After Democratic 2020 candidate Rep. Tulsi Gabbard (D-HI) dressed down Sen. Kamala Harris (D-CA) over her criminal justice record, Harris hit back – suggesting that Gabbard is somehow ‘below her’ – and an “apologist” for Syrian dictator Bashar al-Assad.

In case you missed the original smackdown:

In response, Harris thumbed her nose at Gabbard, telling CNN‘s Anderson Cooperafter the debate: “This is going to sound immodest, but obviously I’m a top-tier candidate and so I did expect that I’d be on the stage and take some hits tonight … when people are at 0 or 1% or whatever she might be at, so I did expect to take some hits tonight.”

Harris added “Listen, I think that this coming from someone who has been an apologist for an individual, [Syrian President Bashar al] Assad, who has murdered the people of his country like cockroaches. She has embraced and been an apologist for him in the way she refuses to call him a war criminal. I can only take what she says and her opinion so seriously, so I’m prepared to move on.”

Wait a second…

Tulsi wasn’t having it. In a Thursday interview with CNN‘s Chris Cuomo, Gabbard punched back – saying “[T]he only response that I’ve heard her and her campaign give is to push out smear attacks on me, claim that I am somehow some kind of foreign agent or a traitor to my country, the country that I love, the country that I put my life on the line to serve, the country that I still serve today as a soldier in the Army National Guard.”

Gabbard also made clear that she believes Assad is “a brutal dictator, just like Saddam Hussein, just like Gaddafi in Libya,” adding “The reason that I’m so outspoken on this issue of ending these wasteful regime change wars is because I have seen firsthand this high human cost of war and the impact that it has on my fellow brothers and sisters in uniform.“

via ZeroHedge News https://ift.tt/2KiqJ8a Tyler Durden

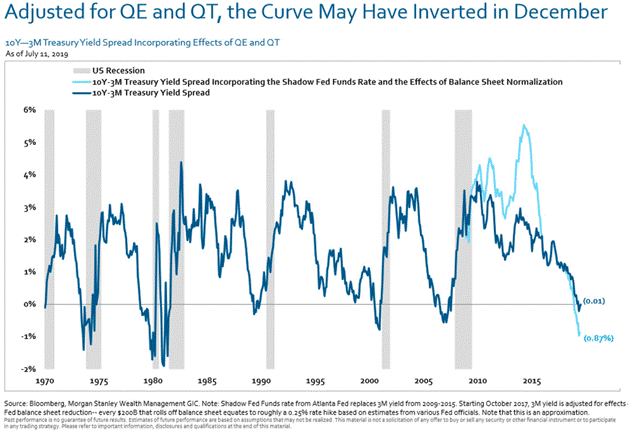

The inverted yield curve is one of the more reliable recession indicators.

I discussed it at length last December. At that point, we had not yet seen a full inversion. Now we have, and it appears the curve was “inverted” back then, and we just didn’t know it.

Now if you assume, as Morgan Stanley does, every $200B balance sheet reduction is equivalent to another 0.25% rate increase, which I think is reasonable, then the curve effectively inverted months earlier than most now think.

Worse, the tightening from peak QE back in 2015 was far more aggressive and faster than we realized.

Worrisome Charts

Let’s go to the chart below. The light blue line is an adjusted yield curve based on the assumptions just described.

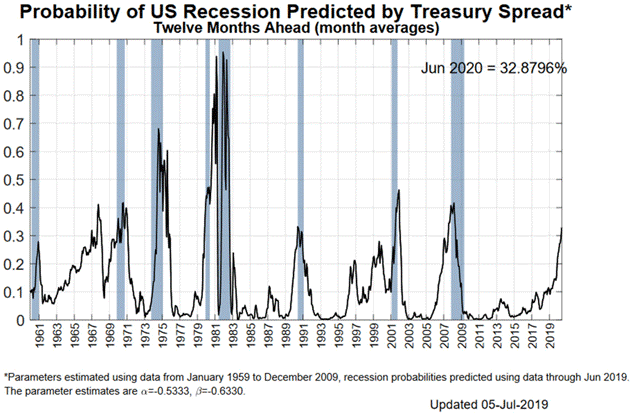

But even the nominal yield curve shows a disturbingly high recession probability. Earlier this month, the New York Fed’s model showed a 33% chance of recession in the next year.

Their next update should show those odds somewhat lower as the Fed seems intent on cutting short-term rates while other concerns raise long-term rates.

But it’s still too high for comfort, in my view.

But note that whenever the probability reached the 33% range (the only exception was 1968), we were either already in a recession or about to enter one.

For what it’s worth, I think Fed officials look at their own chart above and worry. That’s why more rate cuts won’t be surprising.

And frankly, and I know this is out of consensus, I would not rule out “preemptive quantitative easing” if the economy looks soft ahead of the election next year. Just saying…

But that’s not everyone’s view.

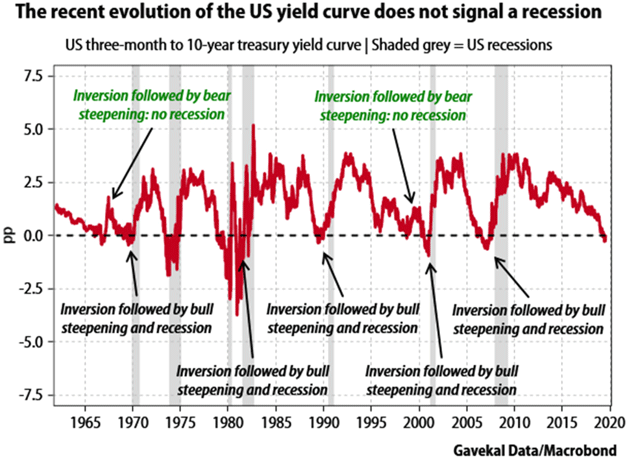

The Other Side of the Argument

Gavekal Research gives us this handy chart showing inversions don’t always lead to recession right away. (I noted 1968 above and I think 1998 is a separate issue. But then again, that’s me.)

Fair enough; brief inversions don’t always signal recession. But as noted, when you consider the balance sheet tightening, this one hasn’t been brief.

Note also that an end to the inversion isn’t an all-clear signal. The yield curve is often steepening even as recession unfolds.

One thing seems certain: While the yield curve may not signal recession, it isn’t signaling higher growth, either. The best you can say is that the mild expansion will continue as it has. That’s maybe better than the alternative, but doesn’t make me want to pop any champagne corks.

The Fed has always been behind the curve. To Powell’s credit, he may be trying to get in front of it, at least this time.

* * *

The Great Reset: The Collapse of the Biggest Bubble in History – New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

via ZeroHedge News https://ift.tt/2ywXbht Tyler Durden

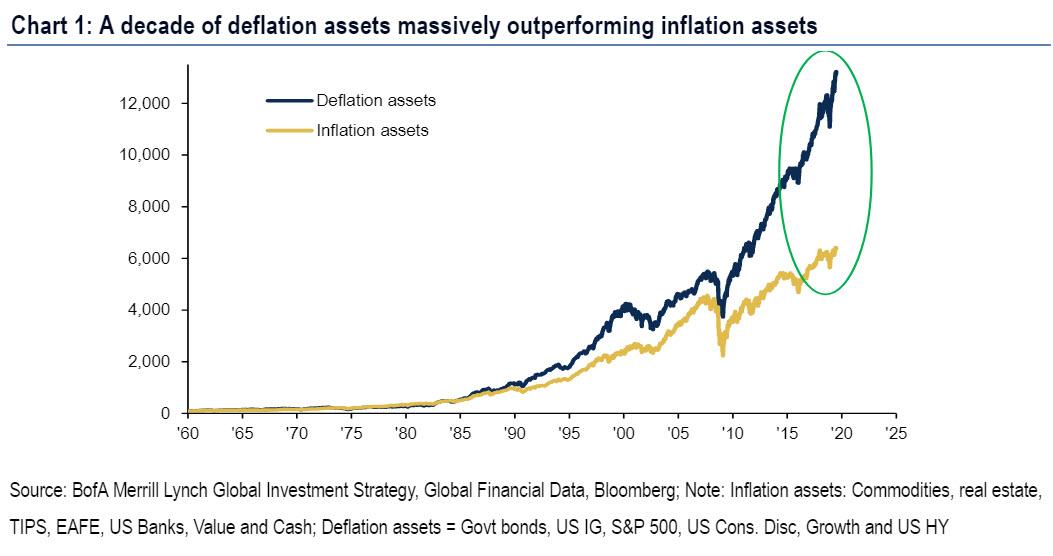

Fishing for some fascinating trivia about the “New Abnormal” period we live in? Here are ten remarkable observations from BofA’s Micharl Hartnett that demonstrate that we live in a time like no other.

Fed cut makes it 729 global central bank cuts since Lehman bankruptcy.

Soaring US consumer confidence at highest level vs. plunging German business confidence since Q4’98…when Fed cut rates “mid-cycle” igniting bubble of ’99.

EM equities at lowest level vs. US equities since 2003…China weak, US$ strong.

Wall St (US private sector financial assets) now 5.5x the size of Main St (US GDP)… between 1950 & 2000 the norm was 2.5-3.5x…Wall Street is now “too big to fail”.

Global debt now 3.2x the size of global GDP, an all-time high.

Fresh China tariffs in Sept would raise average US tariff on total imports to 5.6% from 4.5%, highest since 1972…was 1.5% before Trump.

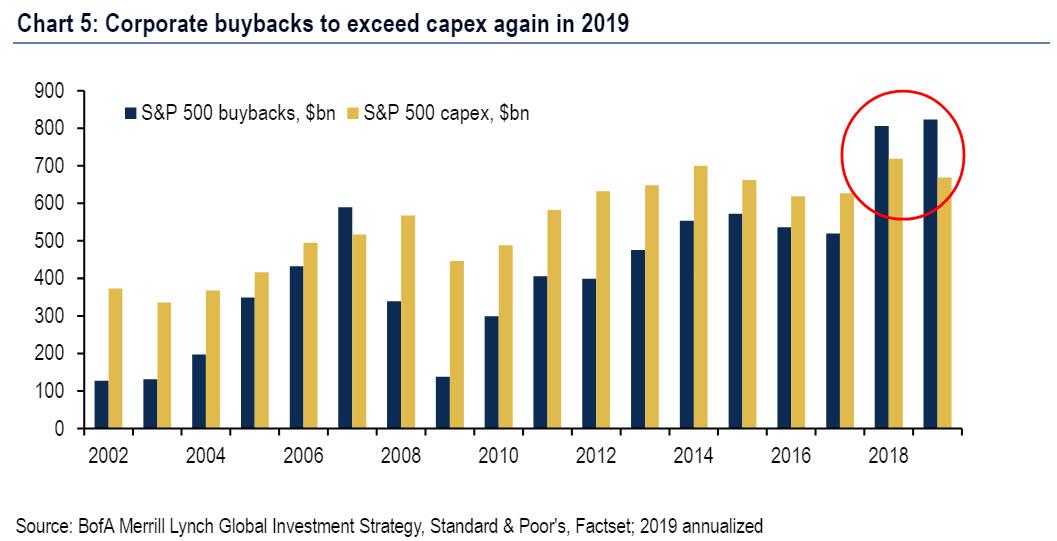

US companies spent $114 on buybacks for every $100 of capex in past 2 years… between 1998 & 2017 they spent $60 for every $100 of capex.

Inflows to bond funds ($278bn) rising at a record pace in 2019.

Past 10 years $4.1tn into passive investment funds vs. $1.5tn out of active funds.

Just 6% of MSCI ACWI stocks account for 53% of YTD global equity return.

As Hartnett summarizes, “the above reflect a decade of Maximum Liquidity & Minimal Growth, of tech disruption, aging demographics & Chinese rebalancing, of polarized outperformance by deflation assets (US stocks, HY bonds, growth stocks) vs. inflation assets, of expectations for higher inflation, yields, volatility consistently being dashed.

His contrarian recommendations for 2020s:

“long inflation” & “short Wall St” driven by populism, protectionism, policy impotence, popping bond bubbles, peak globalization.

In short: brace for the deflationary ice age end of the world as we know it.

via ZeroHedge News https://ift.tt/2ZrzlQ5 Tyler Durden

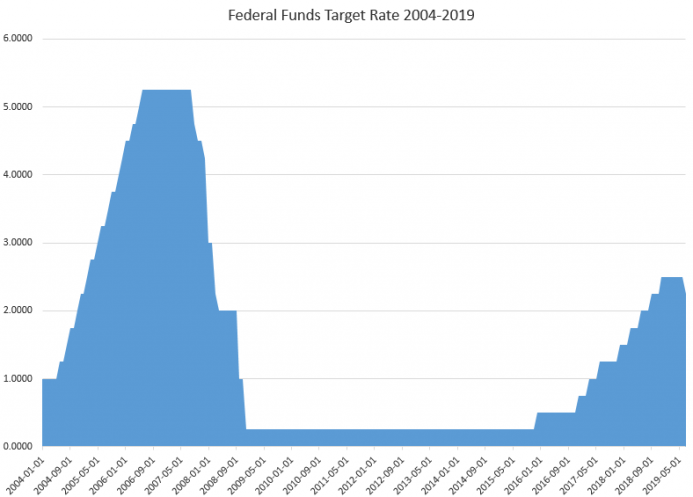

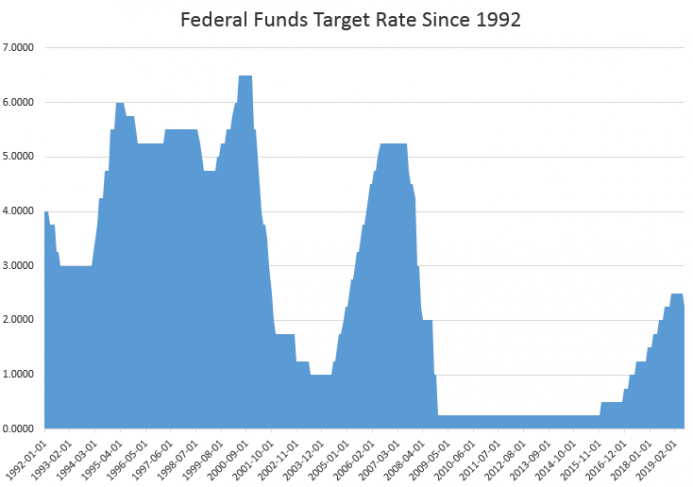

This week, the Fed’s Federal Open Market Committee lowered the target federal funds rate by 25 basis points, dropping it to 2.5 percent. The Fed had last changed its target rate in December of 2018, when it raised the rate from 2.25 percent to 2.50 percent.

It now looks like 2.5 percent is the highest the rate is going to get for the foreseeable future. After all, according to the Fed, the current state of the economy is “moderate” and the job market “strong.” If the economy needs a rate cut under these conditions, it’s hard to imagine a situation in which the Fed will be enthusiastic about another rate increase.

On the other hand, it’s entirely possible the rate cut is not motivated primarily by economic data, but by politics. Donald Trump has repeatedly and publicly pressured the Fed for a rate cut for many months.

It could be that the political pressure has had the desired effect. Economists — who are generally childlike in their naïve and fanciful views of how the political system works — actually appear to think the Fed is “independent” from the political system, or that it at least has been in the past.

But that’s not the reality, and the Fed, for all its protestations of independence, may simply be doing what it has always done. If this alleged independence appears to have diminished in recent times, of course, the difference is really only that Trump is simply more public about the pressure he applies. Past presidents and policymakers have tended to stick to applying pressure behind closed doors.

Fed Admits Economy Weaker than It Says

But, for the sake of argument, let’s assume that the rate cut comes primarily as a result of Fed economists’ consideration of the data.

If the conclusion was that a rate cut was now warranted, this tells us that the economy is not really as strong as the Fed has long pretended it to be. This has been obvious for years, of course.

For a decade, the Fed told us the “recovery” was proceeding nicely, but “oh by the way, we don’t dare allow interest rates to increase to anything resembling even 1990s-type rates.”

Thus, the fed funds rate sat at 0.25 percent from 2008 to 2015. And it was barely allowed to inch up much after that. And now it seems that even 2.5 percent is too much for the fed to stomach.

Inflation and the Phillips Curve

To explain this all away, the Fed has invented the “two-percent” which is a totally arbitrary number at which the economy is functioning with a healthy inflation rate. The fact that years of “strong” job growth hasn’t led to the “official” inflation rate reaching 2 percent suggests that either the method of measuring inflation is wrong, or the economy is weaker than the Fed thinks it is.

It’s possible that both factors are contributing. It’s possible that real wage growth is insufficient to drive sizable inflation. This, after all, is what has long been gospel among mainline economists: strong employment leads to higher inflation. But that doesn’t seem to be the case anymore, and Chairman Powell has even admitted this relationship — described by the Phillips Curve — doesn’t apply anymore.

This is a big admission by a Fed chairman given the importance of the Phillips Curve to the Fed’s economic analysis. The fact the Fed is confused by the apparent irrelevance of the Phillips Curve means the Fed is flying blind.

On the other hand, it could be that the inflation measure is simply wrong. The CPI has long been a measure based on a lot of arbitrary judgment calls, such as those that go into hedonic pricing. This method is used to push down inflation rates by claiming price increases aren’t as big as they seem because products have increased in quality. The reality for most people is that cars simply cost more now — although hedonic pricing would suggest the price of cars hasn’t really increased. But saying those aren’t real prices increases because they reflect increases in quality is a pretty tone-deaf way of looking at inflation.

So, it’s hard to know exactly what’s driving the thinking behind the rate cut. Is it politics? Do Fed members believe their inflation data? Or is the economy truly weaker than the headline data suggests?

We can only guess at the moment. We only know that the Fed is mostly blowing smoke when it tells us that the economy is fine, but we also need a rate cut. Either the Fed doesn’t know what’s going on, or it’s lying about the economy being “strong.” Or it’s just doing what Trump is telling it to do.

Keeping Interest Rates Low as Debt Rises

Another issue that must be mentioned in the importance of keeping interest rates low in an environment of runaway government spending.

As the national debt continues to rise above $22 trillion, and as the annual deficit — in a period of “expansion,” mind you — inches back toward one trillion per year, it becomes ever more important to keep debt service low by pushing down interest rates. As debt payments rise toward half a trillion dollars per year in the coming years, interest rates must be kept low, or federal programs will face real cuts in order to make payments on the debt. That means cuts to things like the Pentagon and Social Security. Those cuts would be politically unpopular. Thus, policymakers will need the Fed to keep debt payments down by manufacturing demand for government debt — via artificially low interest rates.

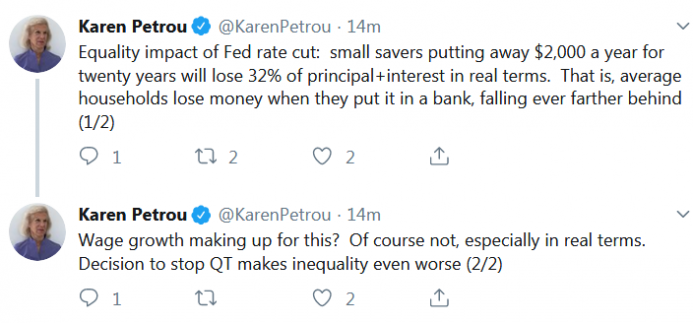

For ordinary and conservative savers, the effect of more than a decade of ultra-low rates has already been devastating. Thanks to the Fed, we now live in an economy designed for the ultra-rich on Wall Street who can afford to chase yield through high-risk investment instruments. For ordinary families who must save through lower-yield and lower-risk methods like savings accounts, this means they will continually lose purchasing power.

Fed policy has long been a war on ordinary families and savers. It’s a policy for the wealthy, and it worsens income inequality, as Petrou notes.

Future Problems

With the target rate now inching back toward 2 percent, the Fed will have even less room to maneuver when the next recession comes. But we don’t even need to wait for that. As Brendan Brown recently explained, we can already see the effect of ultra-low rates in increasing anemic economic growth numbers, and in withering real world savings and capital accumulation. We may not see a dramatic, crash, but simply see growth continue to under-perform.

In any case, the future doesn’t look good for people on fixed income, middle-income savers, or people in general who aren’t already property-owning millionaires.

via ZeroHedge News https://ift.tt/2Mzw9yr Tyler Durden

With the past 3 days sending a shockwave of sentiment reversal around global markets, as first Powell then Trump double-teamed to stun bulls to the point where even grizzled veteran traders like Nomura’s Charlie McElligott said that “That Was One Of The Most Manic 36 Hours Of Trading In My 18 Year Career“, the question many traders are now asking, namely “was this the top” is unlikely to have a positive response, at least not yet.

The first reason why stocks likely have at least one more push higher before the “big fall” is that following the current wobble coming in a period of dovish central bank reversal (which needs a favorable market reaction to avoid being seen as policy failure) is that we will now see another wave of fresh Central Bank “capitulatory easing”, with the danger of a ripping-rally thereafter even more clear when one considers the technicals, i.e,, “the amount of dynamic hedging Futures Shorts laid-out yesterday—as well as the fact that Equities funds were violently pressing their Shorts.”

Another five reason come this morning from Bank of America’s CIO Michael Hartnett who lays out “the case for further upside in risk assets“, which are as follows:

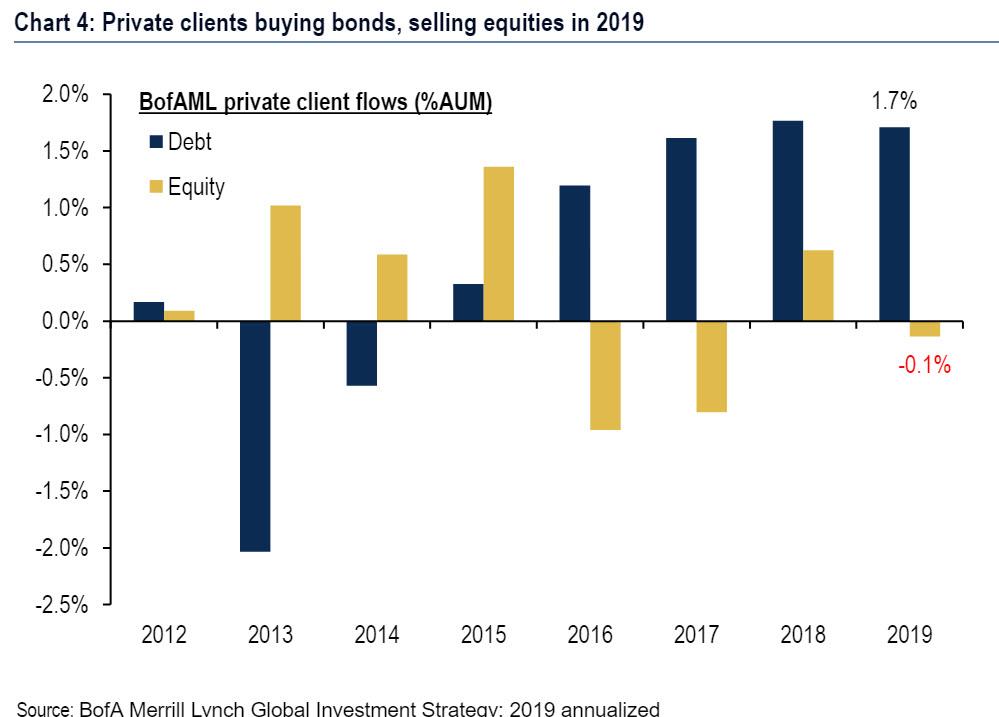

1. There’s no euphoria in global equities: YTD $152 billion in outflows from stocks corroborated by -0.8sd global equity underweight relative to 20-year history in BofAML Global Fund Manager Survey. In the same time there have been record inflows to bonds in in 2019 coinciding with another year of BofAML private clients adding to bonds; As a result, any hint of a late-summer pulse in the global economy leading to a rise in yields would drive rotation from cash & bonds to stocks.

2. US stock buybacks: on course for record $823 billion in 2019: of note, corporations will for 2nd year running spend more on stocks than capital equipment); US companies spent $114 on buybacks for every $100 of capex in past 2 years (vs. $60 for every $100 of capex in prior 19 years), which as even politicians have figured out, is “good for Wall Street, bad for Main Street.”

3. The price of money continues to fall: lower rates have been the driver of the bull market in corporate bonds & equities; key is whether and how forcefully the PBoC joins Fed/ECB easing; in the US, there is limited evidence of Fed policy impotence (lower rates, lower spreads, higher US bank stocks YTD); melt-up risk remains 1998 redux when “mid-cycle” insurance cuts quickly inflated asset prices the moment growth expectations troughed.

4. The US consumer fine and dandy: level of US consumer confidence relative to German business confidence highest since Q4’98.

5. The ECRI US lead indicator has inflected higher, correlates strongly with ISM index; global inventory-shipment ratio has stabilized in recent months and global earnings revisions edging higher; Emerging Market stocks at 16-year low vs. US stocks illustrates bad China/Asia/global macro priced-in.

* * *

That said, one can just as easily counter that the topic has already been seen in the S&P500, in line with the conventional wisdom that when the Fed cuts rates, a recession usually follows… and the market is not too far behind. Below is Hartnett’s “case for downside in risk assets.“

1. The Fed cut this week but financial conditions did not ease: US dollar appreciated, yield curve steepened, credit spreads rose…first hints of US policy impotence.

2. “Trade war” is getting worse: fresh China tariffs in Sept would raise average US tariff on total imports to 5.6% from 4.5%, highest since 1972 (the level was 1.5% before Trump).

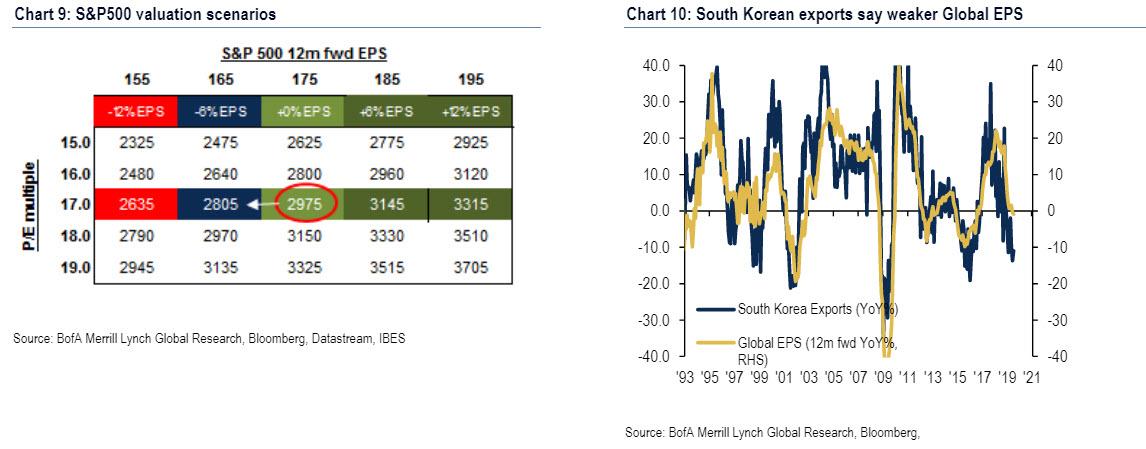

3. BofAML Global EPS Growth Model says EPS recession: model forecasts -7.5% global EPS growth next 12-months driven by stagnant PMIs, weak Asian exports, flattening yield curves, tighter Chinese financial conditions. A projected 5% cut in US EPS even assuming a stable PE of 17.0x PE would imply SPX @ 2800.

4. Euphoria in fixed income: era of Maximum Liquidity & Minimal Growth (and Inflation and Volatility) driving massive capitulation into bonds; nouveau bulls should be wary of deterioration in corporate credit, most ominously spread between HY CCC-rated bonds and BB-rated bonds (aka the “credit curve”, a lead indicator for HY corporate bond spreads) touched 3-year high this week.

5. Equity fast money long: BofAML equity hedge fund client ratio of long-short positions relative to total assets currently 0.63 (0.7sd above norm); US options market shows $469bn delta-adjusted open interest (1.1sd above norm and approaching 1.5sd warning level – Chart 11).

6. Bull market in stocks is very narrow: 6% of MSCI ACWI stocks account for 53% of YTD global equity return and 1803 global stocks (out of 2750) remain in bear market; this is driven by the accelerating shift from active to passive (YTD equity passive inflows $74bn vs. $224bn active outflows).

via ZeroHedge News https://ift.tt/2YHUcl2 Tyler Durden

Less than a week after Dan Coats stepped down and President Trump nominated John Ratcliffe as Director of National Intelligence, the Texas Representative has, according to a tweet by the president, withdrawn his nomination after scrutiny of his qualifications for the position.

Trump blamed the decision on Ratcliff “being treated very unfairly by the LameStream Media,” adding that “rather than going through months of slander and libel, I explained to John how miserable it would be for him and his family to deal with these people.

Trump added that ” John has therefore decided to stay in Congress,” and will announce a new nomination for DNI shortly.

Our great Republican Congressman John Ratcliffe is being treated very unfairly by the LameStream Media. Rather than going through months of slander and libel, I explained to John how miserable it would be for him and his family to deal with these people….

….John has therefore decided to stay in Congress where he has done such an outstanding job representing the people of Texas, and our Country. I will be announcing my nomination for DNI shortly.

As The Hill concludes, Trump’s abrupt announcement came after days of scrutiny of Ratcliffe’s background and past statements critical of former special counsel Robert Mueller’s Russia investigation. Several Republican senators had declined to weigh in on his nomination, as he withstood a barrage of criticism from Democrats.

via ZeroHedge News https://ift.tt/2KjUNAb Tyler Durden

The war of words between the world’s top superpowers is getting more heated by the hour.

China’s new ambassador to the United Nations, Zhang Jun, said on Friday that if the United States wanted to fight China on trade, “then we will fight” and warned that Beijing was prepared to take countermeasures over new U.S. tariffs, Reuters reports.

“China’s position is very clear that if U.S. wishes to talk, then we will talk, if they want to fight, then we will fight,” he told reporters. Calling Trump latest tariff announcement an “irrational, irresponsible act”, Jun said that China “definitely will take whatever necessary countermeasures to protect our fundamental right, and we also urge the United States to come back to the right track in finding the right solution through the right way.”

Zhang Jun, the new China’s permanent representative to the United Nations, speaks to the press at the UN headquarters in New York, July 30, 2019.

The ambassador also took a stab at the disintegration of good relations between the US and North Korea (with Beijing’s blessing no doubt), saying that “you cannot simply ask DPRK to do as much as possible while you maintain the sanctions against DPRK, that definitely is not helpful” Yun said siding the the Kim regime. It was more than obvious who the “you” he referred to was.

Pouring more salt on the sound, the Chinese diplomat said North Korea should be encourage, and “we think at an appropriate time there should be action taken to ease the sanctions”, explicitly taking Pyongyang’s side in the ongoing diplomatic saga between Kim and Trump.

When asked if China’s trade relations with the United States could harm cooperation between the countries on dealing with North Korea, Zhang said it would be difficult to predict. He added: “It will be hard to imagine that on the one hand you are seeking the cooperation from your partner, and on the other hand you are hurting the interests of your partner.”

As North Korea’s ally and neighbor, China’s role in agreeing to and enforcing international sanctions on the country over its nuclear and ballistic missile programs has been crucial.

However, it is what he said last that was most notable, as it touched on what will likely be the next big geopolitical swan, namely Hong Kong. To wit, Jun said that while Beijing is willing to cooperate with UN member states, it will never allow interference in “internal affairs” such as the controversial regions of Xinjiang and Tibet, and – last but not least – Hong Kong.

And in the latest warning to the defiant financial capital of the Pacific Rim, Jun virtually warned that a Chinese incursion is now just a matter of time, he said that Hong Kong protests are “really turning out to be chaotic and violent and we should no longer allow them to continue this reprehensible behavior.”

And so the die has been cast: Hong Kong’s protesting youth has been given its official warning, and with PLA forces now piling on the border, all that will take for Chinese troops to enter is a provocation.

And to show just how serious China is about all this spontaneous “rioting” nonsense, Reuters reported that Refinitiv (which Reuters owned), has removed from its Eikon terminals in China a Reuters story detailing how an official with Beijing’s Liaison Office in Hong Kong had urged residents of a rural area to drive away anti-government protesters days before a violent clash nearby.

The story, which was published late last week, was not visible on the Eikon terminal’s scrolling news feed in China on Friday. Eikon users outside China said they could still see the story. Reuters was unable to determine precisely when the story had been removed from Eikon’s scrolling news feed for clients in China or whether other stories had been blocked.

Refinitiv has a license to provide financial information in China, and a person familiar with the matter said Refinitiv’s regulator there, the Cyberspace Administration of China, or CAC, had said it would shut down the service unless it removed or blocked certain political stories.

“As a global business, we comply with all our local regulatory obligations, including the requirements of our license to operate in China,” Refinitiv said in a written statement to Reuters.

And that is all anyone needs to know about just how nervous China is over the ever growing protest movement in Hong Kong, and how terrified it is that it can eventually spread to the mainland.

via ZeroHedge News https://ift.tt/2GGXHOu Tyler Durden

After months of sternly refusing to pursue impeachment proceedings of Donald Trump over fears that this could have dire consequences for democrats at the polls, Nancy Pelosi suddenly finds herself in a bind. The reason: the movement to oust President Trump from office crossed a new threshold Friday, with a majority of House Democrats endorsing an impeachment inquiry — a development that puts the House majority speaker in confrontation with a majority of democrats, and could potentially lead to a fissure between moderate and progressive Democrats.

As of Friday, a majority of one – or 118 out of 235 House Democrats – said they support at least opening an impeachment inquiry, according to an analysis by The Washington Post. Politico, using different criteria, reported that the threshold was crossed Thursday.

As the WaPo notes the push in the House to remove Trump has been accelerated by testimony from former special counsel Robert S. Mueller III confirming that the president could be charged with obstruction of justice after he leaves office — prompting more than 20 Democrats to announce support for an inquiry since then. Those calls, the WaPo adds, have come amid mounting pressure from liberal activists — applied in some cases by Democratic primary challengers who argue that incumbents, including four powerful committee chairmen, have been too reticent in taking on Trump.

California Rep. Salud Carbajal pushed Democrats past the majority threshold with his announcement Friday. “We cannot ignore this president’s actions, and we cannot let him off the hook because of his title,” he said in a written statement.

Among those newly backing an impeachment inquiry are two prominent House committee chairmen from New York, Rep. Eliot L. Engel of the Foreign Affairs Committee and Rep. Nita M. Lowey of the Appropriations Committee. Both face energetic Democratic opponents in next year’s elections.

Of the Democrats calling for an impeachment inquiry, more than 75 have done so since Mueller made a public statement on May 29 about his findings. The former special counsel said he could neither clear nor accuse Trump of obstructing his probe, leaving room for Congress to make that call.

Rep. Justin Amash (I-Mich.), who recently left the Republican Party, has also said he supports beginning impeachment proceedings against Trump.

* * *

Finding herself trapped, while Pelosi continues to stress investigations over impeachment, last week she gave a green light for lawmakers to chart their own course while telling reporters that it would not necessarily change her views.

CNN’s in house democratic lackey, Brian Stetler, was quick to frame the question as one of Pelosi now ignoring the opinion of the majority, or “Can House Speaker Nancy Pelosi ignore this number?” adding that “That’s the biggest question” and “All eyes on the speaker at this point.”

“Can House Speaker Nancy Pelosi ignore this number?” @PamelaBrownCNN asks.

For now, Pelosi is willing to face the majority onslaught. “I’m willing to take whatever heat there is,” she said.

Pelosi refused to answer questions about impeachment during an appearance on Capitol Hill on Thursday.

Ironically, Pelosi appears to be all that is standing between what is now a majority of Democrats and political suicide: her reluctance about impeachment is based in part on public opinion. A Washington Post-ABC News poll released last month showed 59 percent of Americans believe the House should not begin impeachment proceedings against Trump, while 37 percent believe it should — including 61 percent of Democrats.

And when one considers just how titled to Democrats such polls are, it is safe to assume that only a small, but very vocal minority, of constituents actually want a Trump impeachment. Which also explains why the politically inexperience, ultra progressive wing of the Democrats is now willing to pursue a step that could cost Democrats dearly.

Stetler is right about one thing: all eyes are indeed on Pelosi. What she does next could end up handing the 2020 presidential election to Trump on a silver platter.

via ZeroHedge News https://ift.tt/2KiWJsR Tyler Durden

Tesla has now been sued for the second time in three months by the family of a car owner who was killed while using Autopilot, according to Bloomberg.

50-year-old Jeremy Banner died when his Model 3 sedan failed to break or avoid a semi trailer that ran a stop sign on a Florida highway in March. According to the lawsuit, which also named the semi driver as a defendant, Banner had engaged Autopilot about 10 seconds before the collision.

Tesla didn’t respond to Bloomberg’s request for a comment on the lawsuit, which makes the claim that the company knew its product was defective. We reported back in May that the National Transportation Safety Board had put out a preliminary report on the crash.

The report describes the events leading up to the incident:

As the Tesla approached the private driveway, the combination vehicle pulled from the driveway and traveled east across the southbound lanes of US 441. The truck driver was trying to cross the highway’s southbound lanes and turn left into the northbound lanes.

According to surveillance video in the area and forward-facing video from the Tesla, the combination vehicle slowed as it crossed the southbound lanes, blocking the Tesla’s path. The Tesla struck the left side of the semitrailer. The roof of the Tesla was sheared off as the vehicle underrode the semitrailer and continued south. The Tesla came to a rest on the median, about 1,600 feet from where it struck the semitrailer. The 50-year-old male Tesla driver died as a result of the crash.

The report then goes on to note that Autopilot had been engaged 10 seconds before the collision and that the vehicle, traveling about 68 mph, didn’t execute evasive maneuvers:

The driver engaged the Autopilot about 10 seconds before the collision. From less than 8 seconds before the crash to the time of impact, the vehicle did not detect the driver’s hands on the steering wheel. Preliminary vehicle data show that the Tesla was traveling about 68 mph when it struck the semitrailer. Neither the preliminary data nor the videos indicate that the driver or the ADAS executed evasive maneuvers.

Trey Lytal, a lawyer for the family said:

“We’re not just talking about the consequences of this defect to the Banner family, which is horrific. These products are defective.”

The lawyer compared the crash to one involving a Tesla Model S owner who died in a similar tractor trailer collision in 2016. We also reported that the family of an Apple engineer who died in a Model X last year sued the company in May.

via ZeroHedge News https://ift.tt/2KctwB2 Tyler Durden

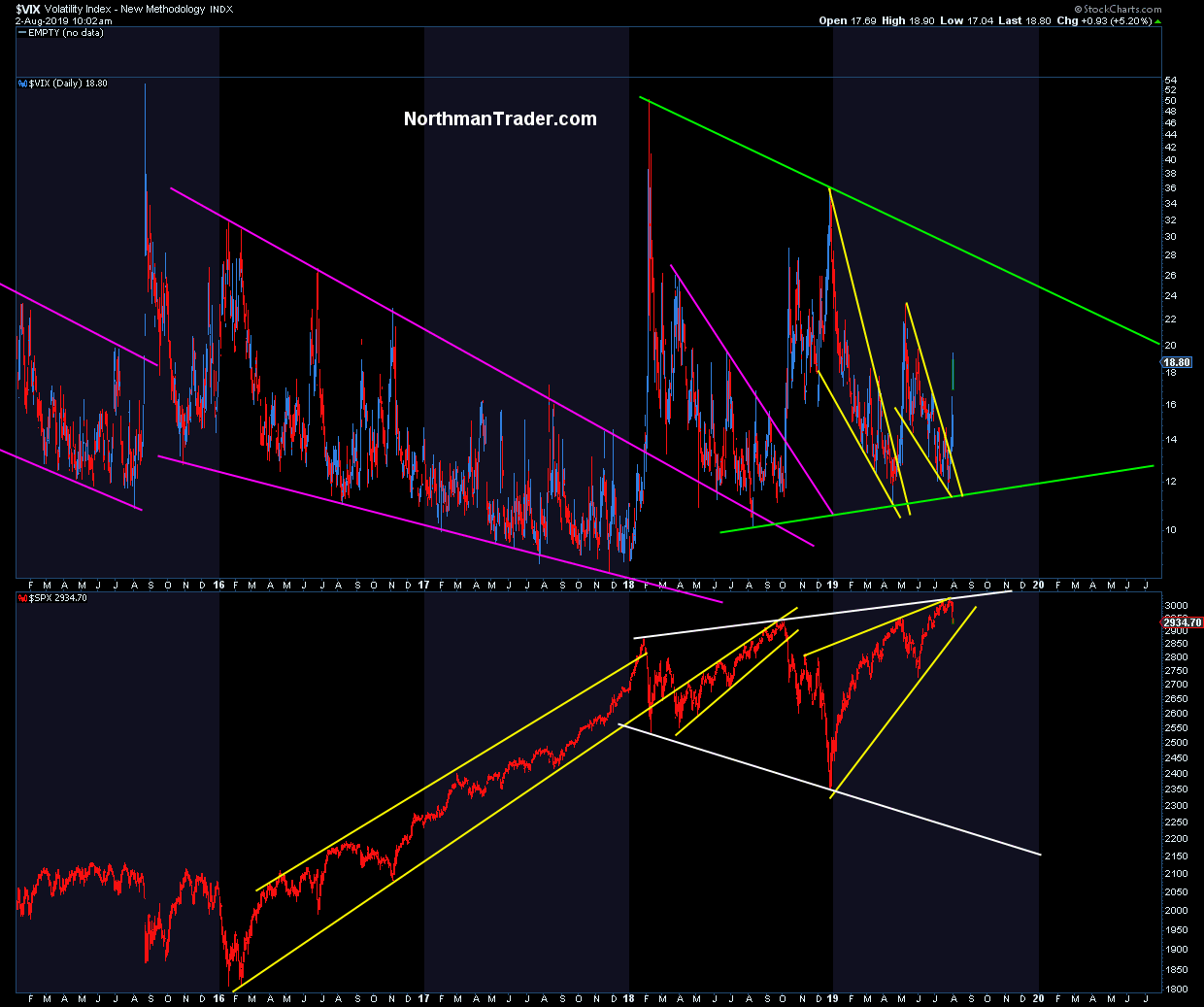

Something significant has happened with US markets this week and whether you’re bullish or bearish I suggest: Watch closely.

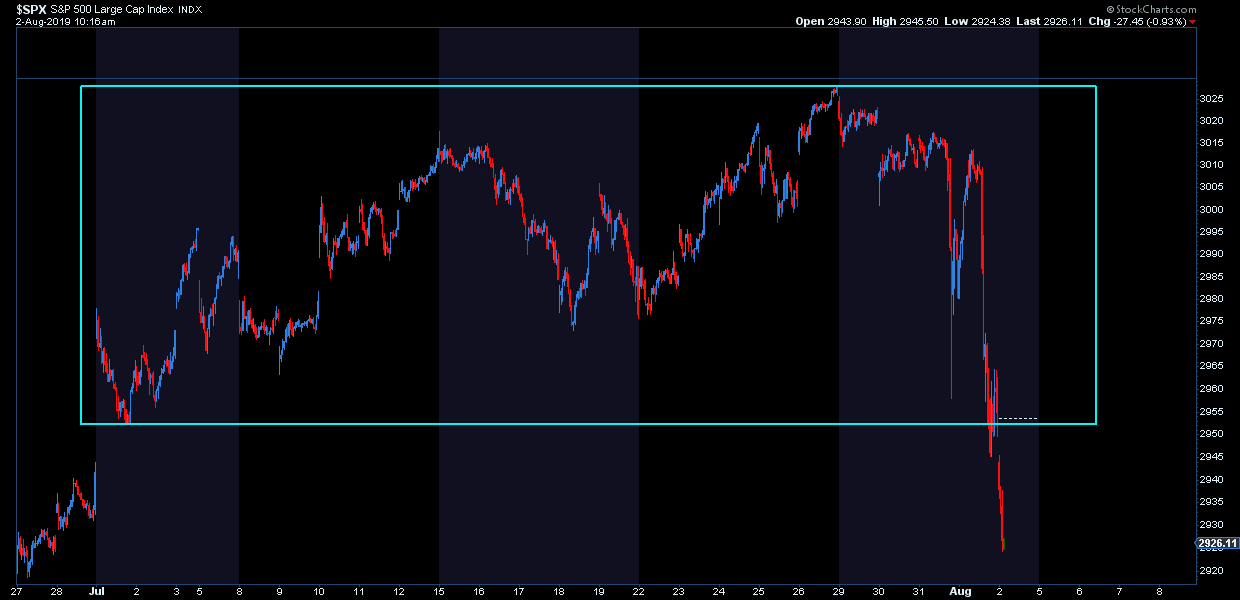

Full disclosure: We’ve been approaching July from the sell side and I’ve been very transparent about this. In late June we identified the Sell Zone, I reiterated it on CNBC on July 5th, talking about the broadening wedge pattern and discussion the 2990-3050 zone on $SPX as key technical resistance. And throughout July I outlined technical problems with the rally on NorthmanTrader as well is in videos. Last week I talked about an imminent $VIXplosion, also on CNBC, when the $VIX was trading at 12, today it as hit 19.98 as of this writing.

That’s not to say I’m right or I told you so, it’s just an technical acknowledgement that so far the sell zone has proven to be worth a fade and the volatility pattern has kicked in.

But that’s not the important part.

The important part is what is happening with markets structurally from a technical perspective and I think everybody needs to pay attention to this.

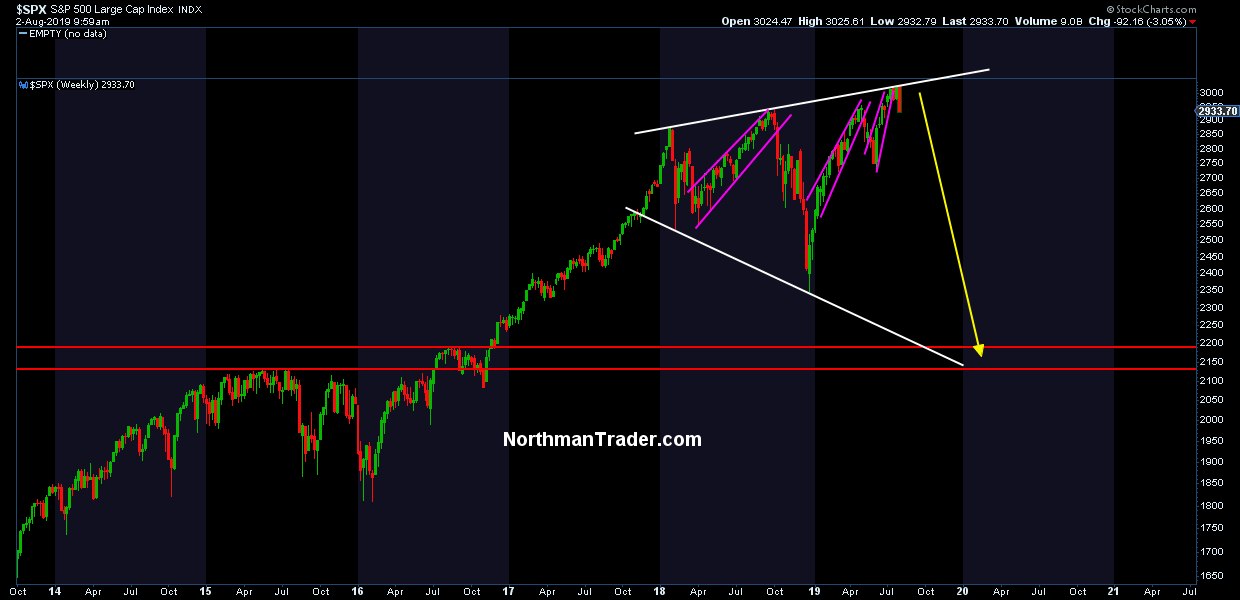

Firstly, we made new highs in anticipation of easy money from the Fed, all of July investors kept pushing prices higher into the Fed meeting this week. $SPX 3028 was reached, right smack in the middle of the sell zone.

All of these buyers are currently under water, with all of July’s prices taken out in just 2 days:

Why is this potentially so significant? Because of where it happened and what the result is.

The where? Price perfectly tagged the broadening wedge we’ve been discussion and finally rejected from there:

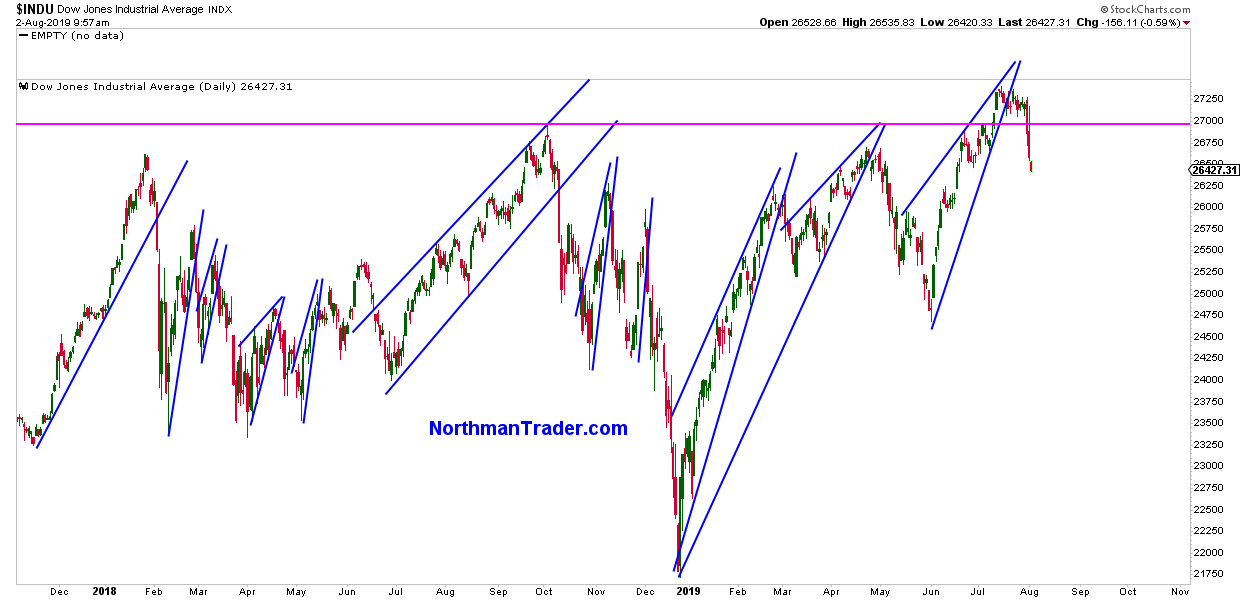

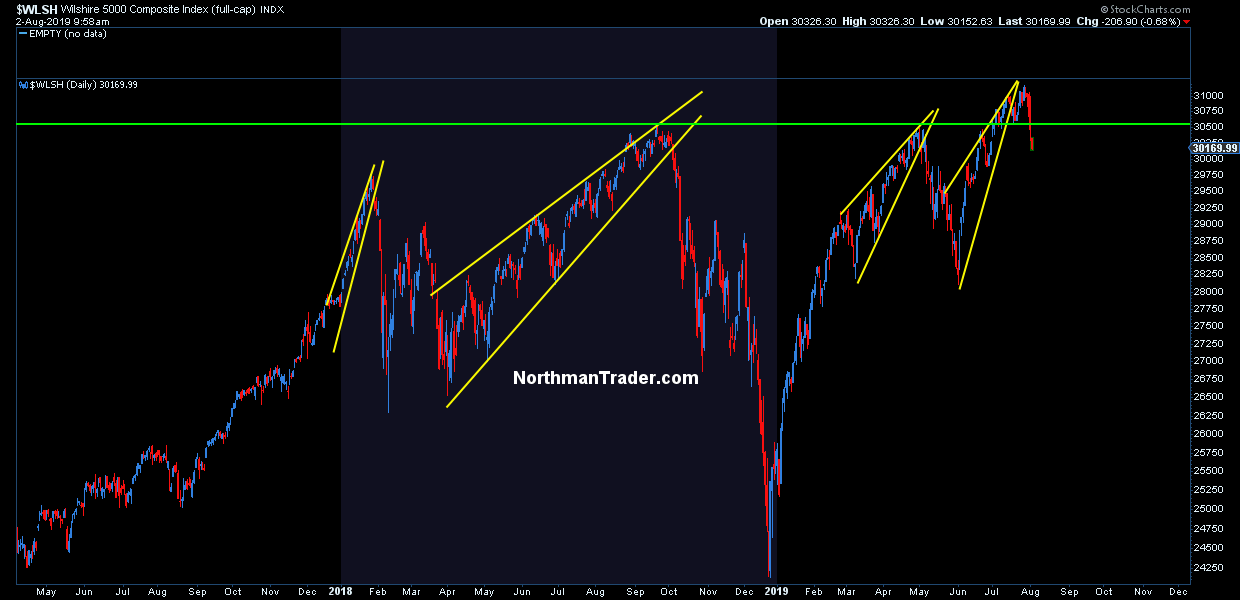

Now this is no confirmation yet that the pattern target will hit, but it’s a warning sign especially in this context: Key indices are losing the highs from last year.

Example $DJIA:

Example $WLSH:

This places these index charts in imminent danger of having printed a fake breakout.

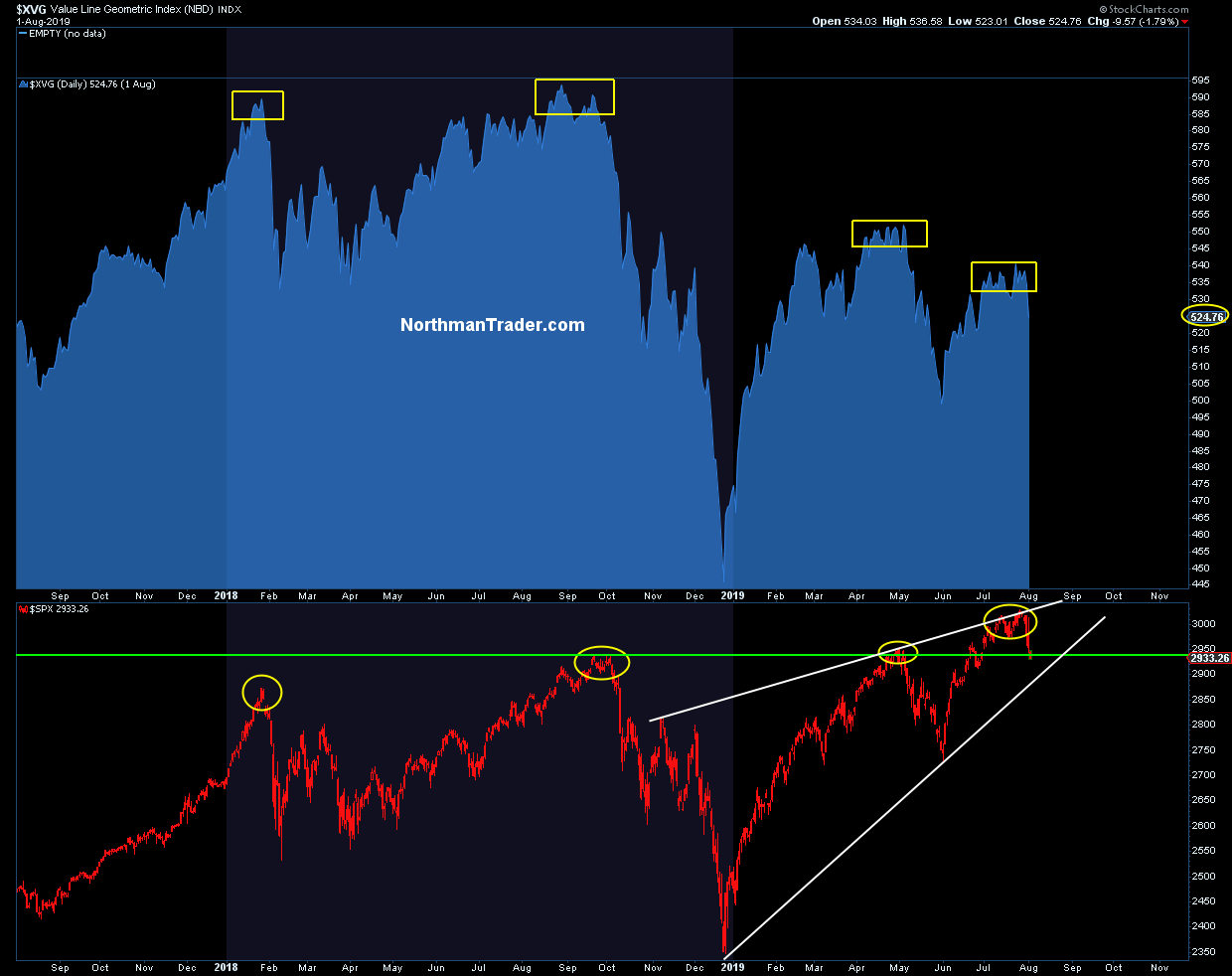

One of my technical criticisms of the rally and a favor in calling it a sell zone was internal weakness compared to previous highs.

The value line geometric index has been making lower highs with each new rally and again in July:

Structurally I’ve been pointing to the $VIX looking for another breakout, this breakout happened this week.

None of this precludes further rallies or confirms yet the validity of the larger structural sell case.

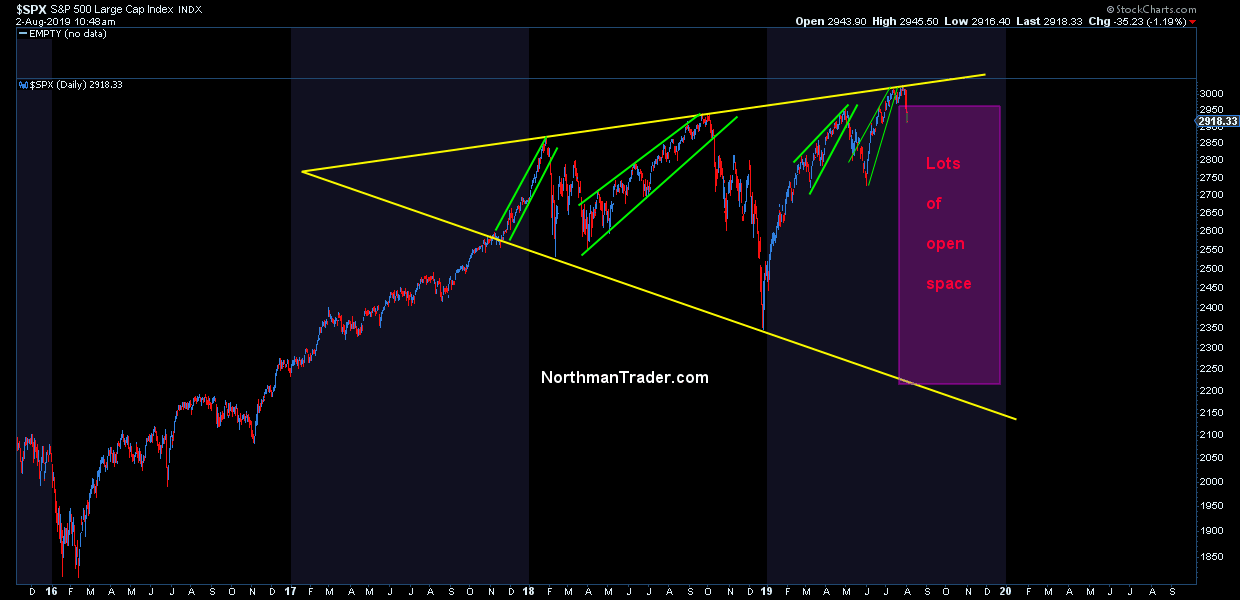

However what it does show is that the resistance zone outlined previously has been valid. As of this writing the low on $SPX has been 2914 (115 handles off the highs). Markets are now getting short term oversold, but as the previous highs from 2018 have now been broken to the downside they represent a mission critical task for bulls to recapture especially in context of the larger megaphone pattern I’ve outlined.

Failure to recapture these highs risks that the larger technical pattern gets triggered and I’ve outlined the other day: There’s a lot of open space below:

This is not about the day to day action, it’s about larger structural technical patterns and they are telling a story and this story needs to be watched closely in the days ahead.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2OBkL7X Tyler Durden

{kind=link}