Stockman: Triumph Of The Woke Mob Led By Two Doddering Old Fools

Authored by David Stockman via Contra Corner blog,

Events of the last few days have made one thing crystal clear: The Democratic Party (and therefore the nation) is being led by two doddering old fools who should be domiciled in a rest home, not the Oval Office and the Speaker’s Chamber.

How that baleful reality coexists with Wall Street’s expectation of an awesome economic future and stock prices which never stop rising to the sky is one of the great enigmas of our times. Or maybe it’s just because $10 trillion of fiscal and monetary “stimulus” in the past year can turn the proverbial sow’s ear into a silk purse. For a time.

By now, of course, we expect idiocy from Sleepy Joe, especially on the economic front.

Accordingly, at his virtual global summit he will be reading-out from the White House teleprompter the demented agenda of the Climate Change Howlers. Therein he will promise to cut greenhouse gases by 50% by the end of this decade, which calamity we can also promise would cut America’s debt-entombed economy to its knees.

That comes after Tuesday’s White House contretemps when he first prayed for a guilty verdict in the Chauvin trial even as the jury was sitting in its deliberations, and then, afterwards, made the risible claim that this tragedy was the spawn of systemic racism.

In fact, Nanny State over-reach was the underlying cause of George Floyd’s arrest and unjust death—just as it is the source of most of America’s unfortunate violence between police and unarmed citizens, back, white and otherwise.

In both cases, of course, we find Sleepy Joe fronting for the hideous core agenda—race baiting and climate hysteria— of a Democratic Party which has lost its way and has been taken over by a camarilla of woke zealots.

Indeed, if there were any doubt about the latter, Nancy Pelosi’s truly venal deification of George Floyd should remove it once and for all.

Yes, the man was a victim, but he was also a drug-addicted criminal lout and grifter, who deserves no place of honor anywhere; and who’s estranged family deserves sympathy and support, but not a $27 million gift of blood money from a woke city council that takes Minneapolis one step closer to its demise every time it meets.

“And thank God, the jury validated what we saw, what we saw,” Pelosi said in front of the U.S. Capitol Building as she delivered remarks with the Congressional Black Caucus. “So, again, thank you George Floyd for sacrificing your life for justice. For being there to call out to your mom. How heart-breaking was that? To call out to your mom, ‘I can’t breathe.’ But because of you – and because of thousands, millions of people around the world who came out for justice – your name will always be synonymous with justice.”

For crying out loud. George Floyd didn’t sacrifice himself in the cause of justice. He got hopped up on a lethal dose of fentanyl and then foolishly resisted arrest when the original officers on the scene attempted to place him in the backseat of a squad car.

That is to say, the entire narrative culminating in Nancy Pelosi’s hideous idolization of George Floyd has been blatantly wrong from the get go. This case is not about racial justice at all, to say nothing of striking a blow against so called “white privilege”.

For want of doubt, we need to repeat the facts. That’s because they show that episodes like the George Floyd case do not fit the stereotypes of either the BLM and its race-card playing progressive/Dem allies or, for that matter, the Foxified Right’s knee-jerk defense of the nation’s over-empowered, over-budgeted, over-militarized police.

Needless to say, the George Floyd case was not an aberration. During the recent past there were 38 such police killings of unarmed black citizens in 2015, and then 19, 21, 17 and 9 during 2016 through 2019, respectively. That’s 104 black lives lost to the ultimate abuse of police powers.

Of course, the number should be zero police killings of unarmed citizens. There is no conceivable excuse for heavily armed cops—-usually working in pairs or groups—to cause the death of lone, unarmed civilians, regardless of race or anything else.

And in this case that was especially so, and not withstanding several mitigating factors.

For instance, the Minneapolis police officers originally attempted to put George Floyd safely in the back seat of a squad car after his arrest for the petty crime of attempting to pass a counterfeit $20 bill, but he resisted them intensely for up to five minutes. That’s plain as day in the other videos—those from the cops’ body-cams.

The trial evidence from these body-cams also showed that during this struggle around the squad car Floyd said he couldn’t breath six times owing to a severe medical reaction to the fatal level of fentanyl in his blood and the methamphetamines that he had ingested shortly before the incident. These reactions were surely compounded by the man’s “severe” and “multifocal” arteriosclerotic heart disease and clinical history of hypertension, which the Minneapolis medical examiner said was the underlying cause of his death.

Yet after Floyd was cuffed and placed prone on the street, as he himself had requested, and the officers had called for an ambulance owing to his obvious medical distress, the arrest went haywire and Chauvin exposed himself to Manslaughter 2, at least, for no plausible or justifiable reason.

That’s because Floyd had been unarmed throughout the incident, was hand-cuffed and incapable of flight or harming others and was surrounded by four armed officers. Accordingly, he was no threat to them, nor anyone else, and he therefore presented no policing reason for the extended knee-hold on the back of his neck—especially after the surrounding crowd had warned the police that Floyd was in self-evident dire distress.

So as we see it, Chauvin’s conviction on second degree manslaughter does indeed comport with the Minnesota statute, which reads as follows:

…..by the person’s culpable negligence whereby the person creates an unreasonable risk, and consciously takes chances of causing death or great bodily harm to another;

But here’s also where the Woke/Progressive Left narrative goes even more haywire. Floyd’s death was due to an arrest which shouldn’t have happened and bad police behavior that has nothing to do with race.

As to the former point, what should have been on trial in this case was not “systemic racism”, but the Nanny State for grotesquely excessive use of force to enforce a petty counterfeiting complaint that should not be police business in the first place. It’s the job of retail store owners to handle petty counterfeiters or people who unknowingly pass bad greenbacks and to absorb the cost of self-protection just like they do in the case of refusing charges on bad credit cards.

So there is zero reason why George Floyd should ever have been arrested.

As to bad police behavior, you do not have to look too hard to see that it’s essentially color-blind and that being non-black is no guarantee against the same unjust fate.

During the same five-year period in which 104 black lives were lost, a total of 127 unarmed white lives were wasted by the police, as well. That included 32 white killings in 2015 followed by 22, 31, 23 and 19 in 2016 through 2019, respectively.

Overall, 302 unarmed citizens were killed by the police during those five years, with the balance accounted for by 71 deaths among Hispanic and other victims. That is, the real issue is illegal and excessive police violence, not racial victimization.

Indeed, the fact that 34% of these police killings involved black citizens compared to their 13% share of the population is not primarily a sign of racism among police forces, although it is continuously construed to be.

It’s actually evidence that the Nanny State, and especially the misbegotten War on Drugs, is designed to unnecessarily ensnare a distinct demographic— young, poor, often unemployed urban citizens— in confrontations with the cops, too many of which become fatal.

Alas, young black males are disproportionately represented among this particular inharms’-way demographic, and that’s the reason they are “disproportionately” represented in the 302 cases cited above.

Stated differently, the Nanny State results in too many black victims of plain old injustice, even if that is not necessarily the intent of the crusaders and zealots who have launched the state into anti-liberty wars on drugs, vice and victimless iniquities and peccadillos.

That is to say, statism in the sphere of law and order is every bit as dysfunctional as it is in the realm of economics, yet neither conservatives nor progressives recognize it.

Conservatives want way too much law and police empowerment in the service of cultural norms that are none of the state’s damn business in the first place; and progressives confuse the often brutal and unjust over-reach of law enforcement agencies as a manifestation of racism, when it is actually just policing expectorations in behalf of inappropriate missions such as the enforcement of drug laws.

Indeed, the main trouble in America today is not overt racism or even simmering racial animosity. The real evil is the relentless aggrandizement of state power in the form of the Nanny State—a conflation of too many laws, crimes, cops, arrests and thereby opportunities for frictions between the state and its citizenry and for abuse by the gendarmes vested with legal use of violence.

In a word, some citizens sometimes can’t breathe their last breath because in far too many instances liberty can’t breathe in today’s unhinged Nanny State, either.

Among the most recent notorious cases, of course, are George Floyd’s fatal arrest for allegedly passing a counterfeit $20 bill; Eric Garner (NYC 2014), subdual for selling untaxed cigarettes; Rayshard Brooks for falling asleep drunk in his car at a subsequently incinerated Wendy’s in Atlanta; and Breonna Taylor of Louisville for being awake in her own apartment at 1:30 AM when police barged in with guns blaring in a drug enforcement raid.

These are anecdotal cases, of course, but the big picture statistics tell the same story. In the most recent year of complete data (2018), there were 9.3 million arrests in the US excluding traffic enforcement charges of DUI. Yet among this massive number of arrests, those involving serious crimes against persons and property accounted for just 521,000 or 5.6%. These included:

-

Negligent murder and manslaughter: 11,970;

-

Rape: 25,205;

-

Armed robbery: 88,128;

-

Aggravated assault: 395,800;

That’s it. That’s the contribution to core public safety delivered by the 850,000 sworn law enforcement officers in the USA—about 0.6 arrests per year for serious crimes per law enforcement officer.

As for what they were doing the rest of the time and the other 8,777,000 arrests that occurred in 2018, we can say this: They clearly provided more occasion for conflict between citizens and the gendarmes and for policing actions to go haywire, as in the George Floyd case, than any additional increments of public safety.

After all, the single largest category of arrests in 2018 was for drug abuse violations, which totaled 1,654,282.

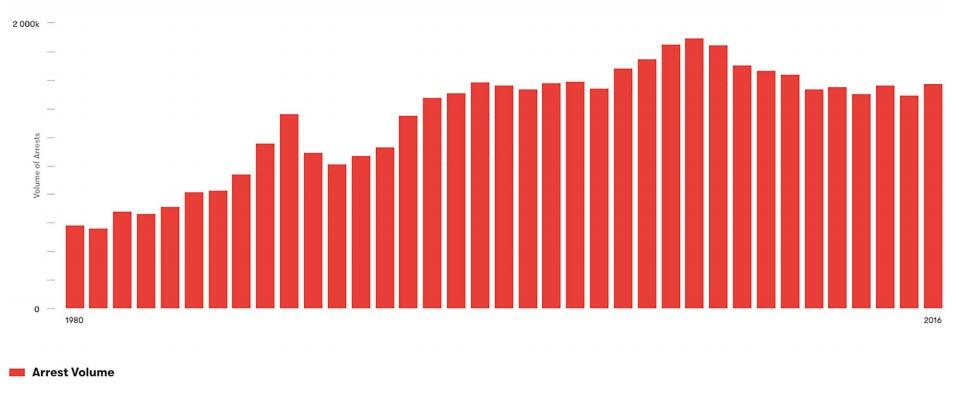

In fact, while total arrests for all crimes in 2018 were no higher than they were in 1977 despite a 100 million/50% growth in the US population, and had actually dropped from a peak of nearly 13 million in 2006, the opposite trend was extant in the case of the nation’s misbegotten War on Drugs arrests.

As shown by the chart below, drug arrests in 2018 were nearly at peak levels and were up by more than 171% since 1977—the vast majority of which are made for drug possession generally, and marijuana possession most often.

War on Drugs Arrests, 1980-2016

Not surprisingly, the next largest arrest category after drugs is one called “other assaults” for which 1,063,535 arrests were made in 2018. Yet the FBI’s own definitions raise considerable doubts as to why these are even a proper matter for law enforcement by the state:

Other assaults (simple) – Assaults and attempted assaults where no weapon was used or no serious or aggravated injury resulted to the victim. Stalking, intimidation, coercion, and hazing are included.

Then, of course, we have all the victimless and vice crimes, including the following number of arrests:

-

Prostitution and commercialized vice: 31,147;

-

Sex offenses excluding rape and prostitution: 46,937;

-

Gambling: 3,323;

-

Liquor law offenses: 173,152;

-

Curfew and loitering law violations: 22,031;

-

Vagrancy: 23,546;

-

Public drunkenness: 328,772;

-

Disorderly conduct: 329,152;

-

Forgery and counterfeiting: 50,072;

-

Weapons carrying and possession: 168,403;

-

All other offenses: 3,231,700.

The latter huge number tells you all you need to know. The UCR lists 27 enumerated categories of crime including all of those itemized above–plus the usual suspects like fraud and embezzlement for which there were about 135,000 arrests in 2018. Yet when the whole lists is exhausted, 32% of arrests occurred for crimes that are so minor even the FBI is embarrassed to enumerate them!

So, yes, we do think there are way, way too many crimes and cops, and that decriminalizing and de-funding law enforcement are the only route to reducing police violence.

But by the same token, the unwarranted and often mendacious racializing of police malfeasance, which the George Floyd case has brought to a fever pitch, will only insure retrogression. That is, it will unleash a blind rallying to the defense of law enforcement by conservative Republicans, blue collar whites and the Foxified Right, thereby insuring a continuing failure to attack and drastically curtail the Nanny State regime, which is the real source of policing injustice.

Of course, don’t expect Nancy Pelosi or Sleepy Joe to be any more enlightened on the matter than Sean Hannity. These doddering old fools are now enthrall to the wokedom of the progressive-Left; and, as Maxine Water’s blatant performance as agent provocateur in Minneapolis the night before the verdict makes clear, these people want the problem to fester and metastasize, not be alleviated.

Indeed, it is probably not too far fetched to say that Congresswoman Waters’ call for a guilty verdict or else a new round of violent uprisings amounted to an insurance policy. Three guilty verdicts could not trigger the latter, but a judicial appeal resulting in a mistrial order surely would.

In other words, the Democratic Party has fallen into the grip of vicious leftist zealots and power-hungry authoritarians. And the events of the last two days suggest that two dangerously wrong-headed and ugly narratives—-race-baiting and climate hysteria— now stand at the center of the Dem agenda because the party’s two supreme leaders are too weak and too senile to resist the mob.

So we’d say to the feverish punters of Wall Street, yes, embrace the putative Economic Boom impending and buy the Greatest Financial Bubble in history, if you must.

But, really, if the events which culminated in Tuesday’s triumph of mob justice do not scare the living bejesus out of you, then, well, you probably deserve to suffer the thundering financial gotterdammerung which is surely coming your way.

Tyler Durden

Thu, 04/22/2021 – 18:25

via ZeroHedge News https://ift.tt/3dHOrux Tyler Durden