Is it possible the Fed over-reacted to a natural disaster?

There are two different types of “recessionary” events that occur throughout history. The first is a “business cycle” recession, which happens with some regularity as excesses build up in the economy. These cycles generally take 12-18 months to complete as those excesses are reversed.

Then there are “event-driven” recessions that can occur from “natural disasters.” These are generally much shorter in duration and can be sector specific. One such event was the Japanese earthquake/tsunami in 2011, which led to a temporary manufacturing recession.

Understanding the type of recessionary cycle you are fighting is essential in ensuring the Government applies the correct monetary and fiscal response. As with any illness, the application of the wrong medication can lead to unintended consequences.

There are growing expectations of the COVID-19 economic shutdown, and the subsequent recessionary backlash will be very short-lived. The assumption is that if the economy reopens, the activity will resume, and the economy will quickly regain its footing.

If such an outcome is indeed the case, has the Fed applied the wrong “medication” to cure the economic patient?

“Over the last month, the Federal Reserve, and the Government, have unleashed a torrent of liquidity into the U.S. markets to offset a credit crisis of historic proportions. A list of programs already implemented has already surpassed all programs during the ‘Financial Crisis.’”

03/12 – Federal Reserve supplies $1.5 trillion in liquidity.

03/13 – President Trump pledges to reprieve student loan interest payments

03/13 – President Trump declares a “National Emergency” freeing up $50 billion in funds.

03/15 – Federal Reserve cuts rates to zero and launches $700 billion in “Q.E.”

03/17 – Fed launches the Primary Dealer Credit Facility to buy corporate bonds.

03/18 – Fed creates the Money Market Mutual Fund Liquidity Facility

03/18 – President Trump signs “coronavirus” relief plan to expand paid leave ($100 billion)

03/20 – President Trump invokes the Defense Production Act.

03/23 – Fed pledges “Unlimited QE” of Treasury, Mortgage, and Corporate Bonds.

03/23 – Fed launches two Corporate Credit Facilities:

A Primary Market Facility(Issuance of new 4-year bonds for businesses.)

A Secondary Market Facility(Purchase of corporate bonds and corporate bond ETFs)

03/23 – Fed starts the Term Asset-Backed Security Loan Facility(Small Business Loans)

04/09 – Fed begins several new programs:

The Paycheck Protection Program Loan Facility(Purchase of $350 billion in SBA Loans)

A Main Street Business Lending Program($600 billion in additional Small Business Loans)

The Municipal Liquidity Facility(Purchase of $500 billion in Municipal Bonds.)

Expands funding for PMCCF, SMCCF and TALF up to $850 billion.

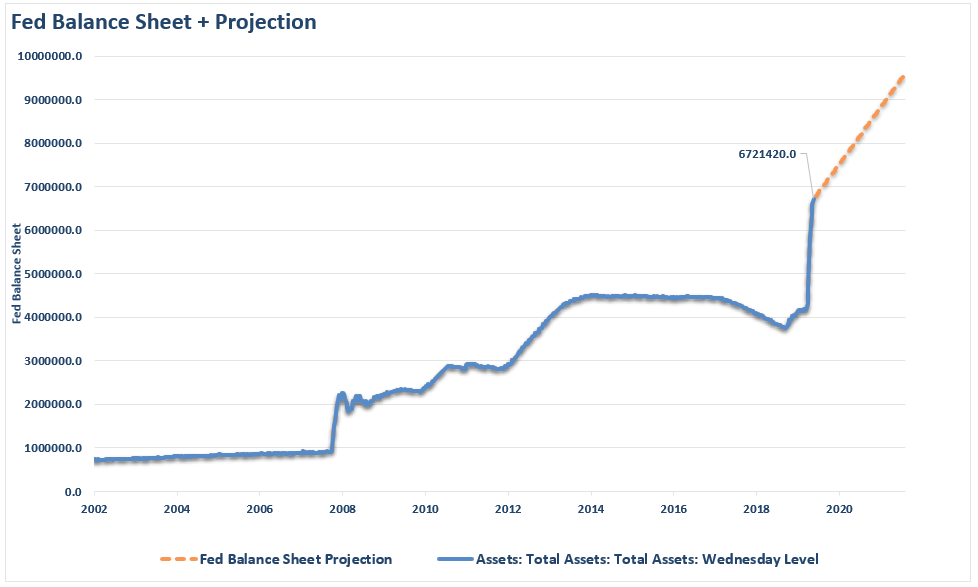

Racking Up The Debt

Here is the Fed’s balance sheet through this past Wednesday (estimated at time of writing)

As investor Paul Tudor Jones stated:

“Investors can take heart that we’ve counteracted this existential shock with the greatest fiscal, monetary bazooka. It’s not even a bazooka. It’s more like a nuclear bomb.”

Was It Too Much?

Jones’s comment was correct. However, was applying a “nuclear bomb” of monetary policy the proper response to a virus? Such is the question for consideration.

Historically, the world has been through several viruses, world wars, financial panics, major natural disasters, inflationary spikes, terrorist events, corporate defaults, attacks, and more. In every case, the economy, markets, and population survived and eventually flourished.

Was COVID-19 going to change history? I doubt it.

In hindsight, it is becoming easier to comprehend that shutting down the entire economy was probably not the right choice. Infection rates and death tolls are far lower than initially estimated, and the economic fallout was a steep price to pay. However, going in to the crisis such a modest outcome was not known and politicians had touch decisions to make.

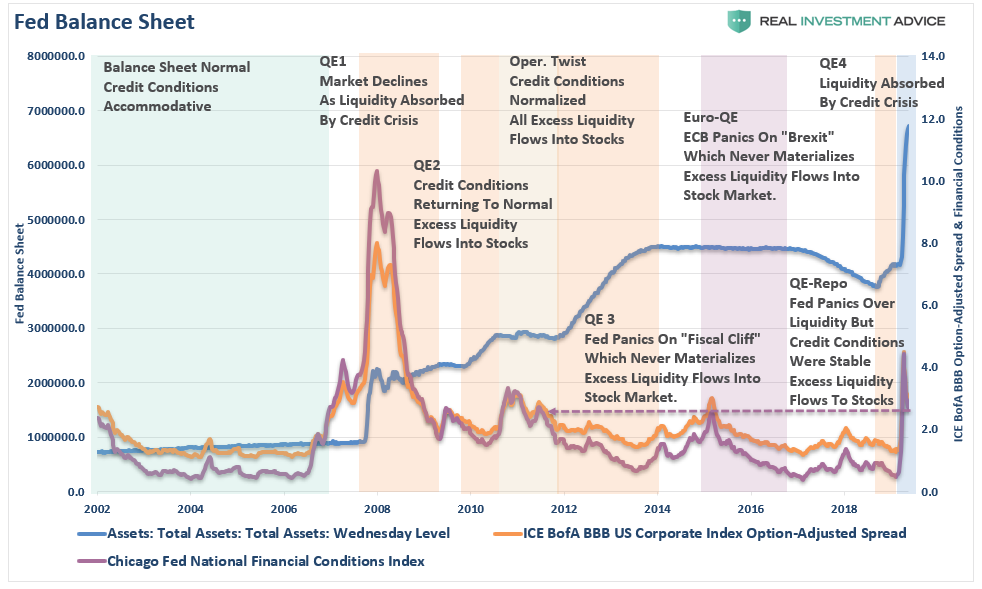

The magnitude of the Fed’s response was also a function of “panic” based more on “recency bias” than facts. The Fed quickly returned to the “Financial Crisis” playbook to anticipate events that may occur in the credit markets rather than responding to outcomes.

There is a difference.

The Financial Crisis was a problem with the banking system. The COVID-19 pandemic is a health crisis.

Notice the difference between the 2008 crisis and today concerning yield spreads, financial conditions, and the Fed’s balance sheet.

The Yield Tale

The singular purpose of the Fed’s actions was to ensure the proper functioning of the credit markets. While yields did initially spike, that ignition was quickly quenched by the “fire hose” of liquidity from the Fed.

However, the Fed has not ceased their actions. Last week, the Fed began its process of buying corporate and high-yield bond ETF’s. These purchases are being done under the SMCCF program (Secondary Market Corporate Credit Facility) with the sole purpose of ensuring corporate credit markets function smoothly.

“Purchases are focused on reducing the broad-based deterioration of liquidity seen in March 2020 to levels that correspond more closely to prevailing economic conditions,” the document said. It listed an array of metrics that would guide investments, including transaction costs, bid-ask spreads, credit spreads, volatility, and “qualitative market color.”

“Once market functioning measures return to levels that are more closely, but not fully, aligned with levels that correspond to prevailing economic conditions, broad-based purchases will continue at a reduced, steady pace to maintain these conditions.”

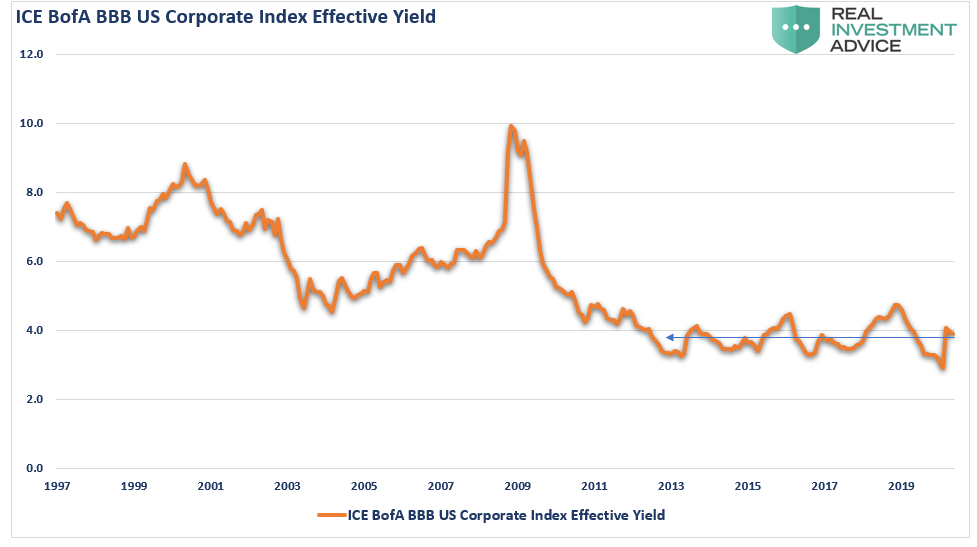

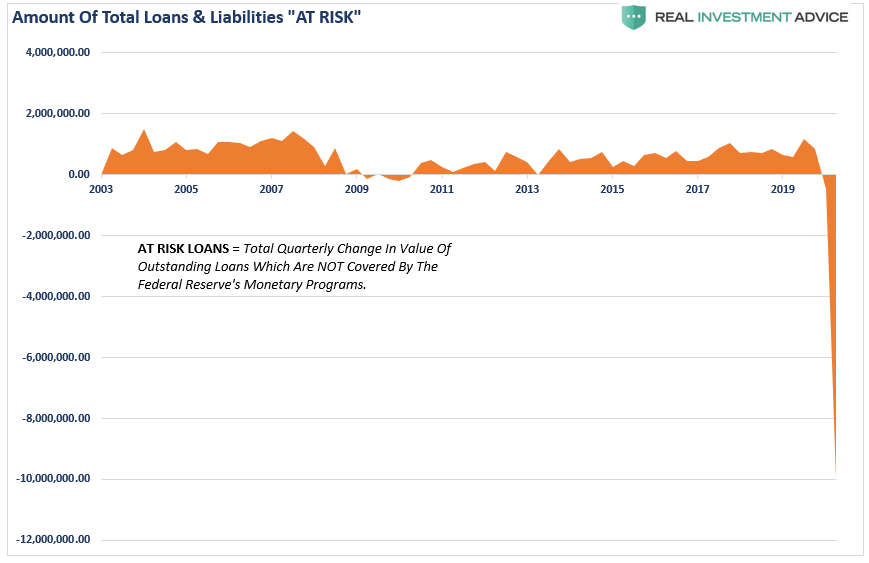

Such is interesting as credit condition never blew out and have already returned to levels more closely aligned with previous economic conditions. In fact, in the one area where there is the densest concentration of bonds “at risk,” effective yields haven’t risen much at all.

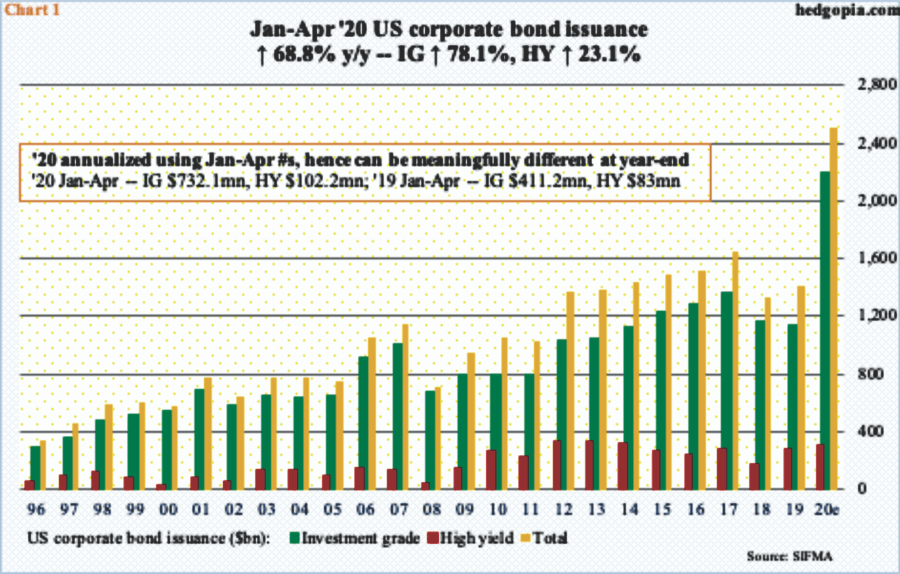

More Debt

Corporate issuers also have had NO trouble issuing debt as of late. In fact, over the past couple of months, there has been a record amount of debt issuance in investment-grade bonds, with high yield issuance close to previous levels.

If yields are within more normal ranges, and bond issuance isn’t a problem, then why is the Federal Reserve continuing to act as if a credit crisis is in process?

Do they see issues in the credit markets the data doesn’t show? Or, are they trying to “front-run” any potential credit disruptions which may occur as the economy reopens?

There Will Be Consequences

If the Fed is correct, and a credit crisis is in process, then the current levels of stimulus may fall short. As noted on April 10th:

“We are now looking at a potential decline of 20% in GDP, which will equate to roughly a $10 Trillion reduction in debt as defaults, bankruptcies, and restructurings rise.

There is a real possibility the Fed is ‘filling in a hole’ that is growing faster than they can fill it. (The Fed is injecting $6 Trillion via the balance sheet expansion versus a potential $10 Trillion shortfall.)”

Unfortunately, that estimate of the decline in GDP was a bit optimistic. Last week, the Atlanta Fed’s real-time economic indicator was predicting a -42.8% decline, or nearly twice the current levels of most estimates.

However, if this turns out to be a short-lived crisis and economic activity comes surging back, then the Fed’s stimulus may be too much, leading to a surge in inflation and downward pressure on the middle class.

Regardless of the eventual outcome, there is one consequence of massive debt and deficit expansions that will not change – slower economic growth.

No Other Choice

With the economy facing an “economic depression,” and in the middle of an election year, the Federal Reserve had a choice to make.

Allow capitalism to take root by allowing corporations to fail and restructure after spending a decade leveraging themselves to the hilt, buying back shares, and massively increasing their executives’ wealth while compressing the wages of workers. Or,

Bailout the “bad actors” once again to forestall the “clearing process” that would rebalance the economy, and allow for higher levels of future organic economic growth.

As the Fed’s balance sheet heads toward $10 Trillion, the Fed opted to impede the “clearing process.”By not allowing for debt to fail, corporations to be restructured, and “socializing the losses.” They have removed the risk of speculative practices and ensured a continuation of “bad behaviors.”

Unfortunately, given we now have a decade of experience of watching the “wealth gap” grow under the Federal Reserve’s policies, the next decade will only see the “gap” worsen.

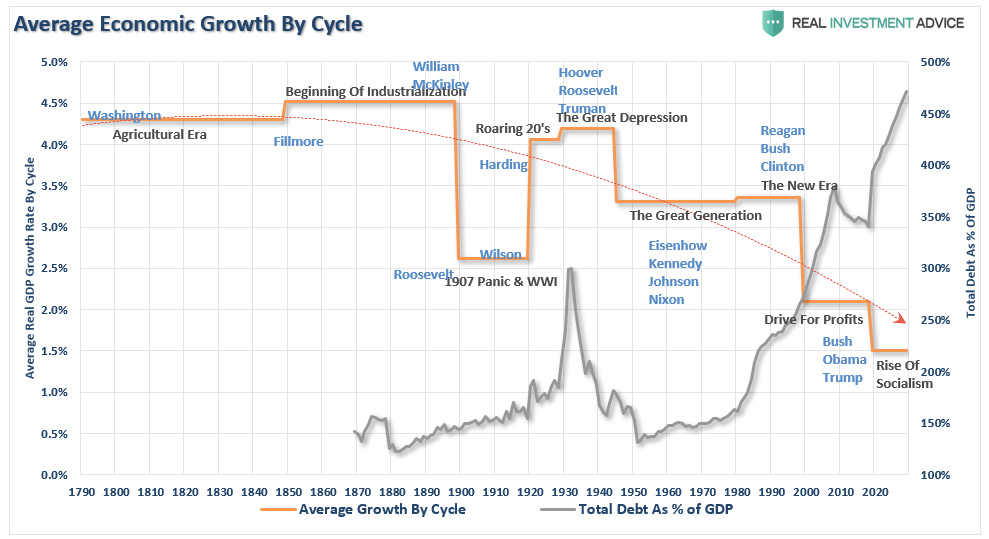

Furthermore, given that we now know surging debt and deficits inhibit organic growth, the massive debt levels added to the backs of taxpayers will only ensure lower long-term rates of economic growth. The chart below shows the 10-year annualized run rates of economic growth throughout history with projected debt and growth levels over the next decade.

The End Game

History is pretty clear about future outcomes from the Fed’s current actions. More importantly, these actions are coming at a time where there were already tremendous headwinds plaguing future economic growth.

A decline in savings rates

An aging demographic

A heavily indebted economy

A decline in exports

Slowing domestic economic growth rates.

An underemployed younger demographic.

An inelastic supply-demand curve

Weak industrial production

Dependence on productivity increases

Yes, another $4-6 Trillion in QE will likely be successful in inflating a third “bubble” to counteract the last deflation.

The problem is that after a decade of pulling forward future consumption to stimulate economic activity, a further expansion of the wealth gap, increased indebtedness; low rates of economic growth will weigh on future economic opportunity for the masses.

Supporting economic growth through increasing levels of debt only makes sense if “growth at all cost” uniformly benefits all citizens. Unfortunately, we are finding out there is a big difference between growth and prosperity.

The United States is not immune to social disruptions. The source of these problems is compounding due to the public’s failure to appreciate it. Until the Fed’s policies are discussed publicly and reconsidered, the policies will remain, and the problems will grow.

Was the “medicine” applied by the Fed to counteract a “virus” the correct prescription? If the patient ultimately dies, we will have our answer.

via ZeroHedge News https://ift.tt/2LFnSY8 Tyler Durden

Key Events This Week: Things Quiet Down Tyler Durden

Mon, 05/18/2020 – 09:10

After several weeks of economic, political and corporate earnings, things finally quiet down this week as Q1 earnings season comes to an end with a handful of retailers (at least the ones that aren’t bankrupt yet) set to report. The main data release this week will be the flash PMIs for May from around the world on Thursday and Friday, according to DB’s Jim Reid. The consensus is expecting services in Europe to bounce from low teens to the mid-twenties area and manufacturing to go up a few points in the thirties. The PMIs are diffusion indices, with respondents simply saying whether things are better or worse than the previous month so they are a little difficult to calibrate to growth at such extreme levels of activity but they will be a big curiosity nonetheless.

There’s a raft of central bank events this week, including a number from the Fed. The highlights are likely to be the two sets of remarks from Fed Chair Powell that we mentioned above. Aside from that, there’ll also be remarks to digest from Vice Chair Clarida and New York Fed President Williams on Thursday, as well as other regional Fed Presidents throughout the week. Finally on the Fed, it’ll be worth keeping an eye out for the release of the minutes from April’s meeting on Wednesday. On Friday, the ECB will also be publishing their account of the most recent monetary policy meeting.

Earnings season continues to wind down over the week ahead, with over 90% of the S&P 500 companies having now reported. This week will only see a further 22 companies from the S&P 500 and 30 from the STOXX 600 announce earnings. In terms of the highlights, today we’ll hear from Ryanair, Lufthansa and Panasonic. Then tomorrow we have Walmart and Home Depot, before Wednesday sees Lowe’s, Target and Experian report. On Thursday, there’s Nvidia, Medtronic, Intuit, TJX and Hewlett Packard Enterprise, and finally on Friday there’s Deere & Company and Alibaba.

Finally on Friday, the National People’s Congress will open in China. The central government is expected to unveil more fiscal measures, aimed at supporting households and encouraging consumption. Another thing that will be interesting to see is whether a numerical GDP target for this year is made, since Bloomberg reported previously that one option that could be done instead is to have a description of the GDP goal.

Below, courtesy of Deutsche Bank, is a day-by-day calendar of events:

Monday

Data: Japan preliminary Q1 GDP, March tertiary industry index, China April new home prices, US May NAHB housing market index

Central Banks: Remarks from the Fed’s Bostic, ECB’s Hernandez de Cos and the BoE’s Tenreyro

Earnings: SoftBank, Ryanair, Lufthansa, Panasonic

Tuesday

Data: Japan March capacity utilisation, final March industrial production, UK March unemployment, employment, average weekly earnings, EU27 April new car registrations, Germany May ZEW survey, US April housing starts, building permits

Central Banks: Remarks from Fed Chair Powell, the Fed’s Rosengren, Kashkari and the ECB’s Lane, Bank Indonesia monetary policy decision, Reserve Bank of Australia release minutes from May policy meeting

Earnings: Walmart, Home Depot

Wednesday

Data: Japan March core machine orders, UK April CPI, Euro Area March current account balance, Euro Area final April CPI, US weekly MBA mortgage applications, Canada April CPI, Euro Area advance May consumer confidence

Central Banks: FOMC release meeting minutes, remarks from BoE’s Bailey, Broadbent, Cunliffe and Haskel, Fed’s Bullard and Bank of Canada’s Lane

Earnings: Lowe’s, Target, Experian

Thursday

Data: Manufacturing, services and composite PMIs from Australia, Japan, UK and US, Japan April trade balance, US May Philadelphia Fed business outlook survey, weekly initial jobless claims, April leading index, existing home sales

Central Banks: Remarks from Fed Chair Powell, Vice Chair Clarida and New York Fed President Williams, monetary policy decisions from the Central Bank of Turkey and South African Reserve Bank

Data: Manufacturing, services and composite PMIs from France, Germany and the Euro Area, Japan April nationwide CPI, nationwide department store sales, UK April retail sales, public sector net borrowing, Canada March retail sales

Central Banks: ECB releases account of monetary policy meeting

Earnings: Deere & Company, Alibaba

Politics: China’s National People’s Congress begins

Key highlights via BofA:

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the Philly Fed manufacturing index and the jobless claims report on Thursday. In addition, minutes from the April FOMC meeting will be released on Wednesday. There are several scheduled speaking engagements from Fed officials this week, including Chair Powell on Tuesday and Thursday, and New York Fed President Williams and Vice Chair Clarida on Thursday.

Monday, May 18

10:00 AM NAHB housing market index, May (consensus 34, last 30)

02:00 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will take part in a virtual discussion about the economy and the coronavirus hosted by the Nashville Chamber of Commerce. Audience Q&A is expected.

Tuesday, May 19

08:30 AM Housing starts, April (GS -26.0%, consensus -24.1%, last -22.3%); Building permits, April (consensus -25.9%, last -6.8%); We estimate housing starts declined by 26.0% in April due to coronavirus-related declines in construction activity.

10:00 AM Fed Chair Powell appears before the Senate Banking Committee: Fed Chair Jerome Powell will testify alongside Treasury Secretary Steven Mnuchin on the Quarterly CARES Act report to Congress before the Senate Banking Committee. Prepared text is expected.

10:00 AM Minneapolis Fed President Kashkari (FOMC voter) speaks: Minneapolis Fed President Neel Kashkari will discuss the economy in a virtual town hall hosted by General Mills.

02:00 PM Boston Fed President Eric Rosengren (FOMC non-voter) speaks: Boston Fed President Eric Rosengren will discuss the impact of the coronavirus on the New England economy and the actions taken by the Fed in response in a virtual talk hosted by the New England Council.

Wednesday, May 20

10:00 AM Atlanta Fed President Raphael Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will speak on the Fed’s response to the coronavirus in a webinar with the JAXUSA Partnership.

12:00 PM St. Louis Fed President James Bullard (FOMC non-voter) speaks: St. Louis Fed President James Bullard will take part in a virtual discussion on the coronavirus and the economy hosted by the Missouri Growth Association.

02:00 PM Minutes from the April 28-29 FOMC meeting: At its March meeting, the FOMC left the target range for the policy rate unchanged at 0-0.25%, as widely expected. The FOMC did not make changes to IOER, the forward guidance, the asset purchase plan, or the credit facilities. In the minutes, we will look for further discussion of the economic outlook and the Fed’s toolkit.

Thursday, May 21

08:30 AM Philadelphia Fed manufacturing index, May (GS -35.0, consensus -40.0, last -56.6): We estimate that the Philadelphia Fed manufacturing index increased by 21.1pt to -35.0 in May.

08:30 AM Initial jobless claims, week ended May 16 (GS 2,500k, consensus 2,425k, last 2,981k): Continuing jobless claims, week ended May 9 (consensus 23,500k, last 22,833k); We estimate initial jobless claims declined but remain elevated at 2,500k in the week ended May 16

09:45 AM Markit Flash US manufacturing PMI, May preliminary (consensus 38.0, last 36.1): Markit Flash US services PMI, May preliminary (consensus 32.3, last 26.7)

10:00 AM Existing home sales, April (GS -21.0%, consensus -18.4%, last -8.5%): After falling by 8.5% in March, we estimate that existing home sales fell another 21.0% in April. Existing home sales are an input into the brokers’ commissions component of residential investment in the GDP report.

10:00 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will take part in a webinar video conference hosted by the Buffalo Niagara Partnership, CenterState CEO, and the Greater Rochester Chamber of Commerce. Prepared text and audience Q&A are expected.

01:00 PM Fed Vice Chair Clarida (FOMC voter) speaks: Fed Vice Chair Richard Clarida will take part in an online discussion on the US economy and monetary policy hosted by the New York Association for Business Economics. Prepared text and a moderated Q&A are expected.

02:30 PM Fed Chair Powell (FOMC voter) speaks: Fed Chair Jerome Powell will make opening remarks at a virtual Fed Listens event on how the coronavirus is affecting US communities. Fed Governor Lael Brainard will moderate the discussion.

Friday, May 22

There are no major economic data releases scheduled today.

Source: Deutsche Bank, Goldman, BofA

via ZeroHedge News https://ift.tt/36bZwOQ Tyler Durden

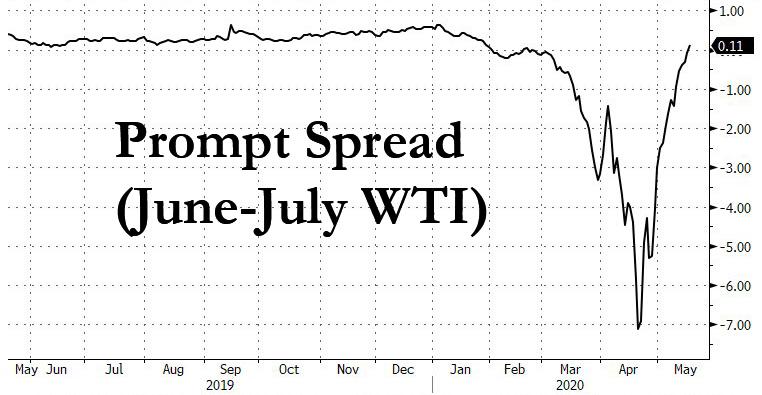

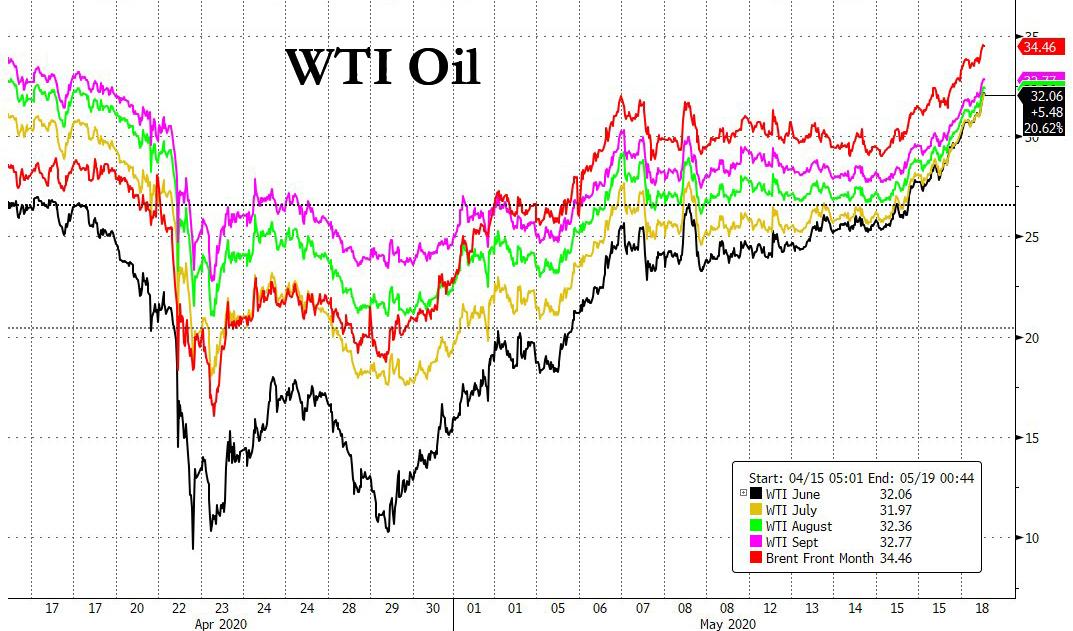

Oil Soars, Prompt WTI Contango Disappears As Chinese Oil Demand “Almost Back To Pre-Crisis Levels” Tyler Durden

Mon, 05/18/2020 – 08:53

After plunging more than 20% in Q1 due to the economic shutdown from the coronavirus pandemic, Chinese oil demand is now “all but back to levels last seen before Beijing imposed a national lockdown to fight the coronavirus outbreak” Bloomberg reported citing people with inside knowledge of the country’s energy industry, who may or may not be long oil futures.

Gasoline and diesel are leading the recovery in China as commuters prefer the safety of their own cars, rather than using public transport, while jet-fuel demand has remained subdued.

The quick turnaround in China, the world’s second largest oil consumer behind only the U.S., has helped tighten the petroleum market sooner-than-expected, and the result is a sharp rally in West Texas Intermediate crude, which a month ago plunged into negative prices and last traded above $32 a barrel.

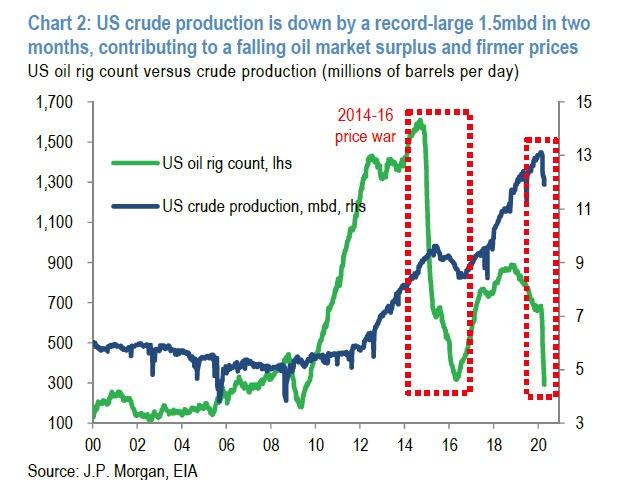

Helping the impressive rebound in oil is the accelerating shutdown in US crude production, which as shown below is down by a record 1.5mmb/d in the past two months, helping reduce supply and firm prices.

According to Bloomberg sources, Chinese consumption of gasoline and diesel has fully recovered as factories reopen and commuters drive rather than use public transport, according to the people, who are long crude asked not to be named because they aren’t authorized to discuss the matter publicly.

The same “people” adds that while pinpointing the exact level of Chinese oil demand in real time is a difficult exercise, executives and traders who monitor the country’s consumption said it was at about 13 million barrels a day, just shy of the 13.4 million barrels a day of May 2019 and 13.7 million barrels a day of December 2019. The overall number would be higher were it not for jet-fuel demand, which is still running well below a year’s ago level, as a result of a continued slump in both domestic and international air travel.

Unlike the “unnamed people” who may or may not be long oil on Monday (before they dump it and change their mind), the International Energy Agency is far more pessimist about Chinese consumption. In a report last week, it predicted that the Asian giant will consume less oil every month for the rest of the year than it did during the same period of 2019.

To reach their optimistic conclusion, the “people” are likely looking at rush hour traffic data (provided publically by TomTom International) in multiple Chinese cities , which has surged in the last couple of weeks, in many cases running either at or even above year-ago levels, according to data from navigation company TomTom International BV. The traffic has particularly intensified in cities other than Beijing and Shanghai, which typically have more space for the drivers that are now using their cars to commute into work.

At the same time, diesel demand is also recovering strongly as Beijing encourages farmers to plant more to guarantee the country’s food security and industrial consumption recovers. The uptick in China’s gasoline and diesel consumption has prompted state and independently-owned refiners to crank up run rates to convert more crude oil into fuel. That means Chinese crude stockpiles are actually being drawn down.

As Bloomberg also notes, Chinese oil refiners had in recent days embarked on a buying spree, snapping up barrels in the physical market, prompting prices to recover. “The Chinese are buying everything in sight,” said a senior executive at a major trading house.

The price of crude that’s popular with Chinese refiners, including Lula from Brazil, Djeno from the Republic of Congo, and Oman has rallied so far this month. A month ago, Lula changed hands at a discount of about $6 a barrel under the benchmark Brent. On Monday, one Chinese company bought a cargo at around $1-$1.50 a barrel premium to Brent, traders said.

“China’s oil demand is starting to show optimistic signs of full recovery, led by diesel,” said Liu Yuntao, a London-based analyst with consultant Energy Aspects.

And as optimism returns to the oil market, and as prices soar, what was until a few weeks ago a super contango in the prompt Jun-July spread is now back to backwardation, which is making the storage of oil on tankers increasingly unprofitable.

via ZeroHedge News https://ift.tt/3cL2ufK Tyler Durden

‘Tidal Wave’ Of Delinquent Mortgages Set To Surpass Great Recession Tyler Durden

Mon, 05/18/2020 – 08:35

With nearly 4 million homeowners in some type of mortgage forbearance plan – representing 7.54% of all mortgages, delinquencies are set to eclipse the great recession which peaked at 10%.

According to a new report from UK-based forecasting firm Oxford Economics, 15% of homeowners will fall behind on their monthly mortgage payments in a ‘tidal wave’ of delinquencies.

Stimulus legislation signed by President Donald Trump allows any borrower with a federally-backed mortgage to request forbearance for up to 12 months, meaning the homeowner can skip or make reduced payments during that time.

Given the risk mortgage companies are facing right now, many lenders have imposed more stringent requirements for loan applicants. “The uncertainty in the mortgage market has contributed to a significant tightening of lending standards that may persist even once a recovery is underway,” Oxford Economics wrote. –MarketWatch

An while the pace of requests for forbearance has slowed in recent weeks – however that could change. “Although the pace of forbearance requests slowed this week, call volume picked up — which could be a sign that more borrowers are calling in to check their options now that May due dates have arrived,” said Mortgage Bankers Association chief economist, Mike Fratantoni.

Keep in mind that Oxford Economics’ forecast is half of the potential mortgage bloodbath predicted by Moody’schief economics, Mark Zandi, who said that as many as 30% of Americans with home loans – or around 15 million households, may stop paying if the US economy remains closed through the summer or beyond.

We assume that a large percentage of Americans refusing to return to pre-pandemic consumption habits would have similar effects.

“This is an unprecedented event,” said Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania in comments last month. She also points out another way the current crisis is different from the 2008 GFC: “The great financial crisis happened over a number of years. This is happening in a matter of months – a matter of weeks.”

via ZeroHedge News https://ift.tt/3cIEmKW Tyler Durden

Business and markets are arbitraging government support packages and central bank QE Infinity to stay “insanely high” despite the massive economic hit of the virus. If the proverbial Martian visited the stock market today, he’d struggle to understand just why markets are so high when prospects look so low.

At which point we come back to earth with a bump. The papers this morning are full of doom and gloom – particularly re the UK. My email is full of analyst gibberish about why I should be buying Bitcoin, Tesla and other crap. I shall ignore them all, and focus on the real picture

Even if the global economy was to magically reopen tomorrow, we’d still see earnings for 2020 massively impacted, reduced credit worthiness as companies leveraged themselves with more debt to see them through the crisis, and an increasingly protectionist trade uncurrent.

That’s not a favourable market for anyone. And we all get it – the world has changed.

Understanding the nuances of this new markets is going to be critical.

It’s not just about listening to what Fed Head Jay Powell was saying when he warned about how assets prices could be impacted by the pandemic, and how it might take 18 months for the US economy to recover. It’s not just understanding the consequences of how UK long-term unemployment might rise to 9%. It’s not even all about the 11.2% decline in US industrial production through April, or the 70% crash in car production – and the knock on effects these have across the economy.

It’s also about understanding behavioural economics – how will people and politicians (note the distinction) respond in this changed environment. What impacts will politically driven decisions and consequences have on markets going forward.

Much has been said about the welfare and mental health crisis the virus lockdown has unleashed. Anxiety and fears for the future are impacting just about everyone – which I why I recommend sailing to everyone. Getting back on the water this weekend has given my feel-good an enormous boost. People are going to cut spending plans if they fear their jobs and livelihoods are under threat because of the virus and the virus recession.

How much damage can Coronaphobics and Coronanazis do to recovery? In the first bracket are the genuinely scared – frightened by the excitable news flow, and what the virus will do to them and their families. How to reassure them?

The CoronaNazi camp is more dangerous.

There seem to be an increasing number of players willing to play politics to delay reopening to prize concessions and control. Corbynistas (yes, there is still a nest of them at the extreme end of the UK political spectrum) are demanding the unions are given control of workplaces to ensure worker safety is a complete red herring – but try to criticise it, and you will be trolled! (Some of the tweets are hilarious.) All political actions have consequences – and when the government has to play to the fears of Corona-phonics and respond to the Virus-Nazis, we are going to get sub optimal outcomes.

Much of the growing China vs US trade war rhetoric is politically inspired. You can’t threaten trade sanctions again a microscopic bug, but you win voters by blaming Beijing!

It’s clear much of government response has been about anticipating the coming blame-game. Just how did the staggeringly well-paid public health managers across the UK so conclusively fail the logistics and preparation tests for the virus? Because the buck doesn’t stop with them – it will be the health minister that takes the can. Bureaucracies have a tendency to become even more entrenched during times of crisis. Although the NHS desperately needs root and branch fundamental reform, and being dragged into the modern age though AI and apps, its unlikely to happen any time soon… Cost constraints etc will ensure the bureaucracy will probably grow.

What businesses and sectors stand to win or lose short, medium and long-term? Clearly some stocks are going to do very well – companies that crack the vaccine and new treatments. But just how secure is the rest of the health sector? We’re hearing talk of being prepared for a second wave of the virus in the autumn/winter, but are governments going to keep the spending spigots open? Or do they start slash and burn cuts on health care to pay the costs of the virus? How vulnerable are any sectors that rely on government spending? Defence? Policing? Health? Education?

There is a well-circulated post doing the internet rounds how the UK’s furlough scheme is costing over £14 bln a month – £168 bln over a year. Put that in context of replacing our nuclear Trident deterrent at £205 bln, the money already spent on the HS2 railway to no-where (£100bln) or how much it’s cost to bail the banks out in 2008 – £500 bln!

The debate about how much governments can afford to leverage up before crisis is going to be an ugly one between the traditionalists who will demand a sharp scale back, and the MMT factions arguing for even greater spending. Somewhere in that argument between spending our way of out recession, and calls for financial orthodoxy, some important lessons are going to be lost. And markets will arb these events.

That’s what they do…

via ZeroHedge News https://ift.tt/2zJPJ6P Tyler Durden

“We Print It Digitally”: Futures, Gold Soar After Powell Vows “Lot More We Can Do” Tyler Durden

Mon, 05/18/2020 – 08:09

It took Jerome Powell just two days to confirm what we said late on Friday, namely that with the Fed expected to boost QE by over $3 trillion (assuming Powell doesn’t cut rates negative), the Fed chair said that “there’s a lot more we can do” and just so everyone, including Ben Bernanke understands what the Fed does, he added “We print [money] digitally… we have the ability to create money digitally and we do that by buying Treasury Bills or bonds or other government guaranteed securities.” Of course, traders ignored the “other” part of Powell’s message, namely that the recovery would take at least until the end of 2021, or the implication that stocks first need to crash before the Fed unleashes more QE, and as a result S&P futures surged more than 2% overnight, rising above 2,920, with the last 30 points in that burst coming after news out of biotech company Moderna which reported it may be getting closer to a coronavirus vaccine.

Positive sentiment was boosted by ongoing reopenings with California’s economy is now three-quarters open after virus restrictions were eased, while Apple said it will open more than 25 U.S. stores this week, adding to almost 100 globally, and helping push Apple stock 1.5% higher.

“With the worst of the pandemic likely behind us, central bank supported equity markets are unlikely to re-test their lows,” said Seema Shah, chief strategist at Principal Global Investors. “Yet, while reopening momentum may well carry risk assets a bit higher over the near term, the tepid economic recovery and deep uncertainty over the virus outlook argue against a pivot to more risk-on positioning.”

The Stoxx Europe 600 Index jumped 2.5% on gains in mining, energy and airline shares. The Stoxx Europe 600 Basic Resources Index rose as much as 4.3% as base metals climb following optimistic housing data from China and gains in risk assets, while iron ore extends its surge on supply concerns. Diversified miners jumped: Rio Tinto +4.5%, BHP +4.2%, Glencore +5.5%, Anglo American +5.1%. Several European countries ended bans on short selling, as they continued to report the lowest number of daily deaths from the virus since March.

Asian stocks also gained, led by energy and materials, after rising in the last session. Most markets in the region were up, with Australia’s S&P/ASX 200 gaining 1% and Thailand’s SET rising 1%, while India’s S&P BSE Sensex Index dropped 2.5%. The Topix gained 0.4%, with Optim and Orchestra HD rising the most. The Shanghai Composite Index rose 0.2%, with Kama and Shanghai Phoenix Enterprise Group posting the biggest advances.

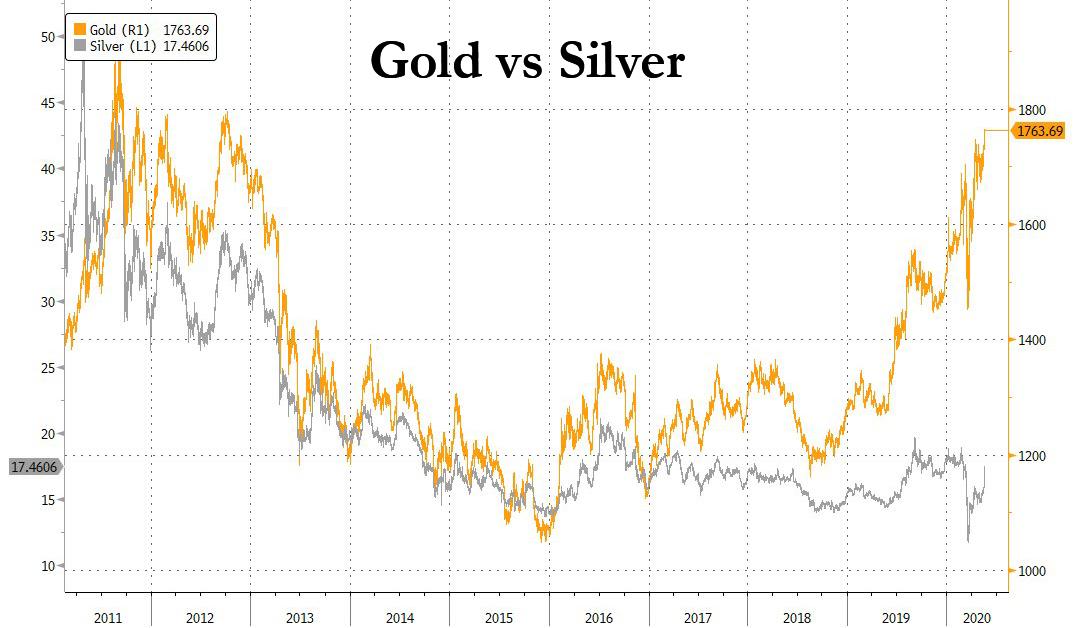

Powell vowing to crank up the printing presses helped not just stocks, but also gold which traded at its highest price in seven years, fast approaching all time highs, and while silver jumped it has a way to go to catch up to gold…

… while West Texas oil rose above $30 a barrel for the first time in two months as producers in the U.S. and elsewhere continued to cut activity.

In rates, Treasuries are little changed except at long end where yields are ~2bp cheap vs Friday’s closing levels, with futures volumes slightly below 20-day average levels. Fed Chair Powell, in televised interview Sunday, said U.S. recovery could “stretch through the end of next year.” Supply is in focus with inaugural 20-year bond sale Wednesday and IG credit issuance expected to total $30b to $35b this week. Treasury 10-year yield higher by 2bps at 0.66%; bunds outperform by 1.5bp, gilts by 2.5bp amid focus on upcoming bond redemption in July. Gilts climbed as traders bet the Bank of England will take its benchmark interest rate below zero in December.

Powell’s comments and the renewed euphoria sent the dollar sharply lower and commodity currencies higher. Norway’s krone and Australian dollar led gains among G-10 currencies as risk sentiment was boosted by oil prices topping $30 a barrel for the first time in two months, and the reopening of some economies. The pound edged higher, after erasing an earlier slide to an almost two-month low on a BOE official’s comment that the institution was examining unconventional policy measures, including negative interest rates. Money markets currently price in the probability that the BOE will take the Bank Rate under zero in December. The euro gave up some modest gains as London came into the market. Italian bonds advanced, extending their outperformance over euro-area peers as equities rose. The yen edged lower on weaker haven demand; Japan’s economy shrank an annualized 3.4% in the three months through March from the previous quarter

No major economic data or earnings are expected.

Market Snapshot

S&P 500 futures up 2.1% to 2,910.00

STOXX Europe 600 up 2.1% to 334.98

MXAP up 0.2% to 145.08

MXAPJ up 0.04% to 466.86

Nikkei up 0.5% to 20,133.73

Topix up 0.4% to 1,459.29

Hang Seng Index up 0.6% to 23,934.77

Shanghai Composite up 0.2% to 2,875.42

Sensex down 2.6% to 30,276.13

Australia S&P/ASX 200 up 1% to 5,460.54

Kospi up 0.5% to 1,937.11

German 10Y yield fell 1.8 bps to -0.549%

Euro down 0.07% to $1.0812

Italian 10Y yield rose 4.5 bps to 1.688%

Spanish 10Y yield fell 4.2 bps to 0.718%

Brent futures up 3.7% to $33.71/bbl

Gold spot up 1.1% to $1,762.39

U.S. Dollar Index little changed at 100.38

Top Overnight News from Bloomberg

Investors are now betting the U.K. will join the negative-rates club by the end of December. Spurred by Bank of England Chief Economist Andy Haldane’s comments that the institution is looking at unconventional policies — including negative rates – – more urgently, overnight interest-rate swaps for December’s meeting dropped below 0% for the first time.

China said President Xi Jinping was invited to address the opening ceremony of the World Health Organization’s decision-making meeting, shortly after Peter Navarro suggested Beijing sent airline passengers to spread the coronavirus worldwide

German Chancellor Angela Merkel and French President Emmanuel Macron on Monday will discuss a range of topics, including a new recovery fund to help the European Union weather the worst recession in living memory, according to an official familiar with the plan

Hedge funds, market-making firms and other traders across Europe can resume short-selling of equities this week after regulators lifted bans instituted when markets plunged during March’s coronavirus outbreak

Some 108 million people in China’s northeast region are being plunged back under lockdown conditions as a new and growing cluster of infections causes a backslide in the nation’s return to normal

Asia-Pac bourses began the week with modest gains and US equity futures extended on their rebound as participants digested recent comments from Fed Chair Powell who continued to dismiss the prospect of negative rates but suggested the Fed was not out of ammunition and that further action may be required. ASX 200 (+1.0%) outperformed with the advances led by strength across mining names after gold prices rose above USD 1750/oz and WTI crude futures reclaimed the USD 30/bbl level. Nikkei 225 (+0.5%) was also higher but with gains capped following GDP data which was better than expected but still showed Japan’s economy moved into a recession. Hang Seng (+0.6%) and Shanghai Comp. (+0.2%) were kept afloat after Chinese officials pledged further support including PBoC Governor Yi Gang who reiterated that China will implement more powerful monetary policy and China’s Government Work Report draft also stressed the launching of stronger macro policies. However, the gains were limited by ongoing tensions following the US move to prevent Huawei from acquiring semiconductors and chipsets made using US technology, while India’s NIFTY (2.3%) failed to hold on to opening gains with sentiment pressured after India extended the lockdown again to May 31st and surpassed China in the number of coronavirus cases. Finally, 10yr JGBs were initially flat with price action kept lacklustre amid the gains in stocks, weak GDP data from Japan and with participants awaiting the 5yr JGB auction which resulted in firmer accepted prices and in turn spurred JGBs upon return from the lunch break.

Top Asian News

Thailand Forecasts Its Economy Will Contract as Much as 6%

Japan’s Economy Sinks Into a Recession Set to Deepen Sharply

Huawei Crackdown Sends Shockwaves Through Asia Supply Chain

Rare Stumble by Listed Firm in Japan Fuels Record Drop in Shares

European bourses post gains across the board [Euro Stoxx 50 +2.4%] and piggy-back on the positive lead APAC lead following supporting comments from Fed Chair Powell that the Central Bank was not out of ammo and can do more if needed in which he suggested there are no limits to what we can do, meanwhile BoE’s Haldane posited the Bank was looking at options beyond and alongside negative rates. That being said, investors need to juggle COVID-19 and the prospect of escalating protectionism between US and China. Earlier source reports via Nikkei noted TSMC has stopped orders from Huawei, albeit this was downplayed by the chip-company as “market rumours”, adding that it cannot disclose order information. If true, this can mark a major blow to the Chinese telecom and could prompt China’s unveiling of “unreliable entity list”. As a reminder, China’s Global Times’ Chief Editor last week said: “if US further blocks key technology supply to Huawei; will restrict or investigate US companies such as Qualcomm (QCOM), Cisco and Apple (AAPL), and suspend the purchase of Boeing (BA) planes.” Back to Europe, sentiment seems more driven by Central Bank comments thus far and as economies continue to ease lockdown restrictions, with broad-based gains seen across major indices; albeit, Italy’s FTSE MIB (+1.3%) is the laggard after Italy’s regulator lifted the short-selling carpet ban ahead of schedule and in synchrony with France, Spain, Greece, Belgium, and Austria. Sectors are all in positive territory with the energy sector the outperformer whilst cyclicals outperform defensives – reflecting risk appetite. The breakdown also shows gains led by oil and mining-related sectors, while Travel & Leisure also resides towards the top. In terms of individual movers, Deutsche Telekom (+1.4%) rises with the market but underperforms the DAX (+2.9%) amid reports SoftBank Group is said to be in discussions to sell a large chunk of its T-Mobile (TMUS) stake to Deutsche Telekom. If the transaction is completed, it would boost Deutsche Telekom’s share to over 50%. according to WSJ citing sources. Note: T-Mobile’s largest shareholders are Deutsche Telekom (42.1% stake) and SoftBank (23.8% Stake). Meanwhile, Diageo (+2%) is underpinned by reports Co. is said to be mulling options to delist United Spirits, according to CNBC-TV18 citing sources. Ryanair (+7%) was bolstered post-FY earnings in which it expects a smaller Q2 loss vs. Q1, Co. also boosted its liquidity. Finally, AstraZeneca (+1.4%) outpaces the broader Pharma sector amid reports it will produce as many as 30mln COVID-19 vaccines available to the UK by September if trials are successful. However, FT’s Elder, on the Co. being the largest FTSE 100 by market cap, suggested that such rises “most commonly, feel like a sell signal”

Top European News

Thyssenkrupp in Fresh Talks to Merge Ailing Steel Division

How Germany’s Relentless Contact Tracers Helped Beat Virus

U.K. Gets Fresh Warnings of Economic Scars Before Sunak Speaks

Billionaire Barclay Brother’s Video Shows ‘Bugging’ at The Ritz

In FX, the non-US Dollars are revelling in a risk on start to the new week, or rather clawing back lost ground amidst high flying precious metals (Gold Usd 1760+ per oz at one stage) and the ongoing revival in crude prices (WTI Usd 31+ and Brent almost Usd 34 per barrel). The Aussie is building a firmer base on the 0.6400 handle and Kiwi is pivoting 0.5950, while the Loonie has rebounded from under 1.4100 even though the DXY remains firm above 100.000 within a 100.470-280 range on the back of gains forged vs ‘safer-havens’ and other G10s with a bigger weighting in the index.

JPY/CHF/EUR/GBP – Renewed risk appetite has sapped demand for the Yen relative to the Greenback in the low 107.00 area, but Usd/Jpy looks capped ahead of 107.50 where hefty option expiries reside (2.2 bn), while the Franc remains mixed after comments from SNB’s Maechler noting that the currency would be significantly stronger without increased levels of intervention evident in yet another marked rise in Swiss bank sight deposits. Usd/Chf is currently above 0.9700, but Eur/Chf still eyeing 1.0500 as the Board member also refuted that the round number is a line in the sand akin to the old official 1.2000 floor that was pulled in January 2015. Moreover, the Euro still looks top heavy vs the Buck on ventures through 1.0800 following Fitch cutting France’s AA ratings outlook to negative from stable and also downgrading Austria from positive to stable. Elsewhere, dovish guidance from BoE’s Haldane has added to the Pound’s seasonal weakness, though Cable has rebounded from sub-1.2100 and Eur/Gbp is off 0.8950+ peaks ahead of more from the MPC via Tenreyro with specific focus on any further mention of NIRP.

SCANDI/EM – No shock to see the Nok, Rub and Mxn welcoming the latest rally in oil, while the Sek is tagging along on broadly bullish risk sentiment and the Try has extended its already impressive recovery to almost 6.8300 vs the Usd after Clearstream and Euroclear both suspended Lira trade on electronic platforms citing a lack of liquidity due to COVID-19 restrictions. On that note, Chinese President Xi will open the World Health Assembly and the Yuan is on a weaker footing in advance of his address and the NPC. Eur/Nok is hovering near 11.0000, Usd/Rub circa 73.0500, Usd/Mxn under 23.9000, Eur/Sek below 10.6400 and Usd/Cnh just shy of 7.1450..

SNB’s Maechler acknowledged the CHF’s appreciation, but stated it would have been much more pronounced if we hadn’t been prepared to intervene more heavily; when asked if 1.05 in EUR/CHF was being an informal upper limit responded ‘no, we look at the entire currency situation’. Additionally, rejected the possibility of a special profit payout from the SNB to the Swiss Gov’t given COVID-19. (Newswires/NZZ)

In commodities, oil futures continue on their upwards trajectories, aided by a rosier demand prospect as economies reopen and with supply contained by producers. Furthermore, reports via Energy Intel noted that OPEC+ could reportedly extend current production cuts to year-end. The production cuts are to be eased from July according to the original pact. Sticking with OPEC, Saudi and Kuwait also agreed to suspend output at the Khafji field in the neutral zone in June, expected cuts to total 80mln BPD. Meanwhile, Friday’s Baker Hughes Rig Count continued to show receding US drilling activity. WTI June and July both trade comfortably above USD 30/bbl, with the front-month holding up heading into tomorrow’s June expiry, thus far suggesting subsiding fears of storage scarcity. Despite a lion’s share of open interest and volume in the July contract, participants will be observing the June contract after WTI May fell deep into negative territory heading into its expiration. Brent July also remains on the front-foot, towards the top if a USD 32.69-34.00/bbl intraday band. WTI June had risen over WTI July in early trade. Spot gold extend its post-Powell gains after the Fed Chair noted that stocks and asset prices could suffer a significant hit and the post coronavirus recovery could last through 2021, while he added the Fed is not out of ammunition and can do more if needed in which he suggested there are no limits to what we can do. The yellow metal sits at an over-seven-year high at USD ~1760/oz (vs. range USD 1743.33-1764.46/oz). Copper prices are supported by the overall risk appetite, but the red metal trades within recent ranges. Meanwhile Dalian Iron ore rose over 6% at one point amid higher demand prospects with economies and factories reopening.

US Event Calendar

10am: NAHB Housing Market Index, est. 34, prior 30

2pm: Fed’s Bostic Holds Virtual Discussion About Economy

DB’s Jim Reid concludes the overnight wrap

The weekend wasn’t bursting with new information. It does feel like we’re in the middle of a phoney war at the moment with all of us waiting to see how efficiently the various economies are able to re-open given all the social distancing that will be required. As you’ll see below last week was the worst for most equity markets since the lows in March but there were still a lot of dip buyers about.

Fed Chair Powell’s recorded appearance on CBS’s “Face the Nation” last night was probably one of the highlights over the weekend. Having said that he didn’t really say too much new but continued a recent pattern of being relatively cautious on the timing and strength of the recovery even if he said people should never bet against the American economy. On negative rates, he said “I continue to think, and my colleagues on the Federal Open Market Committee continue to think, that negative interest rates is probably not an appropriate or useful policy for us here in the United States.” He also reiterated that the Fed hadn’t exhausted its options for aiding the economy and noted that the Fed can increase its emergency lending programs and make monetary policy more supportive through forward guidance and by adjusting the Fed’s asset-purchase strategy. Mr Powell will be speaking again before the Senate Banking Committee tomorrow, and then making some opening remarks at a Fed Listens event on Thursday. So plenty of opportunity for him to continue to get this message across this week.

In other news, after markets closed on Friday, the Trump administration said that it is barring any chipmaker using American equipment from supplying China’s Huawei without US government approval. Commerce Secretary Wilbur Ross said in a tweet that “We must amend our rules exploited by Huawei and HiSilicon and prevent U.S. technologies from enabling malign activities contrary to U.S. national security and foreign policy interests.” That’s weighed on Huawei’s Asian suppliers like TSMC (-2.18%), AAC Technologies Holdings Inc (-5.63%), Optical Technology Group Co (-10.45%) and Win Semiconductors (-6.52%) this morning. China’s Ministry of Commerce has said that it opposes the new U.S. rules and will take all necessary measures to defend the rights and interests of Chinese companies and urged Washington to help create conditions for normal trade and cooperation between enterprises.

Despite the weakness in those tech names, most Asian bourses have started the week on the front foot with the Nikkei (+0.68%), Hang Seng (+0.40%), Shanghai Comp (+0.61%) and Kospi (+0.74%) all up. Futures on the S&P 500 are also up +1.15% as we type while WTI crude oil prices are up +3.74% to $30.48. Spot gold prices are trading up +0.95% this morning to $1,760/oz. Meanwhile, Sterling has pared earlier losses after BoE Chief Economist Andrew Haldane hinted over the weekend that the BoE is examining possible unconventional monetary policy measures.

The main data release this week will be the flash PMIs for May from around the world on Thursday and Friday. The consensus is expecting services in Europe to bounce from low teens to the mid-twenties area and manufacturing to go up a few points in the thirties. The PMIs are diffusion indices, with respondents simply saying whether things are better or worse than the previous month so they are a little difficult to calibrate to growth at such extreme levels of activity but they will be a big curiosity nonetheless. For the rest of the week’s data see the day by day week ahead guide at the end.

There’s a raft of central bank events this week, including a number from the Fed. The highlights are likely to be the two sets of remarks from Fed Chair Powell that we mentioned above. Aside from that, there’ll also be remarks to digest from Vice Chair Clarida and New York Fed President Williams on Thursday, as well as other regional Fed Presidents throughout the week. Finally on the Fed, it’ll be worth keeping an eye out for the release of the minutes from April’s meeting on Wednesday. On Friday, the ECB will also be publishing their account of the most recent monetary policy meeting.

Earnings season continues to wind down over the week ahead, with over 90% of the S&P 500 companies having now reported. This week will only see a further 22 companies from the S&P 500 and 30 from the STOXX 600 announce earnings. In terms of the highlights, today we’ll hear from Ryanair, Lufthansa and Panasonic. Then tomorrow we have Walmart and Home Depot, before Wednesday sees Lowe’s, Target and Experian report. On Thursday, there’s Nvidia, Medtronic, Intuit, TJX and Hewlett Packard Enterprise, and finally on Friday there’s Deere & Company and Alibaba.

Finally on Friday, the National People’s Congress will open in China. Our economists expect that the central government will unveil more fiscal measures, aimed at supporting households and encouraging consumption. Another thing that will be interesting to see is whether a numerical GDP target for this year is made, since Bloomberg reported previously that one option that could be done instead is to have a description of the GDP goal.

Recapping last week now and there was a decidedly risk off tone. The S&P 500 fell -2.26% last week (+0.39% Friday), which was the worst weekly loss for the index since the March lows. Technology and Healthcare stocks outperformed slightly, but the NASDAQ still fell -1.17% on the week (+0.79% Friday), the worst weekly loss since the first week in April. The heavily Technology weighted index is still up an impressive +0.47% YTD.

European equities also declined on the week. The Stoxx 600 was down -3.76% (+0.47% Friday) over the five days. The DAX declined -4.03% (+1.24% Friday), while the Italian FTSE MIB fell -3.37% (-0.09% Friday), and the CAC slid -5.98% (+0.11% Friday). Asian indices were down less than their European and American counterparts. The Nikkei fell just -0.70% over the week (+0.62 Friday) and the CSI 300 lost -1.28% (-0.32% Friday), while the Kospi fell -0.95% (+0.12% Friday). One risk asset that did rise on the week was oil. The commodity continued to rally for a third week in a row after WTI futures went negative back on 20 April. Last week WTI futures rose +18.96% (+6.79% Friday) to $29.43/barrel and Brent crude rose +4.94% on the week (+4.40% Friday). Oil pricing continues to recover as suppliers cut production and demand prospects improve.

The VIX rose +3.91 pts to 31.89 last week (-0.72pts Friday). That was the largest weekly increase since 20 March, when the S&P 500 was at its recent lows. Despite oil prices continuing to rise, the pullback in equities and the subsequent rise in volatility saw HY credit spreads mostly wider on the week. US HY cash spreads were +26bps wider (+1bp Friday), while IG was actually -2bps tighter on the week (-1bp Friday). In Europe, HY cash spreads were +22bps wider (+1bp Friday), while IG widened +7bps (flat Friday).

Even with equities falling, sovereign bonds yields were either flat or just slightly down. US 10yr Treasury yields were down -4.0bps (+2.1bps Friday) to finish at 0.643%, 10bps from the March lows. Meanwhile, 10yr Bund yields rose +0.6bps over the course of the week (+1.2bps Friday) to -0.53%. 10yr Gilts were similarly little changed on the week, down -0.4bps (+2.7bps Friday). Peripheral debt went in different directions. Spanish 10yr yields tightened -4.2 bps to Bunds over the 5 days, while Italian BTPs widened +1.1bps. In other havens, gold rose to its highest level since November 2012, rallying +2.41% (+0.77% Friday) to $1743.67/oz.

Economic data last Friday continued to show the fallout of the coronavirus. US industrial production fell by -11.2% in April (slightly above the -12.0% expected), following a -4.5% decline in March. This is the largest monthly decline in the 101 years that the index has run for. Retail sales in the US fell by -16.4% in April (far more than the 12.0% expected), following an -8.3% decline in March. There was a -60.6% fall for electronics and appliance stores, while clothing and clothing accessories stores fell by -78.8%. The preliminary U. Michigan Sentiment Survey for April offered some good news, coming in at 73.1 (vs. 68.0 expected). In Europe, Euro Area employment in the first quarter fell by 0.2%, the first decline since Q2 2013. German GDP contracted by -2.2 % in the first quarter, the largest quarterly contraction since Q1 2009.

via ZeroHedge News https://ift.tt/2X5OIhj Tyler Durden

Moderna Spikes 20%, Dow Futs Soar On Promising Early COVID Vaccine Trial Data Tyler Durden

Mon, 05/18/2020 – 07:52

In what appear to be the first data from a human vaccine trial, Modern has reported promising early signs that its vaccine “can create an immune-system response in the body that could help fend off the new coronavirus” according to sampling data from a small group of humans who participated in the phase 1 study.

Signs that one of the most hyped vaccines out of the 130+ projects underway around the world have helped Moderna’s shares soar 20%+ in premarket trade.

According to BBG, citing data released by Moderna, the study was primarily designed to look at the safety of the shot, and showed no major warning signs in a small phase 1 trial, the company said in a statement Monday. The trial is being run in partnership of the US government under the watchful eye of Dr. Fauci and the NIH. Moderna plans to continue advancing it to wider testing.

More importantly than the safety-related findings, researchers found that at two lower dose levels, antibodies could be detected, a sign that the vaccine could help those who receive it fend off infection by the virus.

The researchers found that at two lower dose levels used in the study, levels of antibodies found after getting a second booster shot of the vaccine either equaled or exceeded the levels of antibodies found in patients who had recovered from the virus.

Moderna’s CEO – who later appeared on CNBC Monday morning for an interview – praised the results as “a very good sign.”

“This is a very good sign that we make an antibody that can stop the virus from replicating,” Moderna Chief Executive Officer Stephane Bancel said in an interview. The data “couldn’t have been better,” he said.

Bancel said that safety profile appeared to be good, and the reactions were typical of vaccines. They included injection site pain and redness, as well as temporary fever or chills that quickly go away on their own, he said.

Bancel added that the safety profile of the vaccine appeared to be good, and the reactions were mostly typical, including soreness and pain at the injection site. Some patients experienced temporary fever and chills in reaction to the shot. Though Bancel clarified that this only emerged in a few cases during the second round of dose administration. The symptoms mostly went away on their own, according to the company.

The company felt it needed to release these interim data from the trial due to the “high level of interest” in the vaccine (helped by CNBC’s Jim Cramer, who often mentions the company on air).

A phase 2 trial is expected to begin shortly, and a final-stage trial will begin in July, Moderna said. Dow futures are soaring on the news, with the Dow up 560 points in recent trade, building on earlier gains.

via ZeroHedge News https://ift.tt/2LFIcsl Tyler Durden

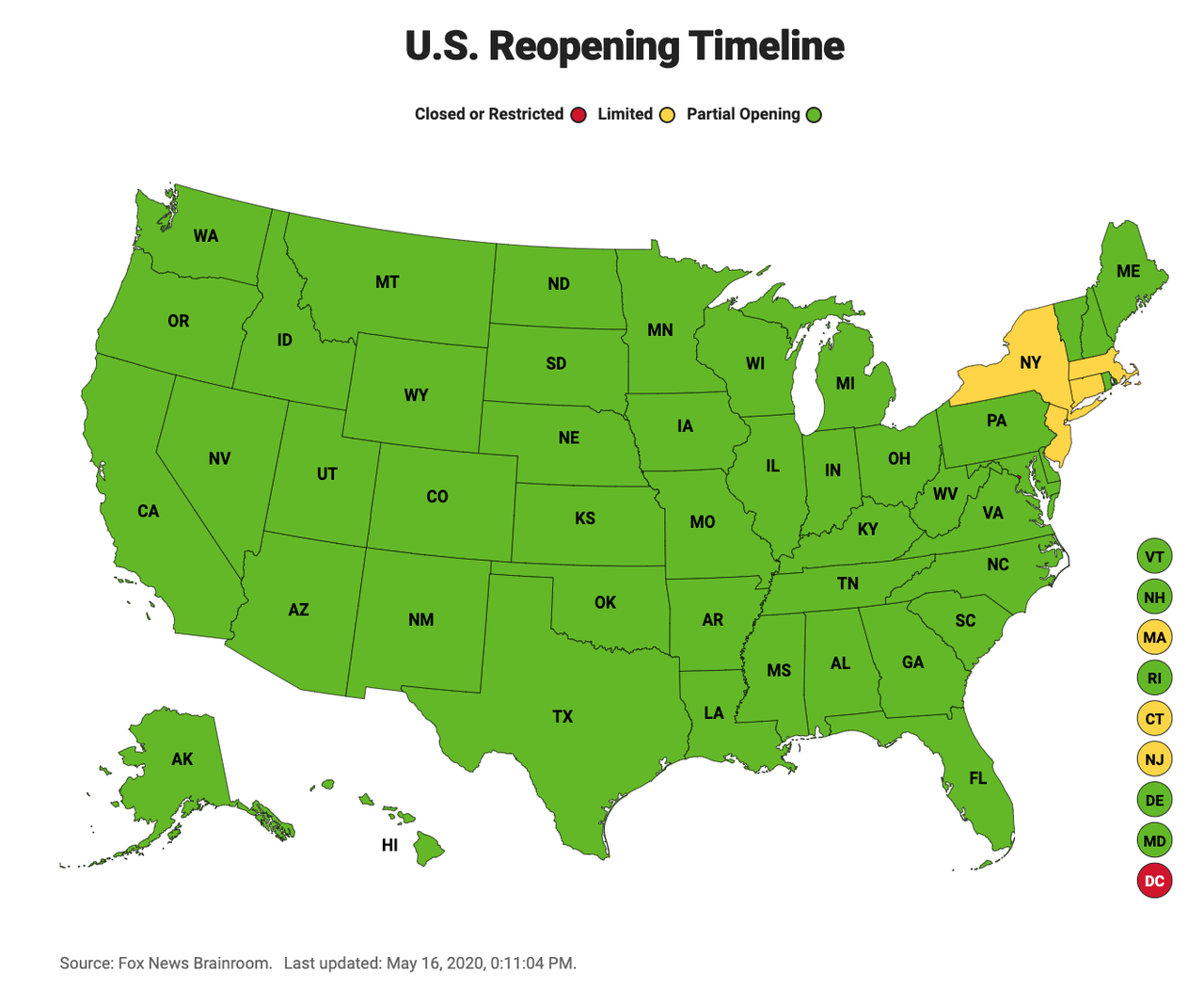

100 Million Chinese Back Under Lockdown As Americans, Europeans Flock To Parks & Beaches: Live Updates Tyler Durden

Mon, 05/18/2020 – 07:24

Summary:

108 million under lockdown in NE China

Beaches, parks reopen across US, Europe

New Zealand reopens schools Monday

Italy plans to reopen most restaurants & businesses by week’s end.

New cases in Brazil, Russia slow as deaths accelerate

In US, all but 4 states have “partially reopened”

WHO annual meeting begins with keynote from President Xi

South Africa reports largest single-day spike in cases

* * *

With two weeks left in May, the pace of deaths across the US has slowed substantially, a reflection of the progress made by the worst-impacted states like New York, Michigan, New Jersey, California and Washington State, and – importantly – a repudiation of the alarmist forecasts published by the NYT earlier this month calling for the rate of US COVID-19-linked deaths to hit 3,000/day. Yesterday, the US reported just 808 deaths (remember, these data are reported with a 24-hour lag) according to data provided by Johns Hopkins University.

As of Monday morning, the US had confirmed 1,486,742 cases (with thousands of patients likely going undiagnosed) and 89,564 deaths, placing it on track to surpass 90k deaths by the end of today.

Reported US coronavirus deaths on date:

Feb. 17: 0 deaths

Mar. 17: 111 deaths

Apr. 17: 37,054 deaths

May 17: 89,562 deaths

Meanwhile, as outbreaks in Russia and Brazil continue to rage, both countries have officially counted hundreds of thousands of additional cases over the last 2 weeks. The two countries, which boast the No. 2 (Russia) and No. 4 (Brazil) highest ‘official’ case counts in the world, are approaching the problem from different angles: In Russia, President Putin is ratcheting up lockdown and social distancing measures, while Brazil – under President Jair Bolsonaro, who has dismissed the virus as “a little flu” – continues to reopen its economy to the consternation of its neighbors.

The death toll has ballooned in the South American nation to 16,118 as of Monday morning in the US, the 6th-highest rally in the world. Two weeks ago the death count was 7,025. On Sunday, Brazil reported 485 additional deaths and 7,938 more cases. That was after Brazil on Saturday reported 816 more deaths, second only to the US with 1,218, and more than 14k additional cases. The numbers pushed Brazil past Italy and Spain on the ranking of hardest-hit countries. Brazil’s “official” tally was 241,080, though with testing rates that lag far behind Europe, many suspect the accurate number is much higher.

While most of the US and Europe have continued to reopen, Chile’s capital city Santiago was locked down on Sunday following a resurgence of new cases and deaths linked to the virus.

VIDEO: With near-deserted streets and police checks, the seven million people of Chile’s capital, Santiago, began a strict quarantine Saturday after a sharp resurgence of coronavirus cases pic.twitter.com/4XMd8abl5C

Russia said Monday that it recorded 9,000 new coronavirus cases over the last 24 hours, the lowest level since early May (the country was reporting more than 10k cases a day). Health officials reported 8,926 new infections in the last 24 hours, bringing the country’s total to 290,678, the second-highest in the world after the US. It was the lowest number of new virus cases since May 1, when Russia announced 7,933 cases, according to the Japanese Times.

A little further south in New Zealand, hundreds of thousands of children were preparing to return to school on Monday after a 2-month ‘home education’ break.

Hundreds of thousands of New Zealand children returned to school Monday after two months of home education as part of a COVID-19 lockdown, according to the AFP. With a population of 5 million, NZ recorded just 1,149 cases of the virus and 21 deaths, attributed to a strict lockdown adopted in March. Most of NZ’s lockdown measures ended on Thursday.

Back in the US, as more states start the process of reopening, Apple is planning to reopen more than 25 of its branded stores in the US, according to a Reuters report. The company said on Sunday that by the end of the week, 1/5th of its retail stores worldwide will have reopened.

Yesterday, we reported that tens of millions of Chinese in the northeastern part of the country had been placed under lockdown again following a new outbreak near the border with Russia. Apparently, that number was way off: Right now, some 100 million Chinese are back under lockdown.

Some 108 million people in China’s northeast region are being thrown back under lockdown as a new cluster of #coronavirus infections emerges.

Some 108 million people in China’s northeast region of Jilin are back under lockdown conditions, BBG reports, in “an abrupt reversal of the re-opening taking place across the nation, cities in Jilin province have cut off trains and buses, shut schools and quarantined tens of thousands of people.” The strict measures have dismayed many residents who had thought the worst of the nation’s epidemic was over.

People “are feeling more cautious again,” said Fan Pai, a worker in Jilin. “Children playing outside are wearing masks again” and health care workers are walking around in protective gear, she said. “It’s frustrating because you don’t know when it will end.”

Meanwhile, according to another Reuters report, beautiful summer weather across the northern hemisphere is enticing millions of people in virus ‘hot spots’ from NYC to the mediterranean coasts of Italy and Spain to visit public parks and beaches, making them the primary centers of recreation in the COVID era.

Most cities and towns have adopted new precautions to prevent the virus from spreading. Many individuals are choosing to keep their distance and wear masks. Greeks flocked to beaches on Saturday as more than 500 beaches reopened, coinciding with temperatures of 34 Celsius (93.2 Fahrenheit).

As the number of new cases accelerates rapidly across Africa, stoking fears about new ‘hot spots’, South Africa reported its highest single-day jump in reported coronavirus cases on Sunday, with an increase of 1,160 infections, according to the country’s National Department of Health. That brings the total number of cases to 15,515, with the Western Cape province accounting for ~60% of that total.

In Brooklyn’s Domino Park, white circles were painted on the lawn to help sunbathers and picnickers keep a safe distance. About half the people in the park appeared to be wearing some form of face covering as they congregated in small groups on a warm Saturday afternoon, as cops in masks kept watch.

In Italy, many restaurants, bars and cafes have reopened now that Italy has seen daily deaths drop to levels not seen since the early days of the pandemic.

Italy’s restaurants, bars and cafes among businesses allowed to reopen as country records lowest single-day Covid-19 death toll since its two-month lockdown began pic.twitter.com/IeEIGFEUSn

After releasing consumer-goods pricing data that hinted at a wave of destabilizing deflation headed China’s way, the mainland press has been searching far and wide for “foreign” experts to reassure the Chinese people that China’s economy will hit its pre-COVID growth benchmarks, just like President Xi said.

The Chinese economy is resilient enough to keep its growth rate despite the impact brought by the #COVID19 pandemic: Egyptian experts pic.twitter.com/6LmNG913P8

As we reported last night, the WHO is holding a two-day annual meeting starting Monday. Chinese President Xi Jinping delivered the keynote address on Monday while members battle over whether to authorized an investigation into the early days of the outbreak in Wuhan, as well as pushing for Taiwan to be made a full member of the organization over the rapid resistance of the CCP.

via ZeroHedge News https://ift.tt/367jxX2 Tyler Durden

While the rest of the world is tentatively coming out of lockdowns, China is taking advantage of the cheapest crude oil in years to stock up as demand is starting to return in the world’s largest oil importer, Bloomberg reported on Friday, citing tanker-tracking data it has compiled.

At present, a total of 117 very large crude carriers (VLCCs) – each capable of shipping 2 million barrels of oil – are traveling to China for unloading at its ports between the middle of May and the middle of August. If those supertankers transport standard-size crude oil cargoes, it could mean that China expects at least 230 million barrels of oil over the next three months, according to Bloomberg. The fleet en route to China could be the largest number of supertankers traveling to the world’s top oil importer at one time, ever, Bloomberg News’ Firat Kayakiran says.

Many of the crude oil cargoes are likely to have been bought in April, when prices were lower than the current price and when WTI Crude futures even dipped into negative territory for a day.

Last month, emerging from the coronavirus lockdown, China’s oil refiners were already buying ultra-cheap spot cargoes from Alaska, Canada, and Brazil, taking advantage of the deep discounts at which many crude grades were being offered to China with non-existent demand elsewhere.

China was also estimated to have doubled the fill rate at its strategic and commercial inventories in Q1 2020, taking advantage of the low oil prices and somewhat supporting the oil market amid crashing demand by diverting more imports to storage, rather than outright slashing crude imports.

China’s crude oil imports jumped in April to about 9.84 million bpd as demand for fuels began to rebound and local refiners started to ramp up crude processing, according to Chinese customs data cited by Reuters.

via ZeroHedge News https://ift.tt/2X5pjUZ Tyler Durden

Anti-Lockdown Protests Accelerate Across Europe As Second COVID-19 Wave Threat Emerges Tyler Durden

Mon, 05/18/2020 – 05:30

Anti-lockdown protests were seen in several European cities on Saturday in defiance of social distancing restrictions. From gatherings in London’s Hyde Park to Poland to Germany — people were furious about government-enforced lockdowns. Warmer weather trends, such as a heatwave across parts of Europe, could quickly affect mood negatively and lead to more social instabilities.

These protests have been increasing over the last several weeks. Read:

Police in several German cities had their hands full on Saturday as thousands of people lined the streets. Officials in Stuttgart said the permitted number of 5,000 demonstrators was quickly exceeded, and mask-wearing was required, or people risked a 300 euro ($325) fine.

Nearly 5,000 people took part in a rally against #coronavirus restrictions in #Stuttgart on Saturday, #Germany‘s largest such protest over the weekend.

About 1,000 protesters were seen in Munich, around the Theresienwiese event grounds, which is the site of the now-canceled Oktoberfest. We explained last month, the canceling of the event has severely impacted the local economy and could devastate local brewers to hop farmers.

Protesters in both Stuttgart and Munich were angry about lockdown measures enforced via Chancellor Angela Merkel. Other demonstrators were mad about rumors of a vaccine plan by Bill Gates.

Stuttgart protest

An anti-vaccine protester in Stuttgart

German protests were led by several groups, including Resistance 2020 and COMPACT. The first group questions official government data on confirmed cases and deaths, and alleges the government is overinflating the data to seize more control over the population. The second group describes itself as a “sharp sword against imperial propaganda.”

“Why aren’t you telling us the truth, Mrs Merkel? How we are losing our freedom, jobs and health?” says COMPACT.

Folks on social media described the German protesters as “covidiots” who risk triggering a second wave of infections that could lead to extensions or stricter lockdowns. We noted last week that this would undoubtedly continue to crash Germany’s economy.

The economic effects of the countrywide lockdown have been devastating. Several weeks ago, we showed how the labor market had been obliterated.

Germany and other member states have begun to relax some lockdown restrictions, a move to restart the economy. Germany’s professional soccer league resumed games over the weekend without fans — as it appears reverting to pre-corona times will be a challenging and drawn-out process.

And for more color on reopening Europe, a border spat has erupted between Spain and France last week, suggesting a V-shaped recovery of the EU will not be seen this year.

Elsewhere, dozens of people in Poland were arrested for violating social distancing restrictions during protests. Police used tear gas to suppress demonstrators as the city of Warsaw said the gathering was illegal because there was no permit.

There have been further protests in Warsaw today against the government’s lockdown measures and alleged lack of support for businesses.

Like last week, police clashed with and detained some protesters, including an opposition senator, Jacek Bury pic.twitter.com/eLAU4Um7bR

— Notes from Poland 🇵🇱 (@notesfrompoland) May 16, 2020

Britain saw anti-lockdown and anti-vaccine protesters assemble in Hyde Park in central London and were met with police. Many chanted freedom songs and held signs blasting lockdowns. London Metropolitan Police Service arrested about a dozen people as police dispersed the crowd.

🚨 Jeremy Corbyn’s brother was arrested during an anti-lockdown protest in Hyde Park yesterday

📣 Piers Corbyn was heard claiming that 5G and coronavirus are linked

Anti-lockdown protesters were arrested in Hyde Park on Saturday at a rally to protest lockdown restrictions. While protesters faced off against police, others enjoyed a stroll round the London park pic.twitter.com/64wUOgBRjd

Our ripple is spreading! Be proud Michiganders that our outcry has boiled over to other states!

The image below is from the protest today called “ReOpen San Diego”. And they have an order in San Diego that says, “No gatherings of more than one person”.#StandUpMichiganpic.twitter.com/Z2VxBtE1DU

— barely informed with elad 🕵🏻♂️ (@elaadeliahu) May 16, 2020

Large crowd at the Reopen Long Island protest today in East Meadow. Most were not wearing masks and obviously very close to one another. The crowd even chanted at one point “No More Masks! No More Masks! Reopen Nassau!!!” pic.twitter.com/pY2bRzKNzz

If a second COVID wave triggers additional lockdowns in the Western world — people will likely become more infuriated with government and result in larger social demonstrations.

via ZeroHedge News https://ift.tt/2X7YcZf Tyler Durden