Pope Frances Will Make ‘High Risk’ Official Visit To Iraq In March Tyler Durden

Mon, 12/07/2020 – 23:20

The Vatican has announced that Pope Francis plans to break his 15-month hiatus from international travel, a delay which was also largely to blame on the coronavirus pandemic, by visiting Iraq in the Spring of 2021.

It’s being widely reported as a surprising and “risky” trip given the tense security situation there, also as COVID-19 infections spike globally. It’s planned for March 5-8.

According to the official announcement Monday, “He will visit Baghdad, the plain of Ur, linked to the memory of Abraham, the city of Erbil, as well as Mosul and Qaraqosh in the plain of Nineveh,” said the Vatican Press Office.

Pope Francis with Sheikh Ahmad el-Tayeb, grand imam of Egypt’s al-Azhar mosque. Image source: CNS

This was prompted by both an Iraqi government invitation and the desire of the local Catholic Church, represented in the Chaldean church. It’s expected that Pope Frances could during the trip declare ‘new martyrs’ or saints who were the victims of what’s remembered as the 2010 Baghdad Church Massacre.

During that al-Qaeda linked attack 58 Chaldean Catholics were killed after an hours-long hostage standoff in a Baghdad church. Over 100 churches and monasteries throughout the country were attacked in terrorist incidents during the US-occupation period.

The as yet unpublished Pope’s itinerary for the Iraq visit will “take into consideration the evolution of the worldwide health emergency.” He’ll be the first Pope to ever visit the country.

Pope Francis will travel to Iraq in March 2021.

He will be the first pope to ever visit the country, which is still recovering from the devastation inflicted by the Islamic State. https://t.co/l0KBWqdtJd

He’s expected to emphasize that the ancient Christian presence in Iraq remains essential. Before the US invasion of Iraq to remove Saddam Hussein in 2003, there were an estimated one million to up to 1.4 million Christians in the country, mostly Catholic and Orthodox.

However, after 2017 estimates are commonly at a much reduced 300 to 400 thousand.

During 2014 through 2016 ISIS also drove many Christians out of the Nineveh Plains region near Mosul. While many families have returned to their villages in the area, the bulk either went to other cities in Iraq like Erbil or Baghdad, but many fled the country altogether.

Mosul also once had a sizeable minority Christian presence of 100,000 or more, but in the past years has been completely liquidated of Christians.

via ZeroHedge News https://ift.tt/39Nntjz Tyler Durden

With Britain, France, the European Union, and now America (soon to be under Joe Biden’s leadership) piling onto the net-zero bandwagon, you’d think that some objectivity about the economic costs and consequences about such absolutist carbon-emission policies would be in order. Traditionally, the International Monetary Fund (IMF) could be relied upon as a source of sound economic advice. No longer.

Under its previous managing director, Christine Lagarde, and now its current one, Kristalina Georgieva, the IMF has traded economic integrity for green wokery – thus giving governments license to push radical green policies in the false belief that there are few or no downsides.

Covid-19 has put what might be called green millenarianism on steroids. In July, Georgieva told an interviewer that the pandemic presents a once-in-a-lifetime opportunity to be part of a transformation necessary for human survival: “you don’t like the pandemic, you’re not going to like the climate disaster.” A characteristic of climate millenarianism is over-hyping of the potential damage of climate change while at the same time claiming that avoiding this damage will cost next to nothing. Thus in its most recent World Economic Outlook, the IMF implies that potentially catastrophic climate change can be avoided with a green fiscal stimulus amounting to 1 percent of GDP and carbon taxes of between $10 to $40 a ton in 2030.

The IMF’s analysis is riddled with errors and omissions. It correctly notes that renewable energy is more labor-intensive than generating energy from fossil fuels. As the American Enterprise Institute’s Mark Perry notes, in 2019 it took 5.2 workers in wind and an astonishing 45.8 in solar to produce the same amount of electricity as one worker in nuclear, natural gas, and coal generation. That’s more jobs in wind and solar, yes, but poorly paid ones – a critical dimension of employment that the IMF entirely neglects.

The IMF also implies that renewable energy is less capital-intensive (“reallocation of activity from high- to low-carbon sectors could therefore be more positive (less negative) for employment than investment”). This shows how little the IMF understands about the energy sector. Wind and solar are intermittent power sources, so keeping the grid stable and the lights on requires investment in parallel generating capacity. This makes renewables extremely capital-inefficient. Consider the U.K. Without renewables, the U.K. would require 22 gigawatts (GW) of new capacity to replace old coal and nuclear. With renewables, 50 GW is required – 28 GW more than without. Switching to renewables more than doubles the investment requirement.

Economic progress and rising living standards have come from capitalism’s ability to produce more from less, through constantly improving capital and labor productivity. Widespread adoption of renewables throws this process into reverse. It is the opposite of progress. President-Elect Biden’s promised 10 million new clean energy jobs can be more than met, Perry calculates, by switching to 100% solar energy – but as he points out, “those energy jobs will come at a high price in the form of higher energy costs for consumers and businesses, less dependable electric power, more blackouts, a reduction of jobs in energy-intensive sectors, reduced economic growth and an erosion of the nation’s prosperity.”

To derive its conclusion that net-zero would be the economic equivalent of a flea bite on global growth, the IMF uses general equilibrium modelling, which can be useful in understanding the effects of, say, a tax change, and mapping its effects throughout an economy. But equilibrium, a concept borrowed from Newtonian physics, implies regularity and stationarity, a system returning to a stable growth path as external forces unwind – conditions that don’t pertain when economies undergo forcible structural transformation lasting decades, and of a severity not seen outside wartime or the centrally planned economies of the Soviet era. The methodological assumptions of equilibrium are violated by the economic process that the method aims to model, thus rendering the IMF’s conclusions worthless.

The most misleading claim that the IMF has seeded into public discourse concerns fossil fuel subsidies. “Fossil fuels are now massively under-priced,” the IMF asserts, with global energy subsidies amounting to $4.7 trillion in 2015, equivalent to 6.3% of global GDP. These aren’t your grandfather’s subsidies in the form of cash payments to oil producers, which is what the green lobby would like us to believe: end the subsidies, transfer the cash to clean tech, and all will be well.

In fact, the IMF acknowledges that producer subsidies are “relatively small.” Rather, the IMF’s elastic definition of subsidy includes a $40 per ton carbon tax, speculative estimates of deaths caused by local air pollution as well as deaths from road accidents, and the cost of traffic delays. The epidemiology of PM2.5 – microscopic particles that make up an air pollution tranche – is highly uncertain, something that the IMF researchers acknowledge. A British government report concedes that unlike with smoking and lung cancer, there is no actual group of individuals whose deaths are attributable to air pollution alone. Indeed, a 2012 study analyzing data across 100 American cities found no evidence that PM2.5 concentrations had any causal impact on increasing mortality rates.

Also problematic is the value of a statistical life assumptions used by the IMF, which are several times the actual willingness of both individuals and countries to spend money on improving health. For the U.S., local air pollution makes up around one-half the IMF’s diesel “subsidy,” and traffic congestion around three-fourths of the gasoline “subsidy.”

Improvements to engine technology mean that modern autos are astonishingly clean. In urban centers with the most modern diesel vehicles, the exhaust can be cleaner than the intake air. The IMF would have us believe that the tailpipe is the sole source of vehicular PM2.5. According to a recent study, non-exhaust emissions are now believed to constitute the majority of primary particulate matter from road transport. Pollution from tire wear can be 1,000 times worse than what comes out of the tailpipe, and with their heavy batteries, electric vehicles will cause more air pollution from tire wear.

The same goes for road congestion. Fossil fuels don’t cause it; vehicles do. If the IMF is against road transportation, it should say so.

As it is, the IMF’s treatment of fossil fuel subsidies is no more than a highly sophisticated hit job. Every fairy tale needs a villain. And living happily ever after only happens in fairy tales – or in net-zero reports.

via ZeroHedge News https://ift.tt/3mUcpF6 Tyler Durden

Chinese FX Reserves Soar Most In 7 Years As Beijing Starts To Intervene Against The Soaring Yuan Tyler Durden

Mon, 12/07/2020 – 22:37

A little over five years since China’s 2015 devaluation, which sparked an avalanche of FX reserve liquidation as Beijing scrambled to halt a tsunami of capital outflows which at one point culminated in a furious wave of bitcoin buying by Chinese residents, China is once again adding FX reserves at a blistering pace.

Around the same time that the Chinese National Bureau of Statistics overnight reported a surge in exports and a record trade surplus, the PBOC also reported that at the end of November, China’s Forex reserves jumped to $3.178 trillion, beating estimates of $3.15 trillion, and the highest number since August 2016.

And, at $50.5BN, this was also the biggest monthly increase in FX reserves since November 2013.

And just like the rapid collapse in yuan reserves in the 2015-2017 period was a result of Beijing’s scramble to sell dollar assets and halt the plunge in the yuan and stem the tidal wave of capital outflows, with the recent surge in FX reserves, it appears that China’s authorities are finally pushing back on yuan appreciation which has reached a level where concerns about imported deflation are starting to emerge. Furthermore, while a chunk of the jump in reserves was likely based on valuation adjustments and FX rate changes as a SAFE spokeswoman said, it is likely that the bulk was the result of USD-buying intervention.

As Bloomberg’s Simon Flint writes, it will be interesting to see just how the authorities slow the pace of yuan appreciation: will they use the daily yuan official fixing, intervention, or further announcements of capital outflow liberalization, to slow the pace of yuan appreciation – should dollar weakness persist in the coming months.

That said, there is always a caveat when dealing with Chinese reserve data: as Flint cautions, these estimates are based on valuation-adjustments can be flawed as we don’t know the exact composition of China’s reserves. Nor is it clear whether China revalues securities within its portfolio on a monthly basis. To get the cleanest picture of Chinese capital flows, it’s best to wait for the SAFE dataset on “cross-border RMB flows” which is Goldman’s preferred FX flow measure and which gives a far more definitive picture of what’s really happening behind China’s opaque capital firewall.

Still, with the Chinese yuan soaring in the past 6 months as the dollar has plunged, and fast approaching where it was around the time of the August 2015 devaluation…

… it is only a matter of time before Beijing will have no choice but to aggressively intervene in the currency market, sending the dollar blasting off in the opposite direction.

via ZeroHedge News https://ift.tt/3oA7XvI Tyler Durden

We already knew that this was going to be the worst winter for the U.S. economy since the Great Depression of the 1930s, but now a new round of lockdowns threatens to rip the guts out of hundreds of thousands of small businesses all around the country. As I write this article, 33 million people are under “stay-at-home orders” in California alone. With each passing day, state governments are implementing even more new restrictions, and those new restrictions are going to increasingly choke the life out of economic activity in this nation.

The good news is that most of the corporate giants have enough resources to weather another round of lockdowns, but countless small businesses do not.

In San Francisco, some small businesses that have served the city for generations now find themselves on the edge of extinction…

“I’ve been walking around the city nonstop talking to small businesses owners and every story is sadder than the next,” said Rory Cox, the founder of the newly-formed San Francisco Small Business Alliance. “Everyone is like, ‘I wake up every day and I don’t know how much longer I can do this. I had 60 employees but now all I have is six, or now it’s only me.’ These are family businesses, these are moms and dads, brothers and sisters. I feel firmly we’re the backbone of the city. And they’re destroying us, they’re ripping us apart, they’re tearing out the heart and soul of the city.”

Traditionally, small businesses have been the primary engine of job growth in the United States, but now they are laying off workers in droves once again.

So far this year, more than 70 million Americans have filed new claims for unemployment benefits, and this unprecedented tsunami of job losses was caused by the original round of lockdowns.

Now a new wave of lockdowns is upon us, and there is going to be extreme economic pain all over America.

Sometimes it can be mind numbing to talk about the millions upon millions of Americans that are now in horrifying financial distress, but each one of those individuals has a name…

Tina Morton recently faced a choice: Pay bills — or buy a birthday gift for a child? Derrisa Green is falling further behind on rent. Sylvia Soliz has had her electricity cut off.

Unemployment has forced aching decisions on millions of Americans and their families in the face of a rampaging viral pandemic that has closed shops and restaurants, paralyzed travel and left millions jobless for months.

As I discussed the other day, the Aspen Institute is estimating that up to 40 million Americans could be facing eviction in 2021 because they have gotten behind on rent or mortgage payments.

We have never seen anything like this before in all of American history. We are literally murdering the economy, and most of the politicians that are doing this don’t seem to care. Perhaps their jobs are secure, but there are millions of others that haven’t been able to find a new job after being laid off months ago. In fact, the percentage of “long-term unemployed workers” as a share of all those that are unemployed is now the highest it has been during this entire pandemic…

In November, the number of workers jobless for at least 27 weeks — economists’ barometer for “long-term” unemployment — grew by 385,000 to 3.9 million.

That accounts for 37% of all unemployed workers — up from a third in October and 19% in September.

And of course most of those that are still working are just barely scraping by from month to month.

According to a survey that was just released, nearly tw0-thirds of Americans say that they are living paycheck to paycheck at this point…

In a year still ravaged by the coronavirus pandemic and its economic fallout however, it appears many will be struggling through the most festive part of 2020. A survey finds over 60 percent of Americans say they’re now living paycheck-to-paycheck as the year draws to a close.

The poll of over 2,000 Americans, commissioned by Highland Solutions, wanted to see how spending habits and personal finances in the U.S. are holding up during the pandemic. Their results find 63 percent of respondents have cut back on their spending due to COVID. Six in 10 say they’re doing it to be more cautious, but 49 percent add it’s because of losing income at work.

Now this new wave of lockdowns is going to push millions more struggling Americans into poverty once they lose their jobs.

I feel especially bad for those that have pouring blood, sweat and tears into their small businesses for years only to have them utterly destroyed by politicians like California Governor Gavin Newsom. What one small business owner named Robert Carroll had to say about the new lockdowns in California will stay with me for a very long time…

“We have basically been left with no options and essentially no hope for the future,” wrote Robert Carroll, the owner of the bar Sodini’s in Redwood City. “We understand COVID-19 is serious, and dangerous, however in this scenario it’s not only dangerous to our health, but our financial and mental wellbeing as well. People need to decide for themselves what risks to take, we don’t take risks at Sodini’s, we insist on masks and distancing, all we want is a CHANCE to maintain our business. If you’ve never had a dream taken away and there’s nothing you can do about it, it’s the worst feeling in the world.”

Even in the most wildly optimistic scenario imaginable, it is hard to imagine how we could possibly avoid the most painful winter for the U.S. economy since the Great Depression of the 1930s.

Perhaps that is why corporate insiders are now selling stocks at the fastest pace that we have seen in almost four years.

Corporate insiders absolutely nailed the two short-term peaks in the market that we witnessed earlier this year, and now they seem to think that an even larger move down is coming.

But ultimately what we are heading into is not just another temporary economic setback. Sadly, the truth is that our entire system has started the process of completely melting down.

The COVID pandemic has greatly accelerated matters, but we were going to get to this point one way or another eventually.

Now a day of reckoning is upon us, and this winter is going to be very dark, very cold and very, very bitter.

* * *

Michael’s new book entitled “Lost Prophecies Of The Future Of America” is now available in paperback and for the Kindle on Amazon.

via ZeroHedge News https://ift.tt/3go6ntH Tyler Durden

India Faces Mass Hospitalizations As Mystery Disease Strikes Tyler Durden

Mon, 12/07/2020 – 22:00

As coronavirus continues to spread across the world, a mysterious illness has been detected in India, with hundreds of people admitted to local hospitals and at least one dead.

New Delhi Television Limited (NDTV) reports that nearly 400 people have contracted a mystery illness that has emerged in Eluru, India. At least one person died on Dec. 5. Local health officials are baffled and have yet to find the source of the illness.

Source: AP

Those who contracted the mysterious illness in the city, which is in the state of Andhra Pradesh, experienced seizures, loss of consciousness, and nausea over the weekend.

At least one dead and hundreds hospitalised in India’s Eluru town from an unidentified illness, with symptoms including seizures, dizziness, nausea, and headaches pic.twitter.com/IwaO1WcksC

This comes as Andhra Pradesh is one of the worst-affected states of COVID-19. Doctors ruled out that none of the patients were infected with the virus.

“All patients have tested negative for Covid-19,” Dolla Joshi Roy, the district surveillance officer of Eluru’s West Godavari District, told CNN, adding that about 180 patients out of the 300 who were admitted to the hospital have been discharged. At the same time, the rest are “stable.” She said the patient who died had similar symptoms to the others but then had a fatal but unrelated cardiac arrest.

Andhra Pradesh’s Health Department published a notice that the patients’ initial blood tests didn’t detect any viral infection, such as dengue or chikungunya.

Government authorities are now testing water samples in Eluru for possible contamination after many of the patients said they received water from a similar source.

“The cause is still unknown but still we are doing all kinds of testing, including testing food and milk,” said Roy

The mass hospitalization over the weekend has prompted a special team of doctors to arrive in the city early this week to conduct an investigation about possible sources of the illness.

To find out the root causes for such sudden illness in Eluru, Andhra Pradesh, the GoI is in continuous discussion with State Authorities and the @MoHFW_INDIA, has deployed a Central Team of 3 Doctors to visit the region tomorrow and submit a preliminary report by evening. pic.twitter.com/8Ri0Vq9rB1

Yet another airline has announced that it sees so called ‘COVID passports’, proof that travellers have been vaccinated and/or tested negative for coronavirus, as “essential” for them to be able to travel.

Lance Gokongwei, President and CEO of Cebu Pacific, the largest budget airline in the Philippines, made the comments to reporters Monday.

“We do think that’s essential, especially as we open up international travel,” Gokongwei said, adding that there are “different vaccines and I think we have to work on a single, global COVID passport so that each country respects the passport.”

Gokongwei also stated that without fears of the virus spreading being allayed by vaccination and herd immunity, “there’s nothing to be spoken about.”

“That has to be the number one priority: to get vaccines in the hands in as much of the global population as possible, and then connecting this to a COVID passport,” he urged.

Watch:

Alex Jones: “The globalists are getting a bioweapon ready to lockdown the internet, and bring in world government – not now but very soon…” – June 2018

Several other airlines have indicated that proof of vaccination, through ‘COVID passports’, will become mandatory in order to fly.

In addition, the world’s largest air transport lobby group is developing a global ‘COVID travel pass’ app designed to link vaccination status and coronavirus test results to a person’s travel documents.

Another ‘COVID passport’ type system known as the CommonPass, sponsored by the World Economic Forum, is under development.

A further ‘COVID passport’ app called the AOKpass from travel security firm International SOS is currently undergoing trials between Abu Dhabi and Pakistan.

Wall Street Gears Up To Trade Water Futures As Scarcity Fears Surge Tyler Durden

Mon, 12/07/2020 – 21:20

Freshwater is an ultimate essential resource for the human race – the loss of it would be fatal for hundreds of millions.

For years we’ve outlined the coming water wars(see: here & here) not just in the US but across the world.

Starting this week, water will be joining crude, copper, soybeans, and other commodities traded on US exchanges, which suggests potential water scarcity problems could be nearing.

Farmers, hedge funds, and municipalities will soon be able to trade water contracts linked to the $1.1 billion California spot water market, according to Bloomberg, citing Chicago-based CME Group.

Water contracts will help users manage risk and better align supply and demand. They were first announced in September as wildfires ravaged western states.

“Climate change, droughts, population growth, and pollution are likely to make water scarcity issues and pricing a hot topic for years to come,” said RBC Capital Markets managing director and analyst Deane Dray. “We are definitely going to watch how this new water futures contract develops.”

Tim McCourt, global head of equity index and alternative investment products at CME, said billions of people around the world live in areas where water scarcity is a major problem.

“The idea of managing risks associated with water is certainly increased in importance,” McCourt said.

Bloomberg notes the contracts are based on the Nasdaq Veles California Water Index and will be “financially settled,” as opposed to physical delivery of the resource. The index started two years ago and sets a weekly benchmark spot price for California’s water rights. Each contract size is equivalent to 10 acre-feet of water, equal to approximately 3.26 million gallons.

Patrick Wolf, senior manager and head of product development at Nasdaq, said the new contracts will give farmers a “best guess” at how much water would cost months from now.

Clay Landry, managing director at consulting firm Westwater Research, which provides data to calculate the water index, said large and small agriculture businesses would be some of the first to trade the contracts.

“Without this tool, people have no way of managing water supply risk,” Landry said. “This may not solve that problem entirely, but it will help soften the financial blow that people will take if their water supply is cut off.”

We may live on a “blue planet,” but with 3% of all of our water is fresh, and much of it is inaccessible – Wall Street has understood the coming scarcity of water and potential wars that could be fought over it.

via ZeroHedge News https://ift.tt/2VN57XM Tyler Durden

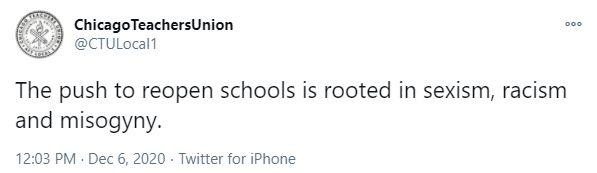

Chicago Teachers Union Tweets Reopening Schools Would Be “Racist, Sexist, And Misogynistic”…And Then Deletes It! Tyler Durden

Mon, 12/07/2020 – 21:00

UPDATE: After getting pummeled on Twitter, the CTU attempts a backpedal. No one’s buying it…

Fair enough. Complex issue. Requires nuance. And much more discussion. More important, the people the decision affects deserve more. So we’ll continue give them that.

Appreciate the feedback of those truly in the struggle.

They couldn’t even scrub the Marxism out of their climb-down. Perhaps keeping Chicago’s public schools closed until the teachers union is dissolved is the wise way to go.

Since we knew they would delete it, we preserved it in digital amber.

Chicago Teachers Union really doesn’t want its teachers to have to go back work.

The union offered no explanation, evidence, or any other factual support for its hot take, probably figuring that including the three magic words would just do the trick on their own. But they’re not, and the tweet is being given its due even after the CTU attempted to get rid of it.

No, the push to open schools is about actually giving a shit about children…rooted in months of data showing rates among students are lower than community transmission rates, while rates among teachers remain equal w/ in-person schooling. There is no excuse.

The city has been in a tussle over when to reopen the schools for months. The union is obviously taking the position that “Never” would be a good time, as its viewpoint is based purely on politics, and even according to the people behind the critical race theory money machine, the -isms involved here will never ever go away. Ever. That would kill their golden Marxist goose. So…never reopen the schools, according to the Chicago Teachers Union.

Imagine if all of the time spent teaching #CriticalRaceTheory or other woke issues to high school students was instead dedicated to teaching basic construction, auto mechanic or excel skills?

How much more valuable would a high school diploma be?

We can no longer imagine such a thing. A Biden administration will only make it all worse.

Mayor Lori Lightfoot, who is a black woman, is now saying the public schools will reopen in January. But that’s in the dead of winter, which won’t help the COVID hospitalization rate.

Is Lightfoot racist, sexist, or a misogynist, CTU? Please show your work.

Another fact the CTU might consider but will undoubtedly ignore is the fact that the science demonstrates clearly that schools are not COVID vectors. Even Dr. Fauci has seen the light on that.

The CTU’s take must be based on something else.

The resistance to reopen schools is rooted in gold-bricking.

For The First Time In 10 Years Companies Will Sell More Stock Than They Buy Back Tyler Durden

Mon, 12/07/2020 – 20:40

For US corporations, the “teens” decade – the years from 2010 to 2019 – was a historic “get rich quick” boom for management when buybacks emerged as the most powerful force levitating stocks (and equity-linked compensation) as companies collectively issued trillions in debt and used the proceeds to repurchase over $10 trillion worth of their own shares, in the process dramatically lifting the stock market and reducing the number of outstanding shares (we called it a slow-motion MBO) and pushing the S&P’s earnings per share ever higher even when there was no actual earnings growth simply because the number of shares declined year after year.

All of that changed in 2020 when thanks to covid, central banks made a triumphal return to their core competency of propping up stocks at all costs (just moments ago we reported that the BOJ is now the single-biggest owner of Japanese stocks) and by injecting over $20 trillion in liquidity in 2020, a rate of over $1.2 billion every hour, buybacks were no longer required to push markets higher and preserve the biggest asset bubble ever created. What also changed is that since buybacks were no longer needed, with the Fed and its central bank peers backstopping all risk assets, buybacks reversed and for the first time since 2010, in 2020 companies will sell more stock than they buy back.

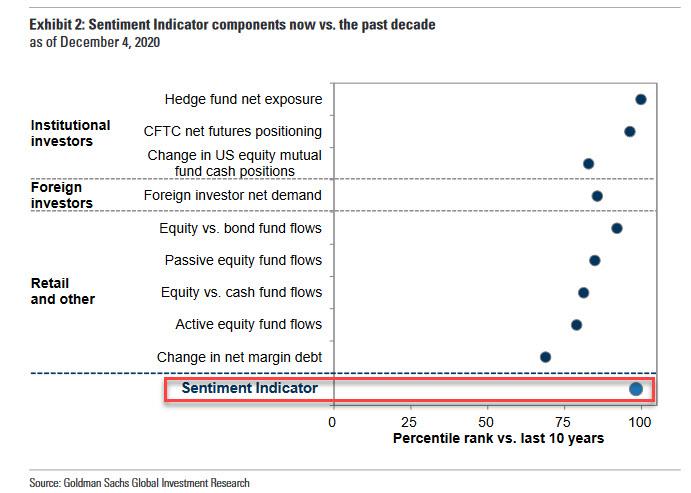

As Bloomberg reports, “while American firms normally repurchase way more stock than they sell, this year has been different, as offerings by everyone from Snowflake Inc. to Warner Music Group Corp. flooded the market with shares.” It’s not just growth stocks that are rushing to capitalize from the market’s peak euphoria phase, which according to Goldman has seen positioning so “extremely stretched” it is currently in the 98th percentile in history:

As Bloomberg notes, companies that were hurt most during the pandemic, from airlines to cruise lines, are also rushing to raise cash and shore up balance sheets. And they are finding plenty of willing buyers.

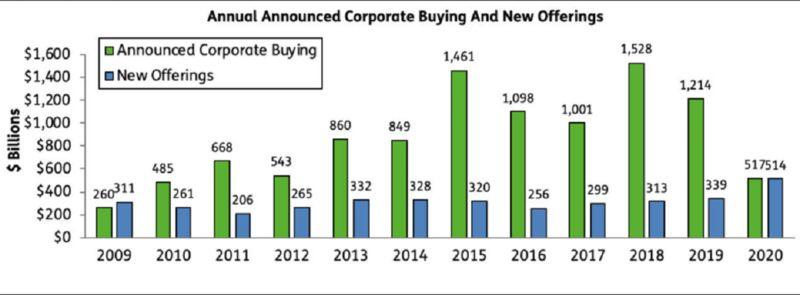

The result is that amid the flood of equity offerings, both initial and secondary, companies have announced plans to raise about $510 billion via share offerings in 2020, up 50% from last year, according to data compiled by EPFR. This means that for the first time since the 2009 crisis, that amount of stock sales matches the amount that companies announced they’d remove via buybacks and takeovers. For context, over the past decade an average of $3 was bought back (thanks to ultra cheap debt) for every $1 raised.

Normally, the reduction in buybacks would be a flashing red alert as the largest source of stock demand was no longer there. However, this is anything but “normal times”, as central banks are now injecting such an unprecedented firehose of liquidity into markets – not the economy – even the BIS is shocked.

It’s also the case that normally, such a flood of selling would hit stocks simply due to excess supply. But, yet again, in this bizarro centrally-planned freakshow of a “market” nobody has any idea what will happen as Randy Frederick, VP of trading and derivatives for the Schwab Center for Financial Research, freely admits: “corporate demand is one component that drives the market higher that is no longer relevant in this risk-on atmosphere. On its own, I would not say it makes the market go down, but it might cause the market to flatten out and not go much higher.” Or it could just send stocks soaring even more; the reality is that we now live in a centrally-planned world where corporate actions no longer impact prices – those are only influenced by fund flows – and as such the surge in stock offerings could merely accelerate the melt up. Ultimately, it’s all what central banks decide.

One thing we do know is that the explosion in offerings is finally increasing the total pool of stocks (another trend that normally pressures stock prices at market tops in the past, but again, this is anything but normal). The S&P 1500 Index divisor, a proxy for outstanding shares, has risen 0.2% this year, its first increase in 10 years according to Bloomberg data.

Yet another warning sign: while the boom in IPOs underscores “a robust market” according to Bloomberg, the increase in share counts could also be viewed as an indication companies are “selling high,” with valuations too attractive to resist – while being too rich to justify buybacks (or simply refusing to take a gamble to issue debt and repurchase stock at a time when the airline industry can’t get a bailout due to its chronic stock repurchases in the past decade). To be sure, at 22 times earnings, the S&P 500 trades near the highest multiple since the dot-com era.

“Obviously when the market is at an all-time high, you want to issue shares now, because the shares are worth a lot more than they would be if the market was tanking,” EPFR analyst Winston Chua told Bloomberg. “Looking at the market broadly, companies are not being supportive of share prices.“

Luckily, markets no longer exist as they have been completely replaces as policy tools for activist central planners armed with money printers. It’s also why skeptics who rely on logic and fundmentals are proven wrong again and again: “There’s a lack of an incremental buyer out there, so that’s a negative, and it still signals some caution as companies let the cash accumulate,” said Mike Bailey, director of research at FBB Capital Partners. Which is true, but one just has to spin the data ever so slightly to represent it in a bullish light, as Bailey does next: “The flip side is, you are building more pressure for companies to really drop the hammer and start to buy back stock next year and into 2022.”

That’s the scenario envisioned by Goldman chied strategist David Kostin: In 2021, he expects net share repurchases will double to $300 billion and equity issuance will fall from this year’s record high, his team forecast. After all, he has to use fundamentals to justify his 4,300 price target – saying “buy because central banks got your back” would be frowned upon.

Of course, for the skeptics out there who are screaming this is idiocy pure and simple, you are right… at least based on empirical data. As Bloomberg notes, Corporate actions on equities showed a close inverse relationship with the market’s performance. During the two decades through 2015, companies boosted net equity demand in 15 different years, 12 of which saw the S&P 500 gain, a study by EPFR showed. In the five years when corporate supply increased, the equity benchmark fell 60% of the time.

But – once again – this is anything but normal times: we now live in a world where central banks have just one purpose: to keep stocks rising even higher because the moment the game of musical chairs stops, it’s all over.

That said, there is a silver lining: companies are once again very cash rich. The new listings on U.S. exchanges have raised more than $150 billion this year. Even firms recently left for dead such as Airbnb – it rents out apartments during the worst pandemic the world has seen in a century – just filed to sell as much as $2.6 billion to cap one of the busiest years ever. Other companies planning listings include food delivery service DoorDash and video-game company Roblox.

“In every cycle, when we say, ‘OK, that was the deal the market rolled over on,’ and all of a sudden everyone’s pulled in their horns,” said Arthur Hogan, chief market strategist at National Securities Corp. “I don’t think we’re there yet, but certainly the number of deals has been pretty historic,” he added. “Companies that shouldn’t be coming out come out and there’s always a tipping point.”

Yes Art, but thanks to Jerome Powell and his central-planning friends, “this time continues to be different.”

via ZeroHedge News https://ift.tt/3qC9FhP Tyler Durden

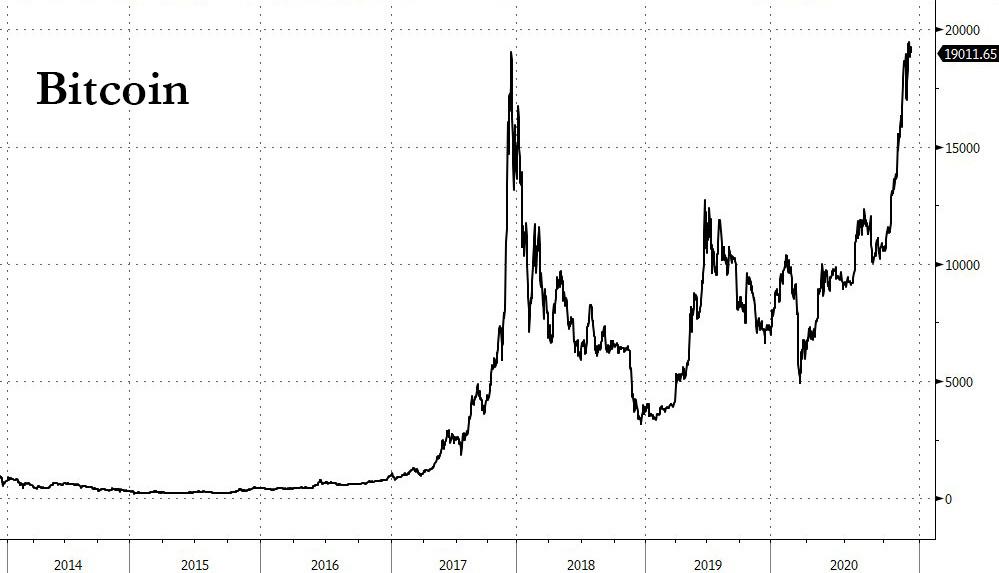

G7 Finance Ministers “Strongly Support” Regulation Of Cryptocurrencies Tyler Durden

Mon, 12/07/2020 – 20:20

With bitcoin trading at fresh all time highs, if just shy of $20,000 for the time being, it was only a matter of time before the establishment renewed its calls for regulation of cryptos, especially now that official central bank digital currencies are in the process of being rolled out to enable instantaneous deposits from central banks (i.e., freshly printed currency which has no matching liability) to end-consumers in hopes of finally sparking one massive inflationary conflagration.

That changed today when G7 finance ministers and central bankers confirmed there is “strong support across the G7 on the need to regulate digital currencies” the Treasury Department said in a statement on Monday after a virtual meeting of the officials.

As Reuters adds, German Finance Minister Olaf Scholz issued a sharply worded statement after the meeting, underscoring his concerns about authorizing the launch of Facebook’s Libra cryptocurrency – which was recently renamed to Diem – in Germany and Europe.

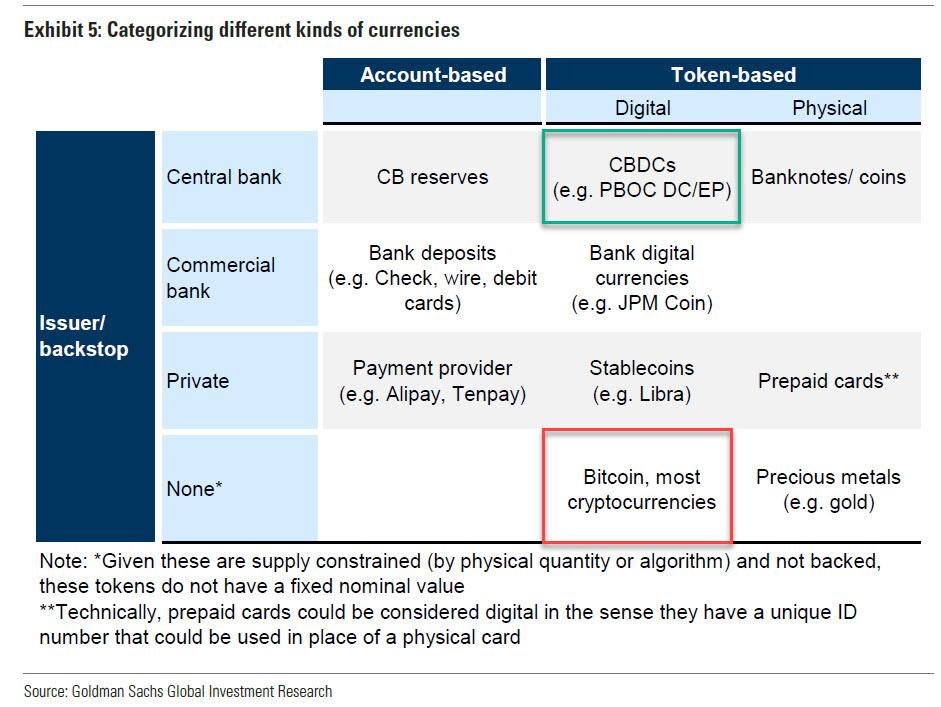

“A wolf in sheep’s clothing is still a wolf,” he said. “It is clear to me that Germany and Europe cannot and will not accept its entry into the market while the regulatory risks are not adequately addressed.” He added: “We must do everything possible to make sure the currency monopoly remains in the hands of states.”

Oddly enough, he had no similar negative comments about digital currencies that are endorsed by central banks. In other words, digital currencies backed by central banks, good; but bitcoin and other cryptos not backed by a central bank, bad.

Steven Mnuchin hosted the 12th meeting of the G7 finance officials this year related to the COVID-19 pandemic as Washington prepares to hand over the presidency of the G7 to Britain next month. The G7 finance officials discussed ongoing responses to “the evolving landscape of crypto assets and other digital assets and national authorities’ work to prevent their use for malign purposes and illicit activities,”Treasury said.

“There is strong support across the G7 on the need to regulate digital currencies,” the G7 statement said, and reiterated support for a G7 joint statement on digital payment in October, which said digital payments could improve access to financial services and cut inefficiencies and costs, but should be “appropriately supervised and regulated.”

In other words, the only cryptocurrency that will be permitted is one which is backstopped by a central bank.

G7 finance officials also discussed domestic and international economic responses to the COVID-19 pandemic, and strategies to achieve a robust global recovery, the statement said.

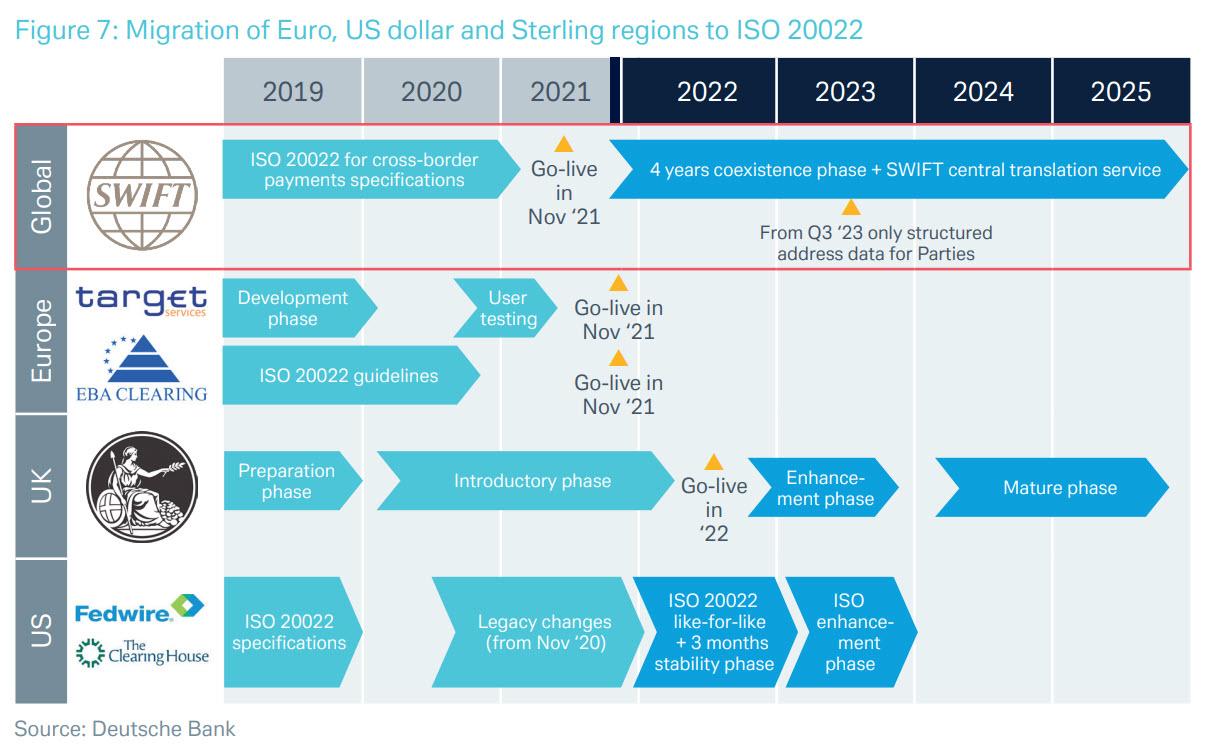

As we showed previously, while not nearly front-page news, the push for central bank-backed digital currencies continues, and according to a recent timeline for the ISO20022 standard, the rollout is expected to take place some time in 2022-2023, once both SFIFT and FedWire adopt the new standard.

via ZeroHedge News https://ift.tt/2JBFVRH Tyler Durden

{kind=link}

{kind=link}