“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

– Ludwig von Mises, Human Action [1949]

Crisis Now or Total Catastrophe Later?

On Tuesday, while still hopped up on anti-coronavirus goofballs, President Trump had a moment of clarity. After 40 years of near uninterrupted credit expansion, it was finally time to cut it off. And he was just the guy to do the cutting.

Trump took to Twitter to make his first snips. He announced that stimulus bill negotiations were severed. Minutes after, the Dow Jones Industrial Average hit a 400 point air pocket. Several hours later, and perhaps following a little tutelage from Mnuchin and Kudlow, Trump reversed course.

We don’t know what Mnuchin and Kudlow said to Trump. But we suppose they informed him that, at this point, the immediate health of the American economy is contingent on delivering printing press money to citizens and non-citizens alike…who cares if the long-term consequences are catastrophic? Thus, Trump called on Congress to approve a second round of $1,200 stimulus checks.

This course of action eschews voluntary abandonment of further credit expansion. This, no doubt, is the path of least resistance for politicians. Unless Trump wants to lose the election, he can’t tell voters there’s no more free money.

The choice is real simple. Voluntary abandonment of further credit expansion and a crisis now. Or further credit expansion and the final and total catastrophe of the dollar system later.

For a politician this isn’t really a choice at all. If you recall, Nero clipped coins in 64 A.D. and fiddled as Rome burned. The decision every president makes is to avoid a crisis now and, with a little luck, leave total catastrophe for some other sucker.

We’ll have more on this in a moment. But first, some perspective…

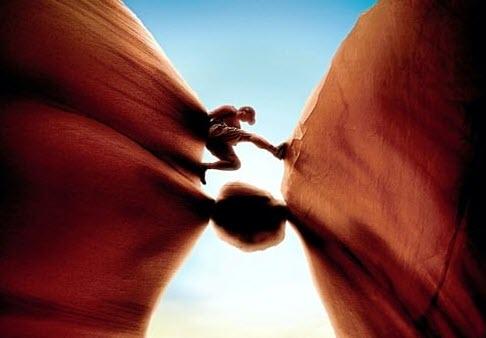

Between a Rock and a Hard Place

In the Spring of 2003, 27-year old Aron Ralston found himself between a rock and a hard place. While solo canyoneering within the rock fissures and tapered caverns of Bluejohn Canyon, in eastern Utah, something heinous happened.

While negotiating a 10 foot drop in a 3 foot wide canyon, Ralston dislodged a boulder he thought was stable. As he fell back, the boulder crashed down and crushed his right hand and lower arm. What’s worse, the 800 pound rock pinned him in the canyon. He was entombed.

Ralston was carrying a small rucksack with just one liter of water, two burritos and a few chunks of chocolate. He also had his rock climbing ropes and a small multi-purpose knife. He hadn’t bothered to tell anyone where he was going. He knew he was invincible.

Over the next 127 hours (more than 5 days), Ralston rationed his water and fruitlessly chipped away at the massive boulder with a dull multi-tool knife. He slowly slipped into a state of delirium. As Ralston weakened and his supplies faded, he was faced with a grim question: Your hand or your life?

Ralston concluded his only way out was to tourniquet his arm with his climbing ropes, and cut off his hand. But when he cut through the flesh with his dull knife he encountered another problem. His bones!

By the fifth day, as Ralston later recounted, he had found “peace” in “the knowledge that I am going to die here, this is my grave.” However, the following morning he had reservations. His peace was gone.

What happened next?

With death staring him in the face, Ralston went into a rage…resulting in another stark revelation. He could fling himself against the boulder to break his own bones.

The snap of his bones “like, pow!” was a horrifying sound “but to me it was euphoric,” recalled Ralston. “The detachment had already happened in my mind – it’s rubbish, it’s going to kill you, get rid of it.”

After snapping his bones and severing his hand (it took about an hour to hack through his flesh), Ralston somehow managed to scale a 65 foot cliff to escape the canyon. He then hiked out to his rescue – minus a hand.

America Has an Epic Choice

America has an epic choice. And it has nothing to do with who will be the next president of the United States. It has nothing to do with if the new stimulus bill is $1.6 trillion or $2.2 trillion.

To review, the choice is as follows: Voluntary abandonment of further credit expansion and a crisis now. Or further credit expansion and the final and total catastrophe of the dollar system later.

The President, Joe Biden, Congress, the Secretary of Treasury, the Federal Reserve, economic advisors, the political class, lobbyists, government contractors, Wall Street, pensioners, CalPERS, transfer payment recipients, social security and Medicare beneficiaries, and so on and so forth, including…

Jamie Dimon, the U.S. Forest Service, the Bureau of Land Management, Arlington Virginia, bureaucrats at the Department of HUD, Anthony Fauci, mortgage brokers, Edward Jones, Lockheed Martin, the staff at the IRS, public private partnerships, teachers unions, and much, much more.

The whole lot – and then some – are firmly on the side of further credit expansion and the final and total catastrophe of the dollar system later. Just this week, for example, Fed Chair Powell offered the following words of encouragement:

“The US federal budget is on an unsustainable path, [and] has been for some time. [But] this is not the time to give priority to those concerns.”

In other words, avoid a crisis now in exchange for total catastrophe later.

The choice, by all measures, is heinous. But sometimes, like Aron Ralston, one must cut off their hand if they want to live. By this, voluntary abandonment of further credit expansion is the way out of the current financial predicament. Stop the madness. Bring on the crisis.

via ZeroHedge News https://ift.tt/2GNLEST Tyler Durden

“Vicious Ideology”: Marine’s Video Rant Against China Now Focus Of Chinese State Reporting Tyler Durden

Sat, 10/10/2020 – 16:30

The 20-year old Marine currently under military investigation for his half-minute Twitter video wherein he rants against China, blaming the country for coronavirus and threatening to shoot Chinese people which was posted this week is now subject of widespread Chinese media reporting.

This will likely create even bigger legal problems under the Uniform Code of Military Justice (UCMJ) for Colorado native Jarrett Morford, who made the video at his training base in Twentynine Palms, California.

The clip which is filled with racial expletives deriding Chinese people is now being upheld by Chinese state media’s top English-language mouthpiece as an example of Trump’s and America’s “vicious ideology” and “hatred” preached to the Chinese people:

What a vicious ideology that spurs such hatred for Chinese people from a young US soldier. Trump and the US political elites who preach that China should be held responsible for the pandemic have created this ideology. It’s a shame for the US as a democratic country. pic.twitter.com/6xyLklJfko

Hu Xijin is the highly visible editor-in-chief of China’s communist government-owned Global Times. Thus the video now appears to be factoring in to worsening Sino-US relations, as if anything else was needed for the continued downward spiral which includes military tensions in the region.

“What a vicious ideology that spurs such hatred for Chinese people from a young US soldier,” Xijin wrote on Twitter Saturday. “Trump and the US political elites who preach that China should be held responsible for the pandemic have created this ideology. It’s a shame for the US as a democratic country.”

PFC Morford made the video while in uniform. “As the honorable Trump said on Twitter today, it was China’s fault,” the young Marine said. “China is going to pay for what they’ve done to this country and the world. I don’t give a f–k!”

Marine IDed in racist video threatening to shoot ch*nks

“If a ch*nk headed mother f*cker comes up to me when I’m in the fleet, say 556 b*tch. That’s all I gotta say. Say 556,” he is heard saying on Twitter.

556 reportedly refers to the 5.56 bullets used in firearms such as the M249 Squad Automatic Weapon.

On Thursday the Marine Corps announced an investigation is underway and that “appropriate action” would would be taken. “There is no place for racism in the Marine Corps,” a Marine statement to Stars and Stripes said. “Those who can’t value the contributions of others, regardless of background, are destructive to our culture and do not represent our core values.”

Now it appears the stakes are higher, given we’ve entered the domain of international incident and angry denunciations out of Beijing.

via ZeroHedge News https://ift.tt/30U8cYP Tyler Durden

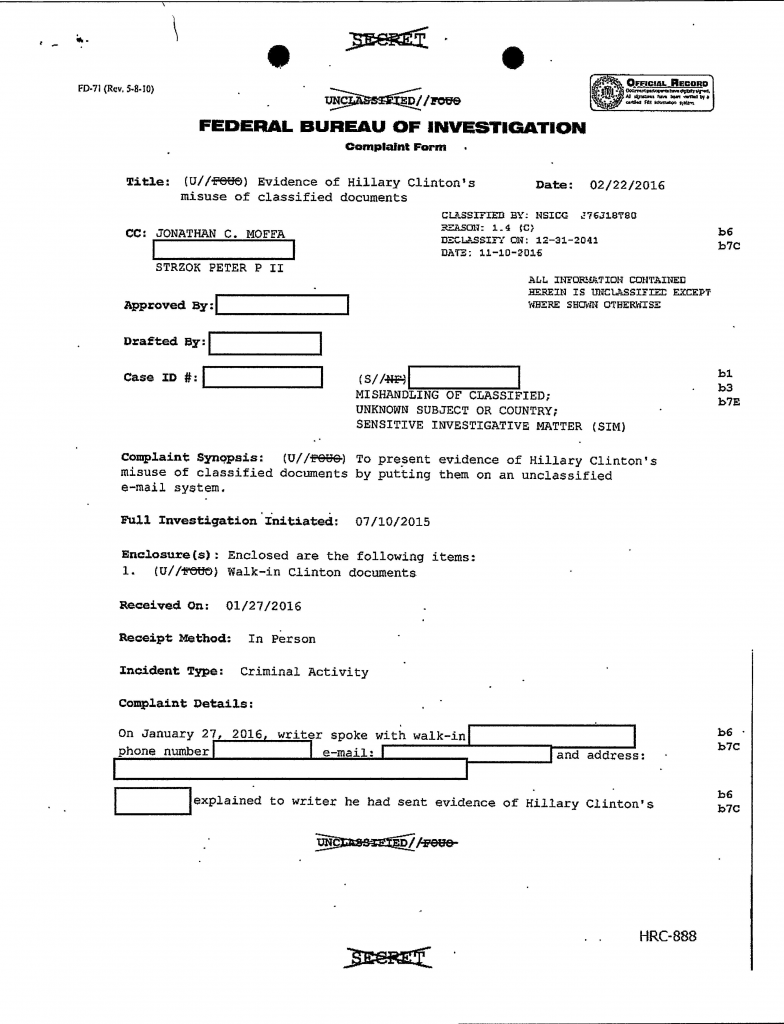

One year before Jim Comey was immersed in his plot to overthrow Donald Trump, the duly elected President of the United States, a brave Foreign Service Officer at the U.S. Department of State came forward with firsthand information of Hillary Clinton’s rampant abuse of Classified material. The man, a senior State Department diplomat who had served as the acting Ambassador (Chargé d’Affaires) in the Asia Pacific region under President Clinton, also was a veteran of the U.S. Army during the Vietnam War.

The letter from this whistleblower is stunning and I am going to present it in total. It is dated 10 January 2016. You can read it for yourself here starting at page 121. I became aware of this letter thanks to the assiduous research and writings of Charles Ortel (he wrote about this recently at the American Thinker).

The letter explains in great detail how Hillary and her cabal of sychophants used an unclassified system to disseminate Top Secret and Secret intelligence. But the Senior Diplomat did not stop there. He explained carefully and specifically who the FBI needed to interview and the questions they needed to ask. You do not need to take my word for it. You can read the letter for yourself…

And what did the sanctimonious, smug buffoon heading up the FBI do? Nothing. But this senior Foreign Service Officer was dogged in making sure the FBI had the information. He called FBI Headquarters and could not get any confirmation that his letter was accepted. Not satisfied, he walked into the FBI’s Washington Field Office. The results of this meeting were reported to three FBI Agents working on the Hillary Clinton investigation. Named in the report are Peter Strzok and Jonathan Moffa (the third name is blacked out).

Here is the report in its entirety. Please note that the State Department official delivered the information on the 27th of January 2016, but the report was not written up until four weeks later–22 February 2016. (You can see the original on the FBI website here starting at page 11.)

I do not know if John Durham has seen these documents. I am posting to make sure that he does. There is no evidence that Inspector General Horowitz examined these documents or interviewed the Foreign Service Officer.

With Secretary of State Pompeo’s promise that Hillary emails will be forthcoming, I think it is worthwhile to revisit what this brave whistleblower tried to bring to the attention of the FBI, who clearly was hellbent on protecting Hillary rather than pursing justice and upholding the law.

Shameful.

via ZeroHedge News https://ift.tt/3nFLeyi Tyler Durden

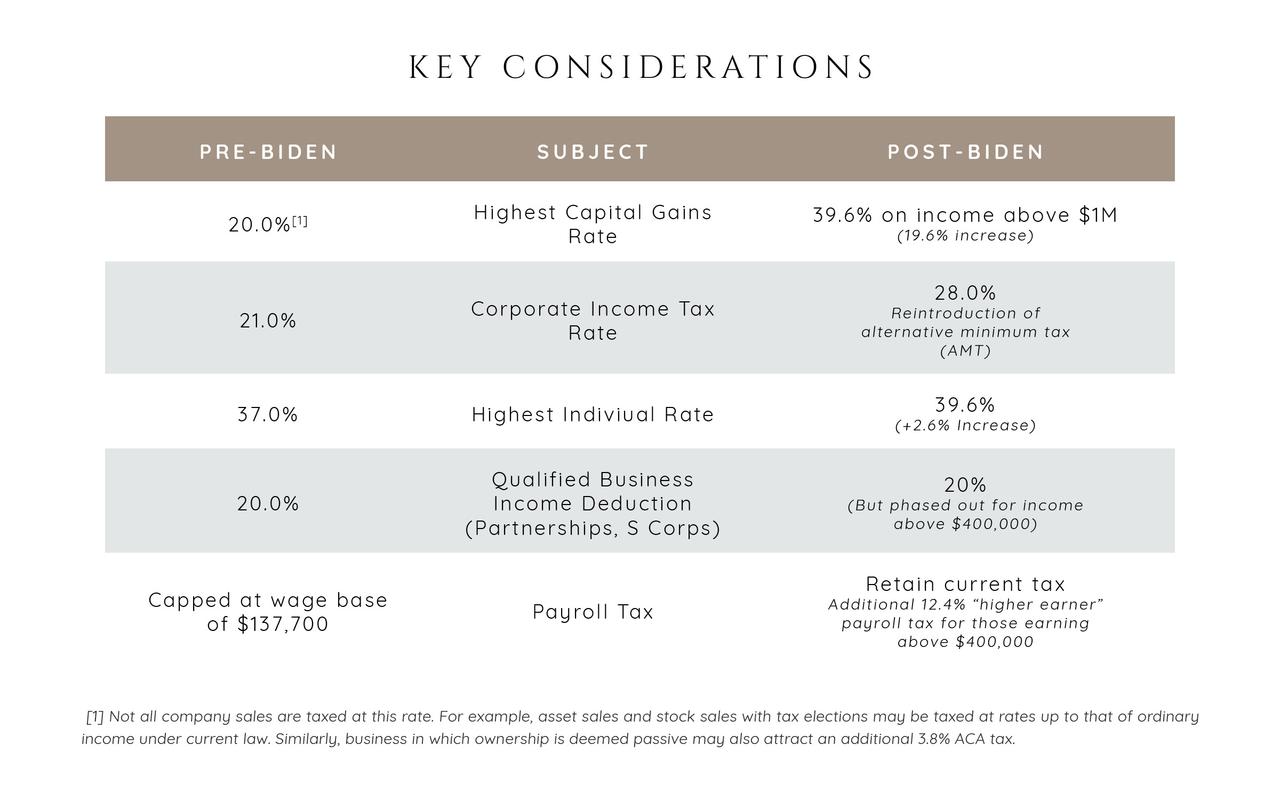

Biden Will Hike The Top Capital Gains Tax Rate To 39.6%: What That Means For Markets Tyler Durden

Sat, 10/10/2020 – 15:30

Over the past few weeks, Wall Street has been busy carefully restructuring the post-election narrative to one where the tax hikes under a Biden presidency would actually be bullish for risk assets.

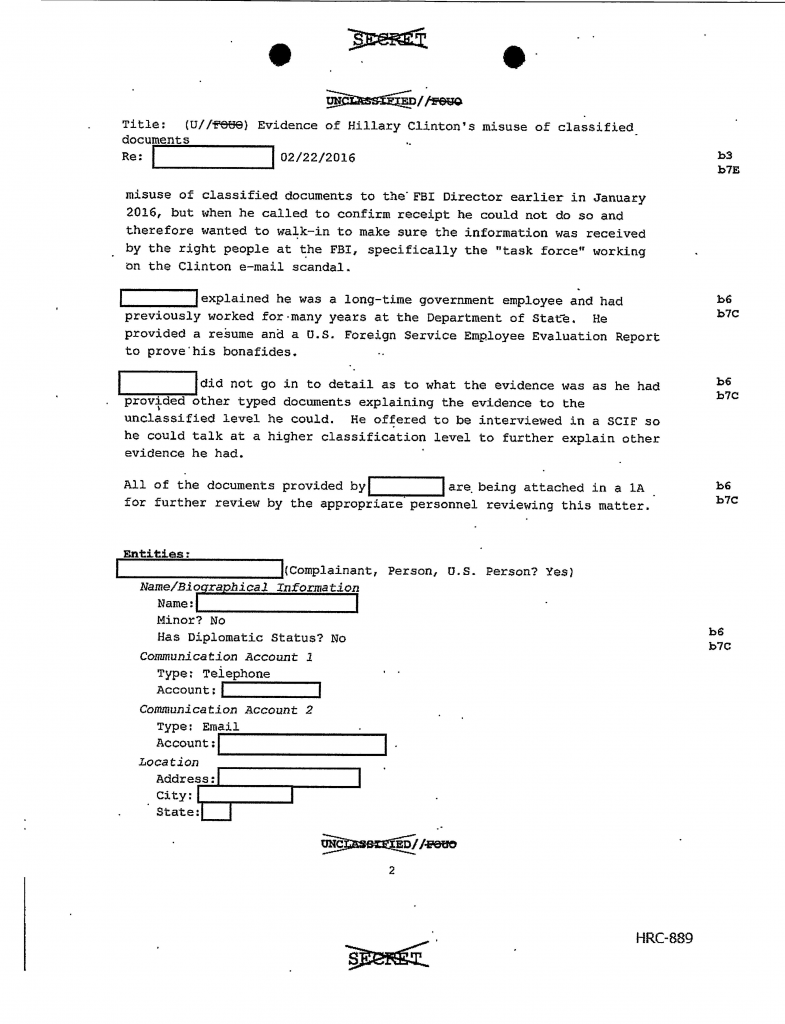

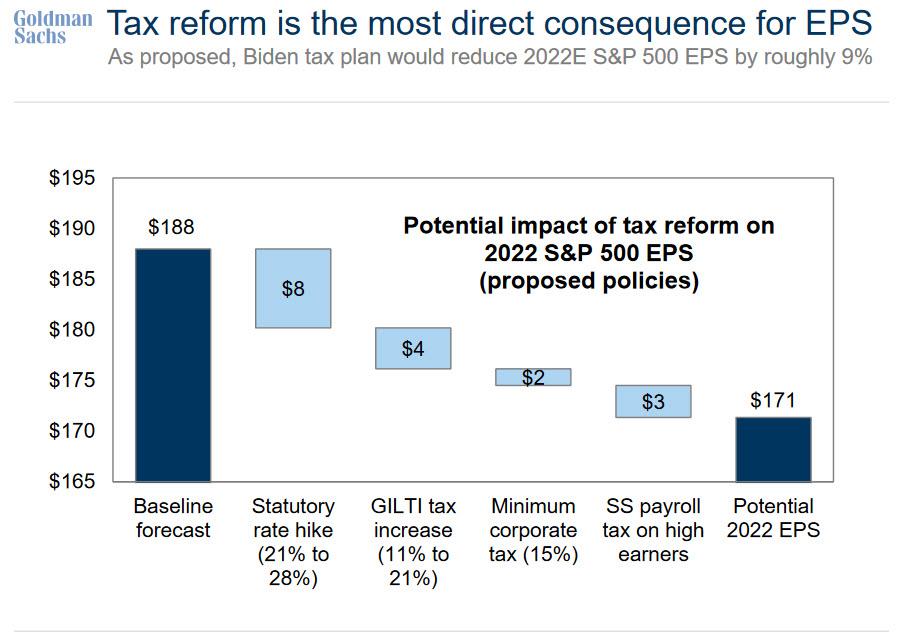

As a reminder, whereas there would be no changes to the tax regime under a 2nd Trump administration, Biden plans to lift the statutory corporate income tax rate by 7% to 33% from 26% (including federal and local) reversing half of the Trump cuts, raising taxes on high earners as well as implementing a number of other tax changes including an increased tax on global, low-tax, intangible (“GILTI”) income…

… which the banks readily admit would adversely hit S&P500 earnings in 2022 by roughly 9%, pushing it from a Goldman baseline forecast of $188 to $171…

… yet ignore all that because, as per the new Wall Street narrative, the Biden admin would also unleash up to $7 trillion in fiscal stimulus which while catastrophic for the long-term viability of the US, its currency and its already ridiculous debt trajectory…

… would be good for stocks until some time in 2023, at which point even more stimulus will be needed (according to the latest Goldman research). As a result, and as we summarized last week, Wall Street now agrees that Biden victory and a Democratic sweep would be great for stocks despite the sharp increase in taxes across the board for many Americans and especially the Top 1…

It remains to be seen just how ‘good’ for stocks a sharp hit to EPS and a potential contraction in PE multiples – which would be sparked by Biden’s aggressively reflationary policies – will be under a Biden presidency, but one aspect of Biden’s tax policies that has received very little coverage is his proposal to increase the maximum tax rate for long-term capital gains by a whopping 66%, from 20% currently (23.8% when accounting for the additional 3.8% ACA tax) to as high as 39.6%, for those making over $1 million, or for proceeds of a business sale over $1 million. A summary of the changes tot he US tax code under a Biden admin is shown below.

While this cap gains increase won’t affect most Robinhood traders (except for the really talented ones), it will have a drastic hit on major market players and corporate strategies involving exit events that include more than $1 million in proceeds, as the following analysis from Benchmark Corporate shows: assume a $2.0M EBITDA (small or medium) business receives a valuation multiple of 10x for a total transaction value (taxable gain) of $20.0M. Under the Biden Plan, the seller would lose $3.92M in the sale. To receive the same net proceeds, a multiple of 13.2x would need to be secured.

This kind of dramatic revision to post-transaction cash flows under a Biden regime is – to say the least – concerning, although because the media has barely discussed Biden’s tax plan (or any of his other policies for that matter) and instead focusing on Trump, Trump, Trump, the impact of Biden’s tax long-term cap gains will come as a shock to the market.

It’s also why on Friday, JPMorgan was quick to jump on the bandwagon of Wall Street defenders of Biden tax proposals – after all no bank wants to see the markets puke in the coming weeks as traders lock in profits under the Trump admin – only instead of defending the corporate tax hike, this time it focused on Biden’s cap gains tax hike. Not surprisingly, it concludes that this too would have “little impact on risk taking and investors’ attitude toward equities as an asset class.”

But first, some background.

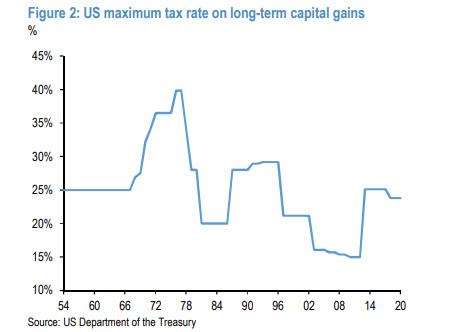

As JPM’s quant Nick Panigirtzoglou writes, while it is relatively easier to quantify the potential impact from Biden’s corporate tax or other proposals, assessing the potential impact from the proposed increase in the capital gains tax rate is more difficult. Biden’s proposal is for the maximum tax rate for long-term capital gains to rise to 39.6% from 23.8% currently, a 66% proportional rise. As the JPM strategist concedes, “given the size of the proposed increase, the potential impact is likely to be at least similar to previous episodes of big capital gains tax rate hikes, i.e., the capital gains tax rate hikes of 1 January 1987 and 2013.”

Between the 1986 and 1987 tax years, the maximum tax rate on long-term capital gains had risen to 28% from 20%, a 40% proportional rise. Between the 2012 and 2013 tax years, the maximum tax rate on long-term capital gains had risen to 25.1% from 15%, a 67% proportional rise.

At this point, Panigirtzoglou launches an assessment of the potential impact from Biden’s proposed capital gains tax increase, in which he distinguishes between the longer-term and the near-term impact.

In terms of the longer-term impact, the quant falls back on conventional wisdom which says that “the friction from a higher capital gains tax would over time reduce capital mobility and investment and thus end up being negative for economic growth and thus for long-term equity market returns. The argument being that higher taxes on capital gains would lower the after-tax rate of return to savers, which in turn would raise the cost of capital to businesses. In addition, a higher capital gains tax rate could reduce incentives for entrepreneurship and risk taking.”

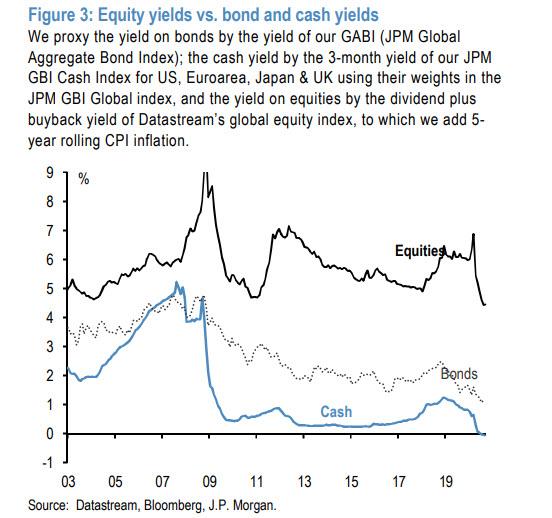

Needless to say, all of this is bad for the broader economy, which is why Panigirtzoglou is quick to admit that a full-blown analysis of the economic impact of a capital gains tax hike “is beyond the scope of this publication” which is ironic because the very next thing he does is an attempt to spin it as favorable because, as he writes, “in a low yield and high equity risk premium environment like the one we are at the moment (Figure 3), any longer term impact from a capital gains tax rate hike on risk taking and investors’ attitude towards equities as an asset class would be even more muted relative to the past.”

In other words, under the massive yield and volatility suppression of the current Fed regime, despite the adverse impact of higher taxes, investors will still have no choice but to go back to stocks.

One wonders how this argument will be “spun” if after a few years of Biden’s trillions in fiscal stimulus, the current “low yield and high equity risk premium” environment is dramatically reversed. Of course, we are confident that JPM will have a bullish spin for that when the time comes.

And just in case that was not enough, Panigirtzoglou then suggests another “positive” aspect of higher cap gains taxes: “an argument could be made that the money invested by individuals in the equity market would likely become more sticky over time as a result of the increase in the capital gains tax rate, perhaps inducing lower long-term equity volatility.” Yes, because the Fed’s constant manipulation of markets by lowering implied and realized vol is not enough.

And while it is easy to spin any long-term scenario as bullish laden with countless favorable assumptions, even JPMorgan finds it impossible to spin the near term impact as bullish: “There is little doubt, that similar to the past, tax optimization would result in one-off bout of asset selling ahead of the effective date of the capital gains tax rate hike so that investors realize their capital gains before the new higher rate applies. “

History is full of such examples: before at the end of 1986 and 2012 ahead of the 1 January 1987 and 2013 increase in the capital gain tax rate.

So assuming Biden becomes President and controls the Congress to be able to implement his plan to increase the capital gains tax rate next year, the most likely effective date JPM envisages is 1 January 2022. In this case, any tax related asset selling would take place in the fourth quarter of 2021, i.e., a year from now. Which brings us the key question: how much tax-related asset selling should we expect at the end of 2021 assuming an effective date of the new capital gains tax rate of 1st January 2022?

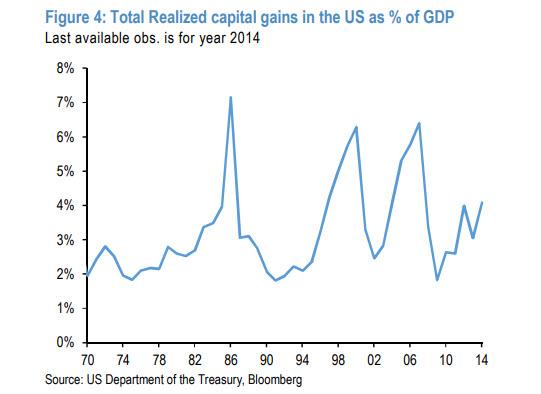

One way of answering this question is to look at the experiences of 1986 and 2012. Figure 4 shows the capital gains realizations in the US as % of US GDP. One can clearly see the big annual increase in US capital gains realizations during 1986 and 2012, by 3% and 1.5% respectively of US GDP. Applying an increase of 2% of US GDP in capital gains realizations in the current conjuncture would imply additional tax-related asset selling of around $400bn due to the prospective increase in the capital gains tax rate.

According to JPM, “such selling would likely put some pressure on the US equity market of around 5% or so as we saw previously at the end of 1986 and 2012 (Figure 5).” However at this point the short-term becomes long-term (similar to how traders become investors after bad trades), and as Panigirtzoglou next posits, “such pressure is likely to be temporary and once the new capital gains tax rate is introduced, the equity market would likely resume its uptrend in even stronger manner.”

Indeed, Figure 5 shows that following a negative to flattish profile in the fourth quarter of 1986 and 2012, the equity market saw a steeper upward trajectory in the first half of 1987 and 2013, i.e. the equity market corrections at the end of 1986 and 2012 proved good buying opportunities. In particular, in 1986 the S&P had seen annualized price returns of around 15% per year on average in the 5 years before the tax rise. In 2012, a 5-year horizon covers the financial crisis, but using a shorter horizon between 2 and 4 years saw annualized gains of 6-12%. And in the first quarter of the year the new higher rate had kicked in, the S&P saw returns of 20% and 10% respectively.

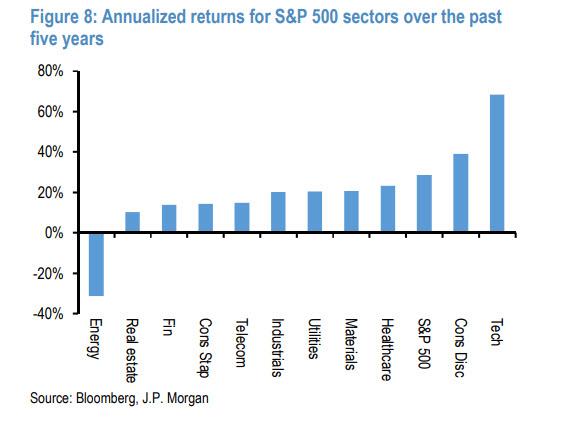

Going back to the less than bullish short-term, JPM next looks at which sectors would be most impacted from the Biden tax changes, and finds that in the event of a Democratic sweep that subsequently sees a change in CGT rates taking effect at end-2021, “the sectors that have outperformed in recent years recent years are susceptible to some volatility around the time when a new higher CGT rate would kick in. Looking at the annualized returns over the past 5 years (Figure 8), this implies sectors

such as tech, consumer discretionary and healthcare.” By contrast, investors might prefer to wait until after the new higher CGT rate kicks in before harvesting tax losses from sectors and companies that have seen weaker returns (e.g. energy) at a higher CGT rate.”

Putting it all together, JPM concludes that even if there is a Blue Sweep in November, “it is perhaps too early to worry about a prospective capital gains tax rate increase in the US” as the likely effective date of the higher capital gains tax rate would be January 2022. As such, JPMorgan admits that “we are likely to see some downward pressure in equity markets in Q4 2021, i.e., in a year’s time.”

Of course, since such a conclusion in isolation would be viewed as too bearish for a bank whose job is to pump markets, JPM then engages the spin cycle, and writes that “once the new capital gains tax rate kicks in, the equity market is likely to resume its upward trajectory in a strong manner as it did previously in the first quarter half of 1987 and 2013.” Because why not: after all the Fed is there to make sure stocks never again suffer the indignity of another bear market.

Finally, and somewhat laughably, JPM writes that “longer term we see little impact from a prospective capital gains tax rate increase on risk taking and investors’ attitude towards equities as an asset class given the current low yield and high equity risk premium environment.”

To summarize: in its quest to spin a Biden administration as positive for risk assets, perhaps even more so than Trump’s, first we had a barrage of banks predicting that the jump in corporate tax rates under president Biden would be a non-event for markets (since it will be offset by trillions more in stimulus), and now we have the largest commercial US bank vouching that an even more draconian increase in capital gains tax may be negative around the end of 2021, but will then supercharge returns in the years after.

So yes, it’s possible that we now live in such an upside down world where Biden’s higher tax rates are bullish for markets… just as Trump’s tax cuts were bullish for markets (here, the question emerges, is there any event than in Wall Street’s view is ever negative for markets, or rather centrally-planned “markets” in which the Fed injects at least $120 billion every month), although we doubt it; after all these forecasts come from the same Wall Street which was dead certain that Trump defeating Clinton would lead to a market crash (we all know what happened then). In any case, now that JPM has done the initial spin cycle on why higher capital gains taxes are bullish for stocks, we expect all other banks to join in the coming days with their own narratives on why the only thing more bullish for stocks than lower taxes is higher taxes.

Finally, since this is all just spin, we leave the final word to another branch of JPMorgan, its Private Bank (which handles all of the bank’s high net worth clients), whose conclusion is that no matter what happens, one should not sell:

Since the end of World War II, there’s been this one constant, regardless of the occupant of the White House and the composition of Congress: equity markets have increased in value over time. Some stocks, sectors or styles do better at some times than others, depending on specific, often unpredictable factors—a fact that underlines the importance of diversification. That is why, to ensure the long-term health of one’s portfolio, we think that time in the market, rather than market timing, is key. Consequently, we advise clients to stay invested, regardless of specific events—including election results.

The punchline: despite the clear differences to the tax regime under a Biden administration, JPMorgan goes so far as to say ignore it all, and in fact, “don’t let the passions of this election lead you to make any key planning or investment decisions.”

In light of all this, one wonders: does it even matter who is president as long as we have a Fed?

via ZeroHedge News https://ift.tt/3jPhuNc Tyler Durden

University of Illinois professor Catherine Prendergast recently tweeted that Mitch McConnell was a Nazi and compared him to a character from Schindler’s list.

“McConnell is a Nazi,” said Prendergast.

“He’s that guy in Schindler’s List who picks off old Jewish ladies with his rifle, for sport.”

McConnell is a Nazi. He’s that guy in Schindler’s List who picks off old Jewish ladies with his rifle, for sport.

Prendergast recently made headlines fire after stating that “MAGA equals Nazi” and advocating for elections “where whites don’t vote.”

Similarly, as Campus Reformreported, a professor at the University of Virginia said in a Washington Post Op-Ed that President Trump’s rhetoric is “echoing” that of southern enslavers.

“In arguing that radical protesters endanger U.S. law and order, Trump is echoing the attacks leveled by Southern enslavers against abolitionist,” Elizabeth Varon wrote.

Campus Reform reached out to Prendergast, but did not receive a response.

via ZeroHedge News https://ift.tt/2SLkjDi Tyler Durden

Having reportedly “capitulated” from $500 million, the GOP’s latest $1.8 trillion COVID-Relief package offer has been flatly rejected by House Speaker Nancy Pelosi (whose latest offer was a $2.2 trillion package)… once again!

In a letter to her Democratic colleagues, Pelosi claims the White House offer falls short on COVID-19 testing, worker safety, and child care (all of which she bundles – obviously – under the need for state bailouts, our words, not hers).

Here is the full letter, providing her campaigning colleagues and the media with their talking points to un-blame the Democrats for delaying payments to suffering Americans for tomorrow’s political shows… (emphasis ours)

Dear Democratic Colleague,

On Friday, the Trump Administration returned to the table with a proposal that attempted to address some of the concerns Democrats have in the coronavirus relief negotiations. This proposal amounted to one step forward, two steps back. When the President talks about wanting a bigger relief package, his proposal appears to mean that he wants more money at his discretion to grant or withhold, rather than agreeing on language prescribing how we honor our workers, crush the virus and put money in the pockets of workers.

At this point, we still have disagreement on many priorities, and Democrats are awaiting language from the Administration on several provisions as the negotiations on the overall funding amount continue.

A key concern is the absence of any response on a strategic plan to crush the virus. We cannot safely reopen schools, the economy and our communities until we crush the virus with the science-based, national plan for testing, tracing, treatment and isolation, and for the equitable and ethical distribution of a safe and effective vaccine once developed. This strategic plan is contained in the Heroes Act.

Please see the Energy and Commerce memo which is attached.

From start to finish, the Trump Administration refuses to honor our heroes and respect the safety our workforce. The funding for state and local remains sadly inadequate. At the same time, the Trump proposal recklessly leaves behind workers by ignoring the need for strong OSHA protections to keep our workers safe as they risk their lives and jobs to keep us safe and keep the economy running. We are urging the Administration to support our strong OSHA language, which requires OSHA to issue an enforceable emergency temporary standard within seven days that covers all workers from COVID-19 infections. Unfortunately, they have a Liability Provision that is reckless in how it ignores safety in the workplace.

At this point, the Trump proposal is insufficient in meeting families’ needs, in stark contrast to the Heroes Act, which secured tens of billions for direct relief and refundable credits. At the end of September, in preparation for the restarting of our negotiations, I had previously written to you about what the Heroes Act mean for families at their kitchen tables. For a family of four earning $24,000:

Direct Relief — Heroes Act: a total $9,890 when including the Earned Income Tax Credit and Child Tax Credit. Trump proposal eliminate Earned Income Tax Credit, Child Tax Credit and Child Dependent Care Tax Credit.

Earned Income Tax Credit — Heroes Act: If the parents lost all of their income in 2020, they could receive up to $5,920 in EITC based on their earnings from 2019. Trump proposal: eliminate.

Child Tax Credit and Child Dependent Care Tax Credit — Heroes Act: fully refundable $4,000 for the two children equaling an additional $1,200 in refund. Trump proposal: eliminate.

Child Care — Heroes Act: $57 billion to enable parents to work while their children are in the uncertain circumstances of in-person, virtual or hybrid learning. Trump proposal: No movement from $25 billion figure, which is totally inadequate. At the same time. Republicans are insisting on a tax credit for the wealthiest people in America, which is retroactive and therefore not coronavirus related, at the expense of tax credit for the families of our poorest children who are directly affected by coronavirus. At a time when children and families are challenged by uncertainty in whether their schools will be actual, virtual or hybrid, the Trump Administration is underfunding education.

Unemployment Insurance — Heroes Act: contains strong funding to protect the five million workers at risk of exhausting all of their regular Unemployment Insurance or Pandemic Unemployment Assistance benefits before January 31. Trump proposal: $200 billion less than what Democrats proposed, which experts tell us is what is needed.

Our Heroes Act is a tribute to the tremendous leadership of Chairwoman Nita Lowey and our Committee Chairs. who once again brought their formidable expertise to assembling a bill that is science, data and evidence-based. Yet. Trump proposal: slash billions of dollars from appropriations.

Despite these unaddressed concerns, I remain hopeful that yesterday’s developments will move us closer to an agreement on a relief package that addresses the health and economic crisis facing America’s families.

As I have said before, the devil and the angels are in the details. With over 213,000 Americans tragically having died, over 7.7 million having been infected and millions having lost jobs and income security, it is long overdue for Republicans to get serious and work with us to defeat this crisis.

These and other issues are unresolved affect lives, livelihoods and the life of our American Democracy. We hope to make progress soon. Updates will continue to be ongoing.

Of course, having used the word “hope” to describe her outlook for a deal every day for the last month, we suspect the market will love this news – no deal means a bigger deal?

Or some such idiotic logic.

She doesn’t want a deal. She cares nothing for the people hurting. It is all an cynical effort to score political points. #sadhttps://t.co/Lv9NKuDI4h

As a reminder, Alec Phillips, a policy analyst at Goldman Sachs, wrote on Friday that the “renewed urgency” from the Trump administration did lead to an “actual narrowing in positions” but a deal was still unlikely. “For now we still think the odds are against substantial pre-election stimulus even if the situation is murkier than it seemed only a few days ago,” Mr Phillips said.

via ZeroHedge News https://ift.tt/3k065Ks Tyler Durden

Ever since the crash of 2008, a trend has developed in U.S. election debate: the near complete avoidance of serious discussion about the economy. Ron Paul was the last candidate to attack the subject with any energy, and that was quite a while ago now. The economic decline of our nation is being aggressively ignored, even though it is the most important issue of the past century.

For example, talk about the actions of the Federal Reserve over the past decade has fallen off the radar. Both sides of the aisle love the Fed and both sides are happy to let the central bank print the dollar into oblivion. Both sides have mentioned little or nothing about the current stagflationary wave hitting the country, causing price inflation in many necessities, from food to electricity to rent (except for certain major cities where no one wants to live right now). And all serious examination of globalism and forced interdependency has ceased, even though global interdependency in manufacturing is one of the major causes of supply chain shortages and price inflation right now.

The real unemployment rate remains high, holding at 26.9% when accounting for U-6 measurements. While some jobs have been recovered from the initial COVID lockdown, most of these are part-time, low-wage retail and fast food jobs.

The question that might arise during the election is: Which side is more likely to keep the lockdowns going despite the economic disaster they are helping to cause?That award obviously goes to Biden, though the President continues to leave lockdown decisions to state governments, which means they will probably remain an issue regardless of the election outcome.

The small business sector has decimated by the “Retail Apocalypse”, which started in 2018 and has hit critical mass in 2020 during the lockdowns. Yelp data recently showed that 60% of small business closures due to the coronavirus are now permanent; that’s over 97,000 businesses gone in the blink of an eye. This showcases and proves that the small business bailouts were a complete failure. That’s what happens when you put global banks like J.P. Morgan in charge of which businesses get bailout dollars and which businesses don’t.

Add this to the 25,000 major retail stores set to close so far in 2020 and one can see that this is a very real crisis that could have repercussions for decades to come, but almost no one is talking about it.

Debate about the trade war with China has also taken a back seat to the pandemic, though the trade war continues and many tariffs remain in place.

Both Trump and Biden have indicated that there will be no change to the trade war posture of the U.S. post-election, and so tensions with China will only increase. While China is one of the worst human rights violators on the planet and, in my opinion, their communist government should be erased from existence, there is a little issue of debt and monetary investment that, again, no one is talking about.

China not only has the ability to dump trillions in U.S. Treasuries back on the market, but it also has the option of dumping the U.S. dollar as the world reserve currency. As the number one exporter/importer in the world, China could cause significant damage to the U.S. economy if they drop the dollar and their trade partners follow their lead. I believe this threat will become clearer in 2021, AFTER the election is over.

The problem of U.S. dependency on Chinese manufacturing has been mentioned during the campaign, but merely in passing. No serious plan to bring production back to the U.S. has been presented by either side, and this seems to be the predictable narrative of every election for the past 12 years: Use buzzwords on the economy to pretend as if candidates care while never offering a practical plan for solving the underlying problems.

Tax cuts or tax increases are irrelevant and do nothing beyond causing minor short-term shifts in cash flows. The very root of the U.S. financial system (and the global financial system) is rotten, and NOTHING is being done about it by either political party.

There needs to be a reckoning, and certain figures within the finance and banking structure need to answer for their criminality. International banks like Goldman Sachs and J.P. Morgan contributed directly to the creation of the mortgage and credit crisis of 2008, and they did so with full knowledge that the derivatives bubble was about to collapse. Yet, to this day, they continue to operate with impunity around the world and offer “advice” to investors and governments on economic management. In 2020 they continue to enjoy bailout dollars from the Fed, and when they are exposed for fraud, they simply get a slap on the wrist and a fine.

The outcome of all this is rather predictable: Small businesses are going to disappear and what’s left of the localized economy in the U.S. is going to be destroyed. International corporations, the only businesses enjoying reliable protection from the Fed, will remain as the only game left in town. It is almost as if the economy is being forcefully streamlined into a global centralized model with the major corporations at the helm…

For those people who put a lot of stock in elections, I think it’s important for them to remember that very little of actual importance changes in the course of political events. Problems are not solved by politicians or presidents; problems are always solved by the people, if they get solved at all.

This means that the ongoing downtrend in the U.S. economy is assured even after the 2020 election, and no matter who ends up in the White House, the crash will likely accelerate because the causes of the crash are never dealt with. Fundamentally, local production and trade is the key to saving America. This is how America’s economy was able to survive and thrive at the formation of our system, and it only makes sense to return to a free market model that was proven to work.

If major manufacturing is ever going to return to the U.S., companies need to be incentivized. Why are corporations enjoying lavish tax cuts without having to give anything in return? Shouldn’t tax cuts come with strings attached, such as a requirement that they bring home a large portion of their factory base to U.S. soil?

Decentralization means more than just moving away from globalism; it also means that each and every community has to pursue self-reliance and establish its own production model. Instead of trading our wealth and work to international companies that siphon dollars away from our communities, we need to develop our own local trade and keep at least a fair portion of those dollars circulating in our own towns and neighborhoods. We also need to start focusing on necessities and being able to provide for ourselves in the event that the international supply chain breaks even further.

The elections do not, and probably will not, address any of the issues I describe above because they are a circus that distracts away from legitimate dangers. Elections are meant to control the narrative, not give the public a voice. By all means, vote for whoever you like, just keep in mind that our duty as Americans does not stop at the voting booth; it is our job to fix this country and to save ourselves. The politicians are irrelevant.

* * *

After 8 long years of ultra-loose monetary policy from the Federal Reserve, it’s no secret that inflation is primed to soar. If your IRA or 401(k) is exposed to this threat, it’s critical to act now! That’s why thousands of Americans are moving their retirement into a Gold IRA. Learn how you can too with a free info kit on gold from Birch Gold Group. It reveals the little-known IRS Tax Law to move your IRA or 401(k) into gold. Click here to get your free Info Kit on Gold.

via ZeroHedge News https://ift.tt/3lvYrIi Tyler Durden

Watch Live: In First Post-COVID-19 Event, Trump Speaks On “Law & Order” At White House “Peaceful Protest” Tyler Durden

Sat, 10/10/2020 – 13:55

Following last night’s interview on Tucker Carlson, President Trump will hold his first “live event” since being diagnosed with the coronavirus Saturday afternoon. Starting at 1400ET, Trump will speak from the South Lawn balcony about “law and order” in an event that has been cheekily dubbed a “peaceful protest”, which CBS News says is expected to draw hundreds of people.

The address notably comes just two weeks after the president nominated Amy Coney Barrett to fill Ruth Bader Ginsburg’s seat on the Supreme Court. Hearings to move her nomination forward are set to begin next week.

Notably, the White House is coordinating with Candace Owens’s “Blexit” group, and black conservative activists are expected to attend.

2,000 invitations have reportedly been issued, and attendees will be required to bring (and wear) masks, all attendees must also complete COVID-19 screenings.

On Friday, Dr. Fauci was widely quoted for describing Trump’s Sept. 26 ceremony unveiling the nomination of Judge Barrett as a “super spreader event”. And many have claimed that the White House is tempting fate by holdng another one.

via ZeroHedge News https://ift.tt/36VTMLF Tyler Durden

‘White Supremacist’ Narrative Unravels: Whitmer Kidnap Suspect Attended BLM Rally, Another Called Trump A ‘Tyrant’ Tyler Durden

Sat, 10/10/2020 – 13:40

Last week, the FBI says it foiled a plot to kidnap Michigan Governor Gretchen Whitmer (D), after the FBI infiltrated an anti-government militia and arrested 13 members who “talked about murdering ‘tyrants’ or ‘taking’ a sitting governor.”

And while the FBI never suggested a race-based ideology in its criminal complaint, the MSM – as well as Michigan Attorney General Dana Nessel (D), took the ‘white supremacist’ ball and ran with it – hard.

On Friday, however, the Washington Post profiled several members of the group. Notably absent were accusations of ‘white supremacy’ – perhaps after acknowledging:

“One of alleged plotters, 23-year-old Daniel Harris, attended a Black Lives Matter protest in June, telling the Oakland County Times he was upset about the killing of George Floyd and police violence.”

Another alleged plotter, Brandon Caserta, called President Trump a ‘tyrant’ – adding ‘Trump is not your friend, dude.‘ Caserta notably has an anarchist flag behind him in several videos he’s recorded.

Wow! This is big. Brandon Caserta, one of the ringleaders of the group of men arrested for a plot where the group planned to kidnap Gov. Gretchen Whitmer, hated President Trump too!

“They are oppressing you for a paycheck. If you’re still supporting law enforcement, you are supporting the people who are enforcing slavery on everyone else.”

This is Brandon Caserta, a man who was arrested for a plot to kidnap Gov. Whitmer. He’s a police hating anarchist. pic.twitter.com/3qGZpPpOJw

What’s more, there isn’t a shred of evidence included in the FBI’s criminal complaint, nor subsequent reporting, that the men adhered to a white supremacist ideology.

And so, it appears that the FBI busted an anarchist, anti-government militia which plotted violence against elected officials – yet hated both sides of the aisle.

Let’s see how fast this entire affair disappears from the news cycle.

via ZeroHedge News https://ift.tt/36TCmiW Tyler Durden

The cybersecurity firm CrowdStrike rose to global prominence in mid-June 2016 when it publicly accused Russia of hacking the Democratic National Committee and stealing its data. The previously unknown company’s explosive allegation set off a seismic chain of events that engulfs U.S. national politics to this day. The Hillary Clinton campaign seized on CrowdStrike’s claim by accusing Russia of meddling in the election to help Donald Trump. U.S. intelligence officials would soon also endorse CrowdStrike’s allegation and pursue what amounted to a multi-year, all-consuming investigation of Russian interference and Trump’s potential complicity.

With the next presidential election now in its final weeks, the Democrats’ national leader, House Speaker Nancy Pelosi, and her husband, Paul Pelosi, are endorsing the publicly traded firm in a different way. Recent financial disclosure filings show the couple have invested up to $1 million in CrowdStrike Holdings. The Pelosis purchased the stock at a share price of $129.25 on Sept. 3. At the time of this article’s publication, the price has risen to $142.97.

Drew Hammill, spokesman for Pelosi, said:

“Speaker Pelosi is not involved in her husband’s investments and was not aware of the investment until the required filing was made. Mr. Pelosi is a private investor and has investments in a number of publicly traded companies. The Speaker fully complies with House Rules and the relevant statutory requirements.”

The Pelosis’ sizeable investment in CrowdStrike could revive scrutiny of the company’s involvement in the Trump-Russia saga since the Democrats’ 2016 election loss.

Dmitri Alperovitch: The CrowdStrike co-founder reportedly was thanked by a senior U.S. official “for pushing the government along” in its DNC hacking probe. CrowdStrike.com

After generating the hacking allegation against Russia in 2016, CrowdStrike played a critical role in the FBI’s ensuing investigation of the DNC data theft. CrowdStrike executives shared intelligence with the FBI on a consistent basis, making dozens of contacts in the investigation’s early months. According to Esquire, when U.S. intelligence officials first accused Russia of conducting malicious cyber activity in October 2016, a senior U.S. government official personally alerted CrowdStrike co-founder Dmitri Alperovitch and thanked him “for pushing the government along.” The final reports of both Special Counsel Robert Mueller and the Senate Intelligence Committee cite CrowdStrike’s forensics. The firm’s centrality to Russiagate has drawn the ire of President Trump. During the fateful July 2019 phone call that would later trigger impeachment proceedings, Trump asked Ukraine’s Volodymyr Zelensky to scrutinize CrowdStrike’s role in the DNC server breach, suggesting that the company may have been involved in hiding the real perpetrators.

Pelosi’s recent investment in CrowdStrike also adds a new partisan entanglement for a company with significant connections to Democratic Party and intelligence officials that drove Russiagate.

DNC law firm Perkins Coie hired CrowdStrike to investigate the breach in late April 2016. At the outset, Perkins Coie attorney Michael Sussmann personally informed CrowdStrike officials that Russia was suspected of breaching the server. By the time CrowdStrike went public with the Russian hacking allegation less than two months later, Perkins Coie had recently hired Fusion GPS, the opposition research firm that produced discredited Steele dossier alleging a longstanding conspiracy between Trump and Russia.

Shawn Henry: Behind closed doors, the CrowdStrike president admitted under oath in December 2017 that his firm “did not have concrete evidence” that Russian hackers actually stole any emails or other data from the DNC servers. “There’s circumstantial evidence, but no evidence that they were actually exfiltrated.” CrowdStrike.com

CrowdStrike President Shawn Henry, who led the team that remediated the DNC breach and blamed Russia for the hacking, previously served as assistant director at the FBI under Robert Mueller. Since June 2015, Henry has also worked as an analyst at MSNBC, the cable network that has promoted debunked Trump-Russia innuendo perhaps more than any other outlet. Alperovitch, the co-founder and former chief technology officer, is a former nonresident senior fellow at the Atlantic Council, the Washington organization that actively lobbies for a hawkish posture toward Russia.

Campaign disclosures also show that CrowdStrike contributed $100,000 to the Democratic Governors Association in 2016 and 2017.

The firm’s multiple conflicts of interest in the Russia investigation coincide with a series of embarrassing disclosures that call into question its technical reliability.

In early 2017, CrowdStrike was forced to retract its allegation that Russia had hacked Ukrainian military equipment with the same malware the firm claimed to have discovered inside the DNC server.

During the FBI’s investigation of the DNC breach, CrowdStrike never provided direct access to the pilfered servers, rebuffing multiple requests that came from officials all the way up to then-Director James Comey. The FBI had to rely on CrowdStrike’s own images of the servers, as well as reports that Justice Department officials later acknowledged were delivered in incomplete, redacted form. James Trainor, who served as assistant director of the FBI’s Cyber Division, complained to the Senate Intelligence Committee that the DNC’s cooperation with the FBI’s 2016 hack investigation was “slow and laborious in many respects” and that CrowdStrike’s information was “scrubbed” before it was handed over. Alperovitch, the former CTO, has claimed that CrowdStrike installed its Falcon software to protect the DNC server on May 5, 2016. Yet the Democratic Party emails were stolen from the server three weeks later, from May 25 to June 1.

Yet the most damaging revelation calling into question CrowdStrike’s Russian hacking allegations came with an admission early in the Russia probe that was only made public this year. Unsealed testimony from the House Intelligence Committee shows that Henry admitted under oath behind closed doors in December 2017 that the firm “did not have concrete evidence” that Russian hackers actually stole any emails or other data from the DNC servers.

“There’s circumstantial evidence, but no evidence that they were actually exfiltrated,” Henry said.

“There are times when we can see data exfiltrated, and we can say conclusively. But in this case it appears it was set up to be exfiltrated, but we just don’t have the evidence that says it actually left.”

The Henry testimony was among a trove of damning transcripts released by House Intelligence Committee Chairman Adam Schiff only after pressure from the then-acting Director of the Office of the Director of National Intelligence, Richard Grenell.

As RealClearInvestigations reported last month, Henry’s House testimony also conflicts with his testimony before the Senate Intelligence Committee two months prior, in October 2017. According to the Senate report, Henry claimed that CrowdStrike was “able to see some exfiltration and the types of files that had been touched,” but not the files’ content. Yet two months later, Henry told the House that “we didn’t see the data leave, but we believe it left, based on what we saw.”

Adam Schiff: CrowdStrike testimony was released by the House Intelligence Committee chairman only after pressure from the then-acting Director of National Intelligence, Richard Grenell. AP Photo/Alex Brandon

Notably, Henry’s acknowledgment to the House that CrowdStrike did not have evidence of exfiltration came only after he was interrupted and prodded by his attorneys to correct an initial answer. Right before that intervention from CrowdStrike counsel, Henry had falsely asserted that he knew when Russian hackers had exfiltrated the stolen information:

Adam Schiff: Do you know the date in which the Russians exfiltrated the data from the DNC?

Shawn Henry: I do. I have to just think about it. I don’t know. I mean, it’s in our report that I think the Committee has.

Schiff: And, to the best of your recollection, when would that have been?

Henry: Counsel just reminded me that, as it relates to the DNC, we have indicators that data was exfiltrated. We do not have concrete evidence that data was exfiltrated from the DNC, but we have indicators that it was exfiltrated.

Henry then improbably argued that, in the absence of evidence showing the emails leaving the DNC server, Russian hackers could have taken individual screenshots of each of the 44,053 emails and 17,761 attachments that were ultimately put out by WikiLeaks.

Keeping Henry’s admission under wraps for nearly four years was highly consequential. The allegation of Russian hacking was elevated to a dire national security issue, and anyone who dared to question it – including President Trump – was accused of doing the Kremlin’s bidding. The hacking allegation also helped plunge U.S.-Russia relations to new lows. Under persistent bipartisan pressure over allegations of Russian meddling, Trump has approved a series of punitive measures and aggressive policies toward Moscow, shunning his own campaign vow to seek cooperation.

Meanwhile, during the several years that CrowdStrike’s own uncertainty about its hacking allegation was kept from the public, the firm has enjoyed a stratospheric rise on Wall Street. In 2017, one year after lodging its Russia hacking allegations, CrowdStrike had a valuation of $1 billion. Three years later, after going public in 2019, the firm’s valuation was set at $6.7 billion, and soon hit $11.4 billion. Just over a year later, its market cap was $31.37 billion. CrowdStrike has more than doubled its revenue on average every year, going from $52.75 million in 2017 to $481.41 million in 2020.

CrowdStrike and Fusion GPS, which spread Trump-Russia collusion allegations via the Steele dossier, are not the only private companies to play a critical and lucrative role in the Trump-Russia saga.

The firm New Knowledge, staffed by several former Democratic Party operatives and intelligence officials, authored a disputed report for the Senate Intelligence Committee that accused a Russian troll farm of a sophisticated social media interference campaign that duped millions of vulnerable Americans. Ironically, the company itself took part in a social media disinformation operation in the 2017 Alabama Senate race to help elect the ultimate victor, Democratic candidate Doug Jones. Just as the Democratic Party’s impeachment proceedings were in full swing a year ago, another cybersecurity firm with Democratic Party ties, Area One, accused the Russian spy agency GRU of hacking into the Ukrainian company Burisma with the aim of uncovering dirt on Joe Biden. Graphika, a firm with extensive ties to the Atlantic Council and the Pentagon, has recently put out reports accusing Russians of impersonating left-wing and right-wing websites to fool hyper-partisan American audiences.

Having generated the seminal Russian hacking allegation, CrowdStrike sits at the top of what has become a booming cottage industry of firms and organizations to help shape the multi-year barrage of Russia fear-mongering and innuendo. And with her new investment in CrowdStrike, Nancy Pelosi — the highest-ranking elected official of a party that has promoted Russiagate above all else — is already profiting from its success.

via ZeroHedge News https://ift.tt/36XKKOt Tyler Durden