Twitter Restricts Account Of Flynn Attorney Sidney Powell Tyler Durden

Mon, 06/29/2020 – 09:54

Twitter has restricted the account of Michael Flynn’s lawyer, Sidney Powell.

Trying to access Powell’s account (@SidneyPowell1) results in a warning which reads “Caution: This account is temporarily restricted” due to “unusual activity.” Users can then bypass the message and access Powell’s account.

It is unclear if this restriction began before or after she retweeted an article from The Federalist calling for conservatives to fight back against Black Lives Matter and its “radical agenda” which have resulted in “angry mobs pulling down statues, taunting police, attacking passersby, and taking over entire city blocks.”

Powell’s involvement Flynn’s case changed the fate of the retired general, who – under advisement from his prior legal counsel from Eric Holder’s law firm – pleaded guilty to lying to the FBI about his interactions with the Russian ambassador during the presidential transition.

Powell fought to force the government to release exculpatory evidence which revealed that rogue agent Peter Strzok overrode the agency’s recommendation to close the Flynn case – instead launching a ‘perjury trap’ against the former Trump adviser.

As a result, the Justice Department dropped its case against Flynn. The judge in the case, Emmet Sullivan, would not accept the DOJ’s request and instead called on a 3rd party judge to outline why Flynn should still be prosecuted. Last week, the Second Court of Appeals for DC ordered Sullivan to drop the matter.

All thanks to Sidney Powell.

via ZeroHedge News https://ift.tt/2ZjPKHt Tyler Durden

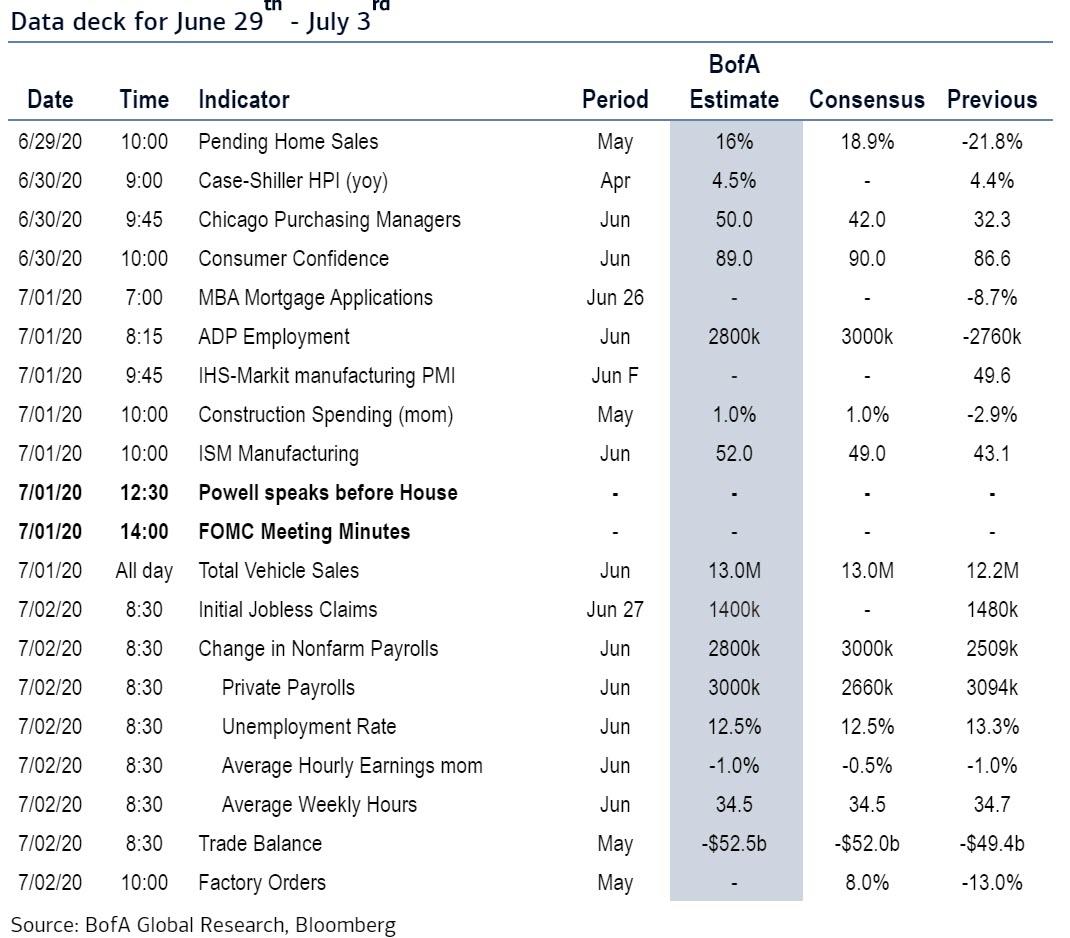

Key Events In THe Coming Holiday-Shortened Week Tyler Durden

Mon, 06/29/2020 – 09:40

As the mid-summer sun rises, we see a shortened trading week with Friday a US holiday in lieu of Independence Day on Saturday, and as DB’s Jim Reid predicts, Thursday will likely see activity wind down early and rapidly ahead of the weekend.

That said, the last major act of the week will be the all-important payrolls report brought forward to Thursday, where DB’s economists are looking for a further +2m gain in non-farm payrolls, following last month’s unexpected +2.509m increase, along with a further reduction in the unemployment rate to 12.6% (unclear if this assume the BLS will continue making the same admitted mistake it has been doing for the past two months). This improved labor market performance chimes with what we’ve seen in other indicators, such as the weekly initial jobless claims that have fallen for 12 consecutive weeks now. That said, it’s worth remembering that given the US shed over 22m jobs in March and April, even another +2m reading would still mean that payrolls have recovered less than a quarter of their total losses, suggesting there’s still a long way to go before the labor market returns to normality again.

The other main data highlight will be the final June PMI releases from around the world. The manufacturing numbers are out on Wednesday before the services and composite PMIs come out on Friday for the most part (ex US), while there’ll also be the ISM manufacturing index too from the US (on Wednesday). For the countries where we already have a flash PMI reading, they generally surprised to the upside, even as many remained below the 50-mark. It’ll also be worth keeping an eye on the numbers for China, given they’re some way ahead in the reopening process relative to the US and Europe.

In politics, a key highlight this week will be a meeting between Chancellor Merkel and President Macron taking place today, where both the EU budget and the recovery fund will be on the agenda. That comes ahead of another summit of EU leaders scheduled for the 17-18th July, where the 27 leaders will meet in person in Brussels for further discussions on the recovery fund. Meanwhile, the start of July on Wednesday formally sees Germany take over the rotating EU presidency, which they’ll hold for the next six months.

Staying with politics, Reid points out that Brexit negotiations between the UK and the EU on their future relationship will return once again. This will be the first set of intensified talks that are taking place every week over the next five weeks, as the two sides look to come to an agreement following fairly slow progress in the talks thus far. Since the last round of negotiations, a high-level meeting took place between Prime Minister Johnson and the Presidents of the European Commission, Council and Parliament, where the two sides agreed in their statement that “new momentum was required” in the discussions. There does seem a bit more positivity now than there was a month ago but much work still needs to be done.

Elsewhere we have the release of the FOMC minutes for the June meeting on Wednesday, along with an appearance by Fed Chair Powell and Treasury Secretary Mnuchin tomorrow before the House Financial Services Committee. Otherwise, speakers next week include the BoE’s Governor Bailey and Deputy Governor Cunliffe, along with the ECB’s Schnabel and New York Fed President Williams.

Courtesy of Deutsche Bank, here is a day-by-day calendar of events:

Monday

Data: Japan May retail sales; Spain preliminary June CPI; UK May consumer credit, mortgage approvals, M4 money supply; Euro area June economic, industrial, services and consumer confidence; Germany preliminary June CPI; US May pending home sales and June Dallas Fed manufacturing activity index.

Central Banks: BoE’s Bailey, Breeden and Vlieghe speeches; Fed’s Daly and Williams speeches; IMF’s Georgieva speech.

Politics: German and French leaders meet to discuss clinching a deal on the EU recovery fund.

Others: EU Brexit chief negotiator Michel Barnier meets UK counterpart David Frost for further talks on a trade deal.

Tuesday

Data: Japan preliminary May industrial production; China June official PMIs; UK final June GfK consumer confidence, June Lloyds business barometer, final 1Q GDP, private consumption, government spending, gross fixed capital formation, exports, business investments, current account balance, imports; France preliminary June CPI, May PPI and consumer spending; Spain final 1Q GDP; Italy preliminary June CPI and May PPI; Euro area preliminary June CPI and Core CPI; US April S&P CoreLogic house price index, June Chicago Fed PMI, Conference board consumer confidence, expectations and present situation index.

Central Banks: ECB Schnabel speech; BoE Cunliffe and Haldane speeches; Fed Williams speech; Colombia rate decision.

Others: Fed’s Powell and US Treasury Secretary Mnuchin testify before the House Finance Panel.

Politics: European Council President Charles Michel and European Commission President Ursula von der Leyen meet with South Korean President Moon Jae-in in a virtual summit, NATO Secretary General Jens Stoltenberg speaks on the geopolitical implications of Covid-19.

Wednesday

Data: Japan 2Q Tankan survey results, June consumer confidence and final June manufacturing PMI; China June Caixin manufacturing PMI; Spain June manufacturing PMI; Italy June manufacturing PMI; France final June manufacturing PMI; Germany final June manufacturing PMI, June unemployment claims rate and unemployment change; Euro area final June manufacturing PMI; UK final June manufacturing PMI; US latest weekly MBA mortgage applications, June Challenger job cuts and ADP employment change, final June manufacturing PMI, May construction spending, June ISM manufacturing, new orders, prices paid and employment, June FOMC meeting minutes, June Wards total vehicles sales.

Central Banks: Sweden rate decision, BoE Haskel speech; Fed Evans speech.

Politics: Russia holds the final day of voting on changes to the nation’s constitution.

Others: The head of Germany’s BaFin financial regulator testifies before the German parliament on the accounting scandal at payment-processing firm Wirecard AG; the U.S.-Mexico-Canada Agreement is due to take effect.

Thursday

Data: Euro area May PPI and unemployment rate; US May trade balance, June nonfarm payrolls, unemployment rate and average hourly earnings, latest weekly initial and continuing claims, May factory orders, final May durable goods and capital goods orders.

Others: SIFMA has recommended an early close (14:00 EDT) for the fixed-income market before the U.S. Independence Day holiday

Friday

Data: Final June services and composite PMIs for Japan, China (Caixin), Spain, Italy, France, Germany, Euro area and UK; France May YtD budget balance; UK June official reserve changes.

Central Banks: ECB Knot speech.

Others: US Independence Day holiday

* * *

Finally, courtesy of Goldman, here is a preview of events in the US, where as Jan Hatzius notes, key events this week are the ISM manufacturing index on Wednesday and the employment report on Thursday. The minutes of the June FOMC meeting will be released on Wednesday.

Monday, June 29

10:00 AM Pending home sales, May (GS +33.0%, consensus +18.0%, last -21.8%): We estimate that pending home sales rebounded by 33.0% in May based on regional home sales data, following a 21.8% drop in April. We have found pending home sales to be a useful leading indicator of existing home sales with a one-to-two-month lag.

10:30 AM Dallas Fed manufacturing index, June (consensus -22.0, last -49.2)

11:00 AM San Francisco Fed President Daly (FOMC non-voter) speaks: San Francisco Fed President Mary Daly will speak on a panel discussion on higher education. Prepared text is not expected. Audience and media Q&A are expected.

3:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will moderate a discussion with IMF Managing Director Georgieva.

Tuesday, June 30

09:00 AM S&P/Case-Shiller 20-city home price index, April (GS +0.7%, consensus +0.5%, last +0.47%); We estimate the S&P/Case-Shiller 20-city home price index increased by 0.7% in April, following a 0.47% increase in March.

09:45 AM Chicago PMI, June (GS 46.0, consensus 44.0, last 32.3); We estimate that the Chicago PMI rebounded by 13.7pt to 46.0 in June—following a 3.1pt decline in May—reflecting improved June readings for other manufacturing surveys.

10:00 AM Conference Board consumer confidence, June (GS 94.0, consensus 90.5, last 86.6): We estimate that the Conference Board consumer confidence index increased to 94.0 in June from 86.6 in May.

11:00 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will give a speech via webinar on central banking during the pandemic. Prepared text and moderator Q&A are expected.

12:30 PM Fed Chair Powell (FOMC voter) speaks: Federal Reserve Chairman Jerome Powell and Treasury Secretary Steven Mnuchin will testify before the House Financial Services Committee. Prepared text is TBD and questions from Members are expected.

02:00 PM: Minneapolis Fed President Kashkari (FOMC voter) speaks: Minneapolis Fed President Neel Kashkari will participate in a virtual panel discussion on race and social justice in economics. Prepared text is not expected. Audience Q&A is expected.

Wednesday, July 1

08:15 AM ADP employment report, June (GS +2,500k, consensus +2,950k, last -2,760k); We expect a 2,500k gain in ADP payroll employment, reflecting a boost from falling jobless claims and higher oil prices. We expect the “active” employment input to understate actual job gains in the ADP model.

10:00 AM ISM manufacturing index, June (GS 49.0, consensus 49.5, last 43.1); We expect the ISM manufacturing index to increase by 5.9pt to 49.0 in June, after rebounding by 1.6pt in May. While we expect the key components – new orders, production, and employment – to improve; faster delivery times will likely weigh on the degree of recovery in the composite index.

10:00 AM Construction spending, May (GS +0.8%, consensus +0.9%, last -2.9%): We estimate a 0.8% increase in construction spending in May, with a faster recovery in non-residential than residential construction.

10:00 AM Chicago Fed President Evans (FOMC non-voter) speaks: Chicago Fed President Charles Evans will host a forum on the future of the city of Chicago. Prepared text is not expected, nor is discussion of monetary policy. Audience Q&A is expected.

02:00 PM Minutes from the June 9-10 FOMC meeting: At its June meeting, the FOMC left the target range for the policy rate unchanged at 0-0.25%; and in the Summary of Economic Projections, participants expected high unemployment, low inflation, and a flat funds rate through 2022. In the minutes, we will look for further discussion of the economic outlook and the Fed’s toolkit, including the Committee’s discussion of yield curve control.

05:00 PM Lightweight motor vehicle sales, May (GS 13.1m, consensus 13.0m, last 12.2m)

Thursday, July 2

08:30 AM Nonfarm payroll employment, June (GS +4,250k, consensus +3,000k, last +2,509k); Private payroll employment, June (GS +4000k, consensus +2,519k, last +3,094k); Average hourly earnings (mom), June (GS -1.0%, consensus -0.8%, last -1.0%); Average hourly earnings (yoy), June (GS +5.3%, consensus +5.3%, last +6.7%); Unemployment rate, June (GS 12.7%, consensus 12.4%, last 13.3%): We estimate nonfarm payroll growth accelerated from the +2.5mn record gain in May to +4.25mn in June. With much of the economy reopening, our forecast reflects a rapid albeit partial reversal of temporary layoffs. While jobless claims remain elevated, alternative data suggest unprecedented increases in the number of workers at work sites. We also expect a seasonal bias in education categories to boost job growth by roughly 0.5mn.

We expect that about half of the 4.9mn excess workers that were employed but not at work for “other reasons” in May will be reclassified as unemployed in the June household survey, applying upward pressure on the unemployment rate. Additionally, we expect the labor force participation rate increased as business reopenings encouraged job searches. Taken altogether, we estimate the unemployment rate as reported will fall by 0.6pp to 12.7% in Thursday’s report. Correcting for misclassification of unemployed workers, we estimate the “true” unemployment rate declined more significantly, but to an even higher level (-2.4pp to 14.0% in June from 16.4% in May).

We estimate average hourly earnings declined 1.0% month-over-month and 5.3% year-over-year as lower-paid workers are rehired and the associated composition shift unwinds.

08:30 AM Trade balance, May (GS -$54.0bn, consensus -$53.0bn, last -$49.4bn): We estimate the trade deficit increased by $4.1bn in May, reflecting a rise in the goods trade deficit.

08:30 AM Initial jobless claims, week ended June 27 (GS 1,375k, consensus 1,336k, last 1,480k): Continuing jobless claims, week ended June 20 (consensus 18,904k, last 19,522k); We estimate initial jobless claims declined but remained elevated at 1,375k in the week ended June 27.

10:00 AM Factory orders, May (GS +11.1%, consensus +7.9%, last -13.0%); Durable goods orders, May final (last +15.8%); Durable goods orders ex-transportation, May final (last +4.0%); Core capital goods orders, May final (last +2.3%); Core capital goods shipments, May final (last +1.8%)

Friday, July 3

US Independence Day holiday observed. US equity and bond markets are closed.

Source: DB, BofA

via ZeroHedge News https://ift.tt/3gcbpbI Tyler Durden

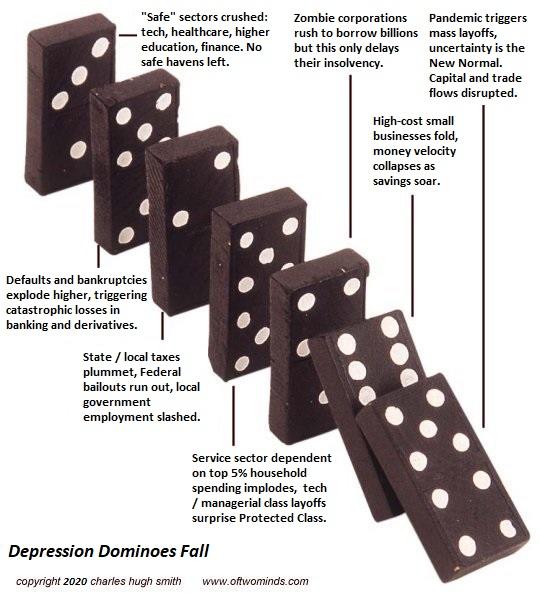

The only realistic Plan B is a fundamental, permanent re-ordering of the cost structure of the entire U.S. economy.

The fantasy of a V-shaped recovery has evaporated, and expectations for a W or L-shaped recovery are increasingly untenable. So forget V, W and L; the letters that will shape the future are N, P, B: there is No Plan B.

All the hopes for a recovery were based on a quick return to the economy that existed in late 2019. All the bailouts and stimulus programs were based on this single goal: a quick return to The Old Normal. This was Plan A.

For all the reasons that have been laid out here over the past six months, The Old Normal is gone for good.The Old Normal economy was too precarious, too brittle and too fragile to survive the toppling of any domino, as the only Plan A “solution” was to push destabilizing extremes to new extremes, i.e. doing more of what failed spectacularly and increasing the fragility of precariously fragile systems.

A short list of what’s been irreversibly destabilized due to a systemic collapse in demand, exponential rise in risk and uncertainty, dependence on over-indebtedness, imploding global supply chains, structural decline in income and employment and the rapid emergence of new business models that obsolete high-cost, inefficient, sclerotic, bureaucratic monopolies include:

1. Healthcare

2. Higher education

3. Commercial real estate

4. Tourism

5. Restaurants / live entertainment

6. Business travel / conferences

7. Office parks, commutes, urban work forces, etc.

8. High-cost urban lifestyles

We could also include entire sectors that have yet to recognize the tsunami that’s about to wash away their Old Normal: marketing, finance, local governance, etc.

The problem is there’s no Plan B for anything in the U.S. economy. There is only Plan A, a return to 2019 / The Old Normal. If that’s no longer possible, there is literally nothing left on the policy / response plate.

What nobody dares even ask is: what businesses and industries will still be financially viable running at 50% capacity? How many cafes, restaurants, resorts, airlines, etc. will turn a profit operating at 50% capacity? How many can not just survive half of the seats being empty, but turn a profit?

The short answer is very few, because the operating costs of most businesses are unbearably high. The likely survivors are those enterprises with low fixed costs and low operating costs– enterprises that own their facilities in locales with low property taxes, and enterprises that can be run by the owners without employees.

How many enterprises have these kinds of barebones cost structures? Very few.

For most enterprises, the only way they can lower their costs to a level that enables their survival is to cut costs by half: cut rent, mortgages, debt service, property taxes, fees, utilities, insurance, etc. by half.

That would mean everyone down the line would have to survive on half of their previous revenues: landlords, banks, local municipalities, service providers, and so on.

How many of these institutions and enterprises could survive on 50% of their previous revenues?

The only realistic Plan B is a fundamental, permanent re-ordering of the cost structure of the entire U.S. economy. Call it DeGrowth, or creative destruction, or disruption if you prefer, but whatever name we use, the reality will be extraordinarily disruptive, uncertain, risky and unpredictable.

As many of us has explained over the years, unstable, brittle, fragile systems characterized by soaring inequality, pay-to-play political corruption and dependence on debt, leverage and speculative bubbles were unsustainable.

Plan B can be a chaotic mess of denial and failed half-measures that only make all the problems worse, or it can be a positive transformation that results in a society that does more with less. The choice is ours.

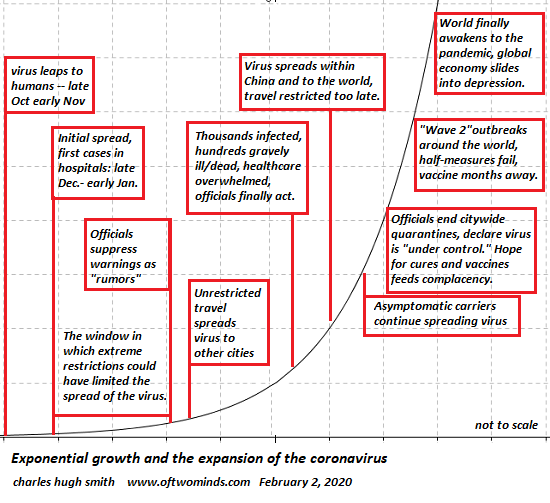

Unfortunately, the pandemic chart I composed on February 2, 2020 is still playing out, increasing uncertainty.

Iran Calls For Trump’s Arrest Over ‘Brutal Murder’ Of Revolutionary Guard General Tyler Durden

Mon, 06/29/2020 – 09:05

Update (0920ET): Iran’s call for the arrest of President Trump has been dismissed as “a propaganda stunt” by the Trump Administration’s special representative for Iran, Brian Hook.

* * *

A top Iranian prosecutor has called for the arrest of President Trump and dozens of other Americans for their involvement in the “brutal murder” of former IRGC General Qassem Soleimani in Baghdad.

According to the AP, “the charges underscore the heightened tensions between Iran and the US since President Trump unilaterally withdrew America from Tehran’s nuclear deal with world powers,” though President Trump “faces no danger of arrest.”

Iran’s state-run IRNA news agency reported Monday that Tehran prosecutor Ali Alqasimehr has accused Trump and more than 30 other Americans (whom Iran believes were involved in planning and executing the Jan. 3 strike that killed Gen. Qassem Soleimani in Baghdad) of “murder and terrorism charges”. The identities of those other than Trump weren’t disclosed, however.

After filing the charges, Alqasimehr on behalf of Iran reportedly requested an Interpol “red notice” be issued calling for the arrest of Trump and the others, which represents the highest level arrest request issued by Interpol. Local authorities end up making the arrests on behalf of the country that request it. The notices cannot force countries to arrest or extradite suspects, though they can put subjects at risk of arrest or detention if they travel abroad.

Interpol hasn’t commented on the requests, suggesting that it isn’t taking Iran’s petition seriously. Interpol’s guidelines for red notices explicitly states that the agency can’t get involved in political issues.

Soleimani, the head of the IRGC’s Quds Force (an international arm tasked with coordinating terror attacks in accordance with Iran’s interests around the world) was killed during the opening days of 2020, kicking off what has been a year of non-stop news and activity as both Iran and the US were soon hammered by the coronavirus as it spread internationally from Wuhan, China.

via ZeroHedge News https://ift.tt/2Zft23k Tyler Durden

Can The Trillions Keep Ahead Of The Millions? Tyler Durden

Mon, 06/29/2020 – 08:48

Submitted by Michael Every of Rabobank

10 million. That’s now the global total of virus infections. Less than a week ago it was 9 million. Deaths are over 500,000. In the US, Texas and Arizona have banned bar drinking as Covid surges in the sunbelt, and 5.3% of NBA players tested are coming back positive as a worrying benchmark; in the UK, Leicester faces a new local lockdown, and one of the government’s scientific advisors says things nationally are on a “knife edge” with a spike in new infections expected by July; Germany has reportedly put in place internal quarantine for domestic travellers in Bavaria; Australia has seen a breakout in Victoria that might mean a new lockdown there; Brazil just had its worst week yet with 259,105 new cases; the New Delhi healthcare system is reported as on the brink of collapse; and as schools get ready to reopen in Europe after the summer, note that Israel –which liked to think it had beaten the virus– is officially now at the start of a second Covid wave (and soon, it sees, lockdown) being blamed on the hasty reopening of schools, which appear to have acted as a major transmission mechanism.

There are people out there still saying that this is not serious, especially in economies that desperately want to open up, or which still refuse to lock own. They point to lower hospitalisation rates and death rates with this second spike than with the first. That is true, but let’s wait a few weeks and see if they follow with a lag once hospitals are overloaded. Moreover, scientists increasingly report that even moderate Covid cases can mean permanent damage to lungs, nerves, the heart, and the pancreas, potentially causing diabetes. So “Happy Monday”…and that’s before we consider other news.

US-China decoupling continues apace. Late last week we saw suggestions from China that US interference via sanctions, especially over Hong Kong, would be a red line that might see Beijing walk away from the US-China trade deal. Tomorrow we will see the national security law for Hong Kong passed in Beijing, and it appears it will include life imprisonment for breaking it. Indeed, the sole pro-Beijing Hong Kong representative working on the bill has openly lobbied for the law to have more than the proposed ten-year penalty –which appears to have been successful– and for it to be retroactive. It is hard to see the current China hawks in the US Congress remaining silent if such a red line is crossed on Tuesday.

It is not like we are short of other US-China decoupling stories anyway: they are spreading like the virus. Even China considering allowing its giant commercial banks to develop into US-style investment banks can be seen as bad news when one wonders exactly what future market share Beijing can then dangle to the Wall Street firms it uses as political counterweights to China hawks.

In other geopolitics the picture is also messy. The India-China border stand-off is far from over, with both sides building up their forces and the Global Times tweeting: “If #India wants to take advantage of US support in border dispute with #China, it is terribly mistaken, as the Chinese PLA is fully prepared & capable of defending on multiple fronts including China-India border, South China Sea and Taiwan Straits: analysts” (How is that trade deal looking again?) In the Middle East we have a major explosion in Iran and potentially explosive Israeli actions from as soon as 1 July, while Egypt is serious about intervention in Libya that would see it facing off against Turkey. In Europe, the US continues to press ahead with plans to move troops from Germany to Poland, which will inflame Germans, Russians, and much of the US establishment alike.

Which is already inflamed by allegations US President Trump has allowed Russia to pay a bonus to those who kill US troops in Afghanistan. Trump claims he had not been presented with this information, and that it is not credible. Is Vladimir Putin deliberately trying to weaken a president whom the New York Times, which published this story, likes to repeatedly claim is a close friend of Moscow? The allegations are literally explosive. The lack of market reaction is partly due to a generalised liquidity anaesthesia, and partly due to little expectation that the US will act on it (other than by say moving troops to Poland in violation of long-held understandings with Moscow); and perhaps partly because the story can be seen as a replay of #Russiagate (i.e., domestic US politics)?

In domestic politics the picture is equally messy. The US is still wracked with protests; French President Macron’s party was handily defeated in mayoral elections in Paris and other major cities by the Green Party, and in the south the far-right National Rally did well; Poland’s incumbent President Duda won the first round of elections with 41.8% of votes, and the outcome of the second round on 12 July vs. the pro-EU and liberal Warsaw mayor Trzaskowski will decide whether the country continues to lean firmly towards conservatism populism or not; and in Australia, an MP is being investigated over allegations his office was infiltrated by Chinese intelligence..

On the economy, the one number so far today was Chinese industrial profits, which were up 6.0% y/y in May. How this is possible when exports are not up and neither is domestic demand, while the Chinese Beige Book says the entire economy remained in recession in Q2, is a good question. To which the answer will be “Look, China! Look, 6%!” The PBOC keeps underlining that it is there to provide ever-more credit to the economy, even as CNY will be kept simultaneously stable. That’s why 10-year Chinese bond yields are at 2.87%, over 220bp above the US.

Indeed, against this global backdrop we have US 10-year yields at 0.64%, the USD on reasonable footing for now, and equities having rare red sessions (the S&P closing -2.4% on Friday, the Nikkei -2.0% at time of writing today). Obviously the key focus will be on tomorrow’s Congressional testimony where Fed Chair Powell and Treasury Secretary Mnuchin will be able to flesh out how many USD trillion more they propose pumping into the economy ahead to try to stabilize the situation.

Can the trillions keep ahead of the millions? That’s the key dynamic.

via ZeroHedge News https://ift.tt/3eNYaxq Tyler Durden

Facebook Pummeled In Pre-Market As Boycott Builds, Liberal Media Takes Aim At Zuck Tyler Durden

Mon, 06/29/2020 – 08:28

Facebook shares are set for the second day of declines as a boycott of advertisers on the social media platform is quickly gaining momentum.

The latest companies pausing ads on the social media platform in response to its handling of hate speech and violence are Starbucks Corp. and Diageo Plc., reported Bloomberg.

Here’s a list of the companies that have said they’re decreasing or halting ad spending with Facebook:

Unilever

Verizon

Hershey’s

Honda

The North Face

Ben & Jerry’s

REI

Patagonia

Eddie Bauer

Upwork

Mozilla

Magnolia Pictures

Birchbox

Dashlane

TalkSpace

LendingClub

Starbucks Corp.

Diageo Plc.

Facebook shares declined about 2.5% in pre-market trading on Monday after the news Starbucks Corp. and Diageo Plc. would pull back on spending. Shares plunged 8.3% on Friday after Unilever, one of the world’s largest advertisers, halted advertisements on the social media channel. From last week’s high, shares are down 16%.

Now it seems Washington Post is going after Facebook’s CEO Mark Zuckerberg…

(WaPo) – Hours after President Trump’s incendiary post last month about sending the military to the Minnesota protests, Trump called Facebook chief executive Mark Zuckerberg.$FBhttps://t.co/rBpzC1cYwI

There is an amusing piece on the FTs’ Alphaville listing 20 things investors should look for when trying to work out who will be the next Wirecard. You don’t need to be a financial genius to work out which company they might be talking about… It’s a basic wake-up call. In periods of economic darkness, its all-to-easy to be persuaded as to the efficacy of snake oil. If something over-promises, makes lots of noise while underdelivering, and is basically a personality cult – then it’s long-term unlikely to be a particularly successful investment.

Back in the real world…

We are nearly half-way through 2020. Although we’ve been shocked, surprised and buffeted by the Virus, and buoyed by the swift and effective intervention of Governments to support companies and mitigate job losses while Central Banks have calmed markets with the opium of QE Infinity, I can’t help wonder if the real earthquake is yet to come.

I am still bullish about long-term recovery as we adapt to the virus and it spurs a new tech development age. But I can’t help feeling deeply uneasy about current markets and the resilience of global financial systems.

This crisis is unlike anything I’ve experienced before. Normally a market crash is explosive event – it occurs when something in the financial sphere breaks; like confidence in housing and financial systems in 2007, or valuations in the Dot.Com crash, or faith in credit constructs like during the European Sovereign Debt crisis in the 2010s. In each of case of financial mayhem I’ve experienced since the Great Perp Crash of 1986, the initial shock and horror gradually lessens as the market discounts the shock, shrugs it off, and carries on.

The Global Financial Crisis of 2007-2008 has some similarities to current events – it was slow. It took more than a year from the gating of Bear Stearns structured credit funds, through the collapse of commercial paper markets, the run on Northern Rock, till we got to the collapse of Lehman in September 2008. As banks were bailed out and rescued, there were around three months in 2008 when it felt like financial markets were irreparably broken. Of course, they weren’t – governments and central banks nursed them through. Stock markets were extremely volatile – but were equally swift to arbitrage that support – triggering a rally that lasted 12 years! (Largely on the back of markets being distorted by ultra-low rates and QE.)

This time it feels different.The crisis started off with a meteor strike – the virus. We’ve never seen anything impact the real economy so dramatically. Normally – it happens the other way around: financial crashes impact the markets and only then does the pain trickle down into the real world. This time it’s real jobs and production that got hit first. That’s fundamentally different.

I’m not convinced that markets really understand that difference. The effect on the real economy of financial failure is felt in terms of the flow of capital to businesses. If a bank blows up – it will impact savers and borrowers. This time we’re looking at how will crashing earnings and diminished rental incomes will hit the financial markets – but they are behaving as if it’s just another round of QE Infinity for the markets to arbitrage. As we all know markets are completely delinked to the real world at present.

Yet, the damage the real world is going to inflict on financial markets is going to be huge – but that’s not what I see the banking regulators and authorities preparing for. They’re pushing financial institutions to participate by easing lending and supporting confidence. You can understand why – yet they also know a crisis coming. Just read the dissenting statement by Fed Governor Lael Brainard after she stepped back from the Fed’s decision to allow bank dividends: “many large banks are likely to need greater loss absorbing capital to avoid breaching their buffers in adverse circumstances next year.”

The bottom line is global central banks know a financial crisis is possible/probable.

There are many issues here. Is the market pricing in a major financial systems crisis – to a limited extent. What if rising real world problems trigger a massive NPL crisis? Effectively the whole financial system now sits on financial assets (stocks and shares) which are underpinned by government support. How sustainable is that?

For instance, In the UK we know commercial landlords have received less than 20% of their rental incomes on the last 2 quarter days – the day tenants are supposed to pay the next three months rent. Property “experts” expect landlords will recover much of that rent in the aftermath of the virus. That will be interesting – how many more names are likely to disappear from high streets and how many more shopping malls will fall into receivership as folk keep shopping from home?

Companies failing to pay rents or dividends is no longer just a banking problem. Risk is now far more widely spread across the whole financial system: insurance companies and sovereign wealth funds own most City offices. Fund managers that rely on dividend income are likely to be sadly disappointed as incomes dry up as a result of government fiat or on the back of the dismal earnings season we’re about to experience.

The path for markets will depend on what surprises us next. In previous crisis I’ve watched markets roiled by a massive shock before falling in a predictable path: the daily news becomes less shocking, the markets become less volatile, and start to seek opportunities.

This time I don’t think the real financial shock has yet occurred. The dominant issue remains the virus. The market news creating the current RO/RO (risk on/risk off) volatility is all about how COVID-19 is slow burning its way across the Southern US stats, triggering renewal lockdowns, and spooking the markets. The sheer size of the US is one issue, but lax lockdowns and early re-openings in states that hadn’t reached anything close to a peak infections is another.

The virus is going to remain a massive threat, but real economic and political issues are going to emerge in coming weeks. Dismal corporate earnings and stories like the collapse of Gas fraker Chesapeake energy, or Boeing struggling to re-launch the dismal 737 MAX will dominate the news flow.

Geopolitics ranging from the deepening China/US standoff, to the EU fighting battles on Brexit, the Poor South and the democratic challenge from the East, are likely to remain negative.

And lets not forget domestic politics. An increasing number of fund managers list the US November Election as their biggest fear. Few would admit to being Trump supporters, but there is clear fear of a Biden presidency achieving a clean sweep of both the Senate and Congress. Meanwhile, Macron’s drubbing in French local elections, and the hopefull pro-European vote in Poland highlights voters unhappiness with current regimes.

As I said – I’m bullish… but selectively, and there is a lot of noise coming our way.

via ZeroHedge News https://ift.tt/2BMBOOb Tyler Durden

Futures Rebound From Early Losses Thanks To Old Faithful Overnight Ramp Tyler Durden

Mon, 06/29/2020 – 08:01

Yesterday, shortly following the reopen for electronic trading at 6pm, we wrote that futures slumped “in a repeat of last Sunday’s gloomy open” however previewing that this slump “had fully reversed overnight with futures nice and green by morning” and sure enough the magical overnight ramp emerged once again, with Eminis reversing all early losses and trading near session highs at 3,016 at last check, with the dollar turning red and 10Y yield higher on the day even as the yield on 5Y Treasurys hovered near a record low.

One catalyst cited for the overnight strength is a report out of China that a coronavirus vaccine developed by a Chinese firm received approval for military use and a stronger-than-expected yuan fixing weighed on demand for haven assets.

Additionally, as Nomura’s Charlie McElligott writes, “equities start lower and USTs start bull-flatter in Asia…before reversing Europe-into-US session, with global stock futs now marginally better, curves bear-steepening, Crude rallying and again Dollar fading lower, as markets continue to feel very constructive on the Eurozone Coronabond issuance project as Germany capitulates away from austerity and towards both debt mutualization and fiscal stimulus.”

Whatever the driver, after major Wall Street indexes had tumbled more than 2% on Friday as several U.S. states imposed business restrictions in response to the surge in COVID-19 cases, sentiment reversed completely even as stocks in Asia and Europe were generally muted overnight as the global death toll from the respiratory illness crossed half a million on Sunday

In premarket trading, Boeing rose 3.2% after the Federal Aviation Administration confirmed on Sunday it had approved key certification test flights for the grounded 737 MAX that could begin as soon Monday, while Facebook looked set to extend declines from Friday as a report said PepsiCo was set to join a growing number of companies pulling ad dollars from the social media platform.

“The recovery is going to be much slower and much more uneven than most people believe,” David Hunt, president and chief executive officer of PGIM Inc., told Bloomberg TV. “Markets are priced for a much sharper V-shaped recovery, which we don’t think is likely.”

European stocks were firmly in the green after starting off on the back food amid light trading volumes. In Asia, stocks fell more than 1% in Japan, Australia and Hong Kong. Japan’s Topix declined 1.8%, with DLE and Watabe Wedding falling the most. The Shanghai Composite Index retreated 0.6%, with Anhui Xinli Finance and Xiamen C&D posting the biggest slides

As Bloomberg reports, “investors began the week studying conflicting signals, as virus deaths surpassed 500,000 globally and the epicenter moves to the America. With U.K. households amassing savings at a record level and paying down debt in May, Prime Minister Boris Johnson has promised a wave of investment in infrastructure and skills.”

In rates, Treasuries were mixed with the curve fractionally steeper into early U.S. session after paring gains as U.S. stock index futures moved higher. Bunds also bear-steepened, underperforming Treasuries. Session low yields were reached as virus cases continued to mount worldwide. Month- and quarter-end needs are expected eventually to provide support. Yields were cheaper by ~1bp in long-end tenors, steepening 5s30s by ~2bp, 2s10s by ~1bp; 10-year yields around 0.65%, cheaper by less than 1bp on the day while front end and belly are richer by less than 1bp; 5-year yield at ~0.30% is within 3bp of its May 8 record low. Bunds lagged by ~1bp vs Treasuries while gilts outperform by ~1bp.

In FX, the dollar started off strong but then edged lower against most Group-of-10 peers, though moves in the crosses were largely confined to narrow ranges; it earlier weakened after a coronavirus vaccine developed by a Chinese firm received approval for military use and a stronger- than-expected yuan fixing weighed on demand for haven assets. The euro advanced, supported by an acceleration in German state inflation rates; it touched an intraday high as European funds engaged in basket-selling of the dollar and bought the shared currency. The pound gave up an Asia session gain which had followed British Prime Minister Boris Johnson’s promise of a “big plan” to help the U.K. bounce back from the coronavirus pandemic, as he seeks to revive his struggling political mission with a major speech on Tuesday. Australia’s dollar pared gains after earlier rising to an intra-day high amid corporated hedging activities into the end of the month and the nation’s fiscal year.

In commodities, oil kept falling after just its second weekly drop since April as coronavirus infections and fatalities surpassed grim milestones in a reminder the outbreak is far from under control in many parts of the world.

This holiday-shortened week (Friday is a day off, and the jobs report will be published on Thursday), investors will focus on employment, consumer confidence and manufacturing data for June for signs of whether the U.S. economy will continue to rebound after indications of a pickup in May. On today’s calendar we have pending home sales, Dallas Fed manufacturing activity, while the Treasury sells 13-week and 26-week bills. New York Fed President John Williams moderates a discussion with IMF Managing Director Kristalina Georgieva.

Market Snapshot

S&P 500 futures up 0.2% to 3,014

STOXX Europe 600 little changed at 358.37

MXAP down 1.2% to 157.17

MXAPJ down 0.9% to 509.88

Nikkei down 2.3% to 21,995.04

Topix down 1.8% to 1,549.22

Hang Seng Index down 1% to 24,301.28

Shanghai Composite down 0.6% to 2,961.52

Sensex down 1% to 34,837.36

Australia S&P/ASX 200 down 1.5% to 5,815.03

Kospi down 1.9% to 2,093.48

German 10Y yield rose 1.4 bps to -0.468%

Euro up 0.3% to $1.1248

Brent Futures down 2.1% to $40.16/bbl

Italian 10Y yield fell 1.3 bps to 1.164%

Spanish 10Y yield rose 1.3 bps to 0.471%

Brent Futures down 1.2% to $40.52/bbl

Gold spot down 0.13% to $1,769.05

U.S. Dollar Index down 0.1% to 97.31

Top Overnight News from Bloomberg

Deaths from the coronavirus worldwide topped 500,000 and infections surged past 10 million, two chilling reminders that the deadliest pandemic of the modern era is stronger than ever

Fast-money hedge funds are rushing to cover their bearish U.S. stock bets even as the equity rally threatens to break down. Speculative investors bought the most S&P 500 Index E-mini since 2007 in the week to June 23, according to the latest Commodity Futures Trading Commission data. Net short positions in the contracts were at their highest in almost a decade as the U.S. equity rebound pushed the benchmark back toward record territory

Germany plans to raise 146 billion euros in the third quarter from bond sales and money market instruments, almost triple an earlier estimate, as the nation seeks to help spur an economic recovery from the coronavirus

China will impose a visa ban on U.S. citizens who interfere with sweeping national security legislation planned for Hong Kong, a move that comes shortly after the Trump administration imposed them on some officials in Beijing

The world’s biggest bond market is holding firm in its conviction that the revival of the American economy from the devastation of the pandemic will be slow and fragmented

The Swiss National Bank says the lower limit for the special liquidity-shortage financing facility rate will be reduced to at least 0% from current level of at least 0.5%

Asian bourses began the week lower across the board with sentiment dampened as focus remained on rising virus infection rates which has forced some key states to back-pedal on their reopening efforts with California, Texas and Florida imposing new restrictions, while the global death toll from the pandemic has surpassed the half million mark. ASX 200 (-1.5%) was dragged lower with energy underperforming the broad weakness seen across Australia’s sectors aside from gold miners which stayed resilient on the safe-haven play, and Nikkei 225 (-2.3%) was pressured after weaker than expected Retail Sales data and with the number of new infections in Tokyo rising to the most since the removal of the state of emergency declaration. Hang Seng (-1.0%) and Shanghai Comp. (-0.6%) declined following a liquidity drain by the PBoC and amid concerns regarding the Hong Kong national security law in which the NPC Standing Committee reviewed a draft on the bill and are set for a vote tomorrow. This is likely to increase the ongoing US-China tensions, which was also not helped by comments from both sides as US Secretary of State Pompeo noted the US is imposing visa restrictions on Chinese Communist Party officials over the autonomy of Hong Kong as well as human rights issues, and Chinese officials warned the US of crossing red lines such as meddling in Hong Kong and Taiwan which could put the trade deal’s purchases at risk. Finally, 10yr JGBs were rangebound with price action only marginally benefitting from the broad risk-averse tone and BoJ’s presence in the market for a total of JPY 600bln of JGBs heavily concentrated in 5yr-10yr maturities. PBoC skipped reverse repos for a drain of CNY 40bln but conducted CNY 5bln of commercial bill swaps. (Newswires)

Top Asian News

Philippine Central Bank Chief Sees No Need for Rate Cut Now

Indonesia Nears Deal With Central Bank on Deficit Funding

Young Blood May Fail to Curb Japan’s Support for Coal Power

An eventful start to the week for the equity-space in terms of price action (Euro Stoxx 50 +0.4%) after the region initially picked up the baton from the relatively downbeat APAC handover. Europe opened with broad losses to the tune of around 0.4-0.5% before immediately trimming downside to trade firmly in positive territory. Thereafter gains dissipated with no fresh fundamental factors immediately affecting the bourses, however, repots that the Chinese Foreign Ministry will be putting visa restrictions on US relations over Hong Kong added to the US-Sino woes ahead of the National Security Bill vote tomorrow – expected to swiftly pass through for implementation from July 1st. It’s also worth bearing in mind month/quarter/HY-end flows influencing price actions as firms rebalance portfolios. Nonetheless, a mixed performance is now seen across major European cash bouses, whilst State-side, the E-Mini S&P failed to breach resistance at its 200 DMA ~3019.00 and currently meanders just under the key level. Sectoral performance is also mixed after the regions opened mostly lower, albeit the IT sector holds its position as the outperformer, potentially on the back of AMS (+4.0%) after EU antitrust regulators gave the green light for its takeover of Osram Licht (+0.3%). The Energy sector meanwhile lags amid price action in the oil complex. The detailed breakdown paints a similarly mixed picture with no clear risk tone to be derived; Travel and Leisure (-0.3%) remains closer to the bottom of the pile as investors fear the repercussions in the sector in light of a second resurgence of global COVID-19 cases. In terms of individual movers, Wirecard (+145%) shares traded higher by over 200% at one point – potentially on consolidation from its recent detrimental performance as its scandal deepens, however, sources over the weekend noted that that several investors are considering purchasing parts of Wirecard. Elsewhere, BP’s (+2.6%) gains were exacerbated as its stated that its Petrochemical unit sale to INEOS will further strengthen finances and will deliver USD 15bln divestment targets a year early. Airbus (+2.3%) shares opened lower with losses deeper than 2% as the group said it will cut production by around 40% over two-years. Commerzbank (+2.4%) holds onto opening gains as sources stated the board is looking at an aggressive cost-cutting plan – potentially including around 7,000 layoffs alongside 400 branch closures.

Top European News

BP Speeds Up Transformation With $5 Billion Chemicals Unit Sale

Europe Slowly Picks Up Pieces After Virus Shattered Economy

Inside the Brexit Talks, Frustration Starts to Give Way to Hope

In FX, the DXY is holding between 97.051-141 parameters amidst the ongoing resurgence of COVID-19 in several US states, but with technical support via the 21 DMA at 97.050 keeping the index underpinned above 97.000 as the clock ticks down to the end of June, Q2 and the first half of 2020. Moreover, several Greenback/G10 pairs are also observing chart levels against the backdrop of fragile/fluid risk sentiment on a variety of (mainly geopolitical) factors beyond the coronavirus and uncertainty about 2nd waves as more countries reopen. Back to the Buck, pending home sales and the Dallas Fed manufacturing index may provide some fundamental impetus ahead of Fed rhetoric from Daly and Williams.

EUR – A marginal outperformer and trying to extend gains above 1.1200 vs the Dollar, but finding resistance around 1.1250, the 200 HMA (1.1241) and 1.1240 pivot tough to convincingly breach before decent option expiry interest at 1.1270 (1 bn) in the run up to preliminary German CPI data. However, the single currency has cleared a psychological, if not really significant from a technical standpoint, marker against Sterling as Eur/Gbp crosses 0.9100 for the first time in some 3 months awaiting the start of intensive Brexit trade talks.

NZD/CHF/CAD/AUD – All marginally firmer vs the Usd, but rangy with the Kiwi hovering above 0.6400 and Franc over 0.9500, though the latter lagging Euro either side of 1.0650 following latest weekly Swiss sight bank deposits showing a rebound in both domestic and total balances. Elsewhere, the Loonie is holding within a 1.3697-46 band ahead of Canadian building permits and ppi even though crude prices remain soft and the Aussie is straddling 0.6865-70 despite a record rise in Victorian virus cases.

JPY/GBP/SEK/NOK – The Yen is sitting just under 107.00 and right in the middle of 10/50 DMAs at the round number and 107.37 respectively after sub-forecast Japanese retail sales overnight, while Cable is drifting back down from circa 1.2390 towards sub-1.2315 stops after weaker than expected UK consumer credit mortgage approvals, but perhaps more jittery about the aforementioned next phase of negotiations with the EU. Nevertheless, offers are said to be in place around 1.2410 and close to the 50 DMA (1.2412-15), while nearest upside targets in Eur/Gbp are at 0.9139 and 0.9144 (March 23 and 24 peaks respectively). Similarly, the Swedish Crown is underperforming in wake of a much narrower trade surplus. Indeed, Eur/Sek is back up near 10.5000, while Eur/Nok pivoting 10.9000 irrespective of the downturn in oil noted above.

EM – Broad declines vs the Dollar, and especially the crude/commodity bloc, such as the Rouble and Mexican Peso, but the Turkish Lira deriving some comfort from an improvement in economic confidence with Usd/Try rotating around 6.8500.

In commodities, WTI and Brent front-month futures trade choppy within a tight range, albeit remain in negative territory after the complex kicked off the trading week on the backfoot amid rising global COVID-19 infections hampering reopening efforts in key US states, whilst some eastern Asian countries extended their alerts level and China’s Hebei province put around half a million residents under a Wuhan-style lockdown. Aside from virus woes, news-flow has been quiet from a fundamental standpoint. Participants will want to keep an eye on how the Hong Kong National Security Bill pans out for wide US-China relations as the sides slap tit-for-tat visa restrictions over the city. WTI August hovers just above USD 38/bbl having found support at USD 37.50/bbl while its Brent counterpart sees itself north of USD 40.50/bbl after touted support touted last week around the USD 40.05/bbl region. Elsewhere, spot gold trades with modest losses sub-1770/oz; albeit more a function of month-end rebalancing as opposed to risk-tone or Dollar dynamics. Copper prices meanwhile climbed over a five-month peak in Shanghai amid a softer Buck and supply risks from its top producer Chile.

US Event Calendar

10am: Pending Home Sales MoM, est. 18.0%, prior -21.8%; YoY, est. -22.0%, prior -34.6%

10:30am: Dallas Fed Manf. Activity, est. -22, prior -49.2

DB’s Jim Reid concludes the overnight wrap

This is the first time I’ve written any piece of work – well since I was doing my GCSEs at school – where I do so in an environment where Liverpool are English Premier League champions. It feels good. I had the day off from the EMR on Friday which was handy as I stayed up late watching the celebrations on telly Thursday night. Let’s hope it’s not the only year of my career where this is the case!! The only bad news from Thursday was that I had bad back spasms playing in the Worplesdon Pro-Am Charity golf tournament and hobbled off the course at the end only just breaking 90!! I play off 6 for context. I’ve completely remodelled my swing over the last 15 months. It now looks beautiful but struggles to connect with the ball properly or send it in a straight line. I’m not sure how much longer I’ll give it before I go back to ugly but effective!

The headline covid case numbers also don’t look too pretty at the moment as we passed 10 million reported cases globally over the weekend and 500k fatalities. Obviously this is only a proportion of the actual case load so it’s difficult to derive too much info from the figure other than the fact that the numbers have been increasing of late, partly due to the wider reported spread of the virus in the Americas and in the likes of India. However the accelerating case numbers also reflects increased testing as well. Fatalities aren’t rising to anything like the same degree as they did in March and April but it’s not easy to work out how much of that is due to more testing diluting the case fatality rate, how much it’s due to better treatment of the virus, and how much is due to a lower risk demographic contracting the virus. As an anecdote, on Friday it was reported via a University of Oxford study that in England, the hospital fatality rate from covid has dropped from 6% at the peak to around 1.5% in June and still declining. It seems we are better at treating the virus now which is good news and it’s also likely that the more vulnerable are being better shielded.

So if this continues it should be seen as a positive. However for now while the virus spread increases in the US there is going to be a lot of concern and confusion about the strategy and the end outcome, especially in the hotspot states and whether it spreads back into the states where the virus has been suppressed.

The latest over the weekend points to things getting worse in case numbers in southern US. The weekly average of covid-19 cases in the US has now surpassed the heights of the spring, while the US recorded an all-time high in new cases on Saturday with over 45,400. Texas, Florida and Arizona have either paused or rolled back reopening plans in light of the new cases, however they are not enacting stricter measures that were seen earlier in the pandemic in places like New York. Over the weekend, Florida Governor DeSantis cited people in the 18-to-44 age group as the cause of the recent rise in positive Covid-19 tests. The Governor said, “Most of this is not because of people going to work, it’s because they’re being social”. This does not sound like someone who wants to shut businesses down again.

While Texas, Florida and Arizona remain among the most worrying in terms of new cases, other southern US states have either slowed down reopening plans or indicated intentions to do so. The positive test rate for Texas has now soared to a record 14.3%. Arkansas, just northeast of Texas, announced they will pause their phased reopening until the current wave subsides, while other neighboring states have indicated similar intentions if case counts continue to rise. In terms of the effective transmission rates (Rt), 33 US states now have Rt values over 1.0. In fact only 2 states, Connecticut and Massachusetts, have their entire confidence level under 1.0 at this point, compared to 7 over 1.0. Fatality rates have yet to see spikes similar to that of cases, and as we have discussed this is hopefully a result of protecting the higher risk and improving treatment. Though for the medium term it seems like US economies are set to reinstitute pauses if the case count continues to get out of hand. So even though the virus seems to be becoming less deadly, confidence has been shaken so much that countries will struggle economically while case levels remain high. In the pdf today (“view report”) we show the usual global case and fatality tables and also repeat the 7 day lagged charts of case and fatalities in the US and the four big hot spot states. We also show what happened with NY for a comparison. There are some signs that deaths in Arizona are responding higher to some degree to lagged case growth but for now the other states are seeing the relationship weaken which is good news. It’s the same for the US overall, especially relative to the first wave.

In terms of markets, bourses in Asia are on the back foot this morning following the heavy losses on Wall Street on Friday with the Nikkei (-2.02%), Hang Seng (-1.59%), Shanghai Comp (-0.71%), Kospi (-1.53%) and ASX (-1.75%) all down. Meanwhile, futures on the S&P 500 are down a much more modest -0.10% and yields on 10y USTs are flat. Elsewhere, WTI crude oil prices are down -1.87% to $37.77.

Here in the UK, Prime Minister Boris Johnson said in an interview in the Mail yesterday that the UK will spend large sums on hospitals, schools and roads to jump-start the economy while rejecting a return to the austerity policies that followed the 2008 financial crisis. PM Johnson is expected to unveil the spending plans in a major speech on Tuesday. In other overnight news, Bloomberg has reported that China’s imports of US goods through May reached c. 19% of the total target for 2020 set in the phase 1 trade deal. China purchased 22.1% of targeted manufactured products, 20.8% of targeted agricultural products and 3.1% of targeted energy products. Meanwhile, French central bank head Francois Villeroy de Galhau played down the prospect that the ECB would buy high yield bonds as part of its pandemic emergency program saying “the debate is probably not urgent,” while further adding “I rule out that we buy bonds that were rated ‘junk’ before the crisis.” However, he also said that the ECB must examine whether it can reduce the dependence of its monetary policy on rating companies.

As for this week, we’ll see a shortened trading period with Friday a US holiday in lieu of Independence Day on Saturday. Thursday will likely see activity wind down early and rapidly ahead of the weekend. The last major act of the week will therefore likely to be the all-important payrolls report brought forward to Thursday. Our US economists are looking for a further +2m gain in non-farm payrolls, following last month’s unexpected +2.509m increase, along with a further reduction in the unemployment rate to 12.6%. This improved labour market performance chimes with what we’ve seen in other indicators, such as the weekly initial jobless claims that have fallen for 12 consecutive weeks now. That said, it’s worth remembering that given the US shed over 22m jobs in March and April, even another +2m reading would still mean that payrolls have recovered less than a quarter of their total losses, suggesting there’s still a long way to go before the labour market returns to normality again.

The other main data highlight will be the final June PMI releases from around the world. The manufacturing numbers are out on Wednesday before the services and composite PMIs come out on Friday for the most part (ex US), while there’ll also be the ISM manufacturing index too from the US (on Wednesday). For the countries where we already have a flash PMI reading, they generally surprised to the upside, even as many remained below the 50-mark. It’ll also be worth keeping an eye on the numbers for China, given they’re some way ahead in the reopening process relative to the US and Europe.

In politics, a key highlight this week will be a meeting between Chancellor Merkel and President Macron taking place today, where both the EU budget and the recovery fund will be on the agenda. That comes ahead of another summit of EU leaders scheduled for the 17-18th July, where the 27 leaders will meet in person in Brussels for further discussions on the recovery fund. Meanwhile, the start of July on Wednesday formally sees Germany take over the rotating EU presidency, which they’ll hold for the next six months.

Staying with politics, Brexit negotiations between the UK and the EU on their future relationship will return once again. This will be the first set of intensified talks that are taking place every week over the next five weeks, as the two sides look to come to an agreement following fairly slow progress in the talks thus far. Since the last round of negotiations, a high-level meeting took place between Prime Minister Johnson and the Presidents of the European Commission, Council and Parliament, where the two sides agreed in their statement that “new momentum was required” in the discussions. There does seem a bit more positivity now than there was a month ago but much work still needs to be done.

Elsewhere we have the release of the FOMC minutes for the June meeting on Wednesday, along with an appearance by Fed Chair Powell and Treasury Secretary Mnuchin tomorrow before the House Financial Services Committee. Otherwise, speakers next week include the BoE’s Governor Bailey and Deputy Governor Cunliffe, along with the ECB’s Schnabel and New York Fed President Williams.

Recapping last week now. Global equities fell on the week with the S&P 500 falling -2.86% (-2.42% Friday) and is now down -1.16% for the month of June with two days of trading left in the month. This could be the first monthly loss since March. The tech-focused NASDAQ underperformed slightly last week, down -3.31% (-2.84% Friday) but is +2.82% in June so far. European equities outperformed the S&P as case growth remains relatively contained versus in the US, with the Stoxx 600 falling a lesser -1.95% (-0.39% Friday) over the five days. The pullback was well correlated as the DAX (-1.96%), FTSE MIB (-2.52%), and FTSE 100 (-2.12%) indices all fell to similar degrees on the week. Asian indices were more mixed. The Nikkei rose +0.15% over the week (+1.13% Friday) and the CSI 300 was up +0.98% on a 3 day week, while the Kospi fell -0.31% (+1.05% Friday).

With concerns over the implications for global growth if the recent virus spread continues, oil prices fell on the week. Brent crude futures fell -2.77% (-0.07% Friday) to $41.02/barrel and WTI crude retreated -3.17% on the week (-0.59% Friday) to $38.49/barrel. In other commodities, gold rallied +1.57% (+0.43% Friday) to levels last seen in October 2012.

Gold was not the only haven to rally with risk assets weakening. Core sovereign bonds gained on the week with US 10yr Treasury yields falling -5.2bps (-4.4bps Friday) to finish at 0.641%, while 10yr Bund yields fell -6.7bps over the course of the week (-1.4bps Friday) to -0.48%. UK gilts fell -6.6bps (+1.8bps Friday) to 0.17%. As risk sentiment turned, peripheral debt widened slightly on the week. Spanish 10yr yields widened +3.2bps to German bunds over the 5 days, while Portuguese bonds widened +1.6bps and Greece bonds widened +5.3bps. Credit spreads widened considerably more, particularly in the US. US HY cash credit spreads were +39bps wider on the week (+11bps Friday), while IG widened +5bps (+1bp). European HY cash spreads were + 17bps wider (unchanged Friday) with IG just +5bps wider (unchanged Friday).

On the data front, US consumer spending rose +8.2% (vs. +9.3% exp.) from the prior month on Friday. This was the highest monthly increase in over 60 years of data keeping, but the overall level still remains far below pre-pandemic levels. This follows spending falling the most on record in April. Incomes declined -4.2% (vs. -6.0% exp.), just below the record decrease, after last month’s ‘largest-ever’ increase that was primarily driven by household relief payments. The University of Michigan Sentiment survey rose from 72.3 to 78.1 (vs. 79.2 exp.), but remains near 7 year lows. The sentiment data was similar in Europe where French consumer confidence rose to 97 from 93 (vs. 95 exp.), while Italian consumer confidence rose 7.3pts to 100.6 (vs. 97.5 exp.). So while sentiment is improving off the lows in April and May, there is still a lot of recovery left. Lastly, Euro Area M3 money supply growth for May was +8.9% (vs. +8.7% exp.).

via ZeroHedge News https://ift.tt/3g6n2AK Tyler Durden

Gilead Will Charge More Than $3,000 For A Course Of COVID-19 Drug Remdesivir Tyler Durden

Mon, 06/29/2020 – 07:56

All those stories about patients being billed for tens of thousands of dollars for coronavirus-related care elicited promises from the White House that “everything will be covered”. Still, as thousands of Americans complain about charges related to COVID-19 testing and care being passed on by their insurance companies, Gilead, the pharmaceutical company that has pushed remdesivir down the world’s throat despite the fact that the cheap steroid dexamethasone has proven – in at least one high quality study – more effective at lowering mortality rates, has just published its expected pricetag for a five-dose course of the drug.

On Monday, Gilead disclosed its pricing plan for Gilead as it prepares to begin charging for the drug at the beginning of next month (several international governments have already placed orders). Given the high demand, thanks in part due to the breathless media coverage despite the drug’s still-questionable study data, Gilead apparently feels justified in charging $3,120 for a patient getting the shorter, more common, treatment course, and $5,720 for the longer course for more seriously ill patients. These are the prices for patients with commercial insurance in the US, according to Gilead’s official pricing plan.

As per usual, the price charged to those on government plans will be lower, and hospitals will also receive a slight discount. Additionally, the US is the only developed country where Gilead will charge two prices, according to Gilead CEO Daniel O’Day. In much of Europe and Canada, governments negotiate drug prices directly with drugmakers (in the US, laws dictate that drug makers must “discount” their drugs for medicare and medicaid plans).

But according to O’Day, the drug is priced “far below the value it brings” to the health-care system.

However, we’d argue that this actually isn’t true. Remdesivir was developed by Gilead to treat Ebola, but the drug was never approved by the FDA for this use, which caused Gilead to shelve the drug until COVID-19 presented another opportunity. Even before the first study had finished, the company was already pushing propaganda about the promising nature of the drug. Meanwhile, the CDC, WHO and other organizations were raising doubts about the effectiveness of steroid medications.

Months later, the only study on the steroid dexomethasone, a cheap steroid that costs less than $50 for a 100-dose regimen, has shown that dexomethasone is the only drug so far that has proven effective at lowering COVID-19 related mortality. Remdesivir, despite the fact that it has been tested in several high quality trials, has not.

So, why is the American government in partnership with Gilead still pushing this questionable, and staggeringly expensive, medication on the public?

via ZeroHedge News https://ift.tt/38a3atK Tyler Durden