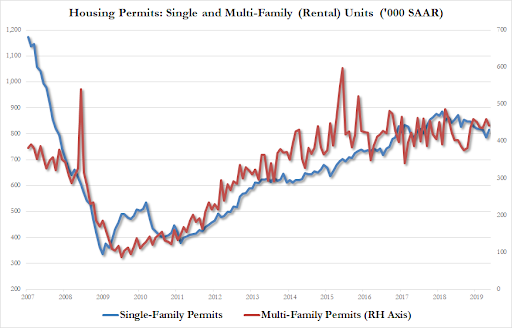

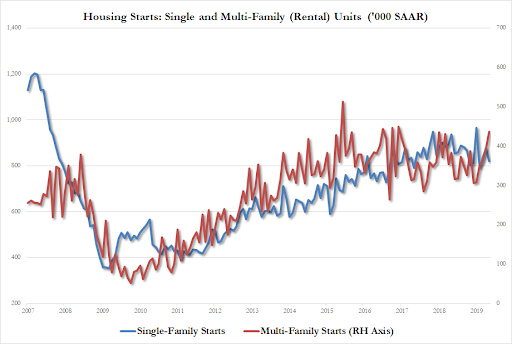

Despite the hype of soaring mortgage applications (refis, not purchases) and homebuilder stocks, housing starts tumbled 0.9% MoM in May (drastically missing expectations for a 0.3% rise), and while permits rose a better than expected 0.3% MoM, it remains very flat for the last six months.

Multi-family permits fell in May (to 820k) as single-family rose modestly (to 449k)…

The better than expected print for overall starts (at 1.294mm), was thanks to a massive spike in rental units…

Breakdown

Housing Starts 1-Unit: -6.4%, from 876K, to 820K

Housing Starts Multi Unit: +13.8%, from 383K to 436K

Not exactly a picture of health for the future of millennial homeownership as rental nation remains front and center, despite plunging mortgage rates.

via ZeroHedge News http://bit.ly/31EVj3N Tyler Durden

Cryptocurrencies are winning. If you need proof look no further than Facebook’s proposed Libra stablecoin. With the release of its White Paper, Tom Luongo explainsthe salient point is Libra is another attempt by the current banking establishment to slow the flow into the world of hard money.

In this respect Libra is no different than Ripple or dollar-settled Bitcoin futures contracts. These are products designed to slow the exodus out of the shadow banking system. Ripple is a way to lower foreign exchange fees and off-chain futures settlement is a way to control Bitcoin prices and exacerbate volatility to slow crypto-adoption by so-called normies.

Now we have Facebook and Libra. As Caitlin Long points out in her excellent Forbes’ article, Libra will get major financial players backing it. The goal is to become a standard creator in the vein of the Dow Jones Committee or the IMF since it will determine the basket weighting of Libra.

It won’t, however, be a cryptocurrency in the traditional sense. It won’t have a limited supply, defined inflation rate or any commodity character whatsoever.

Proof-of-work? Phsaw! Every good Friedmanite knows that opportunity cost in creating new monetary units is simply wasted capital!

Only mouth-breathing rubes stuck in the 19th century think that’s important.

Instead Libra’s supply will be regulated just like every other fiat currency, by a central authority. Facebook already wants all your data, whether you’re an account holder or not.

Now they want to control your currency as well.

The Central Bank of Facebook

When you extrapolate out the power of Facebook’s platform to where this coin will be marketed to, emerging markets, Libra is looking for all the world like Facebook’s application into the cartel of price-setting central banks.

Ms. Long even hints at this in her article. In fact it’s her first of six important points about Libra.

1. Facebook’s cryptocurrency will be a powerful force for good in developing countries, which is where Facebook intends to market the product.

Why? Because central banks in developing countries are notorious for their lack of discipline in maintaining the value of their fiat currencies, which too often lose purchasing power. The best example among many is Venezuela, which is experiencing hyperinflation worse than that of Germany after World War I. By providing citizens of developing nations with access to a store-of-value that is more reliable than their government-backed currencies, Facebook’s cryptocurrency will indirectly exert fiscal and monetary discipline on developing nations—which will improve the lives of many people globally.

Leaving aside the fact that much of Venezuela’s hyperinflation stems from the U.S. sanctioning and cutting Venezuela off from the global banking system, she has a strong point.

Governments are terrible at managing the value of their currencies for all the reasons Austrian economists have laid out in painstaking detail for decades.

Think this through for five seconds and you get to the obvious conclusion. Facebook and the Wall St. banks which actually control it are creating a coin to do away with national currencies in the countries most vulnerable to the Fed’s control over the global monetary system.

This is the next step in the quest to create a world currency.

And if the current system’s long-term health is threatened by, oh I don’t know maybe, the implosion of a bunch of SIFI banks like Deutsche Bank sparking a global sovereign debt crisis, then a stablecoin like Libra to replace a discredited dollar/euro/yen/pound makes some perverse sense.

If the plan has always been, as Jim Rickards has been saying for years, that the response to a collapsing monetary system would be national currencies replaced with IMF SDR’s as the reserves of the banking system, then having a ‘cryptocurrency’ Trojan Horse to bait and switch with has to be part of the plan to maintain confidence in the institutions that fomented the crisis in the first place.

And what better platform to do that with than Orwell’s Panopticon itself, Facebook?

… Bitcoin was born out of the extreme fraud of the financial system under Greenspan and Bernanke.

They used leverage ratcheted up post-Y2K to levels which could only be supported through legislative fiat to wall off capital fleeing the system.

And the response was a group of folks applied the teachings of Austrian Economics and Ludwig von Mises’ Regression Theorem to create a digital asset which became more resistant to fraud the more it was adopted.

The result was Bitcoin.

Bitcoin was a catastrophic mutation. A thing born out of necessity to free human beings from a central issuing authority of new monetary units. That relationship needs to be broken if we are going to free ourselves from the cycle of tyranny of the few at the expense of the many

In short, Government ineptitude and/or fundamental evil created Bitcoin.

This is the essence of what Ms. Long talked about around the same time as that post in her Mises Weekend talk “Will Blockchain Free Us from Wall St.”

It’s a wonderful talk that focuses on the domestic reasons why the dollar is yet to collapse and why Bitcoin provides the framework in which we can craft money that isn’t controlled by a central issuing authority.

This is the key point that she mentions but doesn’t emphasize in her talk. For the first time in history we have been presented the option to choose money whose new units are not subject to the whims and corruption of humans.

That’s set by math. And math both determines the rate of inflation and the rate of trust developed by the money itself. This continues to be Bitcoin’s biggest advantage as long as the economic incentives to maintain the network remain positive and are not perverted.

A Farewell to Kings

It means no philosopher kings deciding the rate of inflation or deflation. It means minimizing rent-seeking behavior. It means an end to counterfeiting as we have experienced in the past.

But as I said earlier, things like off-chain settled futures contracts create ‘Paper Bitcoins’ which suppress its exchange rate versus the U.S. dollar. They are an attempt at counterfeiting through through leverage. So are stablecoins like Tether, if not managed properly and, don’t kid yourself, Libra.

Facebook and Wall St. are banking on Facebook’s pervasiveness to drive mass adoption to build an adjunct to the existing financial system which slows the growth of the real cryptocurrency marketplace.

They value blockchain to lower costs and replace antiquated clearing systems of increasingly opaque ledgers, as Ms. Long points out in her talk. But they still want to retain control over the value of the money itself and what that money represents.

They want to retain the system of perverse incentives they have created which rolls up the wealth of the world to them.

Which is Ms. Long’s conclusion in her recent article:

6.Facebook’s cryptocurrency will turn out, in the end, to be a Trojan horse that benefits Bitcoin.

During a period of monetary upheaval, one in which the faith in the Institutional Order tends towards zero, there will be a fundamental shift away from public-issued money as trusted media of exchange.

If Martin Armstrong is correct and we are approaching the end of a mega-cycle in Public trust and a massive shift in consciousness to Private assets as stores of wealth, then it again makes sense for the powers that be, those I like to call The Davos Crowd to create a private-in-name-only “cryptocurrency” to co-opt that shift and remain in control.

But it also means that these same people, who have fed at this trough for so long, aren’t any more capable of managing it successfully than they were the dollar and the euro.

So we really do have little to fear from Facebook and Libra in the long run, because as we know from the Trojan Rabbit, it came back to land squarely on their heads.

* * *

Finally, as Bloomberg points out, whether Libra will be used in commerce is very much in question. For the last decade, multiple cryptocurrencies starting with Bitcoin have tried and failed to penetrate coffee shops and retail stores. In the first four months of this year, only 1.3% of Bitcoin economic transactions came from merchants, according to researcher Chainalysis Inc. The majority of the rest related to trading, and while many digital-assets enthusiasts are now hanging their hopes on the company’s new digital coin succeeding where Bitcoin has not, there are plenty of concerns.

“While Libra might be a big step in opening up a new wave of users to the benefits of asset-backed digital money, it comes with the risks of centralized pain points and vulnerabilities,” said Joseph Lubin, a co-creator of Ethereum.

“Data silos enable incumbents to maintain pricing power, and also come with the risks of data breaches, privacy, and security issues -— problems that many have already begun to associate with Facebook.”

Blain’s Morning Porridge, submitted by Bill Blain of Shard Capital

“Here’s to all the filthy money and where it went..”

So much to think and worry about the morning – the market showing its love and appreciation for BoJo and the heightened chances of a no-deal Brexit by spanking sterling to a 6 month low, or Boeing deciding to rename its troubled B-737 MAX by dropping MAX as Airbus orders come flooding in at the Paris Airshow, but the main story is the Fed.. or should that be how much faith the market is putting in the Fed and the FOMC meeting today/tomorrow? I’m not persuaded…

The market consensus is the Fed will eventually ease US rates, but not this time. It’s how it communicates/hints at timing tomorrow that will be most closely analysed aspect. Expect pages of dot-plot analysis and explanations of whatever he said and meant. Fed-Head Jerome Powell has already made clear the Fed is willing to act to offset slower growth and counter a trade war; “we will act as appropriate to sustain the expansion”.

This is where it starts to look messy. Is it the Fed’s job to “sustain expansion”?

It’s clearly a laudable objective, but let’s not confuse the stock market for the economy! It plays right into Trump’s agenda, his simplistic message to the electorate that stock strength proves his deal making success. An ease would provide a potent hit of short-term ecstasy to an addicted stock market, and give Trump something to crow about – a factor the Liberal press is all over like the proverbial cheap suit. The economy does seem to be signalling recession and problems ahead: an inverted yield curve, the collapse in govt bond yields, and a few negative economic numbers. On the other hand, even Fed Members say the economy is in “a good place”, inflation is not a threat, employment remains high, and trade woes aside… what’s the real issue?

Maybe the Fed should be asking deeper questions of itself? If the Fed were to cut rates.. who benefits and what would change? The stock market will throw a most excellent party and gorge itself higher. But a higher stock market isn’t actually driving the economy – what rising stock markets do in ultralow rate environments is exactly what’ve we’ve seen through years of QE ultra-low rates; returns from the stock market look better than business investment, so borrow money, or convert equity into debt to buy back stocks? More distortion is now what we need.

And low rates won’t solve the coming corporate debt crisis – it will just sustain the number of zombie companies for longer, putting off the reckoning till later, when it will be so much larger. Zombie companies block market niches, kept solvent when economic Darwinism says they should wither and die, opening their market niche to more nimbler new entrants.

What are America’s problems? A rate cut may give a short-term nudge to a lower dollar, but its problem is not the strength or sustainability of the stock market… Apple and Amazon will still be great firms no matter if their stock is up or down 10-20%. The real issues are real economics – like infrastructure and education, although we should also add heathcare and welfare. Without new infrastructure, America economic potential will keep rotting from the centre. Without a stronger, better up-skilled workforce, it’s not going to reap dividends from new tech like 3D, AI and Robotics. Solve these through investment and that will “Sustain The Expansion” through the long-run rather than the short-term high a cheeky rate ease might engender.

You can apply exactly the same logic to the UK… but zero chance of a rate cut here with sterling looking on the ropes.

Back in the UK – and just who is Rory Stewart? Ok – he’s the disruptive insurgent who looks like he was in Stingray. He has the temerity to appeal to Remainers.. Its unlikely he’d win in a 2 way when it comes to the whole Tory membership, but he’s a reminder how fractured the Tories are, and how unlikely a new solution will be. What’s worse for sterling and the UK? A No Deal Brexit exit in Late October, or, on the basis MPs have already voted down such a possibility, and a riven Tory party still unable to get on board? Oh dear.. this doesn’t look likely to get any better..

I was going to rant about Boeing, but I’ll post some stories on the Website. For anyone interested, I’ve posted my first Blain’s Financial Porridge Podcast on the website. This is still very much a Beta-Test, but please give me comments on improving it… It will go properly live as soon as its good enough…

via ZeroHedge News http://bit.ly/2IPhVpE Tyler Durden

With the deadline for arranging a meeting between the two world leaders coming down to the wire, Beijing would apparently like to make it clear to Washington that, if Trump wants a meeting with Xi in Osaka, he’s going to need to work a little bit harder.

On an already busy Tuesday morning, Global Times editor Hu Xijin brushed off what he described as a feeble attempt by Washington to ease tensions with China in a tweet, threatening to revive trade fears as markets continue their MTD rebound.

Is this a signal of the US to ease tensions? If so, it is too weak. Chinese people are now very distrustful of Washington, whose every move seems to be either a trick or bargaining chip. Beijing believes Washington tends to bully and be greedy, therefore it has toughened up. pic.twitter.com/8vxHRcDj0D

Of course, he was referring to a Bloomberg story about how Mike Pence delayed a speech set for the 30th anniversary of the Tiananmen Square massacre earlier this month in an attempt to curry favor with Beijing. The speech was reportedly going to be critical of China, attacking everything from BRI to its trade abuses.

Hu Xijin

But Trump reportedly delayed the speech to avoid upsetting Beijing ahead of a possible meeting in Osaka, according to Bloomberg. Though, to be fair, this isn’t exactly a shock. When news that the speech had been cancelled crossed the wire, most traders probably assumed Trump was hoping to soften Xi up.

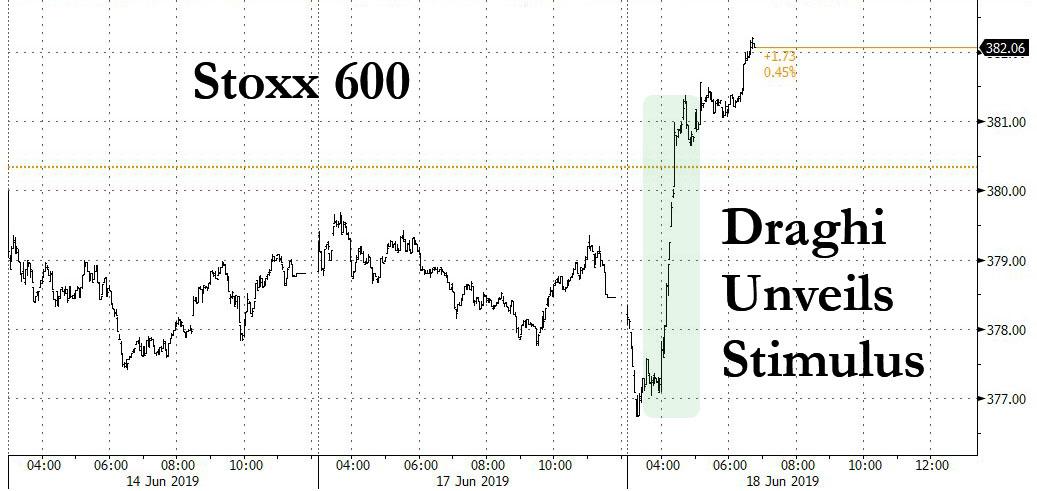

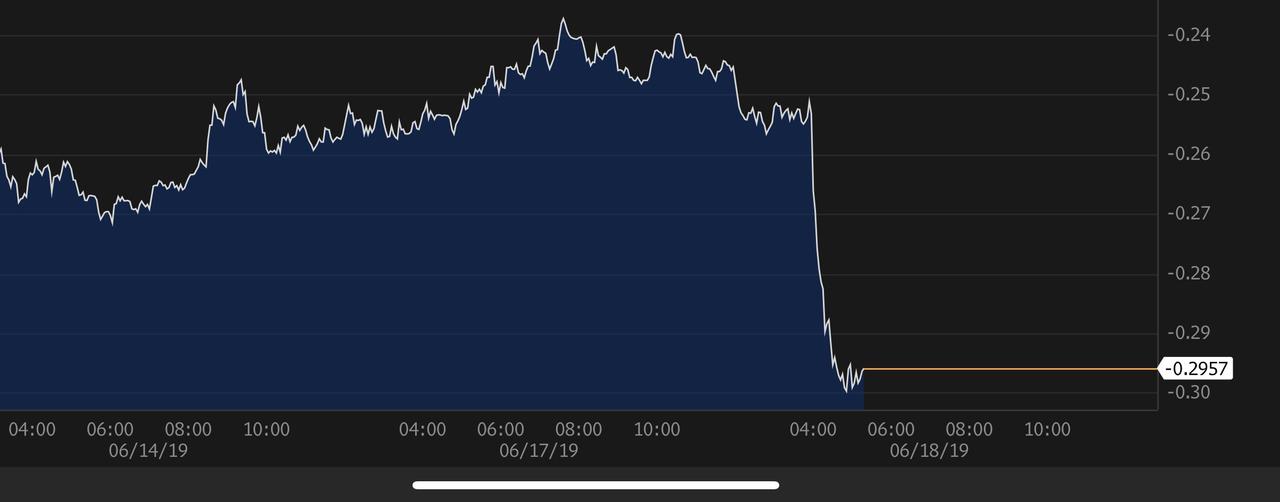

It was shaping up as a slow, boring session with everyone waiting “patiently” for the Fed tomorrow, until right after the European open, when two years after Mario Draghi first laid out the blueprints for the ECB’s rate normalization with a speech about the Eurozone’s “strengthening and broadening recovery” at the ECB’s Sintra forum in 2017, the ECB president finally threw in the towel and said that if the outlook doesn’t improve and inflation doesn’t strengthen, “additional stimulus will be required” adding that the ECB can amend its forward guidance, that rate cuts remain “part of our tools” and asset purchases are also an option. In short, full dovish capitulation by the ECB chief, which in a market addicted to monetary stimulus, was just what the bulls needed to hear.

The news sent global stocks surging…

… the Stoxx 600 rebounding from a loss to a gain of over 1%…

… S&P futures up 14 points, and back over 2,900…

… the German 10Y Bund yield tumbling to an all time record low below -0.30%…

Amusingly, Draghi’s somewhat striking admission of defeat, prompted an immediate response from none other than the US president, who tweeted “Mario Draghi just announced more stimulus could come, which immediately dropped the Euro against the Dollar, making it unfairly easier for them to compete against the USA. They have been getting away with this for years, along with China and others”…

Mario Draghi just announced more stimulus could come, which immediately dropped the Euro against the Dollar, making it unfairly easier for them to compete against the USA. They have been getting away with this for years, along with China and others.

This in turn served to push the Euro slightly higher, recovering some of its losses, as Trump’s warning was interpreted as a threat of more Eurozone tariffs, or alternatively, more pressure on the Fed to cut rates…

… as the final race to the bottom emerges, and looks as follows:

ECB unveils more easing

Trump threatens ECB, responds with Eurozone tariffs

ECB unveils even more easing

So with all these fireworks taking place in just a few short hours, what else happened?

Well, earlier, Japan’s Topix slipped, even as most Asian gauges rose. With European sovereign bonds soaring, led by Italy and Greece, while the Swedish and Austrian 10Y yield dropped below 0% for the first time, as fuel was added to the fire by a report that investor confidence in Germany’s economic outlook worsened dramatically in June…

… US 10Y Yields plunged to new lows, and just 3.2bps away from a 1-handle!

Of course, Draghi isn’t even the main event. Traders were far more focused on what the Federal Reserve announces on Wednesday to see whether Chairman Jerome Powell and his colleagues will validate widespread expectations for interest-rate cuts. The ECB’s announcement may just have changed the calculus.

In currencies, the Bloomberg Dollar Spot Index erased declines as the euro first fell below $1.12, then rebounded above it. Money markets are pricing in a 10bps cut by December from the European Central Bank after President Mario Draghi emphasized the need for stimulus. The kiwi dollar led gains in the Group-of-10 currencies, while the yen was boosted from demand versus the Aussie after RBA’s latest minutes showed more easing is likely

In commodities, oil dropped, with OPEC nations still unable to agree on a date for their next meeting, adding to uncertainty over whether production cuts would be extended.

Expected data include housing starts and building permits. Adobe is among companies reporting earnings

Market Snapshot

S&P 500 futures up 0.5% to 2,911.00

STOXX Europe 600 up 0.6% to 380.85

MXAP up 0.3% to 154.95

MXAPJ up 0.6% to 507.49

Nikkei down 0.7% to 20,972.71

Topix down 0.7% to 1,528.67

Hang Seng Index up 1% to 27,498.77

Shanghai Composite up 0.09% to 2,890.16

Sensex up 0.4% to 39,102.96

Australia S&P/ASX 200 up 0.6% to 6,570.00

Kospi up 0.4% to 2,098.71

German 10Y yield fell 5.0 bps to -0.294%

Euro down 0.2% to $1.1191

Italian 10Y yield fell 4.8 bps to 1.933%

Spanish 10Y yield fell 6.8 bps to 0.458%

Brent futures down 0.7% to $60.54/bbl

Gold spot up 0.4% to $1,345.06

U.S. Dollar Index up 0.1% to 97.68

Top Headline News from Bloomberg

ECB’s Draghi said if the outlook doesn’t improve, and inflation doesn’t strengthen, “additional stimulus will be required.” He noted that the ECB can amend its forward guidance, that rate cuts remain “part of our tools” and asset purchases are also an option. He was speaking at the ECB’s annual forum in Sintra, Portugal

Bond investors are preparing for another wave of QE from the ECB by returning to some of their favorite post-crisis trades. First up: buy the debt of nations such as France that have greater scope for purchases by the ECB. Next, bet on a drop in longer-maturity yields relative to near-term rates. Then go for higher-returning bonds, like Spain and Italy

Investor confidence in Germany’s economic outlook worsened dramatically in June after the Bundesbank predicted the economy will shrink this quarter. An index measuring prospects for the next six months fell to -21.1 in June, a far worse reading than the -5.6 economists expected

President Donald Trump’s top trade envoy Robert Lighthizer will be in the congressional hot seat for two days this week, giving lawmakers the chance to grill him about the prospects for a deal with China, as well as various punitive measures threatened by his boss

Hong Kong leader Carrie Lam personally apologized for backing a bill that would allow extraditions to China for the first time, her latest move to try and defuse protests that have rocked the city

Australia’s central bank is likely to lower interest rates again to drive increased hiring and boost households’ confidence that inflation will return to target. RBA says further rate cut ‘more likely than not’ in period ahead

China cut its U.S. Treasury holdings to the lowest in almost two years as the months-long trade conflict dragged on between the world’s two largest economies. The nation’s holdings of notes, bills and bonds declined by $7.5 billion in April to $1.11 trillion, according to Treasury Department data released on Monday

Rory Stewart, the rank outsider in the contest to become Britain’s next leader, is suddenly winning support and giving his bigger-name rivals a reason to worry. Officials working for three better-known contenders privately said they believed Stewart could deliver a major upset in the Conservative Party leadership votes this week

The U.K. economy will probably flatline in the second quarter and the Bank of England won’t raise interest rates until well into next year, according to a Bloomberg survey

Asian equity markets mostly saw cautious gains ahead of this week’s key risk events and following the marginal gains in the US where trade was otherwise uneventful aside from the strength in tech and telecoms. ASX 200 (+0.6%) and Nikkei 225 (-0.7%) were mixed with Australia led higher by tech and commodity related sectors, in which government plans to introduce a AUD 158bln income tax cut package, as well as anticipation for further RBA policy easing, added to the optimism. Tokyo sentiment was hampered by a firmer currency. Hang Seng (+1.0%) outperformed as business returned to normal following the recent protests and the Shanghai Comp. (+0.1%) was indecisive despite continued PBoC liquidity efforts, as trade uncertainty lingered after economic regulators refused to rule out using rare earths in the trade dispute and the Global Times Editor suggested the potential for a protracted trade war. Finally, 10yr JGBs initially traded steady amid the indecisiveness in the region but were later supported as sentiment in Japan further deteriorated and after the 5yr auction results showed a decline in yields and higher accepted prices from the prior month.

Top Asian News

China Cuts Treasury Holdings to Two-Year Low Amid Trade War

China’s Trade War Has Investors Flocking to Consumer Stocks

Metro Pacific Said Preparing to Start $2 Billion Hospital Sale

European equities are higher across the board [Eurostoxx 50 +1.2%] as the region was bolstered by a dovish Draghi. The DAX (+1.2%) is now back above the 12k level after having visited a pre-Draghi low of 11,986, albeit gains are somewhat limited by a subdued IT sector, meanwhile, the FTSE 100 lags as the index fails to benefit from Draghi’s speech. In terms of sectors, financial names underperform amid the prolongation of negative rates. Defensive sectors are outperforming with healthcare and utilities the standout outperformers. Movers to the downside today include chipmakers following a profit warning from Siltronic (-13.0%) , citing US-China trade issues. The downbeat market outlook spilled onto STMicroelectronics (-2.0%), ASML (-1.2%) and Infineon (-5.7%), albeit the latter is more influenced by the launch of a capital increase to fund the Cypress Semiconductor acquisition. Finally, Lufthansa shares rest near the foot of the Stoxx 600 following three separate broker downgrades.

Top European News

Canary Wharf Group Is Said in Talks to Buy CapCo’s Earls Court

Tieto to Buy Evry for $1.5 Billion in Nordic Software Tie- Up

German Highway Toll Ruled Illegal and Discriminatory by EU Court

Weidmann Waits as Merkel’s Candidate for Juncker Job Falters

In currencies, The EUR currency has slumped to the bottom of the G10 pile and even below the Aussie that was hit overnight by RBA minutes flagging further easing on the basis that benign inflation and wage trends are likely to persist for even longer. In similar vein, ECB President Draghi used the stage at Sintra to deliver a much more dovish/downbeat assessment of price developments and all but signalled another tweak to official guidance at the next policy meeting, if not further stimulus. In short, he acknowledged the recent pronounced drop in inflation expectations and said the GC will look at measures to counter the severity of risks to price severity in coming weeks, and if the situation fails to improve more stimulus will be needed. Eur/Usd has reversed from circa 1.1240 to just over 1.1180 and through 2.1 bn option expiries between 1.1195-1.1205 that may yet influence direction into the NY cut, while Eur/Gbp has pulled back sharply from around 0.8975 to 0.8925. Back down under, Aud/Usd is hovering off 0.6832 lows and Aud/Nzd has reversed towards 1.0500 as the Kiwi keeps tabs on the 0.6500 handle vs its US counterpart ahead of the latest GDT auction and NZ Q1 current account data.

CAD/CHF/GBP – All weaker vs the Greenback and partly in sympathy with the Euro and Aussie, but the Loonie also had more negative Chinese-Canadian headlines to digest as Beijing suspended pork imports pending closer inspection of the product. Meanwhile, the Franc slipped through parity, but strengthened in Eur/Chf cross terms to 1.1175 at one stage and will do doubt arouse SNB attention given that the ECB seems to be on the brink of easing further (-10 bp now priced in for December). Elsewhere, Cable is now eyeing 1.2500 and very early January lows after breaching key support at 1.2560, with the next leg of the Tory leadership race looming before UK CPI, retail sales and the BoE unfolds tomorrow and Thursday.

JPY/NOK/SEK – The major outperformers, as the Yen regains a safe-haven bid to retest support ahead of 108.00, while the Scandi Crowns benefit from single currency weakness and ECB-Norges Bank/Riksbank policy divergence given a widely expected hike from the former on Thursday. Moreover, the Sek derived some traction from a cautiously upbeat Riksbank business survey and significantly improved 2019 budget surplus forecasts from the SNDO. Eur/Nok around 9.7780 vs 9.8170 at one stage and Eur/Sek holding within a 10.6484-6147 range.

EM – Although the Buck has rebounded firmly, if not quite uniformly as noted above (back over 97.500), the Lira has maintained recovery momentum with the aid of some rare constructive comments on the US-Turkey front and reports that talks about the S-400 deal will be held at NATO next week. Usd/Try trading near the base of a 5.8225-8777 band.

In commodities, WTI and Brent futures are lower on the day with the former just above the USD 51.50/bbl level whilst the latter hovers around the USD 60.50/bbl mark. News-flow for the complex was largely surrounding OPEC this morning, with WSJ noting that Saudi intends to push for tighter compliance to OPEC production curbs. Sources also stated that the renewed pact would see the under-complying countries reducing crude supply by 300-400k BPD. In terms of a date, IFX reported that Moscow has reportedly agreed to consider an OPEC+ meeting on July 12th, postponed from the scheduled June 25/26. Looking ahead, traders will be keeping an eye on tonight API inventory release with the street looking for a draw of around 1.75mln barrels. Elsewhere, gold is hovering near intraday highs amid a bout of demand for the safe haven asset. Meanwhile, copper prices are supported despite the underlying risk off tone in the market as Glencore has shut down its Mufulira copper smelter at its Mopani copper mine in Zambia whilst Chile’s Codelco said the Chuquicamata copper mine maintained output capacity at 50% due to the 4th full day of a union strike.

US Event Calendar

8:30am: Housing Starts, est. 1.24m, prior 1.24m; MoM, est. 0.4%, prior 5.7%

8:30am: Building Permits, est. 1.29m, prior 1.3m; MoM, est. 0.23%, prior 0.6%

DB’s Jim Reid concludes the overnight wrap

I’m still in NY and last night I FaceTimed home to find there had been a big furniture delivery. No, not for our new house, but for my daughter’s new dolls house. I bought what I thought was a very good value but nice one only to find that the real money has to be spent furnishing it. It comes completely undecorated and bare. I had a bit of a shock when I saw how much all the trappings to go inside cost. So yesterday a four poster bed, a dining table and various kitchen appliances arrived. Then we spent most of the rest of the conversation debating whether we should also buy dolls house wallpaper! There is part of me that wondered whether I imagined this conversation in some kind of surreal jet lag haze but alas it was only too real.

It was a bit of a sleepy first day of the new week for markets yesterday with fairly minimal news flow to trade off. The good news, however, is that we’ve got a full day of the ECB Forum in Sintra ahead of us and today’s agenda includes an introductory speech from Draghi this morning, comments from various ECB officials including Guindos, Praet, Lane and Coeure, and then a policy panel featuring Draghi, the BoE’s Carney and former Fed Vice Chair Fischer this afternoon. It remains to be seen what will come of the Forum; however, as we mentioned yesterday, we have seen markets move sharply in previous years following comments that emerged from Sintra and with there being plenty of chatter about potentially more stimulus coming from the ECB, it’s worth watching it closely. In his opening remarks last night, Draghi declined to discuss policy or the current outlook, instead keeping his comments focused on the conference and on introducing Olivier Blanchard, who used his keynote address to argue for greater use of fiscal policy in the next downturn; an unusual topic for a central banking conference!

Ahead of the conference yesterday, comments from the ECB’s Coeure attracted a bit of attention following an interview with the FT. Coeure highlighted the dilemma the ECB faces with market pricing, saying that the ECB should neither ignore it nor blindly follow it. Most notably, Coeure said the costs associated with easing policy should not deter the ECB from acting – while also going on to mention rate cuts and the impact of NIRP on banks. In addition to those potential tools, he cited QE and forward guidance as other options. Coeure acknowledged the existing limits on bond-buying, but emphasized that the limits were chosen by the ECB, not by the ECJ or some other outside force, thus hinting that they could be modified. In a similar vein to Blanchard last night, he hinted at the frustration at the lack of fiscal policy from those that could potentially do it. This lack of action might force the ECB to do more in the future, which in turn would magnify the potential lower for longer problem.

With the exception of BTPs – which rallied -4.8bps on minimal news – bond markets were slightly weaker yesterday with 10y Bunds up +1.2bps in yield to the lofty heights off -0.247%. Similarly, Treasuries were +1.4bps higher although they did see a slight rally on the back of a shockingly weak empire manufacturing reading – the biggest monthly decline ever in fact. We’ll have more on that below. That being said, equity markets didn’t appear too fussed with the NASDAQ leading the charge following a +0.62% bounce. FANGS led the way with the NYSE FANG index up +1.75%, though the Philly semiconductor index retreated -0.64%, as cyclical sectors more broadly underperformed. Banks retreated -1.00% and the DOW transports index fell -1.03%. Elsewhere, the S&P 500 (+0.09%) and the STOXX 600 (-0.09%) were both little changed. HY credit spreads were -2bps tighter in the US, while the dollar traded flat. EM currencies were flat as well, while EM equities fell -0.36%.

This morning in Asia markets have mostly followed the lead from Wall Street; however, the exception is the Nikkei, which is down -0.70% after BoJ Governor Kuroda said that the “risks to the global economy are tilted to the downside”. A reminder that the BoJ meeting is this Thursday. Elsewhere the Hang Seng (+0.73%), Kospi (+0.38%) and Shanghai Comp (+0.08%) are all up. In other news, Chinese holding of US Treasuries are continuing to decline with the US Treasury Department data released yesterday highlighting that China’s holdings of US notes, bills and bonds declined by $7.5bn in April to $1.1tn, the lowest since June 2017.

Staying with Asia, yesterday news also broke that President Xi will travel to North Korea on June 20-21, the first time a Chinese leader has made the trip in 14 years. It is possible that North Korea talks are another arena of the US-China confrontation, so developments there could reverberate back onto the tariff war. Separately, Chinese tech giant Huawei said that the new Western sanctions will cost them around $30bn this year and next, as they anticipate 40-60mn fewer smartphone sales this year. While many countries have not joined the US in sanctioning the company, the threat and uncertainty surrounding the firm is enough for many major wireless providers to opt not to carry Huawei’s newest phone model. This was the first time that the company quantified the impact of the US’s sanctions, and the new information was worse than expected.

Also on the trade front, it’s worth keeping an eye on any headlines that could potentially emerge from US Trade Representative Lighthizer’s testimony before Congress today. While the aim of the testimony is to campaign to get Congress to approve the US-Mexico-Canada trade agreement, there’s a reasonable chance that US-China trade issues also get brought up. So that should be worth a watch.

While we’re on politics, here in the UK we’ve also got the second Conservative Party leadership ballot. The cut-off for this round is 33 votes. Unsurprisingly, Johnson remains the front runner following the first round and since then we’ve seen him pick up further support, including that of Health Secretary Matt Hancock – a former contender. While we’re on UK politics, Bloomberg has reported overnight that the UK Chancellor Philip Hammond might leave the government over PM May’s plans to commit nearly £27bn in spending on education over the next three years as this will likely limit the ability of PM May’s successor. Sterling has faded slightly on the back of the story.

Back to the data yesterday and specifically that empire manufacturing print in the US where the -8.6 reading was not only well below consensus for +11.0 , but also marked a drop of -26.4pts from the May reading, which is the biggest ever monthly change based on data going back to 2001. The outright monthly reading is also the lowest since October 2016 and it’s worth noting that this is the first regional Fed survey that usually helps to inform the ISM. The details didn’t make for much better reading, with new orders also down sharply and into negative territory along with employment. So worth watching how other survey data plays out in light of this very soft reading, which will raise concerns about further deterioration in the ISM. Our US economists cited the deterioration in sentiment as a key factor when they downgraded their US growth forecast last week (link ), with the bulk of the -0.4pp revision to 2019 growth coming from reduced capex activity.

As for the other data, the US NAHB housing market index slid -2pts to 64, its first decline of the year. That’s still near its recent cyclical highs. Homebuilder stocks retreated -0.52%, though they actually remain within a percent of their highest levels in a year. In Europe, labour costs rose 2.4% yoy in the first quarter, a 0.1pp acceleration from last quarter. That provides some evidence of tightening labour markets feeding through to wages, albeit gradually.

Looking at the rest of the day ahead, this morning we get the April trade balance and the final May CPI revisions for the Euro Area, as well as the June ZEW survey in Germany, which is expected to deteriorate from the May levels. In the US, we’ve got May housing starts and building permits data. The big event today though is the aforementioned ECB forum in Sintra. Meanwhile, the second ballot in the UK Conservative Leadership Party contest will take place today, while US Trade Representative Lighthizer is due to testify in Congress.

via ZeroHedge News http://bit.ly/2N9AhHt Tyler Durden

President Trump wasn’t thrilled by this morning’s selloff in the euro, and for the first time, is lashing out at ECB chief Mario Draghi for the first time, accusing Draghi in a tweet of intentionally manipulating the value of the shared currency.

Mario Draghi just announced more stimulus could come, which immediately dropped the Euro against the Dollar, making it unfairly easier for them to compete against the USA. They have been getting away with this for years, along with China and others.

After weeks of anticipation, the day has finally arrived: In a dramatic push into uncharted waters for the social media behemoth that saw Mark Zuckerberg make overtures to his former arch-nemises (the Winklevii), Facebook has finally published the white paper for its long-awaited stablecoin, “Libra”.

It wouldn’t be an exaggeration to say that Facebook’s white paper was the most hotly anticipated crypto whitepaper ever – made more so by Facebook’s extreme secrecy surrounding the project, which Zuck reportedly hopes will steer the company out of a morass of scandal and into a new era. But Facebook will also be expanding into a major new business (payments) just as the FTC and DoJ initiate anti-trust investigations against FB and a handful of other tech giants, and regulators on both sides of the Atlantic have already expressed some concern.

Per the white paper, Facebook’s global stablecoin will be dubbed “Libra.” It will operate on its own “Libra” blockchain, and will be backed by a reserve of assets, which technically makes it a “stable coin” (not unlike Tether). The coin will be governed by a non-profit consortium, the “Libra Association,” which will oversee development of the “Libra” ecosystem from Switzerland.

Per the FT, Facebook will spin off a unit called Calibra, which will be “totally separate” from FB, to manage the Libra digital wallet offering, which will be integrated into Facebook’s family of apps. Facebook said that financial data gathered by Calibra wouldn’t be shared without users’ consent.

According to the Guardian, the coin will facilitate payments across Facebook’s various platforms (including WhatsApp and Instagram), as well as a new “Libra” payments app. The coin’s software will be open source according to FB, allowing developers to build out an ecosystem around it (possibly incentivized with gifts of sensitive user data.

Facebook’s new cryptocurrency platform could provide the embattled social media giant with a new revenue stream of historic proportions as it contends with a possible federal antitrust probe and continued scrutiny over its data privacy practices.

[…]

Facebook’s cryptocurrency could thrive in emerging markets, providing a more stable alternative for transferring money in areas with volatile currencies and unstable governments, according to RBC Capital Markets. The firm expects “Libra” to facilitate person-to-person payments, traditional e-commerce and spending on apps or gaming services on Facebook-owned properties.

“We believe this may prove to be one of the most important initiatives in the history of the company to unlock new engagement and revenue streams,” RBC Capital Markets analysts said in a note to investors.

Facebook plans to make transactions no- or low-fee, but reportedly hopes to make money by offering loans and other financial products. The cryptocurrency is set to launch early next year.

We’re amazed that anybody could still be surprised that the European Central Bank might be heading toward more stimulus, particularly after Mario Draghi’s “whatever it takes 2.0” comment earlier this year, but nevertheless, the euro sank and markets shifted into a decidedly more risk-on mode after the outgoing central bank president said during the ECB’s annual conference in Sintra, Portugal that interest-rate cuts are part of the central bank’s “toolkit,” and asset purchases are also an option.

Italian bonds extended gains, outperforming other peripheral peers, while the yield on the 10-year German bund fell to a fresh asll-time low, in response to Draghi’s remarks. The European Stoxx 600 Index erased earlier declines of as much as 0.5% to rise 0.4%, and the euro erased earlier gains. S&P 500 futures extend gains to a session high at 0.3%, tracking European shares.

Banking stocks were the largest decliners, while miners outperformed.

Draghi said risk outlook “remains tilted to the downside,” and that more stimulus will be needed if the outlook doesn’t improve. More interest-rate cuts and more QE are part of the central bank’s arsenal, Draghi said.

“The prolongation of risks has weighed on exports and in particular on manufacturing. In the absence of improvement, such that the sustained return of inflation to our aim is threatened, additional stimulus will be required.”

And the central bank will do whatever it feels is necessary to live up to its mandate.

“The (European) Treaty requires that our actions are both necessary and proportionate to fulfil our mandate and achieve our objective, which implies that the limits we establish on our tools are specific to the contingencies we face. If the crisis has shown anything, it is that we will use all the flexibility within our mandate to fulfill our mandate – and we will do so again to answer any challenges to price stability in the future,” Draghi said.

In an example of central bankers speaking gibberish to sound sophisticated, Draghi added that the ECB is able to enhance forward guidance by “adjusting its bias and its conditionality to account for variations in the adjustment path of inflation.”

When central bankers say absolute gibberish to sound sophisticated and in control:

Draghi says ECB is able to enhance forward guidance by “adjusting its bias and its conditionality to account for variations in the adjustment path of inflation”

Draghi said risks from geopolitical factors, protectionism and vulnerabilities in emerging markets have not dissipated and are weighing on the Continent’s manufacturing industry. Major central banks around the world have taken a dovish turn since the start of the year, with many blaming the drop in global trade. Later this week, both the Fed and BoJ will meet, and, with markets pricing in ever-greater chances of a Fed rate cut that some believe could arrive as soon as Wednesday.

To underscore Draghi’s point, Germany’s ZEW investor expectations index tumbled to -21.1, far below the estimate of -5.6, a sign that sentiment continues to deteriorate.

via ZeroHedge News http://bit.ly/2ZzwioW Tyler Durden

Step into the shoes of a UK supermarket manager. You have gained experience in dealing with customer complaints, some more reasonable than others. Now you are confronted with an irate woman in her thirties, pointing to a cabinet full of fresh produce. She cannot bear to touch any of the items because they are emblazoned with Union Jack packaging.

“Why are you promoting nationalism? This is so divisive.”

“Well”, you calmly reply, “many of our customers like to support British farmers.”

“It’s disgusting”, she shouts back. “I won’t come back to one of your fascist shops again.”

This was an actual exchange described by a woman on Facebook. A perfect illustration of the British social divide: a member of the privileged, progressive middle class taking umbrage at the parochial, patriotic sentiment of ordinary people.

For this person, any expression of national pride or belonging is offensive jingoism. Not surprisingly, her profile identified herself as a Remainer who wants Britain to stay in the European Union.

Birmingham’s Bin-Brexit rally for the Conservative Party conference, September 30, 2018. Via Ilovetheeu, Wikimedia Commons

…

Just as Labour has favored Remainia over Brexitland, Conservative Party HQ is more interested in signaling progressive virtue than defending faith, flag, and family. According to one moderniser, Ben Kelly, it would be a mistake to appeal to “older, patriotic and zealous” people who are dying out.

“Affluent, liberal middle-class voters don’t want nostalgic politics or culturally insular values.” So forget the folk north of Watford Gap.

Neglect of poorer, predominantly white communities has become institutionally acceptable. Consider the massive donations for a Syrian refugee following a YouTube clip of him being bullying in the playground. Contrast this with the lack of response to the thousands of schoolgirl victims of mostly Pakistani-origin rape gangs. Or consider the constant media focus on the gender pay gap among highly-paid presenters or lawyers. All while ignoring the impoverishment of poorer women whose wages are undercut by the flood of cheap foreign labour.

…

Until recently, the upper middle class reserved its animosity for the lower middle class, as expressed in the film Abigail’s Party.

…

There are major flaws in the assumptions of the snob class, who patronize ethnic and other minorities by perpetuating victimhood. A black Brexit supporter, for example, has committed a double crime. Not only having the wrong opinion, but having the wrong opinion while being black. Diversity of thought is as necessary as it is natural.

There are looming threats to the cultural hegemony. The headline value of identity politics is ‘tolerance’, but this will surely eat itself. For all the rainbow murals, tension inevitably arises between favored identity groups.

…

Identity politics are really an expression of hate. As suggested by Professor Robert Tombs: “vehement Remainers motivated less by affection for the EU than by contempt for those they think support Brexit – above all the white working class.”

Meanwhile populism is gaining ground throughout the West, confronting the globalist elite.

…

Rulers and the ruled should be of the same place. The pan-Europeans and global idealists should wise up to what the common people want: a civic nationalism that is inclusive, sustainable, and genuinely democratic.

Our middle-class monitors must relearn the lessons from the past: working class folk are the salt of the earth. They deserve more respect than they currently get. Trash their identity, and they will destroy your identity politics.