Authorities at the Port of New York and New Jersey seized a massive 3,200 pounds of cocaine with an estimated street value of $77 million from a shipping container on Feb. 28, NPR reports. The massive drug bust took place after officials carried out an inspection of the shipment when they noticed tampering of several containers on a large vessel traveling from – where else – Buenaventura, Colombia, DEA special agent in charge Ray Donovan told NPR. That is when they discovered the nearly ton and a half of cocaine.

As NPR notes, the bust was part of a joint operation of the DEA, Customs and Border Protection, Coast Guard, Homeland Security Investigations, New York Police Department and New York State Police.

“This is the type of case that will last years. We’re investigating where it came from, where it’s going, everybody and everyone involved,” Donovan said hinting that a new “Escobar” may have emerged quietly in Colombia in recent years. “Any time an organization is moving that amount of cocaine, they’ve been involved for a long period of time.”

“This interception prevents a massive quantity of drugs from getting to the streets and in the hands of our children,” said Troy Miller, CBP Director of New York Field Operations, in a statement.

The shipment was intercepted when the vessel stopped over in New York/Newark on its way to Antwerp, Belgium. It contained a legitimate shipment of dried fruit, Donovan said. According to the report, it is unclear whether the drugs were destined for the U.S., or meant to continue on to Europe.

“The cocaine was loaded on the very tail end of the shipment,” Donovan explained. “That tells us it was the last thing put onto the container so that it was the first thing to be taken off, which is indicative of a very sophisticated organization that’s been involved in trafficking for some time.”

Donovan said the shipment is part of a larger trend in higher cocaine usage in recent years. “The cocaine market is coming back,” he said, adding that authorities seized about 26,500 pounds of cocaine in 2018; obviously it is unclear how many tons of Colombian cocaine were successfully be smuggled into the US in recent years.

Still, it may be too early to plan the script for a new Escobar TV drama: on a national level, the volume of drugs seized at ports of entry and in the field has been fluctuating. Officials at the borders seized 6,550 pounds of cocaine in 2018, down from 9,346 pounds in 2017, but up from 5,473 pounds in 2016.

Donovan also noted a growing trend in cocaine laced with fentanyl, a powerful opiate often used as a cheap, more potent alternative to heroin.

via ZeroHedge News https://ift.tt/2TC4Fgc Tyler Durden

The FAA remains stoic in its defense of Boeing in the face of the rest of the world banning, grounding, and investigating their latest 737 Max8 aircraft. However, reports today from The Wall Street Journal could force Elaine Chao to take action today.

In recordings of conversations with controllers of the pilot of the Ethiopian Airlines jet that crashed Sunday, he didn’t indicate any external problems with the jet or the flight, like a bird collision, CEO Tewolde Gebremariam told The Wall Street Journal.

The pilot “reported back to air-traffic controllers that he was having flight-control problems” and wanted to return to Addis Ababa, Mr. Gebremariam said.

The executive said he had listened to the recording and there were no other problems cited by the pilot.

The U.S. Federal Aviation Administration reiterated Tuesday that the aircraft is safe.

“Our review shows no systemic performance issues and provides no basis to order grounding the aircraft,” the agency said. U.S. carriers, sticking by the FAA guidance, have said they have no plans to ground flights.

But as the black boxes are investigated and if Ethiopian Air’s CEO’s comments are true – why wouldn’t they be – then both Boeing and the FAA face a more systemic problem than is currently considered.

Boeing shares are down modestly this morning, testing post-crisis lows…

The Wall Street Journal earlier reported that U.S. and Ethiopian officials were discussing the destination of the black boxes, with American officials quietly pushing for them to be sent to the US.

via ZeroHedge News https://ift.tt/2HeKnmk Tyler Durden

President Trump started off hot on Wednesday, tweeting that while he greatly appreciates House Speaker Nancy Pelosi’s statement that she’s against impeachment, “everyone must remember the minor fact that I never did anything wrong.”

Trump boasted that the “Economy and Unemployment are the best ever, Military and Vets are great – and many other successes!”

“How do you impeach a man who is considered by many to be the President with the most successful first two years in history, especially when he has done nothing wrong and impeachment is for “high crimes and misdemeanors”?”

I greatly appreciate Nancy Pelosi’s statement against impeachment, but everyone must remember the minor fact that I never did anything wrong, the Economy and Unemployment are the best ever, Military and Vets are great – and many other successes! How do you impeach….

….a man who is considered by many to be the President with the most successful first two years in history, especially when he has done nothing wrong and impeachment is for “high crimes and misdemeanors”?

Pelosi (D-CA) came out against impeaching President Trump in a Monday Washington Post article – telling the paper that she thinks it would be too divisive to the country, adding that Trump is “just not worth it.”

I’m not for impeachment. This is news. I’m going to give you some news right now because I haven’t said this to any press person before. But since you asked, and I’ve been thinking about this: Impeachment is so divisive to the country that unless there’s something so compelling and overwhelming and bipartisan, I don’t think we should go down that path, because it divides the country. And he’s just not worth it. –Washington Post

“I don’t usually talk about him this much,” Pelosi added. “This is the most I’ve probably talked about him. I hardly ever talk about him. You know, it’s not about him. It’s about what we can do for the people to lower health-care costs, bigger paychecks, cleaner government.”

via ZeroHedge News https://ift.tt/2F9O2Qc Tyler Durden

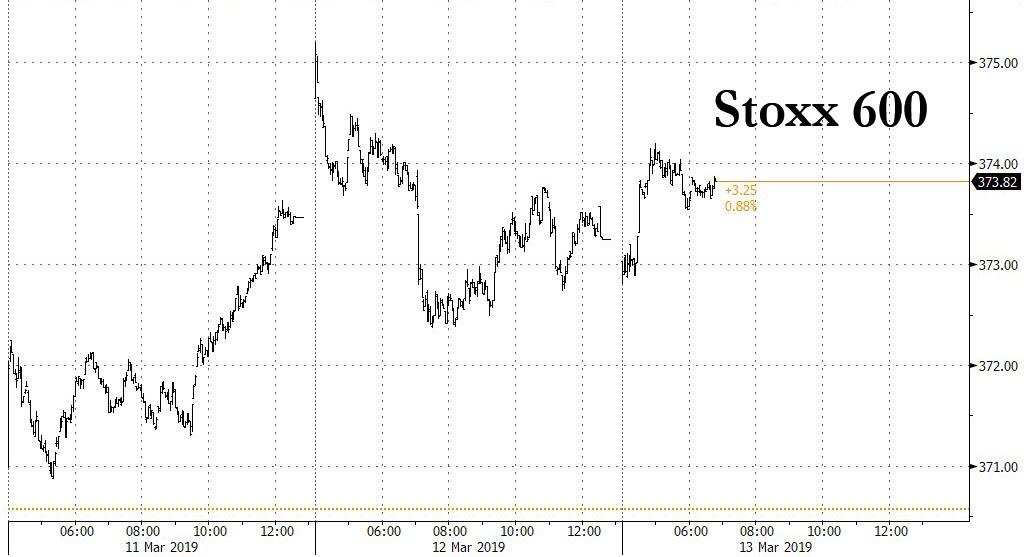

Global markets slipped on Wednesday after two days of gains amid mounting concern over world growth and trade, as S&P500 futures were coiled around the critical 2,800 “quad top” support level again, European stocks edged higher, and Asian shares declined amid mounting concern over world growth and trade and ahead of a key “no deal” Brexit vote, where optimism that lawmakers were set to eventually delay Brexit sent the pound higher.

Europe’s Stoxx 600 index jumped into positive territory, gaining as much as 0.2%, led by oil stocks after a mixed open, as gains for car makers and miners offset a slide for retailers following disappointing earnings from Inditex, owner of the Zara chain, and Adidas.

Attempts to boost European optimism were unable to shake off the somber mood in Asian trading, where last week’s optimism over U.S.-China trade talks has faded after U.S. Trade Representative Robert Lighthizer said it was unclear whether gaps between the two sides could be closed. Meanwhile, Asian data continue to reinforce the picture of a slowing world economy. Japan’s machinery orders fell in January at the fastest pace in four months, pushing the Nikkei down more than 1%.

Australia also continued its run of weak numbers, as the country’s consumer sentiment slipped in March. while U.S. monthly inflation disappointed rising at the smallest pace since September 2016.

As a result, MSCI’s Asia-Pacific equity index lost 0.3%, although sentiment appeared to reverse as the session drew on, with European markets creeping into the green and the S&P set to open just above 2,800. The question, as for the past months is “will it last?“

“Markets are still hopeful for a U.S.-China trade deal — my concern is that this is not necessarily going to ride to the rescue of the weak economy … ,” said Steve Barrow, G10 strategist at Standard Bank. “That means riskier financial assets like equities are going to struggle from here.”

All that’s kept MSCI’s world index off the 4 1/2-month highs it reached when Washington and Beijing appeared close to a trade agreement. The index has failed to make headway in March after two months of gains

Meanwhile, Britain’s political chaos is also weighing on sentiment. It hasn’t been able to agree on how to exit the EU by a March 29 deadline. On Tuesday, lawmakers defeated for a second time Prime Minister Theresa May’s proposed Brexit agreement. But they are expected to reject leaving the EU without a deal following a vote scheduled later today. Those optimistic expectations boosted the pound after this week’s volatile ride. Sterling rose as high as $1.3290 and as low as $1.2945. It was trading 0.7 percent higher at $1.3150. UK stocks and government bonds were flat.

Of course, even if lawmakers rejected no-deal Brexit, the eventual outcome was still unclear, with UBS advising clients to “remain cautious, and avoid chasing short-term rallies in sterling or increasing exposure to UK equities.”

The other big narrative fascinating world markets has been Boeing’s shares, as more and more countries ground its 737 MAX 8 planes after Sunday’s crash in Ethiopia, the model’s second fatal recent crash in les than six months. Boeing’s Frankfurt-listed shares shed another 2 percent to six-week lows. A 6% fall in New York on Tuesday pushed the Dow down 0.4%; Boeing was down another 1% overnight as more countries grounded their 737 Max 8 fleets.

However, the S&P 500 and Nasdaq benchmarks closed higher after a weak inflation report for February reinforced expectations the Federal Reserve will remain patient on rates and may sound more dovish at next week’s meeting.

Those expectations had taken U.S. 10-year bond yields to 10-week lows at 2.596 percent on Tuesday and pushed the dollar lower for a fourth straight day against a basket of currencies. German 10-year bond yields also fell, getting closer to zero percent.

In geopolitics, Iran’s Defence Minister said Tehran will respond firmly if Israel Navy acts against Iran oil sales. Senior Iranian Security official says some regional countries are spending money on “suspicious nuclear projects” which would force Iran to revise its defence strategy. Elsewhere, Secretary of State Pompeo criticized China, Russia, Venezuela and Iran in comments touting increasing US energy supplies, adds will use all economic tools at disposal to deal with Venezuela crisis. Finally, North Korea reportedly appeared close to missile site restoration, with South Korea stating the launch sites restoration is almost complete.

In FX, the dollar lost steam after the London open as fresh demand helped the pound rose ahead of another key U.K. parliamentary vote on Brexit. The Australian and New Zealand dollars slid 0.3 percent, whacked by Australia’s weak consumer confidence figures. The euro was flat against the dollar around $1.129, up from the 20-month lows of $1.1174 it hit after the European Central Bank pushed back its rate-rise schedule and announced a cheap-loans program for banks.

On commodity markets, the dip in the dollar helped gold hit its highest in two weeks at almost $1,307 per ounce. Brent crude oil futures edged up around 0.3 percent to $66.88 a barrel after a Saudi official said the kingdom planned to reduce oil exports and the U.S. government cut its forecast for domestic output growth.

Expected data include mortgage applications, PPIs and durable-goods orders. Empire Co. and MongoDB are among companies reporting earnings.

Market Snapshot

S&P 500 futures little changed to 2,798.50

STOXX Europe 600 up 0.2% to 373.80

MXAP down 0.5% to 158.10

MXAPJ down 0.3% to 521.90

Nikkei down 1% to 21,290.24

Topix down 0.8% to 1,592.07

Hang Seng Index down 0.4% to 28,807.45

Shanghai Composite down 1.1% to 3,026.95

Sensex up 0.6% to 37,740.80

Australia S&P/ASX 200 down 0.2% to 6,161.19

Kospi down 0.4% to 2,148.41

German 10Y yield rose 1.1 bps to 0.066%

Euro up 0.07% to $1.1296

Italian 10Y yield fell 2.1 bps to 2.185%

Spanish 10Y yield rose 0.2 bps to 1.172%

Brent futures up 0.7% to $67.13/bbl

Gold spot up 0.4% to $1,306.45

U.S. Dollar Index little changed to 96.88

Top Overnight News

Britain will confront head-on the threat of a no-deal Brexit in a parliamentary vote with huge ramifications for Prime Minister Theresa May. On Wednesday, lawmakers will decide whether to tear the country out of the European Union with no agreement in place in 16 days’ time, or give themselves the chance to delay Brexit in the hope of securing better terms

The U.K. government won’t apply tariffs on most goods imported into the country in the event of a no-deal Brexit, under a temporary plan announced Wednesday

Frustration among U.K. businesses is reaching boiling point after Prime Minister Theresa May’s latest attempt to get Parliament to back her exit deal from the European Union failed again. “Enough is enough. This must be the last day of failed politics,” said Carolyn Fairbairn, director-general of the Confederation of British Industry. “It’s time for Parliament to stop this circus.”

The U.K. Debt Management Office is expected to announce a hike in its gilt sales to GBP123b for fiscal 2019-20, up a quarter from GBP97.5b in the past year, according to a Bloomberg survey of eight primary dealers. While this is the highest since 2016, nearly GBP100b of redemptions will make net supply the smallest for 17 years, and continued Brexit uncertainty means demand should stay robust

President Donald Trump’s top trade negotiator said the U.S. must keep the option of raising tariffs on Chinese imports as a way to ensure Beijing lives up to a trade agreement that could be finalized in a matter of weeks

Australia’s consumer confidence slumped in March as households were shaken by a slowdown in economic growth and the prolonged downturn in the property market.

ECB chief economist Peter Praet calls general idea behind modern monetary theory a ‘dangerous proposition’. “The general idea that government debt can be financed by central banks is a dangerous proposition. In the past, this has resulted in hyperinflation and economic turmoil. That’s why central banks are independent”

Japan’s machine orders released Wednesday were unexpectedly bad, a warning sign for capital investment which follows other data suggesting the economy is off to a rough start 2019

Industry gave the euro-area economy a surprisingly strong lift at the start of 2019 after months of disappointing data cast clouds over the region’s outlook. A 1.4% month-on-month jump in industrial output in January — higher than the 1% gain forecast — was driven by a rebound in some of the bloc’s largest economies, including France, Italy and Spain

Asian equity markets traded mostly lower following the mixed lead from Wall St and after UK PM May’s Brexit deal was voted down in parliament, while soft data releases also contributed to the subdued tone. ASX 200 (-0.2%) and Nikkei 225 (-0.9%) declined at the open as broad weakness and poor Westpac Consumer Confidence data weighed on Australia, while the Japanese benchmark underperformed on currency effects and after a larger than expected contraction in Machine Orders. Hang Seng (-0.4%) and Shanghai Comp. (-1.1%) conformed to the negative tone but with losses stemmed as the region digested some corporate updates. Finally, 10yr JGBs tracked the recent upside in T-notes which were lifted after soft US CPI numbers, while prices were also supported on safe-haven demand and with the BoJ in the market for JPY 710bln of JGBs in the belly to the super long-end.

Top Asian News

Japan’s Top Life Insurer Taps Derivatives to Fight Low Yields

China’s Hot Stocks Turn Upside Down in Widest Swings Since 2016

European Equities are marginally firmer [Euro Stoxx 50 +0.2%] shrugging off the poor performance seen overnight in Asia where the Shanghai Composite (-1.0%) finished firmly in negative territory on the risk tone following Brexit and a mixed lead from Wall Street. Sectors are mixed, with outperformance seen in energy names as the oil complex is higher by around 0.8%. Notable movers include, Stoxx 600 heavyweight Nestle (+0.4%) in the green after the Co. are said to have selected second round bidders for their skin care unit, which may be valued as high as USD 10bln. Separately, and towards the top of the Stoxx 600 are Pandora (+1.5%) as the Co. are to initiate preparations to identify a new chairman at their annual general meeting today. Elsewhere, and lagging the Stoxx 600 are Inditex (-4.0%) as their FY figures missed on some analysts’ expectations, and in spite of the Co. lifting their dividend by 17%. Adidas (-3.9%) are similarly underperforming as the Co. expect H1 to be impacted by supply chain problems, particularly in the US, may have a 1-2% impact on 2019 sales growth. On the pre-market front Spotify (SPOT) have filed a complaint against Apple (AAPL) stating that Apple abuses its market dominance and engages in anti-competitive behaviour.

Top European News

Inditex Drops as Earnings Growth Slows to Weakest in Five Years

Martin Gilbert Loses Out as Standard Life Aberdeen Picks One CEO

EON Promises Higher Dividend But Earnings Seen Flat in 2019

Ronaldo Hat-Trick Seals Another Stock Market Moving Comeback

In currencies, sterling continues to withstand Brexit-related bearish impulses/knocks and has staged another impressive looking comeback from lows vs the Usd and Eur in wake of a 2nd big defeat for UK PM May on the Withdrawal Agreement, even with legally binding assurances from the EU. In fact, the Pound sits proud at the top of the G10 rankings with Cable back above 1.3100 and briefly through technical resistance in the form of a 50% Fib (1.3148) and the psychological 1.3150 level, while Eur/Gbp has reversed from circa 0.8650 through 0.8600 again.

DXY – The broad Dollar and index remain on the back foot following yesterday’s benign US CPI release, as the data focus switches to PPI, durable goods and construction spending, while the Gbp resilience noted above along with similar resistance in other rival currencies is also impacting. The DXY has subsequently slipped back from 97.000+ yet again and is currently just off a 96.839 base, eyeing chart support at 96.764 (also a 50% retracement) having breached 96.987 (38.2% Fib).

CAD/AUD/NZD – The non-US Dollars are bucking the overall trend of gains vs the Greenback, albeit to varying degrees as the Loonie continues to hold up better around 1.3350 against the backdrop of firmer crude prices. Conversely, the Aussie and Kiwi are underperforming, with Aud/Usd slipping back towards 0.7050 following downbeat Westpac consumer sentiment overnight, and Nzd/Usd retreating through 0.6850 ahead of NZ GDP data that may miss consensus and the RBNZ’s forecast, according to Westpac. However, the Aud/Nzd cross remains weak after a sub-1.0300 dip at one stage.

CHF/EUR/JPY – The Franc has marginally extended recovery gains vs the Dollar to just shy of 1.0050, while the single currency has crossed 1.1300 with the aid of firmer than expected Eurozone IP and bullish near term technical impulses as the headline pair clears 200 hourly a 10 daily MAs (1.1290 and 1.1294 respectively). However, Tuesday’s 1.1305 peak remains (just) intact and the 21 DMA comes in at 1.1313, while decent expiry options sit between 1.1300-10 (2.1 bn). The Jpy has been hampered somewhat by disappointing Japanese data in the form of machinery orders and is currently close to the bottom of a 111.15-38 band.

In commodities, WTI and Brent futures are marginally firmer on the day but remain in within the March range of just over USD 3.0/bbl. WTI futures are approaching the March high of USD 57.86/bbl whilst Brent is also around USD 0.50 from this month’s highs. In terms of production numbers, Russia oil output has reportedly fallen to 11.307mln vs. 11.336mln in February. As a reminder, under the OPEC+ deal, Russia agreed to curb output by 228K BPD in Q1 2019 from the October baseline of 11.418mln. Traders will be eyeing the release of the weekly DoE inventory data which will be released at 1430GMT due to the US clock change. Metals markets are higher across the board as the complex benefits from the pullback in the Greenback. Gold hit a two week high and reclaimed USD 1300/oz to the upside whilst breaching its 50 DMA at USD 1303/oz whilst copper gains more ground above its 100 WMA (USD 2.8993/lb). Finally, zinc prices hit levels last seen eight months ago (USD 2848.50/tonne) as concern grows about an tight market for the metal.

US Event Calendar

8:30am: PPI Final Demand MoM, est. 0.2%, prior -0.1%; PPI Ex Food and Energy MoM, est. 0.2%, prior 0.3%

Final Demand YoY, est. 1.9%, prior 2.0%; PPI Ex Food and Energy YoY, est. 2.6%, prior 2.6%

8:30am: Durable Goods Orders, est. -0.4%, prior 1.2%; Durables Ex Transportation, est. 0.1%, prior 0.1%

8:30am: Cap Goods Orders Nondef Ex Air, est. 0.2%, prior -1.0%; Cap Goods Ship Nondef Ex Air, est. -0.2%, prior 0.0%

10am: Construction Spending MoM, est. 0.45%, prior -0.6%

DB’s Jim Reid concludes the overnight wrap

There is only one place to start this morning and that’s with another tumultuous day in the ongoing Brexit saga. As was expected as soon as the Attorney General offered his legal advice in the morning, Prime Minister May’s amended Withdrawal Agreement was defeated in parliament – this time by a margin of 391-242. That was around a 40-swing improvement from the prior vote on her deal, but still a comprehensive defeat for May’s government.

After the vote, Prime Minister May reiterated that she believes her deal is the best and only option that can be negotiated, as long as Parliament wants to deliver both 1) an exit from the EU per the referendum result, and 2) an exit that does not result in a no-deal, disorderly Brexit. To avoid the latter, May will, as promised, table a new motion today, which will ask Parliament to commit to eliminating the possibility of a no-deal outcome. It should pass, setting up a Thursday vote on an extension to Article 50.

In her remarks, May also suggested that after the Thursday vote on an extension, Parliament needs to work out what it does want to vote on and thus hinting that indicative votes may be likely. The key moving forward will be how any ‘indicative votes’ on new options (revoke Article 50, second referendum, another attempt at a new deal) will be structured for Parliament to express its preferences. It’s not clear what type of outcome would command a majority though. At this stage it’s also difficult to rule out Withdrawal Agreement 3 returning. As someone said on Twitter last night, the WA is like the “Fast and Furious” franchise. It’s never ending.

As for the EU response, chief negotiator Barnier said “the EU has done everything it can (…) the impasse can only be solved in the UK.” Other officials took the same line, indicating zero appetite from Brussels to renegotiate the deal. Notably, a spokesman for EU Council President Donald Tusk said that the EU would consider an extension to Article 50, but it would need to include a “credible justification for a possible extension and its duration.” He also said that the EU’s “smooth functioning” was a priority, signaling that if an extension goes beyond the European Parliamentary elections in May, the UK would need to participate. So watch out for tonight’s vote and all relevant amendments.

After rallying yesterday morning, the pound had shed as much as -1.79% from its early highs following Attorney General Cox’s legal advice. His opinion suggested that the legal risks around the withdrawal were unchanged even with the newly negotiated additions to the deal, with the UK still having no internationally lawful means of exiting the protocol’s arrangements. The pound rallied back to flat on the day as rumours swirled ahead of the vote, but ultimately weakened back toward the lows as it became clear that the motion would be thoroughly defeated. This morning sterling is trading slightly higher (+0.12%).

Wider risk sentiment in Asia has turned negative this morning with the Nikkei (-1.11%), Hang Seng (-0.60%), Shanghai Comp (-0.37%) and Kospi (-0.64%) all heading down. Elsewhere, futures on the S&P 500 are down -0.18% and the Australian dollar is down -0.38% on weak consumer confidence data for March (fell -4.8% mom to 98.8). In yet another sign of the global soft patch, Japan’s January core machine orders came in at -5.4% mom (vs. -1.5% mom expected), marking the third consecutive negative monthly read. However, the series tends to be volatile.

The moves this morning come after risk assets generally stayed above water last night in the US. A slightly softer US CPI print appeared to help keep the carry trade in play, while US Trade Representative Lighthizer played a bit of a straight bat in his testimony in front of the Senate. He said that talks with China were in the final weeks but that he couldn’t predict the outcome at this point. He did reiterate however that “we are going to have an enforceable agreement or the President won’t agree”. For what it’s worth Lighthizer was quiet on the 232 auto tariffs subject however the WSJ did run a story saying that Trump was facing increasing headwinds to imposing tariffs on car imports from congressional opposition, legal challenges, and consumer opposition.

When it was all said and done, the S&P 500 finished +0.30% and NASDAQ +0.44%, however, the DOW again lagged, closing down -0.38% with Boeing (-6.13%) hit by the news of multiple countries grounding the Boeing 737 Max 8 indefinitely. The S&P 500-DOW differential, at 0.68%, joins Monday in being in the top 10 since 2009. Boeing cash bonds were fairly quiet again however, with the 3.2% 29s trading close to flat.

In Europe, the STOXX 600 finished -0.06% after passing through gains and losses with the various Brexit headlines. European Banks (-0.38%) did likewise with a bit of focus also on headlines out of the ECB. Reuters reported that the ECB did not discuss a tiered deposit system, and that only one governor expressed “deep concern” about negative rates. The same story also suggested that the plan for the TLTRO rate not going below zero was still in discussion and that growth weakness could change the terms. Further headlines also suggested that the ECB committee proposed a new TLTRO premium at 25bps above the main refi rate but it was pushed back as being too high. The comment on tiered deposits shouldn’t be a surprise at the moment, however, the TLTRO premium line didn’t appear particularly encouraging for markets.

On a related subject the ECB’s Villeroy also said that the ECB does not do “monetary policy to please banks nor to punish them”, which was notable as the Central Bank of France has been one of the more vocal on the impact of negative rates. Bunds closed (-1.2bps) at the lows of 0.052% having earlier in the session hit as high as a gravity defying 0.101%. Gilts (-1.6bps) were also well off their yield highs while Treasuries closed down -4.1bps to 2.598% post that below market inflation print. This is the lowest yield since 3 January and that was the only day it closed lower than the previous night since mid-January 2018.

Indeed core CPI came in at +0.1% mom (+0.11% unrounded), which compared to expectations for a +0.2% reading with the weakness concentrated mostly in medical care and recreation. It also nudged the year over year rate down to +2.1% from +2.2% with the headline at +1.5%. So modestly lower but unlikely to change the Fed’s view too much. The other US data yesterday was the February NFIB small business optimism reading which rose half a point to 101.7, albeit slightly behind expectations for 102.5. The only data of note in Europe came in the UK, where January industrial production (+0.6% mom vs. +0.2% expected) and January GDP (+0.5% mom vs. +0.2%) both surprised notably to the upside. Much of that was to do with the very weak December data, however, it completely played second fiddle to all the Brexit newsflow in any case.

Finally, while it should be another day of Brexit headline watching, for those wondering, there is the distraction of the January industrial production print for the Euro Area this morning, while in the US we’ll get February PPI (+0.2% mom core expected) and preliminary January durable and capital goods orders (+0.2% nondefense capital orders expected) data. The ECB’s Coeure will also speak this afternoon while EU ambassadors meet in Brussels.

via ZeroHedge News https://ift.tt/2EWb9wq Tyler Durden

The Federal Aviation Administration is facing growing criticism for backing the airworthiness of Boeing’s 737 Max jetliners as the number of countries that have grounded them grows in the wake of the Ethiopian Airlines crash over the weekend, according to CBS News.

Curiously, this is a reversal of the conventional process where the rest of the world typically takes it cues from the FAA, long considered the world’s gold standard for aircraft safety. Yet aviation safety regulators in dozens of other nations have decided not to wait for the FAA to act and have grounded the planes or banned them from their airspace. In addition, at least 10 airlines worldwide have stopped flying them.

Three days after an Ethiopian Airlines jet crashed, killing all 157 people on board, just months following a deadly crash in October of another new Boeing 737 Max 8 operated by Lion Air in the sea off Indonesia, country after country ignored assessments by the U.S. Federal Aviation Administration that the plane is safe to fly. Canada agreed it was too early to act but many fell into line in growing numbers behind the first major nation to ground its 737 Max fleet – China.

In doing so, long-time American allies including the U.K. and Australia broke convention by snubbing an authority that has defined what’s airworthy for decades. New Zealand, the United Arab Emirates and Vietnam on Wednesday became the latest countries to block the 737 Max, helping legitimize China’s early verdict on March 11 that the plane could be unsafe.

“The FAA’s credibility is being tested,” Chad Ohlandt, a Rand Corp. senior engineer in Washington told Bloomberg. “The Chinese want their regulatory agency to be considered a similar gold standard.”

As we reported yesterday, the EU’s Aviation Safety Agency, which covers 32 countries, announced Tuesday it was banning the planes from flying in its airspace. Other countries that have either grounded or temporarily banned them include China, the United Kingdom, India, Indonesia, Singapore, Oman, Malaysia, Vietnam, Australia and the UAE.

One day after the Ethiopian Airlines flight plunged to the ground, the Civil Aviation Administration of China (CAAC) drew a possible connection between the crash and Lion Air’s in October. A preliminary report into the earlier disaster, which killed 189 passengers and crew, indicated pilots struggled to maintain control following an equipment malfunction. Both flights, on almost brand new planes, ended minutes after takeoff.

The CAAC asked domestic airlines to ground their 737 Max 8 fleets. “There needs to be reason for us to change that decision,” said CAAC’s deputy head Li Jian. Domestic carriers including China Southern Airlines Co. and Air China Ltd. account for about 20 percent of 737 Max deliveries worldwide through January, according to Boeing’s website.

According to Bloomberg, Ethiopian Airlines CEO Tewolde GebreMariam told CNN that the latest crash and the Lion Air tragedy had substantial similarities. Separately, the Wall Street Journal reported that Ethiopia wanted to send the flight-data and cockpit-voice recorders to the U.K., causing U.S. investigators to hold intense behind-the-scenes talks to bring the parts to America.

Rep. Peter DeFazio, D-Ore., the chairman of the House Transportation and Infrastructure Committee, said in a statement Tuesday that he’s concerned that international aviation regulators are providing more certainty to the flying public than the FAA.

“In the coming days, it is absolutely critical that we get answers as to what caused the devastating crash of Ethiopian Airlines flight 302 and whether there is any connection to what caused the Lion Air accident just five months ago,” DeFazio said.

Already several U.S. lawmakers have called for the Max jets to be grounded, including Republican Sens. Ted Cruz of Texas and Mitt Romney of Utah and Democratic Sens. Richard Blumenthal of Connecticut, Dianne Feinstein of California, Elizabeth Warren and Ed Markey of Massachusetts and Bob Menendez of New Jersey. So have Democratic Reps. Steve Cohen of Tennessee, Adriano Espaillat of New York and Shelia Jackson Lee of Texas.

Meanwhile, both the Association of Flight Attendants and the American Airlines flight attendants’ union are urging the grounding of Max 8s, yet the FAA continues to ignore their pleas.

In a striking development, on Tuesday it emerged that pilots on at least two flights of U.S. carriers have reported that an automated system seemed to cause their Boeing planes to tilt down suddenly, the same problem suspected of contributing to the crash off Indonesia. The pilots said that soon after engaging the autopilot on Boeing 737 Max 8s, the nose tilted down sharply. In both cases, they recovered quickly after disconnecting the autopilot.

American Airlines and Southwest Airlines operate the 737 Max 8, and United Airlines flies a slightly larger version, the Max 9. All three carriers vouched for the safety of Max aircraft on Wednesday.

The pilot reports were filed last year in a data base compiled by NASA. They are voluntary safety reports and do not publicly reveal the names of pilots, the airlines or the location of the incidents. It was unclear whether the accounts led to any actions by the FAA or the pilots’ airlines.

However, leading the push against US grounding, a vice president of American, the world’s biggest carrier, which has 24 Max 8s, said it has “full confidence in the aircraft.” At the same time, the Southwest Airlines Pilots Association president Captain Jonathan L. Weaks put out a lengthy statement saying, “The data supports Southwest’s continued confidence in the airworthiness and safety of the MAX. … We fully support Southwest Airlines’ decision to continue flying the MAX and the FAA’s findings to date. I will continue to put my family, friends, and loved ones on any Southwest flight and the main reason is you, the Pilots of SWAPA.”

A United pilot echoed that sentiment, telling CBS News, “It’s a safe airplane. I’d put my family on it.”

Boeing has said it has no reason to pull the popular aircraft from the skies and it doesn’t intend to issue new recommendations about the aircraft to customers. Boeing’s CEO Dennis Muilenburg spoke with President Trump and reiterated that the 737 Max 8 is safe, the company said. Its technical team, meanwhile, joined American, Israeli, Kenyan and other aviation experts in the investigation led by Ethiopian authorities.

The FAA said it was reviewing all available data. It said it expects Boeing will soon complete software improvements to the automated anti-stall system suspected of contributing to the Lion Air crash.

“Thus far, our review shows no systemic performance issues and provides no basis to order grounding the aircraft,” acting FAA Administrator Daniel K. Elwell said in a statement. “Nor have other civil aviation authorities provided data to us that would warrant action.”

The FAA’s cavalier response has prompted accusations of “cozying” up to the industry, with Bill McGee, aviation adviser for Consumer Reports, saying the FAA has increasingly become cozy with airplane manufacturers and airlines when it should be more pro-active in safety. The magazine and website on Tuesday called on airlines and the FAA to ground the 737 Max planes until an investigation into the cause of the Ethiopian crash is completed to see if it’s related to the Lion Air crash in October.

“They have not presented any evidence that the problems that we’ve seen with these two crashes are not problems that could potentially exist here in the U.S.,” McGee said.

“Increasingly, the FAA is relying more and more on what the industry calls electronic surveillance,” added McGee, who has written about aviation for nearly two decades. “Not going out and kicking the tires, seeing the work being done, making sure it’s being done properly.”

Former Transportation Secretary Ray LaHood also called for the U.S. to ground the 737 Max, just as his agency halted flights of Boeing 787s six years ago because of overheating lithium-ion battery packs. “These planes need to be inspected before people get on them,” LaHood said Tuesday. “The flying public expects somebody in the government to look after safety, and that’s DOT’s responsibility.”

But veteran accident investigators defended the FAA, which has said there’s no data to link the two crashes.

“I don’t see the facts to justify what they’ve done,” John Goglia, an independent safety consultant and former member of the National Transportation Safety Board, said of the moves by other countries to stop the Max 8 from flying. “If they have facts, I wish they would share them with the rest of the world so we can protect the air-traveling public.”

The FAA said it was reviewing all available data, and so far had found no basis to ground the planes.

John Cox, president and CEO of the aviation consultancy Safety Operating Systems, said countries that have grounded the Max 8 may have linked the Ethiopian and Indonesian crashes even though investigators had yet to analyze the Ethiopian plane’s black boxes.

“The FAA is on solid ground so far,” said Cox, a former airline pilot and accident investigator. “But politics may overwhelm them if enough members get together and demand the planes be grounded.”

Sandy Morris, an aerospace analyst at Jefferies in London, called the string of bans on the Boeing Max jets unprecedented.

“It seems like a rebellion against the FAA,” Morris said.

via ZeroHedge News https://ift.tt/2Tx503P Tyler Durden

Finland’s government has collapsed just weeks before the general election. New socialist and communist reforms have failed due to the rising costs of healthcare.

Healthcare costs, which are high because of governments, have caused the collapse of the Finnish government. Prime Minister Juha Sipila and the rest of the cabinet resigned after the governing coalition failed to pass reforms in parliament to the country’s regional government and health services, the Wall Street Journalreports.

Finland, like much of the developed world, faces an aging population, with around 26 percent of its citizens expected to be over 65 by the year 2030, an increase of 5 percent from today. The strain on the socialized medical system is impossible to ignore, and cannot be fixed by more government interference.

And the problems with socialism continue, as money is taken from some and given to others, eventually, the takers will outnumber the makers.

As an increasing number of people live longer in retirement, the cost of providing pension and healthcare benefits can rise. Those increased costs are paid for by taxes collected from of the working-age population – who make up a smaller percentage of the population than in decades past. -BBC

The only reform that could possibly help these failing systems is to have the government step back and let competition and the free market thrive. Of course, that’s the one thing governments cannot and will not do because it means giving up power and control over people’s lives.

Reuters reports that soaring treatment costs and longer life spans have particularly affected Nordic countries. It isn’t just Finland. Sweden and Denmark face similar bleak outlooks for their socialism as well.

“Nordic countries, where comprehensive welfare is the cornerstone of the social model, have been among the most affected,”according to Reuters.

“But reform has been controversial and, in Finland, plans to cut costs and boost efficiency have stalled for years.”

The Kaiser Family Foundation found that 58 percent of Americans oppose “Medicare for all” if told it would eliminate private health insurance plans, and 60 percent oppose it if it requires higher taxes, according to a report by the Washington Free Beacon. Americans are general living paycheck to paycheck and already suffer under an unjust and burdensome tax system. Socialized medicine would mean one thing is for certain: more of your money will be stolen from you to pay for it. It isn’t about giving everyone healthcare, it’s about a boost in power and control for government officials and politicians who think they have the right to steal from us and run our lives.

When is enough enough?

via ZeroHedge News https://ift.tt/2HtDFIB Tyler Durden

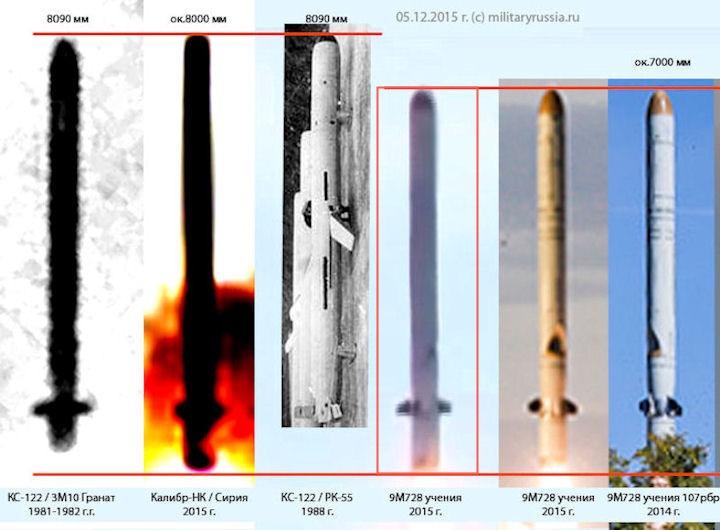

The Pentagon will begin work on fabricating components for a new ground-launched cruise missile (GLCM) formely banned under the now-suspended Range Nuclear Forces (INF) Treaty, reported Aviation Week & Space Technology (AW&ST).

The Pentagon “will commence fabrication activities on components to support developmental testing of these systems – activities that until February 2 would have been inconsistent with our obligations under the treaty,” Lt. Col. Michelle Baldanza said in a Pentagon statement.

“This research and development is designed to be reversible, should Russia return to full and verifiable compliance before we withdraw from the Treaty in August 2019,” Baldanza said.

Pentagon work only covers conventional GLCM technology and excludes nuclear weapons, the spokesperson said.

The INFY Treaty was signed by The U.S. and the U.S.S.R. in 1987 to calm nuclear war fears across Europe. The treaty required both countries to dismantle their ground-launched ballistic and cruise missiles with ranges of between 310 to 3,420 miles.

About a decade ago, the Obama administration believed Moscow was developing and testing a new GLCM with a range forbidden by the treaty. Several years later, the administration announced their concerns about the alleged Russian GLCM program. Then in 2016, Russian officials disclosed the existence of the 9M729 missile (NATO designation: SSC-8) but told the international community it did not violate the treaty.

The Trump administration unleashed a “maximum pressure” campaign on Russia, recruiting allies to pressure Moscow to comply with the INF Treaty despite the Kremlin’s denials that a violation had occurred. The administration then called in 2017 for an authorization bill that would allow the Defense Department to launch research and development on GLCM technologies.

AW&ST said the first indication that the Pentagon had moved beyond GLCM research and development was in early March. In response to a question by an AW&ST reporter about renewing GLCM systems, Army Undersecretary Ryan McCarthy said he had reviewed a report on such technology but was not sure about the current status. The Office of the Secretary of Defense confirmed to AW&ST that research and development work had started on new GLCMs.

“Because the United States has scrupulously complied with its obligations with the INF Treaty, these programs are in the early stages,” the Pentagon spokesperson said.

The INF Treaty will be terminated in August unless Washington and Moscow agree to halt the mandatory, six-month withdrawal process.

Meanwhile, Russian Ambassador to the US dismissed accusations that the missile violated the treaty as a “fairy tale.”

Frank Rose, a former U.S. assistant secretary of state for arms control now at Washington’s Brookings Institution, indicated that the Pentagon’s push for GLCM technologies could be a ploy to bate Russia back into the treaty.

“My best guess is that it is political signaling intended to make it clear the United States is serious about moving forward with the development of a new GLCM (ground-launched cruise missile) unless Russia returns to compliance with the treaty,” Rose said.

The United Nations has requested the US and Russia preserve the treaty, warning its termination later this year could make the world a much dangerous place.

via ZeroHedge News https://ift.tt/2F9cHoa Tyler Durden

After a lot of drama, British Prime Minister Theresa May came back from Brussels with a breakthrough on Brexit.

Only it wasn’t.

While the changes to the protocol that governs the implementation of the Irish Backstop are an improvement they are far fro enough to allay the rightful fears of Brexiteers and the Northern Irish.

From the beginning of this process, the EU has been in blackmail mode. They’ve made it clear that they would not negotiate in good faith or even at all. That much has been clear.

The biggest question has been whether May herself was working in the British people’s best interest or was she simply a stalking horse for further EU integration of the entire continent of Europe.

Never forget that the EU has imperial ambitions. Those that have been its architects saw it as regaining the mantle of the center of the world as the U.S. bankrupts itself maintaining an empire around the world, fighting against the rise of Russia and China.

It sits in the weeds, making byzantine bureaucratic law and building both a fiscal and political union through these under-handed back doors.

And the people of Europe have woken up to it. The Brits voted to leave the EU because of this. Euroskeptic parties are rising across Europe. The latest rebuke of the EU came in Austria’s Salzburg, a traditional center-left stronghold just voted for a Lega-style nationalist/populist majority.

Now people like Theresa May, who never supported Brexit, are using this negotiating period to hand to the EU everything it wants in the Withdrawal Agreement to blackmail the British people to accept an even worse arrangement than had they not voted to leave in the first place.

This point cannot be understated.

Because it is the model for how the EU will fight the rising opposition to its rule.

The withdrawal agreement was crafted by Germany and not negotiated by Jean-Claude Juncker and Michael Barnier to punish the U.K. for standing up to the inevitability of the EU.

It is a message and a warning to Italy, Hungary and Poland.

It was designed to cause irreparable damage to the U.K. with the long-term effects of destroying the majority political parties and fanning separatist instincts in Wales and Scotland.

And no one is more to blame for this mess than the members of Parliament who continue to virtue signal about the horrors of a no-deal which the British people have become less and less scared of every day. Poll after poll shows overwhelming rejection of May’s Merkel’s deal as well as growing support for a No-Deal Brexit.

And if the members of parliament who continue to go through the pantomime of an existential crisis would leave it aside and simply say that’s it, no deal it is, that would end the uncertainty and the worry that is now the dominant narrative in the press.

Businesses are relocating, shipments are stopping, etc. All because of Brexit, they argue. No, all because of MP’s who refuse to embrace the situation as it stands and face the reality that sovereignty is more important than a quarter or two of tightened belts and some annoying paperwork.

Moreover, the biggest fear now is the one which is that Britain ends up better off if they not only threw off the shackles of the EU but also its own corrupt and, frankly, traitorous leadership.

Theresa May’s performance in parliament before the latest vote was almost convincing. But, as always, when someone is giving you an ultimatum, my way or the highway, it’s masking an alternative choice.

The Dublin Unionist Party and the European Research Group within the Tories understand this. I suspect in his heart of hearts Labour Leader Jeremy Corbyn

And the reason for this is May was always on their side. It’s not a negotiation when there’s only one side represented. This is why Juncker et.al. refused to negotiate in any meaningful way.

They didn’t have to.

And that is simply blackmail.

What is obvious watching British parliamentarians at this late stage is that a majority of them are unwilling to face reality that the EU is not in their best interest. Because any organization that would blackmail rather than negotiate is not an organization anyone decent person would want to be a member of.

Fears over a No-Deal Brexit are overblown. If these same MP’s that are so worried about the uncertainty created by the Brexit process would simply end that uncertainty by backing No-Deal then certainty would return.

It might not be the certainty that is the easiest to swallow for both sides but it will be certainty.

Mr. Juncker made it clear there is nothing better forthcoming. That’s an insult and it should be treated as such by Parliament.

But it won’t be as MP’s roll over, show Juncker their bellies and hand-wring about how unfair it all is again later this week.

They cannot see the bigger picture that it is the EU that has the weak hand, not them. They are too blinded by ideology and fear to see that.

* * *

Join My Patreon to get ideas on how to make Brexit work for you.

via ZeroHedge News https://ift.tt/2VPnpp8 Tyler Durden

Due to their indiscriminate and devastating effects, the long-lasting threat posed by their presence and the painstaking efforts required to remove them, anti-personnel landmines have rightfully been prohibited by the United Nations since 1997 – a treaty joined by over 150 countries.

This infographic presents facts and figures from the Landmine and Cluster Munition Monitor, shedding light on the places landmines still threaten life, the countries with the largest stockpiles and the progress being made in the fight to clear the contaminated areas.

Germany has taken the lead among European Union member states to back Washington’s regime-change agenda for Venezuela. Berlin’s hypocrisy and double-think is quite astounding.

Only a few weeks ago, German politicians and media were up in arms protesting to the Trump administration for interfering in Berlin’s internal affairs. There were even outraged complaints that Washington was seeking “regime change” against Chancellor Angela Merkel’s government.

Those protests were sparked when Richard Grenell, the US ambassador to Germany, warned German companies involved in the Nord Stream 2 gas pipeline with Russia that they could be hit with American economic sanctions if they go ahead with the Baltic seabed project.

Earlier, Grenell provoked fury among Berlin’s political establishment when he openly gave his backing to opposition party Alternative for Germany. That led to consternation and denunciations of Washington’s perceived backing for regime change in Berlin. They were public calls for Grenell to be expelled over his apparent breach of diplomatic protocols.

Now, however, Germany is shamelessly kowtowing to an even more outrageous American regime-change plot against Venezuela.

Last week, the government of President Nicolas Maduro ordered the expulsion of German ambassador Daniel Kriener after he greeted the US-backed opposition figure Juan Guaido on a high-profile occasion. Guaido had just returned from a tour of Latin American countries during which he had openly called for the overthrow of the Maduro government. Arguably a legal case could be made for the arrest of Guaido by the Venezuelan authorities on charges of sedition.

When Guaido returned to Venezuela on March 4 he was greeted at the airport by several foreign diplomats. Among the receiving dignitaries was Germany’s envoy Daniel Kriener.

The opposition figure had declared himself “interim president” of Venezuela on January 23 and was immediately recognized by Washington and several European Union states. The EU has so far not issued an official endorsement of Guaido over incumbent President Maduro. Italy’s objection blocked the EU from adopting a unanimous position.

Nevertheless, as the strongest economy in the 28-member bloc, Germany can be seen as de facto leader of the EU. Its position on Venezuela therefore gives virtual EU gravitas to the geopolitical maneuvering led by Washington towards the South American country.

What’s more, the explicit backing of Juan Guaido by Germany’s envoy was carried out on the “express order” of Foreign Minister Heiko Maas, according to Deutsche Welle.

“It was my express wish and request that Ambassador Kriener turn out with representatives of other European nations and Latin American ones to meet acting President Guaido at the airport,” said Maas.

“We had information that he was supposed to be arrested there. I believe that the presence of various ambassadors helped prevent such an arrest.”

It’s staggering to comprehend the double-think involved here.

Guaido was hardly known among the vast majority of Venezuelans until he catapulted on to the global stage by declaring himself “interim president”. That move was clearly executed in a concerted plan with the Trump White House. European governments and Western media have complacently adopted the White House line that Guaido is the legitimate leader while socialist President Maduro is a “usurper”.

That is in spite of the fact that Maduro was re-elected last year in free and fair elections by a huge majority of votes. Guaido’s rightwing, pro-business party boycotted the elections. Yet he is anointed by Washington, Berlin and some 50 other states as the legitimate leader.

Russia, China, Turkey, Cuba and most other members of the United Nations have refused to adopt Washington’s decree of recognizing Guaido. Those nations (comprising 75 per cent of the UN assembly) continue to recognize President Maduro as the sovereign authority. Indeed, Russia has been highly critical of Washington’s blatant interference for regime change in oil-rich Venezuela. Moscow has warned it will not tolerate US military intervention.

Russia’s envoy to the UN Vasily Nebenzia, at a Security Council session last month, excoriated the US for its gross violation of international law with regard to Venezuela. Moscow’s diplomat also directed a sharp rebuke at other nations “complicit” in Washington’s aggression, saying that one day “you will be next” for similar American subversion in their own affairs.

Germany’s hypocrisy and double-think is, to paraphrase that country’s national anthem, “über alles” (above all else).

German politicians, diplomats and media were apoplectic in their anger at perceived interference by the US ambassador in Berlin’s internal affairs. Yet the German political establishment has no qualms whatsoever about ganging up – only weeks later – with Washington to subvert the politics and constitution of Venezuela.

How can Germany be so utterly über servile to Washington and the latter’s brazen criminal aggression towards Venezuela?

It seems obvious that Berlin is trying to ingratiate itself with the Trump administration. But what for?

Trump has been pillorying Germany with allegations of “unfair trade” practices. In particular, Washington is recently stepping up its threats to slap punitive tariffs on German auto exports. Given that this is a key sector in the German export-driven economy, it may be gleaned that Berlin is keen to appease Trump. By backing his aggression towards Venezuela?

Perhaps this policy of appeasement is also motivated by Berlin’s concern to spare the Nord Stream 2 project from American sanctions. When NS2 is completed later this year, it is reckoned to double the capacity of natural gas consumption by Germany from Russia. That will be crucial for Germany’s economic growth.

Another factor is possible blackmail of Berlin by Washington. Recall the earth-shattering revelations made by American whistleblower Edward Snowden a few years back when he disclosed that US intelligence agencies were tapping the personal phone communications of Chancellor Merkel and other senior Berlin politicians. Recall, too, how the German state remarkably acquiesced over what should have been seen as a devastating infringement by Washington.

The weird lack of action by Berlin over that huge violation of its sovereignty by the Americans makes one wonder if the US spies uncovered a treasure trove of blackmail material on German politicians.

Berlin’s pathetic kowtowing to Washington’s interference in Venezuela begs an ulterior explanation. No self-respecting government could be so hypocritical and duplicitous.

Whatever Berlin may calculate to gain from its unscrupulous bending over for Washington, one thing seems clear, as Russian envoy Nebenzia warned: “One day you are next” for American hegemonic shafting.

via ZeroHedge News https://ift.tt/2XV6H9G Tyler Durden