On the heels of President Donald Trump’s attempts to designate Mexican drug cartels as foreign terrorist organizations (FTOs), an attack uncomfortably close to U.S. soil has the Mexican government scrambling and the president fuming. At least 22 died over the weekend as rival cartels struggling for Northern Mexico turf dominance clashed with local law enforcement in Villa Union, Coahuila, an hour’s drive from Eagle’s Pass, TX. The brazen attack seemingly was directed at the Mexican government to send a warning as to who is in charge.

The town of Villa Union was, in effect, shredded, riddled with bullets, as a heavily armed group of alleged cartel members stormed the community in a convoy of trucks. When they attacked local government offices, the federales attempted to intervene. Fleeing, the cartel kidnapped locals and their vehicles, including a hearse on the way to a funeral.

To Designate Or Not

Mexican officials fear that an FTO designation will allow unilateral interventions across the southern border. But Trump is undeterred, saying as much in a recent interview with Bill O’Reilly:

“They will be designated. I’ve been working on that for the last 90 days. Designation is not that easy. You have to go through a process, and we are well into that process.”

At first, there was a lukewarm reception to Trump’s FTO declaration, but now more U.S. government officials support the idea. Former Acting ICE Director Tom Homan believes it’s time for an intervention on Mexican soil. Although he credited the Mexican law enforcement response, he pointed out a failing that allows cartel violence to creep closer to the United States:

“They’re not well-trained, they’re not well-equipped, and they certainly don’t have the expertise at dismantling large criminal organizations like the U.S. law enforcement does. We’ve proven that in Panama with [ruler Manuel] Noriega, we proved that in Colombia with [Pablo Escobar]. The United States can go down to Mexico and help them address this crisis once and for all.”

That is, if the cartels are FTO designated. But securing a commitment from Mexico President Andres Manuel Lopez Obrador — who has been clear in denouncing the terrorist label as none of Trump’s business – is simply a pipe dream so far. Lopez emphatically stands his ground, telling the United States to rethink any offensive action in Mexico: “Our problems will be solved by Mexicans. We don’t want any interference from any foreign country.”

And then we have a dissenting opinion from Ambassador David Johnson, vice president of the International Narcotics Control Board and former assistant secretary of state for International Narcotics and Law Enforcement Affairs. He is lobbying to stay the course:

“Terrorists use violence to expand a political goal. These criminals are interested in money, not politics. They don’t want the responsibility and headaches that come with political control since it could interfere with their profit-maximizing goals. The key reason for not labeling them terrorists is because that is not what they are. They are in it for the money. Period.”

Derek Maltz, former special agent in charge of the Drug Enforcement Administration Special Operations Division in New York, is all for doing whatever it takes to stem the flow of violence. He declared, “Designating the cartels as terrorists and implementing a focused operational plan will save a tremendous amount of lives.”

Trump Is Stubbornly Dug In

Trump has made it his mission to stop illegal immigration, illicit drug trade, human trafficking, and violence on the north side of the shared border. A safer Mexico creates a safer America. With the recent uptick in violence in Mexico, it would seem the country should embrace the help it so desperately needs. Perhaps putting away control issues and focusing on the greater good would make Lopez Obrador and Trump shake hands and get the job done.

Else we may see the violence enacted in Villa Union cross our border.

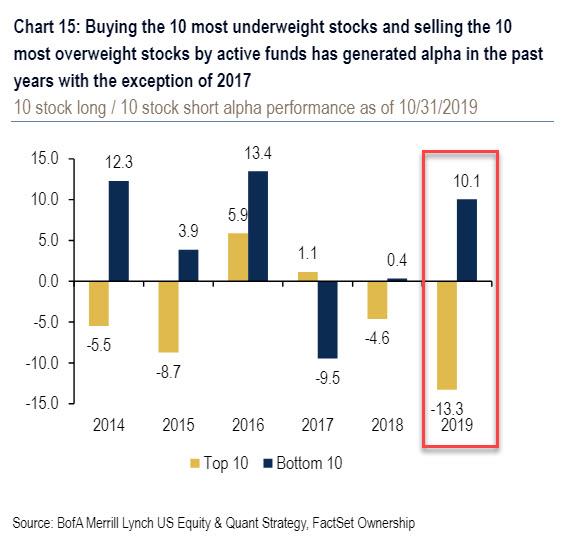

“Is Something Going Wrong? Is Something Broken?” Quants Running “Scared” As Nothing Makes Sense

It was a year where the S&P put the mini bear market of December 2018 in the dust, and after a dramatic reversal which saw most central banks flip from hawkish to dovish throughout the year…

… the MSCI World index is just shy of its January 2018 highs, and the S&P has returned an impressive 24% (despite the jittery start to December), and stands at all time record highs, despite, paradoxically, a year of record equity fund outflow.

On paper, this should have been a great year for investors after a dismal 2018. In reality, however, 2019 has been just as painful for not just for hedge funds, which have substantially underperformed the S&P again and in October saw a record 8 consecutive months of outflows, the most since the financial crisis…

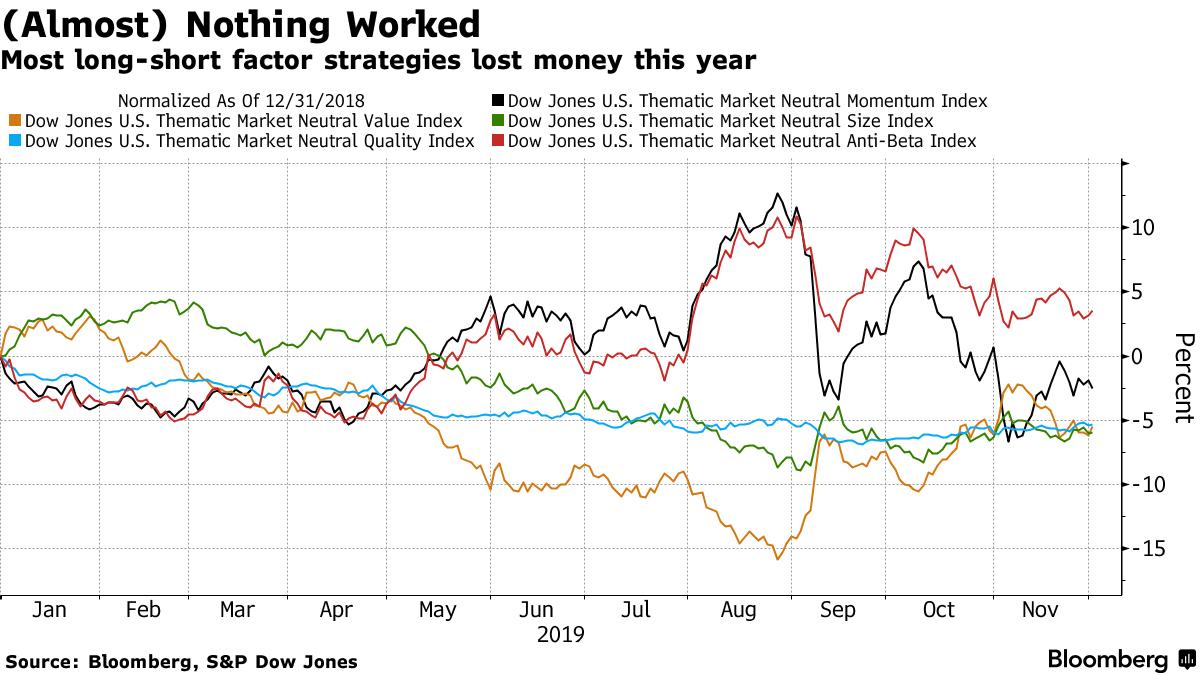

… but especially for quants, which after a relatively solid year, suffered the September quant crash that destroyed most of their YTD gains, and have generally been unable to find their bearings in a year in which nothing seemed to work.

It’s also Georg Elsaesser, a Frankfurt-based fund manager at Invesco, is trying to calm down his newbie quant clients as choppy stock moves make life difficult for anyone trading factors, which wire up all those systematic portfolios on Wall Street.

“Some of them are kind of scared,” Elsaesser told Bloomberg. “They’re asking the questions: Is something going wrong? Is something broken?”

Well actually, the answer is yes: the market is broken, and you can thank central banks for that.

The problem is that the rules-based method of investing based on grouping of stocks by traits like their value, momentum, or balance sheet quality, is misfiring again this year, even more so than it in 2018, when quants suffered their worst year since the financial crisis, and left quant icons such as Cliff Asness’ AQR, suffering its biggest loss since inception.

Here is another problem: while the broader stock market, propped up by central bank stimulus, rate cuts and “NOT QE”, has been on a tear, a peek below the calm surface reveals a tempest of position reversals and catastrophic, at time, performance as a slew of traditional long-short styles are in the red. Market-neutral portfolios have lost 1% this year, according to a Hedge Fund Research index.

While there are numerous, often conflicting, explanations why factor portfolios disappointed in 2019, one can offer some generalizations. Persistent caution over the growth outlook whipsawed riskier trades like value and small caps which slumped all year then soared at the start of September, momentum trades worked all year then got crushed in September, the most shorted stocks soared, and the most heavily owned stocks barely outperformed.

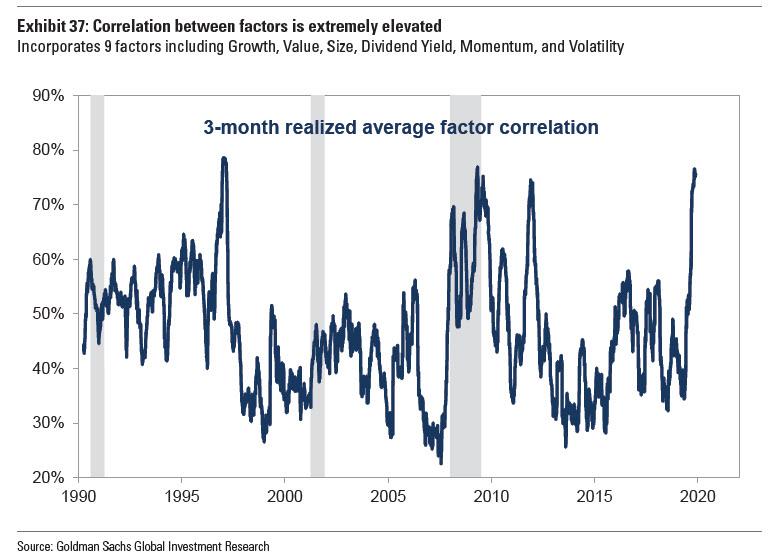

Another, more practical explanation, is that in a world where factors are supposed to offer diversification of risk, they did just the opposite, and the correlation between the most popular factors such as growth, value, size, dividend yield, momentum and volatility exploded. As Goldman wrote in its 2020 year ahead outlook, the average realized pairwise correlation of our factors has reached levels only achieved twice in the last 30 years: in 2Q 2009 as the equity market bottomed in the Financial Crisis and in 1Q 1997 as the Tech Bubble began to build. These elevated correlations underscore the importance that risk sentiment in driving recent market rotations, but more importantly explain why, well, nothing worked, as all of these often conflicting strategies eventually ended up offsetting each other.

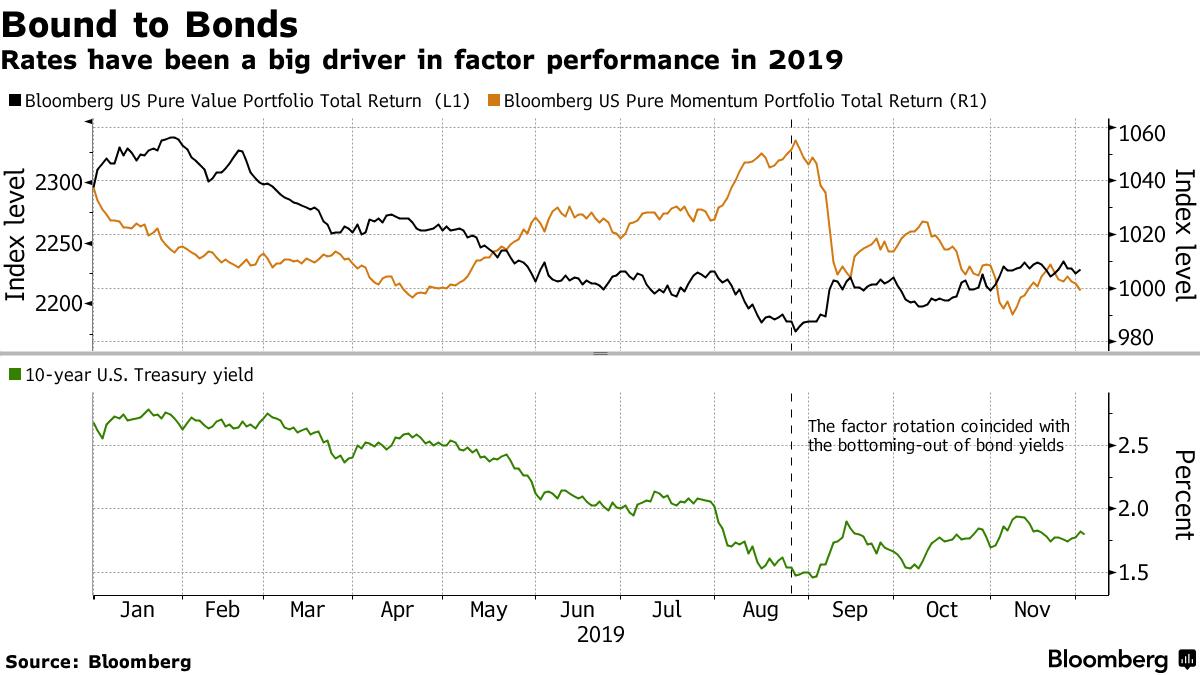

The soaring correlations can also be explained by the bond market: as interest rates dominated factor returns this year, diversification benefits weakened according to analysts at Nomura Instinet.

In light of this dismal repeat performance, it is easy to see why Elsaesser is on the defensive: he is one of many in the systematic community trying to win back hearts with the pitch that factors are time-tested, designed for the long haul and backed by some of the smartest folk in finance and academia (so was LTCM). But as the investing style closes a year to forget, patience is wearing thin among the market-neutral crowd, which plight Bloomberg covered in an article this morning.

“The experienced investors say it’s normal noise in the long run,” Elsaesser said. “But it certainly means we need to explain more.”

You certainly do: after yet another year of carnage for quants, billions of dollars are fleeing the industry which as recently as a few years ago was considered the “next big thing” on Wall Street, now that fundamental analysis no longer matters (again, thanks to central banks).

Sure enough, outflows have soared, and may also have hit industry performance. Market-neutral equity hedge funds lost nearly $4 billion YTD, according to Eurekahedge. Institutions even redeemed $54 billion from long-only quantitative stock funds in the first three quarters, according to eVestment.

However, outflows will continue as long as days like Sept 9 occasionally emerge out of the blue.

On that day, the S&P 500 Index closed flat, equity volatility cruised around its five-year average and commodities were unexciting. Yet factor investors experienced the biggest rotation in a decade after value briefly broke out of its funk at the expense of high-flying momentum stocks. As we showed then, that one day was the most painful for quant funds since the great quant crash of August 2007! And worst of all, nobody knew just why it happened as swiftly as it did.

As a result, Bloomberg writes that quants who failed to diversify into winners like low volatility – which until the September shock would be most of them – are in “soul-searching mode.” Are factors like value structurally broken? Can market-neutral styles roar back to life over the long haul?

The best summary of how nothing for quants has worked this year (and last year) came from Ian Heslop, London-based head of global equities at Merian Global Investors, who did his best LTCM impression: “Some of the themes we expected to diversify our returns in a period of underperformance of value haven’t worked as well.”

That said, it’s not been all gloom. A handful of long-only factor strategies are posting 20%-plus gains this year. But they’re still lagging cap-weighted indexes. Sanford C. Bernstein estimates systematic long-only managers have lagged their benchmark by 2% points on average.

The pain is most acute for market-neutral quants, whose strategies including factor styles gained a paltry 1.2% this year as of Nov. 26 compared with 9.8% for equity long-short funds and 8.7% for discretionary macro funds, according to Credit Suisse data. Recent research by Robeco showed that it was the short legs of factor strategies that have been a drag on performance this year, arguing the value of the investing style mostly comes from the long leg.

Well yes: this is another way of saying that in a manipulated, centrally-planned market, there is no need for short pair trades, i.e., there is no need to hedge. Incidentally, this is precisely what we said all the way back in 2013 when we wrote that the only alpha-generating strategy in a broken market is to go short the most held names and go long the most shorted ones. 6 years later, Bank of America is writing just how correct we were, pointing out that going against the Wall Street crowd has never been more profitable…

And yet, even though we write about this year after year, there will always be those who could never have possibly anticipated this:

“Whether this has been driven by flow events or not, it is finite, it’s very unusual,” said Heslop. His $4.5 billion Merian Global Equity Absolute Return Fund has seen its assets shrink by more than half this year.

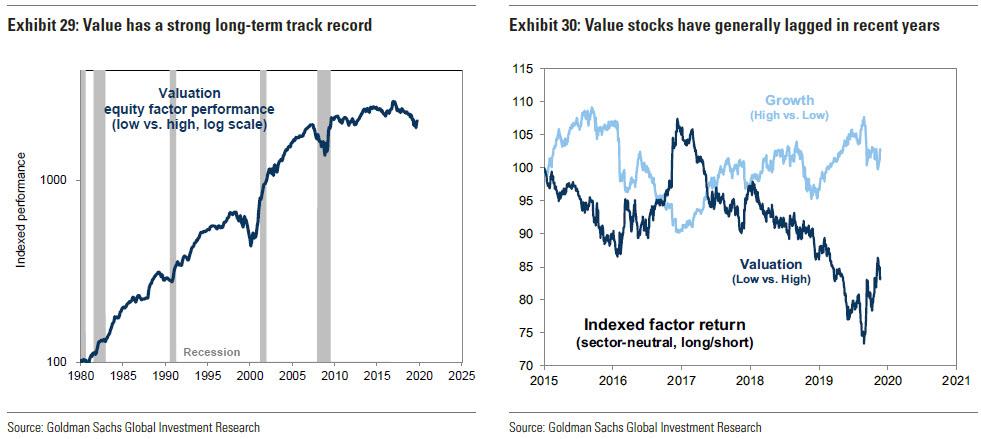

Then there are those who have been betting – year after year – on mean reversion, certain that value was poised for a rebound. They too were left disappointed. As Bloomberg notes, and as we cautioned, since reviving briefly in September, the factor has flatlined since despite JPM’s Marko Kolanovic predicting the value to momentum rotation is a “once in a decade opportunity.” Here, as Bloomberg accurately notes, its outlook continues to divide quant land between bears citing low yields and weak growth, and bulls touting cheap relative valuations.

Alas, neither strategy is beating the S&P500 which is the one asset class directly propped up by central banks.

So where do we stand now?

Well, after another disastrous year for the sector, some quants are revamping strategies. At Merian, Bloomberg notes that Heslop’s team this year tweaked models to penalize exposure to highly correlated factors and to make allocations more defensive against downside risks; it is now on the hunt for smarter definitions of value. The irony, of course, is that most of Heslop’s peers are also doing precisely the same thing, and the outcome will be yet another year of underperformance for quants who are not only fighting themselves, but are also locked in a fight for survival against central banks who have turned the logic of investing and Finance 101 on its head.

Some funds are also deploying alternative data and machine learning in a bid to re-invent now widely known factor strategies. That said, such newfangled methods are a contentious move for a community that’s netted billions riding established factors back-tested over decades. Invesco’s Elsaesser for one is skeptical.

“It’s like a perfect storm for factors at the moment, but they have done what you would expect them to do,” he said. “We’ve seen these drawdowns; we’ve seen them recover. We know the essence of them is the very strong factor logic.”

There is just one problem: when you have a centrally planned market, you don’t have logic. We wonder just how many more year it will take the best and the brightest to finally grasp this simple observation which we have been pounding the table on since our inception in 2009…

Investing is all about probabilities. If the perceived odds of an event are high, certain securities will be priced based on those expected probabilities. The corollary is that when an event is perceived as almost impossible, securities do not price in any chance of it occurring. If that event does occur, all sorts of securities need to re-price—often quite rapidly. I like to spend my time pondering what potential events the market completely ignores. Of all potential economic outcomes, the one that is least anticipated and least priced in, is an uptick in inflation.

It is said that generals always fight the last war. In terms of macro-portfolio wars, Japan’s experience with deflation colors all views. This seems odd to me because we have over two millennia of history showing inflation and currency debasements to be universal constants, with one outlier in Japan. The question is if Japan is the new normal or a true outlier?

Academics have studied the causes and effects of inflation ever since emperors and kings fixated on halting its effects. Despite a massive body of work, there is little agreement amongst experts on the causes of inflation. Since I tend to ignore “experts,” let me start by giving you the Kuppy definition of inflation. “Inflation is when too much of a certain currency chases a scarce resource and pushes its price higher when defined in terms of that currency.” Using that definition, we’ve actually had rather dramatic inflation over the past decade—it just hasn’t shown up yet in the core consumer goods that central bankers are often concerned about.

Did they time-stamp the cyclical low in yields?

When a country prints money, no one knows where within the economic ecosystem it will ultimately flow. If a resource is scarce, it tends to experience inflation—when it is artificially scarce, it has even more extreme inflation. Just think of where the money printing has ended up this cycle; bonds (central banks restricted supply by buying them), stocks (PE and buybacks have restricted supply), gateway city residential housing (local municipalities have restricted supply), medical costs (systematic dysfunction has restricted supply), vintage wines (they aren’t being produced anymore), college education (supply restricted again), I can go on, but you get the point. Meanwhile, traditional inflation stalwarts like food and energy have remained suppressed due to technological advancements, reduced logistical costs and excess liquidity, which has allowed capacity to overshoot and lead to price deflation. To say that we’ve not had inflation over the past decade is wrong, we just haven’t had inflation in places that are key components of the CPI basket.

However, that may be changing. I believe that the number of sectors with restricted supply are starting to expand. Let’s look at labor, which historically has been a primary source of inflation. It’s no secret that US unemployment is at historic lows, laborers now have bargaining power and wages are rapidly increasing—with increases made more extreme by minimum wage laws, healthcare inflation and new mandates in various states. The cost of labor goes into almost every finished good—particularly in a labor-intensive service economy. Politicians on both sides seem willing to pass laws that give labor a bigger share of the pie—what will that do to inflation?

Now think of energy; it’s a crazy world out there and global energy security is no longer guaranteed. Prices have been suppressed for the past few years by excess production due to uneconomic shale—that’s clearly reversing as the funding has been cut off. Where do you think energy prices go if shale growth flat-lines or goes in reverse? What about when key producing regions devolve into chaos? Tanker rates are also expanding—that increases energy prices as well.

Now think about consumer goods; the past few decades were all about increased globalization where manufacturing migrated to the cheapest possible location. Trade wars and regional balkanization upend this trend. Now there ought to be an implicit geopolitical risk premium priced into gross margins on every good. Supply chain disruptions further increase costs. If globalism was deflationary, isn’t the reverse inflationary?

Think about what venture capital has done to costs. Thousands of businesses are losing hundreds of billions a year to gain market share in rather prosaic industries. Think about what Uber has done to transport costs or Chewy has done to the cost of dog food. These are all subsidized by VC firms so they can dump IPOs on unsuspecting retail bag-holders. As these businesses are forced to raise pricing in order to become sustainable, what will that do to consumer inflation? Won’t all sorts of sectors also gain pricing power, now that they don’t have to compete with someone who sells a Dollar for 80 cents hoping to make it up with volume? Isn’t the collapse of the Ponzi Sector bubble inherently inflationary?

What about all the supply restriction as ESG takes its toll on economies? If you can’t get permits to build a new coal mine or oil pipeline, yet demand keeps growing, won’t pricing increase as well?

I can go on and on. All the trends that were deflationary are slowly going in reverse. We haven’t seen the effects of this show up in the data yet, largely because the global economy is rapidly deteriorating, which is putting a brake on the demand side. However, even with the global economy slowing, inflation is starting to tick up in the US. Can the rest of the world be far behind us?

Of course, government policy drives all of this. I think it is obvious that we’ve finally reached the limits of monetary policy. Does the ECB taking rates 10 basis points more negative do anything but accelerate the bankruptcy of the Eurozone banking system? Does it increase consumption or capital expenditures? Of course not. If anything, it just starves the system of capital by taking everyone’s return on capital investment down towards zero and below. Who invests when expected returns are negative? What the world needs is a big reset of the system where leveraged firms default, solvent firms pick up the pieces and get to earn excess returns due to their past fiscal sobriety. Since we live in a democracy, that won’t happen, instead we will have extreme fiscal stimulus in order to kick the can further down the road.

In October, I spent 15 hours in the Sheremetyevo airport in Moscow (damn connecting flight never showed). It hasn’t seen a dollar of cap-ex in years, but it’s still light years ahead of LaGuardia or LAX. Just wait until corporations learn how much they can make from a never-ending airport renovation project. Now multiply that by hundreds of airports in America that desperately need capital investment. Now add bridges, roads, bullet trains, water infrastructure and our electrical grid. Why are all the lobbyists trying to get us into wars with third world nations? Corporations would make more money fixing our infrastructure and it’s going to be a lot less politically contentious.

If you think deflation is a fact of life, you clearly haven’t paid attention to history. Governments around the world have experienced a unique decade where they ran deficits and printed money without “bad inflation” which upsets voters. They think this is a new normal with no consequences. It isn’t. They’re already panicking with the S&P a few ticks from all-time highs. Soon politicians will go into ludicrous mode with fiscal stimulus.

What will fiscal stimulus do to the equity market? I’m reminded of the 1970s—inflation is no friend to most stocks. What happens to trillions in negative yielding long-dated bonds if inflation ticks up? What happens to bond proxies like global large-cap equity indexes or real estate? What happens to risk-parity funds that are leveraged a few times over expecting bonds and equities to increase over time? What if both legs of the trade drop at the same time? No one is ready for inflation, but I believe it’s coming. Maybe not today or next week, but there is a powder keg of monetary supply just waiting to be unleashed by governments who think that inflation can never happen again. At first, markets will cheer a bit of inflation—then they’ll panic. The markets often do whatever the fewest people are positioned for. Who’s positioned for inflation? That’s about as contrarian as buying Argentine sovereign debt.

I think the road-map ahead is a market crash, followed by obscene fiscal stimulus. As always, I’m trying to think a few steps ahead here. I’m making a list of beat-down sectors who benefit from this change in government policy. I want to be ready to buy as soon as they get serious about unleashing the stimulus.

You need a crisis that’s severe enough that both political parties can agree on stimulus. We’re not there yet, but we will be. If you thought QE was nutty, wait until you see what drunken sailor mode looks like. Inflation is coming. Be VERY careful if you own assets with duration risk.

On Wednesday, a Chinese IPO closed below its listing price for the first time since 2012, signaling that the public’s former unquestionable love affair with risk and equities is fading as the economy continues to decelerate,.

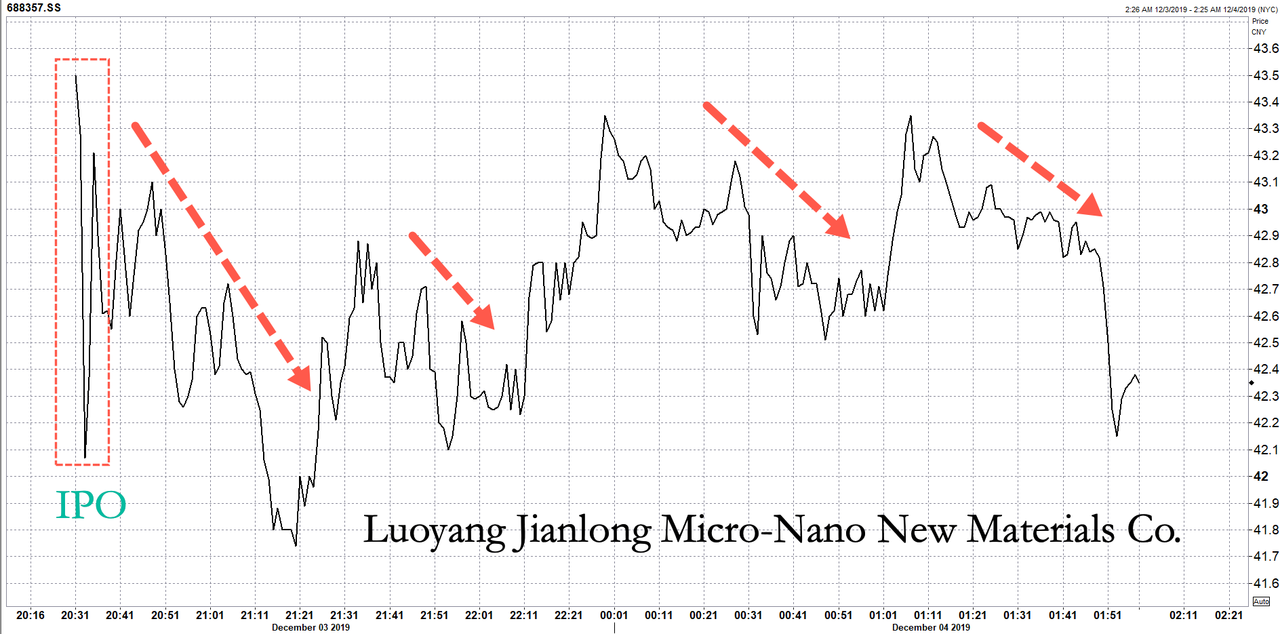

LUOYANG JALON MICRO-NANO NEW MATERIALS SAYS TRADING IN SHARES TO DEBUT ON DEC 4 IN SHANGHAI

Luoyang Jianlong Micro-Nano New Materials shares debuted on the Shanghai Stock Exchange on Wednesday. The stock immediately dropped 7% in the first hour of trading, closing down 2% on the session.

Luoyang Jianlong’s disastrous IPO debut was the first time a mainland Chinese stock closed below its listing price since 2012. The last time this happened, Haixin Foods plunged 8% below its first day listing price in 4Q12.

“Luoyang Jianlong’s debut flop sends a clear signal to the market that buying into IPOs has become more and more risky,” said Jiang Liangqing, a money manager at Ruisen Capital Management in Beijing.

“It will become more difficult for companies to raise money from the capital market as the deteriorating performances of new listings will deter investors,” he said. “On the other hand, it shows that things are becoming increasingly market-driven.”

For at least a decade, China’s IPO market has been one of the strongest in the world, with every newly public stock closing at or near limit-up. Though now it seems large-cap IPOs are showing signs of waning interest from investors as the economy continues to decelerate through year-end, and likely to continue slowing into 1H20. To counter the IPO market bust, China has tried to calm markets by increasing domestic firms with more access to credit to keep equity markets humming along.

State-run media outlets have published frontpage stories telling investors not to worry about the IPO market, and enough liquidity will be provided through 2020.

China’s economy is growing at the weakest point in nearly three decades. A massive turn up in growth in China and across the world is unlikely in early 2020, mostly due to China’s credit impulse faltering.

We warned back in September that the global IPO market was going bust, mostly due to the synchronized global slowdown that has deterred investors from buying IPO shares in companies that don’t make money ahead of a recession.

The rebellion against unicorn IPOs in the US in 2019 shows that investors have lost interest in speculative growth companies. Some of the high-profile US IPO flops this year have been Uber and Lyft. In September, the Peloton IPO plunged 7% below its offering price, making it the third-worst trading debut for a large US IPO since 2008.

How in the world is America supposed to remain “the greatest country on Earth” when other nations are absolutely running circles around us when it comes to education? As you will see below, one survey found that 15-year-old students in China are almost four full grade levels ahead of 15-year-old students in the United States in mathematics. This is one of the most damning indictments of our education system that I have ever come across, and it is yet another clear indication that what we are doing is simply not working. Our children are not being given the tools that they need to compete in our modern society, and we have only ourselves to blame.

Perhaps you are thinking that the survey must be flawed somehow.

Well, this wasn’t some fluky survey that was only given to a handful of students. Every three years, the Program for International Student Assessment evaluates 15-year-old students all over the world in a variety of subject areas, and in 2018 approximately 32 million students participated…

The Programme for International Student Assessment (PISA) is a survey given to 15-year-old students around the world every three years, which tests the core subjects of reading, mathematics, and science. In 2018, 79 countries and economies participated, representing about 32 million 15-year-olds.

When your sample size is 32 million students, I think that it is safe to say that the results of the survey should be taken seriously.

And what the survey discovered is that U.S. students continue to fall behind in math. In particular, we have fallen way, way behind the Chinese. The following comes from Psychology Today…

There is no excuse for the US when students in Beijing-Shanghai-Jiangsu-Zhejiang (B-S-J-Z) performed near four grade levels ahead of US students in mathematics.

In addition, the survey also discovered that the “most disadvantaged” students in China actually performed on par with the average U.S. student…

“The 10% most disadvantaged students in Beijing-Shanghai-Jiangsu-Zhejiang (B-S-J-Z) or in Macao or Estonia… those students actually do as well or better than the average student in the US. So clearly some countries do better with their disadvantaged students, where you see less variability with students from the most privileged backgrounds,” said Andreas Schleicher.

What in the world has happened to us?

We used to have the best education system in the entire world, but now we have become a nation of drooling idiots that can’t even think straight.

Let me give you an example. According to Fox News, a police officer in Los Angeles was recently caught sexually fondling a dead woman by his own body-cam…

The veteran Los Angeles cop, who is assigned to downtown’s Central Division, was caught on his own body-cam footage allegedly fondling the dead woman, and his supervisors have reviewed the video, according to the Los Angeles Times.

The alleged incident took place when the LAPD officer and his partner responded to a call about a possible dead woman in a residential unit, the newspaper reported, citing sources.

That is dumb on so many levels, and now that police officer’s career is over.

Let me give you another example of how dumb we have become. South Dakota has decided to crack down on the meth epidemic in their state, but unfortunately not a lot of thought was put into the advertising slogan for the campaign…

The state of South Dakota has a new anti-drug campaign, but its slogan is raising eyebrows.

Of course it is much dumber to actually be on meth. Approximately 24 million Americans have taken an illegal drug within the last 30 days, and it is getting worse with each passing year.

I know that I am being very hard on the United States in this article, but there is no excuse for what has happened to us.

We were once a great light to the rest of the world, but today a large chunk of our population can barely read, write, speak or function in society. Just consider the following numbers…

#1 One recent survey found that 74 percent of Americans don’t even know how many amendments are in the Bill of Rights.

#2 An earlier survey discovered that 37 percent of Americans cannot name a single right protected by the First Amendment.

#3 Shockingly, only 26 percent of Americans can name all three branches of government.

#4 During the 2016 election, more than 40 percent of Americans did not know who was running for vice-president from either of the major parties.

#5 North Carolina is considering passing a law which would “mean only scores lower than 39 percent would qualify for an F grade” in North Carolina public schools.

#6 30 years ago, the United States awarded more high school diplomas than anyone in the world. Today, we have fallen to 36th place.

#7 According to the Pentagon, 71 percent of our young adults are ineligible to serve in the U.S. military because they are either too dumb, too fat or have a criminal background.

#8 For the very first time, Americans are more likely to die from an opioid overdose than they are in a car accident.

#13 In more than half of all U.S. states, the highest paid public employee in the state is a football coach.

#14 During one seven day period last summer, a total of 16,000 official complaints about human feces were submitted to the city of San Francisco. And apparently the problem is very real because one investigation found 300 piles of human feces on the streets of downtown San Francisco.

#17 Even though we fought a war in Iraq for eight long years, 6 out of 10 young adults cannot find Iraq on a map of the Middle East. And that same survey found that 75 percent of our young adults cannot locate Israel.

#18 Today, the average college freshman in the United States reads at a 7th grade level.

Are you convinced yet?

As a society, we have become exceedingly “dumbed down”, and we can even see this at the highest levels of our government. Just take a look at some of the people we have representing us in Congress. If George Washington, John Adams and Thomas Jefferson were alive today, what do you think that they would make of our current crop of politicians?

When our founders spoke, their language was so elegant. But of course we couldn’t have politicians speak to us that way today because nobody would be able to understand what they were saying.

Our society is literally in a death spiral, but nobody seems to have a way to stop it.

Educating our children properly is one of the most basic things that needs to be addressed, but unfortunately the left has total control of our public schools now, and that means that there is no hope of a major turnaround any time soon.

Elon Musk Tells Jury Despite Being Worth $20 Billion, He’s “Short On Cash”

Just as it did during his deposition, Elon Musk’s wealth became a topic during his testimony at day of his trial versus British cave diving hero Vern Unsworth.

Despite his lawyer’s best effort to object to the question being asked of Musk, the Tesla CEO told the jury that his net worth was about $20 billion, but that he has debt against his SpaceX and Tesla stock, according to Bloomberg. Musk said that contrary to popular opinion, however, he “didn’t have much cash”.

It serves as just another stark reminder of how illiquid Musk’s fortune truly is. Musk has said in the past that he doesn’t intend on selling any of his $14.6 billion SpaceX stake and he has added to his $11.4 billion stake in Tesla during the company’s last financing efforts.

About 40% of Musk’s Tesla shares have been pledged for loans and a May filing showed that Musk had access to about $500 million in credit lines from lenders like Goldman Sachs and Bank of America. His overall fortune is listed at $26.6 billion on the Bloomberg Billionaire’s Index.

It is “unclear” how much of Musk’s credit lines have been drawn upon.

Musk wrapped up his testimony on Wednesday, finishing a cumulative six hours on the stand over two days. Jared Birchall, who runs Excession LLC, Musk’s family office, is slated to testify next.

In the previous day’s testimony, Musk’s lawyers had sought to establish that Musk’s Twitter account isn’t widespread and doesn’t garner publicity. On Wednesday, Unsworth’s attorney continued to examine Musk about it, seemingly catching Musk in his own circular logic.

Wood also asked why Musk made the apology on Twitter. Did he know if Unsworth had a Twitter account? Musk says, “If I write something on Twitter it will get reported, generally.” To which Wood responded, “So you thought your tweet would get widespread publicity?”

— Kerry Flynn 🐶 (@kerrymflynn) December 4, 2019

Vern Unsworth helped play a key role in saving 12 boys and their soccer coach who were trapped in the Tham Luang Nang Non cave in Thailand in July 2018.

Musk had proposed his own solution for the rescue, embarking on a boastful public quest to construct a device that could help rescue the trapped children. But, ultimately, the rescue was done by actual professionals and without the help of Musk.

In a post-rescue interview with CNN, Unsworth laughed off Musk’s proposed solution and told the billionaire he could “stick it where it hurts”, disregarding Musk’s effort as a “PR stunt”.

Musk fired back by calling Unsworth names and insisting that he was a pedophile both on Twitter, and in communications with a reporter at BuzzFeed.

We wrapped up Musk’s first day of testimony, Tuesday, in thisarticle.

Trump May Send Another 14,000 Troops To Middle East To “Deter” Iran

In the latest reversal to his campaign promise to bring American troops home, the Trump administration is considering “significantly expanding” the US military footprint in the middle east, by sending as many as 14,000 additional troops, along with military hardware and a dozen ships to the Middle East, the WSJ reported.

If confirmed, the deployment would double the number of US military personnel who have been sent to the region since the start of a troop buildup in May. The decision whether to send thousands more American soldiers into harms way is expected to be made as soon as this month.

So how will Trump face the electorate with elections in less than a year, and justify his decision to keeps deploying more US troops abroad instead of bringing them back home? Simple: he will blame everything on Iran. As the WSJ notes, on Iran—and partly at the behest of Israel—Trump is convinced of the need to counter the threat his aides say Tehran poses. Apparently that means deploying thousands more troops to places like Saudi Arabia, which already is the biggest US purchaser of weapons yet somehow is incapable of defending itself from those constant “Iranian attacks.”

And this is where the US military industrial complex – which is only paid when more troops are deployed, not when they return – comes into play:

There is growing fear among U.S. military and other administration officials that an attack on U.S. interests and forces could leave the U.S. with few options in the region, officials said. By sending additional military resources to the region, the administration would be presenting a more credible deterrent to Tehran, blamed for a series of attacks, including one in September against oil facilities in Saudi Arabia. Iran has denied involvement.

Ironically, while the new deployment is designed to be a deterrent against possible Iranian retaliation – for mounting sanctions brought about by Trump no less designed to leave the Iranian regime with no way out but military escalation – apparently nobody has considered that a build up of even more American military resources in the region will only further provoke Tehran. Then again, this is the same “thinking” that led to the 2014 Ukraine (and Crimea) fiasco when NATO was “shocked” that its threat to expand into Ukraine would prompt Russia to become take appropriate retaliatory steps.

John Rood, the Pentagon’s senior policy official, on Wednesday hinted at an expanded deployment to counter Iran. Mr. Rood said no decision has been made on additional capabilities but that the situation is expected to remain fluid.

“Deterrence is dynamic, our response is going to be dynamic,” he said at a breakfast with reporters.

Should Trump approve the plan, the additional US troops would join the roughly 14,000 service members already in the region since May, when American intelligence analysts “identified a threat” from Iran and the U.S. Central Command commander, Marine Gen. Frank McKenzie, requested additional ships, missile-defense platforms and troops.

So far that threat has failed to materialize in anything more than an occasional staged false flag attack on some tanker sailing through the gulf.

A Furious Scalise Demands To Know Why Schiff ‘Spying’ On Nunes, Journalist

Contained within a 300-page report on the Democrats’ impeachment investigation was a startling admission; House Intelligence Committee Chairman Adam Schiff (D-CA) had obtained call recordsbetween Rep. Devin Nunes, Rudy Giuliani, Ukraine intermediary Lev Parnas, and journalist John Solomon.

In response, House Minority Whip Steve Scalise (R-LA) said “It raises a lot of serious questions,” before demanding to know what Schiff was up to.

“I want to know all the people Adam Schiff is spying on,” Schiff told the Washington Examiner. “Are there other members of Congress that he is spying on, and what justification does he have? He needs to be held accountable and explain what he’s doing, going after journalists, going after members of Congress, instead of doing his job.”

The records showed calls between Nunes and President Trump’s personal lawyer, Rudy Giuliani, and calls between Nunes and Lev Parnas, a Giuliani associate now under indictment for funneling foreign money to U.S. political candidates.

Schiff said the calls raise questions about whether Nunes was involved in what Democrats believe was a scheme to undermine Trump’s political rival, former Vice President Joe Biden. –Washington Examiner

On Tuesday, Schiff said “I find it deeply concerning at a time when the president of the United States was using the power of his office to dig up dirt on a political rival, that there may be evidence of members of Congress complicit in that activity.”

Nunes says he doesn’t recall speaking with Parnas, and that any discussions with Giuliani would have likely revolved around the Mueller report.

“I remember talking to Rudy Giuliani, and we were actually laughing about how Mueller bombed out,” Nunes told Fox News on Tuesday.

Democrats claim that the Nunes call records reveal that he’s been coordinating with the Trump administration and Giuliani to go after former Vice President Joe Biden, who has been credibly accused of corruption in Ukraine involving his son Hunter.

Democrats have been critical of Nunes since his tenure as the House Intelligence Committee chairman from 2017 to 2019. During that time, Nunes made a trip to the White House to inform Trump his transition meeting messages were intercepted by U.S. intelligence.

“I always felt that Mr. Nunes was a dividing character,” Democratic Rep. Bill Pascrell of New Jersey told the Washington Examiner. “We know of his meetings with the president, which he had every right to do by the way. But in the peculiar position he was in, it was obvious where he was getting his orders and how he proceeded. And I think he’s going to get what’s coming to him.”

Majority Leader Steny Hoyer said “there are serious questions” about the calls between Nunes and Giuliani and Parnas. He said Democrats “need to look at them and see what action ought to be taken, if any.”

Hoyer declined to say whether it would be in the form of a House ethics investigation or a punitive House floor measure.

“I want to have input from other people before I opine on what we ought to be doing. I will be doing that,” he said. –Washington Examiner

The call record produced by House Democrats also reveal calls in late April between Lev Parnas and journalist John Solomon, a previous columnist for The Hill who has broken several bombshell stories regarding the Russia investigation and the Bidens.

“I’m interested in why he was doing this,” said Scalise of Schiff. “And under what authority.”

For more than a year, I’ve been strongly encouraging readers to consider buying gold.

In fact, almost exactly one year ago to the day, I wrote that gold was cheap relative to just about every other asset class in the world.

Since then, gold has been one of the best performing investments in the world.

Over the last 12 months, the price of gold is up 18.8%, handily outperforming everything from the S&P 500 index in the US to stock markets in China, Europe, and Canada, plus bonds, real estate, and even major commodities like oil.

Source: Bloomberg

Gold has even outpaced the stock prices many of the world’s most popular tech investments like Netflix, Tesla, Amazon, etc.

(One of the more interesting exceptions has been Bitcoin, which has more than doubled in value over the last 12 months. We’ll talk about that another time.)

But while gold’s investment performance has been great, I want to tell you today why that doesn’t matter one bit to me.

According to data published by the World Gold Council (WGC), in the last quarter alone, both retail investors and a number of large hedge funds have been piling into gold.

That’s certainly been one factor driving prices higher. But to be frank, that sort of demand is extremely fickle.

The WGC data show that most small investors are buying into gold ETFs (which as I’ve explained previously is probably the dumbest way to own gold.)

Gold ETF buyers are NOT long-term investors. They’ll most likely sell the minute gold prices start to fall.

Hedge fund managers won’t hesitate to sell either, especially if they need to boost their quarterly returns.

So, long-term, gold prices won’t be driven higher by fickle investor demand.

The real demand that’s worth watching comes from foreign governments and central banks– institutions with such a heavy appetite that they buy gold by the metric ton.

In the third quarter of this year, Turkey bought 71 metric tons of gold. Serbia bought 9 metric tons of gold in the month of October alone.

Poland doubled its gold reserves last year. And China has been gobbling up not only gold, but gold miners too.

It’s critical to understand that foreign governments and central banks tend to be buyers of gold. They’re rarely sellers.

In fact up until very recently, there was even an agreement among some of the world’s largest central banks to not sell their gold in order to ensure price stability.

And according to freshly-minted international banking regulations, gold is now considered to be a “zero-risk asset” for central banks and large financial institutions.

This is important– because a number of central banks and foreign governments are really looking for alternatives to diversify away from the US dollars.

Right now the US dollar is still the world’s most popular ‘reserve’ asset… meaning that just about every foreign government, central bank, and large commercial bank on the planet holds US dollars.

China alone has TRILLIONS of US dollars in reserve.

But for the past 20 years or so, the US government has increasingly used its currency, economy, and financial system as a weapon to threaten foreign countries.

If you cross the US government, you’re threatened with sanctions, tariffs, and all sorts of financial penalties.

Think about it– with so many problems and disputes looming, why would a country like China continue accumulating US dollar reserves? It doesn’t make any sense.

And that’s why so many countries are starting to stockpile gold instead. It’s the best alternative to US dollars, and they’re buying up as much as they can.

These foreign governments and central banks do tend to report their gold purchases. But it would be remarkably naive for us to assume they’re giving us the full story.

Why would China willingly tell the world precisely how much gold they’re accumulating? There is absolutely no benefit for them to be transparent. So the real numbers could be far, far greater than what the official statistics say.

This is ultimately what’s going to keep driving long-term gold demand.

Individual investors and even big hedge funds will come and go. But foreign governments and central banks are very likely to continue hedging against the US dollar… and gold is literally the ONLY sensible alternative right now.

This is definitely going to have a positive impact on the gold price. But it doesn’t guarantee higher gold prices over the next year or two.

Roughly half of all gold demand comes from industry (primarily tech manufacturing) and jewelry. And both of these will take a big hit in the next global recession… which could cause the gold price to fall.

And that’s the point I want to convey today. Yes, it’s possible to make money with gold. But frankly there are far more lucrative potential speculations out there, including gold miners.

If you bought gold today and the price soared to $3,000, you’d double your money.

But if you bought shares in a gold exploration company that discovers a huge gold deposit, your shares could increase in value by 2,000%.

The decision to own gold should never be about the investment gain. Gold is a hedge against uncertainties and risks. And there are a lot of those in the world.

We gladly buy insurance policies to protect our homes, cars, boats, and businesses against various risks.

Plus we buy life insurance insurance, liability insurance, and disability insurance to protect our families against the unknowns.

This is a great way to think about gold – it’s like a private, fully redeemable insurance policy with steady cash value and zero counterparty risk.

And when combined with a properly structured retirement plan, it can be very tax efficient.

Gaetz Goes Off On Self-Described ‘Snarky, Bisexual’ Impeachment Witness After Attack On Barron Trump

One would think that House Democrats looking to impeach President Trump would attempt to strengthen their case by inviting moderate constitutional experts to offer measured, yet cogent arguments on why Trump’s interactions with Ukraine are in fact impeachable.

Instead, they peddled three hyper-partisan scholars in front of the House Judiciary Committee who had an obvious emotional investment in impeaching Trump, over claims that he abused his office by asking Ukraine to investigate credible allegations of corruption by former Vice President Joe Biden and his son Hunter.

The lone moderate, a conservative, was George Washington University professor Jonathan Turley, who told House Democratsthat by attempting such an ill-founded impeachment they are the ones abusing their power.

WATCH: Jonathan Turley to Democrats on impeachment:

At one point, self-described “snarky, bisexual Jewish woman” Pamela Karlan – a Stanford law professor who hates “The rich, pampered, prodigal, sanctimonious, incurious, white, straight sons of the powerful” took aim at 13-year-old Barron Trump while trying to make the point that President Trump isn’t a monarch.

In response to Karlan’s comments, Rep. Matt Gaetz (R-CA) slammed Karlan, first asking her about contributions to Hillary Clinton – before calling her out for obvious contempt towards conservatives – including Barron Trump. Gaetz suggested she may not recognize how insulting she’s being “from the ivory towers of your law school,” adding “when you invoke the president’s son’s name here. When you try to make a little joke out of referencing Barron Trump, that does not lend credibility to your argument. It makes you look mean. It makes you look like you’re attacking someone’s family … the minor child of the President of the United States.”

Gaetz ends by suggesting that if “wiretapping a political opponent is an impeachable offense, I look forward to reading that Inspector General’s report because maybe it’s a different president we should be impeaching.

The White House issued a statement in response to Karlan, saying “Only in the minds of crazed liberals is it funny to drag a 13-year-old child into the impeachment nonsense. Pamela Karlan thought she was being clever and going for laughs, but she instead reinforced for all Americans that Democrats have no boundaries when it comes to their hatred for everything related to President Trump.

Hunter Biden is supposedly off-limits according to liberals, but a 13-year-old boy is fair game. Disgusting.”

“Every Democrat in Congress should immediately repudiate Pamela Karlan and call on her to personally apologize to President @realDonaldTrump and the First Lady for mocking their son on national TV.” – @kayleighmcenany