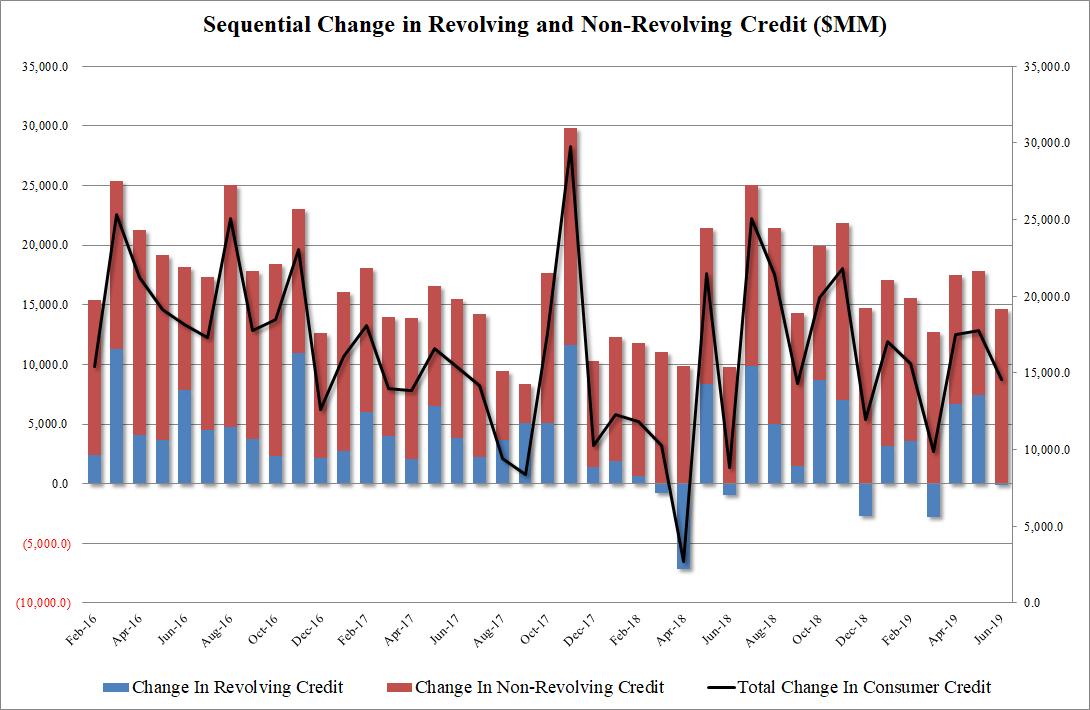

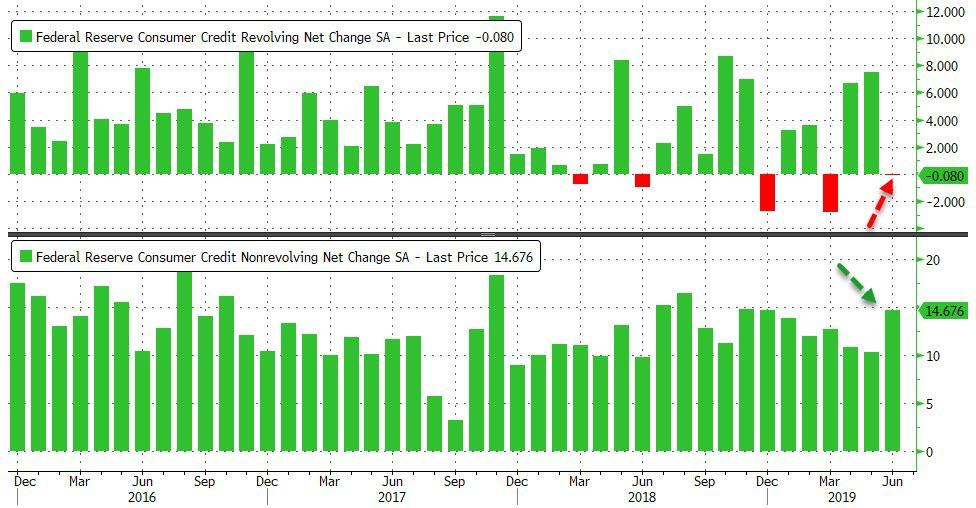

After two months of torrid gains for revolving, or credit card debt, moments ago the Fed reported in its monthly consumer credit report that in June US consumer hit the breaks hard on new credit-fueled spending.

In June, revolving credit declined by $80.5 million, the first such drop since March, and only the sixth decline since 2015. However, this was more than offset by a $14.7 billion increase in non-revolving, or student and auto loan, credit as total consumer credit in June rose by $14.6 billion, modestly below the $16.1 billion expected. Meanwhile, the May data was revised upward, from $17.1 billion to $17.8 billion.

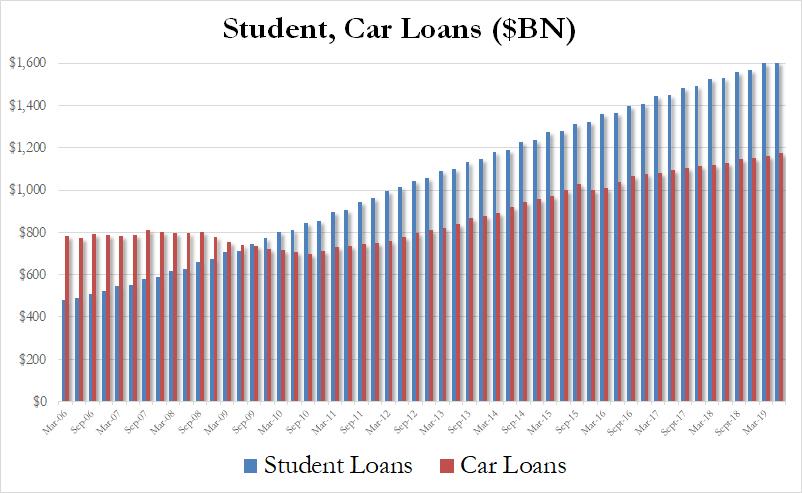

And while the reversal in June credit card use may prompt fresh questions about the strength of the US consumer despite the latest upward revision in the personal saving rates, one place where there were no surprises, was in the total amount of student and auto loans: here as expected, both numbers hit fresh all time highs, with a record $1.605 trillion in student loans outstanding, an increase of $6.8 billion in the quarter, while auto debt also hit a new all time high of $1.174 trillion, an increase of $8.4 billion in the quarter.

In short, whether they want to or not, Americans continue to drown even deeper in debt, and enjoying every minute of it.

via ZeroHedge News https://ift.tt/2ZFoCBJ Tyler Durden

With the world’s central banks aggressively easing monetary policy overnight as analysts watch in stunned amazement as the world’s interest rate careens ever faster toward zero, Trump is angrily watching the dollar as it keeps rising day after day, bringing us ever closer to the moment the US president declares on twitter a “national emergency” over the dollar and unleashes a major dollar devaluation.

Which is why it is not at all surprising that today Bank of America has published a report warning that FX intervention risks are rising, in which the bank notes that it is inclined to think the first stage of any policy shift from the Administration will be to discard the strong USD policy and hope/persuade the Fed to ease rates further. It is also not surprising that BofA’s FX strategist Kamal Sherma believes the odds of intervention to weaken USD have risen in light of this week’s developments, but the success of any such actions would depend on a number of factors including the parameters around which intervention would occur.

Here Sharma reminds us of the textbook example of successful FX intervention, namely the Plaza Accord of 1985 when the G-5 nations coordinated to weaken USD.

So is another Plaza Accord imminent? As the FX strategist explains below, there are similarities between events then and now, but also crucial differences that lead him to conclude the US Administration will not be able to rely on its major trading partners to help weaken the USD.

The Plaza Accord revisited

As Bank of America writes, September 22 marks 34 years since the G5 leaders signed a collective agreement to weaken the USD against the backdrop of growing internal and external US imbalances (the dual deficit). The Plaza Accord is widely held as the most successful episode of coordinated FX intervention and in the following two years, the USD TWI fell nearly 50%. But, while the Plaza Accord is often viewed through the prism of coordinated FX intervention to weaken USD, the basis of the Accord was built on specific economic pledges:

the US promised to reduce its Federal Deficit;

Japan promised looser monetary policy

Germany agreed to a package of tax cuts.

Coordinated FX intervention was therefore part of an overall strategy to address the internal/external imbalances that drove USD appreciation. Though the Accord was ostensibly designed to help alleviate US imbalances versus other G-5 nations, Plaza is seen by economists as a direct response from the US of threat from Japan’s growing status as an economic superpower. It is consequently seen as the catalyst for Japan’s lost decade of growth through the 1990s.

Some history

In the run up to the 1985 Accord, the USD TWI appreciated 55% making it the largest percentage rally in the USD in the past 50 years taking place against the backdrop of tight monetary policy (under Fed Chair Volcker) and expansionary fiscal policy (Reaganomics). Martin Feldstein (former Chair of Council of Economic Advisors) has argued that USD strength was not the problem; it was symptomatic of the US policy mix. US financial conditions (according to the Chicago Fed, Chart 2) are comparable to current levels. To date, USD has appreciated by nearly 40% since its 2011 lows, and while there are similarities between the narrative in 1985 and now (increasing protectionist policies from the US Administration, concern over Japanese economic dominance), there are also differences between 1985 and the present period. In 1985, USD strength prompted extensive lobbying by US industry to weaken the greenback. While recent US earnings statements make it clear that there are rising FX headwinds to profits, systematic calls from US industry to weaken the USD have been largely contained (perhaps thanks to the offsetting benefit of record stock buybacks). In addition, while the driver of USD strength through the early 1980s was largely a function of the US domestic policy mix, the US Administration currently views dollar strength as a function of global central banks deliberately keeping policy loose in an effort to prevent respective currency appreciation.

Meanwhile, as Sharma notes, inflation targeting is increasingly becoming an ineffective tool and as central bank policy rates once again synchronize the result has been a policy of benign neglect toward FX. As the BofA strategist puts it, a weak currency suits the needs of many policy officials outside of the US and the recent downgrade by the ECB to its inflation projections suggests little motivation to challenge current exchange arrangements agreed in G7 communiqués. This is important because many countries (particularly France and Germany) were concerned about a weakening of their respective currencies versus USD in 1985. G5 countries were therefore a willing partner in efforts to weaken the USD. Now, FX is an essential part of the policy armory. Europe and Japan are now more accepting of FX weakness than FX strength.

According to some estimates, the combined interventions by G5 totaled $10bn. According to the BIS Triennial Survey, average daily FX turnover in 1989 was $655bn. Assuming a turnover figure of $500bn for 1985, total Plaza Accord intervention, accounted for around 2% of daily market turnover. With current daily turnover at $5.5tn, an equivalent amount of intervention would imply over $100bn in FX. According to BofA calculations, the US could muster reserves in excess of these levels (~$140bn), although it is clear that the amounts of intervention would have to be substantial and sustained for it to be credible. Meanwhile, in subsequent years, the Bank of Japan intervened on 126 days between January 2003 and March 2004, purchasing over $315bn to weaken JPY. This was a sustained period of intervention, but question marks remain over its long-term efficacy (note: such interventions were disastrous and only the current period of QQE helped stabilize the yen decidedly below 100 vs the USD). The effectiveness of interventions has more broadly involved the element of surprise and positioning: of note, BofA’s own proprietary indicators do not suggest investors are holding sizeable USD longs positions to make USD selling intervention have sustained impact.

How to measure success

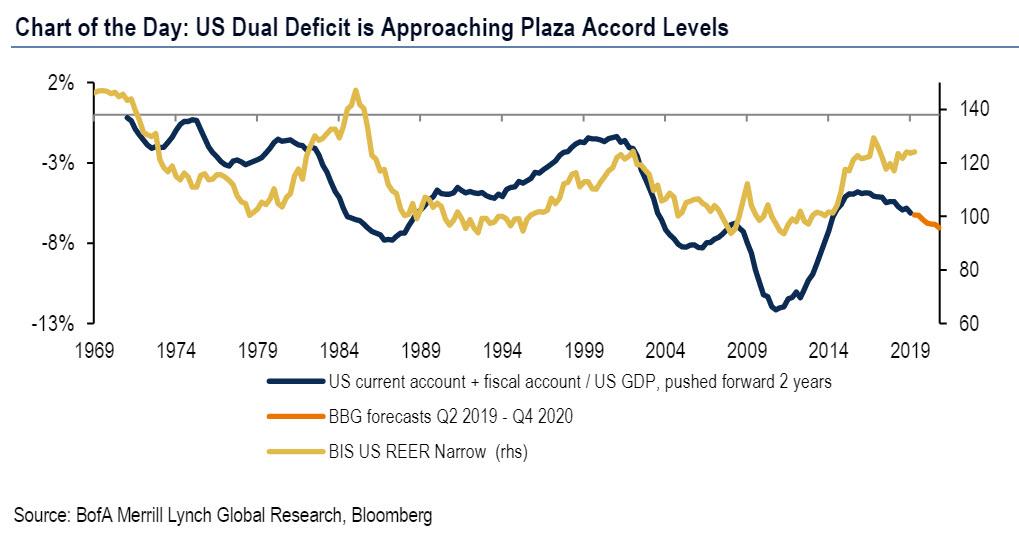

As shown below in the bank’s Chart of the Day: “US Dual Deficit is Approaching Plaza Accord Levels”, the rapid depreciation of the USD following Plaza eventually led to a steady improvement in the dual deficit. However, the issue for the Trump Administration is whether that improvement can come ahead of the 2020 Presidential election for him to claim that his interventionist policy has been a success. His 2016 campaign pledge to narrow the US trade deficit (particularly with China) is currently at odds with the dynamics of external US trade data, which show the merchandise deficit with China hitting a five-year high in June.

Indeed, as noted above, the complicating factor for the US Administration is whether any depreciation of USD will lead to a material improvement in the trade deficit in time for the 2020 election. The J-curve theory suggests a country’s trade deficit will initially deteriorate following currency devaluation. Certainly the evidence from UK and Canadian trade data suggests both deficits have not materially improved since the financial crisis despite the 20% and 30% depreciations of CAD and GBP TWI respectively. What is clear is that with 15 months left until the 2020 Presidential election, any depreciation in USD is unlikely to have a material impact on the US trade balance. The US current account deficit continued to deteriorate until 1987, two years after the Plaza Accord.

What to expect in the coming months?

Ironically, the Osaka G20 Summit held earlier this year reiterated its commitments from March 2018 to refrain from FX intervention:

“Flexible exchange rates, where feasible, can serve as a shock absorber. We recognize that excessive volatility or disorderly movements in exchange rates can have adverse implications for economic and financial stability. We will refrain from competitive devaluations, and will not target our exchange rates for competitive purposes”.

We say ironically, because the latest G20 Communiqué is effectively the antithesis of the 1985 Plaza Accord and along the with the US Administration’s strong USD policy are two initial challenges that it faces were it to intervene. Here, BofA would focus strongly on the Administrations’ commentary around both areas as signs that it is moving toward a more interventionist approach.

One way that this could be formalized is firming up the commitments around the US Treasury FX Manipulation Report, which is due for release in October, even though we already know that China will be declared a manipulator. At present, BofA sees bilateral negotiation as the only recourse the US has if it labels a country as a currency manipulator. There is one other possibility: the US could revise the framework around the FX Manipulation Report so it includes a new metric that takes into account the relative monetary policy stance of foreign central banks as a de facto signal that they have a policy of benign neglect toward their currency. Either the country in question reverses course on its monetary policy, or the US Authorities reserve the right to intervene to weaken the USD to create a “level playing field”.

And since not a single foreign central bank will concede to such a requirement in a time when the global race to the bottom, as the name suggest is “global”, the US will have free reign to finally unleash hell on the dollar.

Finally, we remind readers of an unorthodox – if highly efficient – method to devalue the dollar that was proposed by bond trading legend, and MOVE index creator, Harley Bassman back in 2016 when he worked for PIMCO – the Fed buying gold. Before all is said and done and the central banks’ reign of terror is finally over, we are certain that this dramatic step will also be attempted.

via ZeroHedge News https://ift.tt/2ZEZVFN Tyler Durden

“Let me be clear, what I said was, it’s not the beginning of a long series of rate cuts.”- Fed Chairman Jerome Powell -7/31/2019

“What the Market wanted to hear from Jay Powell and the Federal Reserve was that this was the beginning of a lengthy and aggressive rate-cutting cycle which would keep pace with China, The European Union and other countries around the world….” – President Donald Trump – Twitter 7/31/2019

With the July 31, 2019, Fed meeting in the books, President Trump is up in arms that the Fed is not on a “lengthy and aggressive rate-cutting” path. Given his disappointment, we need to ask what else the President can do to stimulate economic growth and keep stock investors happy. History conveys that is the winning combination to win a reelection bid.

Traditionally, a President’s most effective tool to spur economic activity and boost stock prices is fiscal policy. With a hotly contested election in a little more than a year and the House firmly in Democratic control, the odds of meaningful fiscal stimulus before the election is low.

Without fiscal support, a weak dollar policy might be where Donald Trump goes next. A weaker dollar could stimulate export growth as goods and services produced in the U.S. become cheaper abroad. Further, a weaker dollar makes imports more expensive, which would increase prices and in turn push nominal GDP higher, giving the appearance, albeit false, of stronger economic growth.

In this article, we explore a few different ways that President Trump may try to weaken the dollar.

Weaker Dollar Policy

The impetus to write this article came from the following Wall Street Journal article: Trump Rejected Proposal to Weaken Dollar through Market Intervention. In particular, the following two paragraphs contradict one another and lead us to believe that a weaker dollar policy is a possibility.

On Friday, Mr. Kudlow said Mr. Trump “ruled out any currency intervention” after meeting with his economic team earlier this week. The comments led the dollar to rise slightly against other currencies, the WSJ Dollar index showed.

But on Friday afternoon, Mr. Trump held out the possibility that he could take action in the future by saying he hadn’t ruled anything out. “I could do that in two seconds if I wanted to,” he said when asked about a proposal to intervene. “I didn’t say I’m not going to do something.”

Based on the article, Trump’s advisers are against manipulating the dollar lower as they don’t believe they can succeed. That said, on numerous occasions, Trump has shared his anger over other countries that are “using exchange rates to seek short-term advantages.”

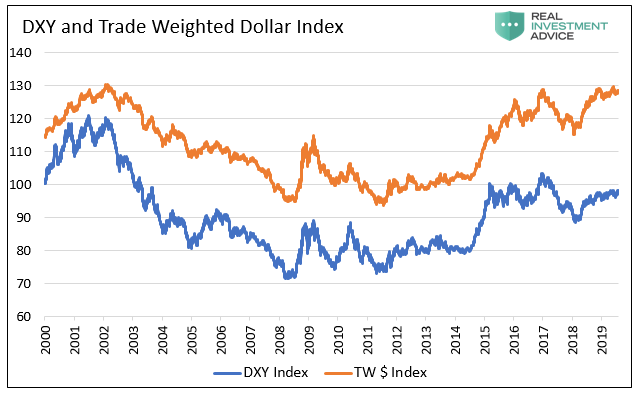

As shown below, two measures of the U.S. dollar highlight the substance of frustrations being expressed by Trump. The DXY dollar index has appreciated considerably from the early 2018 lows but is still well below levels at the beginning of the century. This index is inordinately influenced by the euro and therefore not 100% representative of the true effect that the dollar has on trade. The Trade-weighted dollar which is weighted by the amount of trade that actually takes place between the U.S. and other countries. That index has also bounced from early 2018 lows and, unlike DXY, has reached the highs of 2002.

Data Courtesy Bloomberg

Trump’s Dollar War Chest

The following section provides details on how the President can weaken the dollar and how effective such actions might be.

Currency Market Intervention

Intervening in the currency markets by actively selling US dollars would likely push the dollar lower. The problem, as Trump’s advisers note, is that any weakness achieved via direct intervention is likely to be short-lived.

The US economy is stronger than most other developed countries and has higher interest rates. Both are reasons that foreign investors are flocking to the dollar and adding to its recent appreciation. Assuming economic activity does not decline rapidly and interest rates do not plummet, a weaker dollar would further incentivize foreign flows into the dollar and partially or fully offset any intervention.

More importantly, there is a global dollar shortage to consider. It has been estimated by the Bank of International Settlements (BIS) that there is $12.8 trillion in dollar-denominated liabilities owed by foreign entities. A stronger dollar causes interest and principal payments on this debt to become more onerous for the borrowers. Dollar weakness would be an opportunity for some of these borrowers to buy dollars, pay down their debts and reduce dollar risk. Again, such buying would offset the Treasury’s actions to depress the dollar.

Instead of direct intervention in the currency markets, Trump and Treasury Secretary Steve Mnuchin can use speeches and tweets to jawbone the dollar lower. Like direct intervention, we also think that indirect intervention via words would have a limited effect at best.

The economic and interest rate fundamentals driving the stronger dollar may be too much for direct or indirect intervention to overcome.

From a legal perspective intervening in the currency markets is allowed and does not require approval from Congress. Per the Wall Street Journal article, “The 1934 Gold Reserve Act gives the White House broad powers to intervene, and the Treasury maintains a fund, currently of around $95 billion, to carry out such operations.” The author states that the Treasury has not conducted any interventions since 2000. That is not entirely true as they conducted a massive amount of currency swaps with other nations during and after the financial crisis. By keeping these large market-moving trades off the currency markets, they very effectively manipulated the dollar and other currencies.

Hounding the Fed

The President aggressively chastised Fed Chairman Powell for not cutting interest rates or ending QT as quickly as he prefers. Lowering interest rates to levels that are closer to those of other large nations would potentially weaken the dollar. The only problem is that the Fed does not appear willing to move at the President’s pace as they deem such action is not warranted. We believe the Fed is very aware that taking unjustifiable actions at the behest of the President would damage the perception of their independence and, therefore, their integrity.

To solve this problem, Trump could take the controversial and unprecedented step of firing or demoting Fed Chairman Powell. In Powell’s place he could put someone willing to lower rates aggressively and possibly reintroduce QE. These steps might push financial asset prices higher, weaken the dollar, and provide the economic pickup Trump seeks but it is also fraught with risks. We have written two articles on the topic of the President firing the Fed Chairman as follows: Chairman Powell You’re Fired and Market Implications for Removing Fed Chair Powell.

It is not clear whether the President can get away with firing or even demoting Chairman Powell. We guess that he understands this which may explain why he has not done it already. If he cannot change Fed leadership, he can continue to pressure the Fed with Tweets, speeches, and direct meetings. We do not think this strategy can be effective unless the Fed has ample reason to cut rates. Thus far, the Fed’s mandates of “maximum employment, stable prices, and moderate long-term interest rates” do not provide the Fed such justification.

Getting Help Abroad

One of the core topics in the U.S. – China trade talks has been the Chinese Yuan. In particular, Trump is negotiating to stop the Chinese from using their currency to promote their economic self-interests at our expense. As of writing this, the U.S. Treasury deemed China a currency manipulator. Per the Treasury: “As a result of this determination (currency manipulator), Secretary Mnuchin will engage with the International Monetary Fund to eliminate the unfair competitive advantage created by China’s latest actions.” Said differently, the U.S. and other nations can now manipulate their currency versus the Chinese Yuan.

It is plausible that Trump might pressure other countries, including our allies in Europe and Japan as well as Mexico and Canada, to strengthen their respective currencies against the dollar. Trump can threaten nations with trade restrictions and tariffs if they do not comply. If tariffs are enacted, however, all bets are off due to the economic inefficiencies of tariffs or trade restrictions. To the President’s dismay, such action weaken the economy and scare investors as we are seeing with China.

Threats of trade actions, trade-related actions, or trade agreements might work to weaken the dollar, but such tactics would require time and pinpoint diplomacy. Of all the options, this one requires longer-term patience in awaiting their effect and may not satisfy the President’s desire for short-term results.

Summary

Before summarizing we leave you with one important thought and certainly a topic for future writings.Globally coordinated monetary policy is morphing into globally competitive monetary policy. This may be the most significant Macro development since the Plaza Accord in 1985 when the Reagan administration, along with other developed nations (West Germany, France, Japan, the UK), coordinated to weaken the U.S. dollar.

With the Presidential election in about 15 months, we have no doubt that President Trump will do everything in his power to keep financial markets and the economy humming along. The problem facing the President is a Democrat-controlled House, a Fed that is dragging their feet in terms of rate cuts, weakening global growth, and a stronger U.S. dollar.

We believe the odds that the President tries to weaken the dollar will rise quickly if signs of further economic weakness emerge. Given the situation, investors need to understand what the President can and cannot do to spike economic growth and further how it might affect the prices of financial assets.

On the equity front, a weaker dollar bodes well for companies that are more global in nature. Most of the companies that have driven the equity indices higher are indeed multi-national. Conversely, it harms domestic companies that rely on imported goods and commodities to manufacture their products. The price of commodities and precious metals are likely to rise with a weaker dollar. A weaker dollar and any price pressures that result would likely push bond yields higher.

The statistical relationships between the dollar and other asset classes are important to quantify if in fact the dollar may become an economic tool for the President. A full spectrum of those relationships over various timeframes may be found in an addendum to this article for RIA Pro subscribers. Give us a try. All new subscribers receive a 30 day free trial to explore what we have to offer and view the addendum.

via ZeroHedge News https://ift.tt/2yGv3ZA Tyler Durden

It looks like the honeymoon between Tesla and the NHTSA could be over, effective October 2018.

The U.S. National Highway Traffic Safety Administration (NHTSA) sent a cease and desist letter to Tesla last year, Bloomberg reported today on the 1-year anniversary of the “funding secured” tweet, for “not complying with the agency’s guidelines in its Model 3 safety assertions”. The NHTSA also reportedly subpoenaed Tesla for information on several crashes. The documents were revealed through a FOIA request by non-profit advocacy group PlainSite.

NHTSA lawyers reportedly weren’t happy with a blog post that Tesla made in October, claiming that the Model 3 had “achieved the lowest probability of injury of any vehicle the agency ever tested.” The NHTSA said that the claims were inconsistent with its advertising guidelines regarding crash ratings and that it would ask the FTC to investigate if the claims were unfair or deceptive.

Here’s what an NHTSA subpoena actually looks like. The question is how many are enough to effect some sort of actual change or regulation? pic.twitter.com/obtviJs0cF

Allan Kam, an independent auto-safety consultant who retired as a senior enforcement attorney at NHTSA in 2000 said: “If it’s a subpoena, it’s known to get quicker attention from the manufacturer generally, and it’s not a routine matter. It’s dealt with in a more prompt way and in a more serious way.”

The NHTSA released a statement back in October noting that it took exception with the company’s characterization of its safety ratings. The NHTSA said that its crash tests combine into an overall safety rating and that it doesn’t rank vehicles that score the same ratings. The agency warned that using the words “safest” and “perfect” to describe a rating is misleading.

This isn’t the first time this has happened, either. The NHTSA released a similar statement in 2013 when Tesla said its Model S achieved a score of 5.4 stars, correcting that it doesn’t score beyond 5 stars.

Jonathan Morrison, chief counsel at NHTSA, wrote in an Oct. 17 letter to Musk: “This is not the first time that Tesla has disregarded the guidelines in a manner that may lead to consumer confusion and give Tesla an unfair market advantage.”

Tesla’s deputy general counsel responded about two weeks later: “Tesla has provided consumers with fair and objective information to compare the relative safety of vehicles having 5-star overall ratings.”

In addition, it appears as though more than 450 documents were withheld from PlainSite’s FOIA request, which they are currently appealing.

Having ramped back into the green for the 3rd time today, Nasdaq futures are sliding once again after Fox News reports

“Chinese Trade Sources tell us that China expects 10% tariffs on an additional $300 billion will be added Sept 1st. Those sources also say China expects that 10% to go to 25% because China will stand firm and not buy US Agriculture.”

Chinese Trade Sources tell us that China expects 10% tariffs on an additional $300 billion will be added Sept 1st. Those sources also say China expects that 10% to go to 25% because China will stand firm and not buy US Agriculture. #China#Trade

Weirdo counterintelligence guy seems to be feeding alt-right with conspiracy theories

In another bizarre performance on NBC news programming, former FBI Assistant Director for Counterterrorism Frank Figliuzzi claimed that President Trump may have ordered flags flown at half staff not to honor the victims of the Dayton and El Paso shootings, but rather to celebrate Adolf Hitler.

Figliuzzi explained the reasoning behind his conspiracy theory, claiming that the date the flag is to be at half staff until, August 8 (8/8), is a neo-nazi calling sign because the eighth letter of the alphabet is H, which stands for Hitler, and 8/8 means ‘Heil Hitler.’

Yes, somehow it is even a white supremacist act now to have flags flying at half-staff in honor of victims of a white supremacist murderer.

Lets skip over the fact that Figliuzzi looks downright creepy, and blinks about a million times in that clip, as if he’s attempting to hypnotize the audience into believing his crackpot nutbaggery.

Looks as if there is a conscious effort to make Alex Jones look reasonable.

Remember that Alex Jones is BANNED from all social media, while Figliuzzi is PAID to spew this droolstack on a platform owned by NBCUniversal, one of the largest companies on the globe.

And it isn’t an isolated incident. Figliuzzi vomits out this kind of bile pile every day.

Earlier in the week, Figliuzzi described Trump as a ‘radicalizer’ for white supremacists, and directly compared him to an extremist Islamic cleric inspiring Muslims to commit acts of violent Jihad.

Meanwhile, NBC chief foreign correspondent Richard Engel was literally flown to a neo-nazi festival in Germany, where he concluded that Trump is inspiring hate and the ‘inspiration to murder’ among white supremacists in Germany.

Anyone would think that these former intelligence officials now working in news are deliberately feeding real white supremacists with such theories in order to rile them up.

via ZeroHedge News https://ift.tt/33jbjcE Tyler Durden

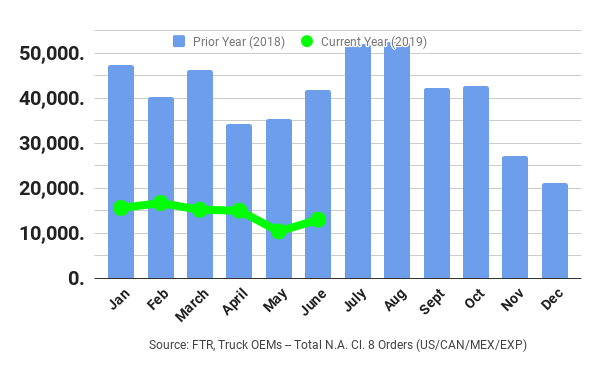

Preliminary North America Class 8 net order data shows the industry booked 10,200 units in July, an astonishing 81% year over year fall, according to ACT Research.

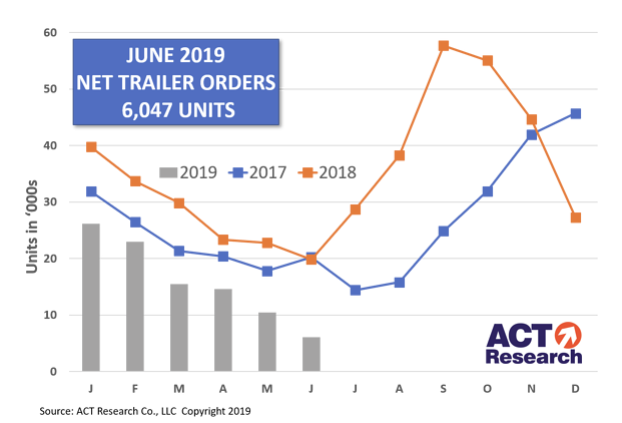

This is also down 21% from June and marks the lowest monthly order tally since February 2010. Net trailer orders also continued to plunge, according to data released about a week ago.

Kenny Vieth, ACT’s President and Senior Analyst said in late July that heavy truck and trailer industries would be heading for a market correction in 2020. He stated:

“Data that support our forecast of an impending market correction continue to mount, with the biggest driver of the change for both Class 8 and trailers being the continued building of new equipment inventories in 2019 that will require right-sizing in 2020. Since March 2018, ACT’s forecasts have targeted 2019’s third quarter as the point at which the supply of Class 8 tractors and demand for freight services would likely tip so far as to break the current period of peak vehicle production, as demand reverts to the mean. Current data and anecdotes make a strong case that the call for a Q3 inflection remains intact.”

Recall, in early July we reported that Class 8 orders were down for the eighth month in a row, falling a stunning 70% in June to 13,000 units, according to FTR data. The figure was up 20% sequentially, but still followed a 71% decimation in May. Jefferies’ Stephen Volkmann wrote in a note last month that the figures indicate a SAAR of ~178,000 Class 8 trucks and noted that the sequential growth compares to a sequential drop of 27% in May, when SAAR estimates were 139,000 units.

We will look to see if he updates his estimates based on July’s data.

Vieth had commented in July:

“Fraying freight market and rate conditions along with a still-large Class 8 order backlog contributed to the worst NA Class 8 net order performance since July of 2016. May saw NA Class 8 orders fall below the 15,900 units averaged through the year’s first trimester, and year-to-date Class 8 net orders have contracted 64% compared to the first five months of 2018.”

via ZeroHedge News https://ift.tt/2Yx30Lw Tyler Durden

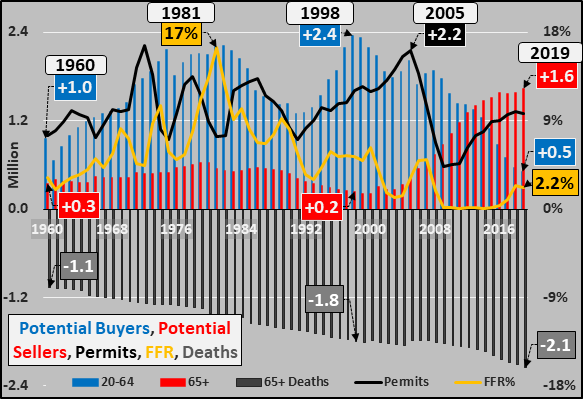

The Quantity of New Potential Homebuyers is Decelerating to a Trickle.

The Quantity of Potential Sellers is Surging.

This Mismatch Will Continue to Drive The Federal Reserve to Cut the Federal Funds Rate (& Resultant Mortgage Rates) to Record Lows.

The Net Result is a National Oversupply of Housing, Particularly in Rural Areas, While Select Urban Markets Continue to Face Housing Shortages.

Just a few charts today to make a simple point regarding the present and future of the housing market.

1960 through 2019

Potential Home Sellers

1- 65+ year-olds have the highest homeownership rate, presently 78% of these folks own their own home and they are over-represented in rural areas

2- 65+ year-olds now account for over 75% of the net annual population growth in America (red columns below)…with annual 65+ growth rising from +0.3 million in 1960 up to +1.6 million as of 2019

3- 65+ year-olds also account for 75% of annual deaths (grey negative columns below)…with elderly deaths accelerating from -1.1 million annually in 1960 to -2.1 million as of 2019 (to clarify, in 2019 this means +3.7 million enter the 65+ crowd but 2.1 million exit…leaving a net increase of +1.6 million)

4- When elderly die, there are a couple options for their property…

-A) will it to their heirs

-B) sell it to settle their affairs (as in the case of reverse mortgages)

Generally their heirs either occupy the home themselves (and sell or rent their existing home) or sell or rent the deceased parties property. The net result in all these scenarios is a net addition of housing to the market (either as a rental or property for sale).

Potential Home Buyers

5- 20 to 64 year-old annual population growth has decelerated from the 1998 peak of +2.4 million annually to just +0.5 million, as of 2019 (blue columns, below)…but they are over-represented in select urban areas

6- Those under 35 years-old (entering the 20-64 year-old population) have just a 36% homeownership rate, but the lack of 20-64 year-oid population growth coupled with record student loan debt, record rents as a percentage of income, minimal savings, record delayed marriages (average now over 30yrs/old) and record low birth / fertility rates all continues to undermine rising homeownership rate and total growth of potential buyers

Potential New Homes

7- The annual quantity of new homes (represented below by annual housing permits…black line) varied from 1 million to 2.2 million annually from 1960 through 2005…on the whole driven by the annual growth of potential buyers among the 20 to 65 year-old population with significant short term gyrations due to the impact of changes in the Federal Funds rate (yellow line), driving mortgage rates up/down.

Since 2005, new permits (like the 20-65 year-old annual population growth) collapsed but permits have partly recovered (thanks to a decade of ZIRP and the re-employment of the workforce following the GFC) while potential population growth among home buyers has continued to decelerate.

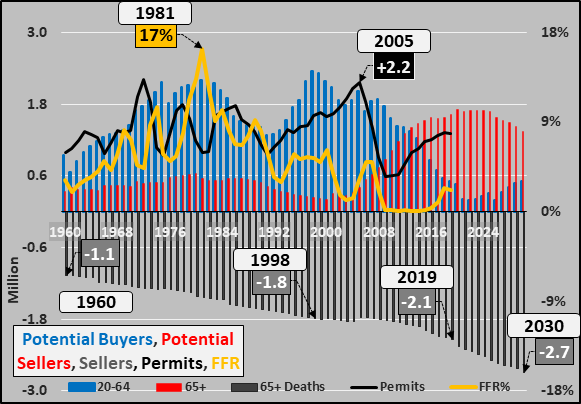

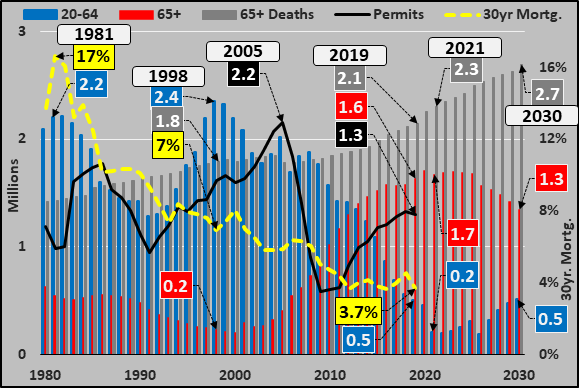

2019 through 2030

These trends only become more acute over the next decade (chart below, same as above but including projections from 2019 through 2030). The imbalance of miniscule growth among potential buyers (blue columns) versus massive growth among potential sellers (65+ year-olds, red columns) and definite sellers (65+year-old deaths…grey columns).

Below, same chart as above but 1980 through 2030 and flipping the annual elderly deaths (grey columns) to put them into perspective against the potential annual change in potential buyers (blue columns), potential sellers (red columns), 30yr mortgage rate (yellow dashed line), and permits (black line). These are the changing ingredients that make up the US housing market (and economy). Just some food for thought.

The 2019 through 2030 chart below highlights the discrepancy of minimal potential buyers (blue columns), surging elderly (red columns), accelerating elderly deaths (grey columns), and likely implementation of NIRP (yellow dashed line) versus best guestimate for new housing creation (permits, black dashed line).

By 2023, the growth of potential home buyers will decline to just 0.2 million annually, deaths among elderly will accelerate to -2.4 million annually (bringing up to 1.9 million properties to the market, either as rentals or “for sale”), and population growth among the elderly will peak at +2.4 million annually.

The net-net of this is an absolute mess. 65+ year-olds (who already own homes) are not likely to buy another and are more likely to downsize &/or enter a nursing/memory care home. The accelerating deaths among the property owning elderly will bring significantly more properties to market against a fast decelerating quantity of new buyers. The Federal Reserve is almost sure to push the Federal Funds rate negative (implementing NIRP) to incent the largest segment of the US economy, homebuilding, to continue creating new product. The NIRP is also likely to push mortgage rates to record lows, (perhaps 2% for a 30yr fixed?) continuing to push leverage, speculation, and valuations higher?!? Of course, the lack of working age population growth and the already existing state of full employment means that potential employment growth over the next decade will likewise be a trickle (at best)…again putting secular downward pressure on the potential for new home buyers.

On a fundamental national basis, this means the imbalance only gets more severe with significantly more potential sellers versus just a trickle of growth among potential buyers…and the Fed will do all it can to kick the can as long as possible. Of course, the local realities are very unique and quite different. Simultaneously, urban markets are exhibiting housing shortages (due to relatively positive demographics, population growth, and jobs growth) while rural markets face overwhelming housing surplus’ (due to awful demographics, depopulation, and declining jobs). I previously detailed the urban / rural discrepancies in demographics, population growth, employment, by region South, West, Midwest, Northeast, and National Overview.

Population data via UN 2019 Population Prospects Report

via ZeroHedge News https://ift.tt/2YwZukl Tyler Durden

In a day when fears about escalating trade and currency wars (and the PBOC’s first imminent yuan fixing below 7.00 tonight) and panicking central banks sent global bond yields to near record lows, there was some positive news involving one of the parallel trade wars that has been taking place in the Pacific Rim periphery of the main event between the US and China.

Specifically, the Nikkei reported that the Japanese government is set to approve some exports of semiconductor materials to South Korea, potentially a minor but notable detente in the recent trade feud between the two countries, and the first such approval since Tokyo tightened export controls on the products in July.

The Ministry of Economy, Trade and Industry determined after a review that there is no risk the shipments will be used for military equipment. Despite the additional bureaucratic hoops exporters must now jump through, the resumption of shipments may mean South Korea’s semiconductor production will not be severely affected.

According to the Nikkei, the ministry is likely to announce the approvals as soon as Thursday, however, “officials are not expected to give details about the shipments or orders as the information is confidential.”

As a reminder, over a month ago, on July 4 Japanese Prime Minister Shinzo Abe decided to require government approval for each shipment of key materials – such as fluorinated polyimide, which is used in smartphone displays, and resists and hydrogen fluoride, used to make semiconductors – to South Korea as part of a sudden reversal in trade policies between the two export-reliant nations. Previously, companies could obtain comprehensive approval that allowed them to export without screenings of individual shipments, for a set period.

The amount of paperwork involved is significant. For resists and fluorinated polyimides, the process involves submitting seven different documents, including technical details about the materials and their specifications.

Hydrogen fluoride is subject to more stringent controls, with nine documents required. The exporter must provide details about the production process at the facility using the gas, going all the way up to finished goods, along with a record of the buyer’s past purchases of the material and output of the products for which it will be used. The importer must also sign a pledge that the gas will not be used for military purposes.

The red tape created major headaches for exporters, which had to field inquiries from the government about South Korean manufacturers’ production processes or needed to get the signatures of those companies’ executives. This bogged down the screening process at the trade ministry as reviews can take up to 90 days, in the process grinding much of the semiconductor trade between the two nations to a halt. “Showa Denko, which reportedly sent in an application for hydrogen fluoride exports in mid-July, is still waiting for approval, according to President Kohei Morikawa” the Nikkei reports.

While Japan also requires approval for individual shipments of these products to China and Taiwan (which typically receive less favorable treatment than South Korea), with those two markets, exporters of resists and fluorinated polyimides can get comprehensive approvals letting them use simplified customs procedures for three years.

It remains to be seen if the move is merely a bureaucratic push or a de-escalation in the ongoing Pacific Rim trade war: last Friday, Japan’s cabinet decided to remove South Korea from its list of preferential trade partners, a move that will take effect on Aug. 28. The new rules allow the trade ministry to order screenings of shipments for nearly all products, other than food and lumber, to South Korea. Observers have expressed fears that this could expand the red tape issue to industrial machinery and other goods.

via ZeroHedge News https://ift.tt/2MMtaCW Tyler Durden

Some 500 political and business leaders including 200 local deputies of China’s top legislature, the National People’s Congress, as well as pro-Beijing Hong Kong execs and chamber of commerce officials gathered Wednesday to discuss the ongoing Hong Kong unrest triggered by the proposed extradition bill earlier this summer.

Unlike prior similar gatherings in mainland China of top officials, there was reportedly little attempt to soften the full blown reality, as the group was told the protest crisis is assuredly becoming “bigger and more violent”. The assessment was issued by Zhang Xiaoming, director of Hong Kong and Macau Affairs Office under the State Council, as reported by the South China Morning Post.

Zhang presented that Beijing views the Hong Kong situation the “most serious situation” since 1997, the year of the handover of Hong Kong when the UK formally ceded control of its colony.

Zhang Xiaoming, director of Hong Kong and Macau Affairs Office under the State Council, making remarks to the media, via Visual China Group/Getty

“From June 9 until now, the extradition saga has lasted 60 days. It has grown bigger, with violent acts getting more intense, and wider sections of society being affected,” Zhang said.

“We can say Hong Kong is facing the most serious situation since handover,” he added. “Therefore, this meeting is very important and special.”

The meeting constituted a rare such briefing sponsored by the Hong Kong and Macau Affairs Office, which reportedly hadn’t taken such action since Hong Kong’s handover from Britain to China. The 500 high-powered attendees were invited to discuss the situation following two hours of formal remarks. Beijing officials sought a forum to “speak more frankly” to accurately address the severity of the crisis.

“The biggest difference is that today’s seminar is convened when Hong Kong’s situation is very unstable,” Zhang said further in his remarks, the few opening minutes of which were made while media was present, after which it became close door.

“Whenever any major political or legal issue arises in the implementation of ‘one country, two systems’ and the Basic Law, the central government would listen to your views and advice, and communicate, so that our decisions and policies can be more compatible with the actual situation in Hong Kong.”

Zhang said with media still present: “The central government is highly concerned about the situation in Hong Kong, and have been making plans from a strategic level and with the full picture in mind.”

Early this week the situation in Hong Kong has been rapidly deteriorating, with violence breaking out in several locations Monday and Tuesday as a citywide strike crippled transportation.

Riot police used crowd control measures in about a half dozen locations – targeting those filing the streets. Close to a hundred people people were arrested upon the start of the week for offences including rioting, unlawful assembly, assaulting a police officer, obstructing police and possession of offensive weapons.

via ZeroHedge News https://ift.tt/2YxWbsX Tyler Durden

{kind=link}