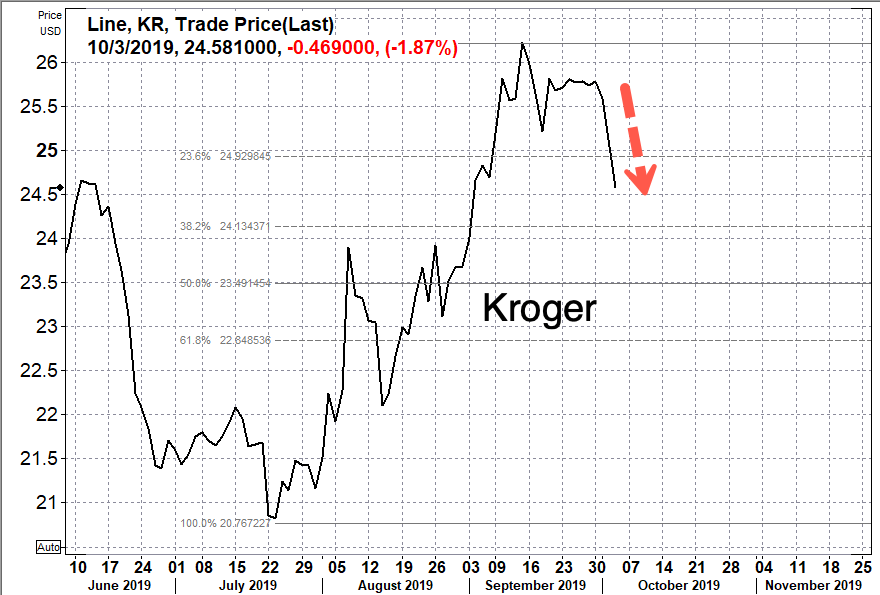

And It Begins: Kroger Lays Off Hundreds Amid Failed Turnaround

Earlier this month, Kroger Co. announced a disappointing 2Q19 earnings call after CEO Rodney McMullen warned that the grocery chain wouldn’t reconfirm its three-year forecast to hit profit targets amid a turnaround effort. As a result, Kroger said this week that it would start the process of laying off hundreds of employees across the family of grocery stores it owns.

“As part of ongoing talent management, many store operating divisions are evaluating middle management roles and team structures with an eye toward keeping resources close to the customer,” a Kroger spokesperson said in a statement. “Store divisions operate independently, but all of them are taking steps to ensure they have the right talent in the right store leadership positions.”

Kroger didn’t specify how many job cuts were anticipated — but sources told CNBC that it’s likely to be in the hundreds.

The company’s turnaround effort is showing signs of distress, and macroeconomic headwinds in the economy could produce a weakening consumer that would contribute to declining retail sales next year.

The grocery chain, which also owns Harris Teeter, Ralphs, Fred Meyer, has 443,000 full-time and part-time employees across its stores as of fiscal 2018.

The layoffs were announced as the company increases technology investments into e-commerce, automation, artificial intelligence, last-mile deliveries, and meal kits. Kroger is trying to stay ahead or at least compete with Amazon and Walmart.

The profit warning earlier this month from McMullen sent shares lower in the last 14 sessions, down nearly 4.5%.

Labor costs continue to be a significant issue for Kroger, as unions continue to gain ground ahead of the 2020 Election, CNBC noted. Kroger, unlike Amazon and Walmart, has a unionized workforce, that has caused tremendous margin compression as the company struggles with unwanted expenses tied to union contracts.

“Our financial results continue to be pressured by inefficient healthcare and pension costs, which some of our competitors do not face,” CFO Gary Millerchip told analysts earlier this month.

Kroger’s failed turnaround into the possibility of a recession in 2020 could result in more job cuts.

The head of Pakistan’s Azad Kashmir said that a small-scale conflict between his country and India-rivals could ignite a nuclear war that would kill hundreds of millions. Kashmir made these comments just days after Prime Minister Imran Khan addressed India with similar rhetoric.

The threat of nuclear war may be upon the globe.

“If a war breaks out between India and Pakistan, it will be quick, dirty and deadly. It will be an Armageddon, hundreds of millions will die in South Asia, and 2.5 billion people will be affected by radiation all over the world,” said Masood Khan, the president of the Pakistani-controlled part of Kashmir, according to a report by RT.

“Even a limited military conflict could evolve into a nuclear war,” said Khan.

Just because other countries wouldn’t be involved in this particular war, the consequences of unleashing a nuclear weapon would have far-reaching effects.

Khan, Pakistan’s former envoy to the United Nations, then struck a milder tone, saying his country is not seeking war, but he wants to predict “a realistic scenario so that international community could intervene and pile pressure on India.”

So basically, Kahn is still asking for violence, just as long as it’s on his side only.

India and Pakistan fought two wars over Kashmir in 1947 and 1965, and have engaged in an array of smaller cross-border skirmishes, most recently this February. At the time, the nuclear-armed neighbors came disturbingly close to full-scale war, but mutual diplomatic efforts and goodwill gestures helped defuse the tensions for a while, reported RT.

Last week, Prime Minister Imran Khan warned that a “bloodbath” was brewing in the disputed territory, and hinted that weapons of mass destruction could be employed against India if war breaks out. The remarks were condemned in New Delhi, with government ministers and pundits accusing him of “warmongering” and “obsession with Kashmir.”

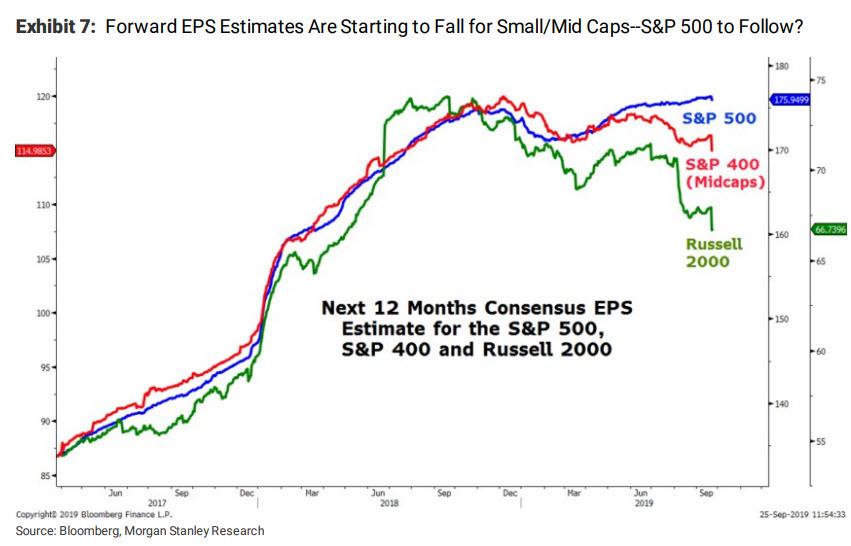

Watch Out Below: Why Earnings Expectations Are About To Plunge

It may come as a surprise to some, but as we first pointed out in late July when Q2 earnings season was peaking, the earnings recession – traditionally a harbinger to the broader, economic recession – is already here as a result of two consecutive quarter of declining earnings Y/Y. And, with Q3 earnings season on deck, its set to get worse.

As Morgan Stanley calculated, S&P 500 y/y EPS growth came in at roughly zero in 1Q and 2Q…

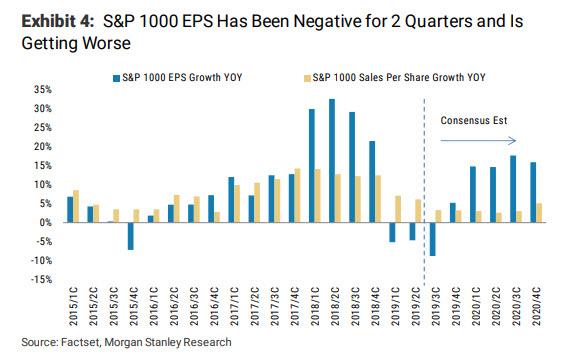

… while the much broader S&P 1000 EPS growth is closer to -6% for 1Q and 2Q.F

Worse, the recession is set to get far worse with consensus now estimating Q3 y/y EPS growth for the S&P 500 will be -4% and S&P 1000 will be closer to -9%. And while some investors have dismissed this as either ‘old news’ or a temporary trough before a reacceleration, the problem with that argument, in the view of Morgan Stanley’s Michael Wilson, is that the same one was proposed in April and then again in July, “yet 3Q EPS growth estimates are now lower than 2Q and 4Q looks vulnerable to further revisions.“

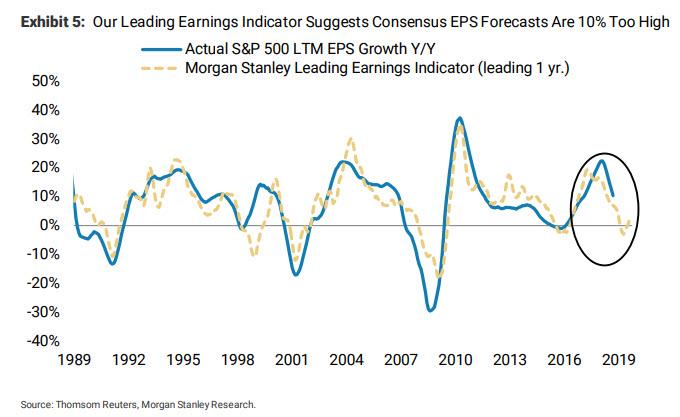

And yet, as Wilson pointed out, “the S&P 500 seems not to care either and so we have to acknowledge that perhaps the market knows something we do not.” To this, the Morgan Stanley strategist counters that the market is once again blissfully complacent, and his own earnings model has proven to be accurate this year, and over time, and is still indicating that next year’s consensus estimates of $181 are about 10 percent too high.

Wilson’s take: it is “hard to believe the market won’t care if next year’s EPS potentially falls $20 over the next few quarters.“

Sarcasm aside, of course the market will care, unless the Fed finds some way to boost P/E multiples by 2-3 additional turns (coughQE4cough). Alternatively, perhaps the market has some uncanny ability to see the future better than the most accurate sellside strategist of 2018. While Wilson briefly considers this possibility, he then quickly dismisses it noting that one key market limitation is that “it has a difficult time thinking beyond 12 months.”

This is also why the MS equity team uses next 12 months EPS rather than calendar year forecasts when looking at valuations; the bank explains that it has found this time period to have the highest efficacy to predicting stock prices, but herein lies a problem, too: “Over the past 20 years, we believe the investment community has become over reliant on company guidance for its earnings forecasts. Therefore, earnings forecasts tend to be more tightly clustered today for the time periods for which there is “company guidance.”

But most companies don’t provide guidance beyond their current fiscal year, which means the following year tends to be an extension of the longer term averages and/or current trends, which is where we find ourselves today.

Indeed, as we have moved through 2019 and watched earnings guidance drop every quarter, the estimates have followed… “but the numbers haven’t changed as much for2020 because companies don’t guide that far out, leaving 2020 estimates unrealistic.“

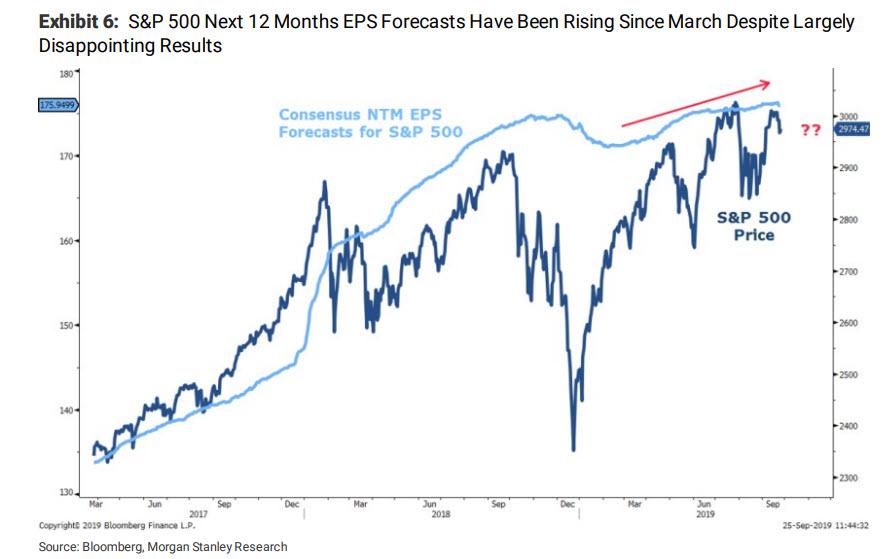

As a result, today consensus bottom up forecasts 10.4% EPS growth for the S&P 500, allowing the forward 12 months EPS to remain flat and even rise this year as we have gone forward in time. According to Wilson, “it is very unusual for the index to sell off much when next 12 months EPS is rising, as it has been this year. Quite frankly, this was a bit of a miss on our part as we just assumed these numbers would follow the 2019 cuts, but they haven’t.”

Why is thie relevant? Because as Wilson concludes, the trend in forward EPS forecasts is about to turn down again, much like it did last fall, for three reasons:

First, this is the time of the year when companies may have to give up any furtherexpectation of a rebound for the year if it has not emerged yet. As a reminder, the second half of 2019 is when many companies expected we would see an earnings recovery; instead this has failed to materialize and another disappointing quarter of results and guidance would seal the deal on 2019.

But what about 2020? While most companies likely will not guide on 2020 until January, some will start to lower the bar if they know it is unachievable to avoid further disappointment, particularly if stocks fall on bad earnings results.

Finally, and perhaps more importantly, we ares tarting to see the forward estimates come down now for the mid caps and small caps which have been leading the S&P 500 lower in this earnings recession (chart below). It is also worth pointing out that small / mid caps have underperformed materially this year which makes sense given the material deterioration in NTM EPS that has been going on all year.

The bottom line on the deteriorating earnings recession is that according to Morgan Stanley, the market (at the index level) has generally ignored the poor results to date simply because the 12 month forecasts have yet to fall. This is largely a technical issue related to stale 2020 estimates that will soon be cleaned up as we go through October and November, much like lastyear.

That, as Michael Wilson concludes, “should put downward pressure on the index like it has for the small and mid cap indices all year”, and lead to the S&P swinging from trading near Morgan Stanley’s upper price target band…

Pity the guys now running the Fed. They’ve inherited an economy that requires ever-bigger infusions of new credit and ever-lower interest rates to avoid financial cardiac arrest. But with interest rates already perilously close to zero the usual leeway is no longer there.

Making the best of a bad hand, Fed chair Jerome Powell has been cutting the Fed Funds rate but managing expectations for future cuts by calling the current ones “recalibration” and “insurance.” In other words, “don’t expect a quick excursion into steeply-negative territory. In fact this latest cut might be all there is.”

But the economy, like any addict, is profoundly uncomfortable with not knowing where the next fix is coming from and is behaving accordingly. From just the past couple of days’ headlines:

What happens next? Almost certainly, a “coordinated” round of aggressive easing by the US Fed, the ECB and BoJ. With some unconventional coercion thrown in by the People’s Bank of China.

As for the timing, it’s just a question of “the number.”

That is, how far does the S&P 500 have to fall before the stampede begins. Since this question will be answered by a bunch of largely clueless men dripping fear sweat and trying to figure out why their models have stopped working (and more poignantly why their life’s work has turned out to be a fraud), the number is unknowable in advance.

But it probably won’t take too many more days like the last couple before the Fed issues its “whatever it takes” statement, cuts rates by a half-point or more, and initiates a QE program that includes equities along with bonds.

Oh, and before a US-China trade deal is signed that accomplishes little but is sold as “historic” and “huge.”

And before a trillion-dollar infrastructure plan passes both houses of Congress with bi-partisan support.

Stocks will of course pop on these announcements, which makes the “short everything in sight” impulse less than the sure thing it appears. But the initial upward thrust won’t hold because there are limits to both how far interest rates can fall and how big central bank balance sheets can become before even the pretense of capitalist free markets evaporates. We don’t know what those limits are but they’re definitely out there.

Source: Bloomberg

Put another way, an economy that has been LBO-ed by its government is no economy at all.

NK Tests Sub-Launched Ballistic Missile In Show Of “Second-Strike Capability”

North Korea has confirmed a new successful missile launch on Wednesday, which notably involved its first submarine-launched ballistic missile (SLBM) in three years, and a new type of “vertical mode” ballistic missile.

The test was “to contain external threats and bolster self-defense” as Reuters reports, and comes just two days ahead of working level talks with the United States in Stockholm, Sweden at the end of this week.

Photo of the launch in the official NK newspaper Rodong Sinmun.

State news agency KCNA hailed the “successful” test as of “great significance” as it marks a “new phase” in defending North Korea from the threat of “outside forces” via a “new-type ballistic missile fired in vertical mode” in waters off Wonsan Bay.

There’s little doubt that the tests are meant to give Pyongyang some last minute leverage just before heading into talks with Washington.

The United States and North Korea will begin working level talks in Stockholm, Sweden beginning tomorrow, Friday Oct 4, according a source with knowledge of the plans. The chief negotiator from the North Korean side will be the DPRK’s former ambassador to Vietnam, Kim Myong Gil.

Noting the crucial timing of the SLMB test, The Guardian reports the following:

Ankit Panda of the Federation of American Scientists described the missile, the Pukguksong-3, as Pyongyang’s longest-range-capable solid-fuel missile, adding that Wednesday’s launch was “unambiguously the first nuclear-capable missile test since November 2017”.

“Kim Jong Un’s ‘rocket men’ kept busy during the diplomatic charm offensives of 2018-2019,” Panda added.

Analysts believe it was likely launched from a special underwater platform designed for the test, or possibly from a submarine.

Wednesday’s SLMB launch, via KCNA/Reuters

The ability to launch SLMBs from submarines or from anywhere in the water gives the north a “second-strike capability”. If its bases or cities come under attack, it can rely on its underwater arsenal, which is considered much harder for other nations’ defenses to detect.

Meanwhile, South Korea’s military described that Wednesday’s test involved the missile traveling about 450km in an easterly direction and reaching an altitude of 910km.

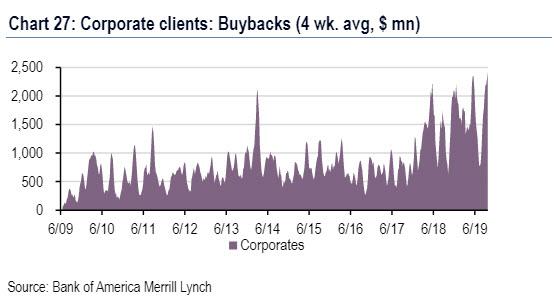

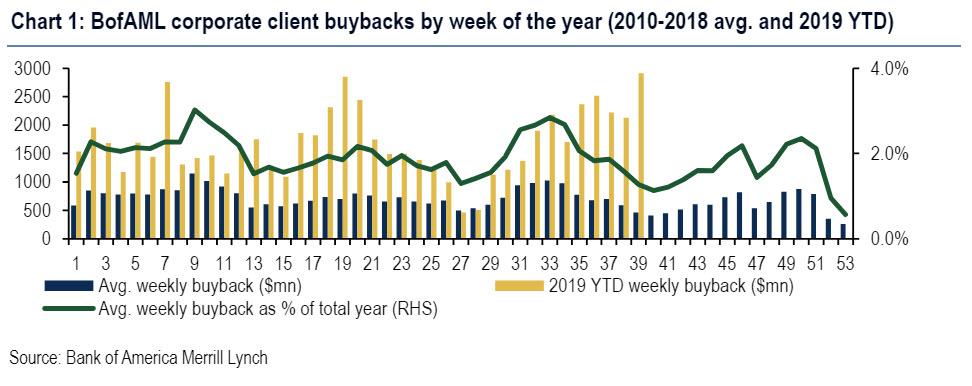

Corporate Buybacks Accelerate To Strongest Weekly Level In History

When it comes to politics, one thing is certain: it is all about fake news, and how it is spun. Which is why some people prefer finance: after all, when it comes to math-based financial data, reality is either a 1 or a 0.

Unfortunately, it now turns out that even financial “data” can mean whatever one wishes to read from it. Case in point: today’s CNBC appearance by Goldman’s chief equity strategist David Kostin, who when commenting on the fate of the market in the context of trade war, warned that stock buybacks – the primary driver of stock upside together with the Fed in the past decade – “are getting muted” (1’40” in the clip below) and thus clients are turning cautious.

There is just one problem with Kostin’s statement: it is dead wrong, at least according to the latest buyback data from Bank of America’s trading desk.

As BofA’s Jill Carey Hall writes in her latest client flow trends, “corporate buybacks accelerated to their strongest weekly level in our data history since 2009″, led by Tech buybacks for the fifth week. This is in line with BofA’s expectations, which had predicted that tech would benefit from a ramp up in buybacks YTD given the high announced/completed buyback ratio for the sector heading into the year.

As a result of this burst in stock repurchases, cumulative YTD buybacks are now +25% YoY, with 3Q to date buybacks +39% YoY and stronger than normal seasonal trends (which typically slow through late Sept, and pick up over the next ~6 weeks amid earnings season).

In other words, far from “muted” – as Goldman claims- stock buybacks heading into the Q3 blackout period have been bigger.

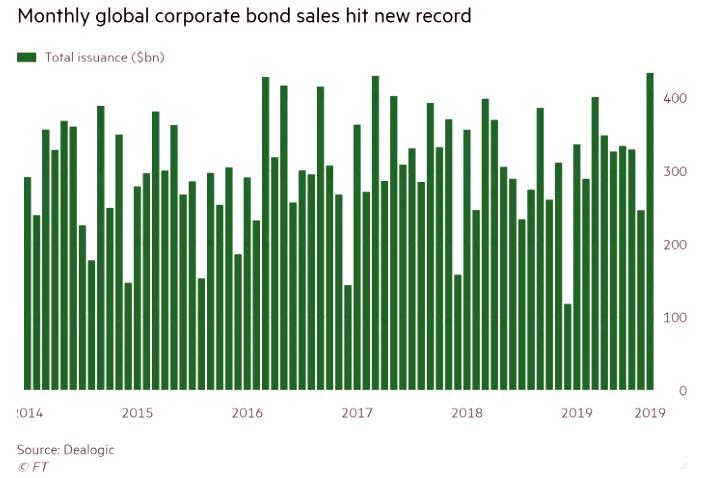

But why did buybacks just soar to an all time high? After all, isn’t it naive and foollish to launch a record stock repurchase program with the S&P at all time highs? Well, no, when the one paying for it is the greatest fool of all – the yield-starved corporate bond investor. Recall that September saw a record monthly corporate bond issuance, with some $434 billion in bonds sold globally, $5 billion more than the previous all time high of March 2017.

And since a substantial portion of the proceeds is used for stock buybacks, it should not come as a surprise that we just saw a record week for stock buybacks… and why stocks are surging today even as both PMIs now suggest the US is headed for a recession.

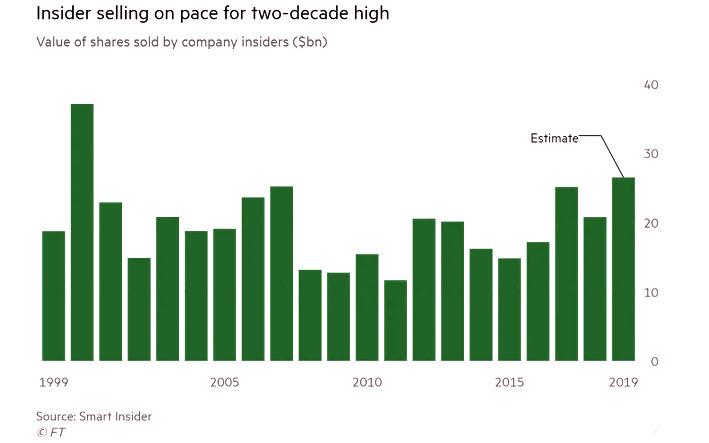

But if companies are buying every share of their stock they can find – with no price discrimination – who are the sellers? We know that answer too: as we reported a week ago, corporate insiders – typically CEOs, CFOs, and board members, but also venture capital and other early state investors – sold a combined $19BN of stock in their companies through to mid-September. Annualized, on track to hit $26BN for the year, which would mark the most active year for insider sales since 2000, when executives sold $37bn of stock amid the idiotic frenzy of the first tech bubble. That 2019 total would also set a post-crisis high, eclipsing the $25bn of stock sold in 2017.

Finally, as for Goldman once again completely misrepresenting reality and peddling “fake news”, we hope that by now that comes as no surprise to any of our regular readers.

Liberal film director Michael Moore – who called Trump’s 2016 victory (and may have inadvertently contributed to it), says that former Vice President Joe Biden is “this year’s Hillary.”

During an interview with MSNBC this week, the “Fahrenheit 11/9” director called out Biden for saying he “never” discussed his son’s business dealings in Ukraine, while in a different interview saying they had spoken a few times.

“Joe Biden is not going to excite the base to get out there and vote on Nov. 3, 2020,” Moore added. “The things that he said publicly are very strong … “But it looks like he’s not really wanting to deal with it. He’s afraid to be out there.”

Moore’s suggestion? “We need all the candidates right now — need to be unified and coming at this full force. No backing down and no trying to placate the other and none of this, ‘Well we have to wait and see.’”

Moore was one of the few liberal personalities to predict Donald Trump would win the presidential election in 2016 — and claimed earlier on that Biden would be the one to overtake Trump in a presidential race.

He still believes that — but feels the former vice president needs to take a stronger stance on the allegations against the Biden family in order to motivate people to come out and “vote against Trump.”

The heat is on Joe Biden’s son, Hunter Biden, following Trump’s and others’ accusations that the two Biden men were in some way involved in corruption connected to Burisma Holdings, the Ukranian natural gas company on whose board Hunter Biden sat (and pulled in $50,000 a month for doing so though he had no experience in this area of business). –The Political Insider

Perhaps Moore will make another campaign ad for Trump this time around?

“What’s in a name? That which we call a rose, By any other name would smell as sweet.”

– Juliet Capulet in Romeo and Juliet by William Shakespeare

Burgeoning Problem

The short-term repo funding turmoil that cropped up in mid-September continues to be discussed at length. The Federal Reserve quickly addressed soaring overnight funding costs through a special repo financing facility not used since the Great Financial Crisis (GFC). The re-introduction of repo facilities has, thus far, resolved the matter. It remains interesting that so many articles are being written about the problem, including our own. The on-going concern stems from the fact that the world’s most powerful central bank briefly lost control over the one rate they must control.

What seems clear is the Fed measures to calm funding markets, although superficially effective, may not address a bigger underlying set of issues that could reappear. The on-going media attention to such a banal and technical topic could be indicative of deeper problems. People who understand both the complexities and importance of these matters, frankly, are still wringing their hands. The Fed has applied a tourniquet and gauze to a serious wound, but permanent medical attention is still desperately needed.

The Fed is in a difficult position. As discussed in Who Could Have Known – What the Repo Fiasco Entails, they are using temporary tools that require daily and increasingly larger efforts to assuage the problem. Taking more drastic and permanent steps would result in an aggressive easing of monetary policy at a time when the U.S. economy is relatively strong and stable, and such policy is not warranted in our opinion. Such measures could incite the most underrated of all threats, inflationary pressures.

Hamstrung

The Fed is hamstrung by an economy that has enjoyed low interest rates and stimulative fiscal policy and is the strongest in the developed world. By all appearances, the U.S. is also running at full employment. At the same time, they have a hostile President sniping at them to ease policy dramatically and the Federal Reserve board itself has rarely seen internal dissension of the kind recently observed. The current fundamental and political environment is challenging, to be kind.

Two main alternatives to resolve the funding issue are:

More aggressive interest rate cuts to steepen the yield curve and relieve the banks of the negative carry in holding Treasury notes and bonds

Re-initiating quantitative easing (QE) by having the Fed buy Treasury and mortgage-backed securities from primary dealers to re-liquefy the system

Others are putting forth their perspectives on the matter, but the only real “permanent” solution is the second option, re-expanding the Fed balance sheet through QE. The Fed is painted into a financial corner since there is no fundamental justification (remember “we are data-dependent”) for such an action. Further, Powell, when asked, said they would not take monetary policy actions to address the short-term temporary spike in funding. Whether Powell likes it or not, not taking such an action might force the need to take that very same action, and it may come too late.

Advice from Those That Caused the Problem

There was an article recently written by a former Fed official now employed by a major hedge fund manager.

Brian Sack is a Director of Global Economics at the D.E. Shaw Group, a hedge fund conglomerate with over $40 billion under management. Prior to joining D.E. Shaw, Sack was head of the New York Federal Reserve Markets Group and manager of the System Open Market Account (SOMA) for the Federal Open Market Committee (FOMC). He also served as a special advisor on monetary policy to President Obama while at the New York Fed.

Sack, along with Joseph Gagnon, another ex-Fed employee and currently a senior fellow at the Peterson Institute for International Economics, argue in their paper LINK that the Fed should first promptly establish a standing fixed-rate repo facility and, second, “aim for a higher level of reserves.” Although Sack and Gagnon would not concede that reserves are “low”, they argue that whatever the minimum level of reserves may be in the banking system, the Fed should “steer well clear of it.” Their recommendation is for the Fed to increase the level of reserves by $250 billion over the next two quarters. Furthermore, they argue for continued expansion of the Fed balance sheet as needed thereafter.

What they recommend is monetary policy slavery. No matter what language they use to rationalize and justify such solutions, it is pure pragmatism and expediency. It may solve short-term funding issues for the time being, but it will leave the U.S. economy and its citizens further enslaved to the consequences of runaway debt and the monetary policies designed to support it.

If It Walks and Quacks Like a Duck…

Sack and Gagnon did not give their recommendation a sophisticated name, but neither did they call it “QE.” Simply put, their recommendation is in fact a resumption of QE regardless of what name it is given.

To them it smells as sweet as QE, but the spin of some other name and rationale may be more palatable to the public. By not calling it QE, it may allow the Fed more leeway to do QE without being in a recession or bringing rates to near zero in attempts to avoid becoming a political lightening rod.

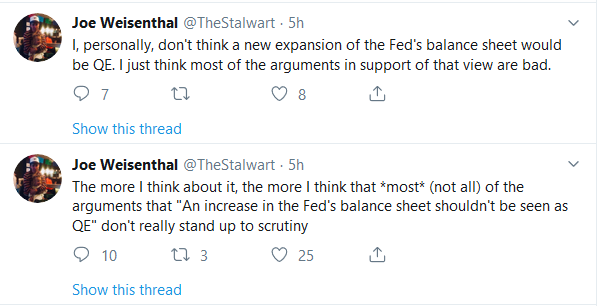

The media appears to be helping with what increasingly looks like a sleight of hand. Joe Weisenthal from Bloomberg proposed the following on Twitter:

To help you form your own opinion let’s look at some facts about QE and balance sheet increases prior to the QE era. From January of 2003 to December of 2007, the Fed’s balance sheet steadily increased by $150 billion, or about $30 billion a year. The new proposal from Sack and Gagnon calls for a $250 billion increase over six months. QE1 lasted six months and increased the Fed’s balance sheet by $265 billion. Maybe its us, but the new proposal appears to be a mirror image of QE.

Summary

The challenge, as we see it, is that these former Fed officials do not realize that the policies they helped create and implement were a big contributor to the financial crisis a decade ago. The ensuing problems the financial system is now enduring are a result of the policies they implemented to address the crisis. Their proposed solutions, regardless of what they call them, are more imprudent policies to address problems caused by imprudent policies since the GFC.

McCarthy Demands ‘Reckless’ Pelosi Suspend Impeachment Inquiry Until She Defines Procedures

House Minority Leader Kevin McCarthy (R-CA) fired off a Thursday letter to House Speaker Nancy Pelosi (D-CA) demanding that she halt the impeachment inquiry into President Trump until she can answer a series of questions defining her game plan for the process.

“As you know, there have been only three prior instances in our nation’s history when the full House has moved to formally investigate whether sufficient grounds exist for the impeachment of a sitting President,” writes McCarthy. “I should hope that if such an extraordinary step were to be contemplated a fourth time it would be conducted with an eye towards fairness, objectivity and impartiality.”

“Unfortunately, you have given no clear indication as to how your impeachment inquiry will proceed – including whether key historical precedents or basic standards of due process will be observed.”

“In addition, the swiftness and recklessness with which you have proceeded has already resulted in committee chairs attempting to limit minority participation in scheduled interviews, calling into question the integrity of such an inquiry.””

READ⬇️ I’ve written to Speaker Pelosi to halt the impeachment inquiry until we can receive public answers to the following questions. Given the enormity of the question at hand—impeaching a duly elected president—the American public deserves fairness and transparency. pic.twitter.com/EFKOghyf9w

McCarthy’s reference to participation refers to reports that House Intelligence Committee Chairman Adam Schiff (D-CA) will limit GOP questions during Thursday’s testimony by former US Ukraine envoy, Kurt Volker.

In his letter to Pelosi, McCarthy asks a number of questions, including whether Pelosi plans to hold a full House vote on authorizing the impeachment inquiry, whether she plans to grant subpoena powers to both the committee chairs and the ranking members, and whether she’ll allow trump’s lawyers to attend the hearings.

After concerns were first raised about an “equal playing field” during the Volker session, Fox News is told Democrats made concessions and agreed to equal representation from Democratic and Republican counsels in the room. However, even though there are representatives from the Intelligence, Oversight and Foreign Affairs Committees, only the Intelligence Committee can ask questions. –Fox News

In response to McCarthy’s letter, President Trump tweeted “Leader McCarthy, we look forward to you soon becoming Speaker of the House. The Do Nothing Dems don’t have a chance!”

Leader McCarthy, we look forward to you soon becoming Speaker of the House. The Do Nothing Dems don’t have a chance! https://t.co/uWPdGJg99F

Pelosi appears to have a poor grasp on what she’s even trying to impeach Trump over – as evidenced by her Wednesday insistance that Rep. Schiff was “using the president’s own words” when he read a fabricated account of a phone call between President Trump and Ukrainian President Volodomyr Zelensky during a hearing last week with the acting director of national intelligence.

Okay what Twilight zone have I entered because this is 2x in one week where @GStephanopoulos called out a Democrat for lying. Here he asks Pelosi about Schiff lying about what’s said in the transcript and correcting her when she says it was Trump’s words. pic.twitter.com/8YrhRNCPJ6

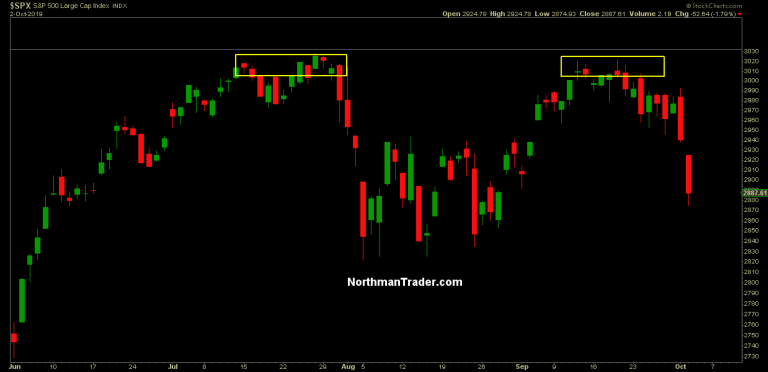

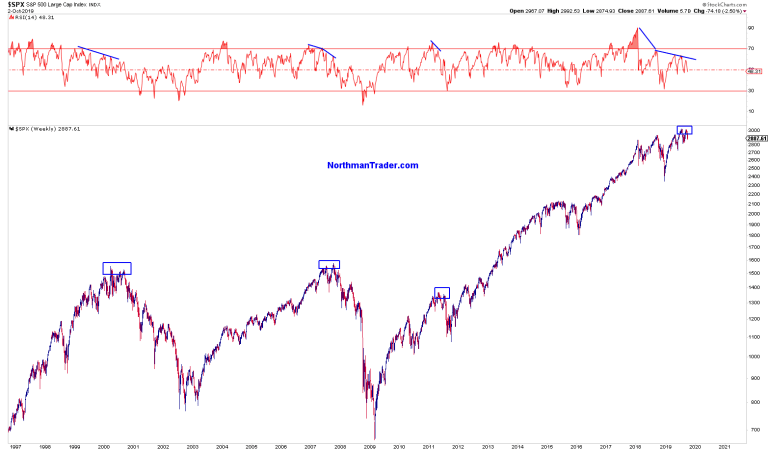

Before you go all “here he goes again” I’m not calling for a double top, I’m highlighting the risk that markets may have made a double top and that has implications.

Let’s explore the evidence, then let’s discuss the risk.

Firstly, a set of plain facts: $SPX made a marginal new all time high in July. 3028 was the peak print. The Fed cut rates in July and markets sold off. Blame trade tensions all you want, but then markets rallied on trade optimism into September, the Fed cut rates again and $SPX peaked at 3022, a slightly lower high, and now has sold off again:

Those are the facts ma’am.

Now is this a confirmed double top? Not necessarily. Get a trade deal and off to the races we go right? What if there’s no trade deal and all you got are regressive earnings? What if the employment cycle is turning? What if the yield curve actually means something? What if decades long trends actually mean something? I’m asking for a friend.

See here’s the thing: Double tops are very rare and when they occur at the end of a business cycle one better pay attention.

But the Fed has our backs, nothing bad happens when the Fed cuts rates right? There won’t be double tops with the Fed cutting rates. Surely.

But we hit 3000+ in July and rejected. We hit 3,000+ in September and rejected. Both rejections have come on Fed rate cuts. What happens when the Fed cuts rates in stocks sell off anyways?

Well, we already know the answer to that question, here’s the $SPX during 2007:

Looks awfully similar to the current $SPX chart doesn’t it?

Funny enough a record high in July followed by a marginal new high in October after the Fed cut rates. That was it. Lights out. Rate cuts did not bring about growth or a rising stock market. The initial instinct was the buy the rate cut, but then it didn’t matter and stocks were sold anyways. For now we see the same thing here and rate cuts are being sold.

But Wall Street is all bullish and says the Fed has our back you say. Yes that was the attitude back then too.

After all in December 2007, with the double top already in place Wall Street projected nothing but new highs for 2008, ignoring the prospect of a double top in place:

A double top was in place and everybody ignored it.

Are they ignoring it again?

Here are famous double tops in recent years:

All have one common characteristic: Negative divergences on new highs or close to new high. In 2000 and 2007 these double tops had especial meaning because they came at the end of a business cycle with unemployment having based at the lows and the yield curve inverted and yields declining.

Sound familiar?

Again, I’m not calling for a double top, I’m highlighting there is risk of one and the only way to invalidate this risk is to make new highs. No new highs and it looks the technical consequences could be dire.

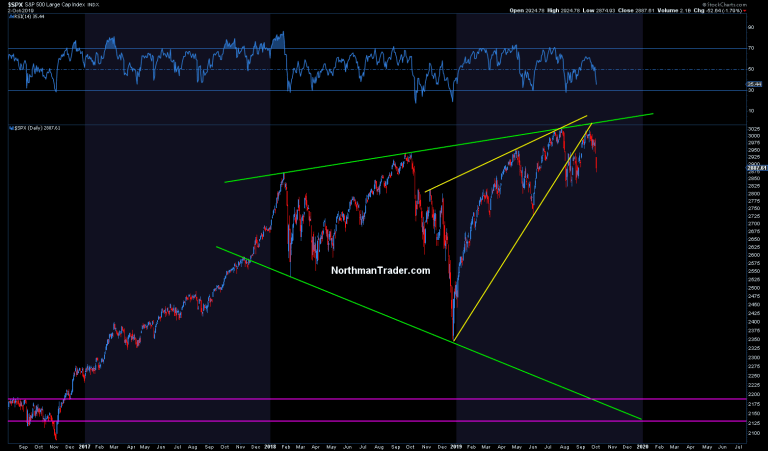

I posted this chart as a warning on September 19 with $SPX at 3006. Yesterday $SPX closed at 2887 confirming the risk of these 3,000 prices a few week ago.

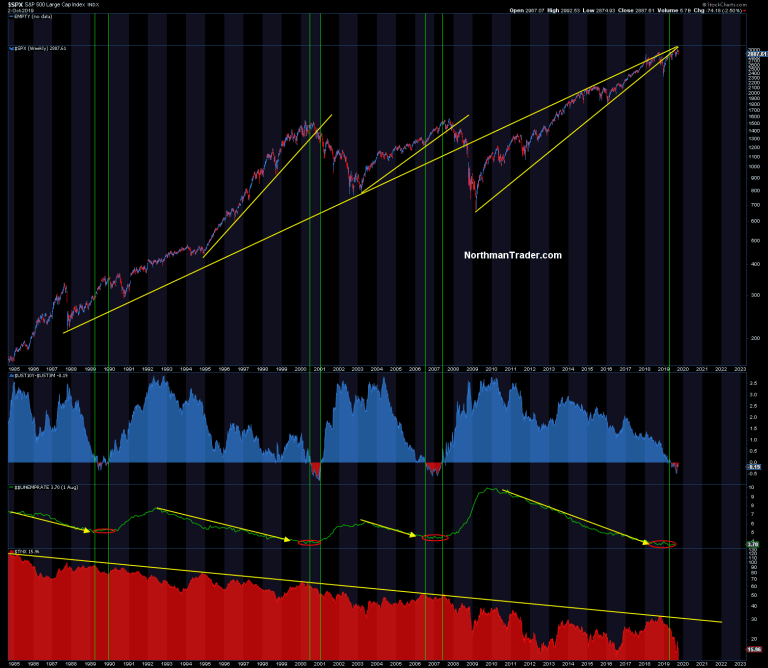

And all this price action is occurring in context of the larger pattern structures we’ve been discussing:

I don’t know why this all being ignored again, but there it is. Megaphone, broken 2019 uptrend and now a potential double top with sell-offs following two rate cuts with a lot of open space below. But ok.

Double tops are only obvious in hindsight and this one remains unconfirmed, but it is a risk for bulls and they need to invalidate it soon. A trade deal may do it and perhaps must do the job as for now the Fed intervening is not showing signs of being able to produce sustained new highs. And yes there will be rallies, but if they fail to produce new highs watch out below.

As I outlined yesterday next week’s trade meeting is shaping up to be critical.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

{kind=link}

{kind=link}