On Thursday and Friday, the market surged on hopes that a “trade deal” was coming to fruition. This was not a surprise to us, as we detailed this outcome two weeks ago:

“‘For Trump, he can spin a limited deal as a ‘win’ saying ‘China is caving to his tariffs’ and that he ‘will continue working to get the rest of the deal done.’ He will then quietly move on to another fight, which is the upcoming election, and never mention China again. His base will quickly forget the ‘trade war’ ever existed.

Kind of like that ‘Denuclearization deal’ with North Korea.’”

As we discussed in that missive, a limited “trade deal” would potentially set the markets up for a run to 3300. To wit:

Assuming we are correct, and Trump does indeed ‘cave’ into China in mid-October to get a ‘small deal’ done, what does this mean for the market.

The most obvious impact, assuming all ‘tariffs’ are removed, would be a psychological ‘pop’ to the markets which, given that markets are already hovering near all-time highs, would suggest a rally into the end of the year.”

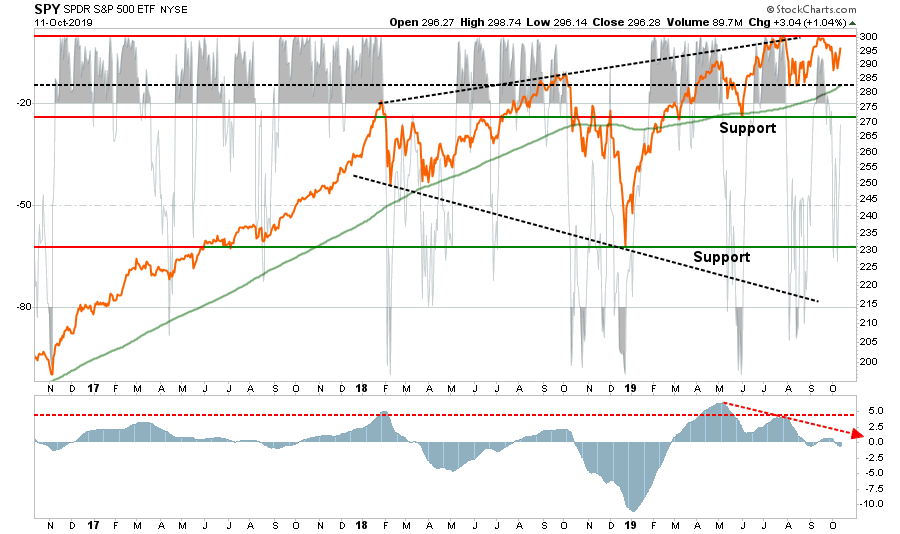

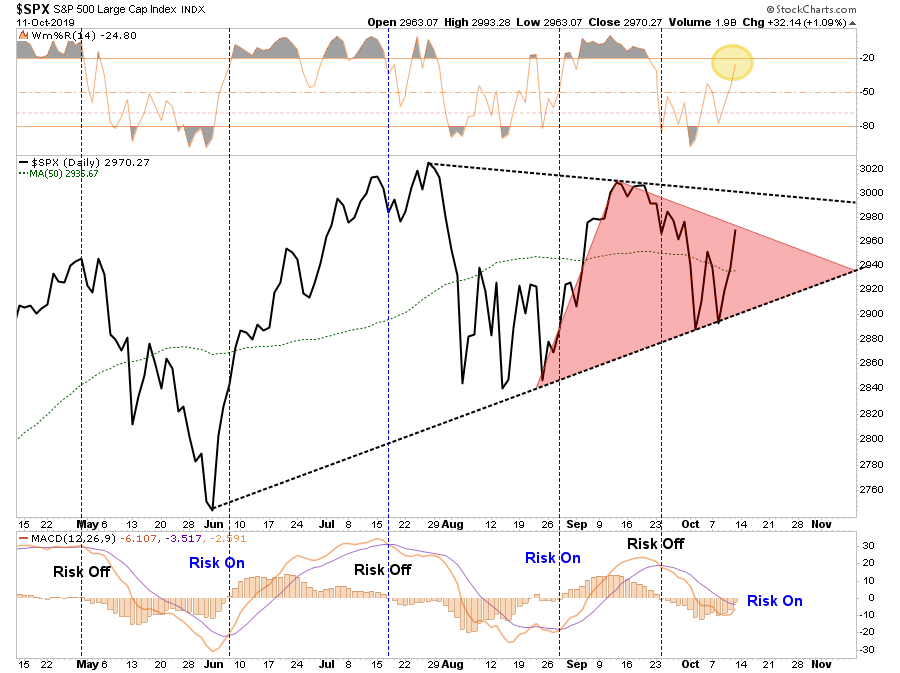

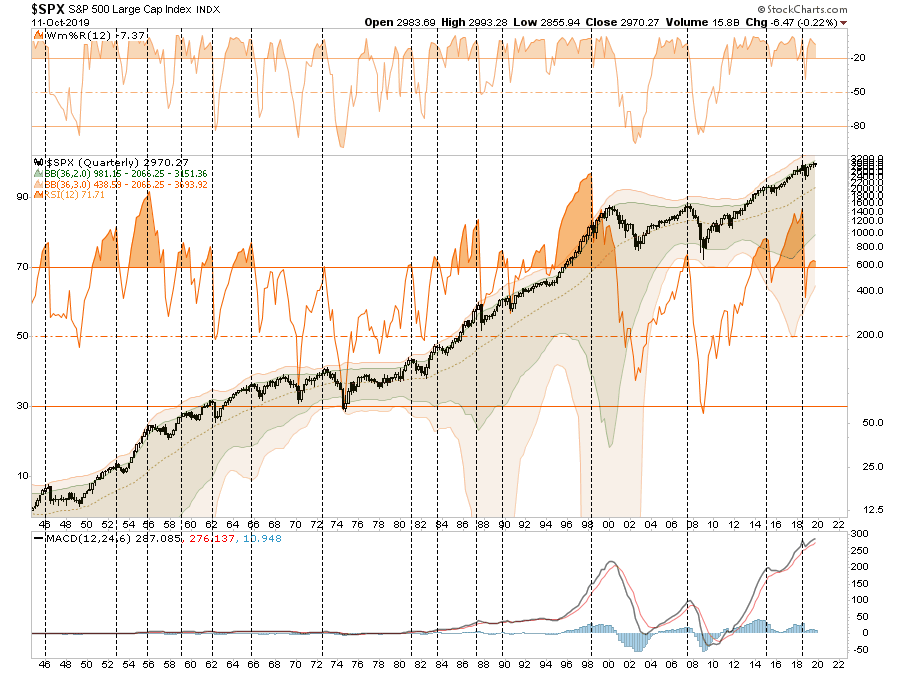

We are still maintaining our core S&P 500 position as the market has not technically violated any support levels as of yet. However, it hasn’t been able to advance to new highs either.

There is likely a tradeable opportunity approaching for a reflexive bounce given the depth of selling over the last couple of weeks.

This is the outcome we expected.

There is no “actual” deal.

The “excuse” will be this deal lays the groundwork for a future deal.

“The U.S. and China reached a partial agreement Friday that would broker a truce in the trade war and lay the groundwork for a broader deal that Presidents Donald Trump and Xi Jinping could sign later this year.

As part of the deal, China would agree to some agricultural concessions and the U.S. would provide some tariff relief. The deal under discussion, which is subject to Trump’s approval, would suspend a planned tariff increase for Oct. 15. It also may delay — or call off — levies scheduled to take effect in mid-December.”

So, who won?

China.

China gets to buy agricultural and pork products they badly need.

The U.S. gets to suspend tariffs.

Who will like the deal?

The markets: the deal removes a potential escalation in tariffs.

Trump supporters: Fox News will “spin” the “no deal” into a Trump “win” for the 2020 election.

The Fed: It removes one of their concerns potentially impacting the economy.

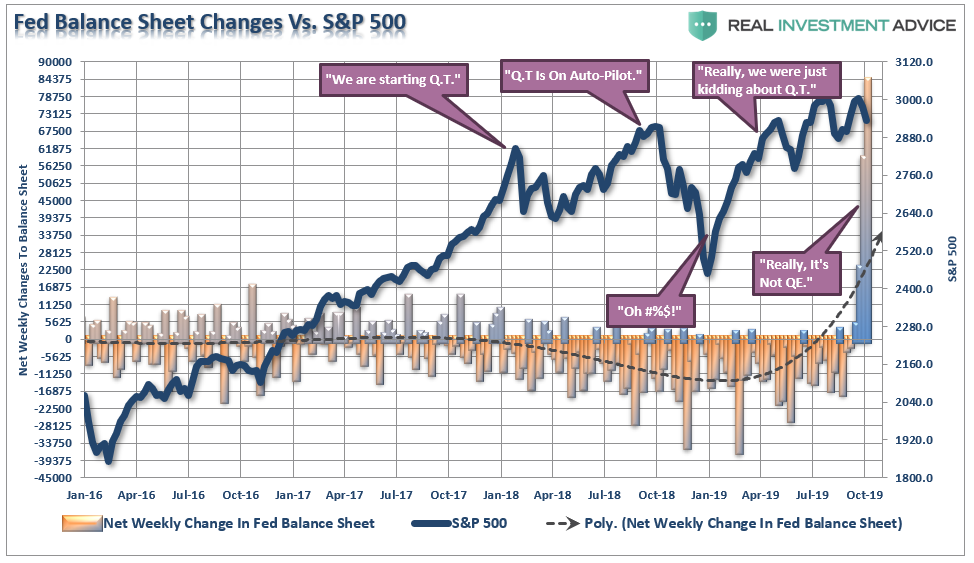

By getting the “trade deal” out of the headlines, this clears the way for the market to rally potentially into the end of the year. Importantly, it isn’t just the trade deal providing support for higher asset prices short term:

There now seems to be a pathway forward for “Brexit”

The Fed is injecting $60 billion a month in liquidity into 2020 (More on this below)

The Fed has cut rates and is expected to cut again by year end.

ECB back into easing mode and running negative rates

Fed and ECB loosening capital requirements for banks (Because they are so healthy after all.)

This is also a MAJOR point of concern.

Despite all of this liquidity and support, the market remains currently confined to a downtrend from the September highs. The good news is there is a series of rising lows from June. With a “risk-on” signal approaching and the market not back to egregiously overbought, there is room for the market to rally from here.

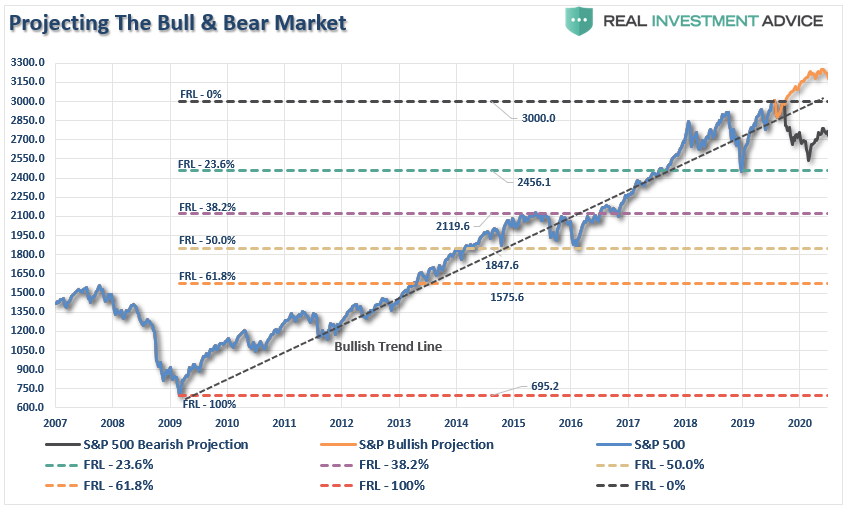

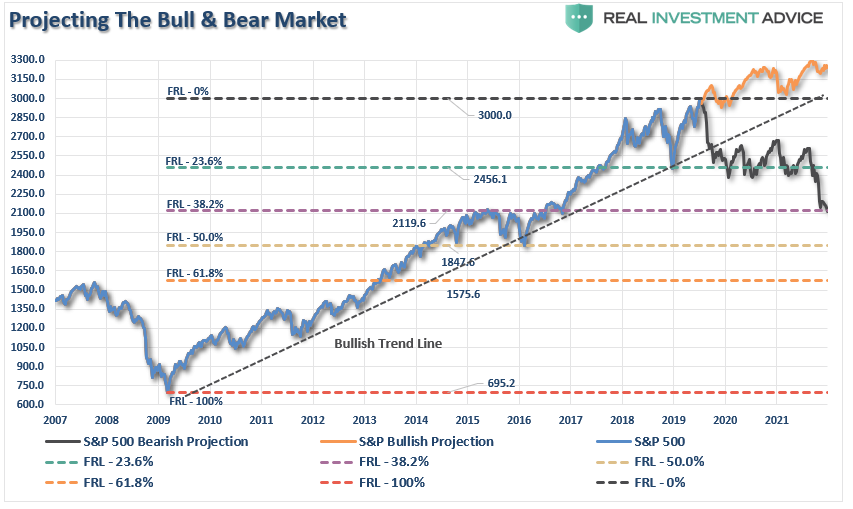

“As we face down the last half of 2019, we can once again run some projections on the bull and bear case going into 2021, as shown in the chart below:”

The Bull Case For 3300

Momentum

Stock Buybacks

Fed Rate Cuts

Stoppage of QT

Trade Deal

However, while the case for a push higher is likely, the risk/reward still isn’t great for investors over the intermediate term. A failure of the market to make new highs, given the amount of monetary support, will be a very bearish signal.

The Fed’s “Not QE”, “QE”

There is no systemic threat from a shortage of reserves or a weak banking system. Some (a few) firms got sideways with new bank liquidity regs. The Fed should let market deal with it, not inject low cost money to encourage this behavior! And, Fed should let us know who they are!

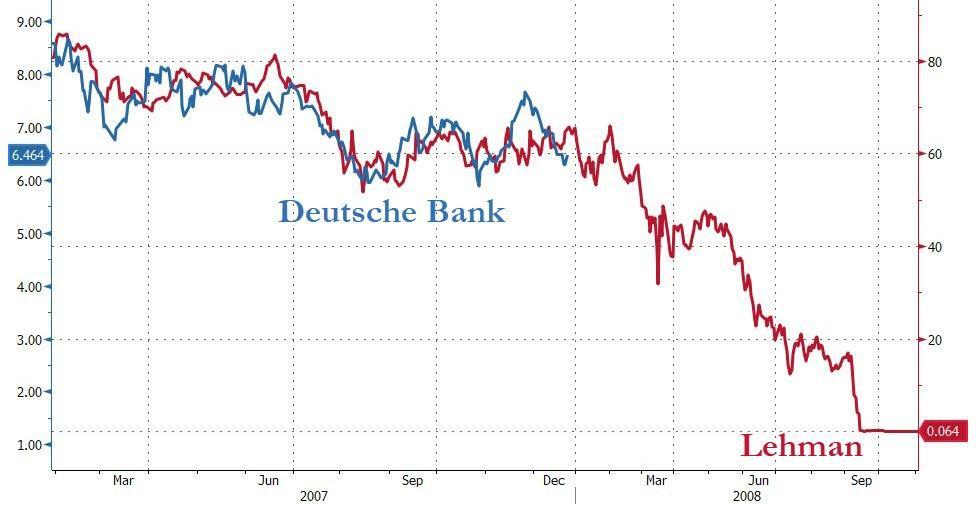

“Then there are the tail-risks of a credit-related event caused by a dollar funding shortage, a banking crisis (Deutsche Bank), or a geopolitical event, or a surge in defaults on “leveraged loans” which are twice the size of the “sub-prime” bonds linked to the “financial crisis.” (Read more here)

Just remember, bull-runs are a one-way trip.

Most likely, this is the final run-up before the next bear market sets in. However, where the “top” is eventually found is the big unknown question. We can only make calculated guesses.”

Think about this logically for a moment.

The yield curve inverts which puts pressure on bank loans and funding.

The Fed cuts rates, which puts pressure on banks net interest margins.

The banks are chock full of leverage loans, risky energy-related debt, subprime auto loans, etc.

The Fed begins reducing excess reserves.

All of a sudden, banks have a problem with overnight funding.

Fed reduces liquidity regulations (put in place after Lehman to protect the financial system)

Fed now has to commit to $60 billion in funding through January 2020 to increase reserves.

The last point was detailed in a recent FOMC release:

“In light of recent and expected increases in the Federal Reserve’s non-reserve liabilities, the Federal Open Market Committee (FOMC) directed the Desk, effective October 15, 2019, to purchase Treasury bills at least into the second quarter of next year to maintain over time ample reserve balances at or above the level that prevailed in early September 2019. The Committee also directed the Desk to conduct term and overnight repurchase agreement operations (repos) at least through January of next year to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation.

In accordance with this directive, the Desk plans to purchase Treasury bills at an initial pace of approximately $60 billion per month, starting with the period from mid-October to mid-November.”

NOTE: If you don’t understand what has been happening with overnight lending between banks – READ THIS.

The Fed is in QE mode because there is a problem with liquidity in the system. Given the Fed was caught “flat-footed” with the Lehman bankruptcy in 2008, they are trying to make sure they are in front of the next crisis.

The reality is the financial system is NOT healthy.

If it was, then we would:

Not still be using “emergency measures” to support banks for the last decade. (QE, LTRO, Etc.)

Not be pushing $17 trillion in negative interest rates on a global basis.

Have reinstated FASB Rule 157 in 2012-2013 requiring banks to mark-to-market the assets on their books. (A defaulted asset can be marked at 100% of value which makes the bank look healthy.)

Not be needing to reduce liquidity requirements.

Not be needing $60 billion a month in QE.

Oh, but that’s right, Jerome Powell denies this is “QE.”

“I want to emphasize that growth of our balance sheet for reserve management purposes should in no way be confused with the large-scale asset purchase programs that we deployed after the financial crisis. Neither the recent technical issues nor the purchases of Treasury bills we are contemplating to resolve them should materially affect the stance of monetary policy. In no sense, is this QE,” – Jerome Powell

It’s QE.

Just so you can understand the magnitude of the balance sheet increase over the last couple of weeks, the largest single week increase from 2009 to September 20th, 2019 was $39.97 billion.

The last two weeks were $58.2 and $83.87 billion respectively.

But, it’s not Q.E.

So, what was it then?

This was not about covering unexpected cash draws to pay quarterly taxes, which was one of the initial excuses for the funding shortfalls.

So true – remember the whole #REPO crisis started because it was just a demand for cash for #tax#payments. Apparently, companies are paying taxes daily until sometime in 2020.

Amazing the #media continually buys into the #narratives as if they were the truth. #ThinkPeoplehttps://t.co/Y3cxdK9AWe

This was bailing out a bank that is in serious financial trouble. It started with the ECB a month ago loosening requirements on banks, then proceeded to the Fed reducing capital reserve requirements and flooding the system with reserves.

Who was the biggest beneficiary of all of these actions? Deutsche Bank.

Which is about 4x as large as Lehman was in 2008 and is currently following the same price path as well. Let me repeat, the Fed is terrified of another “Lehman Crisis” as they do not have the tools to deal with it this time.

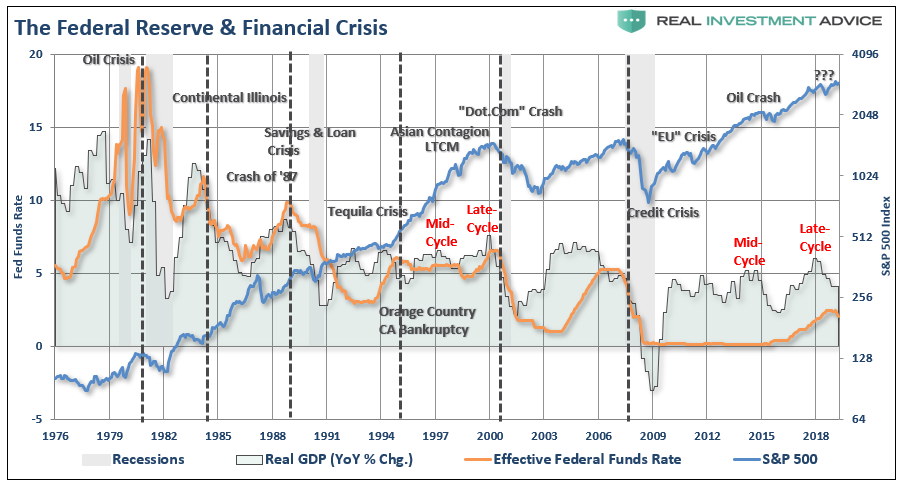

The problem for the Fed, is that while they insist recent rate cuts are “mid-cycle” adjustments, as was seen in 1995 to counter the risk of the Orange County bankruptcy, the reality is the “mid-cycle” has long been past us.

With the Fed cutting rates, injecting weekly records of liquidity into the system, at a time where economic data has clearly taken a turn for the worse, the situation may “not be in as good of a place” as we have been told.

Being a little more cautious, taking in some profits, and rebalancing risks continues to be our recipe for navigating the markets currently.

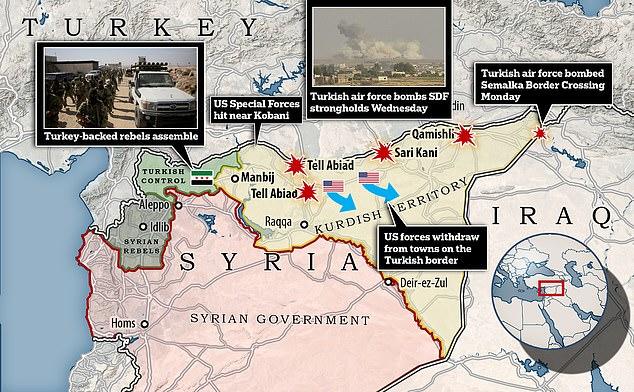

US Troops Can Fire Back If Turkey Attacks Positions Again, Pentagon Says

Defense Secretary Mark Esper told “Face the Nation” on Sunday that remaining US troops were caught between Turkish forces and the SDF and that it would be “irresponsible for me to keep them in that position.” Revealing that Trump has ordered “a deliberate withdrawal” from Northern Syria “as safely and quickly as possible,” which includes some 1,000 troops — Esper further addressed controversy surrounding a Friday incident wherea US base on Kobani came under Turkish artillery fire.

“And so we find ourselves, we have American forces likely caught between two opposing advancing armies, and it’s a very untenable situation,” Esper said. According to defense officials speaking to The Washington Post this weekend, the Army believes Turkish artillery fire on American positions in Kobani were deliberate, specifically accusing Turkey of ‘bracketing’ U.S. forces by firing on both sides of the observation post.

Esper was asked about this dangerous escaltion, to which he responded that US troops“have the right to self defense and we will execute it if necessary” — thus indicating that American forces in Syria have been given the green light to fire back if fired upon. “A senior Pentagon official said shelling was so heavy that the U.S. personnel considered firing back in self-defense,” a prior report cited.

File image via Warfare Today

“A contingent of U.S. Special Forces has been caught up in Turkish shelling against U.S.-backed Kurdish positions in northern Syria,” Newsweek initially reported of the Friday incident.

The Newsweek report cited an “Iraqi Kurdish intelligence official and senior Pentagon official” to say that “Special Forces operating in the Mashtenour hill in the majority-Kurdish city of Kobani fell under artillery fire from Turkish forces” amid operations related to ‘Operation Peace Spring’.

“We had been there for months, and it is the most clearly defined position in that entire area,” an Army officer told the Post. Multiple 155mm shells fell “within a few hundred yards of the base on Mistenur Hill,” the officer said.

US official – the situation on the ground is deteriorating rapidly in Syria. Extremist Turkish proxies have advanced. US Forces at risk of being isolated. increased risk of confrontation between Turkish proxies and US Forces unless Turkey halts their advance immediately.

Later reports suggested the US contingent had temporarily withdrawn from their position in Kobani as a result, but a Pentagon official subsequently said U.S. troops had not withdrawn from Kobane.

Via The Daily Mail

Brett McGurk, a former White House anti-ISIL special envoy to the region under both Trump and Obama, wrote on Twitter of the incident: “[The shelling] was not a mistake.”

“Turkey wants us off the entire border region to a depth of 30 kilometers,” McGurk also told the Post. “These were warning shots on a known location, not inadvertent rounds.”

It now appears, however, that the White House wants to avoid even the possibility that such a close encounter could happen again, given the newly announced “deliberate withdrawal” of American forces from any position in the path of the Turkish incursion.

Hunter Biden Emerges; Quits Board Of Chinese Private-Equity Firm

Hunter Biden is stepping down from a controversial board position at a Chinese-based private-equity company, and has vowed to forego all foreign work if his father, former Vice President Joe Biden, is elected president in 2020, according to Bloomberg.

Hunter will step down from the board on Oct. 31, according to a statement released by his lawyer, George Mesires.

“Hunter always understood that his father would be guided, entirely and unequivocally, by established U.S. policy, regardless of its effects on Hunter’s professional interests,” reads the statement. “He never anticipated the barrage of false charges against both him and his father by the President of the United States.”

“Under a Biden Administration, Hunter will readily comply with any and all guidelines or standards a President Biden may issue to address purported conflicts of interest, or the appearance of such conflicts, including any restrictions related to overseas business interests,” the statement continues. “He will continue to keep his father personally uninvolved in his business affairs.“

In May, journalist Peter Schweizer accused the Bidens of corruption in both Ukraine and China – revealing that in 2013, they flew together to China on Air Force Two. Two weeks later, Hunter’s firm inked a private equity deal for $1 billion with a subsidiary of the Chinese government’s Bank of China, which expanded to $1.5 billion.

“If it sounds shocking that a vice president would shape US-China policy as his son — who has scant experience in private equity — clinched a coveted billion-dollar deal with an arm of the Chinese government, that’s because it is” –Peter Schweizer

As the accusations against Hunter mounted, he attempted to do damage control in a July interview with the New Yorker – in which he opened up about being a crackhead and accepting a ‘bribe’ from a Chinese energy tycoon in the form of a 2.8 carat diamond worth thousands of dollars, which he says wasn’t a bribe – and admitted he and his father had spoken of his business dealings.

President Trump and his attorney Rudy Giuliani have homed in on both China and Ukraine – where Joe Biden leveraged his position as Vice President to have a Ukrainian prosecutor fired who was investigating a company whose board Hunter sat on. Bloomberg calls this claim “unsubstantiated” despite Joe Biden bragging about doing so on tape.

U.S. banking records show that Hunter Biden’s American-based firm Rosemont Seneca Partners LLC, received regular transfers into one of its accounts (more than $166k/month) from the natural gas firm Burisma Holdings that employed Hunter Biden. All of this occurred during a period when Vice President Biden was the main U.S. official dealing with Ukraine and its tense relationship with Russia.

Two years after leaving office, Joe Biden couldn’t resist the temptation to brag to an audience of foreign policy specialists about the time as vice president that he strong-armed Ukraine into firing its top prosecutor. His threat was so severe that Ukraine would have lost $1 billion in U.S. loan guarantees sending Ukraine toward insolvency. So the question is – why? Why did Joe Biden demand the immediate firing of Prosecutor General Viktor Shokin? And what did the State Department know about Hunter Biden’s dealings in Ukraine and Ukraine’s investigations into those business dealings? –SLF

Where’s Hunter? He has totally disappeared! Now looks like he has raided and scammed even more countries! Media is AWOL.

Meanwhile, Ukrainian MP Andriy Derkach announced last Wednesday that Joe Biden received $900,000 from Burisma Group for lobbying activities, citing materials related to an investigation.

Former U.S. Vice President Joe Biden received $900,000 for lobbying activities from Burisma Group, Ukraine’s Verkhovna Rada member Andriy Derkach said citing investigation materials.

Derkach publicized documents which, as he said, “describe the mechanism of getting money by Biden Sr.” at a press conference at Interfax-Ukraine’s press center in Kyiv on Wednesday. –Interfax

“This was the transfer of Burisma Group’s funds for lobbying activities, as investigators believe, personally to Joe Biden through a lobbying company. Funds in the amount of $900,000 were transferred to the U.S.-based company Rosemont Seneca Partners, which according to open sources, in particular, the New York Times, is affiliated with Biden. The payment reference was payment for consultative services,” said Derkach.

Derkach also puiblicized sums of money transferred to Burisma Group representatives – including Hunter Biden.

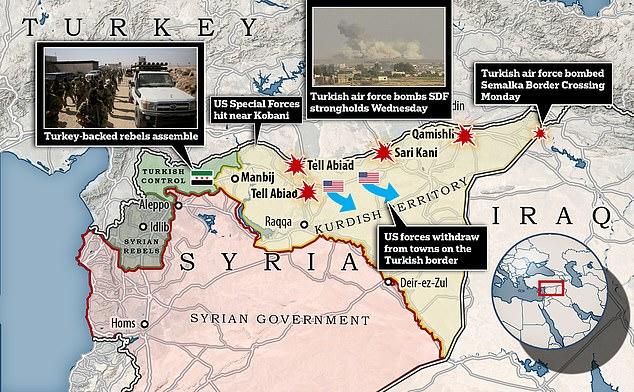

Trump Orders 1,000 Troops To Evacuate Syria, Warns Sanctions On Turkey “Ready To Go”

Defense Secretary Mark Esper told “Face the Nation” in a Sunday interview that the Trump administration is “preparing to evacuate” about 1,000 U.S. troops from northern Syria “as safely and quickly as possible,” CBS reports.

“In the last 24 hours, we learned that [the Turks] likely intend to extend their attack further south than originally planned, and to the west,” Esper said. “We also have learned in the last 24 hours that the… SDF are looking to cut a deal, if you will, with the Syrians and the Russians to counterattack against the Turks in the north.”

Image via the AP

This as President Trump has also announced the US Treasury is “ready to go” with sanctions on Turkey.

This also comes after a week ago Trump ordered the withdrawal of US troops from northern border posts ahead of a Turkish military incursion to establish a so-called ‘safe zone’. That decision has been met with fierce push back among Congressional leaders and pundits, angry at the US “betrayal” of its Syrian Kurdish partners, namely the US-funded and trained Syrian Democratic Forces (SDF).

In his comments to “Face the Nation,” set to air on Sunday, Esper further explained that American forces were now caught between the Turkish assault and the SDF.

“And so we find ourselves, we have American forces likely caught between two opposing advancing armies, and it’s a very untenable situation,” Esper said. “So I spoke with the president last night, after discussions with the rest of the national security team, and he directed that we begin a deliberate withdrawal of forces from northern Syria.”

WATCH: .@EsperDoD on the planned evacuation of U.S. troopers in northern Syria.

“I spoke with the president last night after discussions with the rest national security team and he directed that we begin a deliberate withdrawal of forces from northern Syria.” pic.twitter.com/2Ma0XmypfP

Following a Friday incident wherein Turkish artillery shells landed near US positions in Kobani, Pentagon officials accused Turkey ofdeliberately “bracketing” American forces by firing on both sides of the observation post.

While Turkey claimed it was a ‘mistake,’ US officials said Ankara had known about that specific base for months and that it could have only been intentional.

Esper said on Sunday that US troops “have the right to self defense and we will execute it if necessary” when asked about the incident and future rules of engagement.

Meanwhile Trump tweeted early Sunday: “Very smart not to be involved in the intense fighting along the Turkish Border, for a change. Those that mistakenly got us into the Middle East Wars are still pushing to fight. They have no idea what a bad decision they have made. Why are they not asking for a Declaration of War?”

Very smart not to be involved in the intense fighting along the Turkish Border, for a change. Those that mistakenly got us into the Middle East Wars are still pushing to fight. They have no idea what a bad decision they have made. Why are they not asking for a Declaration of War?

For now it’s unlikely that this means all American forces will make a complete exit from Syria.

When pressed on a timeline for the pullback, Esper merely said it would be done “as safely and quickly as possible”; but given US forces appear to be in the line of Turkish artillery fire, a pullback will no doubt come sooner than later — if not occurring already.

After suspending the service in less than two months after launch in January, Keplerk says that its customers will be able to buy Bitcoin from tobacconists in coupons of 50, 100 or 250 euros, France’s top news channel BFM TV reports Oct. 10.

According to the report, Bitcoin payments in all 5,200 locations will be feasible through Keplerk’s partner Bimedia, which will provide payment terminals.

As previously reported, Keplerk’s initial launch in January 2019 of the service reportedly involved just six tobacco shops, while other publications reported there were as many as 24 shops participating in the program. At the time, Keplerk co-founder Adil Zakhar stated that the firm was planning to expand the project to 5,200 tobacco shops by February despite the reports that France’s central bank did not endorse the initiative.

Bitcoin adoption surges in France

Meanwhile, France is apparently seeing a surge in cryptocurrency adoption. In late September, Cointelegraph reported that over 25,000 points-of-sale of 30 French retailers including sportswear giant Decathlon and cosmetics store Sephora will start accepting BTC payments by early 2020. As reported earlier in September, the French unit of Domino’s Pizza launched an ordering competition with a prize of $110,000 in Bitcoin or cash.

On Sept. 12, French Economy Minister Bruno Le Maire claimed that French authorities do not plan to tax crypto-to-crypto trades, but rather will consider taxation when crypto is sold for fiat money.

Meet The Futuristic, Fully-Autonomous Concept Truck Without A Cab

Swedish manufacturer Scania has introduced a brand new “futuristic fully autonomous concept truck without a cab” called AXL, according to Tuvie.

The vehicle is described as a “heavy-duty self-driving vehicle” and was designed by a group of Scania experts from different fields.

It features the company’s modular system at the core of its design and could be used in many industries that are seeking out “more sustainable, self-driving vehicles to increase their productivity and performance.”

Some examples including mining and construction, which are favorable for self-driving vehicles since they are well-controlled locations.

Scania describes the truck as “a step forward to smart transportation systems of the future”. And the software in the truck will play just as big of a role as the hardware: the AXL is directed and monitored by an intelligent control environment.

In places like mines, autonomous operations can be facilitated by a logistics system that tells vehicle how it should perform.

Many self-driving autonomous trucks in use today still have a cab where a driver can sit, should the need to intervene arise. The AXL is designed without a cab, meaning no driver will be in the truck. Its combustion engine is even powered by renewable biofuel.

Scania is a major manufacturer of heavy trucks and buses, in addition to diesel engines for heavy vehicles as well as marine and general industrial applications. The company was formed in 1911.

The government has stepped up its lies about immunity in the Sacoolas case to a breathtaking degree. I genuinely am astounded by the sheer audacity of the lies now being told, including a staggeringly mendacious FCO-briefed BBC article yesterday stating that “23,000 individuals in the UK have diplomatic immunity” and that it extends to “drivers and cooks”. This follows up the breathtaking FCO statement to Sky News that RAF Croughton “is regarded as an annex to the US Embassy in London” – a total falsehood.

What I cannot understand is why. The entire incident is extremely strange. On the face of it, Harry Dunn’s death was a tragic accident caused by somebody who had not long been in the UK driving on the wrong side of the road. This dreadful mistake is forgivable, as Harry’s very sensible parents have said; there seems little reason to believe the justice system would have been more harsh. There was no conceivable need to run away. That is what they cannot forgive.

Make no mistake; the spiriting of the Sacoolas family out of the UK was a considered act by the US Government and, in the case of a manslaughter in an allied state, the decision not to waive immunity would have been taken right at the top of the State Department. Make no mistake about it either, the FCO would have been informed and complicit in the decision and has only pretended to protest after massive public pressure, got up by Harry’s admirable family a full three weeks after the incident had been, the government would have hoped, successfully buried.

But why? It should be stated that it is the norm to waive diplomatic immunity in serious cases between allied or friendly developed states, where each has confidence in the other’s justice system. Unless the accident did not happen as stated, or there is a Chris Huhne type blame switch involved (Trump yesterday very carefully made the point that cameras had confirmed the identity of the driver – I was not sure why he brought this up when nobody had questioned it), it is very hard to understand why diplomatic immunity has been insisted on in this case. Assuming that Anne Sacoolas was the driver and the incident was as described, the only explanation I can think of is that it was hoped by getting them out the country to avoid all publicity and scrutiny of Jonathon Sacoolas’ real job, which is to spy on British citizens communications’ for GCHQ, who face legal impediments in doing so.

I would like to be able to say that if that cover-up is the plan, it has backfired, except that the media has unanimously censored all reporting of what Sacoolas actually does in the UK. Which is quite extraordinary given the massive but (deliberately) wildly misleading coverage of this case. I wish there were many more places than here you could come to learn the truth, but there are not. In which context, it is worth noting that both Buzzfeed and the Huffington Post have joined the DSMA Notice Committee and become willing tools of the UK security services.

After I pointed out that Sacoolas does not appear on the Diplomatic List, does not hold diplomatic rank and is not accredited to a diplomatic mission, and therefore cannot be a “diplomatic agent” under the Vienna Convention, the FCO first admitted this and claimed his immunity stemmed from a separate bilateral agreement, as reported by Sky News.

Having negotiated many international agreements in my time in the FCO, I know that they need to be given effect in UK domestic law, usually by Order in Council. I therefore searched for legislation giving the Secretary of State authority to grant immunity from criminal prosecution under bilateral agreements for spy bases, and I could find nothing. The legal basis for granting immunities under the Vienna Convention is the Diplomatic Privileges Act 1964, which enacted it into UK legislation. The legal basis for granting military immunity under Status of Forces Agreements, or for NATO personnel, is clear and set out in the Visiting Forces Act of 1952.

I could find nothing that would give legal powers to a Secretary of State to grant immunity to US spies on military bases working on communications interception of UK citizens. No legislation was passed to give legal effect in the UK to the reputed bilateral agreements which cover this.

I therefore wrote to the FCO asking for a copy of the bilateral agreement under which Sacoolas has immunity, and a copy of the UK legislation giving the authority to grant the immunity to the Secretary of State. I have not received any reply, but apparently it concentrated minds because the FCO has now switched to make an aggressive – and nonsensical – assertion that Sacoolas is a diplomat in terms of the Vienna Convention.

Not only that, the FCO’s admission to Mark Stephens, reported in that original article by Sky News, that Sacoolas was not a diplomat under the Vienna Convention has been expunged from history. The Sky News defence correspondent Alistair Bunkall had tweeted a reply to me copying this report, as evidence there was no DSMA notice controlling the reporting of the Sacoolas case.

Yet this article, held up by Bunkall as evidence of a free media, was within 24 hours totally rewritten to remove the FCO’s admission that Sacoolas was not on the diplomatic list, and replace it with the new FCO attack line of strong assertion that Sacoolas is covered by the Vienna Convention, and to highlight Dominic Raab’s entirely insincere and pretend effort to request Sacoolas’ return. The story has in effect been completely rewritten by the FCO. This is what the same page, the same url, Bunkall tweeted out looks like now:

Pretty well all that remains of the original – accurate – story is the url, now totally at odds with the contenthttps://news.sky.com/story/husband-of-us-woman-granted-diplomatic-immun…. There is no acknowledgement that the story has been changed, and the original is strangely not available even on the wayback machine. If Bunkall has not tweeted it, it would be difficult to prove this brief moment of reporting the truth had never existed. The irony of Bunkall’s tweeting a now completely censored report as evidence of press freedom is stunning.

Forgive me but I here must insert my original post on Sacoolas to make plain the actual legal position:

There is no Jonathan Sacoolas on the official Diplomatic list. Neither Sacoolas nor his wife has any right to claim diplomatic immunity under the Vienna Convention.

A diplomatic agent shall enjoy immunity from the criminal jurisdiction of the receiving state

Article 37 extends this privilege to family members living in his household. A “diplomatic agent” is defined in article 2(d).

The “members of the diplomatic staff” are the members of the staff of the mission having diplomatic rank;

Jonathan Sacoolas does not hold, and has never held, a diplomatic rank. He has never been a member of staff of a diplomatic mission. (All those with diplomatic rank appear in the diplomatic list, see above link. That list also includes some attaches who do not have diplomatic rank (depending on the type of attache), but there is nobody with diplomatic rank not in the list).

Jonathan Sacoolas does not have, and has never had, any entitlement to diplomatic immunity in international law. Sacoolas works as an NSA technical officer at the communications interceptions post at “RAF Croughton”. His role is support to the interception of communications from British citizens. As I explained in Murder in Samarkand, the NSA and GCHQ share all intelligence reports, but each faces legal constraints on mass spying on its own citizens. So the NSA has staff here fronting the spying on British citizens, while GCHQ has staff in the US fronting the spying on US citizens, and the polite fiction is that the results are transmitted back over the Atlantic to the US or UK respectively, before being “shared” with the partner intelligence agency.

None of which has anything to do with diplomacy, and Sacoolas must be the subject of a DSMA notice given that all mainstream media are referring to him constantly as a “diplomat”, when they all know that is not true. The irony is of course that if Sacoolas actually was a real diplomat, the US would very probably have waived the diplomatic immunity of his wife, as the issues around his presence and function would be much less sensitive.

The UK has no Vienna Convention obligation to acknowledge the “immunity” of Sacoolas’ wife, contrary to all reporting to date. What does apparently exist between the UK and US is a secret, bilateral agreement to treat GCHQ and NSA staff as if they had diplomatic immunity. That is not at all the same thing as Vienna Convention protection under international law. I cannot conceive the grief of Harry Dunn’s parents, but I do hope that they are not deceived by the pretence at intervention in this case by Johnson and Raab.

I am not at all convinced, as a matter of law, that the government has the power to grant, by bilateral treaty or otherwise, immunity from criminal prosecution to foreign nationals, plainly outside the provisions of the Vienna Convention. This should be tested by the courts.

With this in mind, let us examine the claims made by the FCO to the media in response. From that Sky News report we have:

This is utter nonsense. It is simply untrue. RAF Croughton is not an annex to the US Embassy. The FCO has invented this lie to counter the fact that, to qualify for diplomatic immunity under the Vienna Convention, Sacoolas must be attached to a diplomatic mission. RAF Croughton is not a diplomatic mission. A RAF base cannot be a US Embassy.

That RAF Croughton is an annex of the US Embassy can be immediately disproved. An Embassy is the sovereign territory of the nation which owns it. Within Embassy premises, the law which applies is the law of the Embassy’s state, not the host state. That is not the case in RAF Croughton. That RAF Croughton is not an Annex of the US Embassy can be instantly proven beyond any doubt or argument by the fact that the bye-laws applicable within it are promulgated by the UK Secretary of State for Defence.

If the base were an annex to the US Embassy, the UK Secretary of State could not make bye-laws for it. There is no mention within the bye-laws covering security and management of and access to RAF Croughton of any area within it being part of the US Embassy. The claim is a simple and straightforward lie, and a rather desperate one.

Finally, if RAF Croughton were an annex to the US Embassy and if Mr Sacoolas were a diplomat, the cars of both he and his wife would have diplomatic CD plates. Mrs Sacoolas was not driving a diplomatic car – an obviously vital fact in this case, again omitted from all mainstream media reporting.

There are further lies in the Sky News report.

On the contrary, the Diplomatic List is a comprehensive record of every diplomat notified to the FCO as having diplomatic status by Diplomatic Note – and as specified in Article 10 of the Vienna Convention, a person must be so notified to become a “diplomatic agent”. There are no “diplomatic agents” not on the Diplomatic List.

I was in the Foreign Office for 20 years and a member of its Senior Management Structure for 6 years. It would be nice if you took my word for this, but you don’t have to – it is very neatly explained at the very start of the Diplomatic List:

The entire purpose of the list is to record those with diplomatic immunity and the legislation under which they get it. From page 127 to 137 it lists those who have diplomatic immunity not under the Diplomatic Privileges Act – which only covers national Embassies and High Commissions – but under other legislation as they work not for nations but for international agencies: and in every individual case the Diplomatic List names the specific legislation which confers the immunity.

The major purpose of the London Diplomatic List is to be a compendium of diplomatic status with a precise attribution of immunity and its source. As Sacoolas is not listed as a diplomat of the US Embassy in the Diplomatic List or the Consular List, he is not a “diplomatic agent” entitled to full diplomatic immunity. Full stop. As explained below, Sacoolas’ wife would only have diplomatic immunity while driving privately if he held a full diplomatic rank (in which case her car would have diplomatic CD plates, which it does not).

The FCO claim that the Diplomatic List only covers London is also ludicrous. The same government webpage gives you the full list of consulates, with their consuls, and even of honorary consuls, outside of London. It does not list Embassy annexes outside London because there are none and the concept does not exist in international law. Embassy outposts from the capital are consulates or consular offices.

The FCO is trying to convince you that their entire section of staff who work on diplomatic accreditations and constantly update the Diplomatic List, are wasting their time on an entirely pointless exercise producing futile and incomplete lists. I wonder how those employees’ morale is today.

But Raab’s FCO did not stop there with the lies. They then briefed the BBC to produce an article on diplomatic immunity so full of lies as to be truly astonishing. I am prepared to confess that I could not complete this blog entry for three days because I was genuinely emotionally upset by the realisation that the UK now has a government whose noted penchant for “aggressive” media and opinion management means it is prepared to employ the big lie on any occasion and subject.

The BBC article is plainly based entirely on an FCO briefing and written with the express and sole intention of obscuring the fact that Sacoolas is not a diplomat. It contains so many outrageous lies that I am afraid this article is going to get still longer. If you have had the patience to stick with me so far, please bear with me a bit further.

This is another quite extraordinary lie, as anybody can easily confirm simply by reading the Vienna Convention. As explained above, full diplomatic immunity is enjoyed only by “diplomatic agents” who must be persons “Having diplomatic rank”.

As very plainly set out in articles 37 of the Vienna Convention:

Article 37

1.The members of the family of a diplomatic agent forming part of his household shall, if they are

not nationals of the receiving State, enjoy the privileges and immunities specified in articles 29 to 36.

2.Members of the administrative and technical staff of the mission, together with members of

their families forming part of their respective households, shall, if they are not nationals of or

permanently resident in the receiving State, enjoy the privileges and immunities specified in articles 29

to 35, except that the immunity from civil and administrative jurisdiction of the receiving State specified

in paragraph 1 of article 31 shall not extend to acts performed outside the course of their duties. They

shall also enjoy the privileges specified in article 36, paragraph 1, in respect of articles imported at the

time of first installation.

3.Members of the service staff of the mission who are not nationals of or permanently resident in

the receiving State shall enjoy immunity in respect of acts performed in the course of their duties,

exemption from dues and taxes on the emoluments they receive by reason of their employment and the

exemption contained in article 33.

So “diplomatic agents” “having diplomatic rank” – which, remember, Sacoolas does not have – hold full immunity as do their families.

“Administrative and technical staff” have immunity from prosecution only while performing acts “in the course of their duties”. That is while actually engaged in work for their governments, not outwith their working time. Their families also have exactly the same immunity, and as the families do not have any official duties to be engaged in, in practice their immunity is only civil ie from taxation.

In the case of another spy, Shai Masot, not on the diplomatic list, when challenged as to his diplomatic status the FCO claimed he was not a “diplomatic agent” but only “technical and administrative staff”. As an NSA communications interception expert Sacoolas could arguably be “technical and administrative staff” if it were true that RAF Croughton were an annex of the US Embassy – but that plainly is not true.

However even were Sacoolas covered by immunity as “technical and administrative work” he and his family would only be covered for events that happened in the direct course of his work, and very, very plainly Anne Sacoolas would not have had diplomatic immunity when she hit Harry Dunn. She only had immunity if Sacoolas is a full blown “diplomatic agent” – which he isn’t. We are yet to be told what “diplomatic rank” he allegedly holds. So for the BBC to try to obscure the case with cooks and gardeners – who as “service staff” have even less immunity and their families none at all – is deliberate obfuscation.

This is an utterly tendentious claim. As explained above, the only people with practical diplomatic immunity outside their actual work are full blown diplomats, and there are just over 3,000 of them, all captured in the Diplomatic List. The BBC report attempts to make out that categories such as “international organisations” account for significant parts of this alleged horde of diplomats, but as noted above those from international organisations entitled to diplomatic immunity are all in the London Diplomatic List pp 127 to 137 and amount to just 220 people. It is also worth remembering that the majority of family members who have immunity are children.

There is a much larger number of military personnel who enjoy immunity under the Visiting Forces Act – a total disgrace, in my view – but this is not diplomatic immunity and it is not claimed Sacoolas has it. I have no idea where the ridiculous 23,000 figure for diplomatic immunity originates. Dominic Raab’s arse seems the best bet.

The Johnson/Raab PR strategy here is plain – to drown investigation of Sacoolas’ extremely dodgy claim to political asylum in a sea of tens of thousands of fictitious holders of dodgy political asylum. The government has decided to make us overlook Sacoolas by pretending that there are 23,000 obscure foreigners roaming our country as “diplomats”, each of whom has the license to burgle your home, piss on your floor, kill your daughter and rape your son without facing any possible criminal prosecution or comeback. If this were true, it would be a catastrophic and alarming state of affairs. Thankfully it is a great morass of fiction the government has created within which to try and bury Sacoolas.

This fake “diplomatic immunity” needs to be challenged in court, but I am not sure anyone except Harry Dunn’s family has the locus to do this. Their son was killed by the wife of a spy and to avoid political embarrassment about his activities, the government has falsely connived at a status of diplomatic immunity and then pretended to be trying to get Mrs Sacoolas back. That is an awful lot to take in for people in a terrible state of grief. After losing a son, the cognitive dissonance involved in uncovering state secrets, and learning that the state is malevolent and senior ministerial office holders are liars, is a huge hurdle to surmount. The Dunn family have first to summon the will to fight it, and then to avoid the attempts to hug them in the suffocating embrace of an establishment lawyer – believe me the powers that be will be covertly thrusting one at them – who will advise them they are most likely to make progress if they rock no boats.

The only people I know of who effectively enjoy secret diplomatic immunity are spies from CIA/NSA like Jonathon Sacoolas or from Mossad like Shai Masot. There are not any other categories of pretend diplomats having immunity, and the elaborate charade to pretend that there are is a nonsense. It must not distract from the fact that the claim that the government can grant US and Israeli intelligence agencies diplomatic immunity at will is a lie. The government is acting illegally here. There is no legislation that covers Raab in allowing Mrs Sacoolas to kill – albeit accidentally – with impunity.

I pray both the government and Mrs Sacoolas will be brought to account. I hope Mr and Mrs Dunn find what peace they can with their loss, and are able to remember with due warmth the eighteen wonderful years that I am sure they had with their son.

* * *

Unlike our adversaries including the Integrity Initiative, the 77th Brigade, Bellingcat, the Atlantic Council and hundreds of other warmongering propaganda operations, Craig’s blog has no source of state, corporate or institutional finance whatsoever. It runs entirely on voluntary subscriptions from its readers – many of whom do not necessarily agree with the every article, but welcome the alternative voice, insider information and debate. Subscriptions to keep Craig’s blog going are gratefully received.

A newly released analysis of waste water in European cities by King’s College London has revealed the massive and unmatched scale of London’s cocaine addiction.

As Statista’s Martin Armstrong reports, an estimated 23 kilograms of the illicit drug is consumed in the UK capital – more than Barcelona, Amsterdam and Berlin combined.

Reporting by Sky News indicates that this level of usage equates to 567,445 doses every day and an estimated street value of £2.75m.

Unlike other cities included in the research, Dr Leon Barron, forensic scientist at King’s College London, said that “sustained cocaine usage across the week” was observed in London, with only “a slight rise at the weekend”, adding: “cocaine is an everyday drug in London”.

This article posits that there is an unpleasant conjunction of events beginning to undermine government finances in advanced nations. They combine the arrival of a long-term trend of rising welfare commitments with an increasing certainty of a global-scale credit crisis, in turn the outcome of a combination of the peak of the credit cycle and increasing trade protectionism. We see the latter already undermining the global economy, catching both governments and investors unexpectedly.

Few observers seem aware that an economic and systemic crisis will occur at a time when government finances are already precarious. However, the consequences are unthinkable for the authorities, and for this reason it is certain such a downturn will lead to a substantial increase in monetary inflation. The scale of the problem needs to be grasped in order to assess how destructive it will be for government finances and ultimately state-issued currencies.

Introduction

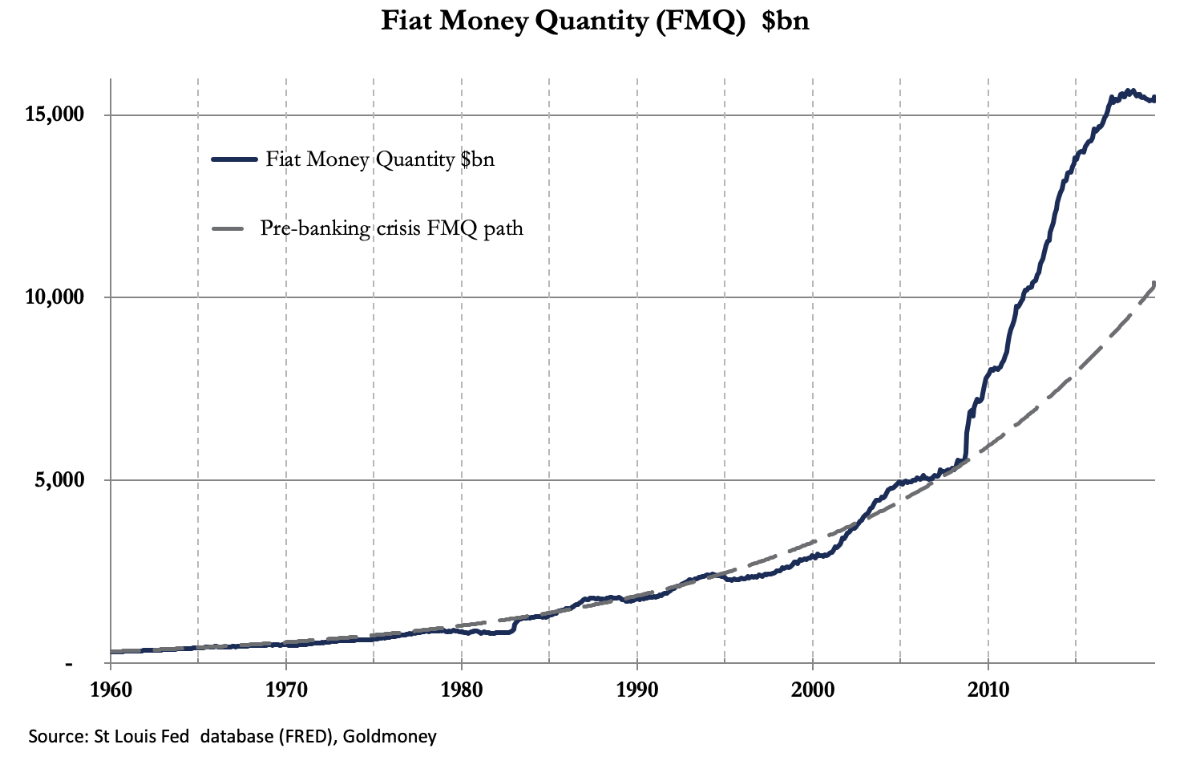

Listening to recent commentaries about the repo failures in New York leads one to suppose there is insufficient money in the system. This is not the real issue, as the chart below of the fiat money quantity for the dollar clearly shows.

The fiat money quantity is the amount of fiat money (in this case US dollars) both in circulation and held in reserve on the central bank’s balance sheet. Before the Lehman crisis, it grew at a fairly constant compound growth rate of 5.86%. Since the Lehman crisis, it has grown at an average of 9.45%, even after the slowdown in its rate of growth that started in January 2017. FMQ is still $5 trillion above where it would have been today if the massive monetary expansion in the wake of the Lehman crisis had not happened. If there is a shortage of money, it is because the process of debt creation to fund current expenditure is spiralling out of control.

It is not just the US. If we take similar (but less detailed) figures for FMQ in other major nations by adding together broad money M3 and central bank balance sheets, we find that it has increased at varying rates for the most important economies. In China, the compound annual growth rate has been 12%, though the growth in Japan at 5.2% and in the Eurozone at 4.9%. has been more subdued, reflecting stagnant levels of bank credit. When for the lack of any other measure statisticians use a GDP money total as a substitute for defining economic progress, we should not be surprised to see that the economies with the greatest rate of monetary growth are reckoned to be the best performing.

Just as GDP tells us nothing about human progress and its benefits to society, other uses of money as a control mechanism for economic management are equally misleading. Much of the monetary expansion has been to fund unproductive government spending. Most of the balance after the government’s cut has fuelled speculation in the financial sector and has funded consumer credit for those whose savings have been tapped out. Not revealed by the acceleration of money supply growth is the wealth transfer effect which impoverishes every productive individual for the benefit of governments, the banking system and the bank’s favoured customers, who are in the main large corporates and directly or indirectly the hedge funds.

Decades of impoverishment by monetary inflation, which has quickened since Lehman, is a very serious matter and is behind the fragility of economic systems dominated by government spending deficits. The reason there appears to be not enough money is because the acceleration of government liabilities in nominal currency terms is catching up with them. Laurence Kotlikoff’s famous 2012 estimate of the US Government’s future commitments of a net present value of over $222bn is very much alive on arrival.

It would be more accurate to say the figure for the US is trending towards infinity. It is already infinity in Japan and the Eurozone, where negative interest rates and bond yields offer the basis for the net present value calculation. As in most things financial, the public is blissfully unaware of the true implications of low and negative interest rates and ultra-low bond yields. They take the view that very low interest rates permit their government to borrow as much as it likes to provide the public with new hospitals, schools and the like. It is a case of fools of politicians and central bankers having turned everyone else into fools, and the few who realise it have no idea how to reverse the process. What they do not see is the government cannot now fund public healthcare and pensions, which make up the bulk of future obligations in a welfare state, without accelerating monetary debasement even more.

No one can know what the true figure is for future government liabilities, of which welfare is an increasing component. Politicians, who claim that a week in politics is the long term, fail to see any problem. The few governments which have raised retirement ages have done so to deal with escalating current welfare liabilities, not addressing those of the future that will lead ultimately to the destruction of what as Westerners we generally agree is civilised democratic society. That is their successors’ problem.

If history and reasoned economic theory is any guide, the demands for credit by the state will terminate in the destruction of government currencies. For the truth of the matter is inflation of money and credit has created the illusion we can all live beyond our income, our income being what we produce.

Nothing, with the sole exceptions of a central bank and its commercial charges can make money without having to advertise for it: the seigniorage is simply taken without public consent. Without questioning how it arises, the extra money allows us to indulge in all our flights of fancy until at some time reality strikes. Rather like Monty Python’s glutton, Mr Creosote, can we force in a little more inflation before we all explode?

The credit cycle is now on the turn

The complaint that the current precarious position faced by major economies is due to a shortage of money is untrue. The problem is one of escalating expenditures, and anyway, the response to any shortage, as we saw recently with problems in the US repo market, is simply to issue more money. But it is no solution, only making the eventual crisis worse.

It is easy to increase the quantity of money, but virtually impossible to increase the quantity of goods to accompany it. For this reason, increases in the quantity of money disadvantage ordinary people, the everyday producers of goods and services in small and medium sized enterprises. And with more money in circulation but the same quantity of goods, the pressure mounts for prices to rise. For a time, consumers can escape price rises by substituting cheaper goods from abroad. This reduces the impact of price rises in the domestic market. Savers are also beneficial for price stability, because they defer their purchases to a future date. But in the absence of savers taking the steam out of inflation-fuelled demand, and contemporary American tariffs on Chinese imports designed to limit them by erasing the price advantage handed to China by America’s monetary inflation, the effect is bound to raise the general level of prices.

Consequently, legacy businesses in America have hoped for a bonanza through not being forced to compete with China. For too long, they have seen the costs of production rise, driven by rising input costs, government regulations, their own expanding bureaucracies, and the natural tendency for expenditure to rise towards the income available. Having been bound hand and foot by red tape they hope that tariffs will protect them from foreign competitors who are not. They maintain their higher uncompetitive prices only to find that consumers, who have not had the benefit of the new free money, are not prepared to pay them or are unable to afford them. Sales volumes suffer and losses begin to accumulate. An international problem provoked by trade protectionism becomes a domestic setback, which is the transition currently hitting the US economy.

We already see the evidence of a developing slump as well in other countries, not directly involved in the trade spat between China and America, but also dependent on the world’s two largest nations measured by trade engaged in their trade war. The member states of the Eurozone are all reporting disappointing internal trade conditions, as are virtually all other nations which report them. The solution, the inflationists say, is more money.

It is a call that has even evolved into a demand that borrowers should be paid to borrow through negative interest rates, killing off the few savers left in the advanced economies. The source for the investment in production deemed necessary to keep the world’s economy from crashing is no longer backed by genuine savings, but by increasing quantities of money conjured out of thin air directly or indirectly by the banking system.

Those that benefit from inflation by expansion of bank credit are those who do not need it, because they are creditworthy and can always raise funds in the market. The problem lies with those who are not creditworthy. No amount of monetary inflation will rescue them, because the banks, in America for instance, have already loaned almost all of the equivalent of their own capital to non-financial borrowers who are deemed to be less than investment grade, in other words junk, both directly and through collateralised loan obligations. In the coming months, or it might even be just a matter of weeks, the banks will protect themselves by turning from providers of liquidity to withdrawing it. Inevitably, a volte-face on credit by the banks will bring on the slump. A systemic crisis will then ensue, and central banks will be forced to ride to the rescue by printing yet more money.

As we saw following the Lehman crisis, the money will be printed to bolster banks’ reserves in return for government debt accumulating at the central bank, so most of that newly printed money ends up covering the government’s deficit through the purchase of government bonds by the central bank.

A credit cycle will have completed: the post-Lehman stabilisation, followed by an uncertain recovery, then a return to normality. Normality matures into complacency, with bank credit being expanded in favour of increasingly risky borrowers. The post-credit expansion crash, mirroring Lehman, is now in the making.

It is a repetitive cycle, the consequence of earlier monetary interventions by the central banks. They have been unable to stop themselves. The decision to pull the plug on Lehman, only a second-rank investment bank, nearly brought down the entire global financial system. No central bank can take that risk again. We can be certain the solution to the next credit crisis will be a further acceleration of the production of money and credit with no one in the financial system being allowed to fail. And the expansion of base money directed at bolstering the banks’ balances will predominantly favour the one borrower class left with any financial standing, the governments.

But what we see is two forces joining together to accelerate the demise of state-issued currencies, which at the end of the day are only backed by the faith and credit the public holds in their governments’ finances. The upcoming credit crunch will occur against a background of a rapidly increasing burden of welfare liabilities, so dramatically identified by Laurence Kotlikoff seven years ago, and likely to have increased markedly from his alarming estimate.

Inevitably, the prolonged suppression of government bond yields will begin to end, and irrespective of central bank interest rate policies, they will rise as investors realise that adjusted for a more realistic estimate of price inflation than that provided by government statisticians, they are a costly safe haven. Then, government finances will become so visibly out of control that even modern monetary theorists will return to their textbooks to see which bit they failed to understand.

The dawning of monetary inflation on the general public

Today, the public is blissfully unaware of the inexorable trend of monetary debasement while enjoying the continuing benefits of government welfare. Government economists tell them that moderately rising prices, the consequence and justification for expanding the quantity of money and credit, are good for them. And who are they to question the experts?

Fortunately, people pursuing their daily lives usually adapt to the circumstances forced upon them by governments. A targeted two per cent inflation rate of prices is not overtly disruptive, and government statisticians have become skilled at goal-seeking price inflation figures. Everyone’s experience of price inflation is different, so government figures become believable by default. But for some considerable time, increases in peoples’ wages have badly lagged the price rises of their normal purchases, which bear little relation to the composition of governments’ consumer price statistics. Coupled with the financial freedom afforded to them to borrow, they have made up the difference between income and expenditure just like any modern government: by borrowing with little or no intention of repaying.

The cause of the problem people face is the continual destruction of their personal wealth by monetary inflation. It has led to a fundamental difference between the credit cycle today and those earlier described in the textbooks of the Austrian School of economists. Before Keynesianism took hold, investment in production was funded by savings. Those savings have been substantially destroyed. Instead of savings being a cushion against uncertainty, for practical purposes they no longer exist.

There are two consequences that concern us here. The first is that the burden of investment and its continuity now falls entirely on the state and its licenced banks, whose only recourse is yet more monetary expansion. The second is the almost total reliance today’s wage earners place on receiving their monthly salary to survive, with a reported 78% of US workers living pay-check to pay-check. British workers are similarly strapped. They have no means of surviving a credit crisis and the economic consequences that follow. That will be another cost that falls to the government and its central bank to add to already escalating welfare commitments.

It is becoming easy to envision the day that the majority of government spending is financed by inflation and inflationary borrowing, through a combination of falling tax revenues and escalating spending commitments. There is also an imbalance between taxpayers, with a mobile wealthy class bearing the bulk of national tax burdens who can up sticks at any time. The question then arises as to how financial markets will react when the triple conjunction of a credit crisis, sharply increased government deficits, and the long-term escalation of welfare costs, materialise in the public consciousness all at the same time.

Ahead of the next credit crisis, the knowledge that things are not quite right has so far led to a flight to perceived safety: in some countries, investors are even paying to own their government’s debt. In the US, the yield on the 10-year US Treasury bond has declined from 3.2% a year ago to 1.4% today.

As the next credit crisis materialises, perceptions of investment risk are bound to change radically. The imperative to print money at an even faster rate will accompany the trend towards deeper negative interest rates, penalising bank deposits, eliminating residual savers from the system. Consequently, if the Fed makes the mistake of even considering negative interest rates, it will put the whole commodity complex firmly into backwardation from the money side because all commodities are priced in dollars.

We can take anticipation of lower and more widespread negative rates as guaranteed when the credit cycle enters its crisis stage. Last time, everyone was so relieved that life after Lehman’s death continued that they still regarded government debt as the risk-free yardstick for financial investment. It would be foolish for a central bank to think this trick could be pulled a second time. Just imagine how high the fiat money quantity in our introductory chart would be above that long-term pre-Lehman trend line. And just think of the damage to the purchasing power of the dollar and the other major fiat currencies from interest rate policies that are bound to drive deposits towards widespread encashment.

This time, the coincidence of a credit crisis and rapidly escalating short- and long-term welfare commitments adds a new dimension to the inflation story. Far from rescuing the global economy, the spreading of zero and negative interest rates can be expected to expose the true worth of fiat currencies. Next time is different in another respect: there is a new generation of educated men and women who through cryptocurrencies have learned of the fiat currency fallacy ahead of the event. In the past, nearly everyone learned of it too late. Now, around the world, particularly in America and China millennials could accelerate the ending of fiat money by triggering an early shift out of fiat into cryptos. Bitcoin at a million dollars becomes no longer pure fancy, only don’t forget that a million dollars might not buy you much.

It is not an expected outcome, except by the very few who understand what is happening to money and the built-in escalation of its quantity. These will include growing numbers in the cryptocurrency community and the few who have studied the subject away from the influence of macroeconomists. Hopefully, they will now include readers of this article.

Anticipating a crack-up boom

As the credit crisis drives monetary expansion into overdrive or leads into a hyperinflationary slump, people are bound to begin to discard their national currencies in favour of any goods they think they might need in future. Minimal cash liquidity becomes the desired position. It can rapidly lead into the final short-lived boom that marks the death of an unbacked fiat currency, when it dawns on the general public that their government’s currency might be worthless. As the conviction of it grows, the pace at which it is dumped for anything of use that they can get their hands on increases exponentially. In Germany, it lasted from about May 1923 until the following November when the mark finally expired.

It has long been a theme of survivalist libertarians that this will occur.

So long as the alternative of owning physical gold and silver exists, it is not necessary to stockpile necessities, unless, that is, disruptions to supplies are anticipated. In a slump, the prices of goods will decline measured in sound money. This, after all, was firmly impressed upon Keynesian inflationists by the experience of the early 1930s, when measured in gold substitutes prices of nearly everything fell heavily. When gold and silver became more desirable relative to owning goods, their purchasing power increases while that of fiat currencies declines.

Putting supply considerations to one side, if in the wake of the next credit crisis the economic conditions of the 1930s return, those that use gold and silver as money will see the prices of their consumer staples fall, so there should be no hurry to hoard them.

The People’s Republic of China, which celebrated its 70th anniversary on October 1, is led by the Chinese Communist Party’s General Secretary, President Xi Jinping. In his speeches, Xi often refers to “Qiang Zhong Gwo Meng” (“the Chinese dream“), a code phrase for the era of rejuvenation when China will eventually overtake the United States as the most powerful nation in the world.

Xi claims that China offers the world a different type of rising global leader — a “guiding power.”

Beijing apologists depict China as a non-predatory power, comparing it favorably to Europe’s colonial countries in the past and to today’s United States.

Similarly, the state-controlled Chinese media depict Chinese statecraft as being based on and reflecting ancient Confucian ethics:

Only when things are investigated is knowledge extended; only when knowledge is extended are thoughts sincere; only when thoughts are sincere are minds rectified; only when minds are rectified are the characters of persons cultivated; only when character is cultivated are our families regulated; only when families are regulated are states well governed; only when states are well governed is there peace in the world.

This portrayal is part of China’s traditional self-image as “Jungwo” (the “Middle Kingdom”), a society synonymous with “civilization,” as opposed to the “barbarians” beyond its borders. Such was the impetus for China’s Great Wall: to keep out uncultured barbarians.

In spite of China’s pretense of being a new type of global power, Beijing’s attempt to restore its historical role as a world leader involves ancient Chinese political concepts. Xi’s call for China’s “rejuvenation,” for instance, is a signal to his people that under the leadership of the Communist Party, the national humiliations endured during the 19th and 20th centuries will be redressed.

Xi’s nationalist sentiment echoes the ideas of Sun Yat-sen, the “founding father” and first president of the Chinese Republic. Sun called for the embrace of “Min-ts’u” (“people’s nationalism”) to redeem the nation from its status as a “hypo-colony” ruled by many colonial masters, including tiny Portugal, which dominated the South China Sea.

Xi’s doctrine includes rejecting as illegitimate any “unequal treaties” forced on China by Euro-Atlantic powers, such as Great Britain’s imposition of the McMahon Line, which awarded to the British Crown Colony of India hundreds of thousands of square kilometers of Chinese territory. China never recognized the McMahon Line; it was among the factors ultimately leading to an India-China War in 1962 and periodic skirmishes ever since.

This determination to retrieve Chinese territory might be rooted in Xi’s sense of humiliation, still felt among Chinese patriots of all political persuasions, who harbor an enduring resentment over such Euro-Atlantic encroachment.

Xi’s posture is also possibly an indirect warning to the West, which may be harboring a desire to assist the people of Hong Kong in their drive for more autonomy from Beijing. This warning underscores the willingness of the Chinese Communist leadership to engage the United States in a limited military conflict, should the US support Hong Kong’s or Taiwan’s official independence from China or if it positions offensive strategic-weapons systems on those lands.

In his essay, “If You Want Peace Prepare for War” — using the famous quote from the ancient Roman strategist, Publius Flavius Renatus — Chinese author Li Mingfu states that if the US attempts to block the Chinese Motherland’s unification with Taiwan, China is ready militarily to force unification.

There can be little doubt that Xi’s China is deeply committed to the retrieval of Formosa (Taiwan) as an integral part of the Chinese patrimony. Historically, China risked war with Japan after Japanese expeditions to the island province. China also has resisted past attempts by Britain to weaken its hold on Tibet. Moreover, despite fierce resistance to Russia’s 19th century invasions in the northwestern province of Xinjiang (Sinkiang), China lost control of the region. That event also might help to explain for China’s willingness to invite universal condemnation for its massive human-rights violations against the region’s Uighur Muslim population, rather than risk again losing control of the province to Islamist independence movements.

Chinese military exercises, new weapons systems and the surreptitious militarization of several landfill and disputed islands in the South China Sea, all indicate that Beijing intends to become — at the very least — East Asia’s dominant regional power, thereby supplanting the US as the pre-eminent authority in the Western Pacific Ocean. According to one American analyst on Chinese military affairs, in 2018 alone, China conducted approximately 100 military exercises with 17 countries.

In recent years, the Chinese Navy has been demonstrating better precision targeting by its anti-ship missile system, the presumed targets being US aircraft carriers. The Chinese Air Force now utilizes runways built on some of the disputed islands, and has also landed heavy bombers there.

In addition, the Chinese also have deployed anti-ship missiles and jet fighter planes on disputed islands. These developments suggest that in the event of a crisis or conflict with the West and its Asian allies, the Chinese Communist Party’s Military Commission is planning to leapfrog any possible Free World strategy to confine China’s naval and air assets to the Chinese mainland.

China’s economic model, according to which a socialist regime will for the first time surpass the world’s greatest capitalist enterprise, also has historical roots. For millennia, China was the premier power in Asia, if not the world. During that time, China’s diplomacy centered on the “Tributary System,” whereby regional states recognized the superiority of Chinese Civilization.”

Many of China’s neighboring states, such as Annam (Northern Vietnam), Korea and even Japan, for a period, rendered an annual tribute to the Chinese imperial court, acknowledging the imperial dynasty’s august standing under heaven. The emperor’s dynastic administration would in turn provide generous support for compliant neighboring countries. Xi’s Belt and Road Initiative bears some — dubious — resemblance to the tributary system of dynastic China. This initiative has China providing the income and expertise to build the logistical infrastructure of a recipient nation, which in turn imports Chinese goods and services employing that new infrastructure. Worse, however, China lends countries money; then when the country cannot repay the debt, China helps itself to resources or infrastructure or whatever, in a “debt-trap.”

To date, it appears that the strategic objective of China to establish regional primacy in the Western Pacific, and possibly in Asia, is militarily, politically and economically achievable. The world, however, is no longer under any illusions about China’s acquisitive intent.

US President Donald J. Trump also indicated recently — during his September 24 address to the UN General Assembly — that America harbors no illusions about China’s unbridled ambitions.

Trump said, in part:

“In 2001, China was admitted to the World Trade Organization. Our leaders then argued that this decision would compel China to liberalize its economy and strengthen protections to provide things that were unacceptable to us, and for private property and for the rule of law. Two decades later, this theory has been tested and proven completely wrong.

“Not only has China declined to adopt promised reforms, it has embraced an economic model dependent on massive market barriers, heavy state subsidies, currency manipulation, product dumping, forced technology transfers, and the theft of intellectual property and also trade secrets on a grand scale…

“For years, these abuses were tolerated, ignored, or even encouraged. Globalism exerted a religious pull over past leaders, causing them to ignore their own national interests.

“But as far as America is concerned, those days are over. To confront these unfair practices, I placed massive tariffs on more than $500 billion worth of Chinese-made goods. Already, as a result of these tariffs, supply chains are relocating back to America and to other nations, and billions of dollars are being paid to our Treasury.

“The American people are absolutely committed to restoring balance to our relationship with China. Hopefully, we can reach an agreement that would be beneficial for both countries…

“As we endeavor to stabilize our relationship, we’re also carefully monitoring the situation in Hong Kong. The world fully expects that the Chinese government will honor its binding treaty, made with the British and registered with the United Nations, in which China commits to protect Hong Kong’s freedom, legal system, and democratic ways of life. How China chooses to handle the situation will say a great deal about its role in the world in the future…”

It is imperative for the administration in Washington to continue to exert maximum pressure on Beijing, to prevent China’s hegemonic aims being realized.

* * *

Dr. Lawrence A. Franklin was the Iran Desk Officer for Secretary of Defense Rumsfeld. He also served on active duty with the U.S. Army and as a Colonel in the Air Force Reserve.

{kind=link}

{kind=link}

{kind=link}