The U.S. Customs and Border Protection unveiled a stretch of new border wall on the Southern Border and said it completed at least 60 miles in all.

“Construction crews continue work on the new border wall system along the SW border near San Luis” in Arizona, the agency wrote on Twitter.

So far, more than 60 miles have been constructed “along the SW border since 2017,” and the agency is expected to “complete 450 miles by the end of 2020,” the tweet read.

Construction crews continue work on the new border wall system along the SW border near San Luis, AZ. In partnership with @USACEHQ, CBP has constructed over 60 miles of new border wall system along the SW border since 2017 and expects to complete 450 miles by the end of 2020. pic.twitter.com/ZMVqVteMUN

The wall is located in the Yuma Sector, which is among the busiest along the southern United States.

According to Arizona station KOLD 13, work on more border wall sections has started in Arizona and New Mexico. The work on the wall, which was a campaign promise from President Donald Trump, stretches 46 miles west of Santa Teresa, New Mexico, and also is on 2 miles of the Organ Pipe Cactus National Monument in Arizona.

The workers broke ground on the construction between Columbus and Santa Teresa in New Mexico, KOLD noted on Aug. 23. In Arizona, crews were seen installing 30-foot steel fencing to replace barriers near the Lukeville Port of Entry.

Wow! Big VICTORY on the Wall. The United States Supreme Court overturns lower court injunction, allows Southern Border Wall to proceed. Big WIN for Border Security and the Rule of Law!

In July, the Supreme Court ruled to allow Trump to use military funds to build sections of the wall. The money had previously been frozen by the lower courts.

By executive order, President Trump redirected previously allocated Defense Department funds to be used for the New Mexico and Arizona construction, according to The Associated Press.

The administration has awarded $2.8 billion in contracts for barriers covering 247 miles (390 kilometers), with all but 17 miles (27 kilometers) of that to replace existing barriers instead of expanding coverage.

Recently-installed bollard style fencing on the US-Mexico border near Santa Teresa, N.M., on April 30, 2019. (PAUL RATJE/AFP/Getty Images)

Various forms of barriers already exist along 654 miles (1,046 kilometers) — about a third — of the border.

The construction comes as immigrant apprehensions have fallen sharply over the past two months due to the summer heat and a clampdown in Mexico.

Construction on a new half-mile section of border fence built by We Build the Wall at Sunland Park, N.M., on May 30, 2019. (Charlotte Cuthbertson/The Epoch Times)

Tens of thousands of people have come into the United States over the past year.

Construction is expected to take about 45 days. The government then plans to tackle two other projects in Arizona, including nearly 40 miles (64.4 kilometers) of fencing in other parts of the national monument and areas of Cabeza Prieta National Wildlife Refuge and San Pedro Riparian National Conservation Area.

In 1962 in a picturesque setting in Santa Barbara, California, two local entrepreneurs opened a low-cost, roadside inn where the nightly room rate was just $6.

They called it Motel 6.

And today the chain has grown to over 1,400 locations.

If you want the most straightforward explanation for why you should own gold, consider your local Motel 6.

It’s noteworthy that, today, the very same Santa Barbara location now rents its rooms for nearly $90 per night.

That’s a 15x increase in 57 years, an average increase of roughly 5% per year.

Are the rooms 15x bigger, or 15x nicer? Not really.

The reason the price has increased so much is because of inflation– the gradual erosion of the US dollar’s purchasing power over the past several decades.

This is why it’s important to have a conversation about gold.

Unlike paper currencies, gold has a 5,000 year track record of keeping up with inflation.

In fact, when priced in gold, a room at the Motel 6 has actually gotten cheaper.

Back in 1962, an ounce of gold would buy you about 6 nights at the motel. Now, despite the 12-fold increase in the price of a room, one ounce of gold will buy you 21 nights there.

That’s because the price of gold has largely outpaced the rate of inflation and the decline in the purchasing power of the US dollar.

Gold is a fantastic long-term store of value. It’s also an insurance policy– a hedge against paper currency, systemic risk, and uncertainty.

And there’s plenty of those in the world.

But there’s also a number of catalysts emerging right now that could send gold prices substantially higher in the near future, so it may be worth considering gold right now as a speculation.

There have been several times in history where gold has experienced wild swings in value against paper currency. And some people got very rich from it.

In the coming days and weeks, I’ll be writing a series of articles on different ways to own gold.

And it’s my hope that you’ll use the information to as part of your Plan B, not only to hedge against looming risks, but also to potentially profit from uncertainty in the system.

We’ll start with physical gold.

Think about your traditional savings: you probably have several deposit accounts at a number of banks. But the way the banking system works, there’s a middle man (the bank) between you and your money.

Having physical gold stored in an at-home safe is a great way to privately preserve your wealth without this sort of counter party risk. There’s no one else standing between you and your gold. No bank bureaucracy, no central bank, no regulator.

Your wealth can literally be held in your own hands.

It’s also a great idea to consider storing some gold overseas in a foreign, non-bank safety deposit box– but we’ll talk more about that soon.

When it comes to physical gold, you can buy either coins or bars. They come in a variety of sizes, from just 1/8th of an ounce (or smaller) to 20 kilograms or more.

And there are dozens of refiners and minters who produce coins and bars.

Now, I avoid buying gold bars because they are typically less uniform than coins. And here’s a great example why:

If you’ve ever seen those giant stacks of gold bars in the movies– those bars are supposed to be 400 ounces. Each.

But here’s a dirty secret few people know about gold–

According to the “Good Delivery” specifications for a 400 ounce gold bar traded on the London Metal Exchange, the bar could weigh as little as 350 ounces, or as much as 430 ounces, and still qualify as a 400 ounce bar.

Every one of those bars is different… there’s no uniformity.

That’s why my preferred way to own physical gold is to buy the most widely recognized coins (i.e. NOT bars) that have the highest purity.

The United States Mint, for example, produces a very famous coin called the “American Gold Eagle”, that contains 91.67% pure gold.

The American Gold Eagle is well-known throughout the world, and pretty much every coin dealer on the planet will buy and sell them.

However, I don’t recommend buying the American Gold Eagle. At 91.67%, its gold purity is too low.

Coins of lower purity can sometimes cause problems for international transport if you’re shipping gold from one country to another; if the purity is below a certain threshold, you might have to pay customs duty.

Also, lower purity coins could cause tax problems (especially for US taxpayers) if you want to qualify for a ‘like kind exchange’ under IRS section 1031. More on that another time.

So, instead of a American Gold Eagle, which is only 91.67% pure, I recommend the Canadian Gold Maple Leaf.

The Canadian Gold Maple Leaf is produced by the Royal Canadian Mint. And with a gold content of 99.99%, the Maple Leaf is one of the purest gold coins in the world.

It’s also just as renowned worldwide as the American Gold Eagle, but without the potential drawbacks. So it’s a better coin to own.

Here are a few widely recognized, high-purity gold coins which you could consider:

Canada Gold Maple Leaf (99.99% purity)

Chinese Panda (99.9% purity)

Austrian [Vienna] Philharmonic (99.99% purity)

Australian Gold Nugget (99.99% purity)

American Buffalo (99.99% purity)

There are plenty of other countries whose national mints produce high-purity gold coins– like Malaysia, Kazakhstan, Poland, Ukraine, etc.

But those countries’ coins don’t have the global recognition of a Canadian Gold Maple Leaf or Chinese Panda. And without the global recognition, they’re more difficult (and more expensive) to buy/sell.

I also recommend avoiding these coins (because the purity is too low) include:

American Gold Eagle (91.67%)

South African Krugerrand (91.67%)

United Kingdom Sovereign (91.7%)

You can buy coins in countless places, whether at a local coin dealer, or online– Kitco, APMEX, even eBay and Amazon.

Speaking at the close of the G7 summit in Biarritz, France on Monday, President Trump said he’s “open” to meeting with Iran’s President Hassan Rouhani.

This was in response to French President Emmanuel Macron stating he hopes to arrange a meeting with the US and Iranian leaders in the “coming weeks”. Trump qualified during his surprise remarks regarding a potential meeting, “If the circumstances were correct or right, I would certainly agree with that.” Trump cited “good feelings” about Iran and its desire to escape currently escalating tensions.

“In the meantime they have to be good players,” he added. Otherwise, he asserted, Iran will be met with “violent force.” Trump said the Iranians “have no choice”.

NEW: Pres. Trump says he would meet with Iranian Pres. Rouhani “if the circumstances were correct.”

It’s not the first time the White House has invited Iran to the table following a summer of escalating “tanker wars” and boiling point tensions in the Persian Gulf, and amid a US military build-up in the region.

It was recently revealed that last month Iran’s Foreign Minister Javad Zarif had rebuffed a secret invitation to meet with President Trump in the oval office, which involved the mediation of Rand Paul. Just days following this, the US Treasury announced unprecedented sanctions against the Iranian top diplomat.

FM Zarif had made a surprise arrival in Biarritz for talks at the French foreign ministry’s invitation. However, there were no reported meetings or talks with American officials.

Reports suggest that Macron could currently be pressing Trump for a resumption of the Iran oil waiver program, which allowed up to eight countries such as China, India, Iraq and others to continue legal imports of Iranian crude without threat of US punishment. Both leaders sought to assure reporters that Macron had made Trump aware that Zarif would be present on the sidelines of the G7, and that they were strategizing together every step of the way.

When Trump was pressed at the G7 press conference over whether it was “realistic” to organize a meeting with Iran in only a matter of weeks, Trump responded “it does.”

“I think he’s going to want to meet. I think Iran wants to get this situation straightened out. Is that based on fact or based on gut? That’s based on gut,” Trump said. “But they want to get this situation straightened out, Jonathan. They’re really hurting badly.”

Iranian President Hassan Rouhani, via the AP.

Macron, for his part, also sounded optimistic that talks will happen: “So, I hope that in the next few weeks based on our discussions, we will be able to achieve the meeting that happen I just mentioned between president Rouhani and President Trump, myself and the partners who have a role to play in nuclear negotiations will also be fully involved in these negotiations,” the French president said.

But it remains the case that Iran has vowed repeatedly that it would never bow to Washington pressures and threats, and likely Tehran will read Trump’s “talk with me or else…” style of rhetoric as precisely a continuation of the “maximum pressure” campaign that’s currently in the process of destroying Iran’s economy.

via ZeroHedge News https://ift.tt/2NBHyhB Tyler Durden

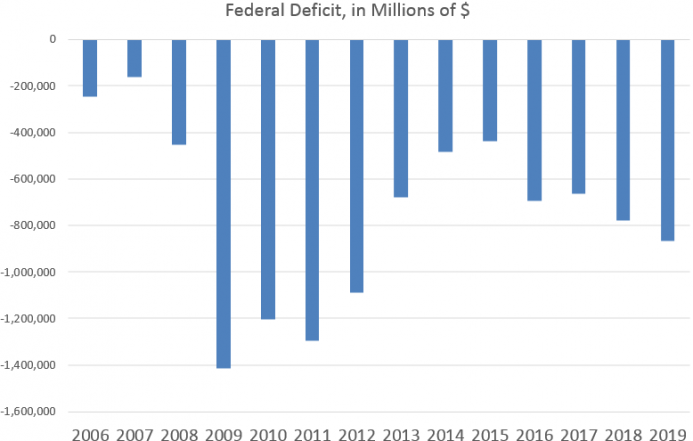

The Treasury Department released new budget deficit numbers last week, and with two months still to go in the fiscal year, 2019’s budget deficit is the highest its been since the US was still being flooded with fiscal stimulus dollars back in 2012.

As of July 2019, the year-to-date budget deficit was 866 billion dollars. The last time it was this high was the 2012 fiscal year when the deficit reached nearly 1.1 trillion dollars.

At the height of the recession-stimulus-panic, the deficit had reached 1.4 trillion in 2009. (The 2019 deficit is year-to-date):

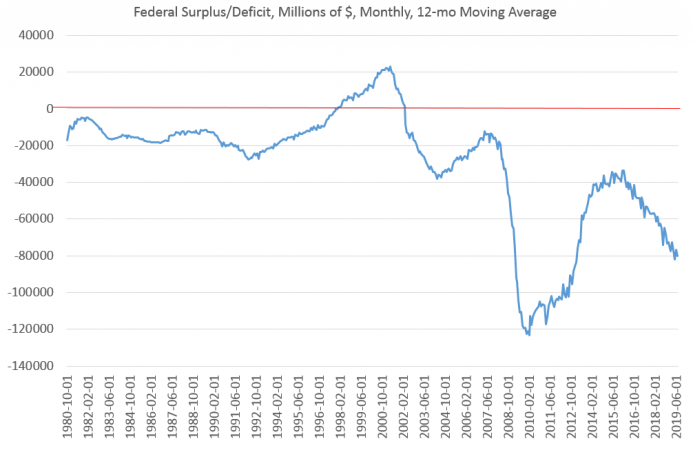

What is especially notable about the current deficit is that it has occurred during a time of economic expansion, when, presumably, deficits should be much smaller.

For example, after the 1990-91 recession, deficits generally got smaller, until growing again in the wake of the Dot-com bust. Deficits then shrank during the short expansion from 2002 to 2007. During the first part of the post Great Recession expansion, deficits shrank again. But since late 2015, deficits have only gotten larger, and are quickly heading toward some of the largest non-recession deficits we’ve ever seen.

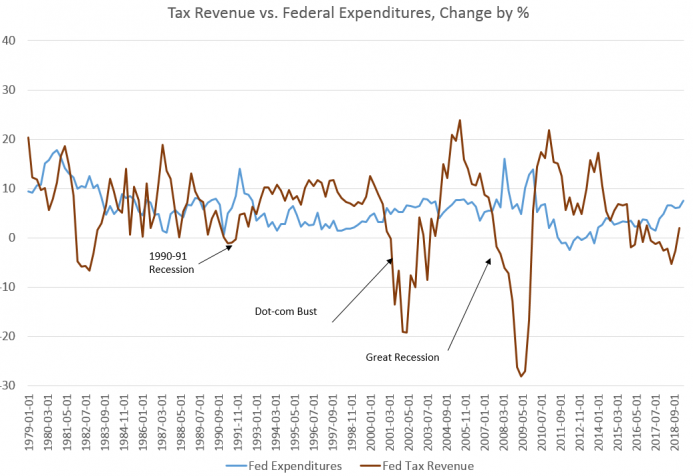

The situation is a result of both growing federal spending and falling tax revenues. As of the second quarter of 2019, year-over-year growth was nearly at a nine-year high. Federal spending rose 7.5 percent, year over year, during the second quarter of this year. The last time growth rose as much was during the first quarter of 2010 when spending increased 13.8 percent, year over year.

Meanwhile, federal revenue growth has fallen, with only one quarter out of the last eight showing year-over-year growth.

Historically, a widening gap between tax revenue and government spending tends to indicate a recession or a period immediately following a recession. We saw this pattern during the 1990-91 recession, the Dot-com recession, and the Great Recession.

The Trump administration has attempted to brag that it has increased revenues through tax hikes (i.e., tariff increases), and as Bloomberg reports, “tariffs imposed by the Trump administration helped almost double customs duties to $57 billion in the period.”

But tariff hikes also cut intro entrepreneurial activity and overall production, reducing earnings and hobbling economic growth. Not surprisingly, tax revenues have not kept up.

Of course, if tax revenues actually limited government spending, there wouldn’t be much to complain about. Lower revenues really would mean fewer resources flowing into government coffers — and that can be a good thing.

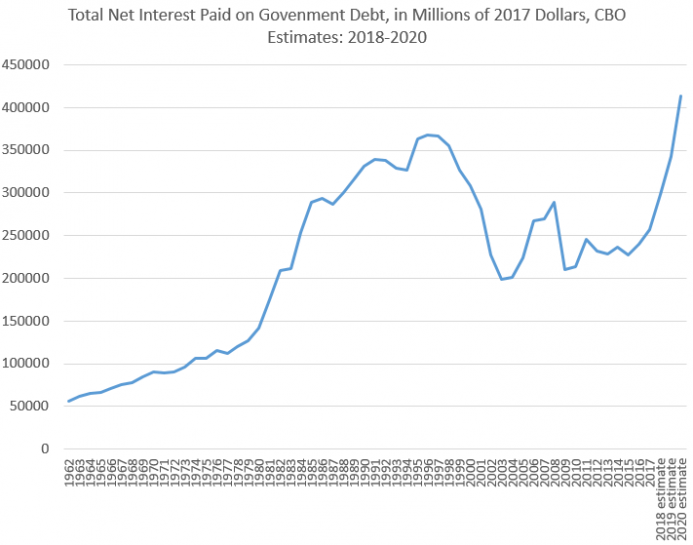

But, in a world where government borrowing allows spending to balloon even in times of falling revenue, we’re setting the stage for future problems. The more the total national debt rises, the more debt service will become a serious issue if interest rates increase even moderately. Given the prospects for higher interest rates in the future, the Congressional Budget Office estimates interest payments on the debt will increase substantially in the future:

It is troubling that after a decade of an economic expansion, the US government is still spending money as it does during and immediately following a recession. Thus, if deficits are this large right now when times are good, how big will they become when the US enters recession territory? Back in 2009, the recession and its aftermath (i.e., massive amoounts of stimulus) drove deficits beyond the trillion dollar mark four years in a row. With 2019’s deficit total now pushing toward 900 billion, we should perhaps expect deficits to top two trillion when the next recession hits. And probably for several years.

The piper will then need to be paid when interest rates increase and substantial cuts must be made to social security, medicare, and to military budgets in order to service the debt and avoid default.

This reckoning can be put off, however, so long as the dollar remains the world’s reserve currency, and the central bank can continue to monetize the debt. As long as the dollar reigns supreme, the central bank can keep this up without causing high levels of price inflation. But when the day comes that the dollar can no longer count on being stockpiled worldwide, things will look very different.

The central bank won’t be able to simply buy up debt at will anymore, interest rates will rise, and Congress will have to make choices about how many government amenities will be cut in order to pay the interest bill. Americans who live off federal programs will feel the pinch. State governments will have to scale back as federal grants dry up. The US will have to scale back its overstretched foreign policy. Not all of this is a problem, of course. But lower-income households and the elderly will suffer the most. Everything may seem fine now, but by running headlong into massive deficits even during a boom, the feds are setting up the economy for failure in the future.

But that’s in the future, and few lawmakers in Washington are worried about much of anything beyond the next election cycle.

via ZeroHedge News https://ift.tt/2MDcSwM Tyler Durden

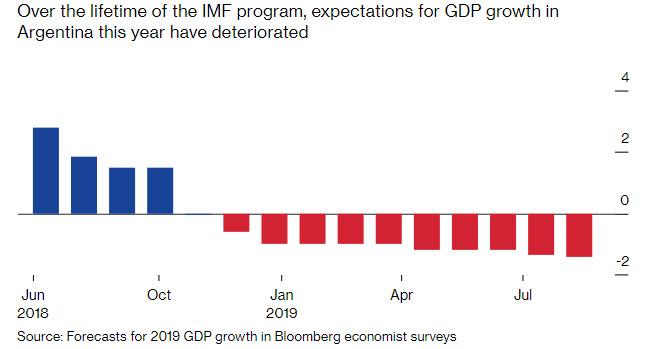

On Friday, when CNBC’s Steve Liesman was interviewing the IMF’s new chief economist, Gita Kopinath, we suggested that he ask what the IMF’s plan is for Argentina now that the country was facing what appears yet another bond default.

Hey @steveliesman can you ask the IMF chief economist what their Argentina plan is now.

And while Steve did in fact ask that question, he didn’t get a direct answer for one simple reason: the IMF has no clue what it will do now that it is facing a historic loss on its latest, and biggest ever, $56 billion bailout of Argentina, which was completed less than over a year ago in September 2018.

It gets worse: not only does the IMF have to scramble to preserve its current bailout, and credibility, having sunk billions into a country which humiliated the IMF at the start of the century when it defaulted last, the monetary fund has to decide whether to keep injecting money into a nation that many believe will soon default on its foreign obligations – and the IMF – again, after President Mauricio Macri just got trounced by the populist opposition in a nationwide primary vote, after his IMF-backed program – based around much hated budget austerity and the world’s highest interest rates – failed to pull the economy out of recession. What happened next, as we reported two weeks ago, was a 20% crash in the peso and a collapse in government bonds, which pushed the implied risk of default above 80%.

It was in this dire context that IMF delegates arrived in Argentina on Saturday and, as Bloomberg reports, immediately began meetings with policy makers, facing a deja vu choice from two decades ago: risk making the turmoil even worse by withholding a $5.3 billion installment due next month – or cough it up, and risk even more losses with the IMF bailout program on the verge of collapse.

The IMF’s henchmen also have to figure out the economic plans of opposition chief Alberto Fernandez – who is set to head a less market-friendly government in a few months, an outcome which the IMF clearly not even once considered when it “offered” Macri’s regime tens of billions in loans in exchange for draconian terms that flipped public opinion against him in just a handful of months. And while elections are still two months away, and miracles can certainly happen, Macri’s 15-point primary defeat has led analysts to write him off as a lame duck.

Lagarde and Macri

“The IMF has put a lot in – not just money, but prestige,” said Hector Torres, a former executive director at the Fund who represented South American countries. “The fact that the arrangement is not performing well right now is an embarrassment,” he said. And the September installment is “going to be a difficult call.”

If the IMF does decide to throw good money after bad, it can justify it by pointing out what until recently, was at least modest success: Argentina was roughly on track to meet an IMF target of balancing the budget this year (excluding interest payments). Of course, the reason why the country performed as expected is also the reason why Macri is now on the way out, and the IMF’s involvement in the Argentine economy and politics has managed to unite the local population in its hatred unlike any other issue.

The Fund may cite that performance in the first half of the year as grounds for handing over next month’s payout, according to Priscila Robledo, Latin America economist at Continuum Economics in New York. “That’s what I think will be the justification: ‘Nothing happened at the end of June, we’re all fine’,” she said.

This is also known as the ostrich head in the sand approach, which works great… until Argentina “unexpectedly” announces it is defaulting once again.

What the fund will not cite is Argentina’s economic performance, as GDP expectations have collapsed under the IMF’s supervision, as the following Bloomberg chart shows.

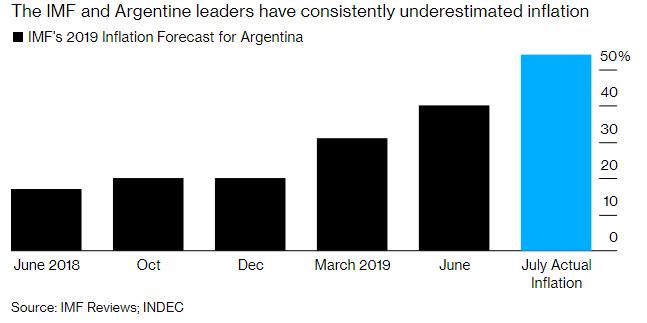

And then there are the IMF’s attempts to tame Argentina inflation. Needless to say, they have failed dismally.

Another reason why the IMFwill be careful how to spin its “success” to date is that even Macri appears to have given up on compliance. Since the ballot reverse, Macri’s government has begun to aggressively loosen policy, in contravention to IMF orders. It froze fuel prices and boosted subsidies, in an effort to shield the poorest Argentines as the peso’s latest slide threatens to push inflation even higher.

“The Fund might say its evaluation going forward is that they won’t be met,” said Daniel Marx, an Argentina “expert” who negotiated with the IMF two decades ago as the country’s finance secretary, and now heads research company Quantum Finanzas in Buenos Aires. In that case, “the disbursement could be at risk.” It would also put the IMF on the hook for billions in losses, mostly funded by US taxpayers who will be curious to learn why their money is sued to perpetuate the IMF’s gross incompetence.

The central bank could also breach IMF targets, as it burns through cash to defend the peso, Marx said. “Now that they’re starting to intervene in spot markets, that might affect net reserves.” While last week, the bank managed to steady currency and bond markets, Argentina’s benchmark debt trades below 50 cents on the dollar, a red flag for the Fund which realizes default when it sees it.

No matter how the IMF spins it, even a cursory look at Argentina’s economic performance over the past year confirms the fund’s intervention has only made the disaster worse.

As Bloomberg notes, the IMF has special criteria, which it adjusted after the Greek crisis, for jumbo loans like the one Macri got – and compliance is reassessed at each review. Two of them are key for Argentina right now: the Fund has to be satisfied that a borrower’s debt is sustainable and that it has decent prospects of access to private capital.

Judging by the markets, Argentina will almost certainly not meet those benchmarks. That opens a range of possibilities, including what the IMF calls “reprofiling” – an extension of debt maturities a la Greece, with few other changes – or the kind of restructuring brokered by the Fund for Ukraine in 2015, which involved haircuts too.

In an amusing twist Fernandez, who trumpets his experience working with the IMF as cabinet chief in the years after the 2001 crisis, insists that there’ll be no replay. “There’s no possibility that Argentina will fall into default if I’m president,” he said on Wednesday. Well, yes: one would probably not expect him to admit his first action as president will be to push the country into yet another sovereign default.

Bracing for the worst, the IMF has already opened channels to the opposition leader, including meetings with advisers Matias Kulfas and Cecilia Todesca, and those contacts are set to deepen starting this week. None of that will have any impact on the ultimate outcome, and explains why Fernandez has been vague about policy commitments and says talks with the IMF are Macri’s responsibility while he’s president. The bottom line is simple: opposition chief has said the program must be revised to allow Argentina to grow again. Failing that, a default is inevitable.

“Fernandez’s first request will be to reschedule,” said Patrick Esteruelas, head of research at EMSO Asset Management in New York. If a deal can’t be hammered out, “private sector debt holders would have to take some form of haircut.”

But while creditors will be hit, it will be the ordinary Argentina citizens that will be crushed:

Ordinary Argentines also have traumatic memories of failed IMF programs. Many blame the Fund for the epic collapse of two decades ago, one reason why Macri’s decision to go to the IMF last year was so risky.

Of course, a worst case outcome won’t be unprecedented as the Latin American nation already has an illustrious history of stuffing the IMF: in late 2001, after a series of missed budget targets and re-upped IMF loans, the government announced it was preparing to restructure debt. Argentines rushed to the banks to pull their money out, finding their deposits had been frozen by authorities, an event known as the “corralito”, an outcome similar to what happened in Greece in the summer of 2015.

A week later, the IMF finally pulled the plug, declining to disburse more funds. Mass protests erupted, leading to dozens of deaths. The political system convulsed, with four presidents succeeding each other in the space of a month. In the longer run, Argentina was frozen out of world markets for over a decade, and millions saw their savings wiped out.

While some analysts are confident that this time will be different, others argue that with an even greater build up of imbalances, the outcome could be even more devastating, especially when considering the prospect of an extended transition of power, something which traditionally results in social upheaval in Argentina.

There’ll be a four-month gap between the Aug. 11 primary and the swearing-in of a new government. And the Fund has its own leadership vacuum: Christine Lagarde, the IMF chief who signed off on Argentina’s loan, is in transit to the European Central Bank and may not be replaced for weeks.

“The IMF is in a serious pickle,” said Esteruelas. “It reminds me of the saying: If you owe the bank $100, it’s your problem. If you owe the bank $100 million, it’s the bank’s problem.”

The best news? After leaving Argentina’s economic in disaster, and the IMF’s reputation in tatters, Christine Lagarde is off to finish off her work by taking over the ECB and doing what she does best: destroying Europe once and for all.

via ZeroHedge News https://ift.tt/2ZtiyeC Tyler Durden

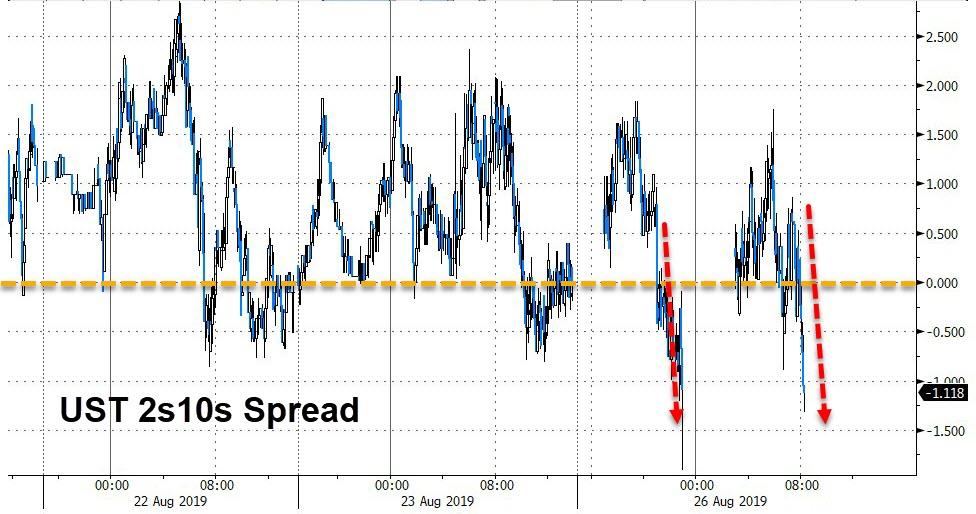

For a few brief hours overnight, the much-watched 2s10s segment of the US Treasury curve un-inverted, following Friday’s collapse. That is now over as the curve has dropped back below -1bps…

Source: Bloomberg

Time to start focusing on another part of the yield curve or else this is getting serious.

via ZeroHedge News https://ift.tt/2Zp9CH9 Tyler Durden

One of the obvious and expected consequences or instances of ‘blowback’ from Israel’s unprecedented decision to extend its “anti-Iran” campaign into Iraq, with three airstrikes widely blamed on either Israeli drones or possibly F-35s in the last five weeks, is that it will force a deepening conflict between Iraq’s military and US coalition forces.

There’s long been a broad base of Iraqi support that would like to see the American presence completely out of the country with the Islamic State long defeated, but now that political bloc just got a lot stronger in the wake of the alleged Israeli raids, at least one of which US officials have already admitted Israel bore responsibility for (a July 19 attack on a Popular Mobilization Forces base in Amirli). A powerful pro-Iran faction of parliament has called Israel’s alleged attacks “a declaration of war”.

Aftermath of the recent ‘mystery blast’ at a military base southwest of Baghdad. Image source: AP

The Associated Pressreports in the aftermath of yet another Israeli drone strike targeting and killing a Kataeb Hezbollah leader in al-Qaim, Iraq near the Syrian border that, “A powerful bloc in Iraq’s parliament is calling for the withdrawal of U.S. troops from Iraq following a series of airstrikes blamed on Israel targeting Iran-backed Shiite militias in the country.”

The influential and powerful Fatah Coalition, representing the country’s pro-Iranian Popular Mobilization Forces (PMF) issued a statement Monday holding the United States responsible for facilitation Israeli aggression on Iraqi soil, “which we consider to be a declaration of war on Iraq and its people,”the statement said. The statement noted further that American troops are no longer needed and only now serve to jeopardize Iraqi national security.

PMF commanders and officials have over the past weeks been the most vocal part of Iraq’s military and government blaming the recent spate of devastating attacks on Israel; however, following last week’s explosion at a base outside Baghdad – believed the result of an Israeli airstrike – it appears this view is now gaining support even from the prime minister’s office amid an ongoing official investigation into the blasts.

Footage showing the August 12th arms depot blast, widely blamed on Israel. Another strike on a munitions storage depot occurred on Aug. 20, and before this a July 19 attack grabbed headlines.

Last week Prime Minister Abdul-Mahdi had called foran end to all “unauthorized flights” including US drones, spy planes, jets, or helicopters. The directive demanded that all aerial vehicles comply with Iraqi law and operations must be under Iraqi government authorization.

via ZeroHedge News https://ift.tt/2L8NZGe Tyler Durden

At the end of last week, the trade war between the United States and China escalated dramatically, and investors all over the globe really started freaking out. Unfortunately, developments over the weekend have only made things worse, and that means that this could be a very “interesting” week for global financial markets. As I write this article, stock prices around the world are plunging, the price of gold is spiking and the Chinese yuan is crashing. There is clearly a lot of fear out there right now, and at this point even CNBC is warning that the last week of this month “could be highly volatile”…

The final week of August – the bittersweet end of summer for many – could be highly volatile, as markets fret over the economy and the latest developments in trade wars.

Of course things can swing rapidly from moment to moment in this environment. President Trump could say something in a few hours that temporarily gives investors some hope, and that could cause markets to swing wildly upward for a little while. Everyone is on edge right now, and every piece of significant news is likely to cause gyrations in the marketplace.

But overall the trend is clearly down. U.S. stocks have now fallen for four weeks in a row, and many are becoming deeply concerned about what September will bring.

And for many U.S. businesses, this trade war has turned into a complete nightmare. Executives crave predictability, but now everywhere we look there is chaos, and this is causing a lot of headaches for business leaders…

Businesses crave predictability so they can make informed decisions and plan for the future. Many companies that depend on Chinese manufacturers and consumers have already shifted supply chains out of the country and taken other steps to reduce their exposure to China. And while Mr. Trump’s tweets are unlikely to trigger immediate changes, more uncertainty is unwelcome.

“Continued escalation and rhetoric are harmful to American businesses, workers and farmers,” said Tom Linebarger, chief executive of Cummins Inc., which makes diesel engines. Cummins pays a tariff on components it imports from its own plants in China for engines assembled at U.S. factories by American workers. The tariffs amount to a tax paid by Cummins’ customers, he said.

Unfortunately, nobody can no longer deny that global economic activity is really starting to slow down. We just learned that global trade was down 1.4 percent in June from a year earlier, and that represented the largest decline that we have seen since the last financial crisis…

World trade volume – a measure of imports and exports of merchandise across the globe – declined in its zigzag manner in June to the lowest level since October 2017, according to the Merchandise World Trade Monitor by CPB Netherlands Bureau for Economic Policy Analysis. The index was down 1.4% from June 2018. This small year-over-year decline is the biggest year-over-year decline since the Financial Crisis, and it’s a reversal from the heady growth in 2017 and 2018 that had topped out at 6.7%.

I have been using phrases like “since the last financial crisis” and “since the last recession” in almost every article recently. We are seeing so many things happen that we haven’t seen for a decade or longer, and yet most Americans still don’t seem to understand that we have a real crisis on our hands.

If the U.S. and China were to mend their relationship and agree to a comprehensive trade deal, that would certainly help things.

When asked if Trump had second thoughts about Friday’s move to escalate the trade war with China, Trump said “Yup.” “I have second thoughts about everything,” he added.

Hours later, the White House issued a statement saying that Trump meant to say that he wished he had raised tariffs on Beijing even higher.

“His answer has been greatly misinterpreted. President Trump responded in the affirmative – because he regrets not raising the tariffs higher,” White House spokeswoman Stephanie Grisham wrote in a statement.

And the Chinese are warning that we should not “underestimate the determination” of the Chinese people and that they will be the ones to “have the last laugh”…

On Saturday, China’s commerce ministry issued a statement calling on Washington not to “misjudge the situation and underestimate the determination of Chinese people” after US President Donald Trump announced new tariffs on Chinese imports.

“The US should immediately stop its wrong action, or it will have to bear all consequences,” the statement said.

At the same time, a sharply worded commentary in the official party mouthpiece, People’s Daily, said China had the strength to continue the dispute and accused Washington of sacrificing the interests of its own people. Published under the pseudonym “Wuyuehe”, the piece described the latest tariff measures by the US as “barbaric”. The op-ed said China’s own tariffs on $75 billion worth of American products, announced late on Friday, were a response to America’s unilateral escalation of the trade conflict, and vowed that China was determined to fight back “until the end”.

“China’s will to defend the core interests of the country and the fundamental interests of the people is indestructible, and will not fear any challenge,” the author wrote, promising that “history will prove that the side on the path of fairness and justice will have the last laugh.”

As I have repeatedly warned, there isn’t going to be a trade deal before the 2020 presidential election.

So that means that things are going to get progressively worse, and we need to be prepared for a lot of economic pain.

Sen. Lindsey Graham, R-S.C., said on Sunday that Democrats should not criticize President Trump for taking on China over trade as they have complained for years about Beijing’s policies but done nothing.

“Every Democrat and every Republican of note has said China cheats,” Graham said on CBS News’ “Face the Nation.” “The Democrats for years have been claiming that China should be stood up to, now Trump is and we’ve just got to accept the pain that comes with standing up to China.”

Sadly, the truth is that the American people are not well equipped to deal with pain. We have been spoiled by decades of debt-fueled “prosperity”, and even a relatively minor economic downturn would result in a massive national temper tantrum.

Right now our nation is a seething cauldron of anger and frustration, and the mainstream media is stirring the pot on a daily basis. It isn’t going to take much to spark an explosion, and this will especially be true the closer we get to the next presidential election.

The season of “the perfect storm” is upon us, and what is coming next is going to be one of the most chaotic chapters in modern American history.

via ZeroHedge News https://ift.tt/30DOEGe Tyler Durden

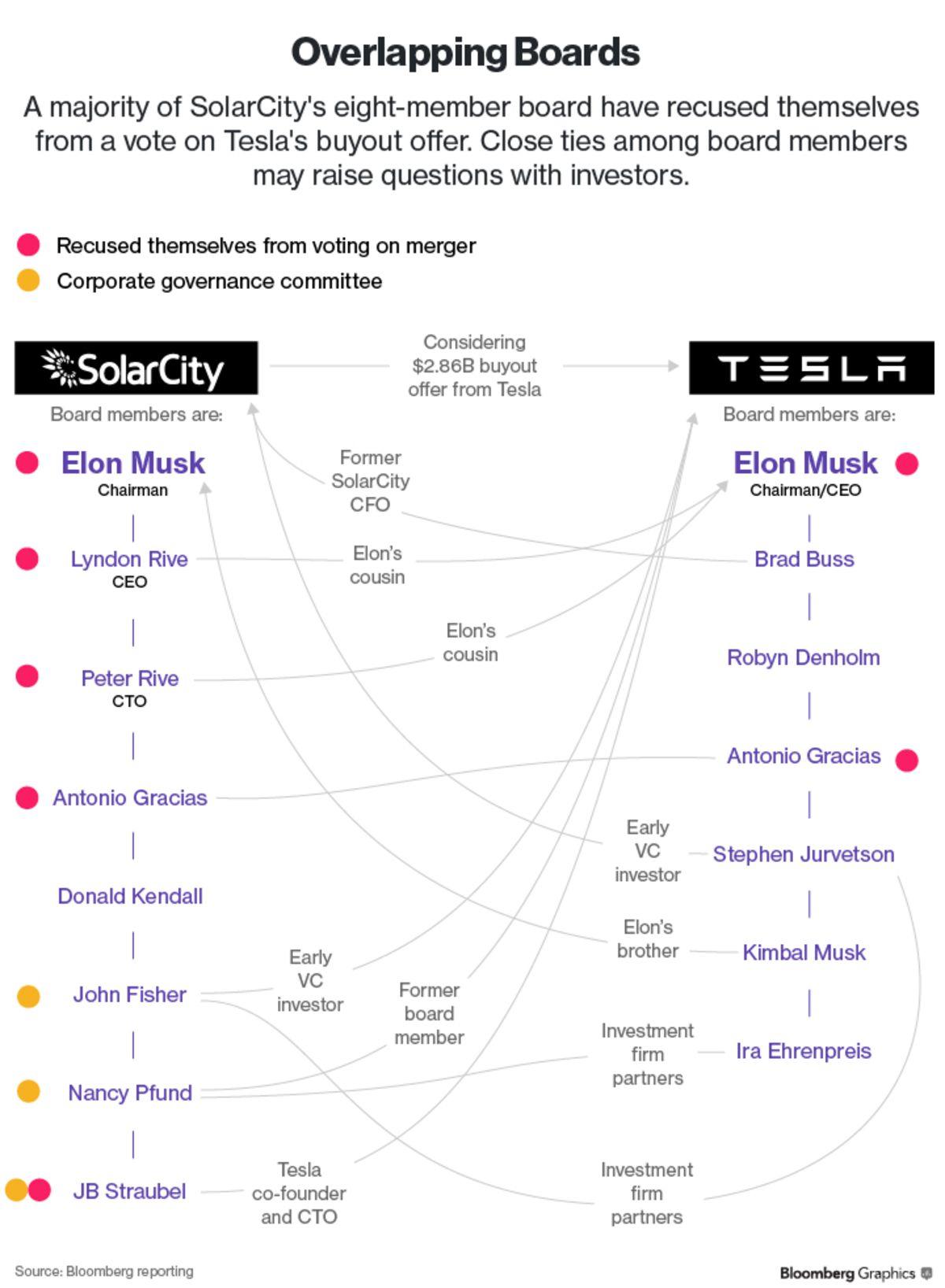

Bethany McLean’s reputation proceeds her, with good reason. She’s mostly known for tackling the Enron scandal and the 2008 financial crisis – two of the biggest financial frauds over the last decade or now. She co-authored Enron: The Smartest Guys in the Room, which was later made into a movie.

And now, she’s setting her sights on Elon Musk and Solar City, something we expected was about to happen last week.

As we said yesterday during our report about Vern Unsworth’s lawyer threatening Elon Musk, the boy wonder has created so many legacy legal liabilities, it is tough to track which ones – and when. Now, it’s appears that one of the biggest whoppers, his “bail out” of Solar City that skeptics such as this website and countless others long believed to be a sham, has finally been thrust into the limelight by an author whose gravitas simply can’t be ignored.

McLean’s Vanity Fair expose begins by focusing on Dennis Scott, a former Buffalo Tesla solar plant employee who was laid off. After being fired, he took to Twitter and randomly re-tweeted a “goofy” photograph of CEO Elon Musk holding something that looked like a machine gun. Scott said: “If I were CEO and someone told me my company wasn’t working right, I wouldn’t be clowning around. I’ve got people counting on me for their livelihood.”

Hours later, his phone rang. “It’s the clown,” the person on the other end said.

For the next 20 minutes, he had a discussion with Tesla CEO Elon Musk. He claims that Musk was “pleasant” but Scott peppered him with questions. “When are you going to fix your company?” Scott asked. “You took $750 million from New York. You gave us hope that you were going to do something.”

Scott said Musk’s responses left him unimpressed: “Musk is a nice guy when you talk to him. But I think he’s full of shit. He’ll tell you whatever you want to hear.”

The article notes that Musk doesn’t speak much about the company’s factory in Buffalo nowadays, which was actually once dubbed “Gigafactory 2”. The plan in Buffalo was, after Tesla’s purchase of Solar City, to build the largest manufacturing facility of its kind in the western hemisphere, producing 10,000 solar panels per day and creating 5,000 jobs in the area. The building is 1.2 million square feet and stands on the Buffalo River, which is replete with abandoned grain elevators and desolate steel mills.

But serious doubts have risen lately about Solar City. Tesla is being sued for the acquisition of the company and former employees want to know what happened to the massive subsidies that Tesla received.

“New York State taxpayers deserved more from a $750 million investment,” a laid-off employee named Dale Witherell wrote to Senator Kirsten Gillibrand. “Tesla has done a tremendous job providing smoke and mirrors and empty promises to the area.”

And just last week, we reported that Walmart sued Tesla, claiming that its solar panels started fires on seven of its store roofs.

The Buffalo plant wasn’t just supposed to save the world with solar, it was supposed to revitalize a poor area. Laid off employee Dale Witherell, for instance, was thrilled to get the job after a divorce and while caring for his disabled daughter. He also believed in the product.

Witherell said: “At some point push is going to come to shove in our world, and fossil fuel use is going to catch up with us. I believed in the product.”

But the Buffalo plant looks as though it’s going to go down in history as just more proof that the government can’t spend your money any better than you, or the free market, can. The plant was part of Governor Andrew Cuomo‘s plan to revitalize upstate New York and in 2014, Cuomo claimed that the plan was “of critical importance to the United States’ economic competitiveness and energy independence.”

From there, the expose points out how two of Musk’s cousins that grew up with him in South Africa (and founded Solar City) were bailed out by Musk’s investment in the company – and later by Tesla’s acquisition of the company.

It highlights how Solar City’s business model changed from installing solar panels to allowing homeowners to pay over time, which created a constant need for cash. All of this was happening while, on the consumer side, customers were complaining about misleading sales tactics and shoddy installations.

Employees started to feel manipulated by the company’s talk about its altruistic mission.

“I turned a blind eye to a lot of the silliness because of the idealism,” says one former senior employee. “I don’t know when the Rubicon was crossed, but there were micro-crossings every day.”

In 2014, Solar City bought Silevo, a solar panel manufacturer, in order to try and build its own solar panels after the board was “growing concerned” about its business model. One former senior employee said of the strategy: “It was shoot first and aim later. There was a lot of machismo going on: bigger, better, badder, faster.”

But the sweetheart deal continued to be pushed further by Governor Cuomo.

By the time Cuomo visited the site three months later, Silevo’s smallish deal had metastasized. The state promised to spend $350 million to build a factory and another $400 million on equipment specified by SolarCity. The company would get a 10-year lease on the facility—for just $1 a year. In return, it promised to employ at least 1,460 people in “high-tech” jobs at the factory, hire another 2,000 to support the sale and installation of solar panels in New York, and help attract an additional 1,440 “support jobs” in the state. Once it achieved full production, the company pledged, it would spend some $5 billion in New York over the following decade.

“It was sold as a perfect marriage,” says the former senior employee. “The area around the factory is terrible, and I remember thinking: Wow, we are going to save the town where steel was made.” Cuomo too was hooked. “He was enchanted with the idea of Elon Musk in Buffalo,” says a longtime lobbyist in Albany. “I think he actually thought Musk was the next Dalai Lama.”

The situation got really ugly toward the end of 2014 when executives begin to exit and Solar City had trouble raising money. It issued what it called “Solar Bonds”, but the market interest was tepid. As a result, SpaceX acquired $255 million of these bonds and Musk himself bought $75 million of them. Musk borrowed against his Tesla and Solar City stock in order to do so. Musk also tried to stop the bleeding in 2016 when Solar City stock plunged and Musk bought $10 million in shares.

Then, after burning through $659 million in the first quarter of 2016 alone, Musk finally proposed that Tesla acquire Solar City.

Even though the board balked at first, Musk kept pushing and finally got the board to agree. Meanwhile, a judge in a shareholder lawsuit recently ruled that it is “reasonably conceivable” that Musk had active control over the Tesla board when he pushed for the acquisition.

Days before shareholders were set to vote on the acquisition of Solar City, Musk gave the now infamous “Solar Roof” presentation, promising that production would begin the following summer. On that note, shareholders had their cue to approve the acquisition, which they did. As a result, Musk converted his stake in Solar City into $500 million in Tesla stock.

The solar roof, three years later, still has not come to mainstream fruition.

Finally, the expose concluded by pointing out how Musk’s stunts are starting to come off as unhinged instead of iconoclastic. And it shows that Musk has a track record of not following through. For instance, it brings up an example of how, in 2001, he offered to give away half of his equity in PayPal, dividing it evenly between employees and altruistic causes, but then never follow through on the pledge. Some people see Musk as purposely manipulative, others just see him as bombastic and overly optimistic, the article notes.

Tesla, in truly ridiculous fashion, defended itself by literally accusing McLean of spreading “FUD” – fear, uncertainty and doubt – a phrase notoriously overused by basement dwelling bagholders of worthless securities that find themselves underwater and desperately looking for a scapegoat:

In a statement to Vanity Fair, Tesla argues that its jobs in Buffalo are competitive, especially when benefits and equity are factored in. It says it has expanded its operations at the factory to include “some of our most innovative and pioneering products.” And it accuses the magazine of presenting a “one-sided view with cherry-picked sourcing aimed at feeding into the fear, uncertainty, and doubt being circulated about Tesla every day by those looking to gain from Tesla’s losses.”

The expose wraps up by highlighting several members of the “$TSLAQ” community on Financial Twitter, like @TeslaCharts, who happens to be a PhD, solar panel expert and recently did a lengthy podcast critical of Tesla’s solar business.

It ends by describing how Solar City’s business, now tucked into Tesla, has all but collapsed.

“Total implosion” is how one Solar City insider described it in the article.

Though there were some rumors that the presser might be called off at the last minute, President Trump and French President Emmanuel Macron were set to hold a joint news conference Monday in Biarritz on the final day of this G-7 summit.

According to the latest update, the news conference was slated to begin at 10:30 am ET. The two leaders were expected to discuss the Iran Deal – seeing as Macron had quietly invited Javad Zarif, Iran’s foreign secretary, to the summit. President Trump insisted on Monday that Macron had asked his permission before inviting the top Iranian diplomat.

Washington sources said Trump didn’t have any contact with Zarif.

The two leaders appear to be on better terms now that they have largely put Trump’s threats behind them. While the two have a tendency to “go at each other a little bit,” Trump said, they still have a “special relationship.”

We suspect the number one question to Trump will be on whether or not a call took place with China overnight, and whether he and Mnuchin lied (as China claims).

It’s also likely that the two leaders will also be asked about the prospects for the White House to slap tariffs on French wine and cheese, whether the G-7 will invite Russia to rejoin it next year, as well as the Paris Climate Accord and Iran Deal, among other questions.

Watch the news conference live below:

via ZeroHedge News https://ift.tt/2MEF6qR Tyler Durden

{kind=link}

{kind=link}

{kind=link}