Muscle’d Out: Gold’s Gym Files For Chapter 11 Due To Government Lockdowns

Gold’s Gym International Inc. filed for Chapter 11 on Monday (May 4) as a way to “facilitate the financial restructuring of the company” after nationwide lockdowns resulted in its inability to service debt payments, read a company press release.

The gym operator filed for bankruptcy in Dallas, Texas, and noted in the filing that it has $100 million in assets and liabilities. The company will continue to operate during the restructuring process:

“We want to be 100 percent clear that Gold’s Gym is not going out of business,” President and CEO Adam Zeitsiff said in a press release. “The brand is strong, and we’ll continue to innovate and grow our digital business, our licensing program and our global footprint as we focus on serving our millions of members across the world.”

Here’s a message from the President and CEO Adam Zeitsiff on today’s bankruptcy filing…

The gym operator said its financial difficulties stem directly from coronavirus lockdowns and said it believes it will remerge from bankruptcy proceedings by the start of August.

“This has been a complete and total disruption of every one of our business norms, so we needed to take quick, decisive actions to enable us to get back on track,” the company said.

The restructuring will only impact company-owned locations, which represent roughly 10% of the 700 locations around the world.

Last month, the company closed 30 locations across the US. This included gyms in Alabama, Colorado, Missouri, Texas, Oklahoma, North Carolina, and South Carolina. At the time, it blamed virus-related shutdowns for its rapid financial deterioration.

Not too long ago, 24 Hour Fitness said it was preparing to restructure. As Americans are confined to their homes in the lockdown, with an increasing number of them canceling gym memberships and opting for a Peloton bike. We noted a little more than a week ago that one Peloton spin class had a record number of riders for a live class, drawing in more than 23,000 riders.

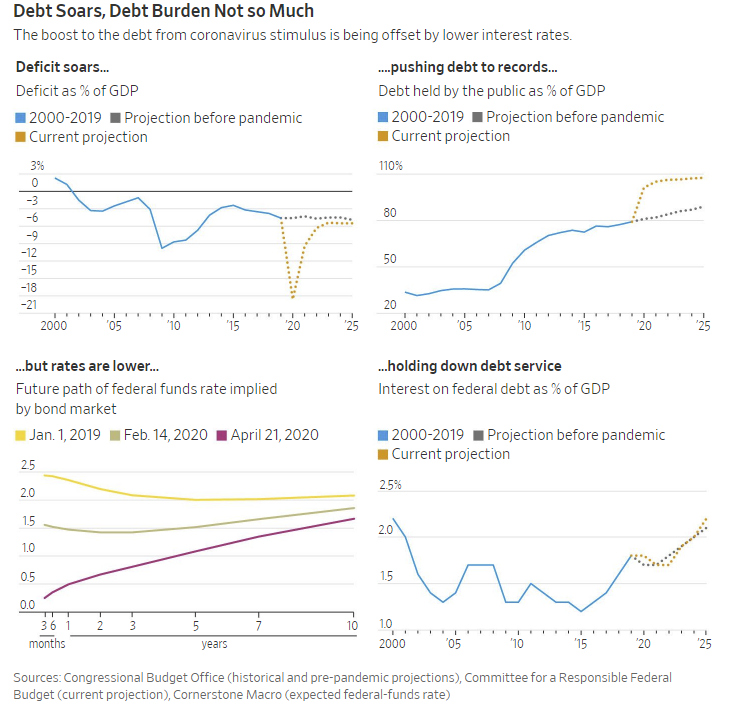

That was the question recently posed by Ben Carlson who laid out several arguments as to why spiraling Government debt may not matter.To wit:

“Is this debt so unsustainable it’s going to wreck future generations and leave them holding the bag? Are we really screwing the grandkids?

Although absolute debt heading into this crisis was high, you could argue we’ve never been in a better position to add debt to the country’s balance sheet. Generationally low interest rates and subdued inflation make for a perfect opportunity to add debt during this type of crisis.”

The Conundrum

On the surface it certainly seems to be a reasonable argument. However, while everyone is in a hurry to rationalize the need to take on trillions in debt, no one is discussing either the consequences of such actions, or more importantly how, to reverse the process.

Ben’s view on debt is not unique. The WSJ maintains a similar view.

“The usual fear is that high government debt leads to a crisis or excessive inflation. But there’s little risk of the first, and nothing inevitable about the second. It depends on choices to be made by the Federal Reserve and, indirectly, Mr. McConnell, since he has some say in who sits on the Fed.”

“This doesn’t mean all that added debt is necessary or being put to its best possible use. It does mean it’s not doing much harm. ‘Interest rates have been trending down for 30 years,’ said Doug Elmendorf, a former director of the Congressional Budget Office who is now dean of the Harvard Kennedy School.

‘That doesn’t just make it manageable to have more debt. It’s a signal that the economic costs of that debt, in terms of crowding out private borrowers, is particularly low.’”

Debt Isn’t A Solution

I would readily agree with both views had the U.S. been fiscally responsible to start with. As I warned repeatedly in 2019:

“With the economy, and the financial markets, sporting the longest-duration in history, simple logic should suggest time is running out.

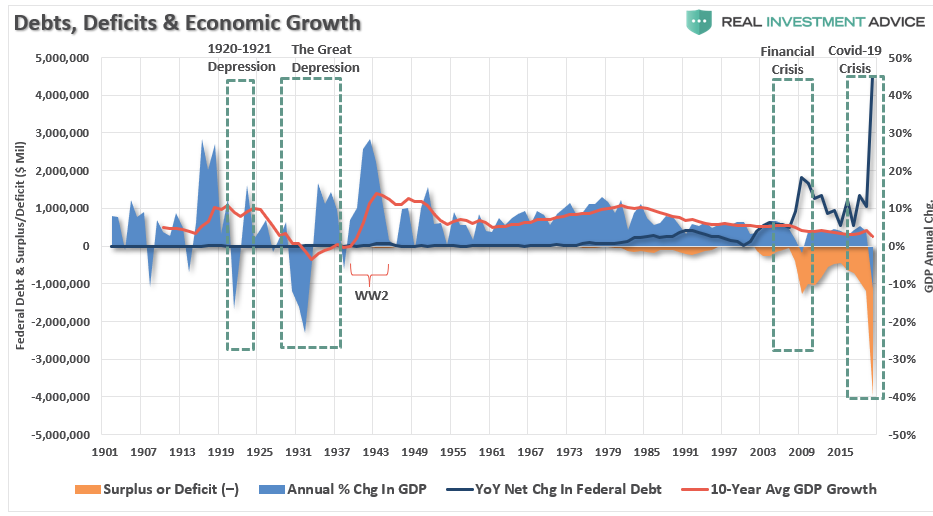

Politicians, over the last decade, failed to use $34 trillion in monetary injections, near-zero interest rates, and surging asset prices to refinance the welfare system, balance the budget, and build surpluses for the next downturn.

Instead, they only made the deficits worse, and the U.S. economy will enter the next recession pushing a $2 Trillion deficit, $24 Trillion in debt, and a $6 Trillion pension gap, which will devastate many in their retirement years.”

Unfortunately, my forecast proved overly optimistic.

Over the next few quarters, the U.S. will push a $4 trillion deficit as Government debt surges toward $27 trillion.

It’s a bit mind-boggling, considering in:

2007, the Senator Barack Obama chastised President George Bush for adding $4.5 trillion to the national debt during is 8-year term.

2016, Donald Trump railed on Barack Obama for adding $9 trillion to the debt load during his two terms as President.

2020, the media is now making excuses for adding $9 trillion in debt in just 4-years.

While it is true that generationally low interest rates seems to make running higher debt levels relatively “risk-free,” this is only because the right question isn’t being asked.

Why Are Interest Rates So Low?

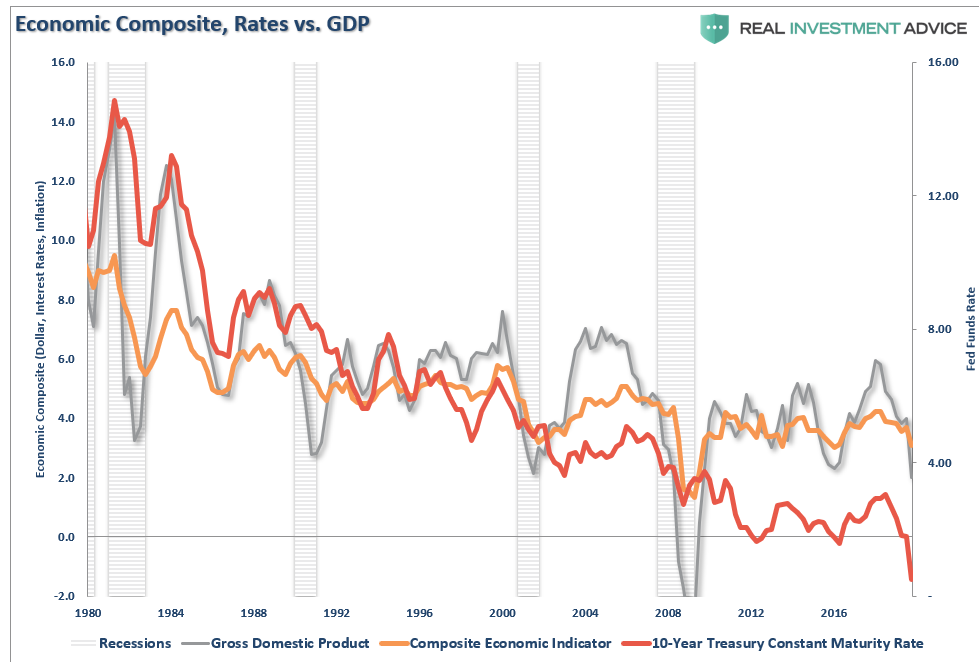

Interest rates don’t operate in isolation.

Rates are a function of three primary factors: economic growth, wage growth, and inflation. The relationship can be seen in the chart below. The composite economic indicator is the composite of the three components.

Understanding that interest rates are a reflection of economic growth, we can view the impact of debt on the growth of the economy.

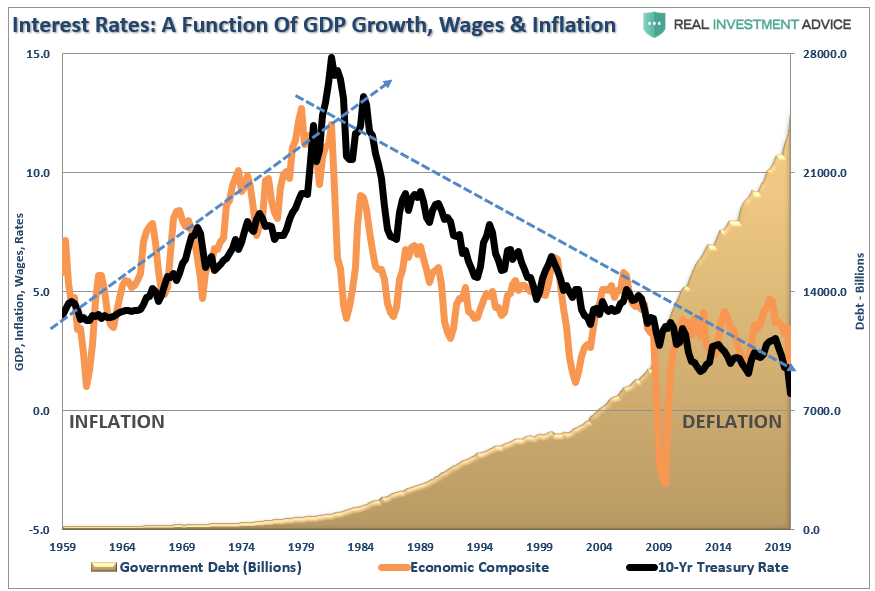

Not surprisingly, prior to 1980, economic growth rates rose as production led to rising incomes and demand. Since debt, and debt to income ratios, were relatively non-existent, savings were reinvested back into economy.

However, beginning in 1980, the view by Government that debt had no consequences, led to 40-years of deflationary pressures, slower economic growth, and ultimately lower interest rates.

Not Just A U.S. Problem

Global economies are currently holding nearly $78 trillion in debt, with nearly 20% of that debt sporting negative interest rates. If the theory “debt has no consequences” and “low interest rates are beneficial,” held true, then those economies should be surging.

However, that isn’t the case. Over the last decade annual GDP growth has remained weak growing at less than 3% annually. Deflation has remained a constant burden with wage growth almost non-existent.

What has risen rapidly? Wealth inequality.

Not surprisingly, we are caught in a “liquidity trap.” Lower interest rates fail to increase economic growth, and any contraction in monetary accommodation results in an almost immediate economic downturn.

Inflation Isn’t The Answer

“Inflation is one way out of this debt as the purchasing power of the money you’re paying back on the debt gets lower over time. This is the reason inflation is the biggest risk to bondholders over time.

If we have to worry about inflation in a few years I view that as a good problem to have because it means we beat this thing and people are out spending money again and wages are rising.

The second way out of debt is simply growing the economy, something we have been very good at over the long haul.”

Taken out of context, such would certainly seem to be the case.

In an economy driven by debt, a rise in inflationary pressures would also be coincident with an increase in interest rates. As we have repeatedly seen in recent history, even small increases in interest rates leads to rapid declines in economic activity.

Ben is correct that rising inflation does diminish the value of the dollar, which is where inflation comes from. However, inflation also reduces the purchasing power of wages. This is problematic when wages have not grown for workers over the past 20-years.

Since debt does not increase economic growth, but retards it as it diverts dollars away from productive investments into debt service, it is hard to suggest we can “grow our way out of debt.”

Otherwise, we would have done it by now.

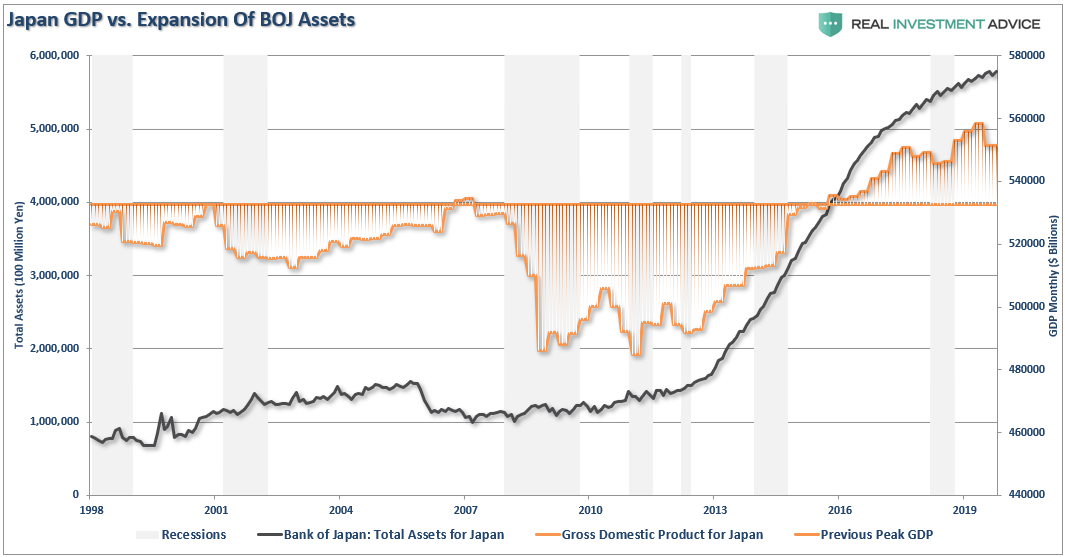

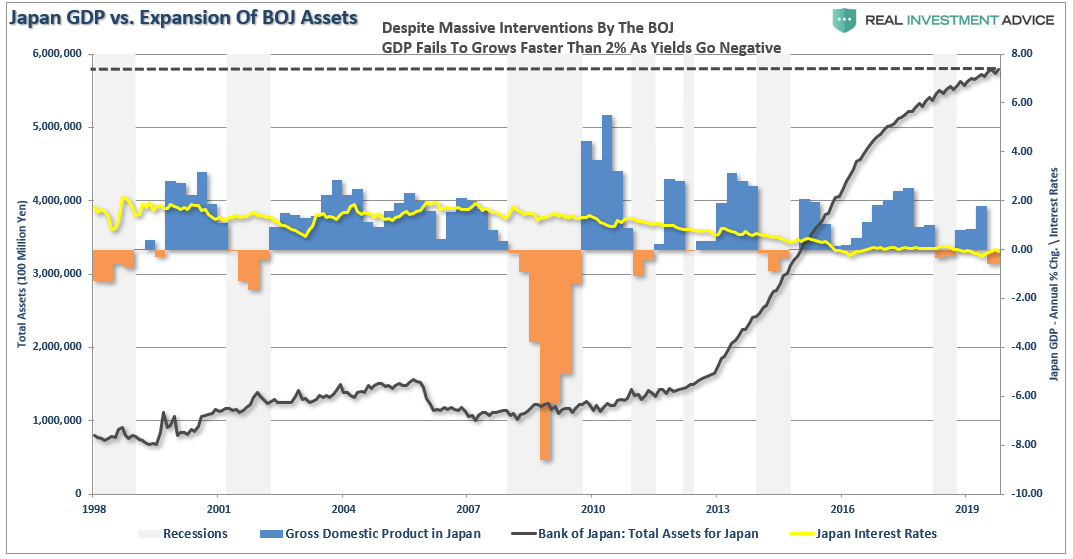

Let’s Be Like Japan

What is clear is that years of low interest rates, weak economic growth, low inflation, and ongoing monetary interventions has lead to a massive surge in debt in the U.S. and globally. While many want to suggests that “debt” isn’t a problem, we don’t have to go far to see what ultimately happens.

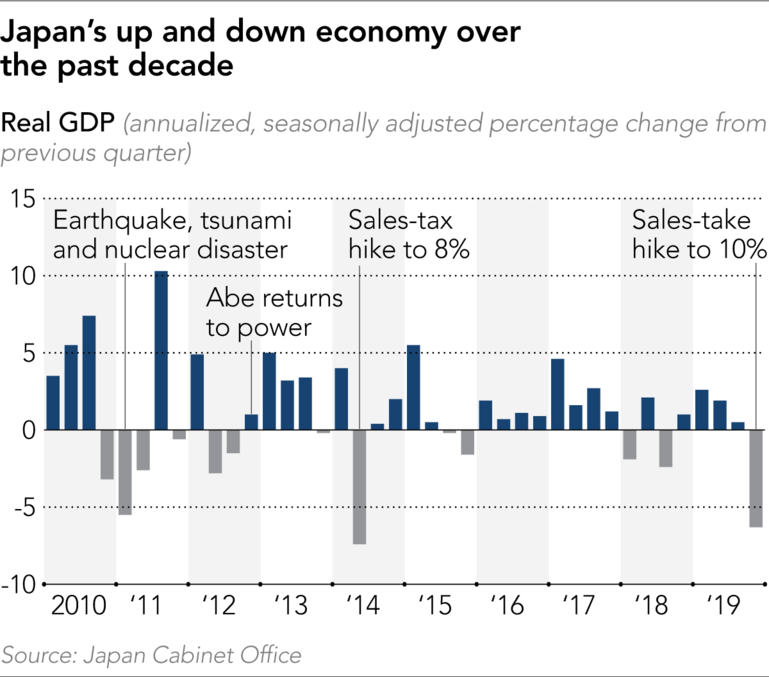

Even before the onset of the COVID-19 virus, Japan has been struggling economically.

There is more to this story.

Since 2008, Japan has been running a massive “quantitative easing” program which, on a relative basis, is more than 3-times the size of that in the U.S. However, while stock markets did rise with Central Bank interventions, long-term performance has remained muted.

More importantly, economic prosperity is only slightly higher than it was prior to the turn of century.

Lastly, despite the BOJ’s balance sheet consuming 80% of ETFs, not to mention a sizable chunk of the corporate and government debt market, Japan has been plagued by rolling recessions, low inflation, and low-interest rates. (Japan’s 10-year Treasury rate fell into negative territory for the second time in recent years.)

The End Game

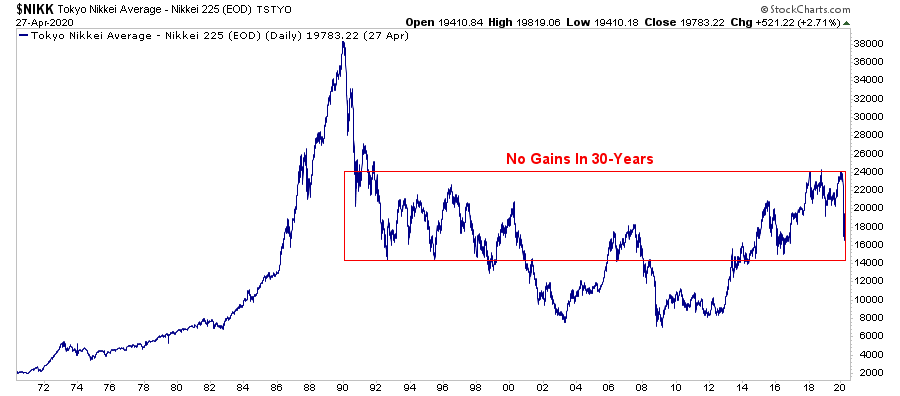

Why is this important? Because Japan is a microcosm of what is happening in the U.S. As I noted previously:

“The U.S., like Japan, is caught in an ongoing ‘liquidity trap’ where maintaining ultra-low interest rates are the key to sustaining an economic pulse. The unintended consequence of such actions, as we are witnessing in the U.S. currently, is the battle with deflationary pressures. The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments, and risk begins to outweigh the potential return.

Most importantly, while there are many calling for an end of the ‘Great Bond Bull Market,’ this is unlikely the case. As shown in the chart below, interest rates are relative globally. Rates can’t increase in one country while a majority of economies are pushing negative rates. As has been the case over the last 30-years, so goes Japan, so goes the U.S.”

Japan Is A Template

Should we worry about the debt? If Japan is indeed an template of what we will eventually face, the simple answer is “yes.”

As global growth continues to slow, the negative impact of debt expands economic instability and wealth inequality. Likewise, hope that Central Bank’s monetary ammunition can foster economic growth or inflation has been sorely misplaced.

“The fact is that financial engineering does not help an economy, it probably hurts it. If it helped, after mega-doses of the stuff in every imaginable form, the Japanese economy would be humming. But the Japanese economy is doing the opposite. Japan tried to substitute monetary policy for sound fiscal and economic policy. And the result is terrible.” – Doug Kass

Japan is a microcosm of what the U.S. will face in coming years as the “3-D’s” of debt, deflation, and the inevitability of demographics continues to widen the wealth gap. What Japan has shown us is that financial engineering doesn’t create prosperity, and over the medium to longer-term, it actually has negative consequences.

This is a key point.

What is missed by those promoting the use of more debt, is the underlying flawed logic of using debt to solve a debt problem.

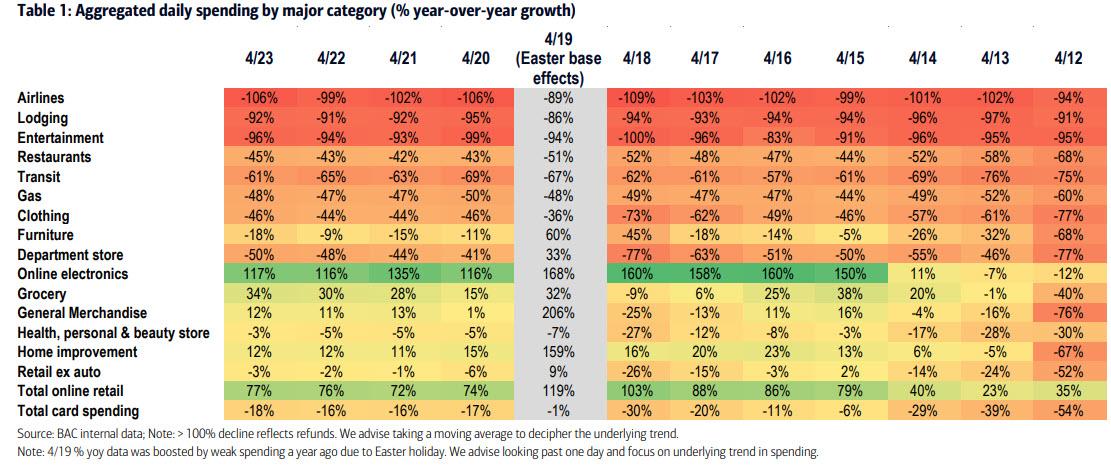

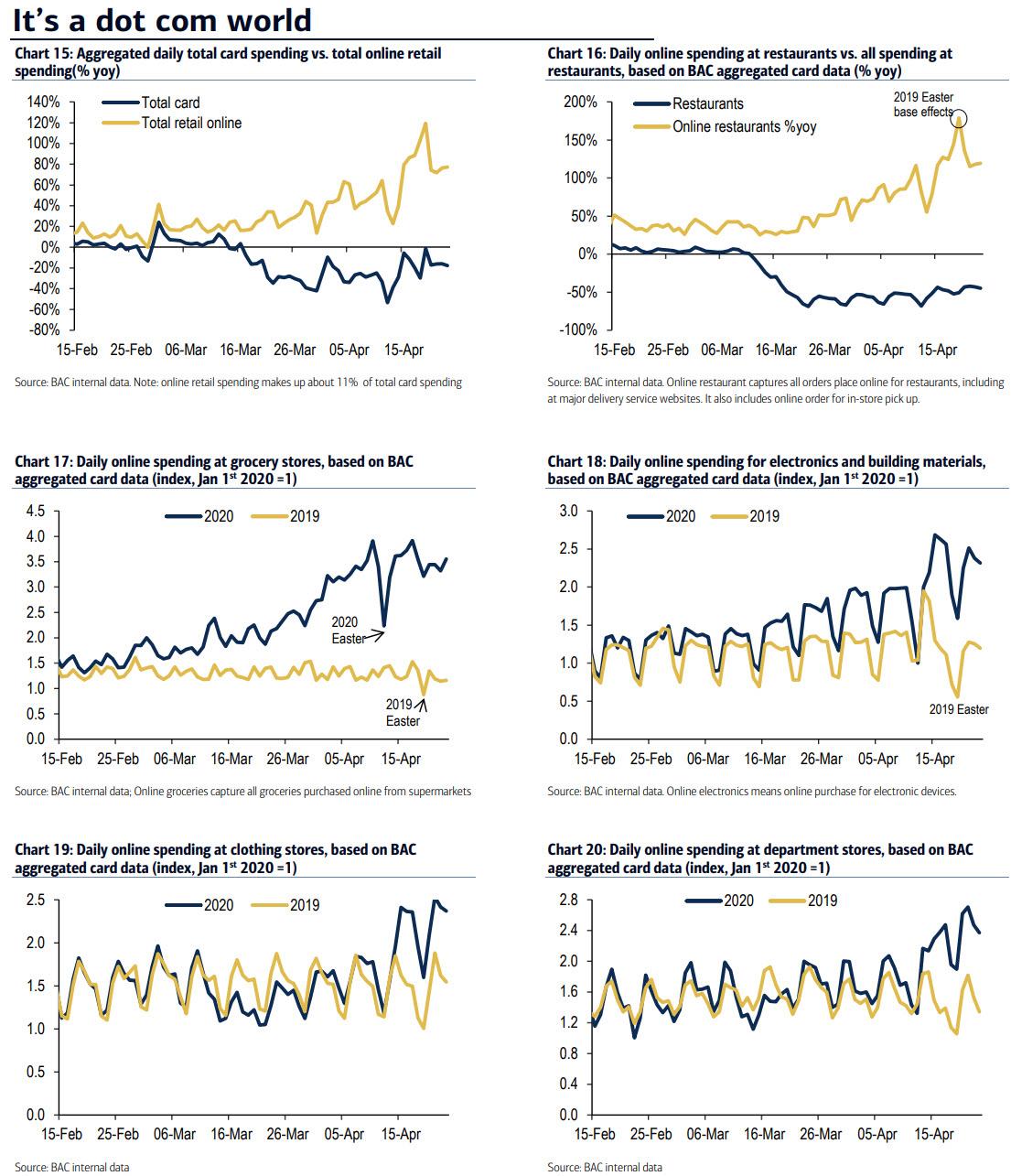

Shopping In A Time Of Corona: This Is What Americans Are (And Are Not) Spending On During The Crisis

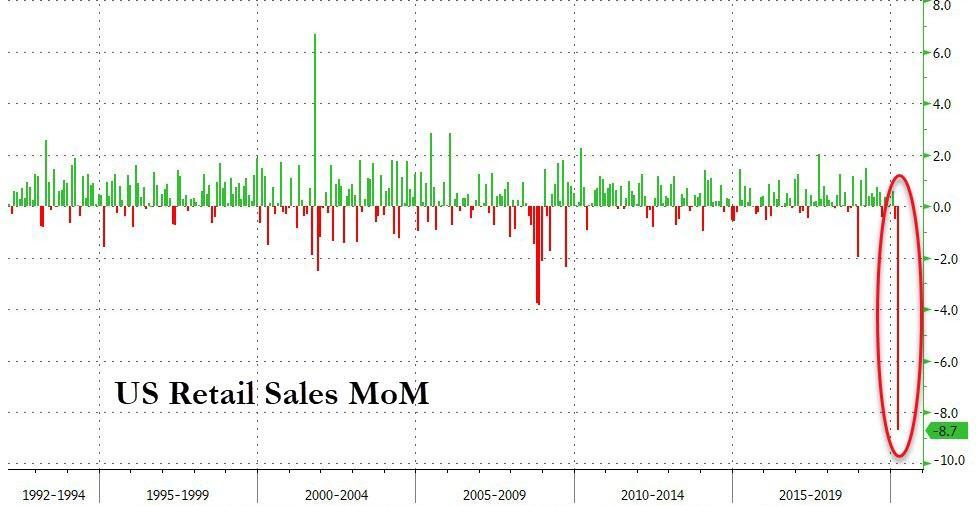

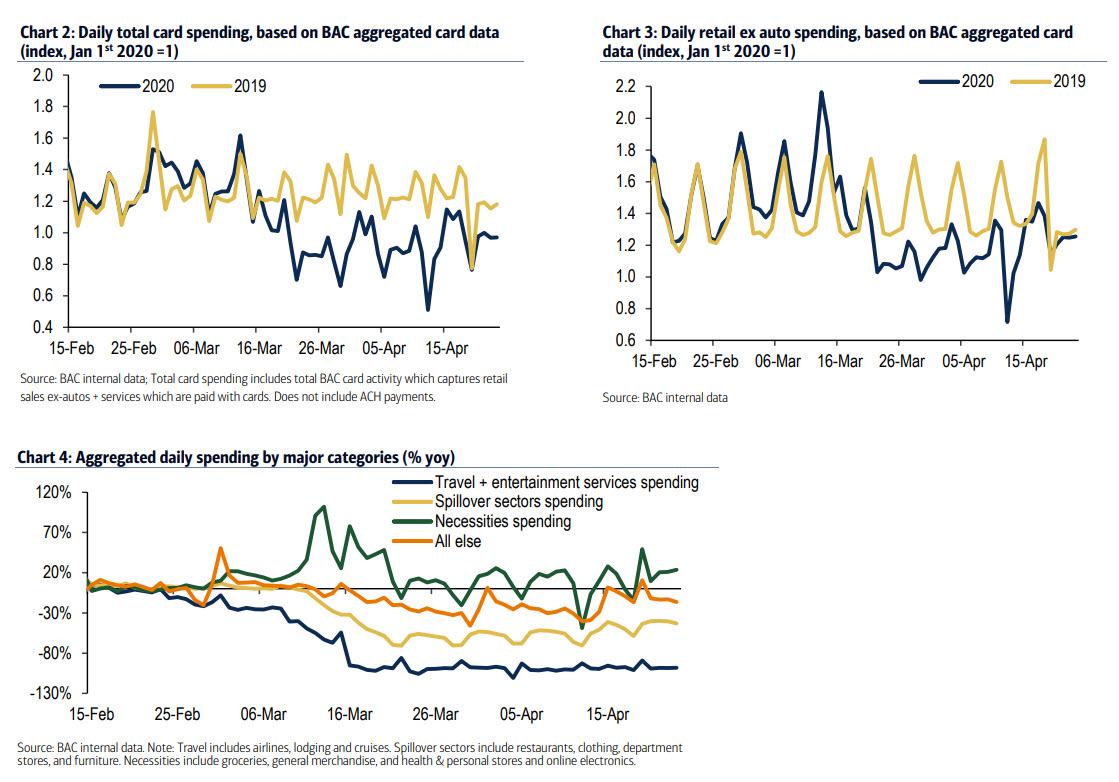

While we wait another two weeks to get the official report on the state of US consumer spending, let’s recall that the March number was abysmal, posting a record 8.2% sequential drop as a result of state closures in the second half of the month.

And while we previously pointed out that subsequent spending had continued to deteriorate, there is some good news in that the credit and debit card data as compiled by Bank of America through April 23, continued to point to stabilization in consumer spending.

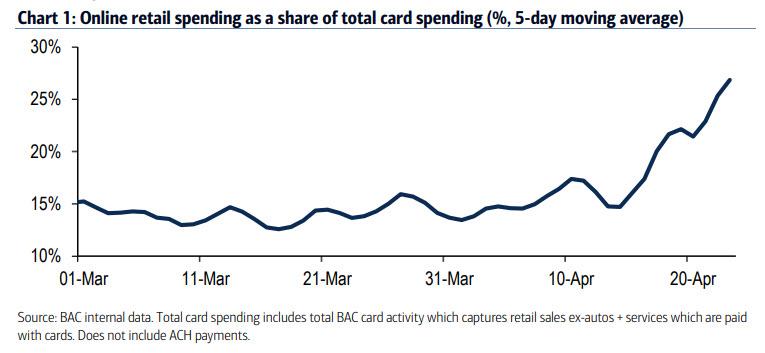

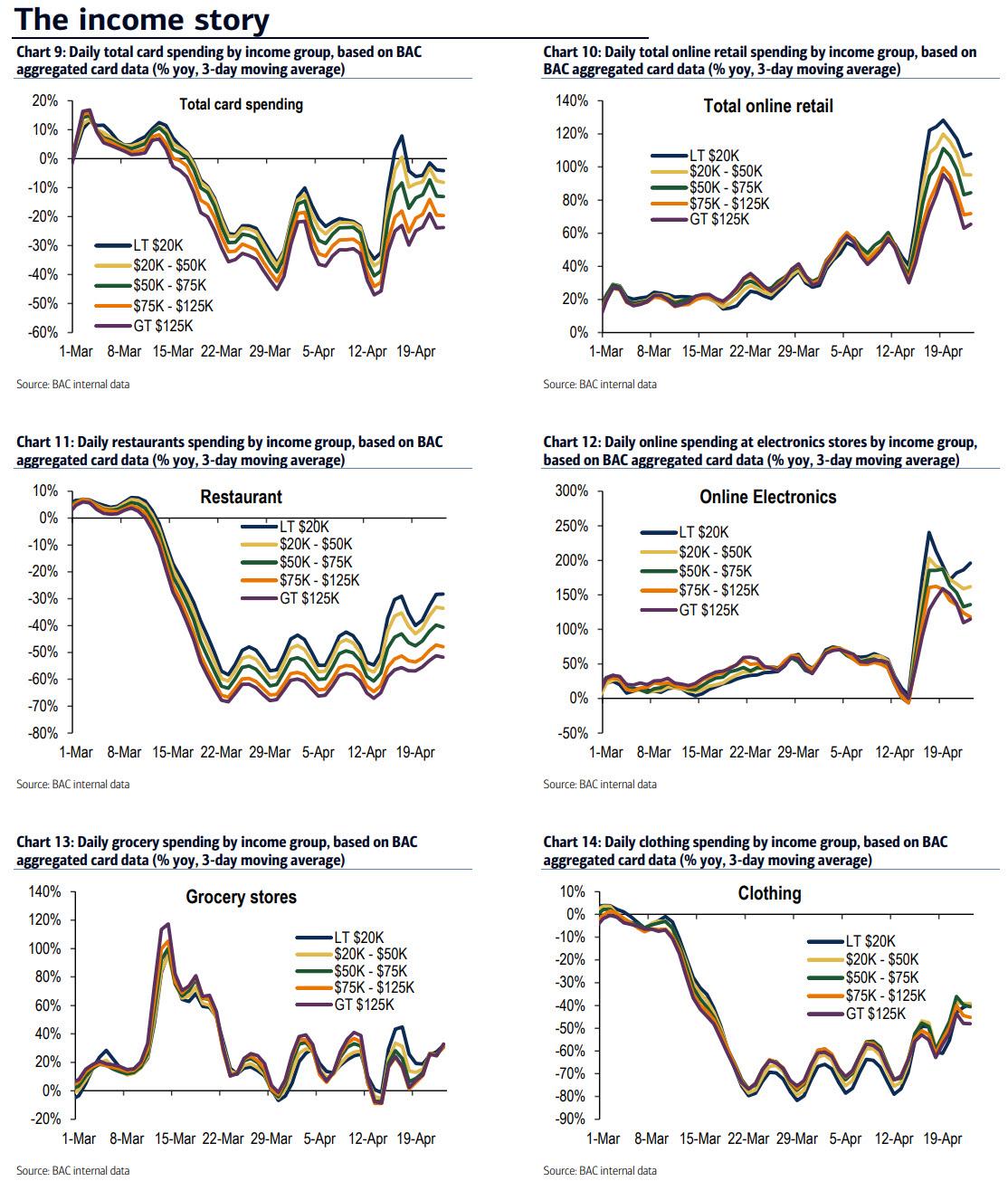

Going over the data, BofA notes that there continued to be a growing bifurcation in spending, with online activity continuing to dominate.

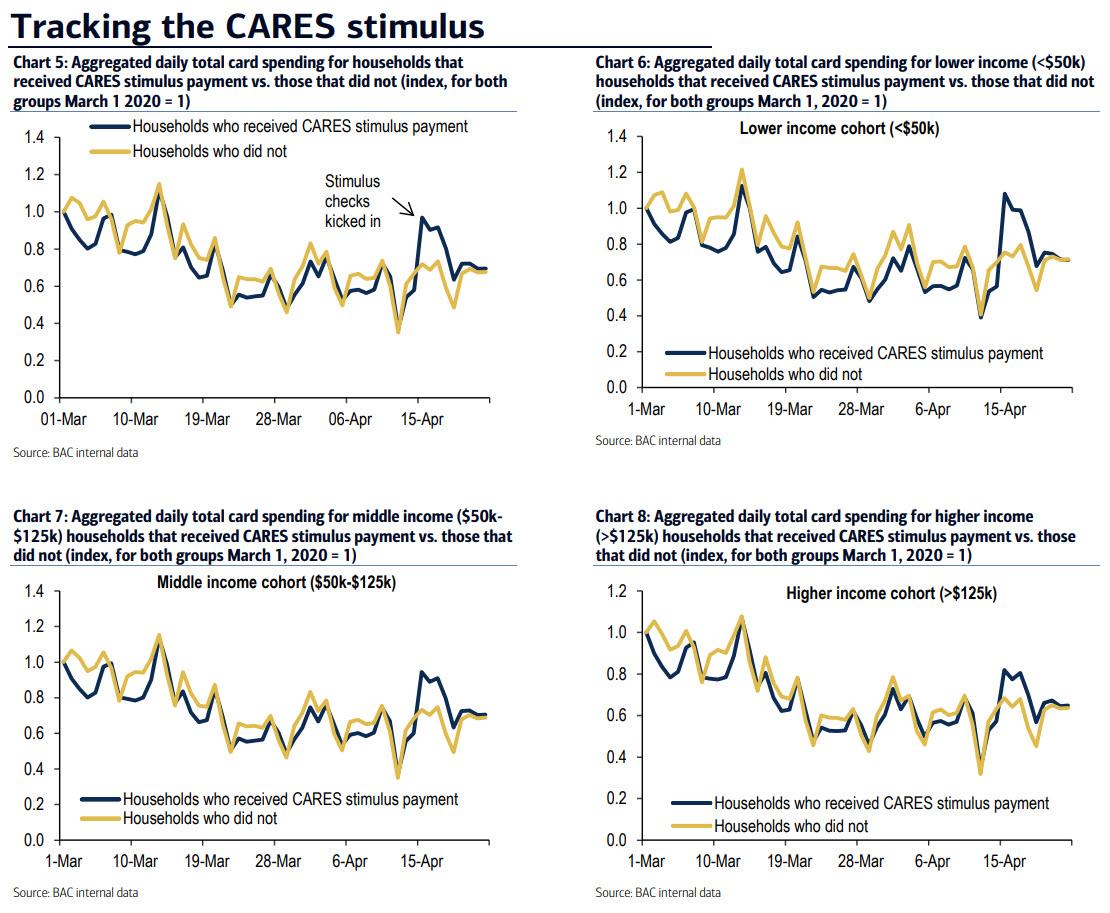

What was behind the tentative April spending stabilization? According to BofA chief economist Michelle Meyer, the key variable was the distribution of the CARES stimulus payments on April 15th – which totaled over $150bn according to the Treasury Department, and which helped boost spending in the middle of the month (as the table below shows, there was some noise in the data over the past two weeks due to the timing of Easter this year vs. last).

As a result, BofA observed a shift higher in aggregated spending for the 5 days following the stimulus payment among the population that received the stimulus. However, after the 5-day period, aggregated spending for those who received the stimulus payment converged to the trend of those who did not. “This shows a relatively transitory boost to spending from the stimulus” according to Meyer.

As expected, the stimulus disproportionately supported spending among the lower income cohort. BofA dug deeper into the composition of spending for this population relative to the other income groups and found a meaningful difference in spending by income group at restaurants and for online electronics where the recovery in spending for lower income households has been stronger than for the higher income ones. In contrast, spending for groceries has been comparable across income groups.

Bottom line: The good news is that consumer spending has stabilized, but mostly thanks to one-time stimulus checks. The bad news is that spending remains at low levels, and in BofA’s view a sustained improvement is unlikely until there is a recovery in the labor market, which as we will show in a follow up post may not happen until 2022.

With that in mind, here is what – and how – Americans spent money on in the time of the coronavirus self quarantines.

As expected, the biggest winner remains Amazon thanks to the ongoing surge in online spending.

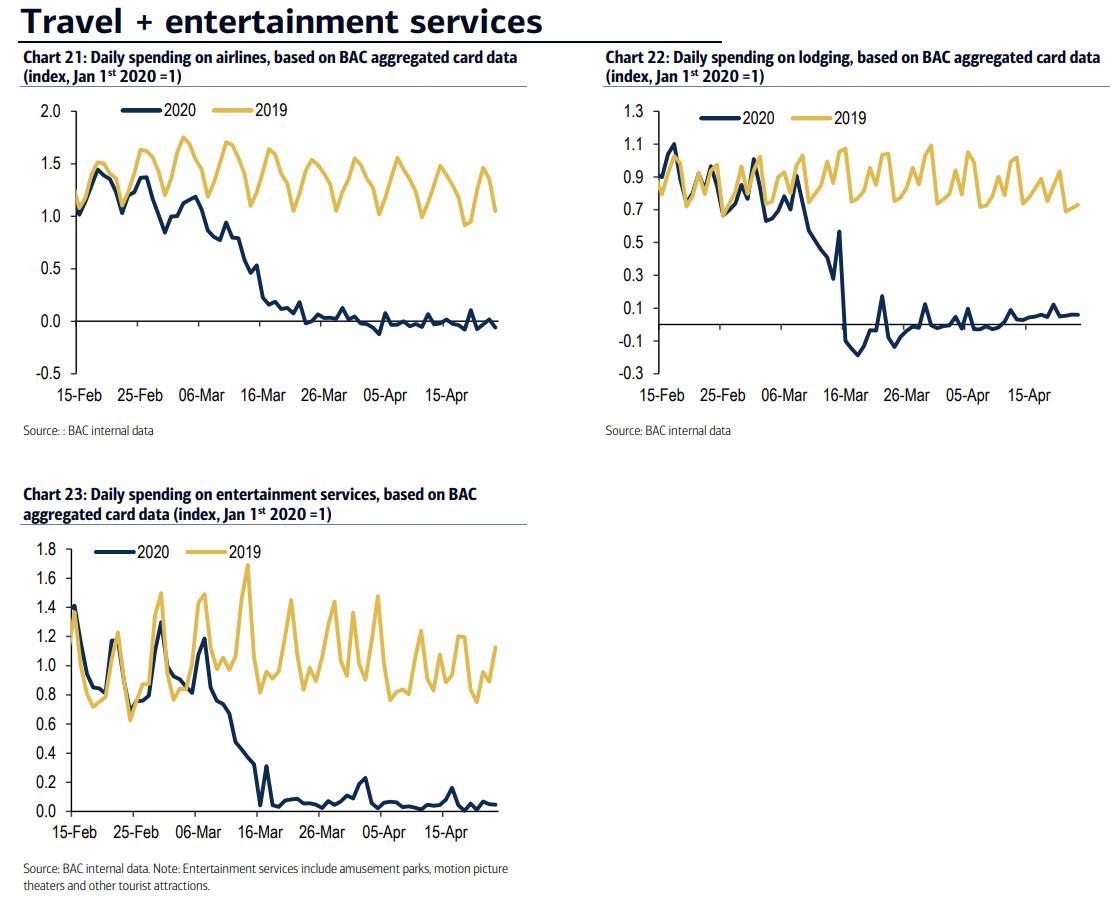

While online is the big winner, travel and entertainment spending is by far the biggest loser, collapsing to near zero.

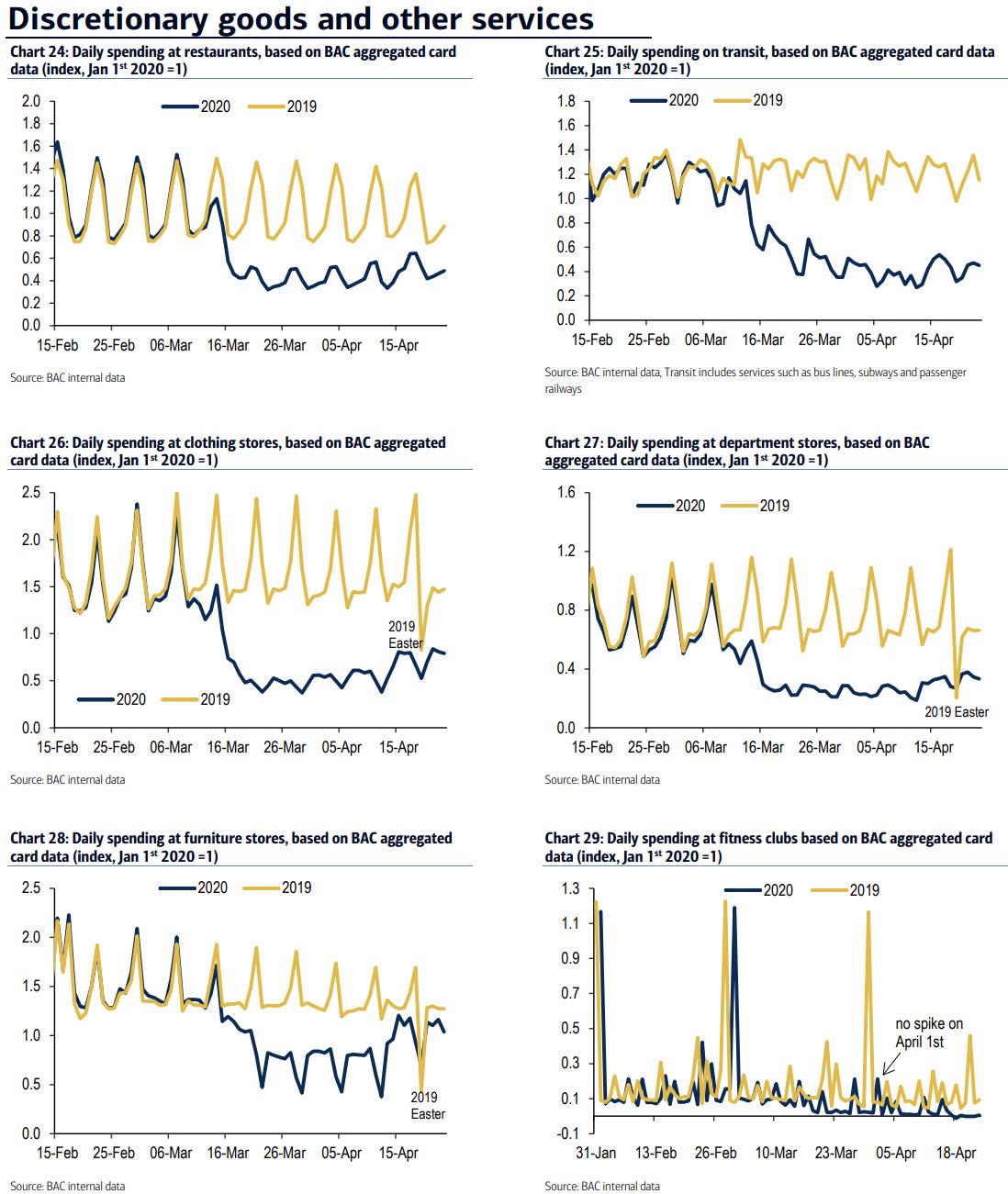

Discretionary spending is not far behind, with restaurant, transportation and clothing spending failing to rebound, although there has been an odd ramp in furniture store spending:

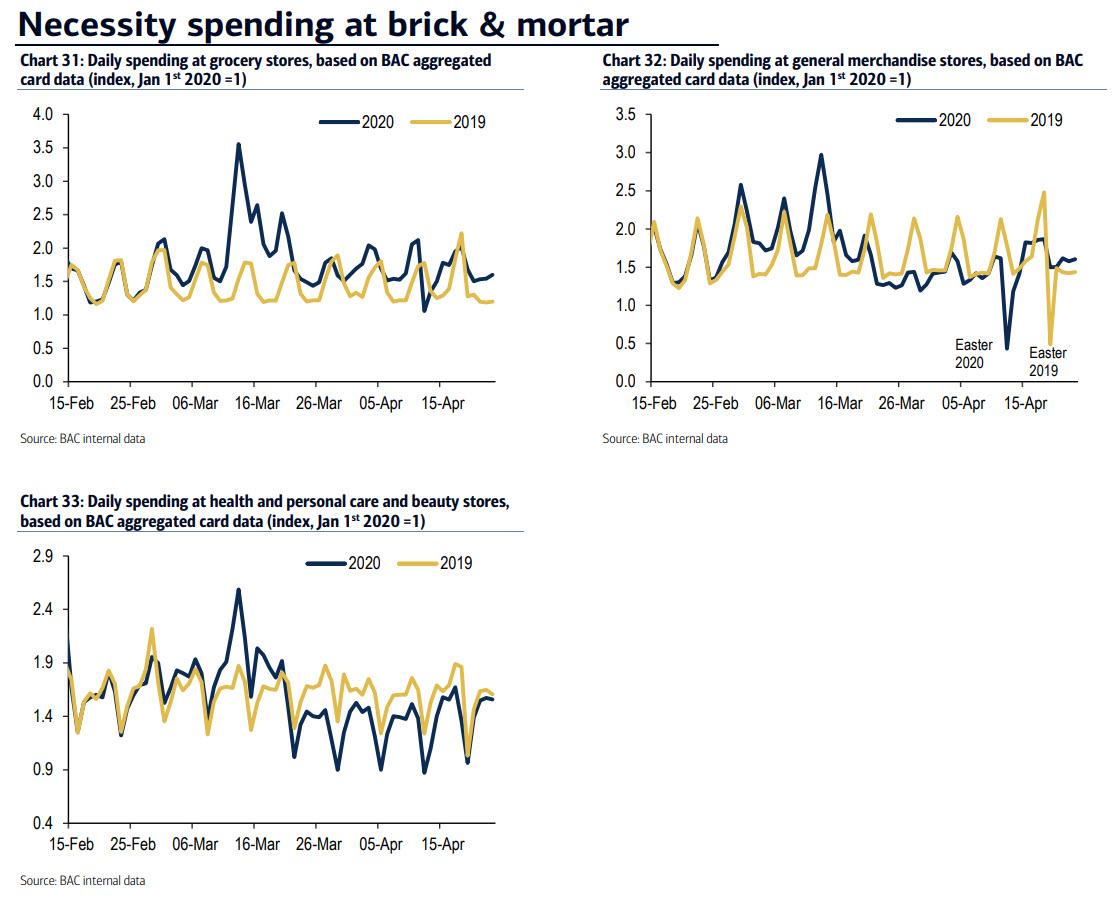

At the same time, spending at grocery, general merchandise and health stores is generally unchanged from a year earlier, although following a burst of spending in mid-March when Americans rushed out to hoard perishables, there appears to be a modest decline in spending in subsequent weeks as one would expect.

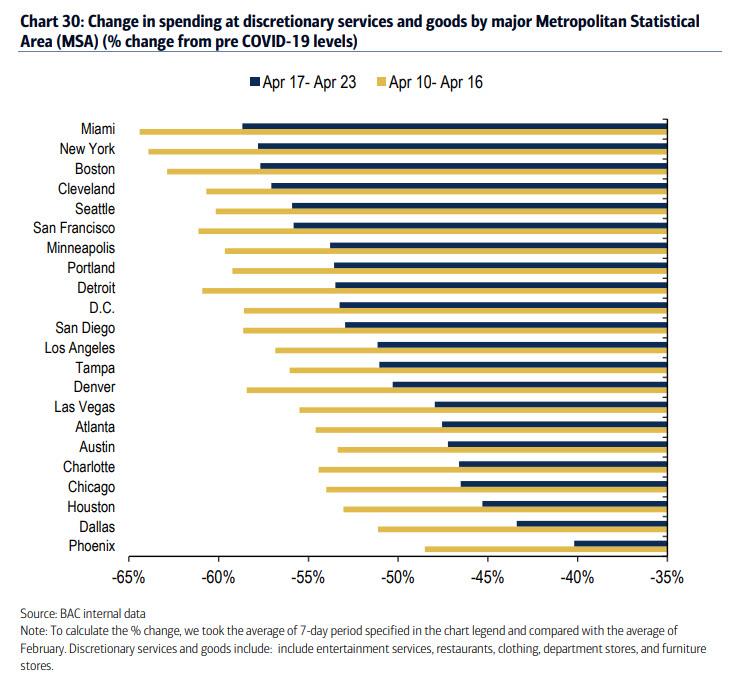

Finally, looking at spending my metro area shows a rebound in late April spending compared to the middle of the month across the country, although a wide dispersion remains with coastal cities such as Miami, New York, Boston, Seattle and San Fran hit the hardest, while landlocked, and less densely populated areas such as Phoenix, Dallas and Houston will likely be the first to emerge back to normal.

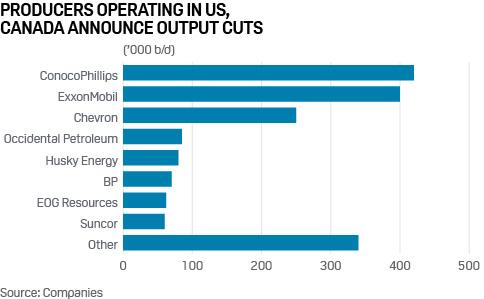

Oil producers in North America have announced vast cuts in output, led by ConocoPhillips, ExxonMobil and Chevron. Plus, contrasting gas market signals from both sides of the Atlantic, Brazilian corn exports under pressure and more, in S&P Global Platts editors’ pick of key trends in energy and commodities this week.

1. North American crude output set to decline in reaction to low oil prices…

What’s happening? Global oil companies have announced production cuts of roughly 4 million b/d in response to a collapse in prices. Of that total, around 1.8 million b/d has been announced by producers focused in the US and Canada, with ConocoPhillips, ExxonMobil and Chevron leading the way. Production cuts could even be higher, as only some of the dozens of companies announcing spending cuts have detailed their output plans.

What’s next? Crude futures have found some support from the cuts, but the NYMEX front-month contract is still lingering below $20/b. The market will likely need to see more cuts to push prices substantially higher, whether from oil companies, or from OPEC and its allies, which have pledged cuts totaling 9.7 million b/d for May and June.

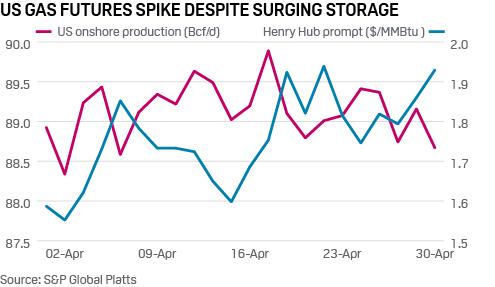

2. Falling rig count, bearish crude support US gas prices…

What’s happening? Despite US natural gas in storage sitting nearly 20% above the five-year average with hefty builds on the horizon likely, Henry Hub futures continue to strengthen as the prompt month approaches the $2/MMBtu mark. As US states discuss plans to begin easing restrictions related to the coronavirus pandemic, demand may see some upside throughout May, cutting into the storage surplus.

What’s next? Weak oil prices and declining rig counts also present a bullish risk to prices at Henry Hub for the second half of the year. Associated gas production is already showing declines. Total US production has averaged 92 Bcf/d the past 10 days, 300 MMcf/d below the April 1 through 20 average. The Bakken and DJ Basin lead US fields in recent declines, at 300 MMcfd/d and 150 Mcf/d, respectively.

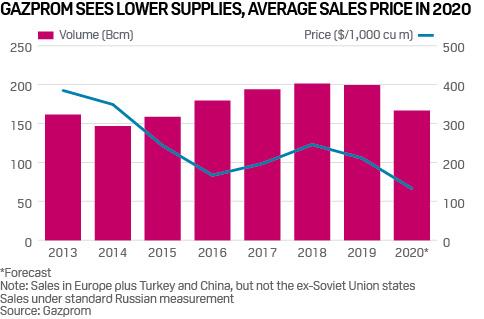

3. … as gas glut sees Gazprom slash exports, sales price outlook

What’s happening? Russia’s Gazprom expects its gas exports to its main international markets to total 166.6 Bcm in 2020, which would mark a 17% reduction compared to last year. The forecast is the first Gazprom has given for 2020 and reflects the extreme shift in European gas market dynamics since the turn of the year. Gazprom has also signaled an expected realized gas price for 2020 as a whole of just $133/1,000 cu m, which would be a 37% decline year on year.

What’s next? Europe has witnessed sharp falls in gas demand due to the mild winter, high storage stocks and the economic impact of the coronavirus, reducing demand for Russian pipeline gas. Limited gas storage injection demand and continuing economic turmoil caused by the virus means a recovery for Russian sales in Europe may be problematic.

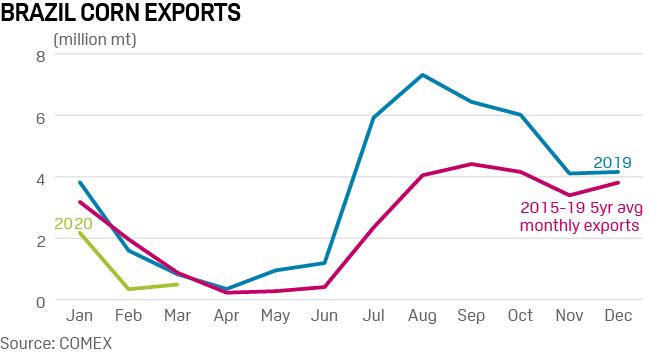

4. Brazil sees sluggish corn export pace amid mounting virus concerns

What’s happening? Brazil’s corn shipments have been significantly lower in 2020, after exporting a record quantity last year. Between January-March, Brazil exported 3 million mt of corn, down 56.5% from the same period last year. Depleted corn stocks, strong local demand, and high export prices have restricted exports in this new marketing season from Brazil.

What’s next? The National Food Supply Company has forecast Brazil’s corn export to reach 34.5 million mt in 2019-20, down 17.3% from the previous marketing season. However, experts doubt Brazilian corn exports will hit this level, as coronavirus-related restrictions are likely to bring down demand from the livestock and ethanol sectors. Concerns also remain as the pace of Brazil’s confirmed coronavirus cases keep surging. Moreover, in the US the collapse of ethanol demand in and the expectation of higher planted areas for corn this season mean the market is likely to be flooded with cheap corn.

5. European power demand stable as first signs of recovery emerge

What’s happening? UK electricity demand was trending up in late April and into May as chilly, unsettled weather swept in from the Atlantic, pushing mid-week demand up over 10% on week. This followed modest demand recoveries in both Spain and Italy earlier in April, these due to partial lifting of coronavirus lockdowns. System data for both Germany and France, meanwhile, showed stabilization of demand levels through April after the massive drops seen in March.

What’s next? The following weeks should see further incremental easing of lockdowns in European power markets, prompting a phased resumption in commercial and industrial activity. It is impossible to say when or even if the drastic declines seen to date will be erased. After the 2008 credit crunch, electricity demand bounced back to varying degrees in most markets, but never fully recovered to pre-crunch levels. This was in large part for positive reasons – as economies recovered, new investment drove down the energy intensity of equipment. It remains to be seen whether social distancing will have a similar constraining influence on recovering demand.

6. Steel demand slump, plant restarts raise specter of protectionism

What’s happening? Steel hot rolled coil prices are again under downwards pressure in Europe as coronavirus-related curbs have hit consumption, halting a recovery glimpsed early in 2020 after a slump in November amid global oversupply. Since March, Europe has seem an estimated 80% fall in steel demand from the automotive industry and 40% in construction.

What’s next? As some mills return to production after virus-related stoppages, price pressure is likely to increase, particularly as Chinese, Iranian and Russian mills are becoming more active in steel export markets. Protectionism is likely to rise: industry sources have reported the European Commission is now accelerating a review of its steel imports safeguards review, following a request from European steelmakers’ association Eurofer and the European Steel Tube Association (ESTA) for a 75% reduction in import quotas for Q2-Q3.

California First To Be Approved For Up To $10 Billion Bailout From Feds To Pay Unemployment Benefits

As politicians argue over whether or not to bailout decades-long bad decisions on the basis of a sudden virus/lockdown-driven drop in revenues, California has stepped up to the plate with what appears to be a direct request for a bailout to fund the benefits for millions of newly-unemployed residents (and illegal immigrants).

“Last year I did a May revise with a $21.4 billion budget surplus,” Newsom said on Friday during his daily coronavirus briefing, according toBloomberg.

“This year I will be doing a May reviselooking at tens of billions of dollars in deficit. We just went tens of billions in surplus in just weeks to deficits.“

The Wall Street Journal reports that California has become the first state to borrow money from the federal government so it can continue paying out rising claims for unemployment benefits during the coronavirus pandemic.

The Golden State borrowed $348 million in federal funds after receiving approval to tap up to $10 billion for this purpose through the end of July, a Treasury Department spokesman said Monday.

“I’m doing everything I can to work with cities and counties, but we are not going to be in a position, even as the nation’s fifth-largest economy, to provide for the needs of all the cities and the counties without federal support,” said Newsom.

Meanwhile, in a memo last week, Newsom’s finance director ordered departments to significantly slash spending immediately using strict measures, including bans on new goods and service contracts.

As the journal concludes, California serves as an early sign of the potential magnitude of the federal assistance that could be required if states are to continue paying out jobless benefits. It is one of more than 20 states and jurisdictions that entered the current economic crisis without enough money in their unemployment trust funds to pay benefits through a yearlong recession, according to Labor Department data.

With 30 million unemployment claims filed since the coronavirus pandemic resulted in the shutdown of broad swaths of the economy, states are reporting that they’ll need at least $1 trillion in aid from the federal government – which has already doled out over $2.2 trillion in relief for business loans, stimulus checks, expanded unemployment benefits and small business assistance.

And with a lack of tax revenue, states with bloated budgets and massive entitlement programs are facing significant pain in the months ahead.

The U.S. government has also approved loans of up to $12.6 billion for Illinois and up to $1.1 billion for Connecticut through the end of July to replenish state unemployment insurance funds, though the two states hadn’t yet started borrowing by the end of April. California was the only state to have accessed the program so far in the current downturn, the Treasury spokesman said.

One wonders if the reason that the other states haven’t been so quick to draw down on the loans is because they are hoping for a broader-based bailout from a Democrat-sponsored Congressional bill that enables pension benefits to be covered… and not just the jobless.

Small Businesses, Many Of Which Couldn’t Get PPP Loans, Have “A Few Months Or Less” To Survive

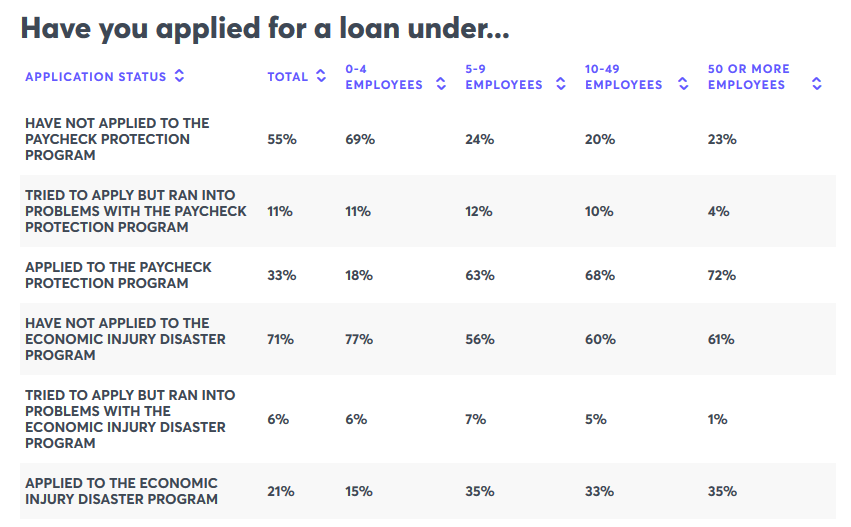

Small business impacted by the coronavirus pandemic have had difficulty obtaining loans from the Paycheck Protection Program (PPP), according to a CNBC/SurveyMonkey Small Business Survey released Monday.

Of 2,200 small businesses owners polled, just 13% of the 45% who applied for a PPP loan were approved. 7% of respondents had already received financing, while 18% are still waiting on a response from a lender, according to CNBC.

Those applying for a different program, the $10,000 Economic Injury Disaster Loan, fared worse – with just 3% of small business owners reporting that they were approved, and 16% still awaiting a response.

Both relief programs are run by the Small Business Administration. PPP loans are capped at $100,000 per employee and can range in size. The $10,000 advance from EIDL does not have to be repaid, making it effectively a grant.

Sole proprietorships that represent 81% of all small businesses in America is a group particularly hard hit in this credit crunch. For them the window for relief loans opened late, giving them a shorter time opportunity to garner the money desperately needed to ensure they can remain in business. –CNBC

Dire straits

Meanwhile, 43% of small businesses surveyed report that they can survive for a few more months or less – with 31% reporting a ‘few months,’ 7% ‘less than a month’ and 6% less than a week under the current economic lockdown.

Rohit Arora, CEO of online lending platform Biz2Credit, which lends to small businesses, confirms what we’ve been reporting for weeks – that multiple problems plagued the PPP rollout for small businesses.

“The law was murky, and both applicants and bank loan officers were ill-equipped to process the data, as requirements were changing so fast.”

“Another issue is the fact that as a general rule, large banks haven’t focused on small business loans given to companies with less than 50 employees,” said Arora. “They have deemed it too labor intensive.”

Meanwhile, small community banks were ill-equipped to handle the flood of applications and were quickly overwhelmed by the massive volume of data being fed into their system in a short period of time.

Karen Kerrigan, CEO of the Small Business & Entrepreneurship Council, says the regulations imposed on borrowers under the PPP has also been a challenge, and many business owners have decided not to tap the program for that reason. Among them: the 25/75 rule that says business owners must use 75% of the funds they receive only for payroll, and 25% for rent, mortgage payments, utilities and other operating expenses in order to get loan forgiveness.

“In many cases this has been a deal breaker. Rent and other operating expenses are high, and getting only a quarter of the loan to cover those costs is not enough,” she explains.

Another requirement for loan forgiveness is that business owners have eight weeks to bring back employees after the money hits their bank accounts. “What happens to those small business owners operating in hard-hit places like New York and New Jersey, where stay-at-home orders are still in place and no one knows when the shutdown orders will be lifted?” she says. –CNBC

In a potentially promising sign for future disbursements, several fintech companies such as Square, PayPal and Intuit are now authorized PPP lenders.

“These companies serve millions of small business owners, many of whom are sole proprietorships and mom and pops. They have the AI and advanced technology to process these loans, as well as strong relationships with many borrowers who regularly use their concierge-type services,” said Kerrigan.

On Sunday, White House National Economic Director Larry Kudlow said that a third round of stimulus may be necessary, but that the Trump administration had made no decision on further funding.

El-Erian Warns “Huge Disconnect” Between Wall Street And Main Street Could Have Devastating Consequences

Authored by Mohamed El-Erian, chief economic adviser at Allianz SE, first published in Bloomberg

Just a few weeks into the coronavirus crisis, many are already pointing to the striking contrast between what has happened to the real economy and financial markets. This Main Street versus Wall Street tension is fueled both by legacy and current issues and sheds light on the state of economic and financial policies. It may also play a role in determining current and future well-being.

Two main factors are driving the tension.

On the legacy front, the memory of the global financial crisis is still fresh in many people’s minds. Unlike the current crisis, Wall Street caused an ugly shock in 2008 that resulted in a Great Recession for Main Street and almost tipped it into a depression. Wall Street was also the primary recipient of a huge bailout that enabled most of it not just to recover quickly but also to pay itself well during the recovery period. Adding to the sense of injustice, relatively few Wall Street leaders were seen to have suffered, let alone been held legally accountable or gone to prison.

Fast-forward to today and, again, there’s a huge disconnect between the fortunes of the two, and it has emerged quickly.

Main Street is dealing with historic collapses in employment (30 million workers have applied for jobless claims in just six weeks) and economic activity (a 4.8% contraction in gross domestic product at an annualized pace in the first quarter with a further 30% to 40% decline in the cards for this quarter). Wages are falling for many of those still lucky enough to have jobs. The pain and suffering associated with all this is visible not only in the long lines outside food banks around the country but also in reports of mounting domestic violence and mental anxiety.

Yet Wall Street is coming off the best month for stocks in 33 years. The capital markets are wide open for most listed companies to issue bond financing. A relatively big part of the financial sector has been immune from the wave of large layoffs and bankruptcies the rest of corporate America is experiencing.

The extent of this divergence has not gone unnoticed and is already raising concerns. Yet there are understandable reasons that make its resolution tricky.

Again in this crisis, the Federal Reserve has proved to be the most responsive and powerful policy-making institution. After an initial hiccup, it moved boldly and effectively to ensure that a 2008-like financial crisis did not amplify the real and present danger of a 1930s-like depression. But this could be done only by injecting trillions of dollars into capital markets, thereby also significantly boosting the prices of financial assets that are mostly held by the better-off segments of American society.

Fiscal policy has also been hard at work. But accomplishing things in this case is inherently trickier. Congressional approval is needed for virtually every action (unlike for the majority Fed policy measures), and there is the added challenge of building new pipes to get the assistance to the targeted places quickly. The result is unavoidably more haphazard and less effective.

The longer this divergence persists, the greater the fuel on the fire of other divisions in America: rich versus poor, corporations versus individuals, current versus future generations, connected versus alienated, etc.

The right response is for government agencies and the Fed to undertake efforts to close the gap from both sides in an orderly way through such steps as: making mid-course corrections to the relief efforts to ensure greater effectiveness; designing new recovery plans that target high, inclusive and sustainable growth, thereby avoiding a repeat of the 2008 mistake of winning the war but failing to secure the peace; and paying much greater attention to mounting moral hazard in financial markets and the associated risk of future financial instability that could contaminate the real economy.

The more fortunate segments of society also have an important role to play, motivated both by collective and individual interests. More companies should be stepping up their social responsibility efforts. Just like the public sector, this should focus both on relief (donations to food banks, for example) and on recovery (for instance, helping, both solo and working with others, in establishing retraining and retooling programs for low-cost jobs that are not coming back).

Some will be tempted to argue that the current stark contrast in the fortunes of Main Street and Wall Street is unavoidable. Forced by the structure of the economy and policy apparatus, it’s an unpleasant stop on a potentially successful recovery journey. Others will see it as a repeated illustration of the extent to which the system has been co-opted to serve those already privileged, both in the good and bad times.

Whatever your viewpoint, we should all agree on the urgent priority of doing more now to ensure an orderly recoupling that delivers a quick and more inclusive recovery in the context of genuine financial stability.

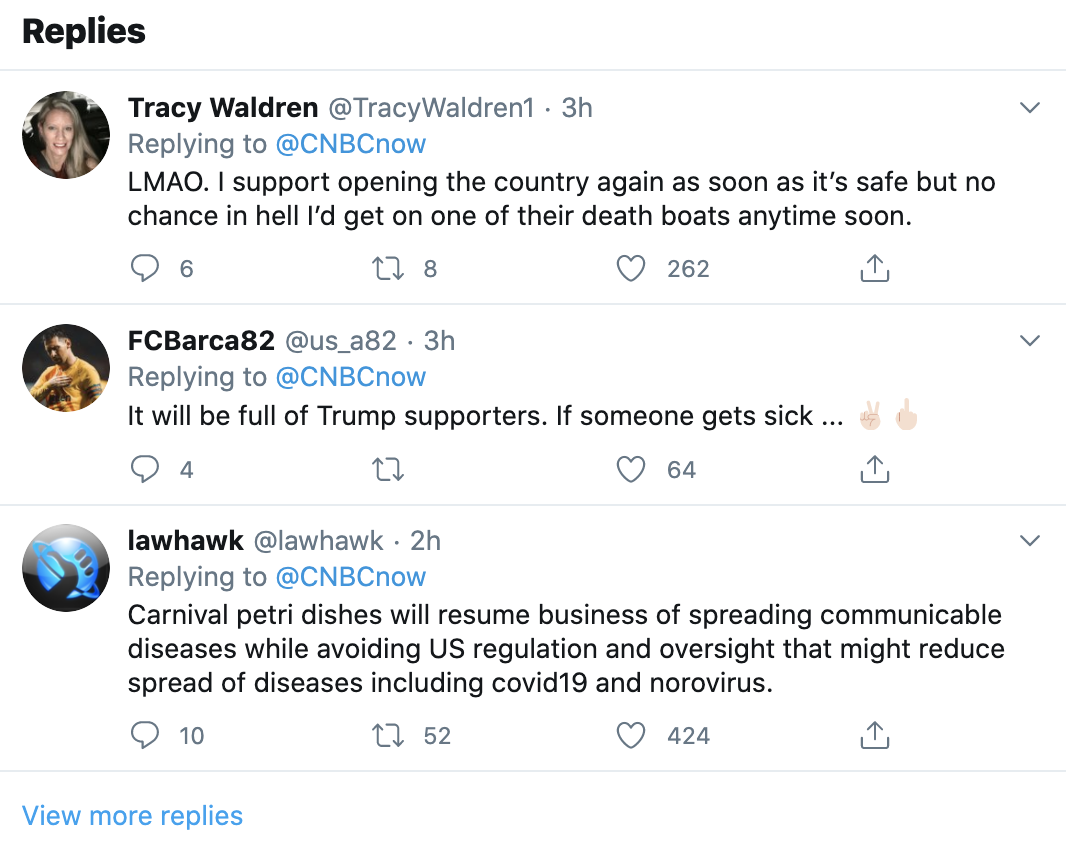

Scandal-Plagued Carnival Books First Post-Corona Cruise For Aug. 1

When we first saw the following headline, our first reaction was to rub our eyes in disbelief, before double-checking the URL to make sure we were really on CNBC.com and not some new Onion vertical.

With an open criminal investigation in Australia and hundreds of thousands of outraged customers and their friends and family members who will likely never voluntarily board another cruise for as long as they live, Carnival Corp – the world’s biggest cruise line operator – is planning to launch its first post-corona cruises on Aug. 1, with 8 ships leaving from ports in Miami, Cape Canaveral and Galveston, Texas.

JUST IN: Carnival Cruise Line says it will begin to phase-in cruises again starting August 1 with eight of its ships leaving from Miami, Port Canaveral and Galveston. https://t.co/jn8limUSe7

The first few replies sum up what we imagine to be the sentiments of many Americans who followed the horrifying reports about what we dubbed “a nightmare at sea”: Every time a new outbreak aboard a cruise ship seemed to explode into an international incident, the cruise line was seemingly inevitably a Carnival subsidiary, particularly the “Princess Cruises” line that drew the ire of Australian public health officials and – later – prosecutors.

Ships from other Carnival subsidiaries also saw outbreaks at sea. Ultimately, dozens died and thousands were infected. Reporting from Bloomberg and the Washington Post has suggested that Carnival management was partly at fault.

Replies to the news were pretty much what we expected…

…and, like Mr. Weisenthal, we suspect there will be quite a bit of coverage when the first cruise sets sail.

What % of that first cruise in August is going to be reporters?

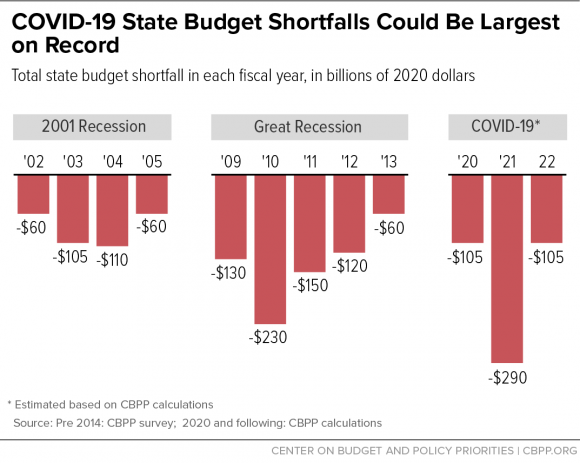

The people running states like New Jersey and cities like Chicago know they’re broke. Ridiculously generous public employee pensions – concocted by elected officials and union leaders who had to have understood that they were writing checks their taxpayers couldn’t cover – are bleeding them dry, with no political solution in sight.

They also know that they have only two possible outs: bankruptcy, or some form of federal bailout. Since the former means a disgraceful end to local political careers while the latter requires some kind of massive crisis to push Washington into a place where a multi-trillion dollar state/city bailout is the least bad option, it’s safe to assume that mayors and governors – along with public sector union leaders – have been hoping for such a crisis to save their bacon.

And this year they got their wish. The country is on lockdown, unemployment is skyrocketing and mayors and governors now have a plausible way to rebrand their criminal mismanagement as a “natural disaster” deserving of outside help.

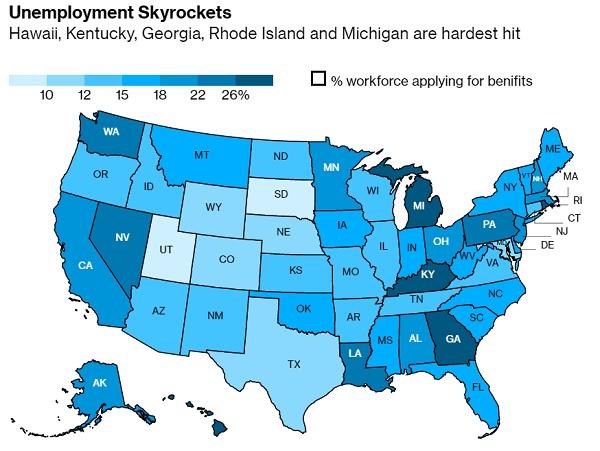

Here, for instance, is an estimate of how high unemployment will spike for various states. Note that overall it’s brutal, but the distribution isn’t what you might expect:

And here’s a table of state rainy day funds (i.e., cash on hand). To their credit, oil-producing states had the discipline to save against that commodity’s inevitable price fluctuations. Other states apparently didn’t see the need:

Illinois, which has the most underfunded pensions but, interestingly, a relatively healthy labor market, apparently had its natural disaster bailout plan prepped and printed before COVID-19 was invented and released. Because governor Gov. J.B. Pritzker almost instantly had his hand out for – get this – $41 billion, a sum equal to three times the state’s estimated pandemic-related revenue loss in the coming year. Overall, governors have asked for about $500 billion in aid.

For President Trump, bailing out “badly run Democrat states” seems politically pointless, since those states will never, ever vote Republican. Senate majority leader Mitch McConnell, meanwhile, trolled his Dem counterparts by suggesting that states just declare bankruptcy (thus freeing them to cut pension benefits).

But of course this is just partisan fantasy. Letting Illinois go bankrupt would send the muni bond market into a “who’s next?” seizure, which would quickly spread to corporate bonds, equities, and real estate, cratering the US and then the global economy. At least that’s the worst-case scenario economists will present to policymakers.

With no stomach for presiding over the end of the world during an election year, Washington will cave, agreeing to whatever governors demand. And so the grossest mismanagement in the history of US state and city government will be swept under the rug – or more accurately will be swept onto taxpayer balance sheets along with that of all the other sectors that are – surprise! – too big to fail.

This is a shame since one of the few things worth looking forward to in the deep recession the world was stumbling towards before the pandemic hit was the collapse of unconscionable public sector pensions, and the disgrace of the people who conned teachers, firefighters, and cops into thinking that those generous benefits were guaranteed. On the list of financial/political crimes of the modern era, theirs ranks near the top. And now they’ll go both unpublicized and unpunished.

Meanwhile, the resulting multi-trillion-dollar addition to the national debt will hasten the fiery end of the fiat currency/fractional reserve banking/unlimited-government-debt world. One can only hope that future historians will get the story right while the perps are still alive to answer for their sins.

NYT Publishes Grim CDC Projections Calling For Daily Coronavirus Deaths To Double By June

Update (1320ET): Unsurprisingly, the White House has rebutted the NYT report – which claimed that these projections represented ‘current conditions on the ground, so to speak – saying it doesn’t reflect current projections.

* * *

Less than 12 hours after we predicted the news media would lose its mind over President Trump’s uttering a new “projected” death toll during a briefing with reporters Sunday evening. For the first time, Trump said he expects up to 100k deaths from the coronavirus outbreak, which is higher than figures he’s quoted in the past.

There’s no debate that the pace of deaths has slowed in the US in recent weeks.

Yet, as Florida allows some businesses to reopen (albeit with strictly limited capacity) on Monday, the NYT has published “internal projections” from the CDC calling for average daily US deaths to accelerate to 3,000 a day by June 1. However, most of the hardest hit states are seeing cases and deaths decline, while some states are seeing a slight acceleration. Overall US mortality has plateaued. According to the CDC’s own coronavirus weekly summary, “nationally, levels of influenza-like illness (ILI) declined again this week. They have been below the national baseline for two weeks but remain elevated in the northeastern and northwestern part of the country. Levels of laboratory confirmed SARS-CoV-2 activity remained similar or decreased compared to last week.”

The NYT reported that the White House continues to expect up to 3,000 deaths a day in June while Trump continues to ‘press’ for states to reopen.

The report also claimed the projections “confirm” public health experts “primary fear” that a premature reopening will instigate a rebound putting us right back where we were in March.

As President Trump presses for states to reopen their economies, his administration is privately projecting a steady rise in the number of cases and deaths from coronavirus over the next several weeks, reaching about 3,000 daily deaths on June 1, according to an internal document obtained by The New York Times, nearly double from the current level of about 1,750.

The projections, based on modeling by the Centers for Disease Control and Prevention and pulled together in chart form by the Federal Emergency Management Agency, forecast about 200,000 new cases each day by the end of the month, up from about 25,000 cases now.

The numbers underscore a sobering reality: While the United States has been hunkered down for the past seven weeks, not much has changed. And the reopening to the economy will make matters worse.

“There remains a large number of counties whose burden continues to grow,” the C.D.C. warned.

The projections confirm the primary fear of public health experts: that a reopening of the economy will put the nation right back where it was in mid-March, when cases were rising so rapidly in some parts of the country that patients were dying on gurneys in hospital hallways as the health care system grew overloaded.

Notice the language the NYT has used: Characterizing the situation in the US by saying “not much has changed” simply doesn’t jive with the data, or with the lived experience of millions of Americans who took to public spaces and parks over the weekend to enjoy the good weather and sunshine.

But even states that have pressed ahead with reopening aren’t seeing anywhere near the activity they saw as recently as mid-March, just as the stay-at-home orders and lockdowns were beginning.

Trump smartly stopped egging on protesters and pushing states to reopen before federal guidelines say it’s acceptable. But at this point, the notion that these projections represent anything more than a “worst case” scenario for the CDC seems far-fetched.