China Seeking “Flexibility” On Phase 1 Trade Pledges As Its Economy Grinds To A Halt

Last night, when we reported the plunge in the yuan below 7.00 vs the dollar – traditionally a level that has been seen as triggering the US Treasury into screaming fx manipulation – we noted that it is only a matter of time before the US and China sat down to discuss just how viable the terms of the Phase 1 remain, especially with China’s economy now expected to slow below a 5% GDP if only in the short term, as the country reels from the fallout of the Coronavirus epidemic which has led to tens of millions of Chinese citizens living under mandatory or self-imposed quarantine.

We didn’t have long to wait, because moments ago, Bloomberg reported that Chinese officials “are hoping the U.S. will agree to some flexibility on pledges in their phase-one trade deal” as Beijing tries to contain the fallout from the health crisis that has infected over 17,500 and killed over 360.

The Phase 1 trade deal which was signed on Jan. 15 – just one day before China finally started reporting virus data – and is supposed to take effect in mid-February, has a clause that states the U.S. and China will consult “in the event that a natural disaster or other unforeseeable event” delays either from complying with the agreement. It’s unclear whether China has formally requested such a consultation yet, but according to Bloomberg sources the plan “is to ask for it at some point.”

As the report goes on to note, Chinese officials are evaluating whether the target for economic growth this year should be softened as part of a broader review of how the government’s plans will be affected by the deadly virus outbreak. However, so far it does not appear that the US is rushing to concede to Chinese demands, especially since Larry Kudlow last week said that the U.S. hasn’t seen any major effects on its economy from the epidemic.

“This is principally a public health problem and the pandemic of course is in China, not the U.S.,” Kudlow said Thursday in an interview on Fox Business Network. “Insofar as the economy, we see no material impact.”

Curiously, the Bloomberg report comes about an hour after the WSJ reported that the Trump administration has been granting fewer exemptions to tariffs on Chinese imports, with the approval rate recently plunging to 3% in the third round of levies from 35% in the first two. More from the source below:

Requests for exemptions have been made by more than 4,500 companies, which typically say they have no viable or cost-effective alternatives to Chinese products. Many companies seek more than one exemption. For just the fourth round alone, more than 8,700 requests for exemptions were made by Friday, the filing deadline.

HealthWay Family of Brands filed for 11 exemptions on electronic and other parts it imports from China to build air cleaners in Pulaski, N.Y. When the U.S. Trade Representative denied all its requests, the company was forced to lay off eight of its 48 workers and sideline plans to expand, said Vinny Lobdell Jr., the company’s global president.

“We were set to build a $2 million expansion,” said Mr. Lobdell. “We had looked at bringing 30 to 40 more jobs to the area as the Intellipure product line was growing.”

With the Trump admin playing hardball with US demands for easier tariffs, it is hard to see just why he would concede, even if China were to wrap its request as a “force majeure.”

Meanwhile, the market’s verdict on the US-China trade deal remains one of pervasive skepticism, with soybean prices – one of the main commodities Beijing agreed to purchase – reflecting rising concern about weaker demand from China. Soybeans traded in Chicago were little changed after nine straight days of declines, the longest losing streak since July 2014.

And in more bad news for Beijing, if it is indeed hoping for mercy from Trump, when asked if the virus will give the U.S. more leverage in the second phase of trade discussions with the Asian nation, Kudlow said the outbreak is “completely separate from trade, jobs and all the rest.”

“This is an issue of helping them if we can, offering our assistance, engaging with them, this is a humanitarian effort on our part — nothing to do with economic rivalries,” he said.

Ironically, so far China has refused every US proposal to help with the coronavirus epidemic: one wonders why – is it to prevent US observers from seeing just how China “handles” the flood of deaths resulting from the disease, which according to numerous sources, is far, far greater than the official number, and that Chinese officials are merely rushing to burn the bodies to avoid having to specify the true cause of death, in order to keep mortality rate calculations low and prevent an even greater panic within Chinese society.

Democrats Gather For Iowa Caucus, Here’s What To Expect

The Iowa caucuses begin tonight at 8 p.m. ET, marking the first nominating contest of the 2020 election cycle. Democrats across the states will head to their local precinct caucus locations to vote for their desired candidate to take on Donald Trump in the November election.

Via the New York Times

There are 1,678 neighborhood locations and 87 “satellite caucuses” around the world, where delegates will be chosen for the Iowa state party convention who will be sent on to the Democratic National Convention in Milwaukee July 13-16 to represent their candidates.

How it works

During each caucus meeting, attendees physically group themselves by candidate, in what’s known as the “first alignment.” Any candidate who fails to garner at least 15% of the vote is declared non-viable, and their supporters can either join other groups or try to appeal to others to join them. Then, a second vote known as the “final alignment” is held to determine how delegates are awarded.

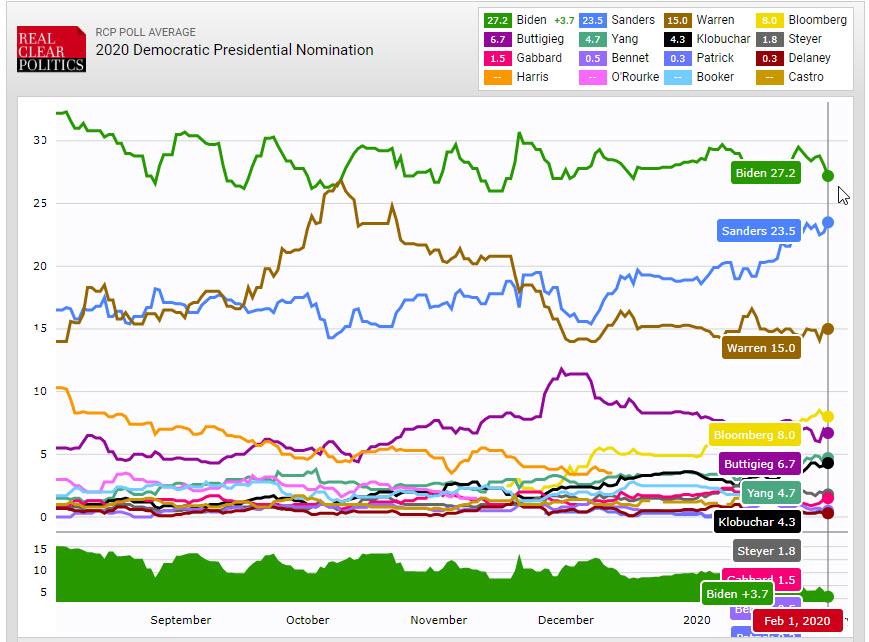

On Sunday, Democratic presidential candidates competed with the Super Bowl in a last-minute bid to appeal to Iowans. And while a Saturday night pre-caucus poll which has historically shed light on where the candidates stand was canceled due to a ‘survey error,’ Sen. Bernie Sanders (I-VT) is largely seen as the frontrunner going into Mondays contest, after an Emerson College poll on Sunday showed him with 28% support followed by Joe Biden at 21%, Pete Buttigieg at 15%, and Elizabeth Warren at 14%. That said, 34% of those polled said they could change their vote.

Notably, President Trump lost the Iowa caucus in 2016.

Public polling has shown Mr. Sanders gaining ground, and he has outspent all of the other leading Democrats on television by a wide margin in recent weeks. A New York Times polling average found Mr. Sanders and former Vice President Joseph R. Biden Jr. tied for first place in the state, with each of them collecting support from about 22 percent of likely caucusgoers. Trailing them in third and fourth place were former Mayor Pete Buttigieg of South Bend, Ind., and Senator Elizabeth Warren of Massachusetts. –New York Times

And if Sanders takes Iowa, he will have a good shot at carrying that momentum into New Hampshire’s primary next week – where he is already considered to have the top spot – and then on to Nevada on February 22.

Via Politico (Photo: M. Scott Mahaskey)

That said, as the Times notes, “there is still widespread concern among Democratic Party leaders and center-left primary voters about the implications of nominating a self-described democratic socialist to take on President Trump.”

His chief opponents are unlikely to give way easily: Even if he is defeated here, Mr. Biden has a strong national following among moderate voters and African-Americans, while Ms. Warren retains a sizable base among educated liberals and women. And Michael R. Bloomberg, the former mayor of New York City, is looming as a competitor in the March primary states. –New York Times

Meanwhile, 2020 candidate Mike Bloomberg – who just got into a fight with President Trump over his height, is skipping Iowa and will instead engage in a massive advertising campaign in later-voting states.

According to the betting lines, Bloomberg is gaining ground as Biden collapses, but it’s Bernie that is becoming the strong favorite to get the Dem nod…

Just like with China’s “surprising” PMI beat, it is hard to know if the respondents for this morning’s US manufacturing surveys were interviewed before or since the coronavirus pandemic has collapsed global supply chains.

Markit’s Manufacturing PMI beat expectations, printing 51.9 vs 51.7 exp, but fell to 3-month lows.

ISM’s Manufacturing survey smashed expectations, surging back into expansion at 50.9 – highest in 6 months.

So you decide which you believe…

Source: Bloomberg

Under the hood, PMI was broadly positive…

Production rose to 54.3 vs 44.8; highest index since April

New orders rose to 52 vs 47.6; best measure since May

Employment rose to 46.6 vs 45.2

Supplier deliveries fell to 52.9 vs 54.6

Inventories fell to 48.8 vs 49.2

Customer inventories rose to 43.8 vs 41.1

Prices paid rose to 53.3 vs 51.7

Backlog of orders rose to 45.7 vs 43.3

New export orders rose to 53.3 vs 47.3

Imports rose to 51.3 vs 48.8

For context this is the biggest MoM jump in ISM since July 2013 – does that make any sense to you?

But, PMI was not, as Chris Williamson, Chief Business Economist at IHS Markit said:

“US manufacturing limped into 2020, with falling exports dampening output growth and causing a pull-back in hiring. The survey data are consistent with factory production falling moderately, meaning the manufacturing sector looks set to act as a drag on the overall economy once again in the first quarter.

“Weakness looks broad-based. Rising demand from households has helped support production in recent months, but January saw a marked slowing in new orders for consumer goods. Production of capital goods such as business equipment, plant and machinery meanwhile fell for the first time in almost four years, hinting at weakened business investment.

“More encouragingly, business expectations for the year ahead perked up, coinciding with an easing of trade tensions and the signing of new North American and Chinese trade deals. Companies are therefore expecting the soft patch to be short-lived, though fears surrounding the Wuhan coronavirus and any further potential escalation of trade tensions could erode this optimism.”

So it seems like a global pandemic is great for US manufacturing!!!! We suspect ISM will see one of its biggest drops in Feb after the hopes of the trade deal crash on the shores of coronavirus.

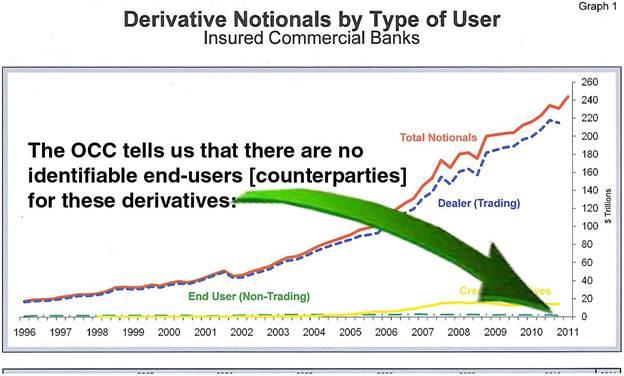

It is impossible to predict what lays ahead! The coronavirus outbreak could be a nothing burger or become a watershed event. A mountain of debt has formed over the years and whether countries and central banks can hurl enough resources at this crisis to calm a growing fear remains to be seen. It is fear versus more promises of stimulus and at some point, all bets are off. To highlight the vulnerability of the financial markets we can always turn the spotlight back upon derivatives. Hundreds of billions of dollars do not matter when we are talking about death or something like the derivative markets.

Currently, China is looking to dump a wagon full of stimulus into an already highly leveraged market to offset the toll taken from virus fear. China said that billions of dollars will start flowing into markets at the opening and the Chinese government has ordered that short-selling of shares be halted. This instability makes it important to revisit issues that have been swept under the rug or simply overlooked. For most people, the derivatives market falls into this category, partly because they don’t understand exactly what derivatives are or why this market is so important. Everyone paying attention knows that the size of the derivatives market dwarfs the global economy. Several books on derivatives have been written and the size of the derivatives market could be larger than $1.2 quadrillion. To put this in perspective it is about 20 times the size of the world economy.

Attempting to regulate and control our complex global markets is easier said than done.This can be seen in derivatives which are usually lengthy complex legally binding agreements that are very difficult to dissect and often reek with potential contagion. Derivatives fall into many categories from futures, options, credit default swaps, and any complex combinations of these. They can also be used to wager, bet, and spectate on a market move or direction. Regulation is difficult and spotty at best in that a derivative transaction in one country might be considered a simple spot trade in another. I have become convinced after studying derivatives that QE following the 2008 financial crisis may have been geared to hold up the underlying value of assets thatfeed into and support the massive derivative market rather than help the economy.

Derivatives Could Explode Like A Bomb!

Way back in the middle of 2014, the Bank for International Settlements revealed that the amount of over-the-counter (OTC) derivatives outstanding was around 710 trillion dollars at the end of 2013. Most of that exposure is held by banks. The US Office of the Comptroller of the Currency at the time reported the exposure of US banks to derivatives totaling 237 trillion dollars. Of that, four big banks, JP Morgan Chase, Citibank, Goldman Sachs and Bank of America accounted for over 219 trillion dollars. The staggering size of this market is beyond anything that can be comprehended.

When I tried to get more recent numbers I ran into fairly stiff resistance which I contribute to the fact nobody knows the true exposure that is difficult to assess. Hopefully, much of the derivative exposure somehow nets out so that real exposure is far less than the hundreds of trillions of dollars on the books. This is only part of a much larger market that includes hundreds of trillions of dollars in non-reported agreements and private contracts. The efforts to achieve more reporting, more platform trading and central clearing of derivatives have fallen behind because of the complexity of crafting mutually consistent regulations at the jurisdiction level, for a highly globalized market.

While This Is Not A Current Chart Note The Trend Line!

Many derivative writers should be called “too clever by half” if they think they have successfully controlled the risk or removed the implications and problems massive defaults would cause. They pump these out because they make money in the process of structuring and selling these agreements. A derivative is in many cases an insurance policy covered by collateral. Sadly, those who buy and write derivatives often play fast and loose with the value of the collateral or flat out lie about it. This moves them from an insurance policy and into the area of high risk.

Those of us skeptical of the market wonder whether the coronavirus will be dismissed as another over-hyped hysteria or devastate economies. The potential that things could get ugly does exist. If at some point, a “mob mentality” takes over logic could get tossed out the window. This is when claims their actions are for the “greater good” becomes irrelevant. Temporarily, we are on hold while events unfold around us. The window has gone dark and our vision is limited. Just remember those in government generally take care of themselves first, in their minds they are the priority.

While the world will be focusing on every development out of China which is struggling to contain the fallout from the coronavirus pandemic which has now infected nearly 17,500 people across the globe, in terms of newsflow DB’s Jim Reid writes that this week the highlight could be today’s first US democratic primary in Iowa – the first of four this month. There’ll also be a number of data releases, including PMIs from around the world (today and Wednesday), before the US jobs report comes out on Friday, now without a lockup and forcing traders and analysts to scramble to decipher what the BLS has reproted. Earnings season will also continue to be in full flow.

While Iowa only makes up about 1% of nationwide delegates, we will start to see some sign as to momentum of the various candidates. Technically there will also be Republican primaries, but these are widely considered a foregone conclusion in favor of President Trump. In terms of what to expect, the national polling average from RealClearPolitics shows former Vice President Joe Biden still in the lead at the moment, with 27.2%, followed by Senator Bernie Sanders on 23.5% and Senator Elizabeth Warren on 15.0%.

However, in Iowa, the polling average shows Sanders in the lead, with 24.7%, and Biden in second on 21.0%. Furthermore, both former Mayor Pete Buttigieg (16.3%) and Warren (15.2%) are around the crucial 15% mark that is important when it comes to accumulating the delegates required to win the nomination.

In terms of what will happen, the race remains competitive, with FiveThirtyEight’s model at time of writing giving Sanders a 40% chance of winning the most votes in Iowa, followed by Biden on 34%, with Buttigieg on 18% and Warren on a 16% chance. It’s true that often the winner of the Iowa caucuses don’t actually go on to be the nominee – indeed on the Republican side the winners in 2008, 2012 and 2016 all lost out to someone else. Nevertheless, it’s the first indicator of real votes we have, and very important in terms of momentum for each of the candidates, as it’s only 8 days later that the next primary takes place in New Hampshire, and between the two votes there’ll be another TV debate between the candidates on the Friday.

The week ahead also has a number of data highlights, with the main ones likely to be the release of manufacturing (today), services and composite (Wednesday) PMIs from around the world. We have already had the preliminary PMIs from a number of countries, so those countries such as Italy where we haven’t had the preliminary numbers will take on added interest. Also of note will be the ISM manufacturing and nonmanufacturing indices from the US, out today and Wednesday respectively. Back in December, the ISM manufacturing reading fell to 47.2, its lowest level since June 2009, though the consensus is expecting an uptick for January to 48.4, so that’s one to keep an eye out for.

On Friday, we’ll also get the US jobs report for January, the first one that will be subject to the new lockup rules meaning it is unclear if wire services will have any prepared data at the time the report comes out. The current consensus expectation is for a +160k increase in nonfarm payrolls in January, up from the +145k increase in December, with the unemployment rate remaining at 3.5%, and average hourly earnings growth ticking up a tenth to +3.0% year-on-year. Other key data out this week will come with the Euro Area’s retail sales for December on Wednesday, while in Germany, there’ll be the release of December’s factory orders on Thursday and industrial production on Friday.

Also earnings season continues this week, with another raft of companies reporting. Looking at things so far, of the 225 S&P 500 companies that have reported, 74.4% have reported a positive surprise on earnings and 64.1% have reported a positive surprise on sales. Looking to the week ahead, today sees Alphabet report. Then tomorrow we’ll hear from Walt Disney, BP and Sony. On Wednesday, there’s Merck, Novo Nordisk, GlaxoSmithKline, Siemens, Qualcomm, BNP Paribas and General Motors. Thursday sees reports from L’Oréal, Bristol-Myers Squibb, Philip Morris International, Total, Sanofi, Enel, Nordea Bank, UniCredit, Société Générale, Twitter and Toyota. And finally on Friday, we’ll hear from AbbVie.

Finally on US politics, tomorrow sees President Trump give his State of the Union address to Congress.

Below is a day by day summary of key events, courtesy of Deutsche Bank:

Monday

Data: January Manufacturing PMIs from Indonesia, South Korea, Japan, China, India, Russia, turkey, Italy, France, Germany, South Africa, Euro Area, UK, Brazil, Canada and US, China December industrial profits, Japan January vehicle sales, US December construction spending, January ISM manufacturing

Central Banks: Fed’s Bostic speaks

Earnings: Alphabet

Politics: Iowa caucuses held in the US

Tuesday

Data: UK January construction PMI, Euro Area December PPI, Italy preliminary January CPI, US December factory orders, final December durable goods orders, non-military capital goods orders excluding aircraft

Central Banks: Reserve Bank of Australia decision

Earnings: Walt Disney, BP, Sony

Politics: President Trump delivers State of the Union address to Congress

Wednesday

Data: January services and composite PMIs from Japan, China, India, Russia, Italy, France, Germany, Euro Area, UK, Brazil and US, Euro Area December retail sales, US weekly MBA mortgage applications, January ADP employment change, ISM non-manufacturing index, December trade balance, Canada December international merchandise trade

Central Banks: Brazil central bank decision, BoJ’s Wakatabe, ECB’s de Guindos, Bank of Canada’s Wilkins and Fed’s Brainard speak

Earnings: Merck, Novo Nordisk, GlaxoSmithKline, Siemens, Qualcomm, BNP Paribas, General Motors

Thursday

Data: Germany December factory orders, January construction PMI, US preliminary Q4 unit labour costs, nonfarm productivity, weekly initial jobless claims, Japan December labour cash earnings, household spending

Central Banks: Reserve Bank of India decision, ECB publishes Economic Bulletin, BoJ’s Masai, ECB’s Lagarde and Villeroy and Fed’s Kaplan speak

Earnings: L’Oréal, Bristol-Myers Squibb, Philip Morris International, Total, Sanofi, Enel, Nordea Bank, UniCredit, Société Générale, Twitter, Toyota

Friday

Data: China January trade balance, Japan preliminary December leading index, Germany December trade balance, industrial production, France December industrial production, manufacturing production, trade balance, Italy December retail sales, US January change in nonfarm payrolls, unemployment rate, labour force participation rate, average hourly earnings, final December wholesale inventories, December consumer credit, Canada January net change in employment, unemployment rate, participation rate

Central Banks: Russian monetary policy decision, Fed’s Quarles speaks (00:15 UK time), Fed releases semi-annual monetary policy report to Congress

Earnings: AbbVie

Politics: US Democratic primary TV debate

Finally, focusing on just the US, Goldman writes that the key economic data releases this week are the ISM manufacturing index on Monday, the ISM non-manufacturing index on Wednesday, and the employment report on Friday. There are a few speaking engagements from Fed officials this week.

Monday, February 3

10:00 AM ISM manufacturing index, January (GS 48.3, consensus 48.5, last 47.2): Our manufacturing survey tracker rose by 2.1pt to 52.5 in December, following firmer regional manufacturing surveys on net. However, we note that late-month surveys like the ISM could be affected by the outbreak of the coronavirus. Additionally, we do not expect improvement among firms exposed to the commercial aircraft supply chain, as Boeing halted production of the 737 MAX in the month. Taken together, we expect the ISM manufacturing index to rise 0.5pt to 48.3 (from its upward revised level of 47.8).

10:00 AM Construction spending, December (GS +0.7%, consensus +0.5%, last +0.6%): We estimate a 0.7% increase in construction spending in December, with scope for increases in both private and public construction spending.

02:00 PM Senior Loan Officer Opinion Survey (Q4) likely released

04:00 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will speak on big data and machine learning at a conference in California. Audience Q&A is expected.

5:00 PM Lightweight motor vehicle sales, January (GS 16.7m, consensus 16.8m, last 16.7m)

Tuesday, February 4

10:00 AM Factory Orders, December (GS +1.5%, consensus +1.2%, last -0.7%); Durable goods orders, December final (last +2.4%); Durable goods orders ex-transportation, December final (last -0.1%); Core capital goods orders, December final (last -0.9%); Core capital goods shipments, December final (last -0.4%): We estimate factory orders increased 1.5% in December following a 0.7% decline in November. Durable goods orders rose in the December advance report, driven by a large increase in defense orders.

Wednesday, February 5

08:15 AM ADP employment report, January (GS +175k, consensus +158k, last +202k): We expect a 175k gain in ADP payroll employment, reflecting the impact of lower jobless claims and other ADP model inputs. While we believe the ADP employment report holds limited value for forecasting the BLS nonfarm payrolls report, we find that large ADP surprises vs. consensus forecasts are directionally correlated with nonfarm payroll surprises.

08:30 AM Trade balance, December (GS -$48.1bn, consensus -$47.8bn, last -$43.1bn): We estimate the trade deficit increased by $5.0bn in December, reflecting a rebound in the goods trade deficit.

10:00 AM ISM non-manufacturing index, January (GS 54.9, consensus 55.1, last 54.9): Our non-manufacturing survey tracker edged down by 0.1pt to 54.1 in January, following mixed regional service sector surveys. We expect the ISM non-manufacturing index to remain unchanged at 54.9 in the January report.

04:10 PM Fed Governor Brainard (FOMC voter) speaks: Federal Reserve Governor Lael Brainard will speak on payment system innovation.

Thursday, February 6

8:30 AM Nonfarm productivity (qoq saar), Q4 preliminary (GS +1.6%, consensus +1.5%, last -0.2%); Unit labor costs, Q4 preliminary (GS +1.6%, consensus +1.2%, last +2.5%): We estimate non-farm productivity growth rebounded to +1.6% in Q4 qoq saar (+1.8% yoy), above the trend achieved during this expansion. This reflects steady business output growth in Q4 and only a modest increase in hours worked. We expect Q4 unit labor costs—compensation per hour divided by output per hour—to decelerate to +1.6% qoq ar (+2.5% yoy).

08:30 AM Initial jobless claims, week ended February 1 (GS 215k, consensus 215k, last 216k); Continuing jobless claims, week ended January 25 (consensus 1,710k, last 1,703k): We estimate jobless claims ticked down 1k to 215k in the week that ended February 1. We expect a persistent winter seasonal bias to continue to exert upward pressure on the continuing claims measure through February.

09:15 AM Dallas Fed President Kaplan (FOMC voter) speaks: Dallas Fed President Robert Kaplan will speak on the economic outlook at an event in Dallas.

07:15 PM Fed Vice Chair for Supervision Quarles (FOMC voter) speaks: Federal Reserve Vice Chair for Supervision Randal Quarles will give a speech on the economic and monetary policy outlook.

Friday, February 7

08:30 AM Nonfarm payroll employment, January (GS +190k, consensus +160k, last +145k); Private payroll employment, January (GS +185k, consensus +150k, last +139k); Average hourly earnings (mom), January (GS +0.2%, consensus +0.3%, last +0.2%); Average hourly earnings (yoy), January (GS +3.0%, consensus +3.1%, last +3.1%); Unemployment rate, January (GS 3.5%, consensus 3.5%, last 3.5%): We estimate nonfarm payrolls increased 190k in January. While employment surveys on net were little changed in the month, initial jobless claims declined further, and an unseasonably dry survey week in the Northeast and Ohio Valley is set to boost weather-sensitive categories. We also note that January job growth tends to accelerate in tight labor markets, as labor supply constraints may lead firms to implement fewer end-of-year layoffs. We do not expect a significant impact from Census employment in this week’s report. We estimate an unchanged unemployment rate at 3.5%, as we believe the increase in continuing claims over the last two months reflects technical distortions related to residual seasonality—and in any event, the uptrend tentatively retraced in the first three weeks of 2020. We estimate average hourly earnings increased 0.2% month-over-month and 3.0% year-over-year, reflecting neutral calendar effects and continued upward wage pressures.

11:00 AM Federal Reserve Board Releases Monetary Policy Report to Congress

Wuhan Begins Human Trials Of New Gilead Coronavirus Vaccine

Last week, scientists in Hong Kong warned that it might take up to a year for them to produce and test a vaccine to fight the deadly coronavirus that has now killed more people than SARS in mainland China. But on Monday, shares of drug company Gilead climbed following reports that it’s conducting a human trial for a drug to fight the outbreak, according to Bloomberg.

Gilead shares have already faded their gains…

…but we suspect that news about the trials is contributing to the forgiving market sentiment in the US, where shares look set to open higher following the bloodbath overnight in Chinese markets.

Here’s more from the Bloomberg report about the clinical trials, which will reportedly be carried out in Wuhan, the epicenter of the viral outbreak. As many as 270 infected patients will be recruited for the study.

Remdesivir, a new antiviral drug by Gilead Sciences Inc. aimed at infectious diseases such Ebola and SARS, will be tested by a medical team from Beijing-based China-Japan Friendship Hospital for efficacy in treating the deadly new strain of coronavirus, a hospital spokeswoman told Bloomberg News Monday.

Trial for the drug will be conducted in the central Chinese city of Wuhan — ground zero of the viral outbreak that has so far killed more than 360 people, sickened over 17,000 in China and spread to more than a dozen nations. As many as 270 patients with mild and moderate pneumonia caused by the virus will be recruited in a randomized, double-blinded and placebo-controlled study, Chinese news outlet The Paper reported on Sunday.

China has kick-started a clinical trial to speedily test a drug for the novel coronavirus infection as the nation rushes therapies for those afflicted and scours for vaccines to protect the rest.

The task of finding a workable vaccine has taken on added urgency now that the outbreak is set to cost the global economy up to 4x what SARS did during the 2002-2003 outbreak, which is why so many companies are racing to develop the vaccine. JNJ is also working on a coronavirus vaccine.

Drugmakers such as GlaxoSmithKline Plc. as well as Chinese authorities are racing to crash develop vaccines and therapies to combat the new virus that’s more contagious than SARS and could cost the global economy four times more than the $40 billion sapped by the 2003 SARS outbreak. The decision to hold human trials for remdesivir shows it’s among the most promising therapies against the virus that so far has no specific treatments or vaccines.

Gilead’s experimental drug hasn’t been approved by any regulators, but it’s being tested on the front lines of the outbreak in the absence of any approved remedies.

All of this begs the question: is ‘we found a workable vaccine’ the new ‘trade deal secured’? Will confirmation be enough to send US stocks to fresh record highs?

Saudi Arabia Pushes For OPEC Production Cut Of Up To 1 Million B/d As Outbreak Weighs On Demand

Half of China’s economy – the second largest in the world – is expected to be offline through at least mid-February. Traders started pricing in the impact on oil demand weeks ago. And now that it’s become clear to everybody that this problem isn’t going away any time soon, and after oil prices recorded their largest monthly drop in 30 years, OPEC might step in to ‘re-balance’ the global energy market.

Confirming earlier whispers, Saudi Arabia is reportedly pushing for a major, short-term oil production cut, WSJ reported Monday morning, citing anonymous OPEC officials.

A group of OPEC countries and their allies – collectively known as OPEC+ – are planning to meet Tuesday and Wednesday to debate possible action thanks to the outbreak in China, the world’s largest oil importer and consumer.

One scenario being discussed is that Saudi Arabia, OPEC’s kingpin, would lead a collective reduction of 500,000 barrels a day. The production cut will remain in place until the outbreak has subsided, cartel officials said.

Another, more drastic, option being considered would involve a temporary cut of 1 million b/d, a cut that would deliver a decisive ‘jolt’ to the market (and potentially trigger another flurry of angry Trump tweets about oil prices – the ‘invisible tax’ – being too high.

According to WSJ, the cartel is still split on what to do. Plans to schedule a full meeting of the cartel and its Russia-led allies were scrapped in favor of a smaller meeting to discuss the impact of the virus outbreak on global demand.

OPEC and its allies are split over how to manage oil supply in the face of the deadly coronavirus, which has already eroded demand in China. Collective responses by oil producers tend to be more efficient in supporting crude prices, which have lost 15% in the past month.

Despite the Saudi prodding, the cartel and 10 allied nations led by Russia stopped short of scheduling an emergency meeting of its full delegation this week and will instead hold a technical meeting to access the virus’s impact and make recommendations to members.

Producers would then decide if they hold a small gathering led by Saudi Arabia and Russia – called a Joint Ministerial Monitoring Committee – or a summit of all 23 producers in Vienna, the officials said.

Oil prices ticked higher on the report. If the cuts are confirmed, we suspect the rebound will be even more pronounced.

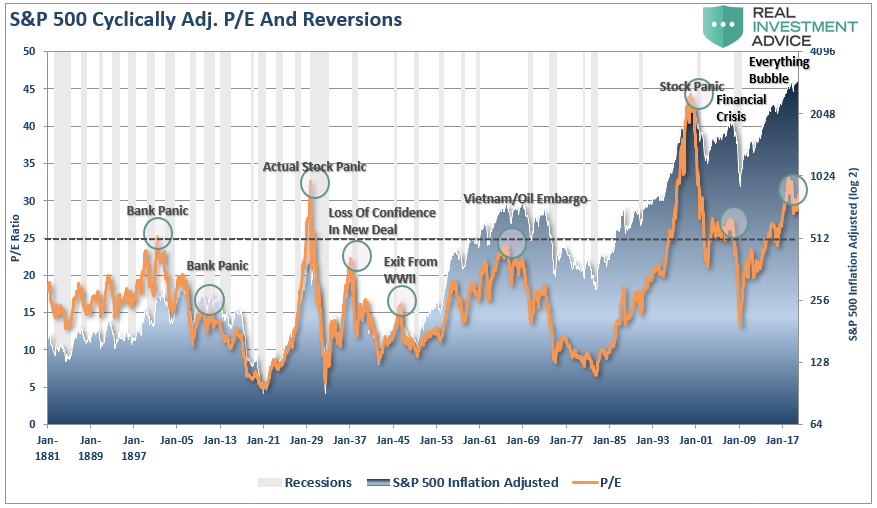

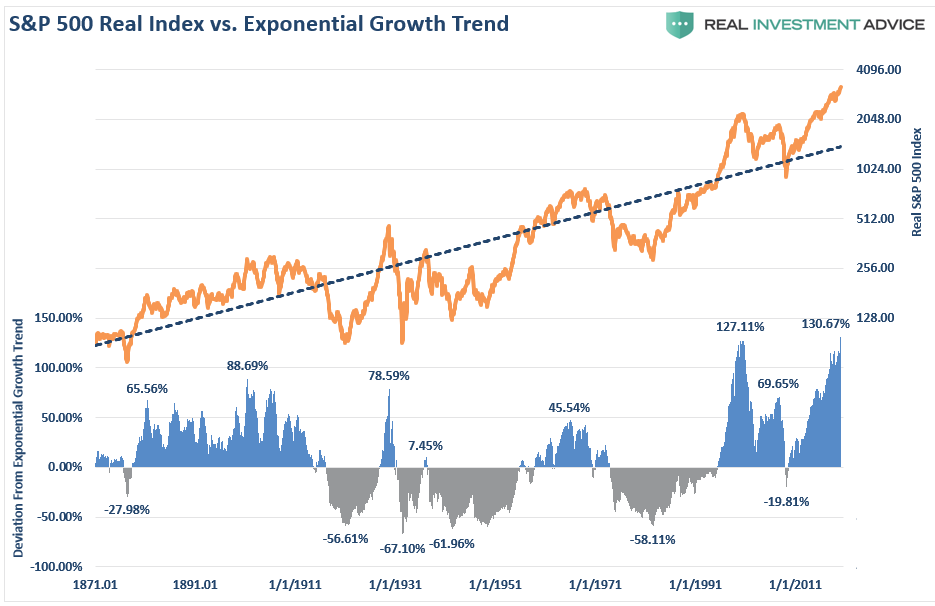

In late 1999, it was stated that “investing like Warren Buffett was the same as driving ‘Dad’s ole’ Pontiac.” The suggestion, of course, was that “value” investing was no longer a viable investment strategy in the new “dot.com” economy where “growth” was all that mattered. After all, in the “new world,” it was indeed “different this time.”

Less than a year later, investors wished they had adhered to Warren Buffett’s strategy of buying value as the “Dot.com dream” emerged as a nightmare for many unwitting individuals.

However, it wasn’t just stocks either. In 2007, individuals were chasing the “momentum” in the real estate market as individuals left their jobs to pursue riches in housing and were willing to “pay any price” under the assumption they would be able to sell higher. Of course, it was long after then Fed Chairman Ben Bernanke uttered the words “the subprime market is contained,” the dreams of riches evaporated like a “morning mist.”

As Warren Buffett once quipped, “price is what you pay, value is what you get.”

Throughout market history, investors have repeatedly abandoned this simple principle during periods where bull market advances seemed to defy logic. Ultimately, those investors paid a dear price for their speculation as the reality of “overpaying for value” led to poor financial outcomes.

As we have noted in a series of articles posted at RIAPRO.net, we believe the market is on the precipice of another monumental shift from “growth” to “value,” and as repeatedly seen in the past will blindside most investors.

Value vs. Growth

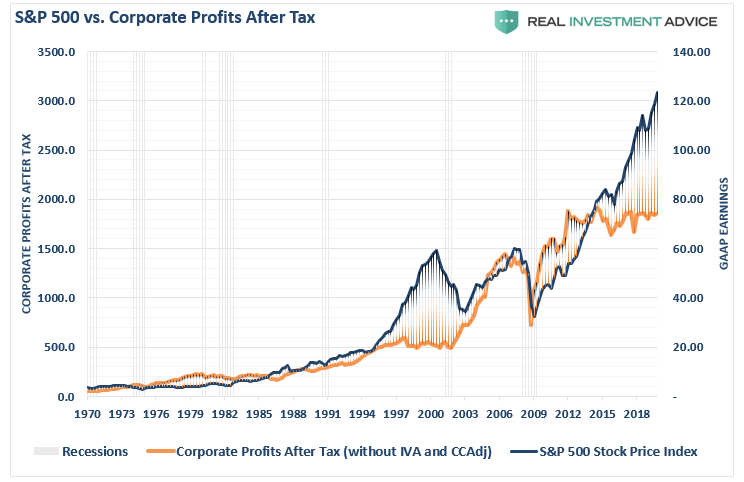

The market’s surge higher since the financial crisis, which has been driven by massive fiscal and monetary policies, have been nothing short of extraordinary. Currently, the S&P 500 is trading at the greatest deviation from its long-term exponential growth trend in history.

This is occurring at a time where market prices are advancing while corporate profitability has been flat since 2014.

While we have previously discussed the unparalleled use of monetary policy to push markets higher, massive fiscal spending designed to keep economic growth positive, and how corporations have shunned future growth with a preference for the short-term incentive of “share repurchases.”

As Michael Lebowitz, CFA previously noted:

“As a result of these behaviors and actions, we have witnessed an anomaly in what has historically spelled success for investors. Stronger companies with predictable income generation and solid balance sheets have grossly underperformed companies with unreliable earnings and over-burdened balance sheets. The prospect of majestic future growth has trumped dependable growth. Companies with little to no income and massive debts have been the winners.”

This was much the same as we saw in late 1999 as companies with no earnings, no revenue, and no real strategy for growth exploded higher in a speculation fueled buying frenzy.

This underperformance of “value” relative to “growth” is not unique. What is unique is the current duration and magnitude of that underperformance. To say unprecedented is almost an understatement.

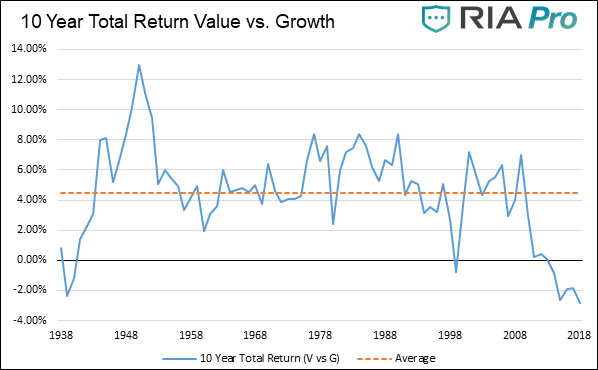

The graph below charts ten-year annualized total returns (dividends included) for value stocks versus growth stocks. The most recent data point representing 2018, covering the years 2009 through 2018, stands at negative 2.86%. This indicates value stocks have underperformed growth stocks by 2.86% on average in each of the last ten years.

The data for this analysis comes from Kenneth French and Dartmouth University.

There are two important takeaways from the graph above:

Over the last 90 years, value stocks have outperformed growth stocks by an average of 4.44% per year (orange dotted line).

There have only been eight ten-year periods over the last 90 years (total of 90 ten-year periods) when value stocks underperformed growth stocks. Two of these occurred during the Great Depression and one spanned the 1990s leading into the Tech bust of 2001. The other five are recent, representing the years 2014 through 2018.

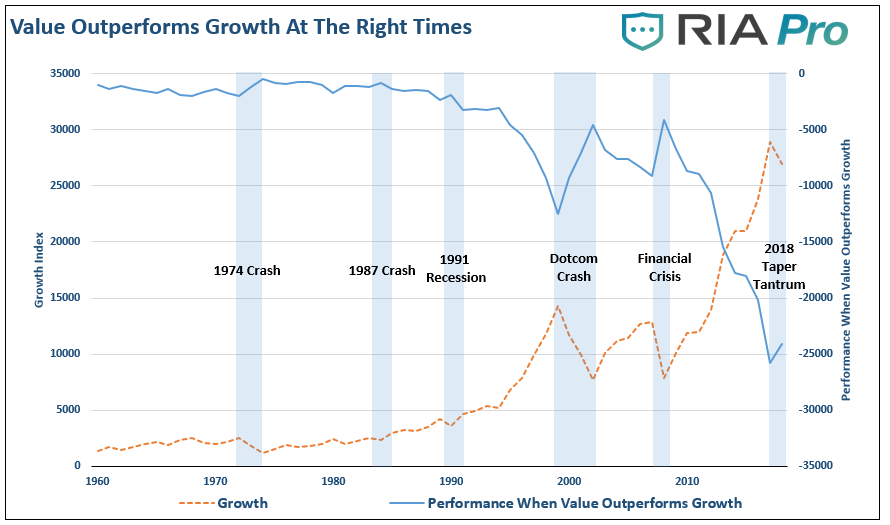

It is important to understand that it is “investor speculation” which drives these deviations in returns between growth and value. Of course, when things ultimately go “pear-shaped,” the return to value tends to be a swift event. The chart below overlays important periods in market history where “value” became “valued.”

The chart below shows the difference in the performance of the “value vs growth” index versus a pure growth index. Both are based on a $100 investment. While value investing will always provide consistent returns, there are times when growth outperforms value and vice versa. What is important to note are the periods when “value investing” has the greatest outperformance as noted by the “blue shaded” areas.

Given that we are statistically, and logically, very likely nearing the end of the current cycle, it is even more crucial to grasp what decades of investment experience tells us about the future.

When the cycle turns, we have little doubt the value-growth relationship will revert back to its long-term mean. Importantly, seldom do such reversions stop at the mean.

“To better understand why this is so important, consider what happens if the investment cycle turns and the relationship of value versus growth returns to the average over the next two years. In such a case, value would outperform growth by nearly 30% in just two years. Anything beyond the average would increase the outperformance even more.” – Michael Lebowitz

History Doesn’t Repeat

It is often noted that history doesn’t repeat, but it often rhymes, particularly when it comes to financial markets. It is not a question of if the rotation to value will occur, it is only a function of when.

However, this is the risk that investors take on currently in the market. Chasing markets is the purest form of speculation. Ultimately, it is a pure bet on prices going higher rather than determining if the price being paid for those assets are selling at a discount to fair value.

Benjamin Graham, along with David Dodd, attempted a precise definition of investing and speculation in their seminal work Security Analysis (1934).

“An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

There is also a very important passage in Graham’s The Intelligent Investor:

“The distinction between investment and speculation in common stocks has always been a useful one, and its disappearance is a cause for concern. We have often said that Wall Street as an institution would be well advised to reinstate this distinction and to emphasize it in all its dealings with the public. Otherwise, the stock exchanges may someday be blamed for heavy speculative losses, which those who suffered them had not been properly warned against.”

While the current market advance seems to be unstoppable, this was the attitude seen by investors at every prior market in history. As Howard Marks once stated:

“Rule No. 1: Most things will prove to be cyclical.

Rule No. 2: Some of the greatest opportunities for gain and loss come when other people forget Rule No. 1.”

The realization that nothing lasts forever is critically important to long term investing. To “buy low,” one must have first “sold high.” Understanding that all things are cyclical suggests that after long price increases, investments become more prone to declines than further advances.

The rotation from “growth” to “value” is inevitable. It will occur against a backdrop of devastation for the majority of investors quietly lulled into the extreme sense of complacency years of monetary interventions have provided.

The only question is whether you will be the buyer of “value” at a time when everyone else is selling “growth?”

It appears that around the time we suggested someone reach out to the Wuhan Institute of Virology to get some answers about the origin of the deadly Coronavirus epidemic (which Twitter decided was sufficient to get us barred from the platform), India was doing just that.

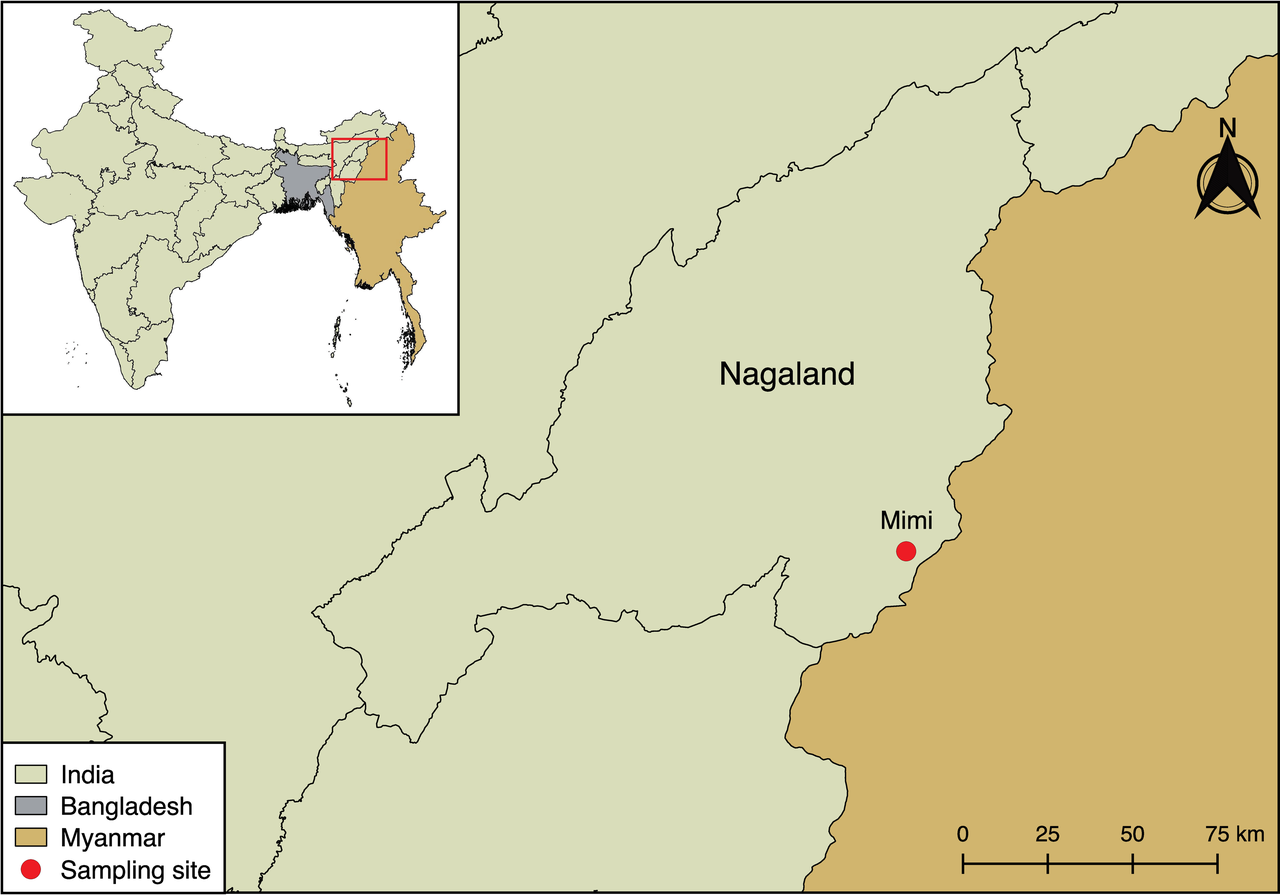

The Indian government has ordered an inquiry into a study conducted in the Northeastern state of Nagaland (close to China) by researchers from the U.S., China and India on bats and humans carrying antibodies to deadly viruses like Ebola, officials confirmed to The Hindu.

The study came under the scanner as two of the 12 researchers belonged to the Wuhan Institute of Virology’s Department of Emerging Infectious Diseases, and it was funded by the United States Department of Defense’s Defense Threat Reduction Agency (DTRA). They would have required special permissions as foreign entities.

The study, conducted by scientists of the Tata Institute of Fundamental Research, the National Centre for Biological Sciences (NCBS), the Wuhan Institute of Virology, the Uniformed Services University of the Health Sciences in the U.S. and the Duke-National University in Singapore, is now being investigated for how the scientists were allowed to access live samples of bats and bat hunters (humans) without due permissions.

The results of the study were published in October last year in the PLOS Neglected Tropical Diseases journal, originally established by the Bill and Melinda Gates Foundation.

Bill Gates, the man who tops the Forbes richest person in the world list had issued a grave warning about a potential Coronavirus-like catastrophe that could kill 30 million people at the Munich Security Conference held in Germany in 2017:

“Whether it occurs by a quirk of nature or at the hand of a terrorist, epidemiologists say a fast-moving airborne pathogen could kill more than 30 million people in less than a year. And they say there is a reasonable probability the world will experience such an outbreak in the next 10 to 15 years.”

“The Indian Council of Medical Research (ICMR) sent a five-member committee to investigate. The inquiry is complete, and a report has been submitted to the Health Ministry,” a senior government official told The Hindu.

The U.S. Embassy and the Union Health Ministry declined to comment on the inquiry. In a written reply to questions from The Hindu, the U.S. Centre for Disease Control (CDC) in Atlanta said it “did not commission this study and had not received any enquiries [from the Indian government] on it.” An American official, however, suggested that the U.S. Department of Defense might not have coordinated the study through the CDC.

The study, ‘Filovirus-reactive antibodies in humans and bats in Northeast India imply Zoonotic spillover’, published in PLOS Neglected Tropical Diseases states the researchers found “the presence of filovirus (e.g. ebolavirus, marburgvirus and dianlovirus) reactive antibodies in both human (e.g. bat hunters) and bat populations in Northeast India, a region with no historical record of Ebola virus disease.”

It adds: “Ebola has posed a global health threat several times, most notably from 2013 to 2016. It is a deadly disease, with a fatality rate of roughly 50 percent.” Now, according to health officials, 2019-nCoV, too, has acquired the ability to pass between people and can do so before symptoms appear.

The Nagaland study suggests bats in South Asia act as a reservoir host of a diverse range of filoviruses, and filovirus spillover occurs through human exposure to these bats. For the study done in 2017, 85 individuals participating in an annual bat harvest at Mimi, Nagaland, were picked. The majority of bat hunters were male, aged between 18 and 50, and participated at least eleven times in the harvest. The study says the potential virus present in the bats may not be an exact copy of the virus responsible for various outbreaks.

Given the widespread challenges from the newly discovered viruses, officials say they want to take no chance on their spread and will take action to ensure all medical studies in the country adhere to strict norms.

Indian military believes that the U.S. Center for Disease Control in Atlanta was involved in the 1994 plague in the Indian city of Surat which killed 52 people and close to a quarter of the city’s citizens fled the area for fear of being quarantined. Even the origin of 1994 plague is mired in controversy to this day.

R. Prasannan, the New Delhi Bureau Chief of The Week magazine, in his piece questioning whether Coronavirus was created in a lab wrote,

During the 1994 plague outbreak in Surat and Beed, it was found that the germs had an extra protein ring which could only have been inserted artificially. Indian scientists had raised concerns about a US biowar experiment having gone awry. THE WEEK had carried reports giving details of germ war reseach being carried on in labs under the Centre for Disease Control in Atlanta and about a newly developed germ detector being tested. The US embassy had denied the allegations. There were also reports that the Surat germ could have been developed in a lab in Almaty, Kazakhstan.

Mr. Prasannan is one of many experts from different fields who have raised doubts over the narrative being paddled by certain sections of the media. Among them is American Senator Tom Cotton who questioned mainstream media’s narrative on the origin of 2019 Wuhan Coronavirus, instead hinting that a biosafety laboratory in Wuhan working with the deadliest pathogens in the world could be the true source.

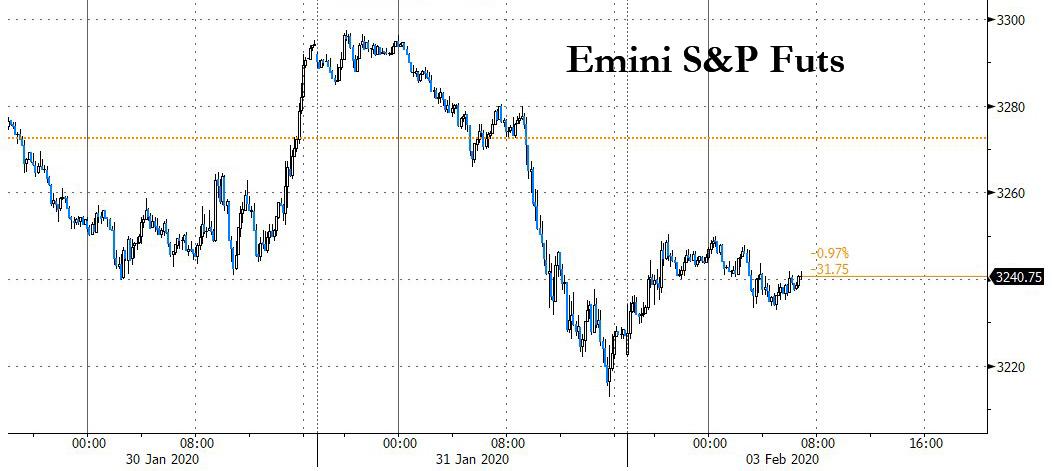

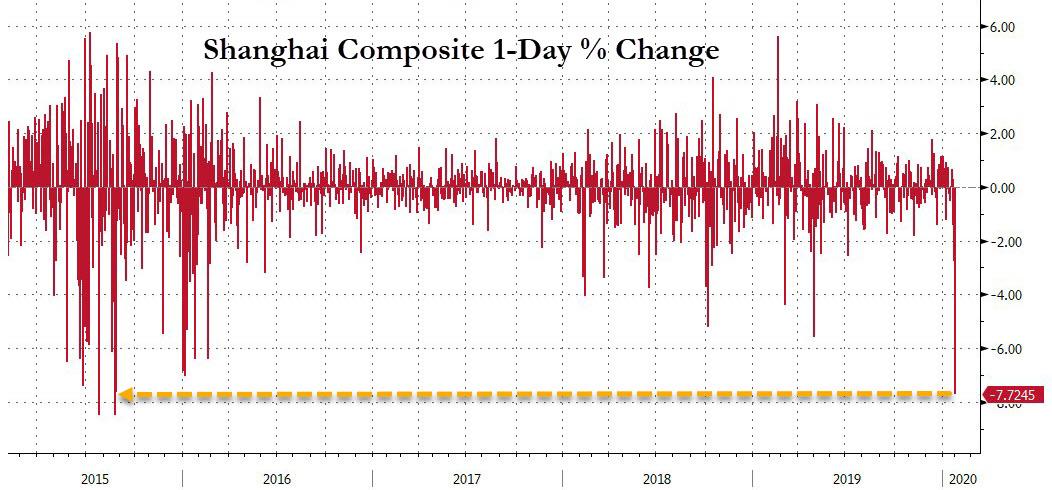

Futures Rebound Despite Historic Bloodbath In China Where 3,257 Stocks Hit Limit Down

While Beijing’s emergency intervention in Chinese markets which included a short sale ban, a dramatic liquidity injection and a cut in reverse repo rates, failed to prevent a rout, it certainly helped stabilize stocks in Europe and US equity futures, which have staged a modest rebound after plunging on Friday in their worst drop since August.

First the good news: European shares opened on apparent relief that the UK had finally exited the European Union (even as cable tumbled amid renewed fears about the ongoing negotiation between Boris Johnson and Brussels), however fears about the coronavirus kept buying in check. Having risen 0.2% in early deals, the pan-European STOXX 600 index was flat by midday in London. Blue-chip British stocks added 0.35%, helped by a fall in sterling

Futures for U.S. stocks were higher by 0.4% in early trading, and contracts on the three main American equity indexes all climbed, with Gilead Sciences rising in the premarket as China prepares to test one of the company’s new anti-viral drugs.

Asian markets more broadly continued to sell off. MSCI’s broadest index of Asia-Pacific shares outside Japan was down for an eighth straight day, falling 0.85% at 527.61 points, its lowest since early December. Japan’s Nikkei dropped 1% to the lowest since November and Australia’s benchmark index ended down 1.3%. But it was China that was the highlight of the overnight session.

Aiming to prevent a market panic, China’s government took emergency steps to shore up an economy hit by travel curbs and business shut-downs, including a short sale ban. In a bid to soften the blow to China’s economy, the country’s central bank also unexpectedly cut reverse repo rates by 10 basis points and injected 1.2 trillion yuan ($173.8 billion) of liquidity into the markets on Monday, of however 1 trillion yuan was to rollover maturing liquidity.

It wasn’t enough, however, and Chinese shares closed deep in the red, with the blue-chip index down 7.8% – the worst return from a Chinese lunar new year for the index in 13 years and the biggest one day drop since the 2015 market rash – to a 4-1/2 month low, wiping out 12 months worth of gains!

Monday’s declines were particularly severe. The CSI 300 Index sank as much as 9.1% – a slump rarely seen in its almost 15-year history.

It was even uglier at the single-stock level, because even though investors tried to log their sell orders order, many of them couldn’t exit the market fast enough, as all but 162 of the almost 4,000 stocks in Shanghai and Shenzhen recorded losses, with about 90% dropping the maximum allowed by the country’s exchanges, and a whopping 3,257 Chinese stocks were closed limit down. Health-care shares comprised most of Monday’s gainers on speculation they will benefit from the virus outbreak. The huge number of stocks trading limit down means it could take days for investors to execute their orders, prolonging the sell-off.

“The sell-off was so quick and intense,” said Li Changmin, managing director at Snowball Wealth in Guangzhou. “We’ll be busy dealing with risk controls and even liquidation pressure if stocks keep falling.”

“I was anxious before the market opened, and had made plans on what to sell and by how much last Friday,” said Bruce Yu, a fund manager with Franklin Templeton SinoAm Securities Investment Management Inc. in Taipei. “Some of my trades weren’t made today — we’ll see if we can sell them tomorrow.”

Fund managers hit the phones to calm investors, seeking to avoid the kind of redemptions and forced selling seen as recently as 2018. China’s securities regulator took steps to support the stock market, telling some brokerages that their proprietary traders aren’t allowed to be net sellers of equities this week, according to people familiar with the matter.

“My biggest concern was that investors would rush to redeem their holdings in private and mutual funds,” said Jiang Liangqing, a money manager at Ruisen Capital Management in Beijing whose team is working from home across China. “A key task for us is to reassure our fund holders and ask them to stay calm.”

The benchmark $7.5 trillion Shanghai Composite index lost $420 billion in value and the yuan opened at its weakest level of 2020, tumbling past 7 per dollar, a level which may spark fresh accusations by the US Treasury that Beijing is manipulating its currency lower.

The sell-off was widespread on Monday: in addition to thousands of stocks, commodity futures from iron ore to crude also sank by the daily limit. That said, while China’s losses were heavy, they were mostly a product of selling pressure that had built up over the Lunar New Year break, not a reflection of new fears among investors.

“The market seems to have reacted quite reasonably,” said David Nietlispach, PM at Pala Asset Management. “There is no panic and no selloff of securities that are unrelated to the coronavirus. The government interventions have been so heavy, though, that you will see an impact on the global economy.”

“The impact in Chinese equity markets has been in line with what futures were suggesting, so the market has taken the slump in its stride,” said Rodrigo Catril, Sydney-based strategist at National Australia Bank. “There was also some cushion from the new measures.”

And so, even with the rebound in US futures, an index of global stocks hovered near seven-week lows on Monday as Asian stocks plunged on their first trading day after a long break, amid growing fears the coronavirus epidemic would hit China’s economy and cripple Chinese supply-chains and demand. MSCI’s All Country World Index, which tracks shares in 47 countries, was down 0.2% on the day, touching its lowest since Dec. 16. The index is down 1.3% this year.

Meanwhile, as we noted yesterday, all attention remains on China, and overnight a raft of banks, including Citigroup, Nomura and JPMorgan, downgraded their forecasts for China’s economic growth.

“Given that we’re 10 years into a global equity bull market, the potential for the virus to trigger a significant market correction is much greater now than it has been during previous epidemics,” said Neil Shearing, chief economist at Capital Economics in a note to clients.

As Chinese markets opened after the 10-day break, Shanghai copper hit its daily selling limit as did Shanghai crude oil while yields on the country’s 30-year government bonds traded in the interbank market were down 18.5 basis points.

In commodities, oil pared early losses after Brent slumped into a bear market since hitting a high in early January following a Bloomberg report Chinese oil demand is down by 20%, while the safe-haven Japanese yen and gold stepped back from recent highs. Chinese commodities were especially hard hit: Shanghai copper hit its daily selling limit as did Shanghai crude oil while yields on the country’s 30-year government bonds traded in the interbank market were down 18.5 basis points. Dalian soymeal plunged 4.1% while Dalian iron ore hit limit down as steel prices fell.

Gold, which posted its best month in five in January, slipped as much as 1% to $1,574.5 an ounce. Yields on U.S. debt came off lows.

In currencies, the yen fell but remained near a 3-1/2 week high against the dollar at 108.50. The euro was 0.25% lower at $1.1066. The dollar gained as the market unwound some of the month-end trades from last week. Norway’s krone fell to a three-month low versus the euro after Norway’s manufacturing PMI data came in weaker than expected and on news that Chinese oil demand has dropped by about three million barrels a day, or 20% of total consumption, amid the coronavirus crisis. The pound slipped by more than 1% against the dollar on fears of a new cliff edge in trading arrangements between Britain and the European Union, as the two sides prepare to negotiate their future relationship.

While Brexit is now in the history books, remarks from UK PM Johnson on post-Brexit talks have been largely in-line with reports via UK press over the weekend; with Johnson saying there is no need to accept various EU rules in a trade deal. In related news, UK will begin free trade negotiations immediately after Brexit and is reportedly aiming to have 80% of trade covered by FTA’s within 3 years, while there were separate comments from DUP’s Foster that it is difficult to see how there will not be new checks between Britain and Northern Ireland.

On the calendar today, expected data include PMIs. Sysco and Alphabet are reporting earnings

Market Snapshot

S&P 500 futures up 0.4% to 3,237.75

STOXX Europe 600 up 0.1% to 411.21

MXAP down 0.9% to 164.32

MXAPJ down 0.9% to 527.16

Nikkei down 1% to 22,971.94

Topix down 0.7% to 1,672.66

Hang Seng Index up 0.2% to 26,356.98

Shanghai Composite down 7.7% to 2,746.61

Sensex up 0.4% to 39,905.62

Australia S&P/ASX 200 down 1.3% to 6,923.25

Kospi down 0.01% to 2,118.88

German 10Y yield rose 0.4 bps to -0.43%

Euro down 0.3% to $1.1063

Italian 10Y yield fell 0.7 bps to 0.769%

Spanish 10Y yield rose 0.4 bps to 0.239%

Brent futures down 3.1% to $56.37/bbl

Gold spot down 0.6% to $1,579.13

U.S. Dollar Index up 0.3% to 97.66

Top Overnight News from Bloomberg

China cut some borrowing costs and injected cash into the financial system to ensure ample liquidity as the nation’s stocks tumbled 9%. The central bank set its daily yuan reference rate stronger than the key 7-per-dollar level as onshore markets resumed trading for the first time since Jan. 23

The dollar advanced and Japan’s currency snapped a three-day winning run as markets took some comfort in the measures the Chinese government were taking, while the 10-year Treasury yield climbed as much as three basis points from an almost five-month low reached on Friday

Norway’s krone fell to a three-month low versus the euro after Norway’s manufacturing PMI data came in weaker than expected and on news that Chinese oil demand has dropped by about three million barrels a day, or 20% of total consumption, amid the coronavirus crisis

The pound slipped by more than 1% against the dollar on fears of a new cliff edge in trading arrangements between Britain and the European Union, as the two sides prepare to negotiate their future relationship

Chinese stocks plummeted by the most since an equity bubble burst in 2015 as they resumed trading to the worsening virus outbreak. The CSI 300 Index dropped 9.1%. China’s benchmark iron ore contract fell by its daily limit of 8%, while copper, crude and palm oil also sank by the maximum allowed

OPEC and its allies considered how to respond to a plunge in oil prices, with Russia signaling for the first time it was open to Saudi Arabia’s push for an emergency meeting. Potential dates being discussed are Feb. 8-9 and Feb. 14-15, though for now the next regular meeting on March 5-6 remains on the schedule, a delegate said

Chinese oil demand has dropped by about three million barrels a day, or 20% of total consumption, as the coronavirus squeezes the economy, according to people with inside knowledge of the country’s energy industry. Fatalities top 360 as China returns from holiday: virus update

The U.K. and the European Union begin their battle over a future trade deal on Monday. In a major speech in London, Prime Minister Boris Johnson will threaten to walk away from talks with the EU rather than accept demands from Brussels to sign up to the bloc’s single market regulations and the rulings of its court

New Zealand Treasury expects economic growth to ease through 2020. Domestic data over December and January showed tentative signs of an improving economy with measures of business sentiment improving but still in negative territory

Asian equity markets mostly traded with heavy losses as markets braced themselves for China’s return from the Lunar New Year holiday in which mainland bourses opened with losses of nearly 9% and several Shanghai commodity prices hit limit down, despite efforts by China to cushion the blow. ASX 200 (-1.3%) was lower in which energy and mining sectors underperformed the broad weakness across Australia sectors aside from the gold miners due to recent safe-haven plays, while Nikkei 225 (-1.0%) traded subdued but off its lows after finding mild relief from currency flows. Elsewhere, a blood bath was seen at the reopen in mainland China as the Shanghai Comp. (-7.7%) played catch up to the global market rout brought on by the coronavirus and with sentiment not helped by a contraction in Industrial Profits, although mainland bourses were slightly off their worst levels and the Hang Seng (+0.2%) recovered into positive territory after several supportive measures including efforts to restrict short selling and the PBoC’s CNY 1.2tln reverse repo operation in which the central bank also lowered repo rates by 10bps. Finally, 10yr JGBs consolidated overnight and although prices eventually retreated back below the 153.00 level, they still held on to the majority of last week’s advances amid the rout in stocks and after the BoJ kept February purchase intentions mostly in line with the previous month.

Top Asian News

Risks Mount for Hong Kong After Economy Shrank in 2019

Billionaire Razon Buys 25% Stake in Ayala’s Manila Water

Turkey’s Real Rates as Low as in Japan After Inflation Surprises

A relatively tame session for European equities thus far [Eurostoxx 50 +0.2%], following on from the frantic Chinese sell-off in which its markets wiped some USD 420bln in its catch-up play, with Shanghai Comp closing with losses of almost 8%. Sectors are mixed with no clear reflection of the current risk tone as defensives and cyclicals remain varied, albeit energy is underperforming amid losses in the complex. In terms of individual stocks Ingenico (+11.4%) shares spiked higher to the top of the Stoxx 600 at the open amid M&A induced moves with Wordline set to acquire the company in a deal value at EUR 7.8bln. Ryanair (+4.6%) shares follow closely behind amid earnings in which the group announced an extension to its share buyback programme. On the flip side, Siemens Heathineers (-4.6%) shares fell to the foot of the pan-European index following double-digit YY declines in adj. EBIT and net income.

Top European News

U.K. Manufacturing Avoids Contraction in Post-Election Bounce

Avast Roller Coaster Exposes Frailty of Sleepy Czech Bourse

Euro-Area Manufacturing Sees Green Shoots at Start of 2020

Macron Seeks Poland Reset as Warsaw Tightens Grip on Courts

In FX, the Yuan suffered from revived angst/catch-up play upon Mainland’s return following its extended Lunar New Year holiday and having had its first opportunity to react to the escalating threats from the outbreak. Moreover, China took a barrage of measures, including lowering rates on its 7- and 14-day reverse repos by 10bps each, in an attempt to cushion losses in the markets amid expectations for a tumultuous session. USD/CNY was propelled at the onshore open as the pair breached 7.00 to the upside (vs. 6.9364 close on Jan 23rd) and eclipsed its 100 DMA at 7.0223 before closing around 7.0250 – the weakest close since December 12th, USD/CNH remains comfortably above 7.00. Subsequently, DXY gained and resides above 97.500 (vs. 97.429 open and low) with the index supported amid weakness in some peers. DXY sees its 200 DMA around 97.720 and 100 DMA at 97.832 ahead of the psychological 98.000 – with traders eyeing the ISM Manufacturing release for influence, whilst the Iowa caucus will also be followed to give a lens into the Democratic presidential candidate.

GBP – The marked G10 underperformer heading into PM Johnson’s speech, the content of this was predominantly flagged by UK press over the weekend; taking a hard stance regarding post-Brexit trade negotiations with the EU – with one of the pledges being to not align the UK with the EU alongside a willingness to leave on WTO terms if necessary. Meanwhile, EU’s Chief Brexit Negotiator was expected to warn that a FTA is unlikely should the UK misalign itself with EU standards. Barnier noted that the EU is not seeking UK regulatory alignment, but “we do want consistency”, which is similar in essence. GBP/USD saw some support around 1.3100, having retreated from Friday’s 1.3200 close and with limited reaction seen by the UK manufacturing PMI being revised higher to neutral from a mild contraction. Thereafter, GBP/USD breached 1.3100 to the downside, breaching Friday’s low (1.3080) and its 50 DMA (1.3075) to a low of 1.3055 ahead of the psychological 1.3050.

AUD, NZD, JPY, EUR – All softer vs. the Buck as DXY gains traction. Antipodeans were supported in overnight trade but have since trimmed gains and reside around flat territory – AUD/USD briefly topped 0.6700 before reversing and finding mild support around 0.6680, whilst its Kiwi counterpart fell back below its 100 DMA (0.6466) having reached an overnight high of 0.6476 and with 0.6450 seen as psychological support. Similarly, the safe-haven currencies succumb to the firmer Dollar, with USD/JPY meandering around 108.50 ahead of its 100 DMA at 108.75. EUR/USD was largely unreactive to a modest revision higher in the EZ manufacturing PMI, which also came with an optimistic accompanying statement from the IHS, noting that economy could see growth strengthen in the period ahead. EUR/USD trades just above the 1.1050 mark (vs. high 1.1095) with the pair eyeing EUR 927mln of options expiring around 1.1075 at today’s NY cut.

EM – Mild reprieve across the EM-sphere, but potentially more-so consolidation following last-week’s hefty losses. TRY saw little reaction as the country’s real rates were dragged further into negative territory amid the uptick in January YY inflation – with participants noting that this may prompt a pause in the CBRT’s easing cycle, although not a cessation given the Turkish President’s pledge to bring rates back to single digits this year. USD/TRY remains flat intraday around 5.9850. Meanwhile, USD/ZAR has retreated back below 15.000 with some noting a correction from last week’s losses alongside profit taking.

In commodities, overall mixed with WTI front month futures firmer but Brent subdued on the demand implications of the cornonavirus outbreak. Furthermore, reports noted that Chinese oil demand is seen falling some 20% on the coronavirus lockdown, which does not bode well for its largest suppliers Saudi and Russia. On the OPEC front, sources noted that OPEC and allies are mulling further output reductions of ~500k BPD, with a meeting reportedly scheduled for February 14th/15th. Note: some desks highlight that a bulk of the “new cuts” could factor in the disruptions in Libya, which net-net may end up in a lower aggregate output reduction. The Joint Technical Committee will be convening on February 4th/5th to assess impacts of the virus and are likely to make a recommendation around any further action to support the market, according to sources. Further sources via journalist Summer Said noted that Saudi Arabia are reportedly considering a drastic temporary cut of up to 1mln BPD in response to the coronavirus. WTI and Brent futures reside under USD 52/bbl and just north of USD 56/bbl with fleeting support seen from the OPEC sources. Elsewhere, spot gold saw early losses amid a firming USD in which prices briefly dipped below 1575/oz. Meanwhile, panic selling seen at the resumption of Chinese commodities trading saw Shanghai copper, crude oil and Dalian iron ore futures all hit limit down in catch-up action from the Lunar New Year holiday.

US Event Calendar

9:45am: Markit US Manufacturing PMI, est. 51.7, prior 51.7

10am: Construction Spending MoM, est. 0.5%, prior 0.6%

10am: ISM Manufacturing, est. 48.5, prior 47.2

10am: ISM New Orders, est. 47.7, prior 46.8

10am: ISM Prices Paid, est. 51.5, prior 51.7

10am: ISM Employment, prior 45.1

Wards Total Vehicle Sales, est. 16.8m, prior 16.7m

DB’s Jim Reid concludes the overnight wrap

Before we get to a busy week ahead, including the start of US primaries in Iowa today, all eyes on this morning’s first Chinese market opening since the extended holiday ended. The CSI 300 (-7.50%), Shanghai Comp (-7.63%) and Shenzhen Comp (7.84%) are all down heavily but are off their earlier deeper loses. Meanwhile, the Nikkei (-0.98%) is also trading down while the Hang Seng (+0.53%) and Kospi (+0.11%) are up. As for fx, the onshore Chinese yuan is down -1.49% to 7.0157, the weakest since December 12, as it also reopened post the holiday. Elsewhere, futures on the S&P 500 are up +0.75% while 10yr USTs yields are +1.7bps higher this morning which shows that the sell-off hasn’t accelerated with the China re-opening. In commodities, Shanghai Iron ore futures are down c. -7.50% today while those on copper are -6.60% with brent oil prices -0.23%. As for overnight data releases, China’s January Caixin manufacturing PMI came in at 51.1 (vs. 51.0 expected) but the survey covers the period before the virus concerns mounted. Japan’s final manufacturing PMI came in at 48.8 vs. 49.3 in the initial release.

The latest on the virus is that there are now 17,205 confirmed cases (up from 9,692 on Friday) and the death toll now stands at 361 (up from 170). Philippines reported the first Coronavirus death outside of China and more cases have been confirmed globally including in the US. Lots more travel restrictions to and from China have been put into place.

This is after the PBoC and other Chinese bodies announced numerous measures over the weekend to try to keep markets orderly at the re-open including a 10bps cut for both the 7- and 14-day repo rates overnight. Yesterday, the central bank had announced the injection of a net 150 billion yuan ($21.7 billion) into money markets this morning with an additional trillion yuan netting off money market redemptions today. Meanwhile, the securities regulator also said yesterday that it would halt night sessions for futures trading from today until further notice, and will allow some share pledge contracts to be extended by as long as 6 months as part of measures to improve market expectations and prevent irrational behaviour. It’s likely more intervention will come if required in the days ahead.

Back here in the UK, Bloomberg reported overnight that the UK PM Boris Johnson will say in a speech today that he wants a comprehensive trade agreement at least as good as the one the EU has reached with Canada but is likely to insist that “Britain will prosper” even without such a deal. He is also likely to say that the UK is not willing to accept demands from the EU to sign up to the bloc’s single market regulations and the rulings of its court. His speech will be followed by a speech from the EU chief Brexit negotiator Michel Barnier in Brussels, where he is due to set out his planned negotiating position with the UK. Sterling is trading down -0.31% at 1.3166 this morning on the news. Expect lots of headlines today.

Overnight we also heard from the ECB Chief Economist Philip Lane and he said that rising labour costs will eventually reignite inflation in the euro zone and that the ECB is on track toward its goal. On the strategic review he said that suggestions so far have included making the target more specific at precisely 2% – instead of the current “below, but close to, 2%” – and possibly adding a band of tolerance around it. He also acknowledged that the ECB will consider whether its measures of inflation should take better account of housing costs, which are currently severely under-weighted.

So a busy start to the week as we kick off a potentially turbulent February. In terms of the rest of this week the highlight could be today’s first US democratic primary in Iowa – the first of four this month. There’ll also be a number of data releases, including PMIs from around the world (today and Wednesday), before the US jobs report comes out on Friday. Earnings season will also continue to be in full flow.

While Iowa only makes up c.1% of nationwide delegates, we will start to see some sign as to momentum of the various candidates. Technically there will also be Republican primaries, but these are widely considered a foregone conclusion in favour of President Trump. In terms of what to expect, the national polling average from RealClearPolitics shows former Vice President Joe Biden still in the lead at the moment, with 27.2%, followed by Senator Bernie Sanders on 23.5% and Senator Elizabeth Warren on 15.0%. However, in Iowa, the polling average shows Sanders in the lead, with 24.7%, and Biden in second on 21.0%. Furthermore, both former Mayor Pete Buttigieg (16.3%) and Warren (15.2%) are around the crucial 15% mark that is important when it comes to accumulating the delegates required to win the nomination.

In terms of what will happen, the race remains competitive, with FiveThirtyEight’s model at time of writing giving Sanders a 40% chance of winning the most votes in Iowa, followed by Biden on 34%, with Buttigieg on 18% and Warren on a 16% chance. It’s true that often the winner of the Iowa caucuses don’t actually go on to be the nominee – indeed on the Republican side the winners in 2008, 2012 and 2016 all lost out to someone else. Nevertheless, it’s the first indicator of real votes we have, and very important in terms of momentum for each of the candidates, as it’s only 8 days later that the next primary takes place in New Hampshire, and between the two votes there’ll be another TV debate between the candidates on the Friday.

The week ahead also has a number of data highlights, with the main ones likely to be the release of manufacturing (today), services and composite (Wednesday) PMIs from around the world. We have already had the preliminary PMIs from a number of countries, so those countries such as Italy where we haven’t had the preliminary numbers will take on added interest. Also of note will be the ISM manufacturing and nonmanufacturing indices from the US, out today and Wednesday respectively. Back in December, the ISM manufacturing reading fell to 47.2, its lowest level since June 2009, though the consensus is expecting an uptick for January to 48.4, so that’s one to keep an eye out for.

On Friday, we’ll also get the US jobs report for January. The current consensus expectation is for a +160k increase in nonfarm payrolls in January, up from the +145k increase in December, with the unemployment rate remaining at 3.5%, and average hourly earnings growth ticking up a tenth to +3.0% year-on-year. Other key data out this week will come with the Euro Area’s retail sales for December on Wednesday, while in Germany, there’ll be the release of December’s factory orders on Thursday and industrial production on Friday.

Earnings season continues next week, with another raft of companies reporting. Looking at things so far, of the 225 S&P 500 companies that have reported, 74.4% have reported a positive surprise on earnings and 64.1% have reported a positive surprise on sales. Looking to the week ahead, today sees Alphabet report. Then tomorrow we’ll hear from Walt Disney, BP and Sony. On Wednesday, there’s Merck, Novo Nordisk, GlaxoSmithKline, Siemens, Qualcomm, BNP Paribas and General Motors. Thursday sees reports from L’Oréal, Bristol-Myers Squibb, Philip Morris International, Total, Sanofi, Enel, Nordea Bank, UniCredit, Société Générale, Twitter and Toyota. And finally on Friday, we’ll hear from AbbVie.

Finally on US politics, tomorrow sees President Trump give his State of the Union address to Congress. The full day by day calendar is published at the end.

Recapping last week now, and global equities continued to fall thanks to the impact from the coronavirus. The S&P 500 ended the week down -2.12% (-1.77% Friday) in its worst weekly performance since early August, and moving the index into negative YTD territory. It came as industrial bellwether Caterpillar fell -2.97% on Friday after it reported a worse-than-expected outlook, with 2020 EPS at $8.50-$10.00, which was below the Bloomberg consensus for $10.55. Furthermore, the VIX climbed +4.3pts to its highest level since October. It was a similar story in Europe, where the STOXX 600 fell -3.05% (-1.07% Friday), while in Asia, Hong Kong’s Hang Seng was down -5.86% (-0.52% Friday), its worst weekly performance since February 2018. The move away from risk assets was also reflected in commodity markets, where Brent crude fell -4.17% (-0.22% Friday), its 4th consecutive weekly move lower. Meanwhile copper fell for a 12th consecutive day, ending the week down -6.22% (-0.28% Friday), its worst weekly performance since December 2011. On the other hand, gold rose +1.12% (+0.95% Friday) to a fresh 6-year high.

Sovereign debt continued its advance last week, with 10yr Treasury yields down -17.7bps (-7.9bps Friday) to 1.507%, their lowest since early September, and 30yr Treasury yields closed below 2% for the first time since early September too. A notable development on Friday came from the yield curve, where the 3m10y curve saw an inverted close for the first time since October, having flattened by -20.3bps over the course of the week (-6.8bps Friday). Over in Germany, 10yr bund yields closed down -9.9bps (-2.8bps Friday), while the spread of Italian ten-year yields over bunds fell by -19.8bps (+2.1bps Friday) as investors reacted to the previous weekend’s regional election results.

Poor European data on Friday really didn’t help the mood for markets, with the flash GDP estimate for the Euro Area showing that the economy grew by just +0.1% qoq in Q4 (vs. +0.2% expected). This was the weakest quarterly growth since Q1 2013, and brings year-on-year growth down to +1.0% (vs. +1.1% expected), the lowest since Q4 2013. We also got the flash inflation estimate, which rose to +1.4% as expected, though the core reading fell to +1.1% (vs. +1.2% expected). In terms of the country-specific data, the French economy unexpected contracted by -0.1% (vs. +0.2% expected), the first quarterly contraction since Q2 2016 and the first of President Macron’s term of office. Meanwhile in Italy, the economy contracted by -0.3% (vs. +0.1% expected), the worst quarter since Q1 2013.

Elsewhere, German retail sales surprised to the downside, with a -3.3% mom decline in December (vs -0.5% expected), which was the biggest monthly decline since May 2007. In the UK however, mortgage approvals surprised to the upside in December, coming in at 67.2k (vs. 65.6k expected), which was the most since July 2017.

{kind=link}

{kind=link}