WTO Decides Trump’s China Tariffs Broke International Trade Rules Tyler Durden

Tue, 09/15/2020 – 10:24

In a long-anticipated ruling, the World Trade Organization has just ruled that President Trump’s tariffs on Chinese imports violate established trade rules, suggesting that the international body, which was established by the West in the 1990s following the trade wars of the 1980s, has joined China and the EU in turning against the US.

Washington has slapped tariffs on more than $550 billion in Chinese exports. The trade war began in earnest during the spring of 2018.

As Bloomberg reports, the ruling – handed down Tuesday by a panel of three trade experts – found that the US violated international trade rules with its use of 1970s trade laws to unilaterally launch what BBG described as a “commercial conflict” – we guess they didn’t want to say ‘trade war’ – with China.

However, though the ruling likely grabbed investors’ attention, the decision is effectively toothless, since the US can lodge an appeal any time during the next 60 days. According to Bloomberg, thanks to changes to the appeals process made by the US, doing so would effectively stymie any further action.

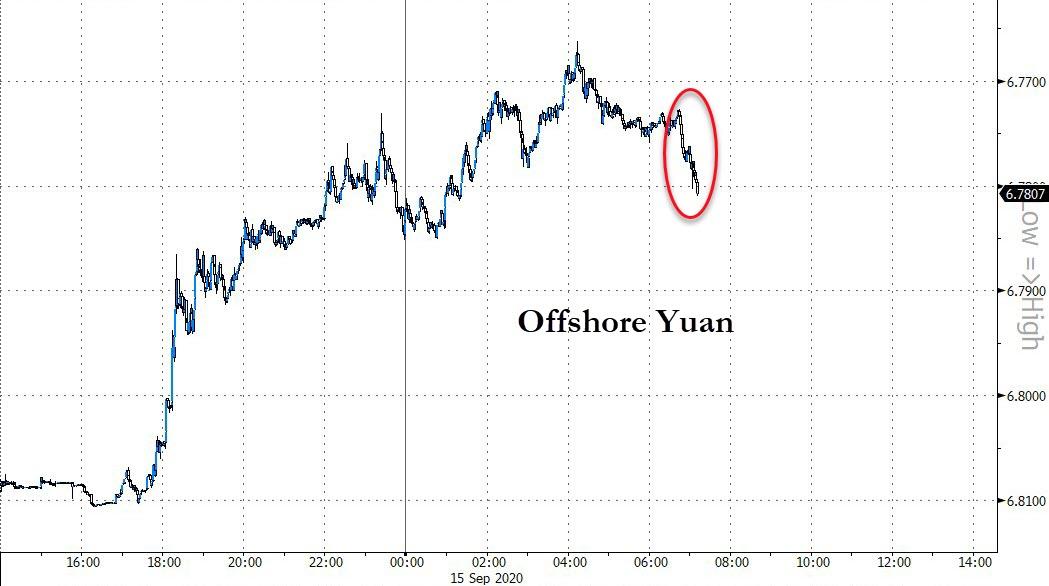

The news prompted a slight pullback in stocks…

…as well as a drop in the trade-sensitive offshore yuan.

In its complaint, China argued the American tariffs violated the WTO’s most-favored treatment provision because they singled out China, and didn’t apply broadly to all international trading partners. Beijing also accused the US of bypassing the WTO’s dispute-resolution mechanisms.

US tariffs against China were authorized under Section 301 of the Trade Act of 1974, which empowers the president to levy tariffs and other import restrictions when “unfair” trade practices negatively impact the US economy. Use of Section 301 isn’t unprecedented – Reagan used it against Japan in the 80s – but it largely fell out of favor in the 1990s, around the time the WTO was created.

As we noted above, it’s just the latest sign that the WTO, and many other international institutions that the US helped create, have continued to side with China against the Trump Administration.

Trump has blamed his predecessors for pushing to admit China to the WTO, then standing by and doing nothing as Beijing stole US technology, illegally subsidized domestic industry and kept tight controls on their economy, and any foreign companies operating therein.

via ZeroHedge News https://ift.tt/33zu0tz Tyler Durden

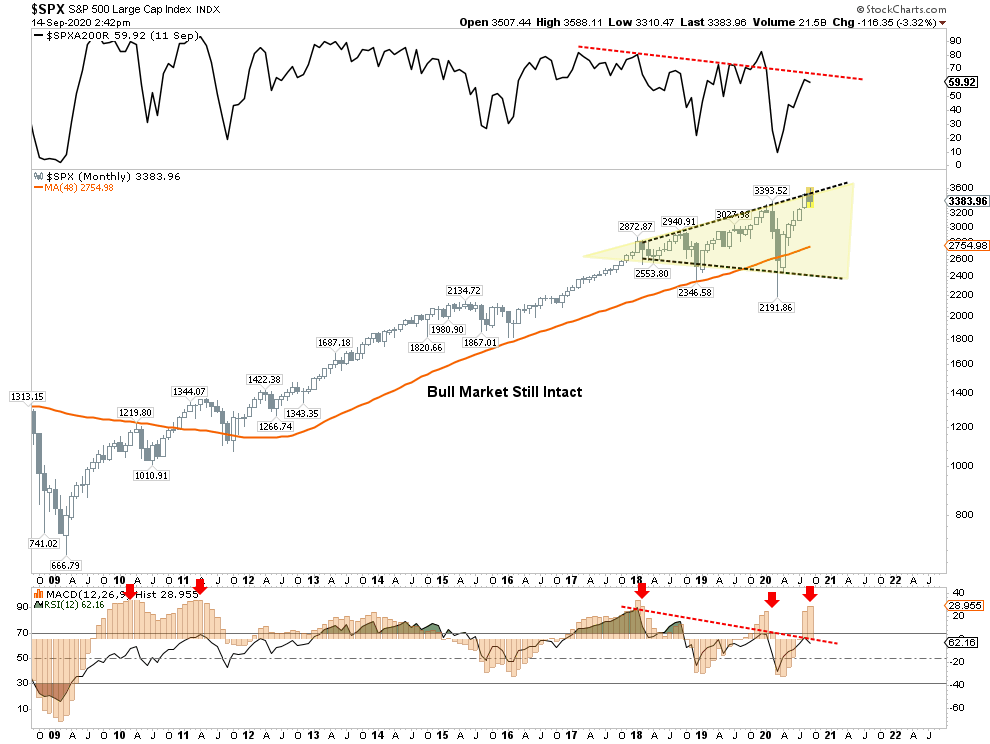

Is everything “priced in?” Investors have gone “all in” with a disregard for caution. But with markets extended and overvalued what should investors do now?

As discussed in this past weekend’s newsletter, investors got even more speculative during the recent correction, which is the opposite of what you would expect. But if markets anticipate “good news,” then are there any “surprises” left?

In other words, if markets have priced in perfection, then there is not a lot of room for “disappointment.” Such was a point I made this morning on Twitter:

Lot’s of room for a bigger #correction at some point with #shortinterest at multi-year lows. All you need is some unexpected, exogenous event to trigger algos to reverse course. pic.twitter.com/OOXEvaNvzj

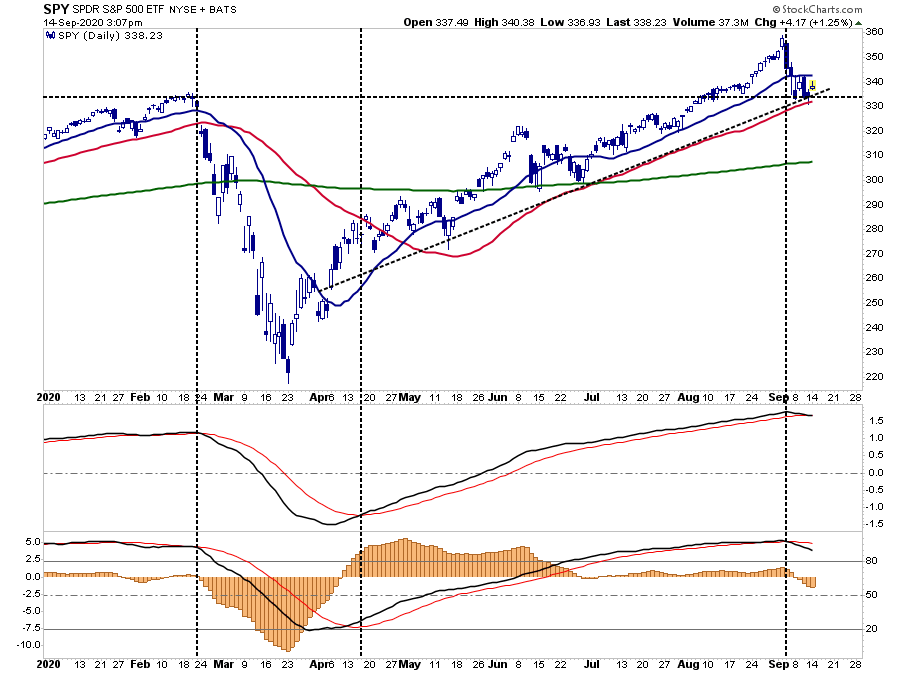

As we have discussed previously, “market momentum” is a hard thing to kill. Such is particularly the case when the “Fear Of Missing Out” overrides logic. In this past weekend’s missive, we laid out the case for a “sellable rally.” To wit:

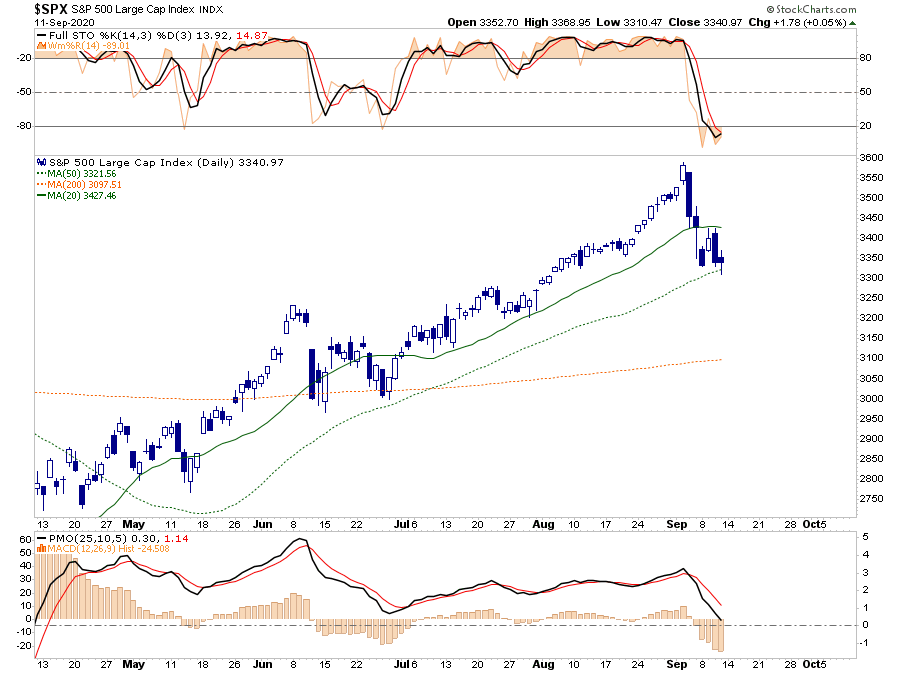

“You can see the failure of the market at the 20-dma and the support at the 50-dma. What is essential are the upper and lower indicators.

Both of the upper indicators are currently registering short-term oversold conditions, suggestive of at least a reflexive bounce next week.

Conversely, both of the lower “sell signals” have been triggered, and as noted in the video, it suggests there is additional selling pressure on stocks currently.”

Chart updated through Monday’s close:

Lots Of Risks To The Bullish Outlook

While we used the sell-off to add some holdings to our portfolios, we remain cautious for several reasons.

The market has fully priced in whatever economic recovery we are likely to see near-term.

There is clear evidence of weakening economic data and slower earnings growth.

Investors are counting on a “vaccine” to restore the economy to its previous strength fully.

The markets have entirely discounted the potential for an election “event.”

Market participants have discounted the need the additional stimulus to sustain economic growth and recovery.

The Fed is on the sidelines for now. Without additional Treasury issuance, the Fed has less ability to provide additional liquidity to the market.

While the economy is indeed recovering, along with employment, it will still likely fall well short of pre-pandemic levels stifling future earnings growth and revenues.

Investors are paying exceedingly high valuations based on a full earnings recovery, which is unlikely to be the case.

Sluggish Growth

The problem, as discussed in “Insanely Stupid,” the ability for stocks to continue to grow earnings at a rate to support such high valuations is problematic. Such is due to rising debts and deficits, which will retard economic growth in the future. To wit:

“Before the ‘Financial Crisis,’ the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt, and leverage increased.

The ‘COVID-19’ crisis led to a debt surge to new highs. Such will result in a retardation of economic growth to 1.5% or less.”

Slower economic growth, combined with a potential for higher taxes, increases the probability that “risk” may well outweigh “reward” at this juncture. However, all of these issues will take time to play out.

In the short-term, it’s all about sentiment.

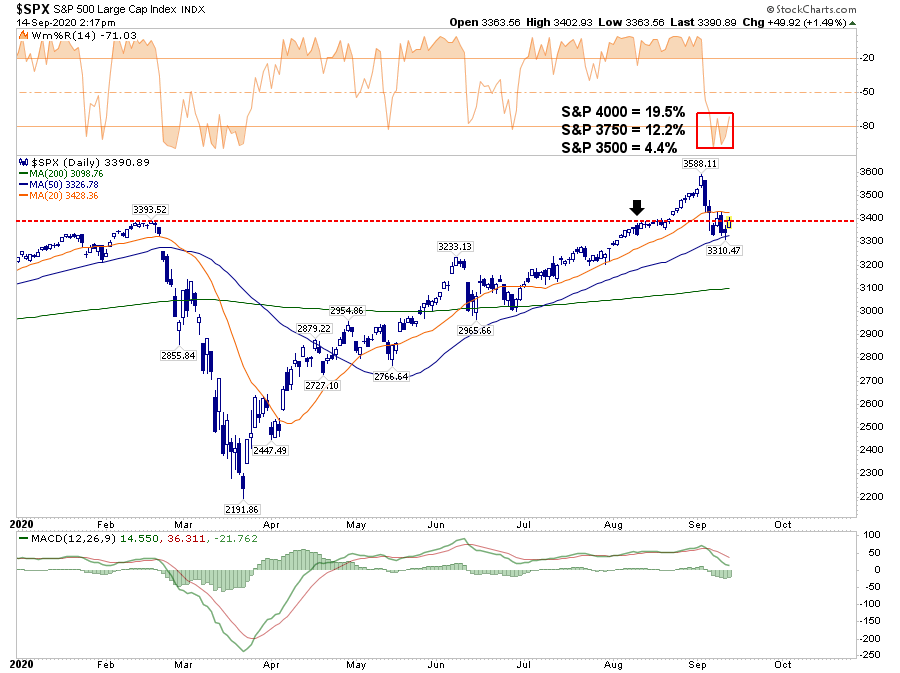

3750 Or Bust!

Stocks can, and likely will, try and go higher in the near term. There is a tremendous amount of bullish sentiment in this regard. Options speculators have not been deterred by the recent sell-off and continue to “buy the dip.”

Such is why, despite some likely wiggles along the way, our target of 3750 may still be viable because of momentum and extreme levels of “bullish bias.”

“With the markets closing just at all-time highs, we can only guess where the next market peak will be. Therefore, to gauge risk and reward ranges, we have set targets at 3500, 3750, and 4000 or 4.4%, 12.2%, and 19.5%, respectively.”

Since that time, the market did indeed rally to, and exceeded, our initial target of 3500. The subsequent pullback to the 50-dma held the bullish uptrend from April for now and did reverse the short-term overbought condition.

Also, as we showed our RIAPro Subscribers (30-Day Risk-Free Trial), the sharp sell-off in Technology specifically pulled the sector out of its Risk/Reward range, providing a “bullish setup.”

It’s Still A “Sellable Rally.”

The reason we suggest selling any rally is because, until the pattern changes, the market exhibiting all traits of a “topping process.”

Weak participation

Failure at long-term resistance

Extreme bullish speculation

Negative divergences in relative strength

We can show this in a long-term monthly chart.

Note that since 2009, whenever the monthly MACD “buy signal” was this elevated, it typically correlated to a short- to intermediate-term market peak. At each point, the “bullish story” was the same.

Earnings are still strong

Economic data suggests the economy is growing strongly

However, the primary warning signs to investors were also the same:

A failure of the economy to live up to market expectations

A rise in volatility

A decline in bond yields.

Some Upside, But Downside

Could that change?

Indeed, and if it does, and our “onboarding” model turns back onto a “buy signal,” we will act accordingly and increase equity risk in portfolios. However, for now, the risk still appears to be to the downside.

Overall, our assessment remains one of caution. In the short-term, we could well see an oversold bounce that could even recover back to the previous highs.

However, we suspect that given the rather numerous headwinds currently facing the markets, from the Fed to the election, that a failure at lower highs would not be surprising.

While we did add some exposure near the lows, we will be using the rally to sell into and increase our portfolio hedges heading into the election.

If you disagree, that is okay.

However, these are the questions we ask ourselves every time we add exposure to portfolios:

What is the expected return from current valuation levels? (___%)

If I am wrong, given my current risk exposure, what is my potential downside? (___%)

If #2 is greater than #1, then what actions should I be taking now? (#2 – #1 = ___%)

How you answer those questions is entirely up to you.

What you do with the answers is also up to you.

Ignoring the results and “hoping this time will be different” has never been a profitable portfolio strategy.

via ZeroHedge News https://ift.tt/2ZCB9I4 Tyler Durden

Putin Withdraws Russian Troops From Belarus Border After Uneventful Lukashenko Meeting Tyler Durden

Tue, 09/15/2020 – 09:45

We noted that during Monday’s much anticipated meeting between embattled Belarusian President Alexander Lukashenko and Putin in Sochi, the Russian leader appeared unmoved by Lukashenko’s urging that the two countries prepare their armies to “resist” the external threat of NATO forces.

Though Putin announced a $1.5 billion loan to Belarus, he made it clear that the smaller Russian neighbor which was formerly part of the Soviet Union would have to solve its own problems internally and in a “calm manner”.

Underscoring that Kremlin focus appears to be moving away from any level of direct intervention, it has ordered national guard troops and police away from the border.

Russian troops are returning from the border with Belarus to their bases after a decision was made yesterday to disband the reserve group formed by Putin’s order in case situation in Belarus gets out of Lukashenko’s control. pic.twitter.com/OrtuYLO6HT

Russian media showed live images of truckloads of the border security units returning to their regular bases on Tuesday morning.

“An important result of the two presidents’ talks in Sochi became an agreement that Russia removes the reserve of law enforcement bodies and the national guard, which was deployed near the Russia-Belarus border, and withdraws people to their permanent bases,” Putin’s press secretary Dmitry Peskov said according to TASS.

As for the loan it likely serves to given Lukashenko more negotiating leverage in terms of gaining support from other powerful Belarusian officials and civic leaders at a moment mass demonstrations continue to swell in the capital of Minsk.

The Guardian reported on Monday’s somewhat awkward press conference that Lukashenko urged, “A friend is in trouble, and I say that sincerely.”

In case you were wondering about how the Lukashenko-Putin talks are going in Sochi. Check out the body language. pic.twitter.com/qSProSQl2N

But the report noted that “Putin at times seemed visibly bored, tapping his hands and feet as Lukashenko embarked on a long monologue.”

So long as there’s not overt evidence of US-NATO and EU meddling in Belarus’ affairs, it seems Russia is content to stay of the sidelines. But the question still remains: ahead of the US November election, will Washington and its intelligence services be willing to go full-blown Ukraine to oust the longtime strongman from office?

via ZeroHedge News https://ift.tt/2FHEQp6 Tyler Durden

University of Chicago English Department graduate programs will only be open to applicants who plan to study “Black Studies” this year.

According to its admissions information webpage, the department is only accepting graduate applications from those who are “interested in working in and with Black Studies” for this academic year.

“For the 2020-2021 graduate admissions cycle, the University of Chicago English Department is accepting only applicants interested in working in and with Black Studies. We understand Black Studies to be a capacious intellectual project that spans a variety of methodological approaches, fields, geographical areas, languages, and time periods,” the university’s English Department website states.

The department’s Black Studies program works “in close collaboration with other departments to study African American, African, and African diaspora literature and media, as well as in the histories of political struggle, collective action, and protest that Black, Indigenous and other racialized peoples have pursued, both here in the United States and in solidarity with international movements.”

The program boasts a “commitment” not just to “ideas in the abstract,” but also to more concrete action in the form of “activating histories of engaged art, debate, struggle, collective action, and counterrevolution as contexts for the emergence of ideas and narratives.”

The university introduced this information by proclaiming “that Black Lives Matter, and that the lives of George Floyd, Breonna Taylor, Tony McDade, and Rayshard Brooks matter, as do thousands of others named and unnamed who have been subject to police violence.”

“As literary scholars, we attend to the histories, atmospheres, and scenes of anti-Black racism and racial violence in the United States and across the world. We are committed to the struggle of Black and Indigenous people, and all racialized and dispossessed people, against inequality and brutality.”

The Black Studies program boasts a number of working groups available to students, including the “Race and Capitalism Project,” an initiative with work focusing on “how processes of racialization within the U.S. shaped capitalist society and economy and how capitalism has simultaneously shaped processes of racialization.”

Black Studies courses advertised by the department include “Black Shakespeare,” during which students will learn how Shakespeare played a role in “the shaping of Western ideas about blackness,” and focus on “Shakespearean plays portraying Black characters.”

Campus Reform reached out to the university for comment but did not receive a response in time for publication.

via ZeroHedge News https://ift.tt/2E1r4Nl Tyler Durden

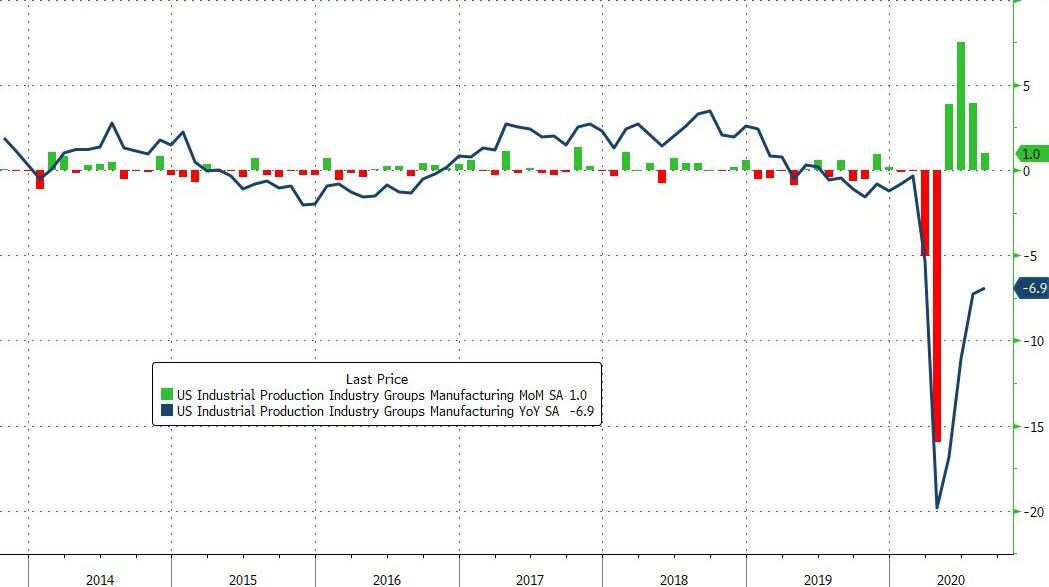

US Industrial Production Big Disappointment In August As “V” Evaporates Tyler Durden

Tue, 09/15/2020 – 09:20

The initial surge recovery from April’s collapse in Industrial Production was expected to slow further in August (from +3.0% MoM in July to +1.0% MoM in August) and in fact it slowed even more with a mere 0.4% MoM rise…pushing the YoY loss in IP down to 7.73%…

Source: Bloomberg

US Manufacturing’s rebound also slowed in August (+1/0% vs +1.3% exp) leaving it down 6.9% YoY

Source: Bloomberg

And finally, the Dow Jones INDUSTRIAL average continues to forecast a much faster and more aggressive recovery in INDUSTRIAL production than hard data suggests…

Source: Bloomberg

But since when did reality have anything to do with market valuations.

via ZeroHedge News https://ift.tt/3c0Akhd Tyler Durden

“We Need China To Move”: Senator Proposes Stripping China’s Most-Favored-Nation Status Tyler Durden

Tue, 09/15/2020 – 09:10

By Michael Every of Rabobank

Chinese data for August show it is moving again. Industrial production was up 5.6% y/y, above the 5.1% consensus; retail sales were up 0.5% y/y vs. flat consensus (though still -8.6% year-to-date); fixed-asset investment was -0.3% y/y vs. -0.4%; property investment 4.6% y/y vs. 4.1%; and, for those who are going to bother following the series, the jobless rate was unchanged at 5.6%.

So spending is up, marginally, but still well behind where it would have been in a normal year. Guess what? The same is true in Western countries: UK and US retail sales are both stronger than China’s measured in some ways; that’s what happens when you pump most of your stimulus into handouts to households. Chinese production is up much, much more, however. Which isn’t really a surprise when exports are running strongly due to global demand for the work-from-home stuff China provides, and as the equivalent of USD500bn in new credit was pumped in during August alone, and as the usual mega SOE infrastructure schemes are rolled out.

Of course, CNY loved this and has broken 6.80. Can it move much further than this? Well, until now the currency —which is not a free float!— has been tracking the overall movement of the USD. If that keeps declining, then perhaps. There seems to be far less of a case to suggest China is suddenly happy with a strong currency ‘because it is going to be looking inwards’. How much deflation does a deflation-prone economy need? Ask the giant property developer who cut prices 30% for a month from 6 September.

Indeed, consider even as net exports mean major USD inflows in recent months, and as net bond portfolio inflows are up too due to the inclusion of Chinese sovereign debt in foreign bond indices –I continue to try to write the scenario where China is in any way restrained in its fiscal actions by what foreign bond holders think– large net capital outflows continue. How else to explain that with all this cash coming in, FX reserves are still USD3.1 trillion (the magic level from which they cannot move)? Local money is moving out even as China is ostensibly ‘moving’.

Meanwhile, it’s not as if one cannot see bumps in the road. The EU-China virtual investment summit, for one. Germany’s Angela Merkel, true to neoliberal form on trade, suggested human rights issues are not the kind of thing to stop Germany from wanting to sell more German stuff. (Is anything?) However, China told the EU that human rights were its internal affair, a European problem too, and that it would take no lectures. The EU meanwhile insist China has to open up its markets and scaling back the role of its SOEs – just as China talks about a shift to internal circulation and as the same SOEs drive the recovery Europeans are salivating over. “China has to convince us that it is worth having an investment agreement,” said the EU’s von der Leyen. “We need China to move.” Will it? Or will the EU blink in the one area in which it sees itself as having global power? What does that say about its strategic options if it does – or if it doesn’t?

On which note, last night UK PM Johnson saw off a Tory rebellion to force through the first reading of legislation that seems to aim for a Hard Brexit and, according to critics, further strain on peace in Northern Ireland and union with Scotland. Boris says this is necessary to prevent the EU ‘blockading’ Northern Ireland’s food supplies; but will we really see EU bureaucrats sailing the Irish Sea like pirates to seize gold, silver, and Marmite? Suffice to say that either the UK or the EU need to move, and soon, or smooth EU-UK trading relations are likely to walk the plank. GBP and EUR with it, presumably….which then flows back to USD and so to CNY.

Meanwhile, in the US, TikTok is perhaps going to have a new ‘owner’, or rather licensee(?),… although that would seem to imply the White House doing a major policy FlipFlop (which is a great name for an app: I may now be able to retire immediately). Being overlooked is that Senator Tom Cotton –of whom I wanted to write the Daily headline “Just a Cotton-picking minute” when his name was, oddly, floated as a potential Supreme Court nomination should President Trump win re-election– has introduced legislation to repeal China’s permanent most favored nation (MFN) trade status. According to Cotton, MFN status would depend on China’s behaviour annually. In other words, “we need China to move”.

China itself is sending a not-so-subtle signal of its own that it wants Australia to move: or at least that’s the interpretation Down Under of the sudden move to declare that Aussie wheat exports are to be subject to enhanced scrutiny for phytosanitary standards: add them to beef and wine and barley, eh?

Of course, the RBA’s minutes today couldn’t capture this further negative development, but the language on the AUD had already shifted. In August, we saw AUD “had also appreciated against the USD to be a little above where it had started the year. The AUD had been broadly in line with its fundamental determinants, such as commodity prices and interest rate differentials, which had returned to their levels at the start of the year”. In September we saw: “While members noted that the AUD was broadly aligned with its fundamental determinants, a lower exchange rate would provide more assistance to the Australian economy in its recovery.” Of course, nobody is going to actually sell AUD on this: the RBA needs to walk the walk rather than mumbling the talk – and it has almost no track record of doing so. However, a journey of 1,000 pips starts with a single step, as they say; and we can see which direction movement will ultimately be in (a lower AUD).

The same can be said for the movement regarding US-China links (away from each other), and for China itself (inwards: it does not attempt to hide what it is doing, after all) – but it cannot be said for either Europe, or the UK.

via ZeroHedge News https://ift.tt/3iEfneQ Tyler Durden

“Effectively Uninsurable”: Tesla Goes Shopping For D&O Insurance, But Forced To Exclude Elon Musk From Policy Tyler Durden

Tue, 09/15/2020 – 08:55

In addition to being the company’s D&O insurance, Elon Musk now appears to be the reason why Tesla can’t get D&O insurance.

Recall, back in April we wrote about (now $300 billion plus) Tesla dropping its D&O insurance and, instead, having Elon Musk personally cover the company.

Now, nearly 6 months later, Tesla is still shopping for D&O insurance but has excluded CEO Elon Musk from its policy, according to Insurance Insider. Tesla is currently “in the market” for a binding quote on a D&O policy with a $100 million aggregate limit, according to the report.

In order to combat the “excessive quotes” the company got in the past (which are what ultimately led Musk to providing insurance to the company personally), the “Marsh JLT Specialty-brokered Tesla policy is currently circulating in the London market” with the one key exemption.

In fact, sources called the CEO “effectively uninsurable” based on his erratic behavior, which notably included a fake $80 billion buyout bid for his company that didn’t exist that ultimately led to allegations of securities fraud with the SEC.

The ironic thing is that Musk is – by far and away – the biggest liability at Tesla. Excluding him from D&O insurance would be akin to excluding arson from fire insurance.

Regardless, D&O insurance is absolutely vital for any public company, but especially for a company that finds itself embroiled in far more controversy and litigation than others. Like a company where the CEO bails out his cousin’s failing solar company. Or a company where the CEO openly and brazenly commits securities fraud on Twitter.

We speculated back in April that nobody wanted to be on the hook for insuring Tesla and it appears we were right; kind of. It appears that no one wants to be on the hook for insuring Musk. But given the company’s massive market cap – which has only grown over the last 5 months – we find it baffling that Tesla doesn’t have the means to pay for insurance including Musk, even if it’s expensive.

Unless, of course, there is simply no offer.

via ZeroHedge News https://ift.tt/35Dyv92 Tyler Durden

Today is the 80th anniversary of the climax of The Battle of Britain. After weeks trying to win air superiority and clobbering 11 Group airfields, the Luftwaffe were given orders to hit London with the biggest raids yet. Far from encountering a few ragtag squadrons cobbled together from the last patched up Spitfires and Hurricanes, London was in range of the RAF reserves held North of London. The RAF’s full force hit the Germans and the Big Wings shot them down in droves.

Later this morning my home village will get a fly-past: the Supermarine Spitfire factory is just down the road, while Hamble’s airfield was the base of the Spitfire-Girls, the Ladies of the Air Transport Auxiliary, who delivered the iconic fighters to RAF bases across the land. There is nothing like the sound of a Merlin engine to brighten up one’s day.

What we remember today is the Blitz spirit, when the whole nation cheerfully rallied to face down the enemy menace. Our resilience then shocked and surprised the world.

As we wake to the news 700,000 UK jobs have been lost to Covid, and redundancies are rising at their fastest rate since 2008, its likely to get worse as the furlough programme ends, and the approaching winter ends our struggling efforts to staycation. Compare and contrast Winston’s rhetoric in 1940 with Boris Johnson’s incoherence today…

I’m sure it’s just a coincidence, but British casualties from the Blitz that followed the Battle of Britain were around 43,000, a not dissimilar number to those who have died from Covid.

The official number of cumulative deaths in the UK ascribed to COVID this morning is 41,637.

That number says little about the human tragedy of each case. It also says nothing about the unidentified excess deaths from the “Big Five” killers that take 150,000 mainly elderly Brits each year. We should shortly be able to work out real excess deaths: how many more dementia sufferers departed early, heart attacks which killed because patients stayed home, cancers missed, respiratory diseases untreated or recorded as Covid, or strokes that missed the golden first hour because hospitals were focused on the disease.

These will be cold statistical numbers. No official data will record the grief, the anxiety, the mental stress the pandemic has raised. It won’t record the social consequences of lockdown or the misery and hopelessness of those who lose their jobs and the financial stresses they face. The markets will tell us all about the long-term economic damage inflicted – rightly or wrongly – on our island.

The numbers won’t record the shattered dreams of young people who make up the bulk of employees in tourism, hospitality and travel who have been most impacted by job losses. That has serious social implications in terms of future votes. It was demonstrating against Margaret Thatcher’s destruction of the Scottish economy in my early 20s that moulded me into the closet lefty I remain today – although I did grow up just enough not to vote for Corbyn last year.

What we will remember long-term about the Pandemic is fear and anxiety, and the apparent confusion in government. The banality of “the rule of six” when we are being told to go back to work is insane. Sound bites don’t make up for stupidity. Resilience has gone out the window. We have become a nation of scared and anxious Corona-nazis encouraged to report our neighbours, or sullen Corona-renegades who want to get the economy moving again and get on with living our lives.

We need Government to be realistic about the Virus. I am seriously wondering if Johnson is up to it. Let’s acknowledge some truths.

The UK has some great statistics on death rates – they are very informative: improved heart-disease treatments have reduced heart-attack deaths since 2000, but that fall has been matched by a rise in deaths from Dementia and Alzheimers. These numbers remind us – death is inevitable. The bulk of Covid deaths have been the elderly and infirm. That’s tragic but the reality is that death comes sooner if you are elderly and have other serious conditions. Covid is an opportunistic predator – it picks the easy targets, the weak and vulnerable just ahead of other conditions.

In younger people the leading cause of death in young men is suicide – 1233 in 2018 compared to only 353 women. That is going to be a key number to watch in coming months. Overall, for all age groups influenza and pneumonia is the leading cause of death (except in Scotland!)

90 people under the age of 30 have died of Covid in the UK. That compares to 434 folk under 30 who died in road traffic accidents. I don’t know how many of these young Covid victims had other underlying conditions.

What we do know for certain is Covid is bad. If you are overweight its likely to be worse. It can take months to recover from the long-term cardio-vascular, gastric, neurological and respiration issues it raises in some patients. Yet the brutal reality remains it is more likely to kill you if you are elderly and have co-morbidities.

Covid is a risk. It’s a virus – like Chickenpox, Measles, Flue, Aids and Herpes. We treat them, cope with them and factor the risk of Shingles or catching Aids into our social decisions. I’m writing this with a painful cold sore on my lip from sailing – risk/reward. There isn’t much we can do to avoid the flue – except quarantine or accept it. We don’t ban people for using private transport because they are 4 times more likely to die that Covid. We acknowledge it’s a risk, a choice and accept the economic and social consequences of 434 young people dying tragic unfulfilled lives

Governments need to be realistic about the Virus and make the risk calculations to inform some tough decisions. Be clear about it. There will be more deaths – but acknowledge they are going to happen. Balance theses against the economic and mental damage being done to the economy. We need to press the resilience button. Now.

It may be too late. Part of the the nation is so scared and traumatised its staying at home.

I am not a herd-immunity or vaccine expert – but it seems pretty clear the reason the numbers are rising are because more people are being tested. That hints the virus is becoming more widespread – but until we all get antibody tests we just don’t know about the health of the herd. But fewer people are dying. The death rate is falling because treatment is better, and more of the people being tested aren’t as susceptible to getting it bad and don’t need hospitalisation. The infections and death rate numbers are increasing in less developed economies less able to cope and still at early stage.

Deaths are well below the forecast levels we were hearing back in March. If we get to 10,000 new cases per day in the UK, but death rates remain low then isn’t it time to reassess the risks? Is it right to close a city because 21 people in 100,000 get it and very few are dying? Would it be better to close the factory that has ignored social distancing and thus allowed the virus to spread like wildfire round workers? You can find the official UK numbers here. Infections are heading back to where they were months ago. Death rates are a fraction of what they were.

And is it right to be wondering if we have herd immunity or pinning our hopes on a vaccine? Probably not. The virus is bad. It kills. But we need to get on and face it. Life is a risk.

Meanwhile… back in la-la-land

The Nikola story is a gas. They filmed a truck but never specifically said it wasn’t actually powering itself. You can’t make it up. But what’s even funnier is its apparently pushed Tesla higher? On the basis there might be far less to Nikola than we were told does that makes Tesla more valuable? If Tesla is vulnerable to competiton, then if you are watching Nikola you are watching the wrong thing.

via ZeroHedge News https://ift.tt/2RvCiwR Tyler Durden

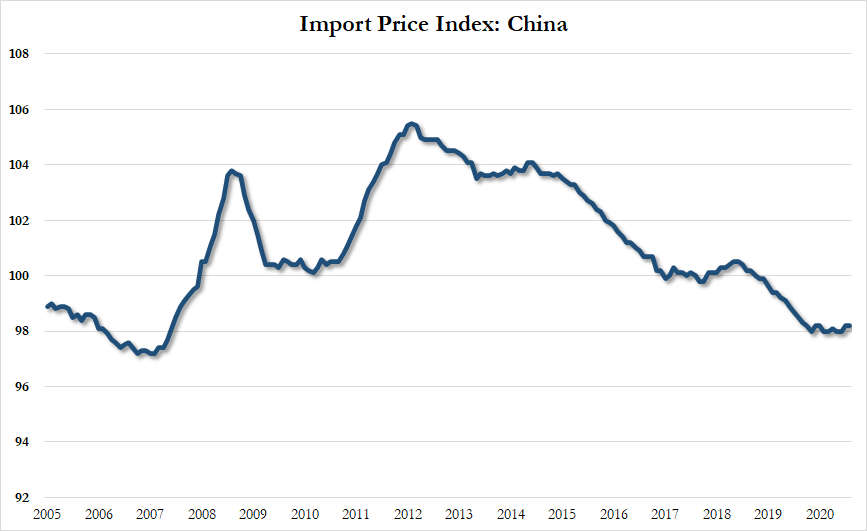

US Import/Export Prices Improve In August, Remain Deflationary YoY Tyler Durden

Tue, 09/15/2020 – 08:35

Despite some v-shaped recovering (with a small ‘v’), US Import and Export YoY prices remain deep in deflationary territory in August.

Import prices rose 0.9% MoM (well above the 0.5% expected) and Export prices rose 0.5% MoM (also better than the +0.4% expected). But despite both the beats, import and export prices remain underwater on a YoY basis.

Source: Bloomberg

However, we note that this deflationary impulse is at odds with the lagged response that is typically seen when China’s credit impulse is expanding so dramatically…

Source: Bloomberg

So either we will see dramatic resurgences in import and export prices or China’s credit impulse is simply filling up an endless bucket of malinvestment domestically… as import prices from China remain stubbornly stuck at 13-year lows…

via ZeroHedge News https://ift.tt/2ZEAUMQ Tyler Durden

You can read it here (just 25 pages); here’s the Introduction:

“No man,” states a venerable common law rule, “should be a judge in his own case.”[1] The impartiality properly demanded of a judge is not possible to those who have a stake in the outcome of the adjudication. According to the United States Supreme Court, this principle is “a mainstay of our system of government.”[2]

For this reason, the law has long required that judges not be parties to the cases they oversee, or closely related to parties in the case, or subject to rewards or penalties based on the outcome of the case. There can be no due process when the one passing judgment is predisposed to judge in favor of one side.

{A case that illustrates the breadth of interest that corrodes due process is Aetna Life Ins. Co. v. Lavoie, 475 U. S. 813 (1986). Although the case arose in the context of judicial disqualification, its holding confirms the general principle that those with a stake in the outcome of a case should not participate in its resolution. In Lavoie, the Alabama Supreme Court issued an unsigned per curiam opinion holding that partial payment by an insurance company did not bar bad-faith suits or punitive damages. Among those joining the majority was Justice Embry, who previously had filed both an individual action and a class action against insurance companies, raising similar issues. When the case reached the United States Supreme Court, the Court held that “Justice Embry’s opinion for the Alabama Supreme Court had the clear and immediate effect of enhancing both the legal status and the settlement value of his own case.” Thus, Justice Embry’s interest in the outcome of the case was “‘direct, personal, substantial, [and] pecuniary,” and he acted as ‘”a judge in his own case.'”}

These rules held well enough until recently, but we believe that it is time to take a broader look at what constitutes impartiality, and due process, in a judicial (and law enforcement) system that increasingly depends on fines, fees, and forfeitures not simply as punishments, but as major sources of operational funds. Inspired by two recent decisions from the United States Court of Appeals, we argue that when everyone participating in the justice system is aware that the system itself depends on sufficient revenue from fines, fees, and forfeitures, that very dependency is a conflict of interest sufficient to violate due process rights.

In this short article, we will look briefly at the history and law of judicial independence, after which we will describe the extent to which the modern judicial system—and, indeed, the entire law enforcement apparatus—depends upon extracting money from a steady stream of individuals who appear before it creating an untenable vested interest in charging and collecting and rendering a fundamentally unfair system. We will then suggest some ways in which the resulting conflict of interest can be remedied. At a time when funding, and defunding, law enforcement is the subject of much debate, it is worth considering the incentives that some sorts of funding can create.

And from the Conclusion:

To operate as legitimate institutions of government, our courts must be freed from serving as revenue centers. If courts are to command respect; if their judgments are to be honored and observed; if, in fact, the most fundamental guarantee of the Constitution is to be valued, then our courts must be funded properly by state revenue. The taint that adheres when courts depend on fines, fees, and forfeitures to operate must be removed and the criminalization of poverty must be permanently eliminated.

from Latest – Reason.com https://ift.tt/2RtXnYo

via IFTTT