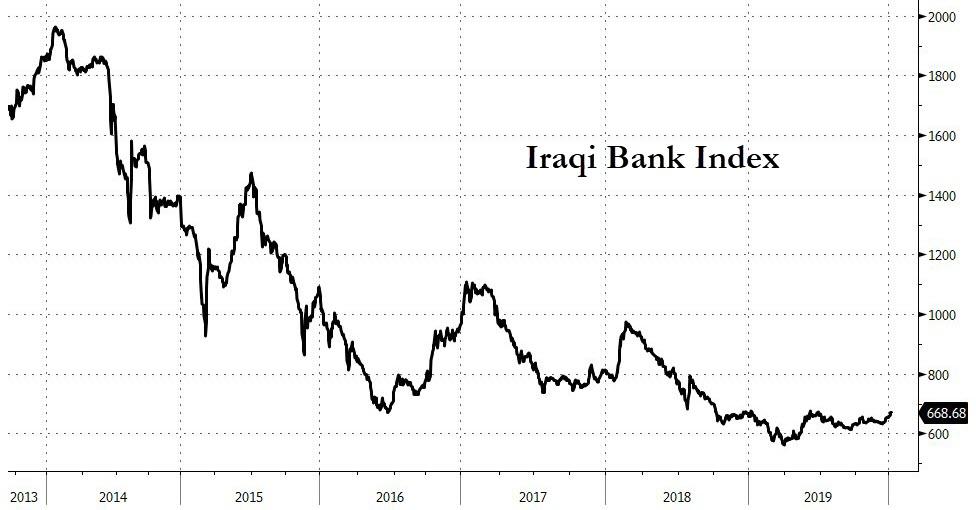

The Wall Street Journal reports that according to Iraqi officials (yes, Iraq has anonymous sources too), the Trump administration warned Iraq this week that it risks losing access to a critical government bank account if Baghdad kicks out American forces.

We are sure, to Schiff et al., that sounds a lot like ‘quid pro quo’, but how will they balance the need to hammer the president with their neocon/establishment desire to keep boots on the ground, whatever it takes?

The warning regarding the Iraqi central bank account was conveyed to Iraq’s prime minister in a call on Wednesday, according to an official in his office, that also touched on the overall military, political and financial partnership between the two countries.

When Iraq needs hard currency, its central bank can request a shipment of bills that it then distributes into the financial system through banks and currency exchange houses. While the country’s official currency is the dinar, U.S. dollars are commonly used.

“The U.S. Fed basically has a stranglehold on the entire [Iraqi] economy,” said Shwan Taha, chairman of Iraqi investment bank Rabee Securities.

The potential economic and financial fallout is weighing on Iraqi officials

“Whenever you have any amicable divorce, you still have the worry about the children, pets, furniture and plants, some of which are sentimental,” said a senior Iraqi politician.

The New York Fed, which can freeze accounts under U.S. sanctions law or if it has reasonable suspicion the funds could violate U.S. law, said it doesn’t comment on specific account holders, but as WSJ notes,this financial threat isn’t theoretical:

The country’s financial system was squeezed in 2015 when the U.S. suspended access for several weeks to the central bank’s account at the New York Fed over concerns the cash was filtering through a loosely regulated market into Iranian banks and to the Islamic State extremist group.

The New York Fed doesn’t publicly disclose how much money it currently holds for Iraq’s central bank. But according to the Central Bank of Iraq’s most recent financial statement, at the end of 2018, the Fed held nearly $3 billion in overnight deposits.

The last few years have seen the Iraqi banking system devastated…

An adviser to the prime minister, Abd al-Hassanein al-Hanein, said that while the threat was a concern, he did not expect the U.S. to go through with it.

“If the U.S. does that, it will lose Iraq forever,” he said.

Perhaps that is why Iraq has been building its de-dollarizing, gold reserves for the last few years…

So, after a year of desperately proclaiming that “The Fed is not political,” it turns out that, in fact, The Fed is extremely geopolitical – we look forward to hearing the Left defend The NY Fed’s “independent” decision to potentially cripple Iran’s entire financial system.

Low natural gas prices have finally brought the decade-long shale gas boom in Appalachia to a halt.

Gas production in Appalachia declined by about 1 billion cubic feet per day (Bcf/d) over the past 30 days, bringing output down to an average of 32.7 Bcf/d, according to S&P Global Platts Analytics. That helped drag down overall U.S. gas production to 91.8 Bcf/d, a 1.7 percent decline from 93.4 Bcf/d in November.

The Permian hogs a lot of attention in the press, but the Marcellus shale has been growing at a blistering rate for about a decade. That is now coming to an end as the shale gas industry struggles with oversupply and low prices, lack of profits, debt, investor skepticism and also competition from associated gas in the Permian.

Natural gas prices fell sharply last year, ending the year down more than 25 percent. The rig count in the Marcellus fell by 1 last week, dropping the total to 40. Eight months ago there were 65 rigs operating in the area.

Front-month gas contracts are trading at about $2.12/MMBtu, although at the wellhead prices can be much weaker. S&P said that prices at Dominion South, a hub in the Marcellus, have averaged just $1.78/MMBtu in the past month. S&P says that average breakeven prices are $1.80/MMBtu, but that likely understates the price level that drillers need, given the struggles that many have gone through.

“Gas prices are down. It has a big impact, the difference between $2.75 gas and $2.50 gas,” Toby Rice, EQT’s new president and CEO, told the West Virginian legislature in December “A lot of this development doesn’t work as well at $2.50 gas.”

An IEEFA analysis from last November found that seven of the largest producers in Appalachia spent nearly a half billion dollars more than they generated in the third quarter. With natural gas prices wallowing down close to $2/MMBtu, the cash burn rate may grow worse, unless the spending cuts continue.

Range Resources announced on January 6 that it would take an ax to its spending plans, cutting capex by 29 percent for 2020 compared to last year’s levels. The company also suspended its dividend, saving $20 million annually, so that it can allocate more money to paying off debt. Fortunately for Range, the company managed to hedge 60 percent of its output this year at an average price of $2.64/MMBtu.

Chevron recently announced a write down on the order of $11 billion for the fourth quarter, with its assets in Appalachia the principle cause.

The situation in the Appalachia is worse than for oil drillers in North Dakota, Colorado or Texas. To be sure, unconventional oil drilling is also riddled with financial problems and is based on a questionable business model. Oil wells still suffer from steep decline rates.

But the underlying commodity is faring better. That is, oil prices rose last year and gas prices declined. Moreover, while oil could just easily decline this year, it has better odds of an unexpected rally than gas does. In fact, the two commodities have been on “divergent paths,” as Reuters put it. The oil-to-gas price ratio recently hit 30:1, the highest ratio since 2013. Over the past five years, the ratio has averaged 19:1, but it really shot up in 2019 as oil and gas went in different directions.

There is little reason to think that they will converge this year. Speculators recently staked out bullish bets on oil (although that likely fell back after the U.S.-Iran de-escalation) and have increased bearish bets on gas.

“Speculative positioning in natural gas remains the most negative across the main metals, energy and agricultural futures market contracts,” Standard Chartered wrote in a note.

The other thing working against natural gas – and is a big problem for Appalachian gas drillers – is that associated gas production in the Permian is expected to continue to rise. Associate gas from the Permian now rivals that of the Marcellus, and crucially, output is not sensitive to price since it is not the primary objective of companies operating there.

It’s not clear if gas production in the Marcellus will continue to decline – analysts see it stabilizing – but at the very least, the drilling boom has come to an end.

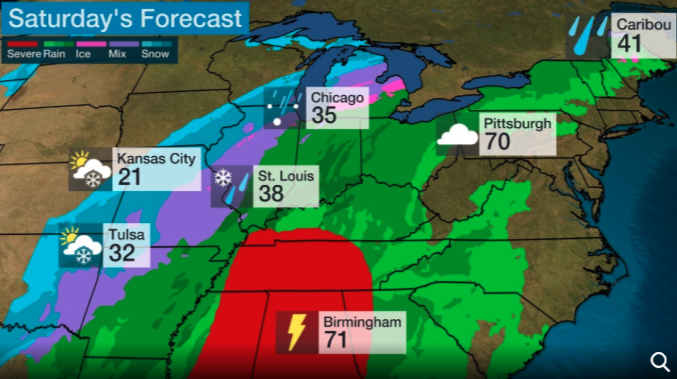

Millions Brace For Weekend Winter Storm Will Hit Plains, Great Lakes, And Northern New England

A powerful storm could bring dangerous winds, snow, and ice over the weekend to millions of people across the US.

The Weather Channel is calling the storm Winter Storm Isaiah and will dump snow and ice early Saturday in parts of Kansas, Oklahoma, northern Texas, and the Ozarks.

Heavy snow is expected to continue through Saturday for regions of Missouri to eastern Iowa, northwest Illinois, southern Wisconsin, and Lower Michigan.

Below the 32 degrees line, ice, freezing rain, and rain are expected for central Missouri into northern and western Illinois and Lower Michigan. A mix of wintery precipitation could be seen in parts of northern New England during the late day.

By the afternoon, Chicago and Milwaukee are expected to see rain transition to snow – this could cause headaches for motorists.

Snow is likely to continue in the Midwest through the nighttime.

Freezing rain should spread into upstate New York and northern New England and continue in Lower Michigan through the overnight.

High winds are expected for Plains and Midwest on Saturday. This could cause blizzard conditions in some areas and lead to blowing and drifting snow. Winds are expected to tick higher in the Mid-Atlantic and Northeast.

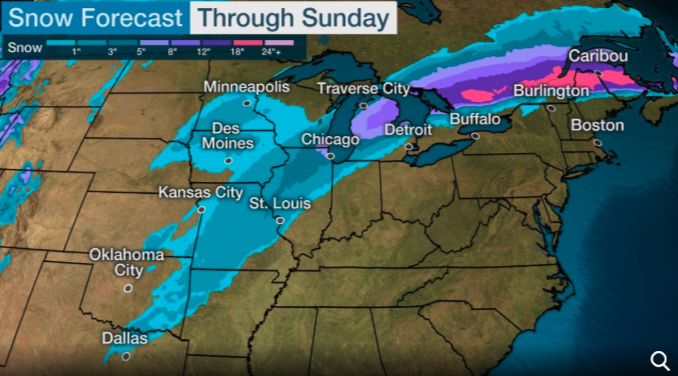

Wintery precipitation is expected to move out of the Plains and Midwest by early Sunday. Snow, sleet, and freezing rain will continue in upstate New York and northern New England through lunch.

The Northeast Interstate 95 corridor from New York to New England will see rain on Sunday.

The Weather Channel’s snow forecast through the weekend shows 1-3 inches for Central and Midwest states. About 6 inches for western Great Lakes and northern Maine.

“We can’t rule out some 6-inch snow accumulations as far south and west as parts of Missouri and eastern Kansas if heavy bands of snow set up there. Some spots from eastern Iowa into Michigan, as well as in northern Maine, could pick up more than a foot of snowfall,” The Weather Channel said.

Ice storms for parts of Oklahoma to Maine are also expected through Sunday night.

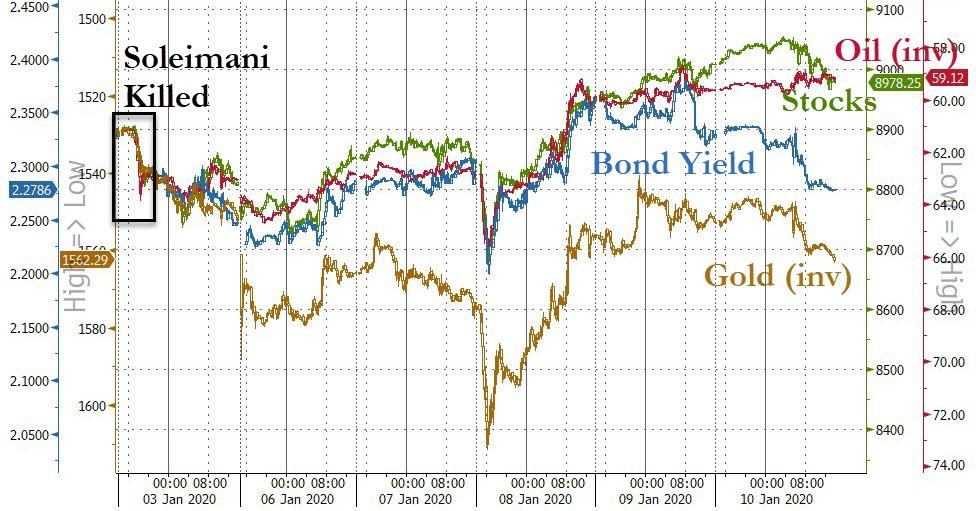

The procession of news through the week – namely that chronicling the aftermath of the targeted drone strike and killing of Iranian General Qasem Soleimani – advanced with an agreeable flow. The reports at the start of the week were that Orange Man Bad had spun up a Middle East mob of whirling dervishes beyond recall. World War III was imminent.

But after Iran’s token missile launch on Tuesday, with no American causalities, President Trump Tweeted: “All is well!”

Then, on Wednesday, major U.S. stock indices gave the “all clear” signal. By Thursday, the Dow Jones Industrial Average (DJIA), the S&P 500, and the NASDAQ were all marching to record highs. The DJIA even came within a horse’s hair from taking out 29,000.

What’s more, the price of crude oil fell below where it was before Soleimani was killed. No harm, no foul. What to make of it?

According to traders, everything is awesome. Still, we have some reservations. Our best guess is that this week’s agreeable flow of news will be followed by a disagreeable ebb. Conceivably, it marks the first paragraph of a new chapter in America’s forever war in the Middle East.

In the interim, however, we’ll consider the events of the last 10 days an experiment. Here, with little consequence (at least for now), we’ve been gifted a sampling of how financial markets behave when a burgeoning geopolitical crisis hits.

We posit that during the initial fog of a geopolitical crisis financial markets don’t have the faintest inkling of potential risk.

Hyperventilating Minds

Financial risk, for our purposes today, is not a quantified statistical measurement. We’re not concerned with the risk differential between high beta and low beta stocks. Rather, at the commencement of a major conflict, risk is specific to the probability of a foundational change resulting that permanently wipes away capital.

Author Fred Sheehan wrote a piece titled, “War of the Nerds,” for the December, 2006, edition of Marc Faber’s Gloom, Boom & Doom Report. Several years ago the article was still posted at Sheehan’s now defunct AuContrarian website. By chance, before the site vanished, we preserved the following excerpt:

“Every generation suffers its particular fantasies. So it was a century ago. Investors had grown so immune to the consequences of war that bond markets from London to Vienna didn’t flinch after the assassination that provoked World War I.

“Three weeks later, in the summer of 1914, the fear premium amounted to a total of one basis point. Then, in quick order, European markets ceased to function. A notable feature of this paralysis is that nothing of substance had changed – war had not been declared by any of the parties, but by now, minds were hyperventilating.”

Perhaps the motivation for the cerebral excitement was the rapid realization during the July 1914 Crisis that complex political alliances had turned the European continent into a giant Mexican standoff. The risk of a stock or bond market selloff was quickly overshadowed by the prospect of something much greater. That the diabolical self-annihilation of European society itself was, in fact, just moments away.

Geopolitical Shocks and Financial Markets

It would be wrong to draw close parallels between the geopolitical landscape in Europe circa 1914 and the Middle East circa 2020. This is not our intent. We’re merely citing this as an example of how quickly financial markets can go from full functioning to complete breakdown.

The question, again, is how financial markets behave when a burgeoning geopolitical crisis hits. The events of the last 10 days serves as our experimental test trial. Here’s a summary of our findings, albeit of a grim comparative nature…

As far as we can tell, bond markets are quick to dismiss the risk of a foundational change resulting in the permanent destruction of capital. For example, the yield on the 10 Year Treasury note briefly dipped below 1.8 percent on January 3 – the day of Soleimani’s death. Since then, the yield has walked back up to 1.85 percent, which is about where it was at the start of the year. This fear premium – as bond prices move inverse to yield – was next to nothing and transitory.

After a brief selloff, stocks, as noted above, were quick to recover and move to new highs. Defense sector stocks like, Lockheed Martin, were the real winners. On news of the Soleimani’s death they jumped upward. Then, in the aftermath, they continues to gain. Year-to-date, Lockheed Martin is up 6.56 percent.

Gold, while exhibiting more caution than Treasuries, has been moderately indifferent of potential risk. On January 2, the price of an ounce of gold was about $1,528. On January 3, it jumped to over $1,550 an ounce. Then, on January 7, gold nearly hit $1,600 an ounce.

But after President Trump Tweeted “All is well!” the price of an ounce of gold slid to just below $1,550 an ounce on January 9 – roughly $20 an ounce higher than before Soleimani’s death.

Geopolitical shocks, as we understand them, generally increase the demand for gold. A threat to stability, quite naturally, challenges the durability of fiat money. Those who see through the thin veneer of full faith and credit desire to hold more gold and less fiat.

Presently, gold, as opposed to stocks, Treasuries, and crude oil, is still holding some of the fear premium it added over the last 10 days. Make of it what you will…

Of course, there’s plenty that can go wrong out there these days – all is not well. Another dustup in the Middle East financed via the printing press, is certainly among them. Place your chips accordingly.

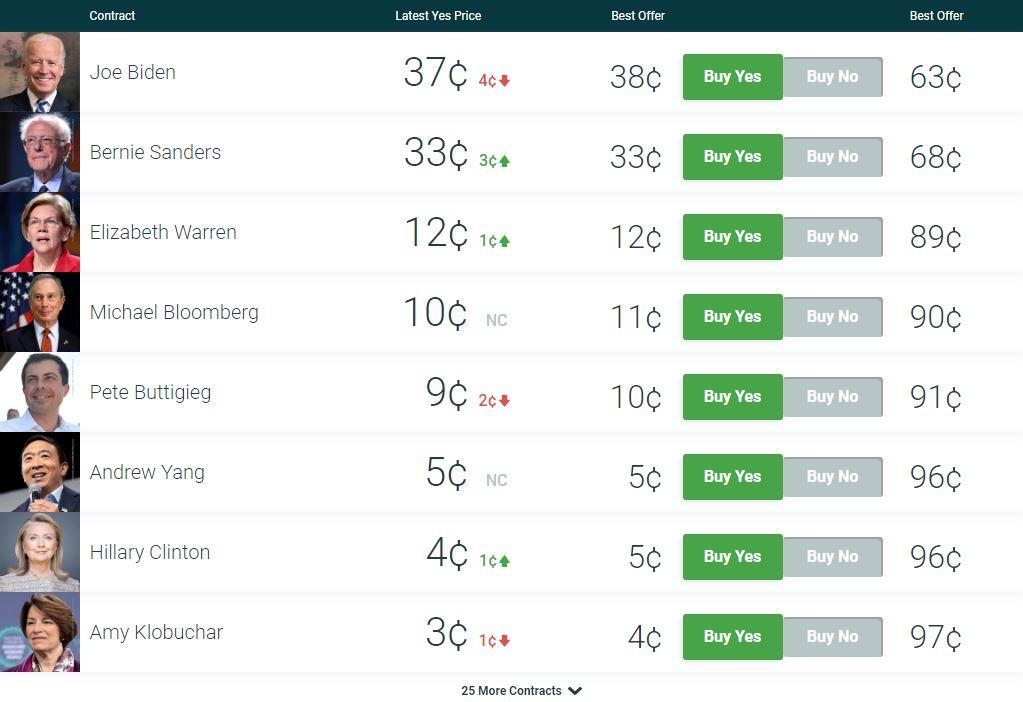

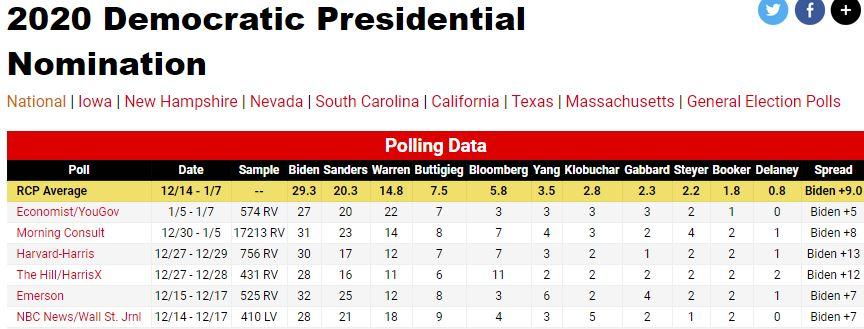

Bernie Sanders Takes The Lead In Iowa Just Weeks Before Caucus

All of those Bernie Sanders’ meme groups on Facebook are going to have something to celebrate over the weekend. Because according to the latest batch of polls, their candidate has retaken the lead in Iowa.

Per the latest Des Moines Register/CNN poll released on Friday, Sanders frog-leaped over his top rivals to secure the No. 1 spot, up from a No. 3 finish back in November.

The poll is widely seen as the most accurate and authoritative predictor of who will win the Iowa caucus, according to the Hill.

Though it’s probably just a coincidence, Sanders latest bump in the polls follows an endorsement from model/actress Emily Ratajkowski, best known for being Hollywood’s most visible proponent of ’empowered’ feminism (so long as it doesn’t come between her and booking another job).

“Bernie is extremely genuine. He’s consistent. He’s powerful, not because of who he is as one person, but because of the way he invigorates people and excites them, and brings together this movement.” –@emratapic.twitter.com/ZTD8jjHHCI

Meanwhile, since the mainstream press simply can’t tolerate the notion of Bernie Sanders nominee, Time Magazine has conveniently published the cover for this week’s edition. Unsurprisingly, it’s a hagiography of Nancy Pelosi.

But Dems weren’t the only ones upset by the poll results. Others speculated that a Trump vs. Sanders matchup in the fall would make them question whether America is still indeed worth saving.

If the two presidential nominees are Trump and Sanders – if that truly reflects what the two main parties stand for – then I honestly have to start asking the troubling question whether this country still has much of a future.

Sanders picked up 20% of support in the Iowa poll (up 5 percentage points from late last year), giving him a plurality, though not by much. Rival Senator Elizabeth Warren placed second with 17%, followed by former South Bend, Indiana, Mayor Pete Buttigieg in third with 16% (a drop of 9 percentage points from the previous poll by the same group).

Joe Biden, meanwhile, came in fourth with just 15%.

Iowa caucusgoers will cast their votes on Feb. 3 for the first-in-the-nation contest.

To be sure, the Iowa caucuses have a reputation for being difficult to forecast. But setting its esoteric system aside (a system that requires caucusgoers to show up on-location in the dead of winter and argue about who is the best candidate in a gymnasium full of strangers), only 40% of respondents said they are sure of their choice, which leaves a wide margin of undecided voters who could still sway the results in the coming weeks.

And there’s still the question of Sanders’ fragile health in the wake of a heart attack that gave many of his supporters reason to reconsider whether he is truly the right candidate to lead the country.

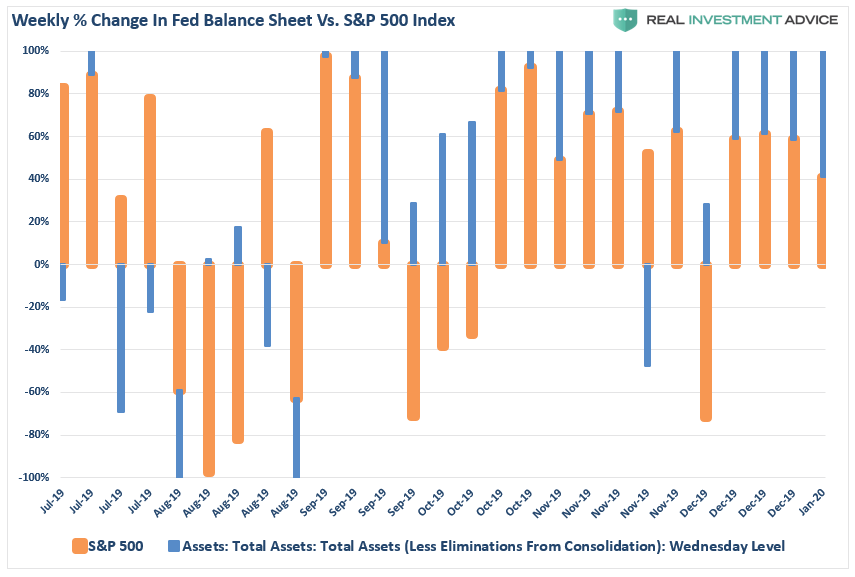

“That is the current mantra of the market as we begin 2020, and it certainly seems to be the right call. Over the last few months, the Federal Reserve has continued its ‘QE-Not QE’ operations, which has dramatically expanded its balance sheet. Many argue, rightly, the current monetary interventions by the Fed are technically ‘Not QE’ because they are purchasing Treasury Bills rather than longer-term Treasury Notes.

However, ‘Mr. Market’ doesn’t see it that way. As the old saying goes, ‘if it looks, walks, and quacks like a duck…it’s a duck.’”

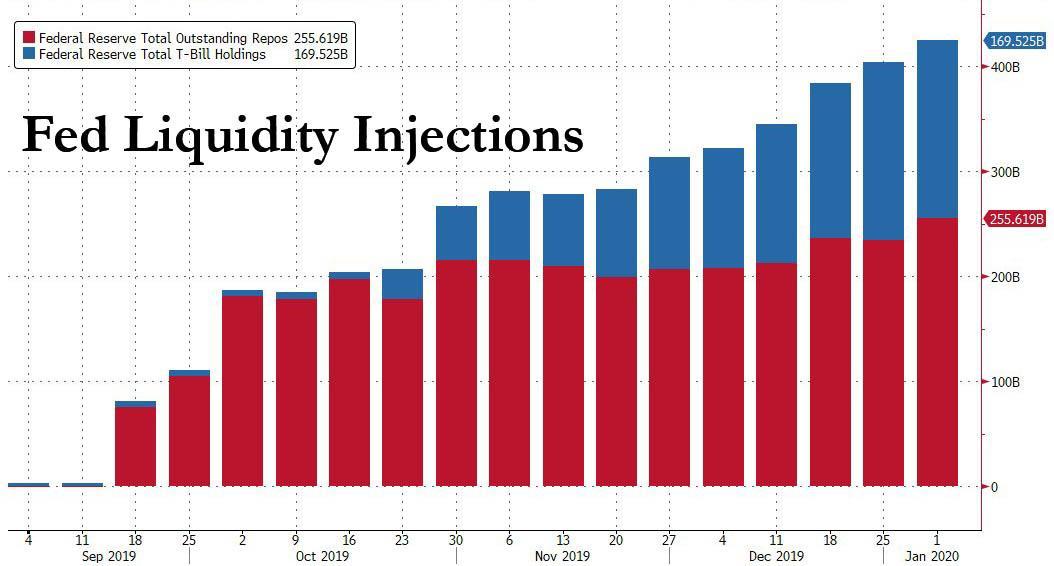

As we discussed, there is something “broken” in the financial system when it requires massive injections of capital to maintain sufficient liquidity. This was a point noted by Curvature Securities’ Scott Skyrm in his daily “Repo Market Commentary” via Zerohedge:

“Indeed, something appears amiss, because the total overnight and term Fed RP operations on Friday were greater than on year end! On year-end, the Fed had pumped a total of $255.95 billion into the market verses $258.9 billion on Friday.”

When these excessive “Repurchase Operations” initially began in late September, we were told they were to meet corporate tax payments. The issue with that excuse is that corporate tax payments come due every quarter and are easy to forecast weeks in advance. Why was last October’s payment period so different? But, following October 15th, the “repo” operations should have been no longer needed, however, the funding not only continued, but grew.

As the end of the year approached, we were told liquidity was needed to meet “the turn,” as 2019 ended, and 2020 began. Once again, this excuse falls short as, without exception, every year ends on December 31st. So, after nearly a decade of NO “repo” operations, as shown below, what is really going on?

What is clear, is the Fed may be trapped in their own process, a point made by Mark Cabana of BofAML:

“It seems implausible to me that the Fed will be able to stop their repo operations by the end of January.”

The Fed’s New Liquidity Trap

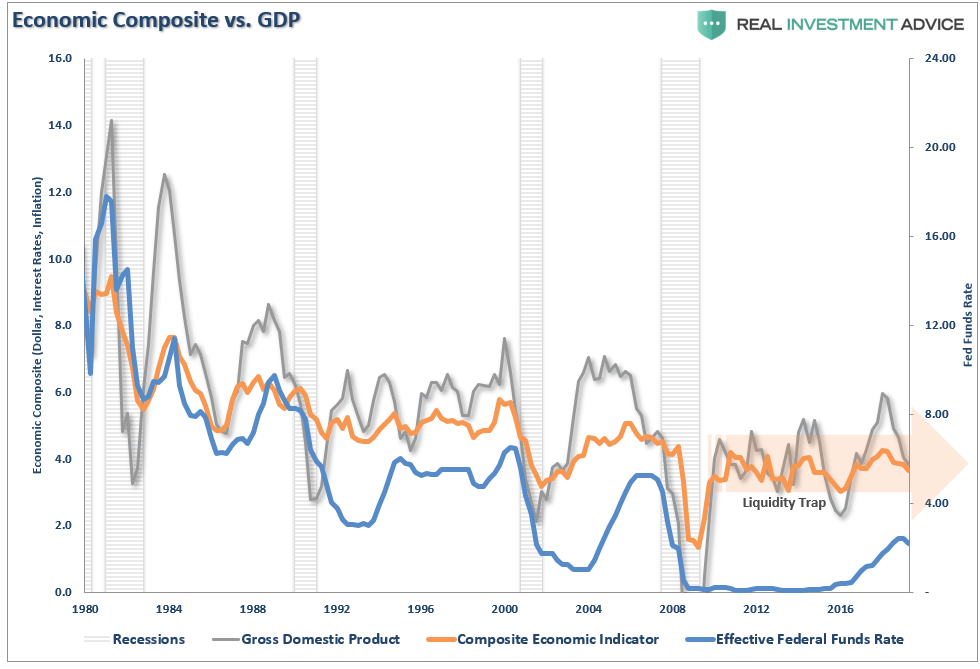

We previously discussed the“liquidity trap”the Fed has gotten themselves into, along with Japan, which will plague economic growth in the future. To wit:

“The signature characteristics of a liquidity trap are short-term interest rates that are near zero and fluctuations in the monetary base that fail to translate into fluctuations in general price levels.”

Our “economic composite” indicator is comprised of 10-year rates, inflation (CPI), wages, and the dollar index. Importantly, downturns in the composite index leads GDP.

The Fed’s problem is not only are they caught in an “economic liquidity trap,” where monetary policy has become ineffective in stimulating economic growth, but are also captive to a “market liquidity trap.”

As Mr. Skrym noted:

“The problem with the broken repo market, and the Fed’s respective Repo operations, is similar to the problem observed with QE, and the Fed’s balance sheet in general, over the past decade. The market has gotten addicted to the easy Fed liquidity.”

This can be seen in the chart below.

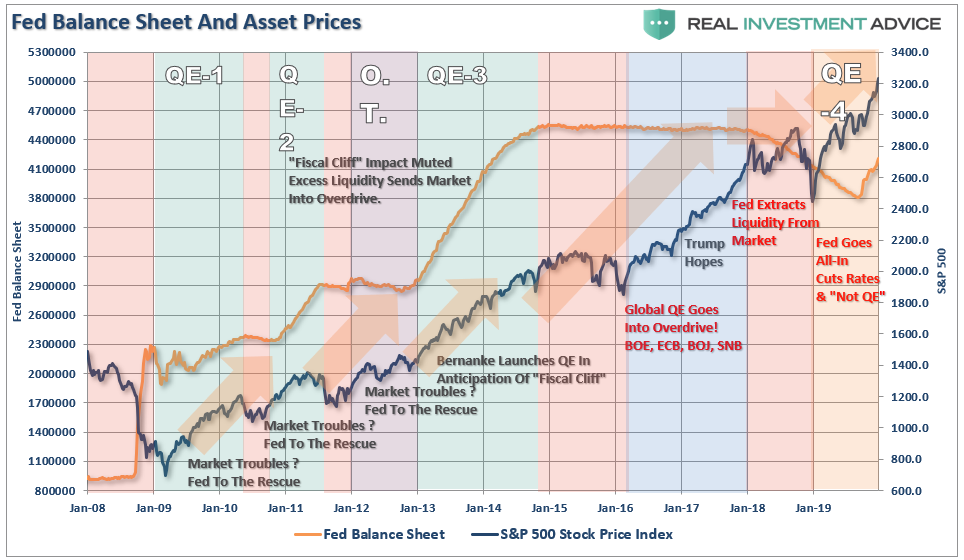

Whenever the Fed, or other Global Central Banks, have engaged in “accommodative monetary policy,” such as QE and rate cuts, asset prices have risen. However, as denoted by the “red” shaded areas, when those activities are not present, asset prices have declined.

In short, the market has become addicted to QE, and like any drug addict, when the drug was taken away in 2018, as the Fed hiked rates and reduced their balance sheet in an attempt to normalize policy, the market dropped by nearly 20%.

To understand why this is important we have to go back to what Ben Bernanke said in 2010 as he launched the second round of QE:

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

I highlight the last sentence because it is the most important. Consumer spending makes up roughly 70% of GDP, therefore increased consumer confidence is critical to keeping consumers in action. The problem is the economy is no longer a “productive” economy, but rather a “financial” one. A point made by Ellen Brown recently:

“The financialized economy – including stocks, corporate bonds and real estate – is now booming. Meanwhile, the bulk of the population struggles to meet daily expenses. The world’s 500 richest people got $12 trillion richer in 2019, while 45% of Americans have no savings, and nearly 70% could not come up with $1,000 in an emergency without borrowing.

Central bank policies intended to boost the real economy have had the effect only of boosting the financial economy. The policies’ stated purpose is to increase spending by increasing lending by banks, which are supposed to be the vehicles for liquidity to flow from the financial to the real economy. But this transmission mechanism isn’t working, because consumers are tapped out.”

If consumption retrenches, so does the economy.

When this happens debt defaults rise, the financial system reverts, and bad things happen economically.

For this reason the Federal Reserve has been engaged in an ongoing campaign to “avoid the pain” experienced during the financial crisis. This was a question asked of Janet Yellen during her semi-annual Humphrey-Hawkins testimony by Rep. Edward Royce. I am going to break this down for clarity.

“ROYCE: I’m worried that the Federal Reserve has created a third pillar of monetary policy, that of a stable and rising stock market. And I say that because then-Chairman Bernanke, when he appeared here, stated repeatedly that,‘the goal of QE was to increase asset prices like the stock market to create a wealth effect.’”

As stated, Ben Bernanke clearly states the goal of Q.E. was to increase asset prices. As Royce continues he clearly identifies the Fed’s “new liquidity trap:”

“ROYCE: That seems as though that was goal. It would stand to reason then that in deciding to raise rates and reduce the Fed’s QE balance sheet standing at a still record $4.5 trillion, one would have to be prepared to accept the opposite result, a declining stock market, and a slight deflation of the asset bubble that QE created.

Yet, every time in the past three years when there has been a hint of raising rates and the stock market has declined accordingly, the Fed has cited stock market volatility as one of the reasons to stay the course and hold rates at zero.

Read the last paragraph again.

Royce understands that in order to normalize monetary policy, and return markets to a more normal state of operation, some pain would have to be expected.

So, what was Yellen’s response.

YELLEN: It is not a third pillar of monetary policy. We DO NOT target the level of stock prices. That is not an appropriate thing for us to do.”

Yes, the Fed absolutely targets the financial markets with their policies. However, as Royce notes above, it will require a level of pain to wean the markets off of ongoing liquidity. In 2018, the Fed learned their lesson of what would happen as the small adjustment to monetary policy they did make resulted in a market decline of nearly 20%, yield curves inverted, and threats of a recession rose.

They aren’t willing to make that mistake again. The subsequent policy reversal pushed the markets to new record highs, which has been a function of valuation expansion due to the lack of improvement in underlying fundamentals and earnings.

The Inextricable Problem

The problem is that stopping the current “repo” operations is that it could well spark another “repo market crisis,” especially with $259 billion in liquidity pumped currently. Notably, that is even more than what was at year end to fulfill “the turn.”

The BIS recently explained why these operations lift asset prices.

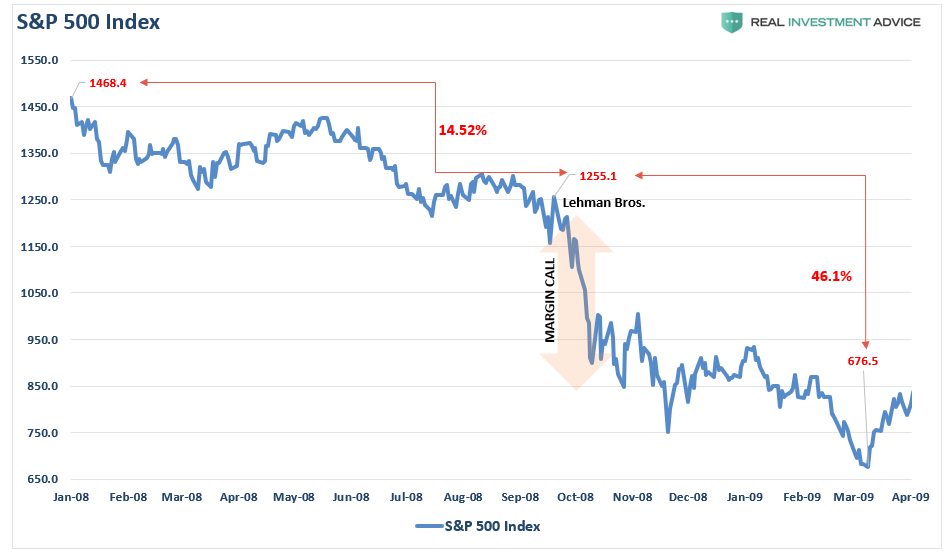

Repo markets redistribute liquidity between financial institutions: not only banks (as is the case with the federal funds market), but also insurance companies, asset managers, money market funds and other institutional investors. In so doing, they help other financial markets to function smoothly. Thus, any sustained disruption in this market, with daily turnover in the U.S. market of about $1 trillion, could quickly ripple through the financial system. The freezing-up of repo markets in late 2008 was one of the most damaging aspects of the Great Financial Crisis (GFC).

You really have to ask what is going on here. Wall Street veteran Caitlin Long provided a clue.

U.S. Treasuries are the most rehypothecated asset in financial markets, and the big banks know this. [They] are the core asset used by every financial institution to satisfy its capital and liquidity requirements, which means that no one really knows how big the hole is at a system-wide level.

This is the real reason why the repo market periodically seizes up. It’s akin to musical chairs – no one knows how many players will be without a chair until the music stops.

Hedge funds are the most heavily leveraged multi-strategy funds in the world, taking something like $20 billion to $30 billion in net assets under management and levering it up to $200 billion. As noted by The Financial Times:

“Some hedge funds take the Treasury security they have just bought and use it to secure cash loans in the repo market. They then use this fresh cash to increase the size of the trade, repeating the process over and over and ratcheting up the potential returns.”

So….it’s a hedge fund problem, right?

Probably.

“The repo-funded [arbitrage] was (ab)used by most multi-strat funds, and the Federal Reserve was suddenly facing multiple LTCM (Long-Term Capital Management) blow-ups which could have started an avalanche. Such would have resulted in trillions of assets being forcefully liquidated as a tsunami of margin calls hit the hedge funds world.”

Think “Lehman crisis” multiplied by a factor of four.

The Fed’s position is they must continue inflating a valuation bubble despite the inherent, and understood, risks of doing so. However, with no alternative to “emergency measures,” the Fed is trapped in their own process. The longer they continue their monetary interventions, the more impossible it becomes for the Fed to extricate itself without causing the crash they want to avoid.

Stated simply, the longer the Fed avoids normalizing monetary policy, and weaning the “crack addicted” markets off of their “liquidity drug,” the bigger the “reversion” will be “when,” not “if,” it occurs.

The only question is how much longer can Jerome Powell continue “pushing on a string.”

The Top 1% Are Much Happier & Content With Their Lives, Study Finds

Well, what do you know: It looks like money really can buy happiness.

For years, the conventional wisdom in American culture has been that the rich have their own set of issues that are under appreciated by the rest of the population. This was perhaps best summed up by rapper Biggie Smalls in his hit song “Mo’ Money, Mo’ Problems.”

But despite cultural taboos about high-paying, high-pressure jobs leading to substance abuse, divorce and familial ruin, one recent study found that the highest-earning Americans actually reported feeling both happier and more fulfilled on a day-to-day basis.

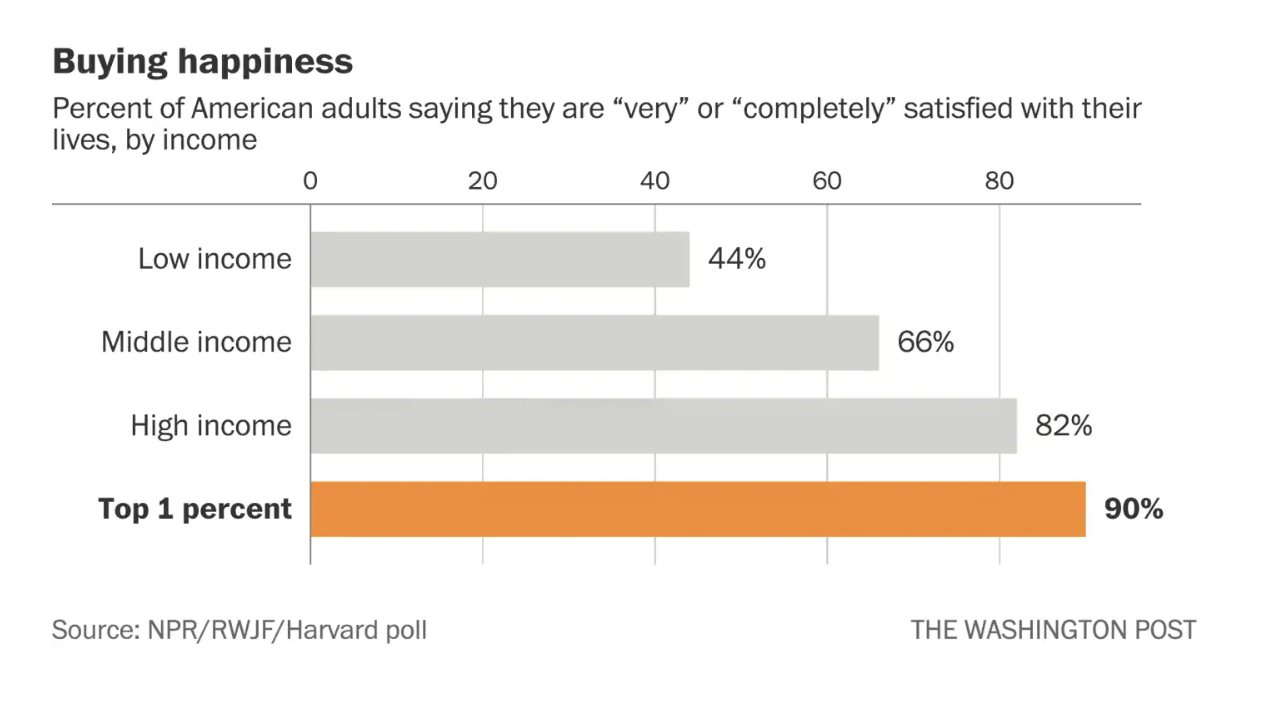

Here’s more on the study from The Washington Post: Adults in the top 1% of U.S. household income (i.e. those who earn at least $500,000 a year) have “dramatically different life experiences” than everyone else, according to a survey sponsored by NPR, the Robert Wood Johnson Foundation, and the Harvard T.H. Chan School of Public Health.

A full 90% of the 1% say they are “completely” or “very” satisfied with their lives in general. That compares with two-thirds of middle-income households – those earning $35,000 to $99,000 a year – and 44% of low-income households – ie those in the $35,000 a year or less bracket.

Even more impressive: The share of 1%-ers expressing “dissatisfaction” with their lives is statistically zero.

As WaPo explains, because the top 1% of US earners represents such a small subset of people, it’s typically difficult to gain insight into their thoughts and feelings via polling.

Previous studies showed that money makes a big difference in an individual’s level of happiness, but that the effect starts to weaken once an individual starts earning a little bit more than $75,000.

But apparently, as this latest study shows, although the rich might not be much happier on a day-to-day basis, individuals earning more than $500,000 a year are typically much more content with their lives.

Inside the top 1%, for example, some 97% say that they’ve already obtained the “American Dream”, as the respondent defines it, or are actively working toward it. Among low-income adults, by comparison, some 4 in 10 believe the American Dream is completely out of their reach.

A PC Specialist ad has been banned in the UK for perpetuating “harmful gender stereotypes” because it doesn’t feature any women.

Apparently, the commercial, which features a white man, a black man and an Asian man, isn’t diverse enough.

The UK’s Advertising Standards Authority cracked down on the ad after just eight offended morons complained.

Despite PC Specialist’s core market being 87.5% male, the fact that their commercial isn’t politically correct enough was its undoing.

As we previously highlighted, a Volkswagen commercial was also banned in the UK for violating “gender stereotypes” because it showed a woman caring for a baby.

The ASA also banned an ad featuring a sexy female mechanic after a single complaint because it could cause “offense” and was sexually suggestive.

Commercials that reinforce negative gender stereotypes against men, such as one about ‘manspreading’ that appear on the London Underground, are apparently fine.

There are also no restrictions on ads showcasing obese people, although commercials featuring slender women who work out are banned.

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Hours before Americans began raising champagne flutes and toasting the arrival of the New Year, the U.S. Food and Drug Administration (FDA) announced its final guidance for food-labeling regulations that manufacturers that must comply with.

The agency’s timing for the announcement, which centers on changes to the mandatory Nutrition Facts label that appears on virtually all packaged foods regulated by the FDA, wasn’t great. First, it makes the classic Friday news dump seem rather ostentatious, given the FDA released the guidance on New Year’s Eve eve. Food executives who were spending time with their families or in line at the liquor store probably missed the guidance—which appeared in the Federal Register on New Year’s Eve itself. Add to that the fact the regulations the FDA’s guidance is intended to explain took effect on January 1—mere hours after the agency released that guidance.

The timing has meant grocers such as Whole Foods and PCC (a co-op in Seattle, where I live) have been scrambling to explain the changes to their customers.

Still, though the timing of the guidance is inopportune, it would be unfair to characterize it as some sort of FDA “gotcha” targeting the food industry. The rules apply right now only to very large food producers—those with at least $10 million in annual food sales. What’s more, the agency is giving food manufacturers six months to come into compliance with the rules. And, according to the FDA Law Blog, last week’s agency guidance differs only slightly from an earlier draft guidance.

But the tardiness of the FDA’s guidance is hardly the only knock against the new rules. In fact, it’s not even among my chief complaints.

If the old “Nutrition Facts” label wasn’t great, then the revised label is hardly an improvement. Visually, it moves some things around and plays with fonts and bold text. As Today.com explains, the new label displays caloric information “in a larger font size[,] and the numbers will be bolder.”

Does a little bold text here and a slightly larger font matter? Probably not. A study I cite here found that only 9 percent of consumers read calorie counts on food labels.

My real complaints, though, concern the substance of the label itself.

For one thing, the “facts” the Nutrition Facts label rests upon might more properly be dubbed the Nutrition Opinions label. After all, the Nutrition Facts label reflects the opinions and recommendations of a federal panel of dietary and nutrition experts. As with the current revision—but unlike actual facts pertaining to human nutrition—that label changes from time to time. Perhaps most importantly, the dietary and nutrition experts’ recommendations, as I’ve explained, rests on shaky ground.

Much has been made of changes to the recommended serving sizes of various foods that appear on the Nutrition Fact label. While serving sizes that reflect the quantities a person actually eats in one sitting make sense logically—a serving size of ice cream, for example, jumped under the new rules from a paltry half cup to a more robust three-quarters of a cup—I’m not sure if the new label requirements add any clarity here. After all, these numbers are averages at best. What’s more, the agency’s new reference amounts for breakfast cereals, for example, suggest a serving size of 20 grams for children ages 1-3 but anywhere between 15 grams and 60 grams for adults.

I’m not sure that makes sense. Then again, this is the same agency that issued a 36-page guidance document in 2018 that contains the words “Serving Size for Breath Mints” in its title.

Finally, some supporters of the revised labels argue that the push to list “added sugar” on the Nutrition Facts label will lead food manufacturers to reduce the amount of sugar they add to foods—in response to consumer demands spurred by the revised label.

It might do that. (Consumers were already angling to consume less sugar before the label change.) But the label will most definitely mislead and confuse consumers greatly. That’s because the “added sugar” requirement, I wrote in 2016, “creates a deceptive health halo around products like orange juice and apple juice, which are high in naturally occurring sugar but [often] contain no added sugar.”

According to the FDA, the new Nutrition Facts label is intended to help consumers make more informed choices and to combat obesity and heart disease. That’s a pipe dream. A 2012 study by E.U. researchers found “no real-life evidence exists linking nutrition label use with measured changes in body weight.” Instead, the authors determined that “price, taste, convenience, and shopping habits are simply far more important than nutrition information when making food purchasing decisions.“

Ultimately, the very small subset of eaters who focus on the minutiae of nutrition data on food labels may be the only ones excited by or capitalizing on them. Years from now, when those same people propose yet another revision to the Nutrition Facts label—this time we’ll get it right—please greet them with the skepticism they deserve.

from Latest – Reason.com https://ift.tt/2tO0Pok

via IFTTT

How Google Quietly Amassed A Real-Estate Empire In Manhattan

After dramatically dropping plans to move part of the company’s HQ2 to the Queens’ neighborhood of Long Island City, Amazon was recently exposed for expanding its headcount in Manhattan by leasing more office space in Hudson Yards – without any financial incentives from the city or state that prompted leftists like AOC to scuttle a deal that would have brought some 25,000 jobs to her district and the surrounding area.

Weeks later, WSJ revealed that, on top of the $3 billion in tax incentive and grants initially offered by NYC and New York State to Amazon, they also offered the e-commerce giant another $800 million in incentives, helping to reignite leftists’ rage.

Amazon’s tech-behemoth rivals were eerily quiet during Amazon’s battle with a coterie of progressive New York lawmakers who eventually triumphed by driving Amazon to scrap its plans to significantly expand its operations in the city. And in a report published Friday, Bloomberg offers some clues as to why.

While Amazon engaged in an extremely public hunt for the location of its HQ2 in a transparent attempt to extract the best deal possible from whatever municipality would eventually play host to its offices and workers, Google parent Alphabet has been quietly expanding its presence in Manhattan, amassing what some experts have described as a mini-real estate empire centered around its campus at Chelsea Market.

Per BBG, Google has more than 8,000 employees in New York across several buildings, and as the company continues to expand under the leadership of Sundar Pichai, the company could surpass 14,000 by 2028.

To help entrench its presence, the company bought Chelsea Market and a building across 15th Street for a total of about $3 billion a few years pack (after leasing space in those buildings). Google has also announced plans to spend more than $1 billion to build a new new campus in Hudson Square, about a mile south of its New York headquarters, in the new Hudson Yards development.

As it has expanded, Google opted not to try and win tax incentives from the city and the state, which helped it grow without stoking the kind of opposition faced by Amazon in a city that’s still dominated by uber-progressives.

Google’s purchase of the Chelsea Market building in 2010 marked an important turning point in New York’s bid to become a major technology hub, according to Doug Harmon, chairman of capital markets for Cushman & Wakefield. Google’s presence attracted other tech firms, who eventually transformed Manhattan’s West Side into a tech-industry corridor.

NYC was home to more than 264,000 tech workers in 2018, a 20% jump from 2013, according to real estate company CBRE Group Inc. In addition to Amazon, Facebook has also opted to rent office space in Hudson Yards.

But as it has grown its presence in Chelsea, Google has manged to avoid the level of controversy that Amazon faced.

“Gentrification was under way long before Google showed its face here,” said Pamela Wolff, a former building manager and member of community advocacy group Save Chelsea.

Instead, residents like Wolfff have praised Google for being a “magnet” that helped fuel development in Chealsea and the Meatpacking district – two neighborhoods that managed to shed their seedy reputations during the Giuliani area, and have seen tremendous growth over the past decade.

“Google has been the hub for this renaissance,” said NYU’s Moss, who has advised Governor Andrew Cuomo and Mayor Bill de Blasio on urban policy. “Once it becomes acceptable for educated workers, then it becomes acceptable for everyone else.”

Google opened its offices at Chelsea market three years before the high line – an elevated park occupying an old above-ground commuter train line. The company arrived almost a decade before the Whitney museum relocated to the neighborhood.

Alphabet is currently sitting on a net cash pile of $117 billion, the largest among non-financial companies in the S&P 500. Despite Alphabet’s tremendous investment in capex to build out new data centers around the country as shifts focus to its cloud business, it’s various businesses are still generating more than $28 billion in free cash flow.

Still, some critics echoed AOC’s insistence that tech companies and their sprawling growth speed up gentrification, forcing thousands of working class people from their homes. However, many of these firms also bring tens – if not hundreds – of thousands of high-paying jobs.

“It’s so attractive that it creates a cocoon around those employees,” Wolff said.

But to insulate itself from criticism, Google has remained responsive to community leaders, as well as their complaints and needs. Every holiday, it hands out turkeys to poor families like Nino Brown. Additionally, Google has provided public internet in a Chelsea park, and helped prevent an 80-year-old mural from destruction.

Jeff Bezos should be taking notes: The lesson for Amazon is that it’s biggest mistake in trying to move HQ2 to Queens was a public relations error: the company should have anticipated the AOC-led backlash and prepared a strategy for undercutting her concerns. Instead, carrying out an ostentatious campaign to try and strong-arm municipal and state leaders into handing out generous tax breaks was simply not the right move.