The financial concept of wealth is broad, and it can take many forms.

While your wealth is most likely driven by the dollars in your bank account and the value of your stock portfolio and house, Visual Capitalist’s Jeff Desjardins notes that wealth also includes a number of smaller things as well, such as the old furniture in your garage or a painting on the wall.

From the macro perspective of a country, wealth is even more all-encompassing — it’s not just about the assets held by private households or businesses, but also those owned by the public. What is the value of a new toll bridge, or an aging nuclear power plant?

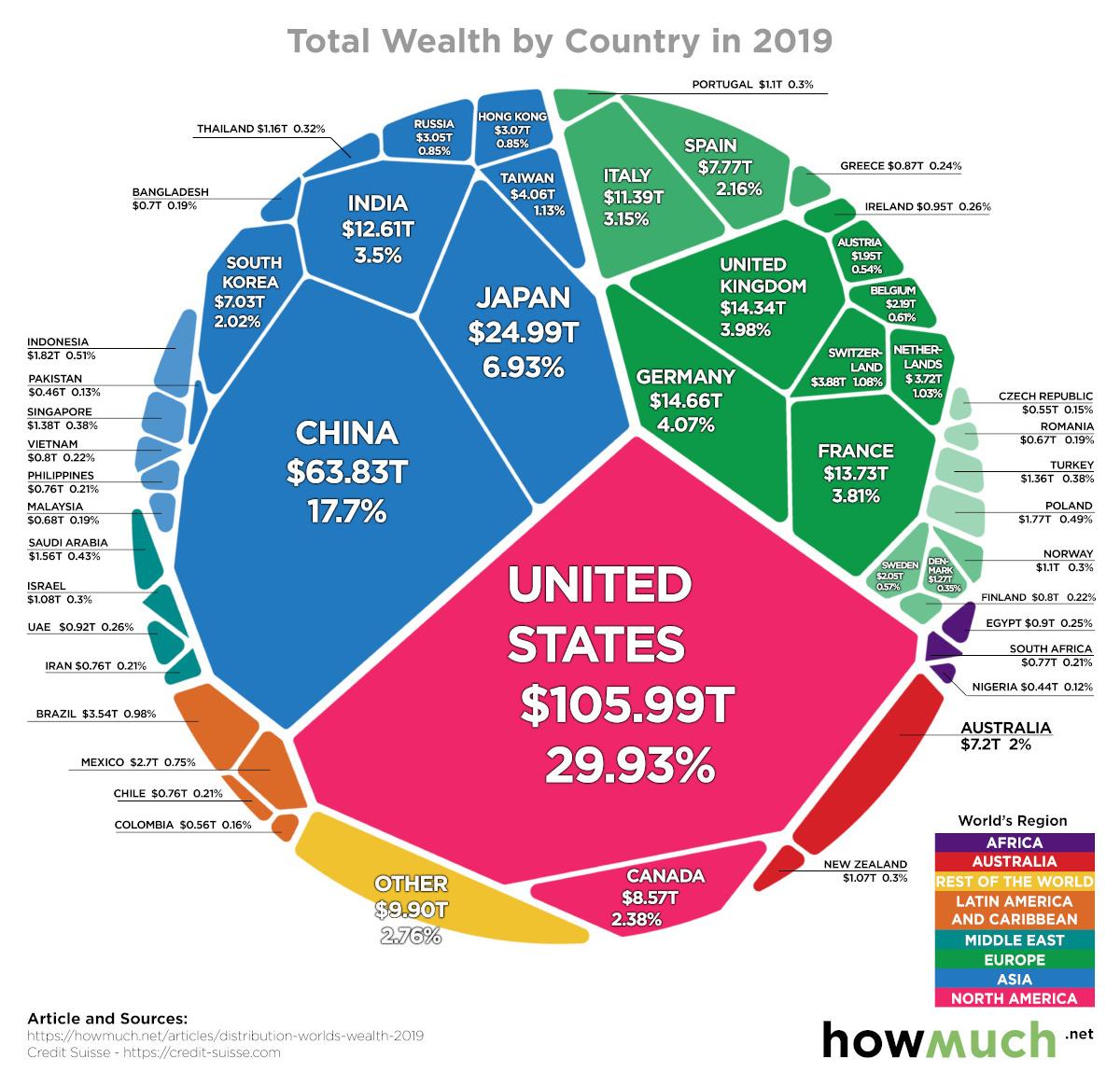

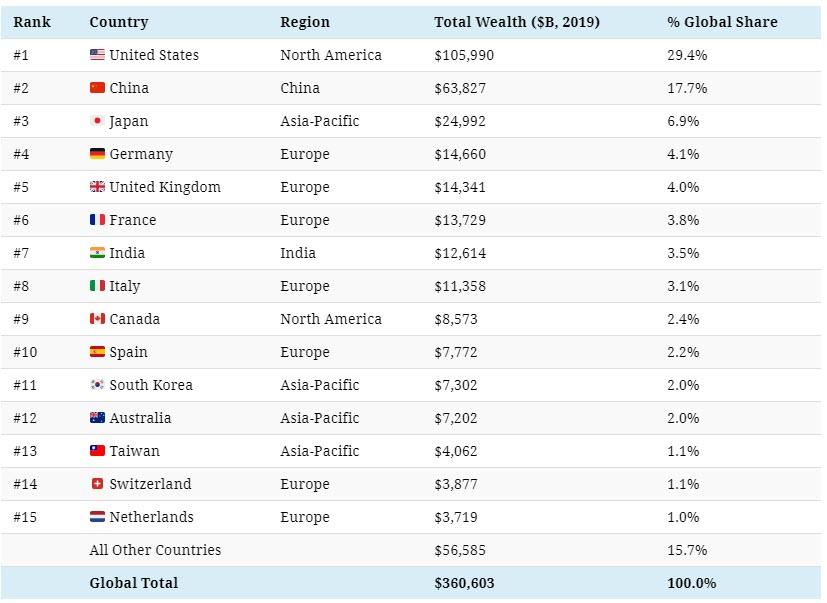

Today’s visualization comes to us from HowMuch.net, and it shows all of the world’s wealth in one place, sorted by country.

Total Wealth by Region

In 2019, total world wealth grew by $9.1 trillion to $360.6 trillion, which amounts to a 2.6% increase over the previous year.

Here’s how that divvies up between major global regions:

Last year, growth in global wealth exceeded that of the population, incrementally increasing wealth per adult to $70,850, a 1.2% bump and an all-time high.

That said, it’s worth mentioning that Credit Suisse, the authors of the Global Wealth Report 2019 and the source of all this data, notes that the 1.2% increase has not been adjusted for inflation.

Ranking Countries by Total Wealth

Which countries are the richest?

Let’s take a look at the 15 countries that hold the most wealth, according to Credit Suisse:

The 15 wealthiest nations combine for 84.3% of global wealth.

Leading the pack is the United States, which holds $106.0 trillion of the world’s wealth — equal to a 29.4% share of the global total. Interestingly, the United States economy makes up 23.9% of the size of the world economy in comparison.

Behind the U.S. is China, the only other country with a double-digit share of global wealth, equal to 17.7% of wealth or $63.8 trillion. As the country continues to build out its middle class, one estimate sees Chinese private wealth increasing by 119.5% over the next decade.

Impressively, the combined wealth of the U.S. and China is more than the next 13 countries in aggregate — and almost equal to half of the global wealth total.

Many decades ago there was an issue of Mad comics that portrayed a future time when everything was done by robots and humans had no function. One day the system failed. As it had been eons since humans had to do anything, no one knew how to fix the system. It was Mad comics version of Armageddon.

I think that is where the digital revolution is taking us.

I remember when appliances and cars responded to humans, and now humans respond to them. When I grew up cars and home appliances did not go “beep-beep” to remind you of the things you were supposed to do, such as turn off the car lights and take the keys out of the ignition, or turn off the oven and shut the fridge.

Cars, except for British sports cars, didn’t have seat belts. Today a car doesn’t stop beeping until you fasten your seat belts. I hear that soon the cars won’t start until the seat belts are fastened.

When the electric company’s outsourced crew failed to connect the neutral line to my house and blew out all appliances, sprinkler system, and garage openers, the electric company replaced everything on a prorated depreciated basis that cost me thousands of dollars. The worst part of it is that the new appliances boss me around.

The old microwave would gently beep three times and stop. The new one beeps in the most insistent way—open the door you dumb human right this second, immediately—and keeps on insisting until I obey. The fridge refuses to let me leave it open for cleaning. The oven insists that I open it immediately, despite my habit of cutting the on time short and leaving whatever it is to cook awhile longer in the hot oven.

We are being told that the Internet of Things is supposed to be our future, everything is connected, everything is a data source. We are told this will make things more convenient somehow, maybe, but your convenience is not what the Internet of Things is being created for. The Internet of Things is being created in a way that things will be associated with your name. So by looking at what the things are doing, people can watch what you are doing. The Internet of Things will be a living, digital organism where you can be found any time of day, watched, identified, and treated like a voluntary member of this new massive database in the sky. Of course, the Internet of Things is a way for government to assure itself that your behavior is not in any way a threat to anyone in government or, if it is, to enable them to quickly pay you a visit in a forceful way.

The Internet of Things will produce more data about you than has ever been collected, and the more data they have on you, the more they can take your stuff from you, the more they can do to you.

Self-driving cars seem to be our future, and robots are taking our jobs away even faster than global corporations offshored them to Asia.

What exactly is it that humans are going to be good for? Nothing it seems.

Why will we need a driving license when cars drive themselves? If there is an accident, who is to blame? The company that made the car? The company responsible for the software? What is the point of car insurance when drivers have no responsibility?

Perhaps it is true that aliens are living among us. Their language is “beep-beep” and they are using our machines and cars to train us, like Pavlov’s dogs, to respond to their command.

I can remember when telephones were a convenience before they became a nuisance. When my land line rings, 95% of the time it is a scam or a telemarketing call, usually robotic. Now, a man will listen to a sexy female voice, for a time, and a woman will listen to a courtly gentleman’s voice, but until sex doll robots catch on, no one wants to listen to a machine’s voice. So why the calls? Why do the telephone companies permit their customers to be scammed and their privacy to be constantly invaded? How do the phone companies benefit from permitting unethical people to destroy the value of phone service?

The same thing, I am told, happens to cell phone users. Recently I finally had to acquire a smart phone, because two people I need to reach only respond to text messages. They refuse to answer any phone, and email is so invaded by scammers, malware, and marketeers that they do not use email. They do not even set up the message system on their cell phones. If you try to call them, you get instead of an answer the message that the person you are attempting to call has not set up their message box.

So there you have it. Except for texting, which can’t (yet) be done with a land line, telephones are a nuisance.

Growing up in Atlanta during the 1940s and into the early 1950s, you could not yourself place a call from your telephone. When you picked up the receiver, an AT&T operator answered and asked: “number please.” You gave her the number, and she rang it and connected you if there was an answer. If you did not know the number, you asked her for information. If you knew the complete name and perhaps the street address, you were provided with the telephone number.

In those halcyon days even in a city such as Atlanta, Georgia, there were party lines. That meant that you shared a telephone line with a neighbor. If you picked up the receiver to make a call through the operator and heard voices speaking, you knew the line was in use and decency required that you hang up immediately. As the talking parties heard the click when you picked up the line, if they didn’t hear the click when you hung up they asked you to get off their call.

In that system, there was no anonymity. Anonymity appeared with dial phones, which allowed you to make your own calls. From a public telephone, the call was not traceable to you. This technology was the beginning of our downfall.

Dial phones, something youths have seen only in antique shops or old movies are still with us in everyday language. We still say “dial the number” when we are punching buttons.

Today thanks to technological “progress,” it is much easier to invade privacy.

Technology is destroying us and the planet. The pollution from technology is phenomenal. 5G itself may do us in. The destruction of privacy, identity, and freedom by the digital revolution is far beyond George Orwell’s imagination. Insouciant humans delight in the gadgets that are turning themselves into unfree people who are under control but who themselves control nothing.

This outcome is easily seen in China where the government uses universal spying to construct for each person a social credit score. If that person is a dissident, has bad habits, etc., that person gets a score too low to qualify for a loan, university admission, employment, etc., and becomes a non-being. Here is Soren Korsgaard’s explanation of our future.

Dystopian classics are back into the spotlight, like Aldous Huxley’s Brave New World and George Orwell’s 1984. They have roared back onto bestseller lists due to whistleblowers’ exposés of government imperialism and totalitarian surveillance of their citizens and foreigners. While the kakistocracy and dystopian surveillance state depicted in 1984 undoubtedly reflected, to some extent, contemporary sociopolitical realities, Orwell extrapolated worst-case scenarios set as warnings for future generations. Nonetheless, his book and implicit warnings seem to have been ignored as an authoritarian surveillance state is now a reality for most people in first and second world countries. In lieu of accountability for criminal mass-surveillance or these revelations deterring or limiting the prying eyes of government-sponsored spy programs, the establishment in conjunction with their media platforms has used it to their full advantage, almost as if they, themselves, masterminded the leaks.

Rather than being dismantled, the establishment has openly added advanced surveillance technology to their arsenal in their cataclysmic War on Truth. The mainstream media now parallels Orwell’s Ministry of Truth that broadcasts official explanations, while it effectively neutralizes those who venture outside the parameters of government-approved thinking, which so often equates to threatening their interests.

While the current Western population control via advanced surveillance technology and social engineering is unparalleled in history, China has nevertheless rolled out a system that sets new standards for government control, the so-called social credit system. In a few decades from now, if the Chinese government succeeds, those who are imprisoned by the social crediting system will have no reference point or conception of freedom; digital tyranny will have become the norm.

To some extent, Western policymakers have been apprehensive of the Chinese program, but as we shall see, it is nevertheless evident that they themselves are working diligently behind the scenes to implement the same technology that makes the Chinese digital prison possible.

OK Boomer: Ex-Citi Banker Wins Ageism Case After Boss Calls Him “Old… Set In His Ways”

Today in “anytime you fire someone it’s always a case of discrimination” news…

A former investment banker for Citigroup has won an age discrimination case against the bank after one of his bosses called him “old” and “set in his ways” when he was laid off at age 55.

A London Tribunal ruled in the ex-banker’s favor this week, finding that Niels Kirk was dismissed unfairly. Kirk had previously been a managing director for energy banking, according to Bloomberg. He had previously been employed at Citigroup for 26 years and wasn’t given any warning about a proposed restructuring.

Citi says it will appeal the decision.

One of his bosses, 54 year old Manolo Falco, denied making the statement but did concede that Kirk “had some very difficult relationships with other senior bankers.” But the judge ruled that Falco’s evidence was “less than convincing”, while Kirk had taken notes in the meeting.

The judge presiding said: “The remark appeared to the tribunal to be the kind of throwaway remark Mr. Falco could make.”

The size of any award will be determined at a later hearing. Once an employee proves they are a victim of discrimination, a tribunal can order damages that are higher than the cap of about $109,000.

Kirk’s performance ranking had fallen from a 1 (best) to 3 (good) between 2014 and 2016. His overall compensation also fell from $1.24 million in 2014 to about $600,000 in 2016.

Citi claims its “position as set out in the litigation is that Mr. Falco did not make that comment.” Citi also says it’s upset with the decision “particularly given the small age gap between Mr. Kirk and the employee who was ultimately appointed to the role.”

Kirk’s hired successor wasn’t much younger, at just 51 years old.

Citi has 51 managing directors in the company’s EMEA Corporate Banking Department and, as of 2016, three were over the age of 55 and fifteen were 50 and older.

“Gray hair is very important in this industry,” Falco told the court last year.

As always, it’s the fear of sanctions that provides the leverage Trump seeks in this cat-and-mouse game with Iran. And this time, the leverage is over Iraq, which would like to see both American and Iranian forces out of the country, for obvious reasons.

There is nothing ISIS would love more than this.

It would also devastate Iraq because the sanctions threatened would include blocking access to Iraq’s U.S.-based account where all the oil revenues are kept. That threat stands if Iraq moves to kick U.S. forces out of the country.

That would mean victory for Iran (temporarily). Kicking out Iranian forces is not nearly as simple because the line between state and non-state actors is blurred, at best.

A few weeks ago, a U.S. drawdown of military forces in Iraq was already expected, but that now seems unlikely because of the implications.

The very military base that Iran attacked following the assassination of General Soleimani was already preparing for a drawdown.

In addition to the threat of sanctions on oil money, a U.S. withdrawal would likely open the door for an ISIS return.

What Iraqis Want

There is no consensus on this question, other than the fact that no one wants Iraq to be the proxy battleground between the United States and Iran.

It’s a fair point, and Iraqis have had a very difficult time enjoying anything close to sovereignty since the fall of Saddam Hussein.

While the Iraqi parliament has voted for U.S. troops to leave, they do not represent a unified voice. The Sunni elements of parliament did not participate in the vote. Neither did the Iraqi Kurds.

Shia factions in Iraq are, of course, pushing for a U.S. withdrawal, but the Sunnis and Kurds see this as a dangerous opportunity for pro-Iranian Shia factions to take even more control of the central government in Baghdad.

They don’t necessarily want a huge U.S. troop presence, but they are more fearful of a complete withdrawal that would leave them over-exposed to pro-Iranian forces. They also aren’t interested in being very loud about this fear.

In this atmosphere, there is already talk in certain Sunni circles of carving Iraq up to create yet another autonomous region such as that governed by the Kurdistan Regional Government (KRG) in the north of Iraq.

A Sunni-dominated region would include Anbar, Saladin, Nineveh and Diyala provinces, and would leave all of Basra’s oil to pro-Iranian factions.

Already, Sunni leaders are mentioning this as an option, pointing to what they call the “successful” example of the Kurdistan region.

The disintegration of Iraq was already progressing prior to the latest showdown between Iran and the United States. The country has been teetering over the edge of anarchy since 2003, when a single party (the Baath Party) was destroyed and Iraq became “governed” by multiple parties with even more fractious factions and a weak military that pro-Iranian Shia militias found easy to influence.

But this is far from just a sectarian conflict.

The mass protests that were already threatening Iraq’s fragile stability were Shi’ite-versus-Shi’ite. The Sunnis were not involved, nor the Kurds. They were just watching things unfold, warily.

One of the biggest mistakes the casual Western news reader makes is accepting a black-and-white narrative when it comes to Iraq. There is a very distinct group of Shi’ites that has a nationalist bent and is militantly against Iranian influence in an independent Iraq. This was a genuine uprising against highly corrupt and ineffective state institutions.

Then there is a second group of pro-Iranian Shi’ites who have been brutally putting down the popular uprising. This group exists in order to maintain Iran’s influence.

The problem now, for the U.S., is that the confrontation between the U.S. and Iran on Iraqi soil is more likely to bring these two groups together than it is to pull them further apart, which would have been a real threat to Iranian influence in Iraq.

Indeed, both Shia groups are calling for a U.S. withdrawal.

In this territory, you have to pick your evil, and for some time it’s been pro-Iranian forces and pro-U.S. forces against ISIS.

That’s not going to happen anymore, to the great delight of the Islamic State.

In 2011, a U.S. troop withdrawal from Iraq sent an open invitation to ISIS. In 2020, it will do the same.

The Biggest Threat to Iraqi Oil

For oil prices, the only real benefit to the Iran-Iraq conflict at this point is that Iraq is at a bit of a standstill when it comes to developing new projects, though its existing production will not be affected by any evacuation of U.S. oil workers, which has been minimal so far.

Since Iraq is already OPEC’s biggest over-producer, this is a bit of a balm on compliance.

But the biggest threat to Iraqi oil in recent months has been Shia protesters fed up with a corrupt government. No one else is willing to touch the oil.

The biggest immediate threat is not Basra oil–it’s Kirkuk oil.

A U.S. troop withdrawal could easily relaunch a sectarian civil war in Iraq, and Kirkuk would be the first to fall.

Kirkuk is in northern Iraq, but outside the official territory of the Kurdistan Regional Government (KRG).

It’s also one of ISIS’ key stomping grounds, and the only reason they have been kept from taking over this region entirely is the effort of a U.S.-led international anti-ISIS coalition, in which Kurdish Peshmerga forces played an integral role since 2014.

A withdrawal of U.S. troops at this point will ensure a return of ISIS, and a sectarian conflict is exactly what the Islamic State is hoping for.

At an attack on the K-1 base just in northwest Kirkuk in December launched the latest round in the Iran-U.S. proxy war in Iraq.

Prior to that, ISIS had already started escalating attacks on this base, with ISIS seeing a window of opportunity in an American shift to defense against Iran and Hezbollah in Iraq. We’re already seeing the uptick in ISIS attacks–and the focus is definitively Kirkuk.

Coalition forces may have won the Battle of Kirkuk in 2016, but ISIS is still there.

Basra oil is safe, for now. The biggest threat is to Kirkuk’s 9 billion barrels. This is where the next round of this conflict starts, and it will be ISIS that ultimately wins any ‘proxy’ war.

Sig Sauer’s Next Generation Machine Gun Receives Safety Certification With Special Forces

Sig Sauer announced Wednesday that the Special Operation Command (USSOCOM) had granted it with a safety certification for the new MG 338 Machine Gun, 338 Norma Mag Ammunition, and Next Generation Suppressors.

A press release from the Sig Sauer details that upon safety certification, it will deliver multiple MG 338 Machine Guns, thousands of rounds of 338 Norma Mag Ammunition, along with high-tech silencers.

“The safety certification of the complete SIG SAUER MG 338 system and delivery of the system to USSOCOM is historically very significant. For the first time in decades the U.S. Military certified a new machine gun, ammunition, and suppressor at the same time, bringing new innovation, portability, and increased lethality to our ground forces, with all components coming from one company,” said Sig Sauer CEO Ron Cohen.

Cohen added that “this certification was achieved following the outstanding performance of the complete MG 338 system through the rigors of the extensive function, durability, and safety tests set forth by USSOCOM.”

The release notes the new machine gun “bridges the gap” between the current M240 (7.62x51cal) machine gun and the M2 (.50cal). The new weapon is “noticeably lighter, weighing only 20 pounds, and provides significantly more range and lethality.”

The MG 338 is a belt-fed, lightweight medium machine gun weighing about 20 pounds, chambered a 338 Norma Mag. The weapon has a greater range and can breach advanced body armor from extended distances. The weapon can be easily convertible to 7.62x51cal.

“We are incredibly proud of this historical accomplishment and honored to have received this safety certification by USSOCOM for the performance of the complete MG 338 system,” concluded Cohen.

Textron Systems’ AAI Corporation delivered their next-generation machine gun to the Army last year that chambers a telescoped round between 6.5mm and 6.8mm and is expected to be the future replacement for the M16 rifle, M4 carbine, and M249 light machine gun.

The Pentagon, flush with new cash from President Trump’s $2 trillion military spending spree, is expected to outfit soldiers with modern weapons in the next 2-4 years. Sig Sauer’s MG 338 Machine Gun and AAI’s next-generation machine gun could be some of the replacement weapons expected to enter service in the near term. With new weapons comes high-tech ammo, the new rounds are expected to penetrate the most advanced body armor Russia and China have to offer.

In emulating the American economic raison d’etre, China has attempted to develop its unique capitalist model while ignoring that it too will soon suffer the same fate for the same reason: Unsustainable debt. When examining the recent realities of Chinese banking and finance over the past year it seems the steam that president Xi Jinping touts as powering the engine of his purported economic miracle of a master-planned economy is only a mirage, now almost completely evaporated before his eyes.

Like the many other similarly foolish western nations, China seeks only one path out of this fiscal death spiral, one that will likely spell doom and/or revolution in many countries soon: More debt.

China is becoming increasingly unable to continue to pay into the base of the world’s largest pyramid scheme of an economy and the cracks in the bubble are showing. This past year, saw three of the 4,279 Chinese lenders almost fail, if not for the massive intervention by the People’s Bank of China (PBoC) of immediate liquidity via more debt. The Chinese economic miracle is built on unsustainable debt-based infrastructure projects over the past two decades that have provided China with a face of prosperity to show the world, but this is only a mask to hide the limited countrywide success of the Chinese miracle into the rural areas. The injection of $Trillions in capital has seen China distribute these sums across the base of its economy creating a GDP that hit a high of 14.2 % in 2007 then averaged nearly 9% for the next decade before dropping yearly to 6.1% in 2018. All this growth had produced a personal affluence to a sub-set of Chinese society that has stoked this appearance of a flourishing economy.

This Chinese economic Keynesian trick of interjection of liquidity into national infrastructure is somewhat similar to the TVA and national works projects funded under Roosevelt’s depression-era New Deal. In this approach employment and therefore a growing tax base accelerated year after year as workers and corporations received the short-lived benefits of this massive windfall of available liquidity.

China’s method of stimulus is of course distinguished from today’s American model that merely shovels the injection of its own manufactured $Trillions by using multiple fiscal tricks to by-pass the citizenry and instead shovel the cash straight into the wallets of the already super-wealthy. Meanwhile, the US peasant once again pines in the “Hope” of yet another election.

The Metrics of a Failing Economy

Many analysts have for nearly a decade opined that China’s belief in national fixed-asset investment, the biggest engine of China’s economy, has long been the fundamental contributor to Chinese GDP growth, which was directly proportional to an ongoing increase in public and private debt. “China has relied on export and debt-financed fixed asset investment for growth for over two decades,” said Ho-Fung Hung, Professor in political economy at the Johns Hopkins University.

But as the world economy slows while the metrics show a recession looming China’s economy is already cooling rapidly. “And as the central government and banking system keeps producing new loans to absorb the debt, it leads to the continuous debt buildup,” Maximilian Kärnfelt, an analyst with the Berlin-based Mercator Institute for China Studies, told news service DW, adding that infrastructure investment still largely drives China’s economic growth since fixed investment contributed to 45 per cent of China’s GDP in 2016.

In a sign of the disaster to come, the first Bank to almost fail was Baoshang Bank Co. in May 2019. In this instance, for the first time in twenty years, the government took over control and seized the bank. This progression next took form when Chinese regulators took a different approach by ordering three state-owned financial institutions to buy significant stakes in Bank of Jinzhou Co. When, Shandong-based Heng Feng Bank, which had failed to disclose its financial statements for two straight years, required a bail-out, the bank sold new shares for about $14 billion to a group of investors including a unit of China’s public sovereign wealth fund and a local government-backed asset management firm.

Although these were some of the smaller rural banks, as shown this past month in Chinese reports, their economy is following the world in a quantified slowdown that has seen GDP slip yearly since 2012. Making the matter worse a similar world slow-down in purchasing is already affecting China’s manufacturing-based economy. The three bank failures were only the tip of a huge iceberg.

China’s $40 Trillion banking system dwarfs the American system at double the size, with over 4,000 small, medium and massive, state-owned banks. The world’s four largest banks, including behemoth ICBC ($4TN), are all Chinese.

The failure of just three banks was important enough that Chinese regulators submitted Chinese banks to a stress test and the results were shocking. China’s central bank admitted that China’s banking sector is “showing signs of strain.” The stress tests had revealed that over 13% of China’s 4,379 lenders were designated “high risk” by the central bank’s report. With this amounting to over 570 banks, and thus multiplied by the three existing examples of bank bail-out funding, with the Chinese economy following the world into recession, the financial numbers and likelihood of any future series of bail-outs are truly biblical. If not, fiscally impossible.

Separately, the PBOC also stress-tested 30 medium- and large-sized banks in the first half of 2019. In the base-case scenario, assuming GDP growth dropped to 5.3% – or well above where China’s real GDP is now – nine out of 30 major banks failed and saw their capital adequacy ratio drop to 13.47% from 14.43%. In the worst-case scenario, assuming GDP growth of 4.15%, or just 2% below the latest official Chinese GDP report, seventeen out of the thirty of these major banks failed the test. Separately, a liquidity stress test at 1,171 banks, representing nearly three-quarters of China’s banking sector by total assets, showed that ninety failed in the base-case and 159 in the worst-case scenario. The metrics of any collective bail-out indicates that China has upwards of an insurmountable $20 trillion problem rapidly approaching.

In reaction to these first three bank failures, the stress tests and poorer economic news China did what centrally planned economies do: Chinese policymakers focused on strengthening oversight and regulation by the PBoC and gave it authority to write new rules for much of the financial sector. The China Banking Regulatory Commission and the China Insurance Regulatory Commission will now be merged as part of an overhaul aimed at resolving existing problems such as unclear responsibilities and cross-regulation as well as closing regulatory loopholes and curbing risk in the $40-43 trillion (€34.78 trillion) banking and insurance industries.

With the metrics of China’s banking system already cause for considerable concern to the tune of $20 Trillion, this huge obligation is as much a mirage as the economy since it fails to add to the account the very large and un-tabulated Shadow Banking loans which would add $Trillions in debt to China’s already highly leveraged systemic banking risk. The International Monetary Fund (IMF), which provides- despite its predatory legacy- some excellent yearly analysis of worldwide economic developments has warned China’s problems could lead to “financial distress” in the world’s second-biggest economy. China is seen as one of the economies most vulnerable to a banking crisis, although Beijing has repeatedly assured that the risks are under control. In response to the PBoC reports, Chinese Finance Minister Xiao Jie echoed that the situation “was under control.”

China’s Economic Tricks of Sustainability.

As the world economic body politic runs out of any remaining gas to keep a pilot light under the rapidly cooling metrics that show their long forestalled recession is near and certain, China is also contracting.

The national debt of China, which is the total amount of money owed by the Chinese government and all organizations and branches stands at nearly CNY 38 Trillion ( $5.4 TN) and 54.44% of GDP.

Chinese debt has been accumulating ever more rapidly. The Institute for International Finance (IIF) reported that year-on-year, in Q1 of 2019 China’s corporate, household and government debt increased 6% more from 297% of GDP to an incredible 303%. However, this is also more than a 100% increase since 2008 and amounts to 15% of all global debt.

These figures do not include the off-the-books “Shadow Banking loans that some estimates predict would triple that debt percentage to much closer to $16 Trillion. The problems are most serious in China’s rural banking sector where an ever nervous public has reacted with two late-2019 bank runs at China’s Henan Yichuan Rural Commercial Bank and then at Yingkou Coastal Bank.

At the end of 2018, the budget deficit of the Chinese government was close to five per cent. However, if the off-balance-sheet (“shadow”) financing of local governments is taken into consideration, the budget deficit rises to over 11 per cent. However, at the end of 2014, the official government deficit stood at less than one per cent, but an accounting which includes local “shadow” funding was around five per cent.

China’s shadow banking system is so-called since this myriad of endemic lending trickery is believed to be massive in total and kept off the books. These risky, undisclosed loans entered China’s financial system in 2009 throwing open the doors to debt for a Chinese population hungry for investment in order to pay for all those Chinese and internationally made western goods.

The main kind of shadow deposit is generally offered as a wealth management product (WMPs). Chinese banks offer these via aggressive marketing of high-interest-rate accounts as their alternative to savings accounts which are regulated to a maximum return of 3 %. Since these sanctioned shadow loans advertise a return of as much as 8% or more, normal banking customers have been throwing their miraculously large paychecks into these funds by the billions.

One reason WMPs offer higher rates is that they are based on much riskier bank loans, much like the precursor to the late ’80s, early ’90’s American savings and loan meltdown. Incredibly, banks don’t hold these loans on their balance sheets or set aside capital against their potential defaults. Instead, they typically extend this debt via intermediaries called trust companies—firms that are not allowed to accept deposits or formally loan out money but are allowed to manage it. The trust companies create investment products like WMPs, which banks market for them in return for a commission.

With some smaller Chinese banks having already found themselves either getting bailed out or the subject of a bank run, one reason is that, like America, China’s interbank/repo rates have surged amid growing counterparty concerns of the many banks seeking depleting available liquidity. This has forced many banks to rely almost entirely on new deposits to fund themselves, forcing them to hike their deposit rates to keep their funding levels stable. Like any Ponzi trick in banking, new cash is required to sustain these thousands of lending pyramids. With the economy in decline, this need has lead to some desperate regional banks offering incentives for depositor’s cash that would make the long-ago American “free toaster” seem ordinary.

China has a massive pork famine that has seen disease wipe out 40% per cent of its pig population in 2019. With China being the world leader in pork consumption these bank’s desperations have created some interesting incentives to attract depositors. The SCMP reports that new clients who deposited 10,000 yuan (US$1,430) or more in a three-month time deposit at the Linhai Rural Commercial Bank in Duqiao in Zhejiang province were then eligible to enter a lottery to win a portion of pork ranging from 500 grams (18 ounces) to several kilograms. Other rural commercial banks in northern China’s Hebei province and western China’s Guizhou province have also launched similar pork rewards programs. Dushan Rural Commercial Bank, located in the remote mountainous county in Guizhou, offered a coupon for 10 yuan (US$1.4) worth of pork for every 10,000 yuan of new deposits.

This solution has been touted as uniquely beneficial to these banks since, instead of offering higher rates which only accelerate the bank’s insolvency due to requiring higher payouts on deposits, the bank is instead making a one-time payment, and the unusual incentive is enough to garner substantial new deposits.

PBoC cuts in its key lending rates in August ’19 designed to stimulate a slowing economy have only exacerbated net interest margin pressures on these banks. With less income from returns on their loans and without the many funding options available to China’s much larger banks, these increasingly high-interest rates that China’s smaller banks have to offer in order to attract new cash deposits could further lead to their insolvency.

It’s been over four years since the last official Chinese benchmark rate cut. With America leading the way across the globe with rate cuts aplenty and China still having a base rate of far higher than the US rate of < 1.5%, it was only a matter of time for China to also drop rates.

With the new authority given to the PBoC, this key Loan Prime Rate (LPR) has become the new Benchmark Reference Rate to be used by banks for lending. This, like most recent decisions are designed to interject further liquidity in the form of debt once again into a still failing economy by lowering borrowing costs for small businesses. This rate will be now set monthly (20th of every month) and will be linked to the Medium-term Lending Facility rate. The current 1 year LPR stands at 4.15% after its latest cut on Nov 30 versus the Benchmark Rate of 4.35%. This number is sure to continue to shrink and can be considered a key indicator of Chinese frustration at retaining needed annual GDP growth since the result of this one move lowered the costs of the roughly 152 trillion yuan ($21.7 trillion) in yuan-denominated outstanding loans held by financial institutions (that are actually on the books) in a further hopeful attempt to again boost economic growth.

Just mere days after the 20 bps cut the PBoC further highlighted its desperate need for capital, announcing that it will be lowering the required reserve ratio (RRR) – or the amount of money banks are required to have on hand – by 50bps for commercial lenders. Currently, the required reserve ratio is 13% for large banks and 11% for small banks. The cut, which is the first since September, will bring the blended reserve ratio for Chinese banks to the lowest level since October 2007. In doing so PBoC effectively released about 800 billion yuan ($115 billion) in instant liquidity from out of the already cash-strapped financial system.

All these adjustments by China and the PBoC do little to control or pay-off increasing debt and are designed to maintain the Chinese miracle of TVA style infrastructural improvements that has been the employment engine of its economic growth. China’s new development of the Belt and Road Initiative (BRI), although a masterstroke in Eurasian commerce, also serves to continue the illusion.

As traditional monetary policy becomes ineffective to boost the economy, Chinese President Xi has installed twelve former executives at the state-run financial institutions across the country who will support the communist government’s ability to combat banking and debt difficulties, reported Taipei Times.

These appointments are in response to growth collapsing to a three-decade low in 2019. New manufacturing orders did increase but this was in large- and medium-sized enterprises. Small enterprises continued deeper into contraction and new non-manufacturing orders slowed, pushing employment further into quantified contraction.

An easier to understand recessionary metric, passenger car vehicle sales, fell yet again in December, plunging 3.6% to 2.17 million units, according to the China Passenger Car Association. This marks the 18th drop in the past 19 months for the country. Sales fell 7.5% in 2019 and 6% in 2018. GM said that its sales were down 15% in China and said that pressure into 2020 would likely continue.

Meanwhile, local Chinese manufacturers’ numbers are also down. BYD Co. posted an 11% drop in 2019 sales and SAIC Motor reported a “similar decline”.

Worse, exports to the United States were down 23% from the prior year.

Running from the Piper’s Call

But, it seems that China has no choice but to carry on with the façade of financed infrastructure projects as the only path to survival. Said Victor Shih, an associate professor of political economy at the University of California in San Diego;

“Because it [infrastructure investment] already is a large contributor to growth, the slowing investment will substantially reduce growth rates. This is not what the leadership wants.”

Shih’s assertion seemed confirmed when last year, President Xi said Chinese banks would lend 380 billion yuan ($55.09 billion) to support Belt and Road cooperation, and Beijing would also inject 100 billion yuan into a Silk Road Fund. Some observers view the project as an instrument designed to help the Chinese economy, with state-owned companies in specific sectors expected to profit massively from its implementation.

But they still need funding and Chinese banks on their own volition may be reluctant to get involved when already having troubles of their own. Andrew Collier, managing director at Orient Capital Research, says

“The banks [may] remain leery of these projects because they doubt they will be profitable and they will be stuck with bad loan. In the end, we are going to see increasing defaults among smaller institutions, the collapse of private loans via wealth management products, and growing layoffs in areas of the country with less political power.”

Making matter worse, a study conducted by the Center for Global Development estimates that the initiative could increase debt sustainability-related banking problems in eight countries also involved in the BRI.

“I still think that if growth falls below a certain level, the top leadership will order a stimulus, which involves acceleration in debt growth,” said Victor Shih. “That is the only viable tool in China’s arsenal if the economy slows too much.”

As noted in a recent article by University of Helsinki economics professor Tuomas Malinen, China has stimulated its economy aggressively in Q1 and Q3 2019 but interestingly has not continued its past emphasis on infrastructure investments as in 2015/2016. Q3 of 2019 saw record-breaking stimulus programs, however, China concentrated instead on providing loose credit to enterprises through both conventional and “shadow” banks.

As Malinen forewarns:

“What is notable is that even with this record stimulus, China has kept its economy growing barely above the ‘official rate’. This tells us that the Chinese economy has reached or is very close to reaching the point of debt saturation, where households and corporations simply cannot absorb any more debt, and any new debt-issuance fails to stimulate the economy.”

Though a massive infrastructure-spending program could revive growth, the ability of China to issue fiscal stimulus is starting to be seriously limited. This effectively means that China is fiscally unable to underwrite massive infrastructure projects and so any new world-economy-saving stimulus from China, as in 2015/2016, will be practically impossible. New infrastructure initiatives- if recessionary metrics continue to deteriorate- could only be realized if those costs are directly monetized by the PBoC. This would be the weapon of last resort for China but , when considering a declining economy, may soon be inevitable.

As Goes China…?

China is just one more working example of the failure of the many globalist economies worldwide that are already similarly suffering in the grip of massive unsustainable- if not orchestrated- debt. Which country becomes the first to trigger the almost certainly pending domino effect of global economic collapse, is merely a rhetorical question at this point. As goes China…?

This week in an interview, former Reagan OMB director David Stockman highlighted the global economic link to China, saying,

“The world economy would be not nearly as good as it looks had the Chinese not been borrowing like there’s no tomorrow and building regardless of whether its efficient or profitable.”

Stockman added, in summation,

“The whole global economy is really dependent on China piling even more debt onto the $40 trillion pile they already have.”

China economically continues to play the financial role of Kenneth Lay to its American mentor’s Bernie Madoff. But in the last few months China has shown, like so many other so-called first world economies, that it too is now all-in at the casino and using only borrowed money in a desperate effort to stay at the table…or starve.

Worldwide, many countries already burn in political turmoil of their own debt-ridden making as their own primal forces of nature squeeze their populations with the resultant new mantra of ever increasing austerity while the IMF and World Bank waits in the wings, salivating to gobble-up the carcass.

Alas, when it comes to unsustainable national endemic debt one primal truth is now being heard clearly in China, as in other Central bank boardrooms across the globe, and the empty dinner plates of their public…

When the time comes to pay the piper, that debt will be paid, no matter…but the Piper will take, in lieu of payment, pork, flesh, blood, or… dreams!

Retail Carnage Continues: Bose Lays Off 100s, Shutters All Retail Stores

Taking the award for Most Continents Covered While Shrinking Retail Footprint this week is Bose, which will be laying off hundreds of employees to close retail stores across the world.

The company plans on closing its entire retail footprint in North America, Europe, Japan, and Australia, according to The Verge. It adds up to a total of 119 stores, according to a spokesperson. The closures are slated to happen “over the next few months”.

And the company was direct in why it was making the move: it stated this week that its products “are increasingly purchased through e-commerce”.

The company has had a brick and mortar presence since 1993 and has locations across many shopping centers and malls scattered around the U.S. The stores help showcase the company’s headphones, speakers and other hardware. But there are usually similar demo areas in stores like Best Buy, which still sells Bose products.

The company hasn’t said exactly how many people would be laid off, stating:

“Originally, our retail stores gave people a way to experience, test, and talk to us about multi-component, CD and DVD-based home entertainment systems. At the time, it was a radical idea, but we focused on what our customers needed, and where they needed it — and we’re doing the same thing now.”

Colette Burke, vice president of Global Sales, continued:

“It’s still difficult, because the decision impacts some of our amazing store teams who make us proud every day. They take care of every person who walks through our doors – whether that’s helping with a problem, giving expert advice, or just letting someone take a break and listen to great music. Over the years, they’ve set the standard for customer service. And everyone at Bose is grateful.”

The company says it will keep stores open elsewhere:

“In other parts of the world, Bose stores will remain open, including approximately 130 stores located in Greater China and the United Arab Emirates; and additional stores in India, Southeast Asia, and South Korea.”

The company also says it is offering outplacement assistance and severance to employees.

Meanwhile, the move may not surprise Zero Hedge readers, as we noted just two days ago that mall vacancies are hitting two-decade highs.

US retailers announced 9,300 store closings in 2019, according to Coresight, indicating that the retail apocalypse and a massacre of malls are far from over. Mall operators saw a surge of store closures in 2H19 and ahead of Christmas despite a relatively stable consumer that has been leveraging up via the use of credit cards.

Barbara Denham, a senior economist at Reis, said one notable trend during the 2019 holiday season was the shift in spending habits from brick and mortar stores to online. Denham said recent vacancy statistics paint a disastrous picture for shopping malls as vacancy rates have surged to a record high of 9.7%.

The notion of “fake news” has entered our vocabulary as a pejorative term for dissemination of bogus information, usually by social media, sometimes by traditional print and electronic channels which happen to hold positions contradicting the tenets of our conventional wisdom, i.e., liberal democracy. The term has been applied to Russian state owned media such as RT to justify denying such outlets normal journalistic credentials and privileges.

In this essay, I will employ the more traditional term propaganda, which I take to mean the manipulation of information which may or may not be factually true in order to achieve objectives of denigrating rivals for influence and power in the world, and in particular for denigrating Russia and the “Putin regime.”

The working tools of such propaganda are

tendentious determination of what constitutes news, which build on the inherent predisposition of journalism to feature the negative and omit the positive from daily reporting while they carry this predisposition to preposterous lengths

the abandonment of journalism’s traditional “intermediation,” meaning provision of necessary context to make sense of the facts set out in the body of a news report. In this regard, the propagandistic journalist does not deliver the essential element of paid-for journalism which should distinguish it from free “fake news” on social media and on the internet more broadly

silence, meaning underreporting or zero reporting of inconvenient news which contradicts the conventional wisdom or might prompt the reader-viewer to think for himself or herself. As a colleague and comrade in arms, professor Steve Cohen of Princeton and NYU, has said in his latest book War with Russia?: the century old motto of The New York Times “All the news that’s fit to print” has in our day turned into “All the news that fits.”

Demonstrations of the arguments I present here could easily fill a book if not a library shelf. However, I think for purposes of this essay, it suffices to adduce several examples of the three violations of professional journalism giving us a constant stream of propaganda about Russia and its political leadership by offering a few reports drawn from the very cream of our print and electronic media.

In particular, I have chosen as markers the Financial Times and the BBC. The use of propaganda methods in their coverage of Russia is all the more telling and damaging, given that in a great many domains these channels otherwise represent some of the highest quality standards to be found in reporting anywhere today and consequently enjoy the respect of their subscribers and visitors, who little suspect they could be so prejudicial in their coverage of select domains like Russia.

* * *

As 2019 drew to a close, many of our media outlets drew attention to two Russia-related anniversaries: the just celebrated thirtieth anniversary of the fall of the Berlin Wall with the retreat of Soviet armed forces from Eastern Europe that it touched off; and the soon to be celebrated twentieth year of Vladimir Putin’s hold on power in the Kremlin. Both subjects may be fairly called news worthy and so fully correspond to traditional journalistic values. What has been exceptional and unacceptable has come in the second category of violations listed above – lack of context.

Starting in October 2019, the BBC’s Moscow correspondent Steve Rosenberg did several programs dedicated to the fall of the Berlin Wall. During the Christmas to New Year’s period, the BBC aired one program which consisted of two parts. In the first half, Rosenberg considered the impact of the withdrawal of Russian forces from East Germany on the Russians themselves and interviewed the former chief of those forces, who explained at length how they “came home” to shocking living conditions in the provinces, how they were abandoned to their fate by their own government. The tone of the reporting was sympathetic to Russians’ hardships and it was good that their side of the story from the ground up was given the microphone. What implied criticism there was of the powers that be came from a patriotic source. However, the second half of the program was turned over to a certain Lydia Shevtsova, a very outspoken Putin-hater, formerly with the Carnegie Center Moscow, till she was finally booted out and moved to a more congenial and supportive think tank, Chatham House, in London, where her anti-Russian vitriol is encouraged and disseminated by her co-author, ex-British ambassador to Moscow Sir Andrew Wood. Among the gem quotations which Shevtsova delivered was the claim that Russia under Putin is a declining power which is capable only of disrupting the world order, a spoiler not capable of any creative or productive contribution. Of course, Shevtsova has a right to her opinions, however the BBC had an obligation to its audience to explain exactly who the lady is and, if they wanted to practice fair play, to offer an alternative interpretation of what Vladimir Putin’s Russia stands for on the global stage today. They did not do either. The result was pure propaganda not news and analysis.

As for violations in the categories one and two above, a very good example arose following the recent publication of a study performed by the Levada Center public opinion polling organization in Moscow during October which showed that “53 per cent of 18-to-24 year-olds wanted to leave the country.” This was written about by many of our news peddlers, including FT. The decision to feature this factoid and use it to support claims that the Putin regime’ is a failure fits well with tendentiousness of our news coverage. Meanwhile, nearly all coverage of that study, including in the Financial Times, offered no contextual information whatsoever, when the context was begging to be told.

The article in FT which carried the Levada Center findings was published on 9 January as “Generation Putin: how young Russians view the only leader they’ve ever known.” The remarks on Levada followed directly on another statement begging for context: “Youth unemployment in Russia is more than three times the rate of the total population, according to 2018 data, compared with just twice the rate in 2000.”

First, as regards those 53% would-be “leavers,” one might ask: and so, why don’t they just leave? Russia today is truly a free country: anyone other than convicted felons who wants a passport can get it, and get it rather quickly. And thanks to the efforts of their remarkably hardworking Ministry of Foreign Affairs, most of the world welcomes Russian travelers without a visa requirement. But for that matter, getting a Schengen visa for the EU is not so complicated either.

However, those 53% are, in fact, not going anywhere. They are just sounding off about their youthful disgruntlement with a world created and run by their parents.

At the same time, as the Financial Times editorial board knows full well, young, middle-aged and even old have been leaving the Baltic States, Bulgaria, Romania and other former Soviet Bloc countries in droves, for the past thirty years up to the present day. That was the subject of an article published in the FT on the next day, 10 January 2020 under a title which speaks for itself: “Shrinking Europe.” The states I mentioned here have seen 25 and 30% loss of their population to citizens voting with their feet and departing the shrinking economies and personal prospects which result directly from deindustrialization and economic colonization by Germany and other founding Member States of the EU since 1991. The issue appears in the news now because, as the FT explains, “Andrej Plenkovic, the Croatian prime minister, has decided to elevate population decline to the top of his agenda as Zagreb assumes the EU’s rotating presidency.” Good for him! Now that the skeleton has finally come out of the EU closet, all the stories about Russia’s demographic crisis can be put in context – by those few who wish to do so.

Second, as regards unemployment in Russia today, I believe that similar ratios of youth unemployment to the general population unemployment can be found most everywhere in Western Europe if not in the world at large. The fact that this ratio has worsened comparatively in Russia since 2000 may be explained by the anomalous situation in Russia prevailing throughout the 1990s in step with the economic collapse that accompanied the transition to a market economy. Precisely the older generations, those over 40, were thrown into the street and their children or grandchildren were the first to be hired by the newly emerging industrial conglomerates, not to mention by Western multinationals settling in. What has happened since 2000 is merely a reversion to more normal distribution of employment and unemployment in the population as the Russian economy stabilizes.

Moreover, it would have been helpful had the author named the current level of youth and general unemployment in Russia. In fact, the general unemployment in Russia stands at something like 5%, so youth unemployment would be 15% by his reckoning. I assure you that there are many EU Member States that would be delighted to have similarly low unemployment rates. Here in Brussels the general rate has been over 20% for ten years or more, while youth unemployment has always been considerably higher.

Dear Reader!

For those who find my examples above too subtle to support my argument for egregious propagandistic treatment of Russia in our media, allow me to introduce violation number three, silence, in a way that should sweep away all objections to my thesis.

I draw your attention to an event that occurred in the past week about which you probably know nothing, or perhaps a wee bit from the odd man out reporting in the Wall Street Journal and a few other outlets. I am talking about the visit of Vladimir Putin to Damascus on Tuesday, 7 January. To their credit, the WSJ carried a short article in their 8 January edition, but went no further than to note this was the second visit by Putin since the Russians joined the fight in support of President Bashar Assad back in September 2015, turning the tide in the civil war his way. That is true, but only represents a tiny slice of what all our journalists, including the WSJ’s could have and possibly did learn from watching Russian state television on the 7th. What our media chose not to report was passed over in silence because it shows the complexity of Russia’s policy in the Middle East that includes but goes well outside the domain of pure geopolitics. This is so not least because of the date chosen for the visit, which happens to be Orthodox Christmas.

On the evening of the 6th, that is to say on Christmas eve, by the Russian Orthodox calendar, Russian state television broadcast live coverage of the Christmas service in the Christ the Savior cathedral in Moscow officiated by Patriarch Kirill, with prime minister Medvedev present on behalf of the Government. Then it cut to the service in St. Petersburg, where Vladimir Putin sat in the congregation, as is his custom. The commentator mentioned in passing that the Patriarch’s father, a parish priest, just happened to be the one who baptized Vladimir Putin as a child where they all lived, in the Northern Capital.

The next coverage of Putin on state television was from Damascus on the 7th, where he obviously arrived on a night flight from Petersburg. I did not see video coverage, perhaps because the journalist pool was very limited for security reasons. But still photos and reports on state television informed us that Putin had not merely held talks with President Assad on the Russian military base outside the capital, but had strolled together with him down the streets of Damascus, had visited the main church in the (still existing) Christian quarter of the city, had presented to the Patriarch of Antioch an icon of the Virgin and had also gone on to visit the city’s oldest and largest mosque.

What you have here is precisely the second line of justification for Russian presence in Syria alongside military/geopolitical reasons: resuming Russia’s 19th century role as protector of the Orthodox population in the Holy Land and the broader Middle East. A similar role was exercised back then by France on behalf of the Catholic populations, but that since has been totally negated by rampant secularism and multiculturalism in Western Europe.

It also has to be said that Putin’s visit to Damascus was back-to-back with other very high visibility political statements: his visit to Istanbul on the 8th for the official opening of the TurkSteam gas pipeline and for lengthy talks with President Erdogan that ended in a joint statement calling for a truce in the Libyan civil war for which Russia and Turkey support opposing sides; and his visit on the 9th to Russian naval exercises in the Eastern Mediterranean that included the launch of Russia’s latest hypersonic missiles, the reality of which U.S. and other Western experts have yet to acknowledge.

With this I rest my case on the unfortunate propagandistic behavior of our media which deprive the broad Western public of any chance to make sense of the most dangerous military and political standoff of our age.

* * *

Gilbert Doctorow is a Brussels-based political analyst. His latest book Does Russia Have a Future? was published in August 2017.

Middle Age Misery Peaks At 47 For Most Americans, Study Finds

Middle age can be a miserable time, particularly for a certain cohort of Gen Xers who are struggling through divorce, a dead-end career, insufficient savings or overwhelming debt.

But David Blanchflower, a professor at Dartmouth College and former BoE policy maker, examined data across 132 countries to measure the relationship between wellbeing and age.

And what he found surprised him, according to Bloomberg.

He concluded that every country has a “happiness curve” that’s U-shaped over a typical lifetime.

“The curve’s trajectory holds true in countries where the median wage is high and where it is not and where people tend to live longer and where they don’t,” Blanchflower wrote in a study that was published Monday by the NBER.

For most of the developed world, the age of peak unhappiness is 47.2 years old.

Most of a person’s middle years are miserable, according to the study. But oddly enough, as we approach the golden years, we start to appreciate life a little bit more.

Perhaps that has something to do with approaching retirement age (something millennials might never reach). Or maybe it’s simply the wisdom of age.

But for most of life, expect the misery to get worse before it gets better. Just one more reason why Americans are seeking mental health advice in droves.

This may not be a surprise to many males, but human females are unlike the rest of the animals on earth. Human females have a unique and totally differentiating factor from nearly all other animal life; their bodies cease being capable of pregnancy approximately half way through their life cycle. This natural change to sterility (menopause) does not happen in the animal kingdom (nor in human males) essentially so long as they live (ok, actually there may be a couple of whales and porpoises that may also go through menopause…but I digress). Animals and male humans are still able to reproduce nearly until the end. But not human females. Even before menopause fully takes over, typically around 50 years of age, fertility rates drop radically after 40 and miscarriages surge among those able to get pregnant. By 45, pregnancies essentially cease.

What the hell does this have to do with economics, you may be asking yourself?

Judging the size and change of humankinds population is quite different than any other species on earth because of this truncated period of fertility among human females. Thus, to gauge the direction of our species, and the future consumption and potential economic activity, we must focus on annual births versus the 20 to 40 year-old female population and understand that the post childbearing, 40+ year-old female population is, from a fertility perspective, simply an inert echo chamber. The 20 to 40 and 40+ year-old populations shown below through 2040 are not estimates or projections but actual persons which already exist and (absent some pandemic, world war, or change in life spans) will slide through the next 20 years. All data (except where noted) comes from the UN World Population Prospects 2019 and they collect / compile all the data from the national and regional bodies. The only real variables in what I’ll show below are immigration, deaths, and births over the next 20 years. I also primarily focus on the world excluding Africa. Africa consumes so little, has relatively very low emigration rates, is highly reliant on the rest of the world for it’s economic growth, but from a population perspective, is growing so rapidly as to skew the picture.

But at the onset of a declining childbearing population (excluding Africa) and ongoing declines in fertility rates, the UN projects that the decline in births (excluding Africa) since 1989 will only continue. But I’ll show why significantly lower annual births are far more realistic than the UN projections. And given nation after nation is reporting “shocking” declines in births in 2018 and again 2019…the estimated numbers of births are only set to be significantly lower as something very momentous is appears to be happening.

Last 70 years…

1950-’89 +32 million annual births, +375 million female 20-40 year-olds, +320 million female 40+year-olds

1989-’20-17 million annual births, +230 million female 20-40year-olds, +680 million female 40+year-olds

Next 20 years…

2020-’40-10 million births annually by 2040, -32 million female 20-40year-olds, +435 million female 40+year-olds

Below, looking at the same data as above, but focusing on the year over year change of 20 to 40 year-olds (red columns) versus the same for 40+ year-olds (blue columns), annual births (black line), and federal funds rate (yellow line). From a global population perspective, the 1980’s were the turning point; federal funds rate peaking in 1981 (restricting access to capital as the growth in global demand was at its zenith), annual childbearing female population growth peaking in 1985 (adding nearly 18 million females in that year alone), and annual births subsequently peaking in 1989. Since 1989, the under 40 year old annual growth keeps decelerating, the births keep declining, and the federal funds rate moving lower.

In 2020 or 2021, the global childbearing population of females (excluding Africa) will begin outright declining. The only thing rising was the annual growth of the 40+ year old population. However, the echo of annual growth among the post childbearing female population will peak around 2028…and then rapidly begin the deceleration glide path (still growing, but much slower while the childbearing population will continue to be in outright decline indefinitely).

Looking at the pictures through the global regions.

East Asia (China, Japan, Taiwan, S/N Korea, Mongolia)

For East Asia, 1989 was peak annual births, and the crossover point of post-childbearing outnumbering childbearing was in 2000. Births continue tanking and so is the childbearing female population. Only the fertility-wise inert post childbearing population continues soaring. By 2040, the region is set to reach a 2.8 post-childbearing to childbearing ratio. The higher this ratio moves, the greater the financial and societal pressure of elderly generations on the younger generations…further negatively impacting fertility rates and economic demand/growth.

China

2020 births will be about 50% lower than the 1989 peak, and given the known decline of a minimum of 45 million females of childbearing age by 2040 (and almost 70 million fewer, or -30% fewer, than the 2000 peak) there is really no good reason (other than massive government intervention) that births don’t fall significantly further. My guestimate in blue is likely to be far too “optimistic”. By 2040, there will be more than 2.7 post-childbearing females for every potential mother. And now a trade deal with a nation that has an indefinitely shrinking domestic demand and massive housing over-capacity, factory overcapacity, etc. for a population (let alone middle class population) that will never be coming…hmm, interesting.

Japan

If Japan were a human, now would be about the time to bring in hospice care. From a growth perspective, they are terminal as even the 40+ year-old segment is now making its turn to decline along with births and the childbearing population. By 2040, there will be more than 3.7 post-childbearing females for every potential mother. What saved Japan during the long decline in domestic demand, a long rise in global export demand…is now over. The Japanese / German models of reliance on exports to make up for decelerating/declining domestic demand was premised on fast rising global demand which is simply no longer supported by a growing population of potential consumers.

South Korea

Again and again I am shocked when I look at South Korea. The 70% collapse in annual births will only continue picking up speed to the downside as those capable of childbearing are in freefall…while the 40+ population dwarf’s the under 40 year-olds by more than 2 to 1 now and will be almost 4 to 1 by 2040 (a done deal, not a prediction). Absent state mandated pregnancies (or the like) births will fall in excess of 80% and may even be down 90%+ by 2040? A society collectively choosing not to reproduce or replace themselves…essentially committing a collective suicide at a time of the most relative plenty Korea has ever known, it boggles the mind!?! Again, collapsing domestic demand while global export markets are turning away and inward to meet their needs…it boggles the mind and this is not going to be pretty.

Eastern Europe (Russia, Belarus, Bulgaria, Ukraine, Czechia, Hungary, Poland, Moldova, Romania, Slovakia)

By 2030, the childbearing females of Eastern Europe will be nearly a third fewer than existed as of 2011. I am suggesting that given a third fewer potential females of childbearing age and given continuing flat to falling fertility rates…births will be significantly lower than the UN is projecting. The existing decline of 50% is likely to be down something like 70%+ by 2040. Like Japan, Eastern Europe’s post-childbearing population is set to begin declining around 2030, and accelerating depopulation will be the order of the day. 2030 will also be the peak post-childbearing to childbearing ratio at nearly 3 to 1.

Western Europe

Not as dramatic as East Asia or Eastern Europe thanks to ongoing immigration, but the destination is the same. Growing quantities among the post childbearing population and ever fewer births and potential mothers. Almost a 2.9 post child-bearing to child-bearing ratio by 2040. The weight of the promises made to the old to be paid from the young is a crushing weight only further depressing births.

United States

The charts for the US have a big problem, they assume high rates of immigration (primarily of childbearing age) to maintain a flat childbearing population shown from 2020 through 2040. However, the reality is that in 2019, the US had the lowest population growth in it’s history for three reasons, tanking births, net outflow among illegal Mexicans, and far tighter border controls reducing immigration to a relative trickle. Further, the locations that US immigrants are now coming from (China, India) and the education and income levels of the females coming in is with fertility rates even lower than the general US population. Surging costs of living (rent, healthcare, insurance, daycare, education, etc.) beyond income is forcing females to work to avoid financial wreck. Getting married, having children is simply a luxury more and more simply find beyond their means…and given widely available contraceptives, this is more of a choice than ever. Minimum of 2.2 ratio by 2040…but if the childbearing population falls, as I expect, the ratio (and societal weight it represents) will move northward.

Latin America (Western Hemisphere except US/Canada)

Births are declining, the childbearing population is at it’s zenith and will shortly begin its secular decline, and only the post-childbearing population is growing. By 2040, the childbearing to post childbearing ratio will be about 1.8 to 1.

Southeast Asia (Cambodia, Brunei, Indonesia, Lao, Malaysia, Myanmar, Philippines, Singapore, Thailand, Vietnam)

The growth of the childbearing population is over and a decades long period of a flat childbearing population is underway. Births will likely slowly recede with declining fertility rates among a zero growth childbearing population. By 2040, the post childbearing will outnumber the childbearing by a 1.8 to 1 ratio.

South Asia (India, Pakistan, Afghanistan, Bangladesh, Iran, Bhutan/Nepal, Sri Lanka)

Like Southeast Asia, a long period of zero growth among annual births will be coming through the childbearing population beginning in 2030. By 2040, India’s childbearing population will essentially be at it’s peak and the 1.4 post childbearing to 1 childbearing ratio will be ready to rip higher over the next two decades. The engine of population growth among the worlds most populous region has already stalled and begun to reverse although it will take decades before this is apparent in the overall population numbers.

But Africa Will Continue To Populate The Earth!?!

Finally, the chart below shows the year over year change in births among the world (excluding Africa) versus year over year change in Africa, from 1950 through 2040. Note the great gyrations for births among the world (black line) versus the smooth and steady year over year increases in Africa (aqua line)…except that one deceleration around 2018?!? All forward growth among births is anticipated to take place in Africa, essentially just offsetting the declining births among the remainder of the world.

Getting a closer look from 2000 through 2040, the great 2008 through 2018 deceleration (still growing, but much slower) in growth of births among Africa is much more noticeable. Also of import, this UN report came out in early 2019, and the last hard data is through 2018 most everything from 2019 on is projections. So, note the hard data 2008 through 2018 is suggesting the same issues plaguing the worldwide slowdown in births is likely impacting Africa as well. Of course, with a fast rising childbearing population in Africa, the UN demographers immediately project that Africa’s births will return to high year over year increases from 2019 onward…rather than suggesting that the same something that has turned global births upside down world-over will continue to show up in Africa. Definitely something to watch as, again, the only thing keeping global births from really tanking has been Africa, but I’ve a funny feeling this depopulation contagion is likely working it’s way through Africa now.

What is the point of all this?

The global economy is premised on perpetual growth of demand, of supply, of money, of asset prices, etc. But the pre-eminent engine for the growth (at least for the last few centuries) has been a rising population. More people need more of everything. This means more factories, more supply networks, more infrastructure, more homes, more cars, creating more employment, etc. Including more loans and debt being lent into existence, particularly among the younger populations allowing for the purchase of vehicles, homes, etc. in the present to be repaid “later”. But when the collective younger adult population, undertaking the vast majority of leverage, ceases growing and all the growth shifts to older and elderly adults, who undertake relatively low levels of debt or in elderly years move to outright deleverage…the money supply ceases to grow organically and begins to shrink antithetically to a perpetually growing system.

It has been a long run-up since WWII to get here; decades of rate hikes during accelerating demand (constricting supply of money and causing inflation), then decades of rate cuts during decelerating demand (expanding supply of money and causing deflation but simultaneously asset inflation), resultant debt through individuals, corporations, and federal governments, all intertwined with the deceleration of population growth. Since 2009, the Fed is committed to buying bonds so as to avoid a free-market pricing for those bonds and avoid yields on US debt that would soar and consume much/most of the federal taxes collected. The Fed is also now committed to not allow free-market pricing of assets based on decelerating population growth of young and large deleveraging among elderly. I think it is also highly likely the Fed (and/or agents at its direction) are also manipulating precious metals and/or crypto’s so as to hide the severity of the situation.

All of this is inorganic money creation taking place now is to mask the fundamental accelerating weakness that a low population growth can organically support. The Federal government and Federal Reserve have now gone so far that any deceleration in inorganic growth (let alone outright declines in balance sheet, rate hikes, declines in excess reserves, tax hikes, lower federal deficits) have a high potential to take the economy into not a recession but a depression unlike the world has known. The primary ingredients for removing ourselves from previous recessions/depressions no longer exist. Global demand will begin declining indefinitely as this demographic picture plays out and rates back at zero will do little to move the needle (aside from more asset inflation). The fast rising population of elderly will continue to consume less than they did in their prime years and deleverage more…far beyond the capability of the young adults to offset the financial, economic, and currency impacts. The true picture is that a generations reset is likely in the offing before the demographic and depopulation dynamics can be turned around, before the debt can all be extinguished, before the overcapacity can be expunged.

And I guess, the trillion dollar question should be how did we get here? Were the gyrations in the population and subsequent decelerations (and imminent population collapses in many nations/regions) simply the result of birth care becoming widely available, urbanization, female employment rates, etc. etc. that happened of their own accord…or if instead this is by design as central banks had an over-riding mandate since the 1970’s (not unlike China…but by a different means), only now becoming clear?!? Was this simply humankind going beyond itself or was this imminent collapse centrally designed and engineered?