QE Defender – Stop The QE Insanity: Helicopter Money And The Risk Of Hyperinflation

Submitted by BullionStar.com,

In 2016 at FreedomFest in Las Vegas, BullionStar first launched the QE Defender game.

With the central banks going all in on debasement of money by all means of quantitative easing and money printing, the QE Defender Game is more relevant than ever. We have therefore updated the characters of the game which can be played for free without registration here.

“There’s an infinite amount of cash in the Federal Reserve” – Minneapolis Fed President Neel Kashkari, March 23

“When it comes to this lending, we’re not going to run out of ammunition, that doesn’t happen” – Federal Reserve Chairman Jerome Powell, March 26

QE COVID

Over the last two months, major central banks and governments across the globe have unleashed a series of monetary and fiscal interventions on markets and economies which are unprecedented in their magnitude and which are bordering on the destruction of the current financial system.

While the global spread of coronavirus COVID-19 provided the trigger and the pretext for the current full-spectrum quantitative easing, money printing, asset purchases and economic bailouts, the size and scope of the current assault on free markets makes all previous central bank and government interventions look insignificance in comparison.

Markets are now officially broken. In some cases, the US Federal Reserve and the European Central Bank have become the markets, such is the scale of their asset buying, and their actions are making the bailouts of 2008 and 1998’s Long Term Capital Management (LTCM) look like a walk in the park.

From quantitative easing to zero bound interest rate cuts and beyond, from helicopter money to economy wide bailouts, the combined monetary and fiscal interference in markets and economies over recent weeks has now distorted everything from market prices to risk preferences to the time value of money, while shattering the concept of freely trading markets and free enterprise.

All of this in an environment of locked down economies, minimal economic activity, huge job losses, shrinking tax revenue and economic stagnation, as well as the impending approach of an unprecedented global recession, that if long lasting, will become a depression.

On the monetary side, the renewed and limitless quantitative easing – with central banks creating money out of thin air to buy up financial assets across all risk categories – combined with interest rate distortions, is both prolonging the very asset bubbles that the same central banks themselves created, while also leading to explosive increases in money supply. This in turn is leading to the destruction of currency values, and most worryingly, setting the scene for the real possibility of hyperinflation.

On the fiscal side, government stimulus packages of direct payments and loan and tax write-offs across vast swathes of economic sectors is not only creating a future dependence on income support and a pretext for the introduction of direct transfers to individuals, but is burdening the very same workforces with future tax burdens and even more debt.

Helicopter Drops

In this scenario, helicopter money, analogous to a helicopter dropping cash directly to the population, comes into play. Essentially helicopter cash represents direct methods of boosting consumer demand by the distribution of currency directly to the public into their bank accounts and into their pockets. Like quantitative easing, direct cash drops pave the way for destruction of currencies and can be the touch-paper to trigger hyperinflation.

Importantly, on both the monetary and fiscal fronts, the sheer flood of official interventions across markets and economies is now creating the largest moral hazard problem the world has ever seen, with investors and economic actors being conditioned to the expectation that central banks and governments will always come to the rescue by propping up asset prices and bailing out entire sectors (think banks, airlines and real estate), thus creating an environment that encourages a lack of individual consequences for future risky behavior, but at the same time creating dire consequences for the collective financial and economic system.

While the scale of what is happening right is daunting and difficult to keep track of, a ballpark estimate suggests that the total size of interventions from just some of the world’s largest monetary and fiscal authorities is currently more than US $10 trillion and counting. For a taste for how uncharted and dangerous this QE is becoming, a quick look at the US and Europe is instructive.

Quantifying QE – USA: Whatever it takes

After cutting interest rates to zero via two emergency decisions during March (March 3 here and March 15 here), the US Federal Reserve then announced on 15 March that over the coming months it would ramp up QE by buying at least $500 billion of US Treasury securities and at least $200 billion of agency mortgage-backed securities.

That’s $700 billion of Fed debt buying from banks and the Treasury across a cross section of widening of risk categories. At the same time, the Fed begun flooding the Fed system with credit in an attempt to boost liquidity, including $1 trillion in repurchase operations per day.

When this didn’t placate markets, the Fed then went ‘all in’ on 23 March and announced the start of open-ended quantitative easing (QE) in unlimited amounts, to buy an even wider range of debt from low to much higher risk classes, promising to:

“purchase Treasury securities and agency mortgage-backed securities in the amounts needed…including purchases of corporate and municipal bonds.”

The Fed then also established swap lines with a whole range of major central banks around the world, providing these central banks with dollar funding in exchange for US Treasuries. This in essence expands the money supply of US dollars all over the world.

Then on 9 April the Fed was back, announcing another $2.3 trillion in QE, in the form of $600 billion purchases of bank loans of individuals and businesses, $500 billion buying of municipal bonds and loans (states, cities etc), and $850 billion in QE related to credit facilities of US corporates and asset-backed vehicles. Incredibly, this includes junk bonds and junk bond ETFs, with such market euphemisms as high yield, extended yield, and beyond investment grade. There is therefore, it seems, no limit to the depths the US Fed will go in its quest to prop up prices, bail out Wall St banks and hedge funds, and destroy financial markets.

Not surprisingly, this new unprecedented and unlimited QE by the Fed over March and April can already be seen in the huge explosion in US money supply, where the monetary aggregate measure M2 (which includes cash, demand deposits, time deposits and money market mutual funds) has rocketed higher from the new money “out of thin air” that has no bearing on underlying economic growth. This can be seen in the below Federal Reserve chart. As a closely watched indicator in forecasting future inflation, this M2 chart speaks volumes.

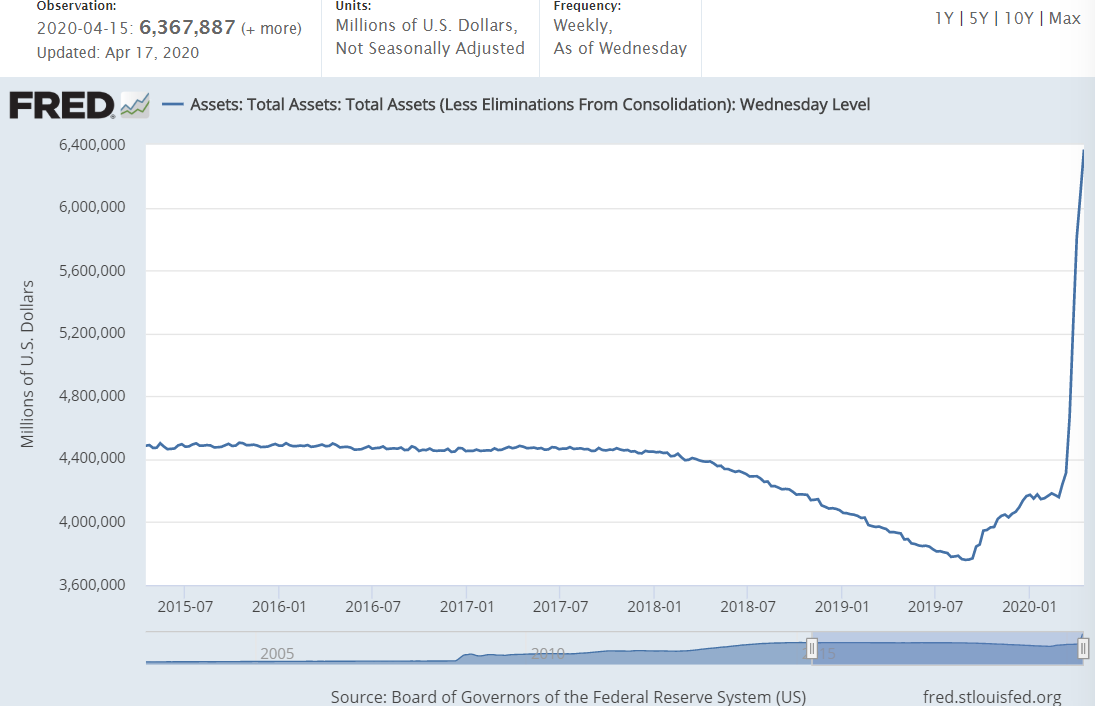

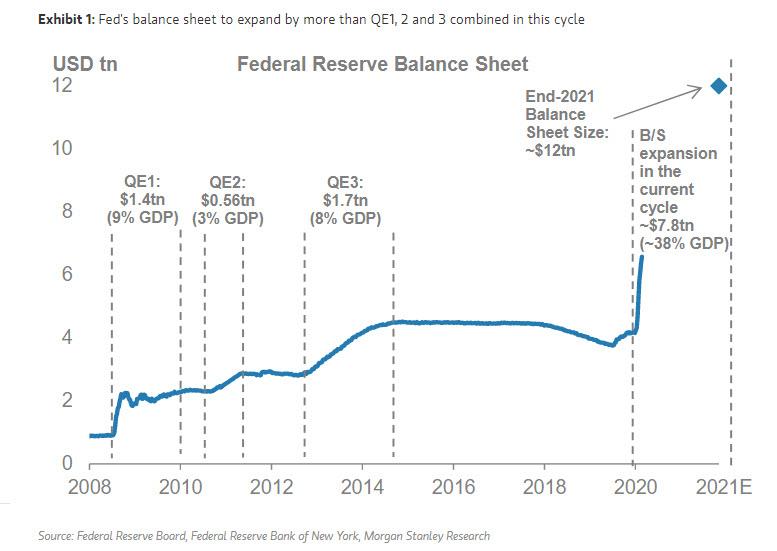

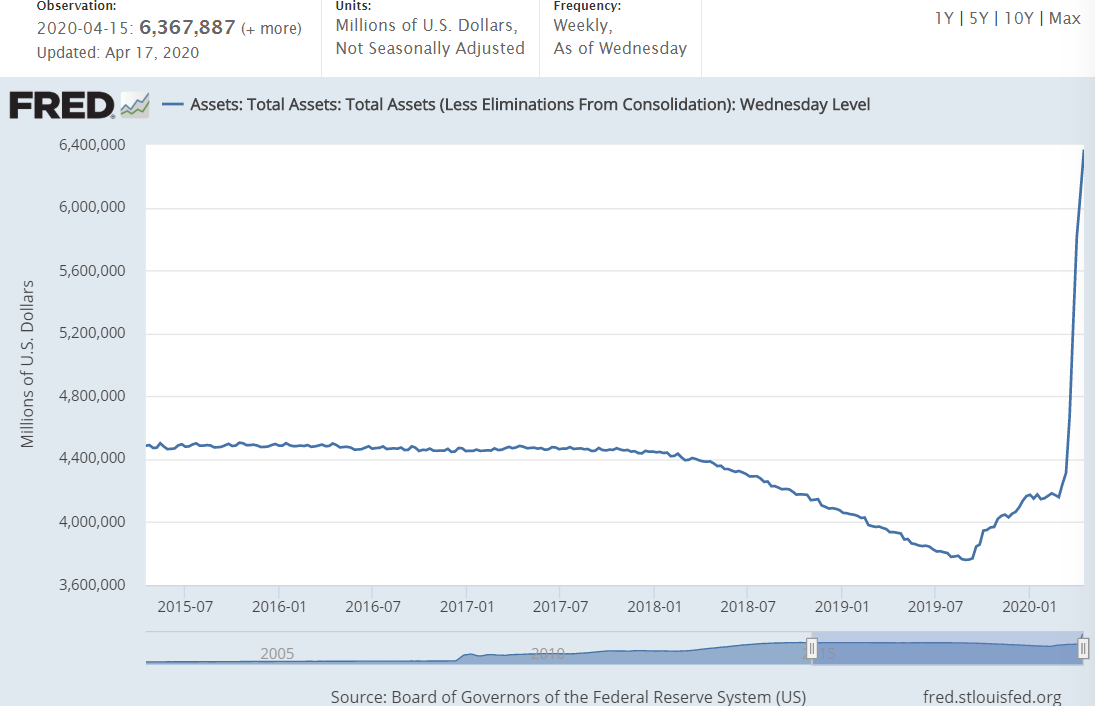

In the same vein, as architect of this rampant QE, the money out of thin air hits the Fed’s bottom line,showing up in the rapid expansion of the Fed’s balance sheet, which has ballooned from $ 4.17 trillion at the end of February to $6.4 trillion now. That’s an insane $2.2 trillion added since the start of March, or in other words, a 50% expansion in the Fed’s balance sheet since the end of February. This is neatly illustrated in the blow out of the Fed’s total assets since early March.

Turning to US fiscal interventions, at the end of March the US federal government pushed through a staggering $2.2 trillion economic bailout package titled the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), an intervention so large that it’s equivalent to 10% of US GDP. This CARES Act (which was ready and waiting in the wings) covers everything from loans to large and small corporations ($750 billion), the bailout of the US airline industry ($26 billion), loans to states and local governments ($340 billion), and most controversially, direct payments to individuals ($300 billion).

This last category is literally ‘helicopter money’, with every taxpayer in the US set to receive a $1200 payment, plus an additional $500 per child, with the transfers being made via stimulus checks (cheques) and direct deposits to bank accounts. The US IRS calls these Economic Impact Payments, but they are really direct cash injections, literally the long predicted helicopter cash drops. This money is printed out of thin air, directly distributed to the population, and most importantly raises the money supply while diluting the purchasing power of all existing currency.

An image from the original version of BullionStar’s “QE Defender’ video game launched in 2016 and featuring the Fed chairs Ben Bernanke and Janet Yellen

Quantifying QE: Europe – ECB

After cutting one of its key refinancing rates to -0.75% in early March, the European Central Bank (ECB) then announced new monetary QE interventions on 12 March in the form of €120 billion of bond buying (quantitative easing) to complement its existing bond buying programme. On the same day, the ECB also announced an intent to flood cheap liquidity to European banks using longer-term refinancing operations (LTROs).

A week later on 18 March, the ECB ramped up the QE and went practically unlimited, announcing an enormous €750 billion Pandemic Emergency Purchase Programme (PEPP), a fancy name for even more QE that aims to buy government and corporate bonds (debt), including non-financial commercial paper (short-term loans). In total, that’s €870 billion in monetary QE interventions from the ECB.

Extraordinary times require extraordinary action. There are no limits to our commitment to the euro. We are determined to use the full potential of our tools, within our mandate. https://t.co/RhxuVYPeVR

— Christine Lagarde (@Lagarde) March 18, 2020

On the fiscal side, Europe is leading the way with the largest fiscal bailout by any economic bloc so far, totaling a massive €3.2 trillion in fiscal bailouts across the continent. This includes emergency packages of individual European countries such as Germany, Spain and France, but also an EU wide bailout fund of €540 billion to which the European Union has agreed, consisting of €240 billion in credit for Eurozone countries via the European Stability Mechanism (ESM), €200 billion in loans for small businesses via the European Investment bank, and €100 billion in loans for job support.

The sheer scale and unprecedented nature of these European union interventions motivated one of its countless bodies, the European Economic and Social Committee, to proudly comment on 16 April that:

“In less than 4 weeks, the EU has done more than in the four years following the 2008 crisis, with interventions already decided that are estimated at over EUR 3 trillions.”

As to how the EU will pay for all of these bailouts, the EU Commission claims to have the answer, saying that it will, surprise, surprise, “propose borrowing to finance the recovery plan“.

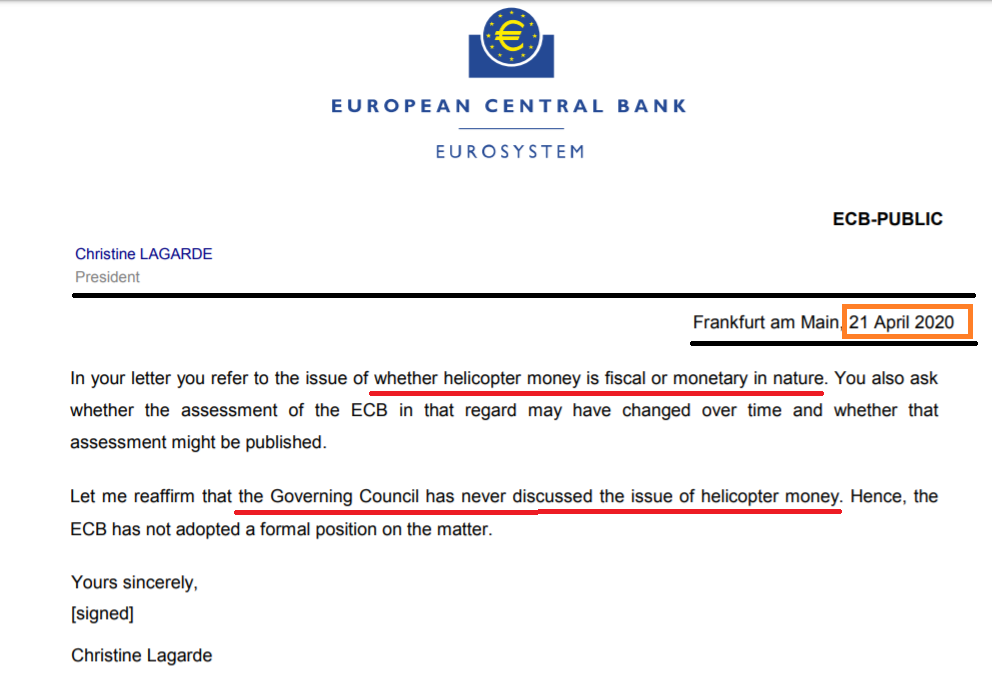

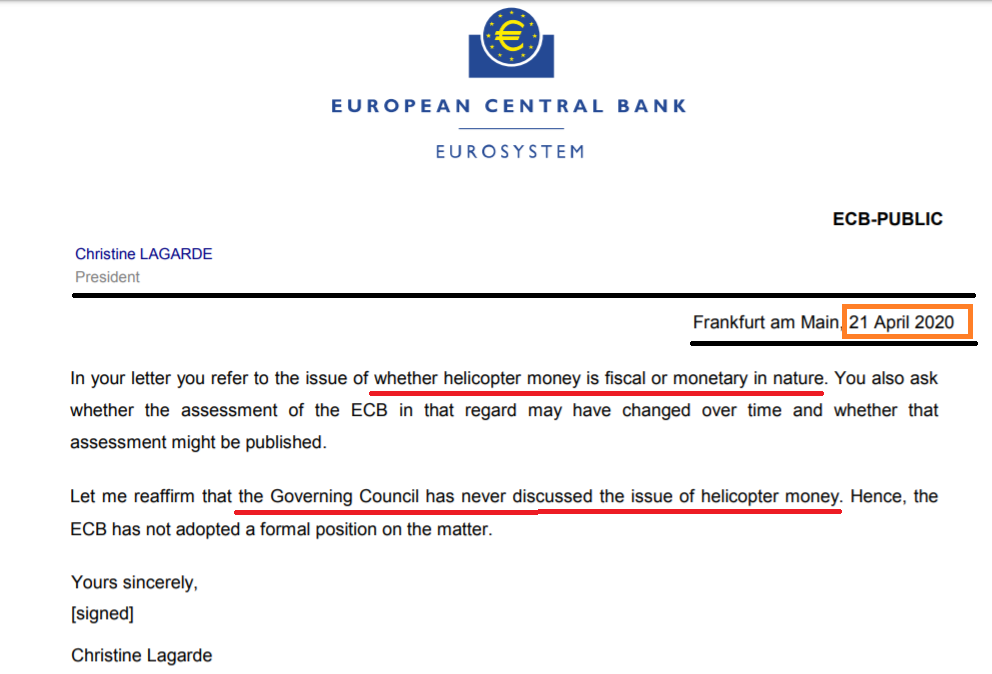

With the US government introducing helicopter money, can Europe be far behind? While the European Central Bank claims that helicopter money is not an option that’s being considered, would you believe them? In a recent letter responding to a member of the European Parliament (dated 21 April), the ECB’s Christine Lagarde avoids the question of whether helicopter money is a fiscal or monetary in nature, only saying that it has never been discussed by the ECB’s Governing Council. But in the infamous words of another fellow Europhile Jean-Claude Juncker, “When it becomes serious you have to lie.“

Beyond the Fed and the ECB, all other major monetary authorities and governments around the globe are also engaging in massive QE and economic bailouts, from the Bank of Japan and Bank of England to the Chinese and the International Monetary Fund (IMF), from Australia to Brazil and from South Korea to Singapore. For example, the Bank of England has its own £645 billion QE programme buying UK government bonds and sterling corporate bonds, and has now moved to directly finance the spending the UK Treasury, a form of helicopter money.

Meanwhile, the Bank of Japan has just announced that it will now consider unlimited bond buying of government and corporate bonds – “Bank of Japan mulling unlimited bond buying at next meeting: Nikkei“. Everywhere one looks, the evidence is there, it’s QE to infinity, buying up all debt of all types and all risk categories at any price, in the process destroying the financial system and setting the scene for hyperinflation.

Hyperinflation

In an interview in 2010, then Fed chairman Ben Bernanke tried to dissuade concerns over Fed money printing, QE and market interventions, saying that:

“This fear of inflation I think is way overstated …What we’re doing is lowering interest rates by buying Treasury securities. And by lowering interest rates, we hope to stimulate the economy to grow faster.

The trick is to find the appropriate moment when to begin to unwind this policy. And that’s what we’re going to do.”

Fake words then from Bernanke, fake words now. There was no real unwind. Tapering was trick and a distraction. This is the same Bernanke who explained how the Fed’s lending is merely electronic printing, creating money out of thin air, and in so doing, inflating the money supply.

Fed’s Ben Bernanke in 2009: “To lend to a bank we simply use the computer to mark up the size of the account” https://t.co/pFLm5FxqM6 #QE

— BullionStar (@BullionStar) April 23, 2020

Quantitative easing, despite the complicated name, is a simple case of massively expanding the money supply. Helicopter money ditto, is also a simple case of massively expanding the money supply.

By artificially boosting demand in a scenario of lower production and constrained supply using the printing press and its electronic equivalent (QE and helicopter money), more fiat currency is entering the existing system. This can lead to product shortages, hoarding, and higher consumer prices, i.e. rising inflation, which is the economic textbook situation of too much money chasing too few goods.

Rising inflation in turn leads to lower purchasing poor and eroding value for a paper currency, loss of confidence in that currency, and in a downward spiral, faster spending to get rid of the increasingly worthless currency, which in turn leads to even higher prices, hoarding and inflation. And all this in an environment of economic stagnation and recession. This then leads to higher inflation expectations, and ultimately hyperinflation.

And what are we seeing right now in the global economy, led by the large central banks and the largest economies? Explosions in money supply brought on by quantitative easing. Increasing experiments of directly transferred helicopter money to artificially boost consumer demand. Supply side shortages and hoarding. Economic turmoil and economies in stagnation due to covid-19 lock downs with massive unemployment and economies slipping into recession and possible depression.

Hyperinflation is essentially a rapid and accelerating inflation amid a collapsing currency value, and it can arrive rapidly in an environment where frequent price rises have already begun to take hold. In such scenarios, national cash becomes worthless and precious metals and reserve currencies become stores of values. For some of the more prominent hyperinflationary events in recent times just look at the hyper inflationary experiences of Argentina, Zimbabwe and Venezuela. See “The Power of Gold in Times of Crisis” for details.

For example, in 1989, prices in Argentina rose by an annualized 500 percent. In 2008, Zimbabwe’s annual inflation rate at one point reached 231 million percent. Annual inflation in Venezuela, which is still in the midst of hyperinflation, is currently over 2300%.

But what if hyperinflation hits major economics such as the US and Europe and their ‘strong’ fiat currencies in the form of the US dollar and Euro? In the current environment of full-scale quantitative easing and the emerging popularity of helicopter money, this is something which populations may soon be about to find out.

Under this possible scenario, physical gold will become one of the few trusted assets to remain a secure store of value and wealth preservation when paper currencies crash and burn. Universally trusted as a safe harbor in times of crisis and emergency, physical gold is both the proven last man standing and the go to asset in a world at risk of hyperinflation.

This article was originally published on the BullionStar.com website under the same title “QE Defender – Stop the QE Insanity | Helicopter Money and the Risk of Hyperinflation”

Tyler Durden

Sun, 05/03/2020 – 21:30

via ZeroHedge News https://ift.tt/2Yw1lEQ Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}