On Wednesday, the Israeli Foreign Ministry summoned the Russian ambassador, Anatoly Viktorov, against the backdrop of statements made to the Jerusalem Post, in which he criticized Israel’s role in the region. “The problem in the region is not Iranian activities,” Viktorov told The Jerusalem Post the day prior, strongly suggesting it’s Israeli aggression that’s the main problem.

The Foreign Ministry said in a statement that it “expressed, through the official for policy and strategy, Alon Bar, its strong rejection of the statements published during a frank interview, and that they are not consistent with the reality of the situation in the Middle East, which was presented to the ambassador more than once and discussed during political dialogues and through diplomatic channels between the two countries.”

Russian Ambassador to Israel Anatoly Viktorov at the Russian Embassy in Tel Aviv, via The Times of Israel.

Israel’s foreign ministry said further it was expressed to the ambassador that they “consider that the discussion on regional issues, especially with regard to the Iranian threat and its terrorist organizations such as Hezbollah, should take place through diplomatic channels, in a way that addresses the reality and threats facing Israel.”

Lastly, they pointed out that the ambassador intends to issue a letter of clarification about his statements after “some of them were inaccurately conveyed.”

“Israel attacks Hezbollah, and it is not Hezbollah that attacks Israel,” adding that he is aware of the existence of tunnels from Lebanon to northern Israel, but there is no evidence that “Hezbollah dug these tunnels.”

He stressed that Israel should not attack the territories of a sovereign state, and any country that is a member of the United Nations, adding that “it is unlikely that Russia will agree to any Israeli raids on Syria, neither in the past nor in the future.”

Syrian anti-air defense activated over Damascus during one of Israel’s many attacks of the past few years.

Commenting on the reports of the International Atomic Energy Agency about Iran’s increase in the number of centrifuges, the ambassador did not consider this a violation of the nuclear agreement, noting that “the first step was taken by the Americans, who unfortunately decided to withdraw from the nuclear agreement.”

He continued: “They withdrew, which allowed the Iranian side to take steps that do not coincide with the agreement, and this is also unfortunate.”

He added that the possible return of the United States to the agreement “will make things easier … It will help dispel concerns, allow the Iranians to develop a peaceful atomic energy program, and allow the IAEA to monitor what is happening in the military field.”

via ZeroHedge News https://ift.tt/2JPsTjr Tyler Durden

A $1.1 Trillion Boost: Why JPM Sees Stocks Rising As Much As 25% Next Year Tyler Durden

Wed, 12/09/2020 – 19:25

Back in July we showed that in the most typical of Wall Street CYA positions, JPMorgan was bullish, bearish and neutral on stocks all at the same time. This appears to have continued into year end because just last week, JPMorgan’s chief equity strategist Mislav Matejka cut his view of US stocks, downgrading the US to neutral (while upgrading Europe to Overweight). This was around the time JPM also unveiled its 2021 year-end price target for the S&P at 4,400, but came just as stocks swooned lower for a few hours perhaps explaining the sudden onset of bearishness.

In short, anyone trying to figure out what JPM really thinks may want to take a deep breath, and simply look at what the market is doing any any given moment to decipher what JPMorgan thinks.

In any case, with the S&P hitting an all time high above 3,700 on Tuesday (ahead of today’s sharp correction, which may lead to an entirely different hot take from JPMorgan’s crack strategist) one would be correct in assuming that any research reports out of JPMorgan published yesterday would be super bullish (after all, JPM has to convince as many clients as possible to buy whatever JPMorgan’s prop desk has to sell to them), and sure enough in the latest note from JPMorgan’s Nick Panigirtzoglou the bulls got yet another “justification” to keep buying stocks at all time highs. The reason: according to the JPM quant, 2021 will see a net improvement in stock demand/supply to the tune of $1.1 trillion, which of course should – in theory – lead to higher prices.

According to his goalseeked analysis, Panigirtzoglou writes that “for 2021 we see an overall improvement in equity demand of around $600bn relative to this year.” This projected improvement will be driven by incremental demand from retail investors as well as Sovereign Wealth Funds and Risk Parity funds. At the same time, JPMorgan also expects that “global net equity supply will return next year to the very low levels of 2016-2018, i.e. a decline of $500bn relative to this year, as share buyback/LBO activities normalize and the need for equity raising subsides.”

Here is the detailed breakdown of how he gets these numbers:

Retail investors demand will normalize next year to around $500bn from a negative -$50bn YTD. Why? Because as JPM explains, “first it is unusual for retail investors to be selling equity funds for two consecutive years. Second, the evidence from November is that the older cohorts of retail investors are abandoning their previous cautious stance, as, in November, they turned net buyers of equity funds delivering the first monthly inflow for the year. It is unlikely that the November pace of more than $100bn of equity fund buying will be sustained going forward, but we envisage just above $40bn per month for 2021, which is close to historical averages. So for the 2021 as a whole we anticipate around $500bn of equity fund buying, which would represent a sequential improvement of $550bn vs. this year flow.”

Institutional investors are seen as having “some room” to further lift stocks next year but more limited than retail investors especially since “certain institutional investors appear to have increased their equity betas in recent weeks, thus finishing the year with elevated equity positioning.” Therefore, JPM envisages rather limited sequential equity flow impulse between 2020 and 2021 for momentum traders, such as CTAs, Equity Long/Short hedge funds and Balanced Mutual funds. Of the $1.2TN in CTA assets, JPM assumes that a quarter is allocated to equities, and with a net $600BN flow to stocks in recent months, JPM believes that the equity positions by momentum traders or CTAs have very little room to increase from here in 2021, “and we are looking for at least modest negative flow impulse by them between 2021 and 2020.”

Equity Long/Short hedge funds are the biggest equity hedge fund sector with an AUM of $900bn and a typical leverage of around x2. JPM finds that their beta to stocks also rose sharply in November, and the elevated beta currently leaves room for a further bullish shift in 2020. For example, a beta change from 0.70 currently to a bit more bullish stance of 0.75, implies an equity flow of around $114bn for 2021 (after multiplying this beta change by their AUM x2 leverage). In terms of changes, i.e. compared to 2020, this represents a small flow deterioration of $114bn-$137bn=-$23b.

Risk Parity funds saw their beta to stocks fall from 0.59 in December 2019 to around 0.40 currently: “Multiplying this beta change

by their AUM x2 leverage implies a negative equity flow of around $60bn this year.” Looking into next year, JPM sees room for a reversal of the decline in the equity exposure of Risk Parity funds, pointing to positive flow of round $60bn in 2021. In terms of changes, i.e. compared to 2020, this represents a flow improvement of +$60bn-(-$60bn) = +$120bn

Balanced Mutual Funds, a $7tr universe of assets, has seen little market beta change for 2020, with a modest increase from 0.63 in December 2019 to 0.64 currently, implying very modest equity buying of around $50bn. Looking into next year, JPM sees little room for the equity exposure of Balanced funds to increase, pointing to another year of modestly only positive flow of around $85bn during 2020. In terms of changes, i.e. compared to 2020, this represents little flow improvement of +$85bn-$50bn=+$35bn.

Pension funds have been typically sellers of equities in the past years due to their structural shift away from equities and towards fixed income. 2002 has seen an interruption in that flow. For 2020 JPM expects net flows to have been effectively flat. Next year, JPM expects them to shift to a more typical stance of equity selling in 2021 of around half of its average since 2013 of $300bn per year, or a decline of around $150bn vs. the 2020 flat flow.

Meanwhile on the supply side, one way to gauge net equity supply is to look at the change in the free float of the global equity universe as captured by tradable indices such as the MSCI AC World index. Adjusted for price and fx changes, this change in the free float should capture the increase or decrease in the quantity of shares available to market participants in each period.

This proxy of net equity supply, shown in Figure 6, suggests that global equity supply had been most of the time positive in the past, as equity issuance and dilution activities tended to outweigh equity withdrawal activities at a global level. But this had not been the case between 2016 and 2018, as global equity supply had been close to zero or negative. In other words, between 2016 and 2018, there was a three years in a row of unprecedentedly low global equity supply. This was due to weak IPO and equity offering activity, coupled with stronger buyback activity, especially during the repatriation episode of 2018. During 2019 there was a big increase in equity supply due to an improvement in equity offerings including IPOs, but also a significant downshifting in share buyback activity in the US from the strong pace of 2018.

According to JPM calculations, this year global net equity supply has been close to $500bn, only slightly above last year’s supply and half of what the bank had previously projected for this year. This year’s overall equity withdrawal has held up much better than we had previously expected, as a sharper decline in announced share buybacks was more than offset by stronger than expected M&A and LBO activity. And while announced buybacks have declined, companies in strong financial condition, such as those in the tech sector, have continued to execute on previously announced buybacks to perhaps take advantage of lower equity prices during the first half of the year. In addition, the swing in equity dilution activities such as the exchange of common stock for debentures and conversion of preferred stock or convertible securities could have created a more benign equity issuance backdrop than that suggested by elevated announced equity offerings. In 2021, JPM expects further normalization in share buyback/LBO activity which, along with reduced need for equity offerings should help global net equity supply to return to the very low levels of 2016-2018. This view implies a large reduction in equity supply of around $500bn from this year’s pace.

So where does this leave us for next year in terms of the overall equity demand/supply balance?

Adding up all the demand flow changes between 2021 and 2020 and subtracting the supply change, JPM comes up with Equity Demand/Supply improvement of around $1.1 trillion in 2021 relative to 2020.

Why is this notable? Because this is similar to the equivalent Equity Demand/Supply improvement in 2019 relative to 2018, which at the time had seen global equities rising by around 25%.

via ZeroHedge News https://ift.tt/3gxxAu4 Tyler Durden

Chicago Public Schools CEO Janice Jackson warned last week that teachers without preexisting conditions who don’t show up to schools when they open will be fired.

The damage inflicted by school shut-downs on Chicago’s youth, particularly minority youth, is already horrifying. Despite no meaningful risk whatsoever, the Chicago Teachers Union is now seeking an injunction against reopening. Nothing could be more just – and better for Chicago students in the long run – than canning teachers who are ducking their obligation.

Remote learning is an abysmal failure.

‘F’ grades are 2.6 times higher than last year in Chicago elementary schools and worse for minority and homeless students.

It’s much worse for minority and homeless students.

Many get no square meal and no adult guidance outside of school. They are being robbed of not just an education but of the only structure in their lives.

Yet the CTU said “the push to reopen schools is rooted in sexism, racism and misogyny.” That tweet, shown here, was later deleted but the perfidy to which the CTU will stoop was there for all to see.

What’s the CTU’s real problem with going back to work? Everything, which is pretty much their usual answer.

“Everything about what they are doing is wrong,”said CTU Vice President Stacy Davis Gates.

Most everything about the schools, Chicago and America is rotten, they routinely say in contract negotiations and elsewhere, so they want everything changed.

CTU V.P. Stacy Davis Gates

So they’re now seeking an injunction against opening Chicago schools. Their demands are based on supposed safety issues. They want safety protocols, personal protective equipment, COVID-19 screening, testing, contact tracing, vaccination, a nurse in every school, smaller classes that allow for social distancing, social and emotional supports for traumatized students, and upgrades to make ventilation safe.

That’s pointless hogwash. The risk to teachers is infinitesimal. Even if one gets infected with coronavirus, the chances of survival are 99.98% according to the Center for Disease Control for those under age 60, which is almost all Chicago teachers. Seventy-seven percent of them, in fact, are under 50. Those who are older or have known comorbidities would be allowed to teach remotely or given another accommodation, which is common for schools that have reopened.

And for students, the risk is near zero — 99.9997% survival rate for those under age 20, if they get infected. Four have died from the virus in Chicago.

“At no time has the CDC suggested school should be closed,” said CDC director Robert Redfield last month.

“…All school should remain open. It is the safest place for children to be,” he said.

“It’s safe to keep schools open,” said Dr. Daniel Johnson, chief of Pediatric Infectious Diseases at the University of Chicago Medical Center.

And “the vast majority of public and private schools in the Chicago area that have reopened in some capacity this fall have had little confirmed exposure to the coronavirus in the past month,” according to a Chicago Sun-Times analysis of state data.

There’s only one challenging circumstance, and that’s where students live in an extended family with elderly relatives who face serious risk. But school could be used to educate children in those families about how to reduce that risk, and those children are probably exposing those families with or without school. That education has been lacking in messaging from health authorities, and fixing that is part of the “focused protection” advocated by a growing number of experts, which we’ve written often about.

What, instead of the virus, is killing kids? Homicide has killed 25-times more Chicago youth since the start of the pandemic. And fifteen suicides — nearly four times the number killed by the virus. Instead of being in school, kids are on the street and sinking deeper into despair.

It’s all falling most heavily on minorities.

Remember above all else that not all Chicago teachers support the CTU, though a majority apparently do. Those that don’t include many who are living saints. But those who stand in the schoolhouse door should be gone.

Fire them.

via ZeroHedge News https://ift.tt/3n760q3 Tyler Durden

Then, overnight, GLJ Research picked up on these moves, publishing a report explaining why it is time to buy, noting not only the growing ESG investor interest, but also listing four catalysts why the Uranium Sector could be poised to move sharply higher.

As Gordon Johnson writes, echoing much of what we have said int he past week, behind the impressive rally in uranium stocks since Oct 28 (+32.6% vs. +12.9% for S&P 500) “we believe the recent strength in “nuclear stocks” is due partially to higher spot volumes in Oct./Nov. (Ex. 1)…

… but also…”

the U.S. Senate Committee on Environment and Public Works, last week, passing a bill that could fund a uranium strategic reserve through Sep. 2021 in the amount of $150mn (down from the initial $1.5bn over 10yrs announced by President Trump earlier this year), and exclude any Chinese or Russian company involvement in supplying the stockpile (implying, following a long lay-off, the US uranium industry may be in the midst of a revival – the Democratic Party included nuclear in its party platform for the first time in five decades (link), likely due to grid issues associated w/ solar, and Joe Biden’s energy plan (link) includes a carve out for nuclear power),

the 11/28/20 announcement by Cameco that someone at its Cigar Lake mine tested positive for COVID-19 (link),

the subsequent 12/7/20 announcement by Cameco that a second person tested positive for COVID-19 at its Cigar Lake mine (link), and

indications last night that the Ukraine (i.e., the 9th largest global producer) has idled all three of its uranium mines due a to lack of funding (link) – admittedly, these mines are capable of just 2.0mn lbs/year of output U3O8, which is <2% of global production (assuming Cigar Lake is running at nameplate). That said, with the global Uranium market in a fundamental supply deficit, any curtailments (no matter how small) will go to helping absorb the inventory overhang from years of excess supply - Cameco and Kazatomprom, which represent ~55% of current global Uranium production, are managing their output with one objective in mind: higher prices.

In short, as GLJ summarizes “with interest in alternative energy and low GHG emissions markets gaining momentum among ESG investors, we see the uranium sector as well positioned to attract new funds as a “catch-up” play, particularly given the Global Uranium ETF Index is up just +6.5% over the past five years, vs. +80.3% for the S&P 500 over the same timeframe.”

“When you add to the above discussions we’ve held with Uranium investors over the past few days, we feel some of the “sidelined” money is poised to come flowing back into the Uranium space. And should Cameco announce further COVID-related issues at Cigar Lake, and ultimately shut the mine down (albeit, temporarily), we feel this would provide acute tailwinds to Uranium contract negotiations currently underway. As a reminder, while uranium spot prices are currently $29.48/lb, when considering spot prices moved above quoted contract prices in the month of May/June, a dynamic which last occurred dating back to 7/30/07…

… it is our opinion that the Uranium market is currently defined as a sellers market; this can be further evidenced by Cameco’s 3Q20 contracted price being up +13% YoY – Ex. 3.”

There is more in the full report (readers can skim it at their leisure) which looks at industry dynamics and supply and demand, as well as deal volumes, but we will fast forward to the conclusion:

The Uranium sector supply/demand balance is the tightest we’ve seen since pre-Fukushima. Furthermore, producers who account for over 50% of global supply are keeping capacity at bay for the sole purpose of driving Uranium prices higher. When you add to this the Uranium stocks are now gaining attention from ESG investors due to their low GHG footprint and quintessential role as a clean energy alternative, we see the set-up for incremental/new Uranium investments as opportune. Under this backdrop, we prefer Cameco given its low-cost industry positioning and solid balance sheet – Cameco currently boasts a cash-to-debt ratio of 79.5%, which was enabled by the company fortifying its balance sheet during the most recent downturn.

GLJ’s full note is below:

via ZeroHedge News https://ift.tt/3m057y9 Tyler Durden

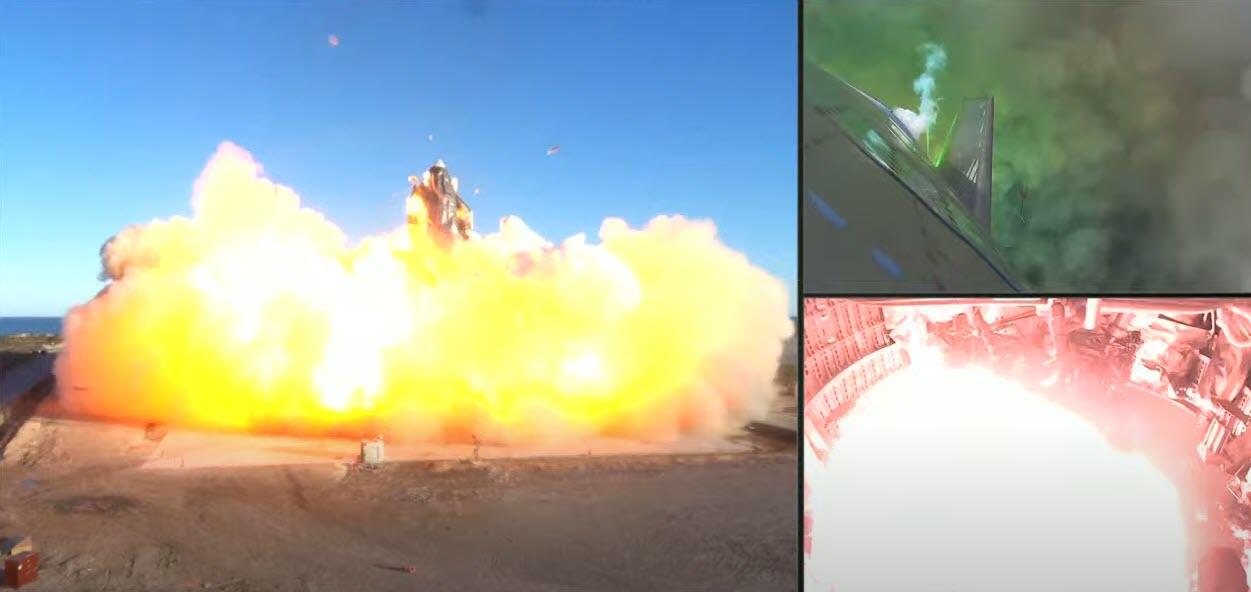

Unmanned SpaceX Starship Flight Test Ends In Massive Fireball Tyler Durden

Wed, 12/09/2020 – 18:05

There’s good news and bad news for Elon Musk’s SpaceX project tonight.

The good news (apparently) is that, as TechCrunch reports, SpaceX is one step closer to replacing its Falcon line of active duty spacecraft: Its Starship prototype ‘SN8’ achieved a major milestone in the ongoing spacecraft’s development program, flying to a height of around 40,000 feet at SpaceX’s development facility in southern Texas.

One of the Starship’s three Raptor engines cut off around 2 minutes into flight, but the prototype rocket continued its ascent. Then at around three minutes, another extinguished, leaving just one lit and firing. The rocket continued to climb, oriented upward, but it was hard to tell from the feed exactly how high it reached. The third flared out at around 4:30, and the Starship oriented into a horizontal position, angling back towards Earth but effectively flat on its belly, gliding.

That was all expected and well according to plan.

“SN8’s flight test is an exciting next step in the development of a fully reusable transportation system capable of carrying both crew and cargo to Earth orbit, the Moon, Mars, and beyond. As we venture into new territory, we continue to appreciate all of the support and encouragement we have received,” SpaceX said in a statement.

But…it all went a little bit turbo as the massive starship came into land…

The Starship’s engines re-ignited as the rocket approached the ground, flipping the rocket into a vertical orientation once again and slowing its descent.

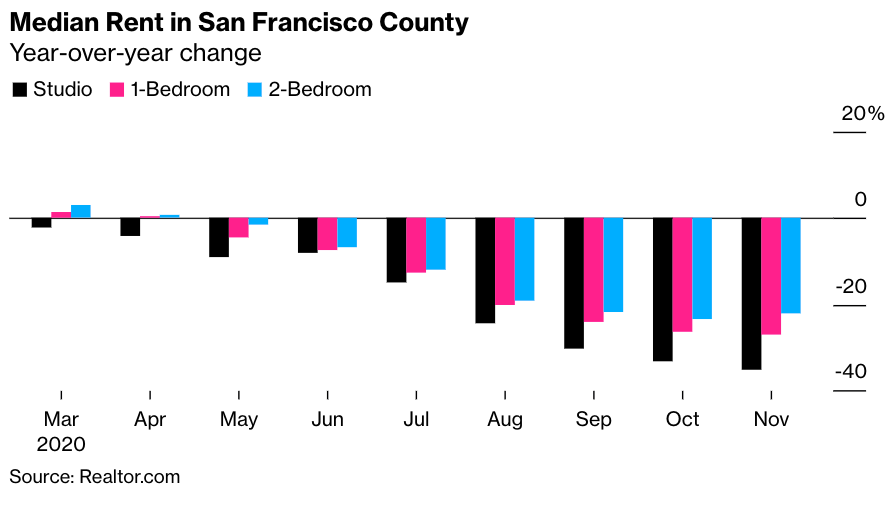

San Francisco Rents Plunge 35% As Exodus Continues Tyler Durden

Wed, 12/09/2020 – 18:05

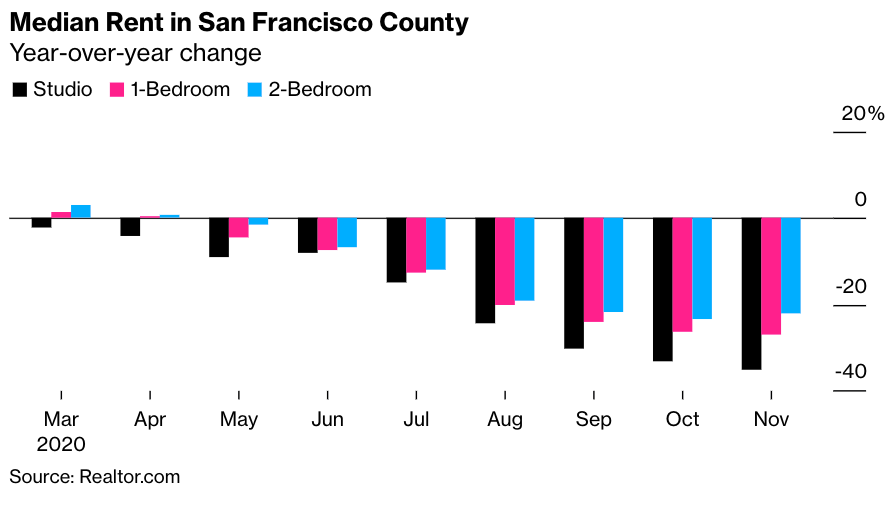

The median rent for a studio apartment in San Francisco plunged 35% in November from a year earlier, to $2,100, while costs for one-bedrooms slumped 27% to $2,716, according to Bloomberg, citing a new report from Realtor.com.

Declining rents is more confirmation of the exodus from the Bay Area (as we’ve noted: here & here) as remote working allows city dwellers to leave the metro area for suburbs, Lake Tahoe, and elsewhere.

Danielle Hale, Realtor.com’s chief economist, said San Francisco-based technology “companies have been among the most flexible with allowing people to work remotely, and a lot of workers are taking advantage of that.”

Hale expects rents in the Bay Area to eventually recover, though it depends on how quickly people return to the office.

But with Contra Costa, San Francisco, and Santa Clara counties, all recording the most COVID-19 cases since the start of the pandemic – tech workers returning to offices might not be happening anytime soon.

As the work from home future marches on – companies are already scaling back on office space.

Real estate firm CBRE said San Francisco’s office vacancy rate has doubled this year to 8.3%, resulting in office rents dropping by at least 9%.

According to Bloomberg, Pinterest Inc. paid a $90 million penalty to terminate a lease at an office building in the downtown area because it wanted to “rethink where future employees could be based.”

Other companies like Hewlett Packard Enterprise Co. and Charles Schwab Corp. are leaving California for lower-cost states.

With major corporations also packing up their bags, this means workers will do the same, and continue to pressure rents in the Bay Area.

Hans Hansson, president of San Francisco office broker Starboard Commercial Real Estate, said the pandemic is like what happened after the 1989 earthquake when people fled the town due to “uncertainty.”

“We rely on tech,” said Hansson, who gets much of his business from early to mid-range startups with downtown offices. “They’re gone.”

Falling apartment rent prices could be an opportunity for folks who’ve been priced out of the area.

Robert Dumas, 58, drives for Lyft and Uber in the Bay Area – lives more than two hours away from the city. He said rent prices haven’t come down enough for him to move to the metro area.

“They haven’t come down enough to make a difference for me yet,” Dumas said, but he thinks they’ll continue to drop.

Real Vision managing editor Ed Harrison joins editor Max Wiethe to put today’s market selloff in context of the broader bullish attitudes that have prevailed amid trouble in the real economy. They also highlight individual stories from the week like DoorDash’s and Airbnb’s IPOs and Tesla’s successful $5 billion dilutive offering as examples of this market favoring corporate managers above all else. Beyond equity markets, Ed and Max touch on the steepening yield curve as another bullish signal and address the knock-on effects for real yields and gold as well as the conflicting signal being sent by a weak dollar.

via ZeroHedge News https://ift.tt/3nglF6J Tyler Durden

If nearly 40 percent of the entire nation anticipates spending the next 12 months in “survival mode”, that is not a good sign for what the coming year will bring.

Traditionally, Americans have looked forward to the turn of the year with tremendous optimism, but this time around things are very, very different. 2020 brought us the COVID pandemic, tremendous violence and civil unrest in our major cities, and the greatest economic downturn since the Great Depression of the 1930s. Sadly, a large chunk of the country is anticipating more difficulties in the coming months, because one recent survey found that 38 percent of all Americans plan to spend 2021 in “survival mode”…

Of the 3,011 surveyed adults, over 38% said they will spend the year in “survival mode,” meaning they’ll focus on the day-to-day rather than long-term goals to try to get themselves and their families through 2021.

The biggest reason why so many anticipate being in “survival mode” is because of the financial problems that they experienced this year. According to that same survey, a whopping 68 percent of all Americans say that they experienced some sort of “financial setback” in 2020…

Although some respondents maintained their usual income over the past year, 68% had setbacks. Of those, 23% lost a job or household income; 20% had an unexpected non-health emergency; 18% had to provide unexpected financial aid to family or friends; and 16% had a health emergency in their family.

As I keep reminding my readers, Americans have filed more than 70 million new claims for unemployment benefits this year, but even many of those that have been able to keep their jobs have fallen on very hard times.

Another new survey found that approximately one-third of all full-time workers in the U.S. “have experienced a pay cut” in 2020…

Roughly 1 in 3 full-time workers have experienced a pay cut due to the coronavirus pandemic this year, according to a recent MagnifyMoney survey of 984 professionals surveyed Nov. 6 to 11.

If you were employed throughout all of 2020 and you are still able to pay all of your bills on time, you should be very thankful for your blessings, because you are now in the minority.

For most Americans, the past 12 months have been exceedingly painful, and this new round of lockdowns promises to extend the economic suffering long into 2021.

Some industries that were absolutely devastated by the first round of lockdowns are officially in panic mode at this point. For example, we have already permanently lost approximately 17 percent of all of the restaurants in the entire country, and the National Restaurant Association is warning that 10,000 more could permanently shut down “in the next three weeks”…

About 17% of America’s restaurants have already permanently closed this year, with thousands more on the brink according to a new report.

The National Restaurant Association is publicly pleading with Congress to pass new stimulus to help the industry that has been damaged by the pandemic. The group said Monday that 10,000 restaurants could close in the next three weeks, in addition to the 110,000 that have already shuttered in 2020.

Even during the best of times, running a successful restaurant is exceedingly difficult. The margins are razor thin, new competition is always popping up, and employees are constantly coming and going.

When you add a global pandemic on top of all of that, it has become almost impossible for many eateries to keep going, and we are being told that the future for the industry looks quite “bleak”…

87% of full-service restaurants (independent, chain, and franchise) report an average 36% drop in sales revenue. For an industry with an average profit margin of 5%-6%, this is simply unsustainable. 83% of full-service operators expect sales to be even worse over the next three months.

Although sales are significantly lower for most independent and franchise owners, their costs have not fallen by a proportional level. 59% of operators say their total labor costs (as a percentage of sales) are higher than they were pre-pandemic.

The future remains bleak. 58% of chain and independent full-service operators expect continued furloughs and layoffs for at least the next three months.

Of course it isn’t just the restaurant industry that is laying off workers in large numbers.

Just about every day there are more major layoff announcements in the news, and many experts are expecting the job loss numbers to accelerate as we make the transition into 2021.

Without paychecks coming in, millions of unemployed Americans are unable to pay the bills, and we are being warned that we could be facing a historic tsunami of evictions starting just after the holiday season…

The day after Christmas, the extended unemployment benefits that have kept 12 million people and their families afloat are scheduled to expire. Then, mere days after that cliff, on New Year’s Day, a national ban on renter evictions from the Centers for Disease Control and Prevention is also set to lapse.

Overnight, an unprecedented bill of $70 billion in unpaid back rent and utilities will come due, according to estimates by Moody’s Analytics Chief Economist Mark Zandi. In all, up to 40 million people could be threatened with eviction over the coming months, research from the Aspen Institute says.

The politicians insist that they are keeping us caged up for our own good, but the truth is that they are absolutely destroying millions upon millions of lives in the process.

There is a lot of debate about whether or not the lockdowns have helped to prevent the spread of the virus, but what we do know is that thousands of businesses have been permanently destroyed, millions of jobs have been lost, more people are committing suicide, and Americans are increasingly engaging in self-destructive behaviors…

Overall, one in three Americans report binge drinking during the coronavirus pandemic. The average person also reports spending about four weeks in lockdown this year; spending 21 hours a day at home. More than seven in 10 people in the survey did not even leave their home for work.

If we cannot even handle the COVID pandemic, how in the world is our society going to be able to handle what else is coming?

As things continue to unravel all around us, people are going to be in great need of hope.

Millions of Americans are already in “survival mode”, and the road ahead is certainly not going to get any easier.

* * *

Michael’s new book entitled “Lost Prophecies Of The Future Of America” is now available in paperback and for the Kindle on Amazon.

via ZeroHedge News https://ift.tt/3qHtTXk Tyler Durden

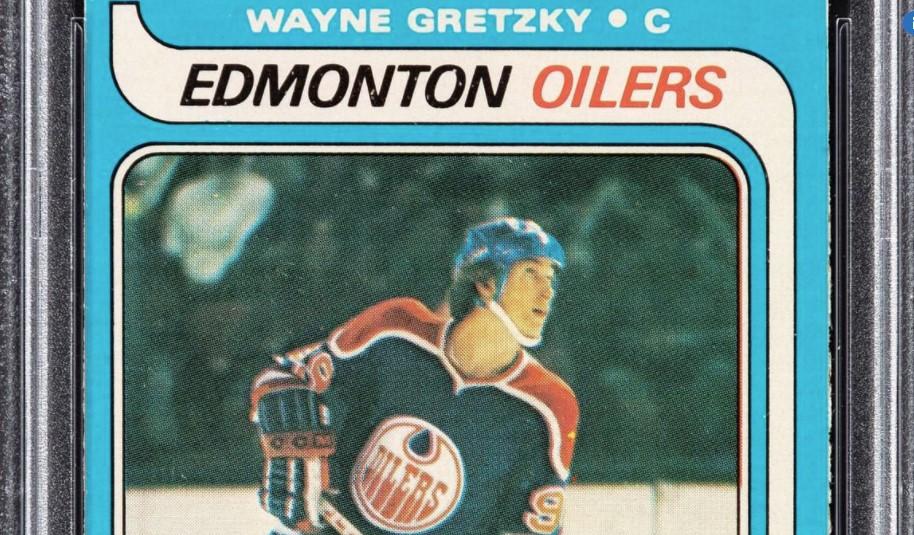

“Where’s The Inflation?”: Wayne Gretzky Hockey Card Expected To Fetch $1 Million At Auction Tyler Durden

Wed, 12/09/2020 – 17:25

While the Fed has a monopoly on most printed pieces of paper that have been assigned ridiculous valuations, they may not have the entire total addressable market. That’s because a Wayne Gretzky hockey card – in fact, a 1979 Wayne Gretzky O-

Pee-Chee rookie card – is set to fetch more than $1 million at an upcoming auction.

“Where’s the inflation?” people routinely still ask.

And it isn’t just Gretzky cards that are skyrocketing in price. The same auction is expected to feature a 1916 Babe Ruth card that could sell for as much as $200,000, a Bloomberg report on Monday noted. Even better is the fact that the Babe Ruth card was “found wrapped up in a plastic baggie in a drawer by a woman in Miami.”

Chris Ivy, director of sports auctions at Dallas-based Heritage Auctions, said: “We’ve certainly seen a lot of growth and interest over the past several years, but it’s been growing exponentially since the spring.”

Hmm. Anyone know what changed this spring?

“When the pandemic started we were tightening our belts,” he continued, “but to my surprise our spring catalog auction surpassed our estimates by over 30%, and that was just the tip of the iceberg.”

And the boom in sports cards isn’t just because of people sitting around with more time to spend on their hobbies during lockdown. Ivy noted that people were using the cards as none other than a hedge against rising prices:

“Prices have surged over the last few months. In addition to nostalgia, there are also a lot of economic factors: Money is cheap right now and people are buying hard assets to hedge against future inflation.”

Perhaps this is why sales of sports cards are up 92% from March to May, compared to the last three months of 2019.

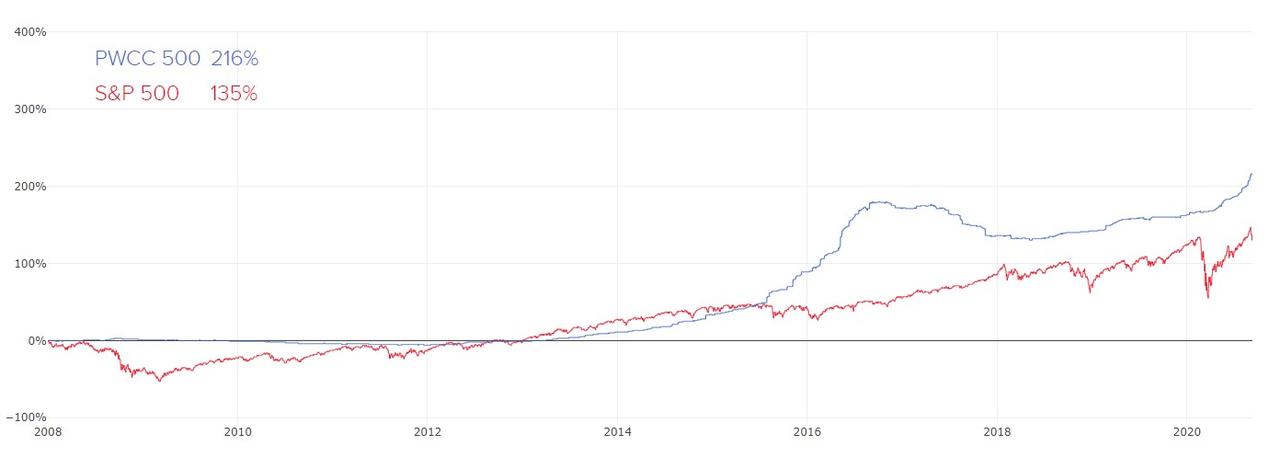

In fact, the PWCC 500, an index of the top 500 trading cards, hit an all time high in May this year and has continued on that trend since then. The index has risen more than 200% since its inception in 2008, Bloomberg notes. This exceeds the returns delivered by the S&P 500 since the trough of the financial crisis.

Recall, we noted back in October that the sports card market was catching fire.

“The market’s just on fire,” PWCC director of business development Jesse Craig told the DailyMail.com in October. “We’re very fortunate to be in the business that we’re in right now during a pandemic and still be thriving.”

via ZeroHedge News https://ift.tt/2W25RrS Tyler Durden

New Yorkers will no longer have to decide if they will receive a COVID-19 vaccine if a bill calling for a mandatory vaccine gets approved.

New York State Assemblywoman Linda Rosenthal, a Democrat who represents New York’s 67th Assembly District, quietly introduced a bill on Dec. 4 that would require “COVID-19 vaccine to be administered in accordance with the department of health’s COVID-19 vaccination administration program and mandates vaccination in certain situations.”

Every New Yorker, except those medically exempt, are required to receive the vaccine if the state’s vaccination efforts do not achieve “sufficient immunity from COVID-19.”

Rosenthal told WGRZ-TVthe bill was “a protective health measure” that would “ensure that our residents are safe and protected against further spread.”

But in an event where not enough people get vaccinated to reach herd immunity, “the department of health of the state can then say that we need people to get the vaccination.” Rosenthal explained that an estimated 75 percent to 80 percent of the population would need to be vaccinated in order to achieve herd immunity.

Barbara Loe Fisher, cofounder and president of the National Vaccine Information Center, described the legislation as inappropriate.

“It is inappropriate for public health officials and state legislators to be introducing legislation that mandates use of an experimental vaccine being considered for release under an Emergency Use Authorization (EUA),” Fisher told The Epoch Times in an email.

“Until a COVID-19 vaccine is formally licensed by the FDA and recommended for use by certain populations by the CDC, it remains an experimental vaccine,” she said. “This kind of bill sends the wrong message to the public.”

The National Vaccine Information Center is a nonprofit organization that publishes “information on diseases and vaccine science, policy, law and the ethical principle of informed consent.”

Food and Drug Administration (FDA) signage is seen through a bus stop at the U.S. Department of Health and Human Services, in Silver Spring, Md., on Thursday, Aug. 2, 2018. (Jacquelyn Martin/AP)

The Food and Drug Administration (FDA) will meet with a panel of independent medical advisers that will discuss whether scientific evidence supports the view that Pfizer’s vaccine, called BNT162b2, is effective in preventing COVID-19 in people aged 16 and older, and if the known benefits outweigh potential risks. COVID-19 is the disease the CCP (Chinese Communist Party) virus causes.

The FDA released an analysis (pdf) of Pfizer’s COVID-19 vaccine prior to its Dec. 10 meeting, along with Pfizer’s own analysis (pdf) of the vaccine’s effectiveness and safety, and says it will issue an emergency use authorization if the advisory panel gives the vaccine a positive recommendation.

In the UK, the government has already begun vaccinating its citizens. The country became the first to approve Pfizer’s COVID-19 vaccine, grant it an emergency approval, and give it immunity from civil lawsuits, under Regulation 345 of the Human Medicines Regulations (pdf) of 2012.

According to a press release from the UK government, individuals experiencing severe adverse reactions that cause them to be “severely disabled as a result of taking a COVID-19 vaccine” are able to “access financial assistance through the Vaccine Damage Payments Scheme (VDPS).”

Vaccine-injured claimants are entitled to a one-time payment of 120,000 pounds ($161,676) under the scheme if they are able to prove they were injured as a result of being vaccinated.

In the United States, vaccines granted emergency authorization are also not liable for the harm they may cause. The Public Readiness and Emergency Preparedness (PREP) Act (pdf) allows the Secretary of the Department of Health and Human Services to issue a PREP Act declaration giving liability immunity to “entities and individuals involved in the development, manufacturing, testing, distribution, administration, and use of such countermeasures.”

People injured by vaccines that have been granted emergency authorization have one year after receiving a vaccine to file a claim and prove their injury under the Countermeasures Injury Compensation Program, a federal government program established as a result of the PREP Act. Certain survivors of people who died from those vaccines also qualify.

The PREP Act declaration for COVID-19 (pdf) went into effect on Feb. 4.

If the New York mandatory COVID-19 vaccine bill is approved, the bill will take effect immediately.

“Informed consent to medical risk-taking is a human right. Legislators should not forget that when proposing bills that use coercion and apply sanctions to force citizens to use vaccines without their voluntary consent,” Fisher said.

via ZeroHedge News https://ift.tt/2VV8gVz Tyler Durden

{kind=link}

{kind=link}

{kind=link}