For all of President Donald Trump’s reputation of affection for Russian President Vladimir Putin, there is at least one point on which Washington and Moscow find themselves at odds: Venezuela, and specifically Russian deployment of about 100 military advisers, intelligence officers, and other officials in support of embattled Venezuelan President Nicolás Maduro.

A clear-eyed view of the situation in Venezuela demands recognition that the Maduro regime is condemnable—and that there is no wisdom in advocating U.S. intervention, especially when Russia is involved. To give the Venezuelan people their best shot at a more free, peaceful, and prosperous future, writes Bonnie Kristian, Washington’s main job is to leave well enough alone.

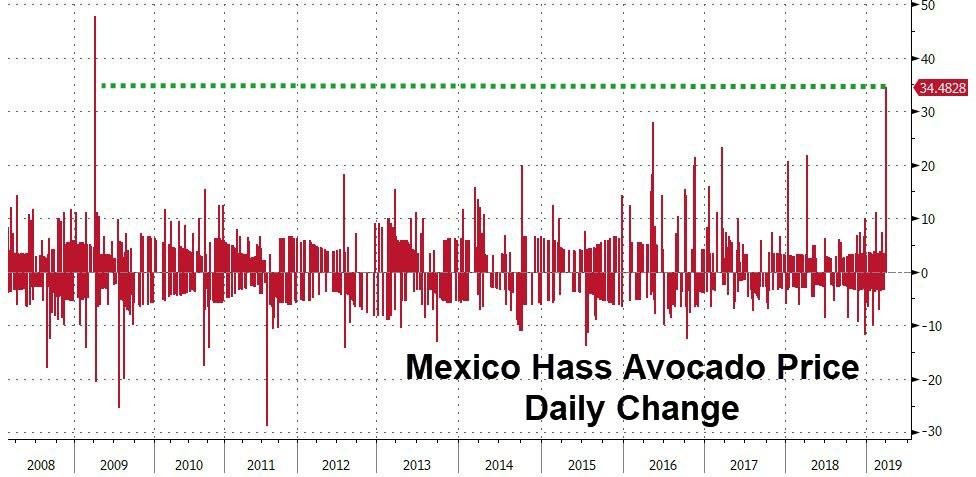

Bloomberg reports that Mexico Hass Avocado prices soared 35% today – the biggest daily spike since early 2009 – following headlines from the Trump administration that threatened to shut the Mexican border.

As we noted previously, the President & CEO Steve Barnard of Mission Produce, a global avocado distributor, told Reuters that Americans would face a severe shortage of avocados within one month upon the border shutdown, adding that, “We would be out of business for a while.”

“You couldn’t pick a worse time of year because Mexico supplies virtually 100% of the avocados in the U.S. right now,” Barnard told Reuters.

“California is just starting and they have a very small crop, but they’re not relevant right now and won’t be for another month or so.”

However, while it’s all very exciting, the surge has pushed avocado prices up to the same level they were at in 2017 at this time of year…

And as Bloomberg notes, the spike may be due to increased demand in anticipation of border closing, although President Trump has retreated from his threat to shut the border.

via ZeroHedge News https://ift.tt/2UcsUlt Tyler Durden

WTI extended its recent run today, breaking above its 200DMA…

While technicals dominated today, “The fundamentals that drove us yesterday — the OPEC production numbers falling, Venezuelan production issues, strong manufacturing numbers and lower U.S. production — all of that is conspiring to take prices higher,“ said Phil Flynn, senior market analyst at Price Futures Group Inc. in Chicago.

But once again all eyes will be on inventories…

API

Crude +3.00mm (-900k exp)

Cushing +18k

Gasoline -2.6mm

Distillates -1.9mm

EIA printed a surprise crude build in the prior week and expectations were for a return to draws this week but API reported a second weekly surprise crude build (+3mm vs -900k exp)…

The WTI 200DMA level is $62.40 – which is exactly where it traded ahead of the API data. After a quick kneejerk higher, WTI slipped lower but remained above the key technical level…

Oil has rallied more than 30 percent this year as Saudi-led production cuts, together with receding fears over the global economic growth outlook, appear to be easing investor concerns.

via ZeroHedge News https://ift.tt/2CNdkly Tyler Durden

The medicinal use of marijuana has been legal in California for over 20 years. Last year, the Golden State legalized recreational use. Yet a great many state residents still have marijuana-related convictions on their records. On Monday, two prosecutors announced a new effort to clear tens of thousands of those weed-related convictions.

The initiative would make use of Code for America’s Clear My Record program. The program takes criminal records, determines eligibility for relief, and then completes the necessary forms which are then filed in court. This helps governments like L.A. and San Joaquin County process applications more quickly. The program creators, who launched their pilot program in California last year, hope to expand the model nationwide.

Record-clearing on this level will be especially beneficial for black Californians. L.A. County Board Supervisor Mark Ridley-Thomas said that the drug war “led to decades-long racial disparities in cannabis-related arrests and convictions.” A 2016 study found that while only 6 percent of the state’s population, black Californians make up nearly a quarter of inmates serving time solely for weed-related offenses in the state.

Harsher drug penalties throughout the country have contributed to the rapid growth of the prison population. States that adopted early legalization measures failed to include provisions for those incarcerated under old rules. Washington state, for example, did not announce clemency measures until last year. States that are currently taking up legalization are making sure to add provisions to forgive old drug convictions in proposed bills.

This month, the Federal Reserve joined its global peers by turning decisively dovish. Jerome Powell and friends haven’t just stopped tightening. Soon they will begin actively easing by reinvesting the Fed’s maturing mortgage bonds into Treasury securities. It’s not exactly “Quantitative Easing I, II, and III,” but it will have some of the same effects.

Why are they doing this? One theory, which I admit possibly plausible, was that Powell simply caved to Wall Street pressure. The rate hikes and QT were hitting asset prices and liquidity, much to the detriment of bankers and others to whom the Fed pays keen attention. But that doesn’t truly square with his 2018 speeches and actions. The Fed’s March 20 announcement suggests more is happening.

I think two other factors are driving the Fed’s thinking. One is increasing recognition of the same slowing global growth that made other central banks turn dovish in recent months. The other is the Fed’s realization that its previous course risked inverting the yield curve, which was violently turning against its fourth-quarter expectations and possibly toward recession (see chart below, courtesy of WSJ’s “Daily Shot”). That would not have looked good in the history books, hence the backtracking.

On the second point… too late. The yield curve inverted, and recession forecasts became suddenly de rigueuramong the same financial punditry that was wildly bullish just weeks ago.

My own position has been consistent: Recession is approaching but not just yet. Yet like the Fed, I am data-dependent and the latest data are not encouraging. Today, we’ll examine this and consider what may have changed.

Let’s start with a step back. The global economy clearly hasn’t recovered from the last recession like it did in previous cycles. Yes, the stock market performed well. So has real estate. We’ve seen some economic growth, which in a few places you might even call a “boom,” but for the most part it’s been pretty mild. Unemployment is low, but wage growth has been sluggish at best. Rising asset prices, fueled by almost a decade of easy monetary policy, also contributed to wealth and income inequality, which fueled populist and now semi-socialist movements around the world.

This slow recovery began fading in the last few quarters. The first cracks appeared overseas, leaving the US as an island of stability. Not coincidentally, we also had (slightly) positive interest rates and thus attracted capital from elsewhere. This let our growth continue longer. But now, signs of weakness are mounting here, too.

Recall, this follows years of astonishing, amazing, unprecedented, and astronomically huge monetary stimulus by the Federal Reserve, Bank of Japan, European Central Bank, and others. In various and sundry ways, they opened the spigots and left them running full speed for almost a decade. And all it produced was the above-mentioned weak recovery. (Chart below from my friend Jim Bianco, again via “The Daily Shot”)

That, alone, should tell you that putting your faith in central bankers is probably a mistake. We can’t know how much worse the last decade would have been without their “help,” but does this feel like success?

Yet here we are, with millions still in the hole from the last recession and another one possibly looming. We also can’t rely on historical precedent to identify where, when, or why it will start. But we can make some educated guesses.

Earlier, I called the US an “island of stability.” Other such islands exist, too, and Australia is high on the list. The last Down Under recession was 27—yes, 27—years ago in 1991. No other developed economy can say the same.

The long streak has a lot to do with being one of China’s top raw material suppliers during that country’s historic boom. But Australia has done other things right, too. Alas, all good things come to an end. While not officially in recession yet, Australia’s growth is slowing. University of New South Wales professor Richard Holden says it is in “effective recession” with per-capita GDP having declined in both Q3 and Q4 of 2018.

(By the way, Italy is similarly in a “technical recession.” Expect more such euphemisms as governments try to avoid uttering the “R-word.”)

As often happens, real estate is involved. Australia’s housing boom/bubble could unravel badly. Last week, Grant Williams highlighted a video by economist John Adams, Digital Finance Analytics founder Martin North, and Irish financial adviser Eddie Hobbs, who say Australia’s economy looks increasingly like Ireland’s just before the 2007 housing collapse.

Australia’s household debt to GDP was 120.5 per cent as of September last year, according to the Bank for International Settlements, one of the highest in the world. In 2007, Ireland was sitting at around 100 per cent.

At the same time, the RBA puts Australia’s household debt to disposable income at 188.6 per cent. Ireland was 200 per cent in 2007, while the US was only 116.3 per cent at the start of 2008.

RBA figures also show more than two thirds of the country’s net household wealth is invested in real estate. In 2008, that figure was 83 per cent in Ireland and 48 per cent in the US. Meanwhile, 60 per cent of all lending by Australian financial institutions is in the property sector.

In 2007, the International Monetary Fund gave the Irish economy and banking system a clean bill of health and suggested that a “soft landing” was the most likely outcome. Last month, the IMF said Australia’s property market was heading for a “soft landing”.

House prices in Sydney and Melbourne have fallen nearly 14 per cent and 10 per cent from their respective peaks in July and November 2017, coinciding with sharp drop-off in credit flowing into the housing sector both for owner-occupiers and investors.

Real estate is, by nature, credit-driven. Few people pay cash for land, homes, or commercial properties. So when credit dries up, so does demand for those assets. Falling demand means lower prices, which is bad when you are highly leveraged. It gets worse from there as the banking system gets dragged into the fray. Losses can quickly spread as defaults affect lenders far from the source.

This is not only an Australian problem. Similar slowdowns are unfolding in New Zealand, Canada, Europe, and China. It’s a global problem, and one company reveals the impact.

Shipping and transport stocks are kind of a “canary in the coal mine” because they are among the first to signal slowing growth. Last week, FedEx reported its international shipping revenue was down and cut its full-year earnings guidance. Its CFO blamed the economy, reported CNBC.

Slowing international macroeconomic conditions and weaker global trade growth trends continue, as seen in the year-over-year decline in our FedEx Express international revenue,” Alan B. Graf, Jr., FedEx Corp. executive vice president and chief financial officer, said in statement.

Despite a strong U.S. economy, FedEx said its international business weakened during the second quarter, especially in Europe. FedEx Express international was down due primarily to higher growth in lower-yielding services and lower weights per shipment, Graf said.

To compensate for lower revenue, Graf said FedEx began a voluntary employee buyout program and constrained hiring. It is also “limiting discretionary spending” and is reviewing additional actions.

FedEx shares have dropped roughly 27 percent in the past year, lagging the XLI industrial ETF’s 1 percent decline.

This little snippet overflows with implications. Let’s unpack some of them.

Revenue fell due to “higher growth in lower-yielding services.” So those who ship international packages have decided lower costs outweigh speed. Likewise, “lower weights per shipment” signals they are shipping only what they must, when they must.

FedEx is responding with an employee buyout program and “constrained hiring.” The company is overstaffed for its present requirements. This might also reflect increased automation of work once done by humans. In any case, it won’t help the employment stats.

In addition, FedEx is “limiting discretionary spending.” I’m not sure what that means. Every business always limits discretionary spending, or it doesn’t stay in business long. If FedEx is taking additional steps, then whoever would have received that spending will also see lower revenues. They might have to “constrain hiring,” too.

Obviously, FedEx is just one company, although a large and critically positioned one. But statements like this add up to recession if they grow more common… and they are.

One reason FedEx is in the vanguard is that it’s uniquely exposed to world trade, the growth of which is diminishing for multiple reasons.

Part of it is technology. The things we “ship” internationally are increasingly digital, and they travel via wires and satellite links instead of ships and planes. These sorts of goods aren’t easily valued for inclusion in the trade stats.

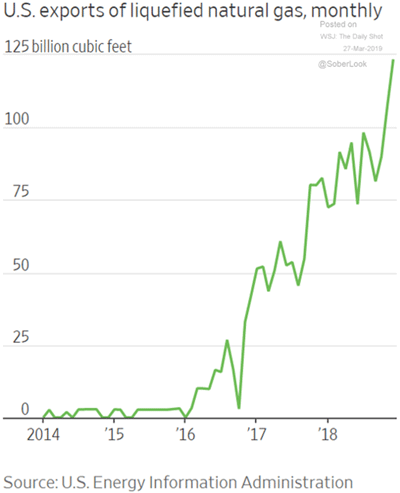

Energy is another factor. Between US shale production and renewable energy sources, we don’t import as much oil and gas from across the seas as we otherwise would. That shows up in both trade and currency values. The US dollar is stronger now, in part because we send fewer dollars to OPEC.

Note the massive (and stealthy!) growth in LNG (liquified natural gas) exports in the past few years. Think what this will look like in a few years, with not one but four LNG export terminals on the US coasts. Natural gas is also the basis for much of the chemical and fertilizer industry. Abundant US supplies (and prices less than half the cost of Russian gas in Germany) help many US industries compete.

Those are just signs of normal progress and change. The economy can adapt to them. The greater threat is artificially constrained international trade, which is what the Trump administration’s trade war is creating.

Last year, I explained how trade wars can spark recession and trade deficits are nothing to fear. I won’t repeat all that here. But we have since seen several market swoons/rallies as harsher trade restrictions looked more/less likely. Whether you like it or not, asset values depend on the (relatively) free flow of goods and services across international borders. Interfere with that and all kinds of assets become less valuable.

Starting a trade war, at the same time growth is slowing for other reasons, is more than a little unwise. Agricultural tariffs have already ripped through US farm country to devastating effect, leaving losses some farmers may never recover.

The president’s tariff threats had other impact as well. Companies raced to import foreign-supplied components and inventory before the tariffs took effect. This jammed ports and highways last year, not with new demand but future demand shifted forward in time.

This is important, and I think we will see the impact soon (if we are not already). Transport and logistics companies geared up for last year’s surge, expanding their facilities and hiring new workers. Importers built up inventory in an effort to avoid tariffs that were supposed to take effect in January. The deadline was extended, but the threat is still alive.

At some point, all this has to stop. Carrying inventory is expensive and will eventually outweigh the benefit of avoiding tariffs. Then the boom will come to a screeching halt. Imports will fall as companies work down inventory. All those jobs and construction projects will disappear.

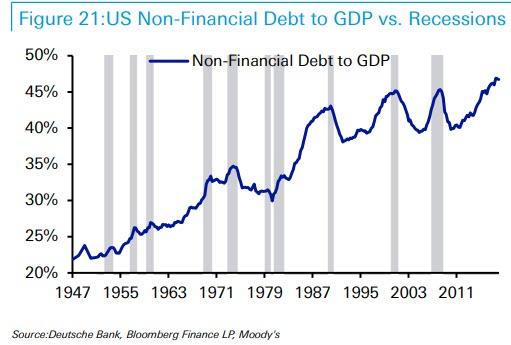

That, combined with the other cyclical factors and high debt loads everywhere, could easily add up to a recession. Exactly when is hard to say. Recessions usually get pronounced in hindsight, so there’s some possibility we are in one right now. But I still think we’ll avoid it this year. Getting into this box took a long time and so will getting out of it.

Regardless, we’ll have a recession at some point. I think the next subprime crisis will be in corporate debt. Next week, we’ll look deeper into the timing question, what the yield curve tells us, and why the next decade will bring little or no economic growth.

I realize this is not a happy conclusion, but I call them as I see them. I’ll leave you with one final but critically important thought: Prepare, don’t despair. Tough times are coming but we can handle them. You have a chance to get ready. I highly suggest you take it.

via ZeroHedge News https://ift.tt/2CQYWsC Tyler Durden

The U.S. Department of Agriculture (USDA) has decided to stop conducting research on cats in response to concerns that the department’s practice of feeding kittens parasite-infected meat and/or other kittens before unnecessarily euthanizing them was inhumane.

Back in May 2018, the White Coat Waste (WCW) Project—an anti-animal testing group—revealed that the USDA’s Agricultural Research Service (ARS) had been feeding parasite-infected meat to young kittens as a way of incubating the parasite Toxoplasma. The parasite was then harvested from the kittens’ feces, after which the little guys were euthanized with a lethal dose of ketamine injected into their hearts.

This practice reportedly dates back to 1982, and has cost the lives of about 3,000 kittens, according to the WCW.

That revelation sparked outrage, both because of the grizzly nature of the USDA’s work, as well as the fact that the euthanasia was likely unnecessary. Critics argued that the Toxoplasma-infected kitties only posed a risk to humans for up to three weeks after the animal was first infected. The parasite is easily treated in both humans and cats, and most people who become infected with toxoplasma do not require treatment.

The reputation of the USDA suffered another black eye when it was revealed (again as a result of a WCW investigation) that the department had also been purchasing cats and dogs from overseas that were then butchered and fed to homebred research kitties. This practice of “kitten cannibalism” took place from 2003 to 2015, and resulted in some 400 dogs and 100 cats being fed to cats held at an ARS laboratory in Maryland.

Two bills—both called the Kittens In Traumatic Testing Ends Now (or KITTEN) Act—were introduced in the House and Senate last year to end any USDA testing on cats. The proposed legislation is effectively made moot by the USDA’s announcement on Tuesday. The department has promised to end all testing on cats in its ARS facilities, and put the 14 felines currently under its care up for adoption.

“We are continually assessing our research and priorities and aligning our resources to the problems of highest national priority. We are excited for the next chapter of work for these scientists and this laboratory,” said ARS Administrator Dr. Chavonda Jacobs-Young in a press release.

“It’s a good day for our four-legged friends across America,” said Sen. Jeff Merkley (D–Oregon), sponsor of the senate’s KITTEN Act, telling NBC News that the USDA “made the right decision today.”

Indeed, while taxpayer-sponsored kitten murder is hardly the moral issue of our time, it’s nice to know that the federal government got a little less evil today.

The Jaws of death between bonds and stocks has never widened so fast…

What will you do?

China was flat to modestly lower overnight…

European stocks extended gains led by UK’s FTSE (and Italy unch on the day)…

Mixed bag in US equities with Dow underperforming thanks to Walgreen Boots, Nasdaq extending yesterday’s gains, S&P unch, and Trannies and Small Caps in the red…

Walgreens Boots plunged over 13% – its biggest drop since Aug 2014 to its lowest since Oct 2013…and accounted for the bulk of Dow losses today…

Treasury yields reversed some of yesterday’s surge higher with the belly outperforming…

10Y broke back below 2.50%…

The yield curve remains non-inverted in 3m10Y but flattened notably on the day…

NOTE – the curve traded all the way back up to pre-FOMC levels before flushing.

The Bloomberg Dollar Index broke above the key 1200 level once again… and reversed once again…

The Mexican Peso pumped and dumped after various headlines including President Trump’s border shutdown threats…

Cable rebounded – in its ubiquitous manner – on hope that yet another May offer will avoid a no-deal brexit…

Just after midnight ET, Cryptos were suddenly panic-bid and while some suggested this was driven by April Fools’ headlines about Bitcoin ETFs, that has been widely disregarded as the extended gains during the day session suggest two larger buyers…

“The Bitcoin market and crypto market in general continues to be small relative to the rest of the markets — and emotional,” said Jehan Chu, managing partner at blockchain investment and advisory firm Kenetic Capital. “It’s still very much subject to waves of enthusiasm. I don’t think today is anything special.”

Bitcoin spiked above $5000 for the first time since Nov 2018, and broke above its 200DMA – the biggest one-day gains since Dec 26th 2017…

“The reason why? Anybody’s guess at the moment,”

Crude continues to surge higher as copper slides with PMs treading water despite USD gains…

If China’s so freaking awesome, why is copper collapsing?

WTI surged above its 200DMA on the day…

Gold managed to recover overnight losses… but remains below $1300

How quickly will the jaws snap shut?

via ZeroHedge News https://ift.tt/2TR4fhj Tyler Durden

Nearly four years ago, over 170 people were arrested after a chaotic scene outside a meeting of biker clubs at a restaurant in Twin Peaks, Texas, in which both police and some bikers fired guns and nine people were killed (at least four of them almost certainly by police) and 20 injured. Today, after years of highly questionable prosecutorial practices, the remaining 24 indictments have been dropped. No one will actually end up convicted for any crimes committed that day in May 2015.

Current McLennan County District Attorney Barry Johnson, who inherited the whole mess from former D.A. Abel Reyna, told the Waco Tribune that he spent 75 percent of his time since taking office in January trying to deal with the aftermath, and has concluded “after looking over the 24 cases we were left with, it is my opinion as your district attorney that we are not able to prosecute any of those cases and reach our burden of proof beyond a reasonable doubt.”

Despite lacking any sure knowledge of who actually harmed anyone and who was just unlucky enough to be there, 155 people were indicted on the identical charge of “engaging in organized criminal activity” and held on punitively large $1 million bonds.

Despite causing severe harm to many of the arrestees’ lives—by either the time they spent in jail or by the indictments hanging over their heads—only one of the indictments ever even went to trial in the intervening years, and that one “ended in mistrial in November 2017, with most of the jurors in his case favoring acquittal,” as the Waco Tribune noted.

Reyna himself, in charge during the initial arrests and charges, had already dismissed all but 24 of the cases, and he re-indicted those suspects on different charges. The Tribune also pointed out that some other possible charges were no longer available to the D.A. as the absurdly overlong process in the case pushed them past the three-year statue of limitations.

New D.A. Johnson jabbed at Reyna, who he beat handily in an election last year:

In my opinion, had this action been taken in a timely manner, it would have, and should have, resulted in numerous convictions and prison sentences against many of those who participated in the Twin Peaks brawl. Over the next three years the prior district attorney failed to take that action, for reasons that I do not know to this day.

Reyna’s bad actions and planning, Johnson claims, cost the county at least $1.5 million in preparation, trial, security, and overtime costs.

And the potential costs to the county aren’t over yet. As the Waco Tribune reported, “more than 130 of the bikers have civil rights lawsuits pending against Reyna, former Waco Police Chief Brent Stroman, the city of Waco, McLennan County and individual local and state officers who were involved in the arrests.”

As attorney Don Tittle, who is representing over 100 such bikers, told the Waco Tribune:

Maybe if law enforcement had stuck with the original plan to focus on individuals who might have been involved in the violence and let the rest of the motorcyclists go after being interviewed, things would have gone differently…. It’s hard to imagine that turning the operation into a dragnet wasn’t a major distraction for the investigation, not to mention a public that grew increasingly skeptical as this thing played out. All this for an ill-advised attempt to prove an imaginary conspiracy theory, which to this day there’s not a shred of evidence to support.

Late in the day Tuesday the official Algerian state press agency APS announced the two-decade long ruler, Presdient Bouteflika, has formally resigned, finally giving in to both popular protests that have rocked the country for weeks, and following demands issued by army chief General Ahmed Gaid Salah that he immediately handover power.

“President Bouteflika notified the president of the Constitutional Council of his decision to put an end to his term,” a translation of the APS news release reads.

Algerian two decade long ruler Abdelaziz Bouteflika stepped down on Tuesday. Prior file photo via Reuters.

Have we just witnessed a quiet military coup in Algeria? Or is this a willing handover of power per constitutional requirements that the ailing 82-year old president Abdelaziz Bouteflika, unable to perform his public duties since suffering a strong years ago, should step down?

The resignation came just moments after the Army repeated calls for him to leave immediately — a demand reportedly coupled with security forces arresting businessmen known to be close to Bouteflika.

One week ago the military said it was prepared to act against the two-decade long ruler who had rarely been seen in public since his stroke in 2013. At that time General Salah, commander of the army as well as the country’s deputy defense minister, said in a live speech broadcast on private television station Ennahar that the protesters’ demands that he not run for a fifth term were “legitimate”.

“To resolve the crisis [in the country] right now, the implementation of article 102 is necessary and is the only guarantee to maintain a peaceful political situation,” Gen. Salah said on March 27. “These protests have continued up till now in a peaceful and civilized way … and could be exploited by parties with bad intentions inside and outside of Algeria,” the general added.

• Army calls for President Bouteflika Exit IMMEDIATELY

• Cites Articles 102, 8, 7

• Says it agrees w people demands

• Said yesterday’s statement Null

• 13 businesssmen arrested, can’t travel (corruption)

• Calls for immediate transition, no delay

Algeria’s army chief further called for the invocation of a constitutional clause declaring the office of the presidency vacant.

The army gave Bouteflika two weeks to vacate, and on Monday state media indicated he was expected to step down before his term expired on April 28.

The Algerian constitution indicates power goes to the chairman of the upper house of parliament, in this case Abdelkader Bensaleh, who becomes interim president until fresh elections are held.

via ZeroHedge News https://ift.tt/2TTr04e Tyler Durden

With investor attention increasingly focusing on what most believe will be the catalyst for the next financial crisis, namely a tsunami in corporate defaults as a result of the disastrous combination of record leverage, higher rates and an economic slowdown, overnight we presented the view of FTI global co-leader of corporate finance and restructuring, Carlyn Taylor, who predicted that “a spike in defaults is on the way, sooner or later.”

The expansion is pretty long in the tooth and there’s definitely a lot of buildup. The activity level of restructuring is rising, maybe not at the rate of bankruptcies, but the pipeline of companies we think are going to end up in restructuring, based on metrics that we analyze, that volume has gone up. And we’re so busy, which we don’t think is just market share, because we think our competitors are also very busy.

Yet while investor worries have centered on record corporate leverage…

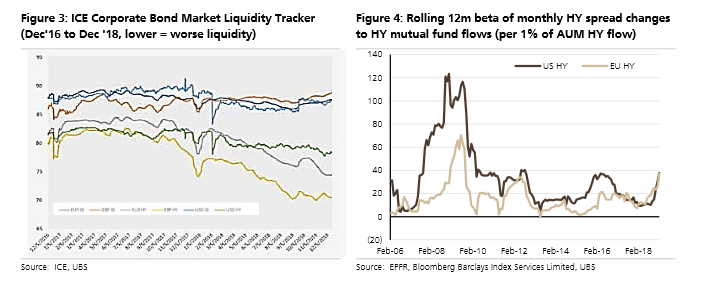

… a growing number of strategists are warning that corporate bond market illiquidity is an even greater risk factor.

Not long after Goldman most recently warned that the biggest threat facing the broader market in general, as well as corporate bonds in particular, is a sudden collapse in liquidity, overnight UBS credit strategist Steve Caprio and his team laid out four major reasons why global corporate bond market liquidity has deteriorated over time.

These are:

Rising investment fund ownership of corporate debt,

Low interest rates,

A lack of dealer intermediation, particularly in periods of rising credit risk, and

Potential new EU regulation on trade settlement failures.

UBS notes that credit investors were shocked by the spread blowout in Q4’18, followed by major spread tightening in Q1’19, and notes that “these spread moves are worrying in that they are somewhat divorced from fundamentals, as default risks remain low.” The bank then notes that it believes these shifts in risk premia are likely to remain with us for the foreseeable future, and as evidence is uses a novel liquidity tracker by the Intercontinental Exchange which highlights that global HY bond liquidity has been deteriorating steadily since 2016, while the bank’s own simple measure of gauging HY liquidity, through the beta of spread changes to flows, is also elevated.

There are two other critical reasons for the collapse in liquidity, one of which is central banks themselves. As Caprio notes, credit returns will be more negative in the future when fundamental stress arises, because there is less (US) or no (EU) room for sovereign yields to fall further. The % of index yield that is spread ranges from 31% and 58% in US IG and US HY, to 100%+ in EU IG and EU HY. This makes global credit a less diversifying asset. The empirics bear this out, with rising correlations of credit to equity returns. In addition, EU HY finds itself behind US HY in terms of reversing the QE-led portfolio rebalancing effect. Lastly, while US IG credit can receive risk-off inflows from broad bond funds, given Treasury yields are attractive as a portfolio hedge; EU IG flows are more dependent on credit-specific funds.

One additional critical reason why bond liquidity is collapsing is because US and EU dealer inventories of credit have declined notably, while dealer reaction functions to spread changes are shifting: “Pre-crisis, dealer purchases of credit were uncorrelated to spread changes. Post-crisis, dealer demand is reacting like retail funds, buying when spreads tighten and selling when spreads widen.” This lack of willingness to provide liquidity, UBS warns, “is likely to remain with us, due to capital & liquidity requirements.”

“In a world where sudden bouts of volatility may become the norm, funds are more likely to sell bonds than dip into cash reserves to meet redemptions when the next leg of risk aversion hits. This increased concentration by investor type both with respect to subordinated debt as well as HY credit exacerbates liquidity risk further in our view, which naturally increases potential downside risk.”

While UBS hedged, trying not to sound too bearish, and noting that it doesn’t believe corporate bond market illiquidity “will bring down a cycle on its own,” the Swiss bank does expect more credit spread volatility going forward, “with the real challenge for markets taking place in a broader downturn when liquidity risk intersects with default risk”, i.e., the perfect storm for the bond market.

Echoing UBS, Deutsche Bank’s credit strategist Jim Reid published an almost identical report at almost the same time, in which he agreed that it’s not so much default risk and deteriorating fundamentals, but rather liquidity that will precipitate the next crisis.

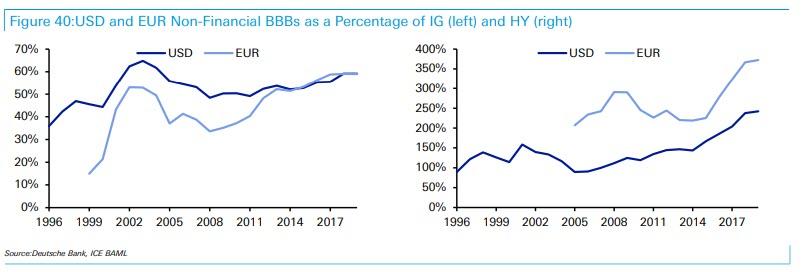

Reid writes that a look at long-term credit fundamentals shows corporates are levering up in this cycle “but that this is more of an IG than HY story and therefore reduces the default implications”, although one could counter that with over $3 trillion in BBB-rated debt just waiting to be downgraded to junk, it is only a matter of time before this becomes a bigly HY story. Deutsche also notes that while leveraged loans are a concern, it’s not clear the increase in cov-lite issuance will bring large-scale defaults in the next cycle as without covenants there are fewer triggers. As a result the German bank doesn’t think corporate fundamentals will cause this cycle to turn but will clearly deteriorate when it does.

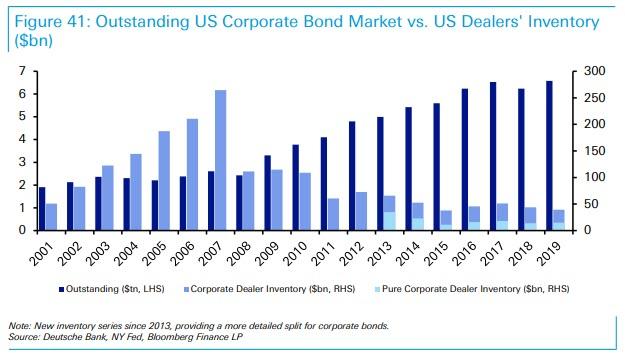

So what will cause the cycle to turn? As Reid suggests, echoing what UBS warned above, the next recession will be not so much about default risk (outside of the natural increase) but instead about liquidity risk. Just like UBS, Deutsche writes that since the financial crisis, the size of the credit market has increased dramatically, but regulation has sharply cut dealer liquidity, and “in a recession we will likely see one-way selling and large gap risk for spreads.” Reid explains:

The overall market dynamics have shifted aggressively since the GFC. Figure 41 republishes a chart we have shown on numerous occasions over the last several years detailing that the US corporate bond market has near tripled in size since the GFC due to QE, lower yields encouraging companies to issue and high demand for fixed income and spread product, thus providing a captive pool of capital. Meanwhile, regulation has ensured dealers/market-makers have less and less ability to warehouse risk.

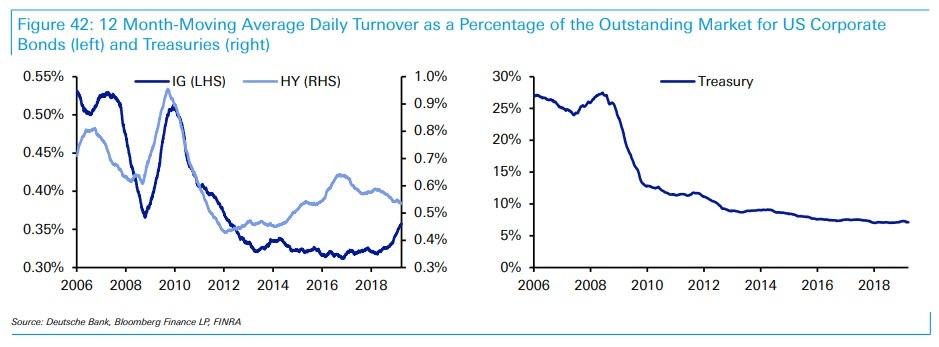

The next chart looks at US IG, HY and Treasury daily trading levels relative to the size of the market:

How bad would this self-fulfilling liquidity crisis be? The answer:

It’s quite possible the next recession will see the third-worst spread peak in history (behind only the Depression and the GFC) due to these market dynamics.

But don’t worry folks: central banks will bail you out, as usual:

… these peaks may not last long as central banks will probably be forced to buy to ease pressure on the market. In fact, this is probably a more traditional function of central banks: to lend money to solvent entities when there is a liquidity problem. Companies are unlikely to have liquidity problems, but those holding the bond might well do.

Meanwhile, keep an eye on the tsunami of fallen angles: “a large BBB market vs. HY will also exacerbate the technicals when downgrades occur.” Finally as to timing, Reid warns that “as many indicators are late cycle, this is a real risk over the next couple of years.”

via ZeroHedge News https://ift.tt/2OFeEM5 Tyler Durden

The medicinal use of marijuana has been legal in California for over 20 years. Last year, the Golden State legalized recreational use. Yet a great many state residents still have marijuana-related convictions on their records. On Monday, two prosecutors announced a new effort to clear tens of thousands of those weed-related convictions.

The medicinal use of marijuana has been legal in California for over 20 years. Last year, the Golden State legalized recreational use. Yet a great many state residents still have marijuana-related convictions on their records. On Monday, two prosecutors announced a new effort to clear tens of thousands of those weed-related convictions.

What will you do?

What will you do?

{kind=link}