Authored by Charles Hugh Smith via OfTwoMinds blog,

If you think this is a robust, resilient, stable system, please check your Ibogaine / Hopium / Delusionol intake.

Correspondent James D. recently asked for an update on the four intersecting cycles I’ve been writing about for the past 10 years. Here’s the chart I prepared back in 2008 of four long-term cycles:

1. Generational (political/social)

2. Price inflation/wage stagnation (economic)

3. Credit/debt expansion/contraction (financial)

4. Relative affordability of energy (resources)

Here are four of the many dozens of essays I’ve written on these topics over the past decade:

Long Cycles: Cheaper Goods, Costlier Capital, Income Disparity Increases (August 1, 2008)

Beyond the False Dawn: Global Crisis 2020-2022 (February 18, 2011)

A Disintegrative Winter: The Debt and Anti-Status Quo Super-Cycle Has Turned (December 5, 2016)

We’re in a Boiling-Point Crisis of Exploitive Elites (June 19, 2017)

The key point that’s not communicated in the chart is there are dynamics that interact with each of these cycles. For example, demographics are influencing each of these trends in self-reinforcing ways.

Governments are borrowing more to fund the promises made to seniors decades ago when there were relatively few retirees compared to the working populace. Now that the ratio of those collecting government benefits to workers is 1-to-2 (one retiree for every worker), the system is buckling.

The “solution” is to borrow increasing sums from future taxpayers to fund pay-as-you-go healthcare and pension programs for retirees.

Technology is another dynamic that is actively influencing all these cycles in self-reinforcing ways. As technology is substituted for human labor, wages stagnate and the size of the populace paying taxes dwindles accordingly. The “solution” is once again to borrow more to substitute for declining purchasing power.

The dynamics driving wealth/income inequality and the rise of politically/financially dominant elites are also powering these cycles. As Peter Turchin has explained–a topic covered in my essay When Did Our Elites Become Self-Serving Parasites? (October 4, 2016)– social disunity / discord rises when the number of people promised a spot in the elite far exceeds the actual number of slots available.

In summary, the four cycles are intact and poised to intersect in a very messy fashion within the next decade. various centralized efforts have been made to paper over the secular stagnation, political polarization, brewing generational wars, resistance to globalism, rising cost of capital, decay of opportunity, soaring debts, rising dominance of speculation / malinvestment /mis-allocation of capital, diminishing returns on centralization, the marriage of Orwell, Huxley and Kafka in officially sanctioned propaganda, increasingly dysfunctional and self-serving institutions and the rising costs of energy, but every one of these makeshift efforts further erodes the resilience of the overall system and increases systemic fragility and vulnerability to self-reinforcing failures of key subsystems.

Here are a few charts that illustrate the trends / cycles:

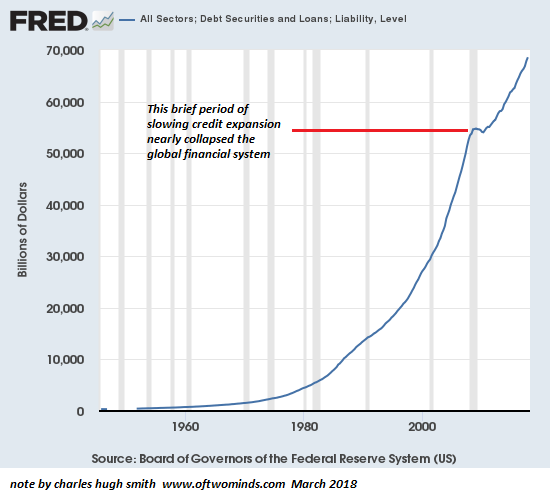

Total systemic debt: note that the tiny wobble in credit expansion in 2008 nearly collapsed the entire global financial system.

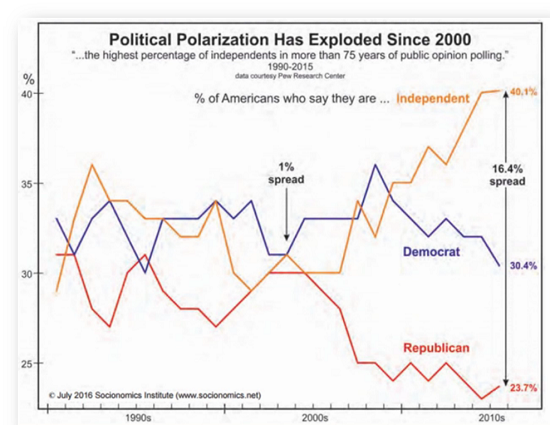

Here’s political polarization: notice any common ground?

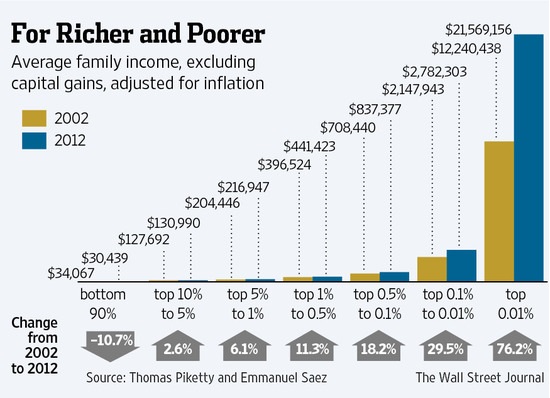

The elites that are safely protected by the moat of the status quo are doing just fine while the disgruntled debt-serfs who were promised security and rising wages/wealth are massing beyond the moat.

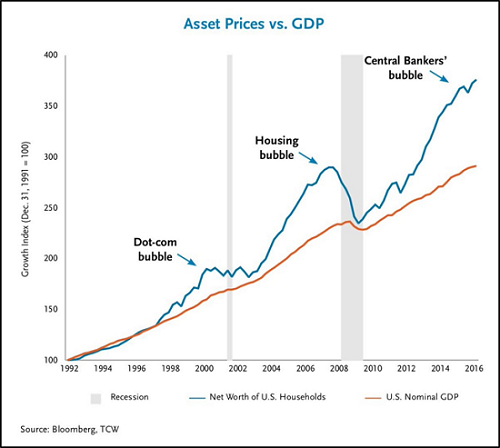

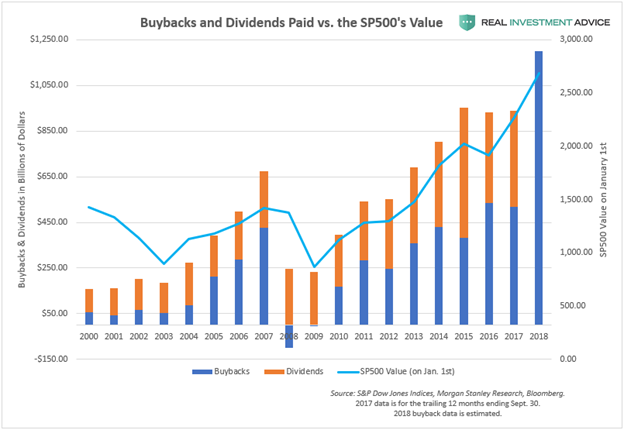

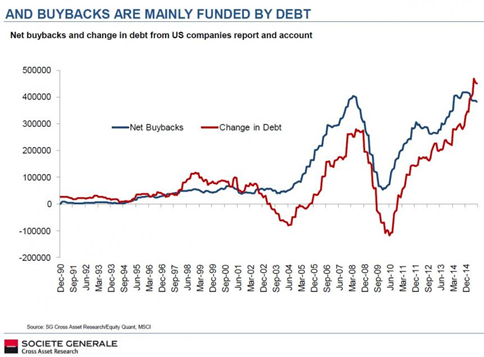

Meanwhile, asset bubbles and soaring debt are the status quo’s go-to fix for every problem:

If you think this is a robust, resilient, stable system, please check your Ibogaine / Hopium / Delusionol intake.

* * *

My new book Money and Work Unchained is $9.95 for the Kindle ebook and $20 for the print edition. Read the first section for free in PDF format. If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

via RSS http://ift.tt/2GrWBon Tyler Durden

In 2017, 84 Americans were freed from prison after revelations of government misconduct helped prove them innocent. That sets a record, according to an

In 2017, 84 Americans were freed from prison after revelations of government misconduct helped prove them innocent. That sets a record, according to an  That fact that physicist Stephen Hawking is an icon of our era was made plain during the production of

That fact that physicist Stephen Hawking is an icon of our era was made plain during the production of

A couple of years ago, Maine’s Republican governor, Paul LePage,

A couple of years ago, Maine’s Republican governor, Paul LePage,