JPMorgan Jumps On FICC Revenue Surge, IBanking Beat Even, But Dimon Sees “Weakening Business Sentiment”

Ahead of today’s barrage of bank earnings reports, there was some concerns that between tumbling 10Y yields and a sharp drop in trading this quarter, the two main sources of bank income would be clogged and financial stocks would disappoint. And while that may yet happen, the first company to report, JPMorgan, is higher in the premarket after beating on both the top and bottom line.

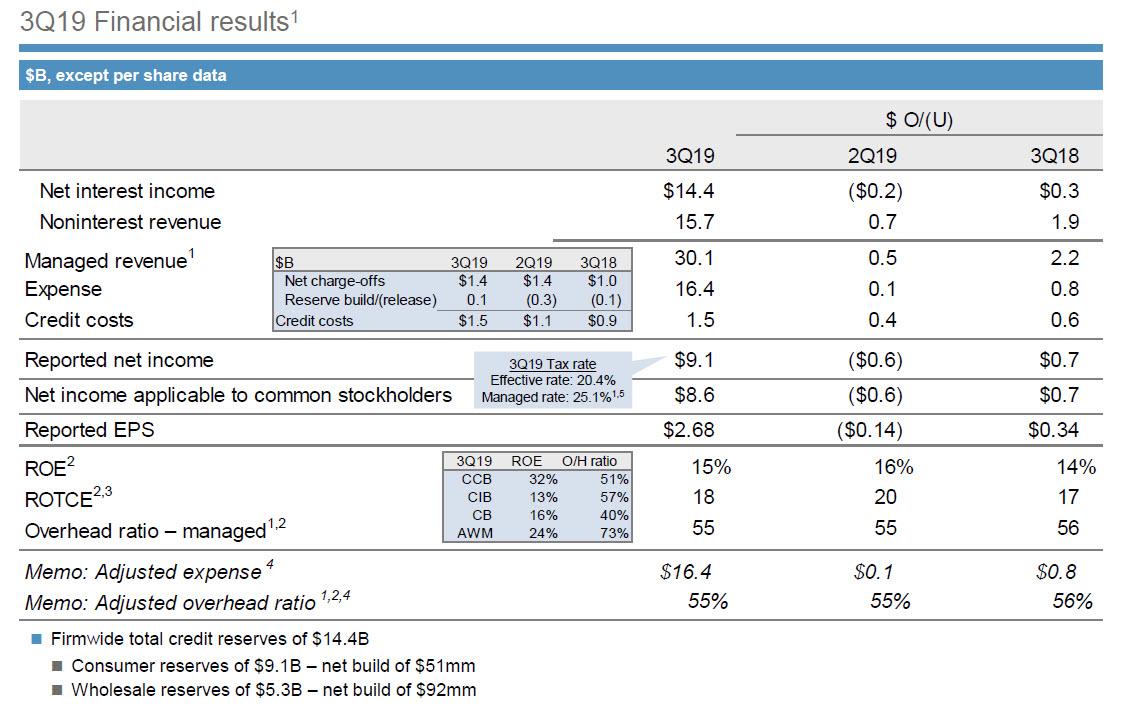

The largest US bank reported Q3 revenue of $29.3BN and manged revenue of $30.1BN, up 8.1% or $2.2 compared to a year ago, both beating consensus expectations of $28.47BN, with earnings rising 34 cents to $2.68, also higher than the $2.51 expected. To get here, JPM reported that its effective tax rate was 20.4%, while its managed rate was 25.1%.

JPM’s closely watched net interest income – a key variable in a time of inverted yield curves – managed to rise 2.3% to $14.23BN from $14.17BN, coming above the highest analyst estimate of $14.20BN. According to Bloomberg, net interest income was up 2% from a year ago, thanks to growing balance sheet and changing mix of assets as declining interest rates bring down margins. As expected, NII growth has collapsed this year for all banks as the Federal Reserve started cutting interest rates. The Q3 net yield on interest-earning assets was 2.41% vs. 2.51% y/y and down feom 2.49% in the prior quarter, in line with the 2.41% estimate.

Not surprisingly, Jamie Dimon mentioned the rate environment in his quote: “JPMorgan Chase delivered record revenue this quarter, demonstrating broad-based strength and the resilience of our business model despite a more challenging interest rate backdrop.”

Yet against this “challenging interest rate backdrop,” Dimon noted the bank’s “consumer lending businesses benefited from our continued investments and a favorable environment for borrowers, which helped drive healthy volumes in Home Lending and Auto and strong loan growth in Card.” Dimon also cited record investment banking fees, and said JPMorgan had “share gains across products and regions.”

Meanwhile, after several quarters of cost-cutting, JPM reported that its total expense rose by $800MM Y/Y to $16.4BN as the period of shrinking for the largest US bank appears to be over.

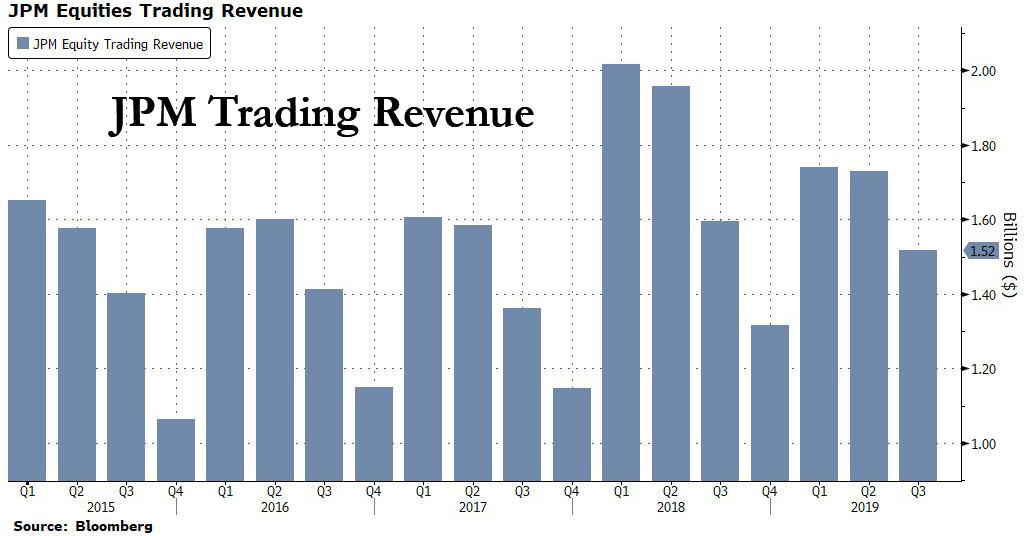

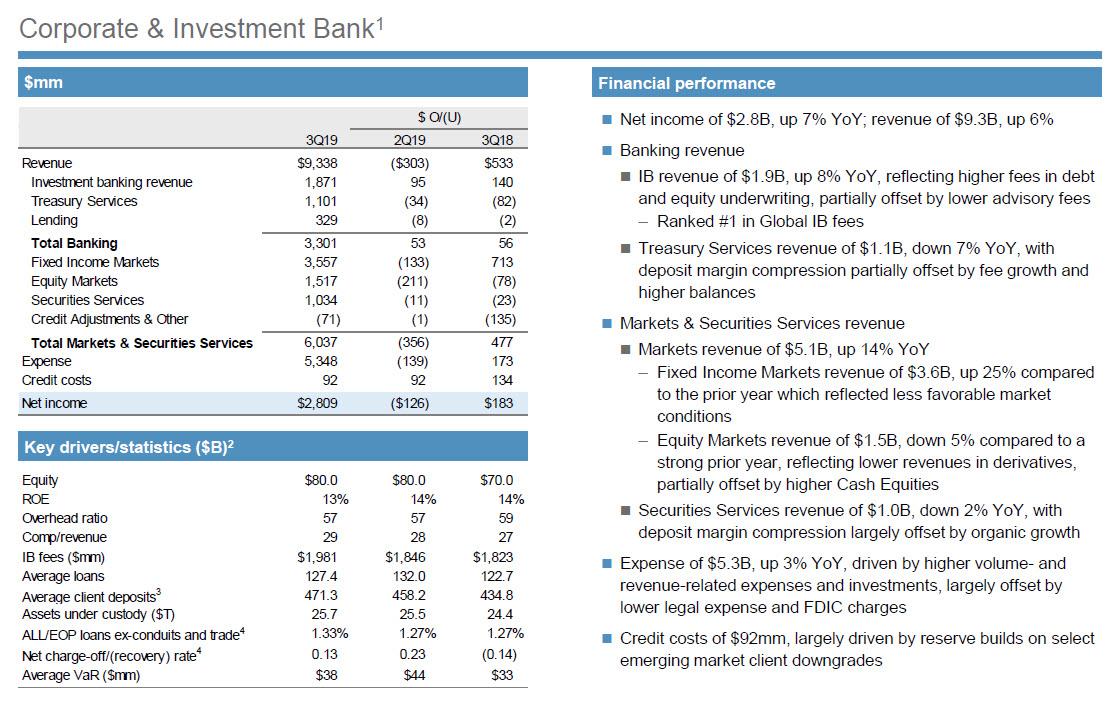

Next, focusing on JPM’s Corporate and Investment Bank, it is here that the bank surprise with an impressive FICC revenue print, which rose a whopping 25% Y/Y to $3.56BN, up $713MM compared to the year ago quarter “which reflected less favorable market conditions.”

At the same time, JPM reported Equity Markets revenue of $1.52BN, missing expectations of $1.66BN and down 5% compared to a strong prior year, “reflecting lower revenues in derivatives, partially offset by higher Cash Equities.”

As Bloomberg puts it, while in the first half of the year, equities were doing better for most big banks and fixed income was lagging, volatility in the past quarter seems to have helped FICC revenue, while depressing equity trading.

Investment Banking also beat, rising 8% to $1.87BN from $1.80BN a year ago, mostly from higher debt and equity underwriting fees. Still, JPM faced lower advisory fees, which was expected in light of the sharp drop in M&A in the quarter.

So a somewhat mixed picture: fixed income up 25%, but equity trading down 5%, which prompted JPMorgan to flag the point that Jamie Dimon brought up in September, namely the prior-year quarter was fairly weak, so the comparison for fixed income makes this quarter’s look a bit stronger than normal.

Offsetting the higher revenue was a 3% increase in expenses, which rose to $5.3B, up 3% YoY, driven by higher volume- and revenue-related expenses and investments, largely offset by lower legal expense and FDIC charges.

Finally, there was an interesting bullet on the IB page with JPM noting that credit costs of $92mm, were “largely driven by reserve builds on select emerging market client downgrades.” One wonders what exactly JPM means by this.

Looking ahead, JPM made the following forecasts:

Expect FY2019 net interest income of <$57.5B, market dependent

Expect FY2019 adjusted expense of ~$65.5B

Expect FY2019 net charge-offs of ~$5.5B

Commenting on the broader economy, Dimon turned decidedly gloomy, mentioning trade tensions and geopolitical worries:

“In the U.S. economy, GDP growth has slowed slightly. The consumer remains healthy with growth in wages and spending, combined with strong balance sheets and low unemployment levels. This is being offset by weakening business sentiment and capital expenditures mostly driven by increasingly complex geopolitical risks, including tensions in global trade. Regardless of the operating environment, JPMorgan Chase will continue to serve our customers, clients and communities globally, while investing in innovation, talent, technology, security and controls.”

Validating Dimon’s gloomy call on the economy, JPM’s provisions in the consumer and community banking businesses climbed 34%. Within the card business, net charge-offs were higher but the bank says that was in line with expectations and partially due to a reserve build as “newer vintages season.” It will be curious what JPM says on this topic even though Dimon said the consumer “remains healthy.”

One final note: there was no mention of WeWork in JPMorgan’s press release or presentation. Overnight, WeWork was said to have preferred JPMorgan over Softbank for its financing package.

Following the strong FICC and IB beat, the stock jumped as much as 2% premarket, rising to $119 a share, just over a dollar away from the all time high of $120.40.

Global markets edged higher on Tuesday even as safe havens were bought as markets tried to balance fading optimism over the latest China-U.S. trade truce with the likelihood of a Brexit deal by Thursday’s European Union summit.

However, S&P futures trimmed dropped a quick 15 points and treasuries rallied after Bloomberg reported China may “struggle” to buy the volume of American goods proposed in the “phase one” trade deal unless the US cuts tariffs.

MSCI’s index of world stocks rose 0.2% with European stocks climbing briefly to a two-week high after comments from the European Union’s chief Brexit negotiator that a deal with Britain over the terms of their divorce was still possible this week. The European STOXX 600 added 0.2%, with 18 of 19 sectors advancing led by retailer shares, with France’s CAC and Germany’s export-oriented DAX both rising while Britain’s FTSE was a touch lower as sterling rose against the dollar and the euro, reflecting the cautious optimism about talks between Britain and the EU.

Yet capping broader gains in equities was a perceived lack of progress coming out of U.S.-China trade negotiations.

Earlier in the session Asian stocks climbed for a third day, led by health care firms, as Japanese shares staged a catch-up rally after a Monday holiday when trade optimism buoyed regional equities. Most markets in the region were up, with Japan leading gains and China retreating. The Topix advanced 1.6% for its biggest gain in more than a month, as Toyota Motor and Daiichi Sankyo provided strong support. The Shanghai Composite Index fell 0.6%, dragged by PetroChina and 360 Security Technology. China’s factory deflation deepened in September due to slowing economic growth and the comparison with faster gains a year ago.

India’s Sensex rose 0.8%, set for a third day of gains, as investors looked toward September-quarter earnings reports. HDFC Bank and Kotak Mahindra Bank were among the biggest boosts for the index

Reports of a “Phase 1” trade deal between the United States and China last week had earlier cheered markets but the dearth of details around the agreement has since curbed this enthusiasm with oil prices extending declines, Chinese stocks weaker and the safe-haven yen holding gains versus dollar.

“Not enough was achieved to alter meaningfully the fundamental global economic outlook,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “Global growth is still slowing and is below trend … There is still scope for earnings disappointment and the remaining uncertainty from trade tensions means business investment is unlikely to improve markedly.”

The focus is now on Europe where officials from Britain and the EU will meet at a make-or-break summit on Thursday and Friday that will determine whether Britain is headed for a deal to leave the bloc on Oct. 31, a disorderly no-deal exit or a delay. The main sticking point remains the border between EU member Ireland and Northern Ireland, which belongs to Britain. Some EU politicians have expressed guarded optimism that a deal can be reached. However, diplomats from the EU have indicated they are pessimistic about British Prime Minister Boris Johnson’s proposed solution for the border and want more concessions. Yet those concerns did little to quash market optimism for now, with Britain expected to make new proposals on Tuesday.

Meanwhile, as algos and buyback programs bought stocks, humans bought bonds, with the 10Y yield dropping to 1.675% while Eurozone bond yields rose with Germany’s benchmark 10-year bond yield was 0.5 basis points higher on the day at -0.45%, flirting with a two-and-a-half month highs reached at the end of last week.

In the currency markets, optimism over a possible Brexit deal lifted sterling by as much as 0.7% to the dollar and approaching a three-month high of $1.2708 and climbing to a five-month high against the euro. The yen, often considered a safe haven in times of economic uncertainty, held steady at 108.33 versus the dollar.

Markets were still analyzing the lack of perceived progress in resolving a prolonged trade row between the United States and China. The United States agreed to delay an Oct. 15 increase in tariffs on Chinese goods while Beijing said it would buy as much as $50 billion of U.S. agricultural products after tense negotiations last week. However, Washington has left in place tariffs on hundreds of billions of dollars of Chinese goods. Trade experts and China market analysts say the chances are high that Washington and Beijing will fail to agree on any specifics – as happened in May – in time for a mid-November meeting between U.S. President Donald Trump and Chinese President Xi Jinping.

Chinese data also added to the woes. The latest numbers showed that China factory gate prices declined at the fastest pace in more than three years in September. That followed customs data on Monday that showed Chinese imports had contracted for a fifth straight month.

Concerns over the health of the global economy weighed heavily on oil prices, with U.S. crude and Brent crude both falling around 1.5% to $52.75 and 58.48 per barrel respectively. By early last week, hedge funds had become the most bearish toward petroleum prices since the start of the year, according to an analysis of position records published by the U.S. Commodity Futures Trading Commission and ICE Futures Europe.

Bank earnings start with Goldman Sachs, JPMorgan, Citigroup and Wells Fargo.

Market Snapshot

S&P 500 futures up 0.6% to 2,981.75

STOXX Europe 600 up 0.6% to 391.93

MXAP up 0.6% to 158.82

MXAPJ up 0.05% to 509.44

Nikkei up 1.9% to 22,207.21

Topix up 1.6% to 1,620.20

Hang Seng Index down 0.07% to 26,503.93

Shanghai Composite down 0.6% to 2,991.05

Sensex up 0.8% to 38,524.63

Australia S&P/ASX 200 up 0.1% to 6,652.01

Kospi up 0.04% to 2,068.17

German 10Y yield fell 0.2 bps to -0.459%

Euro down 0.02% to $1.1025

Brent Futures down 0.6% to $59.00/bbl

Italian 10Y yield fell 2.8 bps to 0.572%

Spanish 10Y yield fell 1.0 bps to 0.201%

Brent Futures down 0.6% to $59.00/bbl

Gold spot down 0.09% to $1,491.86

U.S. Dollar Index down 0.04% to 98.42

Top Overnight News

British negotiators submitted a revised set of Brexit plans to Brussels amid growing optimism that a deal could be struck this week

There will be a lot to watch when bank earnings kick off on Tuesday morning, with reports from JPMorgan Chase & Co., Goldman Sachs Group Inc., Citigroup Inc., Wells Fargo & Co. and money manager BlackRock Inc. all set to hit at or before 8 a.m.

Federal Reserve Bank of St. Louis President James Bullard said U.S. policy makers are facing too-low rates of inflation and the risk of a greater-than-expected slowdown, suggesting he’d favor an additional interest rate cut as insurance.

Some of Europe’s strictest ESG funds are snubbing the world’s most liquid investment — the $16 trillion U.S. Treasuries market

Investor confidence in Germany’s economic outlook remained weak in the latest sign of concern that the nation has slipped into a recession amid trade tensions

Asian equity markets traded mixed following the lacklustre lead from Wall St where the recent US-China trade optimism was tempered by discrepancies in language between the sides and with China wanting more discussions before signing the deal, while looming earnings added to the tentativeness as the large US banks are to begin announcing Q3 results today. ASX 200 (+0.2%) was choppy with the index pressured by underperformance in the commodity-related sectors and Nikkei 225 (+1.9%) outperformed as it played catch up on return from the extended weekend with Japanese officials willing to consider an additional budget for the typhoon recovery if required. Hang Seng (Unch.) and Shanghai Comp. (-0.6%) were indecisive after the trade exhilaration faded, with the HKMA’s announcement of a countercyclical capital buffer reduction and influx of CNY 40bln from the PBoC’s previously announced targeted RRR cut, doing little to spur risk appetite. The latest inflation figures from China were also somewhat inconclusive as CPI topped estimates to print its highest since 2013 although PPI declined at its fastest pace in more than 3 years. Finally, 10yr JGBs traded subdued as demand was dampened amid the strength in Japanese stocks but with downside also restricted by the BoJ’s presence in the market for JPY 1.21tln of JGBs heavily concentrated in 1yr-10yr maturities.

Top Asian News

China’s Factory Deflation Worsens, Adding to Global Economy Woes

Sun Hung Kai Properties Cuts Rents at Some of Its H.K. Malls

China Fertilizer Maker on Brink of Bankruptcy Rallies 51%

Fund Managers Expect Latitude IPO to Be Pulled: AFR

A choppy session for European equities thus far [Eurostoxx 50 +0.7%] following on from a mixed Asia-Pac session. European equity futures saw upside heading into the cash open amid refuelled Brexit hopes after EU’s Chief Brexit Negotiator Barnier struck an upbeat tone regarding a potential Brexit deal by the end of the week; although this has been caveated somewhat by EU Diplomatic sources. That said, futures pared back around half of its gains at the open and continued declining with downside exacerbated by source reports that China will struggle to purchase USD 50bln worth of agri goods. Major bourses in the region are ultimately higher, although UK’s FTSE 100 trades flat as exporters bear the brunt of a firmer Sterling, induced by positive comments from various EU lawmakers. Sectors are all in broadly positive territory although the IT sector is somewhat underperforming as Wirecard shares (-18.5%) plumbed the depths after a fresh FT investigation raised prospect of a concerted effort to fake substantial sales and profit at the company. Wirecard has since dismissed the report as “market speculation”. On the flip side, the financial sector fares better as current Brexit optimism spurred gains in domestic banks with Lloyds Banking Group (+3.4%), RBS (+3.4%) Barclays (+2.1%) all at the top of the FTSE 100. Further, the Italian banking sector is propped up by source reports that Italy is mulling reducing the amount of loan losses that banks can deduct from their taxable income next year. Hence the Italian Banking index opened higher by circa. 1% but has since come off of highs. In terms of individual movers, Indivior (+8.0%) shares spiked higher at the open after the Co. boosted its earnings guidance for a second time this year amid a strong performance of its drug used to treat opioid addiction. Meanwhile, Kloeckner & Co. (-14.3%) shares slumped following a downgrade to its profit outlook due to weaker market conditions.

Top European News

U.K. Employment Falls as Brexit Strains Spread to Labor Market

U.K. Carmakers Hit by $628 Million Brexit Tab Call for EU Deal

Wirecard Drops on News Report Suggesting Accounting Misdeeds

German Steelmaker Kloeckner Slumps as Global Slowdown Bites

In FX, cable seemed destined for or at least drawn towards a hefty option expiry at the 1.2600 strike before another bout of Brexit deal positivity boosted the Pound across the board, and this time from the EU’s chief negotiator Barnier who remains hopeful that a deal can still be struck in time for Thursday-Friday’s Summit, but warns that latest UK proposals remain inadequate. He added that the deadline to reach an agreement is COB today, but separate reports suggest that another meeting could be convened before the current October 31 deadline if needed, while the UK Government believes that the cut-off for this week is actually Wednesday evening. However, the situation remains highly fluid and uncertain, with Sterling hostage to headlines, breaking news and unfolding developments, as Cable fades just ahead of 1.2700 and Eur/Gbp rebounds from just under 0.8700 towards highs of 0.8750.

NZD/AUD – Not much respite for the Antipodean Dollars following further reflection and assessment by China and the US about the state of trade relations and significance of Phase 1 even though Beijing and Washington appear to be more convergent on certain elements of the accord in principle. Indeed, the Kiwi is still capped ahead of 0.6300 awaiting NZ Q3 CPI after the latest GDT auction, while the Aussie remains some way below 0.6800 in wake of RBA minutes underlining guidance for keeping rates low or easing further if required, and with a decent 625 mn expiry at the big figure.

JPY/CAD/EUR/CHF – Comparatively contained trade vs the Greenback again, as the Yen meanders between 108.23-45 and just shy of decent expiry interest residing at 108.00-20 (1.5 bn), while the Loonie is striving to limit losses beyond 1.3240 amidst a deeper retreat in oil prices and Euro remains top heavy into 1.1050, and perhaps also rooted by expiries given 1 bn rolling off just above 1.1000 (1 bn from 1.1015-20). Elsewhere, more soft Swiss inflation inputs via producer/import prices are keeping the Franc depressed just off parity and around 1.1000 against the single currency, as the DXY continues to flit either side of 98.500.

EM – More volatility for the Lira, but a recovery of sorts following US sanctions against Turkey that were perhaps not as severe as many were anticipating. Nevertheless, Usd/Try remains elevated within a 5.8605-9320 range and underpinned on the back of a rise in unemployment plus a big swing in the budget balance from small surplus to onerous deficit.

RBA Minutes from October 1st meeting stated the board judged case for easing at October meeting outweighed arguments against a move and that it is prepared to ease policy further if needed. RBA also reiterated that it is reasonable to expect that an extended period of low rates would be required, while board members noted global trend of lower rates and discussed the possibility rate cuts could have less impact than in past but judged lower rates will still have an effect through AUD. (Newswires)

In commodities, A downbeat day for WTI and Brent futures thus far as downward pressure resumed as markets tilted towards risk aversion in early EU trade and as optimism surrounding the US-China mini deal fizzles out. Analysts at ING highlight that the ICE Brent Dec/Jan time-spread has also narrowed to a backwardation of around 0.17/bbl vs. 0.77/bbl at the end of September which suggests the “tightness in the prompt market is easing”. In terms of newsflow, OPEC Secretary General Barkindo noted that the physical oil market is relatively tight now and current demand is the market driver. WTI futures took out 53/bbl to the downside and tests 52.50/bbl ahead of the psychological 52.00/bbl mark whilst its Brent counterpart eyes 58/bbl to the downside. As a reminder the weekly API crude inventories have been postponed by a day due to US observing Columbus Day yesterday; as has the EIA release. Elsewhere, gold has climbed off lows amid a turnaround in sentiment and remains in close proximity to 1500/oz vs. an intraday low of around 1488/oz. Copper meanwhile has pulled back during the session, albeit prices remain above 2.62/lb.

US Event Calendar

Oct. 15-Oct. 18: Monthly Budget Statement, est. $83.0b, prior $119.1b

Central Bank Calendar

4:25am: Fed’s Bullard Speaks at Bloomberg Conference in London

9am: Fed’s Bostic Speaks on Community Development

12:45pm: Fed’s George Speaks at Payments System Conference

3:30pm: Fed’s Daly Speaks Los Angeles World Affairs Council

DB’s Jim Reid concludes the overnight wrap

With it being fairly quiet in markets yesterday – not helped by US bond markets being closed for a holiday – even a small smattering of trade headlines was likely to be the only talking point for investors. Indeed, after radio silence over the weekend, initially it looked like ‘Phase One’ was turning more into ‘Phase Nought Point Five’ after Bloomberg reported that China wants to hold more talks before signing a trade deal with the US. The story went on to say that China may send a team of negotiators led by Vice Premier Liu He to finalise a deal that could be signed at the Asia-Pacific Economic Cooperation summit next month. The story also suggested that China were advocating for Trump to cancel tariff hikes due in December.

Markets faded immediately after the story broke and continued the trend from late Friday however the S&P 500 later bounced back towards flat on the day after Global Times Editor Hi Xijin tweeted that “based on what I know, China-US trade talks made breakthrough last week and the two sides have the strong will to reach a final deal”. US Treasury Secretary Mnuchin hardly made things any clearer, with CNBC quoting him as saying that he has every expectation that if a US-China trade deal is not in place, December tariffs will be imposed, but that he also expects a deal. So make of that what you will. Clearly there is still lots of headline volatility likely in the weeks ahead with my concern being less about “phase one” but what happens to all the unresolved issues after that. Anyway by the end of play the S&P 500 closed -0.14% lower with materials (-0.74%) leading the move lower, while financials eked out a +0.12% gain ahead of earnings season starting today. The DOW and NASDAQ finished -0.11% and -0.10% respectively, though volumes were around 30% lower than usual. In Europe, the STOXX 600 ended -0.49% but that was after trading as low as -1.15% while elsewhere Gold (+0.21%) was slightly higher and WTI (-2.15%) fell sharply to perfectly retrace Friday’s gain. The small risk off also helped 10y Bund yields edge down -1.5bps. 10 year Gilts rallied -6.7bps as Brexit deal euphoria was dampened down after the mixed weekend news (more below). As mentioned, US bond markets were closed, but the dollar did strengthen +0.22%. One of the bigger underperformers was the Turkish lira (-0.73%) which depreciated after reports that the US is preparing financial sanctions on individuals in response to the offensive in Syria. We indeed got those sanctions as US markets closed with the US Treasury Secretary Steven Mnuchin saying that the US has sanctioned the Turkish ministers of defense, interior and energy while adding that there will also be primary and secondary sanctions for any financial institutions doing significant transactions. The sanctions will also include penalties which will raise steel tariffs on Turkey back to 50%, the level before a reduction in May, and the US would halt negotiations over a $100 bn trade pact. He added that, “these sanctions are very, very strong”. However, House Speaker Nancy Pelosi, accused Trump of unleashing “an escalation of chaos and insecurity in Syria” and added, “His announcement of a package of sanctions against Turkey falls very short of reversing that humanitarian disaster.” In spite of the imposition of these sanctions, the Turkish lira is actually trading up +0.10% this morning.

Looking ahead, the good news for markets today is that we should at least get a temporary distraction from trade and Brexit with some potentially important earnings to dissect with JP Morgan, Goldman Sachs, Citigroup and Wells Fargo all due to report. Our US equity strategists recently put out a note and highlighted that the bottom-up analyst consensus for S&P 500 EPS has been falling for a year and with a typical beat implies flat earnings (+0.8% vs +3.5% in Q2). Their top-down model, however, points lower (-1.5%) suggesting below average beats and a disappointing earnings season. The top-down drivers of earnings have weakened across the board with falling macro growth the biggest drag (-7pp). There is growing evidence of a weakening in pricing power, with corporates focused on the next set of levers to press, including cuts in hours worked and slowing employment growth. See their report here .

Ahead of all this, Asian markets are trading mixed with the Nikkei up +1.88% after reopening from the long weekend while the Shanghai Comp (-0.53%) is down. The Hang Seng (-0.06%) and Kospi (+0.05%) are flattish. Elsewhere, futures on the S&P 500 are up +0.22% and crude oil prices are down a further c. -0.70% this morning. As for overnight data releases, China’s September CPI came in at +3.0% yoy (vs. +2.9% yoy expected) while PPI printed in line with consensus at -1.2% yoy. The rise in CPI was mainly due to food prices climbing 11.2% and a more than 69% jump in pork prices, according to China’s National Bureau of Statistics.

As for Brexit, there were some back-and-forth headlines and a corresponding seesaw in the pound. Sterling fell as much as -1.20% during yesterday’s trading session to 1.252, but has retraced and is up 0.81% from that level this morning. Initially, there was some fading of last week’s slightly premature euphoria and also concern over Barnier’s comments about potential technical challenges and the DUP Dodds’ cautious comments over the weekend. Notwithstanding the weakness yesterday, the most significant point to make right now is that the UK government position has undergone a notable transformation over the last couple weeks to a position where they are negotiating around a version of the EU’s 2017 backstop with potential concessions for the DUP. DB’s Oli Harvey made the point yesterday that assuming PM Johnson doesn’t have a change of heart, this removes the tail risks – if there isn’t a deal by Saturday we will either get a caretaker government, or an election fought between parties that all want a deal (with the exception of the Brexit Party). Overnight the U.K. Telegraph say their sources suggest that talks are inching positively towards a deal, citing “last-minute compromises,” even if they might require an additional EU summit next week to get things over the line. The DUP leadership were also reported to be in talks at no.10 last night so things are hotting up behind the scenes. Elsewhere, Ireland’s foreign minister Simon Coveney said that there was goodwill and determination from both sides to get a deal, but that “it’s too early to say whether it’s possible to get a breakthrough this week or whether it will move into next week”. The BBC also reported overnight that the EU is mulling new emergency summit to ‘get Brexit deal done’. In addition, Mr Barnier will update the EU ministers today at the General Affairs Council in Luxembourg where he is expected to give a press conference. So one to watch.

Finally, it was a very quiet day for data yesterday with only the August industrial production print for the Euro Area. The +0.4% mom reading was slightly ahead of expectations for +0.3% and it followed a -0.4% mom reading in July. Combined with slightly better retail sales data, that points to a very modest positive for Euro Area growth. In the US, the Empire manufacturing survey rose to 4.0, from 2.0 in September.

To the day ahead now, which this morning includes final September CPI revisions in France, August/September employment data in the UK and the October ZEW survey in Germany. In the US the only data due out is the October empire manufacturing print. Away from that it’s a busy day for Fedspeak with Bullard, Bostic, George and Daly all scheduled. The BoE’s Carney is also due to testify on the financial stability report this morning while the BoE’s Vlieghe speaks at lunch time. As mentioned above, US bank earnings from JP Morgan, Goldman Sachs, Wells Fargo and Citigroup will also be a big focus. Finally, the World Bank and IMF meetings will kick off with the World Outlook document expected around 2pm London time, which always gets headlines. This time notable global growth downgrades are likely.

Futures Slump On Report Beijing Wants Tariffs Removed Before Commiting To $50BN In Ag Purchases

Yesterday, we learned that our suspicions were correct, and that the US-China “Phase One” deal purportedly hashed out between the two sides last week appears to be more of the same disingenuous stalling, and that, fundamentally, the situation hasn’t really changed.

And on Tuesday, with the US back from the long holiday weekend, Chinese officials have essentially confirmed that they are back to their old tricks, and that the progress on the ‘Phase One’ deal that was touted last week is a sham. Beijing can make good on the $50 billion of annual agricultural goods purchases that it has promised – but only if Washington agrees to remove all of the trade war tariffs.

Of course, as President Trump has repeatedly made clear, the tariffs must remain in place until a deal has been implemented and Beijing has proven that it has been abiding by the rules. According to Bloomberg, China won’t be able to buy $50 billion of US farm goods unless the tariffs are removed.

Unsurprisingly, futures slumped on the news, indicating a likely lower open.

LeBron James Accused Of Kowtowing To Beijing By Calling Morey Tweet ‘Misinformed’

Offering perhaps the most stark example yet of how pressure from Beijing is influence the discourse both within and around the NBA in the wake of the now-infamous Daryl Morey tweet expressing support for the Hong Kong pro-democracy movement, LA Lakers star LeBron James – the league’s biggest star and one of the world’s most dominant athletes – criticized Morey for not being “educated on the situation” and warned that freedom of speech can sometimes have “a lot of negatives that come with it.”

James’s remark, made during a pre-game interview ahead of the Lakers’ pre-season game against the Golden State Warriors, sparked an immediate backlash, with one lawmaker (Florida’s Rick Scott) criticizing the basketball star for “putting profits over human rights.”

Clearly @KingJames is the one who isn’t educated on the situation at hand.

It’s sad to see him join the chorus kowtowing to Communist China & putting profits over human rights for #HongKong. I was there 2 weeks ago. They’re fighting for freedom & the autonomy they were promised. https://t.co/tVI1XB7g6I

During his response to a question about the controversy, James insisted he didn’t want to “get into a feud” with Morey before gently criticizing his decision to send the tweet, which prompted a furor in Beijing and threatened the future of the League’s broadcast deals on the mainland, a market with hugely lucrative potential.

James claimed that “so many people could have been harmed” by Morey’s tweet, not just financially, but “physically, emotionally [and] spiritually” as well.

“Yes we all do have freedom of speech but at times there are ramifications…that can happen when you’re not thinking about others but you’re only thinking about yourself. I don’t want to get into a feud with Daryl Morey but I think he wasn’t educated on the situation at hand and he spoke…and so many people could have been harmed, not only financially but physically, emotionally, spiritually…so just be careful what we tweet, what we say, what we do. Even though yes we do have freedom of speech, but there can be a lot of negatives that comes with that too.”

As of early Tuesday morning, clips of the interview have already racked up millions of views, even though the clip didn’t start to circulate until Monday evening.

Lakers’ LeBron James on NBA’s China controversy: “I don’t want to get into a … feud with Daryl Morey but I believe he wasn’t educated on the situation at hand and he spoke.” pic.twitter.com/KKrMNU0dKR

James took to twitter afterward to clarify his statement. But instead he mostly just rephrased his earlier criticisms of Morey, adding that the GM could have “waited a week” to send the tweet, after a series of pre-season games played in China had ended.

Let me clear up the confusion. I do not believe there was any consideration for the consequences and ramifications of the tweet. I’m not discussing the substance. Others can talk About that.

My team and this league just went through a difficult week. I think people need to understand what a tweet or statement can do to others. And I believe nobody stopped and considered what would happen. Could have waited a week to send it.

In retaliation for Morey’s tweet, Beijing cancelled broadcasts of a couple of pre-season games and canceled events involving the Brooklyn Nets and other NBA teams as they embarked on a brief tour of China. The NBA has been criticized for kowtowing to Beijing as Commissioner Adam Silver tried to assuage Beijing’s concerns while also insisting that the league supports American values like free speech.

However, as some have noted, if players aren’t free to tweet openly about their political views for fear of losing their livelihoods, then that’s not really free speech, and essentially Beijing is projecting the Communist Party’s censorship on to the US.

This satirical mock-up of the NBA logo effectively embodies the criticism facing the League.

According to all central banks, one of the main problems they are called to solve is that countries cannot reach their inflation target of (close to but below) 2 percent. Even their religious trust in the long-discredited Phillips curve cannot explain why price inflation is low in many countries despite historically low unemployment rates. Nonetheless, central banks still enjoy immense credibility. It’s common to hear such sentences as “never bet against the Fed,” the “ECB has big bazooka primed”… and all market participants monitor each public meeting to understand what the next policy could be and how they should be positioned when it arrives.

To reach the inflation targets and “stimulate the economy,” central banks regularly meet to devise ever-new stimulus programs, and do not despair when, inevitably, the one-off unconventional interventions quickly become the new normal. For example, the world-famous Quantitative Easing (QE) was supposed to be a one-time emergency response to the 2008 crisis, except it has now become one of the many tools of regular monetary policy, and a key component in market demand for financial assets. An undesired but perfectly predictable side effect of QE is that it allows governments to increase their spending without care for the deficit, and still pay negative interest rates in real terms, so no discipline is imposed, except for some empty promise to reduce the deficit some time in the future, if the opportunity comes. Several Western countries have embarked in QE, some in many consecutive rounds, but there is no mention of a reverse-course, an eventual, opposite Quantitative Tightening (QT). Only the United States have tried QT, and the Fed has even announced that they were on a stable and data-driven process back to normalization, to try to maintain their reputation of scientific management of the monetary aggregates. However, the Fed had to quickly abandon the plan, and its balance sheet remains massively bloated under any historical measure.

It is abundantly clear that markets are doing well only thanks to monetary life support, and the help provided by QE cannot be taken out without provoking a serious crisis across all the whole investable universe. Now the Fed has embarked in a new round of QE, although Powell denied in the most absolute terms that it is QE.

There is today a veritable alphabet soup of monetary policy tools (QE, OMT, TLTRO, APP, ABCP…) and the result is that no asset class is free of distortion, including the key markets of foreign exchange and corporate debt. All these tools are only more of the same: they apply the same means (create new money out of thin air) to reach the same end (artificially decrease the interest rate). Clearly these interventions have the same side effects as a regular, conventional decrease of the interest rate. Chief among these problems are a general hunt for yield in all markets, the setting in motion of boom-bust cycles, and the inability for pension funds to provide savers with a long-term real return to support retirement and future consumption. Far from being problems confined to banks and the ultra-rich, this diverts resources from savers and wealth generators to the politically-connected.

As historically low interest rates stifle growth and stimulate consumption but not production, it is easy to find throughout Europe and the US low wage growth, low investment for productivity growth, and growing debt burdens on governments, corporations, consumers.

As always, central banks (like their politician friends) try to solve problems by doing more of the same. Both the Fed and the ECB signaled they’re not finished yet: the ECB lowered its target rate again, and announced a new round of bond purchases. Meanwhile, the Fed lowered its target rate again, likely on the road back to zero. The latest trouble is in the repo market , where banks lend to each other overnight. The Fed has a target rate for interest rates in this market, but the rate skyrocketed well above the upper bound. The Fed stepped in and announced an emergency liquidity assistance (in common speak: bailouts) that will last for months, standing ready to provide print money at will. For a central bank that takes pride in announcing its interventions well in advance to prepare the markets, this is an unseen event. They moved much and quickly, signaling that the problem truly is important. The Fed balance sheet is growing again, and now there is one more moral hazard in town: liquidity risk is not a problem anymore, so the liquidity carry trade is much more profitable. Rest assured that if a liquidity crisis will happen despite interventions, nobody will blame the Fed. Possibly, they will claim the Fed had stepped in too lightly and must do much more.

Still new monetary tools may be tried in the future. All investors are speculating on what the new tools could be, one possibility is that the ECB (and possibly, in the future, the Fed) could follow the lead of the Bank of Japan in creating a new QE to purchase directly stocks and stock ETFs. Few people won’t be shaken reading a sentence as “The BoJ was ranked as a top ten shareholder in some 40 per cent of all listed companies”, but this is precisely the course of the monetary authorities. However, like all monetary interventions, this would prop up all markets into further bubble territory, while the endemic problems of the economy are never addressed.

Now, what does the market think of all this monetary machinery? The central bank targets an inflation rate, so given its immense credibility the market should assume that the target will hit. Currently the inflation rate is below targets, but more troublesome (for the Fed) is that the market expects central banks to continue failing: the expected future inflation rate is on average “only” 1.6 percent in the US , 1.1 percent in Europe , 1.2 percent in Japan . It is thus unclear what this continuous intervention in money is good for, other than pumping up markets and kick the can down the road, pretending that since markets are up then the economy must be doing well.

There are even talks about letting inflation run higher than 2 percent. This number had always been set in stone as the highest number allowed, with central banks standing ready to defend us from higher numbers. Eminent figures such as former IMF Chief Economist Olivier Blanchard have suggested to raise the inflation target to 4%, if not more. This would double prices (and halve savings) in about 18 years, less than a generation. So much for the Fed’s goal: “price stability”. But this is not yet generally accepted, and the current fashion is to claim that the inflation target is not 2% but “symmetrical 2 percent”: after years of undershooting we should have years of overshooting, so the long-term average will be 2 percent. In effect, the BoJ and then the Fed have pre-emptively announced that they will not fight inflation unless it becomes too high, without defining “too high”. This pushes a normalization even further in the future, as a price inflation of 3 percent, 4 percent, 5 percent would be allowed to continue for years, or until it becomes “too high”, but “too high” has not been defined. The ECB is likely to move in the same direction, especially considering the well-known dovishness of the new head Christine Lagarde.

As is clear from economic analysis since the Scholastics of five centuries ago, this lack of sound money and apparently infinite money printing does nothing but send confused signals, increase economic and legal uncertainty, and drive up the rates of time preference in a process of de-civilization and increasing present-orientation. The seeds of all crises since ancient times have been planted through distortions of money, and these concerted crusades of all central banks are no different. Fortunately, there are growing popular movements in Europe and in the United States to push towards a normalization of money and interest, and to restore sound money and free entrepreneurship. This is a process that started with the 2008 crisis, when we saw what happens after 40 years of monetary pumping: the long-run has arrived.

Opera That Cost Marie-Antoinette Her Head Is Performed Again At Versailles

The last time Richard Coeur-de-lion (Richard the Lionheart), an opera comique by the Belgian composer André Grétry, was performed in the Palace of Versailles. It was several hundred years ago for Louis XVI and Marie-Antoinette just before their heads were cut off by a guillotine, reported Radio France Internationale (RFI).

The opera, which debuted last Thur., is about Richard the Lionheart, the English king who had been taken prisoner during the medieval Crusades.

Petite révolution à l’Opéra Royal du Château de Versailles: la première “production maison” depuis 1789, “Richard Cœur-de-Lion” d’André Grétry, va résonner de nouveau dans une salle qui fête cette saison ses 250 ans et ses 10 ans de réouverture au public #AFPpic.twitter.com/OP4YHz1sE9

Grétry, one of Antoinette’s top composers, performed the opera in Versailles in 1789.

The famous lines “Ô Richard, ô mon roi!” (“Oh Richard, oh my king!”) was made popular among royalists during the French Revolution.

At the time, France was thrown into socio-economic chaos, as unpopular taxation schemes, bad harvests, and vast wealth inequality, culminated into the perfect storm that toppled the monarchy, and eventually led to the public execution of Louis XVI and Marie-Antoinette by guillotine.

Versailles’ theatre and events director Laurent Brunner told RFI that Richard the Lionheart was last played on October 1, 1789, and led to significant social upheavals in Paris among peasants.

“It [the opera] sparked a scandal in Paris during the French Revolution,” explained Brunner.

Brunner said the decision to revive the opera in the halls of Versailles coincides with the 250th anniversary of the opera house located on the grounds of Versailles.

“Very few opera houses are as charged with history and yet so poor when it comes to their own music,” said Brunner.

Ironically, the opera has debuted in light of the ‘yellow vest movement,’ a populist political movement that addresses wealth inequality, outlandish taxation by government, a minimum-wage increase, and the resignation of President Emmanuel Macron.

It’s eerier to note, Richard the Lionheart, has only been played at Versailles during revolutions in the country. Does that mean if current conditions in France continue to deteriorate, yellow vest protesters could one day surround Élysée Palace, in Paris? Are Macron’s days numbered?

From almost the very moment in 2016 when Saudi Arabia first announced that it was to float its state-owned oil and gas behemoth, Saudi Aramco, in a dual domestic and international listing, the pool of possibilities for the foreign side of the initial public offering (IPO) has steadily reduced. This has been a result of a simple equation: the more that would-be investors know about Saudi Arabia and Aramco the less appealing the prospect of having anything to do with them becomes. However, because Crown Prince Mohammed bin Salman (Mbs) has staked his personal reputation – and his political future – on the Aramco IPO going ahead in some form, he and his bankers are currently rooting around for at least one international bourse upon which to execute the foreign listing part of the omni-toxic Aramco.

The New York Stock Exchange (NYSE) was one of the original top-two favored candidates, alongside the London Stock Exchange (LSE), as these two bourses are rightly seen as the most liquid, most traded, and most prestigious stock exchanges in the world. Early on, though, a number of major problems began to bubble up for a listing of any Saudi company and particularly Aramco in the U.S. Aside from the usual farrago of lies from Saudi about oil reserves, spare capacity, tax rates, concessions, non-hydrocarbons activities and so on with which investors have now become familiar, a key early sticking point was Saudi Arabia’s perceived links with the ‘9/11’ terrorist attacks.

Of the 19 terrorists who hijacked planes on ‘9/11’, no less than 15 were Saudi nationals. Following the overriding by the U.S. Congress of former President Barack Obama’s veto of the ‘Justice Against Sponsors of Terrorism Act’, making it possible for victims’ families to sue the government of Saudi Arabia, at least seven major lawsuits alleging Saudi government support and funding for the ‘9/11’ terrorist attack have so far landed in federal courts. As one New York-based chief executive officer of a major commodities hedge fund told OilPrice.com:

“If I invested in anything Saudi, my investors would hang me from the nearest streetlight.”

This was the pervasive view even before Saudi continued the indiscriminate bombing of Yemen, led the way in the international ostracising of Qatar, kidnapped Lebanon’s then-President Saad Hariri and forced his resignation (allegedly), and murdered the journalist Jamal Khashoggi (allegedly, although the evidential pointers appear incontrovertible), which would never have been done without MbS’s personal go-ahead.

Making matters even worse was Saudi’s decision to threaten the U.S. shale industry if Washington passed into law the ‘No Oil Producing and Exporting Cartels Act’ (NOPEC). This bill was founded upon the supposition – which still hangs in the air like a Damoclean Sword above the Saudis’ heads – that OPEC is a cartel and that, as such, Aramco – as the principal vehicle of the leading member of OPEC, Saudi Arabia – violates the U.S. (and U.K.’s) stringent anti-trust laws. Given that OPEC’s members account for around 40% of the world’s crude oil output, about 60% of the total petroleum traded internationally, and over 80% of the world’s proven oil reserves – and controls geographical sales policies and pricing – this would appear to be an entirely sensible conclusion.

That Saudi actually threatened to destroy the U.S.’s shale oil industry – yet again – was greeted with actual laughter by a number of senior oil figures spoken to by OilPrice.com at the time.

“OPEC and Saudi tried to do exactly the same thing [destroy the US shale oil industry] in 2014 and 2015 in exactly the same way [push oil prices down by producing all-out] and that did not end well for OPEC’s oil producers in general and Saudi Arabia in particular,” Norbert Ruecker, head of economics and next generation research for Bank Julius Baer, in Zurich, told OilPrice.com.

More specifically, in the two years before the Saudis in 2016 completely reversed its ‘U.S. shale oil destruction strategy’, OPEC member states lost a collective US$450 billion in oil revenues from the lower price environment, according to the IEA. Saudi Arabia itself moved from a budget surplus to a then-record high deficit in 2015 of US$98 billion, being forced to spend over the period around US$250 billion of its foreign exchange reserves that even senior Saudis have said are lost forever.

Given this, Saudi for a time looked at the U.K.’s LSE as an option, following a trip to Saudi Arabia some time ago by LSE chief executive officer, Xavier Rolet, and then-UK Prime Minister, Theresa May, and indeed, according to various sources spoken to by OilPrice last week, this remains an option for MbS. The problem with this from the U.K.’s side – which was conveyed to the Aramco IPO banking team – centres on the creation of a new category of listings for large international companies, in order to accommodate Aramco and its lack of information transparency. More specifically, historically, companies looking to list on the LSE could opt for either a ‘premium’ (formerly ‘primary’) or ‘standard’ (formerly ‘secondary’) listing.

According to the rules, a premium listing that would be included in the benchmark FTSE 100 index would mean that Aramco would need to allow potential investors full access to the company’s books, let minority investors vote on an independent board of directors, and also allow them to approve transactions between the company and its controlling shareholder, the Saudi government, none of which are likely to occur. However, a standard listing would mean Aramco would not be in included in the FTSE100, being relegated instead to the second-tier of companies, alongside mid-cap UK firms groups and family-controlled foreign firms.

The compromise solution – which followed the Rolet-May trip was to create this new category of listings for large international companies that may fail to meet the premium listing standards but is theoretically more prestigious and more appealing to investors than the ‘standard’ category. Clearly, as Jeremy Stretch, senior markets analyst for CIBC, in London told OilPrice.com, simply changing the name of a listing type does not alter the fact that it does not in reality meet the standards expected from FTSE-listed companies in terms of rigorous reporting, operational opacity, and accountability to shareholders, even minority ones. Indeed, a number of major pension and insurance funds have commented to OilPrice.com that there are still ‘very big governance issues’ around how much independently verified data pertaining to the company’s oil reserves would be given, its board structure and the small portion of the company being listed.

At that point, MbS toyed with the idea of doing a private placement of the whole amount – as then, 5 percent to be floated – with China. This would have been extremely advantageous to him for two key reasons.

Firstly, it would have required absolutely no divulging of any information whatsoever on Aramco’s – or Saudi’s – dealings, except to the Chinese who, as one senior oil trader put it to OilPrice: “Don’t care, all it wants is to get control over a favourite toy in the U.S.’s Middle East toy box.”

The second reason why MbS was very keen on the idea is that the price for the 5 percent private placement would never had been made public to anyone, even many senior Saudis, so he could not be accused of having not attained the US$100 billion for the 5 per cent that meant an overall valuation for Aramco of US$2 trillion (which he had already – equally unwisely – committed to). This option also remains on the table but – principally because the bankers working on the IPO would lose too much money if the IPO did not go ahead, MbS is not being encouraged to pursue this line.

All of which rather narrows the options available right now for MbS. Canada’s Toronto Stock Exchange (TSE) made a spirited pitch a while back. MbS, though, was dissuaded from this because of its small size relative to the bigger exchanges and the fact that its value is already dominated by oil companies. This latter point meant that the effect of a drop in the oil price on Aramco’s TSE valuation would be much more pronounced than if it were a reflection of the company’s other assets’ worth, at least as far as the Saudi’s see it. Hong Kong, meanwhile, was for a time a front-runner, given its close links to Chinese money and Chinese oil and gas buyers, but the burgeoning protest movement against Chinese rule by Hong Kong has subsequently marginalized its appeal.

So, as it stands, MbS has trimmed everything back to try to limit the negative personal and political fallout for himself. According to trading and fund manager sources in London, Abu Dhabi, and Tokyo, the sovereign wealth funds of Saudi’s allies in the region have been ‘vigorously encouraged to bid high for big lots’, augmenting the sort of hearty bids from wealthy Saudis that might be expected from people who remember what being locked up in 2017 – albeit at the Riyadh Ritz-Carlton – was like. Tokyo has been pitching aggressively in the last few weeks as the Asia alternative to Hong Kong, and has sought to leverage the involvement of many of its financial institutions in various of MbS’s ‘Vision 2030’ projects to bolster its pitch. Underlying all of these bids will be the bookrunners, of course, who will take up any slack from the huge amounts of money that they stand to make not just from the IPO but also from all related work for Saudi. These include future IPOs, bond offerings, syndicated loans (known for their unerring ability to provide summer houses and matching yachts in the Hamptons for U.S. senior bankers), and other long-term rolling financing facilities.

“We Came From Fire”: A Brief History Of The Syrian Kurds

“You can say the war is like a giant game of chess…” the Syrian Kurdish ‘fixer’ and driver told photographer and author Joey Lawrence as they traveled across the Kurdish northern Syrian heartland locally dubbed Rojava.

As perhaps confusing and chess-like the now eight-year long war might be even for the players on the ground, many in the West woke up Monday morning to a new seeming contradictory reality: US-backed Syrian Kurdish forces (SDF) have struck a deal with the Syrian government, and the national flag of President Bashar al-Assad is now flying alongside that of the Kurdish resistance movement, which had been for years backed by American forces. Currently, US special forces are in retreat from the Turkish border upon White House orders, and simultaneously the Syrian Army is moving in.

How did such a reunion occur seemingly overnight between the two “enemies”? Hours before the deal was struck, the Kurdish-led Syrian Democratic Force’s top commander, Mazloum Abdi, wrote a Foreign Policy op-ed in which he explained to the world: “We know we would have to make painful compromises with Moscow and Assad if we go down that road. But if we have to choose between compromises and the genocide of our people, we will surely choose life.”

Jîn, a YPJ fighter, with rocket-propelled grenade launcher. Credit: Joey L. Photography. All images used with permission.

To understand this, as well as why the invading Turkish Army and its ‘rebel’ proxies now face a nightmarish resistance and insurgency, it is crucial to revisit the little-discussed role of Syria’s main Kurdish militias from the start of the war, how they’ve survived as the region’s fiercest and most experienced ground force, and further how their secular identity and pragmatism has ensured not just survival but flourishing even as they’ve faced extinction by ISIS and the invading Turkish state, and after enduring multiple historic betrayals.

Extracts in the below essay are taken from the book We Came From Fire, by Joey L. published by Powerhouse Books (2019), and are used with permission.

* * *

“For Kurds, fire is extremely important.We came from fire, and we will return to fire— it’s an ancient saying,” one Syrian Kurdish fighter explained to Joey Lawrence.

“The recent war in Iraq and Syria had become a globalized conflict, except rather than a world war fought with state armies, it was fought by proxy, with the blood of the local people. The world had become entwined in the conflict in ways never before imaginable, and events were both amplified and distorted by propaganda from all sides…”

Image via Joey L.

“After the collapse of the Ottoman Empire at the end of World War I, the great European powers divided up the former Ottoman territory. The ensuing treaty — the Treaty of Sevres — promised the Kurds their own continguous and sovereign entity for the first time in modern history. However, three years later, after a series of military victories by the former Ottoman Brigadier General Kemal Pasha (now known as Ataturk), the great powers had to relent to Turkish pressure and replace Sevres with the Treaty of Lausanne. This new treaty established the new Republic of Turkey and squashed Kurdish hopes for a state of their own. The land of the Kurds would be divided between four different countries, splitting tribal lines, villages, and even families…

As the latest conflict in Iraq and Syria, starting in 2011, spiraled out of control, state powers that once kept the Kurdish ethnic minority down found themselves spread thin, fighting against both rebellions and jihadist insurgencies; they were forced to retreat from Kurdish areas and dedicate resources to government heartlands. However grim, the crisis and dismantling of perceived nation-state borders presented Kurds with a golden opportunity. The once-persecuted rose to secure power in the vacuum.”

Image via Joey L.

“Seeing an opportunity to crush the Assad government — an old rival often at odds with the Western and Gulf sphere of influence — Qatar, Saudi Arabia, Turkey, the United States, Israel, the United Kingdom, and other NATO-aligned European powers all acted in their own way against the crumbling Syrian state. Intelligence services sent vast amounts of weapons, money, and other materials to the rebels. Western and Gulf states chose their own champions in the war…

Turkey purposely left its border wide open… It became a gateway for tens of thousands of international jihadists to openly enter Syria and fight alongside the FSA against the Syrian government. These foreign fighters filled the ranks of al-Qaeda’s Syrian franchise, the al-Nusra Front, the Salafist group Ahrar al-Sham, and later, the Islamic State of Iraq and Syria (ISIS). A Syrian jihad was born.”

Image via Joey L.

“As the largest ethnic minority in Syria — some 10 to 15 percent of the population — the Kurds are treated by the government with both deep suspicion and discrimination. While smaller minorities were given status, the Syrian Ba’ath regime viewed the Kurdish population as too large to risk empowering with representation in politics, yet small enough to keep down. The regime outlawed speaking the Kurdish language in public, as well as all related cultural activities. In the 1970s, the Syrian Ba’ath regime had enacted a forced resettlement program that changed the ethnographic makeup of predominantly Kurdish regions…

In April 2011, the Assad government, losing control of the population following the large-scale demonstrations and riots sweeping the country, reversed some of these policies. The Syrian government vowed to issue identity cards back to a small portion of the stateless Kurds, but could never fully reconcile given the growing dissent within the population. The country was in crisis; it was too little too late.”

Image via Joey L.

“In July 2012, the Syrian Arab Army abandoned Kurdish enclaves of Syria to dedicate their dwindling resources to other areas of the country at war. Kurds were now free of the repressive nature of the Assad regime, but at the same time, they were left on their own to defend themselves from the al-Qaeda-linked rebel groups ravaging the land. Even though the Syrian Kurds were predominantly of Sunni faith, the secular nature of the community in general was perceived as heretical by Sunni fundamentalists groups like ISIS, and were therefore targeted for conversion or extermination…

Thus, the People’s Protection Units (YPG) and their all-female wing, the Women’s Protection Units (YPJ), were born. Other spectrums of Kurdish political voices either abandoned the region and fled across the border, or were forced out by the domination of the new power structure.”

Image via Joey L.

“At the same time, the Syrian Arab Army’s retreat was self-serving. As foreign fighters were flooding into Syria from Turkey, the regime left the Kurds — Turkey’s insurgent enemy — to fight jihadist groups along the border. Clashes between the YPG/J and the Syrian Arab Army happened on many occasions, but a pragmatic neutrality would always be restored. Both sides knew that opening fronts against one another would weaken themselves, and both feared the future country falling in the hands of jihadists. It seemed neither the Syrian government nor the Turkish-backed rebels could guarantee minority rights for the Kurds, and the YPG/J chose a delicate third path in the war.

For the first time the term Rojava could be uttered in public. (Rojava, which means “the west” in the Kurdish language, refers to the part of the northeast syria that makes up west Kurdistan, and also is sued to describe the setting sun.) The newly empowered Rojava Kurds immediately began establishing popular governance, from neighborhood communes and academies to citywide councils to a regional administration spread across three different cantons: Afrin, Kobane, and Jazira. In January 2014, the three self-governing cantons declared themselves as autonomous zones.”

Image via Joey L.

“The YPG/J would prove themselves to be one of the first forces capable of stopping the ISIS advance in Syria… Most of these battles were unreported in the Western press, and the war between the Syrian Kurds and the radical Islamists was generally viewed as a sideshow to the greater war between Assad and the rebellion…

ISIS — seemingly the world’s most terrifying boogeyman — was collapsing under every offensive. It was purely a military alliance [the US and YPG/J/SDF forces], and the Americans rejected recognizing any political project of Kurdish autonomy in Syria. The US-led coalition support was extremely limited to the occasional delivery of light weapons and airstrikes, which were called in covertly by a small number of special operations forces embedded among the fighters. The US was wary to give the YPG/J heavy weapons such as the anti-tank TOW missile, perhaps fearing that one day they could fall into the hands of the PKK against their NATO partner, Turkey.”

PKK sniper in Makhmour, Iraq. Image via Joey L.

“After the fall of Idlib Governate and its provincial capital to a controversial coalition of al-Qaeda-affiliated armed groups and CIA-backed FSA rebels, the Syrian conflict took a dramatic turn. Russia entered the war… Although the YPG/J had openly fought Assad’s forces in the beginning of the war, the fragile neutrality that later formed was only seldom broken by odd skirmishes over checkpoints and access to roads. While they were opposed to everything the Assad regime represented,the YPG/J’s reluctance to join the rebels in the beginning of the war had benefited them greatly.”

Image via Joey L.

“They were not yet targets of Russian airpower. After all, the Syrian Arab Army was severely lacking in manpower, and the YPG/J mostly had the same enemies.They say it’s wise to fight your enemy’s enemy last.”

Via The New York Times/Conflict Monitor/IHS Markit

The vicious jail sentences handed down today by the fascists (I used the word with care and correctly) of the Spanish Supreme Court to the Catalan political prisoners represent a stark symbol of the nadir of liberalism within the EU.

As The BBC reports, Spain’s Supreme Court has sentenced nine Catalan separatist leaders to between nine and 13 years in prison for sedition over their role in an independence referendum in 2017.

The prosecution had sought up to 25 years in prison for Oriol Junqueras, the former vice-president of Catalonia and the highest-ranking pro-independence leader on trial.

Junqueras was handed the longest sentence of 13 years for sedition and misuse of public funds.

Others to receive prison sentences for sedition were:

Dolors Bassa, former Catalan labour minister (12 years)

Jordi Turull, former Catalan government spokesman (12 years)

Raül Romeva, former Catalan external relations minister (12 years)

Carme Forcadell, ex-speaker of the Catalan parliament (11.5 years)

Joaquim Forn, former Catalan interior minister (10.5 years)

Josep Rull, former Catalan territorial minister (10.5 years)

Jordi Sànchez, activist and ex-president of the Catalan National Assembly (9 years)

Jordi Cuixart, president of Catalan language and culture organisation Òmnium Cultural (9 years)

The nine leaders, who had already spent months in pre-trial detention, were acquitted of a more serious charge of rebellion.

That an attempt to organise a democratic vote for the Catalan people in pursuit of the right of self determination guaranteed in the UN Charter, can lead to such lengthy imprisonment, is a plain abuse of the most basic of human rights.

I was forced to withdraw my lifelong personal support for the EU when, in response to the vicious crushing of the Catalan referendum by Francoist paramilitary forces, when the whole world saw grandmothers hit on the head and thrown down stairs as they attempted to vote, all the institutions of the EU – Council, Commission and Parliament – lined up one after the other to stress their strong support for the Madrid paramilitary action in maintaining “law and order”.

Today we see the same thing. As the Catalans are imprisoned for efforts at democracy, the EU Commission stated that it “respects the position of the Spanish judiciary” and “this is, and remains, an internal matter for Spain, which has to be dealt with in line with its constitutional order.” The Commission here is simply ignoring what is very obviously a fundamental breach of basic human rights. This is far worse than anything Poland or Hungary have done in recent years, and the Commission is also showing a quite blatant hypocrisy in its relative treatment of its Western and Eastern members.

There was a time when the EU was a shining example of economic and environmental regulation and of regional wealth redistribution. My fondness for the institution dates from it being one of our few defences from economic Thatcherism. But it has evolved into something very different, a mutual support club for neoliberal political leaders.

I do not much blog about Brexit because I am less concerned about it than the majority of the population. I neither think remaining inside is essential nor that leaving it is a political panacea. I do desperately wish to retain freedom of movement, and believe leaving the customs union would be economic self-harm on a large scale. A Norway style relationship would suit me fine, but by and large I prefer to stay out of the argument. I do believe that, as a matter of democratic legitimacy, having had the 2016 referendum the result should be respected; England should leave and Scotland and Northern Ireland remain.

But I also say this. A million people are expected to march on Saturday in support of the EU. That is the EU which has just expressed its active support for the jailing of Catalans for holding a vote. They join Julian Assange as political prisoners in the EU held for non-violent thought crime.

I say this to anyone thinking of marching on Saturday.

It is morally wrong, at this time, to show public support for the EU, unless you balance it by showing your disgust at the fascist repression of the Catalans and the EU’s support for that repression.

Every single person going on Saturday’s march has a moral obligation to balance it by sending a message to the EU Commission that their support for this repression is utterly out of order, and carrying a flag or sign on the march indicating support for the Catalan political prisoners. Otherwise you are just a smug person marching for personal self interest. Alongside the progenitors of the Iraq War, who doubtless will again dominate the platform speeches.

* * *

Unlike his adversaries including the Integrity Initiative, the 77th Brigade, Bellingcat, the Atlantic Council and hundreds of other warmongering propaganda operations, Craig’s blog has no source of state, corporate or institutional finance whatsoever. It runs entirely on voluntary subscriptions from its readers – many of whom do not necessarily agree with the every article, but welcome the alternative voice, insider information and debate. Subscriptions to keep Craig’s blog going are gratefully received.

For close to 40 years the IMF has weaponized its handle on the western economy through the dollar-based western monetary system, and brutally destroyed nation after nation, thereby killed hundreds of thousands of people. Indirectly, of course, as the IMF would not use traditional guns and bombs, but financial instruments that kill – they kill by famine, by economic strangulation, preventing indispensable medical equipment and medication entering a country, even preventing food from being imported, or being imported at horrendous prices only the rich can pay.

The latest victim of this horrifying IMF scheme is Ecuador.

For starters, you should know that since January 2000, Ecuador’s economy is 100% dollarized, compliments of the IMF (entirely controlled by the US Treasury, by force of an absolute veto). The other two fully dollarized Latin American countries are El Salvador and Panama.

The Wall Street Journal recently stated that Ecuador “has the misfortune to be an oil producer with a ‘dollarized’ economy that uses the U.S. currency as legal tender.”The Journal added,

“the appreciation of the U.S. dollar against other currencies has decreased the net exports of non-oil commodities from Ecuador, which, coupled with the volatility of oil prices, is constraining the country’s potential for economic growth.”

Starting in the mid 1990’s, culminating around 1998, Ecuador suffered a severe economic crisis, resulting from climatic calamities, and US corporate and banking oil price manipulations (petrol is Ecuador’s main export product), resulting in massive bank failures and hyper-inflation. Ecuador’s economy at that time had been semi-dollarized, like that of most Latin American countries, i.e. Peru, Colombia, Chile, Brazil – and so on.

The ‘crisis’ was a great opportunity for the US via the IMF to take full control of the Ecuadorian (petrol) economy, by a 100% dollarizing it. The IMF propagated the same recipe for Ecuador as it did ten years earlier for Argentina, namely full dollarization of the economy in order to combat inflation and to bring about economic stability and growth. In January 2000, then President Jorge Jamil Mahuad Witt, from the “Popular Democracy Party”, or the Ecuadorian Christian Democratic Union (equivalent to the German CDU), declared the US dollar as the official currency of Ecuador, replacing their own currency, the Sucre.

Adopting another country’s currency is an absurdity and can only bring failure. And that it did, almost to the day, 10 years after Argentina was forced by the same US-led villains to revalue her peso to parity with the US-dollar, no fluctuations allowed. Same reason (“economic crisis”, hyper-inflation), same purpose: controlling the riches of the country – absolute failure was preprogrammed. Did Ecuador not learn from the Argentinian experience and converted her currency at the very moment the Argentinian economy collapsed due to dollarization, into the US dollar? – That is not only a fraud, but a planned fraud.

Ecuadorian goods and services quoted in dollars, became unaffordable for locals and uncompetitive for exports. This led to social unrests, resulting in a popular ‘golpe’. President Mahuad was disposed, had to flee the country, and was replaced by Gustavo Noboa, from the same CDU party (2000 – 2003). Ever since the dollar remained controversial among the Ecuadorian population. President Rafael Correa’s quiet attempt to return to the Sucre, was answered by a CIA-inspired police coup attempt on 30 September 2010.

In 2017, the CIA / NED (National Endowment for Democracy) and the US State Department have brought about a so-called “soft” regime change. They urged (very likely coerced) Rafael Correa to abstain from running again for President, as the vast majority of Ecuadorians requested him to do. This would have required a Constitutional amendment which probably would have been easily accepted by Parliament. Instead they had Correa endorse his former Vice-President (2007-2013) Lenin Moreno, who run on Correa’s platform, the socialist PAIS Alliance. Therefore, expected to continue in Correa’s line with same socioeconomic policies.

Less than a year later, Moreno turned tables, became an outright traitor to his country and the people who voted for him. He converted Ecuador’s economy to the neoliberal doctrine – privatization of everything, stealing the money from the social sectors, depriving people of work, drastically reducing social services and converting a surplus economy of tremendous social gains into one of poverty and misery.

President Correa left the country a modest debt of about 40% to GDP at the end of his Presidency in 2017. A debt-GDP ratio that would be no problem anywhere in the world. Compare this to the US debt vs. GDP – 105% in current terms and about 700% in terms of unmet obligations (net present value of total outstanding obligations). There was absolutely no reason to call the IMF for help. The IMF, the long arm of the US Treasury – ‘bought’ its way into Moreno’s neoliberal Ecuador, coinciding with Moreno evicting Julian Assange from the Ecuadorian Embassy in London.

The IMF loan of US$ 4,2 billion increases the debt / GDP ratio by 4% and brings social misery and upheaval in return, and that as usual, at an unimaginable cost, by neoliberal economists called “externalities”. It was practically a US “present” for Moreno’s treason, bringing Assange closer into US custody. What most people are unaware of, is that at the same time, Moreno forgave US$ 4.5 billion in fines, interest and other dues to large corporations and oligarchs, hence decapitalizing the country’s treasury. The amount of canceled corporate fiscal obligations is about equivalent to the IMF loan, plunging large sectors of the Ecuadorian population into more misery.

Besides, under wrong pretexts it allowed Moreno to apply neoliberal policies, all those that usually come as draconian conditions with IMF loans and that eventually benefit only a small elite in the country – but allows western banking and corporations to further milk the countries social system.

According to a 2017 report of the Center for Economic and Policy Research (CEPR), an economic thinktank in Washington, Ecuador’s economy has done rather well under Rafael Correa’s 10-year leadership (2007 – 2017). The country has improved her key indicators significantly: Average annual GDP growth was 1.5% (0.6% past 26 years average); the poverty rate declined by 38%, extreme poverty by 47%, a multiple of poverty reduction of that in the previous ten years, thanks to a horizontally distributive growth; inequality (Gini coefficient) fell substantially, from 0.55 to 0.47; the government doubled social spending from 4.3% in 2006 to 8.6% in 2016; tripled education spending from 0.7% to 2.1% with a corresponding increase in school enrollments; increased public investments from 4% of GDP in 2006 to 10% in 2016.

Now, Moreno is in the process of reversing these gains. Only six months after contracting the IMF loans, he has already largely succeeded. The public outcry can be heard internationally. Quito is besieged by tens of thousands of demonstrators, steadily increasing as large numbers, in the tens of thousands, of indigenous people are coming from Ecuador’s Amazon region and the Andes to Quito to voice their discontent with their traitor president. Government tyranny is rampant. Moreno declared a 60-day state of emergency – with curfew and a militarized country. As a consequence, Moreno moved the Government Administration to Guayaquil and ordered one of the most severe police and military repressions, Ecuador has ever known, resulting within ten days to at least 7 people killed, about 600 injured and about 1,000 people arrested.

The protests are directed against the infamous Government Decree 883, that dictates major social reforms, including an increase in fuel prices by more than 100%, reflecting directly on public transportation, as well as on food prices; privatization of public services, bringing about untold layoffs, including some 23,000 government employees; an increase in Aggregated Value Taxes – all part of the so-called “paquetazo”, imposed by the IMF. Protesters called on Moreno, “Fuera asesino, fuera” – Get out, murderer, get out! – Will they succeed?