Iran’s New Top Military Commander Vows To “Remove America From The Region” As Vengeance For Soleimani

Overnight we reported that the power vacuum at the top of Iran’s elite Quds Force, the military organization responsible for Tehran’s numerous proxies across the Mideast as well as Iran’s overall military strategy, was filled quickly in the aftermath of Qassem Soleimani’s killing, with the Jan 3 appointment of Esmail Ghaani, who none other than Ayatollah Ali Khamenei said was “one of the most prominent commanders” in service to Iran, and that the Quds force “will be unchanged from the time of his predecessor.”

Predictably, Ghaani wasted no time to make it clear that continuity would be preserved, saying that Tehran will avenge the assassination of Soleimani by driving the US out of the region, shortly after another Revolutionary Guard commander warned that dozens of American targets are “within our reach.”

“We promise to continue martyr Soleimani’s path with the same force… and the only compensation for us would be to remove America from the region,” Esmail Qaani said on Monday in an interview to local media ahead of the general’s funeral in Tehran.

Ghaani’s comments come just days after General Gholamali Abuhamzeh, who heads the IRGC in Iran’s southern Kerman province, said 35 US targets in the region as well as Tel Aviv were identified “long ago” and are “within our reach.”

Washington responded with a similarly-worded message, with Secretary of State Mike Pompeo threatening “lawful strikes” targeting “actual decision makers” if any American asset is in danger.

Echoing Ghaani’s warning, this morning Al Jazeera reported that an Iranian IRGC Air Force Commander said President Trump “must prepare coffins for his soldiers before” he makes threats to Iran, warning that the real revenge for Soleimani’s assassination is the removal of U.S. forces from the Middle East. It wasn’t clear just how Iran hopes to achieve that goal .

As the war of words has escalated, the Pentagon ordered 3,500 more troops from Fort Bragg’s 82nd Airborne Division to deploy to the Middle East. Meanwhile, as we reported overnight, Iraq’s parliament passed a resolution calling for the removal of foreign troops from the country.

Futures Tumble, Gold Soars To 7 Year High As Iran Escalation Fears Spill Over

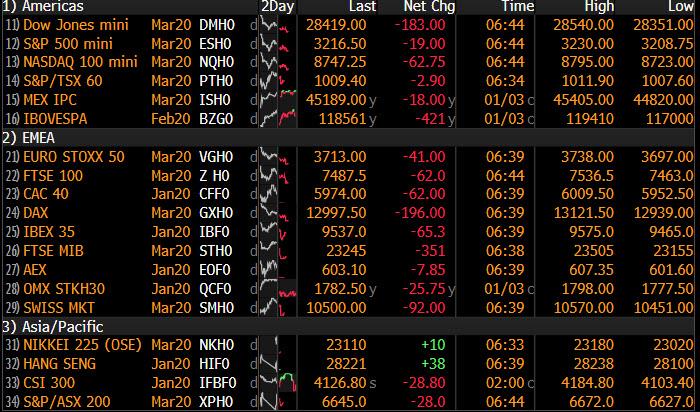

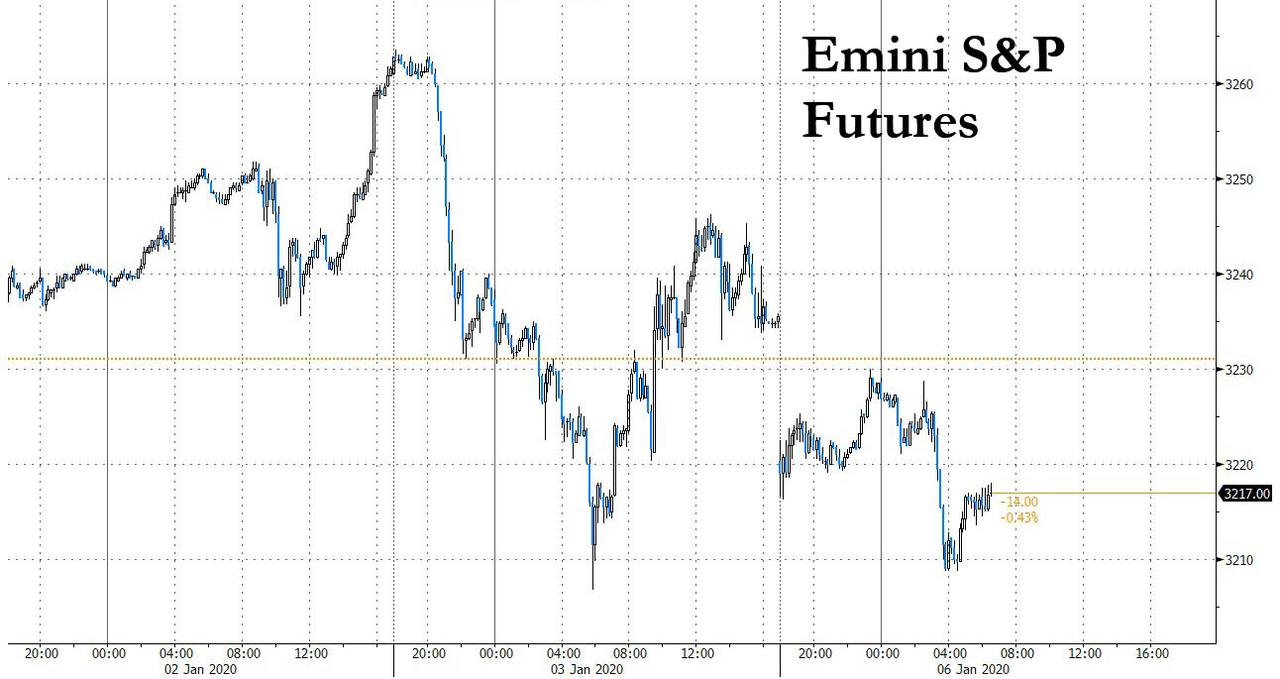

Global markets slumped, and US equity futures tumbled on Monday, wiping out gains for 2020 as tensions in the Middle East soared amid fears of escalation in the Middle East as investors pushed safe-haven gold to a seven-year high, and oil jumped to its highest since September.

The fallout from last week’s targeted US assassination of top Iranian General Qassem Soleimani escalated over the weekend, as the US said it detected a heightened state of alert by Iran’s missile forces (hardly a shock) as President Donald Trump warned the U.S. would strike back, “perhaps in a disproportionate manner”, if Iran attacked any American person or target. Also on Sunday, Iraq’s parliament on Sunday recommended US troops be ordered out of the country, while Trump threatened heavy sanctions on Iraq and said any US troop withdrawal would require Iraq to reimburse the US for billions spent on an air base.

And so, with algos once again looking at geopolitical risk as something more than merely a reason for the Fed to ease further, US equity futures slumped to red for 2020, with Boeing once again dragging down the Dow after a new, potentially “catastrophic” wiring issue was discovered on the 737 MAX…

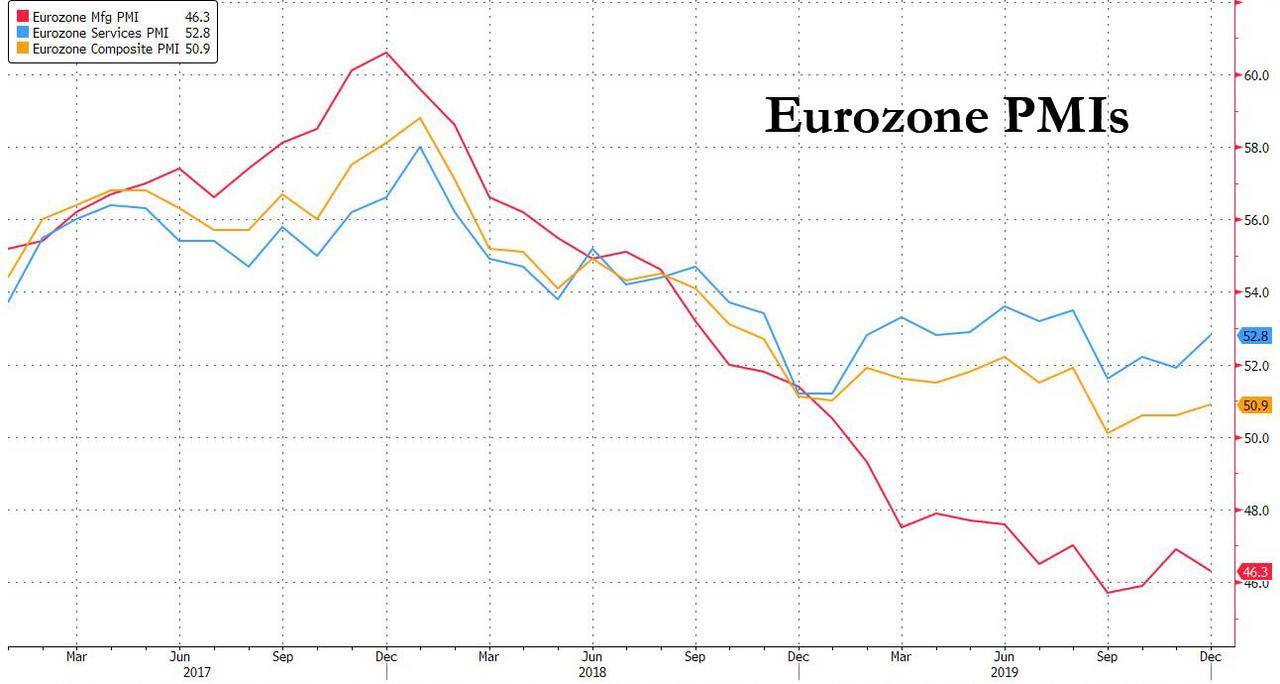

… as European shares extended losses and were set for their worst day in a week, with the European Stoxx 600 index down 1.12%. The European oil and gas stock index rose about 0.74% and was the sole gainer among its peers, hitting its highest since July as Brent briefly topped $70 overnight. Not even the strongest Eurozone Service PMI print since August, which at 52.8 came in well above the 52.4 expected, had any impact on the sudden dour mood.

Earlier in the session, Asian stocks fell, led by health care and consumer staples, as frictions between the U.S. and Middle Eastern countries ratcheted up. The MSCI Asia Pacific Index headed for its biggest drop since Aug. 26, on growing tensions following the killing of Soleimani. In Asia, Japan’s Nikkei slid almost 1.9% in a sour return from holiday, while stocks listed in Hong Kong and mainland China dropped in afternoon trade, with technology-related shares among the worst performers. Chinese shares, which had opened in the red, reversed their losses, as did Australian shares which ended the day flat. Hong Kong’s Hang Seng index lost 0.8%. Most other markets in the region were also down, with India’s S&P BSE Sensex Index and Japan’s Topix Index falling more than 1%.

MSCI’s All-Country World Index was down 0.43%, erasing all its new year gains in its biggest two-day fall since early December.

Naturally, the perpetually optimistic sellside hoped markets would quickly look beyond the recent geopolitical debacle: “Geopolitical events by their nature are unpredictable, but previous periods of increased tensions suggest that the impact on wider markets tends to be short-lived, with more lasting effects confined to local markets,” said Mark Haefele, chief investment officer at UBS Global Wealth Management, adding that “in general, this supports holding a diversified portfolio.”

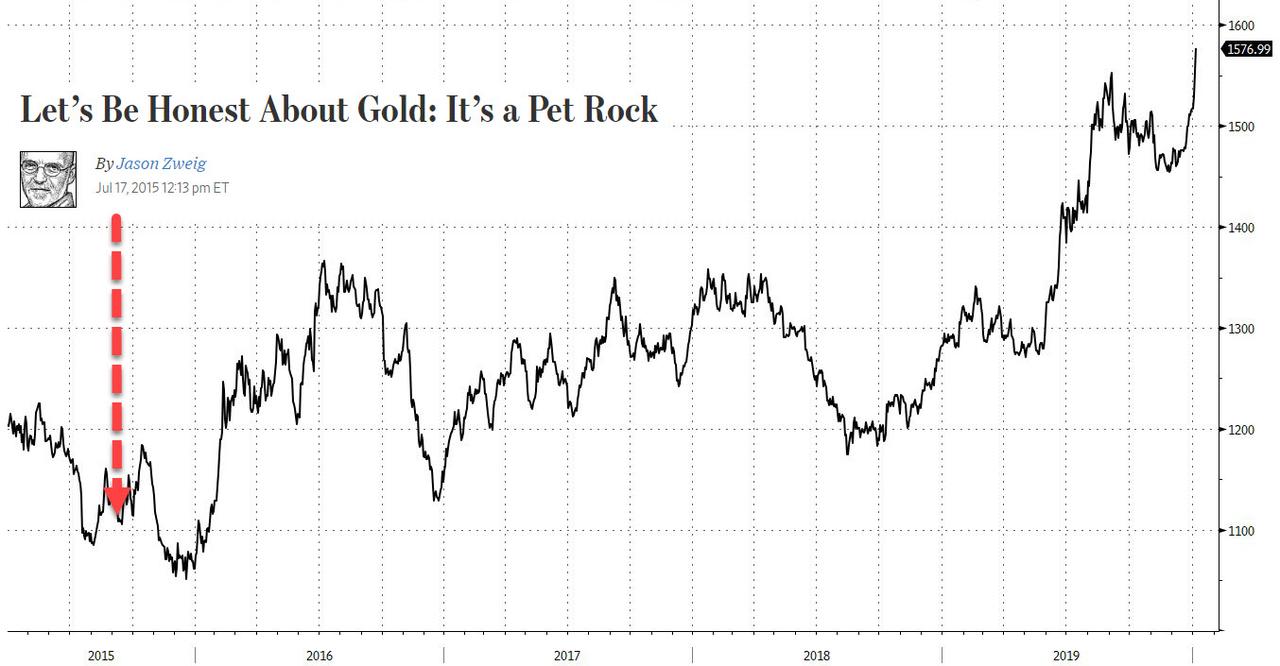

Maybe Haefele will be right, but for now the market is not buying it, with spot gold surging another 1.6% to $1,579.72 per ounce, reaching its highest since April 2013, and making a delightful mockery of certain WSJ commodity “experts.”

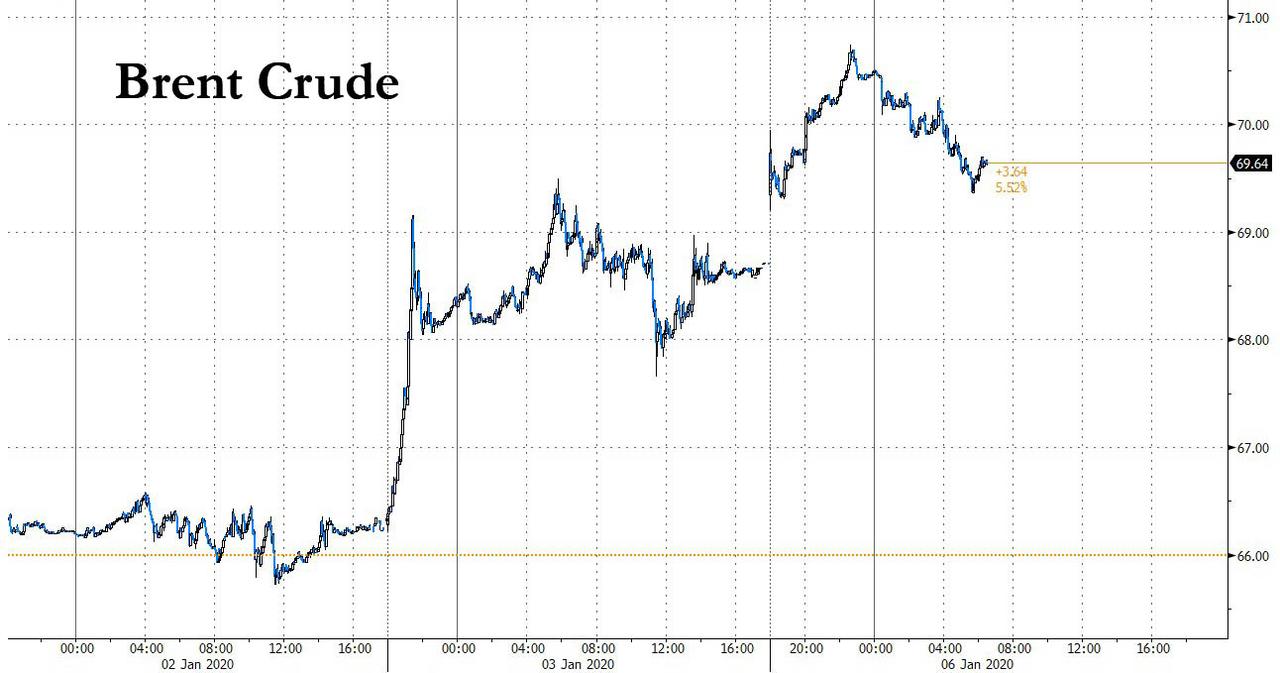

At the same time, oil prices also extended gains on fears any Middle East conflict could disrupt global supplies; Brent futures rose as high as 2% to $70 a barrel, while U.S. crude climbed 1.7% to $64.12.

Commenting on the possible trajectory of oil, Bob McNally, president of Rapidan Energy Group said in a Bloomberg Television interview that potential retaliation for the U.S. killing of Qassem Soleimani could push Brent crude $3-$10 a barrel higher, “we think crude’s going up some more” because there will be further violence as Iran responds to the U.S. attack. “The odds of an overt U.S. military conflict with Iran went from about 5% to about 25%. We think crude has some more risk pricing to do.”

The rapid escalation of tensions in the Middle East continues to damp the enthusiasm that sent the S&P 500 Index to a record on its first trading day of the year. “Everyone got comfortable in that fact that the truce in the trade war had come through and the outlook for 2020 looked a little bit better and then we had another geopolitical reminder come through,” said Suncorp Group Financial Market Strategist Peter Dragicevich. “It’s going to be a big driver of markets in the short term.”

In rates, sovereign bonds benefited from the safe haven bid with yields on 10-year Treasuries down at 1.7725% having fallen 10 basis points on Friday.

In FX, the yen reached its strongest level in three months thanks to Japan’s massive holdings of foreign assets, as investors assume Japanese funds would repatriate their money during a true global crisis, pushing the yen higher. The Bloomberg Dollar index weakened, and the pound gained as the U.K.’s dominant services sector showed signs of strengthening at the end of 2019 following Boris Johnson’s decisive election victory. The euro eased to 120.61 yen having hit a three-week low. The risk sensitive currencies of Australia and New Zealand were on track for their fourth straight session of losses.

“Iran is almost certainly to respond in some scale, scope and magnitude,” said Lee Hardman, currency analyst at MUFG. Therefore “market participants are likely to remain nervous until there is more clarity over how geopolitical tensions between the U.S. and Iran will proceed”, Hardman said, noting that geopolitical tensions could hurt global economic growth, especially if the price of oil increases.

But while investors are having a hard time as they final have to learning to co-exist with an odd red color on their screens, nobody had a worse day overnight than the virtue signallers in Hollywood who were simply crucified by Ricky Gervais’ parting Golden Globes monologue.

On today’s economic calendar, we have the latest Markit services PMI report.

Market Snapshot

S&P 500 futures down 0.8% to 3,209.50

STOXX Europe 600 down 1.3% to 412.76

MXAP down 1% to 170.06

MXAPJ down 0.9% to 551.66

Nikkei down 1.9% to 23,204.86

Topix down 1.4% to 1,697.49

Hang Seng Index down 0.8% to 28,226.19

Shanghai Composite down 0.01% to 3,083.41

Sensex down 1.9% to 40,688.02

Australia S&P/ASX 200 up 0.03% to 6,735.71

Kospi down 1% to 2,155.07

German 10Y yield fell 2.1 bps to -0.299%

Euro up 0.2% to $1.1180

Brent Futures up 1.7% to $69.75/bbl

Italian 10Y yield fell 6.6 bps to 1.177%

Spanish 10Y yield fell 0.4 bps to 0.382%

Brent Futures up 1.7% to $69.75/bbl

Gold spot up 1.6% to $1,577.05

U.S. Dollar Index down 0.1% to 96.71

Top Overnight News from Bloomberg

Iran said on Sunday that it no longer considered itself bound by a 2015 nuclear agreement, while Iraq’s parliament voted to expel U.S. troops from the country

Yen bulls betting the currency will gain in times of stress face one formidable obstacle — Japanese demand for Treasuries. Japanese funds will pounce at every opportunity to buy the dollar cheaply and invest overseas given low domestic bond yields, said Satoshi Nagami, head of global strategies investment group at Sumitomo Mitsui DS Asset Management Co.

The yen’s correlation with the CBOE Volatility Index climbed to the highest in almost three years. Japan’s currency climbed to the strongest since October on Monday after the VIX index jumped last Friday. The correlation between the two has also been increasing as sentiment has swung more wildly in recent months due to global risk events such as the U.S.- China trade war, said Daisaku Ueno, chief currency strategist at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo

Gold surged to the highest level in more than six years, with Goldman Sachs Group Inc. saying bullion offered a more effective hedge than oil to the crisis. Palladium extended gains to an all-time high

BNP Paribas SA is planning to join JPMorgan Chase & Co. and Citigroup Inc. by setting up an electronic currency trading and pricing platform in Singapore. The facility will support electronic trading of 50 currencies in spot, forward, swaps, non-deliverable forwards and options, according to a company statement

Asian equity markets kicked the week off mostly in the red following downside seen on Wall Street on Friday as US-Iran developments and dismal US ISM metrics weighed on sentiment. ASX 200 (Unch) was initially led lower by a bulk of its constituents in negative territory including its largest weighed financial sector, albeit losses were somewhat cushioned by gold miners and energy names as prices in the complexes rose amid the escalating geopolitical tensions, thus the index later pared losses. Meanwhile, Nikkei 225 (-1.9%) underperformed given the recent safe-haven demand in the JPY and as Japanese participants had the first chance to react to the Middle Eastern events after their extended New Year break. Elsewhere, Hang Seng (-0.8%) opened modestly in negative territory but extended losses as heavyweight financial names accelerated downside – with traders attributing the closures of local bank branches due to the protests, albeit the index later climbed off lows as energy names benefitted from the surge in crude prices with oil-giants CNOOC and PetroChina notching gains in excess of 3%. Finally, Shanghai Comp (U/C) oscillated between gains and losses as the overall risk aversion in the market was countered by the tentative dates touted for the US-China Phase One signing and with the PBoC’s RRR cut going into effect today, releasing over CNY 800bln of long-term funds.

Top Asian News

Hong Kong Parents Eye Singapore Schools as Wild Protests Endure

Schuldschein Sets Record For the Third Consecutive Year in 2019

India Stocks Extend Drop as Oil Jumps on U.S.-Iran Rhetoric

Philippines Prepares to Evacuate Citizens in Middle East

European bourses are subdued this morning (Stoxx 50 -1.3%), as geopolitical tensions in the Middle-East weighs on price actions at present. An update on the Iranian situation is available in the Commodity section below. Indices are all in negative territory at present in Europe, with US futures painting a similar picture as well; price action this morning has seen the Dax and Stoxx 50 futures test key levels to the downside, with the Dax having convincingly given up the 13000 mark and the Stoxx 50 testing the 3700 handle on multiple occasions. In terms of sectors, it’s a similar story to Friday, with all sectors in negative territory aside from Energy which continues to benefit from the inflated oil prices; which is, in turn, assisting oil names such as BP (+1.8%) and Shell (+1.2%), and is helping to stem some of the FTSE 100’s losses – although, the bourse is firmly in negative territory. Turning to other notable movers, at the other end of the spectrum from the outperforming oil names, flight names such as Ryanair (-4.4%) and Air France (-3.8%) are weighed on by the crude market. Elsewhere, Metro AG (-5.0%) are suffering after a downgraded at JP Morgan, while ASML (-3.5%) are afflicted on reports that US President Trump’s Administration implemented a campaign to prevent the sale of the Co’s technology to China; do note, this reportedly began in 2018 and as such the significance and current situation may well have changed given the US-China trade war.

Top European News

Euro Zone Edges Away From Stagnation as Services Improve

U.K. Services Get Boost From Election as New Orders Increase

Takeaway Nears Final Victory in $8 Billion Just Eat Battle

European Car Stocks Fall as U.S., U.K. Auto Markets Weaken

In FX, the Pound was already benefiting from broad Dollar weakness amidst escalating US-Iran tensions and in wake of last Friday’s dire manufacturing ISM, but Cable derived some independent impetus from the final UK services PMI that beat consensus in contrast to manufacturing and construction, albeit only reclaiming the 50 level on post-GE relief that did not factor in the preliminary survey. Cable is hovering just shy of 1.3175 compared to lows circa 1.3064, and Eur/Gbp threatening 0.8500 bids even though the single currency also gleaned encouragement from largely firmer than forecast or flash Eurozone services PMIs and a more upbeat than anticipated Sentix index. Indeed, Eur/Usd is inching towards 1.1200 vs sub-1.1160 and further from very early 2020 lows under 1.1125.

CHF/CAD/NZD/AUD/JPY – Also firmer against the Greenback, as the DXY slips towards 96.500, with the Franc crossing 0.9700, Loonie eying 1.2950, Kiwi hovering around 0.6675 and Aussie back above 0.6950. However, the Yen is still finding 108.00 too tough to breach as Japanese markets return from their long New Year holiday and contacts suspect a major player is propping the headline pair.

NOK/SEK – More divergence between the Scandi Crowns, as Eur/Nok repels risk-off rebounds ahead of 9.9000 with the aid of oil’s ongoing rally, but Eur/Sek struggles to cap advances beyond 10.5000 and Nok/Sek extends its advance towards 1.0700 after breaking strong chart resistance below 1.0500.

EM – Risk aversion has prevented many regional currencies from taking advantage of general Buck underperformance, but the Rouble is also getting a boost from Brent and Rand has managed to overcome more Eskom power issues to bounce back above 14.3000 on what appears to be mainly technical grounds.

In commodities, WTI and Brent prices remain elevated on Iranian-US tensions, with prices higher by just shy of a USD 1.0/bbl at present; as crude prices have drifted off of their overnight highs as sentiment continues to deteriorate but the ferocity of newsflow has reduced as mourning proceedings are underway in the Middle-East for Soleimani. Weekend reports highlight that Iran has finalised a retreat from the nuclear deal, and will not be complying with any of the restrictions set out within this; additionally, Iraqi parliament has voted to begin developing plans to end the presence of US troops in the country. For reference, an analysis piece which outlines the impact on oil prices from the ongoing situation is available on the Newsquawk headline feed. The key views are JP Morgan believing that the stress on oil supply will be bearable, looking ahead focus is on whether the situation will disrupt supplies with UBS noting, at a minimum, US assets in the area are at risk – as is the broad infrastructure for oil supply in the region. Separately, ING posit that any substantial increase in crude prices could see US President Trump authorise use of the SPR, which currently has around 635mln barrels of supply. For reference, in 2018 the US consumed on average 20.5mln BPD, given this consumption rate this implies self-sufficiency for the US of roughly one month; excluding additional US production which last week stood at 12.9mln barrels and would significantly extended such a period of self-sufficiency. In terms of metals, spot gold is well supported on the aforementioned tensions with the precious metal having printed a high just over USD 1587/oz overnight, which is a 6-year high for the safe haven. Price action picked up once the USD 1557/oz mark was surpassed, with contacts noting a number of stops were likely present around this figure. Additionally, the yellow metal will be gleaning support from a softer dollar this morning, with the DXY having printed multiple fresh session lows throughout the session.

US Event Calendar

9:45am: Markit US Services PMI, est. 52.2, prior 52.2

9:45am: Markit US Composite PMI, prior 52.2

DB’s Jim Reid has returned from vacation, and concludes the overnight wrap:

As I left for my hols before Xmas I received the seasonally uplifting message from our CEO wishing us all a happy holiday and imploring us to fully recharge our batteries ahead of starting back in January. Well on my first day back today my brain has just flashed up “5% battery – do you want to go into low power mode”. We had an awful 2-week holiday. My wife was in bed for 70% of it with severe flu and still was yesterday. I had a constant bad cough and the children took it in turns to be on industrial strength calpol. Bronte has applied for emancipation. I’ve been longing to return to work to recover and now my dreams have been fulfilled.

Already in the two business days this year markets have been up and down like me in the night on holiday administering medicine to the troops. In today’s EMR we’ll review some of the main action at the back end of last week and also include some bullets as to the major stories you may have missed over the Xmas/NY period if you’ve only just returned from holiday. A reminder that Henry put out the December, Q4, 2019 and full decade multi-asset returns last week (link here).

First lets have a quick look at what we can expect from this first full week of the new decade. Obviously it will be dictated by the seismic events surrounding Iran and the US (more later) but outside of this it’s not the busiest week for data but there are some key highlights still with today’s global services and composite PMIs, tomorrow’s US non-manufacturing ISM and Friday’s US payrolls (after last month’s surprise bumper print) being the main ones. On payrolls, the consensus is +167k, with the unemployment rate expected to remain at 3.5%, its joint lowest since 1969. This follows some fairly strong US employment data recently, with nonfarm payrolls growing by +266k in November, the most since January, while the 3-month moving average also rose above +200k for the first time since January. The full day by day week ahead is at the end.

Bringing you up to speed with markets over the holiday season and in 2020 to date now. Equities finished 2019 at record highs, with the S&P 500 up +28.88% over the year, its strongest annual performance since 2013, while in Europe the STOXX 600 was up +23.16%, its best year since 2009. Markets then had a bumper opening day of the decade on Thursday as Trump suggested he’d sign the phase one deal on January 15th and China announced an interest rate cut (see bullets below).

However, markets were soon knocked off their perch on Friday by the news that a US airstrike had killed the Iranian military commander Qassem Soleimani. In response, Iran’s Supreme leader Ayatollah Ali Khamienei said that “severe retaliation” awaited his murderers, raising fears over the potential for further escalation between the two sides. However, US President Trump said later on that “We took action last night to stop a war. We did not take action to start a war.” The remarks that the US wasn’t looking for conflict chimed with those by US Secretary of State Mike Pompeo, who tweeted on Friday that in a conversation with Russian foreign minister Sergei Lavrov, “I emphasized that de-escalation is the United States’ principal goal.” However the stakes were raised again on Saturday as Trump identified 52 Iranian sites the US would hit if Iran retaliates. Meanwhile on Sunday the Iraqi government voted to expel US troops from the country after a near 17 year period of presence there since the toppling of Saddam Hussein in 2003. In response, Trump said that US troops won’t leave without billions in payment for their base there – or if they do leave Trump would apply sanctions. Also the Iranian government said it no longer considers itself bound by the limits on the enrichment of uranium. Most importantly though we’re left waiting to see if we get an aggressive response from Iran with the whole Middle East likely feeling vulnerable. The US State department said on Sunday that there was ‘heightened risk’ of missile attacks near military bases and energy facilities in Saudi Arabia.

Meanwhile, Esmail Ghaani, the successor to Soleimani, said in an interview with Iranian state television aired today that “Certainly actions will be taken”. He also said that, “We promise to continue down martyr Soleimani’s path as firmly as before with help of God, and in return for his martyrdom we aim to get rid of America from the region.” So, a nervous time awaits markets. Elsewhere, NATO ambassadors are due to meet today in Brussels to discuss the situation in the Middle East.

Away from geo-politics, the SCMP reported over the weekend that the Chinese trade delegation tentatively plans to travel to the US on January 13 for the signing of the phase one deal.

This morning in Asia, crude oil continues to be a key mover with brent (+2.73%) and WTI (+2.38%) oil prices both up a further 2% after Friday’s c. 3% gain (see below). Meanwhile, most Asian markets are trading in the red with the Nikkei (-1.75%) leading the declines as it trades for the first time in 2020 after the holidays. The Hang Seng (-0.52%) and Kospi (-0.80%) including India’s Nifty (-1.10%) are also down while Chinese bourses (Shanghai Comp +0.63%) are up likely on the SCMP news mentioned above. In the Middle East, Saudi Arabia’s Tadawul index (-2.42%), Qatar’s Ex index (-2.14%), UAE’s DFM General (-3.06%), Kuwiat’s KWSE Premier Mkt (-4.07%) and Israel’s Tel Aviv 35 (-0.55%) were all down yesterday. As for Fx, most Asian currencies are trading weak this morning with the currencies of oil importing countries down. Elsewhere, futures on the S&P 500 are down -0.28% while 10yr treasury yields are down a further -1.6bps to 1.773% this morning. As for overnight data releases, Japan’s final December manufacturing PMI came in at 48.4 vs. 48.8 (flash) while China’s December Caixin services PMI came in at 52.5 (vs. 53.2 expected) and the composite PMI stood at 52.6 (vs. 53.2 in last month).

As the news of the US strike broke on Friday the biggest impact was seen in oil, with Brent crude up +3.55% on the day, bringing it to $68.60 per barrel, its highest closing level since just after the drone strike on Saudi oil facilities in September, while WTI also ended the session up +3.06%. Investors fled to safe havens elsewhere, with gold up +1.51% in its biggest daily rise since August, while the Japanese Yen was the strongest performing G10 currency on Friday, up +0.449% against the US Dollar. Equities sold off in response, with the S&P 500 (-0.71%), the NASDAQ (-0.79%) and the Dow Jones (-0.81%) all losing ground, while sovereign debt rallied, with 10yr Treasury yields down -8.9bps to 1.788% having touched 1.944% on Thursday. 10yr bunds closed the week at -0.284% having hit -0.16% (the highest since May) early on Thursday. MSCI’s emerging markets Europe, Middle East and Africa index declined by -0.78% on Friday.

Matters were not helped on Friday by the ISM manufacturing index from the US coming in at 47.2 in December (vs. 49.0 expected), which was the worst reading since June 2009 and below every estimate on Bloomberg. Looking at the index in more detail provided little encouragement, with the employment reading down to 45.1, the lowest since January 2016, new orders falling to 46.8, the lowest since April 2009, and production down to 43.2, also the lowest since April 2009. In terms of other data out Friday, the preliminary reading for German CPI rose to +1.5% (vs. +1.4% expected) in December, its highest level since June on the EU harmonised measure. However, unemployment rose by +8k in December (vs. +4k expected) but at still very low levels.

Finally from the Fed, we got the minutes on Friday from the FOMC’s December meeting, where rates were kept on hold following 3 consecutive 25bp cuts at the previous meetings. The overall takeaway, in line with the median dot showing policy remaining unchanged in 2020, is that “participants regarded the current stance of monetary policy as likely to remain appropriate for a time as long as incoming information about the economy remained broadly consistent with the economic outlook.” In a somewhat dovish note, the minutes said that “While many saw the risks as tilted somewhat to the downside, some risks were seen to have eased over recent months.” So it’s interesting that the risks are still seen as tilting to the downside. Other somewhat dovish points were that “Participants generally expressed concerns regarding inflation continuing to fall short of 2 percent”, and also that “various participants remarked that there were some indications that further strengthening in overall labor market conditions was possible without creating undesirable pressures on resources.” Thursday this week is a big day for Fed speak with Clarida, Williams, Evans and Bullard speaking.

Before the day-by-day week ahead, for those of you who are returning today and need a recap of other major events that have happened in the last two weeks since the EMR last appeared in your inboxes here’s the run-down of the main stories:

China: The People’s Bank of China lowered the required reserve ratio for banks by 50bps, helping to support domestic liquidity. Our China economics team released a note last week about the issue (link here), but they also write that the space for further cuts in the required reserve ratio “is becoming increasingly limited”, and their base case is that the PBoC won’t cut the RRR further in 2020.

US-China trade: President Trump announced that he would sign the Phase One US-China trade deal at the White House on January 15th. He also tweeted that “At a later date I will be going to Beijing where talks will begin on Phase Two!”

Brexit: UK MPs voted in favour of the Withdrawal Agreement Bill at second reading, which is the bill that ratifies the Brexit deal into UK law. MPs will be resuming debate tomorrow, though thanks to the Conservatives’ 80-seat majority following the election, the bill is expected to pass through the House of Commons easily. European Commission President Ursula von der Leyen will be meeting with Prime Minister Johnson on Wednesday.

North Korea: Kim Jong Un announced he would be introducing a “new strategic weapon”.

France: Strikes have continued over reforms to public sector pensions, with President Macron refusing to back down on the proposals. Bloomberg has now reported that unions are aiming for a fourth day of nationwide protests on January 9 and a fifth on January 11. The far-left CGT union is pushing to escalate the demonstrations, calling for a complete blockade of the country’s refineries from January 7 to 10. Elsewhere, a survey conducted Thursday and Friday by pollster Ifop and published on Sunday found that 44% support the strikers, down from 51% just before Christmas.

Spain: Following November’s inconclusive general election, Prime Minister Sanchez got the agreement he needed to form a new government after one of the Catalan separatist parties agreed that they would abstain in a confidence vote. Along with other abstentions, this means that Sanchez’s new coalition government between his Socialist Party and Podemos will be able to win a simple majority vote in parliament.

Data: Not much of significance to report over the last two weeks. The US data included the Conference Board’s consumer confidence reading coming in at 126.5 in December (vs. 128.5 expected). The preliminary durable goods orders reading for November was also worse than expected, down -2.0% (vs. +1.5% expected), as were new home sales in November at a seasonally-adjusted annual rate of +719k (vs. +732k expected). The final Euro Area manufacturing PMI for December was revised up to 46.3 (vs. flash 45.9), with the German reading revised up to 43.7 (vs. flash 43.4). However, the Italian reading fell to 46.2, its lowest level since April 2013. Meanwhile in the UK, the final reading of Q3 GDP was revised up to +0.4% qoq (vs. 0.3% in the prior estimate).

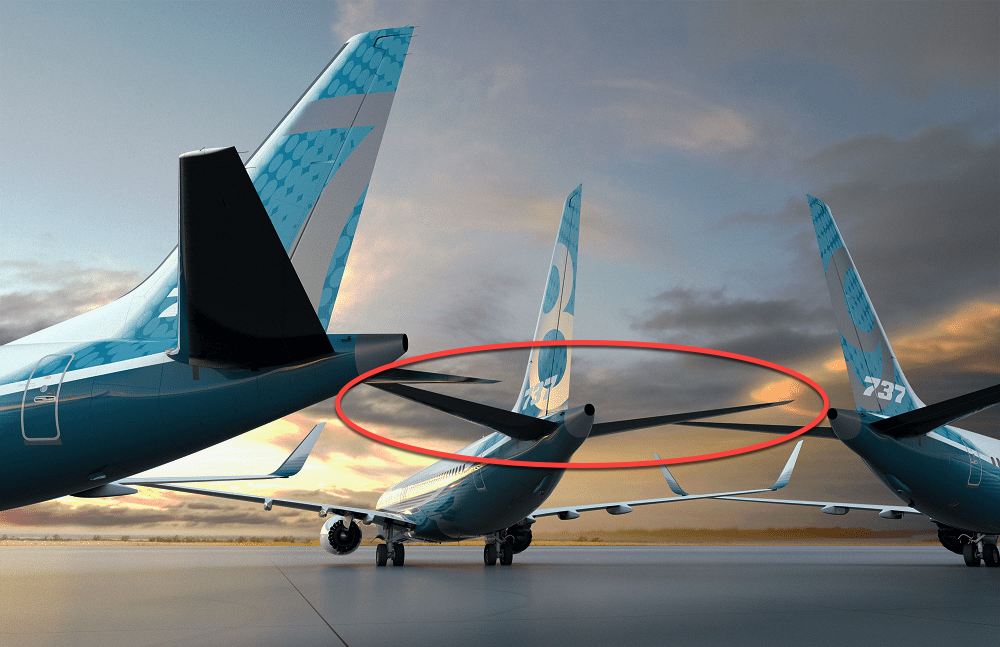

New, Potentially “Catastrophic” Wiring Issues Found In Boeing 737 Max

As if Boeing needed any more bad news.

The Federal Aviation Administration (FAA) conducted an internal audit in December of the Boeing 737 Max and found wiring issues could potentially cause a “catastrophic” short circuit at the rear of the plane and lead to a crash, a senior engineer at Boeing and three people familiar with the matter told The New York Times.

Boeing is examining if two wiring harnesses at the rear of the plane are too close together that would result in an electric short that would cause the plane’s tail to malfunction in flight, said one of the sources.

If Boeing decides to fix the wiring problem, it would mean that more than 800 Max jets would have to see wiring reconfiguration.

Of course, Boeing told The Times that the fix is relatively simple. Spokesman Gordon Johndroe said Sunday the “identified issue is part of a rigorous process, and we are working with the FAA to perform the appropriate analysis. It would be premature to speculate as to whether this analysis will lead to any design changes.”

It was unclear, however, if simple also means cheap, and some have speculated that a full-blown recall could cost tens ofd billions.

An FAA statement Sunday said investigators are “re-analyzing certain findings from a recent review of the proposed modifications to the Boeing 737 MAX.” The agency will “ensure that all safety-related issues identified during this process are addressed.”

The FAA said the wiring harnesses are too close together, located at the rear of the plane, would cause the motors that control the stabilizer, a horizontal fin on a plane’s tail, to malfunction (short circuit) and could lead to a potentially “catastrophic” crash.

Max engines have also become another focus for FAA investigators.

RE: Boeing 737 Max

Anyone who missed this post back in March should read throughly. The issue with the 737 Max is not a software issue, it’s a design issue. Boeing got desperate when Airbus released the NEO, so they too wanted a big engine. Merry Christmas $ba.d$bahttps://t.co/3I8z0p6ljn

All of these issues, of course, are separate from the MCAS software that was likely the cause of two separate Max crashes, killing 346 people. New Max issues could delay the ungrounding even further. There is no clear timeline of when the planes will return to the air.

Meanwhile, confirming that things are going from bad to worse, the WSJ reported that Boeing is mulling raising more debt to “improve finances”, read fund buybacks, as costs related to the grounding of its 737 MAX are raising. The paper reports that Boeing is also considering cutting CAPEX, freezing acquisitions and cutting on R&D to save cash. In total, analysts expect Boeing to raise as much as $5BN in additional debt to help cover expenditures that could rise to $15BN in 1H 2020. It was not clear if all of this new money, or just most of it, would to repurchasing BA shares.

Labour Party Formally Begins Process Of Replacing Corbyn On Monday

Fulfilling Jeremy Corbyn’s promise to step aside following last month’s historic shellacking at the hands of Boris Johnson’s Conservatives (Labour recorded its worst parliamentary showing since before WWII), the Labour Party will formally begin its leadership contest on Monday, Bloomberg reports.

As the contest begins, the remaining members of Labour’s centrist wing (or at least, those who oppose Corbyn’s brand of left-wing populism) have taken to the British press to express their reservations about the prospects of the Labour Party, which is still controlled by the same people who have assiduously backed Corbyn at every turn, electing, in essence, another Corbyn.

Over the weekend, Tom Watson, the former Labour deputy leader, declined to name his pick for the party leadership, but warned that the prospect of the party backing Rebecca Long Bailey, the shadow business secretary under Corbyn, made him extremely worried, according to the Guardian. He attacked her as the “continuity candidate…”

“The one that I worry about – but I don’t know what she stands for – when I look at Rebecca Long Bailey, she’s really the continuity candidate. She stands for Corbynism in its purest sense. And that’s perfectly legitimate but we have lost two elections with that play.

…while also acknowledging the possibility that Long Bailey could choose a more moderate tack if/when she announces her campaign.

“She hasn’t said anything yet; as far as I know she has not formally announced and it might be that she chimes a different note in her opening bid and that she wants to take the party in a different direction and she’s very candid about what went wrong, in which case then she’s in quite a good position to shift things around. But I think it’s fair for me to reserve judgment.”

So far, Labour Shadow Brexit Secretary Keir Starmer (the frontrunner according to the polls) has been the only one of the top-polling candidates to throw his hat into the ring. Starmer, whose leadership of the pro-remain faction in the House of Commons often put him at odds with Corbyn, according to Bloomberg, is polling at 36%, comfortably ahead of Bailey, who came in second, according to the polls.

Though in his launch campaign video, Starmer appeared to try and pitch himself as a natural successor to Corbyn, arguing that the party should “build on” Corbyn’s anti-austerity message and radical socialist agenda.

I believe another future is possible – but we have to fight for it.

That’s why I’m standing to be leader of the Labour Party.

While reporters wait for more candidates to announce, Labour’s National Executive Committee will meet on Monday to set the parameters for the contest, including how much support a candidate needs to qualify for the ballot, and the timetable for the contest, including, crucially, the cut-off point for new members to join if they want to have a vote.

Eventually, a vote will be held among party members to elect the new leader.

During the last two contests, the party membership overwhelmingly backed Corbyn, prompting some MPs to leave the party over Corbyn’s perceived history of antisemitism, as well as his radical agenda, which includes extending public broadband access to all British households.

Starmer is expected to face three women during the leadership contest: Bailey, MP for Birmingham Yardley Jess Phillips (who has declined to rule out the possibility of Labour pushing to rejoin the EU) and Lisa Nandy, the MP from Wigan, who recently told Sky News that “there is definitely a disconnect between the hierarchy of the Labour Party and the people of the country and towns like mine.”

Which is reassuring. Understanding this key fact – which was proven incontestably during the election – should be a prerequisite for entering the contest.

Russia has halted oil supplies to Belarus amid a disagreement over tariffs, according to officials at a Belarusian oil refinery in the northern city of Navapolatsak.

The officials told RFE/RL that the shipments stopped on January 1 and the facility is currently processing only Russian oil delivered before that date.

Belarus has been at odds with Russia over oil-transit prices for some time against a backdrop of increasing pressure by Moscow on Belarusian President Alyaksandr Lukashenka to deepen integration between the two countries.

A two-month deal on natural-gas prices hours before a December 31 deadline helped the sides avoid a gas shutoff to start the year.

Belarus is heavily reliant on Russia for fuel and funding and is a key transit route for Russian energy supplies to Europe. And now, Russia has just broken a new oil production record.

Moscow and Minsk signed an agreement in 1999 to form a unified state, but little progress has been made in the ensuing two decades.

Meetings between Russian President Vladimir Putin and Lukashenka last year failed to bring the two sides together as the Belarusian president complained he was merely seeking “equal” terms.

Belarusian protests in December targeted the perceived secrecy of the talks and objected to closer ties to Russia.

Mike Pompeo this week postponed a planned visit to Minsk to meet with Lukashenka in what would have been the first visit by a U.S. secretary of state to that post-Soviet country in a quarter century.

Prediction Consensus: What The ‘Experts’ See Coming In 2020

Through the ages, humans have feared uncertainty. We’ve searched for clues in everything from entrails to tea leaves to the arrangement of heavenly bodies in the night sky.

In the modern era, data and media are the new magic 8-ball. The jury is still out on whether we’ve gotten any better at anticipating the forces that will shape the coming year, but that certainly hasn’t stopped people from trying.

Of the hundreds of forward-looking pieces of content published in the lead-up to 2020, how many of the expert predictions lined up? Was there a consensus on any particular trend, or were predictions all over the map?

During the month of December, Visual Capitalist’s Nick Routley analyzed over 100 articles, whitepapers, and interviews to answer that question. While there was no firm consensus on where 2020 will take us, there were a few themes that appeared in multiple publications. Today’s graphic highlights these reappearing predictions, and below, we examine seven of them in more detail.

The Promise and Controversy of 5G

One technology that’s sure to capture the headlines in 2020 is 5G. Broadband speeds of over one gigabit per second will become a reality when 5G technology rolls out across the country, without the cable that currently connects most homes. This prediction is a slam dunk, as some carriers are already testing the technology in select neighborhoods around the United States.

Experts also predict that a wave of 5G-enabled smartphone and IoT products will become commercially available in 2020.

The wild card in this 5G story will be guessing which companies end up building out the new network. Huawei was in a strong position to lead the charge, but the company has been stonewalled in a number countries – most notably the United States, Australia, and Japan. Whether due to national security concerns or protectionism, Chinese companies may continue to face an uphill battle in Western markets.

Fake News 2.0

While many predictions for 2020 were fueled by excitement for new technologies, there was one that was decidedly more ominous – the proliferation of deepfakes. Simply put, deepfakes are videos that harness artificial intelligence to create a convincing likeness of a real person.

With the U.S. presidential election just around the corner, many experts fear that deepfakes are going to do serious damage, manipulating public opinion on both sides of the political spectrum. Unlike fake news, which often comes with obvious visual cues to help determine authenticity, even deepfakes created using free online tools are extremely convincing. If predictions come true, the lead-up to the U.S. election could be a wild ride.

Consumerism in Flux

The late 2010’s were a turbulent time for retail. The rise of ecommerce and shifting consumer preferences combined to cause a “retailpocalypse”, and many brands are still struggling to evolve their brick and mortar strategy to compete in an Amazon Prime world. Experts are predicting new evolutions for physical stores that are powered by technology instead of human employees.

The incarnation of this approach that will likely garner the most attention will be the next wave of cashierless Amazon Go locations opening in cities around the country.

Experts also predict that brands will mimic the example of Amazon’s Whole Foods, and incorporate online order pick-up locations within their physical stores. Increasingly, the line between ecommerce and traditional retail is blurring.

The Cookie Begins to Crumble

In 2019, approximately $330 billion was spent on digital advertising, but privacy regulations such as GDPR and the CCPA – California’s new privacy law – are causing massive disruption and upheaval in this industry.

For many years, the humble internet cookie has done the heavy lifting in collecting your personal data from online activity. This data is what advertisers use to reach you as you scroll Instagram or read articles online. Already, changes to Safari and Firefox wiped out about 40% of all third-party cookies, and in a world where people need to physically click a button on each site to allow cookies, it’s unclear how viable the technology will be as privacy measures are enacted.

The Call of the Picket Fence

One of main predictions going into 2020 is that starter homes will be a leading category in new home builds. For millions of millennials around the country in the rental market, a starter home – the first residence a person or family can afford to purchase, often using a combination of savings and mortgage financing – will begin to look more appealing.

Rent in American cities has been marching upward for nearly a decade, and the promise of more space and entry into the home ownership market may lure more of this generational cohort to the suburbs.

Also on the topic of real estate, a few experts noted that even if there is an economic downturn in 2020, the housing market is unlikely to take a big hit.

All Eyes on IPOs

Despite experiencing a rough patch in 2019, SoftBank and its gargantuan Vision Fund will remain one of the most powerful forces in Silicon Valley this year. Masayoshi Son, Softbank’s enigmatic CEO, appears to have adopted a more pragmatic approach, citing a company’s “ability to turn a profit in the future” as a yardstick of evaluating the value of an investment.

Experts predict that in light of the very public PR disasters of unicorns Uber and WeWork, investors will be much more skeptical of high-valuation IPOs.

In 2020, more companies are predicted to opt for a direct listing to go public.

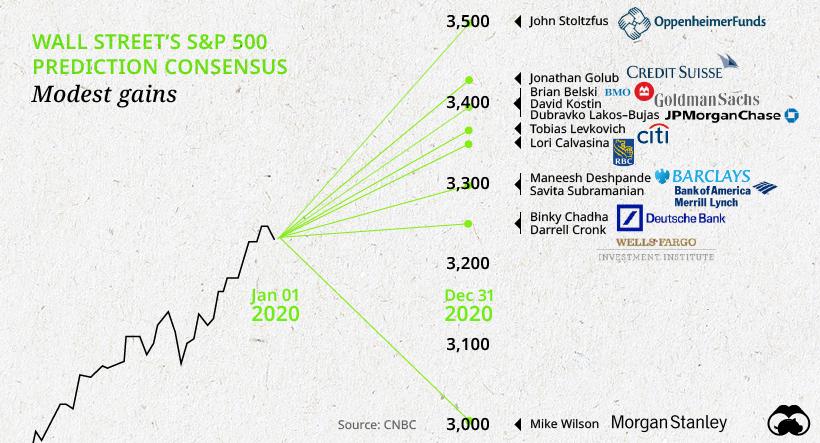

What Goes Up?

When the ball dropped to usher in 2019, market sentiment was leaning toward an impending recession. A year later, the economic expansion is still underway, and many experts now have a more positive outlook for 2020.

The majority of predictions we analyzed foresaw a year of continued job growth and modest gains in the stock market. Here’s a look at S&P 500 end target predictions from some of Wall Street’s top strategists:

The Elephant in the Oval

One prediction nobody seemed particularly keen to make was on the result of the impending U.S. presidential election.

Experts are likely happy to take a wait-and-see approach until the Democratic nominee is announced. Also looming in the back of people’s minds might be the memory of 2016, which was a powerful reminder that even predictions that seem like a sure thing don’t always pan out as expected.

[Experts] can’t predict the markets with any useful consistency, any more than the gizzard squeezers could tell the Roman emperors when the Huns would attack.

The German government said Friday that the United States had reason to strike and kill a the top commander of the Iranian Quds Force late Thursday in Baghdad after the Iranian regime provided support to its militias that targeted U.S. citizens and facilities in Iraq.

The surprise support from Germany on the targeted killing of Iranian Quds Force Gen. Qassem Soleimani was validated by German government spokeswoman Ulrike Demmer in a statement that was posted on Twitter by U.S. Ambassador to Germany Richard Grenell.

Grenell has long stressed the need for European partners to get on the same page with the United States regarding Iran and has worked extensively behind the scenes to push German officials to support U.S. policy on the issue.

“The American action was a reaction to a series of military provocations for which Iran is responsible,” said Demmer.

German government spokeswoman Ulrike Demmer, “The American action was a reaction to a series of military provocations for which Iran is responsible.”

Moreover, German officials have been well aware of the extensive reach of the Iran Quds Force and its umbrella agency the Iranian Revolutionary Guard operations, which works directly under the authority of the Iranian regime.

For example, in January, 2019 Germany revoked the license of Iranian airliner Mahan Air, after evidence revealed it provided support, including financial, to Iran’s Islamic Revolutionary Guards (IRGC).

Grenell was instrumental in working with the German government to ensure that the Iranian airliner’s license was revoked.

At the time, a German foreign ministry spokesman said his nation, “revoked the license of an Iranian airline because it has been transporting military equipment and personnel to Syria and other Middle East war zones.”

While the British monarch appeared on the Most Admired list for the 51st time in 2019, she said it was a “bumpy” year in her annual Christmas speech.

“The path, of course, is not always smooth, and may at times this year have felt quite bumpy, but small steps can make a world of difference,” she said, talking about the need for compassion and understanding.

Many inferred she was referring to Brexit (or perhaps her son Andrew’s debacle). To much controversy and debate, the United Kingdom is slated to withdraw from the European Union no later than January 31, 2020.

Martha Bulus, a Nigerian Catholic woman, was going to her bridal party when she was abducted by Islamic extremists of Boko Haram. Martha and her companions were beheaded and their execution filmed. The video of the brutal murders of these 11 Christians was released on December 26 to coincide with Christmas celebrations. It is reminiscent of the images of other Christians dressed in orange jumpsuits bent on their knees on a beach, each being held by a masked, black-clad jihadist holding a knife at their throats. Their bodies were discovered in a mass grave in Libya.

On the scale of Nigeria’s anti-Christian persecution, Martha was less fortunate than another abducted girl, Leah Sharibu, who has now been in captivity nearly two years and just spent her second Christmas in the hands of Boko Haram. The reason? Leah refused to convert to Islam and deny her Christianity. Nigerian Christian leaders are also protesting the “continuous abduction of under-aged Christian girls by Muslim youths…”. These girls “are forcefully converted to Islam and taken in for marriage without the consent of their parents”.

Nigeria is experiencing an Islamist war of the extermination of Christians. So far, 900 churches in northern Nigeria have been destroyed by Boko Haram. U.S. President Donald J. Trump was informed that at least 16,000 Christians have been killed there since 2015. In one single Nigerian Catholic diocese, Maiduguri, 5,000 Christians were murdered. How much bigger and more extended must this war on Christians become before the West considers it a “genocide” and acts to prevent it?

The day after Christians were beheaded in Nigeria, Pope Francis admonished Western society. About beheaded Christians? No. “Put down your phones, talk during meals”, the Pope said. He did not speak a single word about the horrific execution of his Christian brothers and sisters. A few days before that, Pope Francis hung a cross encircled by a life jacket in memory of migrants who lost their lives in the Mediterranean Sea. Last September, the Pope unveiled a monument to migrants in St. Peter’s Square, but he did not commemorate the lives of Christians killed by Islamic extremists with even a mention.

Cardinal Robert Sarah, one of the very few Catholic Church leaders who mentioned the Islamic character of this massacre, wrote, “In Nigeria, the murder of 11 Christians by mad Islamists is a reminder of how many of my African brothers in Christ live faith at the risk of their own lives.”

It is not only the Vatican that is silent. Not a single Western government found time to express horror and indignation at the beheading of Christians. “Where is the moral revulsion at this tragedy?”, asked Nigerian Bishop Matthew Kukah after the Christmas massacre. “This is part of a much wider drama we are living with on a daily basis”.

European leaders should follow the example of British Prime Minister Boris Johnson, who, in his first Christmas message to the nation said:

“Today of all days, I want us to remember those Christians around the world who are facing persecution. For them, Christmas Day will be marked in private, in secret, perhaps even in a prison cell”.

German Chancellor Angela Merkel has said that her priority will be fighting climate change. She did not mention persecuted Christians. French President Emmanuel Macron in his mid-winter speech was not even able to say “Merry Christmas“.

Meanwhile, The Economistwrote that Hungarian Prime Minister Viktor Orbán, a passionate defender of persecuted Christians, politically “exploits” the issue.

Europe’s leaders failed to condemn the barbaric execution of Christians on Christmas Day: political correctness is corroding Western society from within.

At the beginning of December, another African bishop, Justin Kientega of Burkina Faso, said: “Nobody is listening to us. Evidently, the West are more concerned with protecting their own interests”.

“Why is the world silent while Christians are being slaughtered in the Middle East and Africa?”, wrote Ronald S. Lauder, president of the World Jewish Congress.

“In Europe and in the United States, we have witnessed demonstrations over the tragic deaths of Palestinians who have been used as human shields by Hamas, the terrorist organization that controls Gaza. The United Nations has held inquiries and focuses its anger on Israel for defending itself against that same terrorist organization. But the barbarous slaughter of thousands upon thousands of Christians is met with relative indifference”.

Where were the Western governments when thousands of young Muslims entered Syria and Iraq to hunt and kill Christians and destroy their churches and communities? The West did nothing and suffered for its inaction. The Islamists started with Christians in the East and continued with “post-Christians” in the West. As the French medievalist Rémi Brague said, “The forces that want to drive Christians out of their ancestral lands would ask themselves, why not continue in the West a work so well begun in the East?”.

There has been no outrage in the West about cutting off Christian heads, only silence, interrupted by “Allahu Akbar”, gunshots and bombs. The history books of the future will not look kindly this Western betrayal — depending on who writes them. The end of the Christians of the East will be a disaster for the Church in the West. They will no longer have anyone living in their own cradle of civilization.

What would we be reading if, for instance, Christian terrorists had stopped a bus, separated the passengers according to their faith, ordered the Muslims to convert to Christianity and then murdered 11 of them? The opposite just happened in Kenya. What did we read? Nothing. On December 10, the Islamic terrorist group Al Shabaab stopped a bus in northern Kenya, then murdered only those who were not Muslims. We Westerners are usually moved by the persecution of this or that minority; why never for our Christians?

The Christianophobia of the Muslim extremists who massacre Christians in Middle East and Africa is central to a totalitarian ideology that aims to unify the Muslims of the ummah (the Islamic community) into a Caliphate, after destroying the borders of national states and liquidating “unbelievers” — Jews, Christians, and other minorities as well as “Muslim apostates”. Nigeria is now at the forefront of that drama.

“Nigeria is now the deadliest place in the world to be a Christian”,noted Emmanuel Ogebe, an attorney.

“What we have is a genocide. They are trying to displace the Christians, they are trying to possess their land and they are trying to impose their religion on the so-called infidels and pagans who they consider Christians to be”.

The West goes back to sleep. “The West opened its borders without hesitation to refugees from Muslim countries fleeing war”, wrote the economist Nathalie Elgrably-Lévy. “This seemingly virtuous Western solidarity is nevertheless selective and discriminatory”. Persecuted Christians have been abandoned by the Western governments and public squares.

India’s Prime Minister Narendra Modi has recently been besieged by Muslims protesting a new law that would offer citizenship to neighboring non-Muslims fleeing persecution. Tarek Fatah explained in the Toronto Sun that the Muslim outrage on the new Indian law comes from the fear “that allowing citizenship to persecuted Pakistani Christians, Hindus and Sikhs would increase the non-Muslim population of the country and thus dilute their veto power they’ve exercised in India for the last 70 years”.

Where are the squares filled with Londoners or New Yorkers for the Christian refugees discriminated by the West? In the parts of Syria occupied by Islamists, Christians just spent a “special Christmas” — without chime bells or lights and with many of their churches turned into stables.

The Khabour, the Syrian region where Assyrian Christians lived, is now called “dead valley“. The former Archbishop of Canterbury, George Carey, recently wrote:

“War in Syria has reignited. Once again refugees fill its roads in need of our compassion. Yet those from the ‘wrong faith’ won’t find it from the British Government. The UK’s resettlement of 16,000 refugees from the earlier conflict saw hardly any from the most brutalised minorities reach safety in our land. Of the refugees who came here in 2015 under the Vulnerable Persons Scheme, only 1.6 per cent were Christians. That’s despite this group being 10 per cent of the Syrian population”.

Muslims fill Western squares for their own; but for our persecuted Christian brothers, these squares remain vacant.

In analyzing the causes for the dysfunctional nature of American society (e.g., soaring suicide rates, especially among young people, massive drug addiction and alcoholism, and widespread violence, including irrational mass killings), among the things to consider is the replacement of America’s founding economic, monetary, and governmental system with a different system.

There were good founding principles in America and bad founding principles. Among the bad ones, needless to say, were slavery and denial of women’s rights. It was a good thing that America abandoned its bad founding principles.

But there were also good founding principles. It was the abandonment of those principles that has to be considered a major cause of the many woes that America is undergoing today.

Let’s consider those good founding principles that were abandoned in favor of the system that Americans live under today:

1. Americans were free to keep everything they earned.

No income tax returns. No IRS. No rushing to the Post Office on April 15. No withholding or payroll taxes. No threats of audits, liens, garnishments, and criminal prosecution for failure to pay income taxes. Whatever people earned or received, they kept 100 percent of it.

2. Americans were free to decide for themselves what to do with their own money.

No mandatory charity, including Social Security, Medicare, Medicaid, food stamps, farm subsidies, corporate bailouts, and foreign aid. Charity was entirely voluntary. No one was forced to take care of anyone. No federal welfare departments and agencies.

3. No drug laws.

Americans were free to ingest whatever they wanted, no matter how harmful or destructive, without fear of being punished for it by the government.

4. No immigration controls.

Except for a cursory tuberculosis and mental health examination at Ellis Island, the borders were open to the free movement of foreigners into the United States.

5. No minimum-wage laws and very few economic regulations.

Economic enterprise was free of federal governmental management and control. No federal regulatory departments and agencies.

6. No public schooling systems.

With the exception of Massachusetts in the 1850s, there were no compulsory school-attendance laws at the state and local level. No federal involvement or subsidization of education. The matter of education was left largely to the free market.

7. No gun control.

No gun registration or background checks. While communities sometimes imposed gun restrictions, Americans were free to keep and bear arms without federal governmental control or infringement.

8. No Federal Reserve, fiat (i.e., paper) money, or monetary inflation or debasement of the currency.

The Constitution called into existence a monetary system in which gold coins and silver coins were the official money of the country. The states were expressly prohibited from making anything but gold and silver coins legal tender.

9. No national-security state, foreign military bases, or foreign interventionism.

The Constitution brought into existence a limited-government republic. No Pentagon, military-industrial complex, CIA, NSA, or FBI. No wars of aggression (except the Mexican War), undeclared wars, coups, state-sponsored assassinations, foreign military bases, foreign aid, war on terrorism, war on communism, or alliances with foreign dictatorships or other regimes.

10. No denial of due process of law or trial by jury. No unreasonable searches and seizures. No cruel and unusual punishments. No coerced confessions.

Whenever federal officials targeted a person for criminal prosecution, the accused was guaranteed due process, trial by jury, and other civil liberties.

Those were the founding principles that caused our American ancestors to consider themselves the freest people in history. Moreover, not only did America become the country with the highest standard of living in history, which was why poor people were flooding into America from foreign lands, it also became the most charitable society in history, entirely on a voluntary basis.

Those were the good founding principles that were abandoned by later generations of Americans, in favor of what is commonly known today as a welfare-state, warfare-state way of life.

Ironically, even though they live under an opposite type of system from that of their American ancestors, today’s Americans are themselves convinced that they live lives of freedom. That sentiment is best manifested by the eagerness of modern-day Americans to thank imperial troops serving in faraway lands for protecting “our freedom” by killing and destroying people over there.

Johann Goethe wrote, “None are more hopelessly enslaved than those who falsely believe they are free.”

I submit that that psychological denial of reality with respect to freedom as well as the abandonment of America’s good founding principles are the root cause of the dysfunctional nature of American society today.