Yuan Slides After China Unexpectedly Suspends “Counter-Cyclical Factor” In FX Fixing Tyler Durden

Tue, 10/27/2020 – 08:57

China keeps telling the world to stop buying the yuan, and the world keeps refusing to listen.

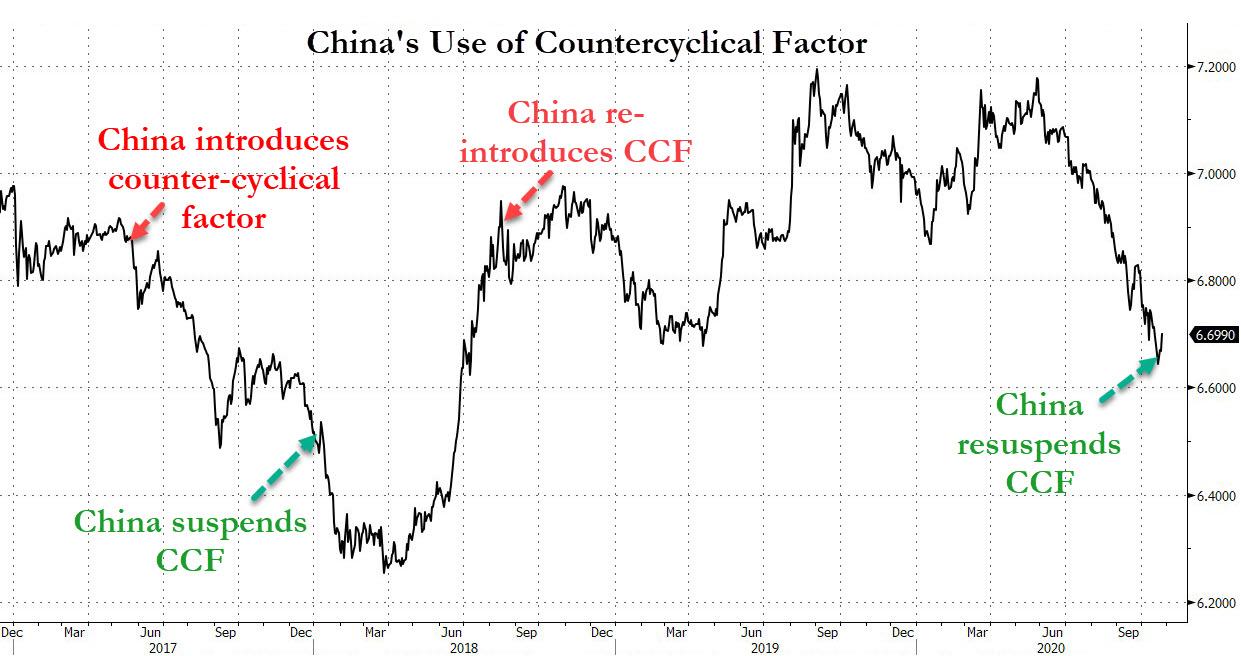

Just over two weeks after Beijing made it easier to short the yuan after the PBOC cut the reserve requirement ratio for FX derivative sales from 20% to 0%, a move which was “an attempt to moderate the yuan’s increase”, and which Goldman said “likely signals the PBOC’s discomfort with the recent rapid appreciation of CNY”, yet which failed to lead to a sustainable drop in the yuan, On Tuesday China lobbed another shot across the bow of the increasingly strong yuan when a statement on website of China Foreign Exchange Trade System announced that some banks that contribute to the yuan’s daily reference rate have recently halted the use of the counter-cyclical factor (CCF).

The confirmation followed a Reuters reports that the PBoC has asked banks to neutralize the counter-cyclical factor which is typically used when the currency is weakening at a pace that is uncomfortable for the central bank i.e. effectively removing it in the midpoint fixing. Under the reported tweak, lenders would have more room to submit quotes for a weaker fixing and guide the currency lower in the spot market, which is precisely Beijing’s goal in light of the recent yuan appreciation. The move followed sellside analyst reports in recent months that as a result of the recent strength in the Yuan, the CCF had not been used.

As a reminder, the counter-cyclical factor was introduced by the PBOC on May 26, 2017 to reduce exchange-rate volatility while undermining efforts to increase the role of market forces. At the time, the move was seen as Beijing “moving the goalposts” in its bid to reduce yuan volatility, to punish currency manipulators (read Yuan shorts) and limit capital outflows (the currency had weakened for three straight years, triggering draconian capital controls and the surge of bitcoin). The CCF was then suspended in January 2018 when the yuan surged, only to be reinstalled later that year when the Yuan slumped again.

And now the CCF has been re-suspended again.

According to Citi FX trader Charmaine Cheok this is “yet another signal from the central bank that they are loosening the reins on the currency and allowing for more flexibility. I reckon the reason the market is moving higher on spot now is merely a reflection of positioning, this announcement doesn’t have any immediate impact on spot.”

Other trading desks agreed, noting that this is in line with the policy direction to allow the FX to be more market driven and ties into the goal to promote RMB internationalization. Or at least allowing it to be market driven when it is strong, hoping the recent deflationary appreciation in the yuan will end.

In any case, now that China has confirmed the move, strategists expect higher volatility of the CNH/CNY given the CCF typically dampens stronger USD impact on fixing more than the appreciation side, even if the actual impact could be relatively limited.

While the market impact was muted indeed, the offshore yuan fell after the Reuters report, dropping as much as 0.34% to 6.7234 a dollar afterward. The currency has rallied 6.9% from a low in May and last week reached a two-year high.

And now that the PBOC has both cut reserves and re-suspended the CCF in hopes of weakening the yuan, and seemingly failed…

… the question everyone should be asking is what will China do now to further devalue its currency which continues to surge on the back of dollar weakness and China’s “V-shaped recovery” One wonders: is China’s economy about to suffer an “unexpected” sharp spike in covid cases to help the PBOC hammer the yuan?

via ZeroHedge News https://ift.tt/34yIj37 Tyler Durden

This post was originally my comment to a person on Facebook, which somebody then deleted. This person repeatedly throws out the 1.2 M deaths worldwide number and I finally lost it and posted a response to him after he scolded people for “spreading disinformation and not listening to science”. He actually told people disputing the Second Wave Hysteria to “shut up and listen to the government and science”.

As one of my all-time favourite economists, Thomas Sowell, would say…. “Oh dear, where to begin?”

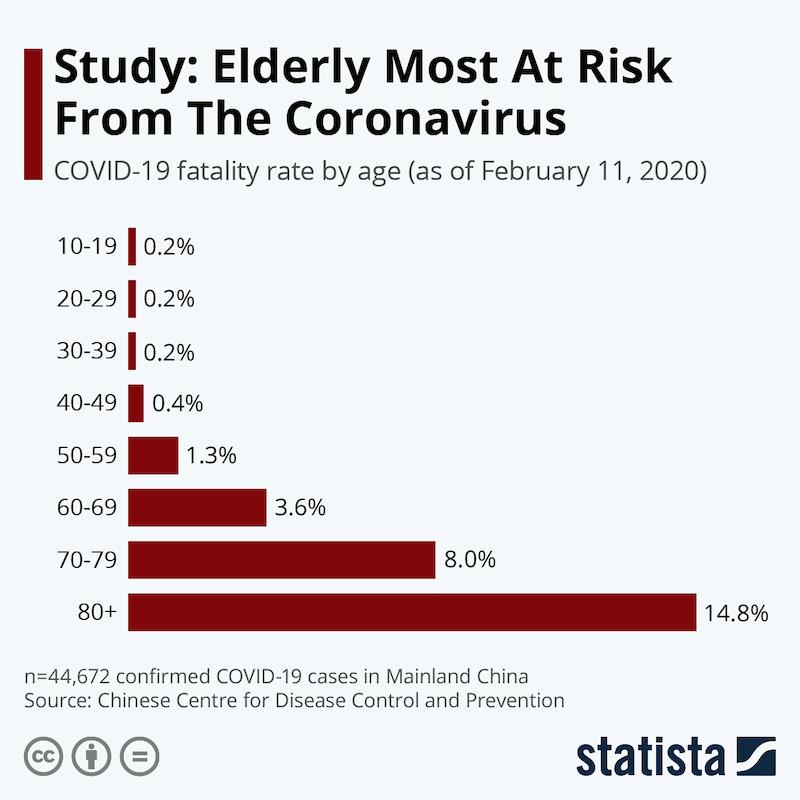

1 million or 1.2 million deaths worldwide sounds like a big number and on its own you can use it to club “Covidiots” into silence, that is, until you actually look at it.

For starters, bandying out a number, any number in isolation is meaningless. For any number to have any relevance, to anything, it has to be part of a data set or otherwise part of some meaningful comparison.

If we take the 1.2 million COVID deaths worldwide, at it’s face (more on that below), the obvious question then becomes “is that good or bad?”

The most useful signal we can get from a global COVID death toll is how it compares to what is called the “Absolute Fatality Rates” globally, which is simply the rate of all fatalities from all causes.

From the charts, we can clearly see, there was a lot of excess mortality in March and April, and then, like every other meaningful metric around Coronavirus, it drops off drastically and starts to level out, with a slight seasonal rise as we head into the winter.

Interestingly, in “no lockdown” Sweden, it turns out their absolute death toll is much lower than one would think:

It could possibly come in lower by the end of the year, but if not, will come in not that much higher. Not as high as, say, the US or England.

If reducing fatalities is the goal, there is a much easier way to do that

Sadly, a lot of people die every day, and I’m sure you’ve seen memes on social media on how many more people die from other causes like Tuberculosis (1.4M in 2019) than COVID-19.

If this is about saving lives, we could literally bring those alcohol related deaths to zero, turning it off like the flick of a switch by instituting a global ban on alcohol. We could do it tomorrow. Should we? The lives we save may include your own.

In fact if we banned alcohol then we could let Coronavirus run and still be ahead nearly 2M preventable deaths annually, provided COVID-19 kept going with the same intensity it was going in March and April, which it clearly isn’t (see below).

Of course, nobody would seriously entertain that, and they could probably articulate some decent logic around why we shouldn’t.

But they may dismiss it without considering how closely the lockdown approach toward reducing COVID fatalities is analogous to a worldwide ban on alcohol to eliminate alcohol related deaths would be. Especially since we also know that a large portion of coronavirus fatalities die with COVID-19 and numerous other comorbidities* than of it (however, see my footnote on that at the end of this post).

In that sense, alcohol related carnage is very similar. Few alcoholics drink themselves to death outright. Comparatively more kill themselves (and others) in car accidents, commit suicide, or generally wreck their livers, hearts, kidneys, brains or generally run themselves down so low nearly anything else will finish them off.

Second Wave Hysteria

Case counts are clearly rising again globally, that much is true and we have oodles of data to track it. With it, there come fears of the dreaded “Second Wave” of fatalities.

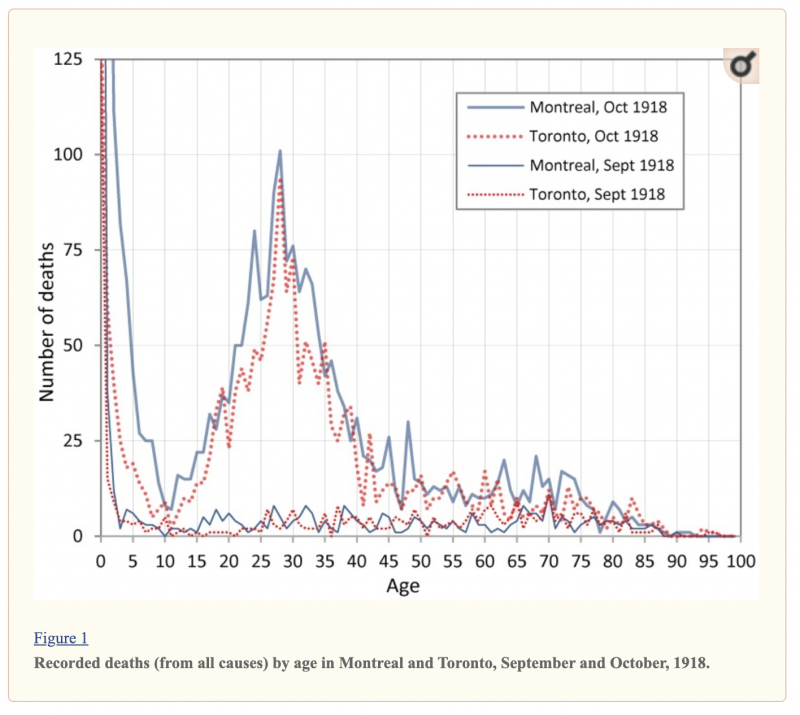

In the often cited Spanish Flu of 1918, the bulk of the fatalities came in the second wave. However, the Spanish Flu was a very different pandemic than the one we have today. That one attacked people right in the early years of the prime-of-life age curve:

Scientists believe the nature of that strain caused “cytokine storms”, the phenomenon where the immune system overreacts and attacks itself. In a perverse twist of fate, this made the population with the strongest immune systems more vulnerable to the flu.

Contrast with COVID-19 where nobody disputes that the most vulnerable members of the population are the elderly and those with underlying medical conditions that render them immuno-compromised. In this sense, comparing 1918 to COVID-19 is not accurate or useful.

So, bear this in mind as I put in the graph below of how the Coronavirus Second Wave is playing out when it comes to case counts vs fatalities:

If we were in for a 1918-style Second Wave fatality overrun, we would see it in the data. As I pointed out in my previous post, the above data comes from the Province of Ontario, but pretty well all graphs from locales undergoing second waves in case counts, look the same. The fatalities are riding the floor (that “spike” in the fatality count was a data correction where they took previously missed data from the proceeding 90 days, and added them all to 2 data points), but the case counts are going up, as are the number of tests.

Right now the slope of the case count far exceeds the slope of the fatalities.

For the fatalities to come in anywhere near the Second Wave of 1918 scenario, the slope of the fatality line needs to blast off in a near vertical line right now. In the Ivor Cummins interview he mentioned Dr. Sunetra Gupta’s work indicating that COVID seems to peter out when it hits 20% of the population (but I can’t find the cite). If true, it is hard to envision a scenario where that is mathematically possible.

If not true, and we’re about to experience a Second Wave of fatalities, it would be impossible to occur without seeing it in the data and right now, all of the data, everywhere is showing either a moderate rise with seasonality, or an aggregate, overall decrease in fatalities.

All of this should be good news, but for some reason, people become very upset when you try to walk them through this. I’m open to all logic, data and science based objections or counter-points to where I am wrong on this, bearing in mind that “SHUT UP AND LISTEN TO THE GOVERNMENT AND SCIENCE” isn’t a logical, scientific or data driven counter-argument.

What to do next.

I would close out with two additional reading exercises, one, I would go look at and sign The Great Barrington Declaration and two, have a look at the comparison of The Great Barrington Declaration with what’s called “The John Snow Memorandum“.

(*The number you see bandied around a lot is 94% of all COVID-19 fatalities had comorbidities. This number largely keys off CDC data that only 6% of fatalities list only COVID-19 as a c.o.d. If you look at the CDC data on what the comorbidities are, the biggest one accounting for close to half of all fatalities, especially in the elderly, is pneumonia and influenza. I think it’s inaccurate to just net-out all of those cases and dismiss them as comorbidities because that is one of the most common ways respiratory viruses manifest. But that said, the data, when you consider comorbidities and the looseness with which COVID gets added to c.o.d’s, what all this means is that the headline number for fatalities is the top boundary. They aren’t higher, and they are probably for all practical purposes, lower).

via ZeroHedge News https://ift.tt/2Tw7oW9 Tyler Durden

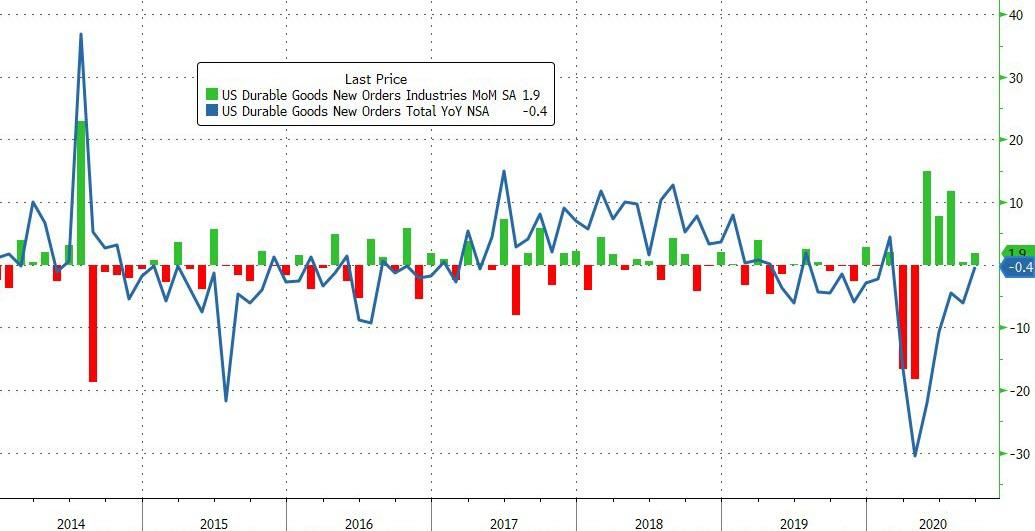

US Durable Goods Orders Beat In September, Remain Lower Year-Over-Year Tyler Durden

Tue, 10/27/2020 – 08:35

August’s significant slowdown in the rebound of US Durable Goods Orders was expected to continue in early September data, but instead the Census Bureau printed a big surprise beat, rising 1.9% MoM (against +0.5% exp).

Source: Bloomberg

However, headline durable goods orders remain (marginally) lower on a YoY basis (-0.4%) and below February’s pre-COVID levels…

Source: Bloomberg

Core capital goods orders, a barometer for business investment which excludes aircraft and military categories, rose 1% in September, also more than forecast, after an upwardly revised 2.1% advance a month earlier.

via ZeroHedge News https://ift.tt/3ovBpU6 Tyler Durden

France Weighs Return To Lockdown As Russia Refuses Despite Spike In COVID-19 Cases, Deaths: Live Updates Tyler Durden

Tue, 10/27/2020 – 08:28

Already Tuesday morning we are seeing some headlines out of Europe that portend more headlines that could spook markets later on in the session. For starters, a second Bavarian county has declared a partial lockdown. Rottal-Inn has recorded well over 200 new infections per 100,000 inhabitants over the past week, well above the threshold of 50 new infections per 100,000 people at which new measures are required.

On Tuesday, the Robert Koch Institute reported 11,409 new infections, bringing Germany’s total to 455,829. Another 42 people died on Tuesday, bringing the country’s overall virus death toll to 10,098. Hospitals and ICUs are filling up again and German Chancellor Angela Merkel has expressed grave concern, saying the current restrictions are not strong enough to slow down the spread of the virus, as the country widely expects her government to impose more nationwide rules shortly. These could include closing restaurants and stopping live events.

Merkel will meet with the state governors Wednesday. The German press has reported that new restrictions are expected, including taking school closures and restrictions on nonessential businesses nation-wide. It comes after Italy, Spain and a host of other European countries imposed new COVID-inspired restrictions over the weekend.

But looking ahead, all eyes are on France, where a government minister recently warned the pace of infections might be as high as 100k/day, 2x the official total. On Wednesday, President Emmanuel Macron, Prime Minister Jean Castex (Macron’s virus point man) and other top officials are meeting to discuss new nationwide restrictions, possibly including another brief lockdown, something that Macron has said would be ‘unavoidable’ if the condition deteriorates beyond a certain point.

The Local published a handy guide to the different types of measures reportedly under consideration, which, at this point, is either localized lockdowns (Paris, Lyon and Marseille and possiby other cities and metro areas) or a nationwide closure (text below courtesy of the Local).

1. Total lockdown

The first option is a total, nationwide lockdown such as the one France imposed in March. Back then, the whole country was confined to their homes and only allowed out for short periods to run essential errands such as grocery shopping, medical appointments and walking the dog.

French political commentators say this is the least likely scenario because of the high economic and psychological costs that would entail.

“I think that Macron is desperate to avoid another complete lockdown – for economic reasons but also for reasons of public order. A second “confinement” would be resisted much more widely than the first,” The Local’s political commentator John Lichfield said.

Delfraissy said the main goals of the government was to protect France’s elderly and vulnerable and maintain economic activity, while at the same time reducing the spread of the virus.

If the government were to impose a new lockdown, it would likely be adapted to the lessons drawn from this spring, avoiding to close down parts of society where the health gains were small compared to the economic and social costs – such as primary schools.

“It would probably allow for a certain level of educational activity and a certain number of economic activity,” Delfraissy said, adding that this kind of lockdown “could be set in place for a shorter period of time if it were to be introduced now.”

He also said this kind of lockdown would likely be followed by a period of curfew such as the one in place now.

2. Local lockdowns

Another option is to continue the government’s strategy to adapt measures to local conditions and introduce lockdowns in the country’s hardest hit areas.

This would target areas with high levels of spread and areas where hospital struggle to cope with the pressure of new Covid-19 patients, such as Paris, Marseille and Lyon.

“I’d rather have local lockdowns now than a nationwide lockdown at Christmas,” Damien Abad, parliament chief for the rightwing opposition Les Republicains, told France Info radio.

3. Weekend lockdowns

The third option would be a lighter and adapted version of lockdown, which could include measures such as a weekend confinement and an earlier curfew than the 9pm curfew currently in place in roughly half of the country.

“This would be much tougher than the curfew currently in place,” Delfraissy said about that option.

Such a strategy has received support from a group of doctors in Lyon, who called for a 7pm curfew and a weekend lockdown.

“The situation is serious and we cannot afford to take half-measures any longer,” they said in a press statement.

This strategy could also entail closing secondary schools, high schools and universities, such as suggested by Antoine Flahault, Director of the Institute for Global Health at the University of Geneva, which monitors the development of Covid-19 in the world.

We already have taken lockdown measures, they might be sufficient,” he told French media.

* * *

Meanwhile, France’s small businesses are understandably anxious. On Tuesday morning, the CPME confederation of small and medium-sized businesses warned that a partial or total lockdown could risk provoking an economic collapse. Companies are “much more fragile than in March” and many, especially the smallest, would be incapable of taking on additional debt, the CPME says in statement on Tuesday “We would risk seeing a collapse in the French economy, a sort of unprecedented third wave, this time an economic one,” CPME says

Here’s some more COVID-19 news from overnight and Tuesday:

Russia is balking at reintroducing tough measures even as its outbreak explodes and deaths hit record highs. Masks will be compulsory in some public places starting on Wednesday, but the authorities are avoiding action that could hurt businesses. The consumer health watchdog recommended on Tuesday to close bars and restaurants from 11 p.m. to 6 a.m. amid reports that many hospitals are at capacity. Kremlin spokesman Dmitry Peskov said earlier the authorities are confident they can handle the latest wave without a lockdown (Source: Bloomberg).

Eli Lilly said last night that it would be ending clinical trials for patients in a hospital setting after NIH researchers found that BAMLANIVIMAB, one of the antibody therapeutics the company is working on, doesn’t help to improve hospitalized patients recovery from advanced stages of the virus, although Eli Lilly noted that all other studies related to its treatment are ongoing. It’s the latest setback to therapeutics. The FDA recently gave remdesivir, a drug developed by Gilead originally to treat ebola, the greenlight for widespread use, even as studies show it has little to no benefit (Newswires).

The French government is reportedly mulling a localized lockdowns for the Paris, Lyon and Marseille metro areas, which would include 7pm curfew, a public transport shutdown and closing non-essential shops, while reports noted that a three-week lockdown could start from Friday evening with the details to be announced on Wednesday (Source: Bild).

Germany Economy Minister says that the number of new infections in the nation are rising exponentially and will likely have 20k daily new infections by the end of the week (Newswires).

Imperial College London/Ipsos MORI study among 365k randomly selected adults which conducted tests at home, showed that 4.4% had antibodies in September vs. 6.0% in June which suggested the antibody immunity may not last over time in some of those that were infected. (Newswires) Russia is to impose new COVID-19 restrictions (Source: RIA Novosti).

via ZeroHedge News https://ift.tt/2TxlI0k Tyler Durden

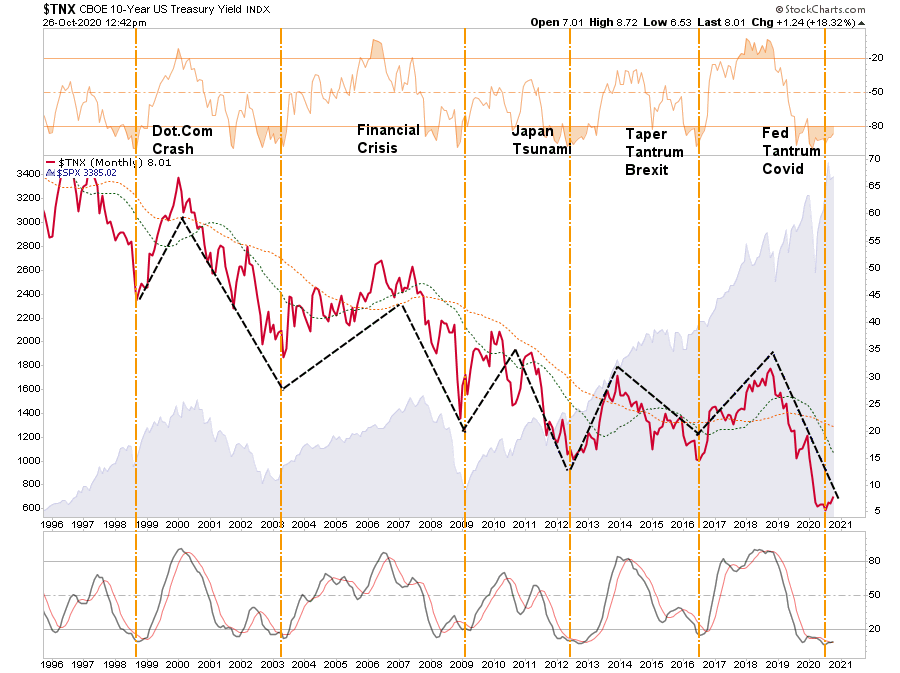

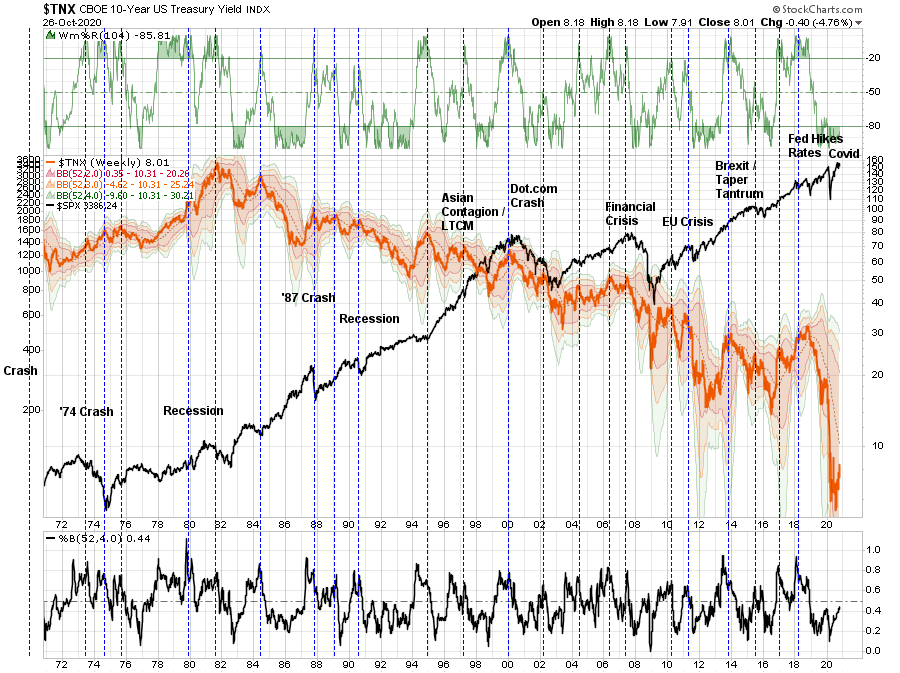

Here we go again. After plunging to new lows, the calls for the end of the “bond bull” market mount each time rates rise. Is this time the end of the “bond bull?”Or, is there another huge bond-buying opportunity to come?

We recently reduced our exposure to bonds, the first time in years, due to the more extreme overbought condition of Treasury bonds following the pandemic’s onset. The long-term chart of yields below shows this to be the case.

There are two critical points to take away from the chart above.

Interest rates are currently extremely oversold (top and bottom panels), suggesting that rates could indeed rise over the next few months. Such could coincide with another stimulus package or the passage of an “infrastructure” bill that leads to short-term inflationary concerns.

When rates do rise from deeply oversold levels, there is a point where high rights collide with debt levels triggering either a credit-related event, a stock-market correction, or worse.

There are currently two significant risks from rising interest rates, which investors should heed.

Valuation Expansion

One of the primary themes used by the “Permabulls” is that “valuations are cheap due to low interest rates.” That argument has been the clarion call of a generation of investors who have ignored fundamentals and valuations to chase market returns.

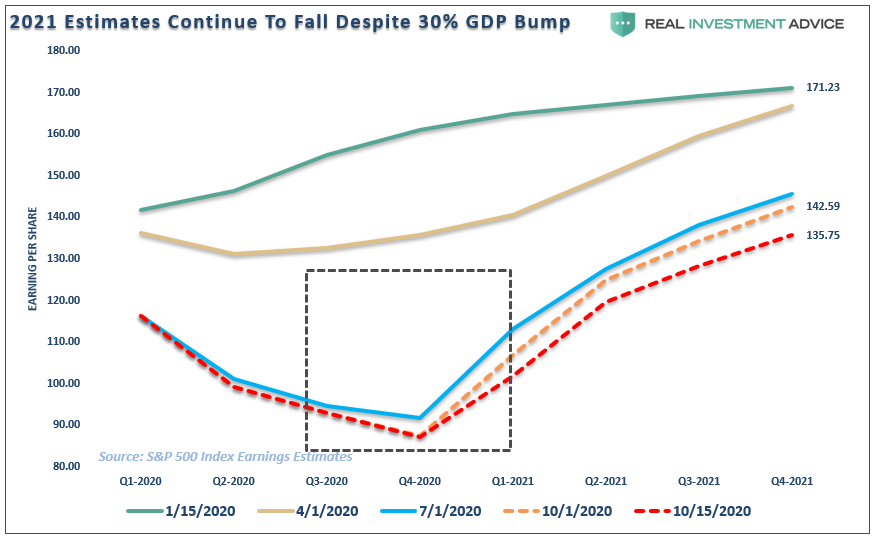

Since 2019, when earnings growth began to deteriorate in earnest, investors bid up shares. As such, the primary driver of returns, as shown below, has come from “multiple expansion.”

The “hope” remains that earnings growth will eventually catch up with valuations. However, despite being 3/4ths of the way through 2020, the outlook for earnings continues to deteriorate. In just the last 15-days, the estimates for 2021 have declined by almost $7 per share despite repeated statements of a recovering economy.

Historically, such has not ever been the case; and,

When rates rise, valuations quickly become an issue.

However, since stock prices reflect economic growth, the impact of rising rates on the economy is a far more significant issue.

The Debt Problem

People don’t buy houses or cars. They buy payments. Payments are a function of interest rates, and when interest rates rise sharply, mortgage activity falls as payments rise above expectations. In an economy where roughly 70% of Americans have little or no savings, an adjustment higher in payments significantly impacts consumption.

Rising interest rates raise the debt servicing requirements, which reduces future productive investment.

As stated above, rising interest rates will immediately slow the housing market taking that small contribution to the economy. People buy payments, not houses, and rising rates mean higher payments.

An increase in interest rates means higher borrowing costs. Such leads to lower profit margins for corporations reducing corporate earnings and financial markets.

The negative impact on the massive derivatives and credit markets is the Fed’s worst fear.

As rates increase, so does the variable rate interest payments on credit cards. With the consumer struggling with stagnant wages and increased living costs, higher credit payments lead to a contraction in spending and rising defaults.

Rising defaults on debt service will negatively impact banks, which are still not adequately capitalized and still burdened by massive levels of bad debts.

Many corporate share buyback plans and dividend issuances are accomplished through cheap debt, leading to increased corporate balance sheet leverage. That will end.

Corporate capital expenditures are dependent on borrowing costs. Higher borrowing costs lead to lower CapEx.

The deficit/GDP ratio will begin to soar as borrowing costs rise. The many forecasts for lower future deficits will crumble as new forecasts begin to propel higher.

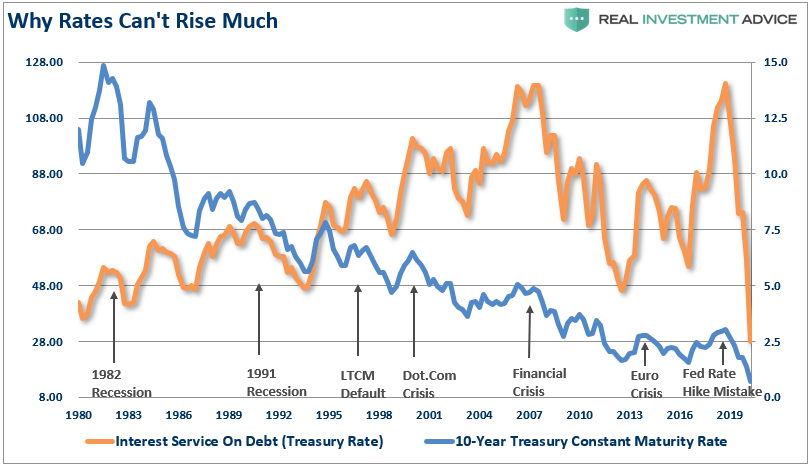

“Such is also why interest rates CAN NOT rise by very much without triggering a debt-related crisis. The chart below is the interest service ratio on total consumer debt. (The graph is exceptionally optimistic as it assumes all consumer debt benchmarks to the 10-year treasury rate.) While the media proclaims consumers are in great shape because interest service is low, it only takes small increases in rates to trigger a ‘recession’ or ‘crisis’ event.”

Am I saying rates can’t rise at all?

Absolutely not. However, there is a limit before it negatively impacts the economy, and ultimately the stock market.

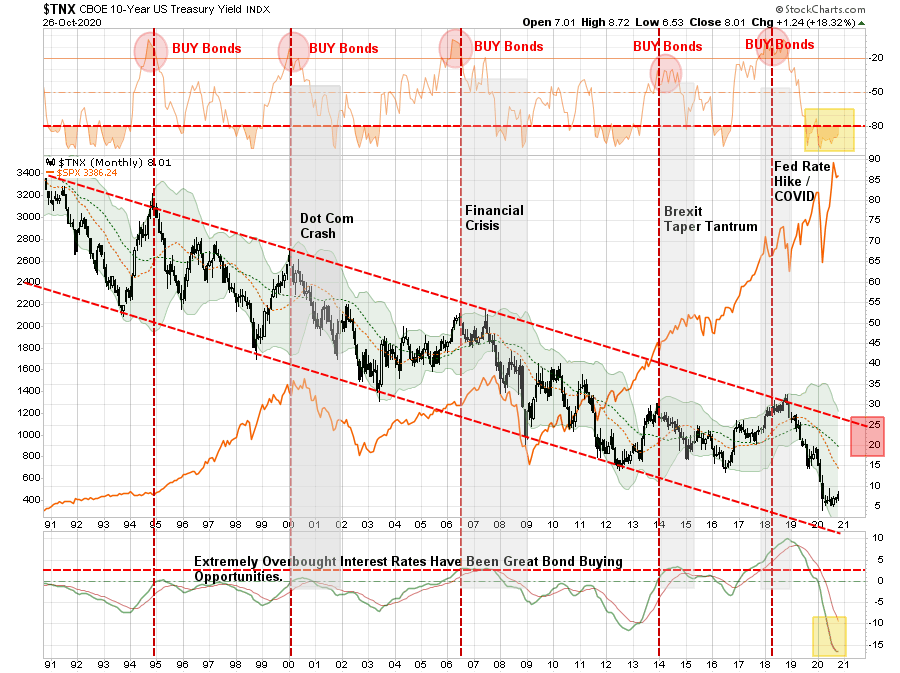

Bond Prices Very Overbought

In June of 2013, when the cries of the “death of the bond bull market” were rampant, I made repeated calls that then was an ideal time to be a “buyer” of bonds.

“However, the recent spike in interest rates has certainly caught everyone’s attention and begs the question is whether the 30-year bond bull market has indeed seen its inevitable end. I do not think this is the case and, from a portfolio management perspective, I believe this is a prime opportunity to increase fixed income holdings in portfolios.”

As shown in the chart below, that was the correct call and, despite repeated wrong calls by the mainstream analysts, bonds remained in an ongoing bullish trend.

Since interest rates are the inverse of bond prices, we can look at a long-term chart of rates to determine when bonds are overbought or oversold.

In 2019, rates began to slide slower as the realization that economic growth was weakening weighed on outlooks. As the yield curve began to invert, the Federal Reserve stepped in with expanded “repo” operations to shore up financial institutions.

Rates kept going lower.

In March of 2020, the economy was shut down due to the pandemic causing rates to plunge to record lows.

Huge Bond Buying Opportunity Coming

The plunge in rates and massive Fed liquidity caused stocks to surge to new highs despite an underlying recessionary economy.

Currently, the plunge in interest rates pushed bonds to an extreme “overbought” condition.

Such suggests the most likely target for rates in the near term could be as high as 2.0%. While an increase of 1.2% from current levels doesn’t sound like much, that increase would push bonds back to “oversold.” That move will provide the best opportunity to increase bond exposure in portfolios.

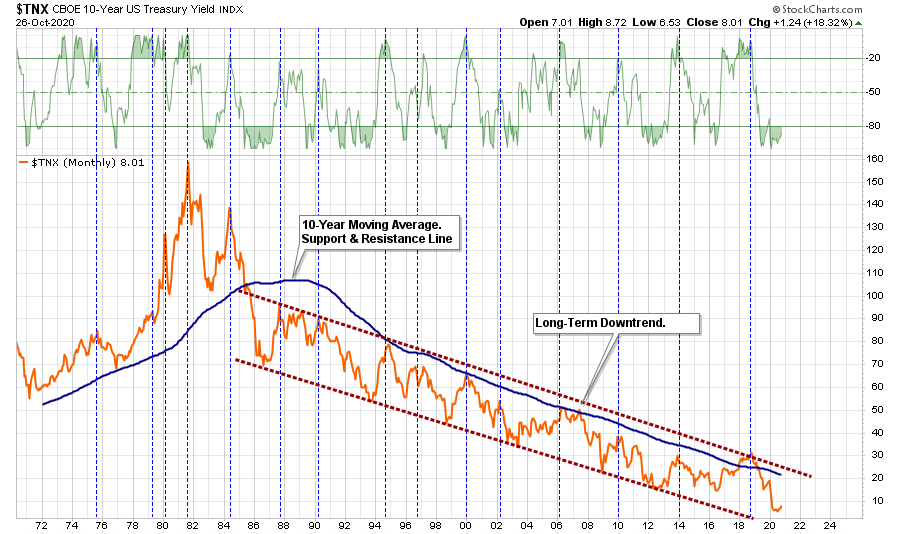

We can confirm the same using a very long-term chart (50-years) of 10-year interest rates overlaid with a 10-year moving average. As you can see, that moving average has provided formidable resistance and denoted every peak in rates going back to 1988.

Currently, with interest rates at the bottom of their long-term trend, the risk is that rates could indeed rise in the months ahead.

What could cause such an increase in rates?

A massive debt-funded stimulus package that sends increased amounts of funds directly to households.

More debt-funded infrastructure programs.

If the government further increases deficit spending programs that fail to produce economic benefits such as universal basic incomes.

An increase of economic activity as the economy reopens, and a post-recessionary recovery occurs.

If there is a point where the Federal Reserve is unable or unwilling to monetize the entirety of the debt issuance

A lack of demand by foreign buyers of U.S. debt over concerns on economic strength and financial stability due to debt-to-GDP ratios.

These lead to concerns over temporary inflationary spikes, which could drive interest rates back to the top of the long-term downtrend.

Where To Invest While We Wait For Bonds

While bond prices currently remain overbought, such a condition will likely not last very long. As shown below, markets and volatility have an inverse relationship with rates, hence the non-correlation for portfolios. The long-term log-chart of interest rates and the stock market tells the tale.

This analysis also suggests that the correction that started in March is likely not over as of yet in the longer term. If rates rise back toward the long-term downtrend, bond prices will come under pressure as the stock market corrects.

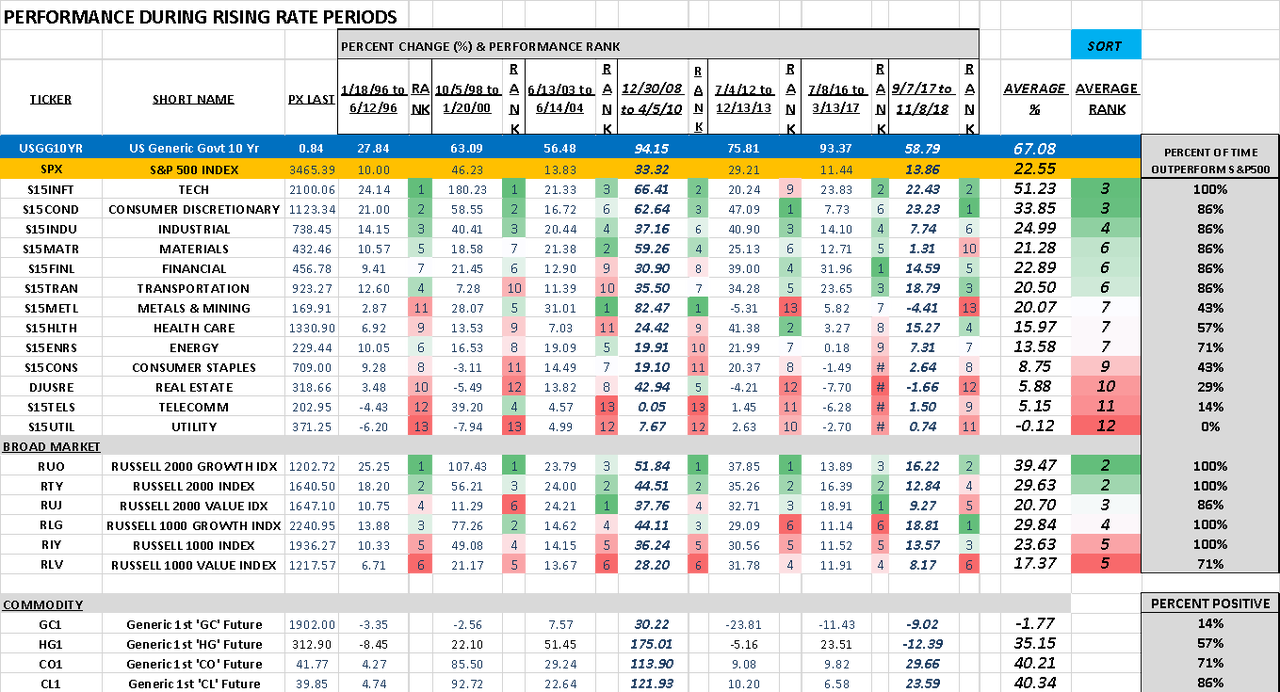

Commodities: Crude and Copper are positive over half the time. Crude is the best performing commodity, historically.

Gold is the worst-performing commodity; it is only positive 14% of the time.

2 more focus items:

TECH beat the S&P500 100% of the time

Utilities underperformed the S&P500 100% of the time”

Not The End Of The Bond Bull

In the short term, we have cut our bond exposure and have begun to shift our allocations to protect portfolios for a rise in interest rates.

However, as rates rise within their technical downtrend, the media will be replete with headlines about the death of the 40-year “bond bull market.”

It won’t be.

The stock market will defy higher rates initially until rates start to undermine the valuation story.

A weaker economy will undermine the valuation story as higher interest rates impede consumption.

The bullishly biased media will find themselves lost as to why stocks crashed and earnings fell.

While in the very short-term, the current overbought condition suggests we could see more downside pressure in bonds over the next few months. Such would not be surprising.

However, as we approach that point where the market begins to realize the impact of higher rates on economic growth and corporate profitability, bonds will again emerge as a haven for investors against market declines.

In an economy that is $75 Trillion in debt, requires $5.50 of debt per $1 of growth, and running a $3 Trillion deficit, rates can’t rise much.

Futures Rebound From Monday’s Plunge On Strong Earnings, Mega Merger Tyler Durden

Tue, 10/27/2020 – 08:10

U.S. index futures and European stocks rebounded on Tuesday following the S&P 500’s worst day in a month as investors parsed through strong corporate earnings which offset Monday’s SAP shocker, while bracing for volatility ahead of Election Day, assessing rising coronavirus cases across the globe and conceding that a fiscal stimulus deal just won’t happen now that the Senate has closed for recess after rushing through the appointment of Amy Coney Barrett to the SCOTUS late on Monday night, which was also Hillary Clinton’s birthday. AMD’s $35 billion acqusition of Xilinx also helped boost trader optimism.

The S&P 500 and Nasdaq hit three week lows on Monday as record number of new coronavirus infections in the United States and some European countries and a lack of agreement in Washington over the next U.S. fiscal stimulus raised worries about the economic recovery. The chances are “very, very slim,” Appropriations Chairman Richard Shelby said talking about a stimulus, pointing out the patently obvious. Differences between the two sides “have narrowed,” but “the more it narrows, the more conditions come up on the other side,” White House economic adviser Larry Kudlow told reporters. Of course, Nancy Pelosi remains optimistic, her spokesman said, but she’s used similar language throughout three months of talks as she does not want to take the blame for the continued gridlock.

Also on Monday, the VIX spiked to its highest closing level in nearly two months on “concerns” about President Donald Trump’s unexpected victory or the uncertain election outcome we first reported on Sunday night. As we also reported, while Joe Biden leads the official polls, the race is much tighter in battleground states which determine the election outcome.

In premarket trading, Drugmaker Eli Lilly fell 4% after it reported a fall in quarterly profit. Industrial companies 3M Co and Caterpillar Inc were also slightly lower after results. Investors are looking forward to results from Apple, Amazon.com, Alphabet and Facebook Inc in an earnings-heavy week as the technology giants have managed to stand out during the coronavirus pandemic. Chipmaker Xilinx soared after AMD announced a $35BN takeover offer, while Merck climbed after the drugmaker boosted its guidance.

At 8am S&P 500 E-minis rose 0.47% to 3,409.5 points.

The Stoxx Europe 600 Index erased most of its decline after earlier heading toward its lowest close since June amid concern about the relentless spread of coronavirus. Declines in miners and energy firms offset positive earnings from banking powerhouses HSBC Holdings and Banco Santander, which both signaled a brighter outlook for dividends. Following two tumultuous quarter, HSBC said it would consider paying a 2020 dividend after the bank unveiled a better-than-expected third quarter profit on lower provisions for bad loans. The bank on Tuesday reported a 36 per cent year-on-year drop in pre-tax profits to $3.1bn for the third-quarter, which was above analysts’ forecasts. Noel Quinn, HSBC’s chief executive, labelled the results “promising.” Energy giant BP Plc warned of many challenges ahead as the pace of recovery in oil demand remained uncertain. Meanwhile, Europe took a step closer to the strict rules imposed during the initial wave of the pandemic, with leaders struggling to regain control of the spread while confronting growing opposition to restrictions.

Earlier in the session, Asian stocks fell, led by the energy and finance sectors, after falling in the last session. Most markets in the region were down, with Australia’s S&P/ASX 200 dropping 1.7% and South Korea’s Kospi falling 0.6%, while India’s S&P BSE Sensex Index increased 0.5%. The Topix was little changed, with Nintendo climbing and Nidec slipping.

As Bloomberg notes, with time effectively over to finish an aid package before Americans vote, investors are looking for market catalysts later on Tuesday from data and earnings. Durable-goods orders and consumer confidence reports are due, as well as results from Microsoft Corp. and AMD after market.

In rates, Treasuries were steady overnight, holding Monday session gains despite gains in S&P 500 e-minis amid poor volumes, trading around 60% of recent average during Asia, early Europe. Preliminary open interest data shows some unwind of long-end short positions into Monday’s rally. Yields were mixed, although within a basis point of Monday’s close across the curve; 10-year steady at around 0.80%, trading inline with bunds and outperforming gilts by ~1bp. Treasury auctions kick-off with $54b 2-year note sale today, followed by 5- and 7- year sales Wednesday and Thursday, respectively.

On Monday, BlackRock strategists downgraded U.S. Treasuries and upgraded their inflation-linked peers ahead of the U.S. election on a growing likelihood of significant fiscal expansion. They said Covid infections in Europe threaten to derail a fragile recovery as they recommended investors hold a neutral position on bunds to hedge a downturn.

“As Covid infections have picked up, the focus on further policy response has shifted to more monetary easing including additional asset purchases,” said strategists Mike Pyle, Scott Thiel and Beata Harasim.

In Fx, a gauge of the dollar’s strength edged lower after Monday’s bounce, while the euro and the pound were little changed; cable slipped earlier with strategists predicting limited gains in the currency on a Brexit trade-deal breakthrough. The Norwegian krone and the Japanese yen led G-10 currency gains, while the Swiss franc and the Swedish krona weakened the most. China’s currency weakened after Reuters reported the country’s central bank asked lenders to suspend a key factor used to calculate the yuan’s daily reference rate.

Elsewhere, crude oil nudged higher while gold remains largely unchanged.

Market Snapshot

S&P 500 futures up 0.2% to 3,3400.50

STOXX Europe 600 down 0.4% to 354.57

MXAP down 0.2% to 175.21

MXAPJ down 0.3% to 581.84

Nikkei down 0.04% to 23,485.80

Topix down 0.09% to 1,617.53

Hang Seng Index down 0.5% to 24,787.19

Shanghai Composite up 0.1% to 3,254.32

Sensex up 0.6% to 40,372.74

Australia S&P/ASX 200 down 1.7% to 6,051.02

Kospi down 0.6% to 2,330.84

Brent futures up 0.7% to $40.75/bbl

Gold spot down 0.1% to $1,900.30

U.S. Dollar Index little changed at 93.07

German 10Y yield unchanged at -0.581%

Euro down 0.04% to $1.1805

Italian 10Y yield fell 1.9 bps to 0.536%

Spanish 10Y yield fell 0.2 bps to 0.184%

Top Overnight News from Bloomberg

The world’s biggest money manager is shorting the dollar on expectations that unprecedented fiscal and monetary stimulus will prolong its losses — regardless of who wins the U.S. election

Turkey’s banking regulator took another step to slow lending after a massive credit boom contributed to a currency rout

U.S. President Donald Trump’s push for a second poll-defying victory is relying on a hallmark of his first — raucous campaign rallies that Trump sees as a crucial sign of voter enthusiasm but that pollsters say may only be cementing his defeat

More than 50 of Boris Johnson’s own Conservative members of Parliament have demanded a clear route out of lockdown for parts of northern Britain that helped give his party a majority in last year’s election. In a letter to the prime minister, the MPs warned that his pandemic strategy of targeting local areas with restrictions is disproportionately damaging the economies of northern regions of the country

via ZeroHedge News https://ift.tt/37XZAFd Tyler Durden

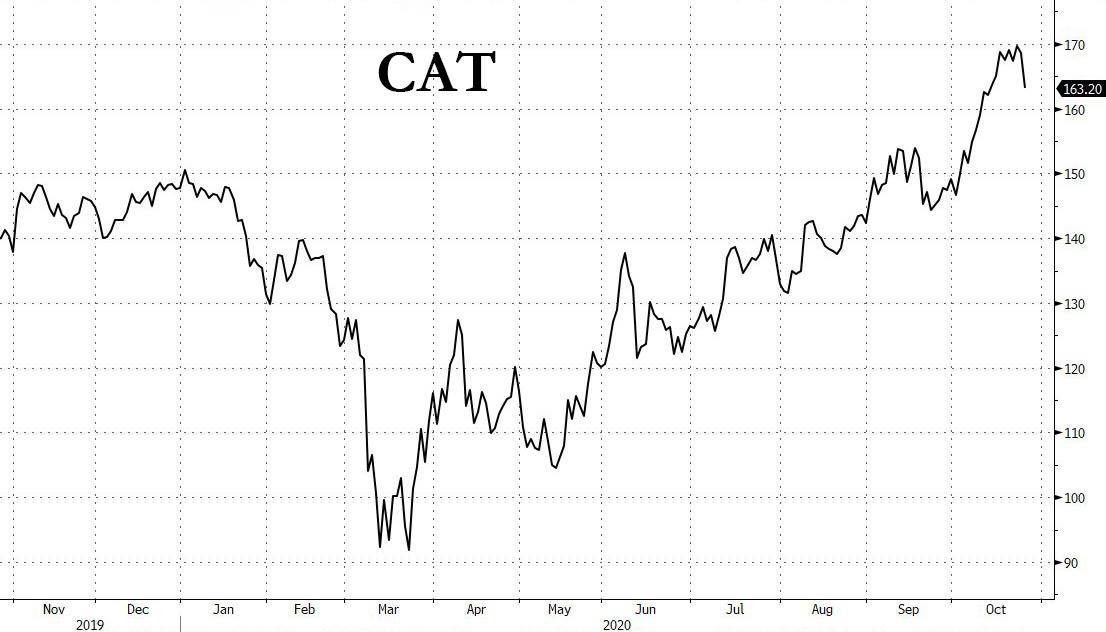

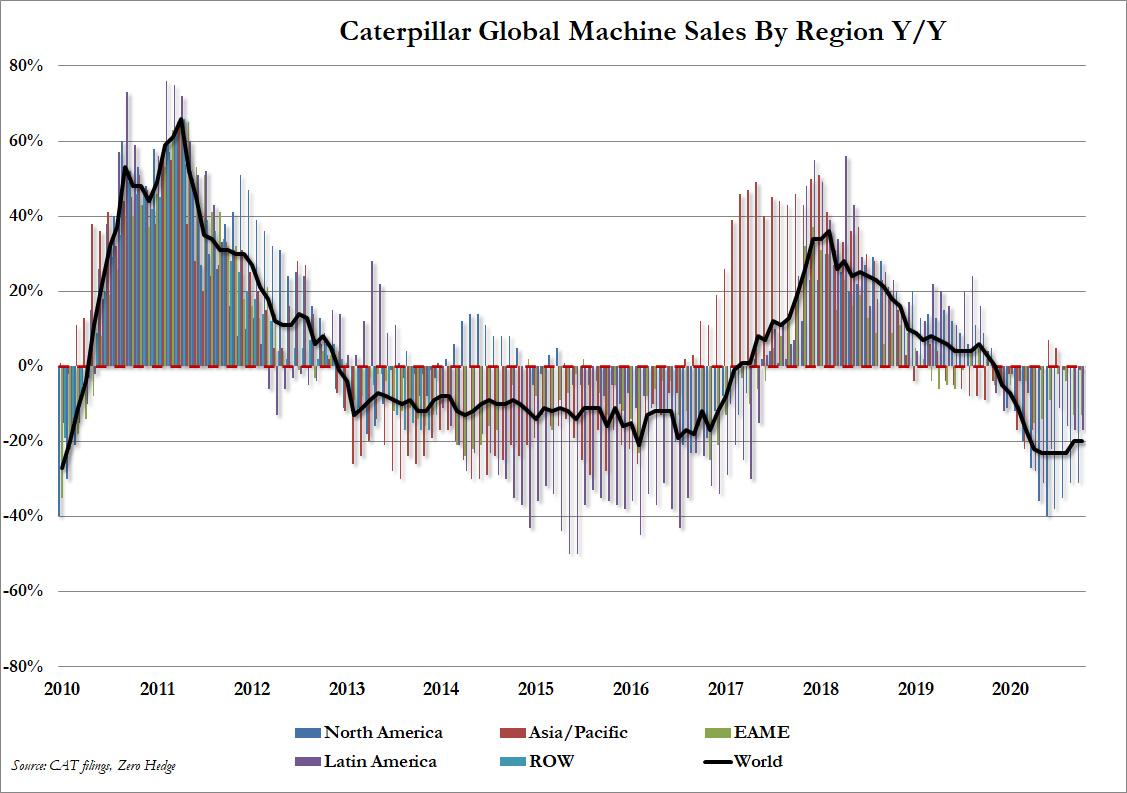

Caterpillar Slides On Lack Of Guidance Despite Revenue, EPS Beats Tyler Durden

Tue, 10/27/2020 – 07:45

Industrial giant Caterpillar dropped on on Tuesday after the company reported lower Q3 earnings as equipment sales fell across all three primary segments. The heavy equipment maker whose stock price had nearly doubled from the March lows on expectations of a V-shaped recovery and massive stimulus…

… reported adjusted Q3 profit of $1.34 per share, down 50% compared with $2.66 per share a year ago, but better than the $1.13 expected. The company also beat on revenue, reporting $9.88BN, down 23% Y/Y, but above the $9.19BN consensus estimate.

Despite the sharp decline in Y/Y results, the company said it sees “positive signs in certain industries and geographies” while failing to give reassurance that the worst of the hit from the coronavirus pandemic is behind the heavy-equipment maker, and refusing to provide guidance.

The Deerfield, Illinois-based company suspended its earnings forecast earlier this year because of uncertainty stemming from the coronavirus. The only hint of an outlook came in presentation slides, in which Caterpillar said it sees less of a decline in end-user demand in the fourth quarter than in the third, and that operating margins should improve. The company also said that dealers inventories are being run down more quickly, expected to decline by $2.5 billion for the full year, which should point to better sales going forward.

As Bloomberg notes, CAT “is typically seen as a bellwether for the economy, so analysts looking for hints as to how the recovery from the pandemic is progressing were likely disappointed.”

Some more details from Q3:

3Q financial revenue $653 million, estimate $709.0 million

3Q Financial Products segment operating income $127 million, -47% y/y, estimate $156.1 million

3Q Machinery, Energy & Transportation segment operating income $925 million, -51% y/y, estimate $845.2 million

Looking ahead:

Sees 4Q Less Decline in End-User Demand Than 3Q

Sees Dealers to Cut Inventory Levels ~$700M in 4Q, about $2.5B full year

Sees 4Q About $100M of Restructuring Expense

Separately, Caterpillar, which has been cutting costs to blunt the impact of still-sluggish orders in energy and mining, said machine sales fell 20% in October on a rolling three-month basis, unchanged on a Y/Y basis since July.

Despite the depressed sales, there was some silver lining in Caterpillar’s presentation slides, where the company’s order backlog increased by $500 million in the third quarter from the previous three months, after dropping $1.2 billion in the previous quarter.

As Bloomberg notes, the report comes as a resurgent virus hampers efforts to reopen economies, renewing concerns over the global demand outlook. Caterpillar was among the best-performing stocks the past few months on bets that the worst of the pandemic hit was behind the industrial bellwether.

“We’re encouraged by positive signs in certain industries and geographies,” Caterpillar Chief Executive Officer Jim Umpleby said in the a statement. “We’re executing our strategy and are ready to respond quickly to changing market conditions.”

Caterpillar CFO Bonfield said there’s strength in their sales to China overall, particularly in 10-ton or above excavators. These excavator sales in China are something investors pay close attention to, given that they act as a sort of proxy as to how much construction is going on in the country.

Yet despite the favorable spin, the lack of blowout earnings for the company which had priced in more than perfection and a V-shaped recovery, saw its stock drop premarket amid concerns that a global second (or third) wave of infections would cripple demand for heavy industrial equipment.

via ZeroHedge News https://ift.tt/3jz7siu Tyler Durden

Leaving Las Vegas? Sheldon Adelson Explores $6BN Sale Of Vegas Casinos Tyler Durden

Tue, 10/27/2020 – 06:57

In the latest sign that Las Vegas’ services and hospitality sector-focused mostly on the gambling industry – is experiencing long term economic scarring, Sheldon Adelson, known for decades as the biggest player in the gambling hub, is reportedly pulling out.

Sources told Bloomberg that Adelson’s Sands is shifting concentration to Asian gaming markets and is seeking an exit from U.S. casino operations. Sands has hired an advisor to prepare Venetian Resort Las Vegas, the Palazzo, and the Sands Expo Convention Center for a $6 billion sale.

Aside from gambling, Adelson is known as a major booster of the GOP, and recently agreed to shell out millions to support Trump’s bid for the White House after a troubling period of reticence.

The sale would position Sands’ as a pure gaming play in Asia, concentrating its casino portfolio primarily in Macau and Singapore. Bloomberg notes, “the U.S. was already a small and shrinking part of his business, accounting for less than 15% of revenue last year.”

“The growing insignificance of the U.S. market explains to you why Las Vegas Sands is looking to offload their U.S. properties,” said Ben Lee, a Macau-based managing partner at IGamiX. “It is 15% of revenue but 80% of regulatory pain and burden.”

Last week, Sands reported third-quarter earnings showing the company could be approaching break-even in Macau, the world’s biggest gambling market. Still, Vegas operations continued to drag as indoor capacity remained limited, and consumers stayed away from indoor spaces as daily U.S. virus cases marched higher.

Sands’ decision to sell Vegas operations at depressed valuations, smack dab in a virus pandemic amid collapsed fundamentals for the tourism and gaming industry only means one thing: “It’s only getting worse,” as we noted Monday evening on Twitter.

Selling a casino at a depressed valuation, in the middle of a pandemic amid terrible numbers means only one thing: it’s only getting worse https://t.co/1gvY8dzTwb

Las Vegas economic analyst Jeremy Aguero recently warned Vegas’ economic recovery could take 18 and 36 months. Just weeks ago, Encore at Wynn Las Vegas, the gaming hub’s largest casino, reduced operating hours as the “V-shaped” recovery narrative for the gambling hub has faltered into fall.

This all could mean that Adelson sees more downside for U.S. gambling markets as Asia recovers more swiftly. Adelson’s potential sale could be the catalyst that triggers a firesale across the Vegas Strip.

via ZeroHedge News https://ift.tt/2JaWByJ Tyler Durden

Xilinx Shares Soar As AMD Clinches Buyout In $35BN All-Stock Deal Tyler Durden

Tue, 10/27/2020 – 06:47

A week ago, when we first heard the news about late-stage talks between California-based chipmakers AMD and Xilinx, headlines touted a $30 billion megadeal, the latest in a massive wave of consolidation across the semiconductor industry that’s occuring amid unprecedented trade disruption caused by President Trump’s campaign against Huawei, a major customer for the world’s largest chipmakers, including American giants like Qualcomm.

Investors responded positively when the $30 billion pricetag first hit, but now that we have some more clarity on the deal, Bloomberg is reporting that AMD has agreed to a pricetag of $35 billion all in stock, with no debt added to the combined company’s balance sheet.

Xilinx investors will get 1.7234 AMD shares for each Xilinx stock they own. That values Xilinx at about $143 a share, 25% more than the closing price on Monday and 35% above the price before news of a possible deal was reported earlier in October. The company’s shares were up 11% in premarket trade.

via ZeroHedge News https://ift.tt/35HhEAF Tyler Durden

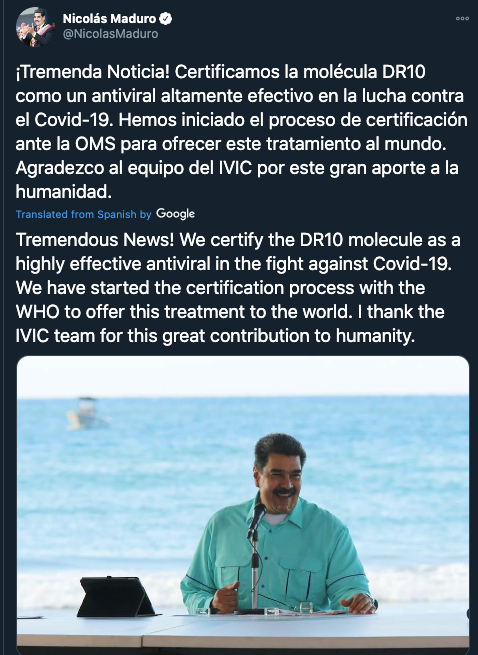

Multiple COVID-19 vaccine trials are in the final stages around the world. But in one unlikely place, that being the collapsed state of Venezuela, President Nicolas Maduro touted Sunday, in an appearance on state television, that his government scientists have developed a “highly effective antiviral” that kills the virus without any side effects.

Maduro tweeted: “Tremendous News! We certify the DR10 molecule as a highly effective antiviral in the fight against Covid-19.”

He continued: “We have started the World Health Organization (WHO) certification process to offer this treatment to the world. I thank the Venezuelan Institute for Scientific Research (IVIC) team for this great contribution to humanity.”

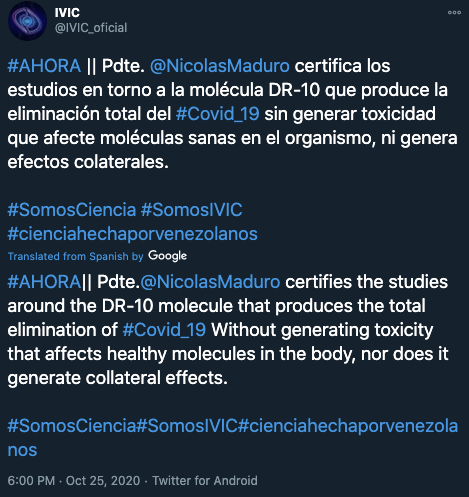

At the IVIC, scientists have been working around the clock to develop a cure for the virus. Maduro said that the vaccine’s active ingredient is a derivative of ursolic acid from a plant and will not harm humans.

Maduro said the vaccine would be transferred to the WHO for further evaluation and possible use worldwide.

“The molecule will be mass-produced and delivered worldwide for the cure of Covid-19,” according to Maduro.

So the question we ask Dr. Scott Gottlieb, who famously expressed skepticism about Russia’s COVID-19 vaccine in August: Is how he would feel about Maduro’s wonder vaccine?

via ZeroHedge News https://ift.tt/37JVkbX Tyler Durden