Small Businesses “Losing Confidence In The Economy” On Record Labor Shortages, Soaring Inflation, Sliding Margins

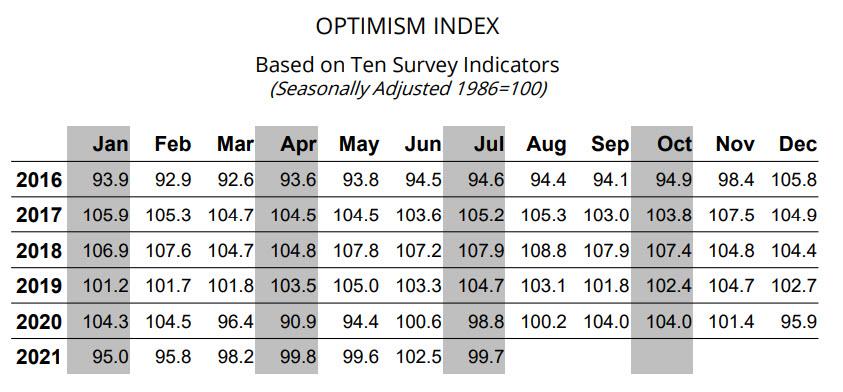

Small business owners grew less confident in the economic recovery in July amid labor shortages that hit a fresh, 48-year record high, according to the latest NFIB survey released on Tuesday. The NFIB Small Business Optimism Index decreased in July to 99.7, a drop of 2.8 points, reversing June’s 2.9-point gain.

Six of the 10 components tracked by the survey declined, three improved, and one was unchanged. The NFIB Uncertainty Index decreased seven points to 76, indicating owners’ views are held with more certainty than in earlier months.

“Small business owners are losing confidence in the strength of the economy and expect a slowdown in job creation,” said NFIB Chief Economist Bill Dunkelberg.

“As owners look for qualified workers, they are also reporting that supply chain disruptions are having an impact on their businesses. Ultimately, owners could sell more if they could acquire more supplies and inventories from their supply chains.”

Dunkelberg’s view coincides with that of a growing number of economists who warn that while the economy is projected to expand this year at its fastest pace since the 1980s, it is starting to cool off as the impact from trillions in fiscal stimulus fades. Supply chain bottlenecks continue to dent manufacturing growth, and consumer sentiment has declined recently amid concerns about inflation.

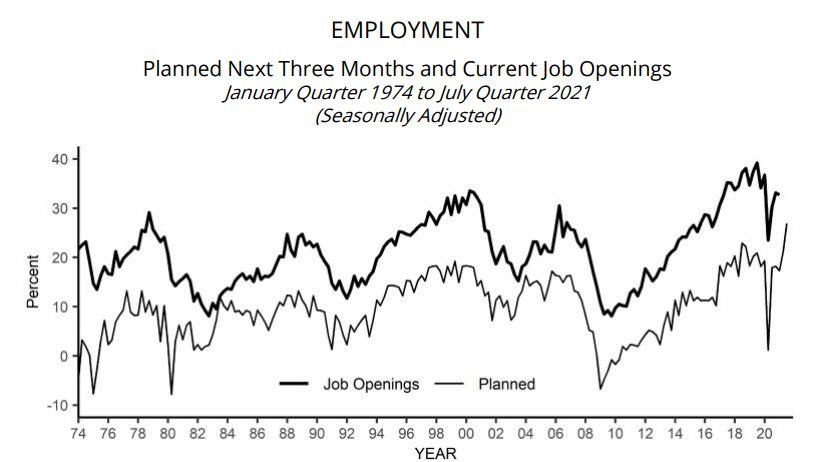

The continuing chaos in the labor market remains the biggest sticking point in small business confidence: while a new record high 49% of small business owners reported unfilled job openings in July on a seasonally adjusted basis amid a historic labor shortage, this is no longer translating into stronger hiring plans, as a net 27% of businesses plan to create new jobs in the next three months, down one point from the month prior, the NFIB survey showed.

“As owners look for qualified workers, they are also reporting that supply chain disruptions are having an impact on their businesses,” Dunkelberg said. “Ultimately, owners could sell more if they could acquire more supplies and inventories from their supply chains.”

Some 57% of respondents said they had few or no qualified applicants for open jobs in July, up one point from June.

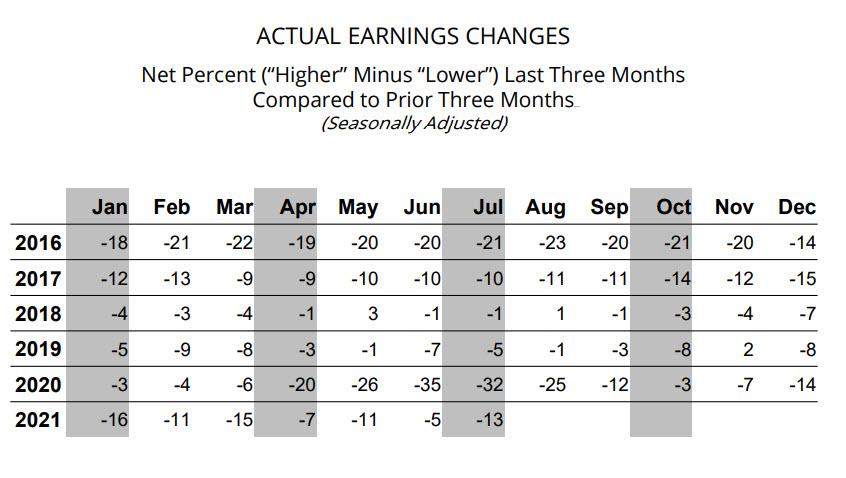

This inability to operate businesses in optimal conditions, is also translating in the first drop in actual compensation since last December: In July 38% of respondents said raised compensation, down from 39% in June, even if compensation plans continue to rise modestly.

The quality of labor ranked as businesses’ “single most important problem,” with 26% of respondents selecting it among 10 issues, near the survey high of 27%, the NFIB said in its latest optimism survey.

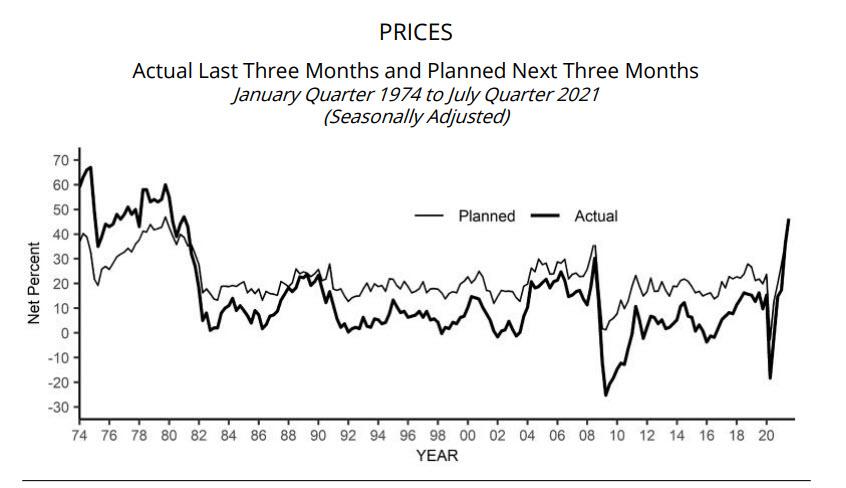

Last but not least, inflation is also impacting sentiment, with some 44% of businesses planning to increase prices in the next three months, which was unchanged from June’s record high reading.

In July, 52% of owners reported raising average selling prices, two points higher than June. Price increases in wholesale and retail trades posted significant declines. The largest increases in price-raising activity were in the non-professional services and transportation.

A net 46% of owners (seasonally adjusted) reported raising average selling prices. Unadjusted, 5% reported lower average selling prices and 52% reported higher average prices. Price hikes were the most frequent in wholesale (73% higher, 0% lower), manufacturing (61% higher, 6% lower), and retail (57% higher, 7% lower). Seasonally adjusted, a net 44% plan price hikes. This is inflation, the question is for how long?

Other key findings include:

- Sales expectations over the next three months decreased 11 points to a net negative 4% of owners.

- Owners expecting better business conditions over the next six months decreased eight points to a net negative 20%.

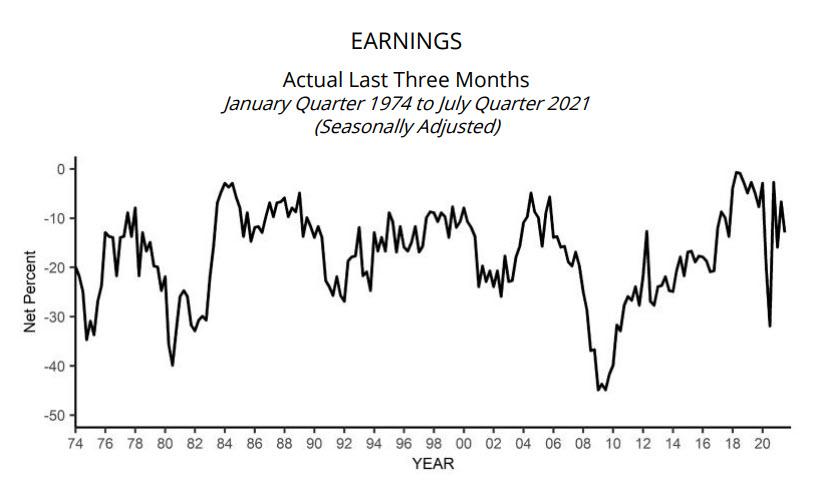

- Earnings trends over the past three months decreased eight points to a net negative 13%.

Fifty-five percent of owners reported capital outlays in the last six months, up two points from June but historically a below average reading. Of those making expenditures, 39% reported spending on new equipment, 23% acquired vehicles, and 14% improved or expanded facilities. Six percent of owners acquired new buildings or land for expansion and 11% spent money for new fixtures and furniture. Twenty-six percent of owners are planning capital outlays in the next few months. At some point, owners will have to step up capital spending to acquire and improve the quality of capital available to support new hires.

A net 5% of all owners (seasonally adjusted) reported higher nominal sales in the past three months, down four points from June. The net percent of owners expecting higher real sales volumes declined 11 points to a net negative 4%, a stubbornly negative view but based on their realities.

The percent of owners reporting inventory increases declined seven points to a net negative 6%. A net 12% of owners view current inventory stocks as “too low” in July, up one point from June and a 48-year record high reading. A net 6% of owners plan inventory investment in the coming months, down five points from June and also a historically high reading.

A net 38% of owners (seasonally adjusted) reported raising compensation, down one point from June’s record high of 39%. A net 27% plan to raise compensation in the next three months, up one point from June and a 48-year record high reading.

Lat but not least, the frequency of reports of positive profit trends declined eight points to a net negative 13%…

… the lowest level since March as small businesses are hit by margin compression.

Among those small employers reporting lower profits, 32% blamed weaker sales, 31% cited a rise in the cost of materials, 10% cited labor costs, 7% cited lower prices, 6% cited the usual seasonal change, and 3% cited higher taxes or regulatory costs. For owners reporting higher profits, 62% credited sales volumes, 20% cited usual seasonal change, and 7% cited higher prices.

Tyler Durden

Tue, 08/10/2021 – 10:50

via ZeroHedge News https://ift.tt/3sdMGuM Tyler Durden