In addition to virtually every Democrat, not to mention Russiagater, there is one more party that is urging the publication of the full 300+ page Mueller report: Russia itself.

On Thursday, Russia called on the U.S. to publish in full Special Counsel Robert Mueller’s report, saying this was the best way to clear up allegations of Russian meddling in the 2016 U.S. presidential elections.

Robert Mueller arrives at his office in Washington, D.C. on March 27, 2019; source: Bloomberg

“I’d like to read the entire report,” Foreign Ministry spokesman Maria Zakharova said in an interview with Ekho Moskvy radio on Thursday. “Let them publish it in full and at least we’ll find out what it’s based on.”

Russia Foreign Ministry spokesman Maria Zakharova

As Bloomberg notes, President Trump scored the biggest political triumph of his presidency on Sunday after publication of a summary of Mueller’s report showed the 22-month investigation found no evidence of collusion between his campaign and Russian officials during the 2016 election (it was followed by icing on the cake when one day later, his nemesis, “creepy porn lawyer” Michael Avenatti was arrested for extorting Nike).

Separately US intelligence agencies concluded that Russia was behind a hacking campaign aimed at damaging Democratic Party contender Hillary Clinton and boosting Trump’s chances of victory. Even though the Kremlin continues to deny this, it remains unclear to this day why it matters if Russia or someone else was behind a leak that revealed all the dirty laundry of the DNC headed into the 2016 election, which ultimately revealed collusion against Bernie Sanders across the established Democratic apparatus and led to the resignation of former-DNC head Debbie Wasserman-Shultz.

Russian officials, who repeatedly poured scorn on allegations of collusion with the Trump campaign, were delighted by the outcome of the Mueller investigation, even as some said it would do little to ease pressure in Washington on the president over his desire to improve relations.

End of the Russiagate withchunt notwithstanding, relations between the US and Russia have continued to deteriorate in recent months, with the latest geopolitical hotspot Venezuela, now the source of consternation over which superpower will end up backing the ruling regime of the socialist country with the world’s biggest oil reserves.

Vladimir Putin eating popcorn

via ZeroHedge News https://ift.tt/2HYbFwQ Tyler Durden

Most people looking at markets right now would tell you that most markets right now are looking pretty bad. Yes, there are a few happy-clappy hold-outs both in terms of markets and people, and the latter include some central bankers. But what else can you say when the 10-year US Treasury yield is at 2.34% and the US curve further inverted? When the market is pricing in a huge chance of a Fed rate cut THIS year? When despite that fact vulnerable EM currencies are tumbling (which, by the way the Daily had flagged as a threat repeatedly – if the US is going down we are ALL going down, and the US is going to land on EM, not EM on the US): e.g., USD/BRL is heading for 4 again, and TRY has only stopped tumbling due to overnight swap rates surging past 1,300%.

And let’s not forget in Europe we’ve just seen Germany issue debt at a negative yield again for the first time since autumn 2016 AND 10-year Bund yields drop below their Japanese equivalent as Eurozone 5Y-5Y forward inflation collapses. Weren’t the ECB talking about a rate hike just weeks ago?! Mixing in the bigger picture, that’s on top of a Europe unable to agree a common stance on China or Huawei, and where yesterday saw a Wall Street Journal op-ed arguing that NATO is likely finished.

China itself is somehow still expected to get us all of this mess again, and over there industrial profits collapsed y/y. Even allowing for the timing of the Lunar New Year that does not bode well for either the economy or the over-heated stock market. Perhaps they need to build another 10-20 million empty new homes to kick the can down the road? And while the US is sending Mnuchin and Lighthizer to talk trade in Beijing this week, it is also talking about selling F-16s to Taiwan, leaning closer to Taipei, sailing ships through the Taiwan strait, hosting persecuted Uighurs at the State Department, and forcing a Chinese firm to divest from one particular US app – Grindr. (Chinese ownership of that has certainly stayed in the closet to the general public.)

Yet if you think all this is bad, yesterday’s UK Parliamentary action was far, far worse. It is often said that if you want to enjoy both sausages and law, you should never see how either is made. Well we just saw the wurst-making process in full effect. The key thing to take away from the latest debacle is that Parliament, after telling the indecisive and split Tory government to grow up and deal with Brexit like adults, showed it too is indecisive and split. In a series of indicative votes that had been flagged by the Bremain press as likely to provide a breakthrough, each and every alternative to PM May’s withdrawal deal, already rejected by historic margins twice, was….rejected! Parliament won’t back No Deal (For 160 – Against 400); or EFTA (188-231); or EFTA and the EEA (65-377); or a Customs Union (264-272); or a Customs Union and alignment with the single market (237-307); or revoking Article 50 (184-293); or a second referendum (268-295); or even contingent preferential arrangements for no deal (139-422). The same farce may happen all over again on Monday if the schedule stays the way it is.

Before then, and adding a chunk of chewy gristle into this particular sausage, Speaker Bercow also made very clear yet again that he does not intend to allow a third vote on May’s deal to come to Parliament without substantial changes. The government still seems to be ignoring that ruling and muttering about giving it one more go by some technical means this week. Yet the DUP are adamant they will not back it even if that does happen, in which case too many Brexiteers are likely to side with them, and the deal will be shot down again. That is even though May has now offered her resignation if the deal does go through – prompting Boris “Moses” Johnson to suddenly back it…talk about sausages! Yet it seems that May is now finished either way, with The Guardian bewailing that although she is the worst PM in living memory, and maybe longer, the prospects are of a hard-line Brexit leadership replacing her in both regards.

As ITV’s Daniel Hewitt states: “Unless DUP come on board we’re surely heading for a really long delay to Brexit. MPs will vote down May’s deal, then pick an alternative which she won’t implement, she’ll resign and EU will give us a long extension while Tories elect a new leader and possibly a general election.” And also the UK taking part in the EU Parliamentary election in May, in that case, which will introduce a UK-sized chunk of indigestible gristle into the EU body politic.

Like I said, from bad to wurst.

via ZeroHedge News https://ift.tt/2TC3qJ3 Tyler Durden

President Trump can still hammer crude prices lower with a tweet, but unfortunately for Larry Kudlow and Steven Mnuchin, optimistic trade headlines just don’t pack the same market “oomph” that they once did. Proof of this arrived Thursday morning, when a pair of ostensibly bullish stories from Reuters and WSJ failed to revive the market’s appetite for risk, even as anonymous US officials teased what they heralded as a “major concession” from Beijing on forced technology transfers, and a top Chinese official told a group of American tech CEOs about a proposal to lift restrictions on foreign cloud-computing companies.

First came the Reuters report, sourced to anonymous US officials, who claimed the Chinese were “talking about forced technology transfers in a way they’ve never wanted to talk about it before.” Though differences on IP and enforcement still exist, proposals from the Chinese “went further than in the past” on a range of issues, including the technology transfers, according to the senior officials.

And while this doesn’t guarantee that a deal would be reached, the officials said it’s enough to support President Trump’s claims that talks have been going “very, very well.” The officials added that talks would continue for as long as necessary – perhaps until May, or even June – so long as the progress was being made on the “core issues.”

Yet, when it comes to the US lifting tariffs, the officials confirmed that “some tariffs” would need to remain in place to ensure compliance, and that this remained a potential obstacle to a final deal.

“Some tariffs will stay,” the second official said. “There’s going to be some give on that, but we’re not going to get rid of all the tariffs. We can’t.”

[…]

“Obviously that is an issue that we need to resolve … and will be an important part of a final deal,” the first official said. He said there was some agreement on enforcement on what he termed the “backend” once a deal was in place: a structure in which both sides could raise grievances and implement tariffs if there were violations to the agreement.

Finally, the officials insisted that Trump had enough political support at home to allow him to hold out for a good deal. “Who would he be pleasing by…selling out?”

Moving on to the WSJ report, the paper said Premier Li Keqiang had disclosed a proposal during a Monday meeting with about three-dozen corporate CEOs to allow foreign cloud service providers to open “trial operations” in China. Executives from IBM Corp. , Pfizer Inc., Rio Tinto PLC, BMW AG and Daimler AG had attended the meeting. As we noted over thee weekend, access for US cloud companies has recently emerged as a major issue in the talks.

During a Q&A session, Li offered more details about what this arrangement would look like.

In response to a question about cloud computing from IBM Chief Executive Ginni Rometty during Monday’s meeting, Premier Li said Beijing is considering a “liberalization pilot” in a free-trade zone to open cloud computing to foreign companies, according to the people briefed on the matter. A key hurdle foreign providers of cloud services need to overcome, Mr. Li said, is to offer adequate “privacy protection” to their Chinese customers.

Under the cloud proposal, foreign providers would be allowed to own data centers in the free trade zone. The most likely one is in the southern city of Guiyang that’s a center for big data, people with knowledge of China’s plans said.

Still, as WSJ pointed out, there are still questions about how the flow of data out of the country would be treated.

Key questions remain: Would China allow free flow of data from the operations in the zone to the rest of the country? What kind of data services can foreign firms setting up data operations in the zone provide? What kind of customers can they offer such services to?

By offering the pilot program, Beijing is showing that it understands there will need to be some movement on this issue. However, the proposed changes might be “too piecemeal” to win Washington’s support.

“It shows that, at the minimum, they get the idea that they’ll have to show some movement in this area and they can’t stonewall the U.S. completely on this,” said Paul Triolo, an analyst specializing in global technology policy at Eurasia Group, a New York-based consulting firm. “But the devil is in the details.”

The pilot proposal, which would still allow the government to keep control of the sector, is also likely to be met with skepticism in Washington that China is moving too slowly to make any meaningful changes to what it sees as Beijing’s unfair trade practices. But Beijing officials argue China has traditionally experimented with reforms in pilot zones before ultimately implementing them nationwide.

The cloud proposal “fits China’s habit of making discretionary, piecemeal adjustments rather than outright liberalization,” said Scott Kennedy, a China expert at the Center for Strategic and International Studies, a Washington think tank.

Larry Kudlow affirmed many of the revelations made in these stories during a statement in Washington later Thursday morning, affirming that the talks were not “time dependent”. Though he did say that he expects the final deal to include “100% ownership” for foreign firms operating in China, which goes beyond the proposals discussed above.

Elsewhere, an earlier trade deal update published by the FT wasn’t nearly as positive. According to the story, talks have effectively been going around in circles, with the US handing written proposals to China, and China handing them back covered in red ink. This, per the FT, shows how successful China has been at resisting American demands, as even agreements on relatively minor details have been incredibly hard fought.

According to people briefed on the process, US officials sent proposed drafts of what could become China’s most consequential trade agreement since it acceded to the World Trade Organization 18 years ago. Then the Chinese side sent the drafts back with strike-out marks and alternative clauses, all in red.

The “red-line” documents sent back by Chinese negotiators, led by vice-premier Liu He, highlight their success thus far in resisting US demands for far-reaching structural reforms to Beijing’s state-led development model. But even agreement in less controversial areas – such as increased purchases of US exports and improved market access for foreign investors – is proving difficult to pin down.

That last report sounds more like what we have heard so far. And it raises just enough doubt that the US officials quoted by Reuters are being unduly optimistic, and the proposal shared by Li is simply that – a proposal. The only solid new piece of information is that the US now expects the talks to drag on for months, but many analysts had expected as much, anyway.

We now wait to see if China dashes the optimistic narrative with a series of its own leaks once they realize the US delegation won’t agree to lift all of the tariffs on $250 billion in Chinese exports that have been imposed over the past year since the start of the trade war.

via ZeroHedge News https://ift.tt/2FHaa4M Tyler Durden

A Los Angeles artist has found a cheesy way to make a grate point about a wedge issue in American politics.

Cosimo Cavallaro’s past projects include a 6-foot-tall milk-chocolate sculpture of Jesus and a hotel room covered in 1,000 pounds of melted mozzarella cheese. His latest effort: A 6-foot-high, 3-foot-wide wall of expired cheese in close proximity to America’s southern border. The cheese wall, which Cavallaro says he wants to extend 1,000 feet at a cost of $300,000, is meant to mock President Donald Trump’s proposed wall on the U.S.–Mexico border.

“To spend all this money to keep dividing the countries, I think is a waste,” he tells the Los Angeles Times. “You see the waste in my wall, but you can’t see the waste in [Trump’s] $10 billion wall, which in time will be removed?”

Cavallaro started building on Monday and has posted videos to Facebook documenting his progress.

According to the project’s website, Cavallaro started with enough funds for a 25-foot long wall made of 200 blocks of spoiled cotija cheese. Each block costs about $100, The Sacramento Beereports, so he’s crowdfunding the rest. A GoFundMe page has raised about $1,435 of his $300,000 goal. He’s also selling cheese-related apparel, including a “Make America Grate Again” t-shirt. (The “Grate” is actually just an image of a cheese grater.)

“The simplicity of the wall is that it shows and exposes the waste,” he adds in a promotional video. “You take a piece of cheese, and after a certain date you have to throw it. I don’t know why. Maybe that’s part of the whole system of Congress. You must waste cheese to keep making cheese here.”

While that metaphor may be a bit strained, Cavallaro is making a valid point about waste and the wall. Trump is trying to use about $8 billion of money from different sources to build the project. In reality, it will cost much more. In fact, erecting the wall is likely to cost as much as $28 billion, followed by $48.3 billion in maintenance expenses over the first decade. All this for a structure that will be ineffective at blocking both illegal immigration and illegal drugs. And don’t even get me started on all the private property that’ll be seized in the process. (There are many other reasons why building a border wall would be a bad idea, which you can read about here.)

The wall has attracted several other trolly responses. Last year there was the “Ladders to Get Over Trump’s Wall” campaign, and in 2017 the company behind Cards Against Humanity announced it had bought a plot of land on the U.S.–Mexico border in order to make it “as time-consuming and expensive as possible” for Trump to build his wall. (Though since Trump doesn’t care all that much for private property rights, it was likely for naught.)

Cavallaro’s cheese wall won’t stop Trump from building anything, so it’s a purely symbolic form of protest. But it is a very well-Krafted troll.

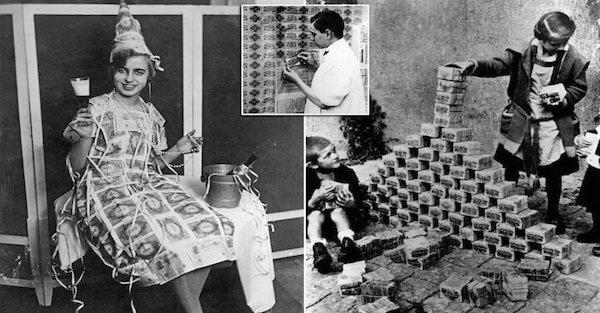

Maximilian Bern had saved up 100,000 German marks for what should have been a modest, but comfortable retirement.

But in 1923, he withdrew every last cent, and spent it all on one purchase: a subway ticket.

He rode around his city one last time before returning home, and locking himself in his home, where he died.

He didn’t kill himself. Hestarved to death… simply because he could no longer afford food. A single egg at the market would cost millions of marks, more than Maximilian Bern had saved over his entire life.

This was one of the most famous episodes of hyperinflation, certainly in modern history.

In the wake of World War One, Germany (known as the Weimar Republic) was completely broke.

The War to end all Wars had bankrupted them; and on top of losing the war, Germany was forced to make ‘reparation payments’ to the victors, including France, the UK, etc.

That took Germany’s overall war debt to impossible levels. So in a feeble attempt to keep the economy afloat and meet its war debt obligations, the German government printed massive amounts of paper money.

Prior to World War I, one US dollar was worth 4.2 German marks.

By 1923, a single US dollar was worth 4.2 TRILLION marks.

I remember the first time I went to Venezuela the official exchange rate was four bolivars to the US dollar—and the black market rate was eight to one.

The next time I went it was hundreds, then thousands and then tens of thousands of bolivars to just one US dollar.

Around two years ago when I was in Caracas, I changed a few hundred dollars and received an entire suitcase full of money in return. (I didn’t get to keep the suitcase).

The rate of inflation now in Venezuela was as high as 1.6 million percent last year. It’s difficult to even imagine what that means.

But we’ve all heard these horror stories of hyperinflation. Everyone seems to understand the horrible effects it has on the economy and individuals.

But somehow we’re supposed to believe that a little bit of inflation is somehow good for the economy. I find that absurd.

The Federal Reserve tries to keep the inflation rate between 2% and 3% per year. That might seem like chump change, but it adds up.

Even John Maynard Keynes, whose works underpin the foundation of modern central banking, once wrote:

“By continuing the process of inflation governments can confiscate secretly and unobserved an important part of the wealth of their citizens.”

It’s so subtle because it only steals a little at a time from you, over the course of many years.

But again, over time, it adds up.

As we’ve seen over the last couple decades, wages have not kept pace with inflation. So year after year, the average workers loses a little bit of prosperity.

1-2% per year doesn’t really matter. A decade or two of this, however, really has an impact.

We keep hearing these Bolshevik politicians calling for a Wealth Tax. They obviously fail to realize that a wealth tax already exists. It’s called inflation.

Ironically, Keynes continued to write about inflation, saving, “And while the process [of inflation] impoverishes many, it actually enriches some.”

And that’s true. Back in Germany’s hyperinflation days, there were a handful of sophisticated people who saw the writing on the wall. They knew that the government could never pay its debts, and that they would print money and debase the currency.

These guys set up their investments in a way to actually profit from hyperinflation.

Donald Trump famously referred to himself during the 2016 Presidential campaign as the “King of Debt” because he has been able to profit by borrowing money.

These investors in the Weimar Republic were known as the Kings of Inflation. And Hugo Stinnes was the King of Kings.

Stinnes had positioned himself perfectly for when hyperinflation hit.

He borrowed vast amounts of German marks and poured them into his coal, steel, and shipping companies.

He also kept gold in Switzerland, and made investments in foreign markets.

When hyperinflation hit, Stinnes was able to pay back his debts with the massively devalued German mark.

But Stinnes’ hard assets weren’t affected by the hyperinflation. They held their value. His businesses and investments flourished, making him one of the wealthiest men in the world.

This is just a reminder that, no matter what happens in financial markets or the global economy, there are always winners and losers.

Democratic House Intelligence Committee Chairman Adam Schiff, who made Donald Trump’s now debunked Russiagate “witch hunt” his one mission in life, furiously pushed back as all nine Committee Republicans demanded his resignation, defending his past comments by lighting into the president and his family and campaign over its contacts with Russia.

Calls from Republicans and president Trump for the Russiagate-obsessed Schiff to resign as head of the House Intelligence Committee have been loud in the days following the release of the four-page Mueller report summary. And on Thursday, the call was made right to the Congressman’s face in what Mediate described was an “explosive” clash, and The Hill dubbed a “striking display.”

At the start of the House intel hearing on Thursday morning, Rep. Mike Conaway (R-TX) called for Schiff to step down — a call which he said was supported by all nine Republican members of the committee.

“Your actions, both past, and present are incompatible with your duty of the chairman of this committee — which alone, in the House of Representatives — has the obligation and authority to provide effective oversight of the U.S. Intelligence community,” Conaway said. “As such we have no faith in your ability to discharge your duties in a manner consistent with your Constitutional responsibility and urge your immediate resignation as chairman of the committee. Mr. Chairman, this letter is signed by all nine members of the Republican side of the committee, and I ask unanimous consent that it be entered into the record at today’s hearing.”

All 9 Republicans on the House Intelligence Committee demand Democrat Chairman Adam Schiff resign: “we have no faith in your ability to discharge your duties in a manner consistent with your constitutional responsibility and urge your immediate resignation” pic.twitter.com/n1oHOn40Dn

A visibly angry Schiff responded immediately after, at which point the “clash exploded” as the Russiagate-obssessed Democrat aggressively pushed back defending his past comments by lighting into the president and his family and campaign over its contacts with Russia.

“My colleagues may think it is OK the president’s son was offered dirt as part of an effort to help Trump,” Schiff said in his statement.

“You might think it is OK. I don’t,” Schiff added, his voice rising as he went on.

In their letter, Republicans impled that Schiff was involved in or aware of leaks of committee information that fueled speculation about collusion.

“Your repeated public statements, which implied knowledge of classified facts supporting the collusion allegations, occurred at the same time anonymous leaks of alleged intelligence and law enforcement information were appearing in the media,” the letter reads.

“These leaks, often sources to current or former Administration or intelligence officials, appeared to support the collusion allegations and were purported to be related to ongoing investigations of President Trump and his associates.”

The letter also notes that committee Republicans also found no evidence of collusion involving the campaign. They released a report April 27, 2018, that laid out the results of the investigation, however, Schiff has vowed to resume the investigation, with a focus on Trump’s financial dealings and whether Trump associates have worked under the influence of Russia.

“Despite these findings, you continue to proclaim in the media that there is ‘significant evidence of collusion,’” reads the letter.

And while Schiff, or as Donald Trump Jr calls him “FullOfSchiff” may plan to keep kicking a dead horse for a long time, the social media response was quick and was largely split along party lines:

#Breaking@ConawayTX11 introduced a letter signed by all the Republicans of the House Intel Committee calling on @AdamSchiff to resign…what do you think?

WATCH: GOP House Intel members call on #RussiaHoax truther Adam Schiff to resign as Chairman of the House Intel Committee for knowingly and repeatedly lying to the American people about collusion. He has been exposed as the fraud he truly is! #FullOfSchiffpic.twitter.com/E9nPOj68XL

If Adam Schiff does not resign from this intel committee post, there is no level of incompetence and cynicism that could ever warrant resignation from it https://t.co/bkjePWKikj

.@RepAdamSchiff-Thank you for speaking out for the American people. Thank you for reminding Republicans on your Committee that the Trump campaign colluded with Russia, and that there’s indisputable evidence backing that up. Well done, Chairman. You’re a patriot. We got your back.

House Republicans on intel committee during hearing on Russian influence operations attack @RepAdamSchiff and call for him to be removed as chairman, claiming he is biased. FLASHBACK: the previous GOP chair was @DevinNunes, who acted as Trump’s poodle.

Chris Heitman, the owner of a successful auto racing supplies business in Wisconsin, is getting hounded by out-of-state revenue officials trying to collect sales taxes for online transactions. Reasondetailed his plight earlier this month.

After years of congressional inaction on the question of whether internet retailers should have to pay state-level sales taxes, the U.S. Supreme Court last year upheld a South Dakota law allowing the state to collect taxes from businesses that make at least 200 transactions or do $100,000 of gross sales into the state. That decision, in Wayfair v. South Dakota, set off a mad scramble in other states to set similar standards for taxing out-of-state businesses. States are eyeing a windfall of revenue by targeting online sellers like Heitman—New Jersey, for example, plans to collect $3 billion in sales taxes this year from businesses outside the state—in what can be described literally as taxation without representation.

For Heitman and other owners of small and mid-sized businesses, that means having to get up to speed on tax codes in 45 different states. (The five other states have no sales tax.) It’s not as simple as looking up what rate to pay; state sales tax codes are notoriously complex.

This week, Heitman emailed to tell me about a “tremendously complicated and expensive compliance labyrinth” he’s encountered in Kentucky.

Heitman says his business made $1,500 in profit on roughly $38,000 in gross sales over 299 transactions in Kentucky during 2018. Because the number of transactions is high enough to trigger the new post-Wayfair standard, he owes sales taxes to the state. It’s going to cost at least $750 to having his accounting firm prepare the 17 pages of tax forms the Kentucky Department of Revenue sent him, he says, and that’s not counting the expense of actually paying the tax itself.

“Tax compliance costs will ensure an actual net loss on Kentucky sales,” he writes. “We would be better off putting a notice on our website saying that we can no longer ship any orders to Kentucky.”

It’s Congress that must ultimately address the chaos created by the Wayfair ruling, as this is plainly a question of regulating interstate commerce. You’d rarely lose by betting against congressional action, but a bipartisan bill introduced Wednesday offers a glimmer of hope for entrepreneurs like Heitman.

The Online Sales Simplicity and Small Business Relief Act, introduced by Rep. Jim Sensenbrenner (R–Wisc.) and cosponsored by Reps. Jeff Duncan (R–S.C.), Anna Eshoo (D–Calif.), and Zoe Lofgren (D–Calif.), would ensure that states cannot require remote online sellers to collect sales tax retroactively on transactions made before January 1, 2019. That gives small businesses at least the rest of this year to adjust to the Wayfair landscape, freeing Heitman from having to pay taxes to Kentucky, and any other states, for sales made during 2018.

More importantly, it would exempt sellers who gross less than $10 million in annual sales from owing taxes to other states. That’s a much higher threshold than the 200 transactions/$100,000 standard created in Wayfair, and it would mean that Heitman’s $38,000 in Kentucky sales would remain tax-free.

That exemption would be repealed, the bill says, if states agree to a simplified sales tax compact that is approved by Congress. In the long term, that’s probably the best way for states to collect remote sales taxes. Rather than having to comply with all sales tax rules in 45 different states, a simplified compact might see all states agree that cross-border sales will be taxed at a single, flat rate.

Until a compact like that exists—and it likely won’t exist unless Congress gives states a strong incentive to agree to one—Sensenbrenner’s bill would protect small and mid-sized online businesses from being hounded by out-of-state taxmen.

By now you’ve probably read a gazillion opinions on the inverted yield curve and seen a ton of analogs being discussed. On the yield front the general bullish consensus seems to suggest to simply ignore it. Like everything else. On the analog front I see references to examples such as 2016 (the earnings recession will be temporary) and 1994 (the yield inversion is a fake out and it won’t matter) and similar. The general consensus: Ignore the inverted yield curve, buy stocks.

My position remains: More open-mindedness and less certitude. How can anyone actually know what is to be ignored and what isn’t?

I suppose if the argument is simply that central banks are dovish and that is good enough then perhaps that is good enough:

No ECB rate hike in 2019.

Probably no rate hike here either, and a coin flip for a rate CUT.

And perhaps it is. I don’t know. It’s worked for 10 years, maybe it will work again.

Maybe central banks can once again render all negatives moot. Yet there are a lot of issues to be mindful of and I listed some of these in Chasing Reality and The Reckoning. The macro wheels are turning.

So an inverted yield curve is bullish and you should buy every dip? Let me at least test this theory by looking at a case a lot less mentioned.

Last year I mentioned the 2000/2001 case quite a bit (see also Imbalance).

What was so interesting about 2000/2001? We had a blow-off top move in tech, markets made a major top, there were multiple 10% moves and an increase in volatility and then something unique happened: A yearly low in December. Sound familiar? It should as the ghost of 2001 is making appearances all over this market.

Back then I said, following this analog, we could see a multi-week rally emerge from the December lows and it did. This one here going even farther than back in 2001.

Let me say upfront here, I’m always cautious with analogs because no situation, economy or market is the same and things always change, hence nothing is like for like.

But in light of the similarities and the now found certitude that an inverted yield curve is something to ignore let’s take a quick peak here how conducive that yield curve inversion then was to buying stocks.

Here’s the current situation:

We had a blast off in January 2018 followed by a 10% correction, a top in September, followed by a 20% correction and now a 21% rally for a, currently, lower high, all the while the yield curve flattening and now resulting in an inversion.

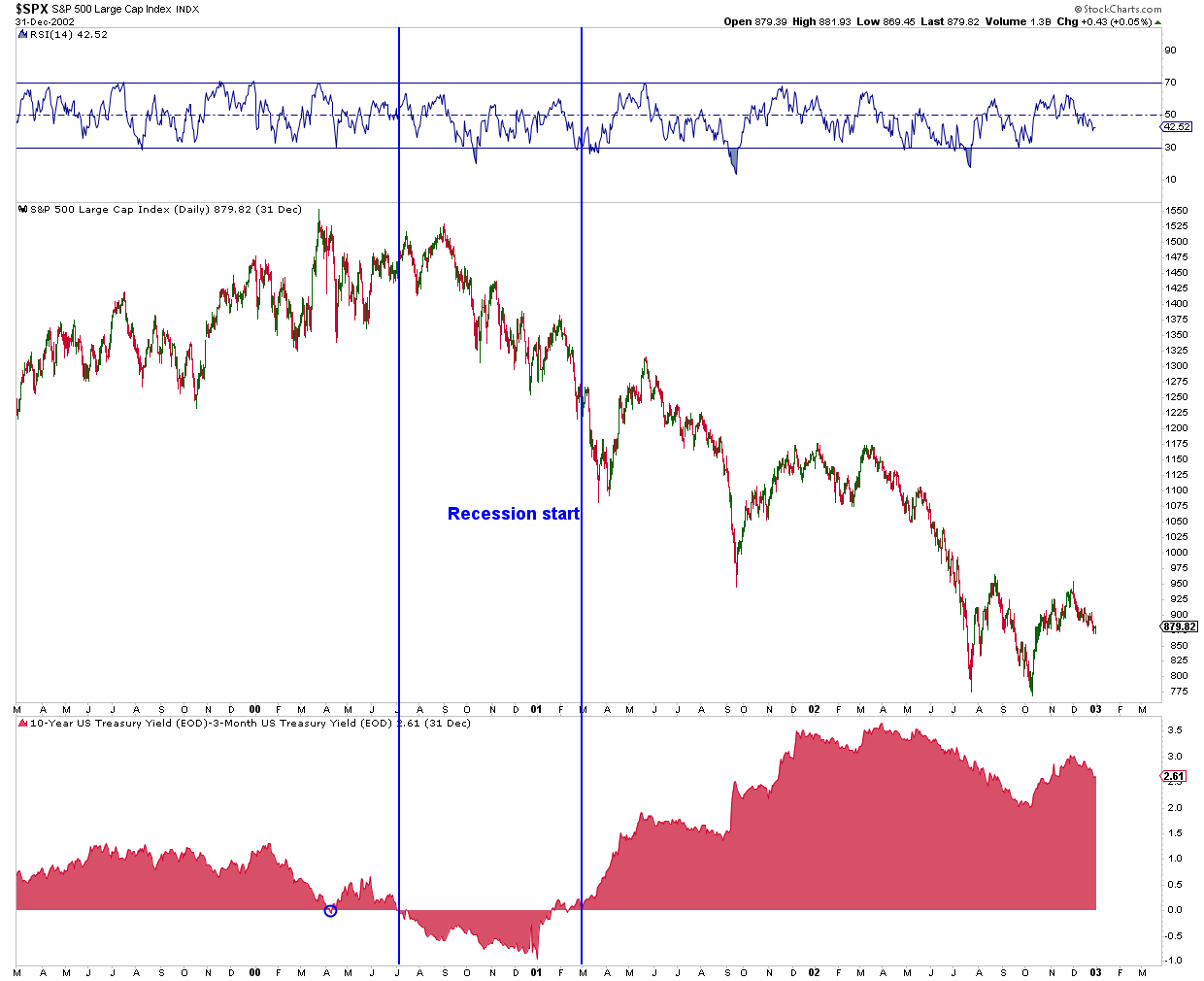

As I said no situation is alike, but here’s how all this played out in 2000-2001:

There was a little fake out inversion following the March 2000 top, but then the inversion really got started in July. Yes there were rallies even in the 2 months following the inversion, but as should be clear markets started trending down following a lower high. The recession officially started in March 2001, or a mere 8 months after the initial inversion and the rest is history as $SPX dropped 50% from its highs and didn’t bottom until late 2002.

In this scenario, where was the inversion of the yield curve bullish for equities? The answer is obvious: It wasn’t bullish for equities. Yes you had rallies, but they were opportunities to sell.

Now I’m the first to say I have no clue how this inversion here plays out. Maybe it’s an initial fake out as in April 2000 and that buys equity markets some more time in chopping around, and perhaps we get some more yield curve optimism as we apparently saw in the summer of 2000. Or maybe it all plays bullish as central banks are now dovish and that’s all there is to it.

All I’m saying is this 2000/2001 scenario is a case of an inversion of the yield curve following a very long business cycle and hyper bull market that was not bullish for stocks at all. I don’t see this being discussed anywhere hence I thought it’s worth pointing out.

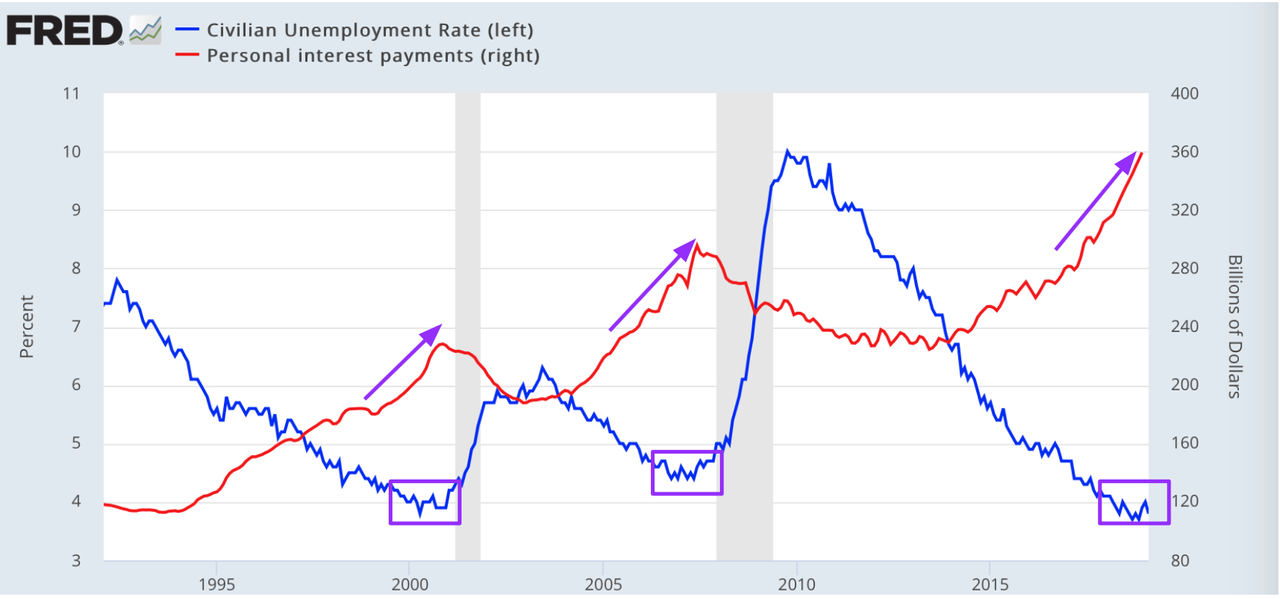

And perhaps I’ll finish off with another little nugget here. Don’t forget we are at a point of cyclical low unemployment and, coincidental or not, personal interest payments are rising aggressively. Oddly enough that sudden acceleration in personal interest payments coinciding with a cyclical low in unemployment is precisely what we saw during the end phase of the previous two bull markets:

Aren’t analogs fun to ponder?

Look, nobody has access to the holy grail here, but dismissing the yield curve inversion as a fluke or fake out given the history outlined above is to be in denial about the alternative outcome possibilities, hence my tweet this morning:

Yield curve denial is the new climate change denial

The ghost of 2001 is all around us. Can anyone else see it, or am I just victim of an apparition? Either way it’s giving me goosebumps hence I’m keeping an open mind.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2HYlNpj Tyler Durden

Pending Home Sales fell 1.0% MoM (against expectations of a 0.5% decline)

Lawrence Yun, NAR chief economist, is (surprise, surprise) optimistic…

“In January, pending contracts were up close to 5 percent, so this month’s 1 percent drop is not a significant concern,” he said.

“As a whole, these numbers indicate that a cyclical low in sales is in the past but activity is not matching the frenzied pace of last spring.”

Yun added that despite the growth in the West, the region’s current sales are well below the sales activity from 2018.

“There is a lack of inventory in the West and prices have risen too fast. Job creation in the West is solid, but there is still a desperate need for more home construction.”

Yun pointed to year-over-year increases in active listings from data at realtor.com to illustrate the potential rise in inventory.

Denver-Aurora-Lakewood, Colo., Seattle-Tacoma-Bellevue, Wash., San Diego-Carlsbad, Calif., Portland-Vancouver-Hillsboro, Ore.-Wash., and Nashville-Davidson-Murfreesboro-Franklin, Tenn., saw the largest increase in active listings in February compared to a year ago. Yun added that he does not anticipate any interest rate increases from the Federal Reserve in 2019.

“If there is a change at all, I would say the Fed will lower interest rates in 2019 or 2020. That would stimulate the economy and the housing market,” he said.

“But the expectation is no change at all in the current monetary policy, which will help mortgage rates stay at attractive levels.”

However, this is the 14th month in a row of annual declines in pending home sales…

This is the longest stretch of declines since 2008.

via ZeroHedge News https://ift.tt/2FyodbG Tyler Durden

“The simplicity of the wall is that it shows and exposes the waste,” he adds in a

“The simplicity of the wall is that it shows and exposes the waste,” he adds in a

Chris Heitman, the owner of a successful auto racing supplies business in Wisconsin, is getting hounded by out-of-state revenue officials trying to collect sales taxes for online transactions. Reason

Chris Heitman, the owner of a successful auto racing supplies business in Wisconsin, is getting hounded by out-of-state revenue officials trying to collect sales taxes for online transactions. Reason

{kind=link}

{kind=link}

{kind=link}