Credit Crisis Unfolds In China As Steelmaker Default Sparks Contagion Fears

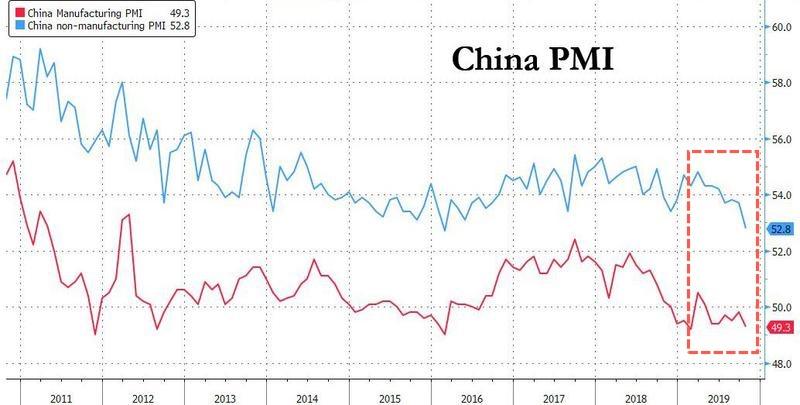

China’s manufacturing PMI slumped deeper into contraction on Thursday — as economic growth in the country fell to its weakest pace in three decades. The economic slowdown, coupled with massive corporate leverage, has created a ticking debt time bomb, which could explode in the next global recession.

The unraveling and coming debt crisis in China will take a series of corporate debt defaults to spook investors, and perhaps, the first series of defaults has already started.

The latest causality is Shandong-based steelmaker Xiwang Group Co., who defaulted on a $142 million bond last week, has sparked contagion fear with other companies in the same region, reported Bloomberg.

Then on Wednesday, Shandong Sanxing Group Co.’s 2021 dollar bond and China Hongqiao Group Ltd.’s dollar bond due 2023 plummeted to their lowest levels ever as contagion from Xiwang’s default continued to frighten investors.

“Xiwang’s default onshore has raised concerns that other privately owned enterprises in Shandong, particularly those from the same locality, may have been associated with the firm,” said Wu Qiong, executive director at BOC International Holdings Ltd. in Hong Kong, who spoke with Bloomberg.

China’s onshore credit markets continue to erupt with stress after 2019 defaulted bonds have already hit 2018 highs.

Fitch Ratings said the default rate of all Chinese issuers in the first three quarters of this year was 1.03%. By historical standards, the default rate is much higher than last year. Most of the firms skipping out on bond payments were private entities.

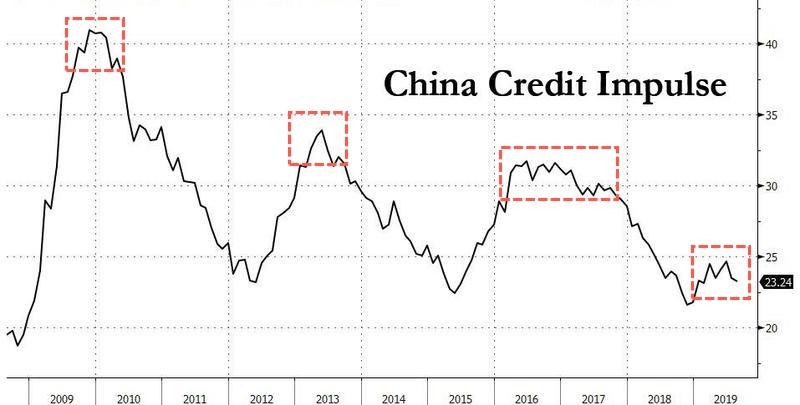

The cash crunch comes at a time when overleveraged companies in China are reeling from a global synchronized slowdown and a controlled deleveraging period by the government to create a soft bottom in the economy.

“Defaults are likely to continue rising, as many medium- and small-sized private firms are facing significant refinancing pressures,” Zhang Shuncheng, associate director of corporate research at Fitch, said in an interview. “Private companies suffer from many problems in their own operations, not to mention the impact from the slowing economy and tight credit environment.”

China’s corporate sector downfall is overleverage, taken on during the global synchronized recovery. Now, a synchronized decline, these firms are starting to deleverage, adding to the downward pressure in the economy.

Hedge fund manager Kyle Bass, the CIO of Hayman Capital Management, has famously said China’s coming economic crash could be three to four times bigger than the 2008 subprime crisis.

Bass said in August, China’s “recklessly built” banking system could come tumbling down in the next global recession.

As long as Beijing refuses to spark a massive credit injection spree, the global economy will continue to falter — this could usher in the next global crisis, one where China’s corporate sector implodes, well that’s at least what Bass thinks…

China is one of the most important economic stories as it and the US have been the main contributors to global GDP growth in this cycle.

As we know, Trump has been driving his trade agenda and has forced China to negotiate; but discussions are stuck on three key points:

Forced knowledge and technology transfer in exchange for Chinese market access

IP theft

State subsidies for key industries

So why are these the key points and why is China so unwilling to negotiate on them?

The answer is that China is an authoritarian state, ruled by the Chinese Communist Party. Their ‘pact with the people’ has been growth, peace and stability in exchange for one party rule. It has worked pretty well for the economy, albeit with large imbalances built up.

As China recovered from the Cultural Revolution, the first stage of growth was in basic industries, then more advanced industries, then high tech and now aiming to be global leaders in new high tech industries.

So how do you make the leap from basic industries to high-tech? You put state resources into education and you invite foreign tech companies to set up manufacturing bases to access cheap labor. You also force knowledge transfer and allow domestic IP theft.

That growth strategy has brought China to the upper level of middle income status with median wages of around $12k a year. Below is a chart showing China’s progress relative to the US from 1960 to 2008 (the most recent one I could find). While China has moved up, relative to the US, its still in middle income status and there are a large number of other countries that are stuck in the middle income trap:

Targeting high-income jobs and industries

If we set aside development issues like corruption, capital flight, inefficient SoEs, lack of basic rights; in order for China to keep growing and avoid the so called middle income trap and get to high income status, China needs to generate hundreds of millions of higher income/ high productivity jobs, mainly in domestic services, but a significant number in goods producing and globally competitive export industries.

Put simply they need global leader companies that can compete in their markets. The problem is the global technology/ pharmaceutical/ biotech/ high end industrial markets are protected by patents and trade secret laws and the owners of those patents are US/ EU/ Japanese companies. To survive without subsidies in most mature global industries you need to be in the top 3 of each segment and while Chinese companies can achieve that domestically, they usually can’t globally.

So China needs to target the new industries where they can register patents and achieve scale and competitiveness. So the government provides state subsidies to companies like Huawei to help them become global leaders in the new markets as they open up. These are the same new markets that US/ EU/ Japanese companies want to compete in. But the Chinese companies can operate at break even or a loss for as long as it takes to drive foreign competition out of a new market. They can also invest whatever it takes in R&D for these new industries.

Trump is pushing back against this development model. But the problem the CCP has is their growth pact. They have to deliver higher standards of living and productivity to avoid falling into the middle income trap and these three core policies are their strategy to deliver it. Without these policies, it is not clear to me how they will create the numbers of high income jobs they need in order to escape middle income status. Then China would become little more than a large market for high end western goods, similar to Russia or India.

So overall it seems unlikely that China will make a full compromise on these areas and for now they are saying these key principles are non-negotiable. I suspect that next year they will try and position a compromise that is in their interest and does not effectively stop this development model.

If Trump does not really want a deal and just wants to make it look like he tried hard before ending negotiations and putting more tariffs on, he has the excuse already. I think this outcome is likely, but that Trump wants the bad news to come out in stages. Partly to not roil markets and partly as it takes years to reposition supply chains.

Hong Kong protests, could they spill into China?

The Arab Spring came about because a baby boom of young men born in the 1980s came of age, couldn’t find work and saw no future. It seems that the Hong Kong protests have similarities. Young Hong Kongers, who have no allegiance to the CCP, live in what is a developed market, but cant afford property and lack the basic self-determination rights.

The Hong Kong authorities can act to bring down real estate prices, but giving democracy and greater rights seems to be incompatible with the Mainlanders not having those same rights. My former colleagues, who are Chinese and based in Hong Kong, are expecting a ruthless crackdown on the protesters by the CCP at any time.

The risk is that leads to more protests and more loss of control or even the protests starting in China itself. My former colleagues are fairly sceptical of this spillover happening, given CCP brainwashing and control of media and communications. They also think the CCP would ruthlessly end any initial Mainland protests, out of sight of the global media.

But I think this comes back to the common issue. If the CCP fail to deliver their growth pact and China starts to stagnate in middle income status, with many economic imbalances built up or starting to unwind, perhaps there can be protests in China as well.

If that happens and the CCP start to lose control, it would trigger a 1997-style Asian and EM meltdown as commodity prices and the flow of USD’s to EM collapse. While China runs a large trade surplus with the US and EU, it runs almost a $200bn goods deficit with Asia and EM.

I don’t know how likely it is that Mainland protests start and my former colleagues are confident they would be ended ruthlessly, as the CCP’s primary aim is survival, but given the potential of this scenario, its worth considering the possibility and the impact it could have.

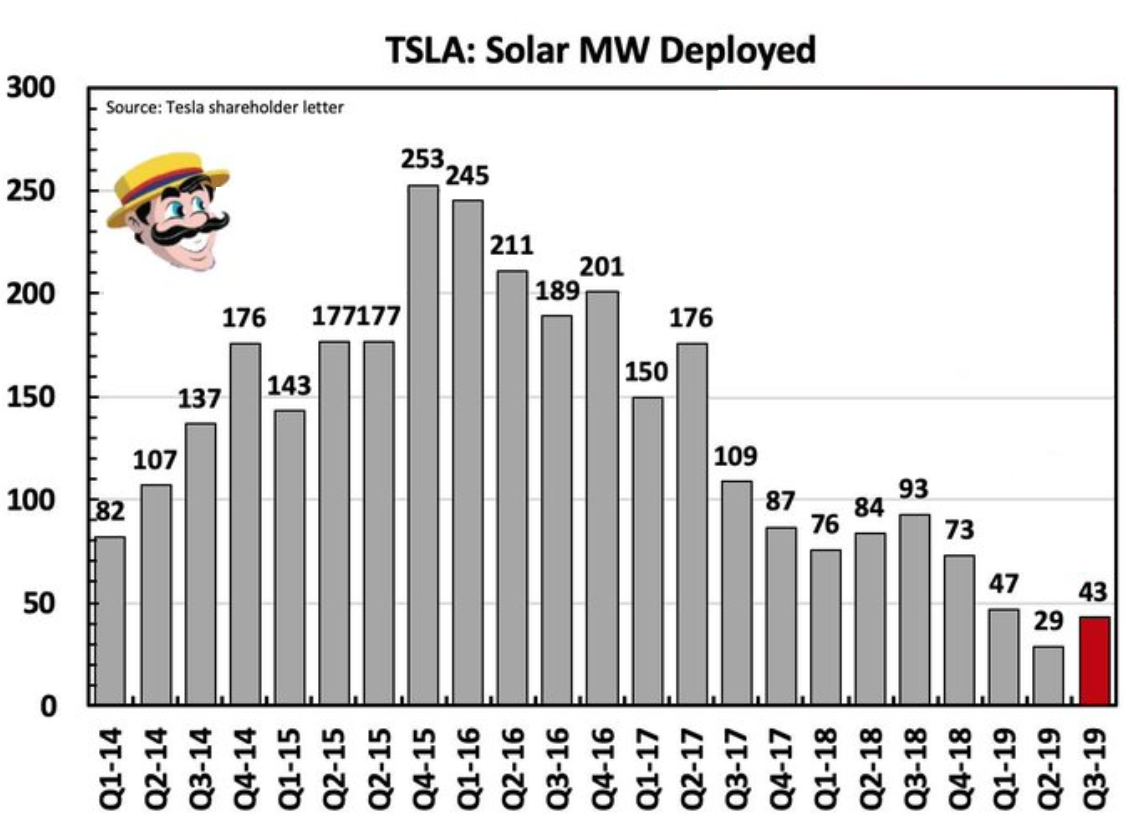

Musk Admits Tesla “Would Have Gone Bankrupt” Without SolarCity Employees Helping Model 3 Production

The SolarCity shareholder lawsuit discovery continues to bear highly disturbing insights into how Elon Musk and his merry band of brothers were running their “pyramid” of money losing companies – SpaceX, SolarCity and Tesla – back in 2015 and 2016.

Most recently, it was revealed that Musk shifted resources from SolarCity in order to save Tesla from bankruptcy while it was preparing to produce the Model 3, according to Bloomberg.

Musk said in a June pre-trial deposition: “If I did not take everyone off of solar and focus them on the Model 3 program to the detriment of solar, then Tesla would have gone bankrupt. So I took everyone from solar, and said: ‘instead of working on solar, you need to work on the Model 3 program.’ And as a result, solar suffered, as you would expect.’’

Of course, at the time, no such disclosures were made to investors.

Musk also acknowledged in the deposition that he “probably wouldn’t support” the SolarCity acquisition again given the stress that Tesla faced during its Model 3 push.

Musk said: “At the time I thought it made strategic sense for Tesla and SolarCity to combine. Hindsight is 20/20. And if I could wind back the clock, you know, I would say probably would have let SolarCity execute by itself; would have let Tesla execute by itself. But I just didn’t realize how difficult it would be to do the Model 3 program. And so that was just a big distraction and sort of offset a lot of things by more than a year, year and a half maybe.’’

To help alleviate the pressure of the Model 3 ramp, Musk took SolarCity employees from engineering, management, sales and service and transferred them to work on the Model 3. Other SolarCity workers were deployed to Tesla retail stores, while some delivered cars to customers.

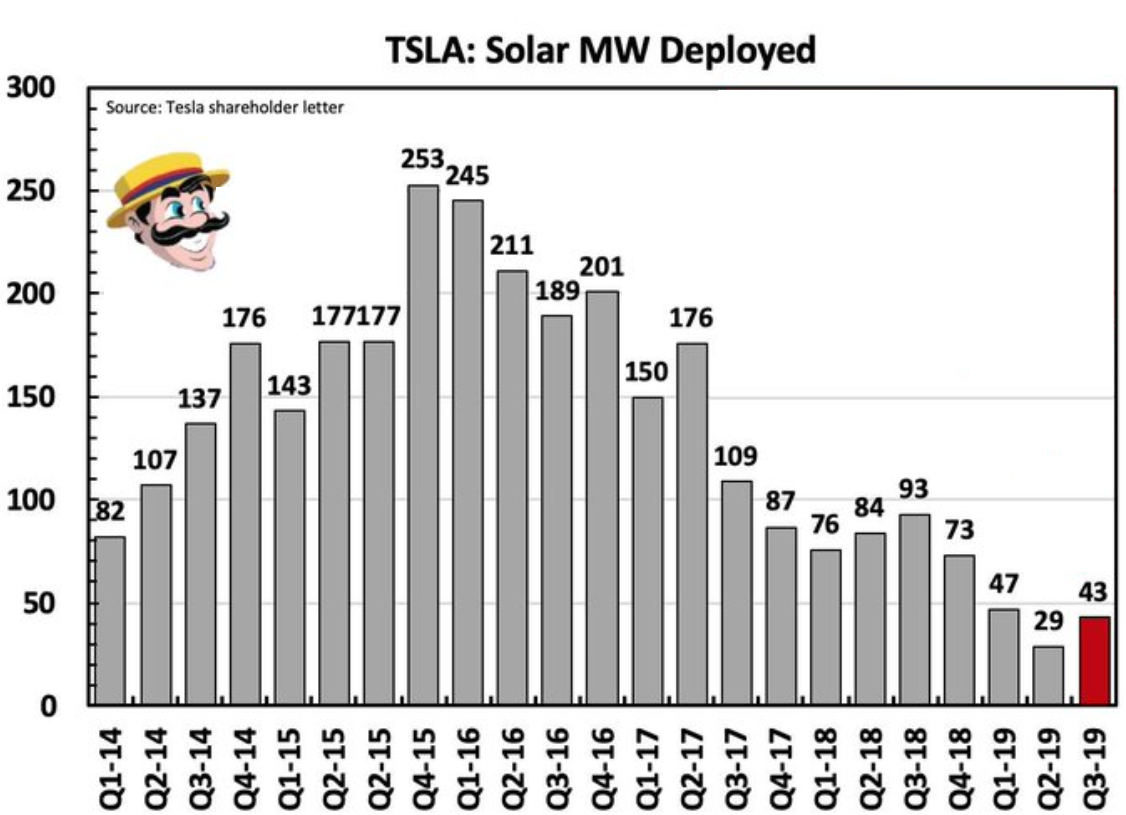

The pension funds who filed the lawsuit against Musk are arguing that Tesla was in no condition to buy a $2 billion company that was already basically insolvent. When Tesla reported Q3 earnings, its rooftop solar business increased for the first time in a year.

Source: @TeslaCharts

And Musk was combative with the lawyer asking him questions about SolarCity’s health at the time, Randy Baron, even calling him “reprehensible” when he questioned whether SolarCity was a viable entity.

Musk continued in the deposition, saying to Baron: “You seem like a very, very bad person. Just a bad human being. And I hope you come to regret your actions in the future, but you probably won’t. And that’s sad.”

When asked if he “bailed out” SolarCity, Musk said to Baron:“Advancing solar is absolutely good for the world. Do you just think about money? What is your purpose in life?’’

“SolarCity would have done just fine by itself and Tesla would have done just fine by itself, but in the long-term, they are better together. And that is what the future will show. That is why I think you should stop wasting your time now,’’ Musk said at one point.

Last week, Tesla introduced its “Version 3” of its solar roof. “It’s been quite hard. Roofs need to last a long time. When you add electrification to the roof, it’s a fair bit of complexity,” Musk said about the product.

Recall, on Wednesday night, we published a comprehensive timeline laying out Kimbal Musk’s SolarCity margin calls that occurred prior to the failing company being bailed out by Tesla.

Tesla skeptic and short seller @TeslaCharts also appeared on a podcast on Sunday to lay out his thoughts both on Tesla’s recent quarterly results, and on the company’s claims about its “Version 3.0” of its solar roof tiles.

Recall, we also noted days ago that despite Tesla’s “headline” Q3 numbers, its U.S. sales actually plunged 39% in the quarter.

Illinois Democrats are attempting to muscle through a so-called “fair tax” by amending the Illinois Constitution to eliminate the flat tax. Their strategy has all the subtlety of a shakedown.

Given Democrats’ “pass it or else!” attitude, the “scare tax” seems a more appropriate name. Here’s a Halloween peek at the Democrats’ two-step strategy for raising taxes in 2020 and beyond.

Step 1 is eliminating Illinois’ flat tax via constitutional amendment. First, Democrats will try to convince voters why this is necessary. Due to the Trump revenue bump, Illinois enjoyed a surprise revenue surplus. This bit of good fiscal news was the grease for getting a budget passed.

But spending increased much more than revenue did, and overspending in 2019 helps the Democrats as we enter 2020 and 2021. Here’s how:

This year’s spending spree creates room for spending cuts next year, just as rug merchants of lore raised prices to offer exaggerated discounts to lure the unwary. Indeed, Democrats are already rounding up ideas for cuts, but they are not discussing, much less driving, the structural reforms needed to address Illinois’ fundamental financial problems.

That’s because Illinois’ fundamental financial challenges are a result of the Democrats’ “Chicago Way;” offering government employee unions sweet deals in exchange for support. With reforms that impact their governing coalition off the table, Democrats obsess over raising revenue to fund their status quo – and they understand that spending cuts will be demanded in connection with a tax hike.

So, much like Inspector Renault did in Casablanca, Democrats round up spending cuts they can live with to feign fiscal probity.

Spending in 2019 will exceed revenues, creating a deficit in the 2020 budget; we should expect an “unanticipated fiscal crisis,” which will justify the Democrats’ pro-tax push next year.

“Shocked” by this “surprise” deficit, Democrats will argue this crisis can be fixed with more revenue and that all of the revenue will be obtained from the rich – but only if voters know what’s good for them and vote for the “fair tax.”

And if voters don’t agree to do as Democrats demand? Democrats will argue that the government will fail without new taxes. Those taxes have to come from somewhere; so, tax the rich or be taxed yourself!

And what will happen if the people of Illinois approve the “fair tax,” thereby eliminating the constitutional protection against arbitrary tax rates? Will doubling the tax on the rich spare the rest of us from paying more taxes too?

Of course not.

The Democrats’ “scare tax” won’t spare anyone for two reasons:

First, their tax won’t raise as much as Democrats advertise because the proposed new tax and Illinois’ entrenched structural problems are already scaring people away to more tax-friendly havens.

Second, Illinois’ structural problems are simply too severe to be fixed by raiding the pockets of a few thousand people.

Which brings us to Step 2 of the Democrats’ strategy: tax everyone else.

Lower-than-projected revenues from the “scare tax” will leave a large and growing hole in Illinois’ finances. Guess whose pockets Democrats will raid in 2021, seeking the billions they inevitably need. Having doubled tax rates on the vanishing rich, Democrats will seek a “much lower” increase in taxes on everyone else.

Make no mistake: taxing the rich is only a speed bump on the road to higher taxes for everyone. The only way to avoid higher taxes is to stop enabling Democrats by raising taxes every time Democrats yell “Boo!”

It’s time to force Democrats to fix the structural financial issues fueling Illinois’ demise. That means voting no on the “fair tax.” Cutting off new tax revenue will force Springfield politicians to deal with its fundamental problems. That is the first step toward inviting back to Illinois the productive and ambitious who have been scared away.

Popeye’s Is Escalating Its “Beef” With Chick-Fil-A

For two chicken companies, the “beef” is starting to reach a fever pitch.

On Sunday, November 3, Popeye’s will be bringing back its chicken sandwich, specifically targeting a day of the week when rival Chick-Fil-A isn’t open, according to Bloomberg.

The chain hopes that the sandwich will bring in more customers as competition in the world of fast food continues to grow, as we pointed out in a recent article about the industry’s growing debt problems.

The sandwich made its original debut in August and sold out within weeks. Now, for the second go-around, franchisees are making sure they are fully staffed to meet the demand.

Popeye’s reported comp sales of 9.7% on Monday, almost twice analyst projections, as a result of the sandwich’s popularity. It was called one of the company’s “best quarters in two decades” by parent company Restaurant Brands’ CEO Jose Cil.

Competitor Chick-Fil-A has closed on Sundays since 1946, when the practice was made tradition by the company’s founder.

Restaurant Brands also owns Burger King and is not only facing leverage headwinds and a slowing global economy, but also declining customer traffic. Competitors like McDonald’s are raising prices in order to try and offset the slowdown.

A Fiscal Policy “Flop”: The US Gov’t Spent Hundreds Of Billions, And GDP Slowed

Submitted by Joseph Carson, Former Director of Global Economic Research, Alliance Bernstein

Its now nearly two year since the Trump Administration and Congress passed major tax cuts for businesses and individuals and followed that legislative initiative up with a relatively large increase in spending for defense and discretionary non-defense programs. The economic results from these tax and spending programs are in and the overall growth numbers are disappointing to say the least, and it would not be wrong to characterize these legislative initiatives as a fiscal policy “flop”.

Over the last seven quarters real GDP growth has averaged 2.4%, which matches the 2.4% growth in 2017, the year before the entire fiscal stimulus took place. Simply put, even though the federal government spent more money (estimated to be $300 billion for various programs) and reduced taxes for businesses and individuals the underlying growth rate of the economy did not change one iota.

As disappointing as the growth numbers have been, the fiscal bill from these legislative initiatives is growing and contrary to public assertions these fiscal stimulus programs will never pay for themselves.

In the fiscal year ending on September 30, the US recorded a $984 billion deficit, more than $300 billion above the budget deficit recorded in fiscal year 2017, the year before the tax cut and spending programs were passed by Congress.

Measured in relation to GDP, the budget deficit equaled 4.6% of GDP in the fiscal year ending at the end of the third quarter of 2019, almost 100 basis points above the 3.7% growth in nominal GDP over the same time frame.

That unbalanced relationship – the budget deficit as a percent of GDP running above the growth in nominal GDP – has been a unique feature of the current decade long business cycle and is something that never ever happened during any other economic expansion of the post-war period. Even if money was free (which it isn’t) there is something wrong with this math.

Budget projections from the Congressional Budget Office indicates that the scale of the budget deficit will continue to outpace the growth in nominal GDP by nearly one percentage point over the next decade. Critics may argue that long run forecasts are notorious for being off the mark, but it is worth pointing out that budget forecasts by CBO in the summer of 2009 under-estimated the growth in the budget deficit for the next 10 years by more than $2 trillion – so to be fair there are upside and downside risks to future budget projections.

It’s premature to say that the US government has entered into a “debt trap”. Unlike businesses and individuals which at some point run into market-determined borrowing limits and face margin calls, the federal government has deep pockets in the form of a “printing press”. Nonetheless, it is impossible to deny that recent fiscal decisions have not worsened the US short run and long run outlay and revenue imbalance. Politicians show no appetite to address the growing budget imbalance so “market forces” (i.e. dollar re-alignment since the US is massively dependent on foreign capital) will eventually at some point reduce the scale of the imbalance.

“You’re Bull*hit Beto!” O’Rourke Flattened By Female Trump Supporter In Viral Pro-Gun Rant

Democratic presidential candidate Beto (Robert Francis) O’Rourke was taken to task by an angry Trump supporter in Newtown, Connecticut – who slammed the former congressman for trying to ‘hijack this town’ and ‘make an issue out of getting guns out of good people’s hands.”

“This is bullshit,” said Rebecca Carnes – a vocal Trump supporter who says she’s a “third-generation” resident of Newtown – where the Sandy Hook elementary school shooting took place in 2012. “It’s about mental health and it’s about this war on boys and masculinity,” she added. “You’re bullshit by being here, shame on you Beto.”

“Why don’t you debate me?“

Here are the top five reactions to Beto’s beatdown on Fox 61‘s YouTube channel, in order of popularity:

“Bitchy Beto can’t say shit cos it’s not Anderson Cooper who’s asking him the questions.”

“It would have great to have seen Beto’s face after that dress down.”

“In Beto’s defense, it is important to remember that Epstein did not kill himself.”

“I’d say that she probably has more testosterone in her system than Beto O’Dork, but I think most women probably do.”

“Good for her.

More people need to be made aware that Newtown has voted more for the republican candidates, in many of the recent local and general elections.

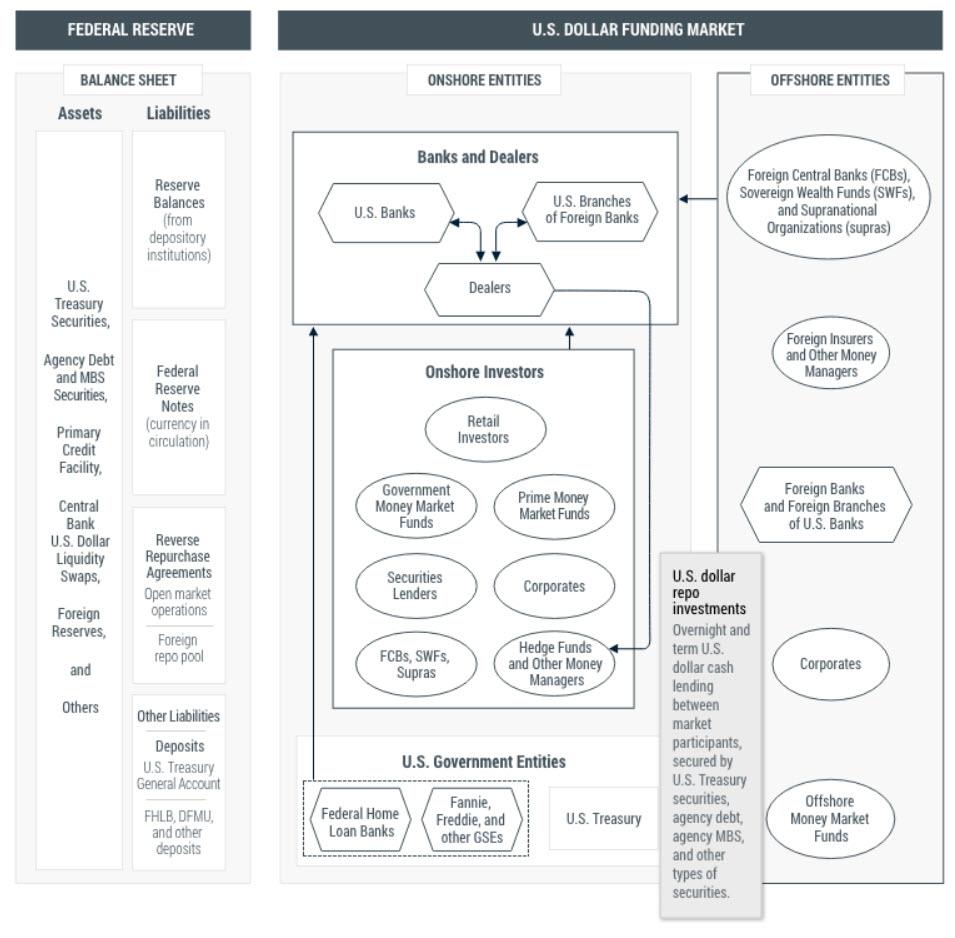

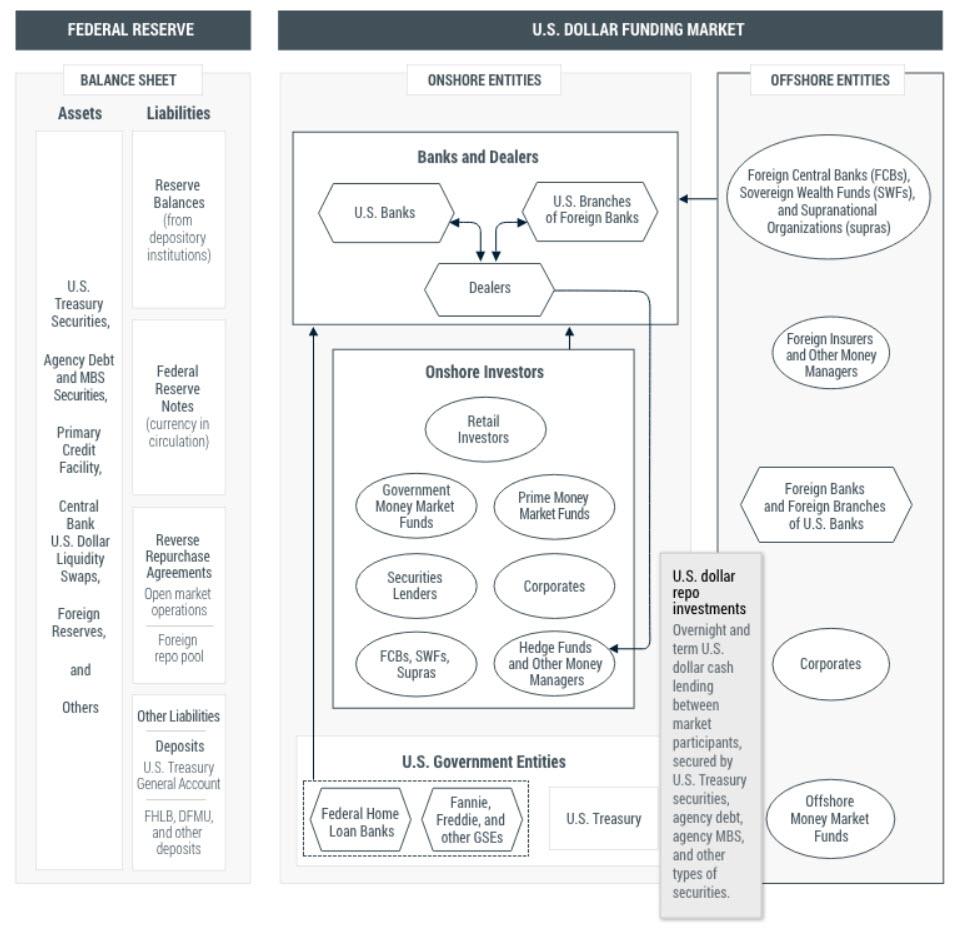

The Federal Open Market Committee cut the target for short-term funds another quarter point last night, raising the question as to whether the central bank can actually defend the 1.75% upper bound of the new policy range. Fact is, demand for short-term funding is pulling rates higher as the year draws to a close.

Ray’s Camp, The Flowage, Princeton, Maine

We got to dine with the risk committee this week, revealing new aspects of the recent repo kerfuffle that deserve mention. Chief among them was the idea of competition and, indeed, even conflict between the retail bank side of the house and the capital markets component inside the Fed’s primary dealers.

It seems that when the Federal Reserve Board was caught napping in mid-September, the bank treasury side of one of the largest US banks basically took a line from the 1990 Martin Scorsese film “Goodfellas” and told the bank’s capital markets side: “Fuck you, pay me.”

Under Regulation W, which implements what we traditionalists know as Section 23A of the Federal Reserve Act, transactions inside the bank holding co do not count against the bank’s statutory allocation for transactions with affiliates. But when market rates spiked, the retail treasury representing a very large insured depository, essentially told the traders to pound sand when it came to price. Reg W requires transactions with affiliates to be at market on an arm’s length basis, even with risk-free collateral supporting the trade.

The lesson here is that regulators do not want the cash-rich retail bank to give carte blanche to the traders, either with respect to the amount of liquidity or the price. The regulatory system worked – but also caused a new problem. A rush of fully motivated capital markets banksters suddenly turned outward and sought funding in the broader market for federal funds.

A squeeze ensued on or around September 16th, needless to say. Risk free collateral went begging for funding. Effective rates to finance Treasury and GNMA collateral spiked to double digits. So then, ask not whether one aspect of federal prudential regulations or another caused the liquidity squeeze seen last December and in June and later in September.

Ask instead why the Fed and other regulators cannot cooperate to tweak the system and fix da plumbing. December is just a month away. The reality, as F.A. Hayek described in his classic 1988 essay “Fatal Conceit: The Errors of Socialism” is that fine tuning the markets is an impossibility. The Fed suffers from the “fatal conceit” that “man is able to shape the world around him according to his wishes.”

Happy Halloween

Softbank Denies WeWork Control??

Meanwhile in the world of finance, a couple of notable events and comments occurred that deserve comment. PIMCO announced that it is reducing allocations to corporate debt, another data point on our worry beads regarding corporate credit in 2020.

Our favorite was the blasé Street reaction to the announcement by Softbank that its 80% stake in the insolvent WeWork did not mean control. Hello?? Further, Masayoshi Son indicated that therefore the company would not be consolidated onto Softbank’s balance sheet. Really? If this transparent evasion of leverage disclosure does not qualify for securities fraud in the US, then we need to buy some new textbooks.

Several managers, ratings firms and former shareholders complained about a “lack of controls” at Softbank in a Wall Street Journal article by Phred Dvorak and Justin Baer, but when one man is in charge is this even up for debate? We have always viewed Softbank as an investor driven Ponzi scheme, but we suspect our readers already knew that.

Of note, we also were reminded over dinner that no less than Deutsche Bank AG (DB) has been the advisor and lender for much of Softbank’s issuance of securities. Would be funny were it not so very sad, especially for the credulous sovereign investors in Softbank. The whole vision thing strikes us as a grotesque speculation verging on outright fraud. On Wednesday, DB reported a third-quarter loss of $955.1 million or about 10% of total revenue, after reporting a profit in the same period a year earlier.

The Softbank strategy goes like this: Give me and lend me enough capital and I will corner the market for innovation or some such version of that theme. We recall that Jim Fisk and Jay Gould attempted a similar operation in the late 1860s. Their machinations resulted in Black Friday September 24, 1869, the first modern financial crisis. Their scheme to corner the gold market – and ensnare President Ulysses Grant in the operation — collapsed in spectacular fashion, leading the US into a credit crisis. Gold, after all, was money in those days.

DOJ/HUD Accord Reached

Hannah Lang of National Mortgage News reports that Department of Housing and Urban Development Secretary Ben Carson announced that HUD and the Department of Justice released a joint a memorandum of understanding, stating that HUD will deal with False Claims Act violations — involving Federal Housing Administration (FHA) lenders — mainly through administrative proceedings. This is a big deal for HUD and the mortgage industry, which has been brutally raped since 2008 to the tune of tens of billions of dollars by a succession of ambitious politicians.

One of the main reasons why Senator Kamala Harris (D-CA), who served as the state’s AG during the 2012 National Mortgage Settlement, won higher office was the billions she extracted from the shareholders of JPMorgan (JPM), Bank America (BAC) et al. And this is why a very angry Jamie Dimon publicly took Chase out of the FHA loan market immediately after, followed by hundreds of other banks.

Today only Wells Fargo & Co (WFC) and Flagstar Bank (FBC) remain as significant bank issuers and servicers of GNMA securities in the FHA/VA/USDA loan market. As former GNMA President Ted Tozer told us last week, without the bond market execution of GNMA-guaranteed securities the FHA/VA/USDA programs are moribund.

We salute Secretary Carson and FHA chief Brian Montgomery for getting this interagency understanding done, but the banks won’t come back to the FHA/VA loan market until 1) the cost of servicing GNMA securities is brought into line with the GSEs Fannie Mae and Freddie Mac and 2) profitability on origination of FHA/VA loans improves a lot more. GNMA MSRs should trade even yield to conventional mortgage servicing assets.

Perhaps the bigger challenge for HUD is convincing the Fed, OCC, FDIC and other prudential regulators to allow large banks to return to the FHA market. So long as the federal regulatory community sees small, low FICO, high LTV loans as being “unsafe and unsound,” the banks are unlikely to return fully to the GNMA market. Small loans are loss leaders. Would you rather service a $280,000 FHA loan for 32bs per year gross or a $3 million prime jumbo loan at 25bps per year?

Are ‘Green Bonds’ The “But It’s For The Children” Trojan Horse For MMT?

While still small, sustainable financing is growing. There’s been $165 billion of so-called “green”-bond issuance from companies and countries this year – more than double 2016’s total – according to data compiled by Bloomberg.

And, under pressure from ‘the people’ demanding policymakers “do something” to save the world from almost certain climate-driven doom, Bloomberg reports that central banks are putting their money-printing malarkey to work in sustainable financing, opening up a new source of demand for the budding asset class.

Most major central banks have signed on to promote sustainable growth, offering incentives that encourage green financing.

“Central banks are important institutional investors, and the fact that they are participating in this market, it gives the market almost like a seal of reliability and maturity,” said Christian Deseglise, global head of central banks and global sponsor of sustainable finance at HSBC Holdings Plc, the biggest underwriter of the bonds this year.

“It’s not so much about adding demand, because we already have demand,” he said. “It’s the quality of that demand that’s really important.”

The European Central Bank has been buying the debt as part of its asset repurchase program.

Hungary and France’s central banks have each created funds dedicated to ecological investments.

Now Peru is considering buying green bonds, too.

While the Federal Reserve, with nearly $4 trillion on its balance sheet, is notably absent from the Network for Greening the Financial System, regional branches have published research on the topic, and Chairman Jerome Powell maintains that it’s a “longer-run issue.”

However, as Bloomberg notes, pricing and liquidity are still limiting factors. As green bonds become more mainstream, investors are offered little additional incentive to buy them as they price comparably to non-green debt.

“As soon as the green-bond market becomes sizable you’ll see central banks investing more in green bonds,” according to Massimiliano Castelli, head of sovereign strategy at UBS Asset Management.

Of course, as most are aware, “green”-bonds are largely a marketing gimmick, and if central banks really do escalate their buying, then you don’t need a crystal ball to forecast that there will be a rise in companies’ “Greenwashing” their issuance – using green labels to spend on not so green things!

The Forest Resilience Bond (FRB) is a financial tool that enables private investment in forest enhancements on public land. The FRB promises to accelerate the pace and scale at which critical work to restore the health and functioning of the nation’s forested landscapes is undertaken.

It does so by engaging private capital to cover the upfront cost of activities to improve forest health and by bringing together stakeholders that benefit from this work to share in the cost of reimbursing investors over time. These beneficiaries sign contracts that jointly cover the project cost plus a modest return to investors, meaning that no one stakeholder shoulders the burden of repayment alone. The result is a collaborative finance model that yields clear ecological, social, and financial returns.

While perhaps less obvious, the FRB model also unlocks opportunities for positive social impact in rural communities across the country. In addition to the direct impact of job creation, FRB projects can catalyze infusions of capital into rural areas by sending signals to the market that there is a steady supply of raw material to fuel forest-based industries. Against a backdrop of declining rural prosperity, this article envisions how the FRB could play a role in assisting rural areas – especially those with historically forest-based economies – transition to a more resilient ecological and economic future.

…

What differentiates the Forest Resilience Bond (FRB) from other approaches is not only its use of investor capital to fund restoration quickly and at scale, but the collaborative model of cost sharing between beneficiaries.

This approach engages a range of stakeholders to split the cost of repaying investors and involves them in project development. As such, the FRB model encourages a collaborative systems-level response to forest health challenges that makes use of funds, experience, and expertise from a range of public, private, and civic stakeholders.

Or, put another way, it’s a public-private partnership that levers taxpayer funds to support ‘green’-led initiatives, without the need for voting (because the central banks are unelected!)

So, to summarize, the concept of “green”-bonds is becoming more and more mainstream – who cares if we don’t get any yield, at least we are signaling just how virtuous we are – and as various ‘wealthy’ western nations hit the monetary and fiscal policy wall, the rhetoric around “People’s QE” or a Modern-Monetary-Theory-driven (MMT) redistribution spreads positively among many (especially the socialism-supporting Millennials).

While common-sense destroys the radical concepts behind MMT, we would argue that “green”-bonds are the perfect trojan horse to create a narrative that monetizing debt “that’s good for the world” is something ‘no one’ can argue with… Let’s just hope not, for the sake of our children’s future loss of purchasing power.

“Central banks are already buying green bonds and they should be buying more,” said Ulrich Volz, director of the SOAS Centre for Sustainable Finance in London. “But at the end of the day we need a mainstreaming of responsible investing across all assets.”

Of course, we look forward to the issuers of “green”-bonds explaining how their bonds mature past the world’s apparent sell-by date in 10-12 years depending on which climate-extremist you ask.

Today, Oct. 31, marks eleven years since the publication of the Bitcoin white paper by the still-mysterious person or group pseudonymously identified as Satoshi Nakamoto.

Bitcoin: A Peer-to-Peer Electronic Cash System — published on Oct. 31, 2008 — outlined a tamper-proof, decentralized peer-to-peer protocol that could track and verify digital transactions, prevent double-spending and generate a transparent record for anyone to inspect in nearly real-time.

The protocol represented a cryptographically-secured system — based on a Proof-of-Work algorithm — in which Bitcoins (BTC) are “mined” for a reward by individual nodes and then verified by other nodes in a decentralized network.

This system contained the possibility of overcoming the need for intermediaries such as banks and financial institutions to facilitate and audit transactions — a major disruption to a siloed, monopolized field of centralized financial power.

Eleven years on, Bitcoin is consistently setting new records for its network hash rate — a measure of the overall computing power involved in validating transactions on the blockchain at any given time.

More power and participation establishes greater network security and attests to widespread recognition of the profitability potential of Bitcoin mining.

As of the middle of this month, network data revealed that since the creation of the very first block on the Bitcoin blockchain on Jan 3, 2009 — known in more technical language as its “genesis block” — miners have received combined revenue of just under $15 billion.

The figure includes both block rewards — “new” bitcoins paid to miners for validating a block of transactions — as well as transaction fees, which broke the $1 billion mark this week.

Bitcoin’s first-ever recorded trading price was noted on Mar. 17, 2010 — on the now-defunct trading platform bitcoinmarket.com, at a value of $0.003.

The cryptocurrency’s appreciation thus stands at a staggering 304033233% as of press time, with Bitcoin currently trading at $9,120.

As of this August, 85% of Bitcoin’s supply in circulation had been mined — leaving just 3.15 million new coins for the future.

Eleven years on, the mystery enshrouding the white paper’s author remains as impenetrable as ever.

Those both within and without the crypto community began attempting to determine Nakamoto’s identity as early as October 2011, just a few months after the mysterious figure first went silent.

{kind=link}

{kind=link}

{kind=link}