FOSTA’s first test? Because the Human Trafficking Grifter Industry hasn’t yet settled on a post-Backpage.com scapegoat (Asian massage parlors are getting there, but haven’t reached full-blown Satanic Panic territory yet), the next wave of “anti-sex-trafficking” lawsuits will apparently go after any service that allegedly enabled Backpage in allegedly enabling exploitation. The first target is Salesforce, a cloud software company.

Backpage was able to beat civil suits like this because Section 230 of the Communications Decency Act prevented them, under the foundational internet principle that web platforms and internet service providers shouldn’t be treated as the speaker of every message they transmit. To do so would put the web and social media as we know it out of business.

But FOSTA, signed into law last year, amended Section 230 so that any digital platform that facilitates prostitution can be taken to court as a sex trafficker. Now a class action lawsuit is doing just that.

The suit, filed in San Francisco Superior Court, says that Salesforce is among the “vilest of rogue companies” because its “data tools were actually providing the backbone of Backpage’s exponential growth.” It alleges that Salesforce is responsible for helping power legal speech on a legal website that was sometimes used by deceptive actors to ill ends.

You see where all this leads, right? Backpage and FOSTA tested the waters. Congressional conservatives and liberals are now talking about carving out more exceptions in Section 230 or abolishing it entirely. That would allow not just any politically disfavored platforms but anyone that provided any services to them—cloud companies, payment processors, any kind of software, vendors, etc.—to be sued or charged criminally. It could make it completely untenable for many such services to work with companies that let user-generated, social, free speech flourish. That’s the end goal. Don’t be fooled by the cynical “sex trafficking” spin.

A housekeeping note:Lately, local and national media has been brimming with legislation, investigations, and other news related to sex work. Because I’m woefully behind in blogging about these developments, today I bring you a very special episode of Reason Roundup devoted entirely to sex policy. Let’s take a whirlwind tour of the good, bad, and bizarre of it. Carrying on…

Robert Kraft Update

Florida police have been trying to strike deals with the men they charged in massage-parlor prostitution stings in and around Palm Beach. County prosecutors offered to drop misdemeanor solicitation charges against New England Patriots owner Robert Kraft and other men if they would take classes about why prostitution is bad, pay a $5,000 fine, do community service, and (in what’s known as an Alford plea) say that the state had enough evidence to have found them guilty if the case had gone to trial. Kraft—who has pleaded not guilty—said no way. Now his lawyers are pushing for the case to not only go to trial but be heard before a jury, not just a judge.

Kraft was one of 24 men targeted by Palm Beach County police. Prostitution stings in neighboring counties—joined by the Department of Homeland Security—led to the arrest of around 275 more men on misdemeanor charges of soliciting prostitution, authorities say. No one was charged with sex trafficking, abduction, assault, compelling prostitution, extortion, or any other charges that involve violence, force, coercion, minors, human smuggling, or fraud. The middle-aged women working at the raided spa and massage businesses are, however, having their assets taken by the county as they sit in jail on various prostitution charges.

Florida Solicitation-Registry Fail

Florida lawmakers have for now ditched plans to create a registry of prostitution clients. A new “human trafficking” bill would have put anyone convicted of solicitation on a special public database. That part failed, after sex workers and activists showed up at the House Criminal Justice Subcommittee to protest and give testimony. Clearwater resident Grace Taylor told the hearing: “I am your neighbor. I am your co-worker. I am the person in the grocery store. I am also a consensual sex worker, and as such, I am the first line of defense in helping you find those who have been trafficked.”

A version of the legislation passed the committee without the solicitation registry included. “This bill, as amended, has made a considerable improvement,” Christine Hanavan of SWOP Behind Bars tellsFlaPol. “We’re glad that we were heard on striking that registry.”

The bill is still, as the kids say, problematic. It requires that cleaning and reception-desk staff at hotels and motels be trained on spotting the “signs” of trafficking—a list of absurd and ordinary behavior that includes not wanting cleaning service—and creates new regulatory liabilities on hospitality businesses that don’t actually help anybody but state coiffers

But sponsoring Sen. Lauren Book (D-32nd District) has showing a willingness to work with sex workers on crafting legislation that doesn’t unnecessarily target them—unlike Rep. Heather Fitzenhagen (R–Fort Meyers), author of the failed solicitation registry idea. “In case it was lost on you, a consensual sex worker, A.K.A. a prostitute, is committing a crime,” Fitzenhagen said. “It is not my intent to work with them going forward.”

“I’m not sure what’s scarier, the idea of putting people permanently on a public list, or aggressively incentivizing hotels to pry into the sex lives of their guests,” says Kaytlin Bailey, director of communications for the advocacy group Decriminalize Sex Work.

D.C. Activist Alleges Entrapment

Dee Curry, 64, a longtime activist and a newly appointed member of the District of Columbia’s committee on street harassment, is speaking out about her recent arrest by D.C. police. Curry told the city’s Committee on the Judiciary and Public Safety yesterday that she was charged with misdemeanor solicitation for prostitution in February as part of a coordinated sting.

Curry “said she considers the police tactics used to arrest her as a form of entrapment that she feels the LGBT community and the public at large should view as a misuse of police resources to target commercial sex workers, especially trans sex workers,” reports the Washington Blade. She maintains that she is not currently involved in sex work and was not soliciting the police officer who picked her up posing as an Uber driver. “Curry disputes the quotes that the [police] transcript attributes to her,” says the Blade:

Curry said she wants to publicize her arrest as a means of drawing attention to what she believes is a misguided policy by D.C. police and some in the community to address the issue of commercial sex work through arrests. She noted that when the undercover officer posing as the Uber driver gave the signal, three or four police cars with flashing lights and sirens rushed to the scene, with at least two officers in each of the cars, to arrest her. In thinking back on how her arrest unfolded Curry said she believes the half dozen or more officers involved in her misdemeanor prostitution arrest could have been better utilized to address the city’s growing problem of violent crime.

For information on efforts to decriminalize prostitution in D.C., see decrimnow.org.

Denying Sex Workers the Vote in Florida

Florida voters approved a constitutional amendment last November to automatically restore voting rights to people with felony convictions “who have completed all terms of their sentence, including parole or probation.” But in hashing out the details, legislators keep trying to subvert the will of the people and declare various groups beyond the scope of those deserving the vote. Right now, this includes people convicted of prostitution (a misdemeanor on offenses one and two) three times and adult entertainment businesses that break zoning laws.

Condoms as Evidence in California

A sting in Sacramento earlier this month “crystallized” the fact that “despite what law enforcement officials tell the public about their efforts to crack down on traffickers and pimps, they continuously arrest many more of the women they say are likely to be exploited,” writes Raheem Hosseini at SN&R Extra. Ten young women were arrested after offering paid sexual activity to undercover officers who had been sent out. Arrest notes state most of the women were carrying unused condoms—which counts as evidence officers can use to make a prostitution case in court. A new state bill (Senate Bill 233) would put an end to this practice. “Using condoms as evidence of sex work is terrible policy and undermines anti-HIV efforts,” Sen. Scott Wiener (D–San Francisco) told the paper. “We should be encouraging safer sex practices, not criminalizing them.”

NXIVM + Michael Avenatti?

An update on NXIVM, the cult-like women’s group accused of being a sex-trafficking operation:

BREAKING: Seagrams heiress Clare Bronfman faints in court after judge seems to suggest that Michael Avenatti was secretly representing her, trying to negotiate deal with US attorney’s office in NXIVM case. An ambulance has been called.

Bronfman is gone, back in court tomorrow. Led to a car on Gergagos’ arm. Geragos declined to answer any questions, saying they would be answered tomorrow when her curcio hearing resumes.

We want migrant massage working and sex working community members to know that we have their back! We know that when workers’ are able to organize and self-determine conditions for their labor our communities are safer and can thrive! #CopsOutOfParlors#MigrantPowerpic.twitter.com/mPcEvZOtmq

Karina Samala: “To me, it should be legalized. Everybody uses sex to get what they want from their partners. Husband and wives use sex to get what they want. Husbands, boyfriends, girlfriends use sex to get what they want from their partners. What’s wrong with two consenting adults having sex in private? What’s wrong with that?” —the longtime Los Angeles activist talking on The Advocate‘s podcast

The impact of end demand: Policies that criminalize paying for sex while treating sex workers as victims are known abroad as the Nordic Model and in the U.S. tend to get described as “End Demand” policy. A new policy brief from the Global Network of Sex Work Projects (NSWP)—The Impact of “End Demand” Legislation on Women Sex Workers—looks at “how these laws not only fail to promote gender equality for women who sell sex, but actively prevent the realisation of their human rights.”

I’m going to be having a weekly ramble @SlixaUS that wraps up the week in news & politics! I’m really excited and hope it’s helpful to stay on top of things! https://t.co/UuyqxZReWT

Irish sex workers are pushing back agains the Nordic Model:

Laws that criminalise sex buyers are making life more dangerous for sex workers in Ireland – sex workers are forced to work alone, and violent attacks are up 92%https://t.co/PRvjNoA8Y3@SWAIIreland#DecrimForSafety

A bill in Rhode Island would create a study group on the decriminalization of prostitution:

I am honored to have the opportunity to support Rhode Island’s H 5354 Which would create a special commission to investigate the health and safety impact of differing policies governing sex work. https://t.co/jeLxyC3s5upic.twitter.com/uBTx1JBZyd

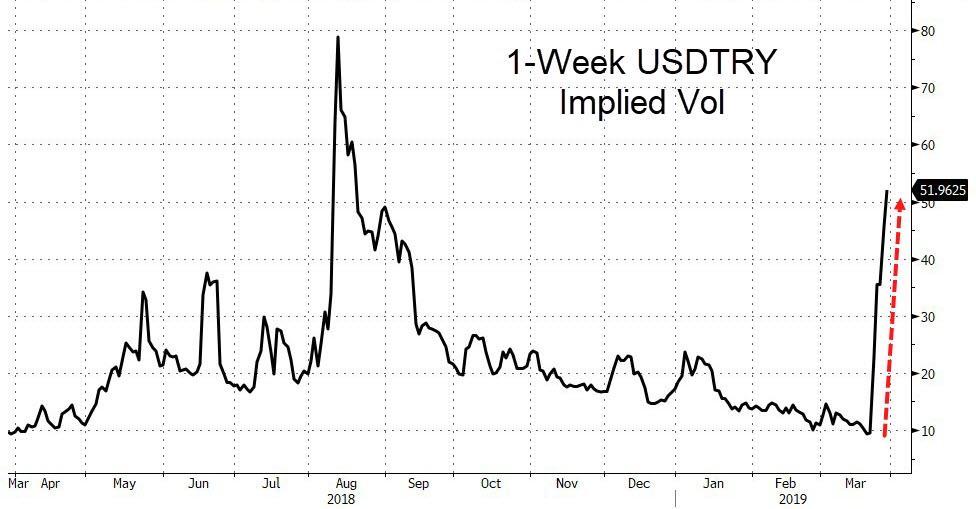

We have extensively documented the ongoing collapse of Turkey’s financial system in the last few days as Reserves plunge, credit risk soars, and the currency plummets…

…but Bloomberg macro strategist Mark Cudmore warns this is far more than just a ‘Turkey’ issue:

“The extraordinary stress currently seen in Turkey’s lira funding market may appear to be a niche issue, but the repercussions will be far-reaching.”

Via Bloomberg,

Many commentators expressed surprise or even disbelief that ructions in the lira swap market caused knock-on effects from Sao Paulo to Jakarta. Yet the transmission is real. And it will persist, thanks to value-at-risk (VAR) limits and volatility targeting

Due to recent policy measures making Turkish lira funding prohibitively expensive — one-week lira implied yields closed at 280% Wednesday — it’s become almost impossible for many foreign investors to sell the lira.

This isn’t just about making it too expensive for short-sellers to borrow the currency. The problem also applies to those who are long lira and wish to exit their positions; they are trapped as it’s too costly to unwind their FX swaps.

This lack of liquidity has effectively prevented the lira depreciating even more significantly. But this isn’t a sustainable equilibrium, as VAR metrics and risk departments will be screaming to cut Turkey exposure.

Illustrating the pressure for exodus: Wednesday was the worst session for the benchmark equity index since July 2016 and Turkey’s bonds have also been walloped.

The contagion comes from these long lira positions that are essentially stuck. If funds don’t want to pay the cost to exit, the Turkey-induced jump in VAR measures force them to reduce positions elsewhere.

This mainly applies to EM funds, given that Turkey’s well-known challenges would have kept away a broader set of investors.

Local Turkish elections are looming, and there’s speculation that funding rates will subside once they are done, allowing investors an easier exit.

The anticipation of how things will play out can be seen in one-week lira volatility, which is at 53% today, up from 9.4% a week ago. (Moves have been exacerbated as some attempted to start covering lira exposure through options).

This creates a feedback loop. The jump in volatility bets based on expectations of a looming exit causes a secondary impulse to feed through to VAR and volatility-risk metrics, putting yet more pressure for investors to reduce positions.

And there’s a longer-term wave to this as well. Turkey has a large weighting in various EM bond indexes. So passive funds are staying invested for now. But what happens when retail investors see the size of their losses on this exposure?

Longer-term, the consequences of declining lira trading liquidity may spur views on Turkey’s membership in EM bond indexes.

This Turkey story is big enough that all global investors should get on top of what’s happening. Lira swap and volatility tickers will soon be on Bloomberg launchpads globally

via ZeroHedge News https://ift.tt/2uviXjM Tyler Durden

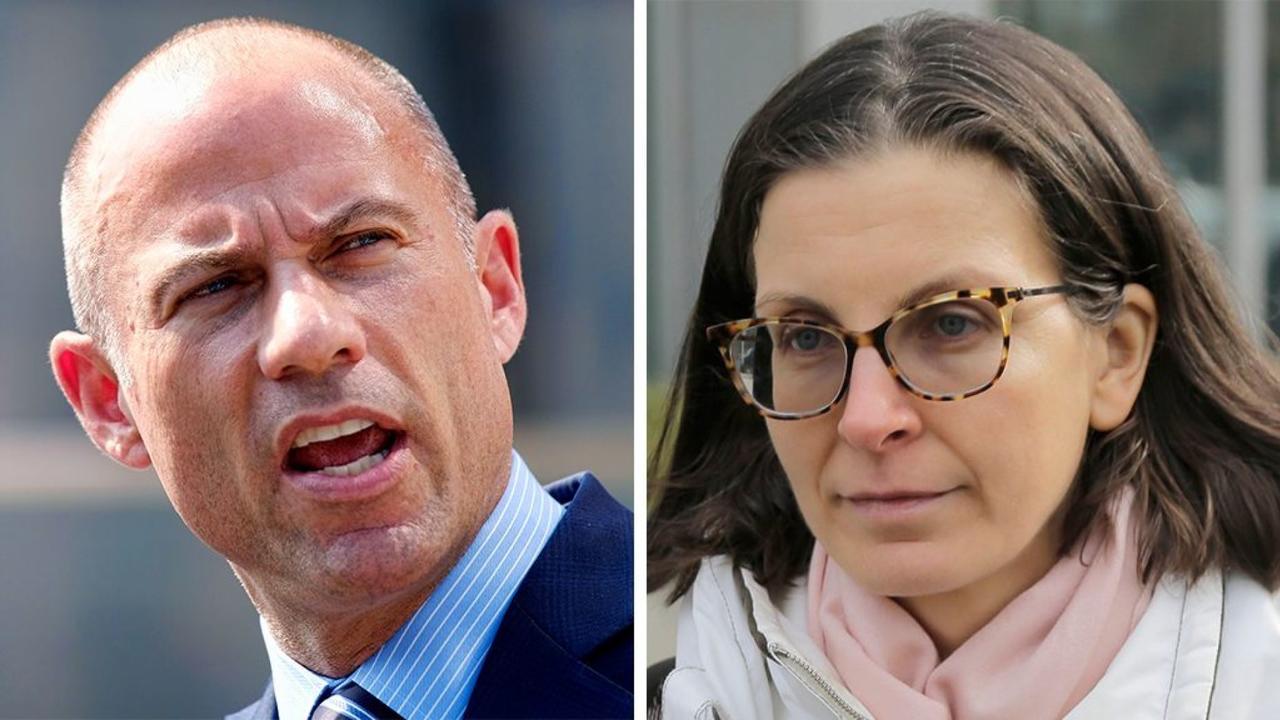

Seagram heiress Clare Bronfman had a dramatic day in court Wednesday where the accused NXIVM sex-cult financier fainted in response to being asked if she’d secretly retained lawyer Michael Avenatti.

BREAKING: Seagrams heiress Clare Bronfman faints in court after judge seems to suggest that Michael Avenatti was secretly representing her, trying to negotiate deal with US attorney’s office in NXIVM case. An ambulance has been called.

Michael Avenatti and Seagram heiress Clare Bronfman (AP)

The 39-year-old daughter of late Seagram CEO Edgar Bronfman (whose funeral Hillary Clinton spoke at) pleaded not guilty last July to charges of racketeering, money laundering and identity theft for NXIVM – a secretive multi-level marketing company founded by Keith Raniere, who was arrested last March along with Smallville actress Allison Mack on federal charges which include sex trafficking, forced labor, wire fraud conspiracy, human trafficking and other counts.

Keith Raniere

Mack allegedly procured women for Raniere – who required that prospective “slaves” upload compromising collateral into a Dropbox account. One such recruit-turned-coach was India Oxenberg – daughter of Dynasty actress Catherine Oxenberg, whomet with prosecutors in New York in late 2017 to present evidence against Raniere.

Allison Mack

According to a 2010 Vanity Fair report, Clare and her sister Sara Bronfman, who joined NXIVM in 2002, contributed approximately $150 million of their trust fund to NXIVM, while Claire bought 80% of Wakaya island off the coast of Fiji for $47 million in 2016.

[I]n the last six years as much as $150 million was taken out of the Bronfmans’ trusts and bank accounts, including $66 million allegedly used to cover Raniere’s failed bets in the commodities market, $30 million to buy real estate in Los Angeles and around Albany, $11 million for a 22-seat, two-engine Canadair CL-600 jet, and millions more to support a barrage of lawsuits across the country against nxivm’s enemies. Much of it was spent, according to court filings, as Sara and Clare Bronfman allegedly worked to conceal the extent of their spending from their 81-year-old father and the Bronfman-family trustees. –Vanity Fair

Last July Clare was charged with a broad range of crimes connected to the cult’s operation, and is currently being represented by attorney Mark Geragos – identified by the Wall Street Journalthis week as a co-conspirator in an alleged scheme by Michael Avenatti to extort $20 million from Nike. Avenatti was arrested on Monday and released on a $300,000 personal recognizance bond.

Bronfman and Geragos leave Brooklyn Federal Court on Wednesday

NXIVM’s Clinton connection

Raniere was run out of Arkansas in the ’90s by then-Governor Bill Clinton’s attorney general on charges of fraud and business deception. After paying fines, Raniere and NXIVM executives would go on to donate $29,900 to Hillary Clinton’s 2006 presidential campaign a decade later. Meanwhile, at least three NXIVM officials are “invitation-only” members of the Clinton Global Initiative, according to the New York Post.

Edgar Bronfman Sr. receiving the Presidential Medal of Freedom from President Bill Clinton in 1999

Most recently, Raniere was accused of having sex with children and producing kiddie porn, to which he has pleaded not guilty.

Raniere, 58, is accused of having a child “engage in sexually explicit conduct for the purpose of producing one or more visual depictions of such conduct, which visual depictions were produced and transmitted,” reads a new indictment released Wednesday.

Raniere’s co-defendants, “Smallville” actress Allison Mack, Seagram heiress Clare Bronfman, Lauren Salzman and Kathy Russell were allegedly aware of his predilection for predation, and even facilitated it, according to prosecutors, who have now charged them for that conduct under a racketeering count.

His co-defendants “were aware of and facilitated Raniere’s sexual relationships with two underage victims: (1) a fifteen-year-old girl who was employed by Nancy Salzman and who – ten years later – became Raniere’s first-line ‘slave’ in DOS,” the filing reads. –New York Post

Both Mack and Bromfman are seeking a separate trial in the wake of the pedophilia charges. Mack’s attorneys argued in a recent filing that “The Court should not allow evidence of Child Exploitation Acts before any jury that will judge Ms. Mack. As an initial matter, any evidence of the alleged Child Exploitation Acts would highly and unfairly prejudice Ms. Mack, who has no connection whatsoever to these new predicate acts or the substantive counts against Raniere,” adding “Given the well-recognized inflammatory effect of such allegations, the Court should sever Ms. Mack from Raniere and order a separate trial.“

Experts in branding

While NXIVM describes itself as a self-help business that has helped thousands of people “reach their potential” through various courses, the women’s-only “inner sanctum” led by Raniere is known as ‘DOS’, which whistleblower Frank Parlato said stands for “dominus obsequious sororium” – Latin for “master over the slave women”. Once they are a member – or “slave” – they are allegedly encouraged to recruit new women into their “slave pods”, stop dating, and be on call 24 hours a day after being branded with Raniere’s initials below the hip using a cauterizing iron.

We wonder if Michael Avenatti knows anyone with an NXVIM scar?

Bronfman faces up to 20 years in prison if found guilty. Good thing she’s got Jussie Smollet’s attorney – though no word on whether Michelle Obama’s former Chief of Staff will put in the good word.

via ZeroHedge News https://ift.tt/2FBEegM Tyler Durden

Last year, I wrote an article entitled “The Upcoming Bond Bull Market,” which, at the time, was pushing against the mainstream consensus which was predicting rates could only go higher. I am updating that article with the latest data points as the overall thesis of “why” we have remained bullish on bonds since 2013 remains intact.

As we said at the time as yields were hitting some of the highest levels seen in the last decade:

“The worse things seem, the better the opportunities are for profit.”

Such is the very nature of investing.

Baron Rothschild, an 18th-century British nobleman and member of the Rothschild banking family, once said:

“The time to buy is when there’s blood in the streets.”

He should know. Rothschild made a fortune buying in the panic that followed the Battle of Waterloo against Napoleon.

Warren Buffett once said the same:

“Be fearful when others are greedy, and greedy when others are fearful.”

In other words, going against the crowd often yields the most successful outcomes.

This is the essence of contrarian investing.

Contrarian investors have historically made their best investments during times of market turmoil. During the crash of 1987 (also known as “Black Monday”), the Dow dropped 22% in one day in the U.S. In the 1973-74 bear market, the market lost 45% in about 22 months. The “Great Financial Crisis” of 2008 saw asset values get cut in half. The list goes on and on, but those are times when contrarians found their best investments.

But being a contrarian is extremely difficult. As Howard Marks noted:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, since momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’)

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

However, as behavioral analysis shows, investors always do the opposite of what they should do – they repeatedly “buy high” and “sell low.”

This is why being a contrarian is both lonely and tough.

Let me ask you a question: If you could buy the stock market today at a 50% discount – would you?

The obvious answer is “Yes.”

However, you had that opportunity in 2009 and most investors were “selling,” not “buying.” Why? Because the emotions of “fear” and “greed” consistently screw up our investing strategies.

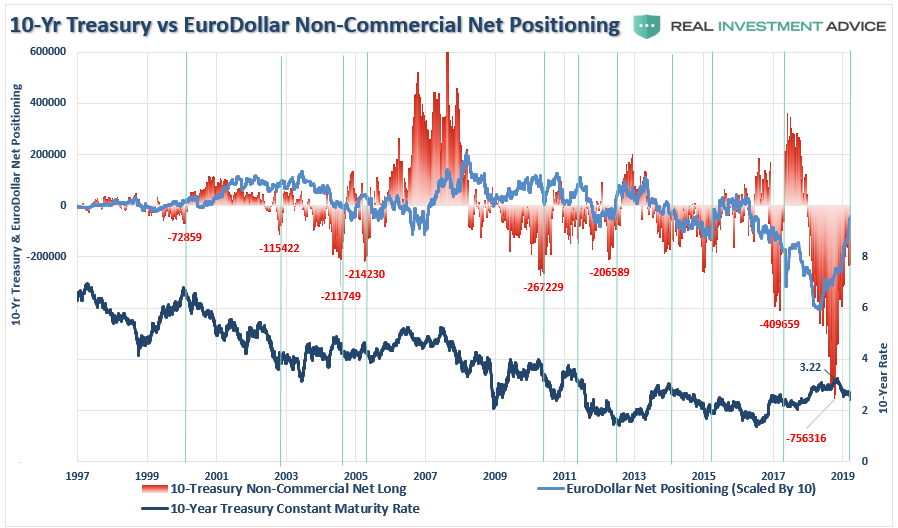

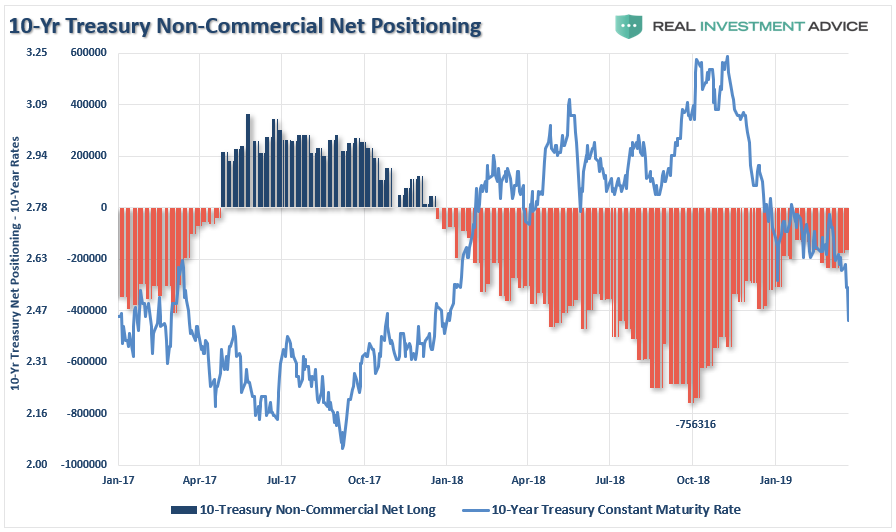

Last year, there was a glaring “contrarian” opportunity to buy Treasury bonds. As I noted then:

“With bond traders more short than at any point in history, the ultimate ‘reversion to the mean’ in Treasury’s will drive rates towards zero.”

Updated Note:I have left the last position when I wrote the article labeled so you can see the reversion since that time.

“The chart below strips out all periods EXCEPT where net-short bond positions exceeded 100,000 contracts. In every case, interest rates turned lower.”

But yet, despite the massive “one-sided bet on bonds,” investors couldn’t wait to sell.

That’s okay – we were buying.

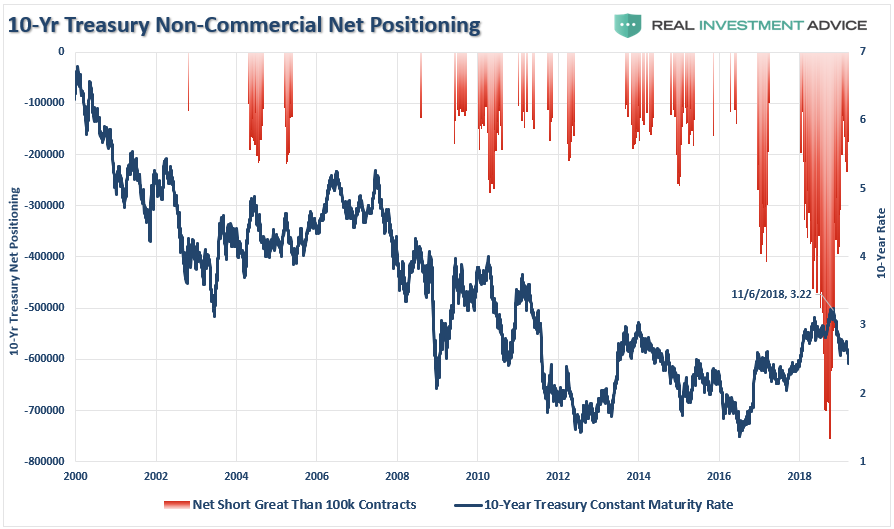

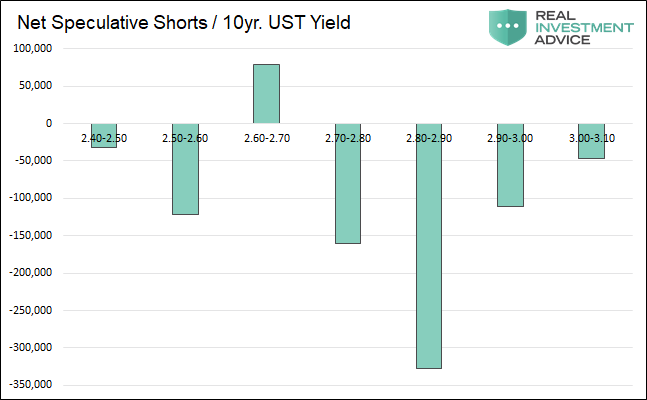

Here is an updated chart showing the current net short position versus rates. While greatly reduced there are still enough shorts outstanding to push yields below 2%.

The Great Bond Bull Market Approaches Is Here

As we quoted then, Eric Hickman made “the” key observation as to why rates will fall in the months ahead:

“With the economic expansion nine months from being the longest in U.S. history, the yield curve nearly flat and housing market indicators peaking earlier this year, it doesn’t take much imagination to see what’s next: a recession and falling interest rate cycle – i.e., a U.S. Treasury bull market.”

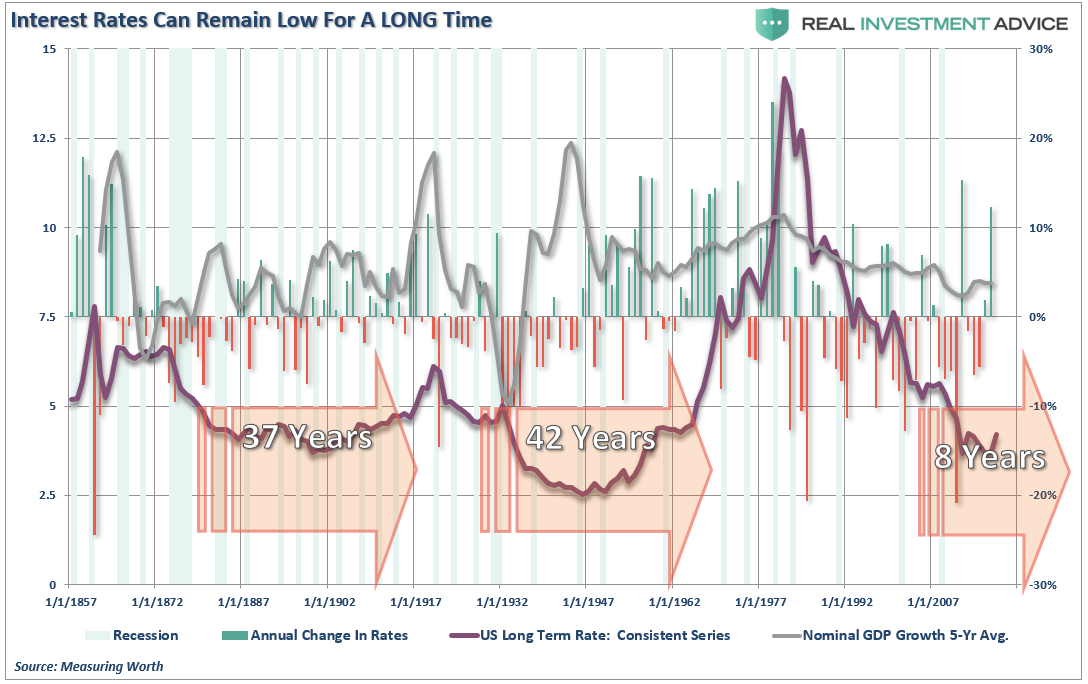

There is a very long precedent to back up his claim. The chart below, which tracks rates back to the late-1800’s, shows that rates not only fall during recessions, but they can, and do, remain low for extremely long periods of time.

The premise is fairly simple.

Rising interest rates are a function of strong, organic, economic growth that leads to a rising demand for capital over time. There have been two previous periods in history that have had the necessary ingredients to support rising interest rates. The first was during the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I, and America began the shift from an agricultural to industrial economy.

The second period occurred post-World War II as America became the “last man standing” as France, England, Russia, Germany, Poland, Japan and others were left devastated. It was here that America found its strongest run of economic growth in its history as the “boys of war” returned home to start rebuilding the countries that they had just destroyed. But that was just the start of it.

Beginning in the late 50’s, America embarked upon its greatest quest in history as man took his first steps into space. The space race that lasted nearly twenty years led to leaps in innovation and technology that paved the wave for the future of America. Combined with the industrial and manufacturing backdrop, America experienced high levels of economic growth and increased savings rates which fostered the required backdrop for higher interest rates.

Today, the ingredients to create that kind of economic growth no longer exists.

The U.S. is no longer the manufacturing powerhouse it once was.

Globalization has sent jobs to the cheapest sources of labor.

Technological advances reduce the need for human labor and suppress wages as productivity increases.

Labor force participation rates remain mired near their lowest levels since the 1970’s.

Demographic trends in the U.S. continue to weigh on the sustainability of pension benefits and long-term economic growth.

Massive debt levels divert capital from productive investment to debt service.

Productivity growth, the engine for economic growth, has ground to a halt.

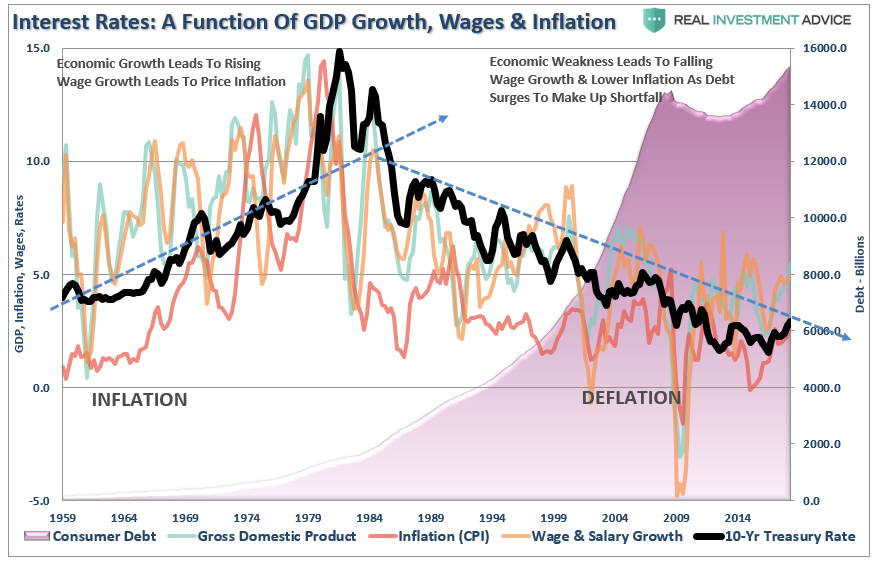

Interest rates are not just a function of the investment market, but rather the level of “demand” for capital in the economy. When the economy is expanding organically, the demand for capital rises as businesses expand production to meet rising demand. Increased production leads to higher wages which in turn fosters more aggregate demand. As consumption increases, so does the ability for producers to charge higher prices (inflation) and for lenders to increase borrowing costs.(Currently, we do not have the type of inflation that leads to stronger economic growth, just inflation in the costs of living that saps consumer spending – Rent, Insurance, Health Care, Energy.)

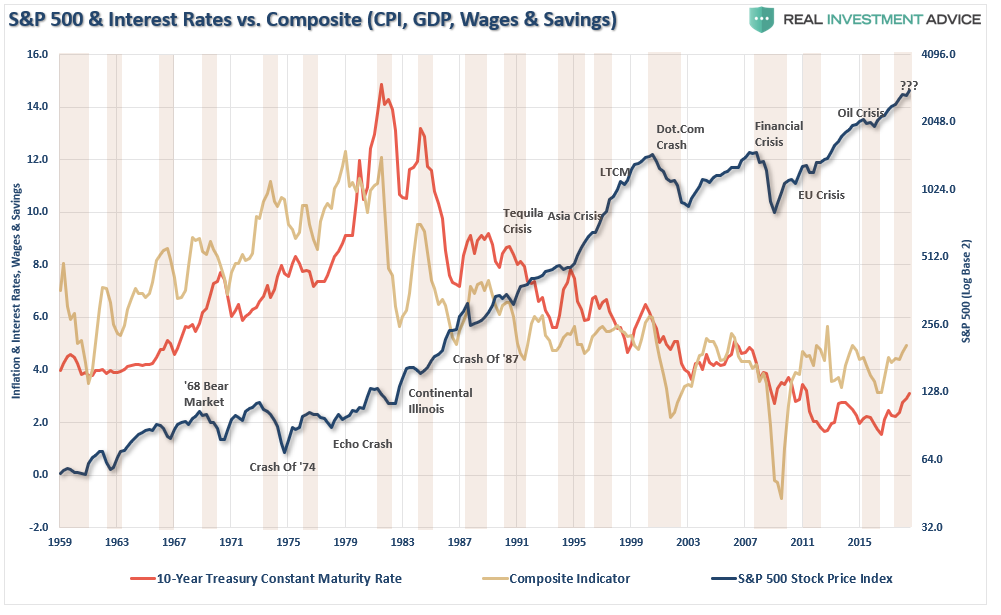

This is shown in the chart below. The rise in rates during the 60-70’s was combined with rising inflationary pressures driven by a rising trend in economic growth and wages. Extremely low levels of household indebtedness allowed rates to rise without severely negative consequences.

With households, corporations, the government and investors more levered today than ever before in history, the rise in rates will have a more immediate and widespread economic consequence.

When rates start to increase, there is NOT an immediate negative consequence on economic growth, employment, or inflation. As the increase continues, early warning signs are dismissed as just a “lull” or “soft landing.” However, those early warning signs have previously been just that.

The problem with most of the forecasts for a continued rise in rates, along with a continued stock bull market, is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds. The issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American the vast majority of whom have no stake in the markets. Interest rates, however, are an entirely different matter and has the greatest effect on the bottom 80% of the economy. Think student loans, auto loans, credit card debt and mortgages.

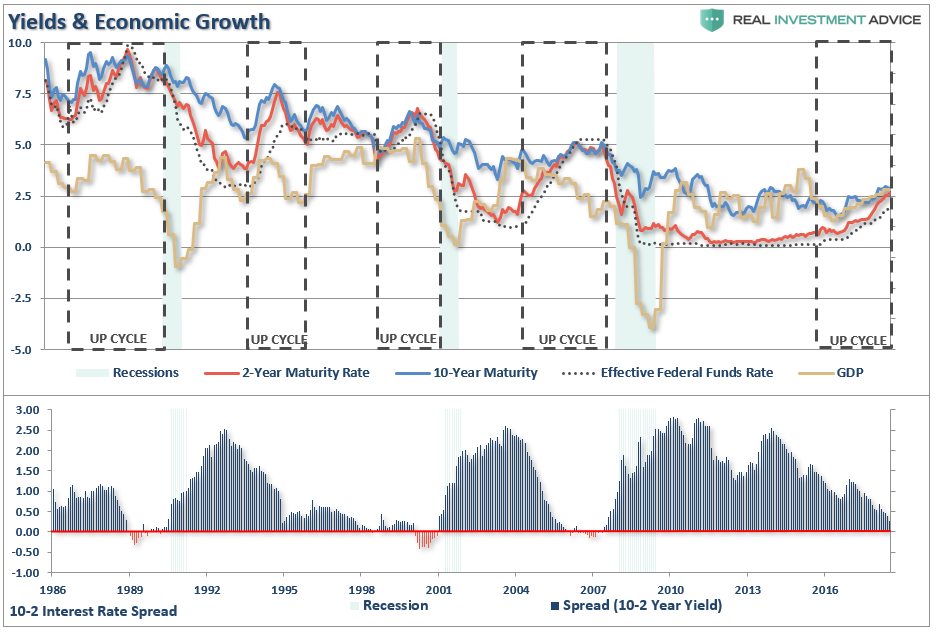

The chart below shows the composite economic indicator of inflation, wages, GDP, and savings as compared to interest rates and the S&P 500. Sharp upticks in rates have historically led to financial events, recessions, market corrections, or a combination of all three.

The irrationality of market participants, combined with globally accommodative central bankers, have continued to push asset values higher and concentrate investors into the ongoing “chase for yield.”

Bull markets, low unemployment, elevated consumer and investor sentiment, economic growth, and inflation are near peaks at the end of the cycle. As Eric noted then:

“Bull markets began far before their accompanying recession did. The bull markets started an average of 1.8 years before. This happens because the start of a recession is marked by a decline in real economic activity, yet long-term Treasury yields start to move lower from the mere hint of a slowdown in activity. This is important because many familiar commentators and banks (Ray Dalio, Ben Bernanke, Nouriel Roubini, Mark Zandi, Societe Generale, JP Morgan) are warning of a recession in 2020. This 1.8-year average combined with a mid-2020 recession would suggest a U.S. Treasury bull market beginning around now.”

We also noted previously that the majority of the record speculative bond “shorts,” were put on between 2.80% and 2.90% on the 10-year Treasury. When rates approach that level, shorts will likely aggressively buy to cover their shorts and prevent loses. Such a “short squeeze” will send rates lower very quickly.

As we said then:

“There isn’t much guessing on how this will end, and history tells us that such things rarely end well.”

But this is where the opportunity currently exists for a contrarian with a longer-term view:

“It is counterintuitive, but U.S. Treasury bull markets begin when the economic weather is the sunniest. It happens when the unemployment rate is the lowest and consumer and industrial confidence the highest. By the time a recession is obvious, a good chunk of the move lower in rates will have taken place. Of course, there are no hard and fast rules to make money in finance, but to the extent that ‘this time isn’t different,’ now is the time to get ready for a large opportunity in the U.S Treasury market.”

The next recession will be much larger and deeper than most currently expect due to the massive amount of leverage built up during the current cycle. A loss of 45-50% on the S&P 500 will not be surprising as a mean-reverting event wipes out a big chunk of the gains made over the last decade. Efforts by the Fed will be restricted as the pension fund crisis expands and a “debt deleveraging” cycle takes hold.

The ideal investment to take advantage of the next cycle will be Treasury bonds.

As I concluded then, you wanted to buy them while they were still cheap because once they began to move, the reversion to the mean will be much more rapid than you can imagine.

via ZeroHedge News https://ift.tt/2U2L6y1 Tyler Durden

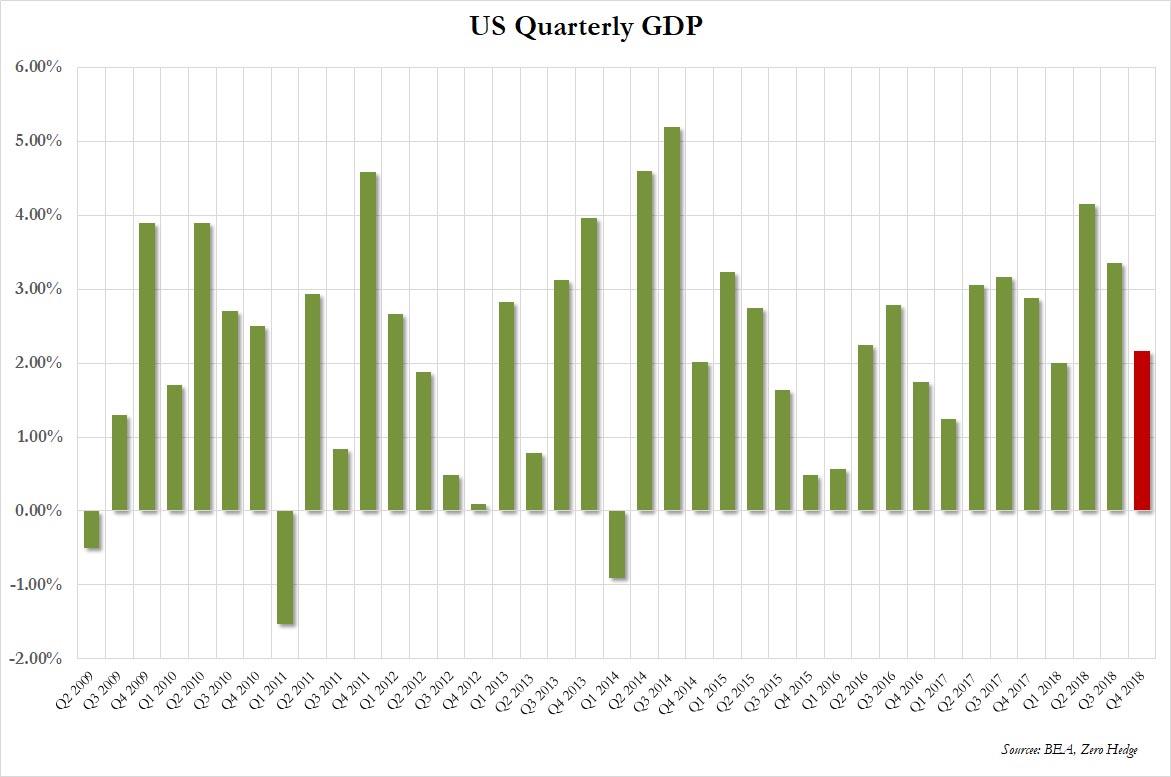

After one month ago the BEA reported that the US economy ended 2018 stronger than expected, with US GDP rising at a 2.6% annualized rate, moments ago the BEA released its third revision to the GDP which was revised modestly lower to just 2.2%, below the 2.3% expected.

The downward revision to real GDP growth was primarily accounted for by revisions to consumer spending, state and local government spending, and business investment that were partly offset by a downward revision to imports. For additional information see the technical note. Here are the specific revisions:

Personal Consumption contribution to the bottom line: 1.66% from 1.92%. On an annualized basis, however, the number was 2.5%, which was down from the 2.8% pre-revision, and just below the 2.6% expected.

Fixed investment was also revised lower, contributing 0.54% to the bottom line, down from 0.69% a month ago

Private inventories, while barely changed, were also revised lower from 0.13% to 0.11%

Net trade (exports less imports) shrank less than initially reported, reducing GDP by 0.08%, down from -0.22% as initially reported

Finally, government consumption ended up being a drag to growth, shrinking by -0.07% vs the initial estimate of 0.07% growth.

Visually:

More importantly for Trump, despite the downward revision, the president can still boast of the first 3% GDP print (on a year over year basis). As the BEA notes, measured from the fourth quarter of 2017 to the fourth quarter of 2018, real GDP increased 3.0 percent during the period. That compared with an increase of 2.5 percent during 2017.

On the inflation front, the GDP Price Index rose 1.7%, below the 1.8% expected, even though core PCE actually surprised to the upside, rising by 1.8% from 1.7% pre-revision, and also above the 1.7% expected.

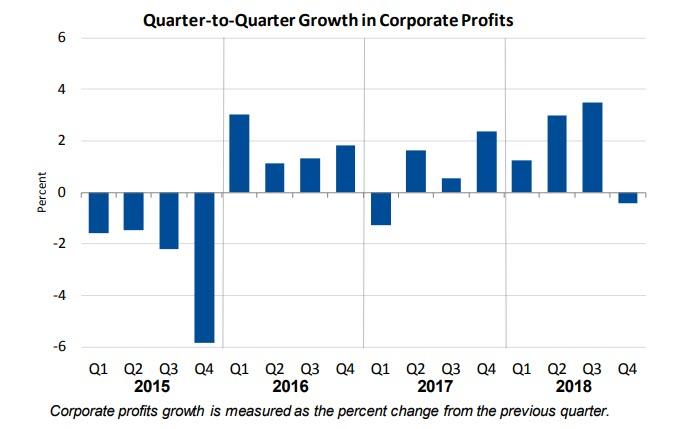

Separately, the BEA reported that corporate profits fell -0.4% after rising 3.5% in prior quarter, with corporate profits up 7.4% on a year over year basis, in 4Q after rising 10.4% prior quarter.

Meanwhile, financial industry profits declined 5.6% Q/q in 4Q after falling 1.3% prior quarter; nonfinancial sector profits rose 1% Q/q in 4Q after rising 6.4% prior quarter. Finally, corporate profits with inventory valuation and capital consumption adjustments increased 7.4 percent from the fourth quarter of 2017.

via ZeroHedge News https://ift.tt/2TF3szS Tyler Durden

After topping $60 a barrel – the highest since Nov 2018 – oil prices slid Thursday morning after President Trump tweeted his latest plea for OPEC to increase oil production, saying that “oil markets are fragile…and the price of oil is getting too high. Thank you!”

Of course, this isn’t the first (or even, the second, or third…) time that Trump has tried to dictate OPEC’s production accords via Tweet. Every time he does it, there’s a favorable (for Trump) reaction in the crude complex, so, like a lab rat who gets rewarded with a food pellet every time it presses a button, Trump will presumably keep doing it until it stops working.

via ZeroHedge News https://ift.tt/2FAKAwX Tyler Durden

For a brief moment earlier this week, it looked as if Theresa May’s supremely unpopular Brexit withdrawal deal might actually pass on the third go. But after the DUP reaffirmed its opposition to the deal last night, and a group of Brexiteers calling themselves “the spartans” said they wouldn’t follow ERG leaders like Jacob Rees-Mogg and Boris Johnson in accepting Theresa May’s “back me then sack me” deal gambit, support for the deal is crumbling once again.

Both Johnson and Rees-Mogg have reportedly rescinded their support for the deal, and though No. 10 insists talks with the DUP are ongoing, it’s unlikely we’ll see them relent, unless May can succeed in securing “material changes” to the agreement, which the EU has already made clear isn’t an option.

The pound broke below a critical resistance level at $1.3125 Thursday morning, as last night’s indicative vote failed spectacularly, with MPs rejecting every alternative to May’s deal. This was a moot point anyway, since the EU has made clear that it’s either the withdrawal agreement, or no deal.

While Parliament is expected to debate May’s Brexit deal tomorrow, it’s unclear whether it will be brought for a third vote, since May must still pass Speaker Bercow’s “significantly different” test.

via ZeroHedge News https://ift.tt/2V05Vqh Tyler Durden

While global markets showed tentative signs of a rebound in sentiment in early Thursday trading, as the global bond rally showed signs of easing, with Treasuries turning lower alongside most sovereign debt in Europe, this quickly reversed around the time US traders start showing up at their desks, and European stocks faded almost all of their earlier gains, while U.S. equity futures drifted, once again within striking distance of the 2,800 key level.

After the 10-year US Treasury yield crept back above 2.37% during Asia trading, a renewed flight to safety saw the yield on the benchmark paper slide in the red again, as global bond yields continued to spiral lower on Thursday as recession fears fed expectations of more policy easing by major central banks, with the 10Y trading below 2.36% at last check.

After shares slumped in Japan and fell in China and South Korea at the start of trading, contracts on the S&P 500 pointed to a modestly red open fading an earlier rebound, while the Stoxx Europe 600 paring earlier gains of as much as 0.4 percent, with banking stocks the regional benchmark’s weakest sector. The Stoxx 600 was steady as of 11:36am in London, with the index tracking banking stocks dropping 1.3% following fresh turmoil in Sweden over money-laundering, while healthcare gauge climbs 0.8%. Rating agency S&P became the latest to cut its euro zone growth forecasts while a Reuters report that the United States and China had made progress in all areas in trade talks seemed to bolster sentiment a little, though sticking points still remained and there was no definite timetable for a deal.

Worries that the inversion of the U.S. Treasury curve signaled a future recession only deepened as 10-year yields fell to a fresh 15-month low at 2.34% on Wednesday. “We think that the ongoing flattening, or outright inversion, of the curve is a bad sign for equities, as it usually has been in the past,” said Oliver Jones, markets economist at Capital Economics. “Arguments that the yield curve is no longer a reliable indicator seem to resurface every time it inverts, only to be subsequently proved wrong.”

Meanwhile, Chinese Premier Li said world economy faces slower growth and increasing uncertainties, while he added that some fluctuation in quarterly economic growth this year cannot be ruled out. Chinese Premier Li further commented that China must achieve goal of tax and fee cuts this year, while it will also publish a revised negative list for foreign investors and will treat domestic and foreign companies equally. Separately, adding that changes in their economy in March have exceeded expectations, adds that China’s economic operations were steady in Q1.

US administration official said US and China made progress in all areas of trade talks but enforcement and intellectual property remain sticking points, while China was also said to have made proposals on trade including tech transfers that are more specific and with wider scope than ever before. However, the official added that there is no specific timeframe for a trade deal with talks to conclude anytime from April-June and whether to lift current US tariffs on China is a sticking point and will be worked out as part of a deal. Subsequently, Chinese Premier Li said China must protect IP to support China’s transformation, adding that he does not think there is a trust deficit between US and China.

As the flight to safety accelerated, so did the rise in the dollar, which headed for a fifth gain in six sessions, while Britain’s pound weakened after the U.K. Parliament rejected eight possible options for a new Brexit strategy.

But it was the Turkish lira, one of the currencies at the heart of last year’s emerging market meltdown, which was once again the overnight highlight as plunged as much as 5% against after the central bank unveiled that it had burned through a third of its reserves in 1 month and the attempt to crush shorts had ended, inviting a fresh wave of bears. As Reuters notes, authorities were showing the first sign of easing a draconian squeeze put on international lira traders ahead of local elections this weekend but a day after the country’s stock market also slumped there was little good will. Ugras Ulku at the International Institute of Finance in Washington said the question was, when the dust settles, whether portfolio managers want to continue to invest in Turkey or not “we will have to wait and see,” he said

Elsewhere, hints of rate cuts from New Zealand’s central bank had the desired effect on its currency, which was pinned at $0.6816 after diving 1.6 percent overnight. The Aussie was on the defensive at $0.7090. Draghi’s comments likewise kept the euro back at $1.1250, and left the U.S. dollar a fraction firmer against a basket of its competitors at 96.874. Only the yen held its own thanks to its safe-haven status and firmed to 110.00 per dollar.

The Swiss franc’s surge to a 20-month high hasn’t spooked strategists at Credit Agricole CIB out of their bearish view. The Swiss National Bank is unlikely to tolerate further franc strength, which would threaten policy makers’ battle against deflation, and may rein in the exchange rate via currency interventions, according to the bank

In commodity markets, palladium was the focus of attention after sliding 7 percent on Wednesday as its meteoric rally finally ran into profit-taking. It was down 0.4 percent on Thursday. Gold was relatively sedate at $1,310.85 per ounce. Oil prices nursed modest losses after data showed U.S. crude inventories grew more than expected last week as a Texas chemical spill hampered exports.

Economic data include initial jobless claims and the final print of quarterly GDP. Accenture is due to report earnings.

Market Snapshot

S&P 500 futures little changed at to 2,811.50

STOXX Europe 600 up 0.06% to 377.51

MXAP down 0.4% to 158.73

MXAPJ up 0.1% to 523.64

Nikkei down 1.6% to 21,033.76

Topix down 1.7% to 1,582.85

Hang Seng Index up 0.2% to 28,775.21

Shanghai Composite down 0.9% to 2,994.94

Sensex up 0.9% to 38,457.70

Australia S&P/ASX 200 up 0.7% to 6,176.08

Kospi down 0.8% to 2,128.10

German 10Y yield rose 0.4 bps to -0.077%

Euro down 0.03% to $1.1241

Brent Futures down 0.7% to $67.37/bbl

Italian 10Y yield fell 1.4 bps to 2.1%

Spanish 10Y yield rose 1.4 bps to 1.07%

Brent Futures down 0.7% to $67.37/bbl

Gold spot down 0.1% to $1,308.46

U.S. Dollar Index up 0.3% to 97.02

Top Overnight News

Britain’s political standoff over Brexit escalated further, with even Theresa May’s announcement that she’ll quit as prime minister doing nothing to move closer to a resolution

Federal Reserve Bank of Kansas City President Esther George says it was appropriate to put policy on hold after the central bank’s interest-rate increases last year. Asked if the Fed’s quarter- point hikes in September and December had been mistakes, George replied: “No, I do not think we made a mistake in September. I was one who advocated for a long time concern about low-for-long interest rates”

Investors dumped Turkish bonds and stocks on Wednesday after the nation orchestrated a currency crunch to prevent the lira from sliding days before an election that will test support for President Recep Tayyip Erdogan’s rule. The cost of borrowing liras overnight on the offshore swap market soared past 1,000 percent at one point on Wednesday

China’s economy is showing further signs of recovery after months of slowdown, though downward pressures still persist. That’s according to a Bloomberg Economics gauge aggregating the earliest available indicators on market sentiment and business conditions

U.S. and China have made progress in focus areas under the trade talks, Reuters reports, citing four senior U.S. administration officials. One official said China had come up with proposals on forced tech transfers that went further than in the past in terms of scope and specifics

The European Central Bank’s chief economist says there needs to be a solid monetary-policy case before officials act to mitigate the side effects of negative interest rates on banks. ECB staff are examining the issue of tiering — where some of banks’ excess reserves are exempt from the lowest rate — but action isn’t a done deal, Peter Praet says

Thailand’s pro-military party won the most votes in Sunday’s election, authorities confirmed on Thursday, bolstering its claim to legitimacy as it competes with an anti-junta alliance to form a government

Asian equity markets traded mostly negative as the downbeat sentiment rolled over from US where all major indices finished lower amid lingering growth concerns and as the yield curve inversion deepened. As such, ASX 200 (+0.7%) opened subdued but with losses eventually pared by resilience across nearly all sectors, while Nikkei 225 (-1.6%) underperformed and briefly slipped below the 21000 level with selling exacerbated by a firmer currency and rotation into bonds. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (-0.9%) were also cautious with weakness in financials due to earnings in which China’s 2nd largest lender China Construction Bank missed on FY net forecasts and posted its first quarterly Y/Y profit decline since 2015 which doesn’t bode well for the other Big 4 banks to report this week, while China Life Insurance also posted a near-65% drop in FY net. Nonetheless, sentiment in China slightly improved as US and China senior trade negotiators began the latest round of trade talks in Beijing and a Trump administration official suggested progress was made in all areas of trade talks but some sticking points remained. Finally, 10yr JGBs were supported by the negative risk tone in Japan and amid the recent bond market rally as global yields declined in which the US 10yr yield fell to a fresh 15-month low and the Aussie 3yr yield printed its lowest on record, while the results of today’s 2yr auction were also bullish as all metric improved from the prior month, albeit marginally.

Top Asian News

Sony’s Turnaround Architect Retires as Tech Giant’s Growth Slows

Guinigundo Sees Flexibility to Consider Philippine Policy Easing

China’s Economy Shows More Signs of Recovery, Earliest Data Show

Thai Pro-Military Party Won Most Votes in General Election

Major European indices have gained some traction following a subdued start to the session [Eurostoxx 50 +0.2%] as the region diverges from the downbeat sentiment experienced in Asia. UK’s FTSE 100 (+0.6%) outperforms its peers as the weaker domestic currency bolsters the export-heavy index. Sector-wise, material stocks lead the gains as base metals benefit from recent turnaround in the risk sentiment whilst utility names lag as investors move away from defensive sectors. In terms of notable movers, Swedbank (-3.7%) shares took another hit amid the slew of open investigations in relation to money laundering. As the bank’s AGM gets underway, it announced that CFO Anders Karlsson has replaced Birgitte Bonnesen as acting President and CEO. Company shares are halted until further notice. Elsewhere, chip names remain pressured in a continuation of yesterday’s sell-off after DAX-listed Infineon (-1.1%) announced a profit warning due to rising global tensions.

Top European News

Iliad Chairman Lombardini Faces French Market-Abuse Case

Iceland’s Wow Air Says It Has Ceased Operations

Hochtief Shares Drop After Atlantia Sells a Quarter of its Stake

Euro Hits 10-Week Low Versus Yen as German Inflation in Focus

In FX, JPY/NZD were the best G10 performers, albeit off best levels as the Usd retains a firm underlying bid in its own right as a safe-haven amidst a tentative and intermittent revival in broad risk appetite. Usd/Jpy is holding above 110.00 within a 110.03-53 range having tested bids/support just ahead of the big figure where decent option expiry interest resides (1 bn) and is back above daily chart resistance between 110.07-12, while Eur/Jpy has also rebounded from sub-124.00 lows and heavy Japanese selling that pushed the cross down through a key Fib (123.81) at one stage. Meanwhile, the Kiwi has regained some composure after its post-RBNZ rout to reclaim 0.6800 status, but Nzd/Usd remains vulnerable following a marked deterioration in NZ business sentiment and expectations according to ANZ’s March survey, which provides more justification for the change in rate guidance towards an ease vs a neutral stance previously. Note, RBNZ Governor Orr is due to orate later on the new framework for monetary policy.

AUD/EUR – Also weathering a bout of downside pressure relatively well, as the Aussie keeps tabs on the 0.7100 handle vs its US counterpart and remains above 1.0400 against the Nzd, however Aud/Usd could be hampered by a 1 bn expiry ahead of the NY cut along with dovish positioning for next week’s RBA on the notion that the balance of risks could shift towards cutting benchmark rates from a balanced prognosis at present, ala the RBNZ. Meanwhile, the single currency succumbed to spill-over Jpy cross sales vs the Usd that forced the headline pair through recent lows and chart support (at 1.1241), but not much further as it consolidates back above the 76.4% Fib retracement of the 1.1177-1.1448 move.

GBP/SEK/NOK/CAD/CHF – All lagging their major peers, and especially the Pound, Swedish and Norwegian Crowns. Cable has fallen below a fairly resilient 1.3150 mark following the latest UK Parliamentary votes on Brexit ended with no majority support for any of the 8 options tabled, and in fact resounding rejection in 6 instances, leaving the situation even more uncertain than it was before the HoC took the baton from PM May. Meanwhile, Eur/Nok and Eur/Sek have both bounced further in wake of yesterday’s worse than expected Norwegian jobs data and as Swedbank suffers more investor angst over money laundering allegations, with the former up to 9.7465 and latter at 10.4935 before easing back. The Loonie is also weaker post-data, between 1.3400-30 vs its US rival, with the Franc still somewhat mixed as it pivots 0.9950 vs the Greenback and 1.1200 against the Euro in advance of a speech from SNB’s Maechler that could fan speculation about intervention to curb excess Chf strength/demand.

DXY – The index has climbed into a higher range after recent declines amidst falling US Treasury yields and deeper curve inversion to probe above 97.000, and from a technical perspective the Buck may be able to overcome residual month end flows that are said to be mildly bearish.

Brazil’s Economy Minister Guedes said that if the pension reform bill of BRL 1tln passes, interest rates would naturally decline by 2 percentage points. (Newswires)

New Zealand ANZ Business Confidence (Mar) -38.0 (Prev. -30.9). (Newswires) New Zealand ANZ Activity Outlook (Mar) 6.3 (Prev. 10.5)

In commodities, WTI (-0.6%) and Brent (-0.6%) futures languish following yesterday’s pullback, although the benchmarks remain off worst levels amid an improvement in market sentiment. Despite this week’s builds in API and DoE crude inventories (API +1.9mln, DoE +2.8mln), UBS analysts note that both weekly data and for the year thus far are more bullish than usual. Meanwhile, WSJ reported that Saudi Aramco plans to issue a USD 10bln bond, to be used as part of a payment for their 70% purchase of Sabic which is valued at USD 69.1bln, according to sources. On the OPEC+ front, Russian Energy Minister Novak told RIA newspaper that the OPEC+ Charter could be signed in either May or June. Elsewhere, precious metals are pressured by firmer buck with gold (-0.2%) hovering close to its 50 DMA at 1307/oz. Meanwhile, base metals are faring better, with risk-gauge copper bouncing off lows as the risk appetite supports the red metal.

US Event Calendar

8:30am: GDP Annualized QoQ, est. 2.3%, prior 2.6%

Personal Consumption, est. 2.6%, prior 2.8%

GDP Price Index, est. 1.8%, prior 1.8%

Core PCE QoQ, est. 1.7%, prior 1.7%

8:30am: Initial Jobless Claims, est. 220,000, prior 221,000; Continuing Claims, est. 1.78m, prior 1.75m

10am: Pending Home Sales MoM, est. -0.5%, prior 4.6%; Pending Home Sales NSA YoY, est. -3.0%, prior -3.2%

11am: Kansas City Fed Manf. Activity, est. 0, prior 1

DB’s Jim Reid concludes the overnight wrap

Last night saw the most exciting European vote in the U.K. since Bucks Fizz won the Eurovision Song Contest in 1981. MPs spent the evening making their minds up on 8 options in relation to Brexit although as expected no majority was found for any path. The vote occurred soon after Mrs May announced to backbench Conservative MPs that she would step down as PM after her Brexit deal was delivered and would not lead the next stage of negotiations. This was aimed at increasing the chances that her WA (MV3) can rise like Lazarus and pass, although as we’ll see later the speaker and the DUP have made it more difficult for the government to try again. Anyway, back to the votes, it is perhaps easiest to list the options available and show the scores on the doors in order of most votes in support of a particular pathway. There were no nul points.

Putting any deal agreed to a second referendum. Defeated 295-268.

Permanent customs union. Defeated 272-264.

Labour’s plan (which includes a permanent customs union, but also involves alignment in a number of other areas). Defeated 307-237.

Common Market 2.0. (stay in the single market, negotiate a customs union “at least until alternative arrangements” to avoid a hard border in Ireland have been found. Defeated 283-188.

Revoking Article 50 if a deal has not been ratified and the House does not approve leaving without a deal. Defeated 293-184.

Leaving with no-deal on 12 April. Defeated 400-160.

Version of the Malthouse plan (UK offers EU payments for two years in return for market access). Defeated 422-139.

Seek to remain a member of the EEA and reapply to join EFTA (so single market but not customs union). Defeated 377-65.

In terms of votes in favour, the amendment for a second referendum led the pack, while the customs union proposal was the closest vote, losing by a margin of only 8 votes. Indeed, both amendments achieved more positive votes than May’s deal did the second time round, when it achieved only 242 yes-votes. The pound depreciated -0.58% versus the dollar after the votes were taken, as the odds of continued stalemate and an eventual general election seem to be rising. The plan now is for a possible MV3 on May’s deal before the end of the week, followed by, assuming MV3 fails again, an additional set of indicative votes on Monday. Speaker Bercow said he would eliminate the less popular options and leave only the top few, to see if a majority can be achieved from a shorter list.

In terms of whether there’ll be a third meaningful vote soon, it’s obviously in the PM’s plan this week. However, this will have to circumnavigate Speaker Bercow’s further intervention that said any further vote would still have to comply with his ruling from March 18 that the House couldn’t vote on the same motion again and would require some form of change. Interestingly, he said that the government couldn’t seek to get round this using a ‘paving motion’, which blocks off a route the government could have possibly used to get round his ruling. Also the DUP said (late last night) at this stage they still can’t support the deal. Whether that changes or whether that just means an abstention is not clear although DUP Dodds said that with regards to the Union they don’t abstain. Before this there were signs that Prime Minister May is making some progress in winning over MPs to the deal, with a number of Conservative MPs who opposed the deal on the last meaningful vote saying they would now be willing to support the deal (generally out of a fear from pro-Brexit MPs that any alternative would only be a softer Brexit than the PM’s deal, or possibly no Brexit at all). However, without the DUP they will likely need a fair amount of Labour MPs on their side. Also, one wonders that with Mrs May now going, will loyal remain Tory MPs be fearful of a harder Brexit replacement PM and decide to vote against it to stop a Brexit that might then get handed over to the hard Brexiteers.

Outside of Brexit, the biggest story was the interaction of Draghi’s comments, European bank stocks, deposit tiering, and a big rates rally. On page 6-7 of our recent “How to fix European banks… and why it matters” (see here ) we explained how strange it was that of all the central banks operating with negative rates, the ECB were the only one not offering deposit tiering. Implementing this was a small part of our policy recommendation list. Recent news hasn’t suggested they were close to this, but things moved quite quickly yesterday. First, we had an early morning Reuters story which said that the ECB were looking at the idea of a tiered deposit rate and then at lunchtime Draghi said that “if necessary, we need to reflect on possible measures that can preserve the favourable implications of negative rates for the economy, while mitigating the side effects, if any.” The ECB have been worried that moving to such a system would lead to concerns that this signals rates staying low or negative for much longer. To be fair, this was what happened yesterday as Bunds rallied -6.6 bps to -0.081% with the front end of the curve flattening even more. Euribor futures for December 2019 and 2020 rallied by -4 and -7bps to their lowest levels ever, leaving the curve as flat as a pancake through the next six quarters. A 10bps hike is not fully priced in until March 2021.

This morning ECB’s Chief Economist Peter Praet has said that the tiered rate would need a monetary-policy case while adding that the lending conditions are not impaired and there is no need to rush for tiering. On TLTRO, he said that the ECB could decide on pricing at its June meeting while adding that the conditions could change during the program.

European banks made strong advances on the news though, albeit on a risk-off day with the STOXX Banks index up +1.85% with Italian banks +1.59%. Another side effect was a rally in 10yr BTPs, -1.4bps lower on the day and -10.2bps from the morning highs. Delving deeper into the bond move we also saw 10-year bund yields falling below 10-year Japanese government bond yields for the first time since October 2016. However, this morning in Asia the yield on 10yr JGBs (-1.2bps to -0.091%) is again below that of 10yr bund as the race to the bottom continues. In the US, yields continued to rally yesterday as well, with 2- and 10-year yields dropping -6.6bps and -5.7bps, respectively. That meant the 2s10s curve steepend again to 16.3bps, back to slightly above its year-to-date average. The 2yr and 10yr treasury yields are both down a further c. -1.2bps this morning with 10yr treasury yields now hovering at 2.355%, the lowest since December 2017.

Overnight, Asian markets are following Wall Street’s lead with the Nikkei (-1.45%), Hang Seng (-0.08%), Shanghai Comp (-0.26%) and Kospi (-0.78%) all down. Elsewhere, futures on the S&P 500 are down -0.24% while the Japanese yen is up +0.32%, alongside most G10 currencies.

Back to Mr Draghi, he also talked about inflation and said “we therefore remain confident that the sustained convergence of inflation to our aim has been delayed rather than derailed”. He nevertheless maintained his stance that “uncertainty remains high” and “the risks remain tilted to the downside.” The euro weakened after the speech, falling -0.17% versus the dollar. Staying with FX, we also saw the Swiss Franc climb to its strongest level against the euro since July 2017 yesterday to 1.1195. DB’s strategists don’t think intervention to prevent appreciation is likely until we approach 1.10, so there’s a bit more room to run before that becomes a risk.

It was a bad day for Turkish assets, with the BIST 100 index closing down -5.67% yesterday, its biggest fall since July 2016, while Turkish bond yields also rose dramatically, with local 10-year yields up +114bps to 17.93% and USD up +19.3bps to 7.74%. The overnight implied yield continued to blow out, rising to as high as 1,350% before ending the day at 750%. The market turmoil comes before local elections on Sunday, with the government likely hoping to maintain FX stability ahead of the votes. This morning the Turkish Lira is -1.94% as sentiment continues to be weak

The S&P 500, DOW, and NASDAQ retreated -0.46%, -0.13%, and -0.63% respectively. All sub-sectors fell except for industrials, which were boosted by a positive day for airlines (+1.92%). Southwest, a major operator of the grounded Boeing 737 Max, announced that the impact on first quarter revenue would be smaller than feared at only $150million. The dollar strengthened +0.19%, weighing on multinationals and exporters, after US trade data showed a smaller-than-expected deficit for January. The bilateral deficit with China narrowed by $2.4bn to -$34.4bn, providing a somewhat more positive backdrop as USTR Lighthizer and Treasury Secretary Mnuchin travel to Beijing today for trade negotiations.

In spite of the strong performance from financials, European equity markets fell back before the close, in line with a falling US market, with the STOXX 600 paring their gains to close flat. The DAX, CAC, and FTSE 100 also all closed flat on the session, although southern European equities put in a stronger performance, with the FTSE MIB (+0.26%) and the IBEX 35 (+0.51%) outperforming. This came despite unconfirmed reports in Italian newspaper Il Sole that the Italian government plans to lower its 2019 growth forecast to 0.1% and raise its deficit to 2.4% of GDP.

Looking at the European data, French consumer confidence was in line with expectations at 96, a seven-month high, but the readings from Italy were more negative, with the consumer confidence indicator falling to 111.2 (vs. 112.5 expected) to reach its lowest since August 2017, while the manufacturing confidence indicator fell to 100.8 (vs. 101.4 expected), its lowest since February 2015. The UK also saw some negative data, with the CBI’s reported retail sales index falling to -18 (vs 4 expected) in March, its lowest since October 2017.

In terms of the day ahead, we have a number of data readings, including German March CPI data, Eurozone M3 money supply data for February, and the final Eurozone consumer confidence reading for March. From the US, we’ll get the third reading of Q4 GDP, personal consumption and core PCE, along with pending home sales for February, the Kansas City Fed’s manufacturing activity index for March and weekly initial jobless claims. From central banks, both Federal Reserve Vice Chair Quarles and Vice Chair Clarida will be speaking, along with Bowman, Bostic and Bullard. From the ECB, we have Vice President de Guindos, while Villeroy de Galhau, Knot and Nowotny will also be making remarks.

Last but not least, we have the aforementioned Lighthizer and Treasury Secretary Mnuchin trip to Beijing today for trade negotiations.

via ZeroHedge News https://ift.tt/2FHSgPn Tyler Durden

The filing of special counsel Robert Mueller’s report on whether there was collusion between President Donald Trump and the Russians to interfere with the 2016 election should put an end to speculations, accusations, and outrage. The report finds that there was no collusion. But long live speculations, accusations, and outrage.

As soon as Attorney General William Barr summed up the report for Congress, Trump administration allies started to call for the heads of those who had fed the rumor mill for months. On their end, the Democrats didn’t wait long to warn the administration that this wasn’t over and that they would continue investigating the president for alleged obstruction of justice. That’s their prerogative, obviously.

Yet, writes Veronique de Rugy, it’s hard to feel that this obsession with the Mueller report and Russians is not just another excuse for each side to continue talking about everything except policy issues. We can argue that since the Republicans lost control of the House, there’s little chance of legislative reforms getting through. Still, that’s no reason to not try fixing what needs to be fixed or do what needs to be done.

Deutsche Bank shares sank on Thursday after the Financial Times reported that the troubled German lender had been discussing tapping equity markets to raise as much as €10 billion ($11.2 billion) in what would be the bank’s fifth return to the equity well in under a decade. At the higher end of the range, the raise – which would help facilitated a “merger of weakquals” with fellow struggling German lender Commerzbank – would be equivalent to roughly two-thirds of Deutsche’s €16 billion market cap, and about 40% of the combined market value of Deutsche and Commerzbank.

The filing of special counsel Robert Mueller’s report on whether there was collusion between President Donald Trump and the Russians to interfere with the 2016 election should put an end to speculations, accusations, and outrage. The report finds that there was no collusion. But long live speculations, accusations, and outrage.

The filing of special counsel Robert Mueller’s report on whether there was collusion between President Donald Trump and the Russians to interfere with the 2016 election should put an end to speculations, accusations, and outrage. The report finds that there was no collusion. But long live speculations, accusations, and outrage.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}