What is your favorite coffee shop or restaurant? Which doctor’s office and dentist do you prefer to go to?

I bet these are all within, say, 15 minutes of your home. That makes sense–who wants to drive three hours to get coffee, or take a plane to their dentist?

But what about your bank?

If you live in the USA or Europe, chances are, the banks in your neighborhood probably aren’t that great.

Europe in particular has a lot of problems; according to the European Banking Authority (one of the EU’s biggest financial regulators), the largest banks in Europe collectively lack more than 100 billion euros to meet minimum capital requirements.

And in some countries (like Italy) the banking system is already teetering on the edge of insolvency.

Banks in the US have their own challenges– like constantly abusing their customers’ trust.

Wells Fargo is the poster child for these types of scandals. They sold customers car insurance they didn’t need, and charged erroneous fees which got 20,000 cars repossessed.

A computer glitch once caused over 500 Wells Fargo customers to have their houses foreclosed on.

Wells Fargo illegally repossessed vehicles soldiers who were deployed overseas, and accidentally charged late fees to more than 100,000 customers when it was the bank that was at fault.

Wells Fargo employees also infamously created fake customer accounts in order to hit their sales goals. Other employees were caught selling customers’ social security numbers.

This sort of thievery is sadly commonplace.

Yet for all these risks– all the abuse, the shaky financials, etc., banks pay almost nothing to depositors. You’re lucky to earn half a percent these days, and most checking accounts pay literally zero.

There are additional issues to consider as well–

Especially if you happen to be living in the most litigation-prone, lawyered-up country that has ever existed in the history of the world… a place where frivolous lawsuits abound and horrendous penalties are the norm…

Having some cash outside of your home country is a way to protect a portion of your assets.

These are all reasons why it’s a smart idea to have a bank account at a well-capitalized bank far away from home.

The central idea is that your money should live in the best place in the world where it has the maximum opportunity to be safe and grow. (It’s the same as you would want for your family.)

And most likely, that’s not going to be at the bank across the street.

To be clear, having a foreign bank account has nothing to do with tax savings.

There are plenty of ways to legally reduce your tax burden. Having a foreign bank account is NOT one of them.

And if you’re a US citizen with a foreign bank account (or multiple accounts) worth at least $10,000 at any point last year, you’re required to file a form known as the FBAR.

The FBAR is a disclosure form that the US government requires; they want to keep tabs on your foreign financial assets. Filing is easy. And not filing comes with all sorts of penalties.

Typically the FBAR (officially known as FinCEN Form 114) is due in April when you file your taxes. But the Treasury Department authorized an automatic extension for all filers to October 15th.

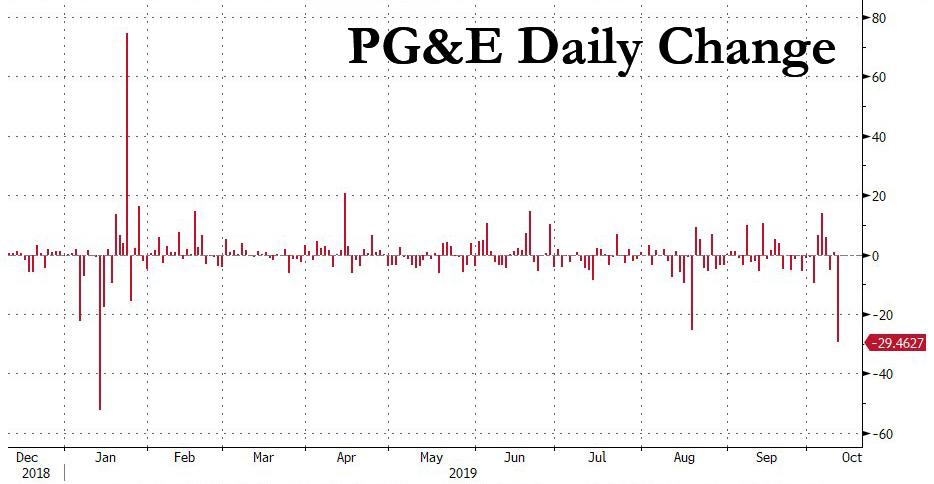

PG&E Plunges Most Since Chapter 11 Filing After Losing Bankruptcy Exclusivity

Things are getting scary for customers of California’s biggest – and bankrupt – utility, PG&E: not only is the state rolling out unprecedented blackouts which threaten to put as many as 3 million California residents in the dark, but overnight U.S. Bankruptcy Judge Dennis Montali stripped PG&E of exclusive control over its recovery process, which threatens to put the fate of the bankrupt power giant in the hands of creditors and outsiders, wiping out the stock in the process.

Immediately after Montali issued his ruling late on Wednesday, PG&E shares crashed as much as 25%. Adding insult to injury, the ruling hit just as PG&E was cutting power to hundreds of thousands of homes and businesses in Northern California in the first phase of an orchestrated shutoff designed to keep its power lines from igniting blazes. The stock reaction was a dramatic wake up call for those PCG BTFDers who were hoping that the equity would be reinstated at a sizable valuation: PCG stock plunged as much as 32%, its biggest one-day drop since the January bankruptcy filing.

The creditors, including the fire victims, have “spoken loudly and clearly that they want their” proposal to be considered, Montali said in his ruling. While PG&E’s plan is “on track as well as can be expected,” he wrote, so is the competing version from creditors. The court also denied requests by other parties to let them offer recovery plans.

Under bankruptcy law, a company has a limited amount of time to develop a reorganization plan and persuade creditors to vote in favor of it. Initially, no other competing proposals are allowed, so the bondholders needed permission from Montali before they could proceed. It’s unusual for a bankruptcy judge to grant such a request.

Montali’s decision to allow bondholders including PIMCO and Elliott Management pitch their own restructuring plan alongside PG&E’s – escalates an already-heated battle for control of the largest utility bankruptcy in U.S. history. According to bankruptcy court, the creditors can now propose their own ways for the utility to deal with an estimated $30 billion in wildfire liabilities. And since, any equity-negative decision is by definition credit-positive, some PG&E bonds soared to their highest levels in almost two years.

As Bloomberg reports, the loss of exclusivity is the latest twist in a massive bankruptcy case that has attracted some of the biggest names in the financial world.

As for the reason why the stock is crashing, it’s because the creditor group led by Pimco and Elliott – which now can propose its own vision for the company – has devised a plan that would wipe out the stake of current shareholders in the utility.

“In the worst case, the competing plan could win and completely wipe out current shareholders,” Greg Gordon, an analyst at Evercore ISI, said in a research note. “In other words, zero is possible.”

Whether shareholders will actually suffer a total wipeout is open to question, because Montali’s ruling doesn’t shut down PG&E’s effort or necessarily favor its rivals.

A shocked PG&E, which is now facing a very uncertain future, issued a statement saying that “we are disappointed that the Bankruptcy Court has opened the door to consideration of a plan designed to unjustly enrich Elliott and the other ad hoc bondholders and seize control of PG&E at a substantial discount.” The company had argued that ending its exclusive control before the company figures out its exact wildfire liabilities would “lead to further distraction, costs and waste” and would jeopardize the company’s chances of exiting bankruptcy by June 2020, a deadline set by the state.

Translation: the world will end if the company’s equityholders are wiped out and the existing management team is shown the door… a typical response.

“It’s a big deal, because now the shape of the reorganization is no longer in existing management’s hands,” said Stephen Lubben of the Seton Hall University School of Law. “Whoever can persuade a critical mass of creditors, along with the regulators, that they have a good way forward will win. That could result in a very different plan than management envisioned when they went into Chapter 11.”

PG&E filed for bankruptcy on Jan. 29 to address liabilities resulting from a series of devastating fires that tore through Northern California in 2017 and 2018. The effects have been rippling through millions of ratepayers, hundreds of creditors, thousands of workers and the state’s political system.

“One plan emerging as confirmable is a very acceptable outcome,” Montali wrote. “And if both plans pass muster, the voters will make their choice or leave the court with the task of picking one of them.” He directed the noteholders to file their plan by Oct. 17.

It’s not the first time the company faced such a dilemma. PG&E’s utility unit filed for bankruptcy in 2001, and in that case, creditors were paid in full and shareholders kept considerable value. This time, however, as a result of mounting legal liabilities, the chances the equity preserves some value are far lower, although as always in a case like this, political considerations come into play.

Regulators and creditors might want to maintain a capital structure of at least 50% equity that’s typical for a utility, which would help PG&E sell new shares and debt. Political and public relations considerations could also emerge if pension funds, workers and individual shareholders with sympathetic stories weigh in.

“This would be devastating for my retirement,” shareholder Andreas Krebs of San Francisco wrote to the judge a day before the ruling. “Please consider the average person that has invested their hard-earned retirement money into PG&E. I don’t even know how to address the greed and gall of these creditors that would want to wipe out average people’s savings in order to profit by taking over PG&E.”

Here’s a thought: perhaps the average person should not have invested their entire nest egg in a terribly run, massively overlevered organization. Then again, in a world in which everyone expects to be bailed out, can anyone blame Andreas for trying?

Putin Planning “Deal Of The Century” Between Syria & Turkey As US Exits

Lebanese Arabic news broadcaster Al-Mayadeen is reporting that Russia has begun organizing “reconciliation talks” between Syria and Turkey, in what would be an unprecedented development, given President Erdogan’s position has long been that Turkey won’t negotiate with Damascus so long as Assad is in power.

The Middle East broadcaster cited Russian Foreign Minister Sergey Lavrov, who said, “Moscow will ask for start of talks between Damascus and Ankara”.

Russia’s TASShas also confirmed the initiative, making it the first significant attempt to bring the two sides to the table, given Ankara severed diplomatic ties with Damascus in 2012. Turkey could indeed be ready given it has finally gotten its way in Syria — with a long planned attack on Syrian Kurds along the border in northern Syria, which began Wednesday with an air and ground offensive.

Previously Ankara had signaled that it would only engage Damascus if it led to Assad being removed from office. But with US troops now largely out of the way, and with Trump signalling that he wants to ultimately bring them all home and let regional powers sort out the aftermath, including the threat of ISIS prisoners in northeast Syria, the final deal-makers that remain are Putin and Erdogan.

“We will be pressing for the beginning of a dialogue between Turkey and Syria. There are reasons to believe that this will meet the interests of both countries. Also, we will be promoting contacts between Damascus and Kurdish organizations that renounce extremism and terrorist methods of activity,” Lavrov said.

“We’ve heard Syrian officials and Kurdish organizations’ representatives say they are interested in Russia using its good relations with all parties to this process for assistance in establishing such a dialogue. We’ll see how to go about this business,” the Russian foreign minister added.

And in a report on Thursday as a ground battle rages between YPG/SDF forces and Turkish-backed proxy ‘rebels’ – backed also by Turkish troops – The Guardian also took note of a potential Putin “deal of the century” to end the war in Syria while ensuring American retreat:

But Putin also wants to see an end to the Syrian civil war. With the US leaving the scene, he may try to forge his own “deal of the century” between Erdoğan, the Syrian regime and the Kurds.

With the US gone from the scene, an acceptable status quo could be reached, which would no doubt involve the Kurds once again coming under Damascus, but with much less autonomy than they hoped for, and with significant security guarantees for Turkey.

Convoy of Syrian National Army (ex-FSA) heading to border at Ceylanpinar – crowds cheering them on pic.twitter.com/kR5xgT3Ci9

At its simplest, the Russian president, Vladmir Putin, who is seeking to embed Russia’s influence across the Middle East, will see a chance to exploit what is viewed as Trump’s betrayal of the Kurds, the US’s bloodied battering ram in the fight against Isis. The lesson is clear: when the crunch comes, the US will not have your back, Putin will argue.

In Lavrov’s Thursday comments, he emphasized this precisely, saying:

“We have been for years warning about an extreme danger of the experiment that the Americans were conducting there, trying to set the Kurds and Arab tribes against each other in every possible way. We were warning against playing the Kurdish card, as this can come to no good, of which we were also warned by our colleagues from other countries in the region having large Kurdish communities.”

Indeed Syrian Kurdish has already this week expressly stated they are open to a deal with Assad.

On Monday the commander of the US trained and armed SDF, Mazlum Abdi, indicated just that in a bombshell statement:“We are considering a partnership with Syrian President Bashar al-Assad, with the aim of fighting Turkish forces,”he said.

The United States has blocked such talks for years, making Trump’s “betrayal of the Kurds” sting much worse, given the White House’s essentially ‘green lighting’ the Turkish invasion did not give the Kurds time for the crucial option of coordinating a defense with the Syrian Army or pursuing a reconciliation deal with Assad, as Rep. Tulsi Gabbard has pointed out.

Meanwhile, with the SDF now taking heavy casualties, and with no response to overwhelming Turkish air power, the Syrian Kurds are no doubt already reaching out to Damascusfor aerial support and assistance from the Syrian Army.

This as President Erdogan announced Thursday, “109 PKK/YPG terrorists have been neutralized during Operation Peace Spring so far.”

Cook Caves To China: Apple Deletes Police-Tracking App Used In Hong Kong Protests

More violent protests are expected in Hong Kong this weekend.

Shopping malls, restaurants, and the city’s metro have already made emergency plans to close early. The violent unrest could start with-in the next 24 hours.

To avoid conversely, due to if a Hong Kong Police Force and or People’s Liberation Army Hong Kong personnel is severely injured or dies in the unrest, Apple has swiftly removed a police-tracking app from the App Store, reported Reuters.

The app, called HKmap.live, has been widely used by protestors to crowdsource real-time locations of law enforcement personnel in Hong Kong. Demonstrators have also used the app to stage elaborate counterattack operations and ambush attacks on government personnel.

We noted yesterday how, on late Tuesday night, China’s official newspaper, the People’s Daily, criticized Apple for allowing the app to remain in the App store.

The paper said Apple has “betrayed the feelings of the Chinese people” by approving the app.

The People’s Daily said Apple shouldn’t provide apps to people conducting illegal activities [protestors], and it also questioned whether the US technology company was “thinking clearly” during the app approval process.

“The developers of the map app had not hidden their malicious motive in providing ‘navigation’ for the rioters,” The People’s Daily wrote. “Apple chose to approve the app in the App Store in Hong Kong at this point. Does this mean Apple intended to be an accomplice to the rioters?”

Apple, who caved into the demands of the Chinese government by removing the app, issued a statement that said it started investigating the app’s use and discovered it “has been used in ways that endanger law enforcement and residents in Hong Kong.”

“The app displays police locations and we have verified with the Hong Kong Cybersecurity and Technology Crime Bureau that the app has been used to target and ambush police, threaten public safety, and criminals have used it to victimize residents in areas where they know there is no law enforcement,” the statement said.

The political crisis intensified last weekend when protestors took to the streets on Saturday and Sunday. Upcoming protests this weekend are expected to be equally as dangerous as last.

Besides Apple, China has put several other American companies into its crosshairs this week for their support of protestors, and one of those companies has been the NBA.

For those curious just what prompted stocks to soar today, besides the now traditional and thoroughly unjustified “trade optimism” barrage of headlines, we present one possible explanation: Dennis Gartman is out with his latest investment recommendation to short the S&P. Her is his latest “hot take” on markets:

… we note that the CNN Fear & Greed Index finished yesterday…. Wednesday, October 9th… at 30, up 1 “point” from Tuesday’s closing level. There is now no question about it: we erred… and rather badly so… in holding steadfast to the thesis that no bearish action was to be taken until this index had made its way above 70 because it had made its way to 68 two weeks ago. 68 should be in anyone’s estimation rather obviously close to 70. Further, the fact that it’s turned lower and is now well below 40 has raised our bearish interest for the first time in quite some while.

At this point we again draw attention to the chart this page of the CNN Fear and Greed index noting that that the peaks since the autumn of ’17 have been progressively lower. This would seem to tell us that the internal and inherent strength of the decade-long bull market has waned and is waning. But we’ve not acted yet. We’ve not actually taken a bearish posture because we are constantly reminded of what “Old Turkey” told the young Jesse Livermore when asked why he’d chosen not to sell his stocks as a correction seemed quite reasonable, to which the wizened old investor replied, “Well, after all, this is a bull market.” But even great bull markets come to an end… eventually. Given that our International Index made its peak in late January of ’18, we have to begin to admit that we’ve actually been in a bear market since then and simply we’ve collectively and individually not recognized that fact.

Finally, it was brought to our attention earlier this week and we’ve commented upon it this week twice already that executives… CEO’s, CFO’s and corporate board members… have been selling stock in their companies at the fastest pace of such selling in the past two decades. Insider selling is not quite as “telling” as is insider buying, but selling of this size and duration has our attention… and well it should.

And the actual recommendation:

As of Tuesday evening’s close we had gotten to what we refer to here as “net beta adjusted zero exposure,” or as close to zero as we were able; “zero” being neutral. It was our intent now to get just a bit “net beta adjusted short” by cutting back marginally on our long positions and by adding… also at the margin… to our derivative shorts. Yesterday we did the former; we cut back… marginally… on our long positions but we did not add to the short derivatives.

NEW RECOMMENDATION: The chaos of last evening shows us just how vulnerable equites [sic] are at this point and so we are sellers today of the December S&P and December EUR STOXX 50 with the former at or near to $2916 and with the latter at or near to 3456. We’ll “do” one unit of each and will risk 2% on each position and no more than that. If/when the December S&P falls below 2875, we’ll add to that trade and if/when the December EURO STOXX 50 falls below 3300 we’ll do the same.

This effectively assures that 2,974 on the S&P is in the bag. And finally, some bad news for gold bulls:

Regarding our gold position, following the PMI “news” early last week we bought a bit more gold. The monetary authorities of the industrialized world really haven’t any choice but to continue to err in favor of monetary expansion, all things being otherwise equal, and thus unless the very rules of monetary policy have been wholly rescinded that shall be bullish of gold. Mr. Powell’s comments on Tuesday only serve to underscore that notion.

Ukrainian Government Will ‘Happily” Investigate Pro-Hillary Election Interference, President Says

Ukrainian President Volodymyr Zelensky says his country will “happily” investigate whether Ukraine interfered in the 2016 US elections – telling reporters on Thursday that “we can’t say yes or no” without first looking into the matter.

Zelensky said that it was in Ukraine’s best interest to determine what happened, according to the Associated Press.

During a July 25 phone call, President Trump asked Zelensky to look into various accusations of Democrat malfeasance in Ukraine, which Trump’s political enemies have seized upon as the foundation of an informal impeachment inquiry against Trump.

Last month, a CIA whistleblower claimed Trump abused his office by pressuring Zelensky to initiate probes into former Vice President Joe Biden and the election interference claims – suggesting that valuable US assistance was used as leverage.

On Thursday, however, Zelensky insisted that there was “no blackmail,” telling reporters from AP that he learned that the US had paused nearly $400 million in military aid after the July 25 phone call.

Trump asked Zelenskiy during the call to investigate Democratic rival Joe Biden, and Congressional Democrats believe Trump was holding up the aid to use as leverage to pressure Ukraine.

Zelenskiy said he thought the call would lead to an in-person meeting with Trump and wanted the American leader to come to Ukraine. –AP via WaPo

Zelensky’s comments came amid an all-day “press marathon” he’s giving in order to answer questions about current events.

Election interference?

In an appearance on Fox News in early October, Trump attorney Rudy Giuliani said: “What I’m talking about, this, it’s Ukrainian collusion, which was large, significant, and proven with Hillary Clinton, with the Democratic National Committee, a woman named Chalupa, with the ambassador, with an FBI agent who’s now been hired by George Soros who was funding a lot of it.”

Rudy Giuliani: “What I’m talking about, this, it’s Ukrainian collusion, which was large, significant, and proven with Hillary Clinton, with the DNC, a woman named Chalupa, with the ambassador, with an FBI agent who’s now been hired by George Soros who was funding a lot of it” pic.twitter.com/nNFyXnHA7r

According to The Hill, Ukrainian Ambassador Valeriy Chaly confirmed that DNC contractor of Ukrainian heritage, Alexandra Chalupa, approached Ukraine seeking information on Trump campaign chairman Paul Manafort’s dealings inside the country, in the hopes of exposing them to Congress.

Chaly says that, at the time of the contacts in 2016, the embassy knew Chalupa primarily as a Ukrainian-American activist and learned only later of her ties to the DNC. He says the embassy considered her requests an inappropriate solicitation of interference in the U.S. election.

“The Embassy got to know Ms. Chalupa because of her engagement with Ukrainian and other diasporas in Washington D.C., and not in her DNC capacity. We’ve learned about her DNC involvement later,” Chaly said in a statement issued by his embassy. “We were surprised to see Alexandra’s interest in Mr. Paul Manafort’s case. It was her own cause. The Embassy representatives unambiguously refused to get involved in any way, as we were convinced that this is a strictly U.S. domestic matter.

“All ideas floated by Alexandra were related to approaching a Member of Congress with a purpose to initiate hearings on Paul Manafort or letting an investigative journalist ask President Poroshenko a question about Mr. Manafort during his public talk in Washington, D.C.,” the ambassador explained. –The Hill

Chalupa, who told Politico in 2017 that she had “developed a network of sources in Kiev and Washington, including investigative journalists, government officials and private intelligence operatives,” said she “occasionally shared her findings with officials from the DNC and Clinton’s campaign.“

Giuliani also said that former Ukrainian prosecutor Viktor Shokin, Biden had fired, “dropped the case on George Soros’ company called AntAC,” adding “AntAC is the company where there’s documentary evidence that they were producing false information about Trump, about Biden. Fusion GPS was there,” Giuliani added. “Go back and listen to Nellie Ohr’s testimony. Nellie Ohr says that there was a lot of contract between Democrats and the Ukraine. (via the Daily Wire).

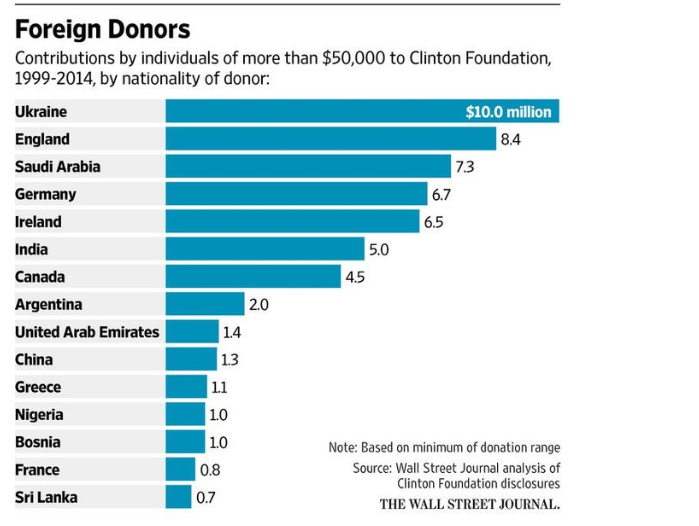

Meanwhile, Ukrainians donated the most cash of any country to the Clinton Foundation between 1999 – 2014, followed closely by Brits and Saudis.

If Hillary does run again in 2020, her Ukraine ties may be her downfall.

Chinese Imports Of US Pork Soar To The Highest Ever As Beijing Faces Food Crisis

In a time when China is losing between a third and half of its pig herds as a result of the unprecedented decimation unleashed by African swine fever – less affectionately known as pig ebola – which has sent wholesale pork prices in China soaring to all time highs…

… China is increasingly finding itself at America’s mercy.

As Bloomberg reports, as China’s hog herd is collapsing, Beijing’s imports of U.S. pork exploded to a weekly record.

According to USDA data, in the week ended Oct. 3, pig imports soared to 142,200 metric tons, more than 7 times greater than September’s total shipments of 19,900 tons.

China signaled it may import as much as 400,000 tons to stem a domestic shortfall, and it now appears that the US may be the easiest source of said pigs, which needless to say grants the US substantial leverage in the ongoing trade talks. The swine fever outbreak killed millions of pigs. The country also appeared poised to boost purchases of agriculture products as a good-will gesture before talks between Washington and Beijing on easing trade tensions.

Meanwhile, as BBG notes, volatility in hog futures in Chicago has surged to a record, spurred by speculation on exactly when Chinese demand would finally surface. The answer: right now.

The USDA data showed 123,500 tons are for shipment in 2020 with the balance set for the end of this year.

On the International Rugby field, Scotland has played Japan 4 times over the last 30 years. Scotland has won all four games, with an average points advantage of +46 points over Japan in each game. The closest Japan ever got was 5 years ago when a development squad of young Scots players beat the Brave Blossoms 42/17. Japan are now a more successful team, most recently beating a gobsmacked Ireland. If World Rugby refuses to reschedule or relocate Sunday’s game because it’s a wee bit windy, then the Japan vs Scotland match will be declared a draw and Scotland will go home. Rugby World argues it is fair – they would need to make similar arrangements for all the other cancelled games. What’s fair about the host nation progressing because of the weather at the expense of another team?

The Scots are furious. Our Nation’s Motto: Nemo Impune Lacessit.

But first…

Before addressing the markets, I went to see the extraordinary Joker last night. Joaquin Phoenix was incredible. Just a hint of the madness of Commodus from Gladiator, and then ratcheted up to 11. It is not a Superhero film. It’s possibly the most disturbing thing I’ve ever watched – and although its apparently set in 1980s New York, the parallels with today are clear. No wonder the authorities are scared it will trigger copy-cat protests. If you want to see Gotham today, then go visit San Francisco. The film should be required viewing for any bureaucrat or politician.

Back to markets… Who hi-jacked Justice?

Today’s markets are overly tactical. Stocks up on some momentary positive trade news, bonds up a bit on hints of further economic weakness. They aren’t really thinking about the earnings season just a few weeks away, or what increasing oil instability Middle East tensions could bring. They aren’t reading the headlines about rising tensions within the ECB about the new bond buying programmes, or figuring out what negative Greek yields might possibly mean for the long term. (Yes. Its happened!)

Is the global outlook so steady we don’t really have to worry about the fact global stocks are still close to all-time record P/Es, or the tightness of bond spreads. Just take a look at the political pages.

Writing about politics and markets after watching Joker is tough. Did Donald Trump really say its OK for American citizens to break the law and kill people if its an accident? Did he really just betray the most dangerous minority in the Middle East to the Turks – chucking the Kurds under the proverbial M60 Tank? The Turks record of genocidal ethnic cleansing is unmatched… Did Donald really try to extort China and Ukraine to frame political rivals?

Yes. He did all these thing. And he will do worse tomorrow.

However bad it looks, Trump is not the fool many dismiss him to be. He is calculating. He is a modern Commodus. Being tough on Trade aligns himself with the electorate against common enemies will win him elections. While markets continue to play the moment by moment moves in the China Trade War, Trump knows tough action wins votes as effectively as Bread and Circuses. If you want to trade “trade”, then role play Trump. When he “extricates” the US from “pointless” Middle East Wars he cares about next years election, not what an Iran dominated fertile crescent will lead to in 4 years time when it becomes a SEP (a Someone Else’s Problem). Don’t expect him to display empathy towards the bereaved family of the young lad killed by an America diplomat’s wife driving on the wrong side of the road. That’s our fault because how can you expect American’s to drive on the left. Trump is a lesson in populism.

In a few years time I look forward to watching Joaquim Phoenix play Trump on celluloid.. Dial it all the way up to 12 on the scale.

Equity Investment Strategy

A number have readers have asked about equity strategy – wondering if I am confused? They charge I seem to be advocating buying stocks while simultaneously warning of an equity meltdown.

If you understand anything I write, then I am miswriting…. is one possible response. But I do think we are coming up to a massive dislocation/switch moment in stocks. The last few years bull market has made index investment – following the market higher by buying indices – a favoured strategy. Asset managers have been spamming their retail clients with pages and pages about how indices beat the stock pickers every time and are a much cheaper way to address market upside.

And generally, they have been right – a rising tide in stocks (which, admittedly has been fueled by stock buybacks on the back of low rates and yield tourism) has lifted all equities.

Forget it going forward. As the threats increase:

recession triggering weaker earnings,

rising liquidity and refinancing risk for highly levered firms,

the unravelling of peak-private equity and

and increasing move towards fiscal policies that will unravel the zerocost debt splurge – then index based investment is going to struggle. At 20 times earnings, current P/Es still look toppy.

But a correction in stocks – and that is all I really expect – will be a fantastic opportunity to move back to fundamental stock investment. While I was working for Bear Stearns back in the 1990s, my boss, Brett, was the grandson of the father of fundamental investment: Ben Graham. I suggest a quick re-read of “The Intelligent Investor” might pay significant dividends.

If we see a switch from index back to stock picking – well, that’s going to drive a whole new market dynamic. I’d even be tempted to buy Buffett at this point… but?

What are the stocks to pick? Readers – I invite your suggestions…

Draghi Steamrolled Over Objections From ECB’s Own Policy Committee When Restarting QE

Shortly before the release of minutes from Mario Draghi’s parting meeting, the Financial Times published a leaked report Thursday morning claiming that Mario Draghi moved ahead with plans to relaunch an “open-ended QE” version of the ECB’s APP over the objections of an influential committee inside the central bank, setting the stage for his successor, Christine Lagarde, to confront these divisions as she begins her term at the central bank’s helm.

Though the minutes stipulated that a ‘clear majority’ supported Draghi’s plan, this was one of the rare examples from the president’s five-year term where there was such strident dissent on the central bank’s governing council.

Concern was expressed that not delivering sufficient stimulus, including through the APP, might trigger a reversal of the current favourable financial conditions. By contrast, restarting net purchases would provide a strong signal of the Governing Council’s determination and willingness to act in the light of the current subdued inflation outlook and the potential risk of an unanchoring of inflation expectations.

There was clearly a strong minority that supported a deeper rate cut of 20 bp, as opposed to the 10 bp authorized as part of the central bank’s stimulus, instead of reviving a more limited and size (but unlimited in scope) APP.

A very large majority of members agreed with Mr Lane’s proposal to lower the rate on the deposit facility by 10 basis points to -0.50%, which – together with the reinforced forward guidance – would act on the whole yield curve, especially in the short to medium-term segments, complementing the effects of net asset purchases on the long end of the curve. In this way, the measure would address the high level of short-term uncertainties that currently prevailed and help preserve very favourable financial conditions. While a few members expressed a readiness to consider lowering the rate on the deposit facility by 20 basis points at the current meeting, in particular as part of a package that would exclude net asset purchases, other members felt unable to support a cut of 10 basis points, as they were concerned about the possibility of increasingly adverse side effects from additional rate cuts.

According to the FT, the bank’s monetary policy committee, on which technocrats from the ECB and the 19 eurozone national central banks sit, advised against reviving the APP in a letter sent to Draghi and other members of the governing council in the days before the ECB meeting.

Not least of which because, as dissenters warned during the minutes, an open-ended APP could swiftly shrink the universe of eligible bonds, forcing the central bank to confront the possibility of buying more corporate bonds, or even equities.

After all, the ECB is already owns a sizable chunk of the extant euro-denominated government debt market (and duration concerns further limit what the central bank can purchase).

As the FT openly admitted, the leak of the letter’s contents is merely the beginning of a battle to pressure Lagarde into changing course.

The leaking of the confidential contents of the committee’s letter comes as opponents to Mr Draghi’s loose monetary policy fight a rearguard action to put pressure on Christine Lagarde for her to change course after she takes over at the ECB on November 1.

This is one of the few occasions where the committee’s advice wasn’t followed during the eight years since Draghi first became ECB president.

It is one of the few occasions that the committee’s advice has not been followed in the eight years since Mr Draghi became president, a council member said. However, the committee’s opinion is not binding and has been ignored at least four times in as many years by the council, which is free to decide otherwise, an ECB official said. The ECB declined to comment.

And its not the only group within the central bank that objected to restarting APP. The heads of the central banks of Germany, France, Slovenia and Estonia, among others, also objected, while the central bank’s legal committee pointed out that the ECB would need to defend itself against accusations that it was breaking bloc rules about directly financing governments via monetization.

Of course, not everybody agreed that the ECB “whistleblowers” – who joined the ranks of former central bankers warning about Draghi’s monetary insanity – were so strident in their criticism. ECB Governing Council member Olli Rehn of the Bank of Finland told BBG that the FT’s report about Draghi ignoring the committee’s advice was “greatly exaggerated.”

With Draghi about to hand the reins to Lagarde, we can’t help but wonder: Will these internal objections make any difference in policy? Or will they be duly noted by Lagarde before she settles in to maintaining the status quo.

The power is off in Northern California but we want to get this out even though it is still in draft form. We are working off desk and not sure when power will be restored. Take this as our first cut or swing in one of four at-bats.

Summary

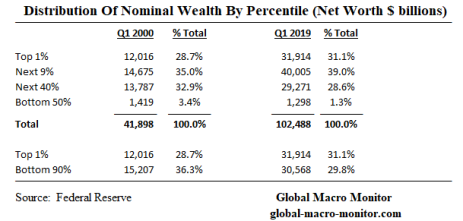

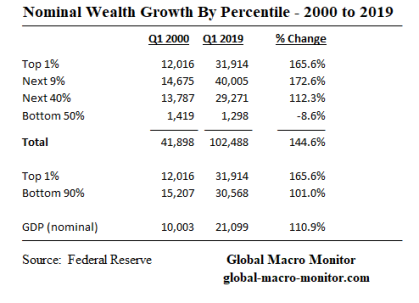

– We analyze the various components of the household balance sheet that drove net worth for the different percentile groups from Q1 2000 to Q1 2019

– The Top 1% are the ownership class, who hold over 60 percent of their assets in equity, in both public and non-corporate business and benefited greatly from QE

– The Bottom 50% of households have not benefited from the great asset inflation of the past ten years as their debt liabilities have exceeded the 93 percent growth in assets, resulting in an 8.6 percent decline in net worth from Q1 2000 to Q1 2019

– This post is a work in progress. Stay tuned for further updates when they turn the power back on in Northern California

In the previous posts, we illustrated America’s growing wealth gap, where the the Top 1% of households now hold more wealth than the Bottom 90%. The Top 1% are households with a net worth north of around $11-12 million. We use the terms wealth and net worth interchangeably.

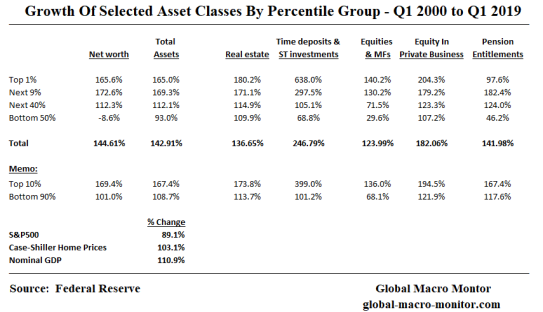

Wealth distribution in America is even more acute when comparing the 165.6 percent growth of the net worth for the Top 1% relative to the stunning 8.6 percent decline of the Bottom 50% of households. Yes, you read that correct, the aggregate nominal wealth of the Bottom 50% of American households has fallen almost 10 percent over the past 20 years, which is politically destabilizing and explains much of the conflict in today’s body politic.

In this post, we look at the composition of wealth by asset class and the contribution each has had to the change to the net worth for each percentile group from Q1 2000 to Q1 2019.

Stock Versus Flows

We only look at the change in the stock of assets and liabilities for each household percentile group, which includes the combination of capital gains, the cumulative income from assets, and the accumulation of new asset purchases with savings out of income. The data is not easily available to breakout the later, so keep in perspective the data includes capital appreciation, asset income, and the accumulated flow of new savings from income over the years. That is the absorption of cumulative savings and thus implicit income growth over the time period.

The above complicates our wealth distribution analysis as households can move from, say, the Bottom 50% to the Top 1% by hitting the lottery, for example. In a more real-life example, one of my daughter’s classmates who was a first-round pick in the recent Major League Baseball draft woke up one morning as a starving college student and went to bed that night with a $7.8 million contract, including a huge signing bonus. Definitely, a meteoric rise from the Bottom 10% to the Top 10%, assuming he and his girlfriend are counted as a household by the Census Bureau.

Income, savings, and the allocation of savings matter big to wealth accumulation. What matters even more is building and maintaining wealth.

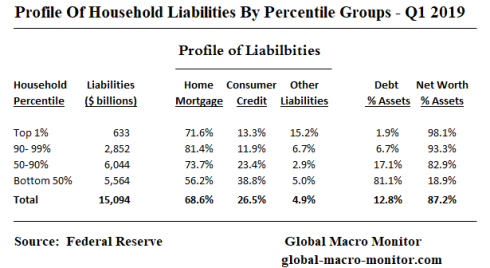

Liabilities

Since liabilities also play a role in determining net worth, we also have a brief look at household liabilities.

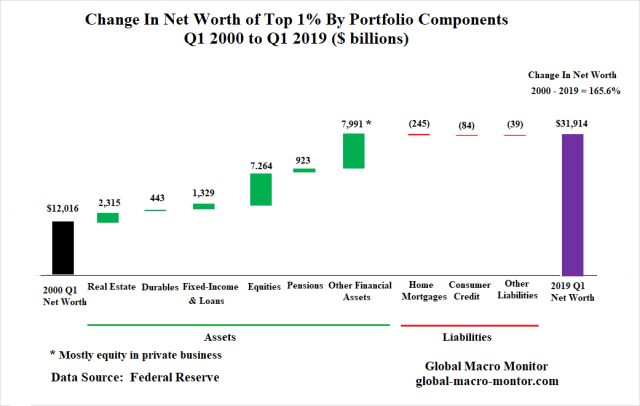

How The Rich Got Richer

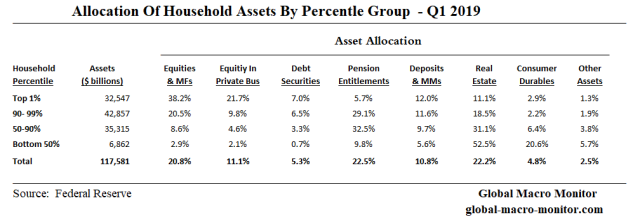

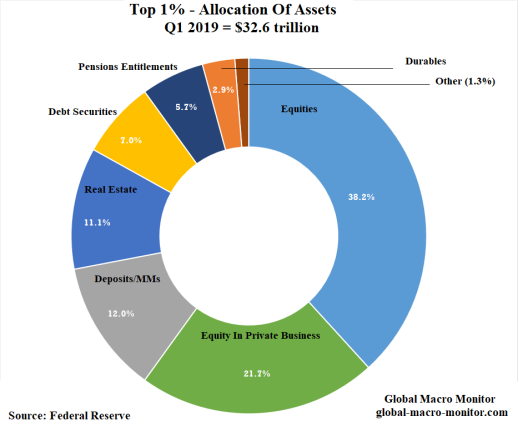

The following chart illustrates the aggregate nominal wealth of the Top 1% of households increased by $20 trillion, 165.6%, from $12 trillion in Q1 2000 to $32 trillion in Q1 2019. Most of the increase, 60.6 percent, came from the appreciation and accumulation of public equities and equity in non-corporate private business: $7 trillion and $4.7 trillion, respectively.

Real estate holdings accounted for 11.6 percent of the change in net worth and fixed-income assets 6.7 percent.

Impact of QE

How much of the Top 1%’s increase in wealth was due to the Fed’s monetary policy of quantitative easing (QE)? We can’t really quantify at this moment and will leave it for a future analysis but it is fairly safe to say, a lot. The Top 1% have effectively become asset surfers riding QE to unfathomable riches!

Is it any wonder why support is increasing for a People’s QE?

Liabilities

The Top 1% of households carry very little debt, less than 2 percent of total assets.

Contributions To Net Worth By Household Percentile Group

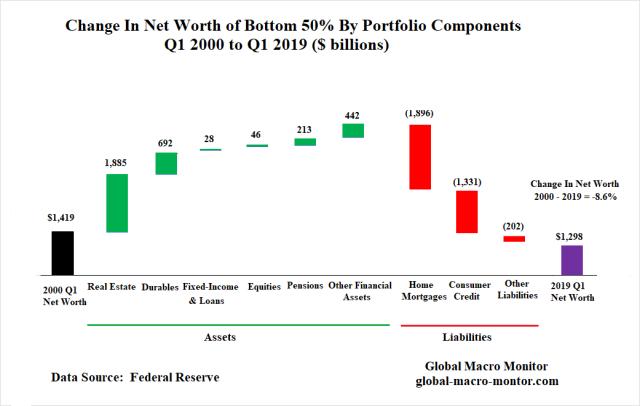

How The Poor Got Poorer

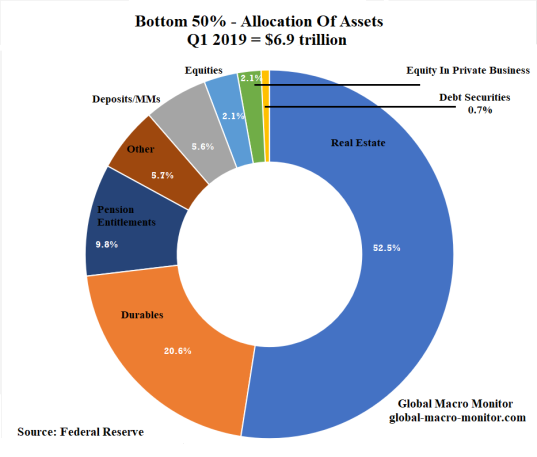

Though the assets of the Bottom 50% of households increased by $3.3 trillion, or 93 percent, over the period, the group’s net worth still fell by almost 10 percent because of their change in debt liabilities exceeded the increase in assets.

Almost 80 percent of the $3.3 trillion increase in assets was in real estate and consumer durables, such as cars, which illustrates just how little the Bottom 50% are invested in the financial markets. Only 2.9 percent of the group’s assets are held in equities and 9.8 percent in pension entitlements (see Asset Allocation chart below).

Liabilities And The Dusenberry Effect

Some of the increase in liabilities over the period was student loans, which we believe, are included in consumer debt.

We were surprised to find that even at the apex of the housing bubble, when the value real estate assets of the lower 50% were growing double digits, aggregate net worth was declining as the group’s borrowing exceeded asset growth. We suspect it was due to leveraging and using their home equity to finance additional purchases of homes and/or using it as an ATM to finance consumption. Moreover, the toxic mortgage debt that was marketed to the lower-income groups also played a role, such as 12o percent mortgages and option ARMs.

Real wages rose at the top of the distribution, whereas wages stagnated or fell at the middle and bottom. Real (inflation-adjusted) wages at the 90th percentile increased over 1979 to 2018 for the workforce as a whole and across sex, race, and Hispanic ethnicity. However, at the 90th percentile, wage growth was much higher for white workers and lower for black and Hispanic workers. By contrast, middle (50th percentile) and bottom (10th percentile) wages grew to a lesser degree (e.g., women) or declined in real terms (e.g., men). – CRS

We also suspect declining real incomes in a large portion of the Bottom 50% of households resulted in the Dusenberry Effect, where households took on more debt to sustain a fleeting standard of living,

One part of the “Dusenberry Effect” basically states that consumers do not give up their consumption patterns very easy even if their incomes decline. They, in effect, “ratchet” down their living standard very slowly by first having a second wage earner enter the workforce as we saw in the 1970’s when women began to enter the workforce en masse and then by taking on debt to finance their previous standard of living. — GMM, August 2017

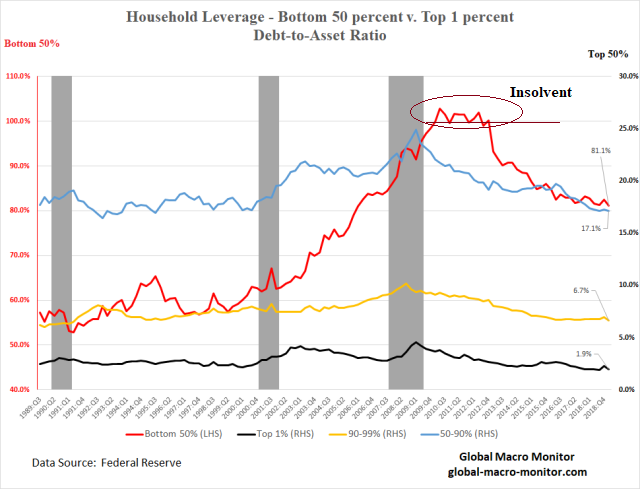

Whatever the case, the Bottom 50% carry a huge relative debt burden, 81.1 percent of assets, compared the 17.1 percent of the households in 50-90% percentile, the next most indebted group.

The data also clearly illustrates why debt forgiveness is a major focus of today’s populist message, even among the so-called moderate presidential candidates.

Democratic presidential frontrunner Joe Biden laid out his higher education platform today. There’s a lot in there, but I want to focus on one part: his proposal to make the income based-repayment (IBR) program for federal student loans more generous by cutting payments to just 5% of discretionary income.

In an earlier post, we showed how the Bottom 50%, on an aggregate basis (i.e., not every household) was insolvent during several quarters just after the financial crisis. Interestingly, we found what initially brought the percentile group back above water was a sharp reduction in its liabilities, which we suspect was getting out from under their bad mortgage debt either through foreclosures or debt forgiveness programs.

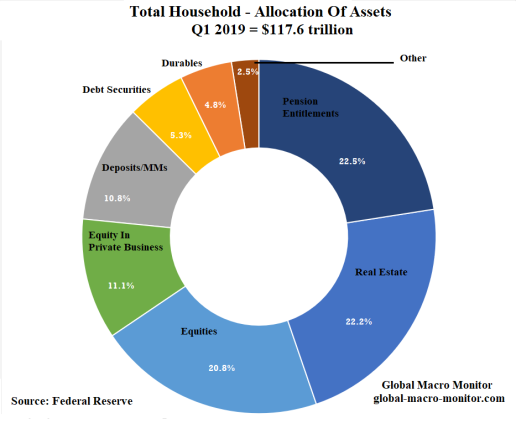

Household Allocation Of Assets

We leave you with the following data on how each percentile group’s assets are allocated. When the power comes back off we’ll have more commentary.

Main Observations

– The Top 1% are the ownership class, holding 60 percent of their assets in equities and equity in non-corporate businesses

– Pension entitlements make up almost 30% of the assets of the 90-99% percentile of households with 40% of their assets allocated to equities and real estate holdings

– The 50-90% percentile group hold almost two thirds of their assets in pensions and real estate with only 8.6 percent held in equities

– More than 70 percent of the Bottom 50% assets are held in real estate and consumer durables, such as autos, and only 2.9% in equities

Growth Of Asset Holdings

Interesting that the net worth of the top three percentiles outpaced the S&P500 and the Case-Shiller national home price index. This clearly reflects the accumulation of assets through savings. Also interesting the outsize growth of short-term assets by the Top 10%, which partially reflects the start date was the March 2000 peak of the dot.com bubble and the latest news that the rich are now hoarding cash.