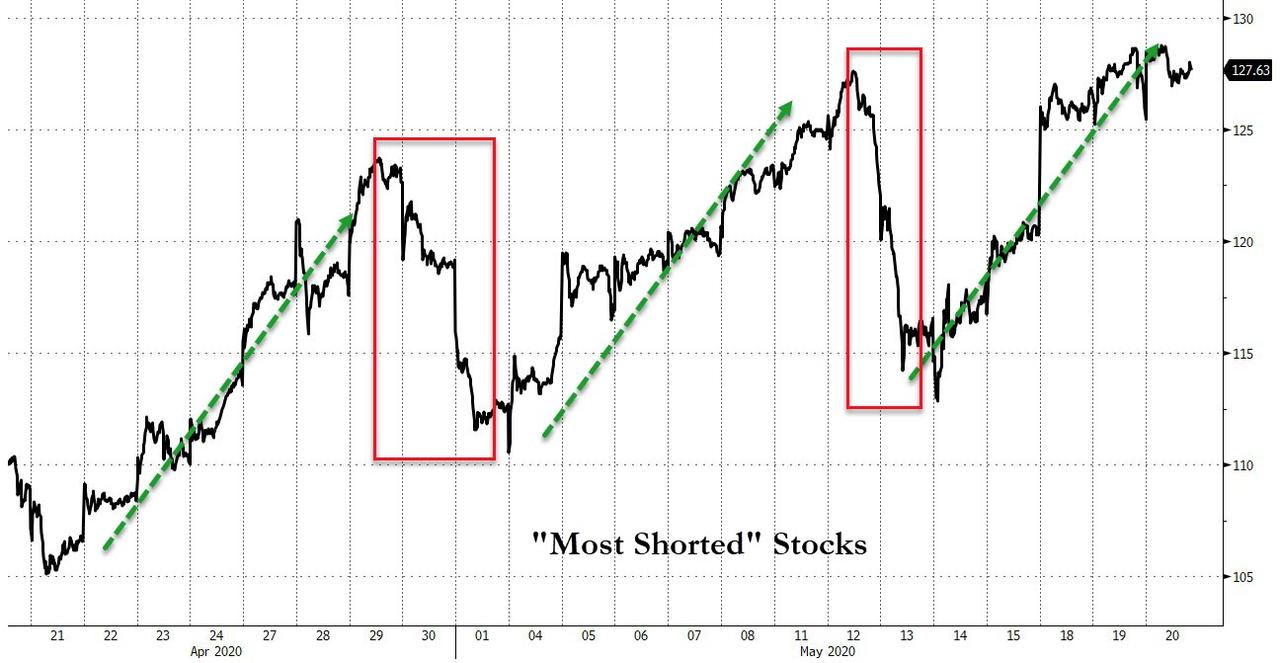

“The Data Is Disturbing” – Extreme Options Sentiment Flash Red Light For Stocks Tyler Durden

Wed, 05/20/2020 – 15:45

Stocks know something… they must do right? Remember, they’re a discounting mechanism… or some other such trite bullshit. They are nothing of the sort, as bond and commodity markets and fundamental earnings expectations signal quite clearly…

But “Fear not…” echo the halls of mirror and smoke vendors appearing on your education channels… Tomorrow, some other drug trial will announce the person its testing its virus on looks slightly happier, or a Central Banker will say something really market supportive like: “We’ve got lots of money and we want to give it to you so that markets don’t fall…”

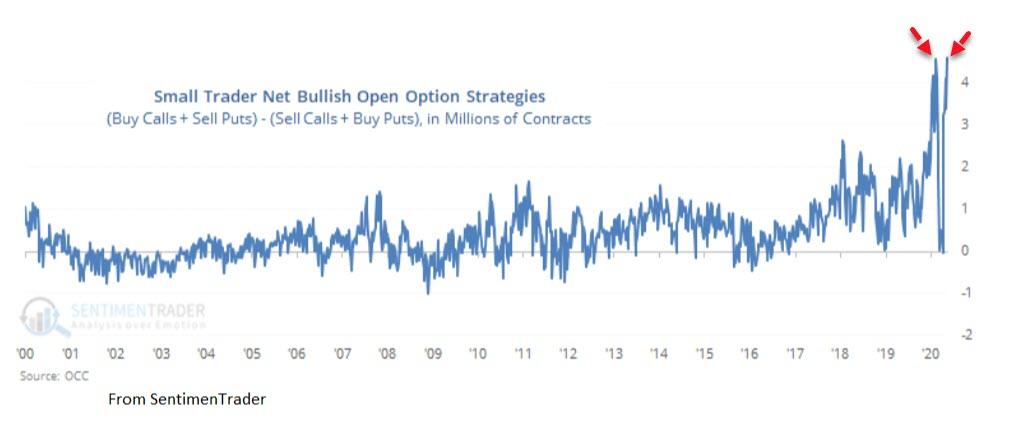

There’s just one thing (well a few, but let’s focus on this one). As Bloomberg reports, small options traders are bullish to a point that signals trouble for U.S. equities, according to Sundial Capital Research.

“Last week, the smallest of options traders, those with trades for 10 contracts or fewer at a time, opened a new record of net bullish positions,” Sundial President Jason Goepfert wrote in a note Tuesday.

In comparison, very large traders, those with trades of 50 or more contracts at a time, haven’t been betting so much on a rally, he said.

That has widened the spread between small- and large-trader net bullish positions to a record, with the gap jumping “like it did in 2008” in the past couple of weeks, he added.

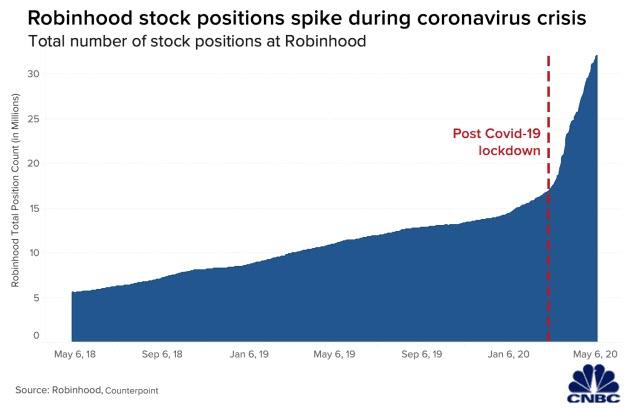

All of which reflects on the buying panic by small millennial retail buyers…

Extremes in the data have consistently led to poor market returns, Goepfert wrote.

“The data from last week is disturbing,” Goepfert wrote.

“It clearly shows that the smallest of traders, who tend to be the most consistently ill-positioned at extremes, have gone aggressively long, in a leveraged fashion.

This has a strong tendency to lead to lower prices over the short to medium term.”

“The big risk is that people are going to tire of this B/S.

Bank analysts and big investors trying to look past the vaccine/treatment noise, past the Central Bank puts, and focusing on fundamentals all say the same thing: Stocks are massively overvalued ahead of a looming recession. Corporate bond yields need to reflect rising default risk. Simple as. “

Trade accordingly.

via ZeroHedge News https://ift.tt/36eU128 Tyler Durden

The Defense Department should prepare to operate in a “globally-persistent” novel coronavirus (COVID-19) environment without an effective vaccine until “at least the summer of 2021,” according to a draft Pentagon memo obtained by Task & Purpose.

“We have a long path ahead, with the real possibility of a resurgence of COVID-19,” reads the memo, authored for Secretary of Defense Mark Esper but not yet bearing his signature.

“Therefore, we must now re-focus our attention on resuming critical missions, increasing levels of activity, and making necessary preparations should a significant resurgence of COVID-19 occur later this year.”

Despite its grim forecast, the draft document lays out a framework for the U.S. military’s proverbial reopening, which includes the resumption of training exercises, increased operational tempo, and the repositioning of forces and supplies to fight the global pandemic.

A Pentagon spokeswoman said the document was outdated but declined to provide more specifics.

The memo was prepared by Kenneth Rapuano, assistant secretary of defense for homeland defense and global security, and is intended to update previous guidance issued by Esper on April 1, 2020. It’s unclear if Esper has seen the memo.

The document has not been officially released, and could see changes since being circulated among the military services at the beginning of May for feedback, a defense official said on condition of anonymity.

“All indications suggest we will be operating in a globally-persistent COVID-19 environment in the months ahead,” the memo reads.

“This will likely continue until there is wide-scale immunity, through immunization, and some immunity post-recovery from the virus.”

The Pentagon framework for operations in a “persistent COVID-19 environment” relies on a number of assumptions, including the chance of successive waves of infection, continued shortages of personal protective equipment, and a lack of a viable treatment or vaccine for COVID-19 until at least next summer.

More waves of infection will occur “in clusters” that will coincide with the seasonal flu season, the memo suggests, while testing “will not provide 100% assurance of the absence” of the virus.

The planning framework detailed in the draft memo also calls for an increase in testing and surveillance, expanded contact tracing capabilities, and the use of a registry “to track and closely monitor outcomes of those infected with COVID-19.”

The memo stands in contrast to more optimistic assessments given by Trump administration officials, including Esper, who said Friday the Pentagon would “deliver by the end of this year a vaccine at scale to treat the American people and our partners abroad.”

“We’d love to see if we can do it prior to the end of the year,” President Donald Trump said Friday. “We think we’re going to have some very good results coming out very quickly.”

The top Pentagon spokesman later clarified the end of year timeline was merely “a goal.”

Meanwhile, Dr. Anthony Fauci, the director of the National Institute of Allergy and Infectious Diseases, recently stated that it’s “doable” to have a vaccine ready in January “if things fall in the right place.”

“Remember, go back in time, I was saying in January and February that it would be a year to 18 months, so January is a year, so it isn’t that much from what I had originally said,” Fauci said on NBC’s Today Show, adding that the goal is “aspirational.”

Army researchers also pointed to the 12-18 month timeframe for when a vaccine would be deemed safe to use in early March. But some experts say that even 12-18 months might not be enough time.

Dr. Amesh Adalja, a senior scholar and infectious disease physician at the Johns Hopkins University Center for Health Security, recently told the New York Times that “everything would have to go perfect” in order to have a vaccine by January 2021.

“Vaccine development doesn’t always go as predicted,” Adalja told the Times. “There are a lot of hiccups in the production process. We’re going faster than we ever have with a vaccine, but we have to be prepared for things to slow down once we get further along.”

via ZeroHedge News https://ift.tt/2AH1N9a Tyler Durden

JPM’s Kolanovic Finds Coronavirus Lockdowns “May Have Caused More Deaths” Than Covid-19 Itself” Tyler Durden

Wed, 05/20/2020 – 15:13

A certain subset of financial commentators who despise Trump and his policies yet are fervent adherents of Marko Kolanovic will have a real “cognitive dissonance” trying to rationalize and comment on the JPM quant’s latest observations on the coronavirus pandemic, in which he finds that “data favors further reopening” in line with what the administration is currently promoting.

Writing that “while the epidemic and markets largely followed our forecasts, politics emerged as a new and significant risk. Despite the conditions for re-opening being mostly met across the US” Kolanovic observes that this is “not yet happening in the largest economic regions (e.g. CA, NY, etc.)” Instead, while “the virus risk is abating globally, political/geopolitical fallout is emerging as a new risk. For example, just today the US senate passed a bill to bar Chinese companies from being listed on US exchanges.”

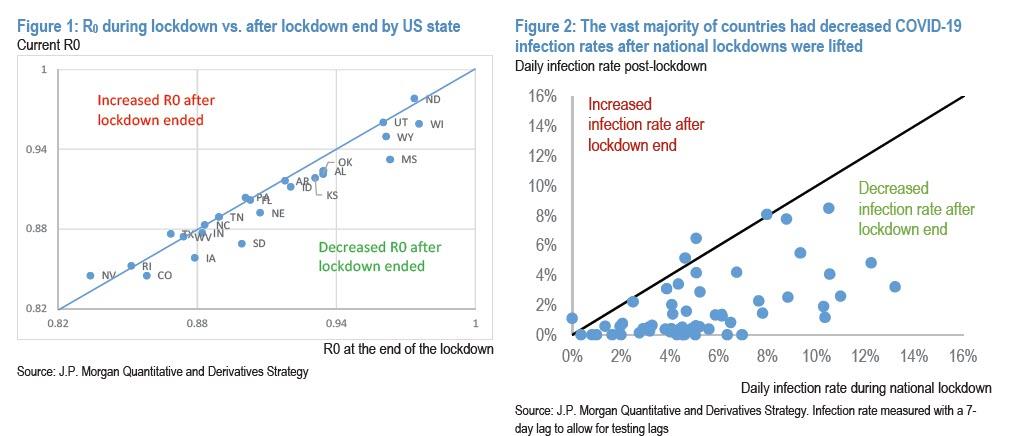

Mocking “flawed scientific papers [which] predicted several million virus deaths in the west”, an outcome which clearly has not happened (with the authors of said papers claiming that this is a result of the measures taken in response to their original forecasts), Kolanovic writes that “in the absence of conclusive data, these lockdowns were justified initially. Nonetheless, many of these efforts were inefficient or late” meanwhile more “recent studies indicate that full lockdown policies in some European countries did not produce any change pandemic parameters (such as growth rates R0) and hence might not have yielded additional benefits vs. less restrictive social distancing measures” where the case study of Sweden is most prominent.

Kolanovic elaborates on this point as follows:

Figure 2 below show virus spread rates before and after lockdown for different countries around the world, and Figure 1 shows the spread for US states that have re-opened. In particular, regression shows that infection rates declined, not increased, after lockdowns ended (for US states we show most recent R0 vs R0 on the day of lockdown end, and for countries we show infection rates). For example, the data in Figure 2 shows a decrease in infection rates after countries eased national lockdowns with >99% statistical significance. Indeed, virtually everywhere, infection rates have declined after reopening even after allowing for an appropriate measurement lag. This means that the pandemic and COVID-19 likely have its own dynamics unrelated to often inconsistent lockdown measures that were being implemented.

Further slamming the continuation of full lockdowns, Kolanovic then writes that “the fact that re-opening did not change the course of pandemic is consistent with mentioned studies showing that initiation of full lockdowns did not alter the course of the pandemic either. These virus dynamics are perhaps driven by the elimination of the most effective spreaders, impact on the most vulnerable populations such as in nursing homes, common sense measures unrelated to full lockdowns (such as washing hands, etc.)and weather patterns in the northern hemisphere, etc.”

To be sure, the lockdowns remained in place “while our knowledge of the virus and lack of effectiveness of total lockdowns evolved.” However, at the same time, “millions of livelihoods were being destroyed by these lockdowns. Unlike rigorous testing of potential new drugs, lockdowns were administered with little consideration that they might not only cause economic devastation but potentially more deaths than COVID-19 itself.“

At this point it is probably worth noting that if Kolanovic had a YouTube channel, he would promptly be banned for the heretical idea that lockdowns not only did not help with the containment of the disease, but lead to even greater suffering as a result of the “economic devastation” they encouraged – just ask the media’s army of “fact checkers” who are dead certain that being stuck at home for months is in your best interest – while creating a cottage industry if “utilitarian” experts who would shriek, at every opportunity, that collapsing GDP is a necessary price to pay if it meant Trump losing the re-election saving even a single human life. We wonder what said experts will say now that their epidemiological quant idol has dared to point out what was obvious to many from the start.

So how can one continue to justify stringent lockdowns in light of the above observations, Kolanovic asks, and correctly points out that “this question has divided the country“, listing some political implications of the lockdowns, including winners, losers, and the economic impact:

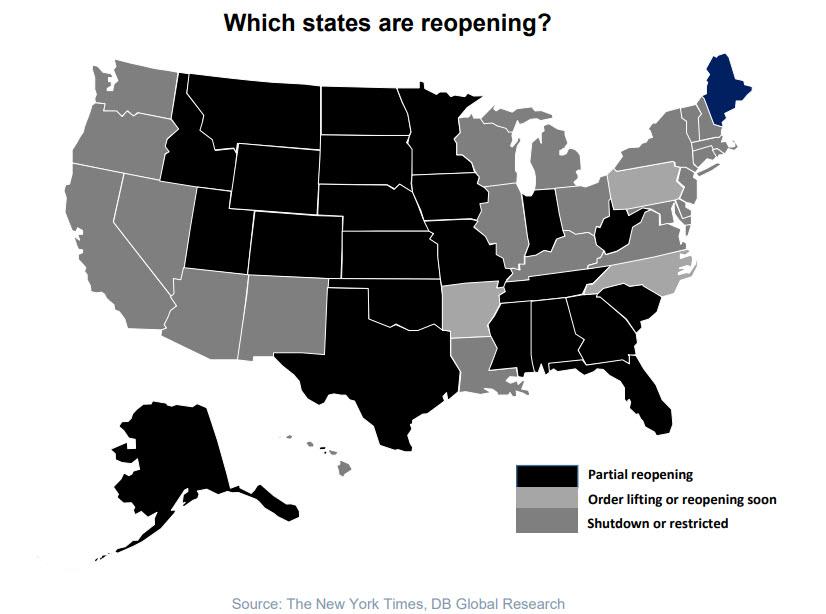

US Elections – Even before the worst of the pandemic hit the US, the response of the current administration to COVID-19 became a focal point of election campaigns (e.g. COVID-19 ads by then candidate Michael Bloomberg). Election logic and backtests would say, the worse the virus impacts the US, the lower the chances of an incumbent’s re-election given the economic pain, high unemployment and lack of health care during the pandemic. Indeed the initial response of the administration was to downplay the risk of the COVID-19 epidemic. However, since then, this simplistic thesis changed significantly. The administration shifted to forecasting a larger negative impact (setting the stage for them to ‘outperform’, and e.g. ‘hedging’ the Georgia reopening), shifting the pandemic blame to China and the WHO, and at the same time shifting the blame for economic pain to large blue states that are perceived to be slowing down the reopening of the economy. Indeed, allowed economic activity across the country is now largely following partisan lines.

This is correct, and is precisely what we said last week when we observed that “in recent days we have observed that this distinction has increasingly fallen along party lines, with democratic states refusing to reopen or happy to wait (and in the case of California warning it may be shut for another 3 months), while mostly Republican states already pursuing a partial or full reopening.”

We concluded by noting that “there will be a very substantial speed limit on the economic recovery, especially as Democratic states do everything in their power to delay reopening for as long as possible.”

Kolanovic then focuses on the economic interest of reopening vs continued shutdowns:

Economic interest – Clearly there are economic winners and losers of prolonged shutdowns and social distancing. Working remotely, software/cloud, online shopping and socializing, etc. all benefit large technology firms. It should not come as a surprise that large tech stocks are near all-time highs. This could create (perhaps wrong) perceptions of conflicts of interest when the leading technology firms are influencing policies related to reopening (such as reimagining education, health care, vaccines, contact tracking and tracing etc.).

This, too is correct, although we are puzzled by why Kolanovic hedges by saying that it is “perhaps wrong” that perceptions would be created that the tech megacaps are doing all in their power to prolong a “shutdown” status quo that benefits them while crushing small and medium businesses: those perceptions are 100% accurate, just take a look at the tremendous gains achieved by the FAAMGs in the past two months at the expense of all other corporations while millions of small and medium businesses, those who employ the vast majority of Americans, are now forced to subsist on monthly handouts from one of the the government numerous bailout programs.

Finally, and in a surprisingly political commentary for the JPM quant, he highlights the role of (big) government in the decision-making process:

Big vs. Small government – another political fault line exposed by COVID-19 is the role and scope of government in everyday life, encompassing questions such as: should lockdowns be recommended or mandated, how much of individual freedoms should be limited, etc. Government employees have been less affected by lockdowns than e.g. small private businesses, etc. Moreover, these ideological fault lines exposed by COVID-19 are to an extent replicated and exported to other countries in the west.

Come on Marko, say it: almost as if liberals, socialists and other proponents of continued lockdowns have a vested interest in keeping the economy shut and the population locked down, while feeding stimulus scraps to the population, pursuing the socialist theory of helicopter money (MMT), all in the pursuit of that inevitable flare up of inflation that the global economy has been desperately seeking to spark for the past decade, yet failing.

After reading this we wonder: is the libertarian, and far more provocative, Marko finally stirring in hopes of waking up from a 3-year hibernation? At this rate, we may soon see a report by the JPM quant asking if – with certain vested interests across the west benefiting extensively from the outcome of the coronavirus shutdowns – the entire pandemic wasn’t, in fact a plandemic?

Of course, Kolanovic couldn’t leave it hanging at that very key question, and so in his conclusion he reverted to what he hedged may be the big risk to his optimistic outlook on the economy, namely that “political/geopolitical fallout is emerging as a new risk”, and specifically the renewed escalation in US-China tensions as the obvious outlet from the coronacrisis, where both regimes are now accusing each other of starting and facilitating the global economic disaster, resulting in an unprecedented collapse in diplomatic relations:

On the other side of the political spectrum, demagogues and radicals across the world will be tempted to use COVID-19 to blame immigrants, people of different race, or use the pandemic as a pretext to intensify geopolitical tensions. Blaming the pandemic on an ethnic group or country can provide a convenient excuse for various failings at home, or may provide pretext to push a geopolitical or protectionist agenda. This is perhaps even more dangerous than using the pandemic to further domestic political outcomes.

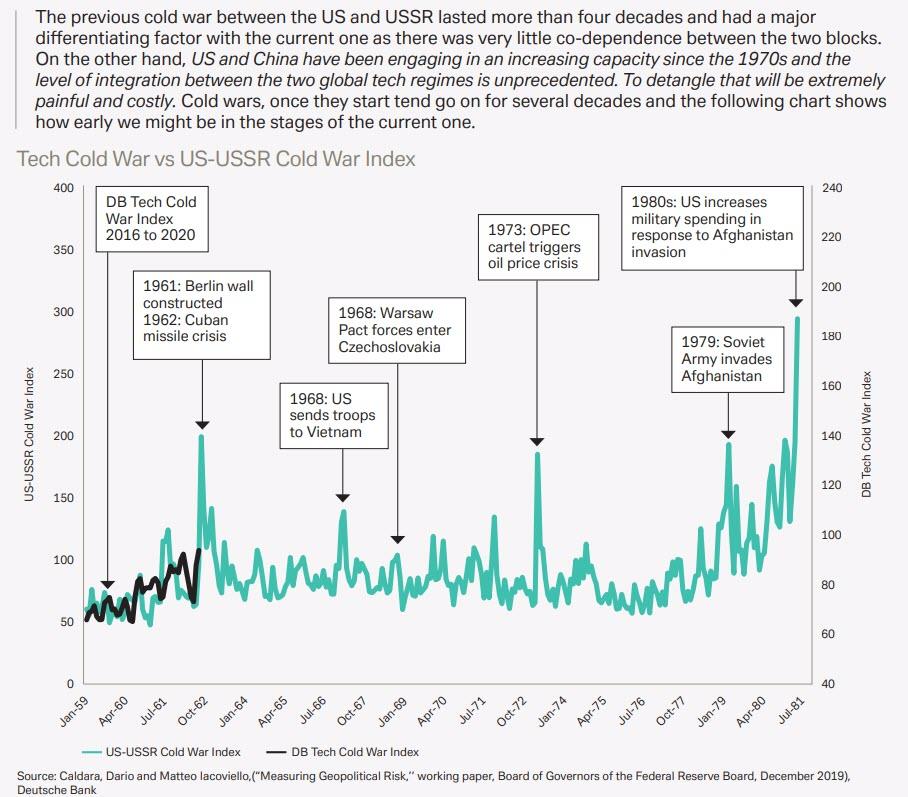

Well, if Marko won’t say it, we will, or rather we will let Deutsche Bank say it, because it hardly takes rocket surgery to extrapolate that the current cold war state between the US and China has just one obvious outcome.

via ZeroHedge News https://ift.tt/3dY8XEm Tyler Durden

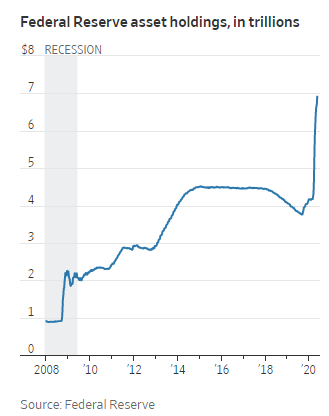

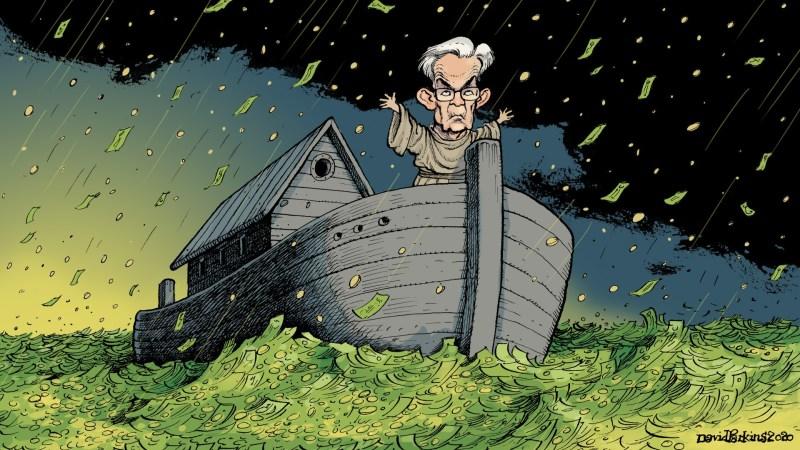

The Fed’s $600 Billion Middle Market “Main Street” Lending Facility Is A Total Disaster Tyler Durden

Wed, 05/20/2020 – 14:52

The Fed is currently undertaking one of the trickiest projects it has ever taken on: lending $600 billion directly to companies that need it. It’s an area where the Fed hasn’t really ventured, as the WSJ points out, and one that puts them far closer to the realm of directing fiscal policy in the country than they have ever been.

In other words, it’s a political and financial headache – even for the Fed.

The goal of the program is to get cash to companies that are too large to get small business loans, but too small to benefit from the Fed’s other genius programs, like buying junk bond ETFs.

The Fed’s middle market “Main Street” program instead allows companies to get loans from banks, who turn around and sell up to 95% of the debt to the Fed. In other words, the Fed is hell-bent on becoming the world’s worst counterparty.

The move is part of a broader response by the Fed, who initially sought to un-freeze credit markets after the coronavirus pandemic started. According to former Fed chair Ben Bernanke, the Fed’s biggest challenge is now “making these programs work”.

A major challenge is the obvious: how do you make the Fed’s balance sheet become more than just a dumping ground for toxic loans? Former Fed chair Janet Yellen even addressed that issue: “The Main Street program is going to be tremendously complicated. One of the problems with this program is that it may turn out to be insufficiently generous.”

The Fed remains sensitive to political blowback, like the kind it faced after 2008, which could be prompting them to do far more than they need – or should – be doing. Regardless, the political buy-in remains key for the Central Bank. Chicago Fed President Charles Evans said: “It’s very important if you’re going to engage in this, that you get take-up.”

The Fed says it is working to “fine tune” the program. “We’re learning as we go,” said Fed Chairman Jerome Powell last week. Meanwhile, the Fed has had to use “special powers granted by congress and the Hoover administration” to make these types of loans.

The Main Street program, which is a result of discussions between Jay Powell and Steve Mnuchin, is open to companies with up to 15,000 employees or less than $5 billion revenue. More than 19,000 companies had between 500 and 15,000 employees in 2017 and they collectively employed between 30 and 40 million people.

Under the program, banks can lend up to $25 million in new loans or refinance up to $200 million in an existing loan if a firm’s total debt. Senator Mark Warner has been advocating for loan forgiveness in the program – also known as just handing out billions of dollars in free money – but the Fed has pushed back. Barely.

Other economists have suggested that perhaps the Fed loosen eligibility terms and lower the rate it charges borrowers. The Fed has already modified the terms of the program to allow larger companies and companies with larger debt loans to qualify.

For David French, senior vice president of government relations at the National Retail Federation, that still isn’t enough: “While those are positive steps, they still have left in place a default bias against assuming too much risk in this program, and as long as that bias is in place, they’re sending the wrong signal to banks about making these loans.”

Mnuchin responded: “I don’t view the success of Main Street as whether we originate $50 billion or $500 billion. The measure of success is, ‘Do companies have access to capital, either through the facilities or the banks?’”

Warner said: “Most of my colleagues presumed that all of the Cares money would be spent and not recouped. What happens if this facility is set up and nobody comes? It’s a valid concern.”

“The Fed has lending powers, not spending powers,” Powell meekly concluded last week.

via ZeroHedge News https://ift.tt/3e1yDju Tyler Durden

The infamous story of Joe Biden’s effort to force the firing of Ukraine’s chief prosecutor in 2016 has taken a new legal twist in Kiev, just as the former vice president is sewing up the 2020 Democratic presidential nomination in America.

In Kiev late last month, District Court Judge S. V. Vovk ordered the country’s law enforcement services to formally list the fired prosecutor, Victor Shokin, as the victim of an alleged crime by the former U.S. vice president, according to an official English translation of the ruling obtained by Just the News.

The court had previously ordered the Prosecutor General’s Office and the State Bureau of Investigations in February to investigate Shokin’s claim that he was fired in spring 2016 under pressure from Biden because he was investigating Burisma Holdings, the natural gas company where Biden’s son Hunter worked.

The court ruled then that there was adequate evidence to investigate Shokin’s claim that Biden’s pressure on then-President Petro Poroshenko, including a threat to withhold $1 billion in U.S. loan guarantees, amounted to unlawful interference in Shokin’s work as Ukraine’s chief prosecutor.

But when law enforcement agencies opened the probe they refused to name Biden as the alleged perpetrator of the crime, instead listing the potential defendant as an unnamed American.

Vovk ruled that anonymous listing was improper and ordered the law enforcement agencies to formally name Biden as the accused perpetrator.

The ruling orders “a competent person of the Office of the Prosecutor General of Ukraine who conducts procedural management in criminal proceedings No. 62020000000000236 dated February 24, 2020 to enter information into the Unified register of pre-trial investigations … a summary of facts that may indicate the commission of a criminal offense under Paragraph 2 of Article 343 of the Criminal procedure code of Ukraine on criminal proceedings No. 62020000000000236 dated February 24, 2020, namely: information on interference in the activities of the former Prosecutor General of Ukraine Shokin, Viktor Mykolaiovych performed by citizen of the United States of America Joseph Biden, former U.S. Vice President.”

The judge added, “the order of the court may not be appealed.”

Shokin’s attorney, Oleksandr Ivanovych Teleshetskyi, confirmed the ruling to Just the News but said Ukraine officials have not yet complied.

“Viktor Shokin publicly appealed to the president of Ukraine with a request to properly respond to illegal inaction in the investigation of criminal cases that are open against Joseph Biden,” Teleshetskyi said. “Let me remind you that they were discovered precisely as a result of the statement of Viktor Shokin.”

The Biden-Shokin saga has dominated headlines for more than a year, and played a central role in the Democrat-led impeachment proceedings that ended earlier this year with President Trump’s acquittal in the Senate.

Biden has admitted on videotape he forced then-Ukraine President Poroshenko to fire Shokin in March 2016 by threatening to withhold $1 billion in U.S. loan guarantees. But Biden has steadfastly denied Shokin’s firing was due to the Burisma case. Instead, Biden said, he and other Western leaders believed Shokin was ineffective as a corruption fighter.

Shokin, however, has alleged in a court affidavit he was told he was fired because he refused to stand down his investigation of alleged corruption by Burisma and after he planned to call Hunter Biden as a witness to question him about millions of dollars in payments his American firm received from the Ukraine gas company.

Shokin has also disputed Democrats’ claims he was fired because he was incompetent or corrupt, producing among other pieces of evidence a letter from the U.S. State Department in summer 2015 that praised his anti-corruption plan as Ukraine’s chief prosecutor.

While the Biden-Shokin factual dispute remains unresolved, the impeachment trial last year generated testimony from State Department witnesses who said they believed Hunter Biden’s role at Burisma while his father oversaw U.S.-Ukraine policy created an uncomfortable appearance of a conflict of interest.

Both Bidens have denied wrongdoing but acknowledged they wished they had handled the matter differently.

Shokin’s continued pursuit of a case in the Ukraine courts could prompt new disclosures this summer as Biden readies for the fall election against Trump.

In an interview, Shokin told Just the News he is confident he can unearth evidence during the proceedings that Ukraine officials were satisfied with his performance and simply acceded to firing him to avoid losing the badly needed U.S. loan guarantees.

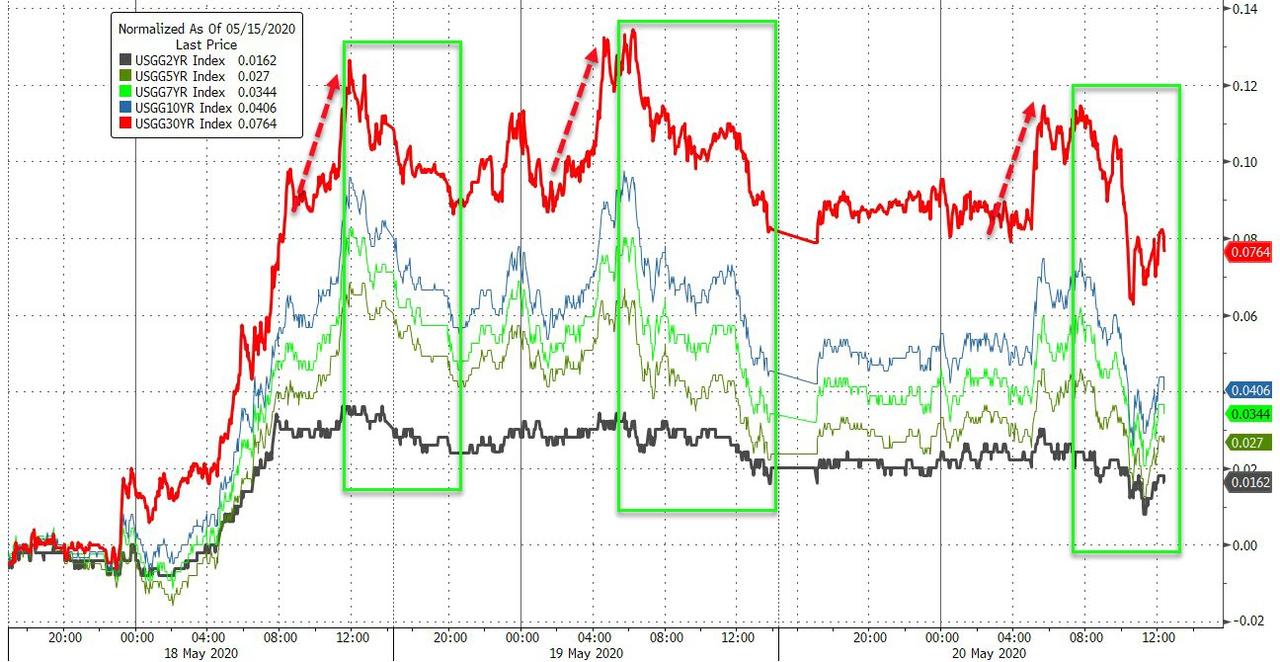

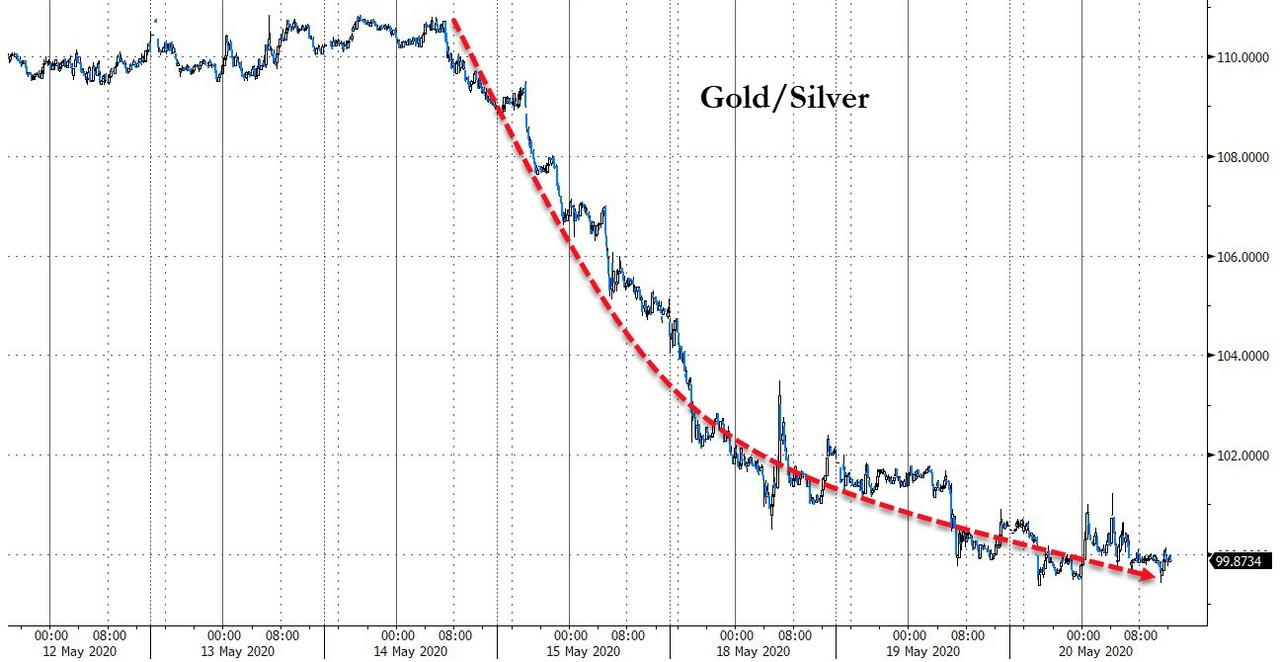

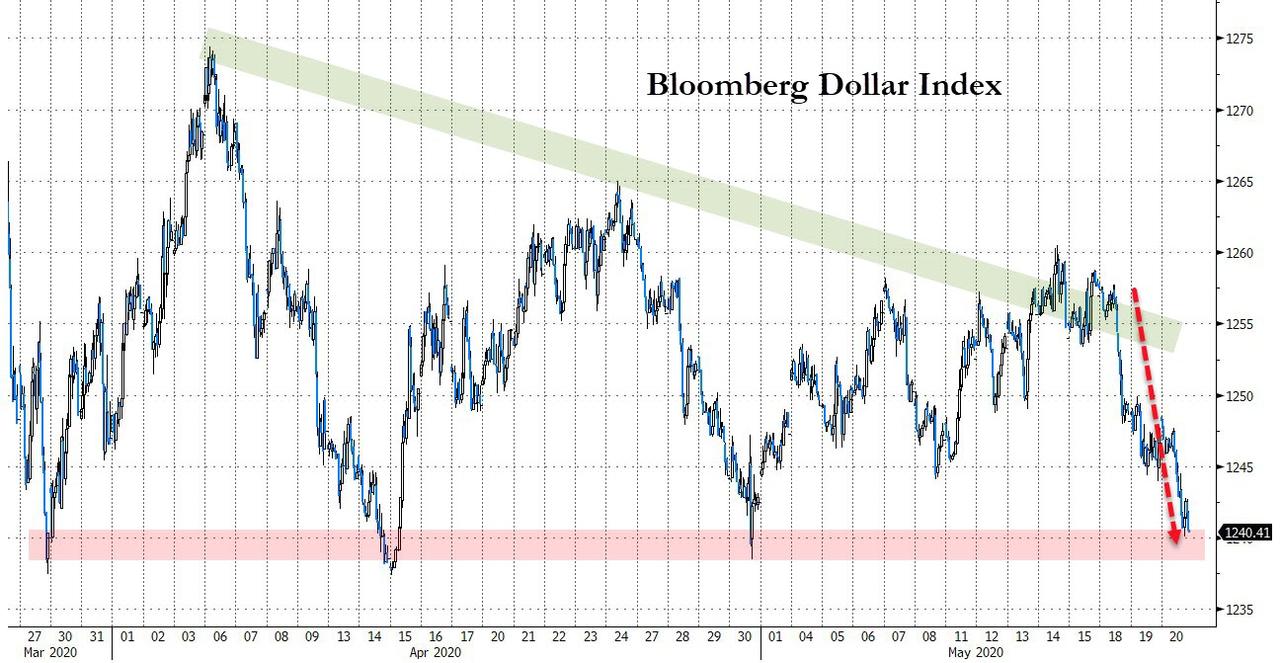

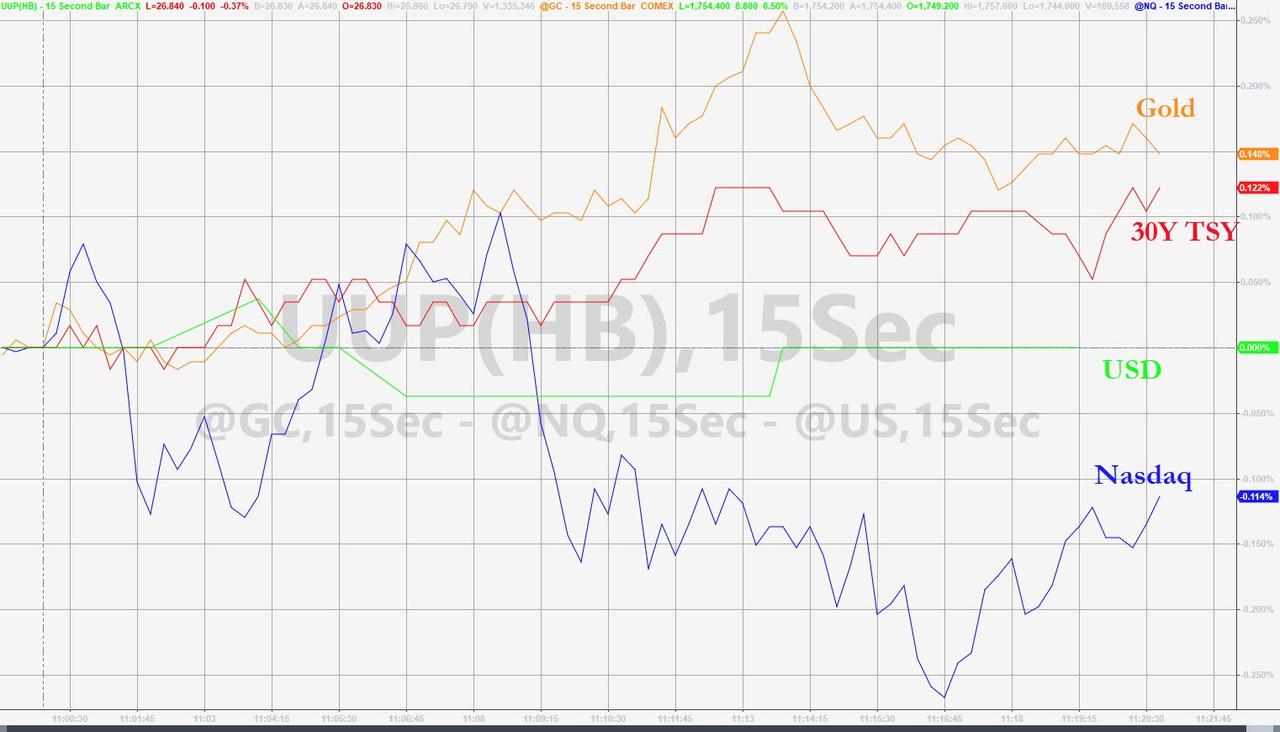

Stocks are modestly lower, the dollar is flat, but gold and bonds are bid after the Fed Minutes showed a nervous Fed willing to do anything and worried about banks…

The main item on the agenda was the possibility of yield curve control and for now rates are lower across the curve.

via ZeroHedge News https://ift.tt/2TnGQ9W Tyler Durden

Gold (and silver) also rallied as the dollar leaked lower since the relatively dovish (if its possible to get any more dovish) statement.

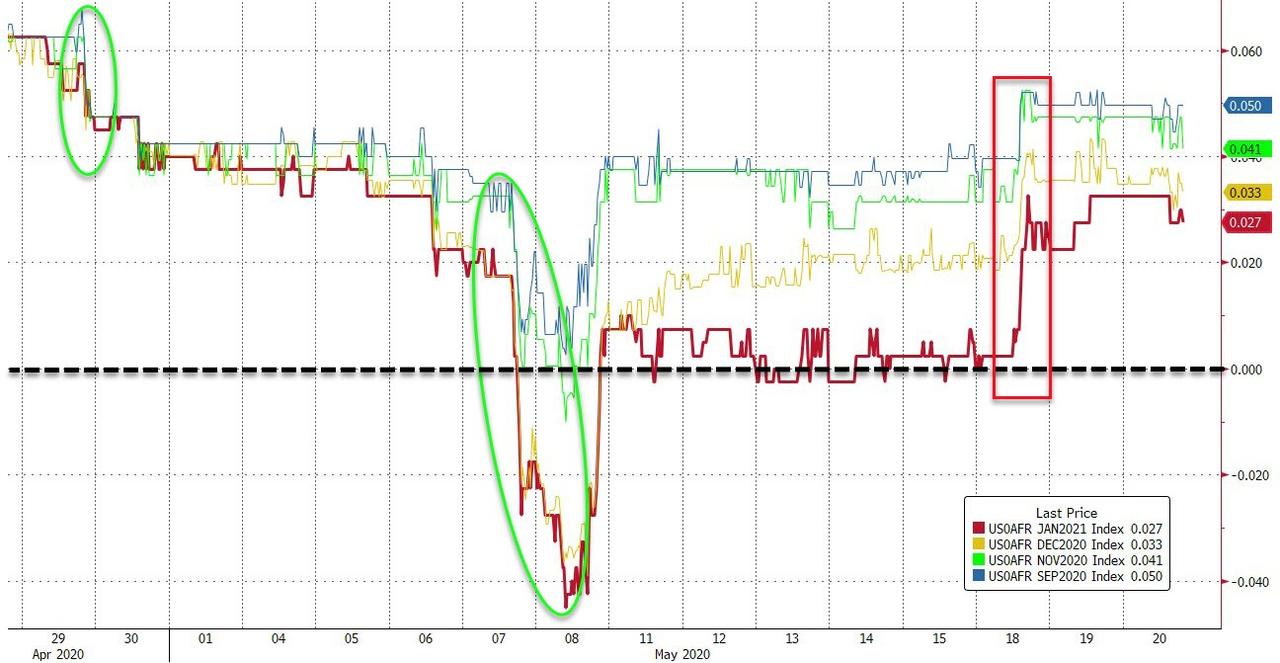

And despite The Fed’s desperate efforts to talk down the possibility of negative rates, expectations for such rates have increased since the last FOMC…

Source: Bloomberg

Realistically, given that the minutes follow a presentation on Tuesday from Chair Powell and also many officials have spoken on the record in public since the meeting, the room for new developments is small.

In fact, as Joseph Trevisani, Senior Analyst at FXStreet, argues, “discussions in the edited minutes may seem somewhat out of date as the national conversation in the almost three weeks since the meeting has rapidly moved from the revelations of the economic debacle to the apparent success of several states in reopening parts of their economies and considerations about the criteria for opening the others.”

Additionally, The Fed took the historic step of beginning purchases of ETFs invested in corporate bonds on May 12, so any discussion of that at the April meeting could be informative; and that has happened as The Fed has already wound its unlimited bond-buying program down to $6 billion of daily Treasury purchases, from a peak of $75 billion in mid-March.

Of course, we don’t truly expect any mention of the increasingly difficult-to-rationalize dichotomy between improving financial conditions (as a result of the Fed and the U.S. government’s massive stimulus) and the ongoing pain in the real economy; but it would be nice to see some rational thinking at the table. As Julian Emanuel, BTIG’s chief equity and derivatives strategist, warned, “The Fed’s Bigger Boat cannot substitute for the consumer’s need to feel safe enough to send kids to college, eat in restaurants, or get on an airplane.”

But, the minutes really focused on Federal Reserve officials’ growing distress at the economic implications of the coronavirus pandemic last month, which sent unemployment soaring and froze swaths of commercial activity.

On the virus’ impact:

“Participants noted that the coronavirus outbreak was causing tremendous human and economic hardship across the United States and around the world. The virus and the measures taken to protect public health were inducing sharp declines in economic activity and a surge in job losses. “

On outcome-dependent forward guidance…

“For example, the Committee could adopt outcome-based forward guidance that would specify macroeconomic outcomes – such as a certain level of the unemployment rate or of the inflation rate – that must be achieved before the Committee would consider raising the target range for the federal funds rate.”

Others favored basing forward guidance on a timeline:

“The Committee could also consider date-based forward guidance that would indicate that the target range could be raised only after a specified amount of time had elapsed. These participants noted that such explicit forms of forward guidance could help ensure that the public’s expectations regarding the future conduct of monetary policy continued to reflect the Committee’s intentions.”

Additionally, Fed officials “raised concerns that banks could come under greater stress.”

Participants were concerned that banks could come under greater stress, particularly if adverse scenarios for the spread of the pandemic and economic activity were realized, and so this sector should be monitored carefully. Participants saw risks to banks and some other financial institutions as exacerbated by high levels of indebtedness among nonfinancial corporations that prevailed before the pandemic; this indebtedness increased these firms’ risk of insolvency.

And raised questions on limiting dividends…

“A number of participants emphasized that regulators should encourage banks to prepare for possible downside scenarios by further limiting payouts to shareholders, thereby preserving loss-absorbing capital.

Indeed, historical loss models might understate losses in this context. A few participants stressed that the activities of some non-bank financial institutions presented vulnerabilities to the financial system that could worsen in the event of a protracted economic downturn and that these institutions and activities should be monitored closely.”

But the highlight appears to be the discussion that “forward guidance could be more explicit” in the context of “capping” yields at short-to-medium term maturities, i.e. imposing Yield Curve Control which the US had in the late 1940s (see the Fed-Treasury accord), which Japan has of course popularized in recent years, and which Zoltan Pozsar said is coming sooner or later:

“A few participants also noted that the balance sheet could be used to reinforce the Committee’s forward guidance regarding the path of the federal funds rate through Federal Reserve purchases of Treasury securities on a scale necessary to keep Treasury yields at short-to medium-term maturities cappedat specified levels for a period of time. “

The Chinese Virus began infiltrating the United States in early 2020, but the communist country already had a foot in the door well before then.

In the last year, Campus Reform has covered multiple instances of U.S. law enforcement officials charging professors and students with lying about their ties to China while conducting U.S.-funded research and even attempting to smuggle U.S.-funded researched to China.

A University of Kansas associate professor and researcher was indicted for allegedly lying about his ties to China while conducting U.S.-funded academic research.

The Harvard University chemistry department chair was arrested for his alleged ties to a Wuhan, China laboratory, where he was paid up to $1.5 million to build the lab, plus an additional $50,000 per month.

An Emory University associate professor and medical researcher was charged in late 2019 with allegedly lying about his employment at a Chinese university while simultaneously working at Emory. He pleaded guilty in May 2020.

A University of Arkansas professor was charged with lying to federal authorities about his ties to China while conducting U.S.-funded academic research.

A UT-Knoxville associate professor and researcher was charged in February with lying to the federal government about his connections to Chinese universities in order to receive a federal research grant.

A Chinese national medical student at Harvard University’s Beth Israel Deaconess Teaching Hospital was arrested in December for allegedly attempting to smuggle vials of cancer research out of the U.S. on a flight to Beijing, China.

Former WVU professor James Lewis pleaded guilty to working for a Chinese university without disclosing the information. The former academic had taken paternity leave but then used the time off to board a plane for China, without his child.

Not only has China attempted to gain a foothold on American university campuses through professors and students, but the communist regime has also targeted dozens of campuses nationwide by paying to open what are known as Confucius Institutes. Campus Reform has covered these centers extensively.

Below, you can see an interactive map of the locations of each Confucius Institute below.

via ZeroHedge News https://ift.tt/2AGMBsE Tyler Durden

“Somebody Is Dumping Everything”: Mystery Investor Pukes $333M In Real Estate ETF In Dark Pool Trade Tyler Durden

Wed, 05/20/2020 – 13:30

Post-coronavirus pandemic, nobody really knows what the real estate market will look like. Will people travel less? Will we work from home more often? Will commercial and residential real estate be able to keep their respective bids once current leases run out?

We’ve found at least one investor who doesn’t want to stick around and find out.

One “mystery investor” blew out more than 10.5 million shares of an S&P 500 Real Estate fund last week, representing a $333 million sale. This amounts to about 7.4% of outstanding shares in the Real Estate Select Sector SPDR Fund, a macro indicator of the industry’s largest companies, according to The Real Deal.

One anonymous investor commented: “That is obscene. It would be like Warren Buffett selling Delta all at once. A very large institution is expecting widespread weakness across the real estate market, more so than is already perceived.”

The fund trades under the symbol XLRE and includes holdings like Prologis and Equity Residential and AvalonBay Communities. At least half of its shareholders are institutional investors, including names like BlackRock and Merrill Lynch, TRD notes.

The trade was made on one of the 53 dark pools registered with the SEC, which is probably why it escaped investor scrutiny when it happened. Per regulations, dark pools only have to report the transaction as it happened and not the names of the parties involved in buying and selling. To that end, the seller remains a mystery.

The trade was confirmed, however, by Stefanie Kammerman, a former trader at Schonfeld Securities, from a dark-pool data feed. She said the shares were sold below the market price and that about 20 minutes before the trade, another entity sold 991,700 shares of the XLRE at the same price in a similar transaction. The ETF, meanwhile, was up about 5% on the day.

“It’s very odd there’s anything big on [XLRE],” she commented about the trade. “It looks like somebody’s dumping everything in my opinion. There’s something very big going on.”

via ZeroHedge News https://ift.tt/2Xe2Tku Tyler Durden