Simply put, you have the right to remain out of prison… even if you are not a US citizen…

Source: Online-Paralegal-Programs.com

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/dLFsAEfeL8g/story01.htm Tyler Durden

another site

Simply put, you have the right to remain out of prison… even if you are not a US citizen…

Source: Online-Paralegal-Programs.com

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/dLFsAEfeL8g/story01.htm Tyler Durden

From Ron Paul

Iraq: The ‘Liberation’ Neocons Would Rather Forget

Remember Fallujah? Shortly after the 2003 invasion of Iraq, the US military fired on unarmed protestors, killing as many as 20 and wounding dozens. In retaliation, local Iraqis attacked a convoy of US military contractors, killing four. The US then launched a full attack on Fallujah to regain control, which left perhaps 700 Iraqis dead and the city virtually destroyed.

According to press reports last weekend, Fallujah is now under the control of al-Qaeda affiliates. The Anbar province, where Fallujah is located, is under siege by al-Qaeda. During the 2007 “surge,” more than 1,000 US troops were killed “pacifying” the Anbar province. Although al-Qaeda was not in Iraq before the US invasion, it is now conducting its own surge in Anbar.

For Iraq, the US “liberation” is proving far worse than the authoritarianism of Saddam Hussein, and it keeps getting worse. Last year was Iraq’s deadliest in five years. In 2013, fighting and bomb blasts claimed the lives of 7,818 civilians and 1,050 members of the security forces. In December alone nearly a thousand people were killed.

I remember sitting through many hearings in the House International Relations Committee praising the “surge,” which we were told secured a US victory in Iraq. They also praised the so-called “Awakening,” which was really an agreement by insurgents to stop fighting in exchange for US dollars. I always wondered what would happen when those dollars stopped coming.

Where are the surge and awakening cheerleaders now?

One of them, Richard Perle, was interviewed last year on NPR and asked whether the Iraq invasion that he pushed was worth it. He replied:

I’ve got to say I think that is not a reasonable question. What we did at the time was done in the belief that it was necessary to protect this nation. You can’t a decade later go back and say, well, we shouldn’t have done that.

Many of us were saying all along that we shouldn’t have done that – before we did it. Unfortunately the Bush Administration took the advice of the neocons pushing for war and promising it would be a “cakewalk.” We continue to see the results of that terrible mistake, and it is only getting worse.

Last month the US shipped nearly a hundred air-to-ground missiles to the Iraqi air force to help combat the surging al-Qaeda. Ironically, the same al-Qaeda groups the US is helping the Iraqis combat are benefiting from the US covert and overt war to overthrow Assad next door in Syria. Why can’t the US government learn from its mistakes?

The neocons may be on the run from their earlier positions on Iraq, but that does not mean they have given up. They were the ones pushing for an attack on Syria this summer. Thankfully they were not successful. They are now making every effort to derail President Obama’s efforts to negotiate with the Iranians. Just last week William Kristol urged Israel to attack Iran with the hope we would then get involved. Neoconservative Senators from both parties recently introduced the Nuclear Weapon Free Iran Act of 2013, which would also bring us back on war-footing with Iran.

Next time the neocons tell us we must attack, just think “Iraq.”

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/fYSLOJBAdUs/story01.htm Tyler Durden

From Ron Paul

Iraq: The ‘Liberation’ Neocons Would Rather Forget

Remember Fallujah? Shortly after the 2003 invasion of Iraq, the US military fired on unarmed protestors, killing as many as 20 and wounding dozens. In retaliation, local Iraqis attacked a convoy of US military contractors, killing four. The US then launched a full attack on Fallujah to regain control, which left perhaps 700 Iraqis dead and the city virtually destroyed.

According to press reports last weekend, Fallujah is now under the control of al-Qaeda affiliates. The Anbar province, where Fallujah is located, is under siege by al-Qaeda. During the 2007 “surge,” more than 1,000 US troops were killed “pacifying” the Anbar province. Although al-Qaeda was not in Iraq before the US invasion, it is now conducting its own surge in Anbar.

For Iraq, the US “liberation” is proving far worse than the authoritarianism of Saddam Hussein, and it keeps getting worse. Last year was Iraq’s deadliest in five years. In 2013, fighting and bomb blasts claimed the lives of 7,818 civilians and 1,050 members of the security forces. In December alone nearly a thousand people were killed.

I remember sitting through many hearings in the House International Relations Committee praising the “surge,” which we were told secured a US victory in Iraq. They also praised the so-called “Awakening,” which was really an agreement by insurgents to stop fighting in exchange for US dollars. I always wondered what would happen when those dollars stopped coming.

Where are the surge and awakening cheerleaders now?

One of them, Richard Perle, was interviewed last year on NPR and asked whether the Iraq invasion that he pushed was worth it. He replied:

I’ve got to say I think that is not a reasonable question. What we did at the time was done in the belief that it was necessary to protect this nation. You can’t a decade later go back and say, well, we shouldn’t have done that.

Many of us were saying all along that we shouldn’t have done that – before we did it. Unfortunately the Bush Administration took the advice of the neocons pushing for war and promising it would be a “cakewalk.” We continue to see the results of that terrible mistake, and it is only getting worse.

Last month the US shipped nearly a hundred air-to-ground missiles to the Iraqi air force to help combat the surging al-Qaeda. Ironically, the same al-Qaeda groups the US is helping the Iraqis combat are benefiting from the US covert and overt war to overthrow Assad next door in Syria. Why can’t the US government learn from its mistakes?

The neocons may be on the run from their earlier positions on Iraq, but that does not mean they have given up. They were the ones pushing for an attack on Syria this summer. Thankfully they were not successful. They are now making every effort to derail President Obama’s efforts to negotiate with the Iranians. Just last week William Kristol urged Israel to attack Iran with the hope we would then get involved. Neoconservative Senators from both parties recently introduced the Nuclear Weapon Free Iran Act of 2013, which would also bring us back on war-footing with Iran.

Next time the neocons tell us we must attack, just think “Iraq.”

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/fYSLOJBAdUs/story01.htm Tyler Durden

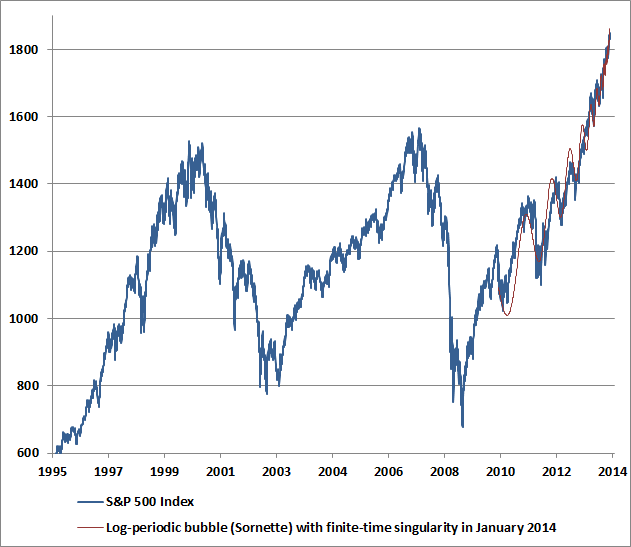

Confidence abounds. Last week, Investor’s Intelligence reported a surge in advisory sentiment to the highest bullish percentage since October 19, 2007. John Hussman notes that NAAIM reported that the 3-week average equity exposure among its members increased to the highest level on record. Given the unfortunate resolution of similarly extreme overvalued, overbought, overbullish, rising-yield periods in history, it's almost mind-boggling that investors actually expect the present speculative run to end well. The accelerating pitch and shallowing corrections of the recent advance are worth noting.

Based on the fidelity of the recent advance to this price structure, we estimate the “finite-time singularity” of the present log-periodic bubble to occur (or to have occurred) somewhere between December 31, 2013 and January 13, 2014. That does not mean that prices must immediately crash – only that the dynamics will then lend themselves to a great deal of potential instability, if prior log-periodic bubbles in equity and commodity markets across history are any indication. It bears repeating that our own defensiveness is driven by a broad ensemble of evidence, not simply price dynamics, not simply valuations, not simply sentiment, but the “full catastrophe” – which includes the fact that strong economic, speculative and monetary enthusiasm has historically been quite a contrary indicator for stocks.

The chart below shows the current position of the S&P 500. The light red line shows the log-periodic price trajectory that most closely approximates the present overvalued, overbought, overbullish, Fed-induced speculative run since 2010. While the initial gains from the 2009 low until about mid-2010 represented what we view as a move from reasonable valuation to full valuation (our stress-testing “miss” was not on valuation grounds), I expect little, if any of the market’s gains since 2010 to be retained by investors over the completion of this market cycle. Despite very short-run uncertainties about market direction, I should note that we now estimate negative prospective total returns for the S&P 500 on every horizon of less than 7 years.

And this is what Hussman said in 2007…

“Wall Street remains exuberant about economic prospects. Last week brought a 6-year high in consumer confidence, evidently supporting the idea that the consumer remains strong and the economic expansion remains intact. Unfortunately, if you examine the data, you'll quickly discover that consumer confidence is a lagging indicator, well explained by past movements in GDP, employment, and capacity utilization. Worse, for the stock market, it's a contrary indicator.

This is a fact that I've noted at both extremes, not only in early 2000 when new highs in consumer confidence supported a defensive position, but conversely in the early 1990's, when new lows in consumer confidence supported a leveraged position in stocks. High levels of economic optimism are regularly observed at the peaks of both U.S. and foreign economic expansions.

This includes the general consensus of individuals, businesses, politicians, central bank officials and notoriously – economists. That shouldn't be surprising. It's the very nature of a peak that it can't be produced except by unusual optimism.”

Hussman Weekly Market Comment, 08/06/07 Strong Economic Optimism (… is a Contrary Indicator)

Sound familiar?

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/upE3ojmwL1U/story01.htm Tyler Durden

While Japanese imports are surging on the back of an ever-depreciating currency and ever-appreciating cost of energy, it would appear the enterprising Easterners have come up with a solution to two problems – exports and radiation. As RT reports, more than 130 "contaminated" used cars from Japan were denied access to Russia last year. The consumer watchdog agency Rospotrebnadzor is also closely monitoring deliveries of fish.

A customs officer holds up a device used for measuring radiation levels, while standing in front of vehicles delivered from Japan, in Russia's far eastern city of Vladivostok.

…

Strict control of all cargo, arriving from Japan, will continue in 2014 as well, Rospotrebnadzor said on its website.

“In 2013, Russia has banned 165 batches of contaminated goods from entering the country. There were mainly used cars – 132, and spare parts for vehicles – 33,” the statement said.

Deliveries of fish coming from Japan and those caught in the Pacific Ocean are also being monitored, the agency said.

“Particular attention is paid to this issue in Russia’s Far East, where radiation control of fish is being wieldy implemented, including the distribution chain,” Rospotrebnadzor said.

The supply of Japanese fish to Russia is currently allowed only under a special declaration that confirms the presence of radioactive substances in the products is within safety standards established by the Customs Union of Russia, Belarus and Kazakhstan.

…

It seems the world is also losing interest in one of Japan's other major exports – Blue-Fin Tuna (as prices have dropped 95% from last year!)

Sushi restaurateur Kiyoshi Kimura paid 7.36m yen (£43,000) for a 230kg (507lb) bluefin tuna in the year's celebratory first auction at Tokyo's Tsukiji market on Sunday – just 5% of what he paid a year earlier despite signs that the species is in serious decline.

…

There were 1,729 tuna sold in Sunday's first auction for 2014, according to the city government, down from 2,419 last year. The 32,000 yen ($305) per kilogram paid for the top fish this year compares with 700,000 yen per kilogram last year.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/EZ0SuiGJU9U/story01.htm Tyler Durden

While Japanese imports are surging on the back of an ever-depreciating currency and ever-appreciating cost of energy, it would appear the enterprising Easterners have come up with a solution to two problems – exports and radiation. As RT reports, more than 130 "contaminated" used cars from Japan were denied access to Russia last year. The consumer watchdog agency Rospotrebnadzor is also closely monitoring deliveries of fish.

A customs officer holds up a device used for measuring radiation levels, while standing in front of vehicles delivered from Japan, in Russia's far eastern city of Vladivostok.

…

Strict control of all cargo, arriving from Japan, will continue in 2014 as well, Rospotrebnadzor said on its website.

“In 2013, Russia has banned 165 batches of contaminated goods from entering the country. There were mainly used cars – 132, and spare parts for vehicles – 33,” the statement said.

Deliveries of fish coming from Japan and those caught in the Pacific Ocean are also being monitored, the agency said.

“Particular attention is paid to this issue in Russia’s Far East, where radiation control of fish is being wieldy implemented, including the distribution chain,” Rospotrebnadzor said.

The supply of Japanese fish to Russia is currently allowed only under a special declaration that confirms the presence of radioactive substances in the products is within safety standards established by the Customs Union of Russia, Belarus and Kazakhstan.

…

It seems the world is also losing interest in one of Japan's other major exports – Blue-Fin Tuna (as prices have dropped 95% from last year!)

Sushi restaurateur Kiyoshi Kimura paid 7.36m yen (£43,000) for a 230kg (507lb) bluefin tuna in the year's celebratory first auction at Tokyo's Tsukiji market on Sunday – just 5% of what he paid a year earlier despite signs that the species is in serious decline.

…

There were 1,729 tuna sold in Sunday's first auction for 2014, according to the city government, down from 2,419 last year. The 32,000 yen ($305) per kilogram paid for the top fish this year compares with 700,000 yen per kilogram last year.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/EZ0SuiGJU9U/story01.htm Tyler Durden

I saw this headline (or something to the effect) somewhere: “Number of Bullish Newsletter Writers Highest Since 2007 Top”.

Ahhh….run for the hills!

To see more proprietary market data, visit TacticalBeta; it is absolutely,100% FREE!! Go to TacticalBeta Now!

The percentage of bullish newsletter writers in the Investors Intelligence sentiment poll now sits at 61.2. This is the highest value since October, 2007, which is exactly 1 week after the SP500 peaked and then went on to drop over 50% in the next 18 months. There must be some meaning to this number. Right?

However, as I showed in the article, “Weekly Sentiment Report: A Noteworthy Extreme (This Is Not What You Think)”, such extremes in the sentiment data are just that– extremes in the data. So while greater than 60% bullish newsletter writers was seen at the 2007 top, this number was also seen throughout the history of the data series and the market did not fall apart or find itself in a bear market over the next year. See figure 1 of examples over the past 15 years. In fact, having lots of bulls, like having extremes in the number of bears, generally does not imply what you think. Certainly, I would not run for the hills based upon 1 number.

Figure 1. % Bullish Newsletter Writers/ weekly

But this should not imply a green light or an “all clear” signal either. From our perspective, I would rather be a buyer (as the data supports) when investors are bearish, and I would rather be a seller when they are bullish. At this point in the price cycle, the trend of prices should begin to flatten out. Rather than being a seller at some extreme point, we typically wait until investor sentiment unwinds. More specifically, we will sell our equity positions 1 week after the “dumb money” indicator crosses below the upper trading band. See figure 4 (below) for details.

The extremes in bullish sentiment that we are currently seeing really suggest that we are late in the current price move. Furthermore, I can certainly state that there are issues under the surface. One issue is the willingness of investors to buy the dip on shorter and shorter time frames. In essence, a market that doesn’t periodically clear itself of the weak hands (i.e., a big, nasty sell off) is a market built on a weak foundation. A second issue is the negative divergence that we are seeing between the $VIX and the SP500. As prices go higher, we should expect the $VIX to move lower, but the $VIX has been unable to break below a level of 12 over the past 12 months despite the near 30% gain in the SP500. As figure 2 below shows, selling has occurred when the $VIX tags the 12 level, but from a big picture perspective, the $VIX has failed to confirm the price move in the SP500. Furthermore, a weekly close above 14.64 on the $VIX would highly suggest a deeper and prolonged sell off in prices. I discussed the implications of support and resistance in the $VIX in this video back in September, 2013.

Figure 2. $VIX/ weekly

Our equity model, which is built around the “dumb money” indicator (see figure 4 below), remains bullish, and will likely remain so for another 2 weeks or more. This current trade has gone on for 17 weeks now when we became bullish during a period of extreme investor bearishness, and it is our expectation that this trade should last on average 15 weeks. The best, most accelerated gains typically occur in the beginning of the trade. Just when investors typically get the all clear, the trend will flatten out. Our plan is to become sellers of equities when investor sentiment unwinds, but we are not at that point. As a reminder, we have moved our stop loss up to SP500 1706.92.

In the final analysis, there are reasons for concern as investors have become and remain extremely bullish. Would I run for the hills? Not yet, but with every passing week, we are getting closer to that point. That’s the conundrum investors must face if they want in to this market now.

Figure 3 is our composite sentiment indicator. This is the data behind the “Sentimeter”. This is our most comprehensive equity market sentiment indicator, and it is constructed from 10 different variables that assess investor sentiment and behavior. It utilizes opinion data (i.e., Investors Intelligence) as well as asset data and money flows (i.e., Rydex and insider buying). The indicator goes back to 2004. (Editor’s note: Subscribers to the TacticalBeta Gold Service have this data available for download.) This composite sentiment indicator moved to its most extreme position 10 weeks ago, and prior extremes since the 2009 are noted with the pink vertical bars. The March, 2010, February, 2011, and February, 2012 signals were spot on — warning of a market top. The November, 2010 and December, 2012 signals were failures in the sense that prices continued significantly higher. The current reading is neutral but heading towards bearish (as in too many bullish investors).

Figure 3. The Sentimeter

![]()

The “Dumb Money” indicator (see figure 4) looks for extremes in the data from 4 different groups of investors who historically have been wrong on the market: 1) Investors Intelligence; 2) MarketVane; 3) American Association of Individual Investors; and 4) the put call ratio. The indicator shows that investors are extremely bullish.

Figure 4. The “Dumb Money”

Figure 5 is a weekly chart of the SP500 with the InsiderScore “entire market” value in the lower panel. From the InsiderScore weekly report: “Market-wide sentiment continues to move further into Neutral territory, away from a Sell Bias, as transactional volume begins a seasonal decline. With earnings season beginning in two weeks, most companies have closed trading windows, limiting the ability of insiders to transact non-10b5-1 purchases and sales. “

Figure 5. InsiderScore “Entire Market” value/ weekly

![]()

To see more proprietary market data, visit TacticalBeta; it is absolutely,100% FREE!! Go to TacticalBeta Now!

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/PPstYmrmkSA/story01.htm thetechnicaltake

I saw this headline (or something to the effect) somewhere: “Number of Bullish Newsletter Writers Highest Since 2007 Top”.

Ahhh….run for the hills!

To see more proprietary market data, visit TacticalBeta; it is absolutely,100% FREE!! Go to TacticalBeta Now!

The percentage of bullish newsletter writers in the Investors Intelligence sentiment poll now sits at 61.2. This is the highest value since October, 2007, which is exactly 1 week after the SP500 peaked and then went on to drop over 50% in the next 18 months. There must be some meaning to this number. Right?

However, as I showed in the article, “Weekly Sentiment Report: A Noteworthy Extreme (This Is Not What You Think)”, such extremes in the sentiment data are just that– extremes in the data. So while greater than 60% bullish newsletter writers was seen at the 2007 top, this number was also seen throughout the history of the data series and the market did not fall apart or find itself in a bear market over the next year. See figure 1 of examples over the past 15 years. In fact, having lots of bulls, like having extremes in the number of bears, generally does not imply what you think. Certainly, I would not run for the hills based upon 1 number.

Figure 1. % Bullish Newsletter Writers/ weekly

But this should not imply a green light or an “all clear” signal either. From our perspective, I would rather be a buyer (as the data supports) when investors are bearish, and I would rather be a seller when they are bullish. At this point in the price cycle, the trend of prices should begin to flatten out. Rather than being a seller at some extreme point, we typically wait until investor sentiment unwinds. More specifically, we will sell our equity positions 1 week after the “dumb money” indicator crosses below the upper trading band. See figure 4 (below) for details.

The extremes in bullish sentiment that we are currently seeing really suggest that we are late in the current price move. Furthermore, I can certainly state that there are issues under the surface. One issue is the willingness of investors to buy the dip on shorter and shorter time frames. In essence, a market that doesn’t periodically clear itself of the weak hands (i.e., a big, nasty sell off) is a market built on a weak foundation. A second issue is the negative divergence that we are seeing between the $VIX and the SP500. As prices go higher, we should expect the $VIX to move lower, but the $VIX has been unable to break below a level of 12 over the past 12 months despite the near 30% gain in the SP500. As figure 2 below shows, selling has occurred when the $VIX tags the 12 level, but from a big picture perspective, the $VIX has failed to confirm the price move in the SP500. Furthermore, a weekly close above 14.64 on the $VIX would highly suggest a deeper and prolonged sell off in prices. I discussed the implications of support and resistance in the $VIX in this video back in September, 2013.

Figure 2. $VIX/ weekly

Our equity model, which is built around the “dumb money” indicator (see figure 4 below), remains bullish, and will likely remain so for another 2 weeks or more. This current trade has gone on for 17 weeks now when we became bullish during a period of extreme investor bearishness, and it is our expectation that this trade should last on average 15 weeks. The best, most accelerated gains typically occur in the beginning of the trade. Just when investors typically get the all clear, the trend will flatten out. Our plan is to become sellers of equities when investor sentiment unwinds, but we are not at that point. As a reminder, we have moved our stop loss up to SP500 1706.92.

In the final analysis, there are reasons for concern as investors have become and remain extremely bullish. Would I run for the hills? Not yet, but with every passing week, we are getting closer to that point. That’s the conundrum investors must face if they want in to this market now.

Figure 3 is our composite sentiment indicator. This is the data behind the “Sentimeter”. This is our most comprehensive equity market sentiment indicator, and it is constructed from 10 different variables that assess investor sentiment and behavior. It utilizes opinion data (i.e., Investors Intelligence) as well as asset data and money flows (i.e., Rydex and insider buying). The indicator goes back to 2004. (Editor’s note: Subscribers to the TacticalBeta Gold Service have this data available for download.) This composite sentiment indicator moved to its most extreme position 10 weeks ago, and prior extremes since the 2009 are noted with the pink vertical bars. The March, 2010, February, 2011, and February, 2012 signals were spot on — warning of a market top. The November, 2010 and December, 2012 signals were failures in the sense that prices continued significantly higher. The current reading is neutral but heading towards bearish (as in too many bullish investors).

Figure 3. The Sentimeter

![]()

The “Dumb Money” indicator (see figure 4) looks for extremes in the data from 4 different groups of investors who historically have been wrong on the market: 1) Investors Intelligence; 2) MarketVane; 3) American Association of Individual Investors; and 4) the put call ratio. The indicator shows that investors are extremely bullish.

Figure 4. The “Dumb Money”

F

igure 5 is a weekly chart of the SP500 with the InsiderScore “entire market” value in the lower panel. From the InsiderScore weekly report: “Market-wide sentiment continues to move further into Neutral territory, away from a Sell Bias, as transactional volume begins a seasonal decline. With earnings season beginning in two weeks, most companies have closed trading windows, limiting the ability of insiders to transact non-10b5-1 purchases and sales. “

Figure 5. InsiderScore “Entire Market” value/ weekly

![]()

To see more proprietary market data, visit TacticalBeta; it is absolutely,100% FREE!! Go to TacticalBeta Now!

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/PPstYmrmkSA/story01.htm thetechnicaltake

Submitted by Adam Taggart via Peak Prosperity,

If you would have told me that we would be in this set of circumstances today ten years ago, I would have told you you were out of your mind.

~ Brian Pretti

This week Chris speaks with Brian Pretti, managing editor of ContraryInvestor.com, a financial commentary site published by institutional buy-side portfolio managers. In their discussion, they focus on the global movement of capital since quantitative easing (QE) became the policy of the world's major central banks.

The ensuing excellent discussion is wide ranging, but the key takeaway is that capital is being herded into fewer and fewer asset classes. With such huge volumes of money at play, very crowded trades in assets like stocks and housing have resulted — bringing us back to familiar bubble territory in record time.

The key for the individual, Pretti emphasizes, is risk management. The safety many investors believe they are buying in today's markets is not real.

I think what we have got going on here in housing is we have got an investment cycle, not an economically-driven housing cycle, from the standpoint that really, never before have 40 to 50% of all residential real estate transactions been for cash. We have never seen that in prior cycles, absolutely not. You know, what is driving that? Well, in one sense – and it is not a point of blame, but more a look at the unintended consequences of what the actions of QE are – when you lower these interest rates and you take away safe rate of return in alternative assets. Five years ago you could have got 5% in a CD, a Treasury bond, even a money market fund. Well, for a lot of those people who had been savers and investors in safe assets, they do not have rate of return any more. What do they do? They take their $300-$400 thousand nest egg out of the bank, and they turn around and buy a rental property where they can theoretical get the 6%, 7% cash on cash rate of return. And all of a sudden that becomes their rate of return.

So, I think we are clearly seeing this, where assets are being lifted out of other investments – whether it is Treasurys or CDs or bank accounts – and being used to buy residential real estate. Of course, the issue becomes one of risk, meaning a Treasury bond never really needs a replacement roof, and the water heater does not break, and there are no vacancies. So, we are increasing risk in these asset class choices and investment choices, but it is a forced choice, because there is no other rate of return. And for people who need that to live, that is why I think we are seeing the big cash transaction levels that we have never really seen before.

Second part of the equation, foreign money is absolutely on the move. I mean, we are talking on the first business day of the new year, and one of the things that is in the news this morning and being talked about is, Is there going to be some type of an IMF-driven 10% deposit tax in the Euro banking system? Well, this has been being talked about now for probably two, three, four months. The trial balloons go up in the air. The Euro banking crowd has also talked about potentially negative interest rates. So may be a very simple question, Chris. If you are a Euro citizen and your net worth is caught up in euros and/or you have assets in the Euro banking system, what do you do? You get them out before something like this happens.

And really, maybe we can draw the parallels, too, with Japan, where we have seen monetary debasement and true currency debasement in very violent form over the last year since Abe’s been elected. If you are a Japanese citizen and your net worth is caught up in yen, you have lost 20% of your global purchasing power. What do you do? Capital begins to move globally.

And I think part of what we are seeing – well, maybe one last piece here, too, is, the current leadership in China is cracking down on corruption. So, I know you know full well, moving capital out of China is illegal. There is only one way to get it out. You have got to have serious capital. So, what is it doing? It is hiding in alternative assets globally. It is coming to what it perceives, for now, the perception of safety that maybe includes the U. S. dollar, and if you are coming to the U. S. dollar, what do you do? Well, you can buy bonds, you can buy stocks, you can buy a business, you can buy real estate, and because safe rate of return has been basically taken away, real estate and perhaps stocks, too, are a repository for that foreign capital.

And then, maybe lastly more than not, that global capital being on the move is concentrating in some of these geographic areas that we are seeing. I mean, prices in the New Yorks, prices in the Londons, prices in the San Francisco Bay Areas are just really off the charts here. So this is very much unlike prior cycles where we saw – and I know this sounds a little simplistic and Pollyannaish – but we see younger families getting jobs, making a little bit more money. All of a sudden, they can afford a home; they take on a mortgage purchase application. Maybe they buy your or my house and the food chain moves up. That is not happening this time. So, this is really an investment cycle, as opposed to a true economically-driven housing cycle.

And I just ask myself, is the lynch pin in all of this the dividing line of alternative rates of return, meaning interest rates? And as we saw rates pick up really since May of last year, we saw things like mortgage purchase apps and refi apps just drop like a rock. So as we move forward, these big metrics that are the interest rates that are Treasury rates are very, very meaningful. And will they be the catalyst of change, ultimately, in the housing cycle, as opposed to the economy being that catalyst? We are just seeing something very different this time.

The minute the Fed started talking about tapering – I mean, if we roll the clock back to 2009 when the Fed started their QE extravaganza, that money absolutely got into U.S. equities and got into U. S. bonds. But as the money kept being printed, it rolled across Planet Earth. It got into the emerging markets, it got into their bonds, their currencies, their equities. It got into global real estate, it got into gold, it got into commodities. The minute the 'taper' keyword was starting to be used by the Fed, all of a sudden, global investors were anticipating the recission of that tidal wave of liquidity. And all of a sudden, these asset classes started to contract to the point where it is really U.S. equities, the very large blue-chip global equities here that continue to perform well. They offer yields higher than safe bonds, for now, and are also the only place we are seeing rate of return.

But within this, we are herding capital into a very, very small sector of asset classes. And then lastly, fortunately or unfortunately, when we have the global central bankers and the global politicians doing what they are doing – Europe, we may take 10% of your assets in the European banking system. Europe, we may invoke negative interest rates; you bring a dollar into a bank, we will give you back 99 ½ cents. You cause capital to move, potentially, and to me this is a big issue. I think 2013 was driven as much by momentum, and there is no place else to go, and all those other wonderful things, as it was driven by the weight and movement of global capital. Global capital coming out of China, because it was scared of – if we are going to crack down on corruption and you have got corrupt capital, you get it out right away. Japan, the drop in the yen, you have got to move some of your capital to an alternative venue in an alternative currency. Europe, the threat of confiscation, and maybe just the basic question of, What the heck is the euro going to look like in three years? I know if my net worth was caught up in euros, I sure as heck would not be 100% vested in the euro.

So, a lot of this, I think, too, is global capital is hiding in an asset class that it considers to be relatively safe, because all these other asset classes have proven to be unsafe. And for right or for wrong, in U.S. and really large blue-chip globals, they have been very, very good stewards of capital over time. Their balance sheets are relatively clean, and if you are looking for safety, then this is just a very simple question. Would you rather lever your family’s balance sheet to one of the global governments, or would you rather lever it to Johnson & Johnson? Which one do you trust more? Which one is going to take better care of your capital over time?

So I think there are so many different factors that have been forcing capital into these narrow asset classes that basically are equities and real estate. The key issue to me, going forward, is risk management. For people who sat this one out, for people who have said, Hey, wait a minute; I am looking at the Bob Shiller CAPE ratio here, and we are at levels that we have only seen four times in the last 100 years.You have got to be kidding me. I am not getting into this thing. The only way to participate in these markets, in my mind, is to make sure that you have a plan for managing risk, period. This is not throw your money into the equity market and hope for a great 2014, because every year that the market was up like it was last year was followed by a year that blah, blah, blah. It does not matter. It is about making sure that we manage risk. And we need to draw hard lines underneath certain levels of capital.

Very easy to say, but for your listeners, too, I think this comes down to individual families and making an assessment of how much risk they can afford to take. Below that line, they do not allow it to happen. I know it may sound trite:You have every day of your life to get back into the market, but sometimes you do not have a second chance to get out.

Click the play button below to listen to Chris' interview with Brian Pretti (101m:31s):

Click here to read the full transcript

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/_bL7yKXfbhc/story01.htm Tyler Durden

Submitted by Adam Taggart via Peak Prosperity,

If you would have told me that we would be in this set of circumstances today ten years ago, I would have told you you were out of your mind.

~ Brian Pretti

This week Chris speaks with Brian Pretti, managing editor of ContraryInvestor.com, a financial commentary site published by institutional buy-side portfolio managers. In their discussion, they focus on the global movement of capital since quantitative easing (QE) became the policy of the world's major central banks.

The ensuing excellent discussion is wide ranging, but the key takeaway is that capital is being herded into fewer and fewer asset classes. With such huge volumes of money at play, very crowded trades in assets like stocks and housing have resulted — bringing us back to familiar bubble territory in record time.

The key for the individual, Pretti emphasizes, is risk management. The safety many investors believe they are buying in today's markets is not real.

I think what we have got going on here in housing is we have got an investment cycle, not an economically-driven housing cycle, from the standpoint that really, never before have 40 to 50% of all residential real estate transactions been for cash. We have never seen that in prior cycles, absolutely not. You know, what is driving that? Well, in one sense – and it is not a point of blame, but more a look at the unintended consequences of what the actions of QE are – when you lower these interest rates and you take away safe rate of return in alternative assets. Five years ago you could have got 5% in a CD, a Treasury bond, even a money market fund. Well, for a lot of those people who had been savers and investors in safe assets, they do not have rate of return any more. What do they do? They take their $300-$400 thousand nest egg out of the bank, and they turn around and buy a rental property where they can theoretical get the 6%, 7% cash on cash rate of return. And all of a sudden that becomes their rate of return.

So, I think we are clearly seeing this, where assets are being lifted out of other investments – whether it is Treasurys or CDs or bank accounts – and being used to buy residential real estate. Of course, the issue becomes one of risk, meaning a Treasury bond never really needs a replacement roof, and the water heater does not break, and there are no vacancies. So, we are increasing risk in these asset class choices and investment choices, but it is a forced choice, because there is no other rate of return. And for people who need that to live, that is why I think we are seeing the big cash transaction levels that we have never really seen before.

Second part of the equation, foreign money is absolutely on the move. I mean, we are talking on the first business day of the new year, and one of the things that is in the news this morning and being talked about is, Is there going to be some type of an IMF-driven 10% deposit tax in the Euro banking system? Well, this has been being talked about now for probably two, three, four months. The trial balloons go up in the air. The Euro banking crowd has also talked about potentially negative interest rates. So may be a very simple question, Chris. If you are a Euro citizen and your net worth is caught up in euros and/or you have assets in the Euro banking system, what do you do? You get them out before something like this happens.

And really, maybe we can draw the parallels, too, with Japan, where we have seen monetary debasement and true currency debasement in very violent form over the last year since Abe’s been elected. If you are a Japanese citizen and your net worth is caught up in yen, you have lost 20% of your global purchasing power. What do you do? Capital begins to move globally.

And I think part of what we are seeing – well, maybe one last piece here, too, is, the current leadership in China is cracking down on corruption. So, I know you know full well, moving capital out of China is illegal. There is only one way to get it out. You have got to have serious capital. So, what is it doing? It is hiding in alternative assets globally. It is coming to what it perceives, for now, the perception of safety that maybe includes the U. S. dollar, and if you are coming to the U. S. dollar, what do you do? Well, you can buy bonds, you can buy stocks, you can buy a business, you can buy real estate, and because safe rate of return has been basically taken away, real estate and perhaps stocks, too, are a repository for that foreign capital.

And then, maybe lastly more than not, that global capital being on the move is concentrating in some of these geographic areas that we are seeing. I mean, prices in the New Yorks, prices in the Londons, prices in the San Francisco Bay Areas are just really off the charts here. So this is very much unlike prior cycles where we saw – and I know this sounds a little simplistic and Pollyannaish – but we see younger families getting jobs, making a little bit more money. All of a sudden, they can afford a home; they take on a mortgage purchase application. Maybe they buy your or my house and the food chain moves up. That is not happening this time. So, this is really an investment cycle, as opposed to a true economically-driven housing cycle.

And I just ask myself, is the lynch pin in all of this the dividing line of alternative rates of return, meaning interest rates? And as we saw rates pick up really since May of last year, we saw things like mortgage purchase apps and refi apps just drop like a rock. So as we move forward, these big metrics that are the interest rates that are Treasury rates are very, very meaningful. And will they be the catalyst of change, ultimately, in the housing cycle, as opposed to the economy being that catalyst? We are just seeing something very different this time.

The minute the Fed started talking about tapering – I mean, if we roll the clock back to 2009 when the Fed started their QE extravaganza, that money absolutely got into U.S. equities and got into U. S. bonds. But as the money kept being printed, it rolled across Planet Earth. It got into the emerging markets, it got into their bonds, their currencies, their equities. It got into global real estate, it got into gold, it got into commodities. The minute the 'taper' keyword was starting to be used by the Fed, all of a sudden, global investors were anticipating the recission of that tidal wave of liquidity. And all of a sudden, these asset classes started to contract to the point where it is really U.S. equities, the very large blue-chip global equities here that continue to perform well. They offer yields higher than safe bonds, for now, and are also the only place we are seeing rate of return.

But within this, we are herding capital into a very, very small sector of asset classes. And then lastly, fortunately or unfortunately, when we have the global central bankers and the global politicians doing what they are doing – Europe, we may take 10% of your assets in the European banking system. Europe, we may invoke negative interest rates; you bring a dollar into a bank, we will give you back 99 ½ cents. You cause capital to move, potentially, and to me th

is is a big issue. I think 2013 was driven as much by momentum, and there is no place else to go, and all those other wonderful things, as it was driven by the weight and movement of global capital. Global capital coming out of China, because it was scared of – if we are going to crack down on corruption and you have got corrupt capital, you get it out right away. Japan, the drop in the yen, you have got to move some of your capital to an alternative venue in an alternative currency. Europe, the threat of confiscation, and maybe just the basic question of, What the heck is the euro going to look like in three years? I know if my net worth was caught up in euros, I sure as heck would not be 100% vested in the euro.

So, a lot of this, I think, too, is global capital is hiding in an asset class that it considers to be relatively safe, because all these other asset classes have proven to be unsafe. And for right or for wrong, in U.S. and really large blue-chip globals, they have been very, very good stewards of capital over time. Their balance sheets are relatively clean, and if you are looking for safety, then this is just a very simple question. Would you rather lever your family’s balance sheet to one of the global governments, or would you rather lever it to Johnson & Johnson? Which one do you trust more? Which one is going to take better care of your capital over time?

So I think there are so many different factors that have been forcing capital into these narrow asset classes that basically are equities and real estate. The key issue to me, going forward, is risk management. For people who sat this one out, for people who have said, Hey, wait a minute; I am looking at the Bob Shiller CAPE ratio here, and we are at levels that we have only seen four times in the last 100 years.You have got to be kidding me. I am not getting into this thing. The only way to participate in these markets, in my mind, is to make sure that you have a plan for managing risk, period. This is not throw your money into the equity market and hope for a great 2014, because every year that the market was up like it was last year was followed by a year that blah, blah, blah. It does not matter. It is about making sure that we manage risk. And we need to draw hard lines underneath certain levels of capital.

Very easy to say, but for your listeners, too, I think this comes down to individual families and making an assessment of how much risk they can afford to take. Below that line, they do not allow it to happen. I know it may sound trite:You have every day of your life to get back into the market, but sometimes you do not have a second chance to get out.

Click the play button below to listen to Chris' interview with Brian Pretti (101m:31s):

Click here to read the full transcript

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/_bL7yKXfbhc/story01.htm Tyler Durden