On March 3, the Supreme Court will consider a constitutional challenge to the Consumer Financial Protection Bureau, one of the federal government’s newest independent agencies. In Seila Law LLC v. CFPB the Court will consider whether the multiple mechanisms used by Congress to insulate the CFPB from executive control go to far.

Like other independent agencies, the head of the CFPB may only be removed for cause (“inefficiency, neglect of duty, or malfeasance in office”), and is slated to serve a set term of five years. Unlike most other independent agencies, the CFPB is headed by a single director, instead of a multi-member commission or board, and is not dependent upon Congressional appropriation for its funding. Instead, the CFPB is empower to request whatever funding is “reasonably necessary to carry out” it substantial responsibilities from the Federal Reserve.

The question for the Court in Seila Law is whether this suite of insulating measures, combined with the CFPB’s broad regulatory and enforcement authority, renders the agency unconstitutional (and, if so, whether this requires overturning some prior Court precedents, such as Humphrey’s Executor).

As it happens, the Trump Administration has concluded that the CFPB is unconstitutional as structured, and the Department of Justice has filed a brief on the side of the petitioners. The Court thus appointed former Solicitor General Paul Clement as amicus curiae to argue in defense of the CFPB’s current structure.

Kathy Kraninger is the current Director of the CFPB. She took office in December 2018. Assuming she completes her term, she would remain in office until December 2023, without regard for who wins the next Presidential election. That is, if the CFPB’s current structure is upheld, Kraninger could serve as CFPB Director for the first three years of the next presidential term, whether we have President Trump, President Sanders, President Bloomberg, or someone else.

The current structure of the CFPB would also give the Trump Administration the ability to prevent its successor from controlling the agency for a full presidential term. Consider the following scenario: If the Supreme Court upholds the CFPB (or is able to avoid the underlying constitutional question), and President Trump is defeated in November, Trump could prevent the next president from appointing their own CFPB director by replacing Kraninger in December 2020 with someone who would be entitled to serve through December 2025.

Could this really happen? Well, Director Kraninger has already concluded that the President may remove her at will, so I suspect she would resign if asked by the President, even if the Supreme Court upholds the CFPB. As a Trump appointee, she may also like the idea of preventing a successor from undoing her work. As for confirmation, I don’t think there’s much doubt that Senate Majority Leader Mitch McConnell would be happy to confirm a last-minute replacement in a lame-duck session of the Senate. Note also, such an appointment could not be filibustered, as there is no longer a filibuster for presidential appointments.

Whatever the Court’s ultimate judgment on the CFPB’s constitutionality, this scenario illustrates how Congress created the opportunity for Presidents to engage in strategic behavior to preserve agency control beyond their time in office—and President Trump could use this power to prevent a Democratic successor from influencing the CFPB long after he has left office.

from Latest – Reason.com https://ift.tt/2ShMwCh

via IFTTT

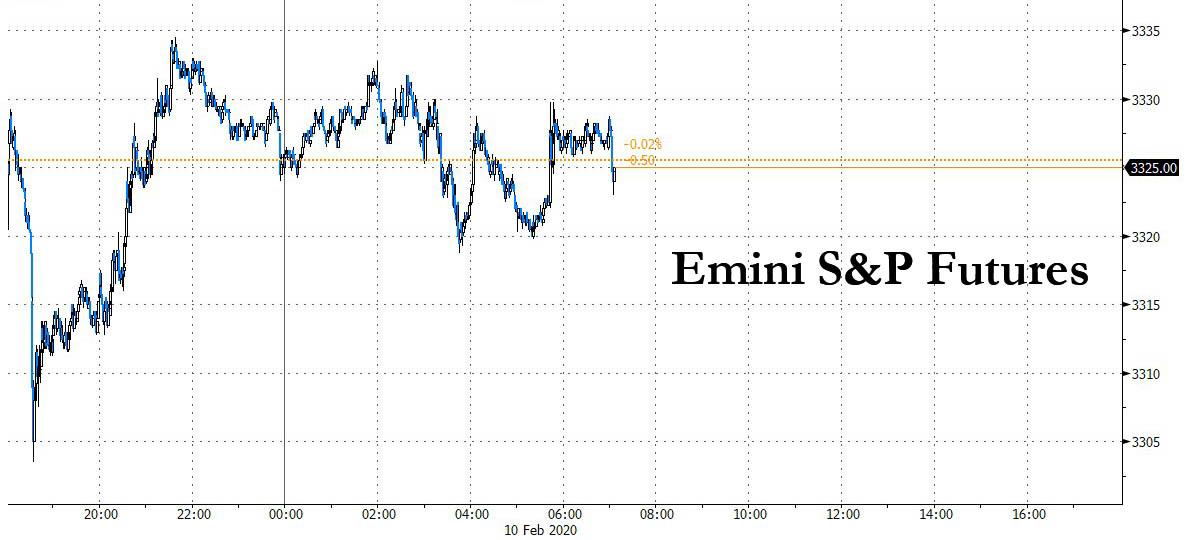

Futures Hug The Flatline As Traders Try To Make Sense Of Latest Coronavirus Updates

Global shares dropped on Monday as the weekend death toll from a coronavirus outbreak even according to Chinese official numbers exceeded the SARS epidemic of two decades ago, though Chinese shares rose as authorities lifted some work and travel curbs, helping businesses to resume operations, and futures rebounded from a steep selloff early in the session following a Reuters report that Apple’s main iPhone supplier Foxconn would resume operations at its biggest Zhengzhou plant, although a subsequent report from Nikkei refuted the original Reuters report without any impact on futures. As a result US equity futures have hugged the flatline after Friday’s drop as fears that China is failing to contain the coronavirus sent risk sharply lower.

MSCI’s All Country World Index was down 0.2%, as European shares rebounded from an early selloff only to edge lower later in the session amid rising fears over the coronavirus’ economic impact still weighed on sentiment. The pan-European STOXX 600 index fell 0.3% in early deals, with the travel and leisure sector the biggest decliner. Ireland’s main index fell as much as 1.2%, dragged down by banks after Irish nationalists Sinn Fein secured almost a quarter of first-preference votes in a general election, while German Chancellor Angela Merkel’s succession plan collapsed when Annegret Kramp-Karrenbauer announced that she will step down as leader of Angela Merkel’s Christian Democratic Union and won’t run as the party’s candidate for chancellor in the next election. Kramp-Karrenbauer, widely known by her initials AKK, has struggled to stamp her authority on the party since taking over from Merkel in December 2018 and was humiliated last week when a local chapter in eastern Germany defied her orders and threw its lot in with the far-right Alternative for Germany.

Earlier in the session, Asian stocks fell with MSCI’s index of Asia-Pacific shares ex-Japan reversing some of losses but still down 0.4%. Japan’s Nikkei was off 0.6%, led by IT and energy companies, as investors puzzled over the impact to economic activity following the hit from the coronavirus. The MSCI Asia Pacific Index extended losses into a second day, with most markets in the region down. Declines were led by Japanese and Hong Kong stocks. Toyota Motor and Takeda contributed the most to the slide on the Topix Index, while AIA Group and Tencent dragged down the Hang Seng Index. South Korea’s KOSPI was 0.5% weaker while Australia’s benchmark index eased a shade. China’s Shanghai Composite dipped into the red before ending the day up 0.5% after the People’s Bank of China moved to keep liquidity ample Monday through reverse-repurchase agreements despite a surge in inflation which hit 11 year high, mostly on the back of soaring food prices but also as a result of higher core CPI. General Motors said it will restart production in China beginning Feb. 15.

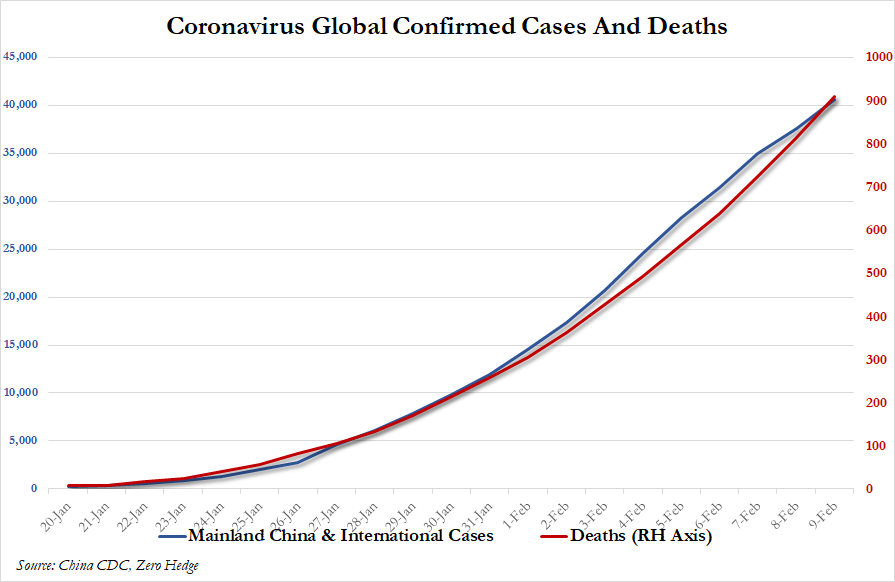

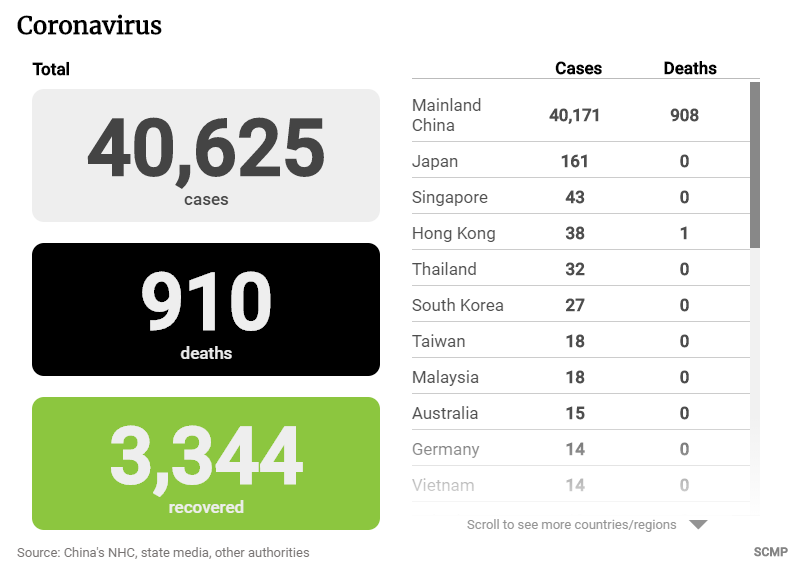

For those who missed our latest viral wrap, the death toll from the coronavirus outbreak reached 910, higher than during SARS. Britain reported four more cases and warned of a serious, imminent threat to public health. Globally, 40,626 have been infected so far.

Having kept a low profile for weeks and sparking questions about his whereabouts, Chinese President Xi Jinping made his first public appearance since the outbreak began, visiting the Chaoyang district in Beijing Monday, according to state-run media Xinhua, which published photos of Xi wearing a mask and having his temperature taken.

Meanwhile, the number of infections among those aboard a cruise liner quarantined off Japan has almost doubled to more than 130, the biggest outbreak outside China.

The lack of containment did not phase some hard core bulls such as UBS Global Wealth Management CIO Mark Haefele, who wrote that “despite the ongoing uncertainty, we continue to filter out the short-term noise and remain overweight emerging market equities,” adding that “while we continue to monitor the risks to our position, we are optimistic that the decisive actions taken by governments will bring the outbreak under control.”

He wasn’t alone: “Whether the coronavirus-related relief is lasting depends on whether this epidemic can ultimately be contained. The new global infections numbers hint at some stabilization suggesting that the speed of the spreading of this virus has come down,” said Martin Wolburg, senior economist at Generali Investments in a note to clients. “The data imply that the spreading of the epidemic could stall by the end of February. Therefore, we view last week’s equity market improvement as backed by fundamentals and continue to see the epidemic as a buying opportunity.”

Not everyone was as optimistic, however: “This coronavirus seems to be going on for longer, is infecting more people and the hit to growth will be longer,” Diana Mousina, an economist at AMP Capital Investors told Bloomberg TV in Sydney. “You won’t be able to recoup all of the negative impacts in the first quarter.”

To contain the spread, China’s government had ordered lockdowns, canceled flights and shut schools in many cities. But on Monday, workers began trickling back to offices and factories though a large number of workplaces remain closed and many white-collar workers will continue to work from home.

The outbreak has killed more people than the SARS epidemic did globally in 2002/2003. The virus has also spread to at least 27 countries and territories, infecting more than 330 people overseas. Over the weekend, an American hospitalized in the central city of Wuhan became the first confirmed non-Chinese victim of the virus. A Japanese man who also died there was another suspected victim.

Also helping markets has been a record injection of stimulus from China’s central bank, which has taken a raft of measures to support the economy, including reducing interest rates, banning short sales and flushing the market with liquidity. From Monday, it will provide special funds for banks to re-lend to businesses working to combat the virus. Despite the measures, analysts expect the world economy to take a hit from an expected slowdown in China.

“For now, our best guess is that the economic disruption related to the coronavirus will cost the world economy over $280 billion in the first quarter of this year,” Capital Economics said in a note on Friday. “If we’re right, then this will mean that global (economic output) will not grow in q/q terms for the first time since 2009.”

In FX, the euro steadied after five losing sessions, even as the region was buffeted by political headlines. German Chancellor Angela Merkel’s succession plan collapsed, and polls put Sinn Fein in place for a possible role in Ireland’s government, depressing the country’s banking stocks. Greece’s 10-year bond yield dropped to a record low. The Bloomberg Dollar Spot index edged down after last week’s biggest five-day gain since August 2018; the euro fluctuated near a four-month low against the dollar. Norway’s krone jumped as much as 0.7% against the euro on the inflation surprise. The pound rose, snapping a three-day decline against the greenback, amid short-term profit-taking. The Aussie rallied after the People’s Bank of China said it’ll provide the first batch of special re-lending funds for combating the coronavirus on Monday. The onshore yuan traded higher after Reuters reported that FoxConn has received the nod to resume production at a key plant in Zhengzhou

In rates, Treasuries were slightly richer across the curve after erasing declines during European morning, led by bunds after weak Italian industrial production data. Gilts lagged slightly ahead of ultra long-dated syndication expected Tuesday. Losses during Asian session pushed 10-year yield as high as 1.597%, before dropping to 1.5696%. Treasuries were pressured in early trading after Reuters reported a key Apple supplier has permission to resume some Chinese production, but that report may have been wrong.

Earnings are due this week from major names like Alibaba Group Holding Ltd., Credit Suisse Group AG and Nestle, with Allergan set to report earnings today. There are no major economic releases on today’s calendar.

Market Snapshot

S&P 500 futures down 0.2% to 3,320.25

STOXX Europe 600 down 0.3% to 423.13

MXAP down 0.5% to 168.86

MXAPJ down 0.4% to 545.22

Nikkei down 0.6% to 23,685.98

Topix down 0.7% to 1,719.64

Hang Seng Index down 0.6% to 27,241.34

Shanghai Composite up 0.5% to 2,890.49

Sensex down 0.5% to 40,925.34

Australia S&P/ASX 200 down 0.1% to 7,012.53

Kospi down 0.5% to 2,201.07

German 10Y yield fell 1.1 bps to -0.397%

Euro up 0.04% to $1.0950

Italian 10Y yield fell 2.1 bps to 0.777%

Spanish 10Y yield fell 1.2 bps to 0.271%

Brent futures down 0.8% to $54.04/bbl

Gold spot up 0.3% to $1,574.35

U.S. Dollar Index little changed at 98.63

Top Overnight News

The death toll from the coronavirus outbreak reached 910, higher than during SARS. The number of infections among those aboard a cruise liner quarantined off Japan has almost doubled to 136, the biggest outbreak outside China. The new virus might have infected at least 500,000 people in Wuhan, the Chinese city at the epicenter of the global outbreak, by the time it peaks in coming weeks. But most of those people won’t know it.

China’s central bank will provide the first batch of special re-lending funds for combating the coronavirus on Monday and will offer the facility weekly to banks later this month. Under the funding facility, nine major national banks and some local banks in ten provinces and cities are qualified for the special funding, according to PBOC Deputy Governor Liu Guoqiang

Oil briefly fell past the psychologically important $50 a barrel mark as hopes for an extraordinary OPEC+ meeting to decide on further production cuts to deal with the demand hit from the coronavirus diminished

German Chancellor Angela Merkel will try to pick up the pieces this week after her party’s flirtation with the far right in eastern Germany led to a political fiasco. Merkel and other leaders of her Christian Democratic Union are now trying to exclude the nationalist Alternative for Germany party from the region’s government

A surge in Sinn Fein’s support upended the Ireland’s traditional two-party power structure. Counting through Sunday confirmed the nationalists’ strength after an exit poll showed a virtual dead heat between Irish Prime Minister Leo Varadkar’s Fine Gael as well as the biggest opposition party, Fianna Fail, and Sinn Fein

Accounts at Japanese banks that typically handle investments for pension funds bought a record amount of overseas bonds last month as a strengthening yen boosted their purchasing power

President Donald Trump’s $4.8 trillion budget for the upcoming fiscal year proposes billions more in funding for defense and a U.S. mission to Mars, but would bring steep cuts to social programs despite almost $1 trillion in deficit spending

The race to lead Germany was thrown wide open on Monday when Annegret Kramp-Karrenbauer announced that she will step down as leader of Angela Merkel’s Christian Democratic Union and won’t run as the party’s candidate for chancellor in the next election

Turkey sent hundreds of tanks, armored personnel carriers and commandos to the Syrian province of Idlib as preparations continue for a likely attempt to break the siege of some of its outposts by Bashar al-Assad’s forces

American forces have started withdrawing from 15 bases in Iraq, Sky News Arabia reported, citing its reporter

Denmark and Switzerland have long shared the world record in negative interest rates, at minus 0.75%. But that may be about to change

Asia-Pac stocks began the week with a sombre tone due to concerns regarding the ongoing coronavirus epidemic which has surpassed the death toll from the SARS outbreak, and following last Friday’s losses on Wall St where markets pulled back from record highs but still notched the best weekly performance since June last year. ASX 200 (-0.1%) and Nikkei 225 (-0.6%) were subdued with underperformance seen in Australia’s tech and energy sectors although downside in the index was stemmed by resilience in gold miners and defensives, while the Tokyo benchmark recouped some of the opening losses on favourable currency flows. Elsewhere, Hang Seng (-0.6%) and Shanghai Comp. (+0.5%) were cautious due to the rising infected numbers and as some businesses resumed operations, although the mainland showed some early resilience amid continued PBoC efforts including the first round of special re-lending funds for tackling the coronavirus and CNY 900bln of reverse repo operations to sustain liquidity levels. Finally, 10yr JGBs were higher amid the cautious risk appetite in the region and with the BoJ present in the market in which it upped the purchases in 10yr-25yr maturities.

Top Asian News

PBOC to Offer First Batch of Special Lending Funds on Monday

Singapore Press Is Said to Pick Banks for Student House REIT IPO

Turkey Deploys Tanks, Commandos to Break Sieges in Syria’s Idlib

Turkey Tightens Grip on Swap Market as Lira Comes Under Fire

Overall a lacklustre start to the week for European equities [Eurostoxx 50 -0.2%] following on from a gloomy APAC session as investors continued to weigh ramifications of the nCoV outbreak in which the death toll exceeded that of the SARS outbreak. Some desks note that this week will be crucial to see if the outbreak morphs into a pandemic (a global epidemic). Back to Europe, bourses are mixed with some mild impetus derived from headlines which reaffirmed China’s commitment to find a breakthrough in drugs for the pathogen (although price action was somewhat fleeting), whilst sectors also broadly mixed with no clear reflection of the overall sentiment. In terms of individual movers, NMC Health (+11.0%) leads the gains in the pan-European index after sources noted that the Co. is in talks with KKR regarding a potential deal, albeit KKR is having trouble fixing a price amid the recent volatility in NMC share prices – a ballpark figure of GBP 2bln is touted. Further, the source added that KKR might face competition from other US-based PE firms. Italian-listed Exor (+6.0%) remains a top gainer in the Stoxx 600 after source reports that Covea is reportedly in discussions regarding the acquisition of the Exor-controlled PartnerRe in an all-cash deal valued at USD 9bln – subsequently, Scor (-2.8%) shares trade lower as Covea hold some 8.5% of Scor. Elsewhere on the downside, Roche (-0.5%) shares are subdued as its top-line results for an Alzheimer’s treatment did not reach a primary endpoint.

Top European News

Storm Hits Parts of Europe With Hurricane-Strength Winds

Atlas Buys Isra for $1.2 Billion as It Moves Into Software

Sinn Fein Ballot Box ‘Revolution’ Rocks Irish Establishment

Italian Banking Mergers Nowhere in Sight as Risks Seen Too High

In FX, the clear G10 outperformers and both fuelled by CPI data, albeit indirectly in the case of the latter. Eur/Nok has recoiled sharply on the back of significantly stronger than expected Norwegian headline and core inflation that was boosted by higher food prices, transport costs and other services items, while Aud/Usd has rebounded on the coat-tails of the Yuan in wake of Chinese CPI beating consensus by some distance and PPI printing positive in y/y terms for the first time in 7 years. The Norwegian Krona is hovering around 10.1300 against the Euro within circa 10.1930-10.1090 parameters and the Aussie is trying to regain grip of the 0.6900 handle vs its US counterpart, as Usd/Cnh pulls back a bit further from recent 7.0000+ peaks despite the PBoC’s firmer Usd/Cny midpoint fix overnight.

GBP/NZD – Sterling has recovered pretty well from another bout of selling pressure that pushed Cable back below 1.2900 and Eur/Gbp over 0.8500 again, but the rationale for the recovery appears as uncertain as the catalyst for the early EU session declines, suggesting technical factors and/or spec positioning looking for sustained Pound weakness that simply failed to materialise. Elsewhere, the Kiwi is pivoting 0.6400 against its US rival, but lagging in Aud/Nzd cross terms ahead of Wednesday’s RBNZ policy meeting even though the prospect of any change in the benchmark rate is deemed remote, and an element of caution could be warranted given a greater chance that guidance may be skewed towards further easing, if warranted and China’s coronavirus causes more widespread contagion.

EUR/CAD/JPY/CHF – All narrowly mixed and rangebound vs the Greenback, as the DXY holds just shy of last Friday’s 97.722 post-NFP high and between 97.709-599, with Eur/Usd tightly bound around 1.0950 irrespective of more poor Eurozone data and political angst (only this time roles somewhat reversed as Italian IP plummeted and Germany’s CDU party leader opts not to run for Chancellor). Similarly, the Loonie is straddling 1.3300 ahead of Canada’s LEI and housing data, while the Yen is holding off recent lows and rebound highs amidst latest reports of a potential anti nCoV ‘breakthrough’ and Franc flitting either side of 0.6775/1.0700 against the Euro after mixed Swiss CPI reads vs expectations and weekly sight deposits.

EM – Broad rebounds against the Dollar, but with the Lira only really stopping the rot with the aid of intervention and capital controls following Turkey’s BDDK lowering bank currency swap and FX forward limits to 10% from 25% previously. Usd/Try meandering from 6.0145 to 5.9775 or thereabouts.

US Event Calendar

Nothing major scheduled

Central Banks

8:15am: Fed’s Bowman to Speak on Community Banks

1:45pm: Fed’s Daly Speaks in Dublin

3:15pm: Fed’s Harker Discusses Economic Outlook

DB’s Jim Reid concludes the overnight wrap

This morning we have launched our 4th monthly market sentiment survey. The link is here. The poll will stay open until around 4pm London time on Wednesday with results out before the EMR on Thursday assuming we’re not using the same app as that used last week in Iowa. Given the primary race is hotting up, the answers to the Presidential questions will be a focus for us this month as will your responses to whether the market has passed the peak point of concern for the Coronavirus or not. We also add back a long term inflation expectations survey we’re going to do every quarter. Most of the other questions remain the same so we’ll be looking at the trends relative to the last three months. We would appreciate as many of you as possible filling it in. You don’t have to answer all the questions, only the ones you’re able to. Many thanks.

I’m about to fly to the US immediately after pressing send on this but given the direction and the intensity of the storm over the last 24 hours here in Europe it might take me until Friday to arrive. Indeed yesterday saw the quickest ever subsonic flight from NY to London due to the jet stream influenced storm. The storm was so wild yesterday that my kids had their noses plastered up to the windows all day at home. By the time it got dark I relented and let them back in.

As we start the new week sentiment has been a little more mixed over the weekend relative to last week as there are some concerns about the spread of the Coronavirus outside of China. The death toll in China has reached 908 (vs 636 on Friday), surpassing the SARS total. The confirmed cases now stands at 40,171 (vs. 31,161 on Friday). The WHO Director-General Tedros Adhanom Ghebreyesus said in a tweet on Sunday that there have been concerning instances of the virus being spread from people with no travel history to China, saying that “we may only be seeing the tip of the iceberg” when it comes to the virus. He also tweeted that “the detection of a small number of cases may indicate more widespread transmission in other countries.” The tweet comes in the light of multiple cases in Europe and Asia being traced to a business meeting in Singapore raising concerns of a super-spreader event. Elsewhere, the quarantined ship in Japan is said to have 60 more cases of the virus adding to the 70 already confirmed. Meanwhile the PBoC have provided the first batch of special re-lending funds post virus and will offer the facility weekly to banks. On a relatively brighter note, Reuters has reported that Hon Hai Precision Industry (Apple’s main local production partner) has received China’s approval to resume some production even if other big companies have further delayed their return from holidays.

Net net, Asian markets are trading lower this morning with the Nikkei (-0.61% ), Hang Seng (-0.62% ), Shanghai Comp (-0.13% ) and Kospi (-0.62% ) all down. However, most markets are off their earlier lows on the Hon Hai news mentioned above. Futures on the S&P 500 are trading flat having been over -0.5% soon after the open. As for overnight data releases, China’s January CPI came in at +5.4% yoy (vs. + 4.9% yoy expected), the highest since October 2011 due to elevated food prices likely around the LNY. PPI stood at +0.01% (vs. 0.0% expected).

We also had elections in Ireland over the weekend and state broadcaster RTE projected late last night that Fianna Fail would win 45 seats, Sinn Fein 37 seats, and Prime Minister Leo Varadkar’s Fine Gael 36 seats — all short of the 80 needed for a majority. It will be interesting to see how the government formation takes place given that both Fine Gael and Fianna Fail have pledged not to enter government with Sinn Fein, which favours higher spending and many more anti mainstream policies.

Moving on, the week after payrolls is often a bit light for macro events but the second Democratic primary in New Hampshire tomorrow will be an additional focus. Meanwhile, attention will also be on Fed Chair Powell, who’ll be testifying before congressional committees on Tuesday and Wednesday. Data highlights include the release of US CPI (Thursday), US retail sales (Friday), and Q4 GDP readings from Germany (Friday) and the UK (tomorrow). Earnings season slows a bit but will still be important.

Going into the New Hampshire primary tomorrow, the RealClearPolitics polling average puts Bernie Sanders in the lead on 26.6%, ahead of Pete Buttigieg on 21.3%. It’s worth remembering that Sanders actually won the New Hampshire primary in 2016 against Hillary Clinton, and it also neighbours his home state of Vermont, which he represents in the US Senate. Nationally the latest poll of polls still have Biden narrowly ahead of Sanders in the race for the nomination but most of the polls are prior to the middle of last week. The last one from Wednesday had Sanders 1pp ahead. In betting markets (PredictIt) Sanders has odds of 46% against Biden who has collapsed to 13% – down over 20pp over the last week.

Staying with the US, the main central bank highlight this week will come from Federal Reserve Chair Powell, who’ll be appearing before the House Financial Services Committee tomorrow, and then the Senate Banking Committee on Wednesday. He’ll be delivering the Fed’s semi-annual monetary policy report to Congress, so it’ll be interesting to hear his latest views on the outlook even if they are unlikely to deviate much from the last FOMC. Another event to watch out for on Thursday will be the hearing held by the Senate Banking Committee regarding the nomination of Judy Shelton and Christopher Waller to be governors on the Federal Reserve Board.

Turning to data releases, they will all be a little backward looking given the Coronavirus but will show the direction of travel pre outbreak. In the US a key highlight will be CPI on Thursday, which is expected to increase to +2.5%, up from +2.3% previously, to what would be its highest level since October 2018. However, the core reading is expected to fall slightly to +2.2%. Other important readings to watch out for include January’s retail sales and industrial production releases on Friday, as well as the preliminary reading of the University of Michigan consumer sentiment index, which rose to an 8-month high in January.

One of the main highlights from Europe will be the preliminary estimate of German GDP for Q4 on Friday. The consensus is expecting a +0.1% increase, following the +0.1% growth in Q3. However it comes against the backdrop of unexpectedly poor German data out this week on factory orders as well as industrial production for December, so an important release to keep an eye out for. In terms of other GDP releases from Europe, tomorrow sees the preliminary Q4 GDP reading from the UK, which is expected to show a flat reading following growth of +0.4% in Q3. Finally, there’ll be the second release of GDP for the Euro Area on Friday, though this is expected to be in line with the first estimate, which saw the region’s economy expand by +0.1%.

Earnings season slows down (148 S&P 500 and Stoxx 600 companies) but in terms of what to look out for this week, Daimler will be reporting tomorrow, then on Wednesday, we’ll hear from Cisco Systems, CVS Health and CME Group. It’s a busy day on Thursday, with companies reporting including Nestle, PepsiCo, Nvidia, Airbus, Linde, Zurich Insurance Group, AIG, Barclays, Credit Suisse and Nissan. Then on Friday, we’ll hear from AstraZeneca, Credit Agricole, Royal Bank of Scotland.

We are now 64% of the way through the S&P 500 Q4 earnings season. 71% of companies are beating estimates which is slightly below the five-year average of 75%. In aggregate, companies are currently beating by +4.6% above the estimates, above the longer-run historical average rate (+3.4%) but below the five year average (+5.4%). Our Asset Allocation team has pointed out that the decline in margins has been led by the Energy and Materials sector. This is likely a reflection of lower commodity prices, but the trend has been broad based with margins down across all sectors.

Recapping last week now, Global equities reversed a two week slide as fears surrounding the coronavirus subsided significantly, especially in US and European markets. The S&P 500 had its best week in 8 months, gaining +3.17% (-0.54% Friday), even with a slight pullback into the weekend. The risk resurgence came on the back of news of stimulus in China, signs that the pace of virus infections were slowing, further tariff cuts on the US, and solid economic data. Europe and Asia saw similar reactions, where the STOXX 600 erased last week’s losses and gained +3.32% (-0.26% Friday), while in Asia, Hong Kong’s Hang Seng rallied +4.15% (-0.33% Friday). Commodities had a more mixed week on the risk front. Copper broke out of a 13 day streak of losses midweek, with 3 up-days a row before retreating -1.77% on Friday, but the industrial metal rallied +2.64% on the week. Even while risk markets recovered around the world, Brent crude continued to fall, retreating -6.29% (-0.78% Friday), its 5th consecutive weekly move lower and its lowest weekly close since December 2018. Gold closed -1.19% lower on the week (+0.23% Friday), as markets rotated away from safe havens particularly in the early part of the week.

As equities rallied, sovereign debt partially reversed its gains from the last few weeks, with 10yr Treasury yields up +7.7bps (-5.9bps Friday) to 1.583%, its largest weekly rise in seven weeks. 30yr Treasury yields closed back over 2%, gaining +4.9bps on the week (-6bps Friday to 2.048%). With German industrial production in December underperforming expectations bund yields fell -1.6bps on Friday, even as they sold off +5.0bps on the week. That was their first weekly rise in yields in four weeks.

In Europe, German industrial production fell -3.5% in December, versus a +1.2% increase in November. Similarly, French industrial production dropped -2.8% in December, after registering no change in November. The US jobs report showed nonfarm payrolls grow by +225K jobs (+164k expected) in January, the unemployment rate rose to 3.6% and average hourly earnings rose by +0.2%. Our Economists believe the outsized print pointed to a warm-weather related boost as construction outperformed, while the unemployment rate was up but mainly due to participation being up. In other data, wholesale inventories fell by -0.2% in December.

…though the image presented by state controlled media was somewhat more optimistic.

Along with many other Chinese cities, Monday marked the first working day in Shanghai after the long Spring festival break. The flow of commuters and traffic amid the #coronavirus outbreak increased significantly compared to previous days. https://t.co/wKFXxhUKKu#NCPpic.twitter.com/46dfKobHAr

Still, western media reported that “millions” returned to work on Monday, even if large swaths of the Chinese economy remained shut down, CNN reports. However, many will be working from home if possible. The total number of cases worldwide has now topped 40,000, while the death toll has hit 910, according to the most up-to-date data from the SCMP:

But even as workers started to log back in, or even returned to the office in some rare cases, nearly 100 more were declared dead from the outbreak, a daily record. Meanwhile, as we noted last night, the WHO – which previously had aggressively kowtowed to Beijing – said the number of cases outside China could be “just the tip of the iceberg,” according to Reuters.

Across mainland China, 3,062 new infections were confirmed on Sunday, bringing the total number to 40,171, according to the National Health Commission (NHC).

Wu Fan, vice-dean of Shanghai Fudan University Medical school, said there was hope the spread might soon reach a turning point.

“The situation is stabilising,” she told a briefing when asked about the spread in Shanghai, which has had nearly 300 cases and one death.

But WHO chief Tedros Adhanom Ghebreyesus, speaking in Geneva, said there had been “concerning instances” of transmission from people who had not been to China.

“The detection of a small number of cases may indicate more widespread transmission in other countries; in short, we may only be seeing the tip of the iceberg,” he said.

Dr. Tedros added that the WHO is monitoring 10 Chinese provinces as possible virus ‘hot spots’.

But outside China, the viral outbreak is beginning to take on more characteristics of a global pandemic. An outbreak at a ski chateau in the French Alps has reawakened anxieties about an uncontrolled outbreak in Western Europe, as government health officials in Britain and France scramble to trace everybody who had contact with a British citizen who apparently picked up the virus during a visit to Singapore.

Authorities worry that this unnamed ‘patient zero’ might be a ‘super spreader’: The man unknowingly carried the virus across continents, and at least six people have already been sickened after coming into contact with him. Research released last week suggested that the virus can spread before symptoms are present. on Monday, the British secretary of state declared the virus “a serious and imminent threat to public health.” This gave the government new powers to forcibly quarantine people after one infected patient tried to leave Arrowe Park, where the British government has quarantined some of those who just returned from Wuhan. In Hong Kong, two people appear to have escaped from a mandatory quarantine, prompting police to issue wanted notices.

“The Secretary of State declares that the incidence or transmission of novel Coronavirus constitutes a serious and imminent threat to public health,” the U.K. health ministry said in a statement on Monday.

“Measures outlined in these regulations are considered as an effective means of delaying or preventing further transmission of the virus.”

All rescued Britons signed a contract agreeing to a 14-day quarantine period at a place of the government’s choosing. On Monday, EasyJet has confirmed that a passenger who recently flew aboard one of its flights had been diagnosed with the coronavirus. The airline said Public Health England is reaching out to passengers.

Public Health England said Monday that anyone who has had contact with the newly confirmed cases should seek help immediately. Dr Nick Phin, deputy director of National Infection Service at Public Health England, said the following, according to the Guardian:

These new cases are all closely linked and were rapidly identified through Public Health England’s comprehensive contact tracing approach and tested quickly.

Our priority is speaking to those people who have had close and sustained contact with confirmed cases so that we can advise them on what they can do to limit the spread of the virus.

Back in China, Reuters reports that more than 300 Chinese firms, including Meituan Dianping, China’s largest food-delivery company, and Xiaomi, the smartphone-making giant, have sought bank loans of at least #8.2 billion (5.4 billion yuan). The PBOC has said it will offer special lending facilities, providing the first batch of re-lending fundings on Monday. It plans to offer the facility weekly until the outbreak subsides. Reuters also reported that Apple supplier Foxconn was ultimately not allowed to resume production at its plant in Shenzen, which had been shuttered by authorities during the outbreak. In another blow to Beijing, Mongolia, China’s impoverished northern neighbor, has suspended exports of coal to China until March 2, according to the country’s National Emergency Commission. The Commission has also recommended cancelling the Mongolian Tsagaan Sar Lunar New Year celebrations set for later in the month.

Picking up from where JPM left off, research firm Capital Economics said Monday that based on forecasts for global GDP, the outbreak could cost the world more than $280 billion during the first quarter of 2020, Bloomberg reports.

Airbnb has suspended Beijing bookings until at least the end of February while promising to “refund and support guests who had cancelled reservations. And we will continue to work diligently to build programs that support our community of hosts.”

Fitch ratings warned overnight that China’s international profile “could diminish” because of the outbreak for two reasons: One, China might once again turn inwards as policymakers focus on maintaining social order and fighting the virus, two, foreigners might start to turn away from China (or maybe even move jobs back to North America, as Wilbur Ross suggested).

Authorities said they would inspect the plant “later this week” to ensure virus-control measures are being properly implemented. This after authorities initially denied reports that the plant wouldn’t reopen, though they said the plant’s reopening would be contingent on it passing an inspection.

But China isn’t the only country feeling the blowback. Sony said earlier that it wouldn’t attend the Mobile World Congress conference in Barcelona later this month because of virus-related fears. After all, the Japanese already have enough on their hands with the ‘Diamond Princess’ and the two dozen-plus infected patients scattered around the country.

More countries are planning evacuation missions to rescue citizens trapped in Wuhan and other parts of China. Reuters has put together a list (text courtesy of the Guardian) of countries that have carried out at least one evacuation mission so far…

Kazakhstan will send two planes to China on 10 and 11 February to evacuate its citizens. Kazakhstan has already evacuated 83 people from Wuhan. Of the 719 Kazakhs remaining in China, 391 have asked to be repatriated.

Singapore: A second evacuation flight is bringing back another 174 Singaporeans and their family members from Wuhan to the city-state on 9 February, Singapore’s foreign ministry said.

Philippines: Thirty Filipinos returned to the Philippines on 9 February from Wuhan, the department of foreign affairs said. The returning passengers and a 10-member government team will be quarantined for 14 days.

UK: Britain’s final evacuation flight from Wuhan, carrying more than 200 people, landed at a Royal Air Force base in central England on 9 February. A plane carrying 83 British and 27 European Union nationals from Wuhan landed in Britain last week.

Brazil: The 34 Brazilians evacuated from Wuhan landed in Brazil on 9 February, where they will begin 18 days of quarantine.

US: Two planes with about 300 passengers, mostly US citizens, took off from Wuhan on 6 February bound for the US. It was the third group of evacuees from the heart of the coronavirus outbreak, the US state department said.

Taiwan: About 500 Taiwanese stranded in Wuhan are the first batch to be evacuated

Uzbekistan: 251 people from China and quarantined them on arrival in Tashkent, the Central Asian nation’s state airline said on 6 February.

Italy: The country flew back 56 nationals from Wuhan to Rome on 3 February. The group will spend two weeks in quarantine in a military hospital, the government said.

Saudi Arabia: 10 students from Wuhan have been evacuated, Saudi state television reported on 2 February.

A plane-load of New Zealanders, Australians and Pacific Islanders evacuated from Wuhan arrived in Auckland, New Zealand on 5 February, officials said.

Thailand: A plane brought 138 Thai nationals home from Wuhan last week. They will spend two weeks in quarantine.

France: Some nationals have been evacuated from Wuhan and would be placed in quarantine. It said it would first evacuate nationals without symptoms and then those showing symptoms at a later, unspecified date.

Canada: The first group of 176 citizens were evacuated from Wuhan to an Ontario air force base early on 5 February, according to the Globe and Mail newspaper. All evacuees will be quarantined on the base for two weeks.

Japan: The country has repatriated 565 nationals since the end of January.

South Korea: About 368 people were flown home on a charter flight that arrived on 31 January. A second chartered flight departed Seoul for Wuhan on the same day, with plans to evacuate around 350 more South Korean citizens.

Indonesia: The government flew 243 Indonesians from Hubei on 2 February and placed them under quarantine at a military base on an island north-west of Borneo.

…and a (much shorter) list of countries that are still in the ‘planning stages’:

Netherlands: The country is preparing the voluntary evacuation of 20 Dutch nationals and their families from Hubei, Stef Blok, the Dutch foreign minister, said. The Netherlands is finalising arrangements with EU partners and Chinese authorities.

Spain: The government is working with China and the European Union to repatriate its nationals.

* * *

So far, two foreigners have died within China, one Japanese, one American, news we reported last week.

Those who have already been rescued from Wuhan in the US, UK and other countries are nearing the end of their 2-week quarantine detentions. Unfortunately, Chinese scientists are now saying 14 days might not be long enough for symptoms to appear. At least one patient exhibited no symptoms for 17 days – a full 2.5 weeks.

That’s bad news for the cruise ship that was allowed to sail away from Hong Kong after just a four-day hold.

Speaking of Hong Kong, CNA reports that a 24-year-old man and his grandmother, 91, were initially confirmed to have the virus, but later spread it to seven other family members, including the boy’s father, mother, two aunts and three cousins were also infected.-

Officials said the family was part of a gathering of 19 who shared the hotpot meal over the Lunar New Year holiday at the end of January. A hotpot – also known as a steamboat – is a bubbling cauldron of stock shared communally, to which diners add ingredients.

Hoarding that started in Hong Kong last week has already spread to Singapore, where CNBC reports shelves are running bare as hundreds of thousands of people scramble to brace for a worsening outbreak.

First found in the city of Wuhan in central China last December, the new coronavirus has infected nearly 37,200 people on the mainland and at least 36 in Hong Kong.

One day after the New York Times published a story asking “Where’s Xi?” in the headline, the President/God-Emperor of China has finally appeared in public, wearing his facemask in the correct fashion (several local officials in Hubei elicited an avalanche of public criticism for appearing in public without masks, or with their masks worn incorrectly).

State Broadcaster CCTV aired a brief segment featuring Xi visiting a neighborhood in Beijing. In keeping with the Chinese state’s propaganda narrative, Xi “investigated and directed” the ongoing virus prevention work and asked after residents and workers.

Video: Chinese President Xi Jinping inspected the #novelcoronavirus pneumonia prevention and control work in Beijing on Monday afternoon. Xi visited residents and staff in a community in Chaoyang District to learn about the situation of the frontline work. https://t.co/n2zr4Ckifspic.twitter.com/fYLk7DqIzs

Xi said Monday that China would take “more decisive” measures to suppress the virus. Those words should send a shudder of anxiety through a population that had expected to return to work on Monday, only to find that one most offices and factories remain closed.

Xi visited the Chaoyang district, according to state-run media Xinhua

As we reported earlier, the number of confirmed cases aboard the ‘Diamond Princess’ cruise ship under quarantine in Japan has climbed to 136.

Across China, public anger over the death of Dr. Li, a martyr who was one of eight doctors punished by local authorities for speaking out about the virus. He succumbed to the virus last week, making him the first outbreak martyr. While his portrait has circulated on the Internet, and in fliers, Weibo has introduced a new emoji on the Chinese Internet to commemorate Li: A chicken drumstick.

“Give Dr Li a fried chicken drumstick!” A new emoji featuring a fried chicken drumstick was added to #China‘s Twitter-like platform, Weibo, to commemorate “whistleblower” doctor #LiWenliang, who was believed to love eating fried chicken drumsticks. Li died from #nCoV Friday. pic.twitter.com/LpUxAPKxcf

The virus has spread to at least 27 countries and territories and infected more than 330 people outside China. While vaccines have been tested on animals, China’s CDC announced Monday that animal testing was in the “very early stage” of vaccine development. With the number dead already having surpassed the total number of deaths from the SARS outbreak by a margin greater than 100, many are bracing for the outbreak to be much worse than experts had anticipated.

Victoria’s Secret Sale To Sycamore Imminent; L Brands’ Shares Pop

Shares of Victoria’s Secret parent company L Brands jumped 10% Monday on news private equity firm Sycamore Partners is close to a deal to purchase the women’s lingerie brand, reported CNBC.

News of the potential deal involving Sycamore was released in the overnight hours, with more details expected this week.

There was no word on a succession plan for L Brands CEO Les Wexner. Still, as we noted several weeks ago, his mediocre performance as CEO and controversial relationship with late sex criminal Jeffrey Epstein, assured that his time at the helm of the company is coming to an end. That said, since we first previewed the potential sale of Victoria’s Secret, there has been no indication if the transaction is tied to Wexner’s relationship with Epstein.

Victoria’s Secret has experienced declining sales in the last four years, which triggered a mass exodus of investors from L Brands’ stock, sending it plunging 74% since 2016. Shareholders criticized Wexner for his inability to evolve Victoria’s Secret to changing consumer demands, despite L Brands having massive success in its other companies, such as Bath & Bodyworks personal care shop.

Victoria’s Secret generated $7.4 billion in sales last year but has been considered a dying brand among consumers.

The brand canceled its once-popular annual fashion show several months ago, ironically as “woke culture” deemed it objectifying of women.

Sycamore already owns department store Belk, office retail company Staples, women’s apparel brand The Limited, music store Hot Topic, and fashion brand Torrid.

Despite the Senate’s vote to reject the two articles of impeachment of President Trump, numerous lawsuits seeking access to White House and other records continue. On March 31, the Supreme Court will hear oral argument in three cases concerning the ability of Congress and a New York grand jury to obtain the President’s financial records (Trump v.Mazars, Trump v. Deutsche Bank, and Trump v. Vance). Meanwhile, other cases pending in the District of Columbia concern efforts to obtain material related to the Mueller investigation.

Last month, I participated in half-day conference organized by the Levin Center at the Wayne State University Law School on “The Emerging Caselaw of Congressional Oversight,” with Professors Victoria Nourse, Kirsten Matoy Carlson, and Andrew Wright. Video of the full event is available here.

For more information on the various cases, the Levin Center has also put together a useful website with documents and summaries of the issues in these and other cases concerning Congressional oversight. It’s a useful resource for more information on the legal issues concerning the scope of legislative oversight of the Executive Branch, and President Trump in particular.

from Latest – Reason.com https://ift.tt/2tJGe4K

via IFTTT

Despite the Senate’s vote to reject the two articles of impeachment of President Trump, numerous lawsuits seeking access to White House and other records continue. On March 31, the Supreme Court will hear oral argument in three cases concerning the ability of Congress and a New York grand jury to obtain the President’s financial records (Trump v.Mazars, Trump v. Deutsche Bank, and Trump v. Vance). Meanwhile, other cases pending in the District of Columbia concern efforts to obtain material related to the Mueller investigation.

Last month, I participated in half-day conference organized by the Levin Center at the Wayne State University Law School on “The Emerging Caselaw of Congressional Oversight,” with Professors Victoria Nourse, Kirsten Matoy Carlson, and Andrew Wright. Video of the full event is available here.

For more information on the various cases, the Levin Center has also put together a useful website with documents and summaries of the issues in these and other cases concerning Congressional oversight. It’s a useful resource for more information on the legal issues concerning the scope of legislative oversight of the Executive Branch, and President Trump in particular.

from Latest – Reason.com https://ift.tt/2tJGe4K

via IFTTT

More than 2,500 homeless individuals sleep on the streets of the 53-square-block Skid Row area in downtown Los Angeles.

“Skid row is the worst man-made disaster in the United States. There’s human waste on the sidewalks. There’s all kinds of disease,” says Rev. Andy Bales, CEO of Skid Row’s Union Rescue Mission, the nation’s largest private homeless shelter.

While California’s homelessness crisis extends far beyond L.A., the city’s predicament is notable for its sheer scale. It has the highest unsheltered homeless population in the country, and more than 1,000 homeless people died on the streets of Los Angeles County last year, according to government figures. The problem is so bad that in 2016, 76 percent of L.A. voters approved a bond referendum to spend more than $1.2 billion in public funds on 10,000 new apartment units for the homeless.

The plan called for completing construction within a decade, but just 1 percent of those apartments will be ready for occupancy by the end of 2019. Now, homeless advocates like Bales are concerned that the city is wasting money on the most expensive possible solution—one that might not work as advertised even if it weren’t behind schedule and likely to bust its own budget.

The city’s approach to homelessness, known as “housing first,” was adopted by municipalities nationwide after Utah reportedly reduced chronic homelessness by 91 percent by giving away permanent apartments with no strings attached. But state auditors later attributed those findings to a data collection error. Utahans don’t actually know what effect various programs have had on the state’s homeless population, which, in any case, is estimated to be two-thirds the size of just Skid Row’s.

What’s more, building housing for the homeless is considerably more costly and complex in Los Angeles than in Salt Lake City, thanks to local and statewide zoning and environmental regulations that allow labor unions, homeowners, and other parties to bring housing development to a standstill. Advocates are now watching in frustration as such roadblocks drive up the cost of the city’s housing first efforts, while cheaper, faster solutions congeal on the back burner.

L.A. initially estimated the permanent units would have a median cost of $350,000 apiece—not cheap to begin with. Three years later, the estimated cost has increased to more than $500,000 per unit, with some units approaching $700,000. (The median price of a condo in Los Angeles was $581,000 as of this writing.)

“We cannot spend $600,000 per person per unit and ever get it done,” says Bales. “We’ve got to think innovatively or we’re going to have a bigger disaster on our hands.”

Union Rescue Mission just opened what’s called a Sprung structure—a relatively inexpensive but sturdy and weather-resistant tent with 120 beds. Bales wants the city to invest more in Sprung structures and other cheap, easily constructed solutions like mobile homes, container homes, or even 3D-printed houses (see page 5). Under increasing pressure in recent months, the city has erected a few of its own Sprung structures to address the crisis, but Bales believes it’s still not nearly enough.

“It’s ridiculous,” he says. “I mean, who would want to leave 44,000 people on the streets to die while you stick with your very expensive plan to help a few?”

For a video version of this story, visit reason.com.

from Latest – Reason.com https://ift.tt/2UD25G8

via IFTTT

‘Diamond Princess’ Reports 66 New Coronavirus Infections, Bringing Total Onboard To 136

The nightmare cruise from hell just got even worse for the thousands of passengers still aboard.

The Diamond Princess, the cruise ship that has been quarantined off the coast of Yokohama, Japan for roughly a week now, saw the total number of confirmed nCoV infections climb to 136 on Monday, cementing its position as the host of the largest outbreak outside China.

Japanese health authorities have been extremely careful in dealing with the ship, which has become a massive albatross for the government of PM Shinzo Abe. While Hong Kong let a cruise ship sail yesterday following a 4-day quarantine (the ship was reportedly found to be free of viral infections), the ‘Diamond Princess’, and the 2,500+ remaining passengers and crew, will be stuck in place until mid-February. The NYT chronicled the growing sense of unease and paranoia aboard the ship, which we cited yesterday.

The ship’s captain Stefano Ravera announced Monday that 66 new cases of the virus had been confirmed, bringing the infection total of passengers and crew to 136, roughly equal to all the other cases in Asia outside China. Media reports have claimed more than 2,500 passengers and crew remain aboard the ship.

According to CNBC, the nationalities of the newly infected are Japanese (45), American (11), Australian (four), Filipino (three), Canadian (one), English (one) and Ukrainian (one). Notably, all of these infections occurred person to person, since they were all spread from ‘patient zero’ to others aboard the ship.

Princess Cruises, the Carnival Japan unit that owns the ship, told NBC News that it was continuing to follow guidance from Japan’s health ministry regarding plans for providing medical care and passengers ultimately disembarking. Meanwhile, one passenger told the NYT yesterday that those aboard the ship are being left in the dark, and have resorted to tracking the comings and goings of ambulances to try to keep abreast of what’s going on. Many suspect the virus has been spread through the ship’s ventilation system.

The ship was quarantined for two weeks after a passenger who disembarked in Hong Kong on Jan. 25 tested positive for the virus six days after leaving. After initially finding no cases aboard the ship, the cruise line copped to the first ten cases, prompting more intense scrutiny by the Japanese government. Princess Cruises said it didn’t expect new cases to be confirmed after the beginning of the quarantine, though that has clearly happened.

So far, it doesn’t look like the virus has made the jump from the ship to the surrounding area. If that happens, expect Japanese authorities to resort to the same types of draconian quarantine measures that have been imposed in China.