One-term Tea Party congressman and current political talk show host Joe Walsh announced Monday that he will challenge President Donald Trump in the Republican primaries. The policy component of Walsh’s pitch is about debt, deficits, and tariffs, though the main thrust is about Trump’s deficient character and fitness. So, uh, about that.

Let's hope that when the Islamists next strike they first behead the appeasing cowards at CNN, MSNBC, etal who refused to show the cartoons.

Well, now Walsh confesses that “I said some ugly things about President Obama that I regret,” and that “I think that helped create Trump.” Can a reformed blowhard make a dent in the unreformed fella sitting in the Oval Office? So begins today’s Editors Roundtable edition of the Reason Podcast, feauring Nick Gillespie, Katherine Mangu-Ward, Peter Suderman and Matt Welch.

One-term Tea Party congressman and current political talk show host Joe Walsh announced Monday that he will challenge President Donald Trump in the Republican primaries. The policy component of Walsh’s pitch is about debt, deficits, and tariffs, though the main thrust is about Trump’s deficient character and fitness. So, uh, about that.

Let's hope that when the Islamists next strike they first behead the appeasing cowards at CNN, MSNBC, etal who refused to show the cartoons.

Well, now Walsh confesses that “I said some ugly things about President Obama that I regret,” and that “I think that helped create Trump.” Can a reformed blowhard make a dent in the unreformed fella sitting in the Oval Office? So begins today’s Editors Roundtable edition of the Reason Podcast, feauring Nick Gillespie, Katherine Mangu-Ward, Peter Suderman and Matt Welch.

Since leaving office President Obama has drawn widespread criticism for accepting a $400,000 speaking fee from the Wall Street investment firm Cantor Fitzgerald, including from Senators Bernie Sanders and Elizabeth Warren. Only a few months out of office, the move has been viewed as emblematic of the cozy relationship between the financial sector and political elites.

But as the President’s critics have voiced outrage over the decision many have been reluctant to criticize the record-setting $65 million book deal that Barack and Michelle Obama landed jointly this February with Penguin Random House (PRH)…

While the Obamas’ deal is unique for the amount of money involved, outsized book contracts between politicians and industries they’ve benefitted has precedent. In a recent report issued by the Roosevelt Institute, the study’s authors, Thomas Ferguson, Paul Jorgensen, and Jie Chen, argue that the mainstream approach to money in politics fails to recognize major sources of political spending. Among the least appreciated avenues for political money, they argue, are payments to political figures in the form of director’s fees, speaking fees, and book contracts.

Back in 2009, when the Obama administration was busy ensuring the nation’s financiers would become larger, more powerful and never serve a day in jail despite their historic crime spree, Larry Summers had dinner with Elizabeth Warren. During the course of that meal, he instructed her about how power really functions in the U.S.:

Unlike prior years, there was a distinct sense of dread and powerless foreboding in this year’s Jackson Hole meeting, starting with Jerome Powell’s “boring” speech in which he blamed Trump’s trade war for the Fed’s and culminating with Mark Carney unprecedented capitulation, effectively admitting that the fiat system has failed and the dollar can no longer be the world’s reserve currency (instead punting that obligation to “global central bankers” Mark Zuckerberg and his Libracoin).

Indeed, as even the FT concludes, “there was a sense that things will never be the same again.”

In its summary of this week’s Wyoming outing, the FT also wrote that “the developed world had experienced a “regime shift” in economic conditions, James Bullard, president of the St Louis Federal Reserve, told the Financial Times. “Something is going on, and that’s causing I think a total rethink of central banking and all our cherished notions about what we think we’re doing,” he said. “We just have to stop thinking that next year things are going to be normal.”

“They’ve priced in that there’s going to be uncertainty, there are going to be tweets, there are going to be threats and counter-threats,” said Mr Bullard. “And that’s the way it’s going to be.”

Interest rates are not going back up anytime soon, the role of the dollar is under scrutiny both as a haven asset and as a medium of exchange, and trade uncertainty has become a permanent feature of policymaking.

In short, central bankers “acknowledged they had reached a turning point in the way they viewed the global system. They cannot rely on the tools they used before the financial crisis to shape the economic environment, and the US can no longer be considered a predictable actor in economic or trade policy — even though there is no imminent replacement for the US dollar in sight.”

While long overdue, the blunt introspection by central bankers was unexpected: a paradigm shift in perception and self-appraisal usually takes place after years of failure – such as that observed ever since the financial crisis, where instead of sparking an economic rebound, central bankers only made the rich richer by creating hyperinflation in fiancial assets while keeping wages and incomes for the vast majority subdued, and inspired the greatest wealth and income divide in history, culminating in such 6-sigma events as Brexit, Trump, and the populist revolution observed across most of Europe.

Although in retrospect, perhaps it should not have been a surprise. After all, this year the symposium has an appropriate catch-all topic: “Challenges for Monetary Policy”, and as Deutsche Bank’s Alan Ruskin said “rest assured there are challenges aplenty” adding that “arguably the basic framework for monetary policy is facing its greatest challenges since the 1970s, when the Keynesian Philips curve framework was succumbing to the Monetarist and rational expectations critique.“

Ironically, and in polar opposition to today, the debate in the second half of the 1970s was how to conquer inflation, when the short-run trade-off between unemployment and inflation was giving way to a vertical long-run Philips curve, where there was no trade-off in growth and inflation. Now the debate is exactly the reverse: how to create inflation when the Phillips curve appears to be flat! Indeed, the basic inflation framework may have lost much of its appeal, which means that the entire “conventional wisdom” upon which bankers have relied for decades has been turned on its head.

So having effectively admitted that they can no longer be replied upon to pull the world out of the next recession, with the BOE’s Mark Carney going so far as to admit that central bankers will be responsible for not only the next crisis, but the next war, something we have argued for the past decade, when he said that “past instances of very low rates have tended to coincide with high risk events such as wars, financial crises, and breaks in the monetary regime” – incidentally, the same low rates that for years central bankers said would save the world and now we learn have doomed it instead, below are 20 blunt questions (with a few implied answers in the questions themselves) for Central Bankers, courtesy of DB’s Alan Ruskin, as they prepare to be swept away by the tsunami of history:

If the Philips curve is so flat, and there is no serious alternative model to explain/forecast inflation, is inflation targeting even feasible? What are the intermediate targets to hit the end inflation target?

If goods Inflation drivers are dominated by global variables like international growth/capacity, how can a Central Bank that influences country specific variables pretend to target inflation?

If Central Banks hit the inflation target is that ‘the be all and end all’? The Fed did a particularly good job hitting its inflation target in the years before the Great Financial collapse in 2008 – what does that say about inflation targeting creating stability?

Central banks are great at creating asset inflation to which they pay lip-service, but they target goods and services inflation they struggle to create. Asset inflation that supports growth is welcomed. What are the long-term repercussions of an asymmetric bias in favor of asset inflation? As this asymmetry fans wealth/income disparity, does it matter, or, is this the least worst only solution? Who will be left exposed when the asset tide goes out again?

Is it the Central Banks job to do away with business cycle? And at what price? Are we witnessing the great moderation interspersed with a great collapse in confidence and wilder big credit cycle, and greater long-term misallocation of resources?

Can inflation be measured accurately enough to warrant distinguishing between core inflation +/-0.25% either side of target? Similarly, on hedonic pricing, how relevant to a consumer is it, that a tech device is worth a fraction of its price a decade ago when adjusted for functionality, but in practice may cost more than the old device when not quality adjusted? Is hedonic adjusted inflation indices the relevant denominator for assessing real interest rates and real money supply?

How is it best to measure the real cost of money? The real cost of buying a house should be based on expected house price (asset) inflation. Higher asset inflation reduces the real cost of money creating pro-cyclicality.

Are we reaching a natural end to the secular decline in inflation and rates that has propelled the asset cycle in the last 40 years. Has asset inflation hidden an even more meaningful deceleration in the natural rate of growth that will evident in the next decade?

How much are Central Banks going to be complicit in a collapse in fiscal standards, by buying public sector assets? Will a passive Central bank simply accommodate and facilitate fiscal actions related to MMT? What is the Central banks future role in pushing back against modern monetary theory.

How much has the unprecedented collapse in the term premia in bond market brought forward the impact of monetary policy that will support US growth in the next 6 – 12 months, but leave much less Fed capacity to ease financial conditions in H2 2020 and 2021?

Is ‘Japanization’ the fate of most advanced economies? How different to Japan is the rest of the developed world when their demographics turn? Do these demographics lower both the natural rate of growth and equilibrium interest rate over the cycle as seems likely?

Japan’s yield curve targeting has seemed to be a relative success, how would this fit in the US context. What will get the US/world out of a zero/negative rate funk? Or is that simply the future?

Is modest goods deflation (say -1% y/y) bad, especially when in any year a certain amount of deflation reflects technical progress? Japan per capita income strength suggests relative stable modest deflation may not be as negative for growth as assumed?

At what negative rate does aggregate demands interest rate elasticity turn positive? As developed countries age, are low interest rates an even less effective policy mechanism for a growing population searching for stable sources of income?

Will the Fed/ECB buy equities/ETFs? How far are central banks willing to distort underlying value, or is distorting value intrinsic to Central Banking as per the Austrian critique? Do the distortion to the price/quantity of credit matter in the longer-term, or, will they contribute to lower trend growth? What misallocation or reallocation of resource have unorthodox policies already caused?

Is r* a broken clock that is right every 24 hours, or a more useful concept? Is r* as described by the FOMC dots, really better described as ‘peak r’, and why does the Fed not acknowledge there is no stable l/t interest rates, and rates have their own cycle?

What is the message that we can take from record low term peremia, but a 10y risk neutral rate that is estimated to be surprisingly high near 2.8%?

Central Bank in a world of deglobalization, or at least a cold war in the tech sector. Will the natural rate of growth (y*) get more depressed? Has the global economy moved beyond the easiest phase of EM growth catch-up and increased financial intermediation? Are deglobalisation/enviromental degradation factors to consider?

Money supply: why is this getting close to no attention? M1 has been sending important leading indicator signals for all of the US, the EUR area and China. M1 has been sending the same corroborating leading indicator signals as the yield curve, yet nobody talks about money supply. Again this is another complete reversal from the late 1970s.

Currency Wars? What are the circumstances when the Fed should not join White House inspired intervention? What are the Fed (and Treasury’s) views on accumulating CNY assets? Do other major Central banks have any aversion to holding CNY currently?

via ZeroHedge News https://ift.tt/2Zlk6fK Tyler Durden

Perhaps the strangest thing about the story that President Donald Trump has expressed interest in using nuclear bombs to stop hurricanes was that it didn’t seem all that strange. Almost no one thought to ask “Can you believe it?” because almost everyone automatically did, while simultaneously acknowledging that in reality, no such intervention would be tried.

So instead of sustained incredulity, there were jokes, and a few #WellActuallys, and eventually Trump himself declared that the story was fake news. But for the most part, the story, first reported by Axios, came and went with the daily tides of Twitter conversation. Trump wants to deploy nuclear weapons to stop summer storms? Wild stuff! 2019, right? Moving on.

One way to understand this is as a basically healthy reaction to the brainfarts of a particularly brainfart-prone president, one who thinks out loud—or online—and who indulges a variety of odd obsessions that rarely become actual policy. Both in public and in private, Trump has a habit of floating half-baked bad ideas that are unlikely to ever be implemented. For many people, constantly worrying about the small chance that they one day might happen is simply too exhausting to keep up.

Yet in another way, the nuke-the-hurricanes episode was a reminder of the ways Trump’s erratic personal behavior has led to a widespread acceptance of presidential ideas that are not only kooky but dangerous, or at least rather risky, even if those ideas are nearly certain to remain unimplemented.

Take, for example, Trump’s declaration last week that American companies “are hereby ordered to immediately start looking for an alternative to China.” This was a presidential “order” that also wasn’t obviously an order in any official sense; it came with no proposed timeline, no potential penalties, and no legally enforceable procedure to back it up. And yet both White House aides and Trump himself nonetheless argued that it could become one if the president were so inclined.

In theory, the argument went, Trump could use the International Emergency Economic Powers Act (IEEPA) of 1977 to declare a state of emergency, expanding the powers granted to the executive, potentially giving him the authority to order U.S. businesses to cease operations in China. Experts disagree about whether the IEEPA could plausibly justify such an order. But it’s fair to say that using it in the way Trump has suggested would be clearly unprecedented and arguably abusive, and that it would almost certainly end up in court.

Still, it is at least possible to imagine a scenario in which Trump finds legal cover for such an order. The result, in turn, would be vast and unpredictable economic consequences for both the American economy and the international order, as two economic superpowers turned a series of economic skirmishes into an all-out economic war. It’s hard to say exactly how it would play out, but as one manufacturer told The New York Times last week, a mandatory exit of U.S. businesses from China “could cause a global depression, not recession.”

Yet just as most people reasonably assume that Trump probably won’t try using nuclear weapons to manage bad weather, few, I suspect, worry that he would ever really try to compel American businesses to fully cut economic ties with another country. It’s an idle threat made by a president with a penchant for bluster, and no more—and thus about as easy to ignore as the idea of deploying a nuclear deterrent against a hurricane.

Or at least that’s what we hope, because the problem with Trump is that it’s almost impossible to ever be fully certain that he won’t eventually pursue his wilder ideas, to be confident that he won’t one day pick up his phone and tweet out an order to pull out of China’s economy that is an actual order, backed up by the force and power of the federal government. This is especially true when it comes to trade and immigration, where Trump has proven willing to act in ways that predecessors of both parties probably would have avoided.

The result is generalized political and economic instability, and a pervasive precariousness to American life. This helps feed more exotic, conspiracy-adjacent theories about Trump himself. And over time, it may well take a serious toll on the American economy. Indeed, some economic consequences are already being felt. Trump’s announcement of tariff hikes last week, combined with his threats against both China and the U.S. Federal Reserve, rattled already jittery markets, sending stocks to their fourth weekly loss in a row.

The point isn’t merely that Trump shouldn’t be playing weatherman with the world’s biggest nuclear arsenal (although he shouldn’t), or that tariffs and trade wars are bad news for the economy (although they are). It’s that Trump’s mercurial behavior, and the lingering possibility that he might try to follow through on one of his more eccentric ideas, exacts a regular low-level toll on our fortunes. He is a constant source of economic and political uncertainty. And that uncertainty, even in the absence of actual action, is bad enough. It makes it harder for businesses to plan future operations, harder for ordinary Americans to plan their retirements, and harder for America’s allies on the international stage to work together.

So no, Trump probably won’t nuke a hurricane, and no, he probably won’t force American companies to stop operating in China, just as he didn’t ever completely close the border with Mexico, despite his threat to do so. Which means that no, you probably shouldn’t spend too much time worrying about the possibility that he might do any of these things, or whatever harebrained idea he tweets out tomorrow. But there’s a lot riding on all those “probably”s, and on the slim-but-real chance that one day a he-probably-won’t will somehow become an actually-he-did. And that alone is cause enough for concern.

from Latest – Reason.com https://ift.tt/2ZhCO87

via IFTTT

Markets blow up on Friday on a series of tweets, markets jam higher on the pronouncement of dubious phone calls on Monday. The rapid back and forth has many heads spinning and makes for dramatic headlines as people are searching for explanations. To which I say: Keep it simple, especially in the age of the great confusion.

Background: In 2019 market gains have been driven by pure multiple expansion resting on 2 pillars of support in the face of deteriorating fundamentals: 1. Hope for rate cuts and Fed efficacy 2. Trade optimism. But in process little to no gains are notable since the January 2018 highs, in fact most indexes are down sizably since then.

And when markets are purely reliant on multiple expansion the risk for accidents increases when confidence gets shaken. Friday’s escalation on the trade war front again highlights this point.

And in context of global growth slowing an escalation in the trade war is akin to playing with fire as it risks being a trigger to nudge the world economy into a global recession. After all 9 economies are either in recession or on the verge of going into recession.

This morning I was speaking with Brian Sullivan and he asked me what matters most here, the China trade war, the Fed, or technicals. The short answer is they all matter as it is a battle for control, but how to delineate a complex interplay of conflicting forces into some clarity?

Let me give you my take on all 3 fronts. Before I do, for background here’s the clip from this morning:

China:

Occam’s Razor: The simplest explanation is often the best one and that’s really what’s happening on the China trade war front as far as I’m concerned. The Chinese sensed weakness when Trump delayed the very tariffs he announced in early August and the ‘tariffs delayed’ newsflash came on the heels of markets selling off and it produced a relief rally of size. The Chinese realized Trump’s vulnerability (the US consumer) and wanted to test him. And they did on Friday by retaliating with tariffs on their own. And if you believe the Chinese propaganda their counter punch announcement was specifically aimed at hurting the US stock market. And Trump predictably reacted with rage and emotion and ended up doing more damage than the Chinese by counter punching immediately on twitter. The impression: A decision made out of anger not prudent strategy.

So what happened? Markets tanked hard again and when the damage became apparent in Sunday overnight futures trading a narrative, true or not, was created to bring markets back up. The signal was clear and hence the rally today:

Markets don’t care whether Trump tells the truth or not.

They care that he freaks out when markets drop and immediately backpedals.

Once a poker player reveals his tell he’ll get called again and again and again.

If the world was wondering how far Trump is willing to go on the trade war front the Chinese got their answer twice in August: $SPX 2800.

After all it’s his stock market alone:

My Stock Market gains must be judged from the day after the Election, November 9, 2016, where the Market went up big after the win, and because of the win. Had my opponent won, CRASH!

Stock market levels are the key measuring stick of the administration’s economic success according the Treasury Secretary Mnuchin. No wonder liquidity calls were needed in December as markets dropped 20%.

The bottomline on China: It’s a double edged sword that breeds both risk and opportunity:

Risk: Failure to curb the rhetoric and show lack of real progress risks triggering a global recession that is already a clear and present danger. Risk that markets are becoming a weaponized tool as part of the trade war. The Chinese already know it, and I suspect so does Trump and his team. They are playing with fire, the appear fine to let the fire smolder, but not let it burn out of control beyond, say 5% of market downside. Then they get itchy. But fires can spread so careful there, especially as there remains zero resolution or specifics other than vague hints at phone calls that neither side can agree to on whether they even took place.

Opportunity: Sentiment is getting so bad on this front that any sign of relief on tariffs and/or progress (i.e. what we saw again today in form of “phone calls” can trigger a massive relief rally. And frankly it only takes a tweet. We saw some of this in the middle of August when some tariffs were delayed. And Trump pretty much hinted at that being a replay possibility today, another rabbit to pull out of his hat again.

So none of this is a mystery, it’s a giant face saving dance with no specifics or path to resolution. Fact is prices can easily be subject to sell-offs and/or rallies based on vague information on tweets. This broad range risk profile remains on the plate into September.

The Fed:

The Fed’s in a very tough position. For one they, like anybody else, are trying to quantify the real risk to the economy coming from trade wars and the slowdown in data. But realistically they are also playing with fire. Reality is they have limited ammunition and need to be judicious how they proceed, for if a global recession is to ensue they only have 8 rate cuts to work with. In 2001 and 2007 it took 500bp in rate cuts to stop the bleeding, they don’t have that now.Hence they are desperately trying to cling to the “mid cycle adjustment” narrative.

Problem is markets are pricing in 100bp in rate cuts over the next year. Coming from 225bp that’s not a mid cycle adjustment. So markets and the Fed are at odds with each other and it comes down to confidence, efficacy and credibility.

To boot: Central banks are signaling that they alone can’t deal with a coming recession, they are asking for a coordinated global policy response. But as we just saw this weekend, the G7 couldn’t even agree on a joint memo for the first time in 44 years, so dysfunctional is the global political stage at the moment. Hence the issue of efficacy is paramount and markets may be placing too much trust in central banks.

Technicals:

Three important technical developments to keep an eye on:

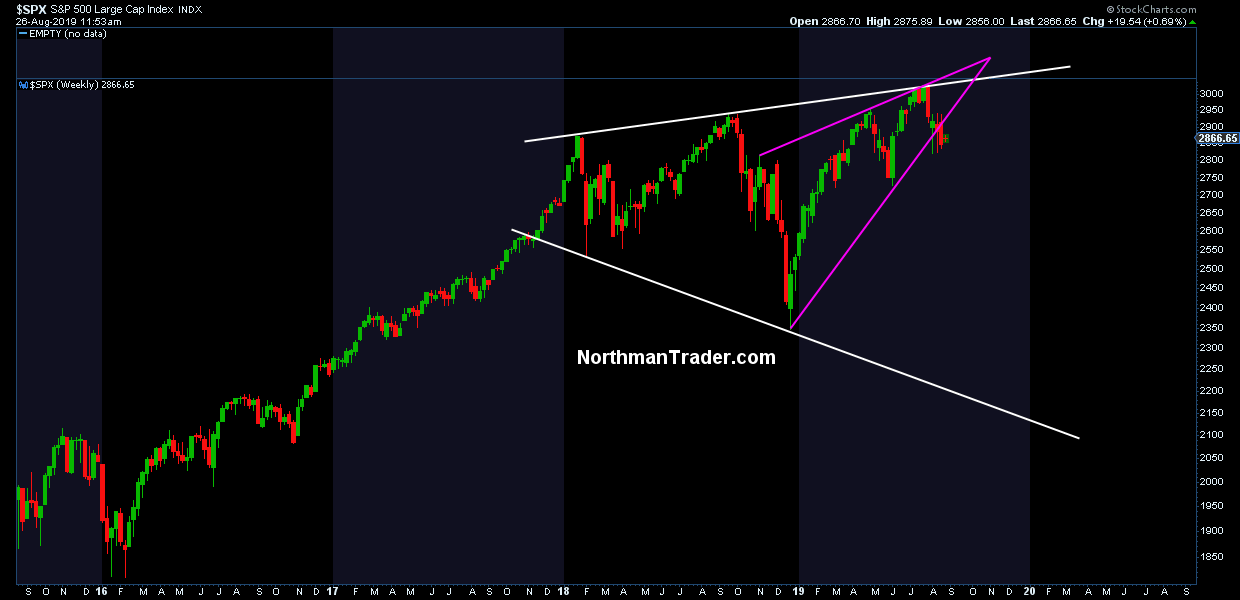

The megaphone structure remains intact and leaves room for lots of downside risk if a global recession is to unfold. The sell zone from 3000-3050 has confirmed and the larger pattern has risk into 2100-2200 $SPX.

A rising wedge has formed in 2019, and that wedge has broken to the downside, another bearish development:

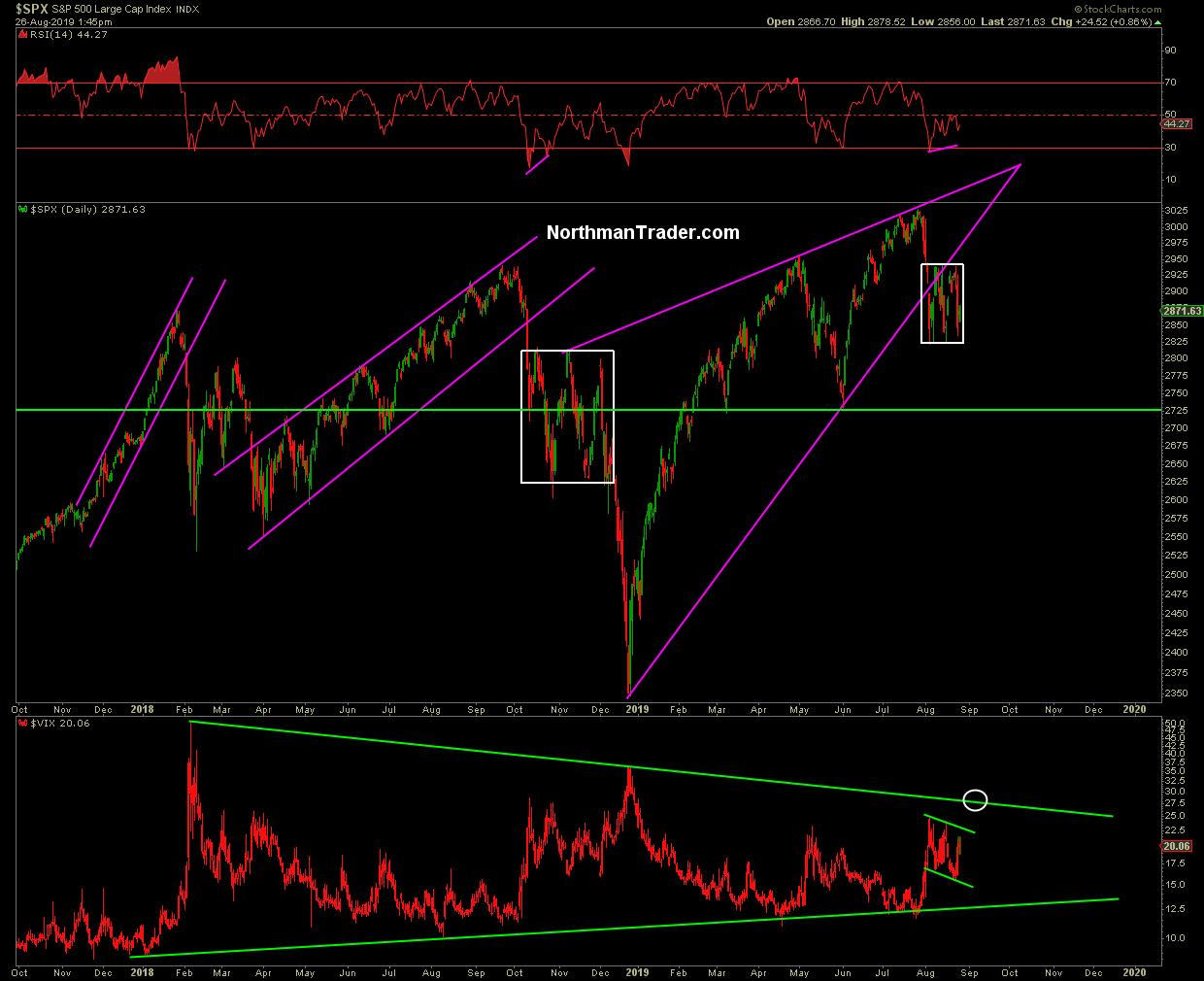

Indeed the last several weeks have shown a consolidation phase similar to the one from last fall, albeit it smaller:

Last year’s consolidation also came on the heels of a pattern break which then resolved lower. A confirmed break of that price consolidation zone to the downside risks lower prices still to come, i.e. a retest of the June lows or lower, and volatility $VIX could break higher into the 28/30 range as it appears to be forming a bull flag.

That said markets have been down 3 weeks in a row and oversold conditions are building which is likely to set up for another rally ahead of critical Fed and ECB meetings in September and certainly markets are attempting to do this today.

But be clear, markets remain structurally at risk and neither bulls or bears can rest easy here in this headline driven environment. It remains a big battle for control. The technicals say lower for markets, but it’s also clear that the forces of intervention are keeping a very close eye on markets and are stepping in to adjust their narratives at any sign of trouble. Looking at the charts they are increasingly at risk of losing control.

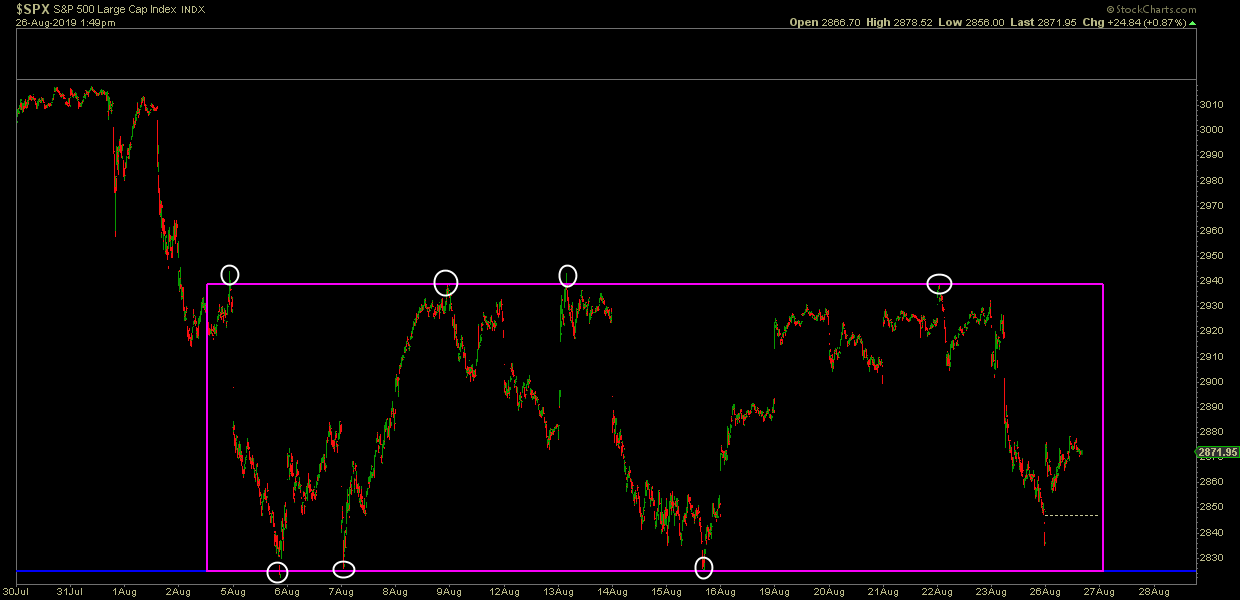

Fact is we remain in a precisely defined price consolidation zone and neither bulls or bears have won the final argument yet. That will only come on a confirmed breakout or breakdown. That range is now 2820-2935 on cash $SPX:

It’s easy to overcomplicate things and game theory the hell out of the Chinese, the Fed, seasonality, buybacks, etc. But let’s just keep it simple: Rallies keep being driven by rate cut hopes and trade optimism. Not by growth, earnings or fundamentals. Technicals continue to reflect patterns and structures that show risk to the downside building. But bears need to prove their case and that means break $SPX 2800 to the downside with conviction. But apparently a tweet or mere mention of a phone call are enough to scare them away 😉 For now anyways. Without a trade deal going beyond vague phone calls the global macro pictures keeps deteriorating. Every single day. Don’t believe me? Check yields. They seem hardly impressed by phone calls.

So what matters more, the trade war, the Fed or technicals? I can only answer for myself and that is technicals, the part of the equation I can see, analyze and react to with reason and a clear view of shifting risk/reward in either direction. I’ll leave the chasing of tweets to others.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2zyN7Fz Tyler Durden

Perhaps the strangest thing about the story that President Donald Trump has expressed interest in using nuclear bombs to stop hurricanes was that it didn’t seem all that strange. Almost no one thought to ask “Can you believe it?” because almost everyone automatically did, while simultaneously acknowledging that in reality, no such intervention would be tried.

So instead of sustained incredulity, there were jokes, and a few #WellActuallys, and eventually Trump himself declared that the story was fake news. But for the most part, the story, first reported by Axios, came and went with the daily tides of Twitter conversation. Trump wants to deploy nuclear weapons to stop summer storms? Wild stuff! 2019, right? Moving on.

One way to understand this is as a basically healthy reaction to the brainfarts of a particularly brainfart-prone president, one who thinks out loud—or online—and who indulges a variety of odd obsessions that rarely become actual policy. Both in public and in private, Trump has a habit of floating half-baked bad ideas that are unlikely to ever be implemented. For many people, constantly worrying about the small chance that they one day might happen is simply too exhausting to keep up.

Yet in another way, the nuke-the-hurricanes episode was a reminder of the ways Trump’s erratic personal behavior has led to a widespread acceptance of presidential ideas that are not only kooky but dangerous, or at least rather risky, even if those ideas are nearly certain to remain unimplemented.

Take, for example, Trump’s declaration last week that American companies “are hereby ordered to immediately start looking for an alternative to China.” This was a presidential “order” that also wasn’t obviously an order in any official sense; it came with no proposed timeline, no potential penalties, and no legally enforceable procedure to back it up. And yet both White House aides and Trump himself nonetheless argued that it could become one if the president were so inclined.

In theory, the argument went, Trump could use the International Emergency Economic Powers Act (IEEPA) of 1977 to declare a state of emergency, expanding the powers granted to the executive, potentially giving him the authority to order U.S. businesses to cease operations in China. Experts disagree about whether the IEEPA could plausibly justify such an order. But it’s fair to say that using it in the way Trump has suggested would be clearly unprecedented and arguably abusive, and that it would almost certainly end up in court.

Still, it is at least possible to imagine a scenario in which Trump finds legal cover for such an order. The result, in turn, would be vast and unpredictable economic consequences for both the American economy and the international order, as two economic superpowers turned a series of economic skirmishes into an all-out economic war. It’s hard to say exactly how it would play out, but as one manufacturer told The New York Times last week, a mandatory exit of U.S. businesses from China “could cause a global depression, not recession.”

Yet just as most people reasonably assume that Trump probably won’t try using nuclear weapons to manage bad weather, few, I suspect, worry that he would ever really try to compel American businesses to fully cut economic ties with another country. It’s an idle threat made by a president with a penchant for bluster, and no more—and thus about as easy to ignore as the idea of deploying a nuclear deterrent against a hurricane.

Or at least that’s what we hope, because the problem with Trump is that it’s almost impossible to ever be fully certain that he won’t eventually pursue his wilder ideas, to be confident that he won’t one day pick up his phone and tweet out an order to pull out of China’s economy that is an actual order, backed up by the force and power of the federal government. This is especially true when it comes to trade and immigration, where Trump has proven willing to act in ways that predecessors of both parties probably would have avoided.

The result is generalized political and economic instability, and a pervasive precariousness to American life. This helps feed more exotic, conspiracy-adjacent theories about Trump himself. And over time, it may well take a serious toll on the American economy. Indeed, some economic consequences are already being felt. Trump’s announcement of tariff hikes last week, combined with his threats against both China and the U.S. Federal Reserve, rattled already jittery markets, sending stocks to their fourth weekly loss in a row.

The point isn’t merely that Trump shouldn’t be playing weatherman with the world’s biggest nuclear arsenal (although he shouldn’t), or that tariffs and trade wars are bad news for the economy (although they are). It’s that Trump’s mercurial behavior, and the lingering possibility that he might try to follow through on one of his more eccentric ideas, exacts a regular low-level toll on our fortunes. He is a constant source of economic and political uncertainty. And that uncertainty, even in the absence of actual action, is bad enough. It makes it harder for businesses to plan future operations, harder for ordinary Americans to plan their retirements, and harder for America’s allies on the international stage to work together.

So no, Trump probably won’t nuke a hurricane, and no, he probably won’t force American companies to stop operating in China, just as he didn’t ever completely close the border with Mexico, despite his threat to do so. Which means that no, you probably shouldn’t spend too much time worrying about the possibility that he might do any of these things, or whatever harebrained idea he tweets out tomorrow. But there’s a lot riding on all those “probably”s, and on the slim-but-real chance that one day a he-probably-won’t will somehow become an actually-he-did. And that alone is cause enough for concern.

from Latest – Reason.com https://ift.tt/2ZhCO87

via IFTTT

Sen. Elizabeth Warren (D–Mass.) is promising to protect Americans from the scourge of…pencils?

In a new video posted to Twitter over the weekend, the presidential candidate promises to create a new federal agency that would expand on the protectionist measures undertaken by Donald Trump. She’s even borrowing Trumpian rhetoric for the project, which she calls “economic patriotism,” as she promises that a Warren administration would put the interests of American workers first.

Warren’s attack on corporations that supposedly harm Americans by shifting jobs overseas is full of intellectual dishonesty and economic fallacies. Rather than making a case for greater government involvement in the corporate boardrooms of America, the video succeeds only at highlighting how misinformed and misguided such interventions are, regardless of whether they are executed by Trump or Warren.

“There are a lot of giant companies who like to call themselves ‘American,’ but face it: they have no loyalty or allegiance to America,” she says in the video.

A lot of giant companies refer to themselves as “American.” But let’s face it, they only have one real loyalty: Their shareholders. A Warren administration will halt the hollowing out of American cities and create good American jobs. Here’s how. pic.twitter.com/pX0VpRXqqR

As proof, Warren points to the “famous no. 2 pencil,” which is mostly manufactured in Mexico and China. Her video doesn’t make clear why pencils should have to be made in America—or why that lack of good, pencil-making jobs in America is a problem.

That Warren chose to use pencils to illustrate the supposed need for “economic patriotism” is darkly hilarious to anyone familiar with “I, Pencil,” the Lawrence Reed’s 1958 parable about the merits of free markets and comparative advantage. Reed’s lesson is that no one on the planet has the means or knowledge to make an item as mundane and ubiquitous as a simple pencil. A pencil requires wood, graphite, brass, and rubber, but each component part is the result of supply chains that might stretch around the world—from the forests of the Pacific Northwest to the mines of Mexico to the factories of Indonesia.

“Neither the worker in the oil field nor the chemist nor the digger of graphite or clay nor any who mans or makes the ships or trains or trucks nor the one who runs the machine that does the knurling on my bit of metal nor the president of the company performs his singular task because he wants me,” Reed wrote in the role of the eponymous pencil. “Each one wants me less, perhaps, than does a child in the first grade.”

And yet we have pencils. Tons of them. Not only that, but the process for obtaining and combining those various component parts is so efficient—despite “the absence of a master mind” directing all those activities, Reed notes—that you can buy dozens of pencils for no more than a few dollars. The simple pencil is a miracle of the modern world, and of trade that crisscrosses national borders.

That Warren fails to grasp this—or that she cynically believes voters don’t grasp it—makes her no better than Trump when it comes to trade policy. Indeed, Trump’s use (and abuse) of executive power to implement his own myopic and self-defeating trade policies may have only paved the way for a more competent protectionist like Warren, if she ends up in the White House.

It’s worth noting that Warren’s proposal for a new federal department to oversee her “economic patriotism” scheme would potentially streamline some government functions. She says the new Department of Economic Development would replace the Commerce Department and “a handful of other government agencies.” Consolidation of the federal bureaucracy can be a good way to root out unnecessary overlap between existing agencies, but this seems like an effort at reorganizing a bunch of things the feds shouldn’t be doing in the first place.

Beyond that, there’s little truth to the claim that American manufacturing has been hollowed out by trade. Foreign investment in American manufacturing reached record highs in 2018, and American manufacturing output has tripled since 1980.

Warren’s proposal smacks of a disingenuous attack on the benefits of free markets, with Warren trying—and failing—to make American corporations seem like a foreign threat.

“The truth is,” she claims in the video,” these American companies have only one real loyalty, and that’s to their shareholders, a third of whom are foreign investors.”

What about other two-thirds of those shareholders Warren is trying to demonize? Well, they would be Americans, of course.

from Latest – Reason.com https://ift.tt/2MGiNkK

via IFTTT

Sen. Elizabeth Warren (D–Mass.) is promising to protect Americans from the scourge of…pencils?

In a new video posted to Twitter over the weekend, the presidential candidate promises to create a new federal agency that would expand on the protectionist measures undertaken by Donald Trump. She’s even borrowing Trumpian rhetoric for the project, which she calls “economic patriotism,” as she promises that a Warren administration would put the interests of American workers first.

Warren’s attack on corporations that supposedly harm Americans by shifting jobs overseas is full of intellectual dishonesty and economic fallacies. Rather than making a case for greater government involvement in the corporate boardrooms of America, the video succeeds only at highlighting how misinformed and misguided such interventions are, regardless of whether they are executed by Trump or Warren.

“There are a lot of giant companies who like to call themselves ‘American,’ but face it: they have no loyalty or allegiance to America,” she says in the video.

A lot of giant companies refer to themselves as “American.” But let’s face it, they only have one real loyalty: Their shareholders. A Warren administration will halt the hollowing out of American cities and create good American jobs. Here’s how. pic.twitter.com/pX0VpRXqqR

As proof, Warren points to the “famous no. 2 pencil,” which is mostly manufactured in Mexico and China. Her video doesn’t make clear why pencils should have to be made in America—or why that lack of good, pencil-making jobs in America is a problem.

That Warren chose to use pencils to illustrate the supposed need for “economic patriotism” is darkly hilarious to anyone familiar with “I, Pencil,” the Lawrence Reed’s 1958 parable about the merits of free markets and comparative advantage. Reed’s lesson is that no one on the planet has the means or knowledge to make an item as mundane and ubiquitous as a simple pencil. A pencil requires wood, graphite, brass, and rubber, but each component part is the result of supply chains that might stretch around the world—from the forests of the Pacific Northwest to the mines of Mexico to the factories of Indonesia.

“Neither the worker in the oil field nor the chemist nor the digger of graphite or clay nor any who mans or makes the ships or trains or trucks nor the one who runs the machine that does the knurling on my bit of metal nor the president of the company performs his singular task because he wants me,” Reed wrote in the role of the eponymous pencil. “Each one wants me less, perhaps, than does a child in the first grade.”

And yet we have pencils. Tons of them. Not only that, but the process for obtaining and combining those various component parts is so efficient—despite “the absence of a master mind” directing all those activities, Reed notes—that you can buy dozens of pencils for no more than a few dollars. The simple pencil is a miracle of the modern world, and of trade that crisscrosses national borders.

That Warren fails to grasp this—or that she cynically believes voters don’t grasp it—makes her no better than Trump when it comes to trade policy. Indeed, Trump’s use (and abuse) of executive power to implement his own myopic and self-defeating trade policies may have only paved the way for a more competent protectionist like Warren, if she ends up in the White House.

It’s worth noting that Warren’s proposal for a new federal department to oversee her “economic patriotism” scheme would potentially streamline some government functions. She says the new Department of Economic Development would replace the Commerce Department and “a handful of other government agencies.” Consolidation of the federal bureaucracy can be a good way to root out unnecessary overlap between existing agencies, but this seems like an effort at reorganizing a bunch of things the feds shouldn’t be doing in the first place.

Beyond that, there’s little truth to the claim that American manufacturing has been hollowed out by trade. Foreign investment in American manufacturing reached record highs in 2018, and American manufacturing output has tripled since 1980.

Warren’s proposal smacks of a disingenuous attack on the benefits of free markets, with Warren trying—and failing—to make American corporations seem like a foreign threat.

“The truth is,” she claims in the video,” these American companies have only one real loyalty, and that’s to their shareholders, a third of whom are foreign investors.”

What about other two-thirds of those shareholders Warren is trying to demonize? Well, they would be Americans, of course.

from Latest – Reason.com https://ift.tt/2MGiNkK

via IFTTT

In the first of potentially thousands of verdicts against pharmaceutical companies accused of inciting the opioid epidemic, an Oklahoma judge on Monday ruled that Johnson & Johnson must pay a $572 million penalty for allegedly helping to fuel the opioid epidemic with irresponsible marketing practices, Reuters reports.

Judge Thad Balkman, of Cleveland County District Court in Norman, Oklahoma issued the ruling shortly after 4 pm ET on Monday. The penalty was only a fraction of the roughly $17 billion that the plaintiffs had been seeking, helping send J&J shares rocketing higher in the after-hours session.

The case, brought by Oklahoma Attorney General Mike Hunter, is the first out of potentially thousands of lawsuits filed by state and local governments against opioid manufacturers and distributors that could go to trial. Only a few cases have been settled, according to Bloomberg. The case is critical, legal experts say, because it will provide defendants with a clearer benchmark for what they can expect.

If J&J loses, Hunter hopes to use the money to help Oklahoma mitigate the fallout from the opioid epidemic over the next three decades by funding treatment and prevention programs.

The trial was held after Oklahoma resolved claims against OxyContin maker Purdue Pharma in March for $270 million, and against Teva Pharmaceutical Industries in May for $85 million,leaving J&J as the lone major defendant.

The seven-week, non-jury trial has been closely watched by plaintiffs and defendants in some 2,000 opioid lawsuits pending before a federal judge in Ohio. The judge has been pushing for a settlement ahead of an October trial.

Lawyers for the state of Oklahoma argued that J&J conducted a years-long marketing campaign that minimized the drug’s addictive qualities. J&J has denied wrongdoing, and insisted that Oklahoma’s case rest

via ZeroHedge News https://ift.tt/2U539QI Tyler Durden