Lira Drops Like A Stone After Turkish Central Bank Unexpectedly Hikes By 200 bps Tyler Durden

Thu, 09/24/2020 – 07:30

With the Turkish economy hammered as a result of a collapse in global tourism, the country’s FX reserves dwindling by the day preventing the infamous Turkish interventions to stabilize the currency, Moody’s warning that Turkey faces an imminent balance of payments crisis, and the entire world cutting rates and easing to stimulate economies, the last thing Wall Street expected this morning from the CBRT was a rate hike – even though the Turkish Lira had been hitting daily record lows every single day for the past two weeks.

And yet moments ago, the Central Bank of Turkey shocked investors when it announced a whopping 200bps hike in the one week repo rate, from 8.25% to 10.25%, the first hike from Turkey in two years following an aggressive easing cycle which was unleashed when the rate hit a record 24% in late 2018.

Until now, political pressure from President Recep Tayyip Erdogan, who has demanded lower rates, forced the CBRT to tighten by stealth. Instead of hiking the main policy rate, the central bank had shut access to the one-week repo window, forcing banks to borrow at more expensive liquidity facilities. In the end, the central bank was forced to hike rates as the lira hit a record low against the dollar and inflation is still in double digits, while the average cost of CBRT funding has risen by almost 300 basis points since mid-July.

Wall Street economists had noted that the combination of an elevated risk premium, the challenging inflation outlook and subdued inflows suggested that the CBT was likely to implement further tightening, but consensus was that this would happen via liquidity measures.

Whether the hike was also driven by Turkey’s obsession with hammering TRY shorts remains unknown but the official explanation from the CBRT is that it decided to increase the policy rate by 200bps to restore the disinflation process and “support price stability” adding that “the Committee assessed that the tightening steps taken since August should be reinforced in order to contain inflation expectations and risks to the inflation outlook. Accordingly, the Committee decided to increase the policy rate by 200 basis points to restore the disinflation process and support price stability.”

The full statement is below:

While global economic activity has shown signs of partial recovery in the third quarter following the normalization steps taken by several countries, uncertainties on global economic recovery remain high. Advanced and emerging economies continue to maintain expansionary monetary and fiscal stances. The pandemic disease is closely monitored for its evolving global impact on capital flows, financial conditions, international trade and commodity prices.

Economic activity is recovering markedly in the third quarter owing to gradual steps towards normalization and the strong credit impulse. Recent monetary and fiscal measures that aim to contain negative effects of the pandemic on the Turkish economy contributed to financial stability and economic recovery by supporting the potential output of the economy. The normalization trend recently observed in commercial loans has started in consumer loans as well. The recent upturn in imports, which has resulted from deferred demand as well as pandemic-related liquidity and credit policies, is expected to moderate with the phasing out of these policy measures. Although tourism revenues declined due to the pandemic, easing of travel restrictions has started to contribute to a partial improvement. The recovery in exports of goods, relatively low levels of commodity prices and the level of the real exchange rate will support the current account balance in the upcoming periods.

Pandemic-related supply-side inflationary factors were expected to gradually phase out during the normalization process and demand-driven disinflationary effects were expected to become more prevalent. Yet, as a result of fast economic recovery with strong credit momentum, and financial market developments, inflation followed a higher-than-envisaged path. The Committee assessed that the tightening steps taken since August should be reinforced in order to contain inflation expectations and risks to the inflation outlook. Accordingly, the Committee decided to increase the policy rate by 200 basis points to restore the disinflation process and support price stability.

The Committee assesses that maintaining a sustained disinflation process is a key factor for achieving lower sovereign risk, lower long-term interest rates, and stronger economic recovery. Keeping the disinflation process in track with the targeted path requires the continuation of a cautious monetary stance. In this respect, monetary stance will be determined by considering the indicators of the underlying inflation trend to ensure the continuation of the disinflation process. The Central Bank will continue to use all available instruments in pursuit of the price stability and financial stability objectives.

In kneejerk response, the Turkish Lira jumped as much as 1.9% to 7.5572 per dollar before fading some of the gains to 7.6165.

It is too early to tell whether this surge can be sustained: in addition to economic considerations, traders are also focusing on the latest geopolitical developments: the EU leader summit scheduled for today was delayed to October 1-2 where Turkey’s tensions with Greece and Cyprus over Mediterranean Sea drilling will be discussed.

via ZeroHedge News https://ift.tt/3hZHggf Tyler Durden

Carmine Di Sibio, the international chairman of EY, said in a letter to clients published earlier thsi month that while he “regrets” the firm’s staggering lapse in supervising Wirecard (something the firm has continued to blame entirely on Wirecard’s deceptions, along with the invisible hand of Russian intelligence), the incident was a lesson learned, though he insisted that EY was ultimately “successful” in detecting the fraud.

While that’s technically true, it’s also true that dozens of red flags surfaced over the years that seemed to openly hint at the ongoing massive fraud operating just below the surface. And as auditors, regulators and prosecutors sift through the wreckage, they’re uncovering more stunning details prompting them to ask themselves: How did Wirecard’s shell game continue for so long without anybody speaking up?

The Financial Times, a paper that put its reputation on the line to back its reporting on Wirecard, and was ultimately vindicated after facing startling pushback from Wall Street analysts, Wirecard and German regulators, obtained a copy of an early report from Wirecard’s administrator. As bankruptcy courts pick through the wreckage, the report reveals that the fraud at Wirecard ran much deeper than the Southeast Asia business that was previously reported as the locus of the fraud.

In reality, Wirecard had only a few profitable business lines. And the stupefying staff and operational bloat that the company carried is almost shocking. Just imagine: Thousands of employees, shuffling paper, performing “busywork” with no real purpose like a nightmarish, real-life take on “Office Space”.

The €1.9 billion in fraudulent profits Wirecard reported between the beginning of 2015 and Q1 2020 was actually a €740 million ($860) loss. Even if the fraud hadn’t been uncovered when it did – even if the FT had never printed a word – the company would have eventually dissolved, as the burn rate far outstripped any reasonable expectation of income or capital raised.

Furthermore, bankruptcy court has determined that the real value of Wirecard’s assets is just €428 million, an amount dwarfed by the €3.2 billion in debt Wirecard carried when it collapsed.

Wirecard’s fabricated Asian business was not its only deception. The rest of the once-lauded German payment provider’s business was chaotic, beset by byzantine reporting lines, hobbled by lamentable IT and racking up losses, according to a report by Wirecard’s administrator and accounts of former employees. The picture that emerges of the Wirecard businesses that did exist is a stark contrast to the one painted by former chief executive Markus Braun, who hailed the group as a highly profitable pioneer in the payments industry. It reveals the scale on which the company, Germany’s biggest corporate fraud in decades, also misled investors about its real businesses. “Only a few units of the group were actually involved in conducting operative business that was customer-facing and generated revenue,” the administrator Michael Jaffé wrote in his report, a copy of which was seen by the Financial Times.

So, what did Wirecard spend all this money on? Well, certainly not IT. The report cited by the FT shows that Wirecard’s businesses ran on a hodgepodge of IT systems that were virtually unworkable. Any IT auditor would have noted significant issues, they said.

Its computer systems were inherited from companies acquired over the years and never fully integrated. Wirecard Bank, for instance, is still running on software originally developed for Germany’s small co-operative banks and which will be switched off by its IT service provider by the end of this year, according to people familiar with the matter. “If IT auditors had been professional and serious, huge risks, weaknesses and non-compliance issues would have emerged a long time ago,” according to a former Wirecard IT employee, who was scathing about the “unbelievable brittleness of [Wirecard’s] IT infrastructure”.

Even up until its final months before diving into bankruptcy, Wirecard continued to expand its head count. All told, the company had more than 6,000 employees around the world. But only a fraction of them were needed to run the business.

Even as Wirecard faced increasing scrutiny of its accounting, the group’s headcount continued to rise, climbing by a quarter from early last year to 6,300 at the time of its implosion. Over the same period, its real revenues grew at less than half that rate, according to the administrator. The report points to bloated costs and a colossal amount of corporate waste. “Employees never faced the necessity to reduce the services they were using to those that were really needed as cash was abundantly available in the past,” it noted, adding that the company was suffering from “excessive overhead and personnel capacities”. “Only a fraction” of the employees were actually required to run Wirecard’s non-fraudulent business, the report found.

With this rate of burn, the company would have needed to raise money by the end of the year, or face insolvency.

By the time it unravelled in late June, the total was €10m a week and the company’s own internal planning predicted that figure would rise to more than €15m — some €200m for the third quarter as a whole, according to the administrator’s report. At that rate, Wirecard would have needed to raise fresh cash by the end of this year to pay its bills.

Wirecard’s “totally opaque” structure and “small business mentality” meant that its 55 subsidiaries were all effectively siloed off from one another. The main office in Munich had no idea what was going on elsewhere. in retrospect, it’s a setup seemingly designed to enable an ongoing fraud.

If extravagant spending is one of Mr Jaffé’s findings, another is what the report describes as Wirecard’s “totally opaque” and inefficient structure, consisting of at least 55 subsidiaries scattered over four continents. Staff at its headquarters on the outskirts of Munich did not know what the group’s different units were doing, the administrator concluded, with neither their tasks and responsibilities — or the payments and loans between the divisions — properly recorded. There was “a small business mentality” at many of its units, former employees told the FT, describing businesses that Wirecard had hoovered up around the world and largely left to their own devices.

At times, this led to “bizarre outcomes”, like employees in the antipodes performing work for distant offices in Europe.

The internal chaos led to bizarre outcomes. A team of IT specialists, working in Athens, but part of a subsidiary with headquarters in New Zealand, provided services to Wirecard’s German HQ that were not needed, the administrator found. In another example, when the administrator asked managers at a different Asian-based subsidiary about how they contributed to the group, the reply was “we don’t really know”, according to a person briefed on the matter.

The FT concluded its report with a comment from a German finance professor who argued that the fraud should have been caught earlier, and the fact that any “Big 4” firm would miss such conspicuous red flags is too difficult to believe. Perhaps a blind eye was turned. Or maybe auditors really were blinded by ex-CEO Markus Baram’s marketing prowess, that they simply didn’t question it when the company launched into technical explanations of its – totally fictitious – business.

via ZeroHedge News https://ift.tt/3cphSzg Tyler Durden

Media Declares “Violence Is Inevitable” As 2 Cops Shot In Louisville; Reporters Arrested In Aggressive Police Crackdown Tyler Durden

Thu, 09/24/2020 – 06:45

As we reported last night, protesters hit the streets in Louisville, NYC, LA, Denver, Oakland, Washington DC and other cities across the US after a Kentucky grand jury decided that no officers would be charged in the killing of Breonna Taylor, a tragic accident that was the result of officers serving a “no-knock” warrant.

In Louisville, the city where Taylor was shot and killed, 2 police were shot as gunfire broke out downtown after hundreds “peacefully” marched earlier in the evening. But as has become distressingly familiar, the real hard-core agitators came out after dark. A suspect in the shooting of the two officers was taken into custody shortly after, but he wasn’t the only “protester” who was packing heat at the “non-violent demonstration.”

LOUISVILLE: a rioter is detainee by police for brandishing a firearm

Reporter @livesmattershow is on the scene now, says reporters are getting arrested

Amazingly, left-leaning media outlets had the gall to frame the shooting of two police as an “inevitable”, while framing the events of last night in distorted terms that served to support their narrative of a corrupt justice system absolving three murderers, instead of reporting the facts: that a jury of their peers – not some unassailable magistrate – decided on the indictments for the three officers.

The Daily Beast reported that none of the officers were charged for Breonna Taylor’s killing. While that’s technically true – officer Brett Hankison was charged with three counts of wanton endangerment for firing into a nearby occupied apartment, not for the shots that killed Taylor, which were fired by a colleague – the result is misleading, and intentionally so, we suspect.

But we digress. Circling back to the events of Wednesday night, the Louisville Metropolitan Police Department – better known as the LMPD – aggressively enforced curfew violations after the shooting. Several reporters – including two journalists for the Daily Caller – were arrested during the sweep, and despite protests from their editors, were charged with breaking curfew and attending an “unlawful” assembly. It’s believed that dozens of protesters and reporters were taken into custody during the sweep of Jefferson Square, which has served as the base for BLM protesters who have been out demonstrating every night for the past 118 days.

Multiple members of the press were arrested tonight and are facing charges, along with an even larger number of protesters facing a multitude of charges. Chaotic night here in Kentucky. #Louisville#LouisvilleProtests

When editors reached out, the department refused to budge.

I’ve now notified @LMPD that both @shelbytalcott and @VenturaReport were reporting for an accredited media outlet and were operating in the capacity of press. My expectation is that they will be swiftly released. https://t.co/BBa1b8yF1W

Update: The Louisville doc tells me @ShelbyTalcott and @VenturaReport will be processed and charged like everyone else, despite my best efforts to alert official channels that they were operating in the capacity of press at a live news event. @LMPD

Another update: @LMPD tells me @ShelbyTalcott and @JorgeVentura05 will be charged with two misdemeanors related to breaking curfew & unlawful assembly for their alleged failure to comply with police orders to disperse and for press to relegate themselves to an “observation area”

Circling back to the wounded officers, Interim LMPD chief Robert Schroeder confirmed the two officers had been shot and sustained life-threatened injuries, and that a suspect was in custody. One of the officers was shot in the abdomen, while the the other was shot in the thigh.

“I am very concerned about the safety of our officers,” Schroeder said. “Obviously we’ve had two officers shot tonight, and that is very serious. … I think the safety of our officers and the community we serve is of the utmost importance,” Schroeder said, according to the Courier-Journal.

As of 11pm local time on Thursday, police had arrested 46 people, which includes those arrested in the sweep of Jefferson Square, which reportedly happened around 8pm.

Independent video journalist Brendan Gutenschwager narrowly avoided arrest last night. Afterward, he chronicled the eerily silent streets, and surveyed the damage.

Within 12 hours of the Breonna Taylor announcement

– Miles of marches through Louisville

– Looting and vandalism in various parts of the city

– Fires lit downtown

– Live ammunition fired off

– 2 officers shot and taken to the hospital

– Mass arrests

This city is on edge.

With a severe crackdown on the curfew, things are ‘calm’ here in Louisville for the night. Simultaneously, the Pacific coast is going off right now in Portland and Seattle. Hearing retroactively about DC, Chicago and elsewhere. Unrest across America’s cities tonight.

Thousands gathered across NYC and LA, and hundreds more in Portland, Chicago, Atlanta and other cities around the country as others marched “in solidarity”.

Expect the unrest to continue Thursday, as it has for nearly 120 days.

via ZeroHedge News https://ift.tt/2RWLp9U Tyler Durden

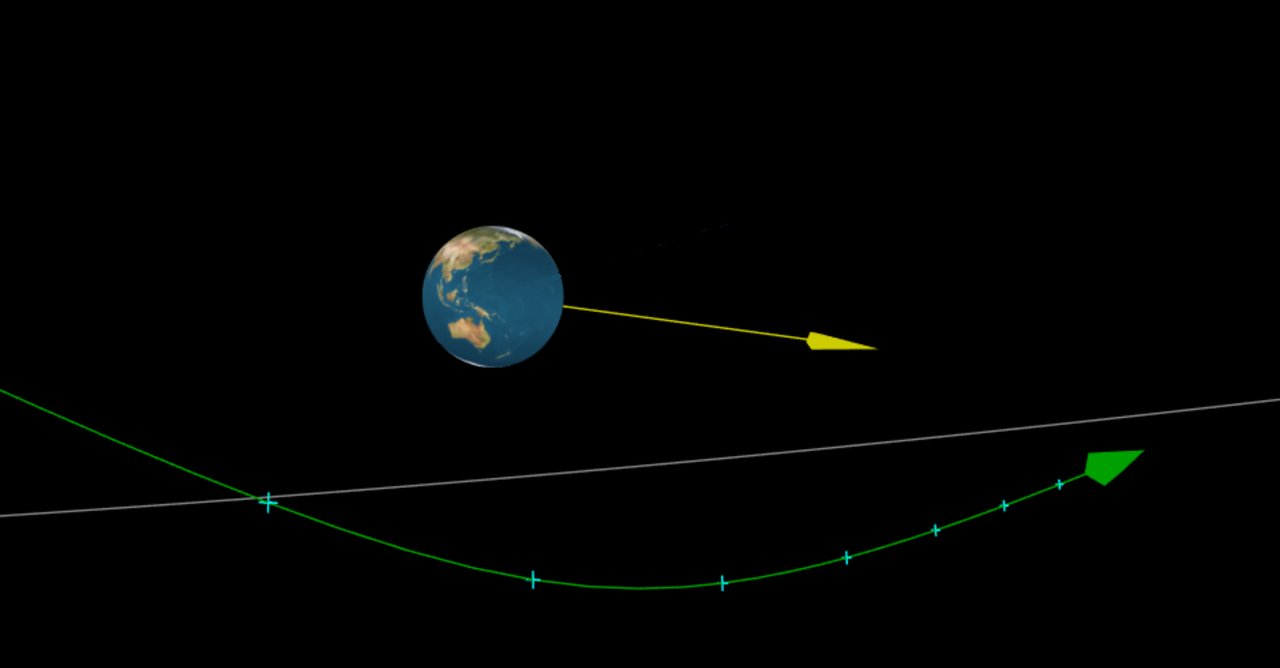

Watch Live: “School Bus” Sized Asteroid Expected To Buzz Earth Thursday Tyler Durden

Thu, 09/24/2020 – 06:40

NASA reports a small near-Earth asteroid (or NEA), the size of a “small school bus,” will buzz Earth Thursday (Sept. 24) at a distance closer than the moon and most geostationary weather satellites.

2020 SW, discovered by @Catalina_sky, is about 15 to 30 ft. wide and will pass by Earth Thurs., Sept. 24, at a distance of about 13,000 miles (22,000 km). Tiny asteroids like 2020 SW approach Earth this closely several times every year and aren’t a threat: https://t.co/xKWtzxLI7Qpic.twitter.com/FpkY77zibw

The asteroid, named 2020 SW, was discovered last Thursday (Sept. 18) by NASA-funded Catalina Sky Survey in Arizona. The size of the asteroid is an estimated 15 feet by 30 feet wide, making it roughly the size of a “small school bus,” said NASA.

The space agency points out 2020 SW is “not on an impact trajectory with Earth, if it were, the space rock would almost certainly break up high in the atmosphere, becoming a bright meteor known as a fireball.”

Paul Chodas, director of the Center for Near-Earth Object Studies (CNEOS) at NASA’s Jet Propulsion Laboratory in Southern California, said: “There are a large number of tiny asteroids like this one, and several of them approach our planet as close as this several times every year.

“In fact, asteroids of this size impact our atmosphere at an average rate of about once every year or two,” said Chodas.

CNEOS expects the asteroid to zoom past Earth at a distance of about 13,000 miles over the Southeastern Pacific Ocean around 0712 ET on Thursday.

In Unprecedented Monetary Overhaul, The Fed Is Preparing To Deposit “Digital Dollars” Directly To “Each American” Tyler Durden

Thu, 09/24/2020 – 04:19

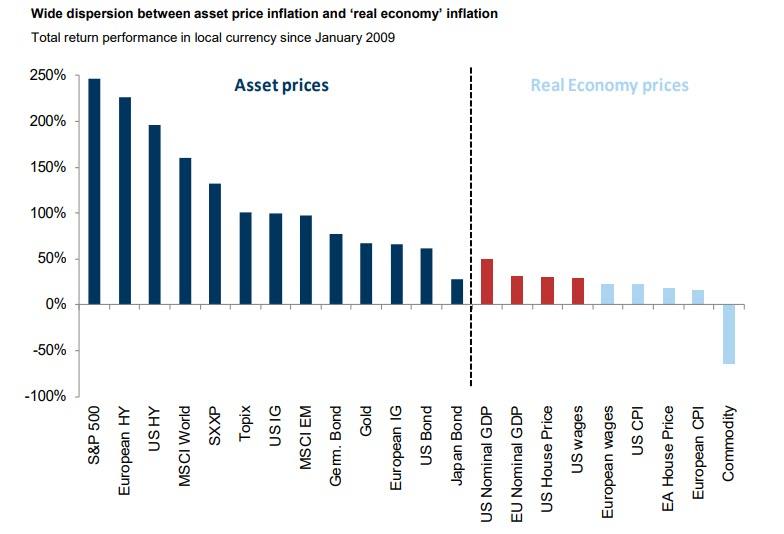

Over the past decade, the one common theme despite the political upheaval and growing social and geopolitical instability, was that the market would keep marching higher and the Fed would continue injecting liquidity into the system. The second common theme is that despite sparking unprecedented asset price inflation, prices as measured across the broader economy – using the flawed CPI metric and certainly stagnant worker wages – would remain subdued (as a reminder, the Fed is desperate to ignite broad inflation as that is the only way the countless trillions of excess debt can be eliminated and has so far failed to do so).

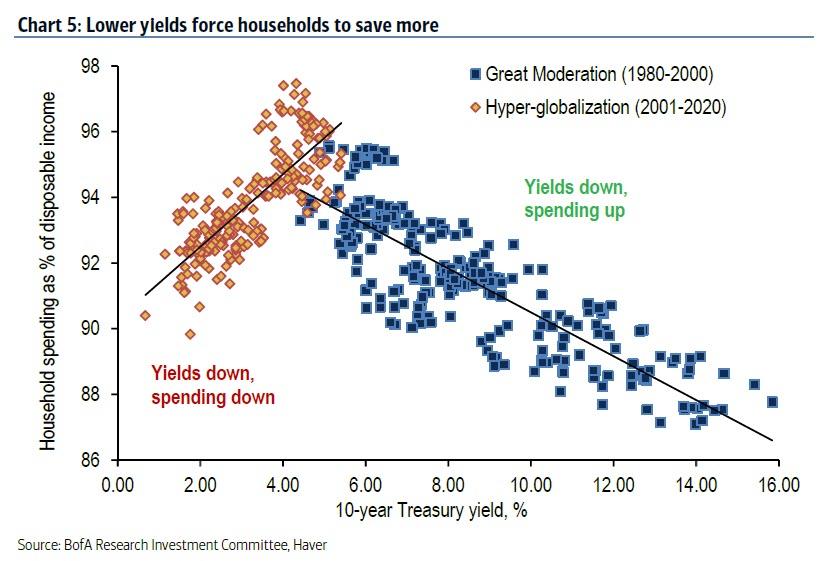

The Fed’s failure to reach its inflation target – which prompted the US central bank to radically overhaul its monetary dogma last month and unveil Flexible Average Inflation Targeting (or FAIT) whereby the Fed will allow inflation to run hot without hiking rates – has sparked broad criticism from the economic establishment, even though as we showed in June, deflation is now a direct function of the Fed’s unconventional monetary policies as the lower yields slide, the lower the propensity to spend. In other words, the harder the Fed fights to stimulate inflation, the more deflation and more saving it spurs as a result (incidentally this is not the first time this “discovery” was made, in December we wrote “One Bank Makes A Stunning Discovery – The Fed’s Rate Cuts Are Now Deflationary“).

In short, ever since the Fed launched QE and NIRP, it has been making the situation it has been trying to “fix” even worse while blowing the biggest asset price bubble in history.

And having recently accepted that its preferred stimulus pathway has failed to boost the broader economy, the blame has fallen on how monetary policy is intermediated, specifically the way the Fed creates excess reserves which end up at commercial banks instead of “tricking down” all the way to the consumer level.

To be sure, in the aftermath of the covid pandemic shutdowns the Fed has tried to short-circuit this process, and in conjunction with the Treasury it has launched “helicopter money” which has resulted in a direct transfer of funds to US corporations via PPP loans, as well as to end consumers via the emergency $600 weekly unemployment benefits which however are set to expire unless renewed by Congress as explained last week, as Democrats and Republicans feud over which fiscal stimulus will be implemented next.

And yet, the lament is that even as the economy was desperately in need of a massive liquidity tsunami, the funds created by the Fed and Treasury (now that the US operates under a quasi-MMT regime) did not make their way to those who need them the most: end consumers.

Which is why we read with great interest a Bloomberg interview with two former Fed officials: Simon Potter, who led the Federal Reserve Bank of New York’s markets group i.e., he was the head of the Fed’s Plunge Protection Team for years, and Julia Coronado, who spent eight years as an economist for the Fed’s Board of Governors, who are among the innovators brainstorming solutions to what has emerged as the most crucial and difficult problem facing the Fed: get money swiftly to people who need it most in a crisis.

The response was striking: the two propose creating a monetary tool that they call recession insurance bonds, which draw on some of the advances in digital payments, which will be wired instantly to Americans.

As Coronado explained the details, Congress would grant the Federal Reserve an additional tool for providing support—say, a percent of GDP [in a lump sum that would be divided equally and distributed] to households in a recession. Recession insurance bonds would be zero-coupon securities, a contingent asset of households that would basically lie in wait. The trigger could be reaching the zero lower bound on interest rates or, as economist Claudia Sahm has proposed, a 0.5 percentage point increase in the unemployment rate. The Fed would then activate the securities and deposit the funds digitally in households’ apps.

As Potter added, “it took Congress too long to get money to people, and it’s too clunky. We need a separate infrastructure. The Fed could buy the bonds quickly without going to the private market. On March 15 they could have said interest rates are now at zero, we’re activating X amount of the bonds, and we’ll be tracking the unemployment rate—if it increases above this level, we’ll buy more. The bonds will be on the asset side of the Fed’s balance sheet; the digital dollars in people’s accounts will be on the liability side.”

Essentially, the Fed is proposing creating a hybrid digital legal tender unlike reserves which are stuck within the financial system, and which it can deposit directly into US consumer accounts. In short, as we summarized “The Fed Is Planning To Send Money Directly To Americans In The Next Crisis“, something we reminded readers of on Monday:

There still appears to be some confusion about the endgame. The Fed itself spelled it out.

The Fed Is Planning To Send Money Directly To Americans In The Next Crisis: “by getting money to consumers you can limit the depth and duration of a recession”https://t.co/bG03TxiviT

So this morning, as if to confirm our speculation of what comes next, Cleveland Fed president Loretta Mester delivered a speech to the Chicago Payment Symposium titled “Payments and the Pandemic“, in which after going through the big picture boilerplate, Mester goes straight to the matter at hand.

In the section titled “Central Bank Digital Currencies”, the Cleveland Fed president writes that “the experience with pandemic emergency payments has brought forward an idea that was already gaining increased attention at central banks around the world, that is, central bank digital currency (CBDC).”

And in the shocking punchline, then goes on to reveal that “legislation has proposed that each American have an account at the Fed in which digital dollars could be deposited, as liabilities of the Federal Reserve Banks, which could be used for emergency payments.“

But wait it gets better, because in launching digital cash, the Fed would then be able to scrap “anonymous” physical currency entirely, and track every single banknote from its “creation” all though the various transactions that take place during its lifetime. And, eventually, the Fed could remotely “destroy” said digital currency when it so decides. Oh, and in the process the Fed would effectively disintermediate commercial banks, as it would both provide loans to US consumers and directly deposit funds into their accounts, effectively making the entire traditional banking system obsolete. Here are the details:

Other proposals would create a new payments instrument, digital cash, which would be just like the physical currency issued by central banks today, but in a digital form and, potentially, without the anonymity of physical currency. Depending on how these currencies are designed, central banks could support them without the need for commercial bank involvement via direct issuance into the end-users’ digital wallets combined with central-bank-facilitated transfer and redemption services. The demand for and use of such instruments need further consideration in order to evaluate whether such a central bank digital currency would allow for quicker and more ubiquitous payments in times of emergency and more generally. In addition, a range of potential risks and policy issues surrounding central bank digital currency need to be better understood, and the costs and benefits evaluated.

The Federal Reserve has been researching issues raised by central bank digital currency for some time. The Board of Governors has a technology lab that has been building and testing a range of distributed ledger platforms to understand their potential benefits and tradeoffs. Staff members from several Reserve Banks, including Cleveland Fed software developers, are contributing to this effort. The Federal Reserve Bank of Boston is also engaged in a multiyear effort, working with the Massachusetts Institute of Technology, to experiment with technologies that could be used for a central bank digital currency. The Federal Reserve Bank of New York has established an innovation center, in partnership with the Bank for International Settlements, to identify and develop in-depth insights into critical trends and financial technology of relevance to central banks. Experimentation like this is an important ingredient in assessing the benefits and costs of a central bank digital currency, but does not signal any decision by the Federal Reserve to adopt such a currency. Issues raised by central bank digital currency related to financial stability, market structure, security, privacy, and monetary policy all need to be better understood.

To summarize, the wheels are already turning on a plan that sees the Fed depositing “digital dollars” to “each American”, a stunning development that essentially sees the Fed bypass Congress, endowing the Central Bank with targeted “fiscal stimulus” capabilities, and which could lead to a dramatic reflationary spike as it is the lower income quartile segments of US society that are the marginal price setters for economic goods and services. And having already implemented Average Inflation Targeting, the resulting burst of inflation would be viewed by the Fed as insufficient on its own (as it would have to persist for a long time over the “average” period whatever it may end up being), to tighten monetary policy. In fact, even as inflation rages – which some alternative inflationary measures to CPI suggest it already is – the Fed will have a semantic loophole in explaining just why it needs to keep inflation scorching hot even as the standard of living in America collapses to the benefit of a handful of asset holders.

Absent a massive burst of inflation in the coming years which inflates away the hundreds of trillions in federal debt, the unprecedented debt tsunami that is coming would mean the end to the American way of life as we know it. And to do that, the Fed is now finalizing the last steps of a process that revolutionizes the entire fiat monetary system, launching digital dollars which effectively remove commercial banks as financial intermediaries, as they will allow the Fed itself to make direct deposits into Americans’ “digital wallets”, in the process also making Congress and the entire Legislative branch redundant, as a handful of technocrats quietly take over the United States.

via ZeroHedge News https://ift.tt/2ZX8H43 Tyler Durden

A reader recently wrote me a long letter on how he feels about all this ‘Plandemic’ stuff. I thought it would be good to share it as there is so much in it which rings bells of truth for me…

[emphasis ours]

I’ve just woken up after reading ZeroHedge late into the night. I awoke with the conviction that Covid is being used to roll out a police state:

They know it’s not deadly, it’s no longer spreading and Lockdown is killing off the few small businesses which remain viable. Yet Boris now insists upon banning the assembly of more than 6 people. He has recalled some petty bureaucrats to act as street enforcers and requested people become snitches who report on their neighbours for any breaches of these guidelines. This automatically means we must now all fear our neighbours, or strangers who take our car number. How better to destroy the mutual trust upon which society is built?

Just think if one were to refuse to bend the knee. In Australia and Spain the police have been caught using excessive force against those not wearing masks. Intimidating isn’t it? I’m thinking I may have to start using one. Yet the science is clear – masks offer no protection.

So we know these new restrictions are not being driven by the authority’s concern for our health. And what is the difference between where we are now and making it normal for the police to come to your door and arrest you for a breach of their protocols? What is the difference between where we are now and an oppressive police state?

There is only one difference between now and full-on state oppression: A change in the Zeitgeist.

They need an event that will change the mood of the people – an event or a series of events that make us afraid of ‘them’. A psychological shock that will give the police the conviction that things are so bad ‘a little force is necessary’ to ensure things don’t get out of control. And then, magically, the current ‘temporary restrictions’ become state oppression. What could that game changer be?

Imagine this November: The US has 100 cities descending into what looks like the start of civil war as patriots turn out to stop Antifa burning down Middle America. Kamala Harris is calling for the army to ‘evict’ Trump because he refuses to leave the White House on the grounds that he won the popular vote while the mail-in ballots were fraudulent.

For the Brits, Brexit has caused problems at the ports – among other things some foodstuffs are not getting through. Germany’s economy has cratered after the EU stopped them exporting cars to the UK (Trumps already tariffed them), and the EU’s bank has insisted Germany let the 500 non-viable, medium sized biz (currently kept alive with emergency funding) go bankrupt.

Deutsche Bank collapses and this initiates a global banking crisis. Europe has no way of saving its banks as all the European economies are so damaged and 20% of workers have already been laid off. It’s a Greek style banking crisis on steroids. People are pulling out cash in the expectation of daily cash limits. Physical gold will have already disappeared from the market place. So any biz with money in the bank is frantically buying bitcoin in an attempt to avoid their working capital being ‘bailed in’.

The banks will have already pulled the plug on their most vulnerable customers – the airlines – so virtually no planes are flying. Dover is jammed up with lorries lining the approach roads. So no one can leave Blighty. And if you did, the emergency measures intended to pre-empt Covid’s Second Wave require you to be kept in quarantine at your destination. Locked down in a hotel, under military guard (as in NZ), for 4 weeks at your own expense and with frequent testing to ensure you are not a carrier. With full bio-metric data being collected and filed on an EU wide register. In practice this means that travel becomes so fraught that escape from your homeland is just about impossible.

You get the gist? November could be the end of world as we know it’ (TEOTWAWKI). But my point is this: Why are we looking at such a catastrophe if their goal is not a police state? No one destroys the globe’s economy and creates the conditions for a 10 year Greater Depression by accident. This has to be a planned, intentional destruction of much of global civilization.

The evidence is overwhelming. This civilization has been purposefully destroyed. Right now we’re in an unreal time (like the beautiful summer just before WW1’s carnage). It’s like Wiley E Coyote who has gone over the cliff, is still running but not yet started to fall. But when we fall, how will people react as they realize that they will never work again, never pay off the mortgage, never collect their pensions? If we have state oppression and economic chaos by Christmas then what will be the next stage of their takeover?

The world’s economy is already doomed. The already broken supply chains ensure it can only get worse. Once the derivative market goes, and banks can no longer fund the credit lines crucial for importers and exporters, then trade will collapse and thus food supplies cease.

It would seem to be inevitable that America is going to see more conflict as the Dems & Soros show no signs of wishing to abort their colour revolution. Maybe in 2021, maybe a year or two later, but there will come a time when a credit shortage leads to deflation. So the banks will print more and then rain down helicopter money which will lead to inflation. And then the currencies will start collapsing. Many people understand that this is inevitable. But what happens when people come to accept that money isn’t go to be worth the paper it’s printed on? And thus keeping a job may not be worth the danger of leaving your house or of leaving safety.

I summarise one of last night’s articles:

“the beasts of burden don’t rebel, they just no longer show up. Not showing up can take a number of forms: early retirement, sick leave, a demand to work halftime, a workers’ compensation stress leave, and of course, resignation and quitting as in: “take this job and shove it”. They slip noiselessly into the cracks and crevasses and once they’re gone, there’s nobody left to replace them.”

“As the Vital Few 4% realize the system no longer works for them and opt out, this will have an out-sized effect on the 64%, most likely urban dwellers, highly dependent on increasingly brittle, fragile services that depend on the Vital Few for their functionality. Think of London’s tube train drivers phoning in sick – ideology won’t matter.

Those dropping out may be Conservative or Progressive or they may have lost interest entirely in politics and all the other circuses that serve to distract the populace from the crises dissolving the glue that held the system together. “So I won’t get rich, that dream died a long time ago.” What I’m interested in now is getting my life back and getting the heck out of Dodge as things fall apart.”

The rich will escape to their holiday cottages. The poor will riot – but what then? As the social facade cracks, and the economic system breaks, there is neither a society nor an economy to fall back on. By Christmas it will be obvious that normality has gone for ever.

So what will ‘they’ do with millions of unemployed, frightened people? If ‘they’ leave the internet on then the people will start to organize – first politically – but when that doesn’t work, riots and then finally revolution. Turn it off and they will riot without being organized. Turn off phones and all hell will break out. Don’t turn them off and the kids will organize against the state – trash cars or burn down the local police station. Have you noticed how some police stations look like forts?

My point is that it’s very hard not to see ‘events’ hitting the fan this November. And once they do it’s very hard to see life ever going back to stability, let alone ‘normality’. Rather, there will be an overwhelming need to control {oppress} the population before they take over the state. But what do you do with millions of unemployed in a failed economy who are doomed to losing their currency, long term poverty and probably food shortages. There is only one thing ‘they’ can do. Kill them.

Ideally, for the elite, Covid’s Second Wave will have a higher morbidity rate. Enough to steadily reduce the population but not so fast they can’t be buried in plague pits. It would have to be bad enough to justify a harsh Lockdown but it’s difficult to see that being feasible without giving the people electricity, internet & food and the money to pay for it. And even then it’s only a temporary fix as Lockdown can’t last for ever. Permanent Lockdown would soon destroy the currency which will mean no electricity or food.

Maybe Covid-19 v1.0 was supposed to kill off more people but it failed. Or maybe it worked as intended – they didn’t want to risk killing off too many in case the Lockdown failed and we revolted. But I don’t see they have much choice now. ‘The Fourth Turning’ will be turbulent until 2025 and things won’t really be resolved until 2030. How are they going to manage us for another 10 years? How will they control us? Feed us?

They can start a war but no one is going to turn up. Fight a war for the elite? Use a gun to kill people you don’t know? That’s not going to happen. And they need to preserve the professional soldiers to ‘maintain the peace’ in the cities. So what options do they have but to release a more potent bio-weapon – nuclear war perhaps?

One of the scary things about working through ‘their’ options is that they don’t have many. Things have gone too far – they’ve destroyed the world’s economy. The system is stuffed. What are ‘they’ going to do with 2bn unemployed people. Even if there is enough food but the US has a developing dust bowl, Africa’s suffered huge locust devastation, and China’s preparing for food shortages. How do unemployed people pay for it? Who can give them money without destroying the currency or if the currency is already destroyed?

A simple thing like the current fall in the number of sunspots is indicating an immediate future of colder weather and lower crop yields. Add into that, fuel shortages for agricultural machinery, lack of fertilizer – Nitrogen is made by burning lots of oil, lack of supply lines, and loss of credit lines. With people in Lockdown ‘they’ would be relying on a planned economy (not a free market) which is going to be inefficient. A planned economy is completely incapable of ensuring a stable food supply when there are shortages and the world is chaotic.

It’s not even feeding our cities that will be prime problem. It will be feeding the cities in Mexico and North Africa. They can’t cope with food price inflation. But they won’t starve – they’ll flood into the USA or cross the Mediterranean – lucky us! And what will Erdogan in Turkey do to feed his people – nothing good! If there are real food shortages then note that there are huge Muslim populations in France & Sweden, Turks and refugees in Germany, Pakistani ghettos in UK and plenty more where they all came from.

I’m feeling concerned. The problem is I can’t see Brexit solving our problems. Sure, it may not exacerbate them as much as I fear. November’s events may not trigger us into a state of oppression. But do you see my point? Things have got so bad, they can only get worse. November is bound to see some changes and they may well trigger a change in the Zeitgeist, though how significant depends on ‘events, dear boy, events’.

But whatever happens I think it’s virtually guaranteed that both the economy and society will keep on deteriorating.

Do you think I’m right?

Will November be the tipping point?

Is there any way back?

Will there be anything to go ‘back’ to?

Or else, is it a case of: “we’re doomed, I tell ya, doomed”. And what happens when more people work out that the elites have created a situation where their only option is to rapidly reduce the population! Famine will lead to uncontrollable social conflict, perhaps with Muslims massacring whites in general or the local Jewish populations in particular. I think that much conflict could see ‘them‘ lose control.

Thus it’s hard to see any other viable method than a bio-weapon. Agenda 21 could be implemented on schedule. And if not, the solution will need to be applied within a few years, certainly before 2025. Timing may depend on vaccine production as there will have to be at least enough vaccine for essential workers, the police, the military and the management class if the elite are to retain control.

via ZeroHedge News https://ift.tt/303rGdc Tyler Durden

UK Grocers Stave Off Panic Buying Amid 2nd Lockdown Fears; Daily COVID Case Record Smashed Tyler Durden

Thu, 09/24/2020 – 04:15

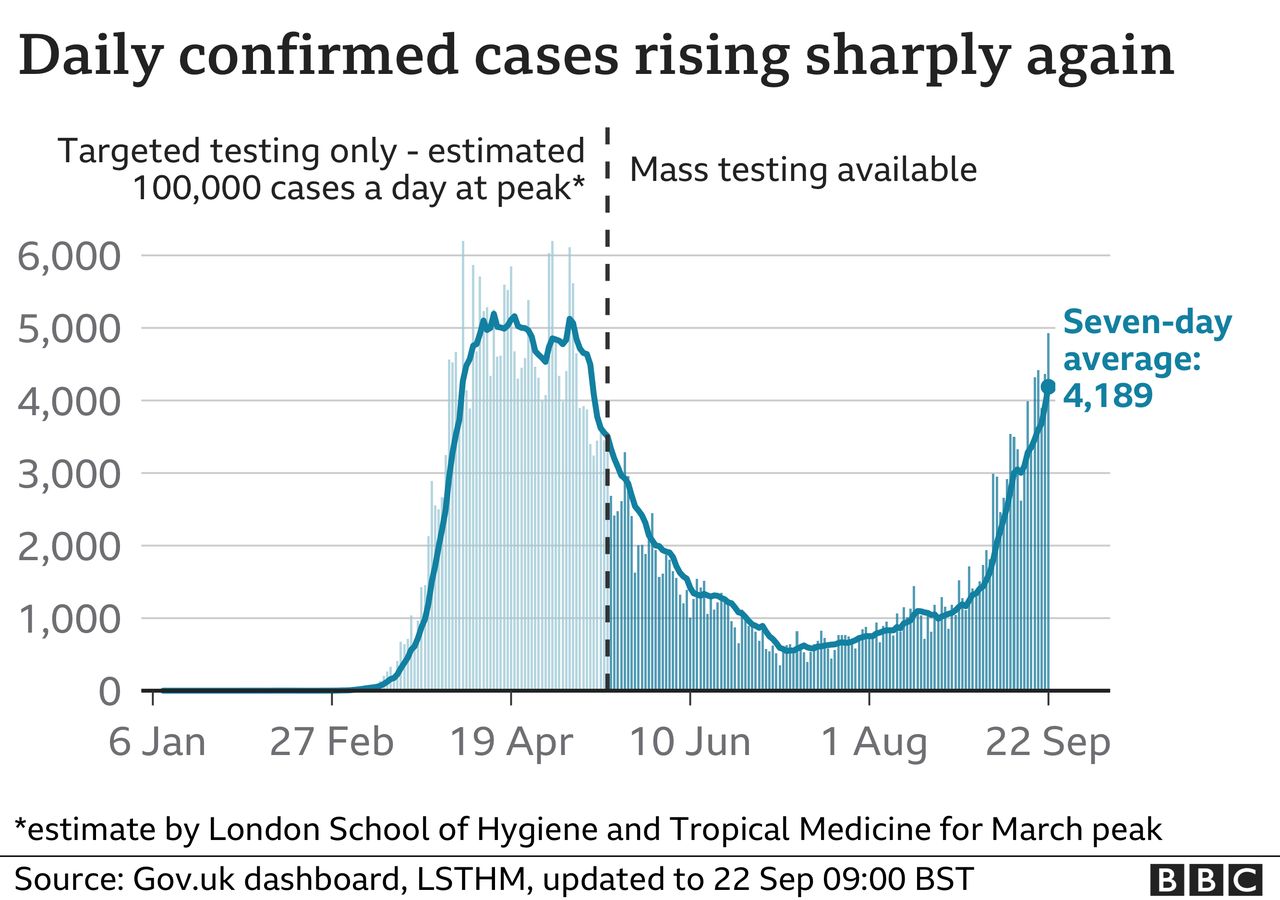

Britain is scrambling to avoid a second lockdown after its first one six months ago, with PM Boris Johnson just introducing expanded new social distancing rules across the UK, as the government’s top adviser Sir Patrick Vallance warns “the epidemic is doubling roughly every seven days.”

Specifically the latest surge in COVID-19 cases at current rates could mean 50,000 cases a day by mid-October, Vallance warned at the start of the week. In introducing new measures to fight the spread Tuesday night, Johnson urged citizens to “summon discipline, resolve and a spirit of togetherness.” The new measures will last a whopping six months with warnings of “a difficult winter”— also at a moment total infection numbers approach the half-million mark (as of Wednesday: 409,729 people tested positive since the start, including 41,862 deaths).

However all the dire pandemic predictions have naturally resulted in a surge of panic buying, similar to what happened across the West and in the United States as lockdowns hit last Spring.

AFP via Getty Images

“Supermarket bosses have urged shoppers not to start panic buying, while Asda is bringing in 1,000 safety marshals, as the industry braces for a potential change in shopping habits ahead of new lockdown restrictions,” The Guardian reports late Wednesday.

Discount supermarket chains Tesco and Aldi urged customers this week not to start stockpiling goods, saying was “unnecessary” and seeking to calm fears of disruption in supply chains.

“There is no need to buy more than you usually would. I would like to reassure you that our stores remain fully stocked and ask that you continue to shop considerately.”

“We have remained open for our customers throughout the pandemic and will continue to have daily deliveries, often multiple times a day, across all of our products.”

And CEO Dave Lewis of the popular store Tesco said in a televised interview that Britons should not panic: “The message would be one of reassurance. I think the UK saw how well the food industry managed last time, so there’s very good supplies of food,” he said, describing an improved plan for rapid restocking.

“We just don’t want to see a return to unnecessary panic buying because that creates a tension in the supply chain that’s not necessary,” he added.

Via NPR: If the U.K.’s rate of new coronavirus cases doubles four more times, Chief Scientific Advisor Sir Patrick Vallance said, “you would end up with something like 50,000 cases in the middle of October per day.”

Given the record number of new cases, the sense of fear and panic is not likely to abate in the short term:

New UK coronavirus cases hit 6,178 on Wednesday, according to the latest government data. The number is the highest daily level since 1 May, when the UK was in full lockdown.

Here were the numbers as of the prime minister’s Tuesday night address:

Local UK grocery stores have reported they’ve started hiring and stationing extra security personnel in preparation to monitor both numbers of shoppers at once, and mask and other guidelines.

via ZeroHedge News https://ift.tt/32VJEQA Tyler Durden

Three power plants in Iran will soon offer their electricity outputs to interested Bitcoin miners.

The move comes after a July ruling enabled power plants to legally mine Bitcoin.

Iran has turned to Bitcoin mining as a potential source of income amidst broader economic worries.

Three major power plants in Iran will soon offer their energy outputs exclusively for Bitcoin mining, the country’s Thermal Power Plant Holding Company (TPPH) announced on Monday, as per a report on local news outlet Tehran Times.

Irani power plants receive benefits and subsidies from the government on their fuel supplies, which are in turn used to produce power. And while they were earlier barred from mining cryptocurrencies, a new ruling in July allowed power plants to engage in the business—albeit after gaining necessary government approval, licenses, and complying with the tariffs set for crypto mining.

The TPPH now wants a slice of that pie. It said it will soon offer a tender for the electricity output of three power plants for the purpose of Bitcoin mining.

“The necessary equipment has been installed in three power plants of Ramin, Neka, and Shahid Montazeri, and the auction documents will be uploaded on the SetadIran.ir website in the near future,” said TPPH head Mohsen Tarztalab.

Tarztalab said that the sale of electricity to Bitcoin miners presented a new, stable way of generating profits in the electricity sector.

He added the three power plants will only use their expansion turbines for the purpose of Bitcoin mining, which uses natural gas to produce power and is a cheaper alternative to liquid fuels like gas oil.

Such turbines are not connected to the national grid—which distributes power across the country for commercial purposes—and will be wholly used by the power plans to mine Bitcoin instead, explained Tarztalab.

Bitcoin adoption for a reason

The July ruling is said to be a savior for the country’s electricity industry. Repeated price hikes and the obligation to supply electricity at stable prices to subscribers has created falling profits for Iranian power producers in the past, the report noted.

Iran’s adoption of Bitcoin comes at a time when the country grapples with a bleak economic outlook and international trade sanctions imposed by influential governments, such as the US, over its controversial nuclear power program.

However, Bitcoin mining is providing them a new way for them to generate income, it added. And mining is a big opportunity.

Iranian ministers said in 2019 that regulated, industrial-scale Bitcoin mining can pull in, annually, an estimated $8.5 billion.

via ZeroHedge News https://ift.tt/2FMG4Qk Tyler Durden

Sweden Dominates Drug-Deaths In Europe Tyler Durden

Thu, 09/24/2020 – 02:45

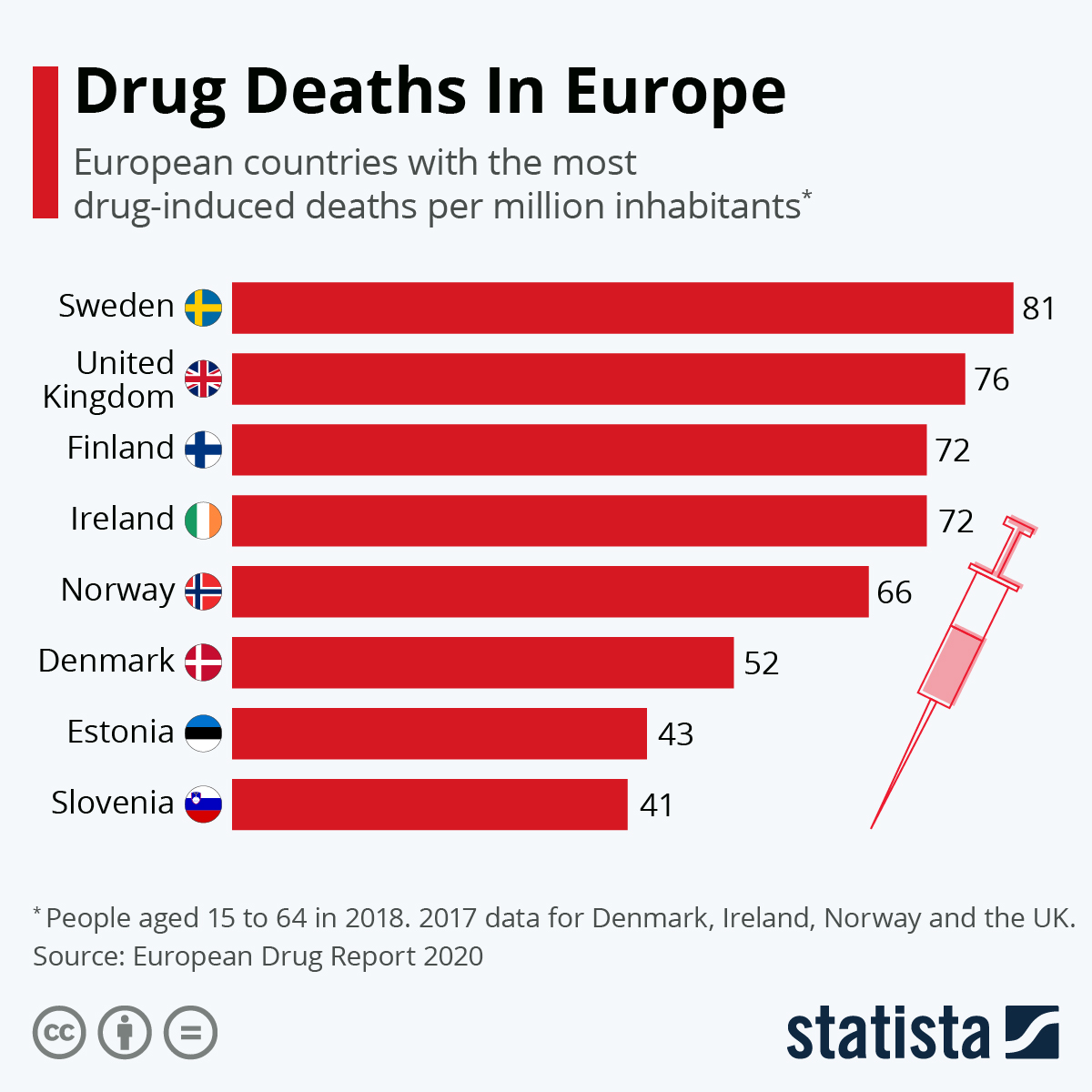

As highlighted by the latest edition of the European Drug Report, Sweden is the country with the most drug-induced deaths per million of the population in Europe.

In 2018, 81 people died per million inhabitants, ahead of the United Kingdom’s 76 drug-induced deaths per million. Finland and Ireland jointly had the third-highest death rate with 72 deaths per million.

In 2018, the U.S. experienced 314.5 drug-related deaths per million of its population and it lost more inhabitants to drugs than the next 20 countries combined.

via ZeroHedge News https://ift.tt/3kGZswK Tyler Durden

A disturbing testimony from a psychiatrist outlines that Wikileaks founder Julian Assange is in such a bad state in prison that he should be considered at ‘high risk’ of suicide.

The Daily Mail reports that Professor Michael Kopelman testified during an extradition hearing in London that Assange has “begun making preparations to end his own life including confessing to a Catholic priest, drafting farewell letters to his family and drafting a will.”

Kopelman, emeritus professor of neuropsychiatry at King’s College London, also said that Assange told him he experienced hearing voices in his head saying “we’re coming to get you.”

“He reported auditory hallucinations, which were voices either inside or outside his head, somatic hallucinations, funny bodily experiences, these have now disappeared,” Kopelman said.

“He also has a long history of musical hallucinations, which is maybe a separate phenomenon, that got worse when he was in prison,” the psychiatrist added.

“The voices are things like, “you are dust, you are dead, we are coming to get you”. They are derogatory and persecutory,” he continued, adding “They seem to have diminished. Subsequently the musical hallucinations have also reduced, and the somatic hallucinations have disappeared.”

Kopelman even noted that Assange “reported a near-death experience and wondered if the CIA would find a way to get him or mess with his head” noting that this “may or may not” be paranoia.

Kopelman warned that “The risk of suicide arises out of clinical factors…but it is the imminence of extradition and or an actual extradition that would trigger the attempt, in my opinion.”

Assange is languishing in Belmarsh, a notoriously horrid maximum security prison housing murderers and terrorists. For much of the time since being arrested on leaving the Ecuadorian embassy, Assange has been kept in solitary confinement. He is also heavily medicated.

The wikileaks founder faces extradition to the US, where he would be charged with an 18-count indictment related to hacking computers and conspiracy to obtain and disclose national defence information.

Professor Kopelman also noted during the hearing that Assange has been depressed “certainly throughout the time I’ve been seeing him.”

“It’s fluctuated a bit, his appetite has fluctuated, he’s had persistent problems with sleep and his mood state is worst in the early hours of the morning and that’s stayed consistent,” Kopelman added.

“Mr Assange was very reluctant to talk about his suicidal ideas and plans because he feared he would be put on constant watch or isolation,” the psychiatrist further explained.

The report notes that the QC for the US government argued that Assange is ‘exaggerating’ his psychiatric symptoms and ‘self reporting’ suicidal ideas, and that Kopelman is an ‘advocate’.

“I’m a psychiatrist, you’re a lawyer. I make my diagnoses on my criteria,” the professor is said to have replied.

Assange’s QC reportedly read out a list of multiple times, at least ten, that Assange had requested the Samaritans suicide prevention helpline number between August and November 2019.

Assange has been in the prison since April of last year:

Since much of the media is now centred around generating outrage and deplatforming dissent, “journalists” don’t have to worry about being targeted by the establishment because they no longer do actual journalism.

That’s why they’re all cheering Assange’s arrest today.

Julian Assange is literally dying in solitary confinement and no one really cares. Everyone who helped Trump get elected was targeted and virtually destroyed, and has there been an adequate response?

{kind=link}