The La Paz County, Ariz., sheriff’s office says it is investigating a deputy who stopped a driver because he had an air freshener hanging from his rear view mirror. Video of the stop by that driver, Phil Colbert, shows the deputy tell Colbert he can’t have the air freshener hanging from his mirror because it could distract him. It also shows the deputy asking him if he has weapons in the car, if he has marijuana in the car, when the last time was that he smoked marijuana, if he has cocaine, if he has heroin, if he has used drugs in the past two days, if he has a medical marijuana card, and if he will consent to a search of the vehicle. The deputy repeatedly accuses Colbert of being nervous, which the deputy says is a sign of deception. The video ends with the deputy giving Colbert a warning for the air freshener and telling him he should have a more positive attitude towards law enforcement.

from Latest – Reason.com https://ift.tt/318I9ue

via IFTTT

The Swedish Board of Education has backed down from a plan to erase teaching of the country’s ancient history and replace it with “postmodernism” classes after a huge backlash.

Skolverket initially announced a plan to abolish teaching of history prior to 1700, including ancient Greece, the Swedish Great Power era in the 17th century, Rome, and the dark ages.

The classes were set to be replaced by a greater focus on “postmodernism” and the post war 20th century era.

However, the board was forced to back down after acknowledging there was “a lack of support for our suggestion.”

The original proposal was widely denounced, including by Professor of History Dick Harrison, who labeled the idea “intellectual suicide and f**king sick.”

One wonders what kind of state a country is in that it would try to abolish teaching of its own history.

Back in 2017, “cultural journalist” Kristina Lindquist said that Sweden is so xenophobic, it doesn’t even deserve to celebrate its own national day and that “nationalism should be wiped out.”

The next year, Sweden appointed a Pakistani Muslim migrant as the head of its national heritage board, with the individual admitting that he had not “read anything about cultural heritage.”

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

“A Serious Malfunction” – How French Intelligence Overlooked The Terrorist In Their Ranks

It’s an alarming oversight with terrifying implications: The intelligence unit of Paris Police somehow overlooked a radicalized Islamic convert within their own ranks. Last week, the troubled individual in question carried out an attack inside Paris Police headquarters that ended with four victims stabbed to death, while the attacker was shot down by his former colleagues.

WSJ has the full the story of how Mickaël Harpon, the 45-year-old attacker in question, evolved from a quiet IT expert into a disaffected convert to Salafism – a fundamentalist version of Islam that is widely credited as the inspiration for Al Qaeda and other terror groups.

According to WSJ, the attack has destroyed the country’s confidence in its intelligence apparatus and its procedures for rooting out potential purveyors of Islamic terror.

Even though he worked inside the Paris Police’s Intelligence Unit, his transformation into a dangerous ideologue somehow went unnoticed. What’s worse: As one of the unit’s IT specialists, Harpon had access to top-secret information, including the identities of agents going undercover inside mosques around the city. His desk was positioned just steps away from the division’s leaders. Now, hundreds of agents are examining flash drives found at Harpon’s desk, and they’re trying to determine whether he shared any classified intel with other extremists.

Despite his seeming importance within the organization, Harpon told friends that he felt he wasn’t being taken seriously at the office, and that he suspected he had been passed over for promotion because of a disability.

The disability? Deafness in one ear that forced him to wear a hearing aid. The disability stemmed from his childhood on the French Caribbean island of Martinique. As a boy, Harpon was afflicted with meningitis in his youth. The sometimes fatal illness caused the hearing loss.

Soon after he was hired by the intelligence division inside the Paris police force in 2003, his superiors found him to be a dedicated and efficient employee. Slowly, he gained more trust and more seniority within the organization. He converted to Islam several years after joining the Paris PD, after he had moved in with a Muslim woman from Madagascar. They eventually married, despite a complaint filed by the woman claiming she had been abused by Harpon. The complaint was later withdrawn, but it resulted in Harpon receiving an administrative sanction.

When he married, Harpon should have triggered another background check for himself and his bride. However, it was never carried out, and he maintained his security clearance.

French Interior Minister Christophe Castaner described this oversight as “a malfunction”.“Would that have changed things? I don’t know,” he added.

But that’s not even the most galling oversight. In 2015, shortly after the shooting at the offices of Charlie Hebdo, a colleague of Harpon’s allegedly heard him comment that the victims “deserved it.” He reported this comment to superiors within the department. But shockingly, nothing was done.

There was neither a mention of the complaint in Harpon’s personnel file, nor a motion to carry out another background check. His next background check to maintain his security clearance was slated for 2020.

Castaner described this oversight as “a serious malfunction.”

A friend of Harpon’s told WSJ that he was a quiet man who never showed any indication that he had become radicalized, and was planning an attack.

“He felt people didn’t take him seriously because of his handicap,” the friend told WSJ.

Even his wife told police that she didn’t suspect an attack. At worst, she feared, Harpon might kill himself.

Hopefully, French intelligence will tighten up its security standards and oversight of its employees after this incident. But winning back the trust of the public will probably require a serious effort on behalf of the agency.

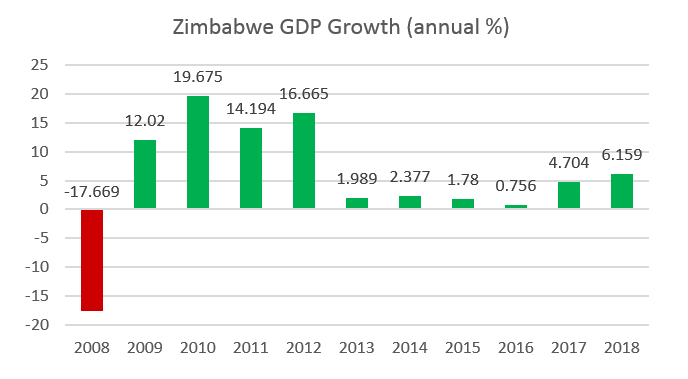

It has been over a decade since Zimbabwe was ravished by one of history’s worst experiences in hyperinflation, reaching 79,600,000,000 percent as prices doubled approximately every 24.7 hours in November of 2008. Today under new leadership, it seems as though the government of Zimbabwe has failed to learn from its previous mistakes in what policy to ascribe to as it enters into another period of tumultuous times and economic hardship for its citizens as hyperinflation has entered the picture again.

Zimbabwe’s horrendous experience with hyperinflation came from monetizing its expenses as a result of several years of failed political reforms such as confiscation of agricultural properties and price controls. This resulted in GDP declining -17 percent in 2008 (see Figure 1). With Zimbabwe’s practice of printing money, the government decided in 2009 to abandon their local currency and replaced it with foreign currency such as the US dollar and African Rand, which helped provide more stabilization.

Figure 1: Source: World Bank (Zimbabwe GDP 2008–2018)

However, after its rapid expansion from 2009 to 2012, Zimbabwe’s economy began to slow down significantly in 2013 as they were met in the beginning of the year with the government having a minuscule balance of $217 in its public account. The same year Robert Mugabe, representing the ZANU-PF party, was reelected in the general election with the promise of continuing indigenization policies. The indigenization policies would attempt to create greater equality and economic growth by violating property rights and requiring foreign or white-owned companies to give a majority portion of their ownership to indigenous blacks. In doing so, Mugabe’s policy sent uncertainty within the market as it discouraged future foreign investment with the threat of asset confiscation, creating a lack of capital to expand production.

In addition, thanks to continued regime uncertainty, and with no monetary policy of its own, by 2014 Zimbabwe began to experience a shortage of physical cash which had reportedly led some people to use candied sweets and condoms in replace of change. Combined with this challenge, Zimbabwe had a poor harvest as it faced a drought in 2016 affecting five million people causing it to run a USD 1.4 billion deficit that made up 10 percent of national output causing an even further shortage of cash.

On November 21, 2017, after 37 years of ruling Zimbabwe with an iron fist, Mugabe resigned amidst political pressure of impeachment through a military coup. By the end of that week on the 24th, Emmerson Mnangagwa had become the new president of Zimbabwe. Immediately following Mnangagwa’s ascension to power, the president assured the population of drastic policy changes to help stabilize and boost economic growth.

Shortages and Price Controls

In the start of 2019, Zimbabwe’s highly-regulated economy began to experience a shortage of fuel. To curb the demand, and as an attempt to keep fuel supplies within the country, Mnangagwa decided to use the state-managed energy sector to raise diesel by 125 percent and petrol by 131 percent overnight. Such a drastic increase immediately led to a three-day protest leaving 12 people dead and 78 treated for gunshot wounds as a result.

In Zimbabwe, the increase in the price of fuel has caused transportation costs to soar, which resulted in detrimental effects for businesses as their costs rose. In order to compensate for the increased cost in fuel, entrepreneurs must offset that by either lowering profit margins or raising prices. In an interconnected economy where entrepreneurs rely on each other to supply goods and services to each other and utilize those goods and services for future production when one entrepreneur increases their prices, this begins to cause other entrepreneurs to raise their prices in order to maintain profitability.

Returning to Local Currency

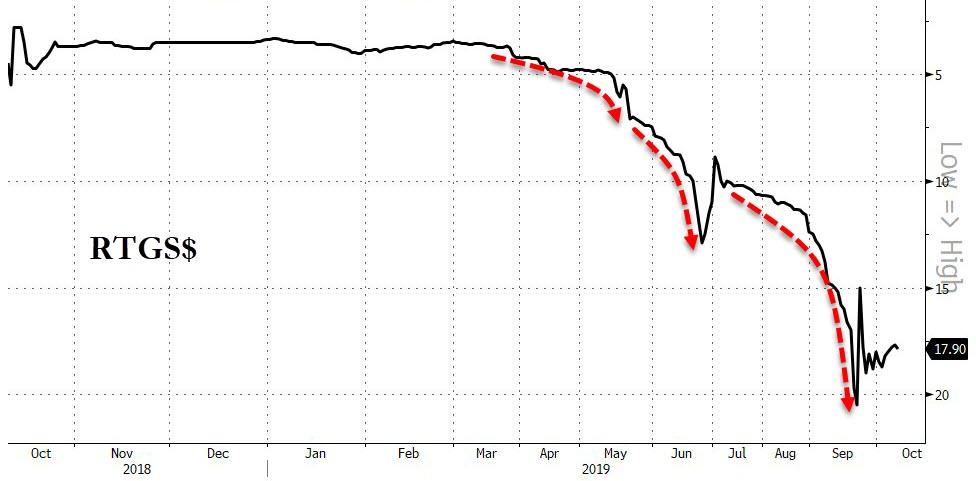

By June of this year, worsened by a variety of factors from fuel prices to declining domestic output, ZIMSTATS (Zimbabwe National Statistics Agency) reported that inflation in Zimbabwe had reached 175.66 percent%. In an effort to to combat this hyperinflation, Zimbabwe’s finance minister Mthuli Ncube then declared that the use of foreign currency will be forbidden in domestic transactions and that its civilians can only use electronic Real Time Gross Settlement Dollars (RTGS) to combat the shortage of US dollars. If a citizen decides to withdrawal the RTGS from their local bank, then they will receive paper bond notes in the denominations of $2, $5, $10, and $20.

Source: Bloomberg

Adopting the RTGS as a single unit of exchange is a rapid change from the not too long ago hyperinflation blunder. After 2009, the Zimbabwean state had stabilized its monetary affairs by using nine different currencies as legal tender. Now, the act of abolishing the use of foreign currency will only invoke the practice of off-the-grid transactions through the black market if businesses lose confidence in the RTGS. Confidence in the RTGS has already taken a hit as the black market ratio for RTGS to USD has reached 11 to 1 compared to the governments set ratio at 6.2 to 1. The difference in exchange ratios has shown that Zimbabwe cannot be trusted by issuing its currency as people have yet to build that confidence since it’s debacle in 2008.

Furthermore, Zimbabwe has suffered a drought this year and is estimated to have its corn crop drop by 54 percent, which would result in the necessity to import corn to make up for the shortage. However, importing goods is challenging, considering the country has been short of US dollars for the past few years. In the same period, Zimbabwe has also undergone continuous power outages due to the drought, lasting up to 18 hours per day and costing manufacturers over $200 million in lost production. To make matters worse President Mnangagwa in August raised fuel for the seventh time up over 500 percent.

Since the inflation report, Zimbabwe’s finance minister Mthuli Ncube said that inflation figures would be postponed until February 2020. The reason for the delay is so that government officials will have more time and information to accurately determine what the inflation rate is as the present prices are not measured in US dollars. However, many citizens have objected to this postponement with the belief that the government is attempting to hide the real inflation rate while the black market inflation rate in Zimbabwe is estimated to be at 558 percent.

When government intervenes within the market by setting the price of a commodity outside of the natural market forces of supply and demand while enforcing legal-tender laws to require its citizens to make transactions in a currency they do not trust, such actions will inevitably lead to hyperinflation such as the situation in Zimbabwe. As we reflect upon the present crisis and monitor the situation until the next inflation statistics come out in 2020, the conditions look gloomy going forward unless Zimbabwe changes its direction toward more free-market-oriented policies and avoids continued government intervention that impoverishes the standard of living of its people.

Former US-Backed Rebel Leader Now Spearheading Attack On US-Backed Syrian Kurds

Turkish President Recep Tayyip Erdogan announced Thursday that his forces have killed 109 Syrian Kurdish militants since the start of the northern Syria incursion, dubbed ‘Operation Peace Spring’.

“The operation is currently continuing with the involvement of all our units… 109 terrorists have been killed so far,” Erdogan stated, as quoted by Reuters.

At the same time pro-Kurdish media sources have cited nearly a dozen pro-Turkish forces killed in border areas where both sides have clashed on the ground.

Currently it appears Turkey is mustering large forces and cutting off communications and ground access points outside the largest Syrian population centers near the border, ahead of expected major clashes.

#Turkey-backed troops crossing into NE #Syria to cut the #Derbassia#Rasulayn roads.

So far, the established bridgehead/corridors show them avoiding the fight in built up areas, cutting communication and supply routes and working on besieging large population centres. pic.twitter.com/1VoF8jYFZP

Local reports suggest Kurdish YPG/SDF forces are prepping their fighters for major urban ground warfare while their families continue to flee to safer zones.

Though at this point it is impossible to gain an accurate civilian casualty toll figure, which is likely much higher, international reports citeat least 8 Syrian civilians killed after yesterday’s first wave of Turkey’s military operation, including at least two children among the dead.

The Turkish-backed Syrian National Army (SNA), comprised of former ‘Free Syrian Army’ (FSA) and Syrian al-Qaeda linked militants (and likely former ISIS members) — now spearheading the ground invasion — have reportedlycaptured at least two towns after pushing south from the Turkish border.

Underscoring the absurd contractions of Washington’s Syria policy over the course of the past seven years of proxy war, the pro-Turkish Syrian National Army rebels areactually led by Salim Idris (among two other top commanders), the former Chief of Staff of the Supreme Military Council of the FSA.

The late Senator John McCain posed for a picture with Syrian ‘rebel’ leader Gen. Salim Idris (2nd Right) in 2013. Others photographed alongside McCain were later confirmed to be terrorists which had been involved in kidnapping Shia pilgrims.

* * *

During the early years of the conflict in Syria, when the US was supporting an anti-Assad insurgency in pursuit of regime change, Idris was the “US man in Syria” among other top FSA leaders.

This means America’s former top “rebel” leader is now leading an invasion force against America’s current Kurdish partners (the SDF) with NATO ally Turkey’s support.

As even The New York Times hasfor years admitted, the United States was paying the salaries of Idris and other “rebel” fighters in Syria seeking to topple Assad, along with supplying them with weapons and increasingly sophisticated military hardware and equipment. Idris was removed as Chief-of-Staff of the FSA’s Supreme Military Council in 2014, after which he became increasingly close to Ankara.

Former commander of the US-funded Free Syrian Army, General Salim Idris, via Getty

And now, Idris is Erdogan’s point man in attacking US-backed SDF forces, as US state-funded Voice of America (VOA) notes in asking ‘Which Syrian Groups Are Involved in Turkey’s Syria Offensive?’:

Salim Idris, an SNA commander, said Monday in a press conference in Turkey that his group “is standing in strength, resolve and support with our Turkish brethren in Turkey” in their military operation into Syria.

Last year the VOA quoted Idris as saying he and his forces were seeking “payback” against Syria Kurds.

“The problem is not only that the Kurdish fighters cooperated with the Syrian regime and the Russians during the battle for Aleppo, but that the YPG burned dozens of Arab villages and displaced their inhabitants,” Idris told VOA.

#Syria

Images showing Salim Idris, commander of Syrian National Army in presence of other forces of this group before start of Turkish operation in east of Euphrates. #SNA is part of Free Syrian Army and manipulated completely by #Turkey in Syria and their base is in Azaz. pic.twitter.com/LjHDGPXaJL

Given Erdogan and other top Turkish leaders’ vow of “demographic correction” in northern Syria through use of military force — which is clearly code for ethnic cleansing along Turkey’s border — it is all the more disturbing.

* * *

Considering the years-long absurd contradictions inherent in America’s actions in Syria, maybe this is why Trump wants to get the hell out?

“I am trying to end the ENDLESS WARS,” the president tweeted again on Thursday.

….the area and start a new war all over again. Turkey is a member of NATO. Others say STAY OUT, let the Kurds fight their own battles (even with our financial help). I say hit Turkey very hard financially & with sanctions if they don’t play by the rules! I am watching closely.

The polarization in American politics has become so extreme there seems no longer to be any center ground. The political establishment is consequently imploding into an abyss of its own making.

President Trump is being driven into an impeachment process by Democrats and their media supporters who accuse him of being “unpatriotic” and a danger to national security.

Trump and Republicans hit back at Democrats and the “deep state” whom they condemn for conspiring to overthrow the presidency in a coup dressed up as “impeachment”.

The White House is being subpoenaed, the Democrat-controlled House of Representatives wants to access transcripts to all of Trump’s phone calls to foreign leaders; Secretary of State Mike Pompeo has blasted congressmen for “harassing the State Department” in their search of evidence to indict Trump. Trump calls the impeachment bid a “witch-hunt”.

Republican Representatives protest that the US is facing a dark day of constitutional crisis, whereby opposing Democratic party leaders are abusing their office by accusing Trump of “high crimes” without ever presenting evidence.

It’s an Alice in Wonderland scenario writ large, where the gravest verdict is being cast before evidence is presented, never mind proven; the president is guilty until proven innocent.

Trump, in his turn, has berated senior Democrat Adam Schiff, the chair of the House Intelligence Committee, for “treason” – a capital offense. Are federal police obliged to arrest him? Schiff is accused of colluding with a supposed CIA whistleblower in concocting the complaint that Trump tried to extort Ukrainian President Volodymyr Zelensky to dig dirt on Democratic presidential candidate Joe Biden.

There seems no end to this political civil war in the US. The American political class is literally tearing itself apart, destroying its ability to govern with any normal function.

So-called liberal media outlets, in lockstep with the Democrats, inculpate Trump for wrongdoing, while they staunchly assert that credible reports of Joe Biden abusing his former vice presidential office to enrich his son over Ukraine gas business are false. Many Americans don’t see it that way. They see Biden as being up to his neck in past corruption; they also see a flagrant double-standard of the establishment protecting Biden from investigation while hounding Trump at every possible opportunity, even when evidence against Trump is scant.

What Trump is being subjected to is the same “highly probable” paranoia that Russia has been subjected to by Washington over recent years. Guilt is asserted without evidence. It becomes a “fact” by endless repetition of baseless claims, such as Russia allegedly interfering in US elections, or allegedly destabilizing Ukraine. Hundreds of economic sanctions have been imposed on Moscow as a result of this blame game, a game that, ironically, Trump has also indulged.

Ironically, Trump and the very highest political office of president is getting the same phobic treatment. No matter that the two-year Mueller Report into alleged Trump-Russia collusion collapsed in a pile of dust for lack of evidence, the Democrats and their media, as well as their deep state patrons, have persisted to accuse the president of enlisting a foreign power, Ukraine, to boost his electoral chances.

The transcript of Trump’s phone call with Ukraine’s Zelensky back in July shows he did not make a quid pro quo demand linking US military aid to a requested investigation into alleged corruption by former Vice President Joe Biden. Nevertheless, Democrats and their political establishment allies are relentless in pursuing the impeachment of Trump. Based on such flimsy reasoning, this impeachment process looks like a euphemism for “coup” – to overturn the result of the 2016 presidential election. The so-called “Russiagate” debacle failed for lack of evidence; now it is “Ukrainegate” that is the pretext for pushing the coup attempt.

Under freedom of information release, Judicial Watch in the past week has uncovered categorical proof that the Mueller probe was a coup attempt to oust Trump. Unsealed communications between the Department of Justice, FBI and liberal media outlets show a clear motive and deliberate orchestration to topple Trump based on no evidence of wrongdoing.

America’s democracy and constitution is being trashed by unelected shadowy forces, aided and abetted by prestigious media outlets like the New York Times. These forces presume to know better or have more privilege than their fellow Americans who “voted the wrong way”.

The inescapable conclusion is that powerful political forces within the US simply do not recognize the democratic rights of the electorate who voted Trump into office. Not only do these forces not respect democratic principle, they also, patently, do not respect due legal process or the high offices of their own government. This is a lurking ideology of dictatorship and fascism. Paradoxically, these labels are pinned on the maverick Trump. More accurately, they apply to the politicians and media who claim to be “liberal” and “democrats”.

The accelerating political implosion in the US nails the lie to oft-repeated American proclamations about their nation being the paragon of “sacred” democratic virtue and rule of law. And the people who are doing the damage to US politics and its constitution are “patriotic” Americans, not Russia or any other imagined foreign adversary.

Is that not poetic justice after all the decades of calumny, deception and self-declared “exceptional” American vanity.

America is at war with itself. It is Americans themselves who destroying their own political system, and perhaps even the very society, with their own hands and their addled, paranoid brains – without any assistance from a “foreign enemy”.

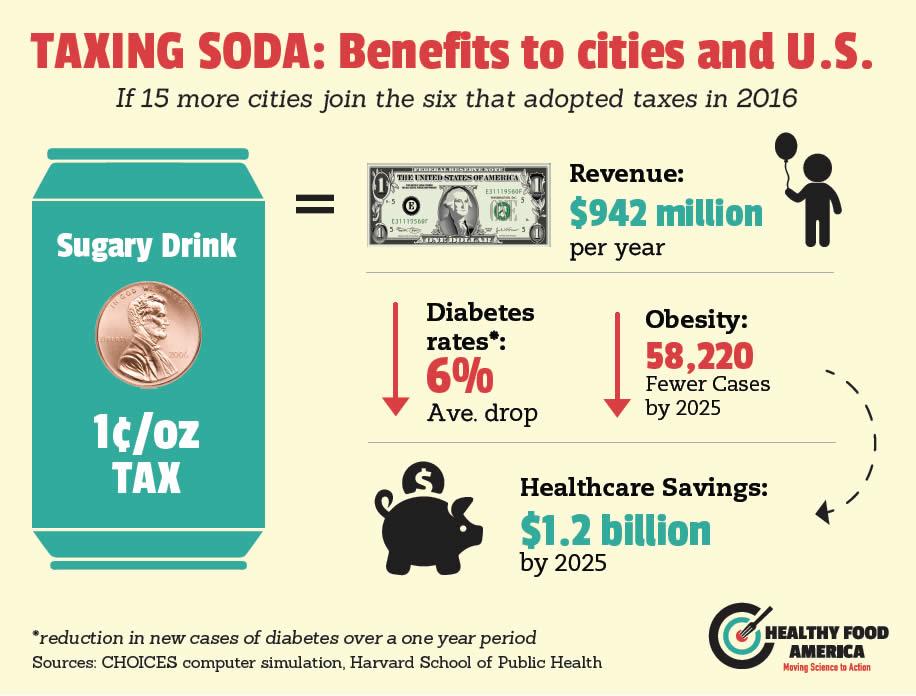

D.C. Considers 1.5C-Per-Ounce Soda Excise Tax One Week After Implementing 2% Soft Drink Sales Tax

Today in “we must find new things to tax, even if we’ve already taxed them” news, Washington DC’s City Council is considering a plan to place a 1.5 cent per ounce excise tax on soda and other sweetened beverages, according to Fooddive.

The proposal comes just a week after the DC Council put an additional 2% sales tax on soft drinks and it already has support from 8 of the 13 DC council members. It will affect soda and any other sugary drinks, such as Gatorade, iced coffee and orange juice.

Drinks like diet soda or other beverages containing artificial sweeteners would be exempt from the tax, as would alcohol and beverages with milk as the main ingredient. The estimated $21 million in annual revenues the tax would bring in will go to educational and food programs.

Naturally, the beverage industry stands in stark opposition to the tax. Ellen Valentino, a spokeswoman for the DC Beverage Association, called the tax a “big mistake” and said “people will flee in order to purchase beverages and other grocery items outside the city’s borders.”

And yet again, it’s the consumers that wind up getting screwed: the tax would add about a dollar to the price of a 2 liter bottle of soda. This will cause manufacturers and retailers to likely hike prices to consumers. Some have speculated that since Washington DC is close to the Maryland border, people could travel across state lines for their soft drink needs.

These types of taxes have also been enacted in several cities in California, Boulder, Philadelphia and in the state of West Virginia. Cook County Illinois implemented a similar tax in 2017 but repealed it just months later after pressure from the American Beverage Association. California’s proposed tax didn’t make it through the state assembly this year, although it may be brought up again soon.

States like Arizona and Michigan have already passed legislation prohibiting local governments from adopting food and beverage taxes.

The effect of the tax has been noticeable where it has been implemented.

A study published earlier this year took five years of data from Berkeley, California, and found a 52% decrease in soda consumption in the first three years after the tax was adopted. After two months of Philadelphia’s soda tax, which is the same rate as the proposed D.C. excised tax, a study found residents were about 40% less likely to drink sugary drinks daily than those in other cities. Philadelphia’s tax projections, however, were lowered 15% in March 2018 and didn’t make major changes in the population’s consumption of healthier fare, so its tax could face a repeal.

Beverage makers are likely to posture up for a significant fight of the DC excise tax. The beverage industry has already spent $48.9 million since 2009 to work to oppose these taxes.

But two other groups of concerned individuals, the American Academy of Pediatrics and the American Heart Association, are both urging legislation to reduce consumption of sugary beverages, not only through taxes, but also through marketing campaigns. They argue that milk and water should be the default drinks for children in vending machines and that soda should not be allowed to be purchased with government benefits.

Last week’s military parade previewed a series of game-changing weapons that could neutralize American seapower…

For decades, the United States has taken China’s ballistic missile capability for granted, assessing it as a low-capability force with limited regional impact and virtually no strategic value. But on October 1, during a massive military parade celebrating the 70th anniversary of the founding of the People’s Republic of China (PRC), Beijing put the U.S., and the world, on notice that this assessment was no longer valid.

In one fell swoop, China may have nullified America’s strategic nuclear deterrent, the U.S. Pacific Fleet, and U.S. missile defense capability. Through its impressive display of new weapons systems, China has underscored the reality that while the United States has spent the last two decades squandering trillions of dollars fighting insurgents in the Middle East, Beijing was singularly focused on overcoming American military superiority in the Pacific. If the capabilities of these new weapons are taken at face value, China will have succeeded on this front.

In the West, it is called RMA, short for “Revolution in Military Affairs.” The term was first coined by Marshal Nikolai Ogarkov in the early 1980s. Ogarkov, who was at the time serving as the chief of the Soviet general staff, spoke of “developments in nonnuclear means of destruction [which] promise to make it possible to sharply increase (by at least an order of magnitude) the destructive potential of conventional weapons, bringing them closer, so to speak, to weapons of mass destruction in terms of effectiveness.”

Ogarkov’s work caught the attention of Andrew Marshall, who headed the Pentagon’s Office of Net Assessment. Marshall took Ogarkov’s premise and put it into action, integrating new technology with innovative operational concepts that positioned the U.S. military to be able to prevail over a numerically superior Soviet army in a ground war in Europe. The capabilities of Marshall’s RMA were potently displayed during the Gulf War in 1991, when the U.S. led a coalition that handily defeated Saddam Hussein.

One of the nations keenly observing the impact of the American RMA in the Persian Gulf was China. Chinese military theorists studied how Marshall adapted Ogarkov’s theories into an American version of RMA, and responded with a Chinese adaptation, developing weapons specifically intended to overcome American superiority in critical areas.

These weapons became known as “shashoujian,” or “the Assassin’s Mace,” derived from the traditional Chinese way of describing a weapon of surprising power. “A shashoujian,” a contemporary Chinese military journal notes, “is a weapon that has an enormous terrifying effect on the enemy and that can produce an enormous destructive assault.” More importantly, the modern Chinese concept of shashoujian envisions not a single weapon, but rather a system of weapons that combine to produce the desired effect.

Defeating the United States in a ground war has never been an objective of the Chinese military—the Korean War was an historical anomaly. China’s focus instead has been to develop shashoujian weapons to safeguard its national security and territorial integrity. This couldn’t be accomplished simply by mimicking the American RMA example; they needed to create a uniquely Chinese military superiority that combined Western technology with Eastern wisdom. “This,” the Chinese believe, “is our trump card for winning a 21st century war.”

For China, the three principle points of potential military friction with the U.S. are Taiwan, South Korea-Japan, and the South China Sea. Apart from South Korea and Japan, where the U.S. has significant ground and air forces already forward deployed, the main threat to China is maritime power projected by American aircraft carrier battlegroups and amphibious assault ships. The Chinese response was to develop a range of anti-access/area-denial (A2/AD) capabilities designed to target American naval forces before they arrived in any potential contested waters.

Traditionally, the U.S. Navy has relied on a combination of surface warships armed with sophisticated air defense systems, submarines, and the aircraft carrier’s considerable contingent of combat aircraft to defend against hostile threats in time of war. China’s response came in the form of the DF-21D medium-range missile, dubbed the “carrier killer.” With a range of between 1,450 and 1,550 kilometers, the DF-21D employs a maneuverable warhead that can deliver a conventional high-explosive warhead with a circular error of probability (CEP) of 10 meters—more than enough to strike a carrier-sized target.

To compliment the DF-21D, China has also deployed the DF-26 intermediate-range missile, which it has dubbed the “Guam killer,” named after the American territory home to major U.S. military installations. Like the DF-21, the DF-26 has a conventionally armed variant, which is intended to be used against ships. Both missiles were featured in the 2015 military parade commemorating the founding of the PRC.

As capable as they were, however, the DF-21D and DF-26 were not the shashoujian weapons envisioned by Chinese military planners, representing as they did reciprocal capability, as opposed to a game-changing technology. The unveiling of the true shashoujian was reserved for last week’s parade, and it came in the form of the DF-100 and DF-17 missiles.

The DF-100 is a vehicle-mounted supersonic cruise missile “characterized by a long range, high precision and quick responsiveness,” according to the Chinese press. When combined with the DF-21/DF-26 threat, the DF-100 is intended to overwhelm any existing U.S. missile defense capability, turning the Navy into a virtual sitting duck. As impressive as the DF-100 is, however, it was overshadowed by the DF-17, a long-range cruise missile equipped with a hypersonic glide warhead, which maneuvers at over seven times the speed of sound—faster than any of the missiles the U.S. possesses to intercept it. Nothing in the current U.S. arsenal can defeat the DF-17—not the upgraded anti-missile ships, THAAD, or even the Ground Based Interceptors (GBI) currently based in Alaska.

In short, in the event of a naval clash between China and the U.S., the likelihood of America’s fleet being sent to the bottom of the Pacific Ocean is very high.

The potential loss of the Pacific Fleet cannot be taken lightly: it could serve as a trigger for the release of nuclear weapons in response. The threat of an American nuclear attack has always been the ace in the hole for the U.S. regarding China, given that nation’s weak strategic nuclear capability.

Since the 1980s, China has possessed a small number of obsolete liquid-fuel intercontinental ballistic missiles as their strategic deterrent. These missiles have a slow response time and could easily be destroyed by any concerted pre-emptive attack. China sought to upgrade its ICBM force in the late 1990s with a new road-mobile solid fuel missile, the DF-31. Over the course of the next two decades, China has upgraded the DF-31, improving its accuracy and mobility while increasing the number of warheads it carries from one to three. But even with the improved DF-31, China remained at a distinct disadvantage with the U.S. when it came to overall strategic nuclear capability.

While the likelihood that a few DF-31 missiles could be launched and their warheads reach their targets in the U.S., the DF-31 was not a “nation killing” system. In short, any strategic nuclear exchange between China and the U.S. would end with America intact and China annihilated. As such, any escalation of military force by China that could have potentially ended in an all-out nuclear war was suicidal, in effect nullifying any advantage China had gained by deploying the DF-100 and DF-17 missiles.

Enter the DF-41, China’s ultimate shashoujian weapon. A three-stage, road-mobile ICBM equipped with between six and 10 multiple independently targetable reentry vehicle (MIRV) warheads, the DF-41 provides China with a nuclear deterrent capable of surviving an American nuclear first strike and delivering a nation-killing blow to the United States in retaliation. The DF-41 is a strategic game changer, allowing China to embrace the mutual assured destruction (MAD) nuclear deterrence posture previously the sole purview of the United States and Russia.

In doing so, China has gained the strategic advantage over the U.S. when it comes to competing power projection in the Pacific. Possessing a virtually unstoppable A2/AD capability, Beijing is well positioned to push back aggressively against U.S. maritime power projection in the South China Sea and the Taiwan Straits.

Most who watched the Chinese military parade on October 1 saw what looked to be some interesting missiles. For the informed observer, however, they were witnessing the end of an era. Previously, the United States could count on its strategic nuclear deterrence to serve as a restraint against any decisive Chinese reaction to aggressive American military maneuvers in the Pacific. Thanks to the DF-41, this capability no longer exists. Now the U.S. will be compelled to calculate how much risk it is willing to take when it comes to enforcing its sacrosanct “freedom of navigation.”

While the U.S. commitment to Taiwan’s independence remains steadfast, its willingness to go to war with China over the South China Sea may not be as firm. The bottom line is that China, with a defense budget of some $250 billion, has successfully combined “Western technology with Eastern wisdom,” for which the U.S. has no response.

Border Patrol Installing Invisible Shields At Wall To Stop Drug Smuggling Drones

A new report from Defense One shows the U.S. Customs and Border Protection (CBP) is installing an invisible shield along President Trump’s Mexico-US border wall that will deny access to drug smuggling drones.

CBP recently signed a $1.2 million deal with Citadel Defense Company to install an automated, invisible defense shield at the border to detect and engage unwanted drones using proprietary machine learning algorithms.

The contract is for six systems, and each will provide a 1.8-mile hemisphere of protection horizontally and 1,000 feet vertically on an unknown part of the wall. This contract is likely a pilot run, and if the results exceed expectations, more systems could be deployed across the border.

According to Citadel, the “autonomous, artificial intelligence-enabled counter-drone solution” is essentially a drone jamming tool that can easily be deployed within minutes. The system monitors the airspace above, can commandeer a drone’s navigation system and reroute its path back to its home base or safely land it on the ground.

The contract includes 12 months of software upgrades, support, and training, said Defense One.

“Drones have become a greater challenge along the border. Our nation’s border agents deserve the safest and most advanced technology available,” Citadel CEO Christopher Williams. “Citadel’s automated solution provides front-line operators with an awareness of drone threats and decision-making to respond faster than the adversary.”

Williams said the initial rollout is for six systems, collectively can provide a hemisphere of protection of about 11 miles.

“Technology is being deployed in limited quantities in 2019 after months of testing and validation,” he said. “Following 2020 presidential budget decisions, the potential for additional systems at larger quantities will be explored.”

Shown below are several examples of drug smuggling drones found on the Mexico-US border.

Drones that carry drugs on the US-Mexico border, narco-buses traveling between Colombia and Ecuador, and even narco-ambulances in Argentina. These are some of the creative strategies criminals are adopting to traffic drugs.https://t.co/dUGcoD6xiupic.twitter.com/3RK3JxGEb9

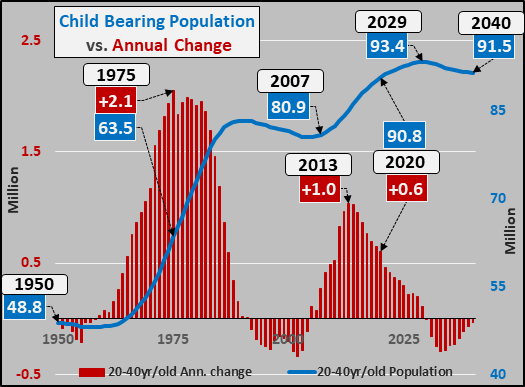

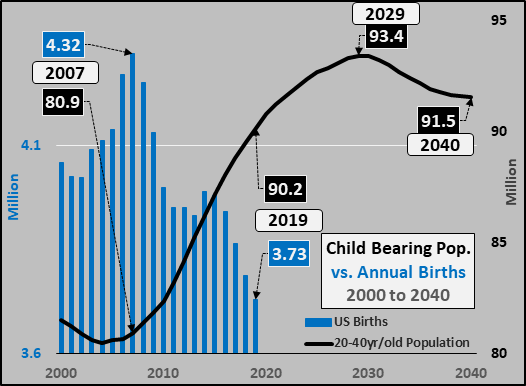

Births in America continue to tumble despite a growing child bearing population.

The growth among the child bearing population is decelerating and this population will begin outright declines around 2029.

US births are likely to continue falling, faster and far deeper, while current Census estimates continue to anticipate growth (continually just around the corner).

The chart below is the 20 to 40 year old US population (blue line) and the columns are the annual change in that population (maroon columns). The 1960 to 1990 population surge in the wake of the baby boom is easy to see as is the echo-boom from early 2005 through the 2020’s.

From a births perspective, it doesn’t matter what the total US population is…the only population that matters are those capable of child birth. I show the 20 to 40 year US population as they are responsible for over 90% of the births while those under 20 and those over 40 are producing so few children relative to 20 to 40 year olds as to be statistical noise (births per thousand by age group is detailed by the CDCHERE).

From 1957 through 2007, the child bearing population increased by 72% while births increased only 0.2% (just two tenths of 1%). Obviously, it was the rise in the child bearing population offsetting the collapse in the fertility rate that maintained the flat birth rate.

1957 through 2007

Child bearing population rose by 34.8 million (72% increase)

Annual births rose by 10 thousand (0.2% increase)

2007 through 2019 was the period that births were anticipated to spike with the rising echo-boom child bear population busily reproducing. An echo baby-boom was anticipated. Instead, a prolonged and deepening baby-bust has taken place. According to the CDC, in the 1st quarter of 2019 births continued to plummet across the board, but I’m assuming 2019 births will come in slightly less negative through the remainder of 2019 (I’m likely overestimating 2019 actual births at 3.73 million).

2007 through 2019

Child bearing population rose by +9.3 million (11.5% increase)

Annual births fell by <590> thousand (13.7% decrease)

The implications for what comes next should be obvious.

2019 through 2029

Child bearing population estimated to rise “just” 3.2 million or a little over 3%

Births are likely to continue falling as deeply negative fertility rates overcome what little child bearing population growth remains

2029 through 2040

Child bearing population estimated to fall 1.9 million

Births likely to fall even faster with a combined declining child bearing population and continued deeply negative fertility rates

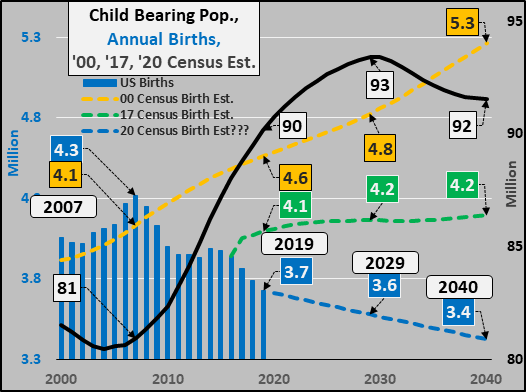

Census birth estimates from 2000 (plus the nearly identical ’08 estimate) and 2017 are displayed below. Clearly, since 2008, the Census is having a hard time adequately curbing their enthusiastic projections. Although each projection is lower than the last, each projection continues significantly overestimating births. With decelerating growth among the child bearing population through the 2020’s and outright child bearing population declines in the 2030’s…there is no reason for birth projections to be rising but the Census is having a very hard time catching down to reality. In truth, there is good reason to begin projecting ongoing and deepening birth declines in the 2020 Census estimate (my estimate at a realistic 2020 Census estimate is included below, blue dashed line).

From 2009 through 2019, actual births versus estimated births were 5.3 million fewer than anticipated (and this includes all births, whether the mother was here legally or otherwise). This is a crack in present and future growth nearly five times larger than all Americans lost in all wars the US has ever fought! That’s 5.3 million Americans not in existence and not consuming the average $25,000 per/capita annually throughout their lifetimes. But what is now a crack turns into a chasm, taking the same ’08 birth estimate versus a more realistic birth estimate through 2040, this represents almost 34 million fewer births (-22%) than was estimated in 2000 and 2008. The Census will be forced to continue collapsing their total US population projections, as they have been doing since 2008 (detailed HERE). The implications for declining potential economic growth based on collapsing quantity of potential consumers (while productivity, innovation, and advancements continue increasing capacity…for a declining basis of consumption) should have the CBO and the like heads spinning.

A continuation of the current falling fertility and birth rates is a really, really good bet (chart below).

The age segment that will continue to grow rapidly, the post childbearing 45+ year old population (red line, below). Notice even showing the broadest child bearing population (15 to 45 year-olds, yellow line), the stall in growth since 1990 relative to the growth of elderly. Among the 45+ year-olds, the majority of population growth over the coming decade will be among 75+ year-olds, a segment with less than 10% labor force participation, consumes at very low relative levels, and utilizes little to no credit (nor should they, primarily living on fixed incomes).

The debt based US economic system premised on perpetual consumptive growth (as a dual net importer and net debtor) is now facing long term depopulation from the bottom-up while the numbers of elderly surge. But only those who suggest this is likely to lead to some sort of “hiccup” are the crazy ones?!?

Population data via US Census Population Projections and UN World Population Prospects 2019

{kind=link}