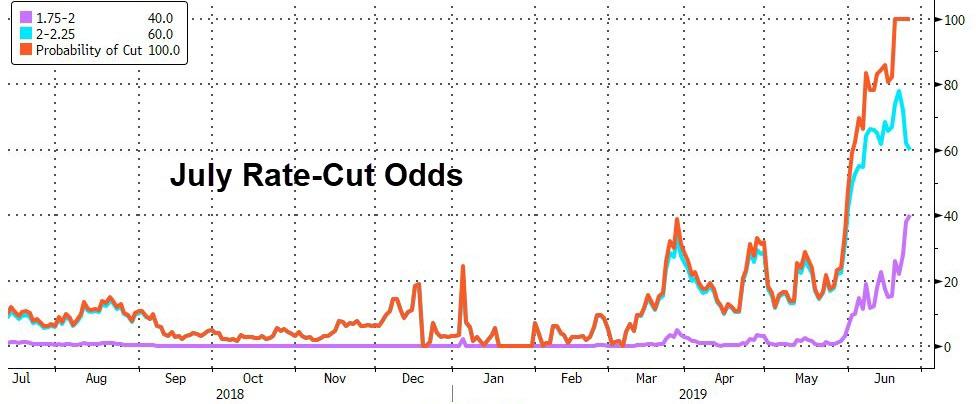

St.Louis Fed President Jim Bullard – and uber-dove – has apparently decide to distance himself from going ‘full-Kashkari’ by noting while “it seems like a good time for an insurance rate-cut,” the situation “doesn’t call for 50bps.”

Unfortunately the market needs moar (40% odds priced in of a 50bps cut)…

And so stocks tumbled to show their disapproval

Don’t worry though, Bullard assures the American public that “he has no immediate concerns about asset bubbles” unlike Kaplan.

Treasury yields spiked…

As did the dollar…

Will The Fed fold even more?

via ZeroHedge News http://bit.ly/2ZMJZRq Tyler Durden

A generation of Wall Street analysts and traders has come of age without many of the esoteric, mortgage-backed bonds and ‘synthetic’ derivatives that nearly destroyed the global economy in the run-up to the financial crisis. But as more financial firms cast about for products that will help pad their revenues as the Fed prepares to embark on its next rate-cutting cycle, products like these synthetic CDOs are being reintroduced as “safer” iterations of their pre-crisis cousins.

In the latest example of this troubling trend, WSJ’s Ben Eisen reported Monday that Cerberus is bringing back bonds entirely backed by home equity lines of credit (or HELOCs) – just in time for a refinancing boom that many expect will be triggered by tumbling mortgage rates.

HELOC-backed bonds disappeared in the aftermath of the crisis as issuance dried up, even as some brazen investors reaped massive profits by scooping up the extant bonds for pennies on the dollar. Yet, this troubling legacy didn’t stop four ratings agencies (including Fitch Ratings) from granting Cerberus’s $174 million issue a triple-A rating, indicating that they are among the safest investments available.

“There has been some caution from issuers” about introducing new types of mortgage bonds, said Grant Bailey, the head of residential mortgage-backed securities at Fitch.

One fund manager described the what’s-old-is-new-again mortgage-backed issues as a “creative” way of taking advantage of a housing market that has been turbocharged by inadequate supply and an army of speculators like ‘house flippers’ (who now count among them a growing number of corporate “iBuyers”).

“We are starting to have a lot more creative issuance around mortgage credit,” said Neil Aggarwal, deputy CIO at Semper Capital Management. “I wouldn’t be surprised if there’s more to follow after this transaction.”

After a bruising May, US equities are on track for one of their best Junes in years. Yet, average home priced appear o have peaked, and even after a decade-long blistering bull run, more than 2 million homeowners are still struggling with mortgages that are ‘underwater’.

But even as investors desperately cast about for yield, the demand for the new Cerberus HELOC-backed bonds was surprisingly muted, WSJ reported, with investors demanding higher-than-expected yields, and largely sticking to the triple-A tranches.

The deal had a yield 1.05 percentage points over the one-month US dollar London interbank offered rate, higher than initial talk of 0.90 percentage point over Libor, investors said. Though the deal was initially structured with multiple portions, only the triple-A-rated tranche ended up being sold, which is relatively common in Cerberus’s mortgage-backed-securities deals.

The market for bonds that pooled exposure to HELOCs – which, unlike traditional mortgages, function much like credit cards backed by the equity in a borrowers home – is still well below the $29 billion peak from 2004.

But with mortgage refis expected to boom, we imagine more firms like Cerberus will seek to cash in on this trend as more buy side firms seek to wrest more facets of a fixed-income trading business that was once dominated by big banks, which have largely been precluded from this part of the market by post-crisis regulations.

So buyers are will be emboldened by sterling credit-ratings (that seem to ignore massive consumer-debt burdens), relatively loose federal oversight and convincing sales pitches advising them that ‘it’s different this time’ and these bonds are far more ‘conservative’ than the offerings from before the crisis.

What could possibly go wrong?

via ZeroHedge News http://bit.ly/2J3Ra0N Tyler Durden

Tesla, from the get-go, has sold itself as a green dream in our era of rapidly-worsening climate change. But there’s a lot about the electric car company that’s more nightmarish than many of its fans or even the California government, which heavily subsidizes Tesla’s operations with hundreds of millions of dollars in tax exemptions and other incentives, would like to admit.

Will Evans, an award-winning journalist with the Center for Investigative Reporting, published a hard-hitting series about Tesla’s flagrant labor violations, exposing Elon Musk’s purportedly progressive business for what it truly is: a green mirage. In the series, Evans reports on the clash between the manufacturing elements of the company and the management that operates like a tech startup, and how this contradiction has created often dangerous conditions for Tesla factory workers. Rather than address these very real issues, however, Musk and his company have chosen to brush them off and hide reports of injuries in order to maintain the illusion its customers buy into when they purchase their luxurious Tesla cars.

“We started looking into Tesla because we were hearing that there was safety problems there, people getting hurt,” Evans tells Truthdig Editor in Chief Robert Scheer in the latest installment of “Scheer Intelligence.”

“It has this great reputation for being this futuristic, forward-thinking, world-saving company that’s going to bring sustainable energy to transportation and revolutionize how we do things. And a lot of people go there because of that.

“What we found was that, under pressure to meet its production goals, it was really leaving safety, worker safety, by the wayside, and had prioritized cranking out cars as fast as possible, and left its workers dealing with all kinds of serious injuries. And then was actually trying to hide those injuries in order to make its safety record look better.”

The revelations should have jolted Musk and California officials to take a deeper look into the company’s operations, but quite the opposite took place. While state officials did in fact grill Tesla after the investigative reports were published, according to Evans, they are mostly afraid regulating the company could push Tesla—with its factory and the jobs it creates—out of the state. As for the CEO, he had a response that anyone reading any newsabout the arrogant tech baron might expect.

“The company and its supporters, and Elon, sees this all as sort of an attack on him and on the company—that people want to see it fail,” Evans tells Scheer. “[Tesla] went as far as to say that [the Center for Investigative Reporting” is] an extremist organization … working on a disinformation campaign. [Musk] went on to attack journalists in general for being beholden to the fossil fuel industry because of advertisements, and gthat that’s why journalists are out to get Tesla.

“When someone pointed out that, hey, over here at the Center for Investigative Reporting we don’t even have advertisements, we’re a nonprofit, he went on Twitter and he called us just a bunch of rich kids from Berkeley who took their political science professor too seriously. That was his diss.”

Scheer points out how stories about Tesla aren’t so different from other troubling stories coming out of Silicon Valley.

“These companies have escaped serious regulation—antitrust, [accountability, occupational standards],” says the Truthdig editor in chief.

“We’ve kind of anointed these new industrialists as somehow prophets of a future, whether it’s at Apple or Google or Tesla or Facebook. They’ve got the magic wand; they know where it’s all headed. What you have in Elon Musk is sort of the poster boy for that arrogance. He just shrugged it off. You could do investigative reporting, you had the facts, it’s solid as can be—and they just don’t have to care, because they’re the wave of the future, right?”

Listen to the full discussion between Scheer and Evans as they talk about the wider issue with Silicon Valley and green washing, as well as the hypocrisy behind tech barons’ libertarian approach to government. You can also read a transcript of the interview below the media player and find past episodes of “Scheer Intelligence” here.

* * *

Robert Scheer: Hi, this is Robert Scheer with another edition of “Scheer Intelligence,” where the intelligence comes from my guests. In this case, it’s Will Evans, a highly regarded investigative reporter with Reveal, which is basically a radio investigative program carried on, I think, 450 stations. And it’s part of the Center for Investigative [Reporting] in Emeryville, California, which has filled in for the void left by the weakening of mainstream newspapers and news organizations, and does terrific work. And what Will Evans does, and what I want to talk to him about, is basically he’s looked into the sausage of internet life and how that sausage is made. He evaluated Uber and got all sorts of prizes for it, and the question of Silicon Valley’s discrimination against different categories of employees. And the one that’s gotten the most recent attention is he dared to look into the inner workings of Tesla, the electric car company that has been celebrated widely. And found, you know what, it ain’t that different than horrible working conditions at lots of assembly-line businesses, no matter how nouveau the product. So why don’t you really tell us what you found in this investigative series?

Will Evans: Sure, thanks for having me on here, appreciate that. We started looking into Tesla because we were hearing that there was safety problems there, people getting hurt. And it had this, as you say, it has this great reputation for being this futuristic, forward-thinking, world-saving company that’s going to, you know, bring sustainable energy to transportation and revolutionize how we do things. And a lot of people go there because of that. And what we found was that, under pressure to meet its production goals, it was really leaving safety, worker safety, by the wayside, and had prioritized cranking out cars as fast as possible, and left its workers dealing with all kinds of serious injuries. And then was actually trying to hide those injuries in order to make its safety record look better.

RS: You know, in a way, this sort of investigative series that you’re doing, and other people at the Center for Investigative [Reporting], really goes to the heart of how do we make things these days. And how does Apple make iPhones in China, and are people paid, what, two bucks an hour, or less or more, and what are the working conditions? And people are so enamored with the product, the slickness, the style. Tesla cars, you know, came in as high product, high quality and very expensive. They don’t want to look under the hood; they don’t want to look at how the sausage is made. And so give us the specifics. Because reading your series, it’s a guy gets his back busted when the, trying to assemble a car, or all sorts of bad products are consumed; paint destroys their health, and what have you. And we forget, it’s still–yes, robots are involved, but there are still human beings out there popping in and out of cars as they’re moving down an assembly line. And it has a lot of the downside of traditional manufacturing, and actually you pointed out Tesla had a worse record than the industry standard.

WE: Yeah, and what you see is, you know, all the–in manufacturing, you have a ton of manual labor, and a lot of heavy machinery and dangerous, potentially dangerous conditions. And a lot of, thousands of people working in that factory. And then you have the tech company operating almost like a startup that’s going very fast, growing very fast, changing things on the fly, as if it were as easy as to change some software. And you end up, those two things clash with each other, and people start getting hurt. And yeah, exactly, you have the guy who has the trunk of a Model X Tesla fall on his back when he’s inside, and he ends up getting sent back to work; you know, they tell him to just go back to work, he can barely walk. You have people, everything from getting your finger cut off, or they had an incident where people were sprayed with molten metal, electric explosions that burned people, breathing toxic fumes from chemical fires or from paint and adhesives, to just a lot of repetitive injuries.

RS: So you know, really what we’re talking about is a glamour industry of Silicon Valley in which very often they don’t even make money, but there’s a lot of venture capital goes into that. And then to justify it, they have to cut corners and squeeze. And in Tesla’s case, they’ve raised a lot of money, they’ve spent a lot of money, and they haven’t made a lot in the way of profits, and they’ve missed their production schedules. And so in a way, you have an old-fashioned assembly line speed-up, don’t you? Trying to get these workers to work harder, when in fact the conditions are not good. And then you rig the system: you have an in-house medical system that, as you documented, is involved in sort of cover-up and corruption of these injuries. Workers are not sent to care that they’re entitled to under workers’ comp. And then finally, a very aggressive medical practitioner, doctor, takes over this business, and he becomes complicit with their profit motives, rather than the health of the workers. Does that sort of summarize what you found?

WE: Yeah, that’s a good summary. I mean, I think they are under the gun to produce these incredible production goals that–I mean, it’s very difficult to meet those.

RS: You can say his name, you can say the name of the man who keeps promoting it.

WE: [Laughs] Well, right, so Elon Musk, right? He’s making a lot of promises, he’s got a lot riding on it. It’s a tremendously valuable company that’s not had a great record at actually making a profit, and has missed goal after goal after goal. And so, yeah, his future is riding on this, the future of the company is riding on this, and the answer has been to just work the hell out of these workers, and do things so fast that precautions aren’t being taken. And safety is not going to get in the way of something that–that’s what, we would talk to these safety professionals who worked in the factory, and they’re hired by Tesla to evaluate the–why people are getting hurt, and try to solve that. And they would come up with these fixes or make these warnings, and say hey, look, someone’s going to get really hurt, someone’s going to die. And they were told again and again that, look, we need to do this this way, Elon wants it, we need to keep the cars moving. And some of them left in disgust, and some of them were fired after raising concerns over and over again. And so, and these are people who, some of them come to Tesla because they really believe in the vision, and believe in Elon Musk. And then they’re disillusioned when they see, on the factory floor, people getting hurt in the name of progress.

RS: So really what it’s about is hype. And these events go unexamined. I mean, why did it remain for you to do this kind of investigation? You got wind of these things, but basically these people were rigging or undermining a system that is supposed to protect workers. If you’re injured, it’s supposed to be reported; you’re supposed to get treatment, right? You’re supposed to–what’d they do? They send people in a Lyft or an Uber to get care?

WE: [Laughs] Right, to the emergency room.

RS: And really, cover up–the whole thing reeks of kind of just old-fashioned cover up, you know. And yet using professionals, doctors and others, to look the other way. And the few people who object, the whistleblowers, they end up getting fired.

WE: Yeah. I mean that, I think that’s why it is hard to unearth this stuff, and some companies get away with it, is because the people who know what’s going on are very fearful that they will, their careers will be ruined if they speak up, that they’ll be sued. I mean, Tesla is very aggressive against whistleblowers. The people who worked for the medical clinic that I talked to have faced threats of legal action; they’ve been reported to the medical board; various forms of retaliation, really, for speaking up about what they saw. And many of them don’t want to talk at all–or will say I’ll talk, but don’t use my name. And so you need to find–you know, I need to find, like, those few courageous individuals who were so upset at what was going on that they’re just willing to risk it. That’s how you know that it really is extreme and serious, where you’d have this medical clinic that was seemingly designed to avoid having any record of these injuries, and a doctor who is operating under a lot of pressure to keep these injuries dismissed, or off the books, or not on workers’ comp. And you have this profit motive driving that. And a lot of people are afraid of both that doctor, they’re afraid of Elon Musk, they’re afraid of the power of Tesla. And so it’s hard to get that out.

RS: And they’re also afraid that it’s a lousy job market for good-paying jobs. You know, we have a lot of young people graduating now, getting out there in the field, and they can’t find–and here you have a glamour job. But let me ask you something about an old-fashioned check and balance that we used to have with labor unions. And that’s sort of not dealt with extensively in your articles, but there is a sort of subtext of keeping a strong union out. Now, it used to be if you were on the Ford assembly line, or General Motors or something, you had shop stewards; you had people, and if somebody was injured, they’d go to their shop steward and say, hey, you know, I just busted my arm, I got to go to emergency, they don’t want to send me. There was a check on the power of the people running the factory. Here, Elon Musk, according to your article, was able to say I don’t want yellow caution tape used around the scene of an accident, because it’s depressing. How do you get that kind of power? What kind of union, what kind of check and balance do they have within the Tesla plant?

WE: Well, so there is no union. That’s the short answer. The UAW was trying to organize, and the company was, fought that effort. And the union has claimed that a lot of its supporters were let go under the guise of layoffs and firings for, you know, production reasons. And then you have, I think there’s still some pending labor relations complaints in terms of how the company dealt with that. But the bottom line is that there is no union. The company and its supporters, and Elon, sees this all as sort of an attack on him and on the company, that people want to see it fail. He argues that, you know, the unionized plants don’t have better records for their workers, and that workers would be worse off with the union. And so far has gotten away with that, and has used the union as this sort of bogeyman–they tried to attack our reporting by saying it was part of some coordinated attack with the union. Which, I mean, we had nothing to do with that, but it’s a convenient excuse. They went as far as to say that we were an extremist organization when we came out with that first piece.

RS: “We” being the Center for Investigative Reporting?

WE: That’s right, yeah. They called Reveal an extremist organization.

RS: OK–

WE: –working on a disinformation campaign. And then another point, he went on to attack journalists in general for being beholden to the fossil fuel industry because of advertisements, and that that’s why journalists are out to get Tesla. And there’s this sort of a complex of, like, that they’re being persecuted. And when someone pointed out that, hey, over here at the Center for Investigative Reporting we don’t even have advertisements, we’re a nonprofit, he went on Twitter and he called us just a bunch of rich kids from Berkeley who took their political science professor too seriously. That was his diss. [Laughs]

RS: So let me–I mean, I want to get at that. Because there’s an aspect of this that relates to green washing, PR, how you spin. And this is not the old Ford company, Henry Ford, and you know, he’ll break the union and call the National Guard out and have his own police force and so forth–no! These people are on the side of enlightenment. And in the enlightened state of California, which is supposed to be deep blue, and you have these progressive governors like Jerry Brown was there during this critical period–the question I want to ask, we’re going to take a break for a minute, but when I come back with Will Evans from the Center for Investigative Reporting, the Reveal series, you can get this on their website. But basically, this is not happening in the Deep South with runaway shops, you know. This is happening in California. And what about all the laws that exist to protect workers when they’re injured, and their rights, and so forth? [omission for station break] I’m back with Will Evans, and we’re talking about his incredible series, really, on how the sausage is made in Silicon Valley. In this case we’re talking about Tesla cars; they’re shiny, they’re wonderful, people like looking at them, they’re expensive, now there’s actually one that’s more reasonably priced. And as with Apple phones, as with all of these products from the new tech industry, they’re not examined very carefully. And when you read this series you understand, no, people get their backs broken, they inhale dangerous fumes, all sorts of bad stuff happens, and it’s covered up. So I want to ask you, what about the state? The state of California has been very pro-electric car. And they actually have given Tesla, through various breaks and so forth, in one of your articles I think it said a $200 million state subsidy. And there’s also federal subsidy. So this is not just free enterprise doing what it has to do; this is a highly subsidized government entity, on the one hand, and yet government is not doing its due diligence of protecting workers in these plants in terms of occupational health and safety. Is that not a big contradiction?

WE: Yeah, there’s a couple of things working here. One is the focus in California on combating climate change and wanting to incentivize sustainable energy, and having these programs to provide tax exemptions to encourage that. They’re using a lot of–you know, Tesla’s the biggest recipient of these tax exemptions. And it’s because it’s like the–you know, it’s this huge hope for electric transportation. And so I think there’s a reluctance to turn that off, because of what it means for–what it promises for sustainable energy, but also in terms of what it promises for jobs. It’s the only car maker here in the state; it provides a lot of jobs. And so it has a lot of support, and powerful support, because of that. And people don’t want to see it leave, and they don’t want to see it go to another state or country. And so you might see a little bit of a lighter touch there. You also have the issue of worker protections, in terms of health and safety protections. They’re not all that strong, here or anywhere else in the country, in terms of how much you get fined for a–you know, when a worker dies, or gets maimed, and it’s deemed the company’s fault and a safety violation. I mean, these are–at most, you’re talking about like over $100,000, or maybe you get tens of thousands of dollars. Maybe you get much less than that, and then it gets reduced because of other, you know, in settlement negotiations. And that’s just not enough to change a company’s practices, I don’t think.

RS: You know, there’s a kind of a, there’s an important cultural critique in your articles. This is a very important series on Tesla, but in the other articles that I’ve read by you, whether it’s Uber or just generally in Silicon Valley, there’s a conceit that they are enlightened. They’re not like the old, industrial barons, and they’re not the people who do strip mining and so forth. That they’re on the side of the angels. So when a lot of, when people were jumping, workers in China jumping out of the window of their dormitories and so forth in desperation, and when we read about the low salaries paid for most of these shiny gadgets–people love the Tesla, and you give fairly wealthy people a tax break to buy one. And let me just, full confession, I own an electric car. I even own a Chevy Bolt, I hope the working–maybe you should tell me about the working conditions, better there, do they still have some check and balance of unions? I don’t know. But the fact is, we’re intrigued–we have an aura of progress, and yet they’re these shiny toys, and we–it’s too good to check. We really don’t want to know how they’re made. Isn’t it–and the reaction to your series was not one that brought about major change or scrutiny. They kind of shrugged it off. And they attacked, they shot the messenger; they attacked you for doing the series, the Tesla folks.

WE: That’s true, and there’s a lot of Tesla supporters, and I don’t think this is unique to Tesla, although I think there is more of a sort of cult following and a belief in the inherent wonderfulness of its leader. But there is a lot of people who just don’t want to hear any criticism, and who see any criticism as an attack, and a cynical attack, and something that is trying–you know, from the forces of darkness that are trying to undermine this great, progressive company that’s going to, you know. And it’s certainly not the only Silicon Valley company that says it’s doing good. So I think it is interesting, and representative in some ways of these, the image, the sleek image of do-gooder companies with an underside that no one wants to hear about. I think you’re right about that.

RS: Well, and it’s also the modern economy. I mean, you know, this is how things are going to be made, and if you don’t like–if the company says well, you’re enforcing these–like you say, they’re afraid in California they’ll take the company elsewhere. They’ll take it overseas, and they’ll find a [workforce], they’ll find governments that look the other way. And that’s really the challenge here. No one denies that we should move to a different kind of transportation, and that electric cars are critical to that. And you can even applaud the effort put into that by different engineering groups, and what have you. But at the end of the day, your description is one that–I wouldn’t say quite comes out of Dickens [Laughter]. But it’s certainly, I mean, people get their bodies destroyed, and they’re told to what, take a Lyft or an Uber and go check it out, and it’s got nothing to do with us, and the government looks the other way? The same government that, I mean, the figure you used I think was $200 million California has given in subsidies? And that government says we’ll subsidize you, but we don’t really care how you make this thing, and the working conditions, and so forth? I mean, that–that’s a prescription for disaster if that becomes the norm in production. And Silicon Valley is certainly the trend center.

WE: Yeah, I mean, I think there’s a–there’s probably people who think that, well, it’s better, even with the current conditions, it’s probably better that it’s being produced here in California than in China. So, you know, and these jobs do pay, and are seen as good jobs by many in the Central Valley. But that’s like only a good job until you get hurt and can’t work anymore, and you end up losing, sleeping in your car, as one of our, one of the people we talked to, had happened to him. I mean, it’s–you know, some people love it, but then, yeah, if you get destroyed by it, that–it’s not worth it.

RS: Well you know, just as a final point, we’ve kind of anointed these new industrialists as somehow prophets of a future, you know, whether it’s at Apple or Google or Tesla or Facebook. They’ve got the magic wand; they know where it’s all headed. And now, there’s sort of, there’s a pushback even from those same people. Tim Cook at Apple, for instance, has said look, we can’t exploit privacy, and we have to care about individual freedom, and we’re going too far. And what you have in Elon Musk is sort of the poster boy for that arrogance. He just shrugged it off. You could do investigative reporting, you had the facts, it’s solid as can be–and they just don’t have to care, because they’re the wave of the future, right?

WE: [Laughs] Yeah, I mean, he not only shrugged it off, but said it just wasn’t true. Said we were, you know, just basically lying, and that’s all. You know [Laughs], there was no, sort of–you know, you’re right, we could do better; it was just, ah, these guys are just lying, and don’t pay any attention to that. And that is scary. That is a scary thing, where there are so many people who are just willing to believe whatever he says on any subject. And I think it is a lesson for, you know, don’t believe the hype, for a lot of these tech leaders.

RS: Well, let me ask you a question structurally about the news business. You were honored by the Investigative Reporters and Editors with an award; your work is highly regarded. So in this case, the character assassination–attacking you, and challenging your motives–didn’t quite work. But I think what you do at Reveal, you know, goes out very wide. I know in fact the station that I’m doing this for, KCRW, carries Reveal; most of the NPR stations do. I think the figure is like 450 or something stations carry it. Do people care? Or is this just, you know, OK, nice, glad you called attention to it, but I want one of those shiny objects and I really don’t care how my iPhone is made or how my electric car is made. Is that what you’re getting?

WE: I think, I actually think there’s a lot of people who care. I don’t know how to measure it, but there was a lot of interest in this story. You know, a lot of pickup, a lot of other publications, a lot of people wrote in. There–it’s partly because it’s one of those companies that is fascinating, and that people are paying attention to, and does represent in some way the future. And so even people who don’t, who aren’t in the market to buy a Tesla, are kind of intrigued and interested in it. And there was–I mean, I definitely hear from people who are upset about this, and who have had their opinions changed, either by this in conjunction with other stories, but just sort of–they have come around to the idea that maybe, maybe some of these tech leaders–and you see it with Facebook, too, right? They’ve had their bubble pierced. You know, that these tech leaders are no longer, should no longer be seen as invincible or that they can’t do, that they can do no wrong. I think that they’re, that people are sort of waking up to the idea that there are problems with even companies that you want to believe in.

RS: So that leaves us, finally, with the big idea that I got out of your series. And it’s not the only place, as you say, with the Facebook controversy now; with the, you know, controversy about how Google uses our data. But it goes to a larger question. These companies have escaped serious regulation–antitrust, you know; accountability. Whether it’s occupational standards on a state level, tax subsidies, communities have fallen all over themselves to attract these companies, and so forth. And there are two questions to raise about it. First of all, who’s going to buy these products if they’re not able to make a decent living, or if they’re not able to sustain their life, or they sacrifice their bodies to make it? I mean, what world are you creating? But also, they have actually, out of a kind of a libertarian ideology, denied the value of government. Assumed that government is something just old-fashioned, and regulation just gets in the way of progress. And yet, as you point out in your articles, without government subsidy we wouldn’t have had Tesla move to this point. And in fact, companies like Google came out of defense department research and, you know, a lot of government funding. And you really, at the end of the day, came up against the basic contradiction for Silicon Valley: is this thing too shiny, a distraction from the reality of life, of how things are produced, how people make a living, and how they can survive.

WE: Well, I think you hit on something that I think is interesting for a lot of the Silicon Valley industry, which is this idea that they’re–you know, it’s a cliché now, but that they’re disrupting this, and revolutionizing that. And a lot of it is new, and this disruption and this sort of “we’re breaking the rules” is seen as a good thing, and a driver of innovation. And the only way that many of these companies–Uber, or whatever it is–can, made it in the first place, and can survive, is by breaking a lot of rules. And some of those rules maybe we’re OK with breaking. And then when you start breaking labor regulations and things like that, then you know, are we still OK with it? I don’t know. And how do you regulate it? Now, when it’s something where you’re talking about gig workers, who aren’t, don’t have minimum wage or all kinds of other protections, or when you’re talking about autonomous vehicles, how do you, what do you do with that? When you’re talking about the tremendous power that Facebook has, that’s something we haven’t dealt with before. And I think there’s probably a lot of grappling that needs to be done with that. But in the meantime, if you’re an entrepreneur, you’re thinking, like, I need to break things in order to succeed. And so the more things that get broken, you might see some troubling things come out sooner or later.

RS: And we seem to be on the cusp of that now, because actually there is, you know, the Federal Trade Commission is–there’s a lot of movement to take a second look at how these companies operate. And some–as I say, Tim Cook is one–have even suggested maybe that’s a good thing. So why don’t we leave it at that–maybe the long-run impact of this kind of reporting will be quite beneficial, hope so. If people want to follow this article, they should go to the Center for Investigative Reporting. What’s the quickest way to get it? Go to Reveal, CIR?

WE: Yeah, RevealNews.org.

RS: OK. RevealNews.org. Thanks again, Will Evans. And our producer for “Scheer Intelligence” is Joshua Scheer. Our engineers at KCRW are Mario Diaz and Kat Yore. Sebastian Grubaugh here at the USC Annenberg School for Communication and Journalism provided another exemplary engineering effort. See you next week with another edition of “Scheer Intelligence.”

via ZeroHedge News http://bit.ly/2xexEJm Tyler Durden

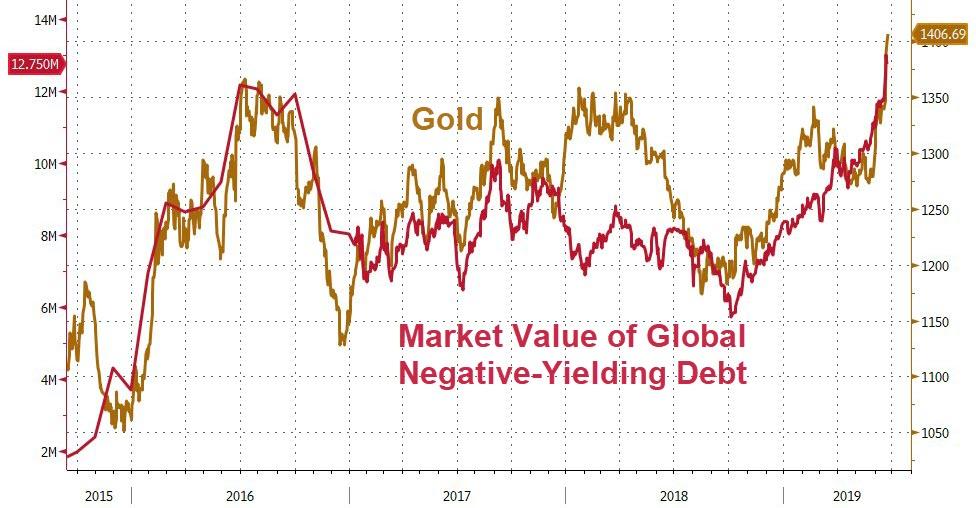

Having tested $1300 numerous times over the past few years, gold has broken dramatically higher in the last month, hitting 6-year highs as President Trump rhetoric around the world raises tensions and increases the odds of WWIII.

The surge in the precious metal has accompanied a collapse in bond yields around the world and a record level of negative-yielding debt…

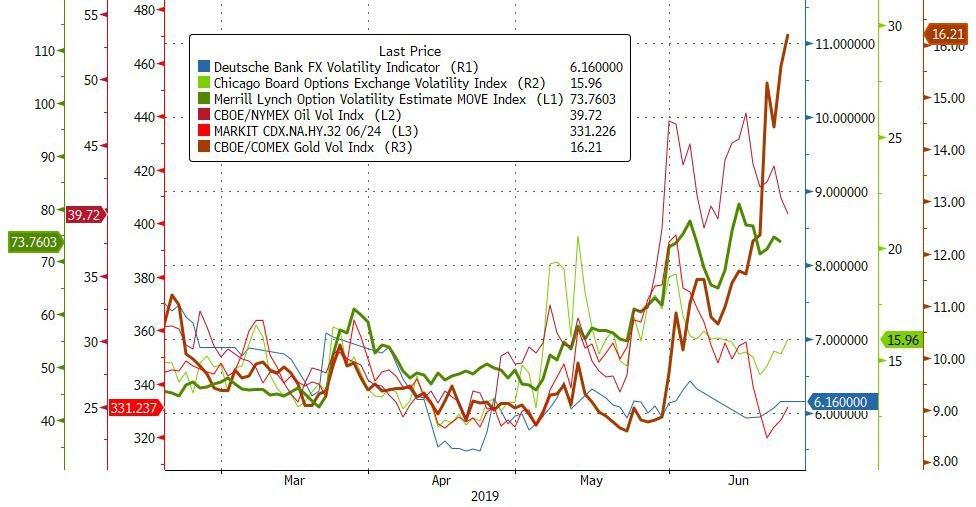

And while Gold volatility is soaring…

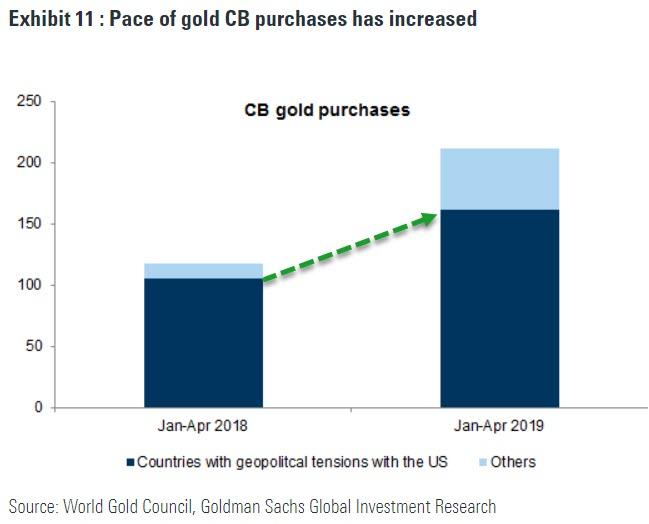

Demand remains abundant, as Goldman details in its latest note, raising its outlook for gold, countries with “geopolitical tensions with the US” are buying everything:

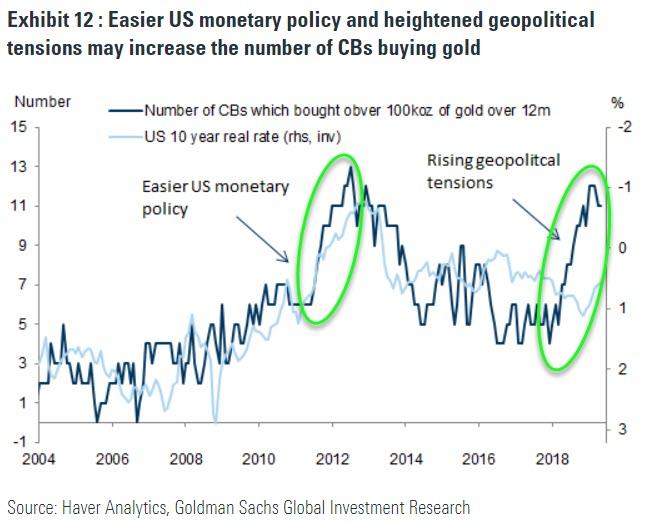

Central bank demand is gaining momentum and we now expect 2019 purchases to reach 750 tonnes vs 650 tonnes last year. Visible gold purchases YTD are running at 211 tonnes until April vs 117 tonnes over the same period last year (see Exhibit 11).

Importantly, China just raised its gold purchasing pace from 10 tonnes per month to 15 tonnes for April and May as it aims to diversify its reserve holdings.

With the Fed and ECB now both likely easing monetary policy, more CBs may decide to add gold to their portfolios as they did between 2008 and 2012 (see Exhibit 12).

Also, just recently, trade tensions between India and the US have begun to escalate as India retaliated with tariffs on US goods in response to US steel tariffs. Rising tensions with the US often create upside potential to a country’s gold purchases

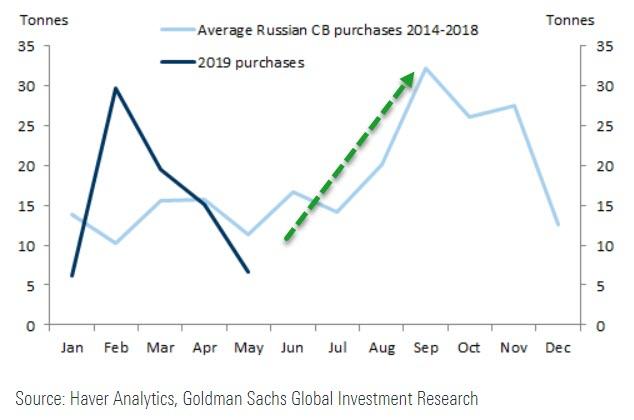

Additionally, in case you thought the move was exhausted, Goldman notes that there is about to a pick up in demand as Russia purchases tend to be strongest in Q3…

And finally, Goldman notes that good economic news and bad economic news could both be positive for the precious metal at this point in the cycle.

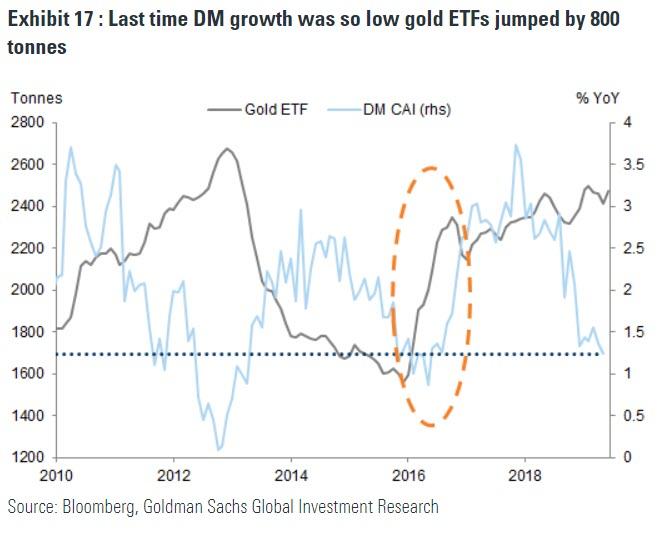

If DM growth fails to pick up in the second half, gold has substantial upside potential

If DM growth continues to underperform, there is room for a much more substantial build in ETF positions. Last time we were in a similar environment was in 2016. DM growth back then was as weak as it is now and both the Fed and the ECB turned more dovish.

But back then the push into ETFs was significantly higher than it is currently… we think that current low growth makes owning gold appealing from a diversification perspective.

And Goldman notes that an improvement in global economic growth is not necessarily bearish for gold.

Our economists expect the bulk of the acceleration in GDP growth to come from ex-US and EM countries in particular. This should support gold through the “wealth” channel. Importantly, a reduced US growth outperformance points to a weakening of the dollar, which should boost the dollar purchasing power of the world ex-US (see Exhibit 7). In addition to this, gold is starting to build momentum in the local currencies of its two biggest consumers, India and China.

And the momentum gold prices built in the first half of 2019 can lead to an increase in EM retail gold demand in the second half.

Goldman concludes, we believe that gold continues to offer significant diversification value with substantial upside if DM growth continues to underperform… or, as we noted above, global tensions continue to rise.

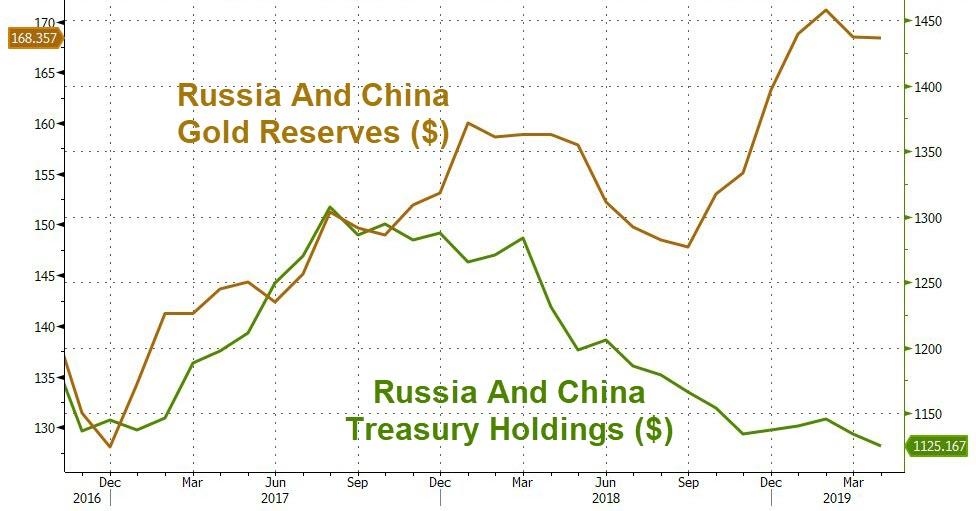

As we noted previously,combined Russia and China Treasury holdings are at their lowest since June 2010 as China and Russia’s gold holdings have soared…

De-dollarization?

via ZeroHedge News http://bit.ly/2FxoJHL Tyler Durden

In lieu of his traditional morning commentary, and while preparing for the key meeting this week, Nomura’s derivatives guru decided to pass-along a few charts “which capture the current market zeitgeist” along with the conclusion that the overall “output still speaks to the investors positioned for the end-of-cycle “Slow-flation” narrative: Long Global DM Bonds / Rates, Under-positioned for Equities rally and now tilting “Short Dollar” via tactical Longs developing in Gold, Commods and even Bitcoin.”

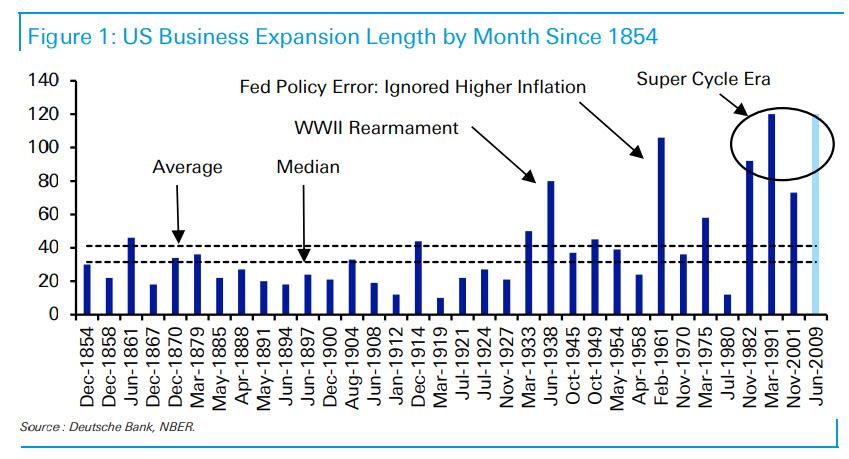

Of course, with the US economic expansion just 6 days away from being the longest on record (unless the NBER decides in the next few months that the recession started some time in Q2), it is not difficult to see why end-cycle trades dominate – both on Wall Street and the Fed, which is doing everything in its power to extend the weakest recovery on record my at least a few months, even if it is kicking and screaming.

So, without furhter ado, here are – as McElligott calls them – the goods:

1. Bitcoin: bitcoin is a play on escaping “negative yielding debt”, as global central banks tilt back to “easing” and currency devaluation in 2019.

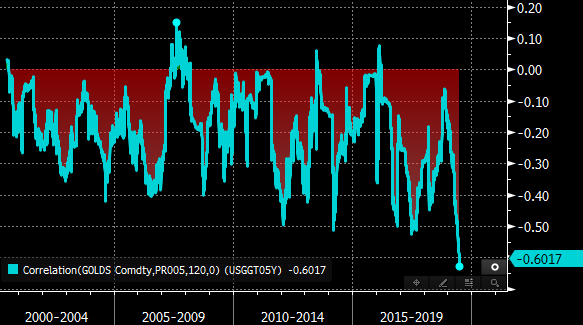

2. Gold: this best way to “short the USD” is the most inversely-correlated asset to US short-term real yields in the past 20 years.

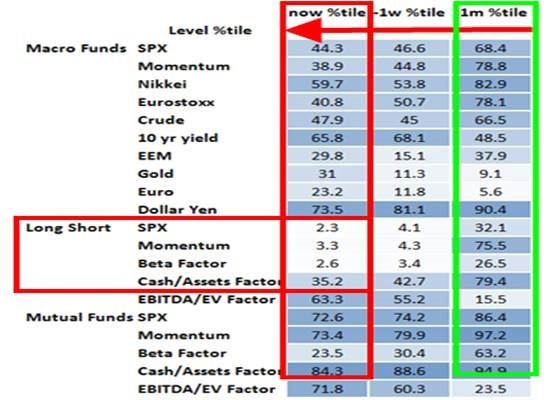

3. Fund Performance: Performance beta across assets/factors shows continued de-risking into the 1 Month move higher from macro, equities L/S and mutual funds (percentiles since 2003).

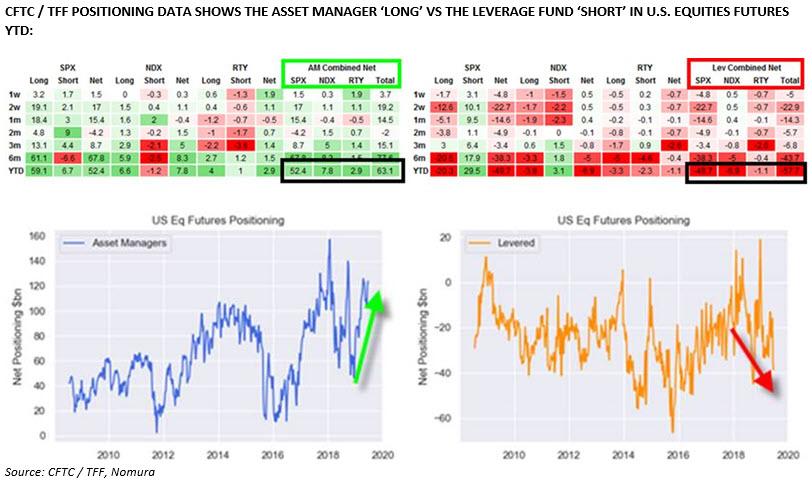

4. Positioning: The latest CFTC data shows asset manager “long” vs leverage fund “short” in US equity futures YTD:

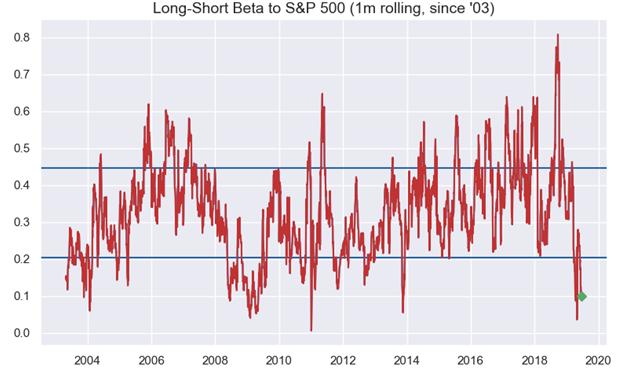

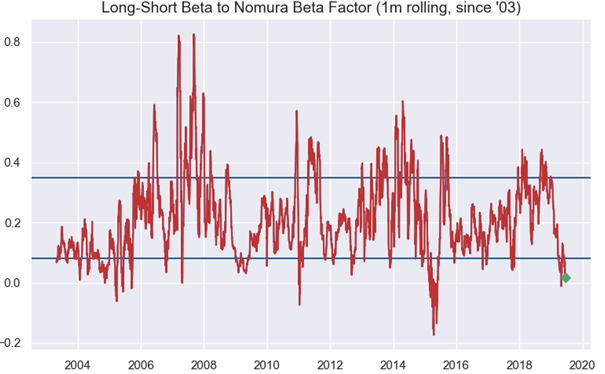

5. Hedge fund faith in stocks (or lack thereof): The equity long/short hedge-fund universe “beta to the S&P” is testing multi-year lows, in the 2.3% percentile since 2003 as nobody believes this fake rally.

It’s just “beta to the market”, but also “beta to the beta factor” which is at 2015 lows, as a red on “long defensives/low vol”, and “short cyclicals/value.”

6. “Slowflation“: For those seeking the expression of “slowflation” in equities, look no further than “long defensives” and “secular growth” against underweight “cyclicals”, a relationship that has caused funds great pain in recent months.

7. Factor exposure: US stocks factor behavior is indicative of the same as per 1Y performance of “growth”, “momentum” and “quality/high cash” versus “value” and various “high beta” risk factors:

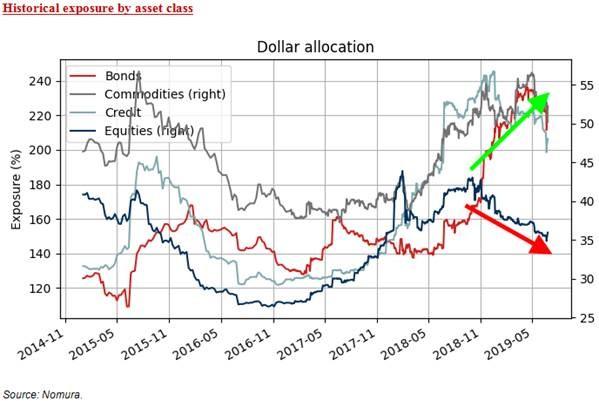

8. Risk-Impairity: Nomura quants’ risk-parity model allocation shows extent of govt bond allocation (leverage deployment) against the ongoing reduction in equities exposure as the outlier.

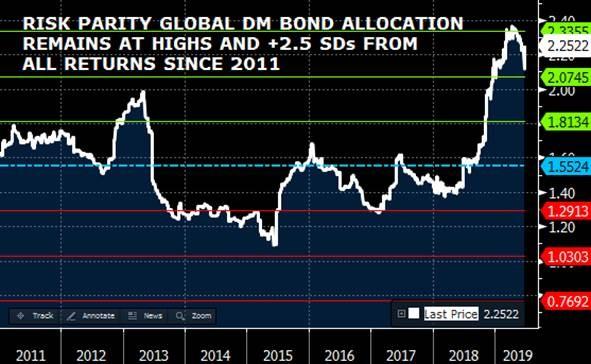

9. Duration im-parity: Nomura’s risk-parity model shows that gross-exposure to global DM bonds remains near new highs since 2011.

10. Risk Pars don’t like equity risk: While risk parity funds are all ine DM bonds, they seem loathe to go heavy into us stocks, as the following chart shows: risk-par exposure to US equities is at a 28 month low.

via ZeroHedge News http://bit.ly/2X4aUpS Tyler Durden

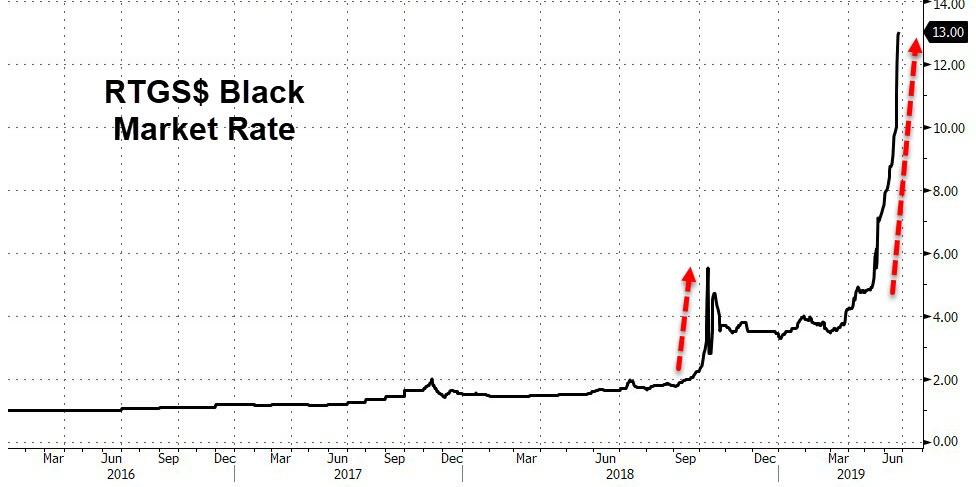

After a decade of dollarization to escape from the hyperinflationary hell of Mugabe’s money-printing, Zimbabwe has implicitly re-introduced the ZimDollar as the nation’s sole legal tender – banning the use of currencies such as the USDollar and South African Rand in favor of its so-called RTGS dollar.

As a reminder, Zimbabwe abandoned its own dollar in 2009 after years of hyperinflation had destroyed trust in the local unit, but, after a hoped-for economic turnaround, promised by new Zimbabwean President Emmerson Mnangagwa, is yet to materialise,

As Reuters reports, Finance Minister Mthuli Ncube said in a video posted on Twitter

“The march towards full currency reform is part of our transitional stabilisation programme…This move is really beginning to restore full monetary policy.”

Additionally, the central bank also hiked its overnight lending rate to 50% from 15% as a part of a set of measures to protect the RTGS dollar introduced in February.

Jee-A Van Der Linde, an economist at South Africa-based NKC African Economics warned that banning the use of currencies such as the U.S. dollar and South African rand could create panic since Zimbabwe did not have large foreign-currency reserves to back the RTGS dollar. There was nothing standing in the way of the Zimbabwean central bank printing money as it had done in the past, he added.

Van Der Linde is not alone in his skepticism, as TechZim reports, local audit firm, Grant Thornton has provided a Commentary of yesterday’s reintroduction of the Zimbabwean Dollar which noted some inadequacies. With the introduction of SI 142 of 2019, and reading between the lines below are some of our comments with regards to the SI:

a) The instrument has all hallmarks of a hastily concocted measure to stop the downward spiral of the RTGS dollar against other currencies. Whether it will have any such effect remains to be seen.

b) Challenges in companies to restock – we envisage that with no foreign currency earnings and obtaining them on the legal market still an issue to be addressed, there is bound to be challenges for companies to restock especially if the current inventory was acquired in USD. This might, at the end of the day, lead to empty shelves and massive job cuts as companies try to streamline their costs.

c) No mention of penalties for those trading in foreign currency – the SI does not state any repercussions on companies who continue to trade in foreign currency.

d) No law prohibiting sale of goods/services or drafting of contracts in foreign currency– there is no law in Zimbabwe that requires prices to be marked up in legal tender or accounts to be drawn up in legal tender. Similarly, if parties agree that a debt should be repaid in foreign currency, then the debtor is obliged to do so. The reason being there is no law in Zimbabwe which invalidates a contract that stipulates payment must be made in foreign currency.

The RTGS dollar has been hitting new lows on the black market in recent days, and as Reuters adds,inflation raced to 97.85% in May, eroding salaries and savings and causing Zimbabweans to fear a return to the hyperinflation era a decade ago.

Banning the use of foreign currency and introducing Zim dollar is a desperate move to stop re-dollarisation, anyway they will not succeed. There is no incentive to continue selling with the dead currency, sooner or later goods will vanish from shops.

All they have done is to wakeup with the OLD & failed bondcoins, bondnote & RTGS$ as the NEW previously failed currency called the Zimbabwe Dollar. You will not find a legitimate government anywhere in the civilised & democratic world engaging in such crude currency racketeering! https://t.co/VpgsJzLIBU

Fracking has been an “unmitigated disaster” for shale companies themselves, according to a prominent former shale executive.

“The shale gas revolution has frankly been an unmitigated disaster for any buy-and-hold investor in the shale gas industry with very few limited exceptions,” Steve Schlotterbeck, former chief executive of EQT, a shale gas giant, said at a petrochemicals conference in Pittsburgh.

“In fact, I’m not aware of another case of a disruptive technological change that has done so much harm to the industry that created the change.”

He did not pull any punches.

“While hundreds of billions of dollars of benefits have accrued to hundreds of millions of people, the amount of shareholder value destruction registers in the hundreds of billions of dollars,” he said.

“The industry is self-destructive.”

The message is not a new one. The shale industry has been burning through capital for years, posting mountains of red ink. One estimate from the Wall Street Journal found that over the past decade, the top 40 independent U.S. shale companies burned through $200 billion more than they earned. A 2017 estimate from the WSJ found $280 billion in negative cash flow between 2010 and 2017. It’s incredible when you think about it – despite the record levels of oil and gas production, the industry is in the hole by roughly a quarter of a trillion dollars.

The red ink has continued right up to the present, and the most recent downturn in oil prices could lead to more losses in the second quarter.

So, questionable economics is not exactly breaking news when it comes to shale. But the fact that a prominent former shale executive – who presided over one of the largest shale gas companies in the country – called out the industry face-to-face, raised some eyebrows, to say the least. “In a little more than a decade, most of these companies just destroyed a very large percentage of their companies’ value that they had at the beginning of the shale revolution,” Schlotterbeck said. “It’s frankly hard to imagine the scope of the value destruction that has occurred. And it continues.”

“Nearly every American has benefited from shale gas, with one big exception,” he said, “the shale gas investors.”’

The industry is at a bit of a crossroads with Wall Street losing faith and interest, finally recognizing the failed dreams of fracking. The Wall Street Journal reports that Pioneer Natural Resources, often cited as one of the strongest shale drillers in Texas, is largely giving up on growth and instead aiming to be a modest-sized driller that can hand money back to shareholders.

“We lost the growth investors,” Pioneer’s CEO Scott Sheffield said in a WSJ interview. “Now we’ve got to attract a whole other set of investors.”

Sheffield has decided to slash Pioneer’s workforce and slow down on the pace of drilling. Pioneer has been bedeviled by disappointing production from some of its wells and higher-than-expected costs.

But, as Schlotterbeck told the industry conference in Pittsburgh, the problem with fracking runs deep. While shale E&Ps have succeeded in boosting oil and gas production to levels that were unthinkable only a few years ago, prices have crashed precisely because of the surge of supply. And, because wells decline at a precipitous rate, capital-intensive drilling ultimately leaves companies on a spending treadmill.

Meanwhile, as the financial scrutiny increases on the industry, so does the public health impact. A new report that studied over 1,700 articles from peer-reviewed journals found harmful impacts on health and the environment. Specifically, 69 percent of the studies found potential or actual evidence of water contamination associated with fracking; 87 percent found air quality problems; and 84 percent found harm or potential harm on human health.

The health impacts have been a point of controversy for years, pitting the industry against local communities. The industry largely won the tug-of-war over fracking, beating back federal and state efforts to regulate it. However, the story is not over.

In many cases, there is an abundance of anecdotal evidence pointing to serious health impacts, but peer-reviewed research takes time and has lagged behind the incredible rate of drilling. Now, the public health research is starting to catch up. Of the more than 1,700 peer-reviewed studies looking at these issues, more than half have been published since 2016.

One need not be an opponent of fracking to recognize that this presents a threat to the industry. For instance, a spike of a rare form of cancer has cropped up in southwestern Pennsylvania recently. The causes are unclear, but some public health advocates and environmental groups are pointing the finger at shale gas drilling, and have called on the governor to stop issuing new drilling permits. The Marcellus Shale Coalition, an industry group, said the request was “ridiculous.” The region is right at the heart of high levels of shale drilling, so any regulatory action coming in response the public health outcry could impact drilling operations. Time will tell.

In the meantime, poor financials are the largest drag on the shale sector.

“And at $2 even the mighty Marcellus does not make economic sense,” Steve Schlotterbeck, the former EQT executive said at the conference.

“There will be a reckoning and the only questions is whether it happens in a controlled manner or whether it comes as an unexpected shock to the system.”

via ZeroHedge News http://bit.ly/2X5dnkd Tyler Durden

Trump began by going after the statement from Iranian leadership, blasting that they don’t “understand the words “nice” or “compassion,” they never have,” adding some threats: “Sadly, the thing they do understand is Strength and Power, and the USA is by far the most powerful Military Force in the world, with 1.5 Trillion Dollars invested over the last two years alone…”

Iran leadership doesn’t understand the words “nice” or “compassion,” they never have. Sadly, the thing they do understand is Strength and Power, and the USA is by far the most powerful Military Force in the world, with 1.5 Trillion Dollars invested over the last two years alone..

Then Trump turned to the Iranian people, who are suffering due to his economic war being waged by sanctions: “….The wonderful Iranian people are suffering, and for no reason at all. Their leadership spends all of its money on Terror, and little on anything else,” reminding his 61 million followers that “The U.S. has not forgotten Iran’s use of IED’s & EFP’s (bombs), which killed 2000 Americans, and wounded many more…”

….The wonderful Iranian people are suffering, and for no reason at all. Their leadership spends all of its money on Terror, and little on anything else. The U.S. has not forgotten Iran’s use of IED’s & EFP’s (bombs), which killed 2000 Americans, and wounded many more…

But he saved the best for last, unleashing a ‘sound-and-fury’-esque warning that “

….Iran’s very ignorant and insulting statement, put out today, only shows that they do not understand reality. Any attack by Iran on anything American will be met with great and overwhelming force. In some areas, overwhelming will mean obliteration.”

….Iran’s very ignorant and insulting statement, put out today, only shows that they do not understand reality. Any attack by Iran on anything American will be met with great and overwhelming force. In some areas, overwhelming will mean obliteration. No more John Kerry & Obama!

At the very moment a Russian warship has docked in Cuba — a mere one hundred miles off the American coast, Russian Deputy Foreign Minister Sergei Ryabkov has slammed US build-up of its weapons systems in Europe by invoking comparisons to the 1962 Cuban missile crisis.

Ryabkov made his comments early Monday, the same day the frigate Admiral Gorshkov, armed with Kalibr missiles, entered the port of Havana.

The Russian frigate Admiral Gorshkov in the port of Havana on Sunday. Image source: Reuters

“If things get as far as an actual deployment on the ground of these sorts of systems, then the situation won’t just get more complicated, it will escalate right to the limit,” Ryabkov was quoted as saying in RIA news agency.

“We could find ourselves in a situation where we have a rocket crisis close not just to the crisis of the 1980s but close to the Caribbean crisis,” Ryabkov said further while using the standard Russian term for the Cuban missile crisis.

Apparently Moscow wanted to provide Washington with a nice easy-to-understand visual of its warnings of a potential future escalating crisis in the form of its warship entering Cuban waters, which international reporters and cameras were on hand to capture.

This also comes in the wake of the collapse of the 1987 Intermediate-range Nuclear Forces Treaty, which was long credited with keeping US missile build-up out of Europe during the end years of the Cold War.

Image source: Reuters

According to Russian media reports, the Admiral Gorshkov left the Russian port of Severomorsk in late February, making multiple stops including in China before docking on Cuba and is accompanied by multiple support vessels, including the logistics vessel Elbrus, the medium sea tanker Kama and the rescue tug Nikolai Chiker.

Cuban state media described the purpose of the ship’s visit as carrying out “a program of activities that includes courtesy visits to the chief of the [Cuban] Revolutionary Navy, as well as touring places of historical and cultural interest.”

Russian sources said that as the Gorshkov approached Cuba, “American warships loomed along Cuba’s coast, with the guided missile destroyer USS Jason Dunham keeping the closest watch just a few miles away.”

Russian Deputy Foreign Minister Ryabkov had also warned of the following concerning NATO expansion and US weapons systems in Europe in conjunction with the warship’s Cuba visit:

If things get as far as an actual deployment on the ground of these sorts of systems, then the situation won’t just get more complicated, it will escalate right to the limit.

The Admiral Gorshkov entered service last year and is armed with cruise missiles, air defense systems and is even rumored to possess a “hallucination weapon” which reportedly makes targeted crews become disoriented, hallucinate, and vomit.

via ZeroHedge News http://bit.ly/2Lda2gB Tyler Durden

[Editor’s note: Yesterday we accidentally sent the wrong version of Simon’s article about Kazakhstan. We posted the correct version to the website– and definitely recommend you check it out.]

Late last week, the Federal Reserve gave its strongest signal yet that they would cut interest rates soon.

And in anticipation of yet another endless flood of cheap money, the US stock market soared to an all-time high.

Honestly it’s a bit absurd when you think about it. Look at Coca Cola as an example: its shares are now trading at a record high price.

Yet Coca Cola’s business is actually shrinking; its revenue has DECLINED each year for the past eight years.

And Coca Cola’s 2018 profits were 43% LOWER than they were back in 2011.

So obviously Coca Cola’s record high stock price has nothing to do the company’s performance… and everything to do with the fact that an unelected committee of central bankers has decided to print more money and slash interest rates.

It’s not just Coke. As we’ve discussed before, most large companies in the United States and much of the world are extraordinarily expensive based on any sensible valuation metric.

Investors are paying near record amounts for every dollar (or euro, etc.) of a company’s assets, revenue, or average long-term earnings.

Now, I grew up in a lower middle class household where my parents each worked multiple jobs to pay the rent… so I was raised to always look for a great bargain. Investing should be no different.

But with central bankers constantly distorting the market and pushing the share prices of shrinking companies to all-time highs, finding a great bargain can be challenging.

That’s why I maintain a global perspective: by expanding my options to the entire world beyond my own backyard, I increase my chances of success.

Uzbekistan is a great example– it’s possibly the cheapest (and most overlooked) place in the world.

You might already be thinking– “Uzbekistan? Is this guy serious?” Most westerners would automatically deem any former Soviet republic to be high risk and not worth discussing.

Well, I’ve written a lot in the past about the difference between perceived risk and actual risk.

Perceived risk is what people believe, often out of complete ignorance. They perceive places like Uzbekistan (or Colombia, another great example) to be extremely high risk. But they know almost nothing about it.

Actual risk, on the other hand, is substantially lower.

Uzbekistan has made impressive reforms over the past several years; we spent the morning at an event we organized for our Total Access members grilling several government ministers, as well as some of the country’s most prominent and successful entrepreneurs.

Many of our members told me they were astonished at Uzbekistan’s progress.

The economy is highly diversified and has been growing admirably for years, with very low levels of debt and high foreign reserves.

(Reserves are like a savings account for a government or central bank.)

Surprisingly, more than 50% of Uzbekistan’s reserves are held in gold, and the country is a major gold producer.

The government has slashed tax rates (small businesses pay just 4%, and larger companies and individuals pay a flat 12%) and abolished certain taxes altogether.

They also set up special economic zones for foreign investors where qualifying businesses can operate tax free for up to 10 years.

The government has also cut regulations, worked to eliminate corruption, reduced their own role in the economy, and steadily improved efficiency to make things easier for business.

The reforms are working.

We heard this morning, for example, from the founder of the largest retail chain in Uzbekistan. His company has grown 4x in just the past three years.

And he believes he can increase another 500% over the next few years.

Insurance companies are another great example; a typical Uzbek insurance company has a loss ratio (i.e. the percentage of its revenue that it pays out each year in claims) of about 30%, and an expense ratio of just 10%.

Lower ratios mean the company is more profitable. And ratios this low are practically unheard of in the West.

In developed countries in North America and Europe, a large insurance company barely breaks even on its core business, with loss ratios often exceeding 50% to 60%, and expense ratios averaging around 35%.

Plus, the insurance sector in Uzbekistan has been growing at more than 50% per year. So while these Uzbek insurance companies are profitable already, their profits have a LOT of room to grow.

Yet high quality Uzbek businesses can sell on the local stock exchange for as little as TWO times its annual profit.

(The average company in the United States in the S&P 500 currently sells for 22x earnings, more than ten times as expensive.)

I would never suggest that Uzbekistan is risk-free. Nothing is.

This country still has plenty of frontier market challenges, and the risk level is obviously higher than in North America or Europe.

But the actual risk of Uzbekistan is MUCH lower than what people believe (mostly because they haven’t come here or done any research).

And that’s really the opportunity: Uzbekistan is a rapidly growing, completely overlooked market that’s incredibly cheap, overflowing with possibilities, and with an actual risk level that’s MUCH lower than what ignorance may perceive.

Now, I’m definitely not writing today to convince you to invest in Uzbekistan. In fact I sincerely hope people think I’m crazy and continue to ignore this place.

But I do think Uzbekistan is a great example in expanding your thinking.

Most people will keep themselves mentally chained to conventional options– popular stocks that are irrationally overpriced.

(Bizarrely, many of these companies are perceived as ‘low risk’ even though they’re shrinking, or losing billions each year.)

But if you expand your thinking to the entire world, you often come across overlooked, ultra-compelling opportunities.

And regardless of what you choose to do, expanding your options always gives you a greater chance of success.

{kind=link}

{kind=link}