Most of you reading this will be aware that Zerohedge’s prolific and highly popular twitter account with over 670,000 followers was on the receiving end of a lifetime ban by the Twitter politburo. This post won’t focus on the details of this specific ban, but if you want to read more about it, see the following: Zerohedge Suspended On Twitter.

It’s imperative not to overly focus on the individual victims of tech giant bans, and instead zero in on the bigger picture. Rather than debating whether or not you like Zerohedge, or whether you think it crossed a line, I want to highlight the dangerous implications of dominant social media companies wielding permanent bans as a weapon on freedom of speech in practice.

This post will cover three main issues. First, the fact that Twitter and other social media companies have essentially created a caste system when it comes to engagement on their platforms. Second, the question of whether or not a lifetime ban from social media platforms is an ethical concept. Third, the dangers of Twitter essentially throwing the entire timeline of a banished account into the memory hole.

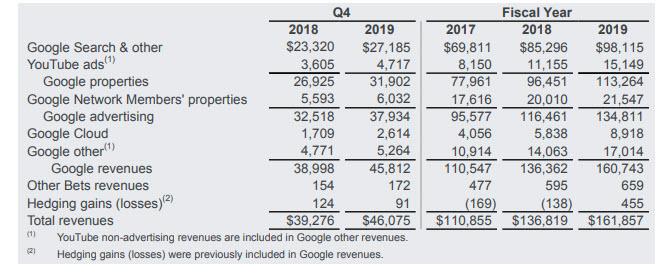

Google Tumbles After Revenue, Profit Miss; Breaks Out YouTube, Cloud For First Time

After the stellar earnings reports from Apple, Microsoft and Amazon (lets ignore Facebook for now), investors were expecting nothing but great news from the world’s biggest search engine, Google, aka Alphabet, despite reports earlier today that DOJ officials are meeting with state attorneys general reps tomrrow afternoon to discuss their antitrust investigations of Google.

Alas, it was not meant to be, and moments ago Alphabet reported Q4 earnings that while beating on the bottom line, missed on revenues, operating margin and operating profit, to wit:

Q4 EPS of $15.35 beat Est. $12.50

Q4 total Revenue $46.08BN missed Exp. $46.94BN

Q4 Revenue Ex-TAC $37.57B missed Est. $38.40B

Q4 Oper Margin 20% missed Est. 24.7%

Q4 Oper Income $9.27B missed Est. $9.79B

Also of note: for the first time ever, Google broke out its YouTUbe and Cloud revenue, and reported it generated $15.15BN in YouTube revenue and another $8.92 billion in Cloud. As Bloomberg notes, “breaking out Cloud and YouTube revenue is monumental for Wall Street.” YouTube revenue nearly doubled from 2017, where it was $8.15 billion, and while some investors had expected overall YouTube sales for 2019 to be as high as $20 billion, they will probably take $15BN.

Meanwhile, on the cloud side the business also more than doubled since 2017, from $4.1 billion to $8.9 for the full year 2019, which while solid still lags the market leader, Amazon Web Services, which reported $9.9BN in just Q4 revenue last week. That said, Google’s cloud business grew 53% Y/Y, far above the 34% growth rate posted by AWS.

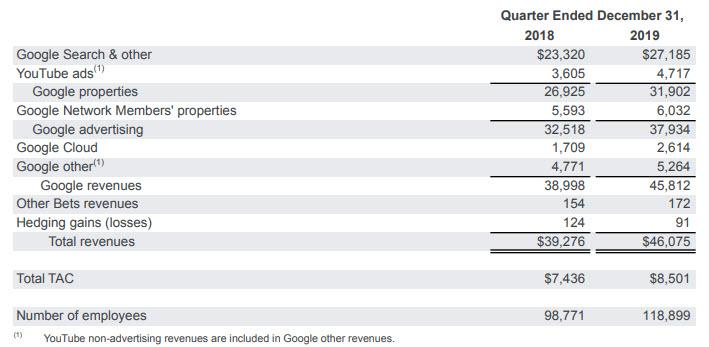

Visually:

Meanwhile, Alphabet’s “other Bets” – from self-driving cars to its biotech units – continued to bleed cash, losing $2.03 billion during the quarter on $172 million in revenue.

Despite the revenue miss, revenue growth was still a solid 18%, although with the stock soaring in the past year, it – like the rest of its FAAMG peers – was priced beyond perfection, and investors were not happy, especially as a result of the sharp jump in TAC or traffic acqusition costs, which rose by $1BN in Q4 compared to a year ago, suggesting that Google’s ads business is getting more costly. And, as shown below, Google has never paid more in comp: Alphabet now employs 118,899 people, up more than 20,000 from a year ago.

There was a silver lining on the cost side: overall CapEx fell year-on-year to $6.05 billion, with almost all of the spending going to Google, not the “Other Bets” companies like Waymo and Verily.

On net, while the business continues to post solid growth, concerns about rising costs, and a miss on the top-line and profit margins left a sour taste in investor’s mouths, and as a result GOOGL stock, with its 27x forward PE…

… dropped sharply after hours, tumbling as much as 5%, before stabilizing slightly below 3% lower.

Chris Matthews was roundly derided by progressives Monday morning after the MSNBC host delivered a two-minute diatribe against 2020 Democratic presidential primary frontrunner Sen. Bernie Sanders, claiming that the Vermont senator would lose to President Donald Trump in a general election matchup.

“The Bernie surge has Chris Matthews on the verge of tears,” tweeted Sanders supporter Samuel Finklestein. “It’s okay, Chris.”

MSNBC host Chris Matthews on “Morning Joe” Monday said he was unhappy with the direction voters are taking the Democratic Party. (Image: screenshot/MSNBC)

Matthews appeared on MSNBC‘s “Morning Joe” as part of a panel discussing the primary. Arms crossed and looking upset, the “Hardball” host claimed that while all of the candidates in the primary contest were flawed, Sanders was one of the worst.

“I’m not happy,” said Matthews. “I’m not happy with this field.”

The longtime newsman and onetime Democratic congressional aide said that Sanders reminded him of George McGovern, whose 1972 bid for the White House against incumbent Richard Nixon was a disaster for the party.

“Moronic cable tv millionaires like Chris Matthews truly believe nothing good can ever happen in America because of an election that happened 50 goddamn years ago,” said Rousseau. “Cry more, Chris, we love to see it.”

Despite his concerns, Matthews admitted that Sanders is likely headed to a strong showing in Iowa’s Monday night caucuses.

“I think he’s gonna win big tonight, real big,” said Matthews.

The cable news host also disparaged Sanders as analogous to the kind of older activists manning anti-war tables at rallies — a comment that echoed Trump’s red-baiting attacks against Sanders in a Super Bowl interview with Fox News host Sean Hannity.

As the Outline‘s Shuja Haider pointed out, that’s not necessarily a knock on Sanders.

“Chris Matthews says Bernie is like an old guy distributing socialist literature at an antiwar rally, as though that’s a bad thing,” said Haider.

“Old people at protests from CodePink, Vets for Peace, etc., are some of the most authentic people you will ever talk to,” said Walker. “Chris Matthews thinks they’re kooks because they spend their time giving a shit about our foreign policy instead of going to brunch because he’s a pig.”

But the paper’s latest long-form piece about Dalio and Bridgewater was especially scathing. Essentially, the paper accused Dalio of being a fraud who portrays himself as a champion of deliberate and hyperrational thought and debate, but is privately vindictive and intolerant of dissent and perceived disloyalty. And they didn’t even get into Dalio’s latest embarrassing virus-inspired flip-flop.

The billionaire hedge fund took to LinkedIn over the weekend to publish a screed lashing out at WSJ’s “fake and distorted” news.

Then on Monday morning, he followed that up with a series of tweets thanking his ‘supporters’ and asserting that he will be “fine”, in case anybody was worried about how he was handling this latest media dragging.

Thank you all for your overwhelming support and your understanding of my particular experience as a result of The Wall Street Journal’s lack of quality control. However, don’t worry about me as I will be fine. (1/4)

But just in case you were worried about Dalio, (for example, if you depend on his reputation for a paycheck), he’s arrived to insist that you shouldn’t worry about him. No, dear reader: what you should be worried about is the corrosive effect that all of this fake and distorted coverage has on society. Dalio’s case is but one example among thousands that transpire every day.

Worry about the state of media, the lack of controls on its quality, and what the resulting false or distorted news means for our society. My case is just one of thousands that transpire in the way I described. (2/4)

The main reason I wanted to draw your attention to it is because I’m in a position to describe this very typical case knowledgeably. I constantly hear of other similar cases that those involved are unwilling to publicly describe because… (3/4)

…they are afraid of the consequences and hope it will blow over. I hope more people will speak up so the problem will be more recognized. If it was more recognized, we might see the pendulum swing against bad journalism and back to more quality journalism. (4/4)

We wonder: Has Dalio spoken to the president lately? When was the last time he really ‘took the temperature of the room’ in Westport?

As much as I’m enjoying watching this ludicrous @raydalio vs @wsj feud from afar, I feel compelled to mention that people inside Bridgewater have been whispering about most of what was in that story for months but only on radically non-transparent background.

Either way, we’d like to welcome Ray to the party. We couldn’t have put it better ourselves. Though for somebody who’s worried about distorted media narratives, Dalio sure spends a lot of time on CNBC.

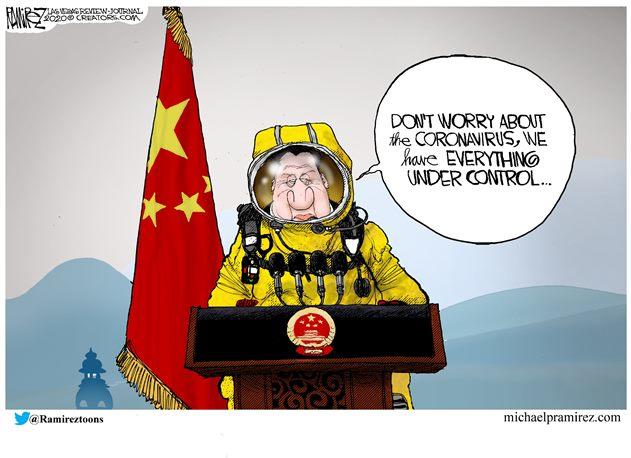

Rabobank: “Coronavirus Is The Kind Of Risk That Doesn’t Just Put You Out Of Your Portfolio, But Out Of The Game”

Submitted by Rabobank’s Michael Green

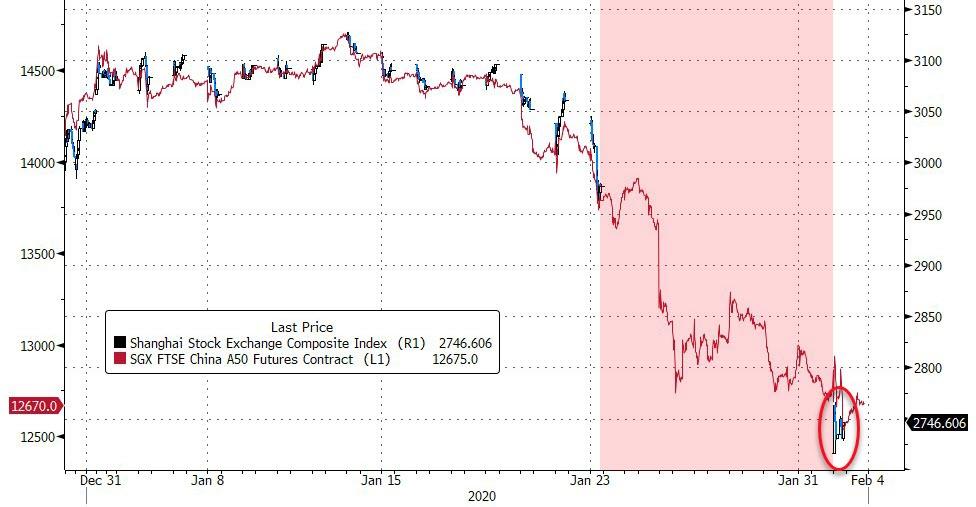

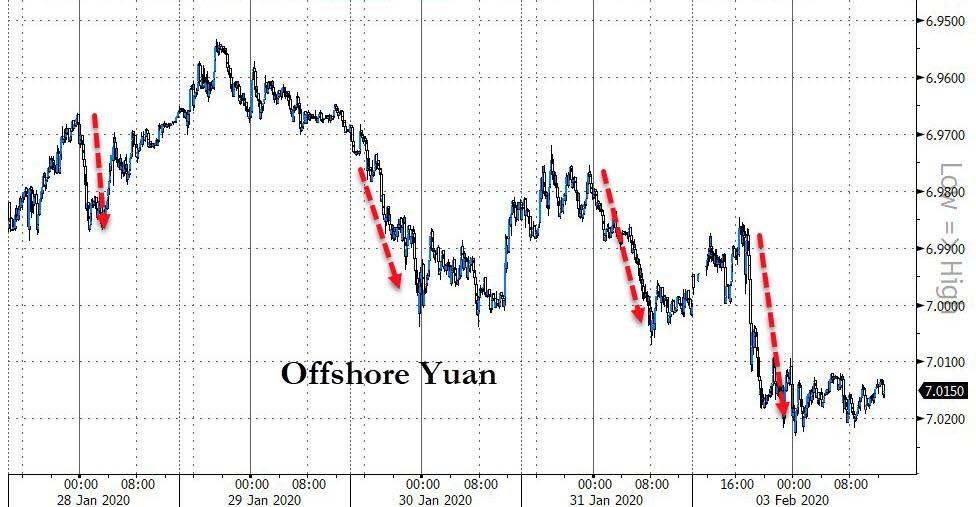

China returned from a longer-than-usual lunar New Year holiday today. Not the swathe of businesses that have been forced to close temporarily; and not the now tens of millions under quarantine at home; and not the villages that have barricaded themselves in from the outside world; just the financial markets. And, despite the promise from the PBOC of CNY150bn (USD21.7bn) in extra liquidity, lower rates, and whatever it takes to get through this ahead of market open, the initial response was a complete collapse: at one point the Shanghai stock exchange was -8.7% on the day – and recall that under the terms of the Phase One US-China trade deal, US financial firms are supposed to be diving in to this kind of market aggressively; the Chinese currency, both off and onshore, has crashed through the psychological 7 level once again; and trading in Chinese commodity markets has been suspended after iron ore, copper, crude oil, palm oil, and eggs all closed limit down on the day.

Of course, there is going to be a spill-over into other markets. You wanted to know what a real decoupling from China might look like, and/or what a “What if everyone just stayed at home and didn’t buy anything?” economic thought-experiment looks like? Well here you are, folks.

In terms of trade, Australia and New Zealand are at the front of the queue, as well as time zone-wise. Add plunging iron ore to a cessation in Chinese tourist arrivals, and to the news that high-value agri imports like lobsters are allegedly not allowed into China anymore, and you have all the ingredients for AUD to give up the 67c level and NZD to give up 65c. Yet other global commodity exporters are likely to feel the pain. For just one example, China’s oil consumption is now down 20% according to sources quoted on Bloomberg. That is the equivalent of an economic depression, not a recession, landing overnight. Expect prices, and global inflation expectations, to follow suite. Indeed, there is already talk of an emergency OPEC meeting. Yet even ordinary exporters (and more so net exporters) of goods and services are going to get hit. In fact, you’d need to be a continent-sized, inward-focused, commodity importer to be able to ride this out comfortably. Perhaps the US and India fit that bill to some degree, but less than one might think, perhaps.

Naturally, this kind of market sell-off imparts a natural tendency on the part of our not-so-natural markets for aggressive dip-buying. However, as opposed to the headline of “World War Three!” which triggered a bout of risk-off action at the start of the year, this sell-off appears far more justified. The same op-ed writers who did not understand the real-politick of the Soleimani assassination and were wrongly screaming “Sell!” after that event are today trying the argument that “More people die from slipping in the shower, etc., than this Coronavirus.”

This overlooks the fact that this virus has the potential to go exponential and become a global pandemic. It’s a small risk, yes – but it’s a FAAAAAAAT tail risk, that tens of millions of people simultaneously slipping in the shower really isn’t. Indeed, it’s the kind of huge risk that doesn’t just put you out of your portfolio position, or out of business, but out of the game, full-stop. Markets are quite right to react in a strongly negative, preventative fashion to this risk until we see evidence that it is being brought under control and the threat has truly passed. And we are not there yet, very regrettably. When we are, we see the real bounce. In short, “panic measures” are not always a sign of panic – they can be rational.

The global establishment of the WHO are, by contrast, remarkably cavalier in their market-friendly approach that there should be no restrictions on free movement or free trade as a safety-first measure, and we should all aim to find a vaccine. All very IMF. It’s not a surprise, perhaps, that once again nation-states are thumbing their noses at that particular economic policy prescription from a famous acronym and imposing travel bans and, in China’s case, import bans too (if the no seafood report is true).

On which note, today is the first trading day of the bold new world of BoJo Brexit. Headlines in that regard are that the UK is going to play hardball and is aiming to keep all its own fish, and for an EU trade deal somewhere between those of Canada and Australia rather than the far closer relationship that had been initially promised. Indeed, BoJo is talking about preparations for full customs/border checks in 2021 once the transition period ends. That also suggests a healthy dose of risk-off is required. However, for whom? Some of the impacts of this kind of scenario could arguably prove more positive than the Brexit naysayers have long warned. Nissan, which runs a huge car plant in Sunderland that has long been flagged as at risk under hard Brexit, is today claimed to have a contingency plan to pull out of European production and double down on the UK market instead, where it would then have a competitive edge vs. tariffed European imports. So less EU exports, more UK local production, and more UK jobs – in that one industry.

Conservative radio icon Rush Limbaugh announced on his Monday show that he has been diagnosed with advanced lung cancer.

Rush Limbaugh just announced on his radio program he has been diagnosed with advanced lung cancer. Says there will be days he won’t be able to be there due to treatment…

All of a sudden, events are looking a bit fluxy out there, as though the world is shuddering through some spooky ch-ch-ch-changes, like a monster waiting to be born, with strange convergences of ecology, politics and economy, and there’s only so much you can do to prepare, really. Criticality is in the air!

The horses are out of the barn on the Wuhan Coronavirus. Air travel was curtailed too late in the game — and still only partially — with asymptomatic-but-infectious human carriers winging to every corner of the world and probably contaminating airports all along the way. There’s plenty of thought and counter-thought on what exactly is going on behind the scenes in China. The ruling party has knocked itself out demonstrating its earnestness in the crisis, performing great feats like the construction of a one-thousand-bed hospital in ten days, shutting down the lunar new year festivities (like cancelling Christmas here), and locking down a hundred million citizens in quarantine. Pretty impressive.

But there’s also a theory that the Coronavirus affords a cover for cascading failures in China’s corrupt and shifty banking system. The country had already stepped across some frontiers in demographics, energy consumption, and industrial growth that were shoving it toward contraction for the first time in two generations. Coronavirus has shut down a lot of production in big things like cars and big-little things like cell phones, and supply lines are shutting down to world markets. This amounts to the first big test of the integrated global economy, as well as the world’s debt-saturated business model.

When a lot of parties and counterparties can’t pay each other because their revenue flows are cut off, the securities, currencies, equities, and other abstract representations of wealth go south. The US and Europe are no better positioned for a crisis in their banking arrangements, and confidence is starting to crack. Both economic mega-regions have relied on central banking hocus-pocus to prop up stock markets and maintain the illusion that the logic of bonds still applies. The first thing to go moneywise in a contracting financial system is the magic of compound interest.

The US Federal Reserve has been massively gaming the Repo markets — overnight lending that uses bonds as collateral — since September, raising suspicions that more than one of its “primary dealer” banks are insolvent. Juicing them with “liquidity” is like painting over sheetrock infested with black mold. Looks good for a week or so, and then you’re in intensive care. Nobody knows yet what the effect of Britain’s escape from the EU will do to the Union’s remainers, but Europe’s bonded debt arrangements are even dodgier than America’s, since there is absolutely no EU central control of each member’s fiscal affairs. Anyway, the meta-trend now is the devolution of governance from giant-and-central to smaller-and-local, so the real question is how much disorder and damage do these nations endure as that happens. It’s been manifesting vividly in France for a year in the yellow vest protests.

Here in the USA, the knock-on effects of converging crises begin to look like a game of four-dimensional eight-ball. The oil markets are getting slammed around the $51 hashmark, making it more difficult for the shale oil producers to meet their onerous debt repayments (in an industry that just doesn’t make a profit). Lower gasoline prices may seem like a boon for US motorists, but it comes at the expense of bankrupting more oil companies and punishing lenders like pension funds that invested in shale securities in the desperate search for “yield.” Shale never was a rational business model despite its fabulous production surge in a very short span of years. Don’t be surprised if there’s an attempt to nationalize it, which will induce new problems of capital allocation and sheer incompetence in a world where central planning of anything is more and more a bad bet.

Looming and converging multiple crises are also behind the gross disorder in US politics, though the connections may not be so discernably visible. President Trump foolishly took credit for financial markets that he had correctly described as being “one big, fat, ugly bubble,” back in the febrile days of the last election. Now it threatens to leave him holding a big fat ugly bag of trouble. That booby trap is surely more hazardous to his reelection chances than the frenetic efforts of pissants like Adam Schiff running Wile E. Coyote ambuscades in the DC Swamp. Mr. Trump spent three years working, jawboning, and bluffing over global trade arrangements that are now suddenly falling apart. How much of that will turn out to be a temporary effect of the Coronavirus, nobody knows. Or maybe it’s an inflection point in the workings of our over-hyper-complexified human ecosystem.

These shifting quandaries leave the Democratic Party between that ol’ rock and a hard place. All of their bad faith ploys against Mr. Trump have failed so far. I speak to supposedly educated people every day upon whom the failure of the Mueller Investigation, the fiasco of impeachment, and the revelations of IG Michael Horowitz have made no impression at all. The Golden Golem of Greatness is still Putin’s Puppet to them. It’s a wonder of the age that they can’t cut their losses. And now Bernie Sanders suddenly looks poised to win the Iowa caucus and inflame the not-quite-so-socialist factions of the party, who appear to be ratcheting up some Wile E. Coyote traps against him.

If that works, it’ll blow the party apart, 1860 style, into rump factions. But if Bernie somehow perseveres and gets the nomination… and the Potemkin financial markets tank… and Coronavirus turns out to be a very big deal for upsetting global trade… then, America may get its first zealous socialist president.

Yes, history repeats and rhymes and all that, but I don’t see Bernie replicating the triumphs of Franklin D. Roosevelt in Great Depression 2.0. Rather, by attempting to overlay command-and-control policies on a zeitgeist that wants to take us smaller and local, Bernie Sanders will only be bucking reality.

The net effect of Bernie Sanders in the White House will be to finish off the economy… and imagine where that will take us.

Two people were killed and another wounded in a shooting at a Texas A&M University dorm hall on Monday at its campus in Commerce, Texas, according to campus police and media reports.

A twitter account believed to be associated with the university confirmed the two deaths.

There have been 2 confirmed deaths. The third victim has been taken to the hospital for treatment. UPD has stationed officers throughout campus, including all key gathering points, for the safety of the campus community.

We will continue to share updates as they are available.

The university police said all classes were canceled for the rest of the day amid an active criminal investigation. Texas A&M’s campus in Commerce, Texas, is over 200 miles north of Texas A&M’s main campus in College Station.

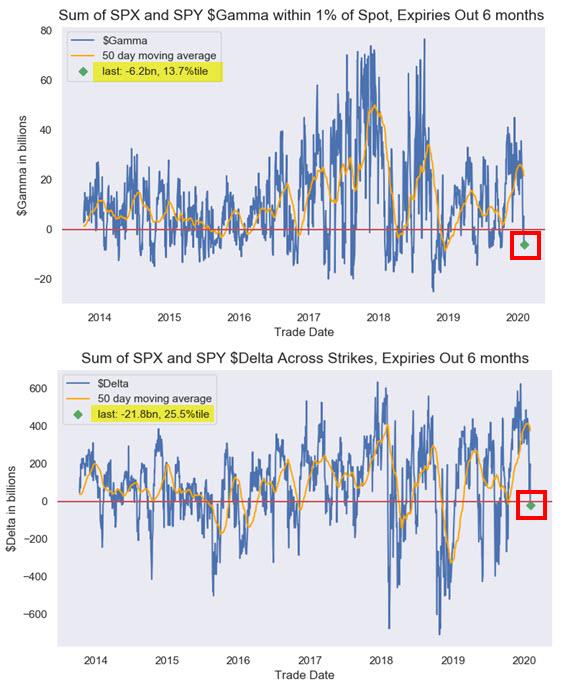

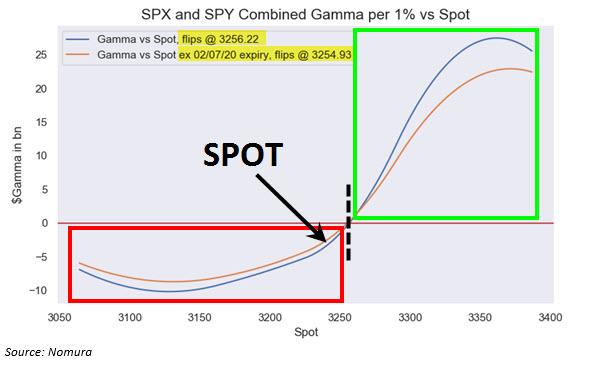

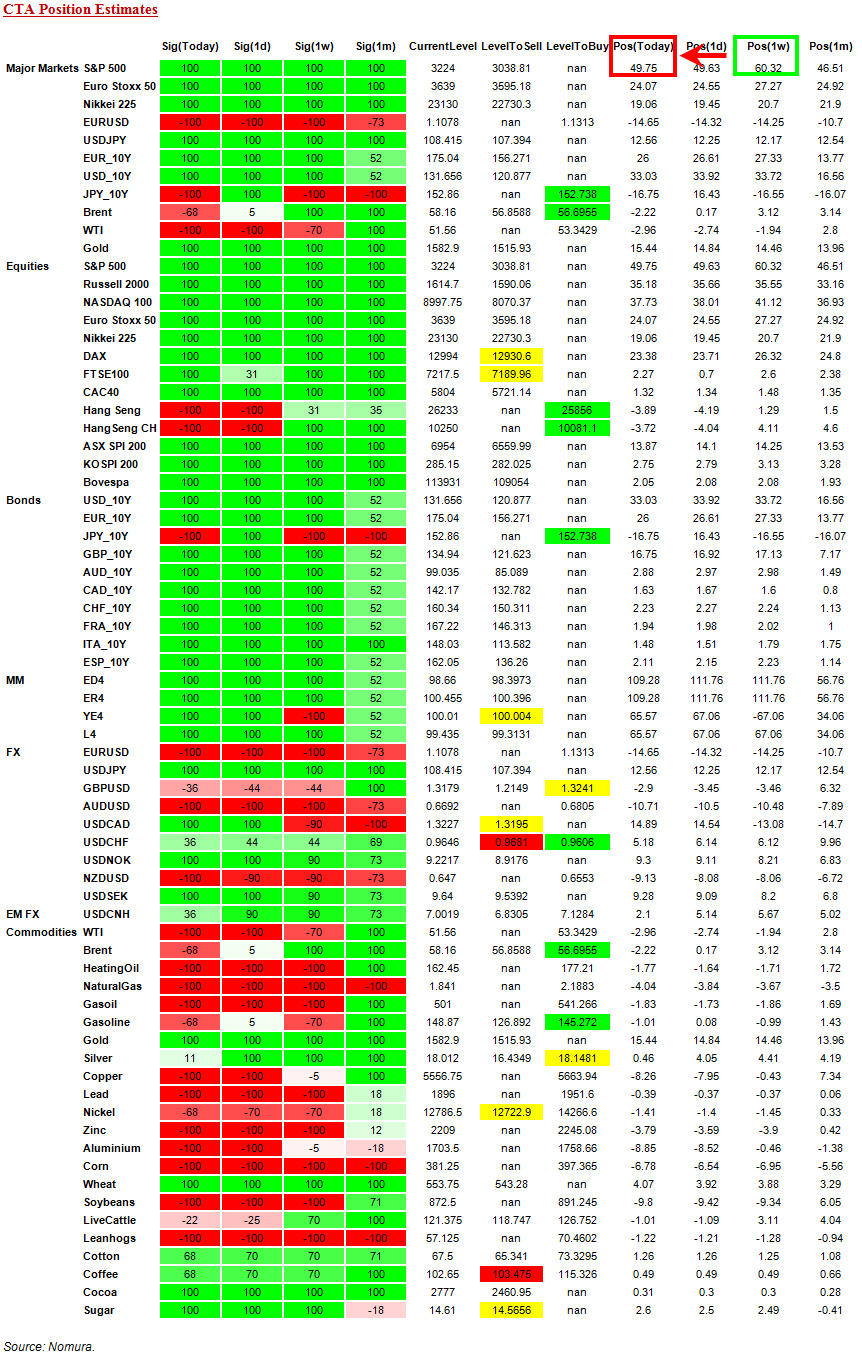

Why 3,254 Is The Only Number That Matters For Traders Today

When commenting on the crash in Chinese stocks late on Sunday night, we pointed out that US equity futures had managed to buck the liquidation trend seen across Asia, rebounding from Friday’s rout lows, rising into the mid-3200s, a level which was critical because as we had pointed out previously on Friday, this is roughly where the critical gamma “flip” level was, below which gamma transforms from a risk dampener into a risk accelerator.

On Monday morning, Nomura’s cross-asset strategist and quant, Charlie McElligott, picked up on this key point again, one which he has been covering for years, and writing that indeed, should stocks fail to rebound from their Friday open, it could get messy as consolidated option positioning shows both dealer gamma and delta is now negative…

… with dealer now back in a short gamma position for the first time since the start of the October meltup. In fact, it now appears that the gamma “flip” level is 3,254, which explains why market makers who hope to preserve the bullish benefits of positive gamma are fighting so hard to keep the S&P at this level. Not surprisingly, at last check, the S&P was trading right on top of this level.

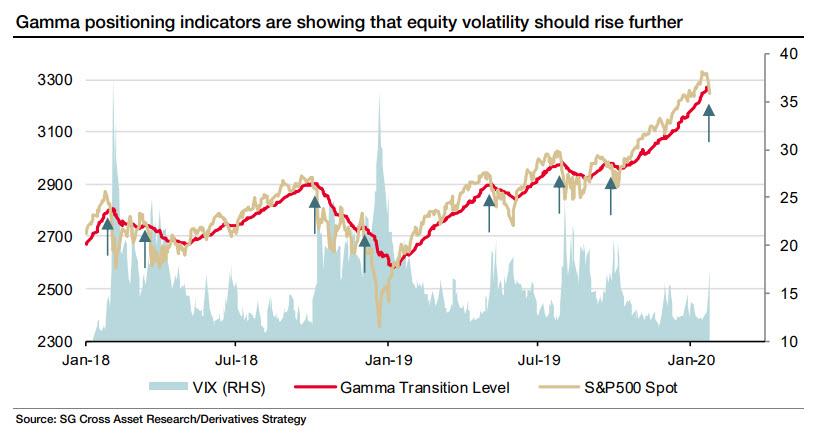

For those confused, here is a quick refresher: gamma-linked indicators are designed to estimate whether hedging by market makers is currently suppressing or elevating volatility. Positive gamma leads to dampening of index moves because the hedgers need to sell when the market moves up and vice versa. Negative gamma leads to hedgers exacerbating volatility as they sell when the market moves down and buy when it goes up. The chart below from SocGen shows that the S&P500 spot moving into negative gamma territory (below the red line) is consistent with higher levels of VIX, which in turn leads to further selling in the S&P, a greater disconnect from gamma, and even higher volatility, and so on, in a feedback loop.

Like Nomura’s McElligott, SocGen’s derivatives strategy team estimated last week that aggregate dealer gamma had briefly moved into negative territory on the S&P500, and remains close to it, a byproduct of the notorious “gamma gravity” effect whereby gamma flip levels tend to serve as “strange attractors” for the broader market, something we have discussed since 2018.

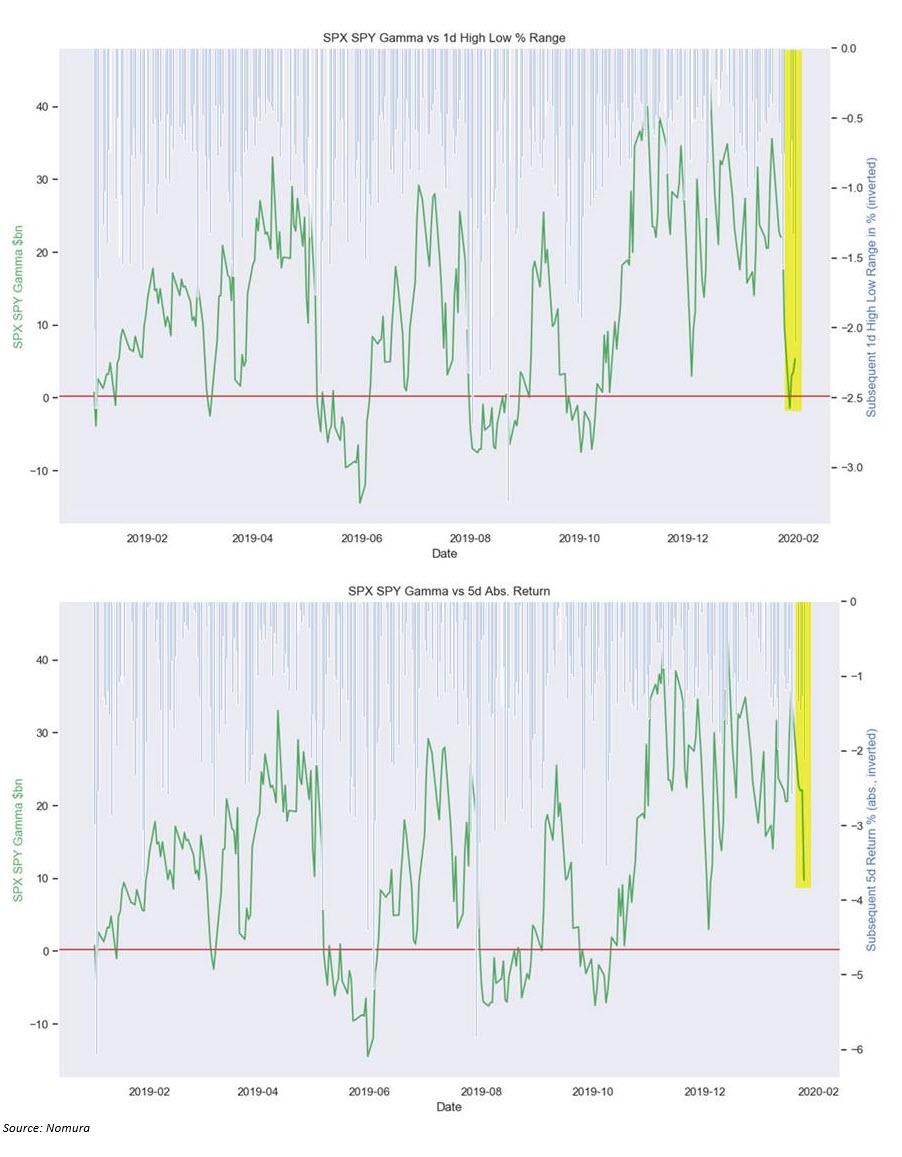

McElligott underscores this point, and notes that once again, the change in the gamma “impulse” took place concurrent with a large move in the S&P.

Alternatively, as a function of market reflexivity, one could claim that it is the drop in gamma that leads to higher vol, and lower prices. Direction of causality notwithstanding, the bottom line is simple: 3,254 is the one level that every trader should be focusing on to determine what the market will do in the very short term, and should SPX spot fail to rise above the gamma flip level, there is great potential for a period of higher turbulence in the short term.

There is another reason why traders should be closely watching the battle over 3,250, and it has to do with an entirely different set of investors: CTAs.

According to Charlie, the Nomura QIS CTA model shows that despite the overall signal for the SPX position remaining “+100% Long” as of this morning (as all three time horizons with any “weighting”—3m, 6m and 12m—are all still “buy” signals), the short-term 2w window has flipped “Short” due to the recent impulse move lower/the jump higher in trailing realized vol — which means that the “gross” exposure in the SPX futures position has been deleveraged from the two year “high” of 60.3% made last week, now reduced to this morning’s 49.8% position

And while the 2-week signal in the CTA model is already a “Sell,” if today the S&P closes flat, or worse, red, McElligott would “expect to see the 1-month signal turn “Sell” tomorrow as well.” Still, the only signals that matter for now are the 3m, 6m and 12m models — thus the position maintains the overall “+100% Long” status.

But that too will change if SPX spot closes below gamma, as dealers now are “incentivized” to chase the market lower, resulting in lower prices, higher VIX, an even greater delta between spot and gamma, even more selling, etc. in a feedback loop; and with VIX spiking it would eventually push all CTAs signals more bearish, until eventually all those green “100% longs” start shrinking until eventually they all go flat, and then turn negative, as CTAs officially join the selling frenzy.

Bottom line: keep an eye on where S&P closes the day: 3,254 is all that matters.

{kind=link}