Chinese stocks trod water early on but faded into the close…

UK’s FTSE 100 was Europe’s outperformer while Spain and Italy were down 0.5% on the day…

US equities pumped at the open once again and then faded into the EU close (once again), only to reverse trend (once again)…Trannies outperformed, followed by Small Caps…

S&P tested back below 2800 once again today (and bounced)…

FANG stocks were flat on the day with no bounce after yesterday’s tumble…

Credit and equity protection costs plunged again today…

As opposed to yesterday’s ugly 5Y auction, today’s 7Y auction saw major demand, but that was not enough to cover the selling which saw yields up 2-4bps (except 30Y which was unchanged)…

30Y yields dropped below 2.80% for the first time since Jan 2018…

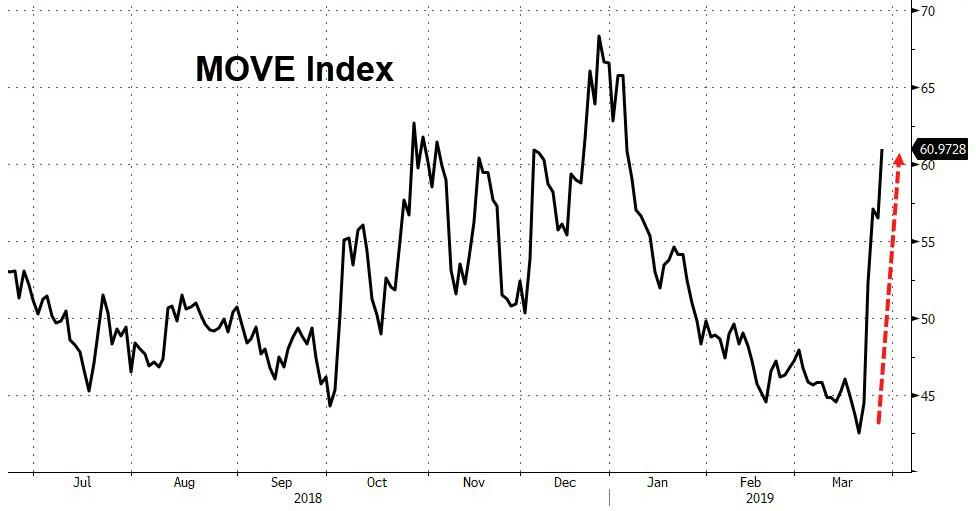

Bond vol exploded in the last week – the biggest spike since 2014…

Spiking to an important resistance level relative to stocks…

The dollar index spiked back above 97.00…

Trending higher in 2019…

The dollar gains were extended by cable weakness…

The Turkish Lira tumbled…

Leading EM FX into the red for 2019…

Cryptos were a snoozefest today…

Ugly day in PMs while copper and crude managed gains despite the stronger dollar…

Following up on yesterday’s data, Permian Nat Gas prices have plummeted into negative territory – yes, drillers are force to pay end-users to take the natgas off their hands…

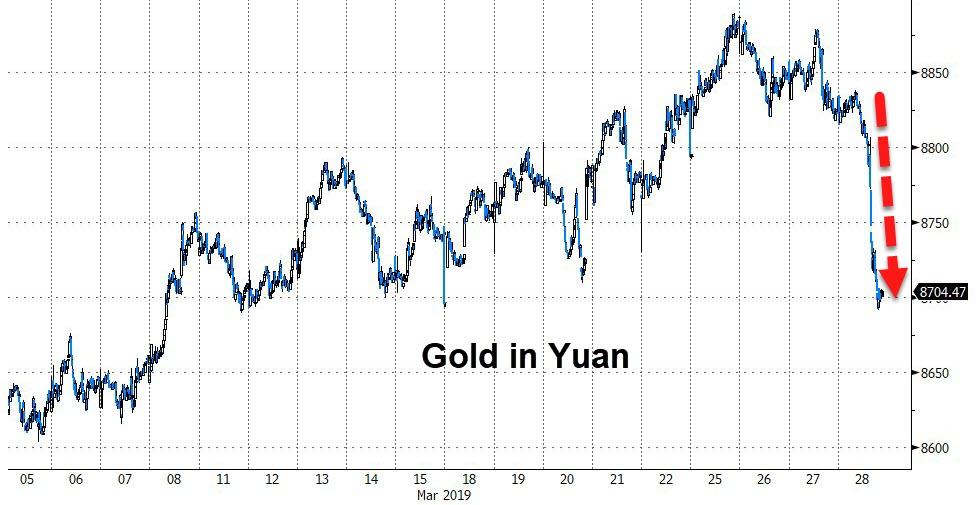

Gold fell on the day (against the dollar and yuan) – biggest drop against Yuan since June 2018…

But Gold in dollars broke below its 200DMA…

And back below $1300…

And silver slipped to its lowest since Boxing Day (12/26/18)…

Finally though, the gap between reality and perception remains near record highs…

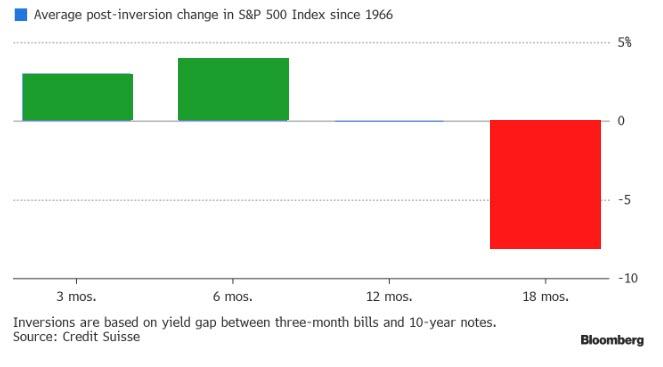

And don’t forget, a year after the yield on three-month Treasury bills rose above the yield on 10-year notes…

The S&P 500 was little changed on average.

Eighteen months later, the index had an average loss of 8 percent — typically because earnings turned lower, Andrew Garthwaite, a global strategist at Credit Suisse, wrote.

via ZeroHedge News https://ift.tt/2WtV4oD Tyler Durden

Over the past few days, many investors have asked why, with its currency in freefall again as its reserves evaporate, did Turkey take the drastic measure of sending its overnight swap rate above 1,000% in a clear attempt to crush the shorts. The answer may be simpler than most expect: if Turkey doesn’t prevent the panic from escalating, there may be nobody who can help it.

That was the implied message delivered today by the head of the Bank for International Settlements, Agustin Carstens, who said that International Monetary Fund does not have sufficient lending capacity to respond, if a major new emerging market crisis affecting several countries suddenly erupted.

Carstens, the former corpulent head of the Bank of Mexico, said that last reviews of IMF quotas, how much member countries pay in and the voting rights that go with that, had failed to ensure it had sufficient financial resources. Which, of course, leaves the question open: if the IMF no longer has the resources to rescue emerging markets and China’s economy is now contracting, who does?

BIS General Manager Agustin Carstens

“This leaves us with the problem of having inadequate resources and having to improvise in times of crisis. The mission of the fund is there,” Carstens told a conference at the French central bank. “If the Fund cannot do it others will have to do it otherwise the economic costs will be huge,” he added clearly hoping to pass the multi-trillion responsibility of bailing out EMs to someone a little more liquid.

But it’s not just emerging market that are woefully unprepared for the next crisis, and will suffer significantly should a “fat tail” event emerge: it turns out that Europe is in the same boat.

While the eurozone is in better financial shape than a decade ago, it is not solid enough to withstand another economic crisis, the head of the IMF, Christine Lagarde, said on Thursday. In a surprising moment of honesty from the Hermes-bag afficionado, Lagarde told a Paris conference that the currency union “is not resilient enough” to emerge unscathed from “unexpected economic storms”.

Lagarde acknowledged that the currency union was now “more resilient than a decade ago when the global financial crisis struck, “but it is not resilient enough,” she admitted.

“Its banking system is safer, but not safe enough. Its economic well-being is greater overall, but the benefits of growth are not shared enough,” Lagarde told the same gathering organized by the French central bank where Carstens spoke earlier.

Lagarde reveals the IMF’s last strategy.

It was unclear what the consequences are if as the IMF head claims, the eurozone will be crushed during the next crisis.

Lagarde’s warning comes as signs of slower economic growth across Europe are becoming increasingly more obvious, especially in the two core economies of Germany and France. On Friday, manufacturers in the 19-nation single currency bloc “reported their steepest downturn for six years” as pressure mounted from trade wars and Brexit fears, IHS Markit said.

On Wednesday, the European Central Bank added to growth worries when its chief Mario Draghi hinted that interest rates would stay low for longer than previously anticipated, to stimulate growth and inflation.

And with central banks now leery of injecting further liquidity via QE, while ZIRP and NIRP no longer suffice to boost economies, it remains unclear just who will provide a lifeline to either Europe or the EM when the next recession and/or global financial crisis strikes, some time over the next 12-18 months.

via ZeroHedge News https://ift.tt/2V3dDzI Tyler Durden

The FBI was ordered by a D.C. judge to hand over copies of former director James Comey’s memos about his interactions with President Trump prior to his firing, in order to determine whether they can be released to the public.

U.S. District Judge James Boasberg in Washington on Thursday ordered the Federal Bureau of Investigation to submit both clean and redacted versions of the documents by April 1 as part of a Freedom of Information Act case brought by CNN and other organizations, including USA Today and the conservative activist group Judicial Watch Inc. –Bloomberg

Meanwhile, CNN argued in a January filing that the public should be permitted to see the memos because Comey and Trump have accused each other “of grave breaches of the public trust,” and that the documents will show “contemporaneous records of disputed conversations.”

The FBI told the court on March 1 that the files are still redacted and classified, and should remain so in order to avoid interfering with special counsel Robert Mueller’s now-completed investigation into Russian interference in the 2016 election.

Last January, the FBI’s chief FOIA officer, David Hardy, gave a sworn declaration to Judicial Watch in which he said that all seven of Comey’s memos were classified at the time they were written, and they remain classified.

We have a sworn declaration from David Hardy who is the chief FOIA officer of the FBI that we obtained just in the last few days, and in that sworn declaration, Mr. Hardy says that all of Comey’s memos – all of them, were classified at the time they were written, and they remain classified. –Chris Farrell, Judicial Watch

Judicial Watch’s Chris Farrell pointed out at the time that Comey therefore mishandled national defense information when he “knowingly and willfully” leaked them to his Law Professor pal at Columbia University, Daniel Richman.

It’s also mishandling of national defense information, which is a crime. So it’s clear that Mr. Comey not only authored those documents, but then knowingly and willfully leaked them to persons unauthorized, which is in and of itself a national security crime. Mr. Comey should have been read his rights back on June 8th when he testified before the Senate.

Given that James Comey ostensibly leaked unredacted information to Richman, the DOJ’s redactions would appear to confirm that Comey did in fact commit the federal crime of leaking classified information.

via ZeroHedge News https://ift.tt/2FGW973 Tyler Durden

The European Union has provisionally agreed on new auto safety rules that will require all cars sold within the E.U.’s 27 member countries to come with a host of new safety features, including intelligent speeding assistance (ISA)—which would prevent cars from going above the speed limit—by 2022.

According to The New York Times, drivers would still be allowed to switch the technology off at their discretion, but the car would have to start with it flipped on.

“Every year, 25,000 people lose their lives on our roads. The vast majority of these accidents are caused by human error,” said E.U. Commissioner Elżbieta Bieńkowska in a press release announcing the new rules. “With the new advanced safety features that will become mandatory, we can have the same kind of impact as when the safety belts were first introduced.”

The E.U.’s goal is laudable, particularly given the death toll cited by Bieńkowska, as well as the fact that the main cause of 30 percent of all fatal accidents on European roads is speeding. Nevertheless, the safety mandates coming out of the E.U. may well be a bit over ambitious.

That’s according to the European Automobile Manufacturers Association (ACEA), which argues that intelligent speeding assistance (ISA) is currently too unreliable to be accepted by customers.

The speeding technology would work either by onboard cameras detecting roadside speed limits signs, or by using a digital database of speed limits to check a driver’s speed versus what’s allowed on a particular road.

Simpler versions of this technology would simply warn drivers when they are going too fast. A more intrusive form of it, which the E.U wants to mandate, would actively prevent a driver from going beyond what is allowed on a particular road.

But as the ACEA notes, there are obstacles to implementation. Road signs are not standardized across Europe. Even if they were, signs are often damaged or covered by foliage. That means onboard cameras might have difficulty seeing and interrupting these visual cues.

There also currently doesn’t exist a single database that keeps up-to-date records on all speed limits across all European roads, which would limit the GPS-based version of this technology.

Requiring all cars to be linked up to such a database at all times also raises privacy concerns.

Even if ISA technology did function perfectly all the time and did not implicate any privacy issues, that does not prove it should be mandatory. Every mandated safety feature is naturally going to increase the cost of a car, with those costs getting passed on to consumers.

This economic fact implicates not just the ISA technology, but also a host of other features the E.U. is pushing, including back-up cameras and a requirement that all new cars come with the ability to have breathalyzers installed in ignitions.

The more these safety mandates cost, the more consumers will be priced out of vehicle ownership or have to cut back on other expenses in order to afford a car. That’s a real cost that can’t be ignored.

The new rules announced this week have only been agreed to in principle by the E.U’s Parliament, Commission (executive branch), and Council of Ministers (which consists of elected officials from each country), but still needs to be formally voted on before it can go into effect.

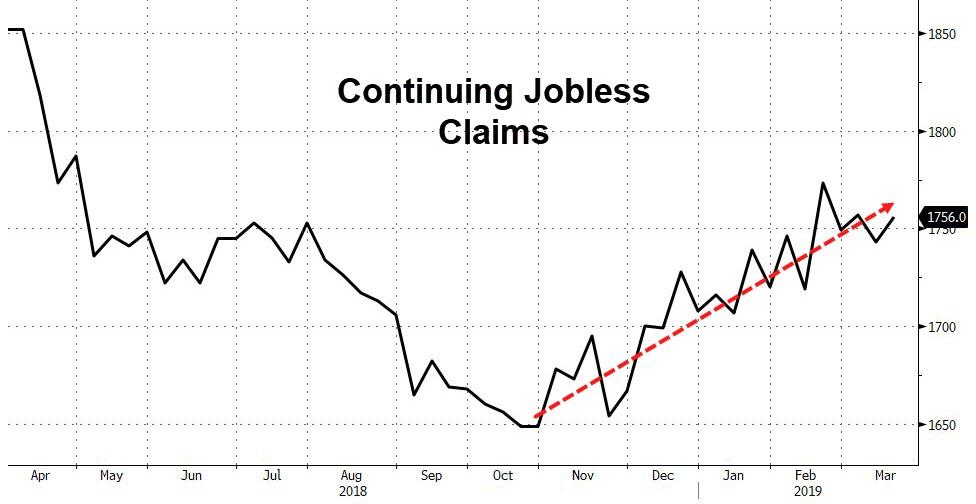

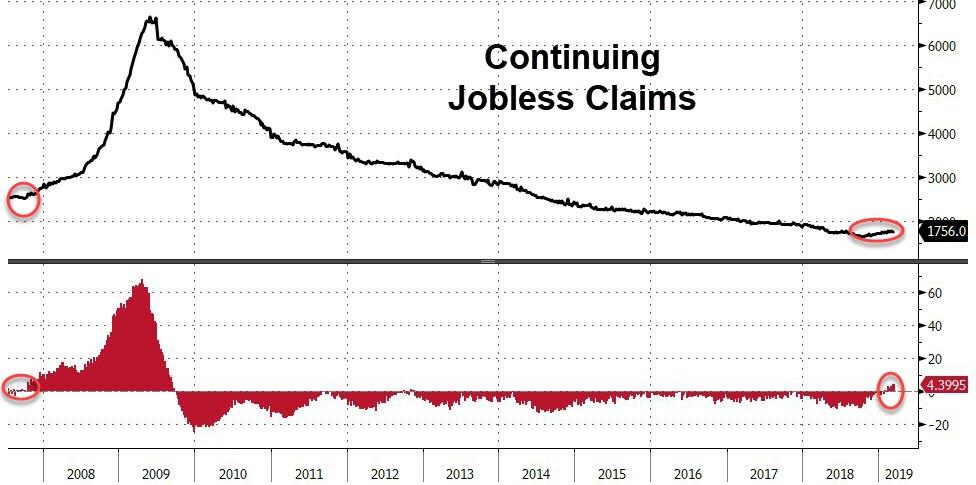

With economic data disappointing en masse and US equity earnings expectations plummeting, talking heads have one last leg left on the stool of buy-and-hold – jobs, jobs, jobs! The unemployment rate (low), participation rate (people coming back into the workforce), wage growth (rising at fastest pace in 10 years), initial jobless claims (back near multi-decade lows), and JOLTS (more jobs offered than people available).

So, why are continuing jobless claims surging in a not-noisy manner higher for the last six months?

We have seen this before…

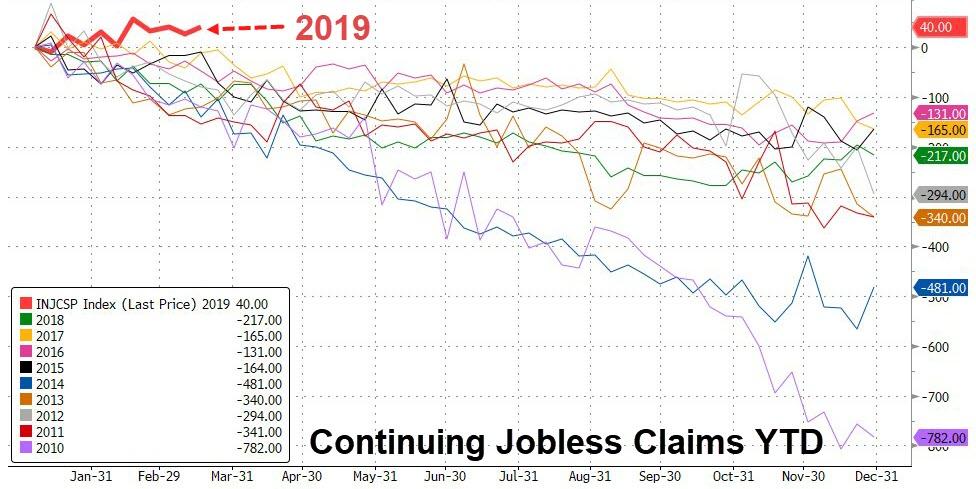

And in fact 2019 is now the worst start to a year for continuing claims since 2009…

So, what is going on?

via ZeroHedge News https://ift.tt/2FGIehd Tyler Durden

During its FOMC meeting last week, the Federal Reserve took 2019 rate cuts completely off the table. It said it will freeze bond sales from its $3.8 trillion balance sheet later this autumn. In other words, balance sheet normalization is pretty much a done deal. Peter Schiff has predicted this would happen. He said from the beginning if and when the Fed tried to normalize rate, it would have to abort the process.

And here we are.

But as Peter explained in his most recent podcast, the Fed still isn’t being honest about why it’s done a monetary policy 180. It’s making excuses.

As I predicted, they are not telling the truth. The markets can’t handle that. The Fed is not telling the markets, ‘We’re not raising rates because the economy is imploding because of all the debt that was accumulated when we kept rates so low. Now we can’t raise them. Or we can’t continue to shrink the balance sheet because the budget deficits are blowing out of control.’”

Indeed, the federal government spent itself into an all-time record deficit in February. Think about that. That means the government is running bigger deficits than it was during the Great Recession.

If we are running these enormous budget deficits now – before the recession – imagine how much greater they’re going to be during the recession. The Fed can’t add fuel to the fire by competing with the Treasury. The Fed can’t keep unloading bonds at the same time that the Treasury is selling them like they’re going out of style.”

Peter said he thinks that by the time Trump leaves office, he will have set deficit records for every single month in the calendar year. He said the only good news – at least for Republicans politically – is that the next president will have to run even higher deficits.

Which is why we’re going to have a sovereign debt crisis and a currency crisis.”

Given the enormity of these deficits and the ever-upward spiraling debt, the Fed has no choice but to call off the tightening. You can’t raise interest rates in an economy built on piles of debt. But the Fed can’t tell the markets that. They will have to figure it out on their own. So far, they seem pretty clueless. But eventually, they will and that’s when the bottom is really going to fall out of the dollar.

When the Fed has to go back to zero, which it will be doing relatively soon, when the Fed has to go back to quantitative easing, nobody is going to believe that it is temporary again. Nobody is going to buy the Fed’s BS about how interest rates are going to stay low only temporarily and then we’re going to normalize them, and we’re going to shrink our balance sheet. We’re not monetizing the debt. After the recession is over we’re going to shrink our balance sheet back down to where it was before the recession. No one’s going to believe that. They couldn’t shrink a $4 trillion balance sheet. They won’t be able to shrink an $8 trillion balance sheet. If they couldn’t raise rates when the national debt was $22 trillion, they sure as hell can’t raise them when the national debt is $30 trillion.”

But at this point, the markets haven’t figured this out. Peter said they don’t really want to.

They don’t want to admit I was right from the beginning – that the Fed checked us into a monetary roach motel and there’s no way to ever check out. But I do believe the markets are going to figure this out, whether the Fed admits it or not – during the next recession.”

Peter pointed out the inverted yield curve, widely seen as a warning sign for a recession. But he pointed out that the spread between 10-year Treasurys and 30-year Treasurys remains positive and is even widening. He goes on to explain why this next recession is actually going to feature stagflation. He also covers some of the recent economic data and touches on the Mueller report.

via ZeroHedge News https://ift.tt/2V49Dzc Tyler Durden

Is Venezuela heating up again or is this just more desperation setting in for the Juan Guaido-led opposition after recent failed efforts to gem up popular support for an anti-Maduro coup?

The US recognized “Interim President” has announced plans for his supporters to launch “tactical actions” starting next week as part of his “Operation Freedom” to overthrow President Nicolas Maduro. The opposition is now telegraphing their regime change maneuvers, in what appears more of a desperate strategy to maintain external and international pressure and visibility on the continuing political crisis in the country, lately felt in a series of major nation-wide electricity outages.

President Trump hosted a delegation headed by Juan Guaido’s wife, Fabiana Rosales, at the White House on Thursday. Image source: The White House

Guaido said via Twitter that such tactical actions are to begin April 6, which will involve “freedom cells” set up across the country rising up in mass protest when the order is given.

He began publicly referencing the plan earlier this month at opposition rallies and described it as a “full-fledged revolution in all states of Venezuela simultaneously.”

This has even included talk of “Operation Freedom” operatives and mass protesters ultimately marching on the Miraflores presidential palace – home to President Maduro.

Tweeting with the hashtag #VamosOperaciónLibertad, Guaido further appealed to “constitutional forces” within the Venezuelan army to rise up and switch loyalties.

All of this comes the same month that hawkish Republican Senator and staunch Guaido supporter Marco Rubio told a Senate Foreign Relations committee hearing that “Over the next few weeks, Venezuela is going to enter a period of suffering, no nation in our hemisphere has ever confronted in modern history.”

¡Atención!

Anunciamos el inicio de la fase preparatoria de la #OperaciónLibertad para lograr el cese de la usurpación. Llegó el momento de la organización, la movilización y la estrategia para liberar a Venezuela.

Also within the past week exchanges between Moscow and Washington over Venezuela have heated up, as days after Vladimir Putin sent military planes and 100 troops to an airport near Caracas over the past weekend, on Wednesday President Trump warned Russia against involvement in the Latin American nation, telling reporters in the Oval Office that “Russia has to get out”.

Reacting to White House condemnation of Russian troops landing in Caracas, the Kremlin responded on Thursday, saying that it deployed military specialists merely to service preexisting arms contracts with Venezuela, and that Russia is not interfering in the Latin American country’s internal affairs.

Russian Foreign Ministry Spokeswoman Maria Zakharova said at a press briefing on Thursday when asked how long the Russian troop contingency led by a high ranking general will stay: “How long? As long as they need it, and as long as the Venezuelan government needs them. It all is being done based on bilateral agreements.”

“Eighty percent of the population in Venezuela has no power. They are trying to break our morale,” Venezuela’s new Interim First Lady said at the White House today. “But let me tell you that there is light, and the light is here.”

The Kremlin has also emphasized that countries should let Venezuelans decide their own fate, in what appears a reference to Washington’s very overt promotion of the opposition, which also included hosting a delegation headed by Juan Guaido’s wife, Fabiana Rosales, at the White House on Thursday.

Notably the White House called Rosales “Venezuela’s new Interim First Lady” in statements related to the event.

via ZeroHedge News https://ift.tt/2TGaF2w Tyler Durden

Patrick Murphy, who’s likely to be executed Thursday night for his role in the 2000 murder of a Texas police officer, is not innocent.

Murphy, convicted of sexual assault prior to the murder, was one of the infamous “Texas 7” who escaped from prison and carried out a botched robbery that led to Irving Police Officer Aubrey Hawkins’ death. But he did not pull the trigger. Neither was he directly involved in the officer’s death, Murphy says.

“I’m not challenging the guilt of the crime,” he told CBS Dallas-Fort Worth this week. “My role was basically really to be the getaway driver.”

In mid-December 2000, Murphy and six other maximum-security inmates were able to steal weapons from the prison armory and drive off in a truck. They would go on to carry out two robberies, according to the Houston Chronicle.

Their luck ran out on Christmas Eve, as they were in the midst of stealing guns and money from a sporting goods store. A concerned bystander called police, and Hawkins was the first officer to arrive on the scene. Murphy, from his post in front of the sporting goods store, warned his co-conspirators that Hawkins was coming. Hawkins went around to the back of the store and was shot 11 times.

“I didn’t even realize shots had been fired for probably 10 or 15 minutes,” Murphy told CBS DFW.

Murphy was eligible for the death penalty due to Texas’ law of parties. “If, in the attempt to carry out a conspiracy to commit one felony, another felony is committed by one of the conspirators, all conspirators are guilty of the felony actually committed, though having no intent to commit it, if the offense was committed in furtherance of the unlawful purpose and was one that should have been anticipated as a result of the carrying out of the conspiracy,” the statute reads.

In layman’s terms, it mean that if a group of people plan to commit a robbery, and someone is killed in the process, all of them are guilty of murder, so long as they could have reasonably anticipated the death occurring as a result of or in conjunction with the robbery.

Murphy said in his written confession that his “purpose was to if pursued by the police I was to initiate a firefight with the AR-15.” So even though he didn’t pull the trigger, he was held criminally responsible for Hawkins’ death.

“It is unconscionable that Patrick Murphy may be executed for a murder he did not commit that resulted from a robbery in which he did not participate,” Murphy’s attorneys, David Dow and Jeff Newberry, said in a statement, according to the Associated Press.

As Lauren Krisai, the former director of criminal justice reform at the Reason Foundation, which publishes this website, explained in 2016, these sorts of laws are not limited to Texas.

Consider Ryan Holle. He was convicted of first-degree murder in Florida because he lent his car to two friends, who would go on to commit a robbery and kill an 18-year-old girl. Holle was sentenced to life without parole, even he was nowhere near the scene of the crime. Felony-homicide laws have led to murder charges for people who weren’t directly involved in victims’ deaths in Virginia and Illinois as well.

Last October in California, then-Gov. Jerry Brown signed into law legislation that limited the state’s ability to bring murder charges against people who weren’t actually involved.

Texas legislators, meanwhile, have proposedlegislation that would prevent people like Murphy from being sentenced to death.

But it likely won’t be enough to save his life. “Five individuals have lost their lives as a result of the role they played in his murder, four of whom have been executed by the State of Texas for their roles in taking Officer Hawkins’ life. Carrying out the execution of Patrick Murphy, who neither fired a shot at Officer Hawkins nor had any reason to know others would do so, would not be proper retaliation but would instead simply be vengeance,” his attorneys wrote in a clemency petition to the state parole board, according to the Chronicle. The parole board declined to take action, after a state appellate court refused to grant him a stay of execution.

Murphy’s hopes now lie with Texas Gov. Greg Abbott, who can grant clemency, and the U.S. Supreme Court. Murphy converted to Buddhism and wants his spiritual adviser, Rev. Hui-Yong Shih, to be by his side when he’s given the lethal injection. Because Shih is not an employee of the Texas Department of Criminal Justice, he’s not allowed in the death chamber, according to Courthouse News Service.

Murphy alleges his First Amendment right to freedom of religion is being violated, though a federal district and circuit court would not grant him a stay. Murphy has appealed to the U.S. Supreme Court, but admitted to CBS DFW that he’s unlikely to be get a favorable ruling there either.

The case draws some parallels to that of Dominique Ray, an Alabama death row inmate who wanted access to an imam before he was executed. As Reason‘s C.J. Ciaramella reported, the Supreme Court said last month that the execution could move forward because Ray waited too long to file his petition for relief.

Murphy’s fate illustrates some of the problems with the death penalty. I’ve previously argued that the state should not be in the business of killing its own citizens, even mass murderers. “The death penalty is uncivilized in theory and unfair and inequitable in practice,” the ACLU rightly says. “Well-publicized problems with the death penalty process—wrongful convictions, arbitrary application, and high costs—have convinced many libertarians that capital punishment is just one more failed government program that should be scrapped,” Ben Jones adds at Libertarianism.org.

If the death penalty isn’t appropriate for mass murderers, then it’s certainly not a suitable punishment for people like Murphy, who, while a criminal, was not directly responsible for a death.

“I don’t think sentencing and culpability about law of parties is about justice,” he told CBS DFW. “I think it’s about vengeance.”

When the yield curve inverted last week, an event which officially started the countdown to the next recession, few felt as vindicated (and perhaps content) as SocGen’s Albert Edwards who has been calling for the next phase of the “Ice Age” (defined by him all the way back in 1996) for years. Predictably, in a note published today, he took a moment or too to gloat over recent developments, writing that “ten years since the start of the QE experiment, the Fed has failed in its objective to drive up CPI inflation, merely inflating asset prices instead. The next phase of the Ice Age is unfolding as US (and eurozone) CPI inflation rapidly falls towards zero, and central bank liquidity continues to rotate out of risk assets into the last game in town – government bonds.”

Yet even in quasi-victory, the bearish Edwards is eager to pour just a little more gasoline on the bonfire of the raging market panic (as recapped earlier by his Rabobank colleague, Michael Every), and cautions that “the barely inverted curve may underestimate the imminent danger.”

Which brings us to an interesting tangent: is Edwards a perma-bear… or just an uber-bear as he describes himself in the following section:

I am frequently referred to in the press as a perma-bear – a label often used to suggest that my views can be safely ignored as any argument I use is merely constructed to support my ‘permanent’ bearishness on equities. Personally, I prefer the title über-bear. I certainly have no intention of being permanently bearish, but to be sure, being strategically underweight equities since the end of 1996 may certainly strike some as “permanent”.

To be sure, expecting a market crash for 23 years may indeed strike some as permanent, but do not fret: as regular readers will know, Edwards’ bearishness on equities sits within the context of his Ice Age thesis, where what’s bad for stocks is good for bonds and vice versa:

I have long used the Japanese experience from 1990 onwards as my template, having watched each successive economic cycle in Japan grind out lower highs and lower lows for inflation and nominal GDP growth until they slid into a sub-zero deflationary hell.

When I first framed my Ice Age thesis back in 1996, I envisaged the US and Europe experiencing a Japanese-style secular de-rating of equities, both in absolute terms and, more importantly, relative to government bonds. Meanwhile, bonds would also re-rerate in absolute terms. So with the next recession expected to begin as soon as late 2019 or early 2020, how long does Edwards see the next economic crisis lasting? “I believe this Ice Age process will end with US 10y close to minus 1%.“

Which, which potentially bad news for stocks, is of course great news for bonds, as he explains in the next section:

My consistent über-bullishness on western government bond markets never seems to attract as much attention as my extreme bearishness on equities. Yet the thesis supporting both is the same. Take a look at the performance of 10y+ world government bonds since the inception of the Ice Age (i.e., from end-1996). A balanced fund following my strategic advice to buy and hold bonds over equities would have only marginally underperformed even at the end the fantastic bull run in equity markets over the last ten years. The contrast in volatility is also striking as is clearly shown in the chart below.

Here, Edwards like so many other commentators, takes the opportunity to remind readers of his own take on why the inverted yield curve has been “so successful in predicting recessions”, and explains as follows:

As far as this author is concerned there is no sophisticated economic or financial market theory that explains the predictive reliability of a yield curve. Being the simple, unsophisticated soul that I am, all I believe the inversion of the yield curve tells us is that the Fed has raised interest rates considerably. This often coincides with inversion, especially when the bond market starts to detect the sickly aroma of an economy slipping away into a recession.

But, somewhat oddly, Edwards is less of an absolutist when it comes to curve inversion, and writes that in his view, “inversion is neither a necessary nor sufficient signal that a recession is imminent.”

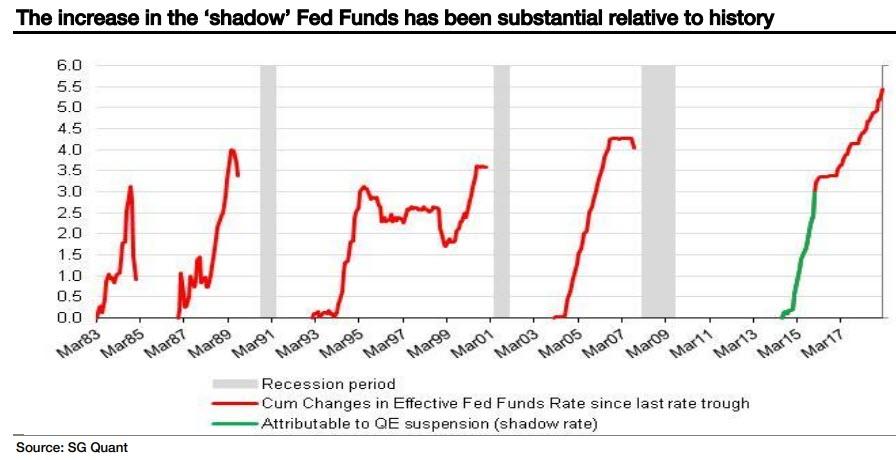

This is where SocGen’s analysis on the ‘shadow’ Fed Funds falling to minus 3% back in 2016 at the height of QE, and which we first presented last June, is so important. What it means, Edwards explains, is that, as far as the impact on the economy and markets are concerned, the increase in Fed Funds interest rate has not been from 0.25% to 2.5% currently but from minus 3.0% to 2.5%, i.e., a much more punchy 5.5 percentage point increase, as shown in the chart below – “the green line depicts the end of QE and start of QT. So considerably more aggressive tightening of interest rates than meets the naked eye and a shift that historically is more than enough to tip the economy into recession.”

Following this surge in the shadow rate, which also takes into consideration the Fed’s balance sheet and the (lack of) QE, with the US economy and equity markets beginning to suffer from a severe dose of indigestion in the wake of this 5½ percentage point hike in rates, no wonder the bond market rallied so hard: “It would probably have done so in a few months in any case, even without the Fed’s panic U-turn on interest rate guidance”, Edwards notes.

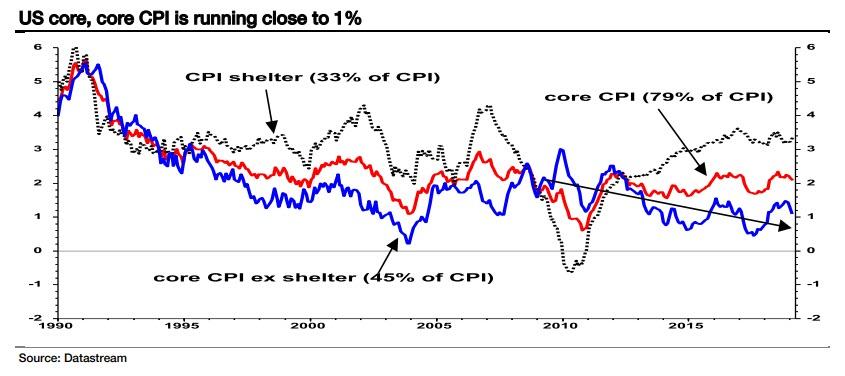

Meanwhile, looking at that other all-important metric – inflation – Edwards sees a sharp reversal on the horizon, because the current CPI basket is heavily skewed toward shelter inflation. Well, with the US housing market having entered a sharp downward trajectory recently, Edwards believes it is only a matter of time before a deflationary flood is unleashed:

The current 2.1% core CPI inflation rate (red line in chart below) is massively inflated by the dominant ‘shelter’ component, which is running at 3.4% yoy (see dotted line below). We have written about this before and do not intend to go into deep detail here apart from noting that, excluding shelter, ‘core core’ CPI inflation is only running at 1.1% and, unless I am mistaken may even be trending down (see blue line below).

Shelter comprises 33% of CPI and some 42% of core CPI and so dominates the latter in particular. It comprises two components: rental of primary residence (8% of CPI), but also an item termed Owner Equivalent Rent (OER, 24% of CPI). The OER series is a mind-bending concept designed to measure the rent a homeowner forgoes if they do not rent out their own home! It was included to replace house prices ejected from CPI in the early 1980s. This strange OER series is ‘imputed’ (made up?), but tends to follow actual rents quite closely (see chart below). From this view, a drop in OER inflation is already slightly overdue.

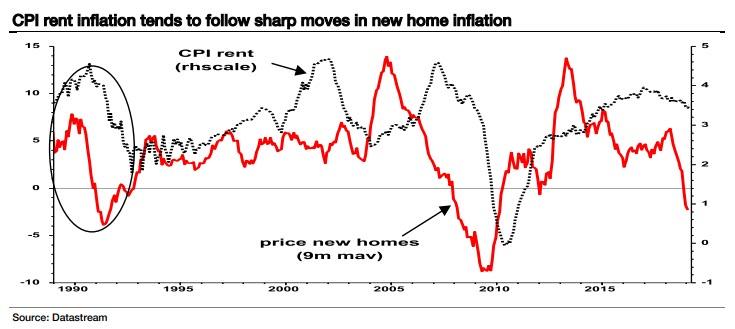

As a reminder, one week we showed that while few discuss it, growth in the US housing market has already hit a brick wall and is in fact reversing in most metros, as such it is only a matter of time before this shock reverberates across all CPI price signals.

“And therein lies the rub”, according to Edwards, who predicts that with the US housing market clearly softening rapidly, “there is good evidence that rent inflation in the US is set to plunge and take the dominant shelter component of core CPI inflation substantially lower.”

As a case study, the SocGen strategist reminds us that back in the early 1990s, a similar decline in new home inflation saw CPI rent inflation slide from above 4% to 2% (as circled below). “A similar outcome now would see core CPI move closer to 1% than the current 2%. In the market’s current mood that would be like throwing gasoline onto a government bond market that is already on fire.“

Edwards ends his latest preview of the coming deflationary apocalypse with a quote by his just as notorious deflationist peer, Russell Napier…

“What a three weeks it has been, particularly in bond markets where, ten years after the launch of QE, the prospect of deflation is priced as a clear and present danger! The good news is that we know what is coming next. The bad news is that we know what is coming next. The current war on deflation, a war lost if the shift in bond yields is to be believed, is bringing forth from the authorities not a new tactic but a whole new strategy – financial repression. So, is the financial repression, now renamed modern monetary theory/makeup strategy (ie allowing inflation above the 2% target to compensate being below for so long)/nominal GDP targeting, imminent as bond yields in New Zealand and Australia reach all-time lows and the tenyear bond yields of both Japan and Germany return to zero?”

… who argues that should the bond investors’ view on deflation be confirmed, it paves the way not for more QE, as the inequality that QE has caused has lost the Fed (and the ECB and BoE) the support of the public and politicians alike. Rather, new policies will be tried, and the trial balloons described above have already been floated by the Fed in recent speeches, ready for use in the next recession. And after 5½pp of Fed tightening, that time could even be now.

This then brings us to Edwards’ conclusion and his brief, but violent forecast of what will happen next:

The recent explosive rally in bond markets and inversion of the US yield curve signals that the next phase of the Ice Age may be arriving. Prepare for huge market moves.

Well, he didn’t call himself an uber-bear for nothing…

via ZeroHedge News https://ift.tt/2Woxc5Q Tyler Durden

Wirecard’s feud with the Financial Times has escalated to absurd new heights.

One day after Wirecard trumpeted findings from Singaporean law firm Rajah & Tann’s investigation into allegations of widespread accounting fraud at the German payments processor – a report that purportedly vindicating the company’s management – Wirecard is following through on threats to sue the British business newspaper over what Wirecard’s lawyers described as “unproven and false allegations” made in a series of blockbuster exposes.

The company has filed suit against the FT and Dan McCrum, one of the investigative reporters who helped break the story, in a Munich court, according to Reuters:

Wirecard has filed a suit at the Munich regional court against both the FT and its reporter, Dan McCrum, seeking a ruling on the merits of its case. If successful, the company would then press for monetary redress.

“Our objective is to seek a halt to the incorrect use of business secrets for the purposes of reporting, as well as damages,” Wirecard said in a statement. No comment was immediately available from the FT.

The fightback comes after the FT alleged in January that Wirecard’s Singapore staff had engaged in fraud and false accounting, basing its reporting on a law firm’s probe of allegations made by an unnamed whistleblower.

Using a preliminary copy of R&T’s reports as its primary source, the FT reported that Wirecard managers, under pressure to win approval from regulators and customers, had fudged the company’s transaction numbers. The reports suggested that the practice had been tacitly approved by the corporate office in Frankfurt, and was widespread throughout Wirecard’s global operations.

However, in its final report, which arrived at conclusions that were very different from the preliminary cited by the FT, R&T concluded that although employees involved in its Asian operations may have committed fraud, these distortions were “not material” to the company’s financial reports. Furthermore, there was no evidence to suggest that the headquarters in Frankfurt was complicit. At least, that’s what Wirecard said: The report itself hasn’t been released; Wirecard merely released a summary of the firm’s findings.

The FT wiped billions of dollars off Wirecard’s market capitalization after the paper published its first report in late January, which alleged that a Wirecard manager had used forged and backdated contracts to manipulate the company’s numbers. But on Wednesday, Wirecard shares surged nearly 30% intraday and notched their best daily performance in ten years after Wirecard released the conclusions from the R&T report.

From the beginning, Wirecard denied what it claimed were “false, inaccurate, misleading and defamatory” allegations, and almost right away, the authorities in Frankfurt appeared to side with the company. In February, German prosecutors opened an investigation into the FT reporter who broke the story. Using a tactic apparently cribbed from regulators in Beijing, Germany’s market authorities briefly banned short-selling in Wirecard’s shares (presumably for fear that it could drag down the DAX, which would weigh on broader European markets).

For its part, the FT has robustly denied allegations that its reporters were involved in some kind of shady market manipulation (see this Alphaville piece for one of the msot entertaining rebuttals we’ve ever read). While Wirecard shareholders celebrated on Wednesday, the FT published a deeper analysis of Wirecard’s statements and pointed out some inconsistencies that might have given investors pause.

via ZeroHedge News https://ift.tt/2uwKzoH Tyler Durden

The European Union has provisionally agreed on new auto safety rules that will require all cars sold within the E.U.’s 27 member countries to come with a host of new safety features, including intelligent speeding assistance (ISA)—which would prevent cars from going above the speed limit—by 2022.

The European Union has provisionally agreed on new auto safety rules that will require all cars sold within the E.U.’s 27 member countries to come with a host of new safety features, including intelligent speeding assistance (ISA)—which would prevent cars from going above the speed limit—by 2022.

Patrick Murphy, who’s likely to be executed Thursday night for his role in the 2000 murder of a Texas police officer, is not innocent.

Patrick Murphy, who’s likely to be executed Thursday night for his role in the 2000 murder of a Texas police officer, is not innocent.

{kind=link}

{kind=link}

{kind=link}