“Only A Matter Of Time Before Developing-Market Stocks Unravel In An Unruly Manner” Tyler Durden

Mon, 05/25/2020 – 08:57

Authored by Marcus Wong, EM market strategist who writes for Bloomberg

Emerging-market equities are looking more fragile as valuations appear out-of-sync with earnings, especially given the increasingly bleak narrative surrounding virus cases and U.S.-China trade tensions. Something akin to a Jenga game nearing its end, with players wondering which move will be the one to bring everything crashing down.

EM valuations appear close to a historical pivoting point, given the MSCI gauge is more than 13 times forward earnings on a 12- month blended basis. The index corrected on four occasions over the past five years when valuations approached or breached that level.

Lofty S&P 500 valuations offer little reassurance for EM stocks, meantime. The outperformance in U.S. equities has been supported by unprecedented intervention from the Federal Reserve, especially via corporate bond buying. With the exception of rich emerging-nations such as South Korea, most developing-nation central banks have been less ambitious with stimulus, perhaps constrained by concerns for their currencies and perceptions of debt-monetization.

Investors continue to pull out from EM ETFs for a record 13th consecutive week, and the bulk of the cumulative $21.9 billion in outflows hit equity funds.

While new virus cases in the developed world have mostly stabilized, key developing nations are catching up. Brazil overtook the U.K. on May 18 as the nation with the third-highest number of virus cases globally. Russia is second only to the U.S., which still has the most coronavirus cases.

Poorer developing economies are dealing with an impossible dilemma — the trade-off between causing starvation and deepening poverty via lockdowns, versus allowing a wider outbreak for the pandemic. With lockdown fatigue setting in, more nations are opting to save people’s livelihoods — risking a resurgence of infections.

Although emerging-market currency volatility has eased, it is still close to the highest in almost 20 months compared to developed-market counterparts.

There is also the risk of rising emerging-market inflation due to food price risk, as my colleague Simon Flint points out. Developing nations are particularly vulnerable to the impact of nationwide lockdowns and border shutdowns, given to weaker food supply chains and a relative scarcity of cold- storage facilities.

Most observers expect another emerging-market stock sell-off this year, probably by September, according to a Bloomberg survey of 61 investors, strategists and traders conducted in April. And those questions were posed and answered before President Donald Trump escalated his war of words with China.

The re-emergence of U.S.-China trade tensions could not have come at a worse time, underscoring concerns that political rhetoric will heat up ahead of November’s U.S. elections. In the near term, China’s announcement of its intention to impose a new security law in Hong Kong has already resulted in threats of sanctions from the U.S. America is due to release a report on Hong Kong Human Rights on May 25.

With the drumbeat of negatives getting louder by the day, it may only be a matter of time before developing-market equities unravel in an unruly manner.

via ZeroHedge News https://ift.tt/2TB42l7 Tyler Durden

S&P Futures Jump, Global Markets Rise In Holiday-Muted Session Tyler Durden

Mon, 05/25/2020 – 08:16

US equity futures jumped in thin holiday volume, rising alongside European and Asian markets, and are now less than 20 points away from 3,000 having put the key resistance level of 2,950 in the rearview mirror, as investors cheered the reopening of more economies while ignoring the rapid deterioration in US-China relations which has put the fate of Hong Kong on the line. The dollar was flat despite the weakest yuan fixing in 12 years, while oil recovered modest overnight losses.

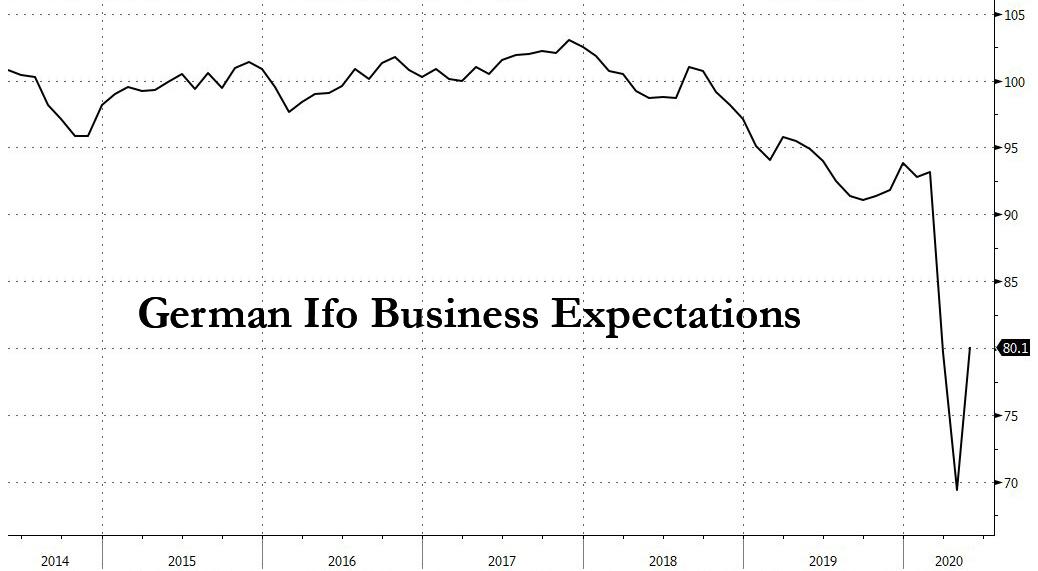

MSCI’s gauge of world stocks gained 0.32%. The pan-European STOXX 600 index climbed 0.8%, with European markets green across the board, after a survey showed German business morale rebounded in May, boosting optimism around economic re-openings, although caution prompted the dollar to snap a rare losing streak.

With nervous investors wary of adding to their equity holdings over concerns on what a post-lockdown world would look like, Germany’s Ifo institute survey for May gave some relief. Its expectations index rebounded strongly to 80.1, from 69.4 last month, beating expectations of 75.0, while the business climate index rose to 79.5 from a downwardly revised 74.2 in April, also higher than forecast, and fueling optimism about the outlook of Europe’s biggest economy after a drop in the first quarter.

“Today’s Ifo index echoes more real-time signals that economic and social activity has started to pick up significantly since the first lifting of the lockdown measures in late April,” ING economists said in a note. “In short, the low point of the slump should now be behind us and there even is the chance for a short-lived strong rebound in the coming months.”

Construction and healthcare shares led a broad advance in the Euro Stoxx Index, with Bayer AG jumping almost 9% after Bloomberg reported it reached agreements to resolve some cancer lawsuits over its Roundup weedkiller.

In Asia, the MSCI’s index of Asia-Pacific shares outside Japan was 0.3% higher on thin volume, as stocks gained led by industrials and health care, after falling in the last session. Hong Kong shares inched higher after Friday’s slump, following police clashes at the weekend with protesters marching against China’s move to crack down on dissent. All markets in the region were up, with Australia’s S&P/ASX 200 gaining 2.2% and Japan’s Topix Index rising 1.7%. The Topix gained 1.7%, with W-Scope and Showcase Inc/Japan rising the most. The Shanghai Composite Index rose 0.1%, with Danhua Chemical Technology and Beijing Sanyuan Foods posting the biggest advances

Contracts on all three major US indexes also rose, but with markets in Singapore, Britain and the United States closed for public holidays on Monday, market moves were relatively small and held within well-worn ranges. Emini futures gained 1%.

Volumes may be light with holidays in the U.S., U.K. and Singapore. Treasuries weren’t trading, and futures on the 10-year note were little changed. Elsewhere, bond markets were stable with Italy’s 10-year yield at 1.60%, just off six-week lows hit on Friday, and safe-haven German 10-year yields down 1 basis point at -0.50%.

In FX, China set its daily yuan reference rate at the weakest level since 2008 after the increasing acrimony drove the currency to a seven-month low on Friday. A benchmark of emerging-market stocks headed for its first rise in three sessions.

The bullishness in the stock markets contrasted with caution in currency markets, where the dollar ended a rare weekly loss to rise to a one-week high against its rivals in early trading, but has since given up much of the gains. The dollar gained after China’s move to impose a new security law on Hong Kong heightened concerns about the stability of the city and global trade prospects.

Traders were rattled on Friday when Beijing announced details of the security legislation, which critics see as a turning point for the territory. Sino-U.S. ties have worsened since the coronavirus outbreak, with the administrations of President Donald Trump and President Xi Jinping trading barbs over the pandemic, including accusations of cover-ups and lack of transparency.

“One big threat to the recovery in markets is the escalating war of words between the U.S. and China,” said Shane Oliver, head of investment strategy at AMP Capital Investors Ltd. in Sydney. Separately, “the main focus will likely remain on continuing evidence that the number of new Covid-19 cases is slowing in developed countries, progress towards medical solutions, the reopening of economies and signs that economic activity is picking up.”

“Rising tensions between the U.S. and China around Hong Kong, trade policy and who is responsible for the 2020 economic dislocation are threatening to end the post March-trough rally,” said Perpetual analyst Matthew Sherwood.

While fresh turmoil in Hong Kong is threatening to damage an already souring Sino-U.S. relationship, investors are looking to the reopening of economies from Japan to Australia and the U.S. to provide impetus to global stock markets, which have already priced in a successful reopening and then some.

In commodities, WTI rose 32 cents, or 1%, to $33.57 a barrel. Brent crude was up 9 cents, or 0.20% higher, at 35.14.

Top Overnight News

China’s Foreign Minister warned the US not to try and change China and said some Americans were risking a “new cold war”

Hong Kong protesters held their biggest rally in months following China’s dramatic move to crack down on dissent in the city as lawmakers are set to consider legislation that would punish anyone who disrespects China’s national anthem

China Investment Corp. is looking for more resilient assets as the nation’s $941 billion sovereign wealth fund seeks to boost long-term returns

Germany’s 9 billion-euro ($9.8 billion) bailout of Deutsche Lufthansa AG is being slowed by discussions meant to ensure the rescue plan receives swift European Union approval once it’s finalized, people familiar with the matter said. Bild am Sonntag reported earlier that Lufthansa would face a three- year deadline for repayment of the aid package to save the ailing airline

U.K. Prime Minister Boris Johnson put his own authority on the line as he fought to save his most senior aide Dominic Cummings in the face of growing demands to fire the adviser for allegedly breaking lockdown rules

The Japanese government was set to end its nationwide state of emergency by lifting the order for Tokyo, its surrounding areas and Hokkaido on Monday, allowing more parts of the economy to re-open as new coronavirus cases tail off

Asian equity markets began the week mostly higher following last Friday’s recovery on Wall St. where the US major indices gradually clawed back opening losses after encouraging comments from NIH’s Fauci and US plans for large Phase 2 trials, spurred vaccine-related optimism. ASX 200 (+1.5%) and Nikkei 225 (+1.5%) traded positive with tech and energy front running the broad gains seen across Australia’s sectors, while sentiment in Tokyo was underpinned by expectations the state of emergency will be lifted today in all remaining areas including the capital and with the government reportedly considering compiling a new package mostly consisting of financial support to companies which would be funded by a second supplementary budget valued more than JPY 100tln. Hang Seng (-1.0%) and Shanghai Comp. (Unch.) lagged their regional peers with the mainland bourse choppy amid ongoing US-China tensions and with the Hong Kong benchmark extending on last Friday’s near-6% slump after thousands of protester rallied on Sunday against China’s national security law, while the protests were met heavy handed by the police which used pepper spray and a water cannon to disperse the crowd. Finally, 10yr JGBs were marginally lower amid gains in Japanese stocks but with downside stemmed by the BoJ ‘s presence in the market for nearly JPY 1.1tln of JGBs mostly concentrated in 1yr-10yr maturities.

European bourses have kicked the week off on the front-foot after taking a positive lead from Asia. In the absence of UK and US participants, European indices initially eked out mild gains but sentiment picked up in recent trade (Eurostoxx 50 +1.1%) in spite of lingering tensions between US and China and ongoing concerns about an impending clash regarding the EU recovery fund with sentiment instead potentially lifted by a pick-up in reopening efforts across the continent. Sectors are higher across the board with outperformance seen in IT and industrial names, with performance for the latter bolstered by German heavyweight Bayer (+6.9%) after the Co. reportedly reached a verbal agreement regarding 50-85k of the 125k US Roundup lawsuits. Elsewhere, individual movers include Lagardere (+11.8%) with Co. shares boosted after French billionaire Arnault agreed to buy a stake in the Co., whilst Deutsche Lufthansa (+2.0%) shares have been supported amid ongoing hopes that the Co. can strike a deal with the German government and reports that the airline will resume more flights as of mid-June; something which has also provided a tailwind in the travel-space for Tui (+11.3%). Elsewhere, gains of over 2% for Renault were faded early doors (currently +1.1%) with the Co. and Nissan set to announce billions of USD in cost cutting measures this week, according to sources. Note, competitor Peugeot (+2.8%) has managed to maintain strength in early European trade as markets await details of support measures for the French auto sector that are due to be announced tomorrow.

In FX, the G10 underperformers thus far in holiday-thinned volumes as the Single Currency eyes a roadblock regarding the EU Recovery Fund – with the “frugal four” (Austria, Denmark, Netherlands, and Sweden) countering the Franco-German proposal of grant distributions. The perceived hawks call for loan allocations – a drawback for peripheries Italy, Spain, and Greece (among others) – with the former also facing a potential rise in domestic anti-Euro sentiment. EUR/USD breached Friday’s 1.0885 low which coincide with the 10DMA to a current low of 1.0871, having briefly dipped below its 21DMA at 1.0873. Further levels to the downside include a Fib at 1.0864 (61.8% of the 1.0775-1.1008 move) ahead of the psychological 1.0850. Unrevised German GDP finals and an overall mixed Ifo survey did little to shift the narrative. Option expiries see EUR 550mln at 1.0875-85, 800mln at 1.0895-1.0900, and EUR 1bln rolling off between 1.0910-20. The Franc meanwhile sees safe-haven outflows, albeit to a greater extent vs. its Japanese counterpart as EUR/CHF revisits support around the 1.0575 area.

DXY, CNY, HKD – The broader Dollar and Index initially extends on overnight gains before pulling back, with support also derived from the heavy EUR basket contribution. DXY inched higher towards 100.000 (vs. low 99.716) to the upside with its 50DMA residing nearby at 100.02. Elsewhere, the Yuan remains on the backfoot amid heightened US-Sino tensions, coupled with international backlash for Mainland’s crackdown on anti-govt Hong Kong behaviour. Further, the PBOC set the weakest CNY fixing since 2008 (7.1209 vs. Prev. 7.0939) following Friday’s losses. HKD meanwhile unsurprisingly experienced weakness but USD/HKD sees itself just above the bottom end of the 7.75-7.85 peg.

GBP, CAD – The marginally better performers ex-USD, but action remains minimal in thin conditions. Cable overnight remained restricted under 1.2200 as PM Johnson was said to face Cabinet revolt after supporting senior adviser Cummings who faced calls to resign after breaching the lockdown – potentially leading to Cabinet dissent and citizens disobeying lockdown rules. Brexit developments have also remained in focus amid the diminishing timeframe to hammer out an FTA by year-end. Weekend developments noted that the UK is in a fresh stand-off with the EU regarding delays in granting diplomatic status to the EU’s representation in London. Furthermore, relations with China should be watched over the Hong Kong developments – with PM Johnson reportedly looking to reduce Huawei’s involvement in UK 5G network within the next three years. Cable resides towards the bottom of the current 1.2162-91 intraday band, ahead of a 61.8% Fib of last week’s bounce coinciding with Friday’s low ~1.2160. The Loonie meanwhile tracks price action in the US energy benchmarks. USD/CAD resides just south of 1.4000, having earlier tested resistance at its 21DMA at 1.4007 (intraday high).

AUD, NZD – Antipodeans tracked the weakness in the Yuan as tensions with China remain elevated and with the US-Sino spat also providing less basis to join in on global lockdown easing optimism/vaccine hopes. AUD/USD drifted off session lows ~0.6520 (vs. high 0.6550) amid a pullback in the DXY, with the 100 and 21DMAs both residing at 0.6490. The Kiwi meanwhile fares modestly worse as the AUD/NZD cross found a current base at 1.0700. NZD/USD meanwhile sees itself just under 0.6100 (vs. high 0.6108) but threatening Friday’s low at 0.6079.

JPY – Modest losses for the Japanese currency, albeit more-so a function of the firmer Buck. Reports noted that Japan is to lift the state of emergency declaration in Tokyo, Kanagawa, Saitama, and Hokkaido today. USD/JPY sees itself hovering on either side of its 55 DMA (107.71) vs. its overnight low at 107.54 and ahead of its 50 DMA at 107.91..

In commodities, WTI and Brent front month futures see mild gains in early trade with traded volumes on the lighter side amid absences from UK and US markets/participants; while fresh fundamental news flow remains light. Eyes remain on the wider implications on global trade and sentiment from the fallout of the US-Sino trade spat threatening a cold war, whilst investors must not be distraction from the prospects of reinstated lockdowns should COVID-19 cases rise again. On Friday, the Baker Hughes rig count printed another decline in active rigs, whilst OPEC Secretary General Barkindo posited tentative signs of recovery and we believe the worst is behind us. WTI July meanders around USD 33.50/bbl (USD 32.50-33.75/bbl range), whilst Brent July sees itself oscillating between gains and losses, now residing north of USD 35/bbl (34.50-35.40 range). Spot gold moves in tandem to the Buck as sees itself with mild intraday losses around USD 1730/oz (USD 1724-35 band) whilst copper mimics price action in stocks to reclaim USD 2.40/lb to the upside.

US Event Calendar

The US us closed for Memorial Day holiday

via ZeroHedge News https://ift.tt/2X1n3Py Tyler Durden

Many analysts and economists are trying to predict the shape of the economic recovery post-Covid 19. To understand how the recovery may look like, we need to look at past recoveries and at the history of pandemics.

Starting with the pandemic, we know a few things.

First, there has never been a vaccine for any of the previous 18 Covid types.

Second, there has never been a pandemic without a second wave before a treatment existed.

Taking both things into account, the idea that many investors have that the worst is discounted may be overoptimistic.

If we look at the past three decades of recoveries after a crisis, we can see that the last three recoveries have been weaker, with less productivity, a lower rise in real wages, and poorer investment growth than the previous three.

We may even say that the recovery from the 2008 crisis was already clear evidence of an L-shaped bounce, where some economic areas, like the eurozone, did not see something resembling a full recovery until 2016. In the case of the United States, the weak labor force participation rate and stale real wage growth with poor investment growth was a constant problem until 2017.

The signs of an L-shaped return to normal post-Covid-19 are starting to appear. In China, most sectors are posting disappointing levels of return to normality, and if we exclude those sectors -like cement- that are driven by government building and state-owned enterprises producing to build inventories, the recovery is clearly very far away from V-shaped.

It is true that this crisis is different than the previous ones. This is a supply shock followed by the forced shutdown of an economy by government decree. However, this is precisely what makes the recovery more challenging. In previous crises, even in the downturn there were sectors that were doing well and growing at double-digit rates. This crisis has hit almost every sector and generated a level of unemployment that is unprecedented in recent history. Such a massive increase in unemployment in so little time makes the recovery more difficult, because the shock to consumers has been enormous, and most may not decide to return to the previous levels of spending even if their job comes back.

If this crisis has told us anything is that even the most bearish have been too optimistic.

Shutting down an economy even for an apparently short period of time has massive long-term implications in solvency ratios that will not be addressed with liquidity. Businesses are collapsing at record pace and even the largest and safest multinationals will see their debt levels soar only due to the fall in profits.

JP Morgan estimates that 2021 will still show a level of corporate profits that will likely be 20% below the 2019 level. This disproves the V-shaped recovery and bullish arguments about most stocks, but also proves that even investment banks, who always provide reasonably optimistic estimates looking at a benign scenario, are pushing back the recovery to 2022.

Jerome Powell has also signaled that the U.S. recovery will not start until the end of 2021 and, like investment banks, if we have learnt anything from the Federal Reserve is that their estimates tend to be diplomatic and generally optimistic. Investors cannot assume that Fed and investment bank predictions are too negative because history proves the opposite is true.

In a recent email to clients, Deutsche Bank mentioned that it takes around 22 days to shut down an economy almost entirely and between four and ten times that time to get it back on track. Considering that 75% of job losses have come from the services sector (travel and leisure, education, health, and professional services), it is also safe to assume that the jobs recovery will be very slow, considering the loss in the number of businesses and the weak response from consumers in the return to activity, as wages are unlikely to rise and households will likely try to save as much as they can to prepare themselves for another shock.

Central banks cannot print jobs.

The biggest problem in this crisis is that the massive stimuli is driven to incentivize a demand that may not come back and, as such, generate further overcapacity in indebted and overinvested sectors. Central banks and governments are bailing out the past and letting the future die.

The massive bail out of indebted sectors that already had overcapacity and were in process of obsolescence may also drive the largest wave of malinvestment in decades. If the previous recoveries came with poor wage and capital expenditure growth and high debt, the next one will likely be even worse.

Recent history tells us that L-shaped recoveries are not an anomaly, but the norm. This one may not be different.

via ZeroHedge News https://ift.tt/3edzlKH Tyler Durden

Americans Are Rushing To Book Vacations In Re-Opened States Tyler Durden

Mon, 05/25/2020 – 05:45

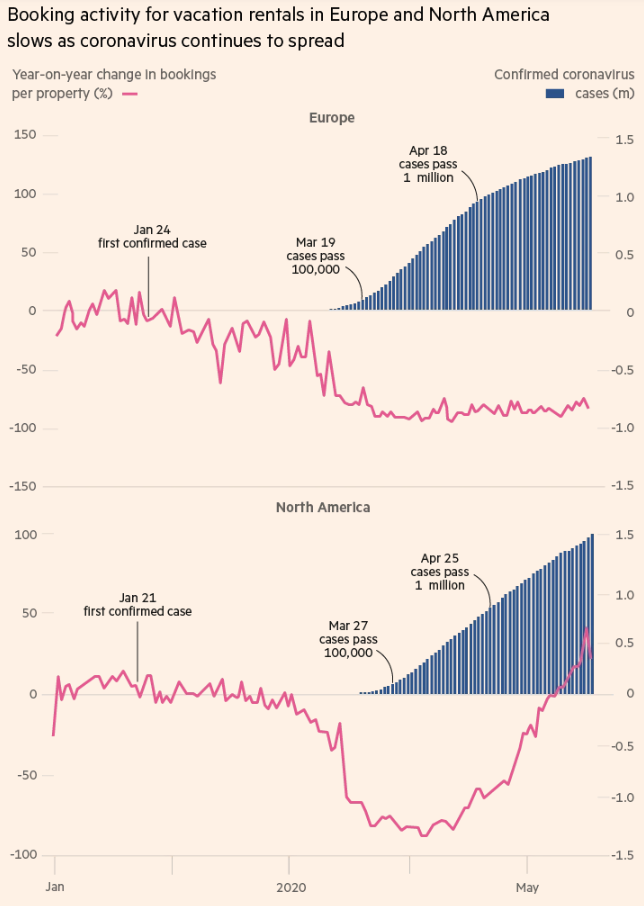

Demand for vacations has seen a meaningful uptick this month, offering the first sliver of hope for the tourism and hospitality industry in months.

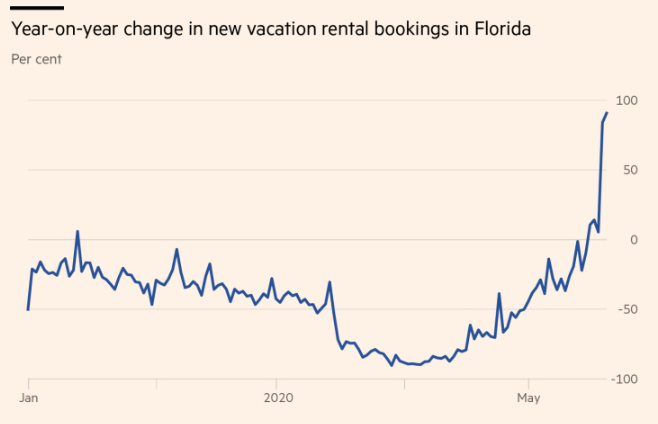

Ahead of the Memorial Day weekend, vacation homes in places like Florida and Georgia, where states are starting to re-open, are also starting to open up. New rental bookings had started to recover in early May and are now 90% higher than a year ago in Florida, according to the Financial Times.

Georgia and Alabama are also starting to see upticks in booking, highlighting that those with the financial means are eager to get out of the house and start their summer vacations. Meanwhile, the U.S. jobless rate is expected to approach 20% this month.

The Florida number suggest a favorable leading economic indicator, FT says. Some of these rentals are set for the next 30 days, which stands at odds with how people usually book summer vacations: well in advance. Jason Sprenkle, chief executive of Key Data Dashboard said: “Over the last week, the demand for vacation rentals across the US has seen a huge increase, now surpassing the demand for this same period last year.”

Hotels and rentals are doing their part, too, loosening cancellation policies to entice more business and adapt to the environment.

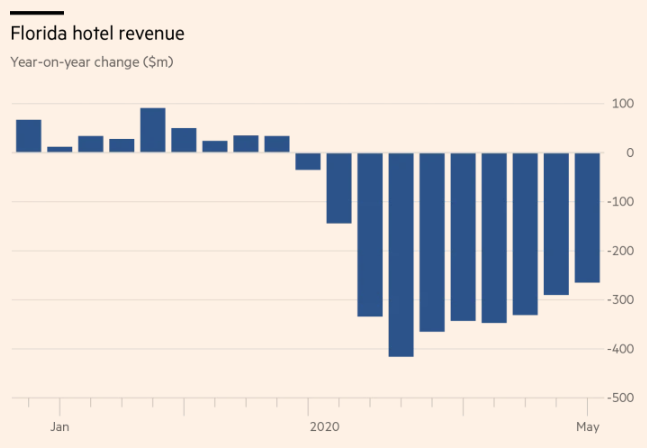

The uptick is also good news for the states, as taxes from these rentals can be a large revenue source for states. For example, in 2019, Airbnb collected $137 million in taxes for Florida, which was up from $86 million the year prior. In 2018, Florida saw a total of $16.6 billion in direct spending for vacation home rentals, which accounted for about 1.6% of the state’s GDP. About 11% of tourists stayed in vacation rental homes in 2018.

Hotel revenues were still down about 74% for the week ending May 16, however, and not all states have seen rental bookings recover. Hawaii, for example, has still not recovered from its April lows due to a lack of air travel. California has also seen new rental books below totals for May 2019, despite a small rebound.

Vince Perez, a property manager and rentals software provider in California said: “The guests are angry about the lockdowns.”

He concluded: “If you are in a destination leisure market and you are outside the cities, you are going to see — and you are seeing — an uptick in bookings.”

via ZeroHedge News https://ift.tt/36wPIzs Tyler Durden

The Greek government recently accused Turkey of seizing some of its territory along its eastern border.

Turkey responded on Saturday by stating that it would not allow de facto borders after Athens complained to Ankara that Turkish forces had seized land at the course of the Evros River that separates the two countries.

Clashes involving refugees/migrants at Turkey’s Pazarkule border crossing with Greece’s Kastanies, near Edirne, Turkey in prior months, via Reuters.

A statement by the Turkish Foreign Ministry said, “Ankara informed Greece that the river course has changed significantly for natural and artificial reasons, since 1926 when the borders were established, and that the solution requires technical coordination.”

Turkish troops have invaded and occupied a small patch of Greek land Greece on their contested border.

Around 35 soldiers marched on to a floodplain site on the east bank of the River Evros at Melissokomeio yesterday.

Turkish soldiers and police special forces now have a solid presence within the Greek territory and have camped in the pocket of Apiary at Feres, reports Greek site Army Voice.

At the camp there is now a small Turkish flag flying from a tree. Troops have rejected Greek demands to withdraw. It comes weeks after thousands of Syrian refugees failed to break through into Greece.

Via The Daily Mail

The Turkish ministry said, “The dispute can be resolved through talks between the technical delegations of the two countries, which is a proposal submitted by Ankara to Athens, adding,” We will not allow any form of de facto on our borders.”

For his part, Greek Foreign Minister Nikos Dendias said last Wednesday that “the course of the river has changed”, indicating that there was tension between the two countries for this reason.

Greek media reported on Friday that Turkish forces occupied a piece of land that is usually submerged in water at this time of the year, located on the Greek side of the border.

via ZeroHedge News https://ift.tt/3gjrHA5 Tyler Durden

Credit Suisse Is Preparing For Layoffs As CEO Admits “Something” Needs To Change Tyler Durden

Mon, 05/25/2020 – 04:35

And the banking layoffs have begun…

Credit Suisse is leading the charge, revealing this week that the investment bank will need less employees on the other side of the coronavirus crisis as a result of lower growth and looming credit defaults.

The popularity of online banking has also reduced the need for branches, CEO Thomas Gottstein said. The company’s staff could work remotely for 10% to 20% of the time and the bank also anticipates needing less office space, Gottstein predicted, according to the Business Times.

The bank is looking at streamlining “many processes,” he said, likely trying to come up with a nice way to say “we’re firing every single non-essential worker in the middle of a global pandemic that we can find.”

Meanwhile banks in Europe are pre-occupied with dealing with a NIRP environment, an oversupply of banking services and looming uncertainty on client loans as a result of the global economy grinding to a halt. What was once an optimistic outlook for the sector for the year has now become a focus on a long and tedious road to post-pandemic recovery.

A margin loan provided to the billionaire founder of Luckin Coffee helped exacerbate the company’s Q1 loan loss provisions, yet Gottstein says high net worth business in Asia remains an area for growth.

Gottstein also said the bank “needs to change something” at its investment banking unit, which has been generating losses for several quarters.

Our guess is that the something that needs to change is the division’s number of employees.

via ZeroHedge News https://ift.tt/3gk1PV2 Tyler Durden

Little has been made of Brexit since the UK ceremoniously left the EU on January 31st and entered into a transition period. Amidst the coronavirus outbreak, multiple rounds of negotiations on the future trading relationship have taken place, with round three having culminated earlier this month.

Rounds one and two yielded no tangible progress. The third instalment was a similar story.

The major obstacle is the EU’s insistence on including a set of novel and unbalanced proposals on the so-called “level playing field” which would bind this country to EU law or standards, or determine our domestic legal regimes, in a way that is unprecedented in Free Trade Agreements and not envisaged in the Political Declaration. As soon as the EU recognises that we will not conclude an agreement on that basis, we will be able to make progress.

Frost labelled the EU’s position as an ‘ideological approach‘, one that must change by the time the fourth round of talks begin on June 1st.

The EU’s lead negotiator, Michel Barnier, countered Frost’s perspective by declaring that ‘without a level playing field there will be no economic and trade partnership agreement.’

To make progress in this negotiation – if it is still the United Kingdom’s intention to strike a deal with the EU – the United Kingdom will have to be more realistic; it will have to overcome this incomprehension and, no doubt, it will have to change strategy.

In the public eye negotiations are deadlocked. Both sides are insisting that the other must change course with just six months of the transition period remaining. As part of the withdrawal agreement, Britain has the option of requesting an extension to the transition, but must do so by the end of June. Failure to do so will mean that if a new trading relationship is not ratified by the end of the year, the UK and EU will trade on World Trade Organisation terms come the start of 2021, a consequence of which will be higher tariffs.

But extending the transition is not as straightforward as just asking for more time. When the withdrawal agreement became law, the government also wrote into legislation that the transition could not be extended beyond this year. To go back on this, Boris Johnson’s administration would have to repeal a law that they themselves devised and put into place.

As Britain was preoccupied with Covid-19 lockdown measures, IMF Managing Director Kristalina Georgieva (who supported ratification of the withdrawal agreement) took the opportunity to effectively recommend that the transition period be extended if the UK and EU fail to agree terms in the short term.

My advice would be to seek ways in which this element of uncertainty is reduced in the interests of everybody, the UK, the EU, and the whole world.

I am very concerned about how little time we have. It seems to me that, on both sides, we should seriously consider whether the negotiations are feasible in such a short time.

I think it would be reasonable to take stock in the middle of the year and if necessary, agree on an extension to the transition period.

As it stands, there is no sign that the government will roll back on their own legislation. An indication of this came immediately after Kristalina Georgieva’s intervention, when the Prime Minister’s spokesman told the media that extending the transition past 2020 would ‘keep us bound by EU legislation at a point when we need legislative and economic flexibility to manage the UK response to the coronavirus pandemic‘.

We will not ask to extend it. If the EU asks we will say no. Extending would simply prolong negotiations, create even more uncertainty, leave us liable to pay more to the EU in future, and keep us bound by evolving EU laws at a time when we need to control our own affairs. In short, it is not in the UK’s interest to extend.

Here is where Brexit and Covid-19 begin to converge. Last week it was announced that government borrowing for the month of April, all in response to the Coronavirus, came to £62.1 billion. By comparison, borrowing in April 2019 amounted to £10 billion. The untold pressure on public finances has reinforced the government’s position of not seeking any extension to the transition period. The prevailing narrative now is that the country can no longer continue paying into the EU budget at a time when all economic resources need to be concentrated into responding to Covid-19.

Leaving the EU with no new trading agreement has been made more likely because of the financial fallout of the pandemic.

You might expect then that with negotiations floundering, those who pushed for a second referendum on the withdrawal agreement would now be campaigning for the transition to be extended. Whilst some on the margins of British politics are doing that, one significant figure has stopped short of calling for more time. His name is Keir Starmer, leader of the opposition Labour party and member of the elitist Trilateral Commission.

Starmer first appeared on the membership list of the Trilateral Commission in 2018. According to the latest list, dated January 2020, Starmer remains a member. Out of 650 members of parliament, Starmer is the only one directly affiliated with the Commission. Coincidentally or not, he now has an elevated platform within both the political and media spheres.

The government says it’s going to get negotiations and a deal done by the end of the year. I’ve always thought that’s tight and pretty unlikely, but we’re going to hold them to that and see how they get on. They say they’re going to do it.

I would seek to ensure that the negotiations were completed as quickly as possible. I’ve not called for a pause because the government says it’s going to get it done by the end of the year. So let’s see how they get on.

At this point Nick Ferrari interjected, and suggested Starmer was communicating mixed messages. ‘Are you riding both horses there?‘ asked Ferrari. ‘With respect you’re saying you don’t think it’s practical but then you wouldn’t press pause.’

Starmer replied by saying:

I don’t think it’s practical but we’re a long way from December so we’ll see how we get on. But the government has said we can do it within the 12 months, so let’s see.

Keir Starmer is the man who after many months of prevaricating on the subject came out in support of a second EU referendum, pledging support for staying in the bloc. But now as leader of the opposition, and with the likelihood of a no deal scenario in December having grown, Starmer is not only reluctant to extending the transition period but is willing to watch the government arrive at a situation where they can walk away from negotiations in the autumn and move onto WTO terms. Parliament would have no authority to block this from happening should the time come.

The moment to ramp up pressure for an extension to the transition period is now. The window for extension will be closed in just five weeks time. Yet Starmer sits on his hands.

Keep in mind also that the threat of WTO terms with the EU was one of the reason why Starmer originally came out in favour of remaining in the union. That threat has not gone away. Starmer appears quite relaxed about the little time that remains. He seems as equally relaxed about allowing Boris Johnson’s government to fall on their own sword over Brexit rather than seek to delay the process further.

For reasons I won’t get into here, I have detailed over the past few years why I believe a ‘hard‘ Brexit scenario benefits global planners. From the evidence I have researched, Brexit has less to do with maintaining the EU status quo at all costs and more about jeopardising pound sterling’s role as a reserve currency. Sterling remains highly sensitive to Brexit developments, and has not recovered from the devaluation seen in the aftermath of the referendum in 2016.

Moves towards a digital currency framework have gained traction over the past four years, to the point where last summer former governor of the Bank of England Mark Carney went on the record as saying that the dollar could eventually be replaced as the world reserve currency by a digital alternative.

The global elite regularly push in their communications the necessity for reforming the ‘architecture‘ of the financial system. What they mean by this is a transition into an all digital construct. To achieve this the current composition of fiat currencies, led by the dollar as well as sterling, will need to be radically changed. This is part of a longer term agenda that ties in with the UN’s sustainable development goals.

In the immediate term we are left with one question: Will the UK renege on their pledge not to extend the transition period? I would say not. I have believed for a while that whatever the end outcome on Brexit, it will be brought about by a political decision made out of the UK. Global figureheads and commentators alike will say that Boris Johnson had the chance of preventing the imposition of a WTO exit, at a time when the UK is attempting to ‘re-open‘ its economy and repair the damage done to supply chains since the onset of Covid-19.

The EU will continue to offer Britain the opportunity to extend negotiations over the next few weeks, which in turn will largely absolve them of responsibility for the economic fallout of a WTO exit at the end of the year.

Contrary to what some may believe, coronavirus has not made Brexit immaterial. Taken together, Covid-19 and a WTO Brexit are a harbinger for a significant spike in inflation over the coming years.

As the economic devastation brought about by the self imposed lockdown becomes more profound, a WTO Brexit will only compound matters, and put further downward pressure on sterling as a result.

via ZeroHedge News https://ift.tt/2ZxOx12 Tyler Durden

The key takeaways of the Two Sessions of the 13th National People’s Congress in Beijing are already in the public domain.

In a nutshell: no GDP target for 2020; a budget deficit of at least 3.6% of GDP; one trillion yuan in special treasury bonds; corporate fees/taxes cut by 2.5 trillion yuan; a defense budget rise of a modest 6.6%; and governments at all levels committed to “tighten their belts.”

The focus, as predicted, is to get China’s domestic economy, post-Covid-19, on track for solid growth in 2021.

Also predictably, the whole focus in the Anglo-American sphere has been on Hong Kong – as in the new legal framework, to be approved next week, engineered to prevent subversion, foreign interference “or any acts that severely endanger national security.” After all, as a Global Times editorial stresses, Hong Kong is an extremely sensitive national security matter.

This is a direct result of what the Chinese observer mission based in Shenzhen learned from the attempt by assorted fifth columnists and weaponized black blocs to nearly destroy Hong Kong last summer.

No wonder the Anglo-American “freedom fighter” front is livid. The gloves are off. No more free lunch. No more paid protests. No more black blocs. No more hybrid war. Baba Beijing’s got a brand new bag.

The three threats

It’s absolutely essential to position the Two Sessions within the larger, incandescent geopolitical and geoeconomic context of the de facto new Cold War – hybrid war included – between the US and China.

This is as clear cut as it gets in terms of how the “free world,” in Pentagonese, perceives the rise of China. Call it the view of the industrial-military-surveillance-media complex.

Beijing, per McMaster, is pursuing a policy of “co-option, coercion and concealment,” centered on three axes:

Made in China 2025;

the New Silk Roads, or Belt and Road Initiative;

and a “military-civil fusion” – arguably the most “totalitarian” vector, centered on creating a global intel network in espionage and cyber-attacks.

Call these the three threats.

Whatever the spin across the Beltway, Made in China 2025 remains alive and well – even if the terminology has been skipped.

The target, to be reached via $1.4 trillion in investments, is to profit from the knowledge accumulated by Huawei, Alibaba, SenseTime Group and others to design a seamless AI environment. In the process, China should be reinventing its technological base and restructuring the entire semiconductor supply chain to be domestic-based. These are all non-negotiables.

Belt and Road, in Pentagonese, is synonymous of “economic clientelism” and a “ruthless debt trap.” But McMaster gives away the game when he describes the cardinal sin as “the goal of displacing the influence of the United States and its key partners.”

As for the “military-civil fusion,” in Pentagonese, that’s all about fast tracking “stolen technologies to the army in such areas as space, cyberspace, biology, artificial intelligence and energy.” It amounts to “espionage and cyber-theft.”

In sum: “pushback” is essential against those China’s commies becoming “even more aggressive in promoting its statist economy and authoritarian political model.”

Chinese diaspora speaks

Apart from this binary, quite pedestrian assessment, McMaster does make an interesting point:

“The US and other free nations should view expatriate communities as a strength. Chinese abroad – if protected from the meddling and espionage of their government – can provide a significant counter to Beijing’s propaganda and disinformation.”

So let’s compare it with the insights of a true master in Chinese diaspora: the redoubtable professor Wang Gungwu, born in Surabaya in Indonesia, who will be 90 years old this coming October and is the author of a delightful, poignant book of memoirs, Home is Not Here.

For outsiders there’s no better explanation of the predominant frame of mind across China:

“At least two generations of Chinese have learnt to appreciate that the modern West has valuable ideas and institutions to offer, but the turmoil of much of the 20th century has also made them feel that the Western European versions of democracy might not be that important for China’s national development. The majority of Chinese seem to approve of policies that place order and stability above freedom and political participation. They believe that this is what the country needs at this stage and resent being regularly criticized as politically unliberated and backward.”

Wang Gungwu stresses how the Chinese think quite differently from the “universalist” trajectory of the West, and thus reaches the heart of the matter:

“Should the PRC succeed in providing an alternative route to prosperity and independence, the US (and elsewhere in the West) would see that as a fundamental threat to its (and Western European) dominance in the world. Those who feel threatened would then do everything they can to stop China. I think this is what most Chinese believe is what American leaders are prepared to do.”

No US Deep State assessment can possibly stand when ignoring the wealth of Chinese history:

“The nature of China’s politics, whether under emperors, warlords, nationalists or communists, was so rooted in Chinese history that no individual or group of intellectuals could offer a new vision that could appeal to the majority of the Chinese people. In the end, that majority seemed to have accepted the legitimacy of PRC’s victory on the battlefield coupled with the capacity to bring order and renewed purpose to a rejuvenated China.”

Remixed long telegram

Federal prosecutor Francis Sempa, author of America’s Global Role and an adjunct professor of political science at Wilkes University, has compared McMaster’s assessment of the China “threat” to the legendary “long telegram” written by George Kennan in 1947, under the pseudonym X.

The “long telegram” designed the subsequent strategy of containing the Soviet Union, complete with the building up of the North Atlantic Treaty Organization. It was the prime Cold War blueprint.

The current, pedestrian long telegram remix might also have long legs. Sempa, to his credit, at least admits that “McMaster’s timid policy recommendations will not lead to the gradual break-up or mellowing of Chinese Communist power.”

He suggests – what else – “containment,” which should be “firm and vigilant.” And he recognizes, to his credit, that it should be “based on an understanding of Chinese history and Indo-Pacific geography.” But then, once again, he gives away the game – in true Zbigniew Brzezinski fashion: what matters most is “the need to prevent a hostile power from controlling the key power centers of the Eurasian landmass.”

It’s no wonder the US Deep State identifies Belt and Road and its spin-offs such as the Digital Silk Road and the Health Silk Road across Eurasia as manifestations of a “hostile power.”

The whole fulcrum of US foreign policy since WWII has been to prevent Eurasia integration – now actively pursued by the Russia-China strategic partnership. New Silk Roads across Russia – part of Putin’s Great Eurasia Partnership – are bound to merge with Belt and Road. Putin and Xi will meet again, face-to-face, in mid-July in St. Petersburg, for the twin summits of BRICS and the Shanghai Cooperation Organization, and will further discuss it in extensive detail.

So presiding, in silence, over the Two Sessions, is the understanding by the Chinese leadership that getting back to domestic business, fast, is essential for a renewed push on the grand chessboard. They know the industrial-military-surveillance-media complex will pull no punches to deploy every possible geopolitical and geoeconomic strategy to sabotage Eurasia integration.

Made in China 2025; Belt and Road – the post-modern equivalent of the Ancient Silk Road; Huawei; China’s manufacturing pre-eminence; breakthroughs in the fight against Covid-19 – everything is a target. And yet, in parallel, nothing – from a remixed long telegram to stale ruminations on the Thucydides Trap – will derail a rejuvenated China from hitting its own targets.

via ZeroHedge News https://ift.tt/3gmpaFg Tyler Durden

Get Ready For Disinfected Dice As Vegas Plans Reopening Tyler Durden

Sun, 05/24/2020 – 23:00

Nevada’s gaming industry could reopen as soon as June 4, Gov. Steve Sisolak stated Friday. The Nevada Gaming Control Board will meet next week with health officials to determine which sanitation protocols are needed at casinos before reopening.

“The board is firmly aware of its statutory duty to protect the public health and welfare of the Silver State’s citizenry while allowing the gaming industry to flourish through strict regulation,” Sisolak said in a statement.

Additionally, the Gaming Control Board will meet Tuesday & will consider any action necessary with regard to reopening. Pending the evaluation of trends in our data and results of this meeting, I have set a target date of June 4, 2020, for reopening Nevada’s gaming industry.

Casinos are expected to submit reopening safety plans to the board next week. When gamblers step inside the casino floor, they will be immediately greeted by staff and screened at temperature check stations. All employees and patrons will be required to wear masks. Table games will have reduced capacity, for instance, there could be three players per blackjack table instead of six. Also, one could expect sanitation stations across the entire property — a move to limit the spread of the virus.

While playing games, dice will be disinfected between shooters, chips, and cards will be routinely swapped out. Resort guests at some casinos will go all-digital via their smartphone — this means phones will be used for touchless check-in, used as room keys, and even used to read menus at the facility’s restaurant(s).

“You’re going to see a lot of social distancing,” Sean McBurney, GM at Caesars Palace, told AP News. “If there’s crowding, it’s every employee’s responsibility to ensure there’s social distancing.”

Wynn Resorts properties and The Venetian will deploy thermal cameras on gaming floors to intercept people with feverish conditions.

Bill Hornbuckle, CEO and president of MGM Resorts International, said his company is losing $10 million per day during the shutdown. He said only 2 of its 10 Strip properties would open first: Bellagio and New York-New York.

Hornbuckle said because of social distancing and new rules, and there will be a lot “fewer people, by control and by design” in his casinos.

Caesars Entertainment is expected to reopen Caesars Palace and the Flamingo Las Vegas, then Harrah’s Las Vegas and the casino floor at The LINQ hotel-casino.

Robert Lang, executive director of the Brookings Mountain West, a think tank at the University of Nevada, said large crowds are not expected to return quickly to the Vegas strip.

Lang is correct, just like the airline industry – which Boeing CEO’s Dave Calhoun recently warned air travel growth might not return to pre-corona levels for several years – the same should be noted for Vegas.

With Vegas imploded, and 1 in 3 jobs in the state tied to the resort industry, Nevada’s unemployment rate has jumped to almost 30% in nine weeks, the worst-ever unemployment rate in state history and the highest in the country.

Getting back to normal, or merely revisiting 2019 growth rates, for the Vegas casino industry and or the economy as a whole, will take several years or more.

via ZeroHedge News https://ift.tt/2zrsoqz Tyler Durden

China Sets Yuan Fix At Weakest Since 2008 Tyler Durden

Sun, 05/24/2020 – 22:32

Just hours after China’s Foreign Minister Wang Yi warned that “some” in America were pushing relations to a “new Cold War”, Beijing made it clear how it intends to retaliate in this new paradigm: by doing the one thing that infuriates Trump more than anything, devaluing its currency.

After the PBOC fixed the yuan at 7.0939 on Friday, the PBOC set the Monday USDCNY midpoint at 7.1209, which was not only weaker than the expected fix of 7.1205 but the weakest fixing since 2008.

Zooming in on the past 10 days shows the sharp bounce in the past three days in both the fixing, the onshore and the offshore yuan, the last of which is now just shy of the lows hit during the March crash, if still below the all time lows hit on Sept 2, 2019 when the USDCNH spiked as high as 7.1940 in response to the escalating trade war.

That said, some – such as Bloomberg – had a different expectation for the fixing, which they saw as 7.1220, which would in turn mean a stronger than expected fixing, and one suggesting that the PBOC has activated its countercyclical buffer to slow the drop of the onshore yuan as the offshore yuan slumps. Their conclusion, which is counter to sellside expectations, is that this marks a shift in the PBOC’s countercyclical adjustments and “could be seen as a warning shot toward speculators betting on a weaker yuan.”

Whether Bloomberg’s fixing model is correct, or consensus expectations for a stronger fix are right, remains to be seen however if indeed it is China’s stance to devalue the yuan in response to the sharp deterioration in Sino-US relations then expect the offshore yuan to take the lead and to keep sliding, giving the PBOC cover for further devaluation and telegraphing how it plans on responding to the “cold war” and any future escalations by the US.

Ironically, the very same Bloomberg, in a different report, notes that “the spread between spot USD/CNH and USD/CNY is likely to become more volatile in coming days, driven by a widening bias. A combination of U.S.-China political tension and unrest in Hong Kong will provide a negative feedback loop into the offshore yuan.”

The PBOC can be expected to maintain a tight grip on the daily yuan fixing and enforce the 2% fluctuation range. But there is no such constraint for the offshore yuan, which is free to roam, only being pulled back into line by FX arbitrageurs or in response to speculation about central bank intervention.

As author Mark Crankfield writes, “the CNH forwards curve can also be expected to see an upward trajectory. The spread spiked to more than 10 big figures several times during previous periods of yuan turbulence. A similar outcome is likely in the near term, as investors consider what the threat of a new cold war will mean for risk assets.“

One thing to note: the last time the offshore yuan was here, the S&P was at 2,300.

Finally, here is a reminder from Rabobank’s Michael Every why in the current environment of escalating hostility between the US and China, the only thing that matters is the Yuan, and why in the not too distant future, the Chinese currency may have a 10-handle in front of it.

This time last year, when we were all still going abroad regularly (right now just ‘outside’ is becoming a psychological barrier if I am honest) I was traveling with a presentation titled “Clause is Cause”. This argued that from a geostrategic ‘Von Clausewitz’ perspective, not a neoliberal “Let’s assume world peace” version, the US would at some point realise the USD/Eurodollar was a weapon it could wield vs. China, and when it did we would see three key strings cut: trade; tech; and then capital flows. The first was evident during the trade war – which has not been concluded is likely to get far worse soon; the second is also abundantly clear on a variety of fronts, much to Silicon Valley’s chagrin; and potentially, now we see the start of that third step – because if the US does block this first USD50bn going in, other such steps will follow, just as they did on the previously unthinkable idea of US tariffs on China.

CNH is right to be selling off, albeit in a traditionally limited fashion, because if you don’t buy from China and you don’t help China up the value-chain and you don’t invest in China then China is not going to be getting much USD liquidity at all. The US hawks probably don’t get the Eurodollar iron logic there; they are likely just pressing buttons in anger. The outcome would be the same nonetheless.

I can hear the market bulls and technocrats of the world saying “But China has USD3 trillion in reserves!” Perhaps. Most think it’s far lower than that. And not earning USD means you have to dig into that stockpile. And when you do, the PBOC either has to contract the local money supply (because every USD is backed by 7.xx CNY on the other side of the balance sheet) or it just creates new CNY anyway and supply-demand sees CNY move sharply lower – as we have been seeing in all other EM FX. Looking at the drop in BRL, ARS, ZAR, TRY, etc., or even THB,this would be how we would get to the ‘unthinkable’ 8 (9? 10?) handle in CNY. That would also crush those other EM crosses in tandem – and AUD and NZD, as the former tries to navigate its own geopolitical spat with Beijing.

And so with the Fed having taken over most US capital markets which have now lost most if not all of their discounting and signaling capabilities, keep an eye on that USDCNH: ironically, it may be the last true market stress indicator left.

via ZeroHedge News https://ift.tt/2zrxK5c Tyler Durden

{kind=link}

{kind=link}