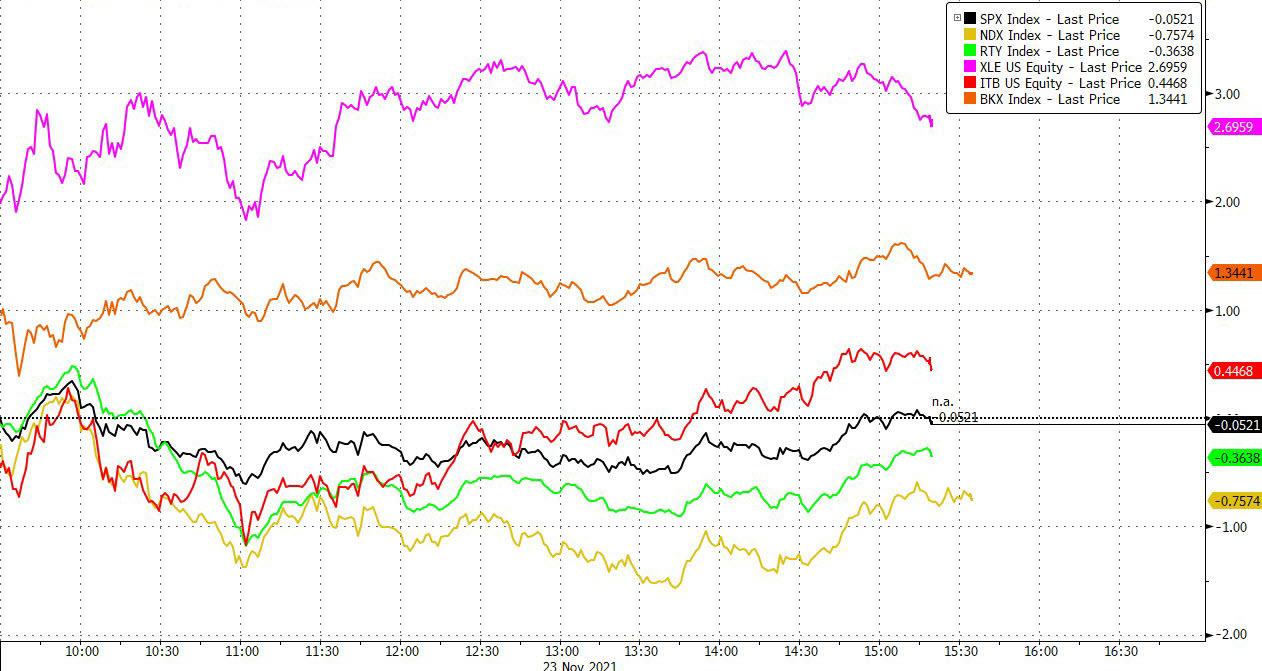

Biden Drops Details On SPR Release, Then Flees From Media Questions

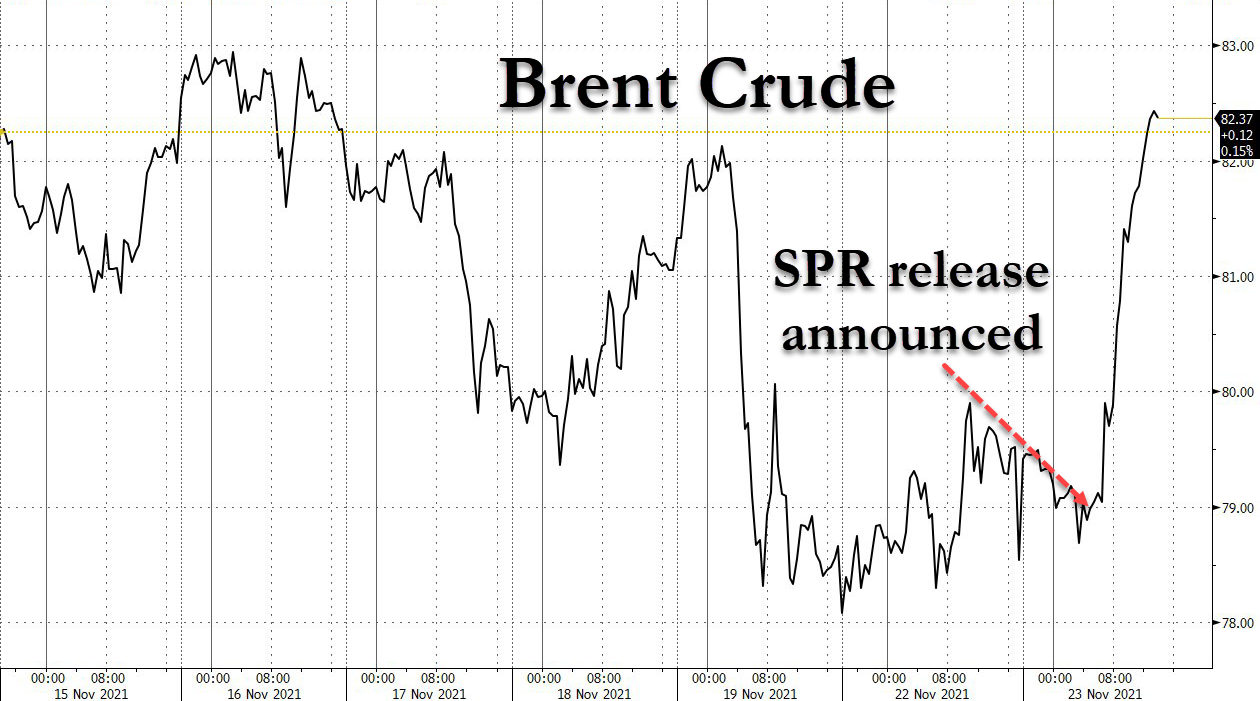

As we noted earlier, Biden’s “exchange-based” release from the global SPR has been a dud, as oil prices surged on Tuesday after the administration confirmed plans for a record-setting 50M barrel release which is contingent on America’s ability to convince Japan, the UK and several other allies to engage in “global” swaps from the strategic reserves.

The decision was aimed at helping alleviate some of the pain Americans have been feeling at the pump this fall.

Of course, we don’t have to explain why Biden shouldn’t bother with that SPR release: his administration did that himself last month – insisting that a jolt from the SPR wouldn’t make a difference in long-term crude prices.

A closer look at the decision might explain the timing; Biden’s SPR announcement comes amid a long-delayed Wednesday sale of oil-exploration leases in the Gulf of Mexico, a decision which has enraged environmentalists, and is ‘unlikely to help tame rising oil and gasoline prices’, according to Bloomberg.

1. Draining ‘strategic’ global #oil reserves when oil is sub-$80

2. Raising cost of capital for O&G until capex is starved

3. Doing *nothing* to alter fossil fuel Demand

Tomorrow begins a new era: $200+ Brent in ~two years is not a tail risk, but a likely outcome #OOTT #OPEC

— Peter Sutherland (@econ_713) November 23, 2021

During his Tuesday speech, Biden promised Americans that the drawdown from the reserves would be global in scope, claiming that he had spoken with China about joining it in releasing more from the reserves, while his press secretary importantly said the White House wouldn’t rule out even more cuts.

Biden reassured Americans that they could “rest easy” knowing that stores would be well-stocked this season, something that they probably appreciated after months of near record-setting inflation (and certainly the highest in 30 years) not just in the US, but across the world.

Bloomberg reports that with Biden’s latest economic speech comes amid “policy whiplash” revealing the tension between Biden’s long-term climate goals and short-term political realities. Some promoters of green energy even insisted that Biden can’t really afford higher energy prices rise so high that voters turn against him.

Former Treasury Secretary Larry Summers made the threat to the economy even more explicit last week when he said inflation threatened to usher in a return to power for former President Donald Trump, who called global warming a hoax. Others acknowledged that Biden was already struggling with the decision.

“That’s a challenging tightrope to walk,” said Dan Pickering, founder and chief investment officer at Houston-based Pickering Energy Partners. With no major breakthrough at the United Nations climate conference in Glasgow, and no cohesive strategy for lowering gasoline prices, Pickering added, “you look not great at either, which seems like the worst place in the world for a politician to be.”

The news comes after President Biden made his speech, which he made earlier Tuesday:

But in one of the most memorable moments from Biden’s administration, the president seemed to almost run away from the press and flee as reporters asked whether the president take questions from reporters.

REPORTER: “When will you answer our questions, Sir?”

BIDEN: *turns around and runs away* pic.twitter.com/i1JhkyU7ny

— Danny De Urbina (@dannydeurbina) November 23, 2021

Tyler Durden

Tue, 11/23/2021 – 16:25

via ZeroHedge News https://ift.tt/3CMXhAz Tyler Durden