Rabobank: “Coronavirus Is The Kind Of Risk That Doesn’t Just Put You Out Of Your Portfolio, But Out Of The Game”

Submitted by Rabobank’s Michael Green

China returned from a longer-than-usual lunar New Year holiday today. Not the swathe of businesses that have been forced to close temporarily; and not the now tens of millions under quarantine at home; and not the villages that have barricaded themselves in from the outside world; just the financial markets. And, despite the promise from the PBOC of CNY150bn (USD21.7bn) in extra liquidity, lower rates, and whatever it takes to get through this ahead of market open, the initial response was a complete collapse: at one point the Shanghai stock exchange was -8.7% on the day – and recall that under the terms of the Phase One US-China trade deal, US financial firms are supposed to be diving in to this kind of market aggressively; the Chinese currency, both off and onshore, has crashed through the psychological 7 level once again; and trading in Chinese commodity markets has been suspended after iron ore, copper, crude oil, palm oil, and eggs all closed limit down on the day.

Of course, there is going to be a spill-over into other markets. You wanted to know what a real decoupling from China might look like, and/or what a “What if everyone just stayed at home and didn’t buy anything?” economic thought-experiment looks like? Well here you are, folks.

In terms of trade, Australia and New Zealand are at the front of the queue, as well as time zone-wise. Add plunging iron ore to a cessation in Chinese tourist arrivals, and to the news that high-value agri imports like lobsters are allegedly not allowed into China anymore, and you have all the ingredients for AUD to give up the 67c level and NZD to give up 65c. Yet other global commodity exporters are likely to feel the pain. For just one example, China’s oil consumption is now down 20% according to sources quoted on Bloomberg. That is the equivalent of an economic depression, not a recession, landing overnight. Expect prices, and global inflation expectations, to follow suite. Indeed, there is already talk of an emergency OPEC meeting. Yet even ordinary exporters (and more so net exporters) of goods and services are going to get hit. In fact, you’d need to be a continent-sized, inward-focused, commodity importer to be able to ride this out comfortably. Perhaps the US and India fit that bill to some degree, but less than one might think, perhaps.

Naturally, this kind of market sell-off imparts a natural tendency on the part of our not-so-natural markets for aggressive dip-buying. However, as opposed to the headline of “World War Three!” which triggered a bout of risk-off action at the start of the year, this sell-off appears far more justified. The same op-ed writers who did not understand the real-politick of the Soleimani assassination and were wrongly screaming “Sell!” after that event are today trying the argument that “More people die from slipping in the shower, etc., than this Coronavirus.”

This overlooks the fact that this virus has the potential to go exponential and become a global pandemic. It’s a small risk, yes – but it’s a FAAAAAAAT tail risk, that tens of millions of people simultaneously slipping in the shower really isn’t. Indeed, it’s the kind of huge risk that doesn’t just put you out of your portfolio position, or out of business, but out of the game, full-stop. Markets are quite right to react in a strongly negative, preventative fashion to this risk until we see evidence that it is being brought under control and the threat has truly passed. And we are not there yet, very regrettably. When we are, we see the real bounce. In short, “panic measures” are not always a sign of panic – they can be rational.

The global establishment of the WHO are, by contrast, remarkably cavalier in their market-friendly approach that there should be no restrictions on free movement or free trade as a safety-first measure, and we should all aim to find a vaccine. All very IMF. It’s not a surprise, perhaps, that once again nation-states are thumbing their noses at that particular economic policy prescription from a famous acronym and imposing travel bans and, in China’s case, import bans too (if the no seafood report is true).

On which note, today is the first trading day of the bold new world of BoJo Brexit. Headlines in that regard are that the UK is going to play hardball and is aiming to keep all its own fish, and for an EU trade deal somewhere between those of Canada and Australia rather than the far closer relationship that had been initially promised. Indeed, BoJo is talking about preparations for full customs/border checks in 2021 once the transition period ends. That also suggests a healthy dose of risk-off is required. However, for whom? Some of the impacts of this kind of scenario could arguably prove more positive than the Brexit naysayers have long warned. Nissan, which runs a huge car plant in Sunderland that has long been flagged as at risk under hard Brexit, is today claimed to have a contingency plan to pull out of European production and double down on the UK market instead, where it would then have a competitive edge vs. tariffed European imports. So less EU exports, more UK local production, and more UK jobs – in that one industry.

Conservative radio icon Rush Limbaugh announced on his Monday show that he has been diagnosed with advanced lung cancer.

Rush Limbaugh just announced on his radio program he has been diagnosed with advanced lung cancer. Says there will be days he won’t be able to be there due to treatment…

All of a sudden, events are looking a bit fluxy out there, as though the world is shuddering through some spooky ch-ch-ch-changes, like a monster waiting to be born, with strange convergences of ecology, politics and economy, and there’s only so much you can do to prepare, really. Criticality is in the air!

The horses are out of the barn on the Wuhan Coronavirus. Air travel was curtailed too late in the game — and still only partially — with asymptomatic-but-infectious human carriers winging to every corner of the world and probably contaminating airports all along the way. There’s plenty of thought and counter-thought on what exactly is going on behind the scenes in China. The ruling party has knocked itself out demonstrating its earnestness in the crisis, performing great feats like the construction of a one-thousand-bed hospital in ten days, shutting down the lunar new year festivities (like cancelling Christmas here), and locking down a hundred million citizens in quarantine. Pretty impressive.

But there’s also a theory that the Coronavirus affords a cover for cascading failures in China’s corrupt and shifty banking system. The country had already stepped across some frontiers in demographics, energy consumption, and industrial growth that were shoving it toward contraction for the first time in two generations. Coronavirus has shut down a lot of production in big things like cars and big-little things like cell phones, and supply lines are shutting down to world markets. This amounts to the first big test of the integrated global economy, as well as the world’s debt-saturated business model.

When a lot of parties and counterparties can’t pay each other because their revenue flows are cut off, the securities, currencies, equities, and other abstract representations of wealth go south. The US and Europe are no better positioned for a crisis in their banking arrangements, and confidence is starting to crack. Both economic mega-regions have relied on central banking hocus-pocus to prop up stock markets and maintain the illusion that the logic of bonds still applies. The first thing to go moneywise in a contracting financial system is the magic of compound interest.

The US Federal Reserve has been massively gaming the Repo markets — overnight lending that uses bonds as collateral — since September, raising suspicions that more than one of its “primary dealer” banks are insolvent. Juicing them with “liquidity” is like painting over sheetrock infested with black mold. Looks good for a week or so, and then you’re in intensive care. Nobody knows yet what the effect of Britain’s escape from the EU will do to the Union’s remainers, but Europe’s bonded debt arrangements are even dodgier than America’s, since there is absolutely no EU central control of each member’s fiscal affairs. Anyway, the meta-trend now is the devolution of governance from giant-and-central to smaller-and-local, so the real question is how much disorder and damage do these nations endure as that happens. It’s been manifesting vividly in France for a year in the yellow vest protests.

Here in the USA, the knock-on effects of converging crises begin to look like a game of four-dimensional eight-ball. The oil markets are getting slammed around the $51 hashmark, making it more difficult for the shale oil producers to meet their onerous debt repayments (in an industry that just doesn’t make a profit). Lower gasoline prices may seem like a boon for US motorists, but it comes at the expense of bankrupting more oil companies and punishing lenders like pension funds that invested in shale securities in the desperate search for “yield.” Shale never was a rational business model despite its fabulous production surge in a very short span of years. Don’t be surprised if there’s an attempt to nationalize it, which will induce new problems of capital allocation and sheer incompetence in a world where central planning of anything is more and more a bad bet.

Looming and converging multiple crises are also behind the gross disorder in US politics, though the connections may not be so discernably visible. President Trump foolishly took credit for financial markets that he had correctly described as being “one big, fat, ugly bubble,” back in the febrile days of the last election. Now it threatens to leave him holding a big fat ugly bag of trouble. That booby trap is surely more hazardous to his reelection chances than the frenetic efforts of pissants like Adam Schiff running Wile E. Coyote ambuscades in the DC Swamp. Mr. Trump spent three years working, jawboning, and bluffing over global trade arrangements that are now suddenly falling apart. How much of that will turn out to be a temporary effect of the Coronavirus, nobody knows. Or maybe it’s an inflection point in the workings of our over-hyper-complexified human ecosystem.

These shifting quandaries leave the Democratic Party between that ol’ rock and a hard place. All of their bad faith ploys against Mr. Trump have failed so far. I speak to supposedly educated people every day upon whom the failure of the Mueller Investigation, the fiasco of impeachment, and the revelations of IG Michael Horowitz have made no impression at all. The Golden Golem of Greatness is still Putin’s Puppet to them. It’s a wonder of the age that they can’t cut their losses. And now Bernie Sanders suddenly looks poised to win the Iowa caucus and inflame the not-quite-so-socialist factions of the party, who appear to be ratcheting up some Wile E. Coyote traps against him.

If that works, it’ll blow the party apart, 1860 style, into rump factions. But if Bernie somehow perseveres and gets the nomination… and the Potemkin financial markets tank… and Coronavirus turns out to be a very big deal for upsetting global trade… then, America may get its first zealous socialist president.

Yes, history repeats and rhymes and all that, but I don’t see Bernie replicating the triumphs of Franklin D. Roosevelt in Great Depression 2.0. Rather, by attempting to overlay command-and-control policies on a zeitgeist that wants to take us smaller and local, Bernie Sanders will only be bucking reality.

The net effect of Bernie Sanders in the White House will be to finish off the economy… and imagine where that will take us.

Two people were killed and another wounded in a shooting at a Texas A&M University dorm hall on Monday at its campus in Commerce, Texas, according to campus police and media reports.

A twitter account believed to be associated with the university confirmed the two deaths.

There have been 2 confirmed deaths. The third victim has been taken to the hospital for treatment. UPD has stationed officers throughout campus, including all key gathering points, for the safety of the campus community.

We will continue to share updates as they are available.

The university police said all classes were canceled for the rest of the day amid an active criminal investigation. Texas A&M’s campus in Commerce, Texas, is over 200 miles north of Texas A&M’s main campus in College Station.

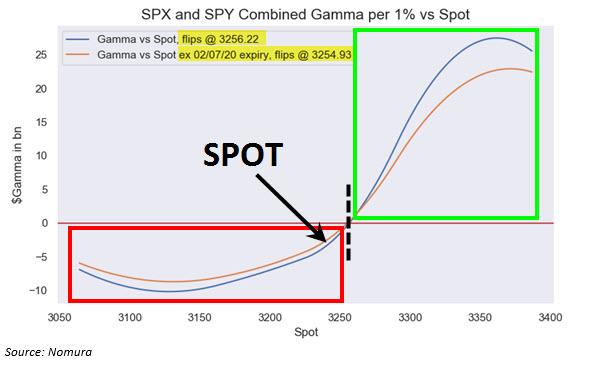

Why 3,254 Is The Only Number That Matters For Traders Today

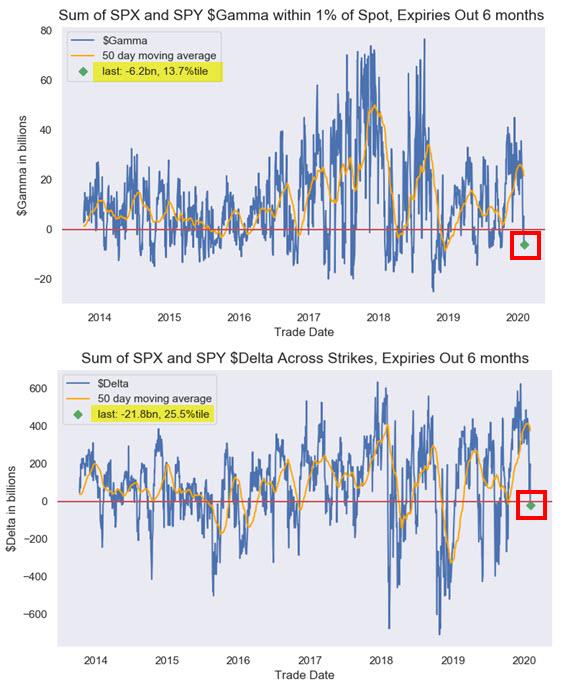

When commenting on the crash in Chinese stocks late on Sunday night, we pointed out that US equity futures had managed to buck the liquidation trend seen across Asia, rebounding from Friday’s rout lows, rising into the mid-3200s, a level which was critical because as we had pointed out previously on Friday, this is roughly where the critical gamma “flip” level was, below which gamma transforms from a risk dampener into a risk accelerator.

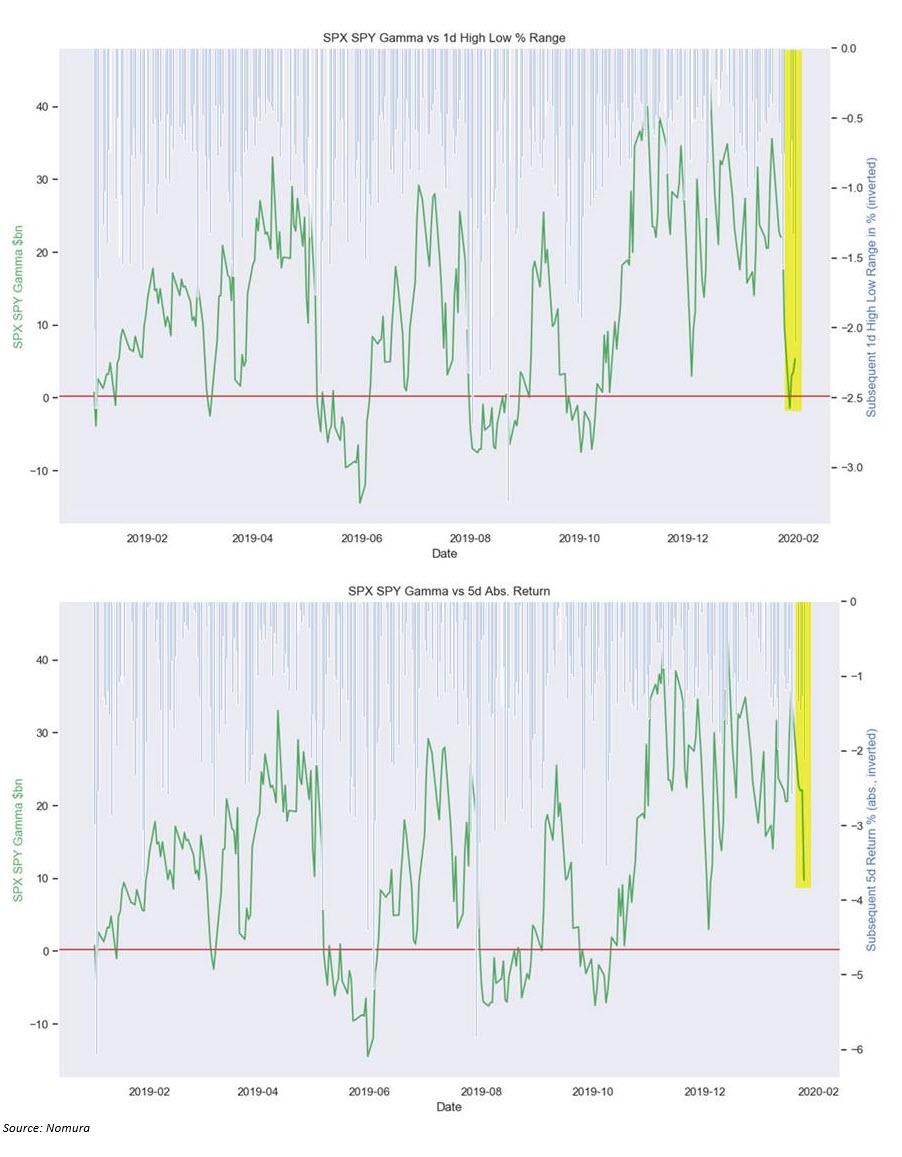

On Monday morning, Nomura’s cross-asset strategist and quant, Charlie McElligott, picked up on this key point again, one which he has been covering for years, and writing that indeed, should stocks fail to rebound from their Friday open, it could get messy as consolidated option positioning shows both dealer gamma and delta is now negative…

… with dealer now back in a short gamma position for the first time since the start of the October meltup. In fact, it now appears that the gamma “flip” level is 3,254, which explains why market makers who hope to preserve the bullish benefits of positive gamma are fighting so hard to keep the S&P at this level. Not surprisingly, at last check, the S&P was trading right on top of this level.

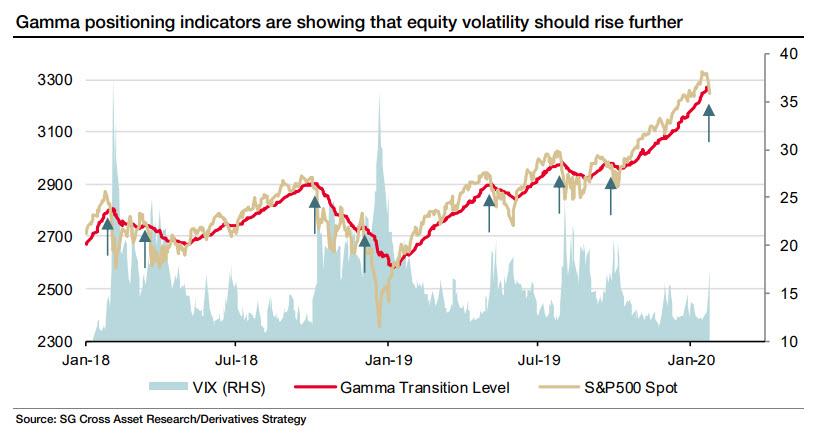

For those confused, here is a quick refresher: gamma-linked indicators are designed to estimate whether hedging by market makers is currently suppressing or elevating volatility. Positive gamma leads to dampening of index moves because the hedgers need to sell when the market moves up and vice versa. Negative gamma leads to hedgers exacerbating volatility as they sell when the market moves down and buy when it goes up. The chart below from SocGen shows that the S&P500 spot moving into negative gamma territory (below the red line) is consistent with higher levels of VIX, which in turn leads to further selling in the S&P, a greater disconnect from gamma, and even higher volatility, and so on, in a feedback loop.

Like Nomura’s McElligott, SocGen’s derivatives strategy team estimated last week that aggregate dealer gamma had briefly moved into negative territory on the S&P500, and remains close to it, a byproduct of the notorious “gamma gravity” effect whereby gamma flip levels tend to serve as “strange attractors” for the broader market, something we have discussed since 2018.

McElligott underscores this point, and notes that once again, the change in the gamma “impulse” took place concurrent with a large move in the S&P.

Alternatively, as a function of market reflexivity, one could claim that it is the drop in gamma that leads to higher vol, and lower prices. Direction of causality notwithstanding, the bottom line is simple: 3,254 is the one level that every trader should be focusing on to determine what the market will do in the very short term, and should SPX spot fail to rise above the gamma flip level, there is great potential for a period of higher turbulence in the short term.

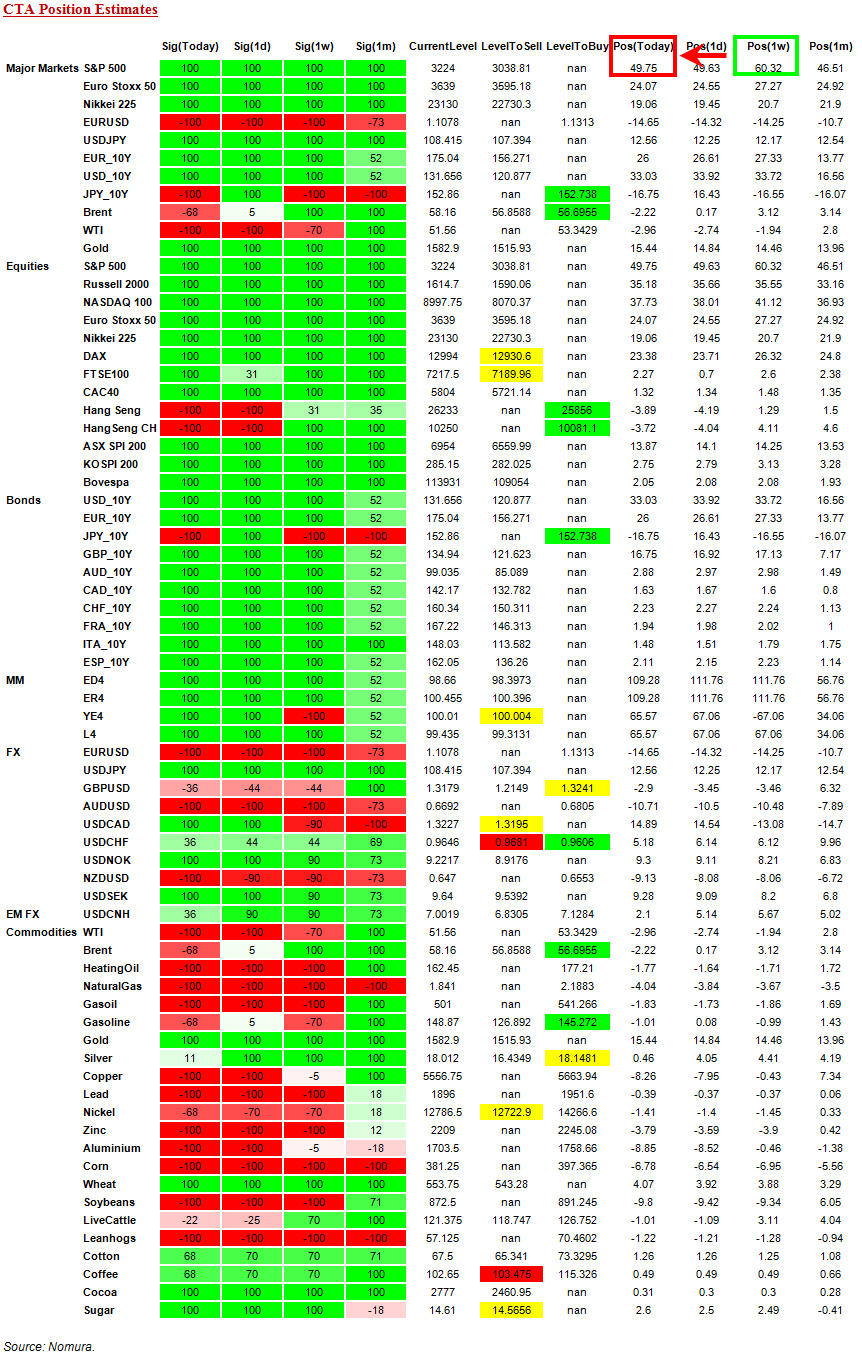

There is another reason why traders should be closely watching the battle over 3,250, and it has to do with an entirely different set of investors: CTAs.

According to Charlie, the Nomura QIS CTA model shows that despite the overall signal for the SPX position remaining “+100% Long” as of this morning (as all three time horizons with any “weighting”—3m, 6m and 12m—are all still “buy” signals), the short-term 2w window has flipped “Short” due to the recent impulse move lower/the jump higher in trailing realized vol — which means that the “gross” exposure in the SPX futures position has been deleveraged from the two year “high” of 60.3% made last week, now reduced to this morning’s 49.8% position

And while the 2-week signal in the CTA model is already a “Sell,” if today the S&P closes flat, or worse, red, McElligott would “expect to see the 1-month signal turn “Sell” tomorrow as well.” Still, the only signals that matter for now are the 3m, 6m and 12m models — thus the position maintains the overall “+100% Long” status.

But that too will change if SPX spot closes below gamma, as dealers now are “incentivized” to chase the market lower, resulting in lower prices, higher VIX, an even greater delta between spot and gamma, even more selling, etc. in a feedback loop; and with VIX spiking it would eventually push all CTAs signals more bearish, until eventually all those green “100% longs” start shrinking until eventually they all go flat, and then turn negative, as CTAs officially join the selling frenzy.

Bottom line: keep an eye on where S&P closes the day: 3,254 is all that matters.

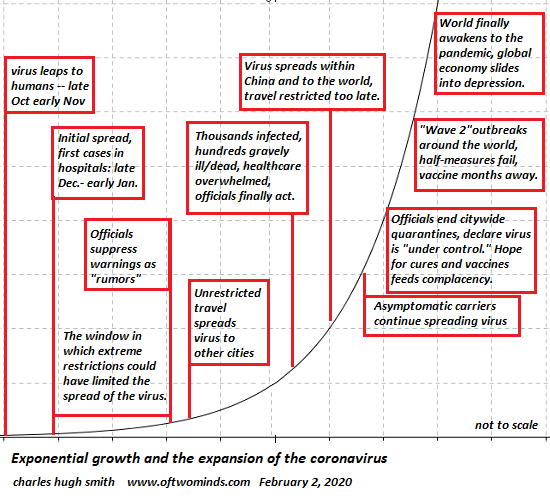

If we accept what is known about the virus, then logic, science and probabilities all suggest we brace for impact.

Here’s a summary of what is known or credibly estimated about the 2019-nCoV virus as of January 31, 2019:

1. A statistical study from highly credentialed Chinese academics estimates the virus has an RO (R-naught) of slightly over 4, meaning every carrier infects four other people on average.

This is very high. Run-of-the-mill flu viruses average about 1.3 (i.e. each carrier infects 1.3 other people while contagious). Chris Martenson (PhD) goes over the study in some detail in this video.

Let’s say the study over-estimates the contagiousness due to insufficient data, etc. Even an RO of 3 means the number of infected people rises geometrically (parabolically).

This matters because it negates any plan to track every potentially infected person who came in contact with a carrier.

Coronaviruses tend to be contagious in relatively close contact (within two meters / six feet) but masks may not be enough protection, as it may spread by contact with surfaces and through the eyes.

All available evidence supports the conclusion that this virus is highly contagious, i.e. it isn’t that difficult to catch.

2. Along with its contagiousness, the most consequential feature of this virus is that asymptomatic carriers can transmit it to other people, who will also be unaware they’ve been infected with the pathogen.

This means carriers have no reason to self-quarantine until they develop symptoms, which may be a week or more after they’ve begun spreading the virus to others.

It’s easy to imagine a situation where an asymptomatic carrier from Wuhan took a flight to Beijing, infecting passengers and people in the airport, who then got on flights going to international destinations, where a few days later they become asymptomatic transmitters of the virus.

(The passenger from Wuhan might also have boarded a flight to the U.S. in Beijing, before flights from Beijing were restricted.)

By the time the initial individual carrier from Wuhan develops symptoms, the virus has already gone through two geometric expansions and everyone infected has no idea they even have the virus.

Common sense suggests that airplanes, airports, crowded markets, elevators–any confined space where a number of people might pass through a two-meter contagious circle around the carrier– might result in a contagion rate far above 4.

It seems entirely possible for one carrier in crowded, constricted areas to infect 12 people, who might infect 12 others. If these 144 individuals infect 12 others, that’s 1,728 infected people from one carrier.

That may sound extreme, but it’s easy to imagine 100+ people passing within two meters of a carrier in crowded venues or touching surfaces just touched by the carrier. It could be that only one in ten exposed people catch the virus, but if the carrier is in close proximity to 120 people, that means 12 individuals will contract the virus.

3. Nobody seems to be tracking the origin point of travelers. If an asymptomatic carrier from Wuhan took a train or flight to Beijing last week (exposing other passengers to the pathogen) and then boarded a flight from Beijing to SFO (San Francisco), the presumption would be that the traveler is from Beijing.

Tens of thousands of people have boarded flights in China over the past month and deplaned in international destinations. The likelihood that some consequential percentage of these travelers originated from Wuhan, or were infected by someone from Wuhan, is high.

It’s basically impossible to thread these three points together and not conclude that a massive expansion of the virus is about to manifest in dozens of international destinations.

Put another way: this virus is a nearly ideal combination of contagiousness and asymptomatic transmission that enables a rapid spread of the virus via people who have no idea they’re carriers.

4. Locking down major cities is a good strategy to contain the spread of the virus if the lockdown outlasts the contagious period of every carrier–say, two weeks–and the lockdown isn’t porous enough to enable an RO of above 1. (Reducing the RO to 1.5 will still enable an expansion of asymptomatic carriers.)

But given that 5 million people already left Wuhan, and some consequential percentage are likely to be carriers, then this doesn’t stop all those travelers from initiating geometrically expanding epidemics in all Chinese cities that aren’t locked down.

As I noted in a recent blog, a very large number of non-resident migrant workers from rural, impoverished western China live and work in every major Chinese city. Once their ability to make a living in the informal economy is impaired, their only choice is to either return to their home village/town or seek work in a city that hasn’t been locked down.

This mass movement of informal-economy workers more or less insures the virus has spread far and wide from Wuhan long before the city was fully locked down.

Locking down Beijing and Shanghai might limit the spread of the virus in these mega-cities, but it won’t stop the virus from spreading to every city that has yet to be fully locked down.

These conclusions are drawn from what is already known about the virus. There would have to be a complete revocation of all that is known to change the parabolic trajectory of the epidemic.

5. The mortality rate of the virus is hard to pin down for a number of reasons. One is that mortality is a time-series, meaning counting those who have died isn’t an accurate measure of all those who are infected who may die in the near future.

Furthermore, the official totals are suspect, as numerous anecdotal reports have come out indicating people who died were mis-classified as victims of “pneumonia.” Other reports indicate the overwhelmed healthcare system in Wuhan has been sending corpses to be cremated without proper identification of the cause of death.

It appears Chinese officialdom is reverting to the same tactics used in 2003 to suppress data about SARS and downplay the dangers of the pathogen. It seems highly unlikely that the death totals being announced are accurate, and highly likely that the totals are a fraction of actual deaths.

There isn’t enough trustworthy data to estimate the mortality rate of the virus, but even the official totals, when coupled with the number of patients in intensive care, suggests a higher rate of mortality than typical flu viruses but less than SARS 9%.

What’s worrisome is the official attempt to downplay the danger of the virus naturally reduces the incentive to be extra-cautious, self-quarantine, etc.

In effect, under-reporting the true mortality rate is actually encouraging the spread of the disease by diminishing the resolve of those worried about dying to be extra-cautious.

If early evidence that a cocktail of anti-viral and HIV medications can reduce mortality is confirmed in large-scale trials, that good news has to tempered with the stipulation that these drugs don’t reduce the risks of contagion; the expectation of a ready cure will also act to reduce the incentives to be extra-cautious. This expectation of a ready cure may be premature, but even if the cocktail meets high expectations, it doesn’t mean the virus won’t spread and sicken those who catch it.

If the cocktail only works on certain classes of patients or is ineffective in some cases, the presumption that a 100% cure is now available could actually accelerate the contagion as authorities and individuals clamor for an immediate “return to normal life.”

Authorities are like the officers on the Titanic who were tasked with both reassuring the passengers everything was under control and urging them into the lifeboats: you can’t tell everyone the risk is low and everything’s under control but it’s also high enough that you better get in a lifeboat. This is a classic double-bind. In the confusion, few understand the risk remains high and act accordingly.

6. Given all this, it seems inevitable that the handful of cases outside China will expand rapidly in the weeks ahead, and the impossibility of tracking all those who came in contact with carriers means the spread of the virus cannot be contained except by locking down all transportation and cities where the virus has spread.

7. Restrictions are half-measures. U.S. travel bans, for example, exempt U.S. citizens / green card holders and their immediate families. This amounts to thousands of people who will be allowed into the U.S. from China with a caution to monitor themselves for 14 days.

8. As I mentioned in the blog a week ago, a large number of Chinese people work overseas, and they will be returning to their jobs this coming week, as the official New Year’s holiday ended 2 February. While some airlines have stopped flights to and from China, not all airlines have done so. So these workers have a number of ways to get back to their overseas jobs: catch a flight to somewhere outside China and then catch a flight to Europe, Africa, the U.S. etc.

If you’re not sick, or only have the sniffles, you don’t want to be stuck in China. You want to get back to your job. If you do have the sniffles, you wear a mask and take over-the-counter medications to reduce fever. You tell yourself the risk of having the coronavirus is low and so you proceed on that basis.

9. The quarantines in China are more porous than advertised. Thousands of people are coming and going into quarantined cities every day. How long can China quarantine tens of millions of people before supplies are exhausted and the financial pain becomes unbearable? If the quarantine ends and there is still a pool of carriers in the city, the virus will quickly re-emerge. The quarantine is only effective if literally every last carrier of the virus either dies or recovers and is no longer contagious.

If 100 asymptomatic infected people move into the city after the quarantine is lifted, this pool of carriers will re-introduce the virus, which will spread anew.

Quarantining a few cities and leaving hundreds of other cities, towns and villages as reservoirs of the virus insures the virus will return to the quarantined cities as soon as the restrictions are lifted.

To stop the spread of the virus, every community, village, town and city in the entire nation would have to be locked down.

The horse already left the barn a month ago, and so closing the barn door now has little effect. Five million people already left Wuhan and tens of thousands have already traveled to dozens of other countries. The virus can no longer be contained with half-measures. Yet half-measures are all the authorities are willing to impose.

Nassim Taleb co-authored a paper (download available on his site) that explained why the only way to limit the spread of the virus is to severely limit connectivity of people and transport: the more connections exist, the greater the number of avenues for the virus to spread.

If China reduced connections with the rest of the world to zero, even for a month, the financial impact would trigger a global recession due to the fragility of the global economy and its dependence on China. Since authorities are unwilling to risk a global depression, they pursue half-measures which insure that multiple pathways for the pathogen to spread remain open.

10. The general assumption in the U.S. is that this will all blow over and the virus will burn itself out as a result of the Chinese quarantines and U.S. travel restrictions. This is akin to passengers on the Titanic looking around 10 minutes after the minor collision with the iceberg and seeing zero evidence the ship was in danger of sinking. Yet the ship’s sinking was already inevitable despite the lack of visible evidence.

For the virus to burn itself out, all of these conditions must hold: only a handful of the tens of thousands of people who’ve landed in the U.S. from China over the past month are infected with the virus, and virtually every one of the infected people, despite having no symptoms, will rigorously self-quarantine themselves for 14 days to insure they won’t infect anyone else.

Furthermore, these carriers can’t have transmitted the virus to others on their airline flight, in the airport, in baggage claim, in Immigration Control, in the subway, etc. before they started their rigorous 14-day self-quarantine. In other words, not one person exposed to the virus caught it.

In addition, those expecting the virus to burn itself shortly must assume that no one slipping through the exceedingly porous restrictions will be an asymptomatic carrier, and that any asymptomatic carriers that do slip through will not have any close contact with other people.

Lastly, those expecting the virus to burn itself shortly must assume that the virus will not mutate into a more contagious or deadly form, even though viruses mutate at very high rates: the more people carry the virus, the greater the opportunities for a mutation to occur that can be spread to other hosts.

None of these assumptions are even remotely realistic.

Neither is the expectation that an effective vaccine will be ready for mass inoculations in a month or two. Realistic timelines for an effective vaccine are four to six months for development of a vaccine, then additional months to test its safety and effectiveness and more months if all goes well to produce hundreds of millions of doses of the vaccine, and then more time to distribute the vaccines.

It’s natural to grasp at straws in crisis, and natural to take every false dawn for sunrise. Announcements that the rate of infection is slowing will be taken as evidence the virus will soon be completely under control, when a decline from RO 4 to RO 3 or RO 2 doesn’t mean the virus is about to disappear; all it means is the rate of expansion has declined. Premature announcements of a cure will encourage a complacent expectation of a quick return to “normal life” that will be severely challenged by the “Wave Two” global expansion of the virus.

The economic, political and social consequences of the extreme measures required to control the spread of the virus (total lockdown of an entire country’s transportation systems)–or the failure to pursue such extreme measures, enabling the spread of the virus–are the second-order effects I’ve been exploring in recent blog posts: consequences have their own consequences.

If we accept what is known about the virus, then logic, science and probabilities all suggest we brace for impact.

John Solomon’s Laptop Stolen Near White House Using ‘Sophisticated Device’; Contained Sensitive Data On Ukraine, Bidens

A thief absconded with John Solomon’s laptop on the eve of the Senate impeachment trial, snatching the evidence-filled device out of the investigative journalist’s car which was parked near the White House, according to RealClearInvestigations, citing a report by the D.C. Metropolitan Police Department.

Solomon told RCI‘s Paul Sperry that the laptop – which has since been recovered – contained ‘notes on Ukraine and former Vice President Joe Biden and other sensitive information.’

The case is currently under investigation by a MPD detective.

The Secret Service is also involved in the matter, which appears suspicious. Break-ins are rare in the high-security area where the crime occurred, just outside the White House perimeter, and a sophisticated device appears to have been used to get into the vehicle.

In the early evening of Jan. 20, the police report states, Solomon’s Apple MacBook laptop and computer bag, valued at around $1,800, were stolen from his 2019 Toyota SUV parked at 1776 F St. NW, across from the White House’s Eisenhower Executive Office Building. No windows were broken, and there were no other signs of forced entry. Authorities suspect the thief or thieves used an electronic jamming device to open the car door lock.

Nothing else was stolen from the vehicle, according to Solomon, including his US Capitol press security badge.

The computer bag was discovered the next day a block away from where his car was parked, with the contents dumped out on a picnic bench near the FDIC building – a location with no security cameras which authorities described as one the rare “dark spots” in the area.

Solomon says he is working with a computer forensics experty to determine whether any of the information on his laptop was exploited, or if his hard drive was scanned.

“It’s a pretty professional job,” said Solomon, adding “but it’s probably just a coincidence.”

“It was probably just a street criminal searching for pass codes,” he expounded. “Or it could be someone searching for my Ukraine stuff. We don’t know at this point.”

Solomon targeted by Democrats

As Sperry notes, Solomon’s private phone number was published by House Intel Chair Adam Schiff (D-CA) in December, while citing the journalist at least 35 times in his impeachment report over Solomon’s involvement in reporting Ukrainegate from the perspective of the prosecutor who former Vice President Joe Biden had fired while he was investigating Ukrainian energy giant Burisma – whose board Hunter Biden sat on.

“I’m the only [reporter] who ends up having his records released,” Solomon told Fox BusinessNews recently.

“It makes me wonder whether it’s a political payback, because a few months ago, I wrote a story exposing the fact that Chairman Schiff had met with Glenn Simpson at the sidelines of the Aspen Institute at a time when he shouldn’t have been having contact with Glenn Simpson,” he added. “It feels like a political payback.“

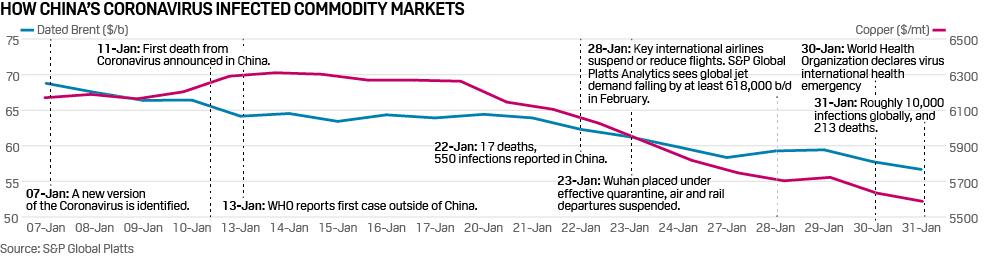

The spread of coronavirus outside China and the WHO’s escalation of the outbreak to emergency status last week continue to stoke fears over weaker energy demand and disruption to key mineral resource supply chains. In this special edition of Commodity Tracker, S&P Global Platts editors take a look at the impact across a number of energy products and raw materials.

1. Key benchmarks fall

Dated Brent lost approximately 5% of its value during the course of last week (January 24-31), while copper – seen as a barometer of economic health – saw an even larger slide. However, by the end of the week market participants were seeing the metal as oversold, with some looking to take long positions in anticipation of China returning to the market.

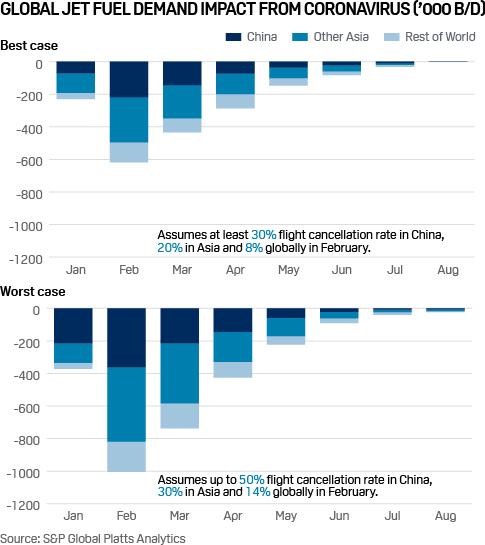

2. No blue skies for jet

Key international airlines including British Airways, Lufthansa, American Airlines, United Airlines, Swiss International Air Lines and Austrian Airlines, suspended or reduced flights due to the outbreak. S&P Global Platts Analytics forecasts show potential for a steep drop in jet fuel demand. In the best case scenario, global demand for jet fuel could fall by 618,000 b/d in February, and in the worst case scenario, by 1 million b/d.

3. Palm oil problems

Prices of crude palm oil, commonly used in food products, fell sharply last week following a three-month long rally, correcting by 10% in a single day, on a combination of a huge selloff worries about lower demand. China, the world’s second-largest palm oil buyer, imported 6.8 million mt of the product in 2018-19 (October-September).

4. Double blow for LNG

The coronavirus outbreak has compounded an already depressed market for LNG. The JKM Asian spot LNG price has fallen below $4/MMBtu to levels not seen since May 2009 on persistent oversupply and weak demand. China has driven global LNG demand growth in recent years, so any slowdown in import growth in the country could have a significant impact. If reduced industrial activity across Hubei Province extends to end-February, S&P Global Platts Analytics estimates it would reduce Chinese LNG demand in the month by 5%-7% relative to its base case, or 11-15 million cu m/d.

5. Iron ore falls

Prices of iron ore 62% Fe fines delivered to north China (IODEX) fell 10.3% over the past week alone (January 24-31) to $81.65/dmt on Friday, after steel market demand prospects deteriorated. Some steel mills in Shandong and Shanxi provinces have reportedly reduced production by up to 20% in February. Transport restrictions to control the spread of coronavirus have made it difficult to obtain raw material supplies or export steel, while many local construction projects have been halted.

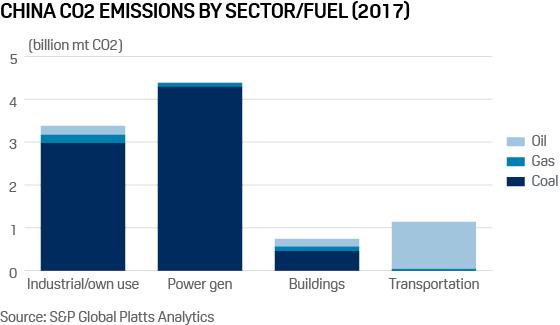

6. Emissions impact

Quantifying the impact of the coronavirus outbreak on China’s carbon emissions is a hugely complicated endeavour. However, the most obvious sector impacted is oil, which dominates China’s transport emissions at 1,094 million mt CO2 in 2017. China’s power sector – which is dominated by coal – generated 4,393 million mt CO2 in 2017, while the industrial sectors emitted 3,380 million mt. A key factor will continue to be the extent of Chinese government curbs on transport and industry. Even a 1% drop in China’s annual CO2 emissions from energy consumption would amount to 96 million mt, , equivalent to France’s annual regulated CO2 emissions.

Rare Direct Clash Between Turkish & Syrian Armies Leaves Scores Dead & Wounded

Turkey has accused the Syrian Army of shelling Turkish positions in Idlib, killing six troops and a civilian, and wounding an additional seven soldiers, according to Al Jazeera.

Turkey’s Defense Ministry said its military immediately hit back against Syrian positions, destroying the source of fire; however, it’s unclear the extent to which the Syrian side suffered casualties. Turkey claims it’s defensive attack killed and wounded scores of Syrian troops.

Defense officials further condemned the aggression given they say Turkey gave advanced notice of their coordinates as part of a cooperative agreement with Russia. But Russia responded Monday to the criticisms by saying the Turkish positions were hit out of a lack of information.

Turkey heavy armored units in Syria, file image.

Though disputed by Syrian sources, President Erdogan subsequently claimed the Turkish counterattack killed between 30 and 35 Syrian troops, which involved fighter jets and artillery unleashed on Syria’s military.

“Those who test Turkey’s determination with such vile attacks will understand their mistake,” he said, suggesting further Russia authorized such defensive strikes when needed. “It is not possible for us to remain silent when our soldiers are being martyred,” Erdogan added.

However, Syrian Army statements and sources still say despite the Turkish interference they’ve advanced on the flashpoint town of Saraqeb, considered crucial to liberating Idlib.

In an alarming sign that the Syrian and Turkish armies could be on the brink of broader war in Idlib and northern Syria, the Britain-based opposition group Syrian Observatory for Human Rights, said Turkey shelled Syrian Army positions across three provinces, killing a total of eight soldiers as of Monday.

Ankara has said Damascus’ push to take Idlib province is forcing hundreds of thousands of civilians to flee the assault towards the Turkish border, adding to Turkey’s refugee woes, which it claims has now reached 3.5 million it is hosting in its borders.

Erdogan has threatened to act militarily against pro-Assad forces if they don’t cease their destructive offensive in war-torn Idlib. It now appears he’s making good on that threat, and we could see things escalate quickly — though it remains that Idlib is still recognized by the UN as sovereign Syrian soil (now occupied by al-Qaeda linked Hayat Tahrir al-Sham), which Assad has vowed to liberate “every inch” of.

There have been suggestions that the White House defense team could be brought up on bar charges for their arguments in the Senate.I have previously written that such statements by Speaker Nancy Pelosi and others are vindictive and ill-informed. The White House team were effective advocates for their clients and we do not disbar lawyers for making arguments or defending individuals that we do not like. I was surprised and disappointed therefore that my fellow witness from the Trump impeachment hearing, North Carolina Law Professor and CNN Legal Analyst Michael Gerhardt joined this dubious argument on CNN yesterday. The call for ethics charges seems dangerously close to the view of Lawrence O’Donnell that Trump defenders are barred from his MSNBC program because they are all “liars.”

Obviously, Gerhardt and I have substantial disagreements. Gerhardt supported the articles of impeachment based on bribery and other crimes. I opposed those four articles, which were ultimately rejected by the Committee. The Committee went forward with the two articles that I said would be legitimate but remained unproven. We later disagreed when Gerhardt declared that this impeachment was the first time that the White House closely coordinated with his own party on the handling of the impeachment trial. Those however were academic differences over the history and interpretation of prior presidential impeachment cases.

This however is different. Proponents of the impeachment seem to be lashing out at counsel and suggesting that they were acting unethically in zealously advancing the President’s defenses. After disagreeing with me that the impeachment was not “rushed” prematurely, Gerhardt asked to make a different point about the defense team. He declared

“I think what we are seeing as well is that the lawyers who presented his case in the Senate basically misled or lied to the Senate. And so at one point – at some point we are going to see ethics charges brought against these lawyers for making false statements, which we now all know were false.”

CNN host Poppy Harlow followed up by asking Gerhardt “Do you think the D.C. Bar . . . is actually going to hold Pat Cipollone, for example, to account for this?” Gerhardt doubles down against everyone on the legal team: “I think what we are seeing as well is that the lawyers who presented his case in the Senate basically misled or lied to the Senate. And so at one point — at some point we are going to see ethics charges brought against these lawyers for making false statements, which we now all know were false.”

It is not clear what Gerhardt believes were statements “we now all know were false.” It is incumbent on an attorney to be specific about the false representation when he is saying that “we are going to see ethics charges brought against these lawyers for making false statements.” He is saying that the entire team will be charged with ethical violations – a very serious allegation against all of these lawyers. Indeed, such a statement itself can be viewed as a matter of per se slander for impugning professional ethics and conduct. Even clients have been held liable for unsupported claims.

Moreover, bar associations are equally concerned about the ethics of impugning the conduct of other lawyers without sufficient support. Various ethics opinions warn that threatening or declaring bar violations can be unethical, particularly when (if true) you are under an obligation to actually report such conduct. If there is a lack of a good faith basis or support, it can violate professional standards.

The Gerhardt charge appears to be a loose reference to the a series of leaks and newly obtained evidence that showed that Trump was involved in seeking the investigations in May 2019. It is a curious foundation. The team did not deny that Trump wanted the investigations and cited the fact that the controversy over the Biden contract had been raised in the media since the Obama Administration. Recently, discussed emails also show that Trump was communicating on the possible freeze with other officials. Again, that is not on its face proof of any intentional false statements by counsel, who argued that Trump was long concerned about foreign assistance to the country.

There is also the report that former national security adviser John Bolton claims in his forthcoming book that Trump directed him to ensure that Ukrainian President Volodymyr Zelensky would meet with Rudy Giuliani, the president’s personal attorney — a meeting allegedly attended by acting White House chief of staff Mick Mulvaney and White House counsel Pat Cipollone. Once again however that such a statement, if made, would not be materially different from what was argued. The White House released the transcript showing that Trump wanted to arrange a meeting with Giuliani. What Trump has recently denied is that he ever told Bolton that the Ukrainian aid was linked to the investigations.

Moreover, the White House team landed some haymakers themselves in showing that the House Managers misrepresented aspects in the record. House manager Adam Schiff was previously given four Pinnochios by the Washington Post for his denial of any contacts between his staff and the whistleblower. Should he join this line of counsel to be frog-marched to the bar? Such disagreements tend to be the grist of the litigation mill. Lawyers often present one-sided views of the record that the other side views as unfair or unsupported. We do not declare on national television that the entire opposing legal team “will” (not even “may be”) called before the bar.

The defense took the record of the House and did what good lawyers do: they argued the best case within that record. We cannot allow the age of rage to adopt William Shakespeare’s line from Henry VI: “The first thing we do, let’s kill all the lawyers”.

It is even worse when it is lawyers seeking to shoot lawyers.

{kind=link}