New York City can now fine residents up to $250,000 if they refer to someone as an “illegal alien” or threaten to call U.S. Immigration and Customs Enforcement (ICE) on someone “when motivated by discrimination.”

The NYC Commission on Human Rights announced on Sept. 26 that they had released a new legal enforcement guideline (pdf) that clarifies discrimination based on someone’s immigration status and national origin is illegal in any public accommodations, employment, and housing. According to the guidance, public accommodations include “businesses such as restaurants, fitness clubs, stores, and nightclubs, and other public spaces, like parks, libraries, healthcare providers, and cultural institutions.”

Any violations of the law could be fined up to $250,000.

BREAKING:

New York City has made it illegal to threaten to call ICE based on a discriminatory motive or to tell someone “go back to your country.” Hate has no place here. pic.twitter.com/8PaIozjQty

“This new legal enforcement guidance will help ensure that no New Yorker is discriminated against based on their immigration status or national origin,” said Deputy Mayor Phil Thompson in a press release on Sept. 26.

Under the guidance, phrases such as “illegal alien,” and “go back to your country” used with the intent to “demean, humiliate, or harass” a person is illegal under the law. Moreover, it states that harassing or discriminating a person based on their use of another language or their limited English proficiency is also against the law.

In its 29-page directive, the commission lists several examples as to what would constitute a violation of the law, which includes harassing people based on their immigration status or discriminating someone based on their accent.

“An immigrant shop owner asks a couple of customers to leave his store after they start breaking merchandise. The customers tell the owner he should ‘go back to where he came from,’ and exit the shop. The next morning, the owner discovers that the windows have been smashed and the walls spray-painted with anti-immigrant obscenities,” one example said.

“An employer interviews a highly qualified applicant for a new position. Upon hearing the applicant’s accent, the employer decides not to hire them, assuming that their accent indicates that the applicant is not very smart,” another example states.

This comes after Mayor Bill de Blasio expressed opposition to a nationwide ICE enforcement operation targeting illegal immigrants who have received final deportation orders issued by immigration judges.

Carmelyn Malalis, the agency’s commissioner, told the New York Post that the new guidelines were partly made in response to a crackdown on illegal immigration by the federal government.

“In the face of increasingly hostile national rhetoric, we will do everything in our power to make sure our treasured immigrant communities are able to live with dignity and respect, free of harassment and bias,” Malalis told the newspaper.

Federal immigration officials have reported record highs in the apprehension of illegal immigrants at the border to Congress in the past months, saying that the numbers have overwhelmed border patrol facilities and resources. In May, border patrol agents apprehended or deemed inadmissible over 144,000 people crossing from Mexico—which were record-high numbers. The number of people apprehended or deemed inadmissible has been steadily falling after President Donald Trump pushed Mexico, through the threat of tariffs, to put more focus on the humanitarian crisis.

According to the city, 37 percent of the city’s population was born outside the United States, meanwhile, 16 percent of the population are noncitizens. New York City is also a sanctuary city, which refers to a city that limits its cooperation with ICE to enforce immigration law.

After Trump Accused Of Cover-Up, Susan Rice Admits Obama Put Transcripts On Top Secret Server Too

After President Trump was accused of a cover-up for moving details about his July 25 phone call with Ukrainian President Volodymyr Zelensky in a separate, highly secured computer system, former Obama national security adviser Susan Rice admitted that Obama did the same thing.

The difference? Rice says that Trump’s conversation didn’t meet the threshold to justify that level of classification, according to The Federalist.

“We never moved them over unless they were legitimately, in the contents classified,” Rice said at the Texas Tribune Festival when asked how often the Obama administration engaged in this practice – without explaining the methodology used to determine what qualified.

.@AmbassadorRice: “Normally there is a full, verbatim transcript” of calls like Trump’s w/ the Ukraine president.

Says he tried to “bury” it on a more secure server, but acknowledges the Obama Admin. sometimes did the same. pic.twitter.com/B6zZNbZsTG

Rice’s revelation may soften arguments of a cover-up by the Trump administration to “lock down” the conversation.

The revelation from Rice comes amid media reports and comments from political leaders that have painted the use of this top secret server as proof that Trump was trying to cover up the contents of his conversation with the Ukrainian leader, a full transcript of which the administration has now released to the public.

While Rice admitted that the Obama administration also used this server to protect sensitive presidential phone calls, she left open the question of whether the Trump administration used the server in this particular case to save the president from damaging, perhaps even impeachable, comments he made to Zelensky regarding investigations into political rival Joe Biden. –The Federalist

What’s more, The Federalist notes that “reporting from ABC News shows that this practice of securing presidential phone transcripts has been in use in the White House since early 2017, after sensitive conversations with foreign leaders were leaked to the press.”

In an August 12 letter, a CIA ‘whistleblower’ claimed that President Trump had inappropriately pressured Zelensky to investigate Joe and Hunter Biden, after the elder Biden bragged about forcing Ukraine to fire its lead prosector ‘or else’ $1 billion in US loan guarantees would be pulled. Moreover, Democrats have also pointed to the Trump administration pausing nearly $400 million in US military aid as a bargaining chip.

Both Trump and Zelensky have denied that there was any pressure, which was made clear when Trump released a transcript of the call in question. In addition, Zelensky had no clue the $400 million was being withheld until a month after the call, according to the New York Times’ Kenneth Vogel in a Wednesday tweet.

The Ukrainians weren’t made aware that the assistance was being delayed/reviewed until more than one month after the call. https://t.co/qDJ3FT261a

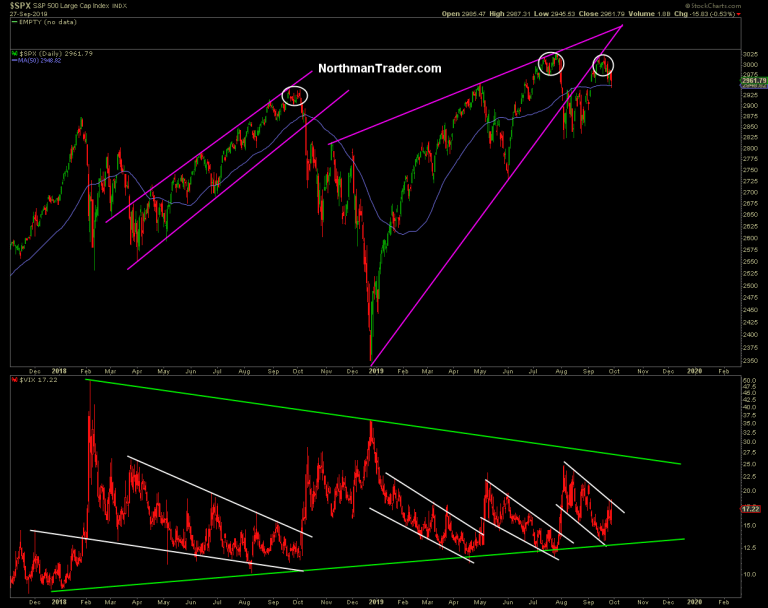

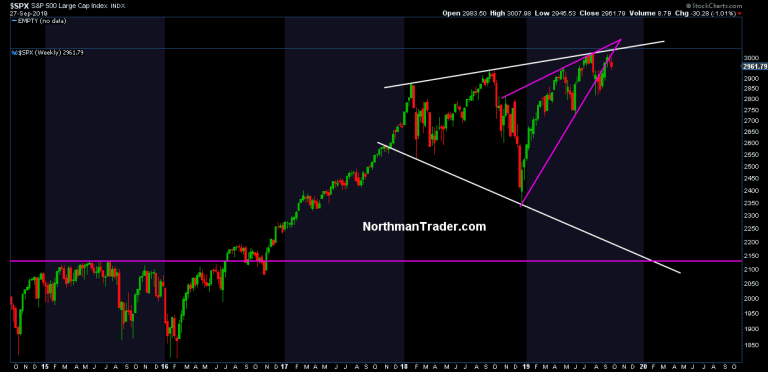

Where is it? The great bull market? Where is the imminent great bear market? Fact is markets are in engaged in a big game of stalemate. Bulls keep buying every dip, but all rallies are sold and are selling opportunities. Nobody’s making any progress whatsoever chasing from headline to headline that are associated with the various daily moves but accomplish previously little in the big scheme of things.

That said one can’t shake the sense that this stalemate is soon coming to an end and October may well be the month that provides clarity.

Let’s look at the facts and risk factors.

Fun facts:

On October 2, 2018 $DJIA made an all time high with a print of 26824. This past Friday, almost 1 year later, $DJIA closed at 26820. Virtually the same price.

On September 21, 2018 $SPX printed an all time high of 2940.91, last Friday’s intra-day low was 2945.53, both data points reflective of the nowhere state of affairs over the past year. That is on the surface. Underneath plenty of things have changed.

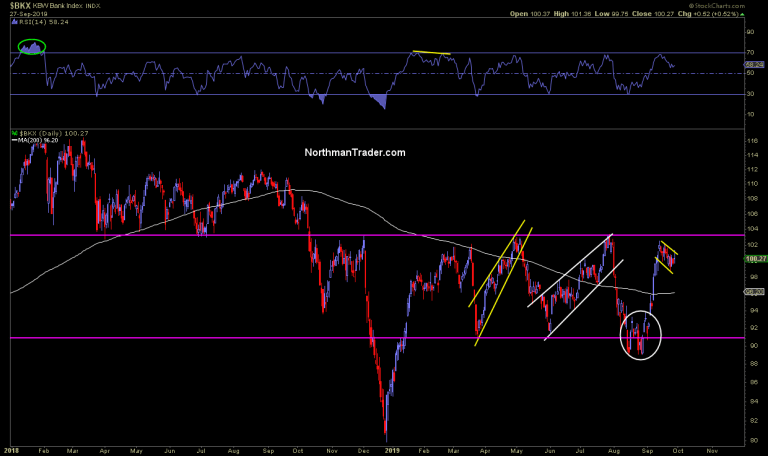

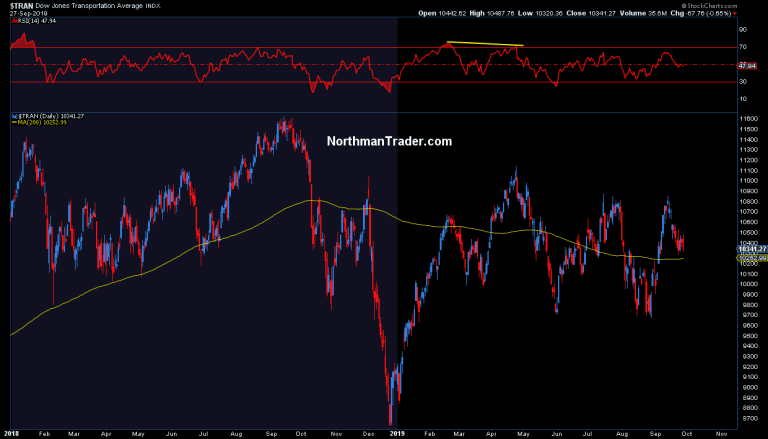

$DJIA, $SPX and $NDX are near the same levels, other indices such as the banking sector, small caps and transports are 9%-11% below last year’s levels:

These lagging indices continue to show no progress and continue to chop in the same range they’ve been in for months.

For $BKX the positive that may be said is that it may be setting up for a bull flag here that may push it across resistance:

Small caps made another lower high and are currently trying to defend support at the 200MA while its underlying volatility index continues to show a well defined bull flag that shows risk of a coming volatility breakout:

Transports? Stalemate and chop:

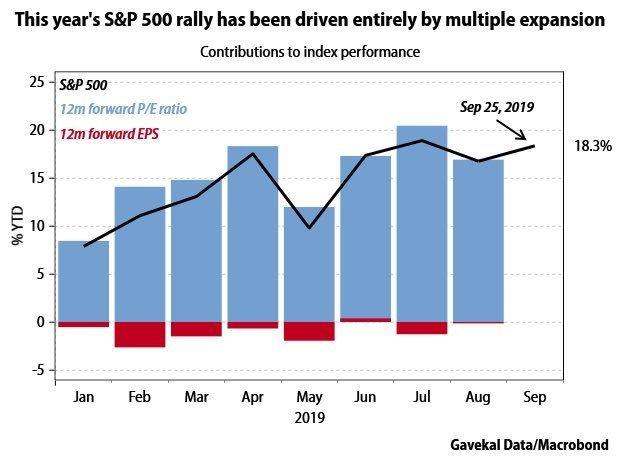

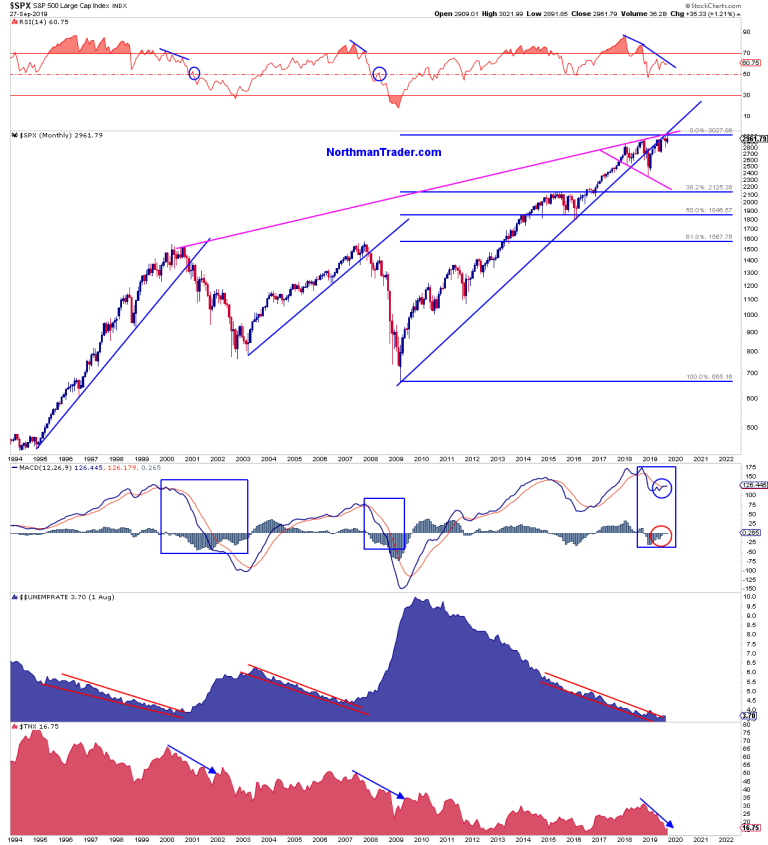

The great re-inflation trade in the main indices of course driven by multiple expansion pure:

This multiple expansion greatly aided by a renewed intervention cycle of central banks desperate to keep extending an aging business cycle, but in doing so are re-inflating asset prices further above the underlying size of the economy reaching new record levels of household net worth versus GDP:

Money for free, value out of thin air.

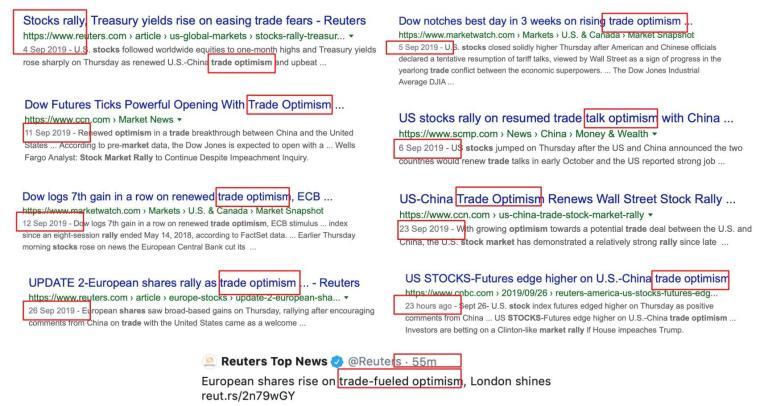

The other driver: Trade optimism headlines, a faithful source of market rallies in 2019, went into overdrive in September:

And as such expectations are high for the October 10 trade meetings set between the US and China. I’ve been saying for months a trade deal will be key for markets this year. The longer the trade war drags on the worse the continued uncertainty will dampen investment and consumer sentiment and this is precisely what we’re seeing with global PMIs not showing any real improvements and consumer uncertainty approaching levels that risk that consumer spending may get negatively affected.

Whether the recent positive signals on trade were partially fueled by the Chinese’s desire to have a positive social mood for the upcoming 70 year celebration on October 1st remains to be seen. Like the rest of the world they are likely to closely watch the upcoming impeachment inquiry in the US. The US election is a mere 14 months away and the Chinese will want to assess the unfolding developments in their strategic assessment on how to proceed in their trade negotiation strategy.

Why accept a bad deal if things can change rapidly?

Can things change rapidly? Conventional wisdom currently suggests that nothing much will change as Donald Trump’s continued support in the Senate is presumed and even is House Democrats were to impact him a Clinton like outcome would support a continued market rally into 2020.

The alternative being the unexpected Berlin Wall effect. Assumed to be the status quo for years sentiment suddenly changed out of the blue and the Berlin Wall was no more. A similar fate that Richard Nixon experienced when impeachment was initially not viewed as popular either by voters nor by Republicans, but then the tapes came out and 3 days later Nixon resigned knowing he lost support by Republicans.

None of us can know how events will unfold, but as we are rapidly approaching the 2020 elections history teaches that strong support can dwindle rapidly when new facts emerge hence they next few weeks may well be critical in determining whether the status quo remains or whether a new unexpected reality emerges.

I recognize readers may have strong feelings and views on the subject one way or the other, what I am suggesting is that everyone stay open minded as unfolding events may well impact trade negotiations and thereby markets.

In last week’s bear case I made the argument that downside may well emerge and that a generally assume market breakout to new highs was perhaps not sustainable or perhaps not even in the cards.

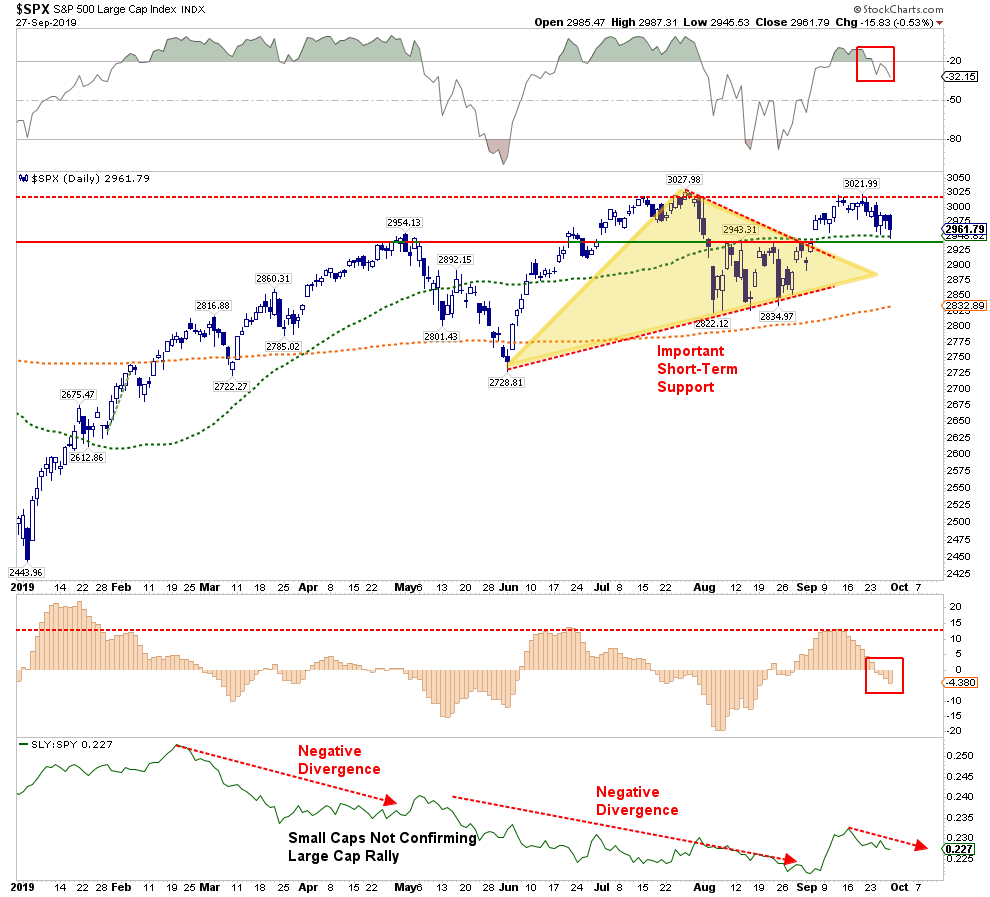

As it were markets took the route south and again rejected any attempts above $SPX 3,000:

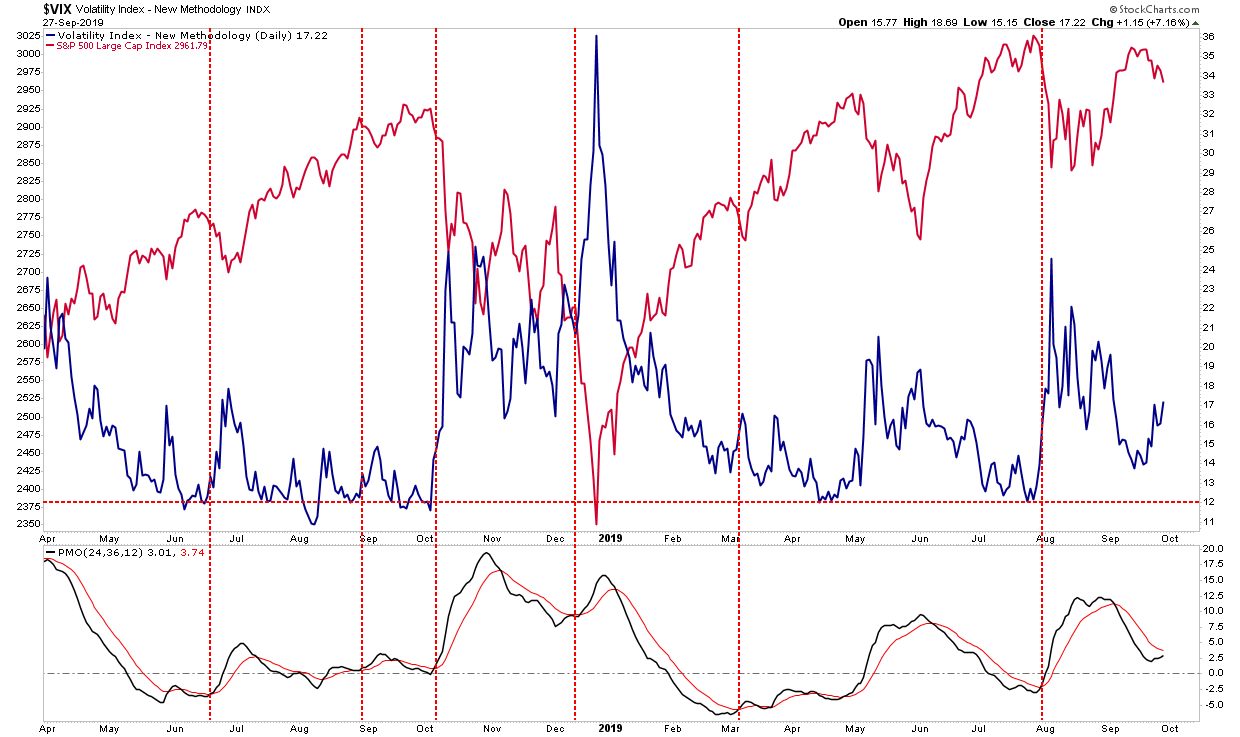

While $SPX saved 50MA support on Friday markets are now also confronted with the prospect of a potential double top on $SPX while $VIX continues to build its bull flag pattern (see also $VIX getting jiggy). Friday’s rejection at the trend line again confirming the relevance of the structure.

In Replay in early September I suggested that markets appear to be following a similar script to last September and for all the noise in headlines one can’t help but be impressed how similar in structure the price action keeps unfolding compared to the same month last year:

An early month dip followed by a rally into September Opex, then a dip following Opex. If the script continues it suggests another rally into early October. In 2018 markets peaked in early October followed by a 20% correction into December. It seems incredulous to think that markets will follow a similar path into Q4 of 2020, rather, with continued central bank support, one may expect a buyable dip scenario followed by a year end rally before a larger bear market is to unfold into 2020.

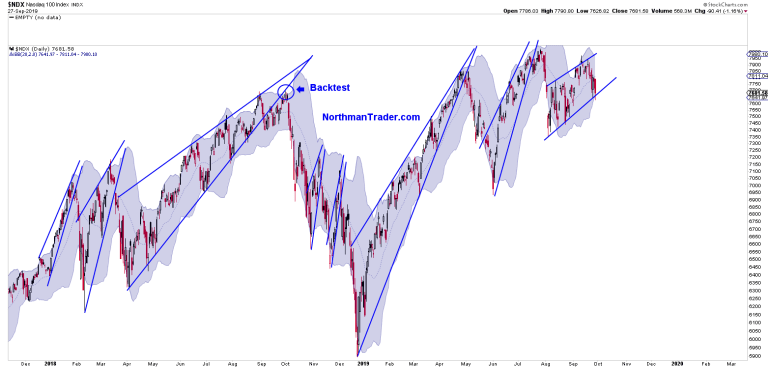

But note the road of reflation in asset prices to new highs in 2019 has come on a much weaker participation even in the strong indices and negative divergences once again permeate the landscape.

In $NDX new highs versus new lows have been much weaker compared to 2018:

Indeed $NDX may actually be engaged in a bear flag pattern which again serves as tenuous support on Friday:

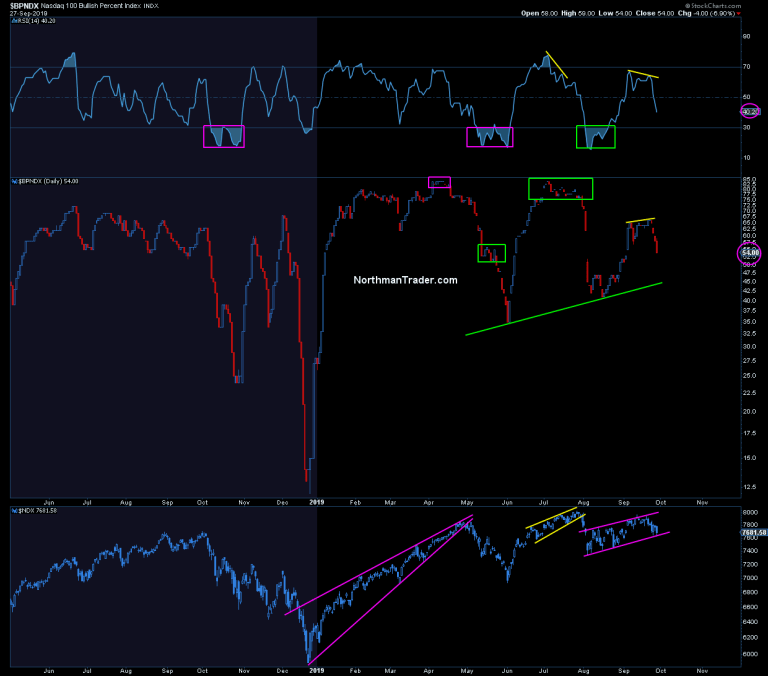

$BPNDX showed a rollover in September:

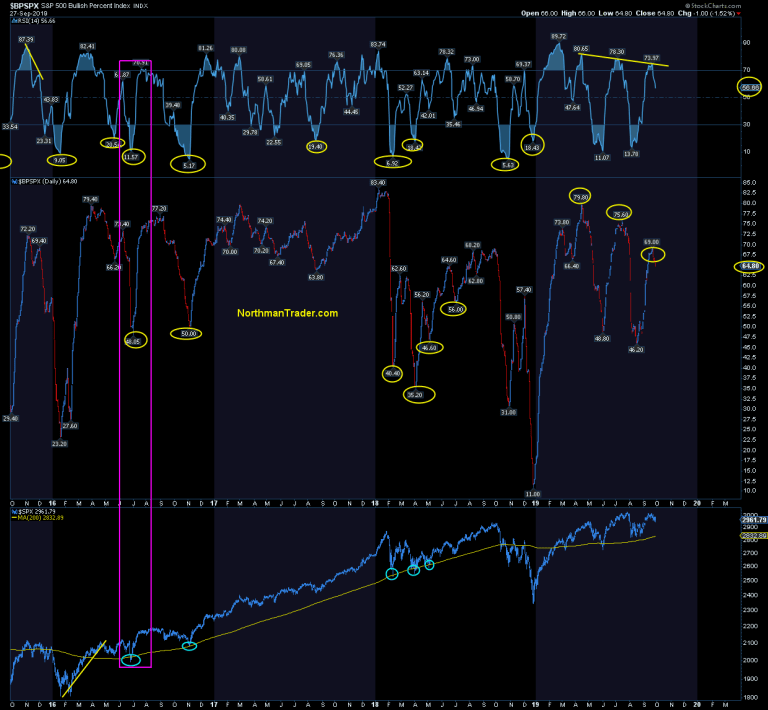

While $BPSPX printed lower highs all summer:

Where’s the bull market in that?

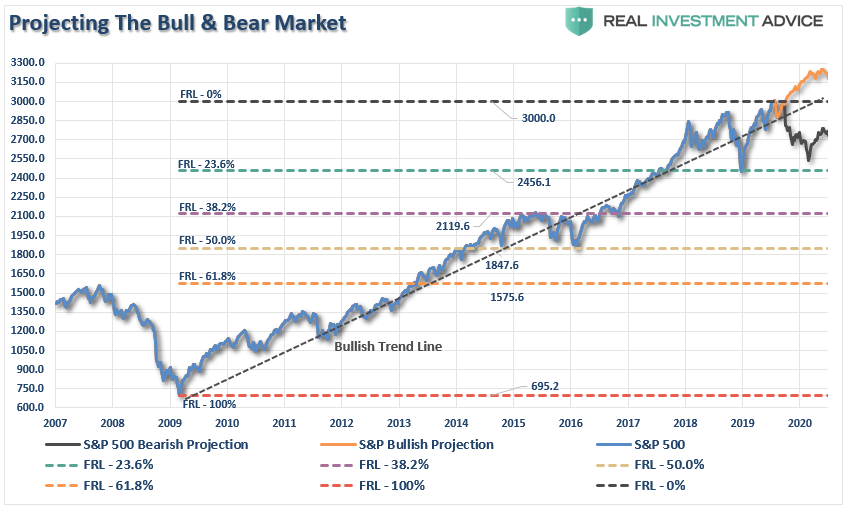

And so the main facts I outlined on CNBC Fast Money at the end of August remain: The larger megaphone pattern has not been invalidated and the 2019 trend remains unprepared:

And hence markets remain in a state of stalemate. Bulls continue to fail to making a sustained breakout and bears have not been able to bring about a breakdown, but keeping lagging indices at bay.

October may likely be a decisive month on this front. Aside from trade talks earnings reports will bring about some clarity as to the impact of continued of uncertainty not only on earnings but also on forward outlooks. The big question: Will we get a sense if compressing operating margins will filter into the unemployment picture the missing link to the bear case?

The larger market structural view suggests we’ve arrived at a key decision node:

Market strength continues to be sold and shows negative divergences, but dips keep being bought. Volatility structures continue to show higher lows and patterns suggestive of a coming volatility spike. I maintain that a market driven by pure multiple expansion on headlines and central bank actions alone can ill afford disappointments. Market indices trading near all time highs chasing every trade optimism headline appear to have not priced in any continued failure in trade talks. An interim deal or news of progress may well be a source of future rallies and even new highs, the question is one of sustainability.

Political uncertainty has suddenly become front and center and its impact on consumer confidence and spending has to be carefully gauged in the weeks ahead.

Having failed to make new highs in September market now face the technical prospect of a potential double top. The message is clear: Bulls absolutely need sustained new highs in October or Q4 may have to contend with the ghosts of Q4 2018. This stalemate is coming to and end one way or the other.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

Clinton Emailers Rattled After State Department Fires Off ‘Culpability Letters’ For Homebrew Server Messages

The State Department’s Bureau of Diplomatic Security has finally finished sifting through millions of emails from Hillary Clinton’s controversial ‘basement server’ – many of which were classified, and/or blind-copied to a Gmail address bearing the name of a Chinese company according to intelligence community inspector general (ICIG) Frank Rucker.

While State Department investigators began contacting former officials around 18 months ago, the probe actually began under President Obama. In recent weeks, the State Department has contacted approximately 130 officials whose emails which went through Clinton’s special server have been retroactively classified and may now pose potential security violations, according to the Washington Post.

“This has nothing to do with who is in the White House,” said a senior State Department official. “This is about the time it took to go through millions of emails, which is about 3½ years.“

The flood of letters which began in August read “You have been identified as possibly bearing some culpability” regarding “security incidents,” according to the report.

The list of State officials being questioned includes prominent ambassadors and assistant secretaries of state responsible for U.S. policy in the Middle East, Europe and Central Asia. But it also includes dozens of current and former career bureaucrats who served as conduits for outside officials trying to get important messages to Clinton.

In most cases the bureaucrats and political appointees didn’t send the emails directly to Clinton, but passed them to William Burns, who served as deputy secretary of state, or Jake Sullivan, the former director of policy planning at the State Department. Burns and Sullivan then forwarded the messages to Clinton’s private email. –WaPo

President Trump’s opponents will likely take WaPo‘s editorialized cue and accuse the president of targeting political adversaries – like the Obama administration did with the IRS. Note how WaPo is lying in order to bolster the new narrative behind the Clinton email revival – claiming that Trump “used multiple levers of his office to pressure the leader of Ukraine,” when the leader of Ukraine announced on Wednesday “Nobody pushed me” to investigate former Vice President Joe Biden – nor did he know about $400 million in US military aid Trump paused prior to a July 25 phone call.

To many of those under scrutiny, including some of the Democratic Party’s top foreign policy experts, the recent flurry of activity surrounding the Clinton email case represents a new front on which the Trump administration could be accused of employing the powers of the executive branch against perceived political adversaries.

The existence of the probe follows revelations that the president used multiple levers of his office to pressure the leader of Ukraine to pursue investigations that Trump hoped would produce damaging information about Democrats, including potential presidential rival Joe Biden. –WaPo

So while the State Department said they are bound by law to adjudicate any violations, former Obama administration officials say the probe is a ‘remarkably aggressive crackdown.’

“It is such an obscene abuse of power and time involving so many people for so many years,” said one former US official of the inquiry, adding “This has just sucked up people’s lives for years and years.”

WaPo lies again in suggesting that President Trump has no grounds to pursue Clinton associates as he has “improperly disclosed classified information to foreign officials.” Except that the president has an inherent constitutional authority to declassify information at will, meaning the rules of disclosure of classified information don’t apply to him.

Back to the Clinton email saga, WaPo reports that in many cases, “the incidents appear to center on the sending of information attributed to foreign officials, including summaries of phone conversations with foreign diplomats — a routine occurrence among State Department employees.”

There is no indication in any of the materials reviewed by The Post that the emails under scrutiny contained sensitive information about classified U.S. initiatives or programs. In one case, a former official was asked to explain dozens of messages dating back to 2009 that contained messages that foreign officials wanted relayed rapidly to Washington at a time when U.S. Foreign Service officers were equipped with BlackBerrys and other devices that were not capable of sending classified transmissions. The messages came in through “regular email” and then were forwarded through official — though unclassified — State Department channels. –WaPo

And while The Post may have no indication that any of the emails contained sensitive information about classified US initiatives or programs, they don’t disclose how many of the underlying emails they reviewed, or who they came from.

According to the report, many of those contacted in the probe have been found “not culpable” – with many letters reading that investigators “determined that the [security] incident is valid,” but that the person did not “bear any individual culpability.”

Friday morning stocks rose as optimism over “trade” seemed to “trump” the ongoing antics in Washington as Democrats are once again trying to find a “smoking gun” to impeach the “Trumpster.” Then, the market tanked, as Bloomberg reported the White House is weighing limits on U.S. portfolio flows into China – which promptly tanked stocks.

“The discussions are occurring as Washington and Beijing negotiate a potential truce in their trade war that’s rattled the world’s two biggest economies and investors for more than a year. They also come as China is removing limits on foreign investment in its financial markets. A U.S. crackdown on capital flows would therefore expose a new pressure point in the economic dispute and cause disruption well beyond the hundreds of billions in tariffs the two sides have levied against each other.

Among the options the Trump administration is considering: delisting Chinese companies from U.S. stock exchanges and limiting Americans’ exposure to the Chinese market through government pension funds. Exact mechanisms for how to do so have not yet been worked out and any plan is subject to approval by President Donald Trump, who has given the green light to the discussion, according to one person close to the deliberations.”

With the Fed out of the picture for now, the market has become almost entirely dependent on “Trump tweets” for direction.

As noted last week, despite the short-term disappointment, the bulls continue to remain in charge currently, as markets cling near all-time highs. As we pointed out last week:

“The risk/reward does not favor the bulls short term. The market is back to very overbought conditions; the upside to the top of the bullish trend channel is about 1.9%. The downside risk is about 5.5%.”

The chart below is updated through Friday’s close. The good news is the overbought condition has been reduced while the market held support at the 50-dma. This potentially sets the market up for a rally next week, providing we get a “tweet” over the weekend confirming a “trade deal” is in progress.

However, on an intermediate-term basis, a “sell signal” has been registered, which suggests there is downward pressure on stocks over the next month. The July and September tops are nearly identical suggesting a “double top” is in progress. This also increases the difficulty of the markets moving higher in the short-term. The good news is a break above resistance will support a move to 3300 as discussed previously.

Currently, there is support at the 50-dma, which coincides with the January 2018 top, but a break of that level will put the 200-dma into focus. The negative divergence between large and small-cap stocks continues after a brief reversion week before last. Whatever that was, seems to be over for now.

The volatility index (VIX) has also turned higher and is very close to triggering a “buy” signal. Given the non-corollary nature of the index versus the S&P 500, it suggests that further downside risk could be in the offing if a signal is triggered. Spikes in volatility, and declines in stock prices, tend to happen very quickly, so it is better to anticipate the event by adding hedges, raising cash (ie take profits), and rebalancing risks accordingly.

In our portfolios, last week, raised a bit of cash, and continue to remain hedged currently. While the bullish trend of the market keeps us allocated toward equity risk currently, we are doing so with defensive positioning. We also slightly increased our intermediate-term bond holdings and Gold. Cash remains a slight overweight in model allocations and equities slightly underweight..

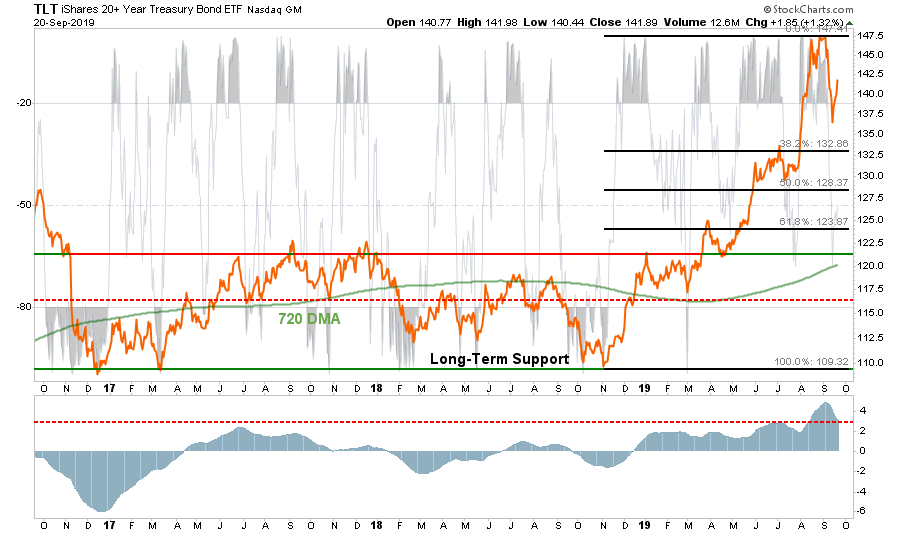

Like GLD, Bond prices finally cracked and have reversed a good chunk of the EXTREME overbought condition.As with GLD, we swapped bond positions this past week selling short-term bonds and swapping into longer duration Treasuries. We are very close to further increasing our exposure to bonds as well.

Trade Deal In Time For The Election

As noted above, on Friday, the Trump administration is putting a “review on investment limits” for China. This would potentially include:

Delisting Chinese companies from U.S. stock exchanges, and;

Limiting Americans’ exposure to the Chinese market through government pension funds.

This is a direct hit at China which has made huge strides in economic ambitions and technological advances on the back of American financing. This chart below, courtesy of Zerohedge, shows the market capitalization of Chinese companies trading on U.S. exchanges:

As noted above, this is all “talk” by the administration. While Trump has green lighted the discussion, there is reportedly no timeline for any action which suggests this is nothing more than “posturing” ahead of trade talks. While the markets didn’t like the news on Friday, this plays well into the strategy we believe Trump is setting up for the mid-October meeting with China to “negotiate a trade deal.”

This additional “threat” is being brought to the bargaining table in October, and is one Trump can easily back off of in exchange for greater market access for American companies in China. (This is something Trump has previously asked for, and China has already agreed to provide.)

However, while the Democrats are busy trying to impeach President Trump over the latest White House scandal, Trump has continued to try and keep the markets happy by promising a “trade deal is coming,” just as he told the White House press pool on Wednesday:

“They want to make a deal very badly… It could happen sooner than you think.” – Reuters

I remain unconvinced as China responded immediately afterward.

“China’s top diplomat hit back at U.S. criticism of its trade and development model in a speech on Tuesday after Trump spoke at the United Nations. Wang Yi, China’s foreign minister and state councilor, said Beijing would not bow to threats, including on trade, though he said he hoped the high-level trade talks next month would produce positive results.” – Reuters

If this all sounds rather familiar, it should, because it is the same thing they said a month ago.

“Beijing’s latest ‘gesture’ has increased the prospects for a narrow trade deal with the US. But it’s a small deal. It means that there would be no escalation of tariffs as China has agreed to make more purchases.It could provide a certain level of comfort to US farmers and give Trump something to brag about.” – Hua Changchun, economist at Guotai Junan Securities, PRC

China is indeed making “small concessions” for things they need as a country. As we noted two weeks ago:

“China, smartly, is using the opportunity to buy soy and pork products (which they desperately need due to a virus which wiped out 30% of their pig population) to restock before the next meeting.

This is a not so insignificant point.

China is out for “China’s” best interest and will not acquiesce to any deal which derails their long-term plans. In the short-term, they may “play the game” to get what they need as a country, but in the long-run, they will protect their own interests.”

However, don’t mistake China’s move as “caving” into Trump. Such is hardly the case.

“China will allow the import of soymeal livestock feed from Argentina for the first time under a deal announced by Buenos Aires on Tuesday, an agreement that will link the world’s top exporter of the feed with the top global consumer.” – Reuters

The pressure is on the Trump Administration to conclude a “deal,” not China. Trump needs a deal done before the 2020 election cycle; AND he needs the markets and economy to be strong. If the markets and economy weaken because of tariffs, which are a tax on domestic consumers and corporate profits, as they did in 2018, the risk of electoral losses rise.

Trump Looking For A Fast Exit

This is an important point.

China knows that Trump needs a way out of the “trade war” he started, but that he needs a something that he can “boast” as a victory to a largely economically ignorant voter base. Here is how a “trade deal” could get done.

Understanding that China has already agreed to 80% of demands for a trade deal, such as buying U.S. goods, opening markets to U.S. investors, and making policy improvements in certain areas, Trump could conclude that “deal” at the October meeting.

It is only the final portion of Washington’s demands which have stalled negotiations so far:

Cutting the share of the state in the overall economy from 38% to 20%,

Implementing an enforcement check mechanism; and,

Technology transfer protections

These are the “big ticket” items that were the bulk of the reason Trump launched the “trade war” to begin with. Unfortunately, for China, these items are seen as an infringement on its sovereignty, and requires a complete abandonment the “Made in China 2025” industrial policy program.

However, Trump can set aside the last 20%, drop tariffs, and keep market access open, in exchange for China signing off on the 80% of the deal they already agreed to.

Which is precisely what Trump’s comments recently alluded to:

“Not surprisingly, as Trump said on Thursday, while he prefers a broad deal, he left open the possibility of a more limited deal to start.” – Reuters

That is code for: “Let’s get a deal on the easy stuff, call it a win, and go home.”

This is the strategy we suggested was most likely two weeks ago:

“For Trump, he can spin a limited deal as a ‘win’ saying ‘China is caving to his tariffs’ and that he ‘will continue working to get the rest of the deal done.’ He will then quietly move on to another fight, which is the upcoming election, and never mention China again. His base will quickly forget the ‘trade war’ ever existed.

Kind of like that ‘Denuclearization deal’ with North Korea.”

Would A “Deal” Change Anything

Assuming we are correct, and Trump does indeed “cave” into China in mid-October to get a “small deal” done, what does this mean for the market.

The most obvious impact, assuming all “tariffs” are removed, would be a psychological “pop” to the markets which, given that markets are already hovering near all-time highs, would suggest a rally into the end of the year.

This is not the first time we presented analysis for a “bull run” to 3300.To wit:

“The Bull Case For 3300

Momentum

Stock Buybacks

Fed Rate Cuts

Stoppage of QT

Trade Deal”

As I noted then, price momentum has been in control of the markets over the last several months. Given that “an object in motion, tends to stay in motion,” momentum is a hard thing to stop without a bigger event triggering a reversal in investor attitudes.

When I wrote the article previously, the Fed had not cur rates yet. Since that writing, they have cut rates twice, increased their balance sheet, and are hinting at the return of more “QE” if needed by letting the “balance sheet grow organically.”

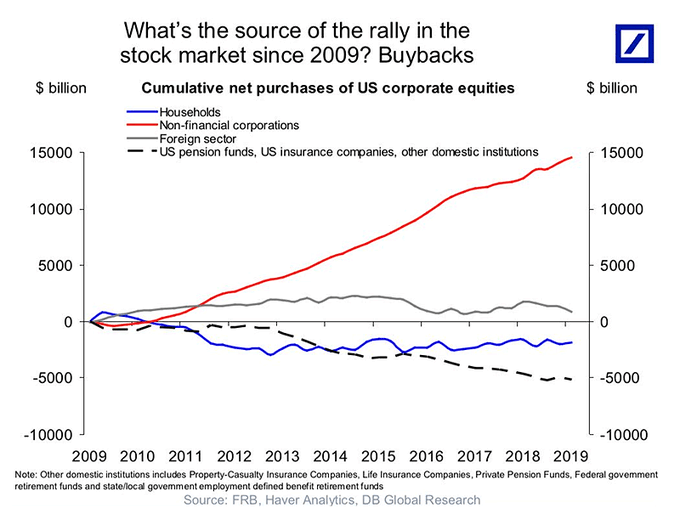

Thursday, I wrote in detail about the continuation of corporate share repurchases and the impact on the financial markets. Companies remain almost the sole source of net equity purchases.

“Between the Federal Reserve injecting a massive amount of liquidity into the financial markets, and corporations buying back their own shares, there have been effectively no other real buyers in the market.”

The only thing left is the “Trade Deal.”

A deal would alleviate some concern on corporate profitability, and as J.P. Morgan’s chief equity strategist Dubravko Lakos-Bujas previously told MarketWatch:

“If you have a trade deal, and if the trade deal coincides with one or two rate cuts from the Fed, we see an upside scenario of 3,200-3,300.”

Yep, the same number we came up with.

The Bear Is Still Coming

Just remember, bull-runs are a one-way trip.

A trade-deal only undoes the immediate negative impacts to corporate profits and the economy. However, higher interest rates from the Fed and tariffs were in place long enough to negatively impact growth, consumption, and confidence.

Furthermore, given the markets never reverted to any meaningful degree, higher prices combined with weaker earnings growth, has left the markets very overvalued, extended, and overbought from a historical perspective.

Lastly, investors are all-in already, so there is little “buying power” left to substantially drive markets higher outside of a short-term short-covering rally from any “trade deal.”

“Cash is low, meaning households are fairly fully invested.” – Ned Davis

In other words, the “pent up” demand for equities is no longer available to the magnitude that existed following the financial crisis, which supported the 300% rise in asset prices.

Most likely, if a deal is done, whatever rally comes will likely be the last leg of the bull market.

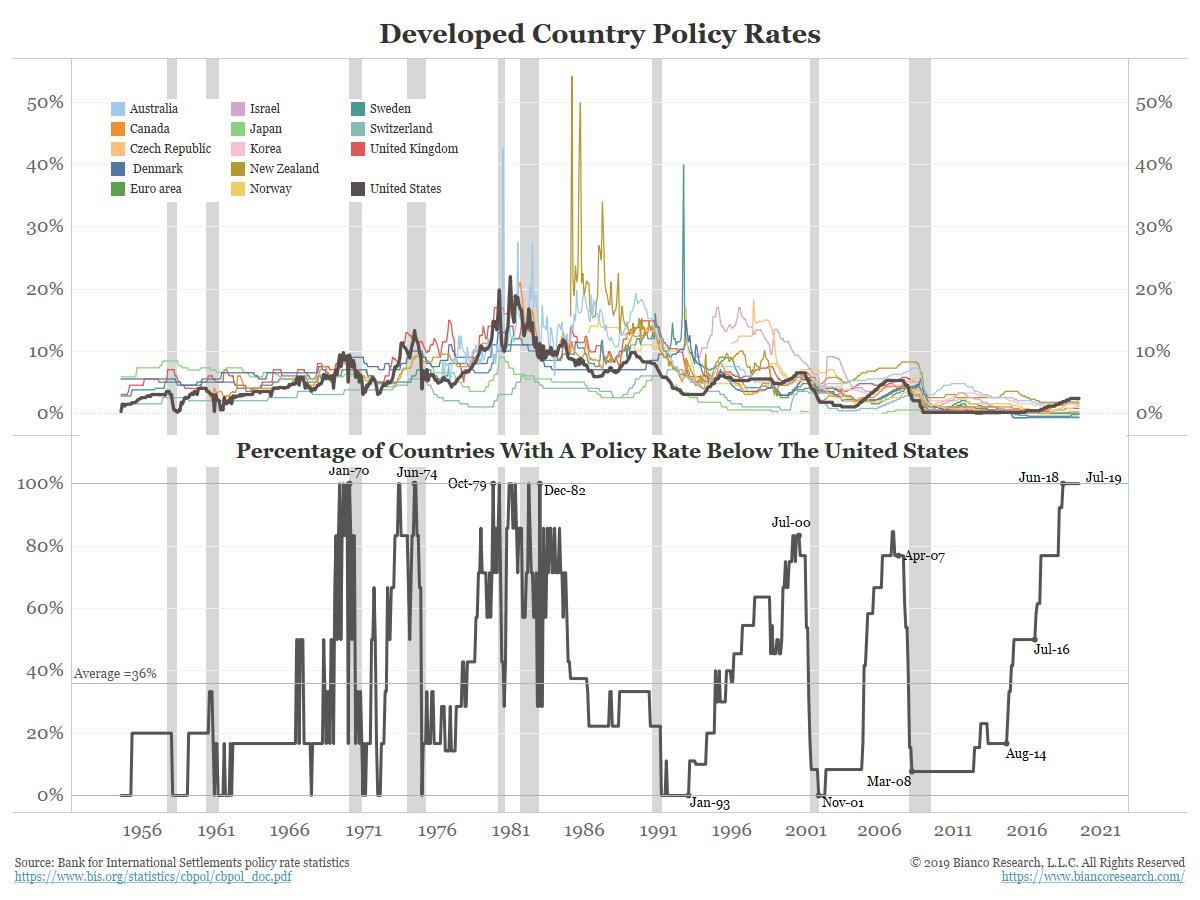

The global economy is slowing, negative rates are proliferating within sovereign debt, and there is not an inconsequential chance of a credit-related event in the months ahead. Jim Bianco showed a long-term perspective that when global rates are lower than U.S. rates, a recession has always occurred.

It is easy to get wrapped up in the bullish narrative, it is worth remembering that making up a loss of capital is not actually an investment strategy.

While the media, and bulk of the financial commentary continue to suggest “riding the bull,” they are not going to tell you when to get off. Moreover, when the ride does come to an end, the media will ask first “why no one saw it coming?”

Then they will ask “why YOU did not see it coming when it so obvious.”

In the end, being right, or wrong, does not affect the media. They don’t manage your money. Nor are they held responsible for consistently poor advice. However, being right, or wrong, has a very big impact on you.

Let me repeat:

“While our portfolios remain long currently, we do so with hedges and stops in place, a thorough methodology of analysis, and a strict investment discipline we follow to mitigate the risk of long-biased exposure. In other words, whenever the market does turn, we will sell and move to cash.”

If you are going to “ride this bull,” make sure you do it with a strategy in place for when, not if, you get thrown.

Yet More, High-Quality Video Of Trudeau In Blackface Has Emerged

“It is a racist shame by any measure, a self-imposed humiliation that will cling to Justin Trudeau for life, regardless of how Canada’s next election ends up,” theToronto Starwrote upon publishing the full backstory behind Canadian Prime Minister Justin Trudeau’s blackface scandal.

The publication has gotten hold of a previously unreleased high-quality video of Trudeau’s third blackface incident, after a grainy and very brief version had been first released by Global News.

“It was a costume day for river guides on the whitewater rafting operation that I worked at in the summer between ‘92 and ’94, roughly,” Trudeau had admitted apologetically over a week ago after the brief, grainy clip had initially surfaced. From the full context and close-up of the new higher quality video, it’s evident that Trudeau, who would have been between 21 and 23 years old at the time, was the only one on the trip wearing the offensive ‘blackface’ make-up, along with an afro wig what appears to be a shirt with toucans on it (when the grainier first version surfaced, there was some debate over whether bananas were printed on the shirt).

Wow he really committed to the getup. He even wore a wig.

Also, I kind of expected more people to be dressed up for the minstrel show. But nope, just him. pic.twitter.com/JBPivnELol

A young Trudeau is seen just after the 40 second mark in the rafting trip video montage in full blackface, with the make-up covering his legs as well, making gestures toward the camera and sticking out his tongue.

Over the weekend the Toronto Star put up the high-quality video, but then without explanation set it to ‘private’ – removing it from public view, only leaving the still frame picture.

Of course, it quickly appeared on social media thereafter. Following pressure from other outlets, the video was set to public again. “After seven hours, the Star has finally made the video available to the public,” Canada’s The Post Millennialreported.

A new high quality video of @JustinTrudeau dancing in blackface

As The Sun explains further, it’s the first video to show the full context of one of the three incidents which surfaced earlier this month, but the fuller version certainly makes it worse, considering he’s “the only one who dons blackface and afro” among the many people filmed on the trip:

A previous blurry image from this moment was widely circulated, but now a high-quality video showing Mr Trudeau has come out.

In the full clip, pals are white water rafting and kayaking during the day before a fancy dress party.

Mr Trudeau is the only one who dons a blackface and afro as he cheekily sticks his tongue out for the camera.

The clip shows he even went as far as to paint his knees and his tongue black.

But this was not a one-off for the holier-than-thou politician, who is known for calling others out for racism.

As multiple publications have highlighted, now only weeks out from Canada’s federal elections, Trudeau quickly pivoted away from the controversy after issuing a brief apology, first proposing a ban on military-style assault rifles, and this past week joining climate change protests.

His lame attempt at dramatic political distraction controversial arms restriction proposal also seeks to give cities the power to ban handguns. This is as there’s clear evidence suggesting he and his Liberal Party are slipping in the polls in the wake of the blackface scandal.

There’s also the distinct possibility that even more images and video could emerge, considering he himself previously admitted there could be more out there, and that “he didn’t totally remember”.

NATO Rejects Putin’s Request To Ban Missile Deployments In Europe

At the end of this week NATO announced a bombshell that’s gone largely underreported given the Ukraine transcript brouhaha and Democrats’ push for impeachment. NATO officials said they’veformally rejected a Russian request to prohibit placing missiles previously banned under the now defunct Intermediate Nuclear Forces (INF) Treaty in Europe.

“NATO declined the proposal Thursday, because it says Russia still possesses missiles — for the SSC-8 system — that were banned under the INF pact,” United Press International (UPI) reports.

Image via US Defense Dept/Defense One

The Russian request was made directly by President Putin, who has expressed fears of “a new arms race” following both Moscow and Washington pulling out of the landmark 1988 INF treaty; however, NATO spokeswoman Oana Lungesu told the Financial Times:

“Unless and until Russia verifiably destroys the SSC-8 system, this moratorium on deployments is not a real offer.”

The SSC-8 is a ground-launched cruise missile labeled by the US a “missile of concern” within Russia’s arsenal. A series of tests of the system from a road-mobile launcher over the past years have brought down US condemnation and accusations the tests violated the INF. Thus NATO considers Putin’s proposal is “not a credible offer”.

Oana Lungescu, Nato spokesperson, confirmed receipt of a letter from Russian authorities pitching the moratorium idea but said the western allies had “heard this proposal before” and saw it as “not a credible offer”. — FT

In June NATO issued Russia a 5-week deadline to destroy the SSC-8s, and any other treaty-violating missiles; however, Putin responded with more missile tests, citing similar Pentagon tests this summer.

While there’s been no indicators that the US or NATO is moving forward with placing previously banned missiles in Europe, the fact that such a simple Russian request has been so publicly spurned is a deeply worrisome sign of a potential new arms race to come.

Italy’s new government, which haspledged to reverse former Interior Minister Matteo Salvini’s hardline approach to migration policy, appears to have triggered a new wave of mass migration from northern Africa.

More than 1,400 migrants reached Italian shores since the new government took office on September 5,according to data compiled by the International Organization for Migration (IOM).

During just the past several weeks, the number of migrant arrivals to Italy has increased incrementally: 59 migrants arrived on September 6; 67 arrived on September 9; 121 arrived on September 14; 259 arrived on September 15; 275 arrived on September 18; and 475 arrived between September 19 and September 25, according to the IOM. Overall, the number of migrant arrivals in September 2019 is up by more than 100% over the number of arrivals in September 2018.

Many of the new arrivals are reaching Italy by using new people-smuggling routes that originate in Turkey. In recent weeks, at least five migrant boats have landed in Calabria, in the far south of Italy. On September 21, for instance, 58 migrants, all Pakistani males, reached the Calabrian port of Crotone.

People-smuggling mafias are also using new routes in the Southern Mediterranean to move people to Italy from sub-Saharan Africa. In recent weeks, criminal groups have used small boats to transport migrants from Libya to Tunisia, from where the crossing to Lampedusa, Italy’s southern-most island, is shorter and less risky. On September 20, for example, 92 migrants from sub-Saharan Africa — Gambia, Ivory Coast, Mali and Senegal — reached Lampedusa.

At the same time, Italy’s new government also appears to be taking a more lenient approach to the migrant rescue ships operated by European charities, which have been accused of coordinating with people-smuggling mafias to pick up migrants off the coast of Libya and transport them to Italian ports.

On September 14, the Italian government authorized the Norwegian-flagged Ocean Viking, operated by the French charities SOS Méditerranée and Médecins Sans Frontières (MSF), to dock at Lampedusa, where 82 migrants picked up off the coast of Libya were allowed to disembark.

On September 24, the Italian government allowed the Ocean Viking, this time carrying 182 migrants, to dock at the Sicilian port of Messina.

Whereas Salvini had banned migrant rescue ships from docking at Italian ports, the new government’s more lenient approach appears also to be encouraging European non-governmental organizations (NGOs). On September 23, the Spanish NGO Open Arms announced that it would resume migrant rescues on board a vessel called Astral.

In August, Open Arms and its rescue ship of the same name were involved in a three-week stand-off with the Italian government, which refused to allow the vessel to dock in Italian ports. After more than a dozen migrants jumped overboard and tried to swim to shore, Sicilian prosecutor Luigi Patronaggio on August 20 ordered the Open Arms, anchored one kilometer off Lampedusa, to dock in Sicily so that its passengers could disembark. Subsequent video footage showed that Open Arms staged the jumps to manipulate public opinion. Italian authorities later impounded the ship.

The Spanish government vowed to take a harder line against the Open Arms NGO. On August 21, Spain’s acting Deputy Prime Minister Carmen Calvo told Cadena SER radio that the Open Arms did not have a permit to transport migrants and could be fined €900,000 ($1,000,000) for violating a ban on sailing to the seas off Libya. That threat does not appear to have deterred the Open Arms NGO. It now says it will rescue migrants in the Aegean Sea between Greece and Turkey.

NGOs such as Open Arms claim to be playing an invaluable humanitarian role in saving the lives of refugees and asylum seekers fleeing war and oppression in their home countries. Statistics show something else entirely.

Of those who arrived in Italy by sea during the first six months of 2019, 600 (21%) were from Tunisia; 400 (14%) were from Pakistan; 300 (10%) were from Algeria; 300 (10%) were from Iraq; 200 (7%) were from Ivory Coast; 200 (7%) were from Bangladesh; 100 (3.5%) were from Sudan; 100 (3.5%) were from Iran; 100 (3.5%) were from Morocco; and 50 (1.7%) were from Egypt, according to the UNHCR.

The data indicates that most of the migrants arriving in Italy are economic migrants, not refugees fleeing warzones.

In some instances, migrants arriving in Italy are hardcore criminals posing as refugees. On September 26, the Italian newspaper Il Giornalereported that a German migrant rescue ship called Sea Watch 3, which in June rammed an Italian border-control vessel that was trying to stop it from reaching shore, allowed three human traffickers who were posing as refugees to disembark in Lampedusa.

A Guinean, Mohammed Condè, and two Egyptians, Hameda Ahmed and Mahmoud Ashuia, recently were arrested in Messina. They are accused of operating a migrant detention camp in Libya where they allegedly tortured, raped, kidnapped and even murdered migrants from sub-Saharan Africa who were trying to make their way to Europe. Il Giornalereported that the new Italian government had tried to conceal information about the arrests from the general public before the story was leaked to the media.

Meanwhile, the interior ministers of France, Germany, Italy and Malta met on September 23 in the Maltese capital, Valletta, where they agreed to a tentative proposal for shipwrecked migrants to be “voluntarily redistributed” throughout the European Union.

The four-point plan, which will be presented to the interior ministers of all 28 EU member states at a summit in Brussels on October 17-18, is designed to boost Italy’s new government by showing “European solidarity.”

Similar proposals have failed in the past and there is no reason to believe this one will be different, largely because the concept of European solidarity is a myth. So far only six EU states have agreed to migrant redistribution: France, Germany, Greece, Italy, Malta and Spain.

Italian Prime Minister Giuseppe Conte has insisted that the issue of immigration “must no longer fuel anti-European propaganda.” He has also said that the government’s softer line on illegal immigration is based on “the formula of a new humanism.” He appointed Luciana Lamorgese, a career bureaucrat who has moderate views on immigration, as Italy’s new interior minister. Italian journalist Annalisa Camilli explained the changes:

“Basically, Italy is saying to Europe, we’re breaking with the past policy. It’s a big message that Italy has chosen to come back in line with Germany, France and Spain instead of aligning with [anti-migrant] countries such as Hungary and Poland under the former far-right interior minister Matteo Salvini.”

Salvini has condemned the new government as one “produced by Paris and Berlin, born out of a fear of giving up power, without dignity and without ideals, with the wrong people in the wrong place.”

Salvini has also accused Conte of re-opening the floodgates of mass migration:

“Conte has reopened Italian ports, the migrant landings are increasing for the first time in two years,” he said in an interview with Sky Tg24 television.

He also tweeted: “The new government reopens the ports, Italy is once again the REFUGEE CAMP of Europe. Abusive ministers who hate the Italians.”

Since Salvini announced his hardline immigration policies in June 2018, the number of migrant arrivals to Italy — as well as the number of dead and missing — significantly decreased. The number of arrivals by sea fell from 119,369 in 2017 to 23,370 in 2018, a drop of 80%, according to the United Nations High Commissioner for Refugees. During that same period, the number of dead and missing fell from 2,873 to 1,311, a decline of more than 50%.

A similar trend has continued in 2019: 2,800 migrants arrived in Italy by sea between January and June of 2019, compared to 16,600 during the same six-month period in 2018 and 83,800 in 2017, according to the UNHCR.

This downward trend clearly reversed immediately after the new government took office in September, as the IOM data show.

The return of mass migration to Italy is likely to push Italian voters to the arms of Salvini, who is now the most trusted politician in Italy, according to a new poll published by the newspaper Il Giornale on September 19. The poll also revealed that Salvini’s League party is now the most popular political party in Italy, and that if elections were held today, Salvini would win by a wide margin.

“The new government will not be able to escape the judgment of Italian voters for too long,” Salvini tweeted.

“We are ready. Time is a gentleman. In the end it is we who will win.”

China May Have Accidentally Revealed New Supersonic Cruise Missile In Now-Deleted Footage

A now-deleted video clip published by China’s military on Wedensday containe what appears to be the launch of a new type of supersonic cruise missile, according to SCMP.

The original footage which ran just over one minute in length was released on Chinese social media by the People’s Liberation Army Rocket Force in connection with the 70th anniversary of the founding of the People’s Republic of China next Tuesday.

Within the film is a two-second clip featuring an unusual missile being fired from a mobile launcher. In the new version, the scene is replaced with footage of two different missile launches in a desert environment, according to the report.

In the clip the missile appears to have slim dorsal fins, foldable tail fins and additional propellant, all of which, according to one expert who asked not to be identified, suggests it is designed to fly long distances and faster than the speed of sound.

“The new missile would probably have a range of more than 1,000km [680 miles],” the person said. –SCMP

Sound and seizure warning:

The PLA currently possesses the Changjian-10 land-attack subsonic missile which has an operation range of approximately 932 miles.

Ballistic and cruise missiles differ in a number of ways but the latter tend to fly at lower altitudes and at slower speeds, making them more vulnerable to defence systems.

However, the Rocket Force has made significant progress in the development of glider vehicles for its ballistic missiles, like the Dongfeng-17 (DF-17), which is now capable of gliding in outer atmosphere at upwards of five times the speed of sound, making it more able to evade missile defence systems. –SCMP

“Now that the DF-17’s glider technology is becoming more mature it could be used elsewhere. Other missiles, like this cruise missile [in the video clip], could also adopt similar vehicles to carry the warhead,” according to SCMP‘s source.

The missile seen in the original footage also appeared to have several unidentified items – which may be jamming and anti-jamming devices.

“These would enhance the missile’s ability to avoid electronic interference or guided interception by enemy missile defence systems, and therefore increase its chances of penetration,” he said.

I told you the other day that there was a coup underway by the elites I call The Davos Crowd. It started with the British Supreme Court overturning centuries of the balance of powers and ended with the Democrats in Congress announcing impeachment proceedings against President Trump.

So, now with this ruling in place what’s next and what’s really going on tactically and strategically?

Johnson, for his part, refuses to resign. He can’t or won’t get anything past this hostile Parliament. This Parliament will reconvene to push more legislation to attempt to tie his hands against negotiating with the EU from any position of strength.

Remember what made this ruling necessary. Parliament doesn’t want any meaningful Brexit and refused to accept Johnson’s offer of a General Election to allow the people to form a new government to break the deadlock.

Why? Because they know that a new Parliament would be decidedly more Leave than Remain. The polls are perfectly clear on this. Neither Jo Swinson of the Liberal Democrats nor Jeremy Corbyn of Labour have a prayer in hell of becoming Prime Minister.

If they did, they would have accepted Johnson’s offer. In fact, his offer was derided as a cheap political trick.

If Johnson were to resign here, he would be replaced by a caretaker government under Corbyn, most likely, which would then table a Second Referendum with two versions of Remain on the ballot.

This strategy neatly bypasses the original referendum to ensure the threat to the European Union is nullified.

After the shouting match in Parliament on Tuesday Jeremy Corbyn declined to table a motion of No Confidence. I believe his side of the House was as surprised by Johnson’s refusal to step down as Johnson and crew were taken aback by Corbyn’s refusal of a General Election.

And now that they’ve had a couple of days to think it over, we now know that this is what they are planning to do.

Nicola Sturgeon, the head of the Scottish National Party (SNP) tweeted out:

Agree with this. VONC, opposition unites around someone for sole purpose of securing an extension, and then immediate General Election. Nothing is risk free but leaving Johnson in post to force through no deal – or even a bad deal – seems like a terrible idea to me. https://t.co/VYSOLLdR21

Furthermore, the Liberal Democrats are talking in public about a coup against Johnson. But they won’t move against him until they “know Jeremy has the numbers.” Every day they delay is another day in which he doesn’t have the numbers.

So, why wouldn’t he?

At least 20 former members of the Conservative Party, when push came to shove, would vote with Labour, the LibDems and the SNP on this. But, the bigger question is how many from their own parties would ‘defy the whip’ and not vote against the Government.

They would ‘defy the whip’ because they are rightly scared of a General Election which would see them booted out of office. But, that said, would they do it? My guess is yes because the pressure on them at this point to betray Brexit is enormous.

The entire British political and social elite want this pesky Brexit bother binned so they can move on with erecting their new, more perfect European Union on the ashes of trivial things like sovereignty and basic human dignity.

Editorial comments aside, here’s the situation as it stands. If the vote happens and Johnson is deposed, they will have 14 days under the Fixed Term Parliaments Act to form a ‘caretaker government.’ If Corbyn ‘has the numbers’ and the agreement from the other parties then this will happen.

It will take All of Labour (247 seats), the SNP (35), the LibDems (18) and at least another 11 MP’s to get this done. And then they have to also agree on what their proposal to the EU is.

Most of Corbyn’s shadow cabinet are with the LibDems and want Article 50 revoked and the whole thing called off. Corbyn doesn’t want that and has only reluctantly been dragged down this course in order to try and preserve some semblance of Brexit, which he does believe in.

What they will offer the EU is the biggest stumbling block to this backroom deal. But, at the final moment, goal-oriented behavior will take over and an agreement will be reached.

After Johnson is gone and Corbyn installed, the Benn bill will come into effect, an extension will be negotiated and a bill for a 2nd referendum will be tabled immediately. Once Corbyn secures a deal with the EU that referendum will happen with two choices, Remain (which shouldn’t be on the ballot) and Corbyn’s deal.

Basically Remain vs. Remain. This will ensure that the most forceful point of the Leave camp, that the 17.4 million people who voted to Leave are being ignored, is neutralized.

I told you, only Hobson’s Choices from here on out for the unwashed, thick and uppity plebes who think they have any other obligation than to be tax cows milked by vampiric oligarchs convinced of their own superiority.

Then they will go for a general election hoping that the Referendum will dispirit British voters to the point of not voting, which will give Remain the win and the General Election will be a moot point. The outcome would likely be a hung Parliament, as the malaise over Brexit betrayed will keep people at home. Parliament will be paralyzed and in no position to negotiate the final terms of surrender to the EU or carry out the next stage of the negotiations.

That’s why the Second Referendum is so important. It gives Remainers all the ammunition to throw back at the Leavers saying, “See the people have spoken!”

It’s vicious and dishonest, but that’s politics, folks.

But all of that is moot if they don’t have the numbers. Then Johnson will continue to run the clock down, go to Brussels on October 17th and try to work for a deal that isn’t BRINO — Brexit in Name Only. That’s why it’s obvious that there will be a coup against Johnson without an election.

The strategy now is to whip MPs into overthrowing Johnson’s government, securing that extension and destroying what’s left of the British political system.

{kind=link}